pinnacle foods inc. presentation to cagny

TRANSCRIPT

1 1

PINNACLE FOODS INC.

Presentation to CAGNY March 11, 2015

2 2

Bob Gamgort Chief Executive Officer

Craig Steeneck EVP & CFO

Maria Sceppaguercio SVP IR & Communications

Pinnacle Management

Mark Schiller EVP & President North America Retail

3 3

Forward-Looking Statements & Non-GAAP Financial Measures

This presentation contains “forward-looking statements” within the meaning of U.S. federal securities laws. Forward-looking statements are not historical facts, and are based upon management’s current expectations, beliefs, projections and targets, many of which, by their nature, are inherently uncertain. Such expectations, beliefs, projections and targets are expressed in good faith. However, there can be no assurance that management’s expectations, beliefs, projections and targets will be achieved and actual results may differ materially from what is expressed in or indicated by the forward-looking statements. Forward-looking statements are subject to significant business, economic, regulatory and competitive risks and uncertainties that could cause actual performance or results to differ materially from those expressed in the forward-looking statements, including risks detailed in Pinnacle Foods Inc.’s (“Pinnacle Foods,” “Pinnacle” or the “Company”) filings with the U.S. Securities and Exchange Commission (the “SEC”). Nothing in this presentation should be regarded as a representation by any person that these forward-looking statements will be achieved.

Forward-looking statements speak only as of the date the statements are made. The Company assumes no obligation to update forward-looking statements to reflect actual results, subsequent events or circumstances or other changes affecting forward-looking information except to the extent required by applicable securities laws.

This presentation includes certain financial measures, including Adjusted EBITDA, Adjusted Gross Profit and Unleveraged Free Cash Flow, which differ from results using U.S. Generally Accepted Accounting Principles (GAAP). Non-GAAP financial measures typically exclude certain charges, which are not expected to occur routinely in future periods. The Company uses non-GAAP financial measures internally to focus management on performance excluding these special charges to gauge our business operating performance. Management believes this information is helpful to investors in understanding trends in the business. The most directly comparable GAAP financial measures and reconciliations to non-GAAP financial measures are set forth in the slides in this presentation and included in the Company’s filings with the SEC.

4 4

Agenda Overview

Creating Value in a Challenging Environment

Driving Margin Expansion and Cash Flow

Outlook

5 5

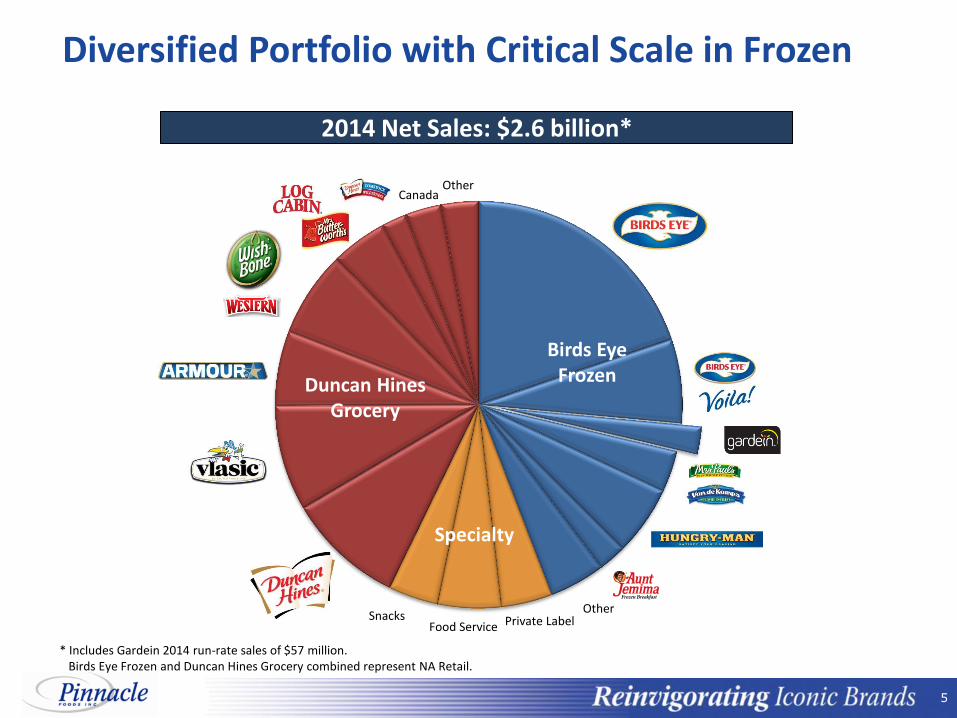

Other Private Label Food Service

Snacks

Canada Other

Diversified Portfolio with Critical Scale in Frozen

2014 Net Sales: $2.6 billion*

Birds Eye Frozen

Specialty

Duncan Hines Grocery

* Includes Gardein 2014 run-rate sales of $57 million. Birds Eye Frozen and Duncan Hines Grocery combined represent NA Retail.

6 6

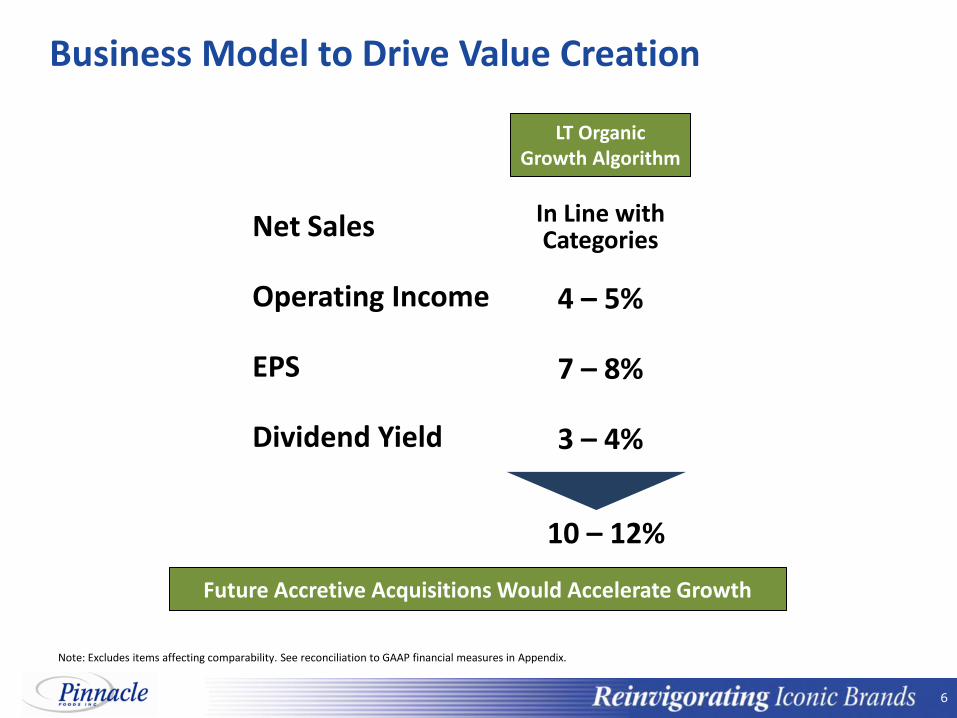

Business Model to Drive Value Creation

Net Sales

Operating Income

EPS

Dividend Yield

In Line with Categories

10 – 12%

4 – 5%

7 – 8%

3 – 4%

LT Organic Growth Algorithm

Future Accretive Acquisitions Would Accelerate Growth

Note: Excludes items affecting comparability. See reconciliation to GAAP financial measures in Appendix.

7 7

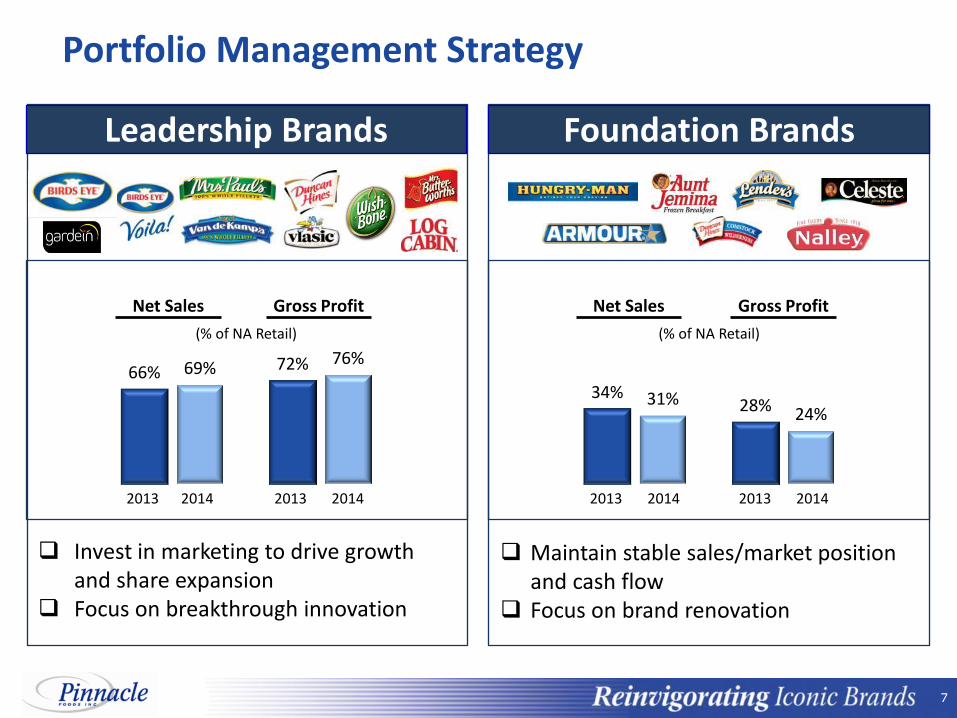

Portfolio Management Strategy

66% 72% 69% 76%

Net Sales

2013 2014 2013 2014

34% 28% 31%

24%

2013 2014 2013 2014

Invest in marketing to drive growth and share expansion

Focus on breakthrough innovation

Gross Profit Net Sales Gross Profit

Maintain stable sales/market position and cash flow

Focus on brand renovation

Leadership Brands Foundation Brands

(% of NA Retail) (% of NA Retail)

