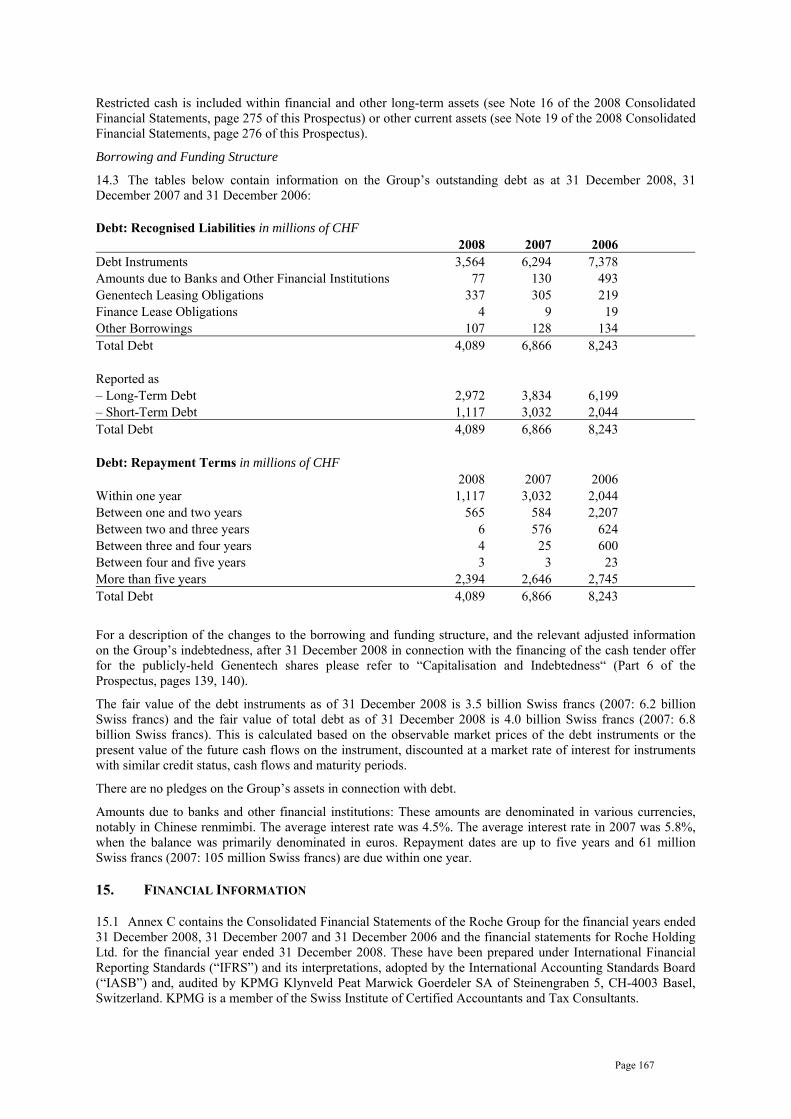

prospectus - cmvmweb3.cmvm.pt/sdi2004/emitentes/docs/fsd14422.pdf1.1 founded in 1896 in basel,...

TRANSCRIPT

PROSPECTUS

dated 26 March, 2009

relating to

the offer of 702,562,700 non-voting equity securities (“Genussscheine”) of

Roche Holding AG

(International Securities Identification Number (“ISIN”) CH0012032048) and the right to purchase such Genussscheine

under the

Roche Genussschein Purchase Plan - Roche Connect (the “Connect Plan”)

to certain employees of Roche Holding AG (the “Company” or “Roche”) and its subsidiaries (together with Roche, the “Group” or the “Roche Group”) in certain member states of the European Economic Area (“EEA”).

See “Risk Factors” in Part 2 of this Prospectus for a discussion of certain risks that should be considered in connection with an investment in the Genussscheine.

Certain terms used in this Prospectus, including all capitalised terms, are defined and explained in Part 8 “Definitions”.

Page 2

CONTENTS

CONTENTS..............................................................................................................................2

PART 1 SUMMARY............................................................................................................5

1. INFORMATION ON ROCHE .......................................................................................5

2. STRATEGY......................................................................................................................5

3. GENENTECH..................................................................................................................6

4. RISK FACTORS..............................................................................................................6

5. SELECTED FINANCIAL INFORMATION................................................................8

6. SUMMARY OF THE CONNECT PLAN .....................................................................9

GERMAN TRANSLATION OF THE SUMMARY / ZUSAMMENFASSUNG ........................12

TEIL 1 ZUSAMMENFASSUNG...........................................................................................12

1. INFORMATIONEN ZU ROCHE................................................................................12

2. STRATEGIE ..................................................................................................................12

3. GENENTECH................................................................................................................13

4. RISIKOFAKTOREN ....................................................................................................14

5. AUSGEWÄHLTE FINANZINFORMATIONEN ......................................................16

6. ZUSAMMENFASSUNG DES CONNECT PLANS ...................................................17

PART 2 RISK FACTORS ..................................................................................................19

PART 3 THE BUSINESS ...................................................................................................27

1. OVERVIEW AND HISTORY......................................................................................27

2. STRATEGY....................................................................................................................28

3. SELECTED FINANCIAL INFORMATION..............................................................29

4. PRINCIPAL ACTIVITIES AND MARKETS............................................................30

PHARMACEUTICALS ................................................................................................30

DIAGNOSTICS..............................................................................................................45

5. PRINCIPAL MARKETS ..............................................................................................55

6. PRINCIPAL INVESTMENTS .....................................................................................55

7. TOTAL RESEARCH AND DEVELOPMENT ..........................................................59

8. EMPLOYEES ................................................................................................................60

9. CURRENT TRADING AND PROSPECTS................................................................60 PART 4 DIRECTORS, EXECUTIVE COMMITTEE AND CORPORATE

GOVERNANCE ...................................................................................................61

1. DIRECTORS AND EXECUTIVE COMMITTEE.....................................................61

2. BIOGRAPHIES OF THE DIRECTORS AND MEMBERS OF THE EXECUTIVE COMMITTEE AND THE ENLARGED EXECUTIVE COMMITTEE .................63

3. CORPORATE GOVERNANCE ..................................................................................78

Page 3

PART 5 OPERATING AND FINANCIAL REVIEW.........................................................80

PART 6 CAPITALISATION AND INDEBTEDNESS .....................................................139

PART 7 ADDITIONAL INFORMATION .......................................................................142

1. INCORPORATION.....................................................................................................142

2. RESPONSIBILITY......................................................................................................142

3. SUMMARY OF CERTAIN PROVISIONS OF THE ARTICLES OF INCORPORATION AND BY LAWS........................................................................142

4. MANDATORY BID RULES ......................................................................................144

5. DIRECTORS’ AND MEMBERS’ OF THE EXECUTIVE COMMITTEE INTERESTS .................................................................................................................145

6. DIRECTORS’ AND MEMBERS OF THE EXECUTIVE COMMITTEES’ TERMS OF EMPLOYMENT ....................................................................................146

7. REMUNERATION OF THE DIRECTORS AND MEMBERS OF THE EXECUTIVE COMMITTEE.....................................................................................153

