polymer logistics n.v. annual report as of · pdf filethe company reports its financial...

TRANSCRIPT

POLYMER LOGISTICS N.V.

ANNUAL REPORT

AS OF DECEMBER 31, 2014

POLYMER LOGISTICS N.V.

ANNUAL REPORT

AS OF DECEMBER 31, 2014

EUROS IN THOUSANDS

INDEX

Page

Report of the Board of Directors 1-6

Consolidated Balance Sheets 7-8

Consolidated Statements of Income 9

Consolidated Statements of Other Comprehensive Income 10

Consolidated Statements of Changes in Equity 11

Consolidated Statements of Cash Flows 12-13

Notes to Consolidated Financial Statements 14-48

Company Balance Sheet 49-50

Company Profit and Loss 51

Notes to the Company Financial Statements 52-57

Other Information 58

Independent Auditor’s Report 59

- - - - - - - - - - - - -

- - 1

Polymer Logistics N.V.

Year Ended December 31, 2014

Report of the board of directors

General

Polymer Logistics is a provider of 'one-touch' logistics solutions to leading retailers and suppliers in the UK,

Continental Europe and the US. It designs and supplies reusable 'Retail Ready Packaging' ("RRP") units that

function as both transport storage containers/pallets and in-store displays. The Group is a provider of pool

equipment services, supplying RRP units directly to retailers, or indirectly to major suppliers to retailers, through

rental agreements. Both methods are aimed at establishing long term rental relationships with customers. The

Group has ongoing supply and service arrangements with a number of key customers, which have continued for

up to 10 years and seeks to enter into contracts with new customers for terms typically between 2 and 6 years,

which in some cases include an automatic renewal policy. In addition to pooling services, the Group also develops

products for sale rather than rental.

The Company is based in The Netherlands with subsidiaries in the UK, Italy, Israel and the USA and a branch office

in Spain.

The Company has 220 employees as at December 31, 2014.

The Company reports its financial reports in Euro.

The Business

The Group develops and owns its RRP units and oversees the operation of the supply chain from suppliers to

retailers. Polymer Logistics provides a logistics solution, which begins in the supplier's packaging facility and

includes product transportation, quality inspections, cleaning and repairs, as well as inventory management

reports and invoicing provided by an online logistics system for all rental products.

By using the Group's RRP units, retailers can benefit from the following advantages over more traditional

methods of delivering products into the retail outlet:

• Increased in-store availability of stock, thereby promoting the opportunity for increased sales;

• Reduced supply-chain costs (i.e. replenishment, labor, transport, logistics);

• Reduced retail loss from damage and/or wastage; and

• Reduced packaging waste as Polymer Logistics' RRP units are reusable.

In addition, Polymer Logistics' products offer the following potential advantages to suppliers:

• Robust design and accurate dimensions of RRP units allowing automation in the filling process;

• Maximizing capacity of delivery vehicles thereby decreasing transport costs. Full RRP units are stacked en

route from supplier to retailer and, following delivery, are returned folded/nested from the retailer to the

supplier;

• RRP rental is charged on a per-use or per-trip basis enabling the supplier to take advantage of a variable cost

structure;

• The Group's logistics solutions enable the supplier to sub-contract responsibility for elements of the logistics

process to the RRP service provider;

• The Group commits to delivery of RRP units "in time" and "in place"; and

• An online tracking system capability is available to certain customers.

- - 2

Business model

Pooling

Polymer Logistics is primarily a third party supplier of pool management services of RRP, executed through

agreements with retailers and/or major suppliers to retailers. In marketing its pool management services, the

Group usually markets directly to the retail chain. Polymer Logistics' business model is based on being a high

quality service provider to its retail customers and suppliers, which requires intimate knowledge of its customers'

wants and needs.

Polymer Logistics works with its customers to identify packaging solutions to meet their specific requirements. In

this way, the Group can provide a tailor-made service to each customer while benefiting from the potential to

roll-out its designs to other retailers with similar requirements. The Group first identifies the specific needs of the

customer and then develops a product which is suitable for use by other customers in the same or other

industries. The development process is usually conducted in conjunction with a customer in order to allow for

regular feedback to the development team.

The rental pool model generates high recurring revenues and provides high revenue visibility for the Group. By

seeking to expand its product range for existing customers, recurring revenues have historically represented a

higher proportion of total pool revenues than revenues generated from new customer contracts and the

Directors believe this trend is set to continue in the near term.

Sales

The Group also develops products for sale to customers in retail for internal logistics and in other industries. The

division of revenues generated from rental pooling contracts compared to the sales (including financial leases)

has been approximately 72:28 of total Group revenues respectively (in 2013: 77:23).

Products

The Group works closely with its clients, from the initial conceptual briefing through to the various design and

production phases, in order to deliver a reusable 'one-touch' solution. The Group's product lines are used

primarily in the supermarket retail industry in the following market categories: fresh produce, beverages,

groceries and meat. Within each market category there are different pooling products, including bins, foldable

crates, trays and pallets, all of which are available to rent on a per-use or per-trip basis. Polymer Logistics' products are designed to increase the in-store availability of its customers' products, thereby

facilitating increased sales for the retailer. Furthermore, Polymer Logistics' products seek to utilize the capacity of

delivery vehicles by being stackable, foldable (bins and crates) and nestable and thereby providing an advantage

over traditional products, such as wooden pallets. The Group's products are designed to be easy to clean and are

robust in construction and are designed to ensure that products packed in them are well protected in order to

prevent damage and wastage of goods. Many of the Group's products (if required by the retailers' specifications) can be used with wheels to avoid the

need for using pallet jacks within the store. Pallet jacks tend to disturb consumer traffic in-store and can reduce

accessibility to shelves.

Research and Development

The Group attaches great importance to its Research and Development ("R&D") function and the Directors view it

as one of the Group's key strengths. The R&D function works closely with the Marketing Department once specific

customer needs have been identified and the teams regularly research the market in order to anticipate future

market needs. The Group's design teams aim to ensure its products are easy to use and maintain an aesthetic

appeal.

- - 3

Financial Highlights and Business Developments

A Summary of the key financial results for the year is:

• The total revenues in 2014 were €66.0m compared to €65.8m in 2013, a decrease of 6.6% in the rental

activity and an increase of 24.4% in the sales activity. The decrease in the rental activity resulted mainly from

a settlement agreement which resolved patent infringement actions in the UK done by a competitor and from

a settlement agreement due to change of terms with one of the subsidiaries' retailers in 2013. The increase in

the sales activity resulted mainly from the UK and Israeli markets.

• The company reported EBITDA of €10.1m for 2014 compared to €12.2m in 2013, a decrease of 17.2%.

• Total EBIT for 2014 was €1.8m compared to €4.3m in 2013 a decrease of 57.6%.

• Free cash-flow from operation in 2014 was €8.8m compared to €13.0m in 2013, resulting mainly from both

the decrease in profit and changes in operating assets and liabilities.

• The company invested €9.6m in fixed assets out of which €7.0m in rental equipment. Most other investments

were in the improvement of the Company’s service centers, contributing to the sustainable improvement in

operation performance.

• Main risks and sensitivities are detailed in note 21 to the financial statements.

Revenues from Pool and Sales

In 2014, the Company maintained its rental business.

The Company enjoyed a substantial increase in its sales activity in the UK and Israel but shows decrease in its sales

income in the US and the Spanish markets.

Investments

During 2014, the Company invested in increasing its pool equipment fleet mainly in the US, Italy and in the UK.

Total investment in pool equipment was €6.9m.

The Company had also supplemental investments in its wash-sites in the USA and Italy and in the production plant

in Israel. Total investments were €0.9m.

Other investments in equipment were mainly in molds for new products that supplement the Company's

products portfolio. Total investment was €1.4m.

Financing

The Group borrowed NIS 8,600 (€1,875) from two investment funds (affiliated to shareholders of the Company).

The loan are subordinated and secured by a 2nd rate debenture of Polymer Logistics (Israel) Ltd assets and are

repayable in 10 equal quarterly payments starting from December 31, 2016 and ending on March 31, 2019. The

loans bear an interest rate of 8.0% and are linked to the Israeli consumer price index.

As an incentive for the lenders to provide the loans, the Company will issue shares to the lenders which will

amount to 1.01% of the Company’s outstanding shares on a fully diluted basis against payment of their par value.

Based on market interest rates the Company assumed a value of €130 to the newly issued shares. As this value is

not material, the Company decided to allocate no value to the new shares and to allocate the full amount to the

loan instead.

The Company positive cash-flow from operation and its facilities with banks are supporting the Company's

investment needs.

The Company meets its bank covenants.

- - 4

Staff

Total number of employees on the 31st December 2014 was 220 (Israel-93, UK-53, Italy-22, USA-41, Holland-6 and

Spain-5).