8 8

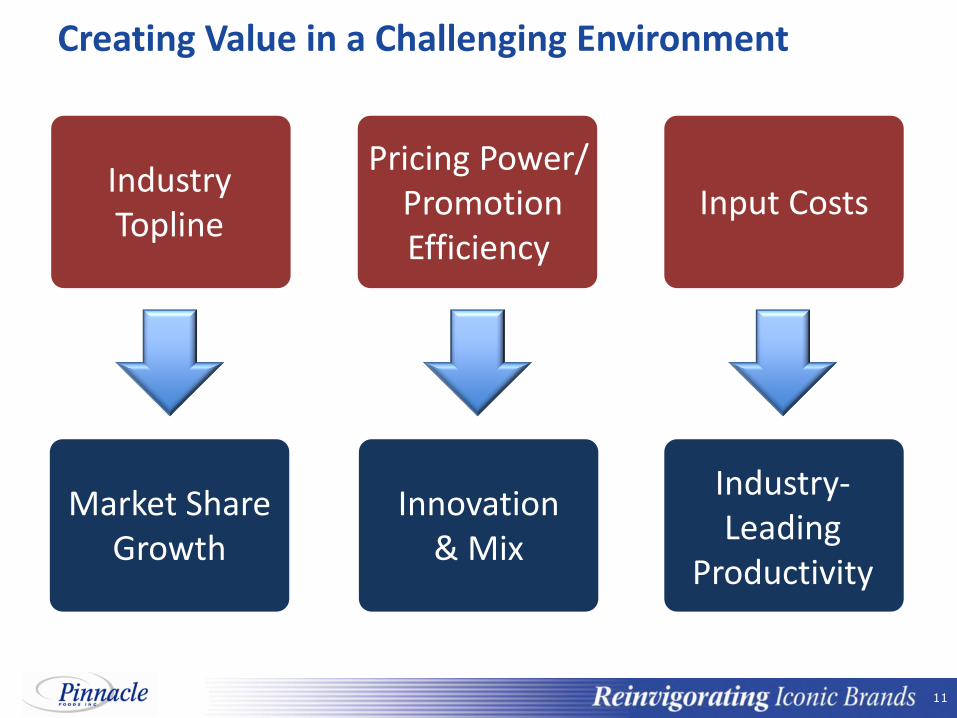

Creating Value in a Challenging Environment

Industry Topline

Input Costs Pricing Power/

Promotion Efficiency

9 9

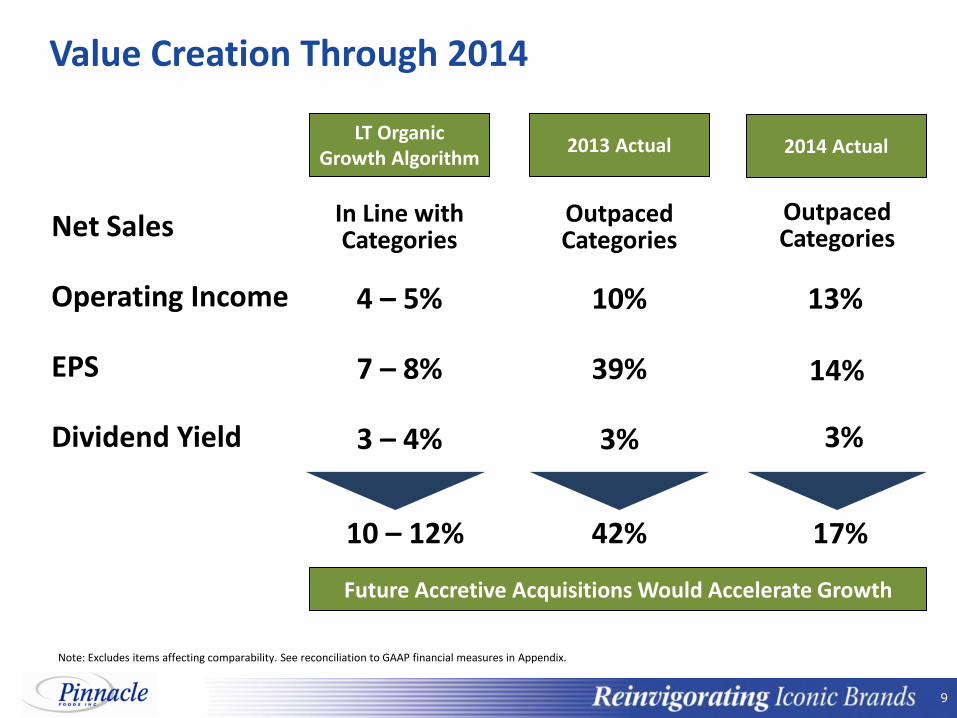

Value Creation Through 2014

Net Sales

Operating Income

EPS

Dividend Yield

In Line with Categories

10 – 12%

4 – 5%

7 – 8%

3 – 4%

LT Organic Growth Algorithm

10%

39%

3%

Outpaced Categories

42%

2013 Actual

17%

14%

2014 Actual

Outpaced Categories

3%

Future Accretive Acquisitions Would Accelerate Growth

Note: Excludes items affecting comparability. See reconciliation to GAAP financial measures in Appendix.

13%

10 10

Agenda Overview

Creating Value in a Challenging Environment

Driving Margin Expansion and Cash Flow

Outlook

11 11

Creating Value in a Challenging Environment

Industry Topline

Input Costs Pricing Power/

Promotion Efficiency

Market Share Growth

Industry- Leading

Productivity

Innovation & Mix

12 12

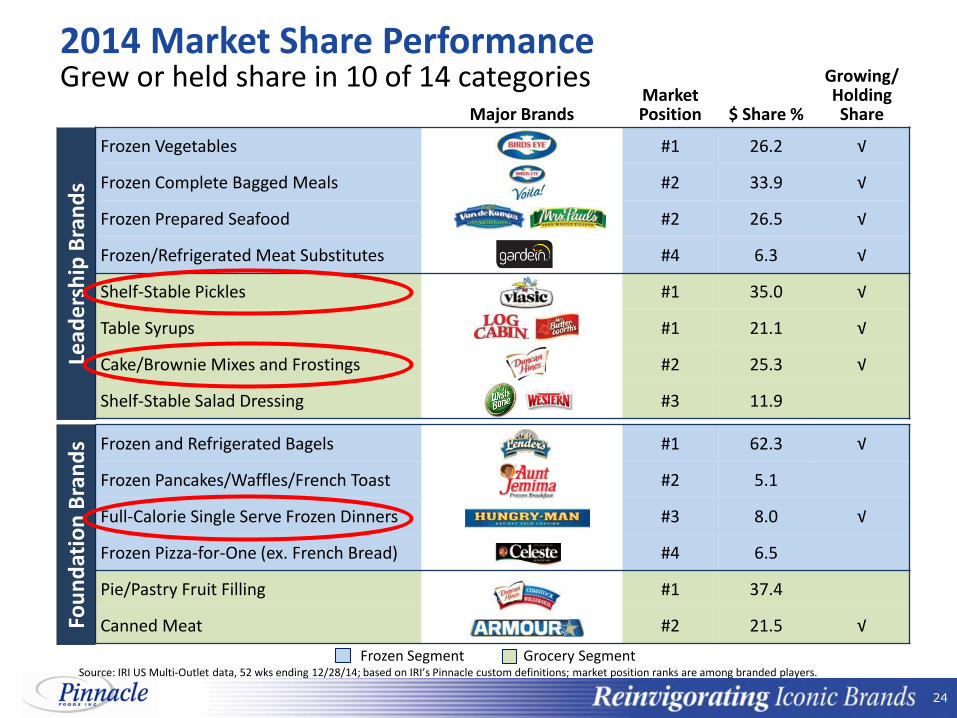

2014 Market Share Performance

Source: IRI US Multi-Outlet data, 52 wks ending 12/28/14; based on IRI’s Pinnacle custom definitions; market position ranks are among branded players.

