presentación institucional - santander.com on innovation to increase customer loyalty and ......

TRANSCRIPT

Santander Institutional Presentation

2017

2

Santander, a leading financial group

(*) Excluding Banco Popular

People (employees) 202,251

Branches 13,697

Market capitalisation (€ bill.; 29-12-17) 88

Shareholders (mill.) 4.0

Customers (mill.)* 133

Total balance sheet (€ trill.) 1.44

2016 Attributable profit (€ mill.) 6,204

Gross loans (€ bill.; w/o repos) 854

Customer deposits + mutual funds (€ bill.; w/o repos) 890

Communities (million people helped, 2017)* 2.1

2017 Attributable profit (€ mill.) 6,619

Key data 2017

3

Our purpose and business model

Aim and value creation

Corporate governance and Internal control

Group structure and business units

2017 Highlights – Results and Activity

Agenda

4

A model of sustainable, predictable growth

to help people and businesses prosper

to be the best retail and commercial bank, earning the lasting

loyalty of our people, customers, shareholders and communities

Our

purpose

Our aim

A bank

that is

Our model and the results it generates show that Santander is on the right track

5

Our strengths to continue to grow and to be successful in the long term

We have SCALE and the potential to grow organically

PREDICTABLE GROWTH: diversification by country and business,

which contributes higher profits in a more stable manner

Focus on INNOVATION to increase customer loyalty and

operational excellence

6

Spain 9%

SCF 15%

Poland 3%

Portugal 3%

UK 19%

Brazil 29%

Mexico 11%

Chile 3%

Argentina 3%

USA 4%Others 1%

02

Customers by country, Dec’17

133million customers

133 million customers in markets with a total population of more than one billion

15.217.3

Dec'16 Dec'17

Loyal customers (millions) Digital customers (millions)

20.925.4

Dec'16 Dec'17

Huge potential for organic growth throughincreased loyalty and digitalisation

Note: All figures excluding Banco Popular

+13%+21%

Our scale gives us efficiency, sources of growth and new business opportunities

SCALE

7

We are leaders in market share in five of our core markets

(1)Lending (2) UK mortgages (excluding Social Housing), Consumer credit and commercial lending (excluding Financial Institutions) (3) Including Santander Consumer Finance business (SCF) (4) In the states where the Group operates. (5) Including SCF UK (6) Including Banco Popular. Excluding it: 13% (7) Argentina and Portugal only include private sector banks.Data: Dec’17 or latest available. Branches do not include Santander Consumer Finance business

USA

Mkt. share1,4: 3%

Branches: 683

Argentina

Mkt. share1: 10%

Branches: 482

Mkt. share1: 16%

Branches: 563

PortugalBrazil

Mkt. share1: 9%

Branches: 3,465

UK

Mkt. share2: 10%

Branches: 808

Mkt. share1,6: 18%

Branches: 2,843

Spain

Mkt. share1: 19%

Branches: 439

Chile

Mkt. share1,3: 10%

Branches: 576

Poland

Mkt. share1: 13%

Branches: 1,401

Mexico

Nº countries5: 15

Branches: 546

SCF

7

SCALE

8

Our model is based on a balanced geographic diversification…

(*) Excluding Corporate Centre and Real Estate Activity Spain(1) Popular included (3%)

Underlying attributable profit 2017*

EuropeAmericas

48% 52%UK, 16%

Spain1; 15%

SCF, 13%

Portugal, 5%

Poland, 3%

USA, 4%

Mexico, 7%

Brazil, 26%

Chile, 6%

Argentina, 4%Other Latam, 1%

Balanced distribution between mature markets, which provide stability, and developing markets, which fuel growth in revenue

GROWTH

9

…with good business mix between products and segments…

Individuals demand deposits, 38%

Individuals time deposits, 13%

Individuals mutual funds, 14%Consumer, 4%

SMEs, 9%

Corporates, 13%

GCB, 9%

Other individuals, 11%

Home mortgages, 36%

Consumer, 18%

SMEs, 9%

Corporates, 15%

GCB, 11%

Note: Excluding Popular. Loans excluding repos. Customer funds: deposits excluding repos + marketed mutual funds

Loan portfolio by business Customer funds by business

Good mix between products for individuals, consumer finance, SMEs, companies and other products

€774bn €816bn

GROWTH

10

…is key to our stable and predictable growth

Profitability drivers

Pre-provision profit / loans

1.02% 1.36% 1.40% 1.65%

2.44%

1.69% 1.43% 1.25% 1.18% 1.07%

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

3.03% 3.28% 3.26% 3.25% 3.06% 2.94% 3.04% 2.90% 2.83% 2.97%

Note: 2017 figures include Popular.

