presentation at luiss university

TRANSCRIPT

Alitalia – Etihad Transaction Case Study

Presentation at Luiss University 1 December 2014

Alitalia (AZ) Summary Overview

The Birth of the “New” Alitalia

Alitalia – Compagnia Aerea Italiana (“CAI” or the “Company”) is a private company that started its

operations in January 2009

The Company currently flies to 103 destinations, of which 26 in Italy and 77 for the rest of the world, 186

routes and more than 4,700 weekly flights. In 2013:

– Carried 23 million passengers

– Generated €3.4 billion revenues

One of the youngest fleets in the world with an average age of 6.5 years

Alitalia is a member of the SkyTeam global alliance and, since 2010, forms part

with Air France-KLM and Delta Air Lines of the main air transport

Transatlantic Joint Venture

The Hub Fiumicino Airport

The Crew The Fleet

Source: Companies press releases and websites, news articles.

1

Alitalia: A Long Story of Difficulties Since 2000 Alitalia has cumulated negative results in excess of ca.€9.0bn, including ca.€3.0bn of liquidation costs related

to Alitalia – Linee Aeree Italiane.

Sources: Alitalia annual reports.

Note: (1) As estimated in the report “Alitalia – La privatizzazione infinita”; financial accounts FY2008 not available since on September 2008 Alitalia – Linee Aeree Italiane was declared insolvent and subject to a special bankruptcy

procedure termed extraordinary administration (“amministrazione straordinaria”). (2) Average of two Italian press news, namely “Ecco chi ha pagato il conto. Salvataggio da 3,2 miliardi” (Corriere della Sera, 8 August 2013) and

“Quanto costa chiudere Alitalia. In totale lo Stato pagherebbe direttamente circa 2,9 miliardi” (lavoce.info, 16 September 2008).

Net Income Evolution (€m)

Cumulated Net Income (€m)

Alitalia – Linee Aeree Italiane Alitalia – Compagnia Aerea Italiana

Net Income Evolution (€m)

Cumulated Net Income (€m)

In the period 2000 – 2008E, Alitalia – Linee Aeree Italiane

posted a cumulated net loss of ca.€4.7bn

According to Italian press news, the estimated liquidation cost

amounted to ca.€3.0bn(2)

In the period 2009 – 2013, Alitalia – Compagnia Aerea Italiana

posted a cumulated net loss of ca.€1.4bn

(256)

(907)

93

(512)

(844)

(168)

(626)

(495)

(1,000)

2000A 2001A 2002A 2003A 2004A 2005A 2006A 2007A 2008E

(327)

(168)

(69)

(280)

(569)

2009A 2010A 2011A 2012A 2013A

(327) (494) (563) (843)(1,411)

2009A 2010A 2011A 2012A 2013A

(256)(1,163) (1,070) (1,582)

(2,426) (2,594)(3,220) (3,715)

(4,715)

2000A 2001A 2002A 2003A 2004A 2005A 2006A 2007A 2008E

2

(1)

Alitalia: History Overview

Source: Companies press releases and websites, news articles.

Notes: (1) Scarcity of connections (rails sand highways) to the city of Milan and other main cities located in the Northern part of Italy. (2) Namely Fiumicino, Linate, Malpensa. (3) Italian State remained with a 49.7% stake. (4) Italian State

remained with a 64% stake.

1950: Alitalia

acquired Lati and

started serving also

LatAm

1946:

Incorporation of

Alitalia

Aereolinee

Italiane

Internazionali

1968: Awarded as 7th

airline globally and 3rd

in Europe, and

became the first

European airline to

have an all-jet fleet

1957:

Alitalia merged

with LAI and

became Alitalia

Linee Aeree

Italiane

2001: Alitalia entered

SkyTeam, joining Air

France, Delta Air

Lines, Korean Air,

Aeromexico and CSA

Czech Airlines

2000: Following the

Malpensa failure to

become an

international hub(1),

KLM decided not to

proceed the alliance

with AZ(2)

2003: Business plan

proposal for

recapitalization and

disposal of the stake

held by the Government

2000-2003:

Global drop in air

traffic. Strategic

refocus on

domestic hauls

End of 2006:

Government failure in

selling a 39.9% stake in

Alitalia, with all the 11

potential buyers

withdrawing their bids

2007: AF – KLM

selected as

potential

candidate to take

over Alitalia

1970-1990: All

airlines except

Alitalia developed

industrial plans to

face the oil crisis

1996: Italian state

disposed 21%

stake to employees

and listed a 15%

stake(4)

1946 – 1970 1970 – 1990 1990 – 2000 2000 – 2006 2007

Early stage growth Deregulation /

Oil Crisis First privatisation

Attempts to relaunch the business through several

industrial plans

Second and third

privatisation attempts

(failed)

Established as State-owned company, Alitalia grew in the early decades up to face the first difficulties following the

deregulations of the sector and the higher competition in the domestic market

2003-2004: Proposed a

new business plan

(Alitalia daily lost €1m).