8. SHAREHOLDINGS ....................................................................................................158

9. RELATED PARTY TRANSACTIONS.....................................................................159

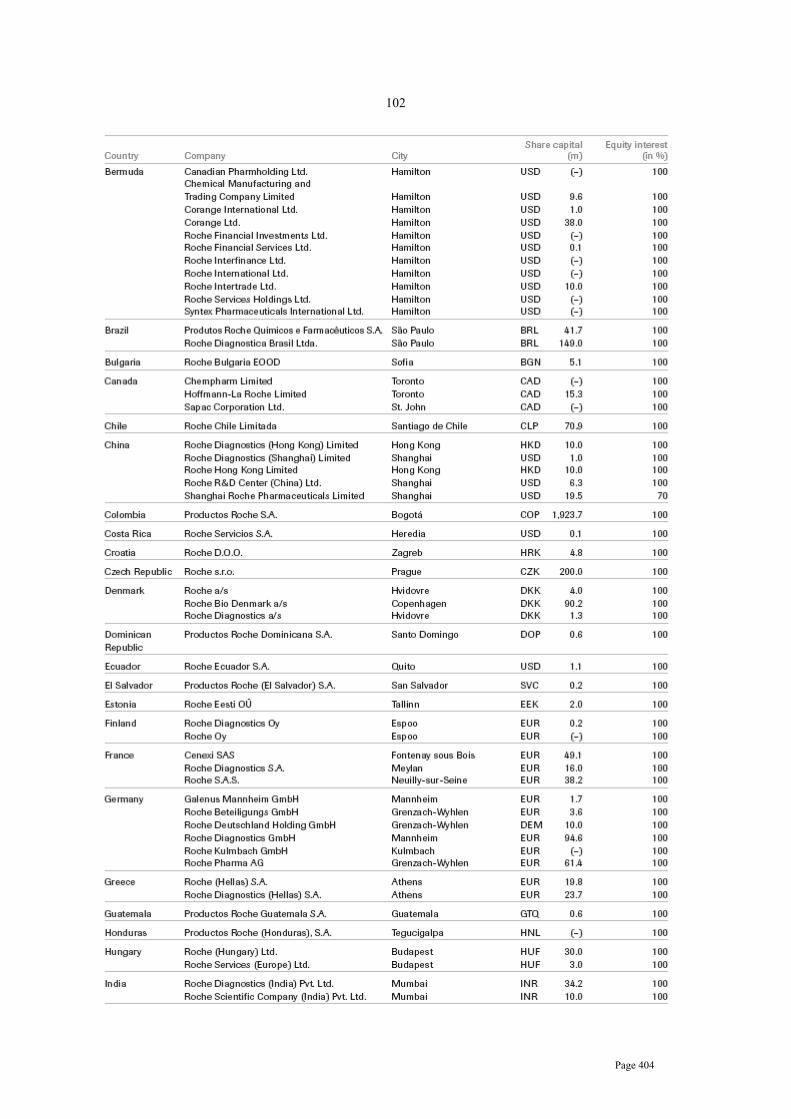

10. SUBSIDIARIES ...........................................................................................................161

11. PRINCIPAL ESTABLISHMENTS ...........................................................................161

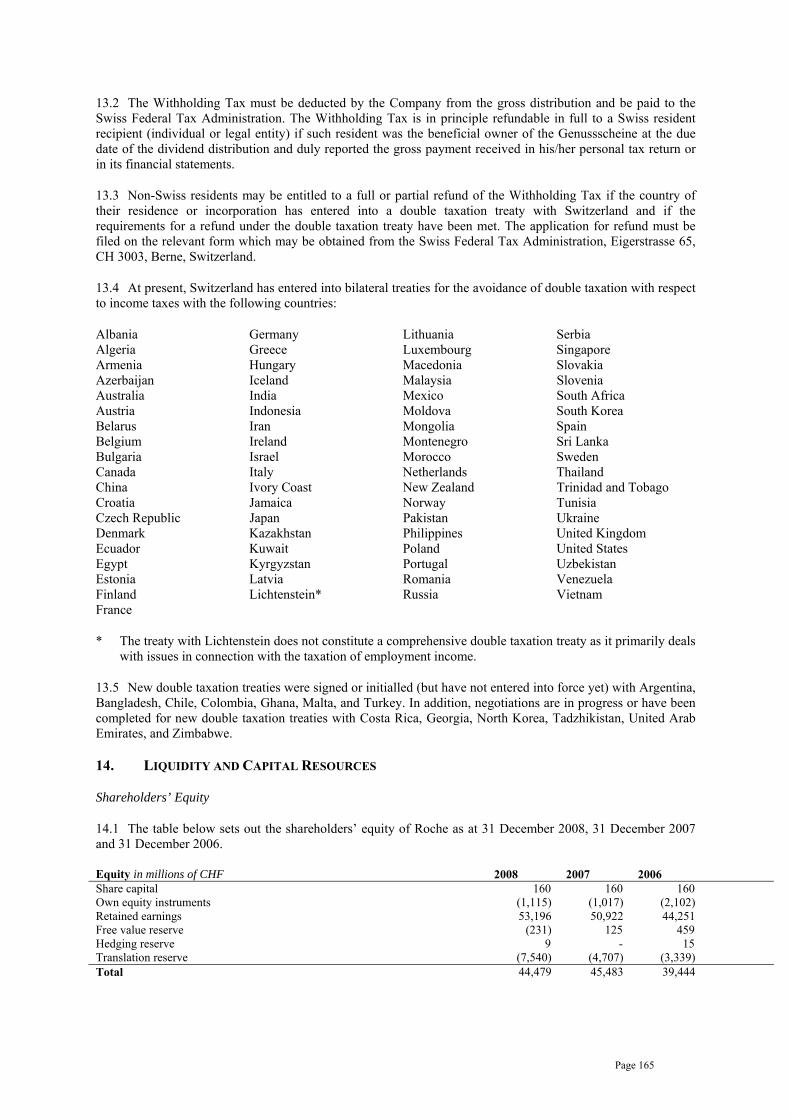

12. DIVIDENDS .................................................................................................................164

13. TAXATION..................................................................................................................164

14. LIQUIDITY AND CAPITAL RESOURCES............................................................165

15. FINANCIAL INFORMATION ..................................................................................167

16. WORKING CAPITAL................................................................................................168

17. SIGNIFICANT CHANGES ........................................................................................168

18. EXPENSES...................................................................................................................169

19. PASSPORTING ...........................................................................................................169

20. SELLING RESTRICTIONS ......................................................................................169

21. INFORMATION NOT CONTAINED IN THIS PROSPECTUS ...........................169

22. STATEMENTS REGARDING PRODUCT SALES AND COMPETITIVE POSITION....................................................................................................................169

23. LEGAL AND ARBITRATION PROCEEDINGS....................................................170

24. THE CONNECT PLAN ..............................................................................................174

25. PAYING AND DEPOSITARY AGENT AND EXTERNAL PLAN ADMINISTRATOR.....................................................................................................176