Financial Risk Management Objectives and Policies

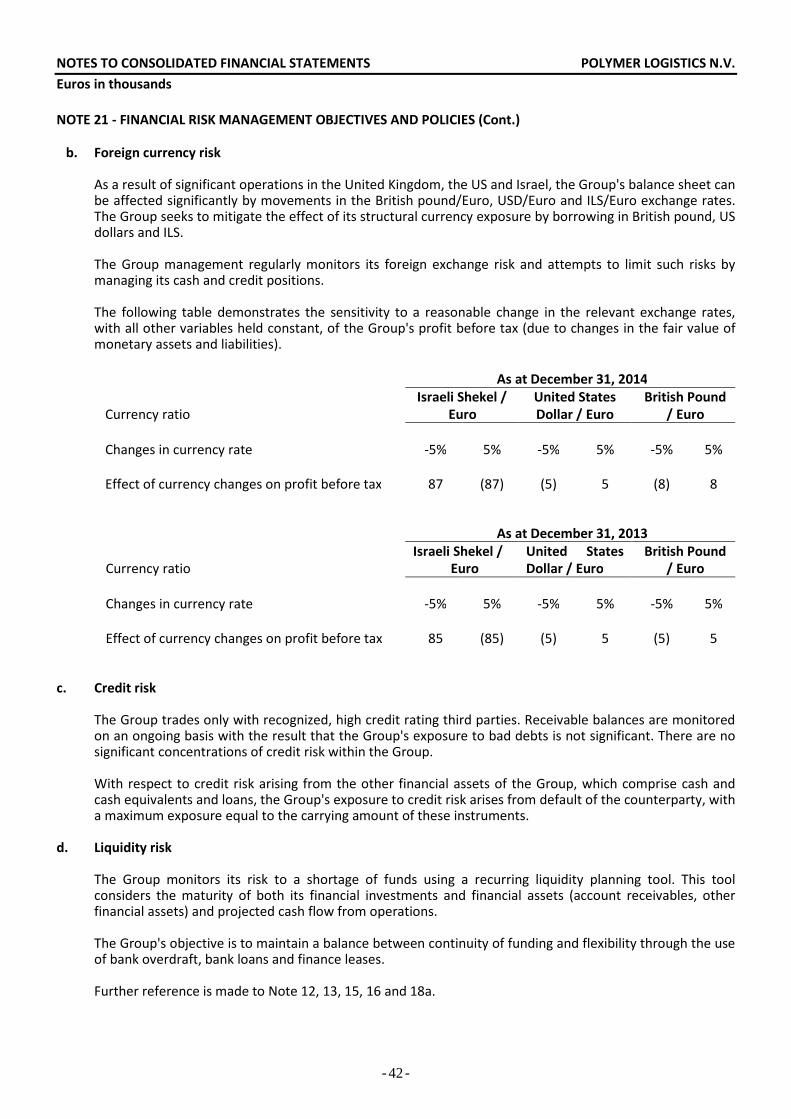

The main risks arising from the Group's financial instruments are cash flow interest rate risk, liquidity risk, foreign currency risk and credit risk.

Interest rates risk

The Group's exposure to the risk for changes in market interest rates relates primarily to the Group's long-term debt obligations with a floating interest rate. The Group's policy is to manage its interest cost using a mix of fixed and variable rate debts and short-term deposits at variable rates. Foreign currency risk As a result of significant operations in the United Kingdom, the US and Israel, the Group's balance sheet can be affected significantly by movements in the British pound/Euro, USD/Euro and ILS/Euro exchange rates. The Group seeks to mitigate the effect of its structural currency exposure by borrowing in British pound, US dollars and ILS. The Group management regularly monitors its foreign exchange risk and attempts to limit such risks by managing its cash and credit positions and also by Foreign exchange forward contracts. Credit risk The Group trades only with recognized, high credit rating third parties. Receivable balances are monitored on an ongoing basis with the result that the Group's exposure to bad debts is not significant. There are no significant concentrations of credit risk within the Group. With respect to credit risk arising from the other financial assets of the Group, which comprise cash and cash equivalents and loans, the Group's exposure to credit risk arises from default of the counterparty, with a maximum exposure equal to the carrying amount of these instruments. Liquidity risk The Group monitors its risk to a shortage of funds using a recurring liquidity planning tool. This tool considers the maturity of both its financial investments and financial assets (account receivables, other financial assets) and projected cash flow from operations. The Group's objective is to maintain a balance between continuity of funding and flexibility through the use of bank overdraft, bank loans and finance leases.

- - 5

Corporate Governance

Corporate Structure

The Company's head office is based in Dongen, the Netherlands.

The Company has 3 subsidiaries:

� Polymer Logistics (Israel) Ltd, established in 1992 - responsible for the R&D and production, and financial

management & controls.

� Polymer Logistics (UK) Limited, established in 2000 - responsible for the pool management in the UK and

sales activities;

� Polymer Logistics Srl, established in 2008 - converting the Italian branch into a limited Italian company,

responsible for the pool management in Italy.

Polymer Logistics (UK) Limited has one subsidiary:

� Polymer Logistics Inc., established in 2006 - responsible for the company pool management and sales

activity in the North America.

The Company also operates a branch in Spain.

Corporate Governance

The Directors are committed to maintaining a high standard of corporate governance in such respects as are

appropriate for a company of the size, nature and stage of development of the Company. The Board is

responsible for formulating, reviewing and approving the Company's strategy, budgets and corporate actions.

The Board

The Company's board of directors (the “Board”) as of December 31, 2014 comprised the non-executive Chairman,

the CEO, the CFO, and two additional non-executive directors. The non-executive directors are not involved in the

day to day management. Gender balance on the Board is 20-80, four members being men and one woman.

As of 1 January 2013 the Act on Management and Supervision (‘Wet Bestuur en Toezicht’) came into effect. With

this Act, statutory provisions were introduced to ensure a balanced representation of men and women in

management boards and supervisory boards of companies governed by this Act. Balanced representation of men

and women is deemed to exist if at least 30% of the seats are filled by men and at least 30% are filled by women.

Since the Company does not comply with the law in this respect, it has looked into the reasons for non-

compliance. The Supervisory Board recognizes the benefits of diversity, including gender balance. However, the

Supervisory Board feels that gender is only one part of diversity. Supervisory Board and Management Board

members will continue to be selected on the basis of wide ranging experience, backgrounds, skills, knowledge and

insights.

Non-executive directors are appointed for an initial period of three years terminable (a) by resolution of the

Company's shareholders with immediate effect; (b) by the director with one month notice; or (c) by the director

with immediate effect, in the event that the Company ceases to maintain reasonable directors' and officers'

liability insurance.

The ability to appoint and dismiss director’s falls within the authority of the Shareholders' Meeting of the

Company.

CONSOLIDATED BALANCE SHEETS POLYMER LOGISTICS N.V.

Euros in thousands

- - 7

December 31,

Note 2014 2013

ASSETS Current assets Cash and cash equivalents 3 1,268 729 Trade receivables 4 12,878 12,636 Other accounts receivable and prepayments 5 2,283 2,389 Income tax receivables 229 152 Inventories 6 4,403 3,970

21,061 19,876 Non-current assets Property, plant and equipment 7 17,926 19,464 Assets held for lease 8 54,750 53,123 Investment in a joint venture 9 657 - Finance lease receivable 10 - 4 Deposits 347 298 Deferred tax assets 11 1,807 1,725

75,487 74,614

Total assets 96,548 94,490

The accompanying notes are an integral part of the consolidated financial statements.

CONSOLIDATED BALANCE SHEETS POLYMER LOGISTICS N.V.

Euros in thousands

- - 8

December 31,

Note 2014 2013

EQUITY AND LIABILITIES

Current liabilities Bank borrowings and current maturities of long-term loans 12 13,780 9,534 Trade payables 13 11,914 12,300 Other accounts payable 14 4,291 3,975 Deposits from customers 15 4,817 4,202 Income taxes payable 18 16

34,820 30,027 Non-current liabilities Long-term loans 16 15,179 18,190 Deferred taxes liabilities 11 301 260 Other long-term liabilities 17 579 657

16,059 19,107

Total liabilities 50,879 49,134 Equity 19 Issued capital 804 779 Share premium 35,335 35,333 Foreign currency translation reserve 1,109 152 Retained earnings 8,421 9,092

Total equity 45,669 45,356

Total equity and liabilities 96,548 94,490

The accompanying notes are an integral part of the consolidated financial statements.

CONSOLIDATED STATEMENTS OF INCOME POLYMER LOGISTICS N.V.

Euros in thousands

- - 9

The accompanying notes are an integral part of the consolidated financial statements.

Year ended December 31,

Note 2014 2013

Revenues Rental income 22a 47,609 50,969 Sale of goods 18,437 14,820

66,046 65,789 Cost of revenues Cost of rentals 22b 30,828 30,319 Cost of goods sold 22c 14,277 11,205 Depreciation of molds, machines and factory 7 744 873

45,849 42,397

Gross profit 20,197 23,392

Selling and marketing expenses 22d 9,592 9,160 General and administrative expenses 22e 8,801 9,973 Finance income 22f (6) (93) Finance costs 22g 2,423 2,292 Other expenses, net 22h (20) 74 Share of profit from a joint venture 9 37 -

Profit (loss) before taxes (556) 1,986

Income tax expenses 11 115 92

Profit (loss) for the year (671) 1,894

Attributable to equity holders of the parent (671) 1,894

CONSOLIDATED STATEMENTS OF OTHER COMPREHENSIVE INCOME POLYMER LOGISTICS N.V.

Euros in thousands

- - 10

Year ended December 31,

2014 2013

Profit (loss) for the year (671) 1,894 Other comprehensive income Other comprehensive income to be reclassified to profit and loss in subsequent periods:

Exchange differences on translation of foreign operations 957 (282)

Net other comprehensive income to be reclassified

to profit and loss in subsequent periods 286 1,612

Attributable to equity holders of the parent 286 1,612

The accompanying notes are an integral part of the consolidated financial statements.

CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY POLYMER LOGISTICS N.V.

Euros in thousands

- - 11

Issued

Capital

Share

Premium

Foreign

Currency

Translation

Reserve

Retained

Earnings Total

At January 1, 2013 779 35,366 434 7,198 43,777

Profit for the year - - - 1,894 1,894

Other comprehensive income - - (282) - (282)

Total comprehensive income - - (282) 1,894 1,612

Payment on account of shares - 21 - - 21

Share-based payment - (54) - - (54)

At December 31, 2013 779 35,333 152 9,092 45,356

Profit (loss) for the year - - - (671) (671)

Other comprehensive income - - 957 - 957

Total comprehensive income - - 957 (671) 286

Issue of share capital 25 (21) - - 4

Share-based payment - 23 - - 23

At December 31, 2014 804 35,335 1,109 8,421 45,669

The accompanying notes are an integral part of the consolidated financial statements.