Frozen Segment Grocery Segment

Major Brands Market Position $ Share %

Growing/ Holding Share

Frozen Vegetables #1 26.2 √

Frozen Complete Bagged Meals #2 33.9 √

Frozen Prepared Seafood #2 26.5 √

Frozen/Refrigerated Meat Substitutes #4 6.3 √

Shelf-Stable Pickles #1 35.0 √

Table Syrups #1 21.1 √

Cake/Brownie Mixes and Frostings #2 25.3 √

Shelf-Stable Salad Dressing #3 11.9

Frozen and Refrigerated Bagels #1 62.3 √

Frozen Pancakes/Waffles/French Toast #2 5.1

Full-Calorie Single Serve Frozen Dinners #3 8.0 √

Frozen Pizza-for-One (ex. French Bread) #4 6.5

Pie/Pastry Fruit Filling #1 37.4

Canned Meat #2 21.5 √ Fou

nd

atio

n B

ran

ds

Lead

ers

hip

Bra

nd

s Grew or held share in 10 of 14 categories

13 13

Birds Eye is a $1 Billion Health & Wellness Brand Poised to Capitalize on America’s Need to Eat More Vegetables

14 14

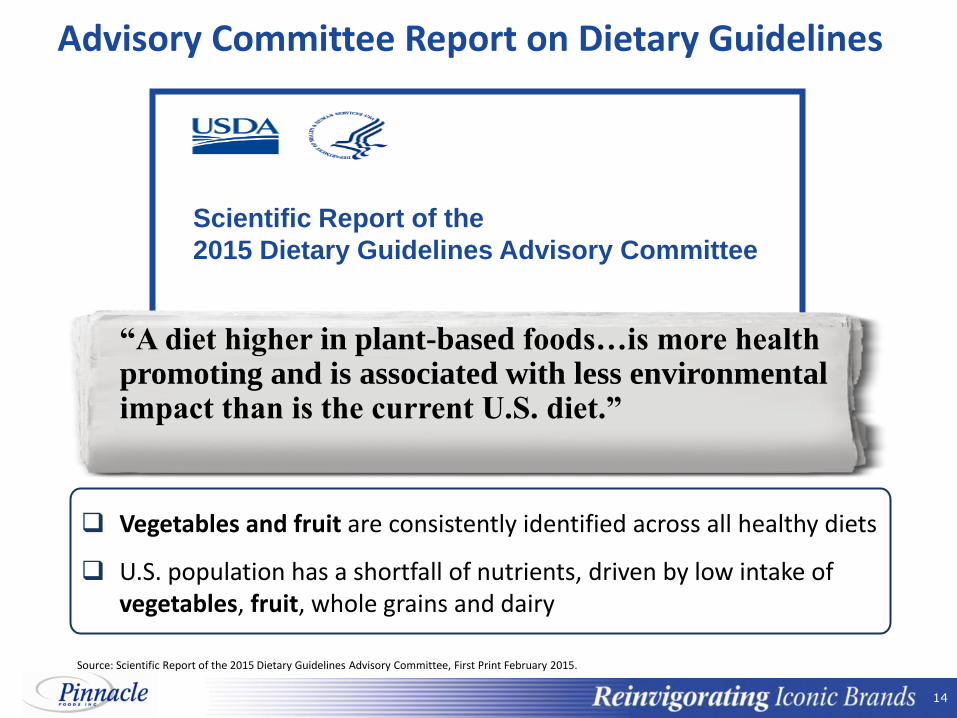

“A diet higher in plant-based foods…is more health promoting and is associated with less environmental impact than is the current U.S. diet.”

Advisory Committee Report on Dietary Guidelines

Vegetables and fruit are consistently identified across all healthy diets

U.S. population has a shortfall of nutrients, driven by low intake of vegetables, fruit, whole grains and dairy

Source: Scientific Report of the 2015 Dietary Guidelines Advisory Committee, First Print February 2015.

Scientific Report of the

2015 Dietary Guidelines Advisory Committee

15 15

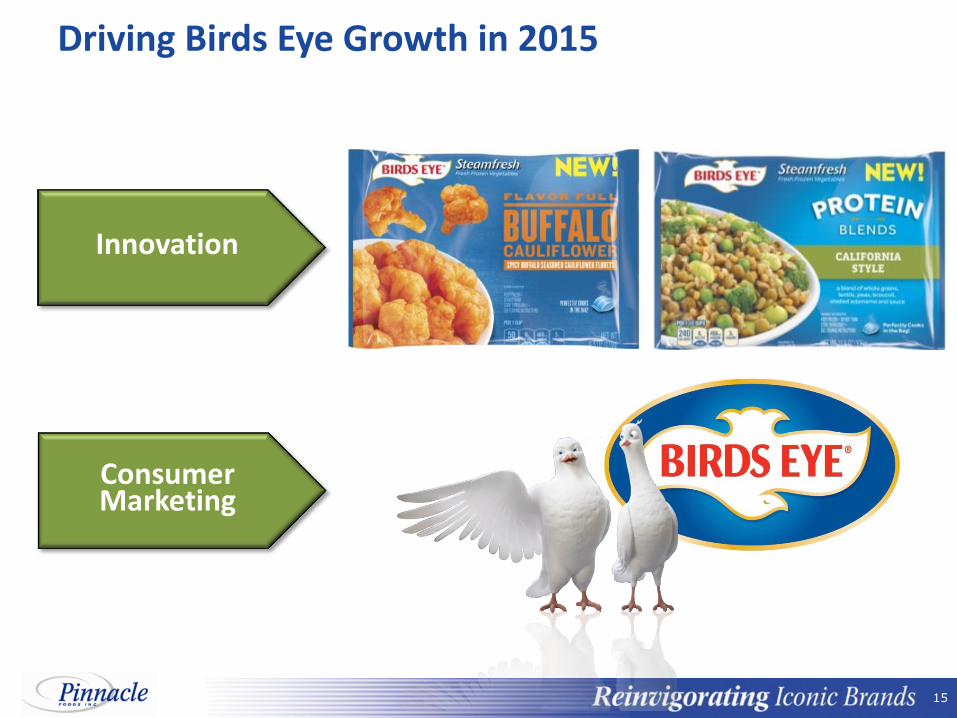

Driving Birds Eye Growth in 2015

Innovation

Consumer Marketing

16 16

New Birds Eye Platform: Flavor Full Pairing of popular vegetables with on-trend flavors creates a perfect combination of taste and nutrition

17 17

New Birds Eye Platform: Protein Blends Delivering plant-based protein benefit through the power of nutrient-rich vegetables, beans and whole grains…

…with additional platforms planned for the 2nd half.

18 18

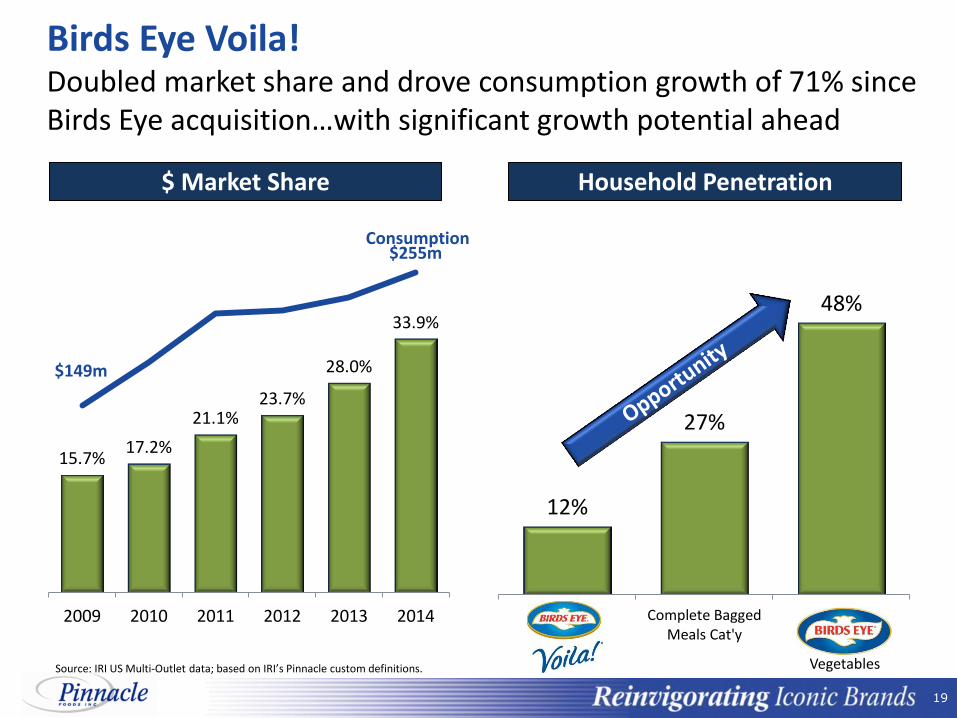

Birds Eye Voila! A winning combination of vegetable-rich complete meals at a great value

Family Size Expansion

19 19

Birds Eye Voila!

15.7% 17.2%

21.1% 23.7%

28.0%

33.9%

2009 2010 2011 2012 2013 2014

Doubled market share and drove consumption growth of 71% since Birds Eye acquisition…with significant growth potential ahead

$ Market Share

Source: IRI US Multi-Outlet data; based on IRI’s Pinnacle custom definitions.