Italian State provided a

€400m bridge financing

and disposed a 12.3%

stake(3)

3

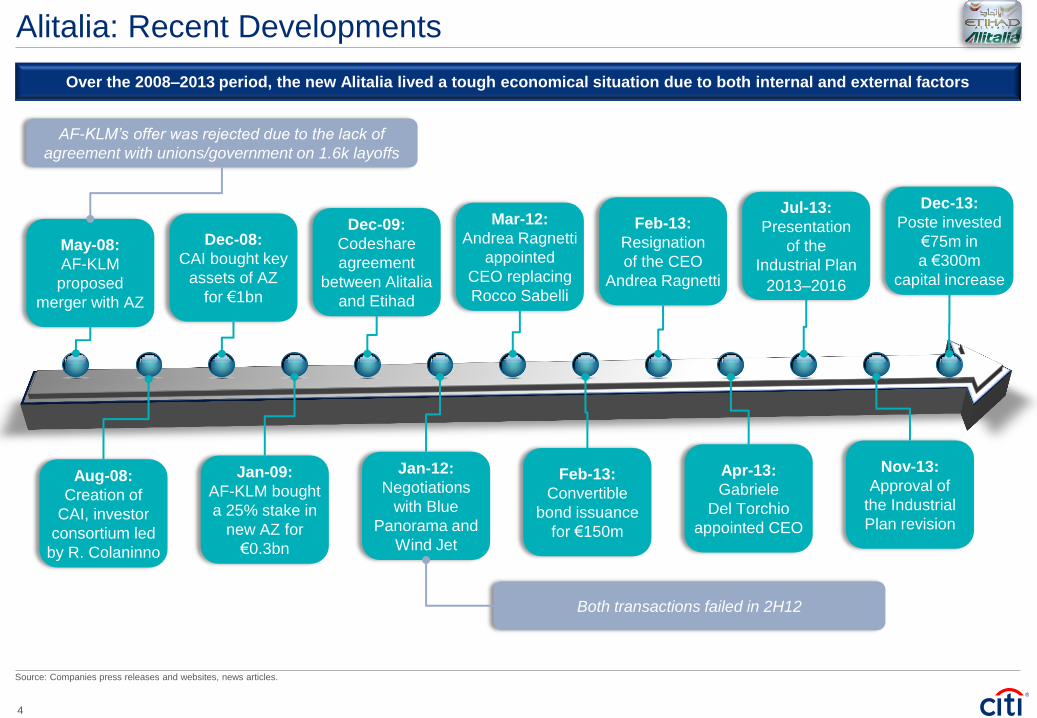

Alitalia: Recent Developments

Source: Companies press releases and websites, news articles.

Over the 2008–2013 period, the new Alitalia lived a tough economical situation due to both internal and external factors

Aug-08:

Creation of

CAI, investor

consortium led

by R. Colaninno

May-08:

AF-KLM

proposed

merger with AZ

Jan-09:

AF-KLM bought

a 25% stake in

new AZ for

€0.3bn

Dec-08:

CAI bought key

assets of AZ

for €1bn

AF-KLM’s offer was rejected due to the lack of

agreement with unions/government on 1.6k layoffs

Feb-13:

Convertible

bond issuance

for €150m

Mar-12:

Andrea Ragnetti

appointed

CEO replacing

Rocco Sabelli

Apr-13:

Gabriele

Del Torchio

appointed CEO

Feb-13:

Resignation

of the CEO

Andrea Ragnetti

Nov-13:

Approval of

the Industrial

Plan revision

Jul-13:

Presentation

of the

Industrial Plan

2013–2016

Dec-13:

Poste invested

€75m in

a €300m

capital increase

Both transactions failed in 2H12

Dec-09:

Codeshare

agreement

between Alitalia

and Etihad

Jan-12:

Negotiations

with Blue

Panorama and

Wind Jet

4

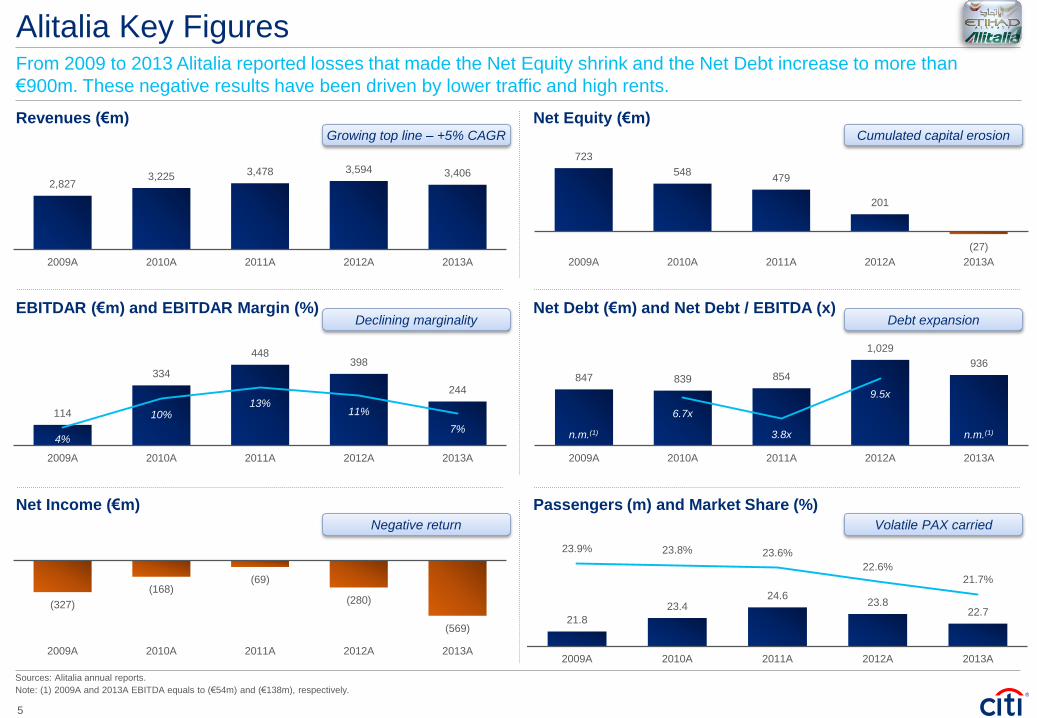

Alitalia Key Figures From 2009 to 2013 Alitalia reported losses that made the Net Equity shrink and the Net Debt increase to more than

€900m. These negative results have been driven by lower traffic and high rents.

Revenues (€m)

EBITDAR (€m) and EBITDAR Margin (%)

Net Income (€m)

Net Equity (€m)

Net Debt (€m) and Net Debt / EBITDA (x)

Passengers (m) and Market Share (%)

2,827 3,225 3,478 3,594 3,406

2009A 2010A 2011A 2012A 2013A

114

334

448 398

244

4%

10% 13%

11%

7%

2009A 2010A 2011A 2012A 2013A

(327)

(168)(69)

(280)

(569)

2009A 2010A 2011A 2012A 2013A

723

548 479

201

(27)

2009A 2010A 2011A 2012A 2013A

847 839 854

1,029

936

6.7x

3.8x

9.5x

2009A 2010A 2011A 2012A 2013A

21.8

23.424.6

23.822.7

23.9% 23.8% 23.6%

22.6%

21.7%

2009A 2010A 2011A 2012A 2013A

Growing top line – +5% CAGR

Declining marginality

Negative return

Cumulated capital erosion

Debt expansion

Volatile PAX carried

n.m.(1) n.m.(1)

Sources: Alitalia annual reports.

Note: (1) 2009A and 2013A EBITDA equals to (€54m) and (€138m), respectively.