Source: Bloomberg; Note: GAAP criteria Note: Standard deviation of the quarterly EPS starting from the first available data since Jan’99

Quarterly reported EPS volatility (Jan’99-9M´17)

4x6x1x2x3x2x5x1x-1x-9x1x

711% 358%

128% 113%92%

78%52% 46%

9%

44% 32%

Our unique business model allows us to deliver better results with less volatility and higher growth

Net income increase 1999-2016

EPS volatility calculated using quarterly date from Jan’99-Sep’17

GROWTH

Cost of credit

11

Our profitability allows us to grow, to accumulate capital and to pay dividends

+11% customer

revenues(2017 vs. 2016)

+29 bps10.84% FL CET1

(2017 vs. 2016)

Finance business growth Accumulate capital

GROWTH

+11% Cash dividend

per share (2017 vs. 2016)

Pay dividends

12

Focus on innovation to efficiently improve customer experience

• Santander ONE

• Consignado, 100% digital

• WebCasas

• New digital account opening process

• Investment Hub

• New app

• Digilosofía

• We are market leaders in mobile payments

• Súper Wallet

• Select Me

• Automatic service by bots

• Full digital On Boarding process

• WorkCafé

• Biometric voice solution aimed at large companies

• Electronic guarantees

INNOVATION

Blockchain

Payments

Data & A.I.

Platform &

Services

Focus on digital innovation

We have launched a wide array of initiatives at the bank

13

New digital solutions: agile global platforms

Superdigital

A digital mobile-first payment solution

Openbank

The fully digital bank

Santander Cash Nexus

An agile cash management platform

Machine learning

Global platform to know our customers better

• >1Mn customers

• +2.4x Revenues (2016-17)

• +26% Loyal customers

• +20% Deposit growth

• Single entry point

• Up to 75% workload reduction

• Open source platform and a team of

>100 data scientists

• Learning from >5Bn transactions

• Results obtained on >10Mn customers

INNOVATION

14

Digital transformation: simpler and more personalised and modern products & services…

Smart watch Pay

First bank to offer

smart watch payments

Santander App

Speak directly or set up a meeting

with your banker from your App

Facebook ChatBot

Real time assistant through

Facebook Messenger

INNOVATION

15

…increase digital sales, customer satisfaction and loyalty

Our digital transformation is paying off: as well as more digital

customers, we have more digital transactions and sales

Percentage of transactions and sales in digital channels Top 3 in customer satisfaction

39%of transactionsare digital

31%oftotal salesare digital

INNOVATION

16

Agenda

Our purpose and business model

Aim and value creation

Corporate governance and Internal control

Group structure and business units

2017 Highlights – Results and Activity

17

Aim and value creation

202,251employees

People

133million

Customers

4.0million

Shareholders

2.1million people helped in 2017

Communities

Note: Figures excluding Banco Popular, except number of employees and data on shareholders

Santander is a strong brand

Global Bank of the Year award(The Banker magazine)

6th best global Retail Banking brand (BrandZ ranking)

2nd most valuable bank brand in Europe(Brand Finance Banking 500 ranking)

Risk culture: risk pro

Risk pro defines the way in which we

understand and manage risks in our

day-to-day activities

>94%of employees recognise

and are responsible for the

risks in their daily work

18

Our people management strategy focuses on six key areas

I show

respectI truly listen

I talk

straight

I keep

promises

I actively

encourage

cooperation

I bring

passion

I support

people

I embrace

change

The SPF culture is based on our corporate behaviours

81%employees believe that their

colleagues behave in ways thatare more simple, personal and fair

77%employee

engagement rate in 2017People

Talent management

Knowledge and

development

Remuneration

and benefits

SystemsEmployee

experience

Culture

202,251employees

Dec'17

Our aim is to be

the best bank

to work for

Top 3 leading banks to work for in 5 countries

A new corporate management evaluation model

Global

engagement

survey

45%with university

degrees

55%women

60%what we do

40%how we do it

19

New digital solutions

Our value proposal aims to meet the needs of our different customer profiles

Operational excellence to maximise the bank’s efficiency and customer service quality

17.3 (+13%)million loyalcustomers

25.4 (+21%)million digitalcustomers

(1) Corporate benchmark of customer satisfaction

Innovative, simple, personalised solutions

Customers

Our value proposition for individual customers:

• A new global division: Santander Wealth Management

• A global solution making us partners in SMEs’ growth:

Note: All figures excluding Banco Popular

133millionDec’17

Openbank Santander

Cash NexusSuperdigital Machine

Learning

1|2|3 World Santander Plus As I Want it Account

Santander SMEs

New and redesigned branches

WorkCafé

Smart Red

Digital branch20% more productive

96% customer satisfaction

Increase brand visibility

Top 3 bank in seven countries in customer satisfaction1

20

+11%Cash dividend per

share growth in 20171

Among the best banks

in Europe by profitability

Share capital distribution

(By investor, 31-December-17)

Largest bank in the Eurozone

by stock market valueWe strengthened our capital

Group Strategy Update: sharing the bank's strategy

and outlook with analysts and investors

Chairman, CEO, CFO, UK, Brazil, Spain, USA,

Mexico and Country Heads of the rest of units

Increased shareholder remuneration, maintaining the payment of the four dividends

We offer our shareholders an attractive sustainable returnto maintain their lasting confidence

Shareholders

Note: All figures including Banco Popular. (1) Total dividends charged to 2017's earnings are subject to the Board and AGM approval.