Consumption

$149m

$255m

12%

27%

48%

Voila! Complete BaggedMeals Cat'y

BE

Household Penetration

Vegetables

20 20

Birds Eye Advertising New campaign with dedicated advertising for Voila! for the first time

21 21

New Health & Wellness Platform

Rapidly-growing innovator in the plant-based protein segment

“The art and science of transforming plants into meat wasn't there 30 years ago. Potvin's efforts at Gardein, however, are nothing short of a miracle.” LA Magazine, Mar 2015

22 22

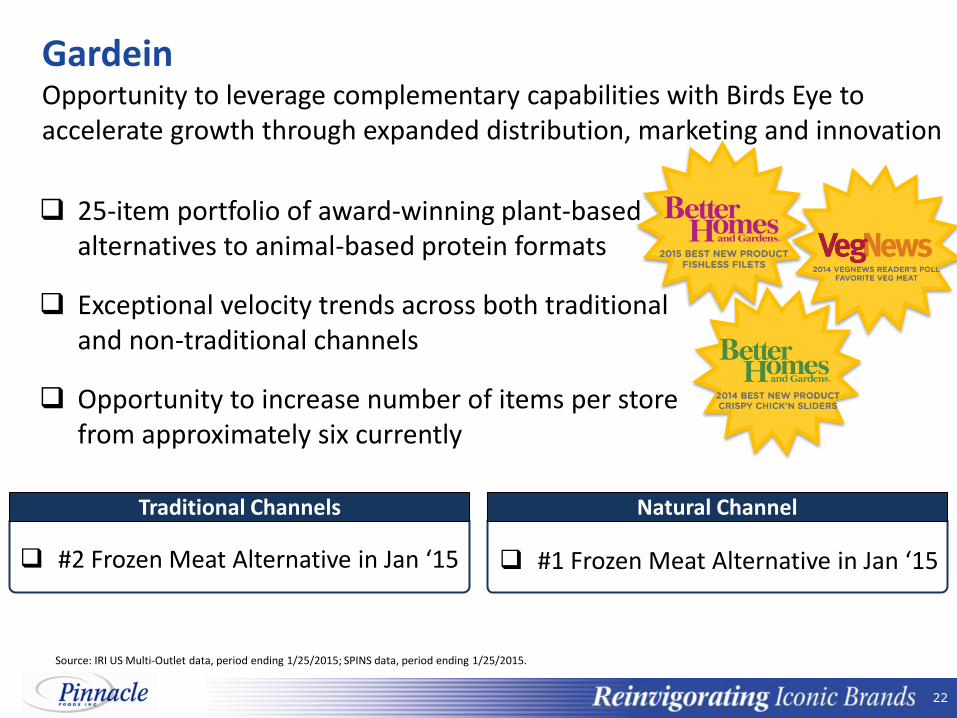

Gardein Opportunity to leverage complementary capabilities with Birds Eye to accelerate growth through expanded distribution, marketing and innovation

25-item portfolio of award-winning plant-based alternatives to animal-based protein formats

Exceptional velocity trends across both traditional and non-traditional channels

Opportunity to increase number of items per store from approximately six currently

#1 Frozen Meat Alternative in Jan ‘15 #2 Frozen Meat Alternative in Jan ‘15

Natural Channel Traditional Channels

Source: IRI US Multi-Outlet data, period ending 1/25/2015; SPINS data, period ending 1/25/2015.

23 23

Gardein New Products

24 24

2014 Market Share Performance

Source: IRI US Multi-Outlet data, 52 wks ending 12/28/14; based on IRI’s Pinnacle custom definitions; market position ranks are among branded players.

Frozen Segment Grocery Segment

Major Brands Market Position $ Share %

Growing/ Holding Share

Frozen Vegetables #1 26.2 √

Frozen Complete Bagged Meals #2 33.9 √

Frozen Prepared Seafood #2 26.5 √

Frozen/Refrigerated Meat Substitutes #4 6.3 √

Shelf-Stable Pickles #1 35.0 √

Table Syrups #1 21.1 √

Cake/Brownie Mixes and Frostings #2 25.3 √

Shelf-Stable Salad Dressing #3 11.9

Frozen and Refrigerated Bagels #1 62.3 √

Frozen Pancakes/Waffles/French Toast #2 5.1

Full-Calorie Single Serve Frozen Dinners #3 8.0 √

Frozen Pizza-for-One (ex. French Bread) #4 6.5

Pie/Pastry Fruit Filling #1 37.4

Canned Meat #2 21.5 √ Fou

nd

atio

n B

ran

ds

Lead

ers

hip

Bra

nd

s Grew or held share in 10 of 14 categories

25 25

Hungry-Man Satisfying, protein-packed comfort food

Selects Premium Price Tier Regular On-trend Flavors

2014 consumption +2.4% driven by innovation and Selects expansion

41g

PROTEIN

26 26

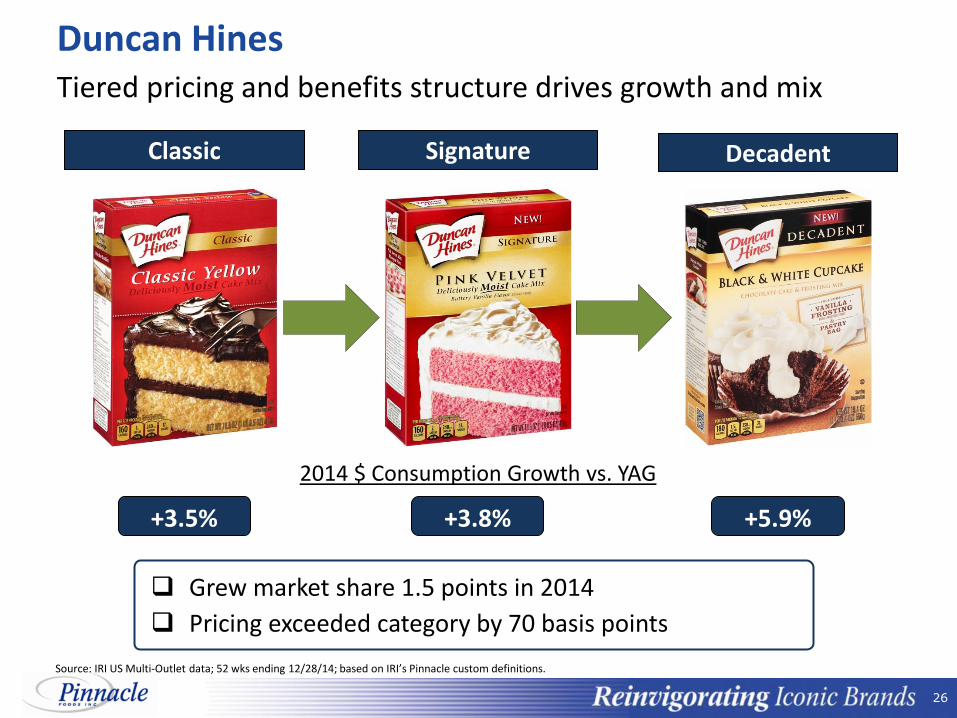

Duncan Hines Tiered pricing and benefits structure drives growth and mix

Signature Classic Decadent

+3.5%

2014 $ Consumption Growth vs. YAG

Grew market share 1.5 points in 2014

Pricing exceeded category by 70 basis points

+3.8% +5.9%

Source: IRI US Multi-Outlet data; 52 wks ending 12/28/14; based on IRI’s Pinnacle custom definitions.

27 27

Vlasic Leveraging innovation to drive consumption growth in an expanding category

Premium offering incremental to the category and Pinnacle

Bold & Spicy Farmer’s Garden

Three new varieties tap into Intense Flavor trend

28 28

Agenda Overview

Creating Value in a Challenging Environment

Driving Margin Expansion and Cash Flow

Outlook

29 29

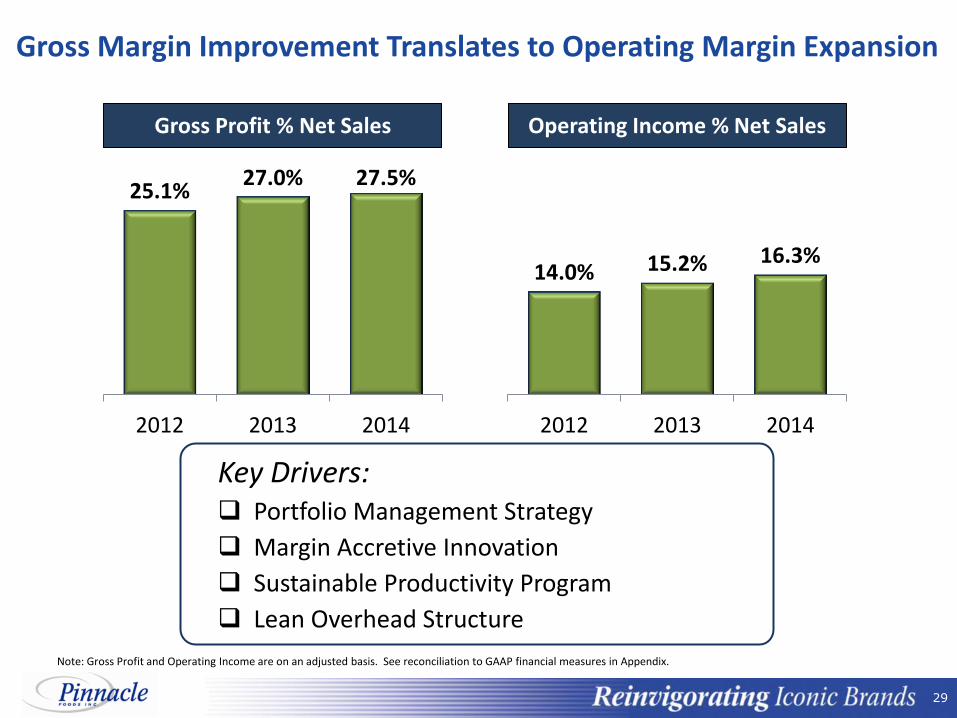

Gross Margin Improvement Translates to Operating Margin Expansion

25.1% 27.0% 27.5%

2012 2013 2014

Gross Profit % Net Sales

14.0% 15.2% 16.3%

2012 2013 2014

Operating Income % Net Sales

Note: Gross Profit and Operating Income are on an adjusted basis. See reconciliation to GAAP financial measures in Appendix.