26. EMPLOYEE STOCK OPTIONS AND OTHER EQUITY COMPENSATION BENEFITS....................................................................................................................176

27. INFORMATION REGARDING FORWARD-LOOKING STATEMENTS ........176

Page 4

28. DOCUMENTS AVAILABLE FOR INSPECTION .................................................176

PART 8 DEFINITIONS ...................................................................................................177

ANNEX A CONNECT PLAN REGULATIONS.............................................................178

ANNEX B TERMS AND CONDITIONS OF THE GENUSSSCHEINE......................210

ANNEX C FINANCIAL INFORMATION......................................................................213

CONTENTS……………………..........................................................................................214

AUDITED CONSOLIDATED FINANCIALS STATEMENTS OF THE ROCHE GROUP AS AT AND FOR THE YEAR ENDED 31 DECEMBER 2008 ......................215

AUDITED ACCOUNTS OF ROCHE HOLDING LTD, BASEL FOR THE YEAR ENDED 31 DECEMBER 2008 ...........................................................................................312

AUDITED CONSOLIDATED FINANCIAL STATEMENTS OF THE ROCHE GROUP AS AT AND FOR THE YEAR ENDED 31 DECEMBER 2007 ......................325

AUDITED CONSOLIDATED FINANCIAL STATEMENTS OF THE ROCHE GROUP AS AT AND FOR THE YEAR ENDED 31 DECEMBER 2006 ......................410

SIGNATURES……………………………………………………………………………..487

Page 5

PART 1 SUMMARY

This summary must be read as an introduction to this securities prospectus (the “Prospectus”). Any decision to invest in any Genussscheine should be based on consideration of the Prospectus as a whole. Liability for this summary including any translation thereof attaches to Roche but only if the summary is misleading, inaccurate or inconsistent when read together with the other parts of the Prospectus. Where a claim relating to the information contained in this Prospectus is brought before a court, the plaintiff investor may, under the national legislation of the Member States of the European Economic Area (“EEA”), be required to bear the costs of translating this Prospectus before legal proceedings are initiated.

1. INFORMATION ON ROCHE

1.1 Founded in 1896 in Basel, Switzerland, Roche Holding AG (“Roche” or the “Company”, and together with its subsidiaries, the “Group” or the “Roche Group”) has grown from a small drug laboratory into an international research-based healthcare company. For more than 100 years Roche has been active in the discovery, development, manufacture and marketing of novel healthcare solutions. Roche’s products and services address prevention, diagnosis and treatment of diseases, thus enhancing well-being and quality of life. Roche, led and supported by the group headquarters in Basel, Switzerland employs more than 80,000 people and sells its products in over 150 countries. Roche’s multinational presence reinforces its ability to offer healthcare solutions world-wide and to anticipate needs in all regions of the world.

Divisions

1.2 Roche is divided into two operational sectors: pharmaceuticals and diagnostics. Key pharmaceutical products are in oncology, anaemia, transplantation, virology, and rheumatoid arthritis. Roche’s oncology portfolio is impressive, it markets five medicines for cancer on the market that have been shown to increase patient survival.

Research and Development

1.3 Roche’s focus is not just the diagnosis and treatment of manifest disease but also offering ways of identifying and targeting diseases early, when their damaging effects can still be prevented through vigorous research and development. Global R&D activities are focused on areas of high unmet medical need. Roche’s highly skilled people discover and develop innovative medicines addressing prevention, diagnosis and therapy to offer physicians and patients integrated healthcare solutions. With continuous investment in R&D – in cutting-edge sciences and state-of-the-art technology – Roche does all it can to meet tomorrow’s healthcare needs. Roche believes that it can continue in the future to make innovative contributions to healthcare and provide excellence in the service of health.

2. STRATEGY

Healthcare in the 21st century

2.1 Evolving consumer needs, innovation and market dynamics are likely to be the key drivers of change in healthcare in the years ahead. Despite enormous progress in the fight against disease, there are still many areas of high unmet medical need. And the demand for new and better healthcare products and services is bound to grow as a result of population ageing and other demographic changes. The advances that have occurred in science and technology in recent years clearly have implications for clinical practice, raising hopes that Roche may one day have better treatments for mankind’s most serious diseases, and perhaps even ways of preventing or curing them. But as demand for healthcare grows, so will the pressures to control its costs, which may have the unintended effect of hampering innovation.

A Distinctive Strategy

2.2 Roche’s major divestments over the last several years, most recently the sale of the consumer health business, have been aimed at focusing the Group’s energies entirely on its two innovation-intensive divisions: Pharmaceuticals and Diagnostics. Today’s Roche is a highly focused company, and as a result it is well positioned to be an industry pioneer in healthcare – from predisposition testing and prevention to diagnosis, therapy and treatment monitoring. Roche believes based on data provided by IMS Health Incorporated and/or data published by pharmaceutical companies that it is the market leader in oncology, transplantation and hepatitis and believes that it is a world leader in in vitro diagnostics and diabetes management.

Page 6

2.3 Roche aspires to be distinctive in its ability to drive value creation through the discovery, development and commercialisation of medically differentiated products. More specifically, Roche is pursuing industry leadership in the emerging field of personalised healthcare, which is gaining in importance as advances in areas such as genetic profiling enable earlier diagnosis and facilitate better patient stratification. Because of their clinical and economic benefits, preventive therapies and targeted medicines will appeal not only to consumers but to payers and regulators as well.

2.4 Roche’s pharmaceuticals and diagnostics businesses, including Roche’s majority shareholdings in Genentech and Chugai, are the hub of the Roche innovation network. Because Roche is both a diagnostics and a pharmaceuticals company, Roche can capitalise on broad synergies in research, development and marketing. These capabilities are augmented by technology collaborations and a constellation of alliances to develop individual products and product portfolios.

2.5 Biotechnology is an important factor in Roche’s innovation strategy. Today, biopharmaceuticals account for over half of Group sales.

Creating Value for Today and Tomorrow

2.6 Roche’s business model is focused on creating sustainable value for all Roche’s stakeholders: not just for Roche’s shareholders, but also for patients, Roche’s employees and society at large.

3. GENENTECH

3.1 In July 2008, the Roche Group announced its intention to purchase all of the shares of Genentech not owned by it. Following months of unsuccessful negotiations with the independent directors of Genentech, on 9 February 2009, Roche Investments USA Inc. commenced a cash tender offer for the publicly-held Genentech shares at USD 86.50 per share. On 12 March 2009, Roche entered into a merger agreement with Genentech pursuant to which the Group is making a tender offer to purchase all of the shares of Genentech not owned by the Group for USD 95.00 per share in cash. The tender offer expired at midnight, New York City time, on 25 March 2009. As at the close of the offer on 25 March 2009, 84.7 per cent of the outstanding publicly-held shares of Genentech have been tendered. Roche Investments USA Inc. has accepted for payment all shares validly tendered pursuant to its tender offer. Together with the 55.7 per cent of the outstanding shares already held by Roche, Roche now holds a total of approximately 982.9 million or 93.2 per cent of the 1,054,555,886 Genentech shares outstanding. In addition, a further 3.0 per cent of Genentech’s outstanding shares were guaranteed to be delivered within the next three business days from the closing of the tender offer which, if added to the shares already received in the tender offer and Roche’s existing stake, would represent approximately 96.2% of Genentech’s total outstanding shares. Public shareholders who have tendered their shares will promptly receive USD 95.00 per share for their shares. Pursuant to the merger agreement Roche has caused a short-form merger in which all remaining Genentech stockholders after the tender offer will receive USD 95.00 per Genentech share in cash, subject to stockholders’ statutory appraisal rights. Genentech has become a wholly-owned subsidiary of the Roche Group. Genentech’s common stock will no longer be traded on the New York Stock Exchange after Thursday, 26 March 2009.