5

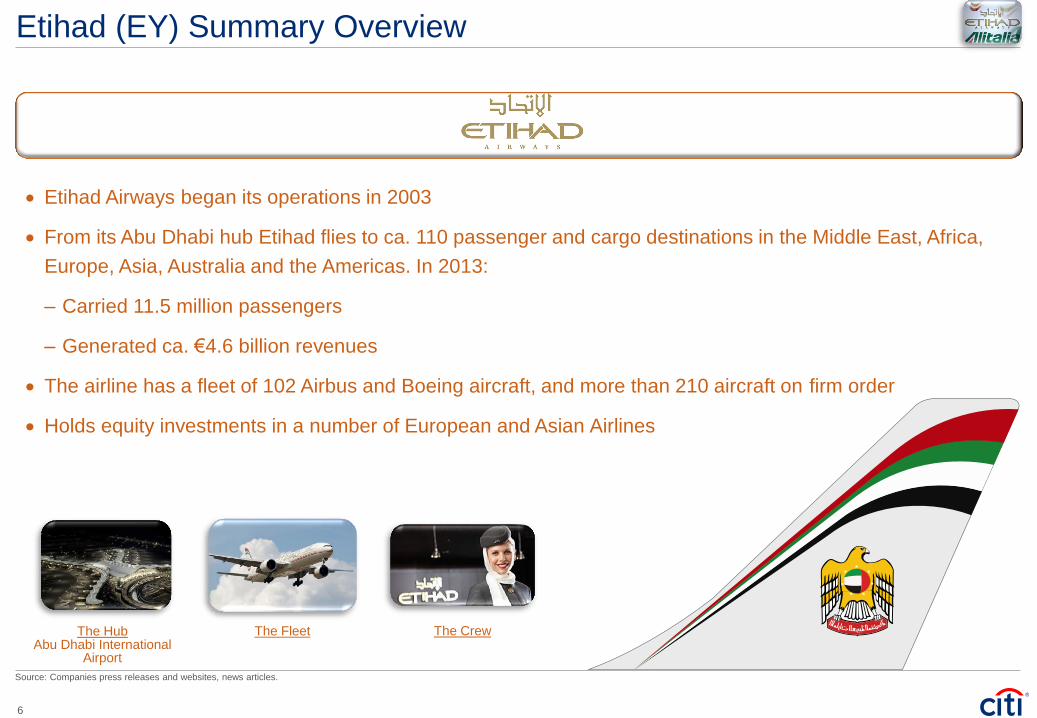

Etihad (EY) Summary Overview

The Birth of the “New” Alitalia

Etihad Airways began its operations in 2003

From its Abu Dhabi hub Etihad flies to ca. 110 passenger and cargo destinations in the Middle East, Africa,

Europe, Asia, Australia and the Americas. In 2013:

– Carried 11.5 million passengers

– Generated ca. €4.6 billion revenues

The airline has a fleet of 102 Airbus and Boeing aircraft, and more than 210 aircraft on firm order

Holds equity investments in a number of European and Asian Airlines

The Crew The Hub Abu Dhabi International

Airport

The Fleet

Source: Companies press releases and websites, news articles.

6

Snapshot on Alitalia and Etihad: Side by Side

Despite a smaller workforce and fleet, Etihad has been able to achieve ca.€4.6bn revenue covering more destination than

Alitalia.

FLEET

137

86 Mid-range

22 Long-range

20 Regional

9 Air One

Smart Carrier

Fleet Age Average

4.9 years

FLEET

102

28 Mid-range

10 Cargo airplanes

Fleet Age Average

6.5 years

EMPLOYEES

7,900 DESTINATIONS

96

EMPLOYEES

14,000 DESTINATIONS

103

REVENUES

3,406 € million

REVENUES

4,573 € million

Sources: 2013 annual reports, Companies press releases and websites, news articles.

206 aircraft

to be

delivered

by 2015 (of

which 52%

long-range

and 47%

mid-range)

64 Long-range

done

7

Etihad: the Right Partner

1st Class Service Provider

Proven M&A Track Record

40% stake 49% stake

10.5% stake

3% stake

24% stake

Complementarity with AZ

Solid and Supportive

Shareholders

Expected High Growth

Minority Stake Acquisition

Sources: Companies press releases and websites, news articles.

Selected Recent Awards

Airline Market Leadership ‘14

M. East’s Leading Airline ‘14

Best Economy Class ‘14

World’s Leading Airline ‘13

Airline of the Year ’13

World Leading First Class ‘13

8

Key Stakeholders

Lending Banks

European Airlines Public Stakeholders and Unions

Sources: News articles.