CONSOLIDATED STATEMENTS OF CASH FLOWS POLYMER LOGISTICS N.V.

Euros in thousands

- - 12

Year ended December 31,

2014 2013

Cash flows from operating activities

Net profit (loss) (671) 1,894

Adjustments necessary to reflect cash flows from operating activities (a) 9,430 11,069

Net cash flows provided by operating activities 8,759 12,963

Cash flows from investing activities

Purchase of assets held for lease (6,954) (7,407)

Purchase of property, plant and equipment (2,388) (3,127)

Investment in Joint venture (209) 269

Long-term deposits (49) 26

Net cash flows used in investing activities (9,600) (10,239)

Cash flows from financing activities

Proceeds from long-term loans from banks and others 4,228 17,612

Repayment of long-term loans from banks and others (6,244) (13,430)

Short-term bank credit, net 2,984 (6,684)

Issue of shares 3 21

Net cash flows provided by (used in) financing activities 971 (2,481)

Net increase in cash and cash equivalents 130 243

Net foreign exchange difference 409 (16)

Cash and cash equivalents at the beginning of the year 729 502

Cash and cash equivalents at the end of the year 1,268 729

The cash flows resulting from payments on finance lease receivables that are related to sales are presented as

operational cash flows.

The accompanying notes are an integral part of the consolidated financial statements.

CONSOLIDATED STATEMENTS OF CASH FLOWS POLYMER LOGISTICS N.V.

Euros in thousands

- - 13

Year ended December 31,

2014 2013

(a) Adjustments necessary to reflect cash flows from operating activities

Income and expenses not involving operating cash flows

Depreciation and amortization 8,323 7,927 Deferred taxes, net (41) 23

Exchange differences on long-term liabilities, net (18) (309) Loss (income) on disposal of property, plant and equipment and

assets held for lease 140 74 Share-based payment 23 (54)

8,427 7,661

Changes in operating assets and liabilities

Decrease in trade and finance lease receivables 625 194 Decrease (increase) in other receivables and prepayments (including

long-term) (834) 132

Decrease in inventories 743 1,938 Receipt of deposits from customers, net 615 531 Increase (Decrease) in trade and other accounts payables (68) 737 Decrease in other long-term liabilities (78) (124)

1,003 3,408

9,430 11,069

Non-cash activities

Depreciation of molds and machines capitalized to assets held for lease 1,336 1,380

Reassignment of assets held for lease into inventory 1,495 2,039

Supplemental disclosure of cash flows

Interest paid 1,808 1,855

Interest received 11 59

Taxes paid 184 251

Taxes received 29 247

The accompanying notes are an integral part of the consolidated financial statements.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS POLYMER LOGISTICS N.V.

Euros in thousands

- - 14

NOTE 1 - CORPORATE INFORMATION

Polymer Logistics N.V. ("the Company") and its subsidiaries ("the Group") specialize in developing, manufacturing and providing services for one-touch plastic packaging for the retail, industrial, and commercial markets. The Group's main markets are the UK, Italy and the USA. Its main product lines include plastic bins, crates, pallets and dollies for the retail market. The Company is a public limited liability company incorporated in the Netherlands. The Company's registered office is located at Bolkensteeg 25, 5103 AA Dongen, The Netherlands. In January 2014, the Company's subsidiary, Polymer Logistics Inc., and Denham Plastics established a joint venture, CleanTec Logistics LLC in Salinas, California in the US. This joint venture provides wash services for RPC's. The subsidiary owes 50% of the joint venture and each party will invest up to USD 1,100.

The Company profit and loss account is prepared under the application of Article 402, Book 2 of the Dutch Civil Code.

The consolidated financial statements of the Group for the year ended December 31, 2014 were authorized for issue in accordance with a resolution of the directors on April 2, 2015.

NOTE 2 - SIGNIFICANT ACCOUNTING POLICIES

2.1 Basis of preparation

The consolidated financial statements of the Group have been prepared in accordance with International Financial Reporting Standards ("IFRS") as issued by the International Accounting Standards Board (“IASB”).

The consolidated financial statements have been prepared on a historical cost basis, unless stated otherwise in the notes. The consolidated financial statements are presented in Euros and all values are rounded to the nearest thousand (€000).

2.2 Basis of consolidation

The consolidated financial statements comprise the financial statements of the Group and its subsidiaries as at December 31, 2014. Subsidiaries are fully consolidated from the date of acquisition, being the date on which the Group obtains control until the date such control ceases. The financial statements of the subsidiaries are prepared for the same reporting period as the parent company, using consistent accounting policies. All intra-group balances, transactions and unrealized gains and losses resulting from intra-group transactions are eliminated in full.

2.3 Significant accounting judgments, estimates and assumption

The preparation of the Group’s consolidated financial statements requires management to make judgments, estimates and assumptions that affect the reported amounts of revenues, expenses, assets and liabilities, and the accompanying disclosures, and the disclosure of contingent liabilities. Uncertainty about these assumptions and estimates could result in outcomes that require a material adjustment to the carrying amount of assets or liabilities affected in future periods. a. Judgments

In the process of applying the group's accounting policies, management has made the following judgments, which have the most significant effect on the amounts recognized in the financial statements:

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS POLYMER LOGISTICS N.V.

Euros in thousands

- - 15

NOTE 2 - SIGNIFICANT ACCOUNTING POLICIES (Cont.) Operating and finance lease commitments - Group as lessor The Group has entered into commercial equipment leases on its products portfolio. The group classified a lease as a finance lease if it transfers substantially all the risks and rewards incidental to ownership. A lease is classified as an operating lease if it does not transfer substantially all the risks and rewards incidental to ownership.

b. Estimates and assumptions The key assumptions concerning the future and other key sources of estimation uncertainty at the reporting date, that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial year, are described below.

Share-based payments The Group measures the cost of equity-settled transactions with employees by reference to the fair value of the equity instruments at the date at which they are granted. Estimating fair value for share-based payment transactions requires determination of the most appropriate valuation model, which is dependent on the terms and conditions of the grant. This estimate also requires determination of the most appropriate inputs to the valuation model including the expected life of the share option, volatility and dividend yield and making assumptions about them. The assumptions and models used for estimating fair value for share-based payment transactions are disclosed in Note 19. Deferred tax assets Deferred tax assets are recognized for all unused tax losses to the extent that it is probable that taxable profit will be available against which the losses can be utilized. Significant management judgment is required to determine the amount of deferred tax assets that can be recognized, based upon the likely timing and level of future taxable profits together with future tax planning strategies. Further details on Taxes are disclosed in Note 11b. Taxes There are estimation uncertainties with regard to tax positions taken by the Group which are only validated after tax audits. Assets held for lease The Company carefully examines its depreciation policy and considers various parameters which have material impact on its asset evaluation. The Company evaluates the residual value for each product group (bins, pallets, trays and crates) and their location (Europe or USA). The residual value is evaluated based on raw material cost and the Company regrinding costs.

2.4 Summary of significant accounting policies

a. Current versus non-current classification The Group presents assets and liabilities in the balance sheet based on current/non-current classification. An asset is current when it is: � Expected to be realized or intended to be sold or consumed in normal operating cycle � Held primarily for the purpose of trading � Expected to be realized within twelve months after the reporting period, or � Cash or cash equivalent unless restricted from being exchanged or used to settle a liability for at

least twelve months after the reporting period All other assets are classified as non-current. A liability is current when: � It is expected to be settled in normal operating cycle � It is held primarily for the purpose of trading � It is due to be settled within twelve months after the reporting period, or

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS POLYMER LOGISTICS N.V.

Euros in thousands

- - 16

NOTE 2 - SIGNIFICANT ACCOUNTING POLICIES (Cont.) � There is no unconditional right to defer the settlement of the liability for at least twelve months

after the reporting period The Group classifies all other liabilities as non-current. Deferred tax assets and liabilities are classified as non-current assets and liabilities.

b. Foreign currency translation The group’s consolidated financial statements are presented in Euros, which is also the parent company’s functional currency and its subsidiaries in Italy and Israel. The functional currency of the subsidiary in the UK is the British Pound and the functional currency of the subsidiary in the USA is the US Dollar. i) Transactions and balances

Transactions in foreign currencies are initially recorded by the Group entities at their respective functional currency spot rates at the date the transaction first qualifies for recognition.

Monetary assets and liabilities denominated in foreign currencies are retranslated at the functional currency spot rates of exchange at the reporting date. Differences arising on settlement or translation of monetary items are recognized to the income statement. Non-monetary items that are measured in terms of historical cost in foreign currency are translated using the exchange rates at the dates of the initial transactions.

ii) Group companies

On consolidation, the assets and liabilities of the subsidiaries in the UK and the USA are translated into Euros at the rate of exchange prevailing at the reporting date and their income statements are translated at exchange rates prevailing at the dates of the transactions. The exchange differences arising on translation for consolidation are recognized as other comprehensive income.

c. Revenue recognition

Revenue is recognized to the extent that it is probable that the economic benefits will flow to the Group and the revenue can be reliably measured, regardless of when the payment is being made. The specific recognition criteria described below must also be met before revenue is recognized. Sale of goods Revenues from the sales of goods is recognized when the significant risks and rewards of ownership of the goods have passed to the buyer, usually on delivery of the goods. Finance leases Revenues from finance leases where the Group substantially transfers the risks and rewards incidental to legal ownership and the Group is the manufacturer of the goods, are accounted as sales-type leases. The present value of minimum lease payments computed at a market rate interest is recorded as revenues. Unearned finance income is recognized over the term of the lease using the effective interest rate (EIR). Interest income is included in finance income in the income statement. Rental income Revenues from operating leases in which a significant portion of the risks and rewards of ownership are retained by the lessor are recognized over the term of the lease agreement or at the time that services are rendered.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS POLYMER LOGISTICS N.V.