New York, October 2017

4.0millionDec’17

+16.6%Total shareholder

return in 20171

Underlying RoTE

2017

11.8%

Market capitalisation

2017 year end

€88,410Mn

Fully loaded CET1

Dec’17

10.84%

Meeting ourcommitments

61%

1%

38%

Institutional investors

Board

Retail shareholders

21

Contributing to the economic and social progress of

people and businesses in a responsible and sustainable way

44,862scholarships

granted in 2017

1,295agreements with universities

and academic institutionsin 21 countries

Additional information in the 2017 sustainability report (click link )

Communities

In the DJSI socially responsible investment index

(since 2000) and in the FTSE4Good (since 2002)

Note: All figures refer to 2017 and exclude Banco Popular

2.1million people helped in 2017

Firm support of higher education

Community investment: we invest more in supporting

education than any other private company in the world

We support and promote financial inclusion

Firm commitment to the environment

Project finance

to support

renewable energies

€150 millionin microfinance loans

micro-entrepreneurs

supported

>250,000

3,390 MWTotal installed capacity of solar and wind generation supported by the Bank in 2017

22

Employees

Top 3 bank to work for

in the majority of our

geographies

Our 2017 performance makes us highly confident to meet our 2018 targets

(*) Except the US – approaching peers

People Customers1 Shareholders Communities

17 million loyal retail customers

1.6 million loyal SMEs and corporates

Customer loans growth above peers

All geographies top 3 in customer service*

30 million digital

customers (x2)

C. 10% CAGR of fee income 2015-2018

Cost / Income 45-47%

2015-2018 average cost of

credit: 1.2%

RoTE >11.5%

Increasing EPS, reaching double digit growth by 2018

30%-40% cash dividend pay-out: Yearly DPS increase

FL CET1 > 11%

People supported

in our communities:

5.0 mill. in 2016-18

c. 130k scholarships

in 2016-18

23

Agenda

Our purpose and business model

Aim and value creation

Corporate governance and Internal control

Group structure and business units

2017 Highlights – Results and Activity

24

11%

19%

33%36%

2011 2013 2015 2017

Corporate governance

Balanced Board

composition

Respect for

shareholders’ rights

Maximum transparency

in terms of remuneration

At the forefront of best practices

and long-term vision

Clear and robust governance, with well-defined accountabilities

and prudent management of risks and opportunities

Composition of the Board

Percentage of women on the Board

Non-executive directors(independent)

Executive directors

Non-executive directors(neither proprietary nor independent)

Proprietary non-executive directors(proprietary)

57%

22%

14%

7%

(*) Data as of 31/12/2017

25

Internal control framework

Parent-subsidiary governance model

The Group’s appointment and suitability assessment procedure is a key element of Governance

Presence of Santander Group in the Boards ofDirectors of the Subsidiaries and guidelines for Boarddynamics and effectiveness

Reporting of the CEO/ Country Heads to the GroupCEO and Group Executive Committee

Interaction between Group and Subsidiaries Control,Management and Business Functions

1

2

3

26

Agenda

Our purpose and business model

Aim and value creation

Corporate governance and Internal control

Group structure and business units

2017 Highlights – Results and Activity

27

Based on 9 markets and on the consumer finance business in Europe, supported by the Corporate Centre activities and other functions

Group structure

Units and businesses

USABrazilMexicoChileArgentina

UruguayPeru Colombia

Spain

Portugal

United Kingdom

SCF1

Poland

Asia Pacific

Representative offices

Global Corporate Banking

Group functions and Corporate Centre activities

(1) Santander Consumer Finance (SCF) with presence in Austria, Belgium, Denmark, Finland, France, Germany, Italy, the Netherlands, Norway, Poland, Portugal, Spain, Sweden, Switzerland and the UK

Communications, Corporate Marketing and Research

Technology and Operations

General Secretariatand Human Resources

UniversitiesCompliance & Conduct

Santander Digital

Internal Audit

Chairman’s Office and Strategy

Risk

Financial Accounting and Control

FinancialFin. Planning

& Corporate Development

Costs

Wealth Management

28

Spain – excl. Popular

(*) Million euros (**) Including Popular: 15%

Note: Loans excluding repos. Funds: deposits excluding repos + marketed mutual funds