Largest Shareholders Customers

Suppliers

done

9

Invo

lve

d

Pa

rtie

s

New Partner Shareholders Lending Banks

% of Total Transaction Value

32% 13% 4% 17% 34% 17% 100%

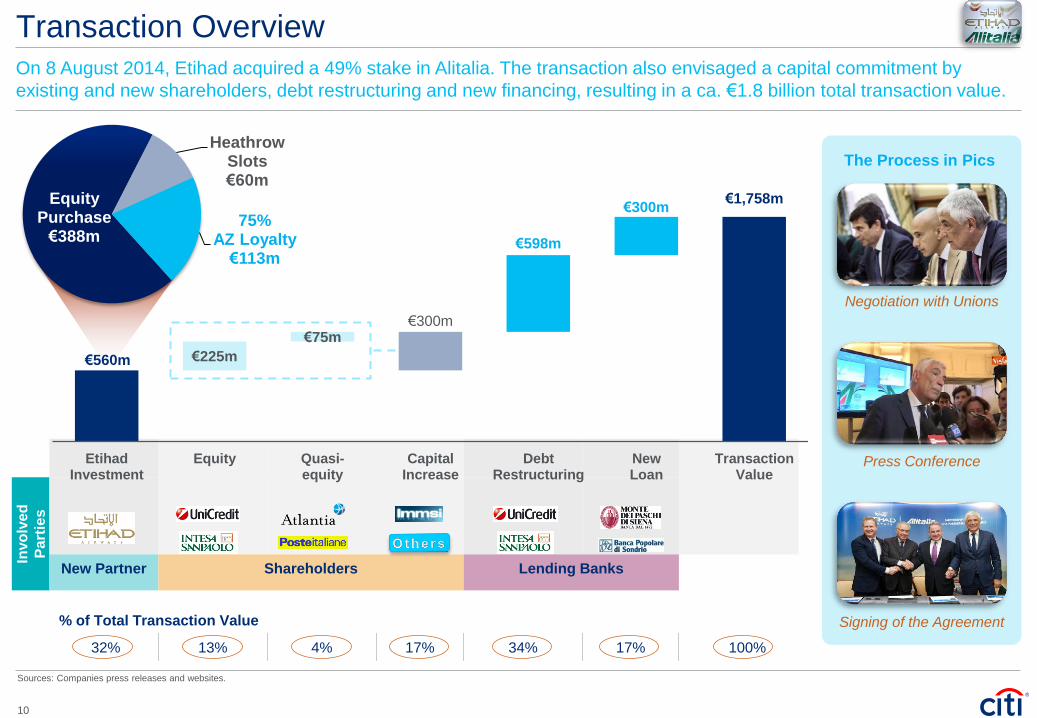

Transaction Overview On 8 August 2014, Etihad acquired a 49% stake in Alitalia. The transaction also envisaged a capital commitment by

existing and new shareholders, debt restructuring and new financing, resulting in a ca. €1.8 billion total transaction value.

Sources: Companies press releases and websites.

The total announced

investment amounts to ca.

€1.8bn and comprises the

following:

– Etihad’s investment of

€560m through a

combination of equity

injections, asset

purchases and other

funding arrangements

– Existing and new core

shareholders

contribution with a

capital increase of up to

€300m (€225m in

equity and €75m in

quasi-equity)

– Current lending

institutions restructured

up to €598m and also

committed to provide

new loan facilities for

€300m

The Process in Pics

Negotiation with Unions

Press Conference

Signing of the Agreement

€560m

€1,758m

560

785

560

860

1,458 €225m

€75m€300m

€598m

€300m

EtihadInvestment

Equity Quasi-equity

CapitalIncrease

DebtRestructuring

NewLoan

TransactionValue

EquityPurchase

€388m

HeathrowSlots€60m

75%AZ Loyalty

€113m

done

10

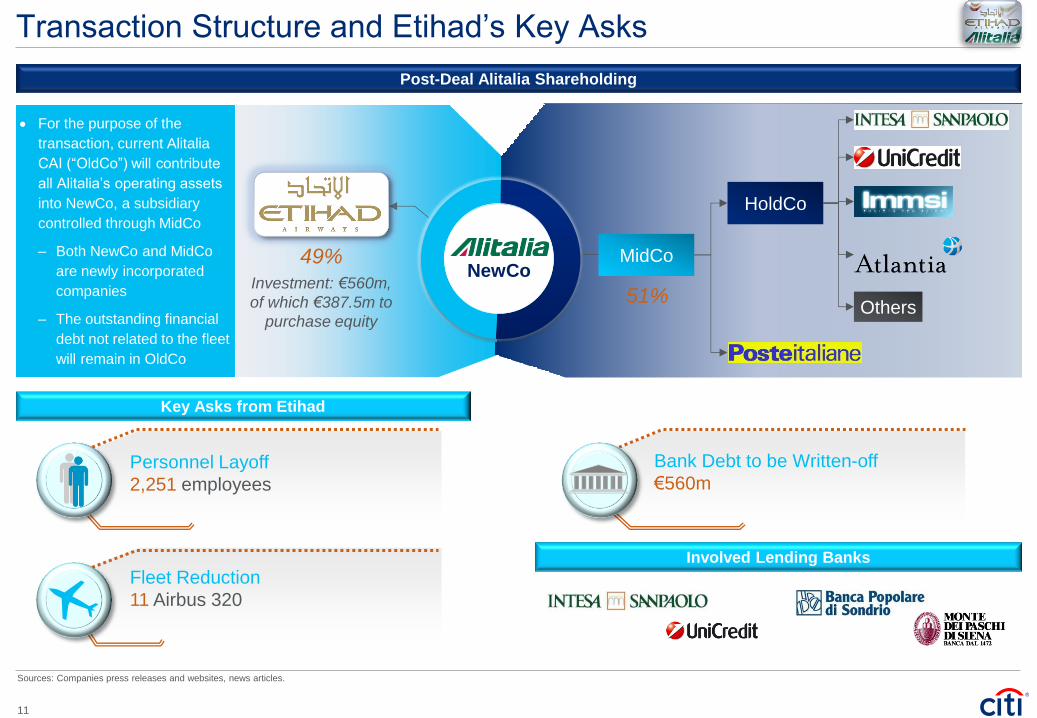

Transaction Structure and Etihad’s Key Asks

Personnel Layoff

2,251 employees

49%

Investment: €560m,

of which €387.5m to

purchase equity

Bank Debt to be Written-off

€560m

MidCo

51%

HoldCo

Others

Involved Lending Banks

Sources: Companies press releases and websites, news articles.