Euros in thousands

- - 17

NOTE 2 - SIGNIFICANT ACCOUNTING POLICIES (Cont.)

d. Financial instruments - initial recognition and subsequent measurement

i) Financial assets

Financial assets are classified at initial recognition as financial assets at fair value through profit or loss, loans and receivables, held-to-maturity investments, AFS financial assets, or as derivatives designated as hedging instruments in an effective hedge, as appropriate. The Group determines the classification of its financial assets at initial recognition.

All financial assets are recognized initially at fair value plus transaction costs, except in the case of financial assets recorded at fair value through profit and loss.

Purchases or sales of financial assets that require delivery of assets within a time frame established by regulation or convention in the marketplace are recognized on the trade date.

The Group's financial assets include cash, trade and other receivables, loan and other receivables and derivative financial instruments.

The subsequent measurement of financial assets depends on their classification as described below:

Financial assets at fair value through profit and loss includes financial assets held for trading and financial assets designated upon initial recognition at fair value through profit and loss. Financial assets are classified as held for trading if they are acquired for the purpose of selling or repurchasing in the near term. Financial assets at fair value through profit and loss are carried in the balance sheet at fair value with gains or losses recognized in the income statement.

Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. Such financial assets are subsequently measured at amortized cost using the effective interest rate method (EIR), less impairment. Amortized cost is calculated by taking into account any discount or premium on acquisition and fees or costs that are an integral part of the EIR. The EIR amortization is included in finance income in the income statement. The losses arising from impairment are recognized in the income statement in finance costs for loans and in other operating expenses for receivables.

The Group assesses, at each reporting date, whether there is any objective evidence that a financial asset or a group of financial assets is impaired. A financial asset or a group of financial assets is deemed to be impaired if, and only if, there is objective evidence of impairment as a result of one or more events that has occurred after the initial recognition of the asset (an incurred ‘loss event’) and that loss event has an impact on the estimated future cash flows of the financial asset or the Group of financial assets that can be reliably estimated.

A financial asset is derecognized where the rights to receive cash flows from the asset have expired.

ii) Financial liabilities

Financial liabilities are classified, at initial recognition, as financial liabilities at fair value through profit or loss, loans and borrowings, payables or as derivatives designated as hedging instruments in an effective hedge, as appropriate. The Group determines the classification of its financial liabilities at initial recognition.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS POLYMER LOGISTICS N.V.

Euros in thousands

- - 18

NOTE 2 - SIGNIFICANT ACCOUNTING POLICIES (Cont.)

All financial liabilities are recognized initially at fair value and, in the case of loans and borrowings and payables, net of directly attributable transaction costs.

The Group's financial liabilities include trade and other payables, bank overdraft, loans and borrowings and derivative financial instruments.

The subsequent measurement of financial liabilities depends on their classification as described below:

Financial liabilities at fair value through profit and loss includes financial liabilities held for trading and financial liabilities designated upon initial recognition at fair value through profit and loss. Financial liabilities are classified as held for trading if they are incurred for the purpose of repurchasing in the near term. Financial liabilities at fair value through profit and loss are carried in the balance sheet at fair value with gains or losses recognized in the income statement.

Loans and borrowings - after initial recognition, interest-bearing loans and borrowings are subsequently measured at amortized cost using the EIR method. Gains and losses are recognized in the consolidated income statement when the liabilities are derecognized as well as through the amortization process.

A financial liability is derecognized when the obligation under the liability is discharged or cancelled or expires.

e. Derivative financial instruments and hedge accounting

Initial recognition and subsequent measurement The Group uses derivative financial instruments such as forward currency contracts and put/call options (hereinafter - "hedge instruments") to hedge its foreign currency fluctuations. Such derivatives financial instruments are initially recognized at fair value on the date on which a derivative contract is entered into and are subsequently remeasured at fair value. Derivatives are carried as financial assets when the fair value is positive and as financial liabilities when the fair value is negative. For the purpose of hedge accounting, hedges are classified as cash flows hedges when hedging exposure to variability in cash flows that is either attributable to a particular risk associated with a recognized asset or liability or a highly probable forecast transaction or the foreign currency risk unrecognized firm commitment. The Group uses forward exchange contracts and put/call options as hedges for its exposure for foreign currency risks of forecasted net cash-flows in the different currencies the Group is working with. Any gains or losses arising from changes in fair value on derivatives during the year are taken directly to the income statement.

f. Cash and cash equivalents

Cash and cash equivalents in the balance sheet comprise cash at banks and on hand and short-term deposits with an original maturity of three months or less.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS POLYMER LOGISTICS N.V.

Euros in thousands

- - 19

NOTE 2 - SIGNIFICANT ACCOUNTING POLICIES (Cont.)

g. Inventories

Inventories are valued at the lower of cost and net realizable value.

Costs incurred in bringing each product to its present location and conditions are accounted for as follows: Raw materials - using the average cost method. Work in progress and finished goods - using the average cost method which includes materials, labor, direct manufacturing expenses and other indirect expenses.

h. Trade receivables

Trade receivables, which generally have 30-90 days terms, are recognized and carried at original invoice amount less an allowance for any uncollectible amounts. A provision is recorded when there is objective evidence that the Group will not be able to collect the debts. Bad debts are written off when identified. As of December 31, 2014 and 2013, there is allowance for uncollectible accounts of € 137 and € 407, respectively. The Group has leased equipment to customers under a sales-type, finance lease. These receivables are recorded at their discounted contractual amounts. As of December 31, 2014 and 2013, there is no allowance for uncollectible accounts.

i. Leases

Operating lease is a lease of assets under which substantially all risks and rewards of ownership are effectively retained by the lessor. Group as a lessee Finance leases that transfer substantially all the risks and benefits incidental to ownership of the leased item to the Group, are capitalized at the commencement of the lease at the fair value of the leased property or, if lower, at the present value of the minimum lease payments. Lease payments are apportioned between finance charges and reduction of the lease liability so as to achieve a constant rate of interest on the remaining balance of the liability. Finance charges are recognized in finance costs in the income statement. A leased asset is depreciated over the useful life of the asset. Operating lease payments are recognized as an operating expense in the income statements on a straight-line basis over the lease term.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS POLYMER LOGISTICS N.V.

Euros in thousands

- - 20

NOTE 2 - SIGNIFICANT ACCOUNTING POLICIES (Cont.)

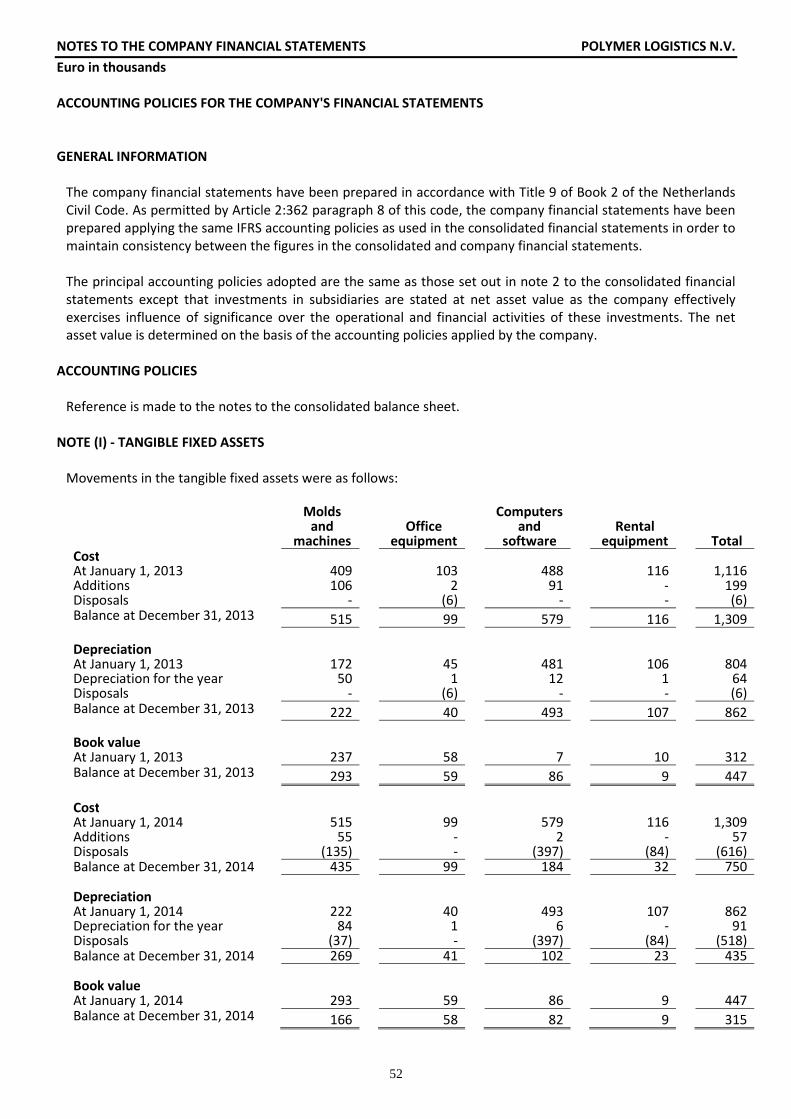

j. Property, plant and equipment

Property, plant and equipment are stated at cost, net of accumulated depreciation and accumulated impairment losses, if any. Such cost includes the cost of replacing part of the plant and equipment if the recognition criteria are met. All other repair and maintenance costs are recognized in the income statement as incurred.

Depreciation is calculated on a straight-line basis over the estimated useful lives of the assets as follows:

The carrying values of property, plant and equipment are reviewed for impairment when events or changes in circumstances indicate that the carrying value may not be recoverable. As for impairment, see note l below.

An item of property, plant and equipment is derecognized upon disposal or when no future economic benefits are expected from its use or disposal. Any gain or loss arising on derecognition of the asset (calculated as the difference between the net disposal proceeds and the carrying amount of the asset) is included in the income statement when the asset is derecognized.