3.2 The acquisition of all public shares, including shares issuable under Genentech's outstanding employee stock options and payment of related fees and expenses, costs approximately USD 46.8 billion. The Group has financed the transaction by a combination of the Group's own funds, commercial paper back-stopped by a credit facility, and debt securities. The Group has raised net proceeds of approximately USD 46 billion (based on 20 March 2009 exchange rates) through a series of debt offerings. The series of notes offered to finance the transaction consists of U.S. dollar-denominated notes, Euro-denominated and Sterling-denominated notes, Swiss franc-denominated notes, as well as commercial paper (as of 26 March 2009 a nominal amount of USD 3,250 million).

3.3 On 25 February 2009, Roche completed an offering of U.S. dollar-denominated notes to qualified institutional buyers in the United States under Rule 144A and to persons other than U.S. persons outside the United States under Regulation S of the U.S. Securities Act of 1933. Roche received approximately USD 16,263.7 million in aggregate net proceeds from the issuance and sale of these fixed- and floating-rate notes.

3.4 On 4 March 2009, Roche issued Euro- and Sterling-denominated notes under a European Medium Term Note (EMTN) programme. Roche received approximately EUR 11,176.7 million and GBP 1,237.5 million in

Page 7

aggregate net proceeds from the issuance and sale of these notes. The Euro and Sterling-denominated notes were fixed- and floating-rate senior unsecured notes.

3.5 On 20 March 2009, Roche completed a further offering of U.S. dollar-denominated notes under Rule 144A of the U.S. Securities Act of 1933. Roche received approximately USD 2,499.8 million in aggregate net proceeds from the issuance and sale of these fixed-rate notes.

3.6 The notes mentioned in paragraphs 3.3 to 3.5 are obligations of Roche Holdings, Inc., a wholly-owned subsidiary of Roche Holding Ltd, the ultimate parent company of the Roche Group and the guarantor of the notes.

3.7 On 23 March 2009, Roche Kapitalmarkt AG and Roche Holdings, Inc. completed an offering of Swiss franc-denominated bonds and notes guaranteed by Roche Holding Ltd. Roche received approximately CHF 7,960 million in aggregate net proceeds from the issuance and sale of these fixed-rate bonds and notes.

4. RISK FACTORS

4.1 Roche’s business, results of operations and/or financial condition could suffer from:

● loss of patents or marketing exclusivity or if its patents expire;

● failure through R&D to deliver commercially successful new products;

● the weakness of intellectual property protection in certain countries;

● exposure to litigation (product liability litigation, patent infringement litigation, anti-trust litigation) and government investigations;

● intense competition and potential product substitution;

● pricing controls, pricing pressure, restrictions on reimbursement - governmental and payer;

● regulatory controls;

● interruption of product supply;

● environmental damage/liability;

● employee injuries/damage to health;

● accidents involving hazardous materials;

● loss or restrictions on operating licences, including as a consequence of the occurrence of environment damage/liability, employee injuries/damage to health or accidents involving hazardous materials;

● human resources problems;

● public pressure on the pharmaceutical industry;

● reliance on information technology;

● the ongoing global financial and economic crisis and other changes in global economic conditions and politics which could adversely affect its business and results of operations;

● changes in tax laws adversely affecting the Group’s earnings;

● earthquakes affecting its business and results of operations.

Page 8

4.2 In addition the Group is exposed to various financial risks arising from its underlying operations and corporate finance activities such as:

● foreign exchange risks;

● interest rate risk;

● market risk of financial assets;

● credit risk;

● liquidity risk.

4.3 In addition the Group faces risks related to the acquisition of Genentech’s publicly-held shares such as:

• a limitation of the Group’s operating flexibility as a result of the Group incurring a substantial amount of indebtedness in connection with the proposed acquisition;

• a potential downgrade of Roche’s credit rating;

• the risk that the costs and expenses for the acquisition will be higher than the anticipated;

• the risk that the expected benefits of the acquisition may not be realised because of integration or other challenges.

4.4 In addition there are risks relating specifically to the Genussscheine and the Connect Program:

● the market price of the Genussscheine may be volatile;

● Genussscheine holders in countries with currencies other than the Swiss franc face additional investment risk from currency exchange rate fluctuations;

● Genussscheine holders will generally be ‘locked in’ under the Connect Program for three years;

● Genussscheine holders will be unable to vote at general meetings;

● subscribers to the Connect Plan will be committing themselves to future investments in Genussscheine.