For the purpose of the

transaction, current Alitalia

CAI (“OldCo”) will contribute

all Alitalia’s operating assets

into NewCo, a subsidiary

controlled through MidCo

– Both NewCo and MidCo

are newly incorporated

companies

– The outstanding financial

debt not related to the fleet

will remain in OldCo

Fleet Reduction

11 Airbus 320

Key Asks from Etihad

Post-Deal Alitalia Shareholding

NewCo

done

11

Alitalia (NewCo) Renewed Board of Directors

Silvano Cassano

CEO

Alitalia and Etihad

Luca Cordero di

Montezemolo

Chairman

Alitalia MidCo

James Hogan

Vice-Chairman

Etihad

Giovanni Bisignani

Director

Etihad

Jean Pierre Mustier

Director

UniCredit

Board Member Name

Role

Reference Shareholder

Antonella Mansi

Director

MPS

Paolo Colombo

Director

Intesa SanPaolo

Roberto Colaninno

Director

IMMSI

James Rigney

Director

Etihad

NewCo

Sources: News articles.

Legend

12

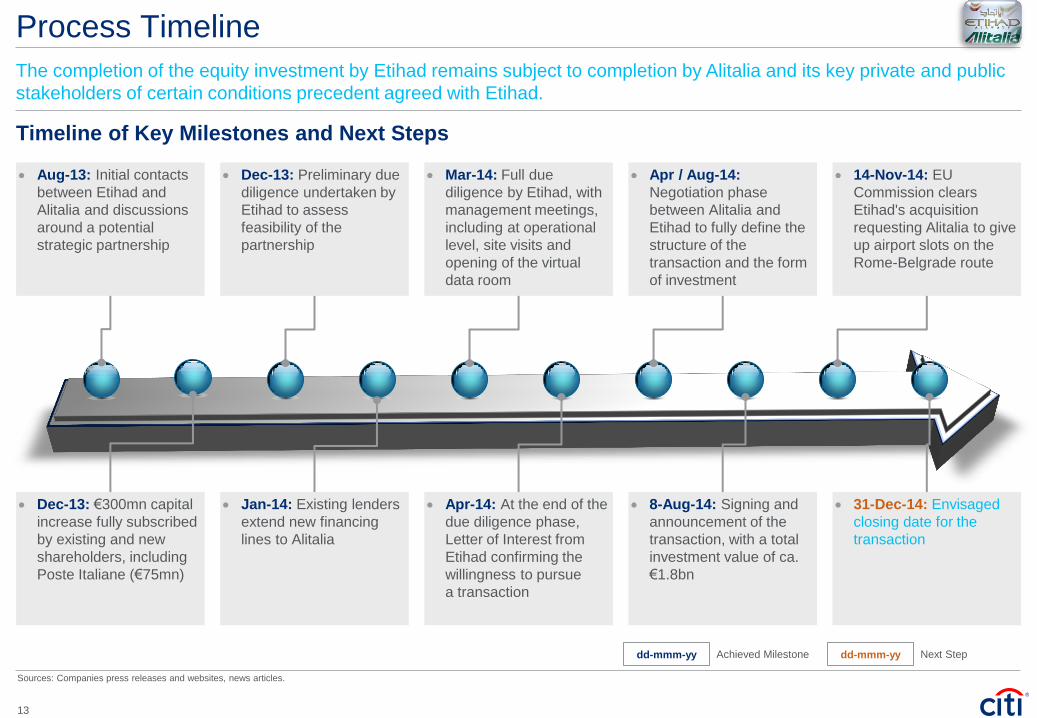

Mar-14: Full due

diligence by Etihad, with

management meetings,

including at operational

level, site visits and

opening of the virtual

data room

Jan-14: Existing lenders

extend new financing

lines to Alitalia

Dec-13: Preliminary due

diligence undertaken by

Etihad to assess

feasibility of the

partnership

Dec-13: €300mn capital

increase fully subscribed

by existing and new

shareholders, including

Poste Italiane (€75mn)

Aug-13: Initial contacts

between Etihad and

Alitalia and discussions

around a potential

strategic partnership

Process Timeline

Timeline of Key Milestones and Next Steps

Sources: Companies press releases and websites, news articles.

dd-mmm-yy dd-mmm-yy Achieved Milestone Next Step

31-Dec-14: Envisaged

closing date for the

transaction

14-Nov-14: EU

Commission clears

Etihad's acquisition

requesting Alitalia to give

up airport slots on the

Rome-Belgrade route

8-Aug-14: Signing and

announcement of the

transaction, with a total

investment value of ca.