Santander Spain maintains its loyalty-centred strategy and is makingprogress in its digital transformation

2017 Highlights

Branches 2,843

Employees 22,916

Loyal customers (millions) 1.9

Digital customers (millions) 3.2

Gross loans* 148,585

Customer funds* 251,196

Underlying attributable profit* 1,180

Contribution to Group’s profit** 12%

Bank of choice for SMEs and corporates

Integrate Banco Popular combining the best of both banks

Digital transformation to improve efficiency and the customer experience

Profitable, loyalty-based growth

Strategicpriorities

29

Santander Consumer Finance

(*) Million euros. Note: Loans excluding repos. Funds: deposits excluding repos + marketed mutual funds. Underlying profit does not include -€85Mn related to integration costs.(1) UK data considered in SAN UK; (**) Customers with an active contract

• Germany

• Spain

• Italy

• Portugal

• Poland

• France

• Finland

• Norway

• Sweden

• Denmark

• Netherlands

• Austria

• Belgium

• Switzerland

• UK1

SCF is the consumer finance leader in Europe, present in 15 European countries1

Branches 546

Employees 15,131

Customers** (millions) 19.9

Gross loans* 92,431

Customer funds* 35,398

Underlying attributable profit* 1,254

Contribution to Group’s profit 13%

Digital interaction

Mobile payments

Develop innovative products and digitalise the customer cycle processes

Maintain our leadership position

Implement open e-commerce platforms in the businesses and sign new agreements with distributors

Support the transformationof manufacturers and dealers

E-commerce open platform Awards

Strategicpriorities

2017 Highlights

30

Poland

(*) Million euros

Note: Loans excluding repos. Funds: deposits excluding repos + marketed mutual funds

Third bank in Poland reinforced by theacquisition of the retail and private banking

business of Deutsche Bank Polska

Branches 576

Employees 11,572

Loyal customers (thousands) 1,387

Digital customers (thousands) 2,089

Gross loans* 22,974

Customer funds* 27,803

Underlying attributable profit* 300

Contribution to Group’s profit 3%

Gain market share in volumesTop 3 in quality of service, increasing the number of loyal customers

Remain the leader in profitability

Remain the leader in digital channels in Poland

Strategicpriorities

2017 Highlights

31

Portugal – excl. Popular

(*) Million euros

Note: Loans excluding repos. Funds: deposits excluding repos + marketed mutual funds

Portugal’s most profitablebank with high market share

in loans and deposits

Branches 563

Employees 5,895

Loyal customers (thousands) 686

Digital customers (thousands) 558

Gross loans* 31,296

Customer funds* 32,213

Underlying attributable profit* 440

Contribution to Group’s profit 5%

Keep on gaining profitable market share

Integrate Banco Popular Portugal, improving efficiency

Deepen our digital transformation and streamline processes

Increase loyaltyStrategicpriorities

2017 Highlights

32

United Kingdom

(*) Million euros

Note: Loans excluding repos. Funds: deposits excluding repos + marketed mutual funds

One of the leading banks in thecountry, with an innovative value offering for

retail customers and small businesses

Branches 808

Employees 25,971

Loyal customers (millions) 4.2

Digital customers (millions) 5.0

Gross loans* 235,783

Customer funds* 210,305

Underlying attributable profit* 1,498

Contribution to Group’s profit 16%

Achieve profitability growth and a strong balance sheet

Increased customer loyalty as the key driver of business growth

Leverage our Investment Hub and increase cross-border customer relationship

Provide operational anddigital excellence through expertise and innovation

Strategicpriorities

2017 Highlights

33

Brazil

SantanderWay

(*) Million euros

Note: Loans excluding repos. Funds: deposits excluding repos + marketed mutual funds

Santander Brasil met its profitability target thanks to its customer-centred model and a strategy focused on profitable growth

Branches 3,465

Employees 47,135

Loyal customers (millions) 4.2

Digital customers (millions) 8.6

Gross loans* 74,341

Customer funds* 106,959

Underlying attributable profit* 2,544

Contribution to Group’s profit 26%

SMEs Agribusiness

Payrolls

Santander One

Risk and recovery management

Maintain a sustainable profit and solid organic growth

Continue the digital transformation in terms of innovative products and services

Gain market share in acquiring, consumer credit, SMEs, …

Strategicpriorities

2017 Highlights

34

Mexico

Select Me – Women proposition

(*) Million euros

Note: Loans excluding repos. Funds: deposits excluding repos + marketed mutual funds