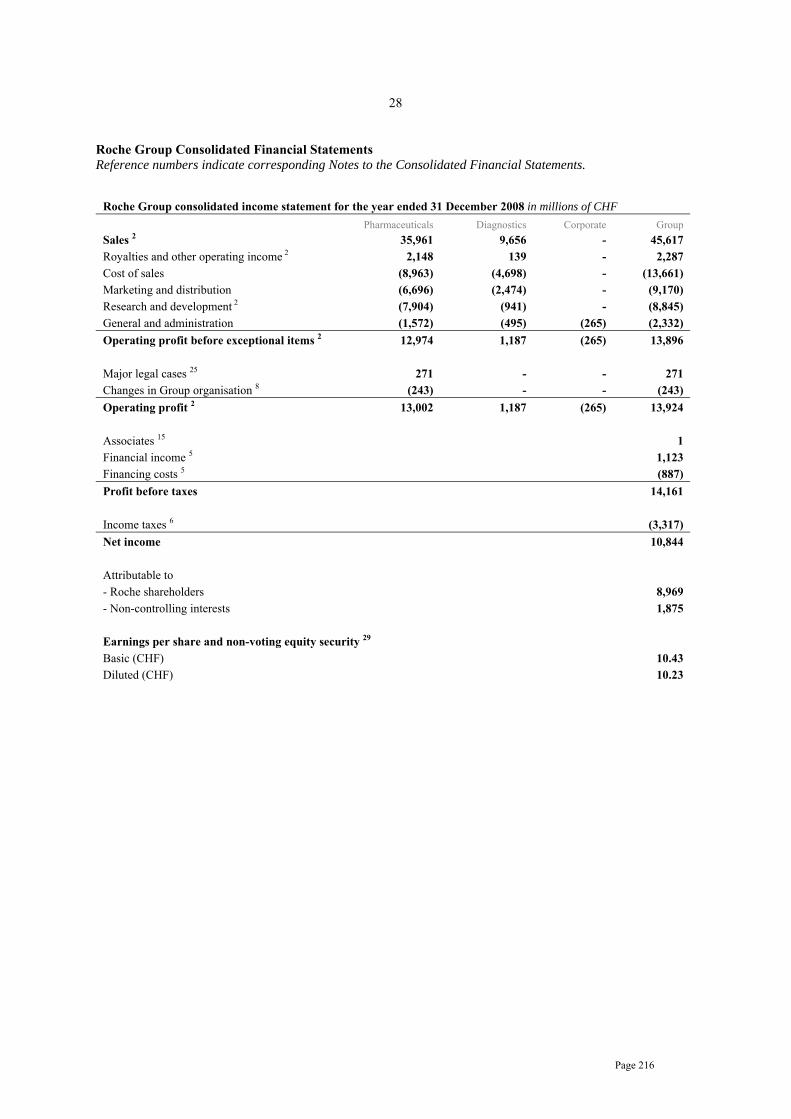

5. SELECTED FINANCIAL INFORMATION

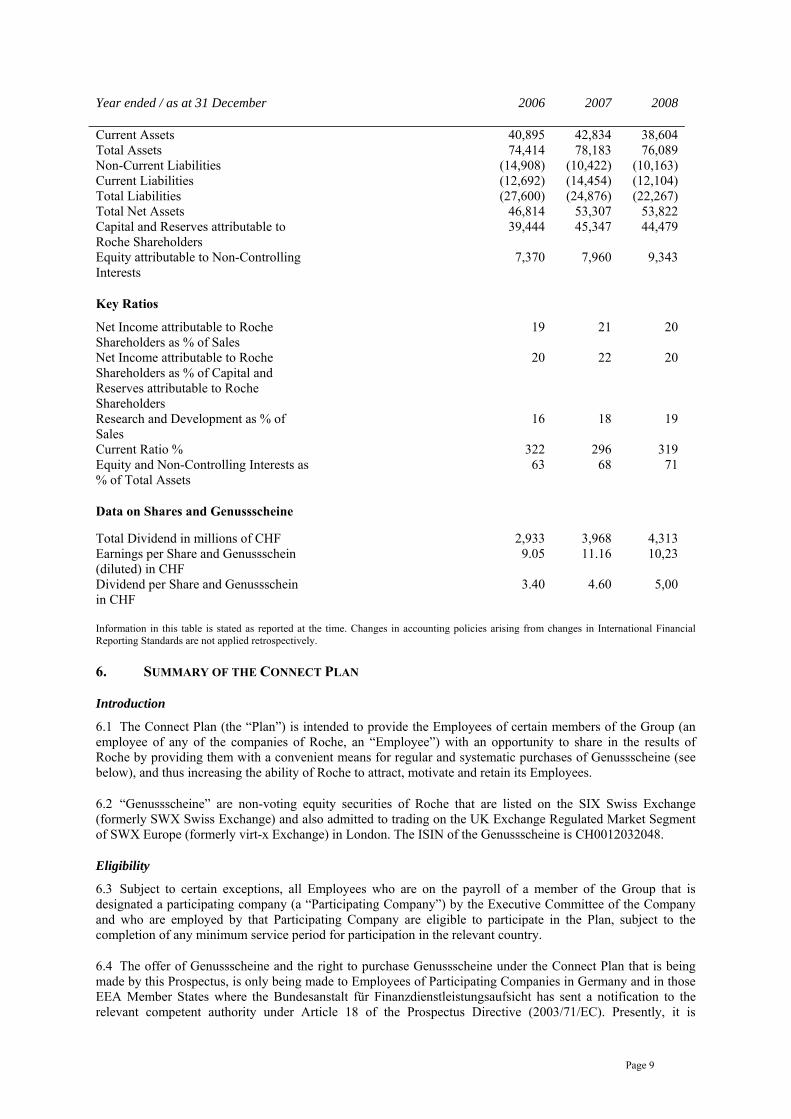

The following selected financial information has been extracted from the audited Consolidated Financial Statements and has been prepared in accordance with International Financial Reporting Standards:

Year ended / as at 31 December 2006 2007 2008

Consolidated Income Statement in millions of CHF

Sales 42,041 46,133 45,617 Operating Profit 11,730 14,468 13,924 Net Income attributable to Roche Shareholders

7,880 9,761 8,969

Research and Development 6,589 8,385 8,845

Consolidated Balance Sheet in millions of CHF

Non-Current Assets 33,519 35,349 37,485

Page 9

Year ended / as at 31 December 2006 2007 2008

Current Assets 40,895 42,834 38,604 Total Assets 74,414 78,183 76,089 Non-Current Liabilities (14,908) (10,422) (10,163) Current Liabilities (12,692) (14,454) (12,104) Total Liabilities (27,600) (24,876) (22,267) Total Net Assets 46,814 53,307 53,822 Capital and Reserves attributable to Roche Shareholders

39,444 45,347 44,479

Equity attributable to Non-Controlling Interests

7,370 7,960 9,343

Key Ratios

Net Income attributable to Roche Shareholders as % of Sales

19 21 20

Net Income attributable to Roche Shareholders as % of Capital and Reserves attributable to Roche Shareholders

20 22 20

Research and Development as % of Sales

16 18 19

Current Ratio % 322 296 319 Equity and Non-Controlling Interests as % of Total Assets

63 68 71

Data on Shares and Genussscheine

Total Dividend in millions of CHF 2,933 3,968 4,313 Earnings per Share and Genussschein (diluted) in CHF

9.05 11.16 10,23

Dividend per Share and Genussschein in CHF

3.40 4.60 5,00

Information in this table is stated as reported at the time. Changes in accounting policies arising from changes in International Financial Reporting Standards are not applied retrospectively.

6. SUMMARY OF THE CONNECT PLAN

Introduction

6.1 The Connect Plan (the “Plan”) is intended to provide the Employees of certain members of the Group (an employee of any of the companies of Roche, an “Employee”) with an opportunity to share in the results of Roche by providing them with a convenient means for regular and systematic purchases of Genussscheine (see below), and thus increasing the ability of Roche to attract, motivate and retain its Employees.

6.2 “Genussscheine” are non-voting equity securities of Roche that are listed on the SIX Swiss Exchange (formerly SWX Swiss Exchange) and also admitted to trading on the UK Exchange Regulated Market Segment of SWX Europe (formerly virt-x Exchange) in London. The ISIN of the Genussscheine is CH0012032048.

Eligibility

6.3 Subject to certain exceptions, all Employees who are on the payroll of a member of the Group that is designated a participating company (a “Participating Company”) by the Executive Committee of the Company and who are employed by that Participating Company are eligible to participate in the Plan, subject to the completion of any minimum service period for participation in the relevant country.