€1.8bn

Apr / Aug-14:

Negotiation phase

between Alitalia and

Etihad to fully define the

structure of the

transaction and the form

of investment

Apr-14: At the end of the

due diligence phase,

Letter of Interest from

Etihad confirming the

willingness to pursue

a transaction

The completion of the equity investment by Etihad remains subject to completion by Alitalia and its key private and public

stakeholders of certain conditions precedent agreed with Etihad.

done

13

The Role of Thanks to its longstanding execution experience and on-the-ground presence, Citi provided investment banking services

in all the aspects of the transaction.

Citi acted as exclusive financial advisor to Alitalia in the entire transaction and all its related arrangements. In

particular, Citi:

Managed and coordinated the due diligence process and management meetings

Drove the negotiation and structuring discussions with Etihad

Advised Alitalia on the structure of the entire transaction and on the capital increase

Drove and coordinated the debt restructuring negotiations with the existing lenders

Facilitated the arrangement of the new financing package

Advised Alitalia in its discussions with the different constituencies, including the Italian government

Supported and presented Alitalia’s BoD meetings

Successful Track-Record of M&A Transactions in The Sector

Adviser to Poste Italiane for the

Alitalia's €300m capital

increase

€75m - 2013

Advisor to Alitalia in the

Selection of a Strategic Partner

2007/2008

Advisor to Alitalia in the

disposal of a 25% stake to Air

France

€323m - 2009

Advisor to Fintecna in the

Acquisition of a Controlling

Stake in Alitalia Servizi

2005

14

Dedicated Team to Citi assembled a uniquely qualified team with proven M&A, industry and on the ground presence both in Italy and globally

to advise and assist Alitalia in the execution of the process with Etihad.

Italian Speakers

Corporate and Investment Banking

EMEA Investment Banking

Gianmario Spissu

Associate

Italy Investment Banking

Enrico Prato

Vice President

EMEA Diversified Industrials

Italy M&A Coverage

Andrea Nappi

Managing Director

Head of Italy M&A

Giovanni Castaldo

Director

Italy Investment Banking

Alexander Setness

Director

EMEA Transportation London

Federico Polo

Analyst

EMEA Diversified Industrials

Project Oversight

Leopoldo Attolico

Managing Director

Co-Head of Italy Investment Banking

Senior Coverage

Luigi de Vecchi

Managing Director

Chairman of Continental Europe for Corporate

and Investment Banking

Munawar Noorani

Managing Director

Head of EMEA Aviation Banking

Aviation Banking Core M&A Execution Team

15

Plans and Future Expectations

The new-born Alitalia – Etihad Group is expected to grow significantly by 2019.

€560 Million

from Etihad to become

shareholder

Investment

Plan

211 Destinations

232 Airplanes

34 million Passengers per annum

32.500 Direct employees

2 hub Fiumicino

Abu Dhabi

10 New intercontinental

hauls in 5 years

25 Long- hauls from

Malpensa (from 11) 5 New long-hauls from

Fiumicino in 4 years

Key Figures of

the Deal

The Business

Plan

€300 Million

Capital increase

subscribed by

current

shareholders

€690 Million

from Etihad to invest

in fleet renewal

Sources: 2013 annual reports, Companies press releases and websites, news articles.

16

The New Network Leveraging on Etihad, Alitalia will implement its destinations network with additional flights from Abu Dhabi and 7 new

intercontinental flights.

New Intercontinental

Flights

7

Most Connected

Hauls

3

Departures

from Abu Dhabi

(Hub for Asia)

New Long Haul

Planes

7

Passengers

Served

23 million

Malpensa

More long-hauls flights

(from 11 to 25 per

week); re-launch of

Cargo activities

Linate

More international

flights, less national

Fiumicino

Hub for local flights

and feeder at both

national and

international level

San Francisco

Mexico City

Chicago New York

Rio de Janeiro

Santiago de Cile

Abu Dhabi

Peking

Shanghai

Seoul

Milan

Venice

Bologna

Rome

Catania

Destinations

105 26 national

61 international

18 intercontinental

Sources: 2013 annual reports, Companies press releases and websites, news articles.