Key Drivers: Portfolio Management Strategy

Margin Accretive Innovation

Sustainable Productivity Program

Lean Overhead Structure

30 30

Margin-Enhancing Innovation All innovation is targeted to be margin accretive to the portfolio

31 31

4.0% 4.1%

3.7% 3%-4%

Productivity

Maximizing Value through Productivity

2012 2013 2014 2015E

Sustainable ongoing program targets 3-4% annual savings in COGS

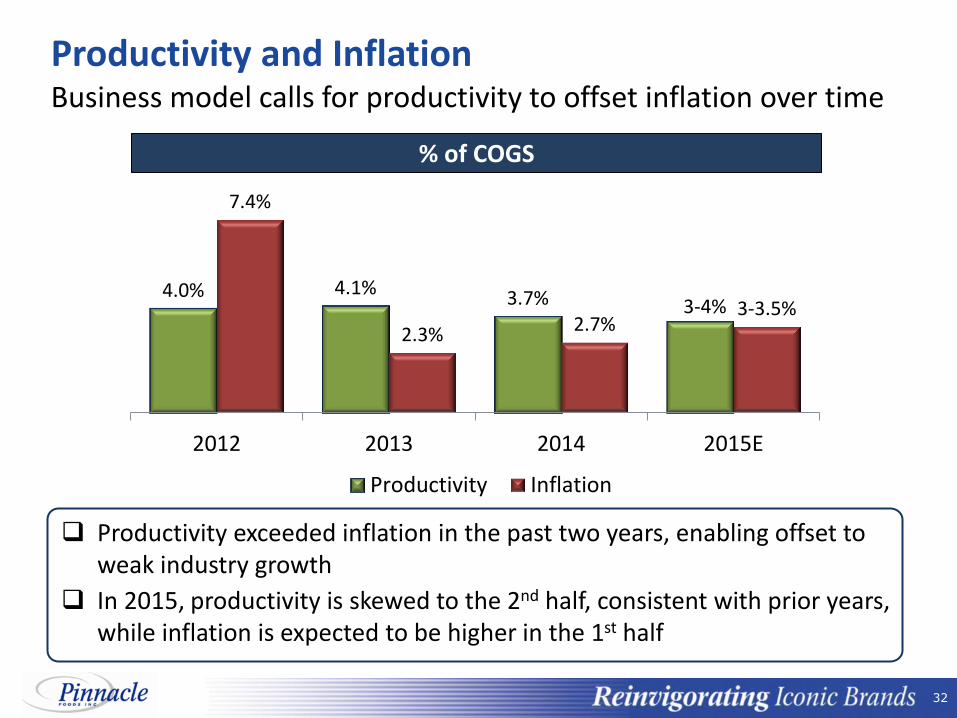

32 32

Productivity and Inflation

4.0% 4.1% 3.7% 3-4%

7.4%

2.3% 2.7% 3-3.5%

2012 2013 2014 2015E

Productivity Inflation

% of COGS

Productivity exceeded inflation in the past two years, enabling offset to weak industry growth

In 2015, productivity is skewed to the 2nd half, consistent with prior years, while inflation is expected to be higher in the 1st half

Business model calls for productivity to offset inflation over time

33 33

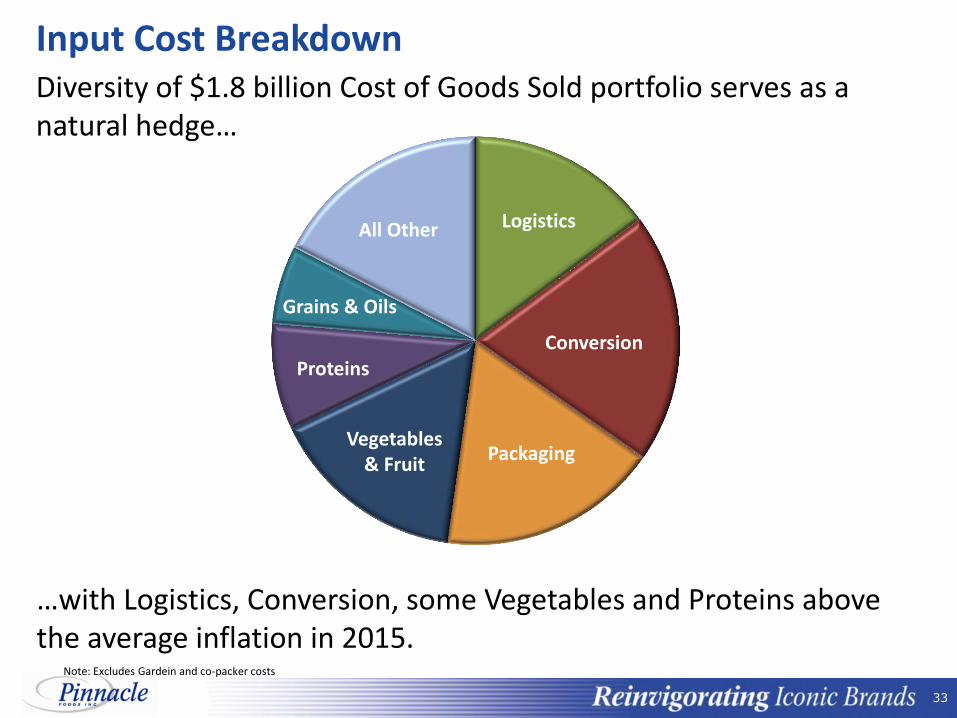

Input Cost Breakdown

Conversion

Logistics

Proteins

Grains & Oils

Packaging Vegetables

& Fruit

All Other

Note: Excludes Gardein and co-packer costs

…with Logistics, Conversion, some Vegetables and Proteins above the average inflation in 2015.

Diversity of $1.8 billion Cost of Goods Sold portfolio serves as a natural hedge…

34 34

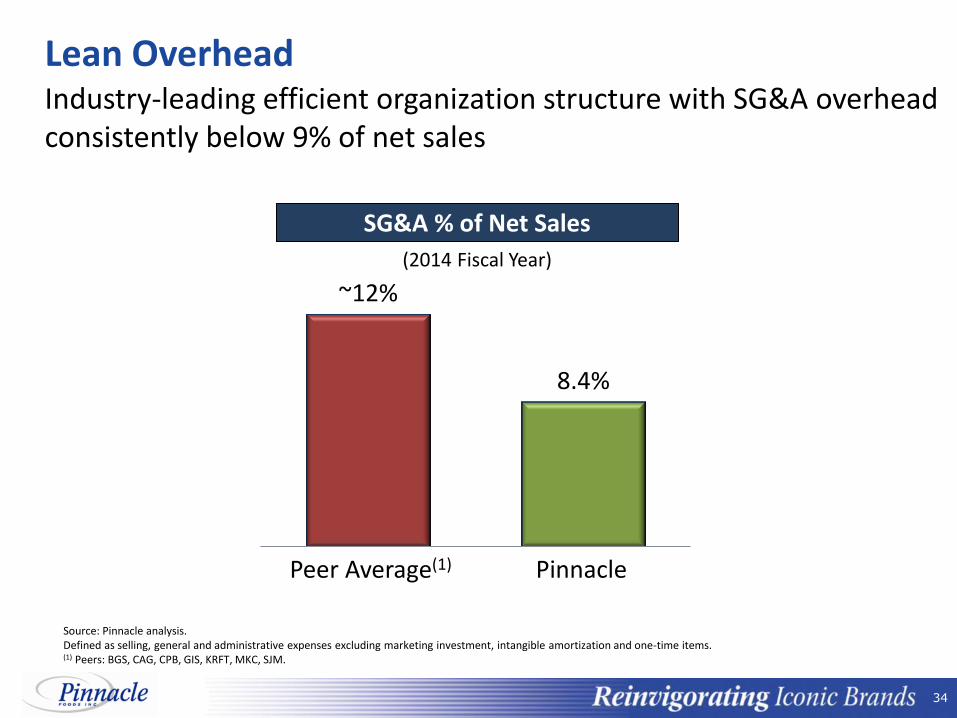

Source: Pinnacle analysis. Defined as selling, general and administrative expenses excluding marketing investment, intangible amortization and one-time items. (1) Peers: BGS, CAG, CPB, GIS, KRFT, MKC, SJM.

Lean Overhead Industry-leading efficient organization structure with SG&A overhead consistently below 9% of net sales

(2014 Fiscal Year)

SG&A % of Net Sales

~12%

8.4%

Peer Average(1) Pinnacle

35 35

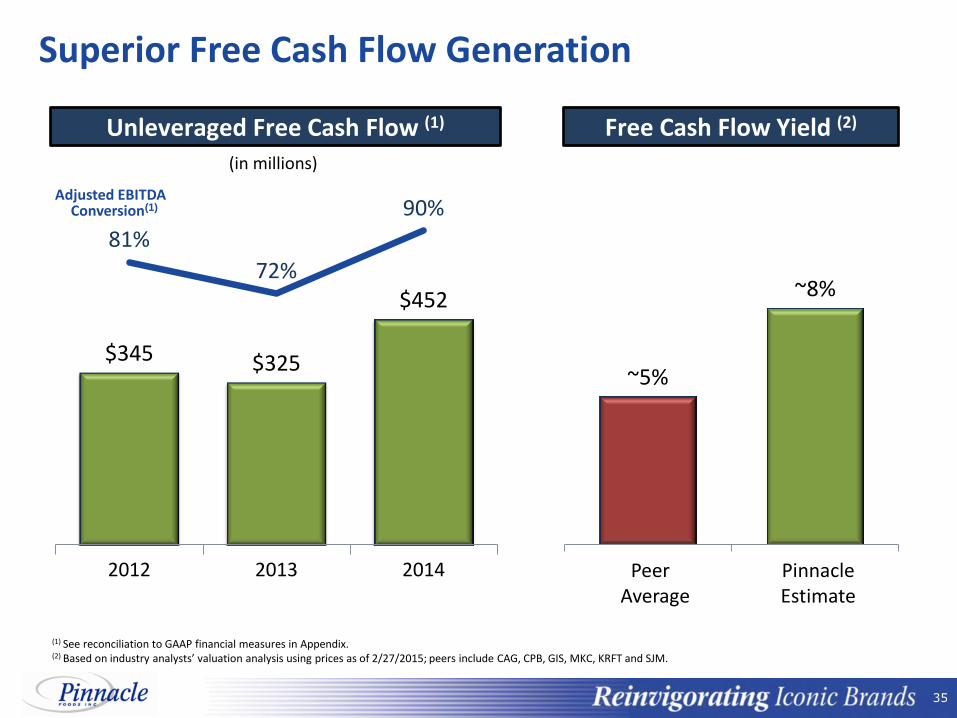

$345 $325

$452

81%

72%

90%

0%

25%

50%

75%

100%

$0

$100

$200

$300

$400

$500

$600

$700

2012 2013 2014

(1) See reconciliation to GAAP financial measures in Appendix. (2) Based on industry analysts’ valuation analysis using prices as of 2/27/2015; peers include CAG, CPB, GIS, MKC, KRFT and SJM.

