pitchbook · 2015-11-12 · pitchbook deal terms & multiples survey better data. better...

TRANSCRIPT

PitchBookDeal Terms & Multiples Survey

Bet ter Data. Bet ter Decisions.PitchBook

4Q 2012 Private Equity

4Q 2012 Private Equity Deal Terms & Multiples Survey

Introduction

COPYRIGHT © 2012 by PitchBook Data, Inc. All rights reserved. No part of this publication may be reproduced in any form or by any means – graphic, electronic, or mechanical, including photocopying,

recording, taping, and information storage and retrieval systems – without the express written permission of PitchBook Data, Inc. Contents are based on information from sources believed to be reliable,

but accuracy and completeness cannot be guaranteed. Nothing herein should be construed as any past, current or future recommendation to buy or sell any security or an offer to sell, or a solicitation

of an offer to buy any security. This material does not purport to contain all of the information that a prospective investor may wish to consider and is not to be relied upon as such or used in substitution

for the exercise of independent judgment.

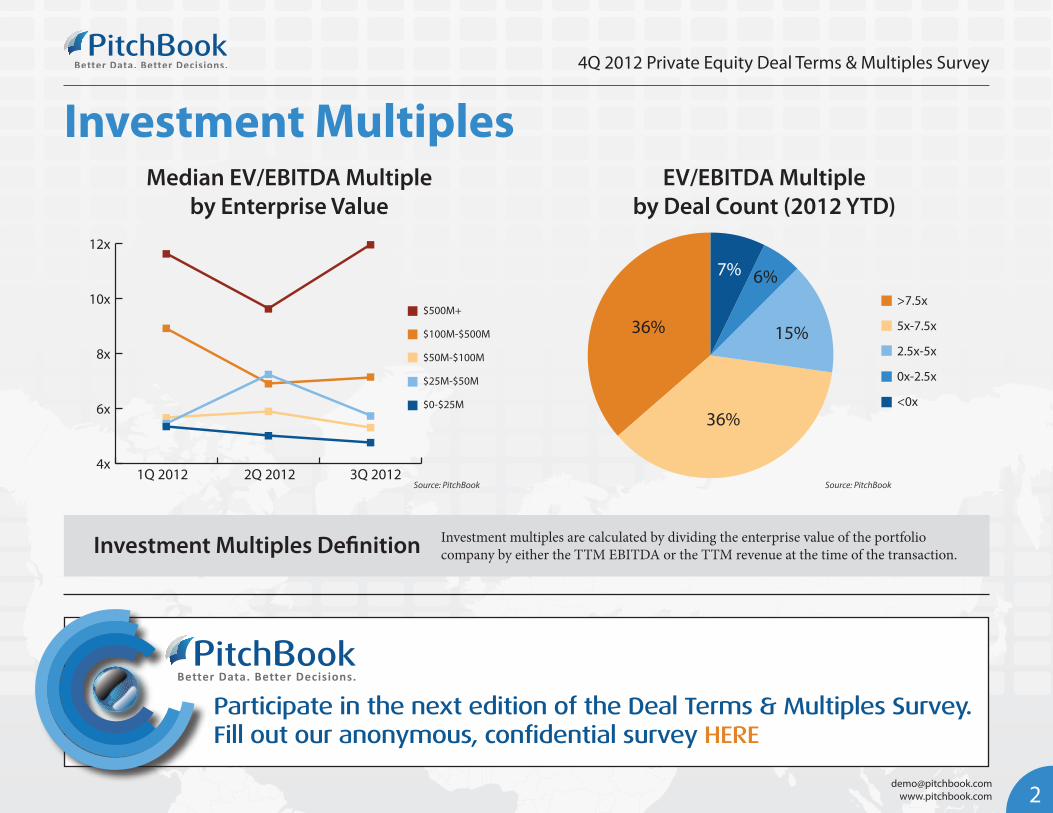

When PitchBook released the first edition of our Deal Terms & Multiples Survey last quarter, we knew that obtaining information on investment multiples, debt levels, fees, and other propriety deal information would be no easy task. However, by combining our survey responses with the verified deal information found in the PitchBook Platform, we have been able to gather in-depth deal terms and multiples data from 56 transactions that were executed in the first three quarters of 2012.