The residual values, useful lives and methods of depreciation of property, plant and equipment are reviewed at each financial year end, and adjusted prospectively, if appropriate.

k. Assets held for lease

Assets leased to customers under operating leases are classified as assets held for lease. Assets held for lease are stated at cost less accumulated depreciation. Depreciation is computed (after deducting estimated residual value) using the straight-line basis over the estimated useful life of the asset. The annual depreciation rates are 10%-20%.

As for impairment, see l below.

l. Impairment of non-financial assets

The Group assesses, at each reporting date, whether there is any indication that an asset may be impaired. If any indication exists, or when annual impairment testing for an asset is required, the Group estimates the asset’s recoverable amount. An asset’s recoverable amount is the higher of an asset’s or cash-generating unit's (CGU) fair value less costs of disposal and its value in use. The recoverable amount is determined for an individual asset, unless the asset does not generate cash inflows that are largely independent of those from other assets or groups of assets. When the carrying amount of an asset or CGU exceeds its recoverable amount, the asset is considered impaired and is written down to its recoverable amount.

%

Machines 7.5-10

Molds 14-20

Furniture and fittings 6-15

Computers 20-33

Buildings 4

Motor vehicles 15

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS POLYMER LOGISTICS N.V.

Euros in thousands

- - 21

NOTE 2 - SIGNIFICANT ACCOUNTING POLICIES (Cont.)

m. Taxes

Current income tax Current income tax assets and liabilities are measured at the amount expected to be recovered from or paid to the taxation authorities. The tax rates and tax laws used to compute the amount are those that are enacted or substantively enacted, at the reporting date in the countries where the Group operates and generates taxable income.

Current income tax relating to items recognized directly in equity is recognized in equity and not in the income statement.

Deferred tax Deferred tax is provided using the liability method on temporary differences between the tax bases of assets and liabilities and their carrying amounts for financial reporting purposes at the reporting date. The carrying amount of deferred tax assets is reviewed at each reporting date and reduced to the extent that it is no longer probable that sufficient taxable profit will be available to allow all or part of the deferred tax asset to be utilized. Unrecognized deferred tax assets are reassessed at each reporting date and are recognized to the extent that it has become probable that future taxable profit will allow the deferred tax asset to be recovered. Deferred tax assets and liabilities are measured at the tax rates that are expected to apply in the year when the asset is realized or the liability is settled, based on tax rates (and tax laws) that have been enacted or substantively enacted at the reporting date. Deferred tax assets and deferred tax liabilities are offset if a legally enforceable right exists to set off current tax assets against current tax liabilities and the deferred taxes relate to the same entity and the same taxation authority. Taxes that would apply in the event of the realization of investments in subsidiaries have not been taken into account in computing the deferred taxes, as it is the Company's intention to hold these investments. Similarly, taxes that would apply in the event of the distribution of earnings by subsidiaries as dividends have not been taken into account in computing deferred taxes, when the distribution of a dividend does not involve an additional tax liability or when the Company is able to control the distribution of dividends that will cause an additional tax liability.

n. Severance pay

The Group liability for severance pay is calculated pursuant to the law in each subsidiary's country. The Group's liability is covered by monthly deposits to severance pay funds, insurance policies and by an accrual on the balance sheet. Deposits with severance pay funds and insurance policies are not under the control or administration of the Group, and accordingly, neither those amounts nor the corresponding liability are reflected in the consolidated financial statements.

o. Borrowing costs

Borrowing costs directly attributable to the production of an asset that necessarily takes a substantial period of time to get ready for its intended use or sale are capitalized as part of the cost of the asset. All other borrowing costs are expensed in the period they occur. Borrowing costs consist of interest and other costs that as entity insures in connection with the borrowing of funds.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS POLYMER LOGISTICS N.V.

Euros in thousands

- - 22

NOTE 2 - SIGNIFICANT ACCOUNTING POLICIES (Cont.)

p. Share-based payment transactions

In accordance with IFRS 2, "Share-based Payment", an expense is recognized when the Company buys goods or services in exchange for shares or rights over shares ("equity-settled transactions"), or in exchange for other assets equivalent in value to a given number of shares of rights over shares ("cash-settled transactions").

The cost of equity-settled transactions is measured by reference to the fair value at the date at which they were granted. The fair value is determined by using an option-pricing model.

The cost of equity-settled transactions is recognized, together with a corresponding increase in other reserves in equity, over the period in which the performance conditions are fulfilled, ending on the date the options vest.

q. Research and development

Research costs are expensed as incurred. Development expenditures on an individual project are recognized as an intangible asset when the group can demonstrate: � The technical feasibility of completing the intangible asset so that the asset will be available for

use or sale � Its intention to complete and its ability and intention to use or sell the asset � How the asset will generate future economic benefits � The availability of resources to complete the asset � The ability to measure reliably the expenditure during development

Following initial recognition of the development expenditure as an asset, the asset is carried at cost less any accumulated amortization and accumulated impairment losses. Amortization of the asset begins when development is complete and the asset is available for use. It is amortized over the period of expected future benefit. Amortization is recorded in cost of sale. During the period of development, the asset is tested for impairment annually.

2.5 Changes in accounting policies and disclosures

The Group applied, for the first time, certain standards and amendments that require restatement of

previous financial statements. These include IFRS 10 Consolidated Financial Statements, IFRS 11 Joint

Arrangements, and IAS 32 Financial Instruments - Presentation.

Several other amendments apply for the first time in 2014. [However, they do not impact the annual

consolidated financial statements of the Company.

The nature and the impact of each of the following new standards, amendments and/or interpretations are

described below:

• IFRS 10 Consolidated Financial Statements, effective 1 January 2014

• IFRS 11 Joint Arrangements, effective 1 January 2014

• IFRS 12 Disclosure of Interests in Other Entities, effective 1 January 2014

• IAS 27 Separate Financial Statements (revised 2011), effective 1 January 2014

• IAS 28 Investments in Associates and Joint Ventures (revised 2011), effective 1 January 2014

• Amendments to IAS 36 Impairment of Assets - Recoverable Amount Disclosures for Non-financial

Assets, effective 1 January 2014

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS POLYMER LOGISTICS N.V.

Euros in thousands

- - 23

NOTE 2 - SIGNIFICANT ACCOUNTING POLICIES (Cont.) 2.6 Standards issued but not yet effective

The standards and interpretations that are issued, but not yet effective, up to the date of issuance of the Group’s financial statements are disclosed below. The Group intends to adopt these standards, if applicable, when they become effective.

Amendments to IAS 1 Presentation of Financial Statements – Disclosure Initiative The amendments mark the completion of the five, narrow-focus improvements to disclosure requirements.

They are designed to further encourage companies to apply professional judgement in determining what

information to disclose in their financial statements. The amendments make clear that materiality applies

to the whole of financial statements and that the inclusion of immaterial information can inhibit the

usefulness of financial disclosures. Furthermore, the amendments clarify that companies should use

professional judgement in determining where and in what order information is presented in the financial

disclosures. The Company is currently assessing the impact of these improvements. The amendments

become effective for annual periods beginning on or after 1 January 2016. Early adoption is permitted.

IFRS 9 Financial Instruments

In July 2014, the IASB issued the final version of IFRS 9 Financial Instruments which reflects all phases of the financial instruments project and replaces IAS 39 Financial Instruments: Recognition and Measurement and all previous versions of IFRS 9. The standard introduces new requirements for classification and measurement, impairment, and hedge accounting. IFRS 9 is effective for annual periods beginning on or after 1 January 2018, with early application permitted. Retrospective application is required, but comparative information is not compulsory. Early application of previous versions of IFRS 9 (2009, 2010 and 2013) is permitted if the date of initial application is before 1 February 2015. The adoption of IFRS 9 will have an effect on the classification and measurement of the Group’s financial assets, but no impact on the classification and measurement of the Group’s financial liabilities.

IFRS 15 Revenue from Contracts with Customers

IFRS 15 was issued in May 2014 and establishes a new five-step model that will apply to revenue arising

from contracts with customers. Under IFRS 15 revenue is recognized at an amount that reflects the

consideration to which an entity expects to be entitled in exchange for transferring goods or services to a

customer. The principles in IFRS 15 provide a more structured approach to measuring and recognizing

revenue.

The new revenue standard is applicable to all entities and will supersede all current revenue recognition

requirements under IFRS. Either a full or modified retrospective application is required for annual

periods beginning on or after 1 January 2017 with early adoption permitted. The Group is currently

assessing the impact of IFRS 15 and plans to adopt the new standard on the required effective date.

Amendments to IAS 16 Property, Plant and Equipment and IAS 38 Intangible Assets – Clarification of

Acceptable Methods of Depreciation and Amortisation

The amendments are applied prospectively and clarify the principle in IAS 16 and IAS 38 that revenue

reflects a pattern of economic benefits that are generated from operating a business (of which the asset is

part) rather than the economic benefits that are consumed through use of the asset. As a result, a revenue-

based methods cannot be used to depreciate property, plant and equipment and may only be used in very

limited circumstances to amortise intangible assets. The amendments will have no impact on the

Company’s financial position and performance. The amendments become effective for financial years

beginning on or after 1 January 2016. Early adoption is permitted.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS POLYMER LOGISTICS N.V.

Euros in thousands

- - 24

NOTE 2 - SIGNIFICANT ACCOUNTING POLICIES (Cont.) Amendments to IFRS 11 Joint Arrangements: Accounting for Acquisitions of Interests

The amendments to IFRS 11 require that a joint operator accounting for the acquisition of an interest in a

joint operation, in which the activity of the joint operation constitutes a business must apply the relevant

IFRS 3 principles for business combinations accounting. The amendments also clarify that a previously held

interest in a joint operation is not remeasured on the acquisition of an additional interest in the same joint

operation while joint control is retained. In addition, a scope exclusion has been added to IFRS 11 to specify

that the amendments do not apply when the parties sharing joint control, including the reporting entity,

are under common control of the same ultimate controlling party.