Unleveraged Free Cash Flow (1)

Superior Free Cash Flow Generation

Adjusted EBITDA

Conversion(1)

Free Cash Flow Yield (2)

~5%

~8%

Peer Average

Pinnacle Estimate

(in millions)

36 36

Capital Allocation Strategy

Acquisition CAPEX

Significant cash of $628 million deployed to drive shareholder value through multiple actions

Debt Reduction

Share Repurchase

Strategic Acquisitions

Dividends Base

CAPEX

Note: $628m of cash deployed represents Net Cash Used in Investing Activities ($270m) plus Net Cash Used in Financing Activities ($358m)

37 37

A Disciplined Approach to M&A

North America focus

Existing or adjacent categories

Market leadership or line of sight to leadership

Synergy-rich transaction

Speed of integration

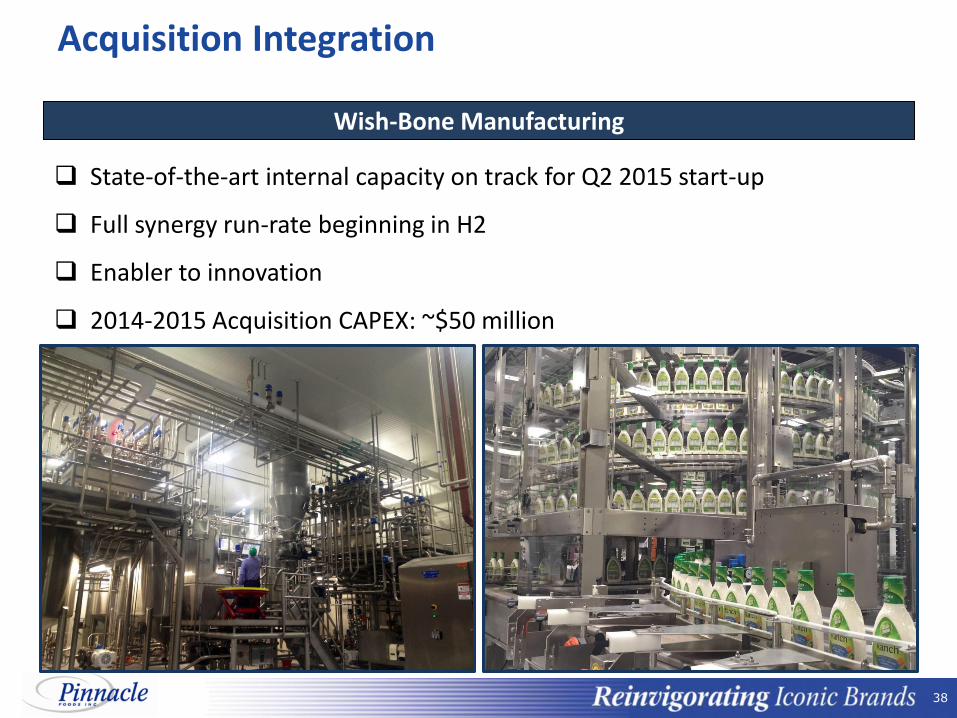

38 38

Acquisition Integration

State-of-the-art internal capacity on track for Q2 2015 start-up

Full synergy run-rate beginning in H2

Enabler to innovation

2014-2015 Acquisition CAPEX: ~$50 million

Wish-Bone Manufacturing

39 39

Acquisition Integration

Duncan Hines Manufacturing

Largest Duncan Hines co-manufacturing operation acquired in 2014

Internal capability expected to enhance innovation and enable productivity

2014-2015 Acquisition CAPEX: ~$5 million

40 40

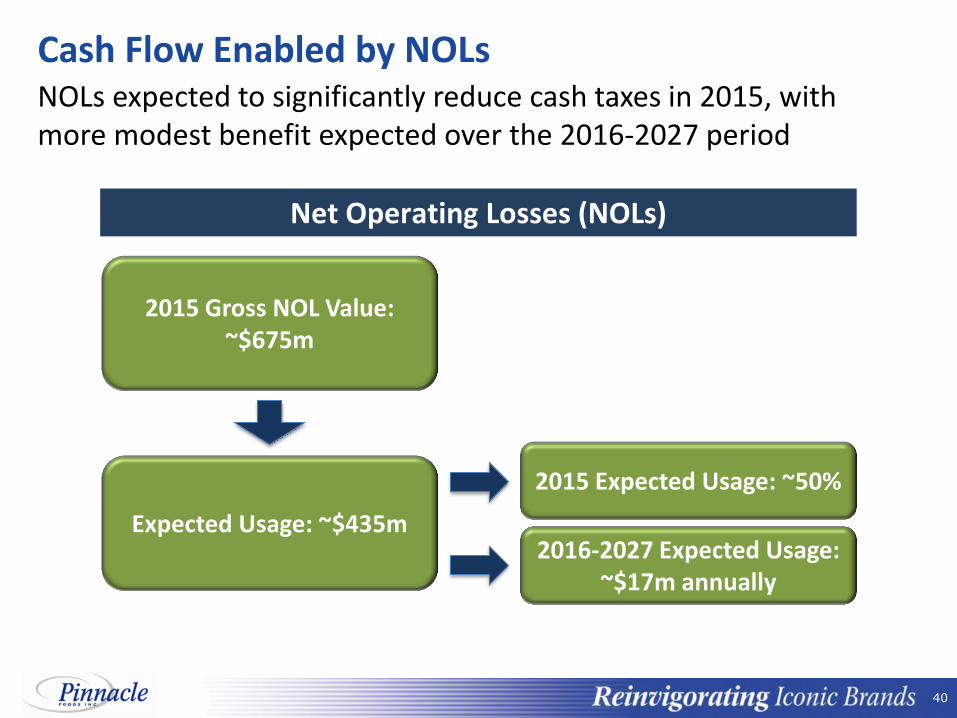

Cash Flow Enabled by NOLs NOLs expected to significantly reduce cash taxes in 2015, with more modest benefit expected over the 2016-2027 period

Net Operating Losses (NOLs)

2015 Gross NOL Value: ~$675m

Expected Usage: ~$435m

2015 Expected Usage: ~50%

2016-2027 Expected Usage: ~$17m annually

41 41

Tax-Related Cash Benefits Beyond 2015

Tax Shield

Cash Benefit

NOL tax benefit $17 $6

Wish-Bone & Gardein amortization 45 17

Effective Tax Rate Reduction* 4

Total Cash Tax Benefit $27

Future Cash Tax Benefits $m

Tax benefits continue beyond 2015 driven by residual NOLs, acquisition-related tax amortization and a lower effective tax rate

Duration of Benefit

12 years

13-14 years

Indefinite

*Reflects benefit of Domestic Manufacturing Deduction that is available upon becoming a full cash taxpayer, which Pinnacle will migrate to during 2015.

42 42

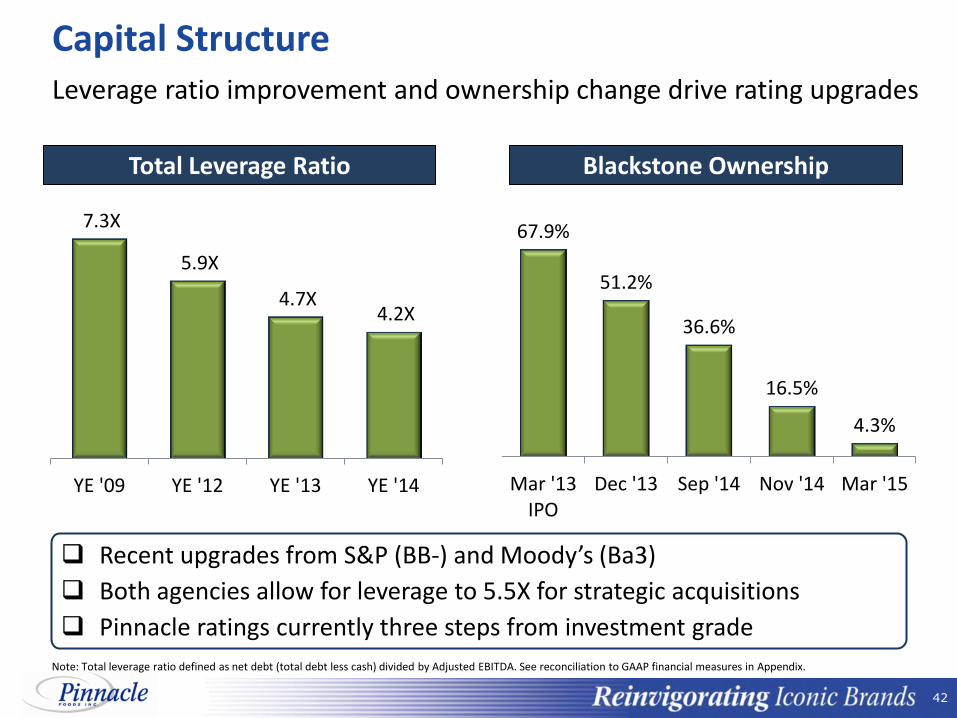

Capital Structure Leverage ratio improvement and ownership change drive rating upgrades

Note: Total leverage ratio defined as net debt (total debt less cash) divided by Adjusted EBITDA. See reconciliation to GAAP financial measures in Appendix.