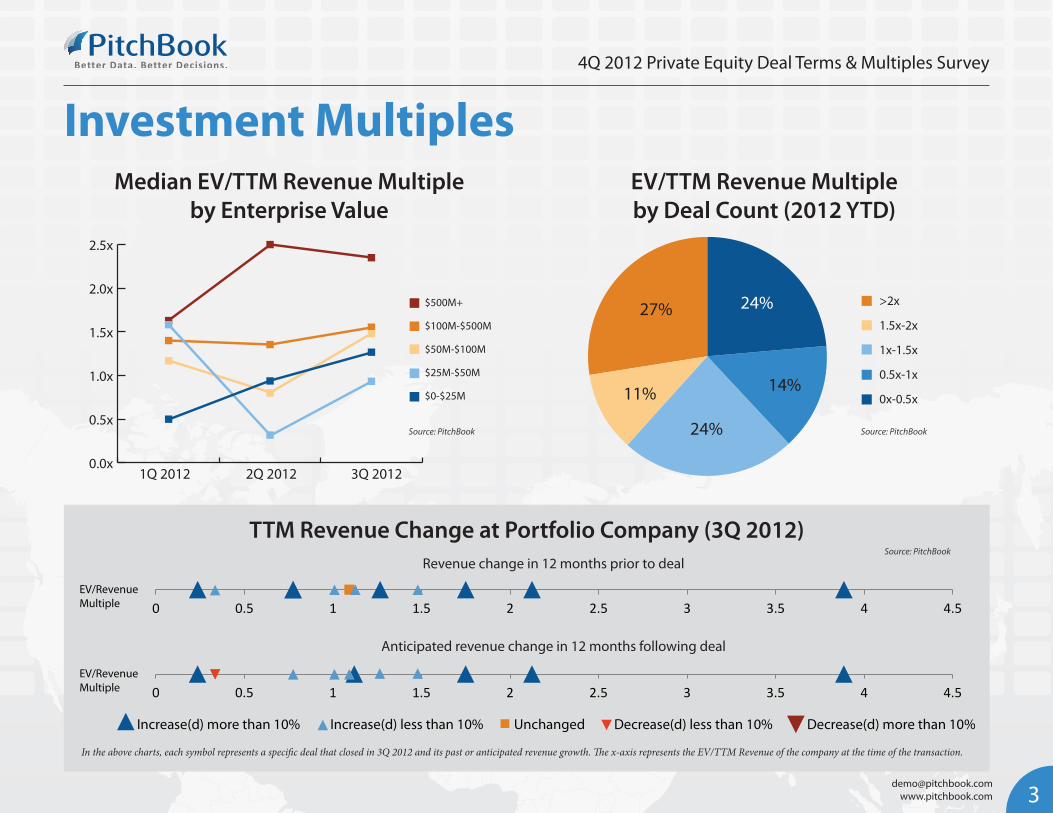

Some significant findings jumped out in the data when comparing 3Q to past quarters and looking slightly longer term at the YTD timeframe. First, the median enterprise value-to-revenue multiple rose from 2Q to 3Q for transactions in every size bucket except the $500 million and above range. The survey also shows that the average time to close a deal has dropped from 16 weeks in 1Q to 14 weeks in 3Q. We expect the heightened pace of deal execution to continue in 4Q as investors rush to close deals before the end of the year. In a new question for this edition of the survey, we asked respondents about the past and anticipated revenue growth of the target company. The correlation between these responses and the enterprise value-to-EBITDA multiple was significant, particularly for the forward-looking projections.

