port development & expansion asia 2013 - tankedgetankedge.de/onewebmedia/port devolpment &...

TRANSCRIPT

Port Development & Expansion Asia 2013 Greenfield Port Construction – case study Karimun / Riau Province

04 December | 2013

Port Development & Expansion Asia 2013 Page | 2

I. OUR COMPANY

II. THE POTENTIAL OF INDONESIA

III. REGULATORY CHALLENGES

IV. SITE SELECTION

V. PT OILTANKING KARIMUN

VI. CLOSING

OVERVIEW

Port Development & Expansion Asia 2013 Page | 3

MARQUARD & BAHLS

I. OUR COMPANY

MARQUARD & BAHLS GROUP

More than 60 years in the international

and energy business

Key services encompassing oil trading,

tank terminal storage, aviation fuelling

and renewable energies

Headquartered in Hamburg and strategic

business presence in many parts of

Europe, The Americas, Africa & Asia

Port Development & Expansion Asia 2013 Page | 4

Marquard & Bahls Group

MARQUARD & BAHLS

Quality

Management

Marquard & Bahls AG

Tank Storage

Bunker Service

Retail Services

Aviation Service

Oil Trading

Biogas Solutions

Shareholdings

Port Development & Expansion Asia 2013 Page | 5

MARQUARD & BAHLS

Turnover (excluding petroleum tax) 17.1 billion EURO

Oil Trading Sales 22 million MT

Tank Capacity 20.2 million CBM

Tank Terminal Throughput 170.7 million MT

Employees 8,560

Key Figures FY 2012

Port Development & Expansion Asia 2013 Page | 6

I. OUR COMPANY

OILTANKING GROUP

An independent logistic service provider to

the oil and chemical industry

Specialized in tank storage and related

services

Storage and handling of dry bulk (UBT)

OILTANKING GROUP

Port Development & Expansion Asia 2013 Page | 7

OILTANKING GROUP

Our business includes:

Storing and handling bulk liquids & solids

Building and operating single and multi-users terminals

Managing logistic infrastructure

Providing uncommon customer service along with high

operational integrity

I. OUR COMPANY

OILTANKING GROUP

Port Development & Expansion Asia 2013 Page | 8

Tank Terminal & Port Network: Asia Pacific

Singapore (Chemical) Storage: 388,000 cbm

TANK TERMINAL NETWORK

Oil Terminal

Chemical Terminal

National Terminal Network

Representative Office

New project

Singapore (Petroleum) Storage: 1,870,000 cbm

Daya Bay, China Storage: 97,000 cbm

Nanjing, China Storage: 151,000 cbm

Merak, Java Indonesia Storage: 289,000 cbm

Karimun, Riau Indonesia Storage: 760,000 cbm

Port Development & Expansion Asia 2013 Page | 9

THE INDONESIAN MARKET

II. THE POTENTIAL OF INDONESIA

Population – 250.5 mln

(est 2013)

GDP (2012) – US$878b

GDP Growth – 6%

2008 : 6.0%

2009 : 4.6%

2010 : 6.1%

2011: 6.5%

2012: 6.2%

Per Capita (2010) – US$3,557

Unemployment Rate

2007 : 12.5%

2008 : 9.1%

2009 : 8.4%

2010 : 7.7%

2011: 6.6%

2012: 6.1%

Refining Industry

11 Refineries/1,165kbpd

Port Development & Expansion Asia 2013 Page | 10

II. THE POTENTIAL OF INDONESIA

Indonesia offers:

Young and growing population

Growing economy and wealth

Increase in energy consumption

Market entry for foreign companies to sell petroleum fuels

THE INDONESIAN MARKET

Port Development & Expansion Asia 2013 Page | 11

FUEL CONSUMPTION FORECAST

Max Domestic

Production:

40 million kl

(w/o future refineries)