6.4 The offer of Genussscheine and the right to purchase Genussscheine under the Connect Plan that is being made by this Prospectus, is only being made to Employees of Participating Companies in Germany and in those EEA Member States where the Bundesanstalt für Finanzdienstleistungsaufsicht has sent a notification to the relevant competent authority under Article 18 of the Prospectus Directive (2003/71/EC). Presently, it is

Page 10

expected that such EEA Member States will be Austria, Belgium, the Czech Republic, Denmark, Finland, Greece, Italy, the Netherlands, Norway, Poland, Portugal, Spain, Sweden and the United Kingdom. No offer is being made by this Prospectus to any other persons in any other jurisdiction.

Enrolment in the Connect Plan

6.5 Employees eligible to participate in the Plan will be sent an enrolment form, which will contain details of the plan administrator (the “Plan Administrator”) to whom such enrolment form should be returned. Employees eligible to participate in the Connect Plan must file an enrolment form with the relevant Plan Administrator specified therein between 27 April 2009 and 15 May 2009 (the “Enrolment Period”). The relevant Plan Administrator may, in its sole discretion, but will be under no obligation to, accept enrolment forms filed outside the Enrolment Period.

Contributions

6.6 The enrolment form will permit a participant in the Plan (a “Participant”) to elect a fixed annual rate for contributions in local currency. Generally, the Participant’s annual rate for contributions may not be less than 0.5% of the Participant’s annual base salary and may not exceed 10% of the Participant’s annual base salary. Contributions based on this annual rate will be deducted from a Participant’s base salary on each payday and placed into a “Cash Account” held on behalf of that Participant. In addition, any dividends paid on Genussscheine held in a Participant’s Custody Account (see below) will be credited to that Participant’s Cash Account.

Purchase of Genussscheine

6.7 Once a month, Genussscheine will be purchased on behalf of the Participant by the Plan Administrator using the entire credit balance in the relevant Participant’s Cash Account. Genussscheine so purchased will be deposited in a “Custody Account” held on behalf of that Participant.

6.8 All Genussscheine used for the Plan are purchased in the market by the Plan Administrator. However, Participants do not pay the price that was paid by the Plan Administrator in the market for Genussscheine that are purchased on their behalf. Rather, the average price paid in the market by the Plan Administrator for all Genussscheine purchased in the month is used to determine the purchase price (the “Purchase Price”) that is paid by Participants (and deducted from their Cash Account) for Genussscheine purchased on their behalf. Generally, the Purchase Price will be 80% of the average price paid in the market by the Plan Administrator for Genussscheine, except where the Purchase Price is funded using reinvested dividends, in which case the Purchase Price will be 100% of such average price paid. These percentages are also subject to variation for Participants in certain countries, as set out in the relevant country addenda. Any difference between the price paid in the market by the Plan Administrator for Genussscheine and the Purchase Price applicable to Participants will be funded by Roche.

6.9 The Plan Administrator will ordinarily purchase Genussscheine on the 18thday of each month, or the next trading day following the 18th if the 18th is not a trading day. Participants will be informed of the average market price paid by the Plan Administrator in the month for the Genussscheine allocated to their Custody Account in the quarterly statement referred to in the next paragraph. The Genussscheine will be offered, and the Purchase Price will be determined, on an ongoing basis. Information about the initial Purchase Price will be made available in a printed form for delivery to the public free of charge on 23 July 2009 at the registered office of Roche in Grenzacherstrasse 124, 4058, Basel, Switzerland. Furthermore, Employees of Roche who are eligible for participating in the Connect Plan will be individually informed about the subsequent Purchase Prices on an ongoing basis.

Notification of Total Investment and Number of Genussscheine held

6.10 Participants will be sent a statement on a quarterly basis detailing the total amounts invested by (i) the Participant; (ii) Roche; and (iii) the reinvestment of dividends paid on Genussscheine held in the Participant’s Custody Account, together with the total number of Genussscheine held in the Participant’s Custody Account and the price paid by the Plan Administrator for the purchase of such Genussscheine.

Transferability

6.11 The right to purchase Genussscheine under the Plan is non-tradable and may not be assigned, pledged or transferred.

Page 11

6.12 Generally, Genussscheine acquired under the Plan cannot be transferred or pledged during a “holding period” of three years from their date of purchase. This restriction is generally lifted if a Participant ceases to be employed by Roche for any reason.

Duration

6.13 The Plan may be terminated, amended or suspended by the Executive Committee at any time by the giving of notice to Participants.

Country Addenda

6.14 There are additional terms and conditions for Austria, Belgium Denmark, Finland, Germany, Greece, Italy, the Netherlands, Norway, Portugal, Spain, Sweden and the United Kingdom which are set out in specific country addenda. However, there are no such country addenda for Poland or the Czech Republic.

Further Information

6.15 Employees to whom an enrolment form is sent will be given contact details of a person to whom they can direct queries concerning the Plan, including any country specific rules contained in country addenda as referred to above.

Page 12

GERMAN TRANSLATION OF THE SUMMARY / ZUSAMMENFASSUNG

TEIL 1 ZUSAMMENFASSUNG

Die vorliegende Zusammenfassung ist als Einführung zu diesem Wertpapierprospekt (der "Prospekt") zu verstehen. Anleger sollten daher ihre Entscheidung zur Anlage in die Genussscheine auf die Prüfung des gesamten Prospekts stützen. Roche kann für diese Zusammenfassung, einschließlich jedweder Übersetzungen dieser Zusammenfassung, haftbar gemacht werden, jedoch nur für den Fall, dass die Zusammenfassung irreführend, unrichtig oder widersprüchlich ist, wenn sie zusammen mit den anderen Teilen dieses Prospektes gelesen wird. Für den Fall, dass vor einem Gericht Ansprüche aufgrund der in diesem Prospekt enthaltenen Informationen geltend gemacht werden, könnte der als Kläger auftretende Anleger, die Kosten für die Übersetzung dieses Prospekts in Anwendung der einzelstaatlichen Rechtsvorschriften der Staaten des Europäischen Wirtschaftsraums („EWR“) vor Prozessbeginn zu tragen haben.

1. INFORMATIONEN ZU ROCHE

1.1 Die Roche Holding AG („Roche” bzw. die „Gesellschaft”, und zusammen mit ihren Tochtergesellschaften der "Konzern" oder "Roche-Konzern") wurde 1896 in Basel, Schweiz gegründet und entwickelte sich aus einem kleinen Arzneimittellabor zu einem internationalen, auf Forschung basierenden Unternehmen im Gesundheitssektor. Roche hat sich seit über 100 Jahren aktiv bei der Erforschung, Entwicklung, Herstellung und Vermarktung neuer Lösungen im Bereich des Gesundheitswesens betätigt. Die von Roche angebotenen Produkte und Dienstleistungen zielen auf die Vorbeugung, Diagnose und Therapie von Krankheiten ab und verbessern dadurch den Gesundheitszustand und die Lebensqualität. Unter der Führung und mit der Unterstützung ihres Konzernhauptsitzes in Basel, Schweiz beschäftigt Roche mehr als 80.000 Mitarbeiter und vertreibt seine Produkte in über 150 Ländern. Infolge multinationaler Präsenz ist Roche in der Lage, weltweit Lösungen im Gesundheitsbereich anzubieten und den Bedarf in allen Regionen der Welt frühzeitig zu identifizieren.