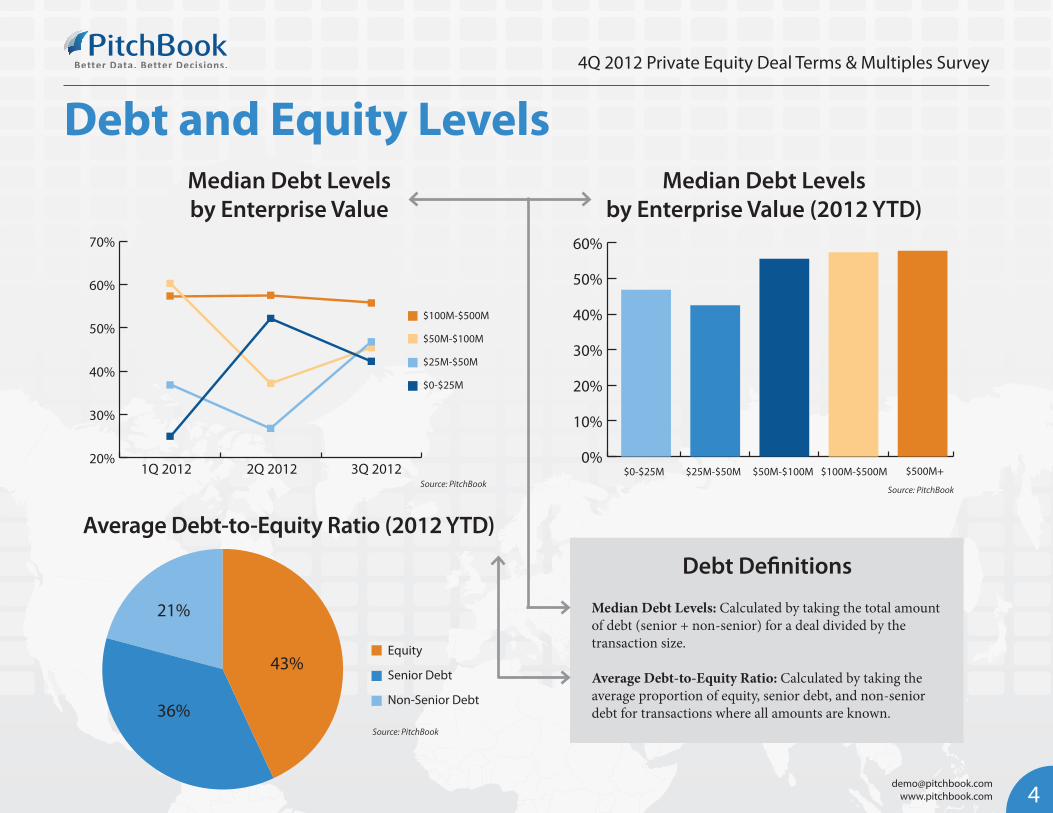

Here are some of the key takeaways from the survey data for 2012 YTD: » The median EBITDA multiple for all deals is 6.4x » The median revenue multiple for all deals is 1.2x » The median debt percentage for all deals is 50% » The average time to close a deal is 19 weeks

Of course, we are always looking to improve and augment the quality of the data used in our surveys and reports. To that end, we would greatly appreciate your participation in our forthcoming Deal Terms & Multiples Surveys. All information provided will remain completely anonymous and not be integrated into the PitchBook Platform or any deliverables besides the Deal Terms & Multiples Survey. You can provide information for your 4Q 2012 transactions here.

4Q 2012 Private Equity Deal Terms & Multiples Survey

Investment Multiples

4x

6x

8x

10x

12x

1Q 2012 2Q 2012 3Q 2012

$500M+

$100M-$500M

$50M-$100M

$25M-$50M

$0-$25M

>7.5x

5x-7.5x

2.5x-5x

0x-2.5x

<0x

36%

36%

15%

6%7%

Median EV/EBITDA Multipleby Enterprise Value

EV/EBITDA Multipleby Deal Count (2012 YTD)

Participate in the next edition of the Deal Terms & Multiples Survey. Fill out our anonymous, confidential survey HERE

Source: PitchBook Source: PitchBook

2

Investment Multiples Definition Investment multiples are calculated by dividing the enterprise value of the portfolio company by either the TTM EBITDA or the TTM revenue at the time of the transaction.

4Q 2012 Private Equity Deal Terms & Multiples Survey

Investment Multiples

0.0x

0.5x

1.0x

1.5x

2.0x

2.5x

1Q 2012 2Q 2012 3Q 2012

$500M+

$100M-$500M

$50M-$100M

$25M-$50M

$0-$25M

>2x

1.5x-2x

1x-1.5x

0.5x-1x

0x-0.5x

27% 24%

11%

24%

14%

Median EV/TTM Revenue Multipleby Enterprise Value

EV/TTM Revenue Multipleby Deal Count (2012 YTD)

Source: PitchBook Source: PitchBook

0 0.5 1 1.5 2 2.5 3 3.5 4 4.5

Increase(d) more than 10% Increase(d) less than 10% Unchanged Decrease(d) less than 10% Decrease(d) more than 10%

0 0.5 1 1.5 2 2.5 3 3.5 4 4.5EV/Revenue Multiple

Revenue change in 12 months prior to deal

EV/Revenue Multiple

Anticipated revenue change in 12 months following deal

TTM Revenue Change at Portfolio Company (3Q 2012)Source: PitchBook

In the above charts, each symbol represents a specific deal that closed in 3Q 2012 and its past or anticipated revenue growth. The x-axis represents the EV/TTM Revenue of the company at the time of the transaction.