Recent upgrades from S&P (BB-) and Moody’s (Ba3)

Both agencies allow for leverage to 5.5X for strategic acquisitions

Pinnacle ratings currently three steps from investment grade

67.9%

51.2%

36.6%

16.5%

4.3%

Mar '13IPO

Dec '13 Sep '14 Nov '14 Mar '15

Blackstone Ownership

7.3X

5.9X

4.7X 4.2X

YE '09 YE '12 YE '13 YE '14

Total Leverage Ratio

43 43

Dividends

$0.72 $0.72

$0.84 $0.84 $0.84 $0.94 $0.94

Jul-13 Oct-13 Jan-14 Apr-14 Jul-14 Oct-14 Jan-15

Annualized Dividend Per Share

Dividends payout ratio targeted at 50% of net earnings

44 44

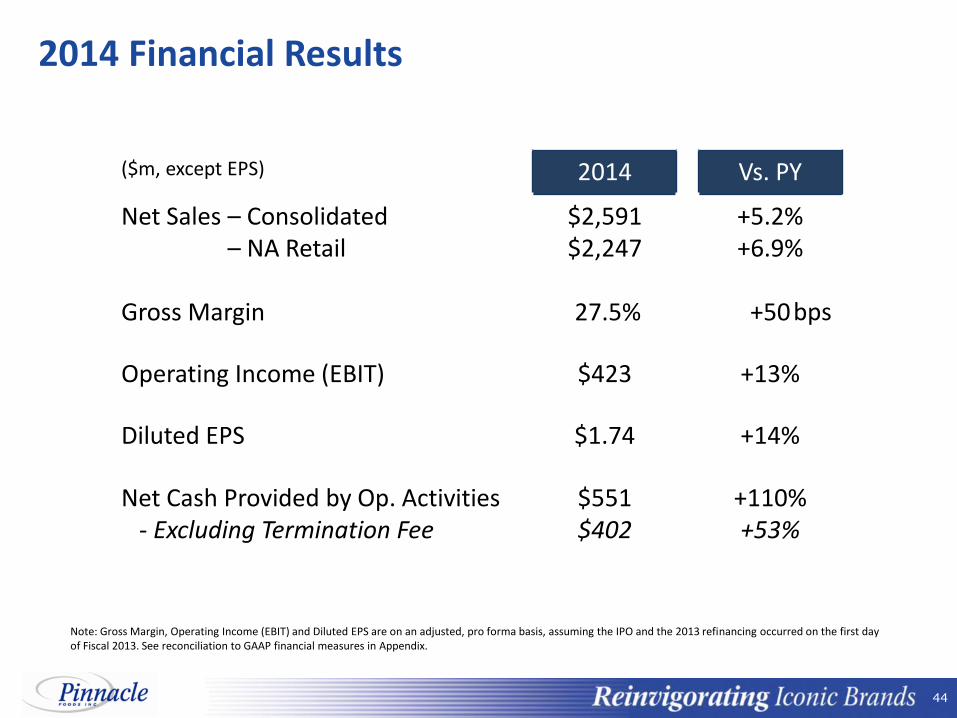

2014 Financial Results

($m, except EPS) 2014 Vs. PY

Net Sales – Consolidated Net Sales – NA Retail

$2,591 $2,247

+5.2% +6.9%

Gross Margin 27.5% +50

Operating Income (EBIT) $423 +13%

Diluted EPS $1.74 +14%

Net Cash Provided by Op. Activities - Excluding Termination Fee

$551 $402

+110% +53%

bps

Note: Gross Margin, Operating Income (EBIT) and Diluted EPS are on an adjusted, pro forma basis, assuming the IPO and the 2013 refinancing occurred on the first day of Fiscal 2013. See reconciliation to GAAP financial measures in Appendix.

45 45

Agenda Overview

Creating Value in a Challenging Environment

Driving Margin Expansion and Cash Flow

Outlook

46 46

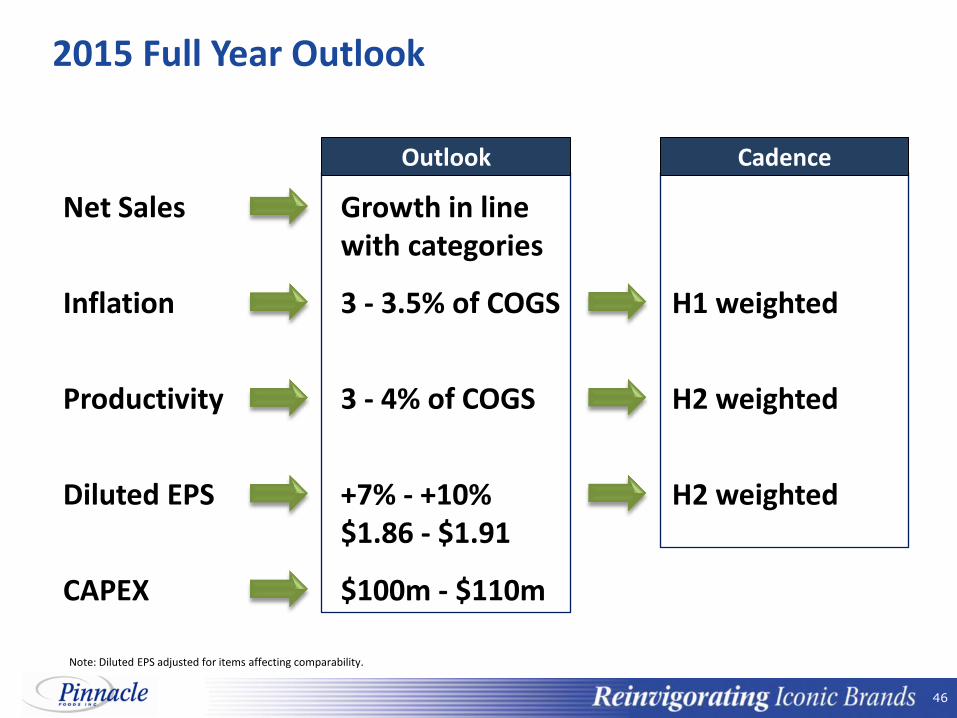

2015 Full Year Outlook

Net Sales Growth in line with categories

Inflation 3 - 3.5% of COGS Nm

Productivity 3 - 4% of COGS nm

Diluted EPS +7% - +10% $1.86 - $1.91

CAPEX $100m - $110m

Note: Diluted EPS adjusted for items affecting comparability.

Outlook Cadence

H1 weighted

H2 weighted

H2 weighted

47 47

Attractive Value Creation Potential

Long-Term Organic Growth Algorithm

Net Sales

Operating Income

EPS

Dividend Yield

Note: Excludes items affecting comparability.

In Line with Categories

10 – 12%

4 – 5%

7 – 8%

3 – 4%

Accretive acquisitions would accelerate growth further

Realistic organic growth targets

Sustainable productivity program

Strong FCF providing optionality

Disciplined M&A approach with demonstrated value creation

48 48

PINNACLE FOODS INC.

Appendix

49 49

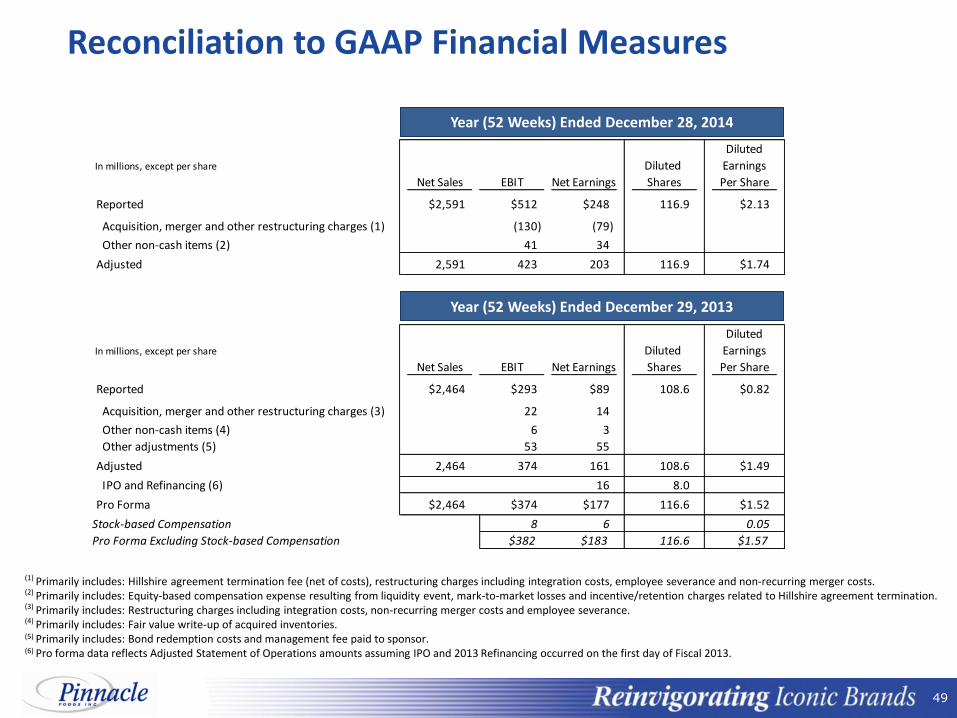

Reconciliation to GAAP Financial Measures

(1) Primarily includes: Hillshire agreement termination fee (net of costs), restructuring charges including integration costs, employee severance and non-recurring merger costs. (2) Primarily includes: Equity-based compensation expense resulting from liquidity event, mark-to-market losses and incentive/retention charges related to Hillshire agreement termination. (3) Primarily includes: Restructuring charges including integration costs, non-recurring merger costs and employee severance. (4) Primarily includes: Fair value write-up of acquired inventories. (5) Primarily includes: Bond redemption costs and management fee paid to sponsor. (6) Pro forma data reflects Adjusted Statement of Operations amounts assuming IPO and 2013 Refinancing occurred on the first day of Fiscal 2013.