Unternehmensbereiche

1.2 Roche ist in zwei Unternehmensbereiche, die Division Pharma und die Division Diagnostics, unterteilt. Die wichtigsten pharmazeutischen Produkte werden in den Bereichen Onkologie, Anämie, Transplantation, Virologie und Gelenkrheumatismus angeboten. Roche kann ein eindrucksvolles Produktportfolio im Bereich Onkologie vorweisen und vertreibt fünf Präparate zur Krebsbehandlung auf dem Markt, die erwiesenermaßen die Überlebensrate der Patienten steigern.

Forschung und Entwicklung

1.3 Roche legt seinen Schwerpunkt nicht nur auf die Diagnose und Behandlung sich bereits manifestierter Krankheiten, sondern bietet auch Möglichkeiten zur frühzeitigen Erkennung und gezielten Behandlung von Krankheiten zu einem Zeitpunkt, wenn deren Auswirkungen noch durch intensive Forschung und Entwicklung verhindert werden können. Die globalen Forschungs- und Entwicklungsaktivitäten haben ihren Schwerpunkt auf Gebieten mit heute noch nicht abgedeckten medizinischen Bedürfnissen. Die hochqualifizierten Mitarbeiter von Roche erforschen und entwickeln innovative Medikamente zur Vorbeugung, Diagnose und Therapie, um Ärzten und Patienten integrierte Gesundheitslösungen anzubieten. Durch laufende Investitionen in die Forschung und Entwicklung - d.h. in modernste Wissenschaften und fortschrittlichste Technologie – unternimmt Roche alles, um den Gesundheitsbedürfnissen von morgen gerecht zu werden. Roche ist davon überzeugt, dass es auch in Zukunft innovative Beiträge zur Gesundheitswesen leisten und herausragende Dienste in diesem Bereich anbieten kann.

2. STRATEGIE

Gesundheitswesen im 21. Jahrhundert

2.1 Veränderte Verbraucherbedürfnisse, Innovation und die Dynamik der Märkte in den kommenden Jahren werden wahrscheinlich die wichtigsten Triebkräfte für den Wandel im Gesundheitssektor sein. Ungeachtet großer Fortschritte im Kampf gegen Krankheiten gibt es weiterhin zahlreiche Gebiete, auf denen noch keine befriedigenden medizinischen Antworten gefunden worden sind. Und dieser Bedarf nach neuen und verbesserten Produkten und Dienstleistungen im Gesundheitswesen wird unweigerlich in Folge einer steigenden Lebenserwartung sowie anderweitiger demografischer Veränderungen weiter zunehmen. Die in den letzten Jahren in Wissenschaft und Technologie erzielten Fortschritte wirken sich deutlich auf die klinische Praxis aus

Page 13

und geben Anlass zu der Hoffnung, dass wir eines Tages möglicherweise über bessere Behandlungsmethoden für die schwerwiegendsten Krankheiten der Menschheit verfügen und vielleicht sogar Wege zur Vorbeugung oder zu ihrer Heilung finden werden.

Eine eigene Strategie

2.2 Das Ziel der wichtigsten Desinvestitionen von Roche in den letzten Jahren, zuletzt der Verkauf des Selbstmedikationsgeschäfts, bestand darin, die gesamten Kräfte des Konzerns auf die beiden innovationsintensiven Geschäftsbereiche Pharma und Diagnostics zu konzentrieren. Roche ist heute ein klar fokussiertes Unternehmen und ist in Folge dessen gut für eine Pionierstellung in der Gesundheitsbranche positioniert – von Prädispositionstests und Vorbeugung bis hin zur Diagnose, Therapie und Behandlungsüberwachung. Roche ist basierend auf den von IMS Health Incorporated und den von anderen pharmazeutischen Unternehmen veröffentlichten Daten der Auffassung, dass der Roche-Konzern marktführend in den Bereichen Onkologie, Transplantation und Virologie ist. Nach Einschätzung von Roche ist zudem der Roche-Konzern weltweit führend in den Bereichen Molekular- und In-vitro-Diagnostik sowie auf dem Gebiet des Diabetes-Managements.

2.3 Roche geht es darum durch die Erforschung, Entwicklung und Vermarktung medizinisch differenzierter Produkte in ganz besonderer Weise zur Wertschöpfung beizutragen. Genauer ausgedrückt strebt Roche eine branchenführende Position in dem neuen Feld der individualisierten Gesundheitsversorgung an, die in dem Maße an Bedeutung gewinnt, wie Fortschritte in Bereichen wie z.B. der Genprofilanalyse, die eine frühzeitigere Diagnose und eine bessere Patientenklassifikation ermöglichen, erzielt werden. Auf Grund ihrer klinischen und wirtschaftlichen Vorteile sind vorbeugende Therapien und gezielte medikamentöse Behandlungen nicht nur für Patienten, sondern auch für Kostenträger und Aufsichtsbehörden von Bedeutung.

2.4 Die Geschäftsbereiche Pharma und Diagnostics stellen einschließlich unserer Mehrheitsbeteiligungen an Genentech und Chugai den Kern des Innovations-Netzwerkes von Roche dar. Da sich Roche als Unternehmen sowohl mit Diagnostik als auch mit Pharmazeutika befasst, kann Roche von umfassenden Synergien bei Forschung, Entwicklung und Marketing profitieren. Diese Kapazitäten werden durch Zusammenarbeit im Bereich Technologie und ein Netz von Allianzen bei der Entwicklung individueller Produkte und Produktportfolios noch gesteigert.

2.5 Biotechnologie ist ein wichtiges Element unserer Innovationsstrategie. Derzeit sind ungefähr die Hälfte der Konzernumsätze auf biotechnologisch hergestellte Pharmazeutika zurückzuführen.

Wertschöpfung für die Gegenwart und die Zukunft

2.6 Das Geschäftsmodell von Roche ist darauf ausgerichtet, nachhaltige Werte für alle Interessengruppen zu schaffen: nicht nur für die Aktionäre von Roche, sondern auch für Patienten, die Mitarbeiter von Roche und die Gesellschaft insgesamt.

