planning & control - luiss guido carli

TRANSCRIPT

Cost classifications, terms and purposesCost behaviour: Fixed and Variable CostsContribution Margin - Breakeven point

Cost-Volume-Profit analysis

Planning & Control

Definition of cost

Cost – the monetary value of the resources sacrificed to

achieve a specific objective

Cost Object – anything for which a separate

measurement of costs is desired (e.g., product, service,

project, activity, department, etc).

Product – a bicycle

Service – an airline flight from Manchester to Rome

Project – an airplane assembled by Airbus for BA

Activity – a test to determine the quality of a car

Department – the resources consumed by the marketing dpt.

2

Different Costs Classification for different purposes

Cost behavior in relation to Output

*Fixed and *Variable Costs

Assignment to Cost Object

*Direct and *Indirect Costs

3

Different Costs Classification for different purposes

4

Cost behavior in relation to Output

*Fixed and *Variable Costs

Assignment to Cost Object

*Direct and *Indirect Costs

Financial statement perspective

*Product (capitalized) and *Period Costs

Business Function

*Manufacturing (raw material, labor, other manufacturing costs)

*Non-Manufacturing: (marketing, distribution, customer service, legal)

BREAK-EVEN POINT AND

COST-VOLUME-PROFIT ANALYSIS

COSTING SYSTEMS – 1ST PART

JOB COSTING AND PROCESS COSTING

COSTING SYSTEMS – 2ND PART

ACTIVITY-BASED COSTING

5

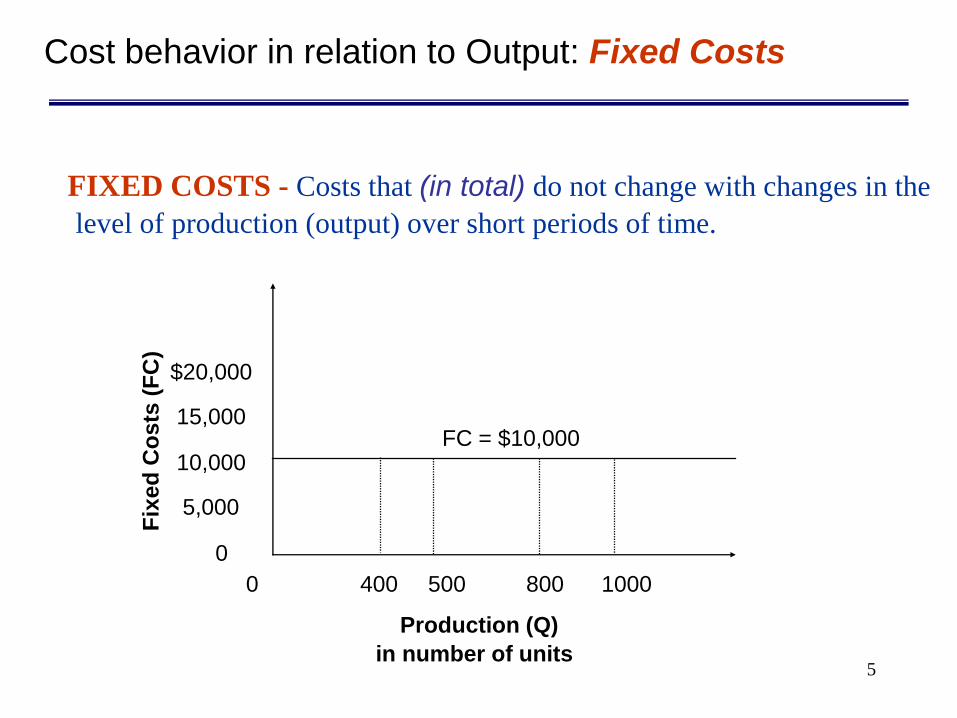

FIXED COSTS - Costs that (in total) do not change with changes in the

level of production (output) over short periods of time.