60m 64m

76m

92m

107m

127m

+43.3%

FUEL CONSUMPTION

Source: Ministry of Energy & Mineral Resources

Port Development & Expansion Asia 2013 Page | 12

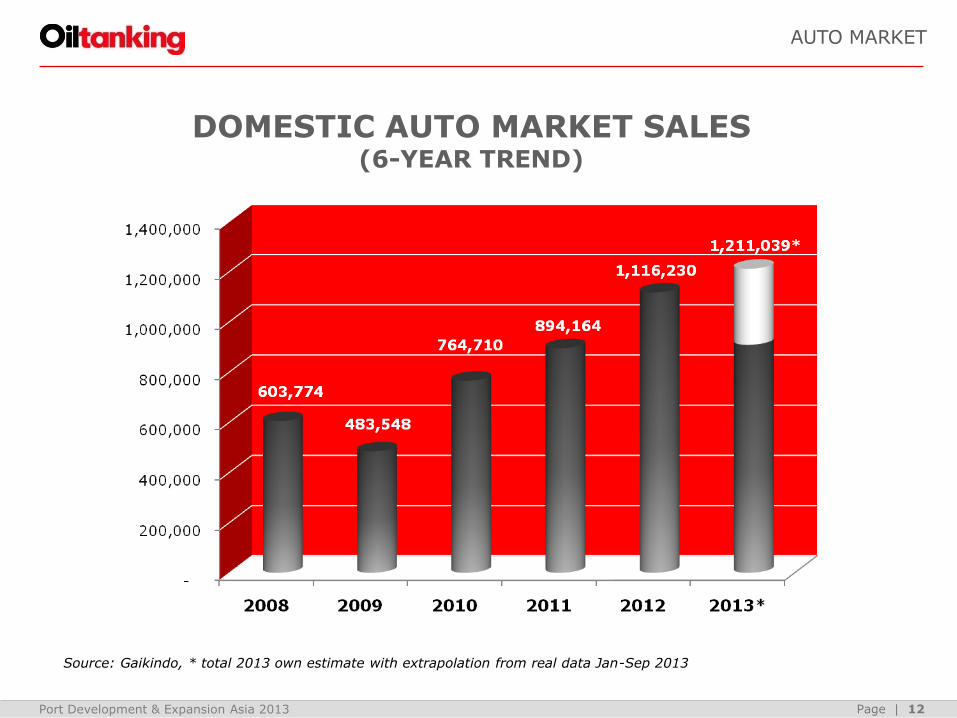

DOMESTIC AUTO MARKET SALES (6-YEAR TREND)

Source: Gaikindo, * total 2013 own estimate with extrapolation from real data Jan-Sep 2013

433,341

483,548

764,710

813,856

603,774

AUTO MARKET

Port Development & Expansion Asia 2013 Page | 13

REFINING CAPACITIES

II. THE POTENTIAL OF INDONESIA

Refining Capacities:

Now, Indonesia has 11 refineries

(ranging from 3.8 kbpd to 340 kbpd)

Designed capacity of 1.165m bpd but

actual main fuel production only approx

663k bpd (as per Pertamina’s annual report 2012)

Pertamina runs 5 of the largest refineries

Shell, Total and Petronas are developing

retail stations network

Clean Petroleum Product import terminals

mostly controlled by Pertamina

Shortage of Clean Petroleum Product

import terminals and ports, particularly in

Sumatra, Kalimantan and East Java

Company & Site CDUPT. Pertamina

Pangkalan Brandan* 4.5

Dumai 127.0

Sungai Pakning 50.0

Musi 127.3

Cilacap 348.0

Balikpapan 260.0

Balongan 125.0

Kasim 10.0

Non-PertaminaTPPI 100.0

Tri Wahana U 10.0

Pusdiklat Migas 3.8

Total 1,165.6

Port Development & Expansion Asia 2013 Page | 14

LAWS & REGULATIONS

III. REGULATORY CHALLENGES

Petroleum Market

BPH Migas / Downstream Regulatory Body of Oil & Gas

Deregulation of the downstream industry (Y2004 - …….)