17

fa

Citi believes that sustainability is good business practice. We work closely with our clients, peer financial institutions, NGOs and other partners to finance solutions to climate change, develop industry standards, reduce our own environmental

footprint, and engage with stakeholders to advance shared learning and solutions. Highlights of Citi’s unique role in promoting sustainability include: (a) releasing in 2007 a Climate Change Position Statement, the first US financial institution to do

so; (b) targeting $50 billion over 10 years to address global climate change: includes significant increases in investment and financing of renewable energy, clean technology, and other carbon-emission reduction activities; (c) committing to an

absolute reduction in GHG emissions of all Citi owned and leased properties around the world by 10% by 2011; (d) purchasing more than 234,000 MWh of carbon neutral power for our operations over the last three years; (e) establishing in

2008 the Carbon Principles; a framework for banks and their U.S. power clients to evaluate and address carbon risks in the financing of electric power projects; (f) producing equity research related to climate issues that helps to inform investors

on risks and opportunities associated with the issue; and (g) engaging with a broad range of stakeholders on the issue of climate change to help advance understanding and solutions.

Citi works with its clients in greenhouse gas intensive industries to evaluate emerging risks from climate change and, where appropriate, to mitigate those risks.

efficiency, renewable energy and mitigation

© 2014 Citigroup Global Markets Limited. Authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. All rights reserved. Citi and Citi and Arc Design are

trademarks and service marks of Citigroup Inc. or its affiliates and are used and registered throughout the world.

IRS Circular 230 Disclosure: Citigroup Inc. and its affiliates do not provide tax or legal advice. Any discussion of tax matters in these materials (i) is not intended or written to be used, and cannot be used or relied upon, by

you for the purpose of avoiding any tax penalties and (ii) may have been written in connection with the "promotion or marketing" of any transaction contemplated hereby ("Transaction"). Accordingly, you should seek advice

based on your particular circumstances from an independent tax advisor.

In any instance where distribution of this communication is subject to the rules of the US Commodity Futures Trading Commission (“CFTC”), this communication constitutes an invitation to consider entering into a derivatives

transaction under U.S. CFTC Regulations §§ 1.71 and 23.605, where applicable, but is not a binding offer to buy/sell any financial instrument.

Any terms set forth herein are intended for discussion purposes only and are subject to the final terms as set forth in separate definitive written agreements. This presentation is not a commitment to lend, syndicate a financing, underwrite or

purchase securities, or commit capital nor does it obligate us to enter into such a commitment, nor are we acting as a fiduciary to you. By accepting this presentation, subject to applicable law or regulation, you agree to keep confidential the

information contained herein and the existence of and proposed terms for any Transaction.

Prior to entering into any Transaction, you should determine, without reliance upon us or our affiliates, the economic risks and merits (and independently determine that you are able to assume these risks) as well as the legal, tax and accounting

characterizations and consequences of any such Transaction. In this regard, by accepting this presentation, you acknowledge that (a) we are not in the business of providing (and you are not relying on us for) legal, tax or accounting advice, (b)

there may be legal, tax or accounting risks associated with any Transaction, (c) you should receive (and rely on) separate and qualified legal, tax and accounting advice and (d) you should apprise senior management in your organization as to

such legal, tax and accounting advice (and any risks associated with any Transaction) and our disclaimer as to these matters. By acceptance of these materials, you and we hereby agree that from the commencement of discussions with

respect to any Transaction, and notwithstanding any other provision in this presentation, we hereby confirm that no participant in any Transaction shall be limited from disclosing the U.S. tax treatment or U.S. tax structure of such Transaction.

We are required to obtain, verify and record certain information that identifies each entity that enters into a formal business relationship with us. We will ask for your complete name, street address, and taxpayer ID number. We may also

request corporate formation documents, or other forms of identification, to verify information provided.

Any prices or levels contained herein are preliminary and indicative only and do not represent bids or offers. These indications are provided solely for your information and consideration, are subject to change at any time without notice and are

not intended as a solicitation with respect to the purchase or sale of any instrument. The information contained in this presentation may include results of analyses from a quantitative model which represent potential future events that may or

may not be realized, and is not a complete analysis of every material fact representing any product. Any estimates included herein constitute our judgment as of the date hereof and are subject to change without any notice. We and/or our

affiliates may make a market in these instruments for our customers and for our own account. Accordingly, we may have a position in any such instrument at any time.

Although this material may contain publicly available information about Citi corporate bond research, fixed income strategy or economic and market analysis, Citi policy (i) prohibits employees from offering, directly or indirectly, a favorable or

negative research opinion or offering to change an opinion as consideration or inducement for the receipt of business or for compensation; and (ii) prohibits analysts from being compensated for specific recommendations or views contained in

research reports. So as to reduce the potential for conflicts of interest, as well as to reduce any appearance of conflicts of interest, Citi has enacted policies and procedures designed to limit communications between its investment banking and

research personnel to specifically prescribed circumstances.