0

5,000

10,000

15,000

$20,000

0 400 500 800 1000

Production (Q)

in number of units

Fix

ed

Co

sts

(F

C)

FC = $10,000

Cost behavior in relation to Output: Fixed Costs

6

Examples of fixed costs include:

• Rent of buildings

• Salary paid to a supervisor

• Insurance and leasing of a plant

• Depreciation of a machine calculated on a straight-

line basis

Note: a fixed cost is by definition “unchanged” over a given

period of time, but it may vary in the longer term (where we

may change our production capacity, i.e. build another plant,

employ more supervisors, etc.)

Cost behavior in relation to Output: Fixed Costs

7

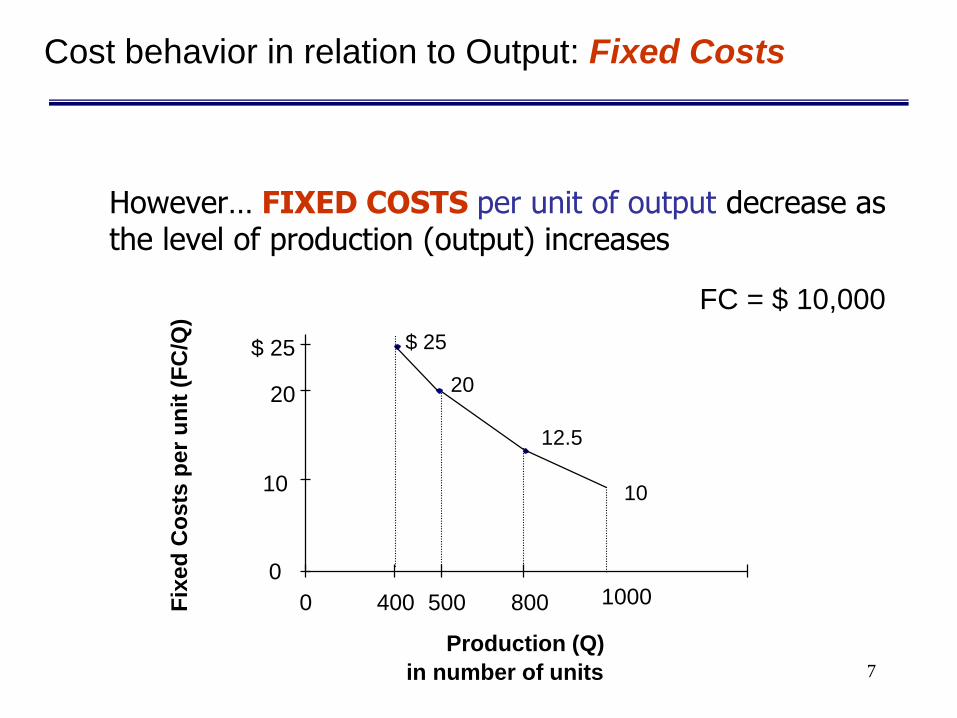

However… FIXED COSTS per unit of output decrease as the level of production (output) increases

0

10

$ 25

0 400 500 800 1000

Production (Q)

in number of units

Fix

ed

Co

sts

pe

r u

nit

(F

C/Q

)

20

$ 25

20

12.5

10

FC = $ 10,000

Cost behavior in relation to Output: Fixed Costs

8

Vari

ab

le C

os

ts(V

C)

VC = $5 * Q

Slope = 5

$10,000

$30,000

0

10,000

20,000

30,000

$40,000

200 400 600 800 1,000

Production (Q)

in number of units

VARIABLE COSTS - Costs that (in total) change in proportion to

changes in the level of production (output)

Cost behavior in relation to Output: Variable Costs

$20,000

9

Examples of variable costs include:

• Material used

• Labor costs

• Commission paid to a sales person

Cost behavior in relation to Output: Variable Costs

10

Va

riab

le C

osts

per

un

it

(VC

/Q)

1

2

3

4

$ 5

0 200 400 600 800 1,000

Production (Q)in number of units

VC/Q = $ 5 per unit

VARIABLE COSTS per unit of output are assumed to be constant as

the level of production (output) changes.