The second largest bank in Mexico in terms of mortgages and loans to companies, and

the third largest in credit cards

Operational & IT transformation through digital platforms & investment plan

Branches 1,401

Employees 18,557

Loyal customers (thousands) 1,993

Digital customers (thousands) 1,948

Gross loans* 26,962

Customer funds* 35,548

Underlying attributable profit* 710

Contribution to Group’s profit 7%

Boost payrolls & strengthen Santander Plus offering to drive attraction & loyalty

Improve customerservice in all channels andthroughout the Bank

Consolidate our positioning in SMEs and recover leadership in mortgages

Strategicpriorities

2017 Highlights

35

Chile

(*) Million euros

Note: Loans excluding repos. Funds: deposits excluding repos + marketed mutual funds

Chile’s leading private sector bank in terms of assets and customers

Branches 439

Employees 11,675

Loyal customers (thousands) 622

Digital customers (thousands) 1,012

Gross loans* 38,249

Customer funds* 33,104

Underlying attributable profit* 586

Contribution to Group’s profit 6%

Strengthen business with large and medium sized companies through non-lending services

Consolidate commercial transformation via the new branch network model and digital banking

Boost growth among mass consumer market customers

Continue to improve the quality of customer attention and experience for individuals and SMEs

Strategicpriorities

2017 Highlights

36

Argentina

(*) Million euros. Note: Loans excluding repos. Funds: deposits excluding repos + marketed mutual funds(1) Incorporation of Citibank's retail portfolio into balance sheet on March 31st (P&L from 2Q’17)

The country’s leading private sector bank in terms of business market share following

the integration of Citibank's retail bank

Branches 482

Employees 9,277

Loyal customers (thousands) 1,340

Digital customers (thousands) 1,957

Gross loans* 7,608

Customer funds* 12,855

Underlying attributable profit* 359

Contribution to Group’s profit 4%

Growing loans sustaining profitability

Continue the transformation towards a fully digital bank

Develop business with the Public Sector and grow wealth management businesses

New Citi customers: focus on increasing profitability

Strategicpriorities

2017 Highlights

37

United States – excl. Popular

(*) Million euros (**) Santander Bank Note: Loans excluding repos. Funds: deposits excluding repos + marketed mutual funds. Underlying profit does not include -€76Mn related to hurricane provisions, increased stake in SC USA, tax reform and others

Santander US has built a strongpresence in the Northeast of the US

Branches 683

Employees 17,560

Loyal customers** (thousands) 303

Digital customers** (thousands) 814

Gross loans* 75,389

Customer funds* 59,329

Underlying attributable profit* 408

Contribution to Group’s profit 4%

Improve profitabilityImprove customer experienceand loyalty across segments

Continue to comply with regulatory expectations

Provide auto financing to allcustomer segments

Strategicpriorities

2017 Highlights

38

33%

25%

31%

11%

Global Transaction Banking

Global Debt Financing

Global Markets

Capital & Other

Underlying attributable profit* 1,821

Contribution to Group’s profit 20%

SGCB is the global business division for

corporate and institutional customers that

require a tailored service and

value-added wholesale products

2017 Highlights

Santander Global Corporate Banking (SGCB)

Revenuesbreakdown

(2017)

(*) Million eurosNote: excluding Banco Popular

Evolve towards a low capital consumption business

Capture international business flows between the countries in which the Group is present

Be the best bank for its customers in LATAM and Europe, with solid business units in the USA and Asia

Offer value-added products for specialised customers of the retail and commercialbanking network