The amendments apply to both the acquisition of the initial interest in a joint operation and the

acquisition of any additional interests in the same joint operation and are prospectively effective

for annual periods beginning on or after 1 January 2016, with early adoption permitted. These

amendments are not expected to have any impact to the Group.

Amendments to IAS 27: Equity Method in Separate Financial Statements

The amendments will allow entities to use the equity method to account for investments in

subsidiaries, joint ventures and associates in their separate financial statements. Entities already

applying IFRS and electing to change to the equity method in its separate financial statements

will have to apply that change retrospectively. For first-time adopters of IFRS electing to use the

equity method in its separate financial statements, they will be required to apply this method

from the date of transition to IFRS. The amendments are effective for annual periods beginning

on or after 1 January 2016, with early adoption permitted. These amendments will not have any

impact on the Group’s consolidated financial statements.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS POLYMER LOGISTICS N.V.

Euros in thousands

- - 25

NOTE 3 - CASH AND CASH EQUIVALENTS

December 31,

2014 2013

Cash at banks and on hand 1,268 729

The fair value of cash is €1,268 (2013: €729).

NOTE 4 - TRADE RECEIVABLES

Trade receivables are non-interest bearing and are generally on terms of 30 to 90 days.

As at December 31, the ageing analysis of trade receivables is, as follows:

Past due but not impaired

Neither past due

nor impaired

<30

days

30-60

days

60-90

days

>90

days

Doubtful

debts Total

2014 8,072 2,221 1,234 611 877 (137) 12,878

2013 8,619 2,968 391 167 898 (407) 12,636

The book value less provision for doubtful debt is the maximum exposure to credit risk. Further reference is made to Note 21c.

See below for the movements in the provision for doubtful debts:

December 31,

2014 2013

Balance at January 1 407 252

Charge for the year 68 183

Utilized debts (338) (28)

Balance at December 31 137 407

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS POLYMER LOGISTICS N.V.

Euros in thousands

- - 26

NOTE 5 - OTHER ACCOUNTS RECEIVABLE AND PREPAYMENTS

December 31,

2014 2013

Government authorities 1,029 518 Employees 56 18 Prepaid expenses 1,012 563 Income receivable 34 121 Current maturities of finance lease receivable (*) 148 1,015 Others 4 154

2,283 2,389 (*) See Note 10

NOTE 6 - INVENTORIES

December 31,

2014 2013

Raw materials 2,059 1,017

Work in progress 458 617

Finished goods 1,886 2,336

Total inventories at the lower of cost and net realizable value 4,403 3,970

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS POLYMER LOGISTICS N.V.

Euros in thousands

- - 27

NOTE 7 - PROPERTY, PLANT AND EQUIPMENT

Machines Molds

Furniture and

fittings Computers

Land and

building

Motor

vehicles Total Cost Balance at January 1, 2013 14,270 19,396 3,485 2,927 2,946 240 43,264Additions during the year 2,565 891 143 398 101 - 4,098Disposals during the year (404) - (70) (271) - (61) (806)Foreign currency translation adjustments (288) - (62) (14) - (7) (371)Balance at December 31, 2013 16,143 20,287 3,496 3,040 3,047 172 46,185 Accumulated depreciation Balance at January 1, 2013 5,785 13,304 1,413 1,880 701 65 23,148Additions during the year 1,320 1,878 331 436 151 28 4,144Disposals during the year (108) - (56) (274) - (17) (455)Foreign currency translation adjustments (61) - (24) (6) - (2) (93)Balance at December 31, 2013 6,936 15,182 1,664 2,036 852 74 26,744 Work in progress 23 - - - - - 23 Depreciated cost at December 31, 2013 9,230 5,105 1,832 1,004 2,195 98 19,464

Cost Balance at January 1, 2014 16,143 20,287 3,496 3,040 3,047 172 46,185Additions during the year 885 843 167 371 48 77 2,391Disposals during the year (1,520) (170) (60) (477) - (123) (2,350)Foreign currency translation adjustments 440 - 192 334 - 5 971Balance at December 31, 2014 15,948 20,960 3,795 3,268 3,095 131 47,197 Accumulated depreciation Balance at January 1, 2014 6,936 15,182 1,664 2,036 852 74 26,744Additions during the year 1,332 1,713 311 455 187 18 4,016Disposals during the year (964) (162) (9) (466) - (81) (1,682)Foreign currency translation adjustments 76 - 97 117 - (1) 289

Balance at December 31, 2014 7,380 16,733 2,063 2,142 1,039 10 29,367 Work in progress 96 - - - - - 96 Depreciated cost at December 31, 2014 8,664 4,227 1,732 1,126 2,056 121 17,926

€ 3,282 of the capitalized machines relates to finance leases (2013: € 3,812)

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS POLYMER LOGISTICS N.V.

Euros in thousands

- - 28

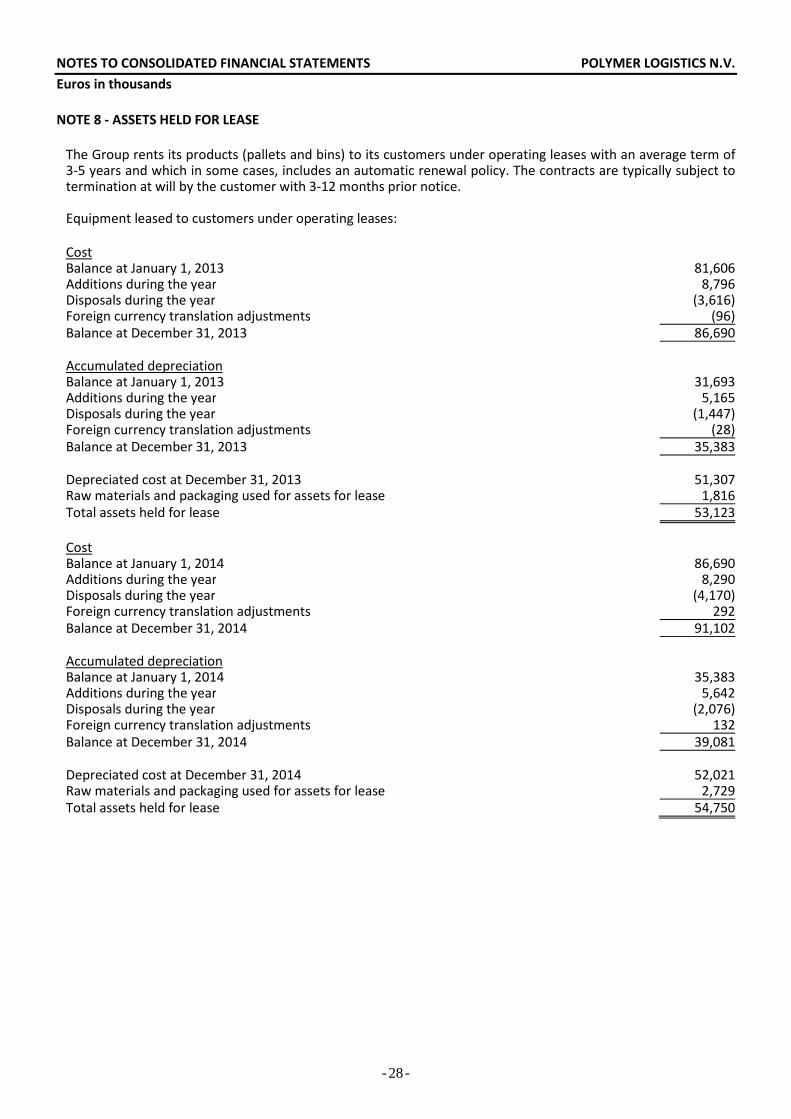

NOTE 8 - ASSETS HELD FOR LEASE

The Group rents its products (pallets and bins) to its customers under operating leases with an average term of 3-5 years and which in some cases, includes an automatic renewal policy. The contracts are typically subject to termination at will by the customer with 3-12 months prior notice.

Equipment leased to customers under operating leases:

Cost Balance at January 1, 2013 81,606 Additions during the year 8,796 Disposals during the year (3,616) Foreign currency translation adjustments (96) Balance at December 31, 2013 86,690

Accumulated depreciation Balance at January 1, 2013 31,693 Additions during the year 5,165 Disposals during the year (1,447) Foreign currency translation adjustments (28)

Balance at December 31, 2013 35,383 Depreciated cost at December 31, 2013 51,307 Raw materials and packaging used for assets for lease 1,816

Total assets held for lease 53,123

Cost Balance at January 1, 2014 86,690 Additions during the year 8,290 Disposals during the year (4,170) Foreign currency translation adjustments 292

Balance at December 31, 2014 91,102

Accumulated depreciation Balance at January 1, 2014 35,383 Additions during the year 5,642 Disposals during the year (2,076) Foreign currency translation adjustments 132

Balance at December 31, 2014 39,081

Depreciated cost at December 31, 2014 52,021 Raw materials and packaging used for assets for lease 2,729

Total assets held for lease 54,750

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS POLYMER LOGISTICS N.V.

Euros in thousands

- - 29

NOTE 9 - JOINT VENTURES

In January 2014, the Company's subsidiary, Polymer Logistics Inc., and Denham Plastics established a joint venture, CleanTec Logistics LLC in Salinas, California in the US. This joint venture provides wash services for RPC's. The subsidiary owes 50% of the joint venture and each party will invest up to USD 1,100. The joint venture has been accounted for in accordance with equity accounting and amounts to € 657 as per December 31, 2014. No unrecognized commitments to acquire the full interest, or any material contingent liabilities exist relating to CleanTec Logistics LLC.