Cutting of fuel subsidies

Free market access

Fair level playing field

Without deregulation

Fuel supply risk likely to increase

Potential bottlenecks in future expected (demand > supply)

Heavy burden on state budget remains

Port Development & Expansion Asia 2013 Page | 15

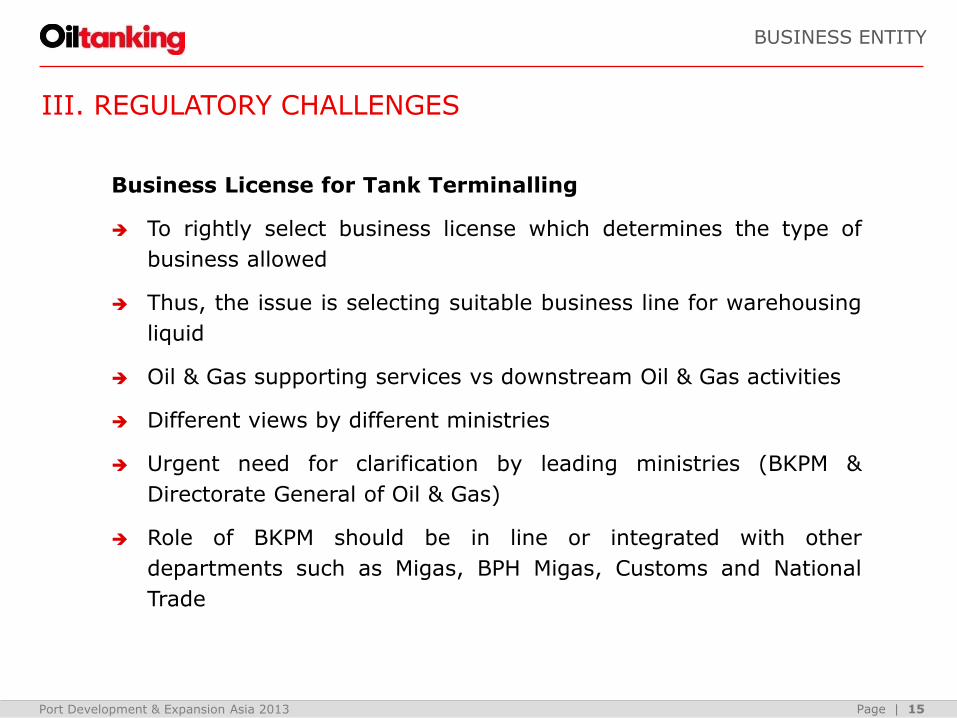

BUSINESS ENTITY

III. REGULATORY CHALLENGES

Business License for Tank Terminalling

To rightly select business license which determines the type of

business allowed

Thus, the issue is selecting suitable business line for warehousing

liquid

Oil & Gas supporting services vs downstream Oil & Gas activities

Different views by different ministries

Urgent need for clarification by leading ministries (BKPM &

Directorate General of Oil & Gas)

Role of BKPM should be in line or integrated with other

departments such as Migas, BPH Migas, Customs and National

Trade

Port Development & Expansion Asia 2013 Page | 16

SEA COMMUNICATION

III. REGULATORY CHALLENGES

Sea & Port

Adpel and local Port Master position merged into the new post of

Port Administrator

Considered more investor / operator friendly

Better coordination between local and national level expected

Local port service providers (BUP’s)

Regulation requires BUP to handle loading & unloading of cargo

Expertise for handling dangerous cargoes ?

BUPs have to work together with PELINDO as they have the expertise and equipment

International Maritime Organization (IMO) only acknowledges PELINDO as reputable port service provider

Port Development & Expansion Asia 2013 Page | 17

SEA COMMUNICATION

III. REGULATORY CHALLENGES

Sea & Port

Cabotage rules

Only Indonesian vessels can load cargo from domestic port and

discharge at another domestic port

Permits NO LONGER given to foreign fleet oil tankers for domestic

trade

Hence, owners and charterers need to employ only Indonesian

vessels

Issues:

Less flexibility for cargo owners

Availability of vessels

Competitive pricing

Attraction of investors likely to suffer

Port Development & Expansion Asia 2013 Page | 18

SEA COMMUNICATION

III. REGULATORY CHALLENGES

Sea & Port

Jetty permit (TUKS) for construction cum

operation

Investors to consider long permit

processing time into project scheduling

Adds uncertainty into a project

schedule/business case

TUKS versus appointed port in Free Trade

Zone area

Suitability of government appointed ports

to be reviewed

Port Development & Expansion Asia 2013 Page | 19

III. REGULATORY CHALLENGES

Operations

Bonded warehouse limitations outside of FTZ areas

Segregation of import & export tanks required in order to enjoy duty exemption

Not flexible and attractive for our customers

Not in line with international bonded warehouse practices

Local permits

National guidelines / regulations very broad

Permit duplication to suit both local and national level.