Strategicpriorities

39

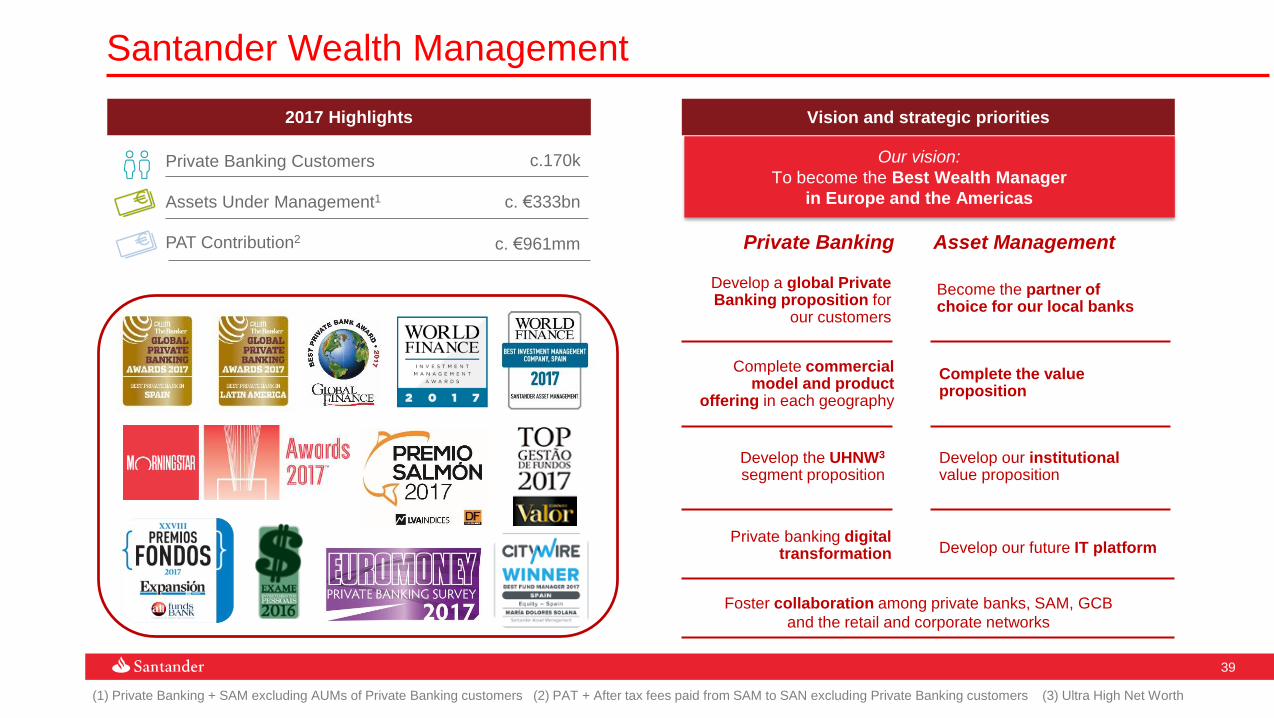

Santander Wealth Management

(1) Private Banking + SAM excluding AUMs of Private Banking customers (2) PAT + After tax fees paid from SAM to SAN excluding Private Banking customers (3) Ultra High Net Worth

Our vision:

To become the Best Wealth Manager

in Europe and the Americas

Develop a global Private Banking proposition for

our customers

Develop the UHNW3

segment proposition

Complete commercial model and product

offering in each geography

Private banking digital transformation

Become the partner of choice for our local banks

Complete the value proposition

Develop our institutionalvalue proposition

Develop our future IT platform

Private Banking Asset Management

Foster collaboration among private banks, SAM, GCB

and the retail and corporate networks

2017 Highlights

Private Banking Customers

Assets Under Management1

PAT Contribution2

c.170k

c. €333bn

c. €961mm

Vision and strategic priorities

40

Banco Popular

Santander acquires Banco Popular, strengthening its leadership

in Spain and Portugal

Strengthening of the franchise • The appointments of new members to the board of

directors and its committees

• A capital increase of Banco Santander of €7,072 million

to support the transaction. The issue was eight times

oversubscribed

• Strong deposit recovery since acquisition

• Disposal of 51% of Banco Popular’s RE business

• Loyalty bonds: €764Mn subscribed, 78% of the total

amount

• Agreement to sell TotalBank: estimated positive impact

in capital (+5 bps)

• Agreement with Labour Unions for the Corporate

Centre integration

Key figures and milestones of this acquisition

Expected return

on investment of

13-14% in year three

Largest bank

in Spain

~19% market share

in business

Portugal’s leading

private bank

~17% market

share in lending

Banco Santander + Banco Popular

41

Agenda

Our purpose and business model

Aim and value creation

Corporate governance and Internal control

Group structure and business units

2017 Highlights – Results and Activity

42

2017 Key achievements

GROWTH PROFITABILITY STRENGTH

+12% (+2% ex-Pop)

Loans1

c.12% (+70 bps)

Underlying RoTE

4.08% (+15 bps)

NPL ratio

+17% (+8% ex-Pop)

Customer funds1

€0.404 (+1%)

EPS

1.07% (-11 bps)

Cost of credit

€45,892Mn (+11%)

Customer revenues

€13,550Mn (+20%)

Underlying PBT

10.84% (+29 bps)

FL CET1

(1) % change in constant euros. Loans excluding repos. Funds: deposits excluding repos + marketed mutual funds

43

Note: Contribution to the SRF (net of tax) recorded in 2Q’16 and 2Q’17. Contribution to the DGF (net of tax) in 4Q’16 and 4Q’17.