NOTE 10 - FINANCE LEASE RECEIVABLE

The Group has leased equipment to customers under a sales-type finance lease with a term of six years, at a weighted average annual interest rate of 5.5%.

December 31,

2014 2013

Receivables from finance leases 148 1,019

Less - current maturities (included in other accounts receivable and prepayments) (148) (1,015)

- 4

Future lease payments receivable are as follows:

December 31,

2014 2013

First year 148 1,050

Second year - 4

Third year - -

Fourth year - -

Fifth year - -

Unearned finance income - (35)

148 1,019

NOTE 11 - TAXES ON INCOME

a. Taxes on income included in the statements of income

Year ended December 31,

2014 2013

Current taxes 65 157

Deferred taxes 50 2

Current taxes in respect of previous years - (67)

115 92

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS POLYMER LOGISTICS N.V.

Euros in thousands

- - 30

NOTE 11 - TAXES ON INCOME (Cont.)

b. Deferred taxes

Balance at

January 1, 2014

Amounts recorded in

statement of income

Amounts recorded in

capital reserve from

translation

Balance at

December 31, 2014

Property, plant and equipment (691) )14( )17( )722(

Employee benefit liabilities 51 9 - 60

Allowance for doubtful acc. 72 - - 72

Carry forward tax losses 1,789 31 50 1,870

Share based payments 59 - - 59

Change in tax rates 45 )24( - 21

Timing differences 18 - - 18

Intellectual property 40 )54( 60 46

IPO expenses 82 - - 82

Total 1,465 )52( 93 1,506

Balance at

January 1, 2013

Amounts recorded in

statement of income

Amounts recorded in

capital reserve from

translation

Balance at

December 31, 2013

Property, plant and equipment (430) (277) 16 (691)

Employee benefit liabilities 13 38 - 51

Allowance for doubtful acc. 34 38 - 72

Carry forward tax losses 1,516 293 (20) 1,789

Share based payments 67 (8) - 59

Change in tax rates 11 34 - 45

Timing differences 84 (66) - 18

Intellectual property 111 (48) (23) 40

IPO expenses 82 - - 82

Total 1,488 4 (27) 1,465

Presented in the balance sheet, as follows:

December 31,

2014 2013

Non-current assets 1,807 1,725

Non-current liabilities (301) (260)

1,506 1,465

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS POLYMER LOGISTICS N.V.

Euros in thousands

- - 31

NOTE 11 - TAXES ON INCOME (Cont.)

c. A reconciliation of theoretical tax expense assuming all income is taxed at the statutory rate applicable to

the income of companies in the Netherlands, and the actual tax expense is as follows:

December 31,

2014 2013

Profit before taxes, as reported in the consolidated statements of income (593) 1,986

Statutory tax rate in the Netherlands 25% 25%

Theoretical tax expense (148) 497

Increase (decrease) in taxes resulting from:

Non-deductible expenses (exempt income) (183) (296)

Items for which deferred taxes were not recognized 227 157

Adjustments in respect of currency difference for statutory tax purposes (1) (11) 248

Difference in statutory tax rates in various jurisdiction and other diff, net 237 (465)

Taxes in respect of prior years and others (7) (49)

115 92

(1) Polymer Logistics (Israel) calculates its taxable income in NIS.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS POLYMER LOGISTICS N.V.

Euros in thousands

- - 32

NOTE 11 - TAXES ON INCOME (Cont.)

d. The Group companies are subject to tax laws applicable in the countries which they operate. The principal tax rates applicable to the companies whose place of incorporation is outside the Netherlands are:

A company incorporated in Israel - See e below. A company incorporated in England - tax at the rate of 23.25%. A company incorporated in Italy - tax at the rate of 31.4%. A company incorporated in Spain - tax at the rate of 30%. A company incorporated in the USA - tax at the rate of 34%.

e. The tax laws applicable to the company incorporated in Israel ("PL Israel"):

Income Tax (Inflationary Adjustments) Law, 1985: According to the above law, the results for tax purposes are measured based on the changes in the Israeli CPI. PL Israel is taxed under this law. The Law for the Encouragement of Industry (Taxation), 1969: PL Israel has "industrial company" status as defined by this law. According to this status and by virtue of regulations published, PL Israel claims a deduction for accelerated depreciation on equipment used in industrial activity, as determined in the regulations effective under the Inflationary Law. The Law for the Encouragement of Capital Investments, 1959: According to the Law, PL Israel is entitled to tax benefits by force of the "Approved Enterprise" status granted to its enterprises, defined by this law. The principal benefits are:

1. Reduced tax rates

PL Israel has three approved programs in two different tracks (grant track and alternative track). Under the grant track, PL Israel has one program and will be entitled to a tax rate of 25% for a period of 10 years ending in 2008 in respect of the income that will be generated from the approved investments. Under the alternative track, PL Israel has two expansion programs and will be entitled to a tax exemption for a period of 10 years ending in 2012 and 2014 in respect of the income derived from the expansion of the enterprise.

If a dividend is distributed out of tax exempt profits, as above, PL Israel will then become liable for tax at the rate applicable to its profits from the "Approved Enterprise" in the year in which the income was accrued, had it not chosen the alternative track of benefits (tax at the rate of 25%). PL Israel's policy is not to distribute dividends out of these profits.

2. Conditions for the entitlement to the benefits:

The above benefits are conditional upon the fulfillment of the conditions stipulated by the Law, regulations published thereunder and the letters of approval for the specific investments in the approved enterprises. Non-compliance with the conditions may cancel all or part of the benefits and refund of the amount of the benefits, including interest. In management's estimation, PL Israel is complying with the aforementioned conditions.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS POLYMER LOGISTICS N.V.

Euros in thousands

- - 33

NOTE 11 - TAXES ON INCOME (Cont.)

3. Amendment to the Law for the Encouragement of Capital Investments, 1959:

In December 2010, the "Knesset" (Israeli Parliament) passed the Law for Economic Policy for 2011 and 2012 (Amended Legislation), 2011 ("the Amendment"), which prescribes, among others, amendments in the Law for the Encouragement of Capital Investments, 1959 ("the Law"). The Amendment became effective as of January 1, 2011. According to the Amendment, the benefit tracks in the Law were modified and a flat tax rate applies to the Company's entire preferred income under its status as a preferred company with a preferred enterprise. Commencing from the 2011 tax year, the Company can elect (without possibility of reversal) to apply the amendment in a certain tax year and from that year and thereafter, it will be subject to the amended tax rates. The tax rates under the amendment are: 2011 and 2012 - 15% (in development area A - 10%), 2013 - 12.5% (in development area A - 7%) and in 2014 and thereafter - 16% (in development area A - 9%). The Company apply the Amendment effective from the 2012 tax year.

NOTE 12 - BANK BORROWINGS AND CURRENT MATURITIES OF LONG-TERM LOANS

Weighted average interest % December 31,

2014 2013 2014 2013

a. Bank overdrafts

In NIS 3.73 4.10 1,441 1,100

In Euro 2.88 4.67 4,140 2,705

In British Pounds 3.02 (15) (258)

In US Dollar 3.98 (5) (294)

b. Loans from banks

In Euro 4.13 4.12 1,546 870

7,107 4,123

c. Current maturities of long-term loans 6,673 5,411

13,780 9,534

d. Bank overdrafts The bank overdraft facilities of the UK and the Israeli subsidiaries are secured by a floating charge over their assets. The overdraft facilities are renewed annually. Interest is calculated on the utilized facility only.

e. Bank loans Those loans are secured by a floating charge over certain of the Group's assets. The loans are renewed automatically unless the Company would like to change the loans terms.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS POLYMER LOGISTICS N.V.

Euros in thousands

- - 34

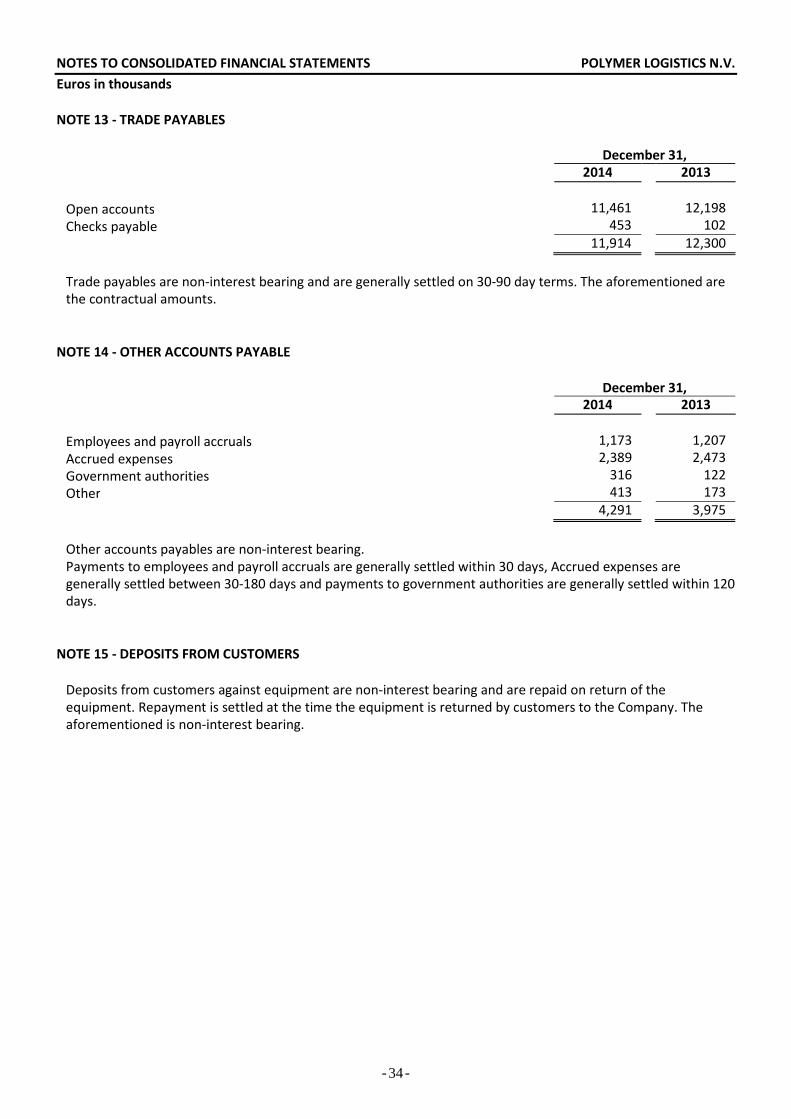

NOTE 13 - TRADE PAYABLES

December 31,

2014 2013

Open accounts 11,461 12,198

Checks payable 453 102

11,914 12,300

Trade payables are non-interest bearing and are generally settled on 30-90 day terms. The aforementioned are

the contractual amounts.