Cost behavior in relation to Output: Variable Costs

Cost behavior in relation to Output: Semi-variable costs

Semi-variable costA cost which is partially fixed and partially varies with the changes in the

level of quantity (activity)

Examples: telephone costs; fixed lump sum plus costs for the calls –

IT help desk; fixed basic charge plus a variable element depending

on the number of call-outs

Ele

ctr

icit

y C

ost

0

20

40

60

80

100 200 300 400

Production (Q)

100

Variable cost element

Fixed cost element

The slope of this

line is the

variable cost per

unit

Cost behavior in relation to Output: Step costs (“costi a gradini”)

Production Level (Q)

Co

st

(C)

A cost which is fixed over a certain range of production (quantity)

but then increases as the capacity (and the usage of a particular

activity) increases

13

Contribution Margin (CM) analysis

Contribution Margin (in total)

TOTAL REVENUES – TOTAL VARIABLE COSTS

…what is left from the revenues after having covered the variable costs...

(1) to cover the Fixed Costs, and

(2) “to get” some profit.

Contribution Margin (per unit)= Selling price – variable cost per unit

14

Break-even pointTC = TR

FC + (VCu X Q*) = SP X Q*

FC = SP X Q* - (VCu X Q*)

FC = Q* (SP - VCu)

FC

(SP - VCu)

Cost-Volume-Profit (CVP) analysis:

break-even point

Q* =FC

Contribution

Margin per unit

=

15

Total cost equation ... TC = FC + (VCu X Q)where

TC = total cost

FC = fixed costs

VCu = variable cost per unit of production

Q = quantity of production

Total revenue equation ... TR = SP X Q

where

TR = total revenue

SP = selling price per unit

Q = quantity of unit sold*

(*unit sold = unit produced)

Cost-Volume-Profit (CVP) analysis

16

Co

sts

(C

)

0

10,000

20,000

30,000

40,000

200 400 600 800 1,000

Production (Q)

in units of production

$50,000

Variable cost

Fixed cost

Cost-Volume-Profit Analysis

Total Costs (TC) = Fixed (FC) + Variable (VC)

TC= FC+VC

TC = FC + (VCunit * Q)TC

17

Co

sts

(C

)

0

10,000

20,000

30,000

40,000

200 400 600 800 1,000

Production (Q)

in units of production

$50,000

Variable cost

Fixed cost

Cost-Volume-Profit Analysis

Total Revenues (TR) = SP * Q

TC= FC+VC

TC = FC + (VCunit * Q)

TC

TR

TR= SP * Q

18

Co

sts

(C

)

0

10,000

20,000

30,000

40,000

200 400 600 800 1,000

Production (Q)

in units of production

$50,000

Variable cost

Fixed cost

Cost-Volume-Profit Analysis

TC= FC+VC

TC = FC + (VCunit * Q)

TC

TRTR= SP * Q

BEP

Q*

19

Co

sts

(C

)

0

10,000

20,000

30,000

40,000

200 400 600 800 1,000

Production (Q)

in units of production

$50,000

Variable cost

Fixed cost

Cost-Volume-Profit Analysis

TC= FC+VC

TC = FC + (VCunit * Q)

TC

TRTR= SP * Q

BEP

Q*

20

CVP analysis:

Example

Fixed costs per annum £ 60 000

Unit selling price £ 20

Unit variable cost £ 10

Relevant range 4 000 - 12 000 units

• Break-even point (in units) = Fixed costs

Contribution per unit

= £60 000/£10 = 6 000 units (within the relevant range)

• Units to be sold to obtain a desired (£40 000) profit:

Fixed costs + desired profit = £100 000/£10 = 10 000 units

Contribution per unit

Example : Cost-Volume-Profit Analysis

BREAK EVEN POINT

level of output

at which TC = TR

21

Cost-Volume-Profit Analysis

22

Cost-Volume-Profit Analysis