Excellent quality and strong top-line growth with performance sustained QoQ

2,582 2,6082,836 2,913

7,6327,969

8,342 8,458

Net interest income 34,296 10 10

Net fees 11,597 14 13

Customer revenues 45,892 11 11

Other income 2,499 -3 -2

Gross income 48,392 10 10

Operating expenses -22,918 9 9

Net operating income 25,473 12 11

Net loan-loss provisions -9,111 -4 -6

Underlying PBT 13,550 20 21

Underlying attrib. profit 7,516 14 14

Net capital gains and provisions -897 115 117

Attributable Profit 6,619 7 7

€Mn Constant

eurosEuros

2017 % vs. 2016

1,6381,523

1,679 1,734 1,790 1,711

2,022 1,993

1,700

1,8541,909

1Q'16 2Q 3Q 4Q 1Q'17 2Q 3Q 4Q

635 535 519 560

1Q'16 2Q 3Q 4Q 1Q'17 2Q 3Q 4Q

NII

Fees

Other

Incl. Pop

Excl. Pop

Quarterly gross income performance excluding Popular (constant €Mn)

Underlying attributable profit (constant €Mn)

44

(€Mn, net of tax)

• Allfunds +297

• Integration processes -385

• Goodwill -603

• Other -206

• Total -897

Net interest income 34,296 10 10

Net fees 11,597 14 13

Customer revenues 45,892 11 11

Other income 2,499 -3 -2

Gross income 48,392 10 10

Operating expenses -22,918 9 9

Net operating income 25,473 12 11

Net loan-loss provisions -9,111 -4 -6

Underlying PBT 13,550 20 21

Underlying attrib. profit 7,516 14 14

Net capital gains and provisions -897 115 117

Attributable Profit 6,619 7 7

€Mn Constant

eurosEuros

2017 % vs. 2016

Results impacted by several one-offs, mainly related to integrations and goodwill

45

RoTE improves +70 bps YoY to c.12%

c.12%

9%

Global

Peers

Europe

8%

Local

peers avg.

12%

Americas

17%17%

(+1pp)

(+2pp)

(YoY)

Local

peers avg.

(YoY)

Source: Company data and Bloomberg. Note: RoTE as of 9M´17 for peers. Global Peers included in the average are Wells Fargo, JP Morgan, Bank of America, UBS, BBVA, ING, BNP Paribas, HSBC,

Unicredit, Lloyds, Citibank, Intesa Sanpaolo, Société Générale, Standard Chartered and Deutsche Bank. Santander vs peers average based on RoTEs in local criteria

Underlying RoTE

46

c.47%

64%

Our cost-to-income improves by 70 bps YoY to c.47%

Global

Peers

Source: Cost to income company data and Bloomberg. Note: Cost-to-income as of 9M´17 for peers. Peers included for average are Wells Fargo, JP Morgan, Bank of America, UBS, BBVA, ING, BNP

Paribas, HSBC, Unicredit, Lloyds, Citibank, Intesa Sanpaolo, Société Générale, Standard Chartered, Deutsche Bank and Barclays

Cost-to-income Top 3 in customer satisfaction

47

2016 2017

1.18

1.07

Loan-loss provisions: lower even though the loan portfolio increased

Better cost of credit at Group level… …and in most geographies

48

3.93 3.74 3.55 3.51 3.38

5.374.24 4.08

D'16 M'17 J'17 S'17 D'17

Including Popular

NPL ratio: The Group's ratio improved YoY for the 4th straight year (ex-Popular)

Group NPL ratio improving YoY… …backed by 8 geographies

49

Progress in reaching our target of fully-loaded CET1 >11% in 2018

10.5510.84

1.14

-1.14

0.53

-0.19 -0.05

Dec’16 Popular acquisition

Corporate transactions

Dec’17Capitalincrease

Organicgeneration

Markets& other

+0.29

Fully-loaded CET1 evolution

50

2017 Targets2017

Loyal customers (Mn) 1717

Digital customers (Mn) 2525

Fee income1 Increase13%

Cost of credit risk Improve1.07%

Cost-to-income Broadly stable47.4%

EPS (€) Increase0.40

DPS (€)2 Increase0.22

FL CET1 +40 bps+53 bps

RoTE3 Increase11.8%

Note: Customer metrics exclude Popular

(1) % change (constant euros) (2) Total dividends charged to 2017 earnings are subject to the Board and AGM approval (3) Underlying

(organic per year)

Delivered all strategic targets ahead of plan

51

Santander financial informationFor more details on the Group & countries, click below

Quarterly Financial Report

Group presentations:

Activity and Results

Units’ presentations

Investor Day 2015 Annual Report 2017 Group Strategy Update 2017

SCF

52

Banco Santander, S.A. ("Santander") cautions that this presentation contains statements that constitute “forward-looking statements” within the meaning of the U.S. Private Securities

Litigation Reform Act of 1995. Forward-looking statements may be identified by words such as “expect”, “project”, “anticipate”, “should”, “intend”, “probability”, “risk”, “VaR”, “RORAC”,