Year (52 Weeks) Ended December 29, 2013

Diluted

In millions, except per share Diluted Earnings

Net Sales EBIT Net Earnings Shares Per Share

Reported $2,591 $512 $248 116.9 $2.13

Acquisition, merger and other restructuring charges (1) (130) (79)

Other non-cash items (2) 41 34

Adjusted 2,591 423 203 116.9 $1.74

Diluted

In millions, except per share Diluted Earnings

Net Sales EBIT Net Earnings Shares Per Share

Reported $2,464 $293 $89 108.6 $0.82

Acquisition, merger and other restructuring charges (3) 22 14

Other non-cash items (4) 6 3

Other adjustments (5) 53 55

Adjusted 2,464 374 161 108.6 $1.49

IPO and Refinancing (6) 16 8.0

Pro Forma $2,464 $374 $177 116.6 $1.52

Stock-based Compensation 8 6 0.05

Pro Forma Excluding Stock-based Compensation $382 $183 116.6 $1.57

Year (52 Weeks) Ended December 28, 2014

50 50

Reconciliation to GAAP Financial Measures

(1) Primarily includes: Accelerated depreciation from plant consolidations, restructuring charges including integration costs and employee severance. (2) Primarily includes: Mark-to-market gains / losses. (3) Primarily includes: Bond redemption costs. (4) Pro forma data reflects Adjusted Statement of Operations amounts assuming IPO occurred on the first day of Fiscal 2012.

Diluted

In millions, except per share Diluted Earnings

Net Sales EBIT Net Earnings Shares Per Share

Reported $2,479 $284 $53 86.5 $0.61

Acquisition, merger and other restructuring charges (1) 45 28

Other non-cash items (2) 0 0

Other adjustments (3) 21 23

Adjusted 2,479 350 104 86.5 $1.20

IPO (4) 30 30.9

Public company costs (4) (3) (2)

Pro Forma $2,479 $347 $132 117.4 $1.13

Year (53 Weeks) Ended December 30, 2012

51 51

Reconciliation to GAAP Financial Measures

(1) Primarily includes: Accelerated depreciation from plant consolidations, restructuring charges including integration costs and employee severance. (2) Primarily includes: Mark-to-market gains / losses, fair value write up of acquired inventories, equity-based compensation resulting from liquidity

event and incentive/retention charges related to Hillshire agreement termination. (3) Represents miscellaneous other expenses.

Reconciliation of Adjusted Gross Profit to Reported Gross Profit- $m

2012 2013 2014

Reported Gross Profit $584 $654 $681

Acquisition, merger and

other restructuring charges 38 4 12

Other non-cash items (1) 6 18

Other adjustments 2

Adjusted Gross Profit $623 $664 $711

(1)

(2)

(3)

52 52

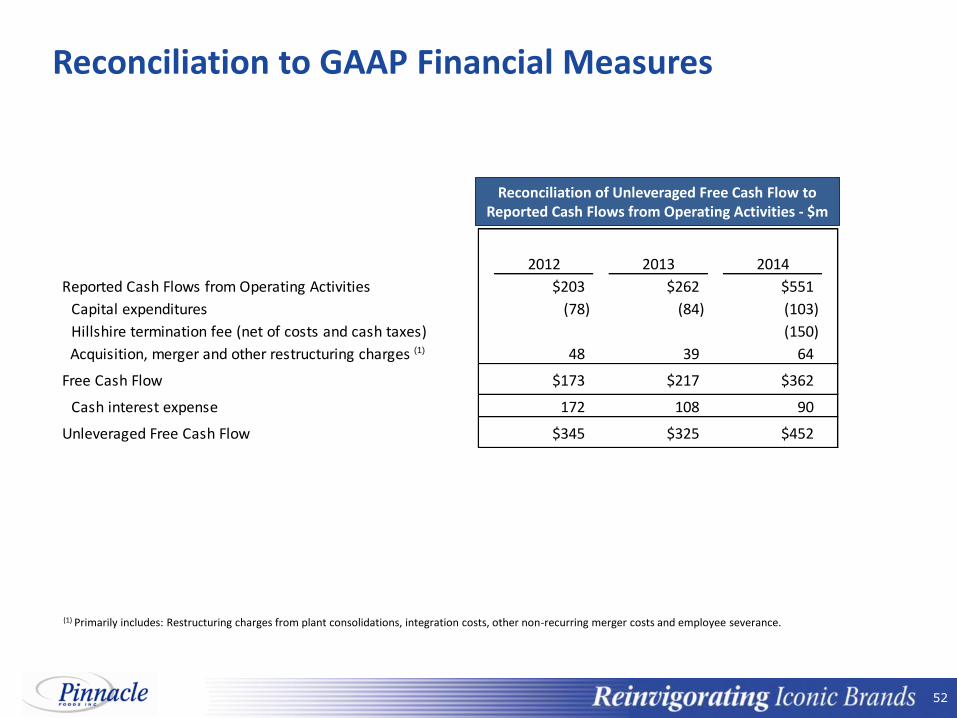

Reconciliation to GAAP Financial Measures

(1) Primarily includes: Restructuring charges from plant consolidations, integration costs, other non-recurring merger costs and employee severance.

2012 2013 2014

Reported Cash Flows from Operating Activities $203 $262 $551

Capital expenditures (78) (84) (103)

Hillshire termination fee (net of costs and cash taxes) (150)

Acquisition, merger and other restructuring charges 48 39 64

Free Cash Flow $173 $217 $362

Cash interest expense 172 108 90

Unleveraged Free Cash Flow $345 $325 $452

(1)

Reconciliation of Unleveraged Free Cash Flow to Reported Cash Flows from Operating Activities - $m

53 53

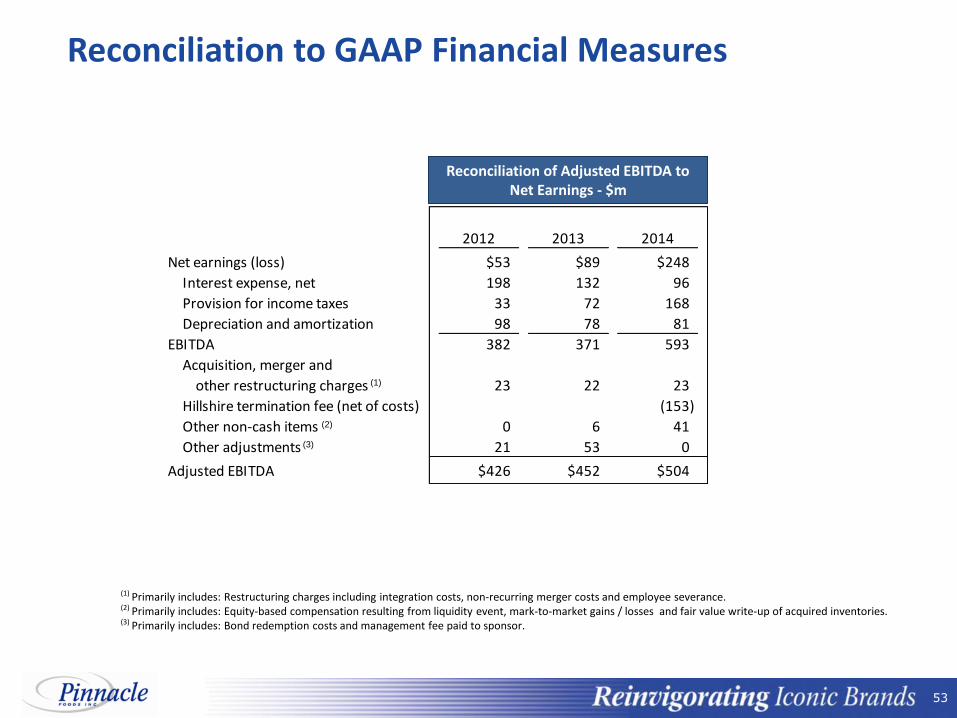

Reconciliation to GAAP Financial Measures

(1) Primarily includes: Restructuring charges including integration costs, non-recurring merger costs and employee severance. (2) Primarily includes: Equity-based compensation resulting from liquidity event, mark-to-market gains / losses and fair value write-up of acquired inventories. (3) Primarily includes: Bond redemption costs and management fee paid to sponsor.

2012 2013 2014

Net earnings (loss) $53 $89 $248

Interest expense, net 198 132 96

Provision for income taxes 33 72 168

Depreciation and amortization 98 78 81

EBITDA 382 371 593

Acquisition, merger and

other restructuring charges 23 22 23

Hillshire termination fee (net of costs) (153)

Other non-cash items 0 6 41

Other adjustments 21 53 0

Adjusted EBITDA $426 $452 $504

Reconciliation of Adjusted EBITDA to Net Earnings - $m

(3)

(1)

(2)