NOTE 14 - OTHER ACCOUNTS PAYABLE

December 31,

2014 2013

Employees and payroll accruals 1,173 1,207

Accrued expenses 2,389 2,473

Government authorities 316 122

Other 413 173

4,291 3,975

Other accounts payables are non-interest bearing.

Payments to employees and payroll accruals are generally settled within 30 days, Accrued expenses are

generally settled between 30-180 days and payments to government authorities are generally settled within 120

days.

NOTE 15 - DEPOSITS FROM CUSTOMERS

Deposits from customers against equipment are non-interest bearing and are repaid on return of the

equipment. Repayment is settled at the time the equipment is returned by customers to the Company. The

aforementioned is non-interest bearing.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS POLYMER LOGISTICS N.V.

Euros in thousands

- - 35

NOTE 16 - LONG TERM LOANS

a. Composition

Interest Rate December 31,

% 2014 2013

Euro - Suppliers 2.80-7.00 862 1,607 Euro - Bank Euro LIBOR + 3.50-4.66 (1) 10,792 12,865

British Pound - Bank LIBOR + 4.30 (2) 1,626 2,001

British Pound - Suppliers 5.40-6.96 17 66 Israeli Shekel - Bank Prime ILS + 0.71(3) 165 441

Israeli Shekel - Shareholders CPI + 8.00 6,893 5,041

US Dollar - Bank 3.60-3.65 1,464 1,543

US Dollar - Suppliers 3.50 33 37

21,852 23,601

LLess - current maturities (6,673) (5,411)

15,179 18,190

(1) The Euro LIBOR rate as of December 31, 2014 - 0.029% (2013: 0.117%). LIBOR is repriced on a monthly and

quarterly basis.

(2) The British Pound LIBOR rate as of December 31, 2014 - 0.453% (2013: 0.463%). LIBOR is repriced on a monthly

basis.

(3) The Israeli Shekel Prime rate as of December 31, 2014 - 1.75% (2013: 2.50%). PRIME is repriced on a quarterly

basis.

The aforementioned long-term loans represent the contractual amounts with suppliers and banks and do not include amortized costs.

In August 2014, the Group borrowed NIS 8,600 (€ 1,875) from two investment funds (affiliated to

shareholders of the Company). The loan is subordinated and secured by a 2nd rate debenture of Polymer

Logistics (Israel) Ltd assets and are repayable in 10 equal quarterly payments starting from December 31,

2016 and ending on March 31, 2019. The loan bear an interest rate of 8.0% and is linked to the Israeli

consumer price index.

As an incentive for the lenders to provide the loans, the Company will issue shares to the lenders which will

amount to 1.01% of the Company’s outstanding shares on a fully diluted basis against payment of their par

value.

Based on market interest rates the Company assumed a value of € 130 to the newly issued shares. As this

value is not material, the Company decided to allocate no value to the new shares and to allocate the full

amount to the loan instead.

b. As for charges, see Note 18b.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS POLYMER LOGISTICS N.V.

Euros in thousands

- - 36

NOTE 16 - LONG TERM LOANS (Cont.)

c. The following long-term loans are repayable in the years subsequent to December 31, 2014:

Fixed Rate

Floating

Rate

Total

Interest Shareholders Suppliers Banks Banks

2013

Year 1 - 719 682 3,990 5,391 2,437

Year 2 - 370 749 2,455 3,574 2,228

Year 3 492 249 769 2,294 3,804 2,087

Year 4 1,967 221 644 4,983 7,815 1,418

Year 5 &

after

2,588 153 196 80 3,017 587

Total 5,047 1,712 3,040 13,802 23,601 8,757

2014

Year 1 - 363 982 5,358 6,703 1,080

Year 2 689 206 1,009 5,083 6,987 697

Year 3 2,757 190 752 527 4,226 573

Year 4 2,757 128 236 86 3,207 198

Year 5 &

after

689

24

16

-

729

14

911 Total 6,892 911 2,995 11,054 21,852 2,562

d. The Company meets its bank covenants.

For further information, see Note 18c.

NOTE 17 - OTHER LONG-TERM LIABILITIES

December 31,

2014 2013

Accrued severance pay 370 332

Accrued expenses 209 325

579 657

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS POLYMER LOGISTICS N.V.

Euros in thousands

- - 37

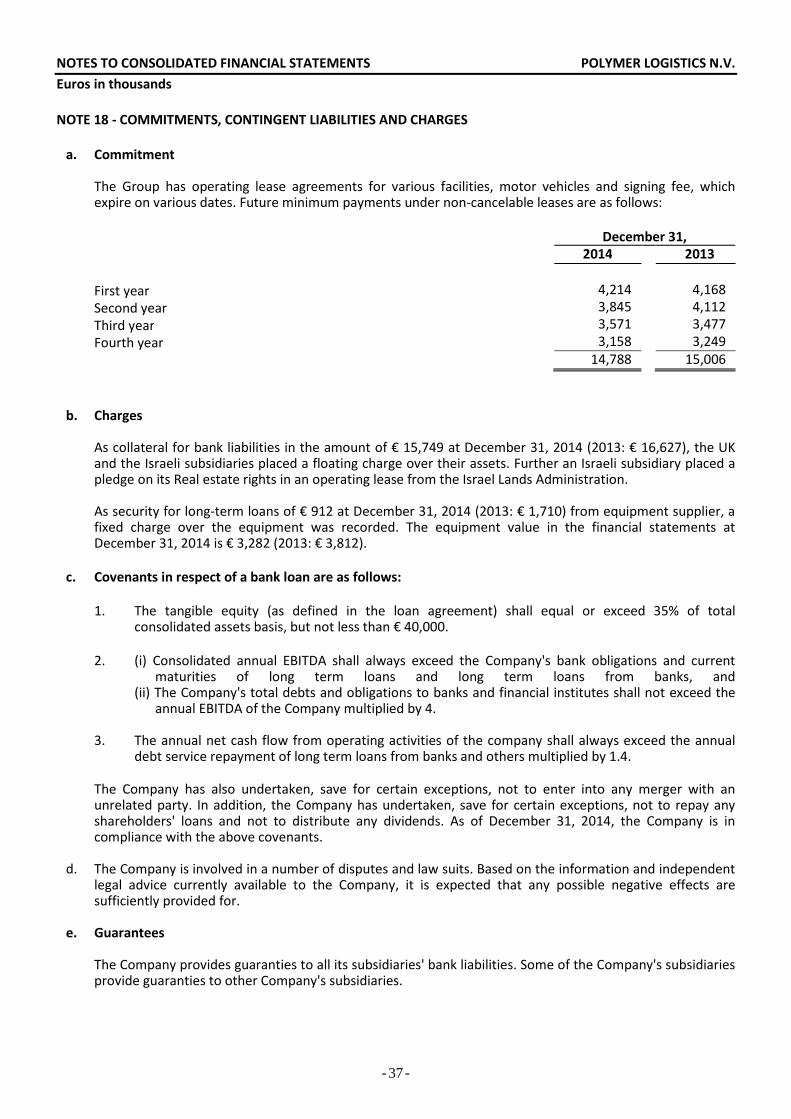

NOTE 18 - COMMITMENTS, CONTINGENT LIABILITIES AND CHARGES

a. Commitment The Group has operating lease agreements for various facilities, motor vehicles and signing fee, which expire on various dates. Future minimum payments under non-cancelable leases are as follows:

December 31,

2014 2013

First year 4,214 4,168

Second year 3,845 4,112

Third year 3,571 3,477

Fourth year 3,158 3,249

14,788 15,006

b. Charges

As collateral for bank liabilities in the amount of € 15,749 at December 31, 2014 (2013: € 16,627), the UK and the Israeli subsidiaries placed a floating charge over their assets. Further an Israeli subsidiary placed a pledge on its Real estate rights in an operating lease from the Israel Lands Administration. As security for long-term loans of € 912 at December 31, 2014 (2013: € 1,710) from equipment supplier, a fixed charge over the equipment was recorded. The equipment value in the financial statements at December 31, 2014 is € 3,282 (2013: € 3,812).

c. Covenants in respect of a bank loan are as follows:

1. The tangible equity (as defined in the loan agreement) shall equal or exceed 35% of total consolidated assets basis, but not less than € 40,000.

2. (i) Consolidated annual EBITDA shall always exceed the Company's bank obligations and current maturities of long term loans and long term loans from banks, and (ii) The Company's total debts and obligations to banks and financial institutes shall not exceed the annual EBITDA of the Company multiplied by 4.

3. The annual net cash flow from operating activities of the company shall always exceed the annual

debt service repayment of long term loans from banks and others multiplied by 1.4.

The Company has also undertaken, save for certain exceptions, not to enter into any merger with an unrelated party. In addition, the Company has undertaken, save for certain exceptions, not to repay any shareholders' loans and not to distribute any dividends. As of December 31, 2014, the Company is in compliance with the above covenants.