“RoRWA”, “TNAV”, “target”, “goal”, “objective”, “estimate”, “future” and similar expressions. These forward-looking statements are found in various places throughout this presentation

and include, without limitation, statements concerning our future business development and economic performance and our shareholder remuneration policy. While these forward-

looking statements represent our judgment and future expectations concerning the development of our business, a number of risks, uncertainties and other important factors could

cause actual developments and results to differ materially from our expectations. These factors include, but are not limited to: (1) general market, macro-economic, industry,

governmental and regulatory trends; (2) movements in local and international securities markets, currency exchange rates and interest rates; (3) competitive pressures; (4)

technological developments; and (5) changes in the financial position or credit worthiness of our customers, obligors and counterparties. Numerous factors, including those reflected in

the Annual Report on Form 20-F filed with the Securities and Exchange Commission of the United States of America (the “SEC”) –under “Key Information-Risk Factors”- and in the

Documento de Registro de Acciones filed with the Spanish Securities Market Commission (the “CNMV”) –under “Factores de Riesgo”- could affect the future results of Santander and

could result in other results deviating materially from those anticipated in the forward-looking statements. Other unknown or unpredictable factors could cause actual results to differ

materially from those in the forward-looking statements.

Forward-looking statements speak only as of the date of this presentation and are based on the knowledge, information available and views taken on such date; such knowledge,

information and views may change at any time. Santander does not undertake any obligation to update or revise any forward-looking statement, whether as a result of new information,

future events or otherwise.

The information contained in this presentation is subject to, and must be read in conjunction with, all other publicly available information, including, where relevant any fuller disclosure

document published by Santander. Any person at any time acquiring securities must do so only on the basis of such person's own judgment as to the merits or the suitability of the

securities for its purpose and only on such information as is contained in such public information having taken all such professional or other advice as it considers necessary or

appropriate in the circumstances and not in reliance on the information contained in the presentation. No investment activity should be undertaken on the basis of the information

contained in this presentation. In making this presentation available, Santander gives no advice and makes no recommendation to buy, sell or otherwise deal in shares in Santander or

in any other securities or investments whatsoever.

Neither this presentation nor any of the information contained therein constitutes an offer to sell or the solicitation of an offer to buy any securities. No offering of securities shall be

made in the United States except pursuant to registration under the U.S. Securities Act of 1933, as amended, or an exemption therefrom. Nothing contained in this presentation is

intended to constitute an invitation or inducement to engage in investment activity for the purposes of the prohibition on financial promotion in the U.K. Financial Services and Markets

Act 2000.

Note: Statements as to historical performance or financial accretion are not intended to mean that future performance, share price or future earnings (including earnings per share) for

any period will necessarily match or exceed those of any prior year. Nothing in this presentation should be construed as a profit forecast.

The businesses included in each of our geographic segments and the accounting principles under which their results are presented here may differ from the included businesses and

local applicable accounting principles of our public subsidiaries in such geographies. Accordingly, the results of operations and trends shown for our geographic segments may differ

materially from those of such subsidiaries.

Important Information

53

Important Information

In addition to the financial information prepared under International Financial Reporting Standards (“IFRS”), this presentation includes certain alternative performance

measures as defined in the Guidelines on Alternative Performance Measures issued by the European Securities and Markets Authority on 5 October 2015

(ESMA/2015/1415es) as well as Non-IFRS measures. The APMs and Non-IFRS Measures are performance measures that have been calculated using the financial

information from the Santander Group but that are not defined or detailed in the applicable financial information framework and therefore have neither been audited

nor are capable of being completely audited. These APMs and Non-IFRS Measures are been used to allow for a better understanding of the financial performance of

the Santander Group but should be considered only as additional information and in no case as a replacement of the financial information prepared under IFRS.

Moreover, the way the Santander Group defines and calculates these APMs and Non-IFRS Measures may differ to the way these are calculated by other companies

that use similar measures, and therefore they may not be comparable. For further details of the APMs and Non-IFRS Measures used, including its definition or a

reconciliation between any applicable management indicators and the financial data presented in the consolidated financial statements prepared under IFR, see

Section 26 of the Documento de Registro de Acciones for Banco Santander filed with the CNMV on July 4, 2017 (available on the Web page of the CNMV -

www.cnmv.es- and at Banco Santander -www.santander.com), Item 3A of the Annual Report on Form 20-F for the year ended December 31, 2016, filed with the U.S.

Securities and Exchange Commission on March 31, 2017 (the “Form 20-F”) and section Alternative Performance Measures of the Consolidated Directors’ Report

which is part of the 2017 Auditors’ Report and Annual Consolidated Accounts (available at Banco Santander –www.santander.com). For a discussion of the

accounting principles used in translation of foreign currency-denominated assets and liabilities to euros, see note 2(a) to our consolidated financial statements on

Form 20-F and to our consolidated financial statements available on the CNMV’s website (www.cnmv.es) and on Banco Santander’s website (www.santander.com).

Thank you

Our purpose is to help people and

businesses prosper.

Our culture is based on the belief that

everything we do should be