Eg. 1 - For fuel trade where BPH Migas collects a fee as well as local government (Pemda)

Eg. 2 - Storage license from Migas as well as depo permit from local level required

TERMINAL & PORT OPERATIONS

Port Development & Expansion Asia 2013 Page | 20

III. REGULATORY CHALLENGES

Operations

Ever changing permit requirements

Adds uncertainty into business planning

Discomforts shareholders

Makes investments in Indonesia less attractive

TERMINAL & PORT OPERATIONS

Port Development & Expansion Asia 2013 Page | 21

IN SUMMARY

III. REGULATORY CHALLENGES

In Summary

Implementation and integration of regulations can be still

improved

Inter-departmental corporation should be encouraged

Strive for STRONGER TOGETHER by closer corporation between

national and local level as well as investors

Port Development & Expansion Asia 2013 Page | 22

IV. SITE SELECTION

LOCATION

Criteria

THE right location

Feasibility of bonded warehouse / FTZ benefits

Land price

Deep-water access suitable for business case

Geotechnical conditions

Plot accessibility and sufficiency of public road infrastructure

Power and utility availability

Security on & offshore

Port Development & Expansion Asia 2013 Page | 23

IV. SITE SELECTION

LOCATION

Marine Environmental Factors

Wind and waves

Seismic and Tsunami risks

Tides and currents

Fishing grounds

Feasibility of dredging

Sedimentation tendency and trend

Underwater pipelines and cables

Port Development & Expansion Asia 2013 Page | 24

PORT OF KARIMUN

V. PT OILTANKING KARIMUN

Riau Province

Port Development & Expansion Asia 2013 Page | 25

V. PT OILTANKING KARIMUN

Riau Province

PORT OF KARIMUN

Port Development & Expansion Asia 2013 Page | 26

V. PT OILTANKING KARIMUN

Port Features – Highlights

Close proximity to Singapore oil hub

Part of the so called Greater Singapore Area recognized by Platt’s*

Strategically located along the Malacca Straits, the major oil route

from west to east

Post dredging water depth of -21mCD suitable for very large crude oil

vessels (VLCC)

Port services available (PELINDO I)