4Q 2012 Private Equity Deal Terms & Multiples Survey

Debt and Equity Levels

0%

10%

20%

30%

40%

50%

60%

$500M+$100M-$500M$50M-$100M$25M-$50M$0-$25M

Median Debt Levels by Enterprise Value (2012 YTD)

20%

30%

40%

50%

60%

70%

1Q 2012 2Q 2012 3Q 2012

$100M-$500M

$50M-$100M

$25M-$50M

$0-$25M

Median Debt Levels by Enterprise Value

Equity

Senior Debt

Non-Senior Debt36%

21%

43%

Source: PitchBookSource: PitchBook

Source: PitchBook

4

Average Debt-to-Equity Ratio (2012 YTD)

Debt Definitions

Median Debt Levels: Calculated by taking the total amount of debt (senior + non-senior) for a deal divided by the transaction size.

Average Debt-to-Equity Ratio: Calculated by taking the average proportion of equity, senior debt, and non-senior debt for transactions where all amounts are known.

4Q 2012 Private Equity Deal Terms & Multiples Survey

Fees and Closing Times

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

1Q 2012 2Q 2012 3Q 20120.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

1Q 2012 2Q 2012 3Q 2012

Median Monitoring Fee as % of Deal Size Median Transaction Fee as % of Deal Size

Source: PitchBook Source: PitchBook

1Q 2012 2Q 2012 3Q 2012

>20 wks

15-20 wks

10-14 wks

5-9 wks

100%

80%

60%

40%

20%

0%

Source: PitchBook

Weeks to Close by Deal Count

Source: PitchBook

Percent of Transactions with Deal Fees

60%

80%

100%

Monitoring Fee Transaction Fee

1Q 2012 2Q 2012 3Q 2012

5

4Q 2012 Private Equity Deal Terms & Multiples Survey

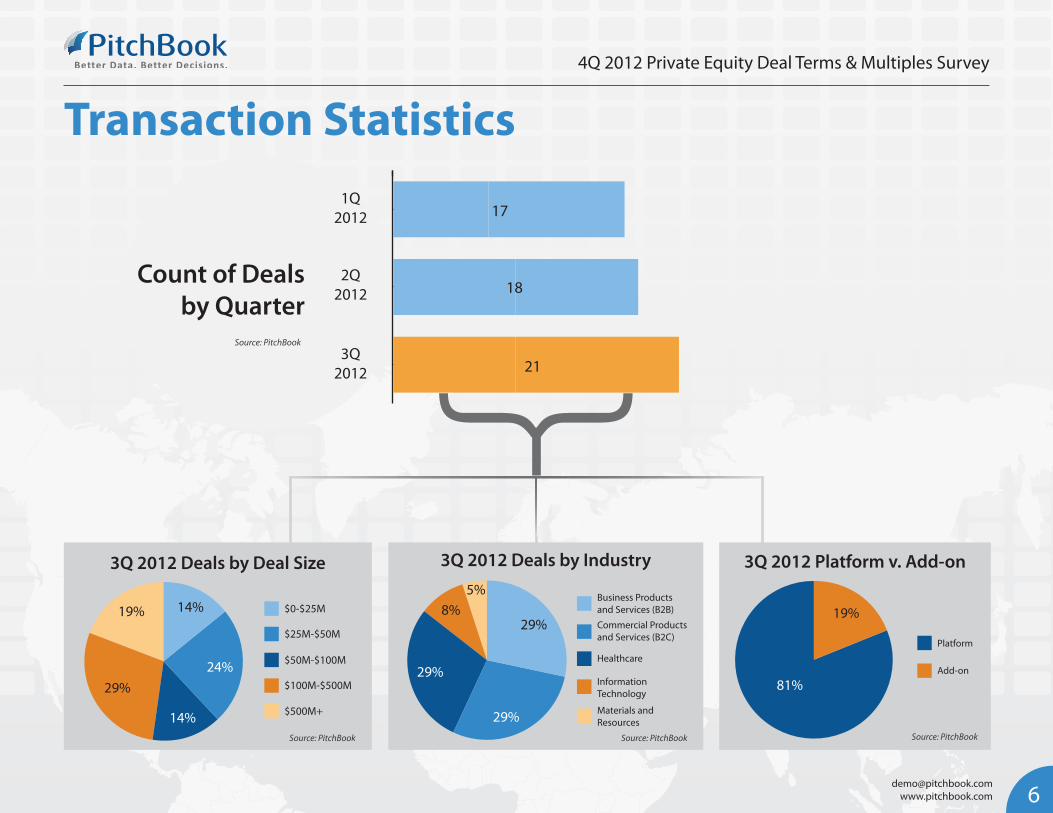

Transaction Statistics

}Count of Deals by Quarter

14%

24%

14%

29%

19% $0-$25M

$25M-$50M

$50M-$100M

$100M-$500M

$500M+

5%

29%

29%

29%8%

Business Products and Services (B2B)