However, there is no established shipping channel yet to connect from

the Malacca Straits to our proposed jetty infrastructure…

*energy information & benchmark pricing assessment company

PORT OF KARIMUN

Port Development & Expansion Asia 2013 Page | 27

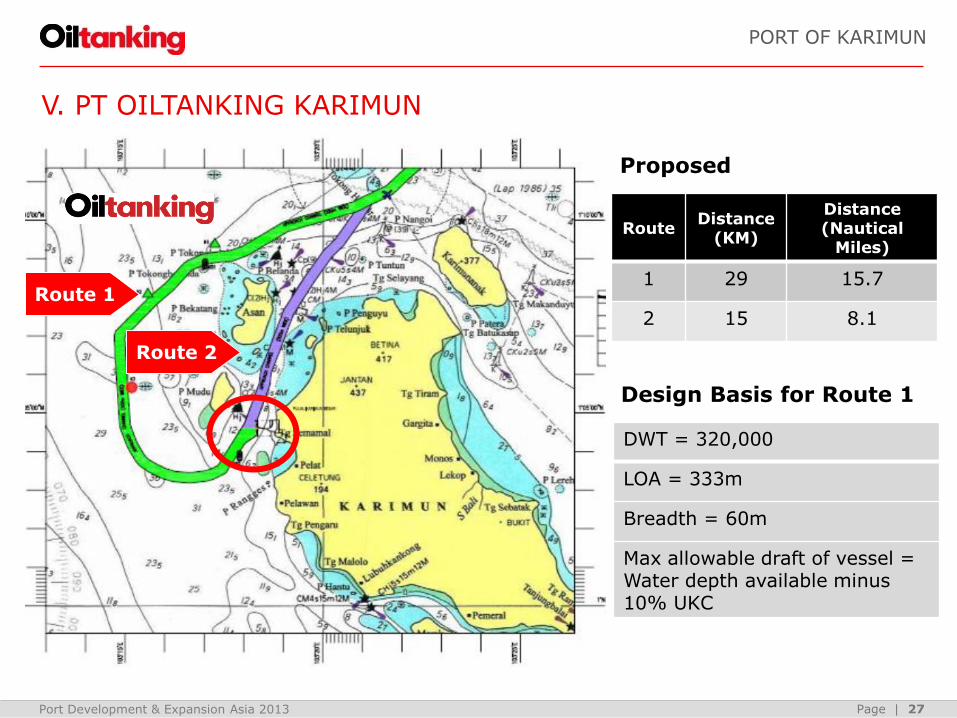

Route 1

PORT OF KARIMUN

Route Distance

(KM)

Distance (Nautical

Miles)

1 29 15.7

2 15 8.1

Route 2

V. PT OILTANKING KARIMUN

Proposed

Design Basis for Route 1

DWT = 320,000

LOA = 333m

Breadth = 60m

Max allowable draft of vessel = Water depth available minus 10% UKC

Port Development & Expansion Asia 2013 Page | 28

Parameter Formulae Remark

Design depth 1.1 x D UKC = 10%D

Width for 1-way traffic 5 x B Minimum

Width for 2-way traffic 10 x B Minimum

Diameter of turning basin 2 x L Minimum

Requirement on the channel navigational design based on recommendation

from PIANC:

D = Draft of vessel in metres

B = Beam of vessel in metres

UKC = Under Keel Clearance

PIANC = Permanent International Association of Navigation Congresses

PORT OF KARIMUN

V. PT OILTANKING KARIMUN

Port Development & Expansion Asia 2013 Page | 29

V. PT OILTANKING KARIMUN

Tanker Size

Definition

Deadweight

Tonnage

(dwt)

Length

Overall

(L)

Beam

(B)

Fully Laden

Draft

(D)

Design Depth

Required

(1.1D)

Small 15,000 150 22 9.0 9.9

Handymax 45,000 223 30 11.2 12.3

Panamax 75,000 250 36 13.6 15.0

Aframax 120,000 290 43 15.6 17.2

Suezmax 135,000 300 45 16.3 17.9

Suezmax 160,000 320 46 17.0 18.7

VLCC 200,000 325 50 18.0 19.8

VLCC 320,000 335 52 20.0 22.0

Typical Petroleum Tanker Dimensions

Port Development & Expansion Asia 2013 Page | 30

PORT OF KARIMUN

V. PT OILTANKING KARIMUN

Straits of Malacca

Straits junction and pilot boarding ground

Port Development & Expansion Asia 2013 Page | 31

V. PT OILTANKING KARIMUN

Issues encountered

Regulation No. PM 68 of Y2011 regarding ship channels states clearly

that government is supposed to provide and maintain shipping

channels but reality is that investors have to take action and provide

funding for:

AMDAL and dredging & dumping permits

Initial dredging scope

Annual channel bathymetric survey

Any maintenance dredging required thereafter

Provision, installation and maintenance of navigational aids

Consequence Competitive Disadvantage

PORT OF KARIMUN

Port Development & Expansion Asia 2013 Page | 32

PORT OF KARIMUN

V. PT OILTANKING KARIMUN

Proposed Jetty Capacities

Jetty Dwt LOA Design Depth

Required Water Depth

Available

1 75,000 240m -14mCD -18mCD

2 320,000 320m -25mCD -22mCD

3 15,000 150m -10mCD -16mCD

4 120,000 290m -17mCD -20mCD

Port Development & Expansion Asia 2013 Page | 33

VLCC

Aframax

Panamax

15,000 dwt

PORT OF KARIMUN

PHASE 1

PHASE 2

option land

V. PT OILTANKING KARIMUN

Port Development & Expansion Asia 2013 Page | 34

PORT OF KARIMUN

V. PT OILTANKING KARIMUN

Terminal Characteristics

Functions:

Import and Export by ship

Regional break bulk services

Break bulk services for Indonesia at large

International cargo trading terminal

Product range:

• Crude Oil

• Fuel Oil

• Gasoil

• Gasoline & Naphtha

• Gasoil & Diesel

• Jet Fuel & Kerosin

Port Development & Expansion Asia 2013 Page | 35

PORT OF KARIMUN

V. PT OILTANKING KARIMUN

Terminal Characteristics

Services

Storage in Free Trade Zone area

Break bulk capabilities

Redelivery to vessels/barges

Ship-to-ship transfer

Tank-to-tank transfer

Blending to specification

Additivation & dying

Circulation & homogenization

Heating of products (if required)

Port Development & Expansion Asia 2013 Page | 36

PORT OF KARIMUN

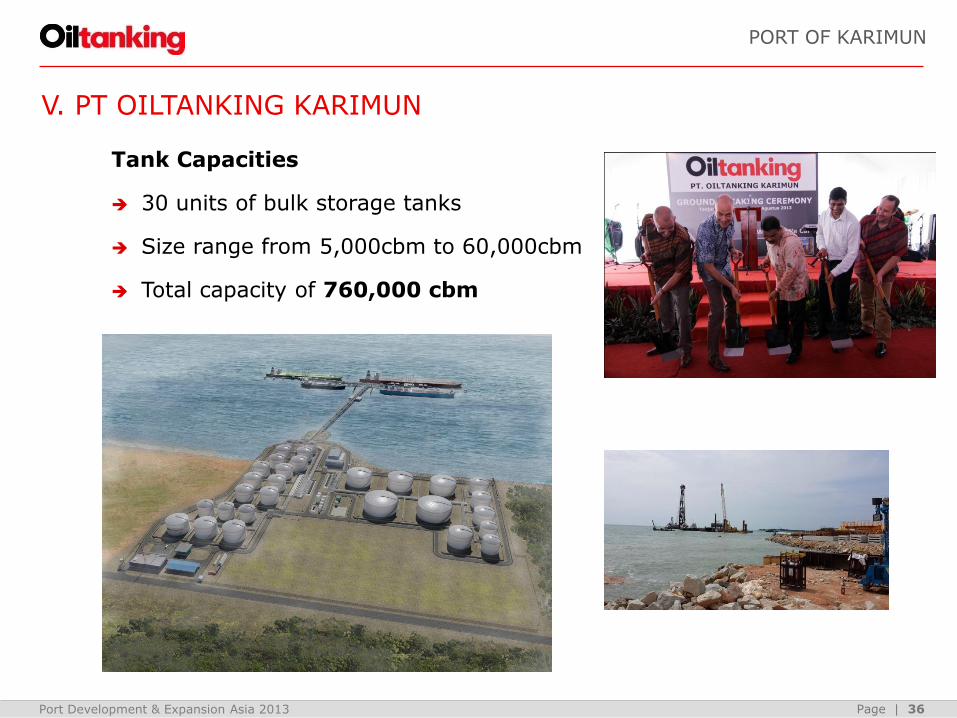

V. PT OILTANKING KARIMUN

Tank Capacities

30 units of bulk storage tanks

Size range from 5,000cbm to 60,000cbm

Total capacity of 760,000 cbm

Port Development & Expansion Asia 2013 Page | 37

V. PT OILTANKING KARIMUN

Performance Enhancements

VLCC capabilities in addition to Singapore port

HFO & crude oil handling

Creating economies of scale

Higher unloading & loading flow rates

Faster ship turn-around

Minimizing ship demurrage

Better utilization of onshore as well as

port assets

Dedicated pipeline concept

Lower risk of product contamination

Less downtime and resulting in higher

availability of infrastructure

PORT OF KARIMUN

Port Development & Expansion Asia 2013 Page | 38

VI. CLOSING

Take away’s

Deregulation of the Oil & Gas downstream industry still in progress

Permitting & licensing to be simplified

Increase in fuel consumption expected

Increase in product imports required to match future demand

Shortage of bulk tank storage facilities

Indonesia as alternative storage place for oil trading community

Demand for petroleum storage terminals

Demand for port facilities to feed terminals

Port Development & Expansion Asia 2013 Page | 39

Uncommonly well

Doing the Common