Commercial Products and Services (B2C)

Healthcare

Information Technology

Materials and Resources

6

3Q 2012 Deals by Deal Size 3Q 2012 Deals by Industry

19%

81%

Platform

Add-on

3Q 2012 Platform v. Add-on

1Q2012

2Q2012

3Q2012

17

18

21

Source: PitchBookSource: PitchBookSource: PitchBook

Source: PitchBook

PitchBook tracks more Private Equity and Venture Capital data than anyone.

* All

Pitc

hBoo

k da

ta s

ourc

ed fr

om th

e Pi

tchB

ook

Plat

form

as

of 1

2/4/

2012

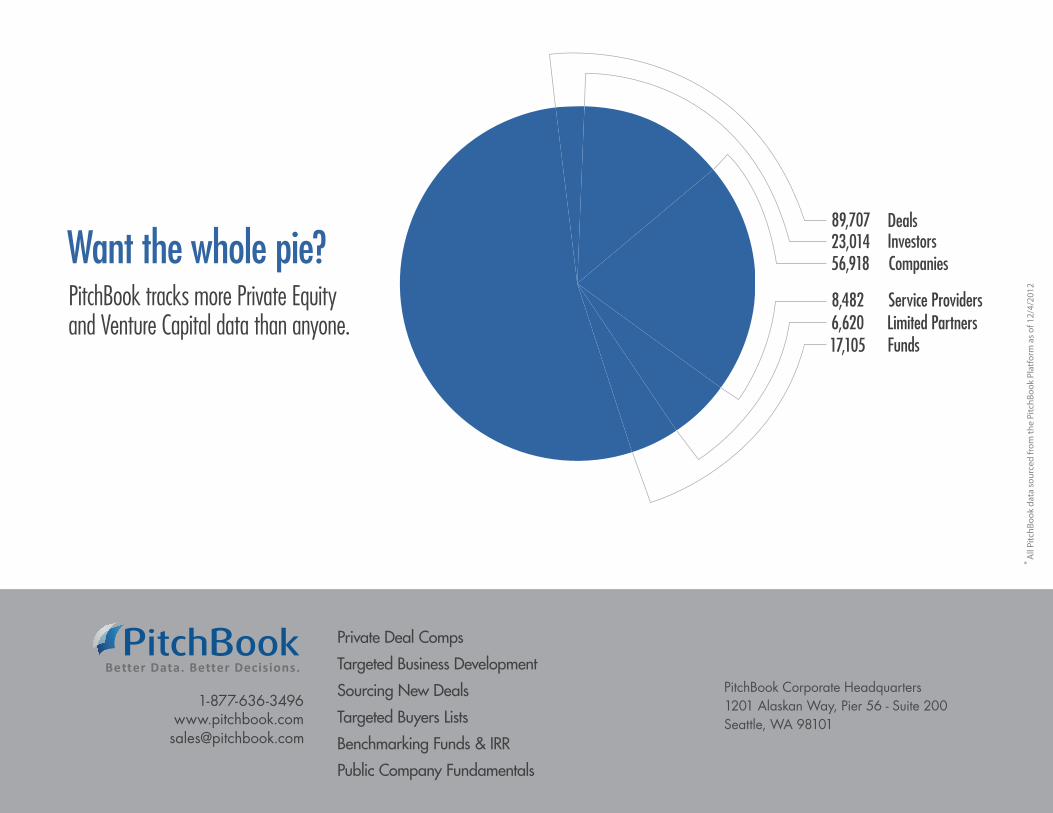

Want the whole pie?

Bet ter Data. Bet ter Decisions.PitchBook

1-877-636-3496 www.pitchbook.com

Private Deal Comps

Targeted Business Development

Sourcing New Deals

Targeted Buyers Lists

Benchmarking Funds & IRR

Public Company Fundamentals

89,707 23,014

17,105

56,918

6,620 8,482

Limited Partners

Investors

Funds

Companies

Deals

Service Providers

PitchBook Corporate Headquarters1201 Alaskan Way, Pier 56 - Suite 200Seattle, WA 98101