3. GENENTECH

3.1 Im Juli 2008 hat der Roche-Konzern bekanntgegeben, alle ihm noch nicht gehörenden Aktien von Genentech erwerben zu wollen. Nach monatelangen Verhandlungen mit den Independent Directors (unabhängige Verwaltungsräte) von Genentech hat Roche Investments USA Inc. am 9. Februar 2009 ein öffentliches Angebot für den Erwerb aller ausstehenden Aktien von Genentech zu einem Preis von US-Dollar 86,50 je Aktie in bar abgegeben. Am 12. März 2009 hat Roche mit Genentech eine Übernahmevereinbarung abgeschlossen, wonach der Konzern ein öffentliches Angebot für den Erwerb aller dem Konzern noch nicht gehörenden Genentech-Aktien für US-Dollar 95,00 je Aktie in bar abgibt. Das öffentliche Angebot endete am 25. März 2009 um 24.00 Uhr (New York Zeit). Bei Angebotsschluss am 25. März 2009 waren 84,7 Prozent der ausstehenden, öffentlich gehaltenen Genentech-Aktien angedient. Die Roche Investments USA Inc. hat alle gemäß ihres Kaufangebotes rechtsgültig angedienten Aktien zur Bezahlung angenommen und damit das öffentliche Angebot beendet. Zusammen mit den 55,7 Prozent der ausstehenden Aktien, die von Roche bereits gehalten wurden, hält Roche nun insgesamt etwa 982,9 Millionen Aktien oder 93,2 Prozent der 1.054.555.886 ausstehenden Genentech-Aktien. Zusätzlich wurde die Lieferung weiterer 3,0 Prozent der ausstehenden Genentech-Aktien innerhalb der nächsten drei Geschäftstage nach Abschluss des öffentlichen Angebots garantiert, was zusammen mit den bereits im Zuge des Kaufangebots eingegangenen Aktien und dem bisherigen Anteil von Roche etwa 96,2 Prozent aller ausstehenden Genentech-Aktien ausmachen würde. Aktionäre, die ihre Aktien angedient haben, werden unverzüglich 95,00 US-Dollar pro Aktie für ihre Anteile erhalten. Gemäß der Übernahmevereinbarung hat Roche eine Fusion in der Form eines Short-form Merger veranlasst, in

Page 14

welchem alle nach dem Übernahmeangebot noch verbleibenden Genentech-Aktionäre einen Betrag von US-Dollar 95,00 in bar je Genentech-Aktie erhalten werden, vorbehaltlich des gesetzlichen Bewertungsrechts der Aktionäre. Genentech ist damit eine hundertprozentige Tochtergesellschaft des Roche-Konzerns. Die Genentech-Aktien werden nach Donnerstag, 26. März 2009 nicht länger an der New Yorker Börse gehandelt.

3.2 Der Erwerb aller verbleibenden Publikumsaktien (einschließlich der aufgrund von Genentech's ausstehenden Mitarbeiteraktienoptionen und für Zahlungen diesbezüglicher Gebühren und Auslagen zu begebenden Aktien) kostet ungefähr USD 46,8 Milliarden. Der Konzern hat die Transaktion durch eine Kombination aus dem Einsatz konzerneigener Mittel, der Ausgabe von Commercial Paper, deren Refinanzierung durch eine Kreditfazilität abgesichert ist, und Schuldverschreibungen finanziert. Der Konzern hat durch eine Serie von Schuldverschreibungsemissionen Reinerlöse von ungefähr US-Dollar 46 Milliarden (basierend auf den Wechselkursen vom 20. März 2009) erzielt. Die zur Finanzierung der Transaktion begebene Serie von Schuldverschreibungen besteht aus auf US-Dollar lautenden Anleihen, auf Euro und Pfund-Sterling lautenden Anleihen, aus auf Schweizer Franken lautenden Anleihen sowie aus Commercial Paper.

3.3 Am 25. Februar 2009 hat Roche ein Angebot von auf US-Dollar lautenden Anleihen an qualifizierte, institutionelle Käufer in den Vereinigten Staaten gemäß Rule 144 A sowie an Personen außerhalb der Vereinigten Staaten, die nicht US-Bürger sind, gemäß Regulation S des U.S. Securities Act von 1933 abgeschlossen. Roche hat aufgrund der Emission und des Verkaufs dieser fest und variabel verzinslichen Anleihen insgesamt einen Reinerlös in Höhe von rund USD 16.263,7 Millionen erzielt.

3.4 Am 4. März 2009 hat Roche Euro- und Pfund-Sterling-Anleihen unter ihrem European Medium Term Note (EMTN) Programm emittiert. Roche hat aufgrund der Emission und des Verkaufs dieser Anleihen insgesamt einen Reinerlös in Höhe von ungefähr EUR 11.176,7 Millionen und GBP 1.237,3 Millionen erzielt. Bei den Euro- und Pfund-Sterling-Anleihen handelt es sich um fest und variabel verzinsliche, nicht nachrangige und unbesicherte Schuldverschreibungen.

3.5 Am 20. März 2009 hat Roche ein weiteres Angebot von auf US-Dollar lautenden Anleihen gemäß Rule 144 A des U.S. Securities Act von 1933 abgeschlossen. Roche hat aufgrund der Emission und des Verkaufs dieser festverzinslichen Anleihen insgesamt einen Reinerlös in Höhe von ungefähr USD 2.499,8 Millionen erzielt.

3.6 Die in den Absätzen 3.3 bis 3.5 genannten Anleihen sind Verbindlichkeiten der Roche Holdings, Inc., einer hundertprozentigen Tochtergesellschaft der Roche Holding AG, der obersten Muttergesellschaft des Roche-Konzerns, die auch Garantiegeberin hinsichtlich der Anleihen ist.

3.7 Am 23. März 2009 haben die Roche Kapitalmarkt AG und die Roche Holdings, Inc. ein Angebot von auf Schweizer Franken lautenden und von der Roche Holding AG garantierten Anleihen abgeschlossen. Roche hat aufgrund der Emission und des Verkaufs dieser festverzinslichen Anleihen insgesamt einen Reinerlös in Höhe von ungefähr Schweizer Franken 7.960 Millionen erzielt.

4. RISIKOFAKTOREN

4.1 Die Geschäfte, Betriebsergebnisse und/oder finanzielle Lage von Roche könnten durch Folgendes beeinträchtigt werden:

● Verlust von Patenten oder der Exklusivität der Vermarktung oder den Ablauf von Patenten;

● keine Schaffung von kommerziell erfolgreichen neuen Produkten durch Forschung und Entwicklung;

● den unzulänglichen Schutz geistigen Eigentums in bestimmten Ländern;

● Rechtsstreitigkeiten (Rechtsstreit auf Grund von Produkthaftung, Verstoß gegen Patentrechte oder Kartellgesetze) und staatliche Ermittlungen;

● intensiven Wettbewerb und potenzielles Ersetzen von Produkten;

● Preisbildungskontrollen, Preisdruck, restriktive Auflagen bei der Rückerstattung – Staat und Kostenträger;

Page 15

● Gesundheitsreform;

● aufsichtsbehördliche Kontrollen;

● Unterbrechung der Produktlieferung;

● umweltbedingter Schadensersatz/Haftung;

● Personenschäden bei Mitarbeitern/gesundheitliche Schäden;

● Unfälle mit gefährlichen Stoffen;

● Verlust bzw. Einschränkung der Betriebserlaubnis, u.a. in Folge des Eintretens umweltbedingter Haftung, Personenschäden bei Mitarbeitern/gesundheitlicher Schäden oder Unfällen mit gefährlichen Stoffen;

● Schwierigkeiten bei der Personalbeschaffung;

● von der Öffentlichkeit auf die pharmazeutische Industrie ausgeübten Druck;

● Abhängigkeit von Informationstechnologie;

● die andauernde globale Finanz- und Wirtschaftskrise sowie weitere Veränderungen der globalen Wirtschaftsbedingungen und Politik, die sich auf das Geschäft und die Betriebsergebnisse auswirken könnte.

● Änderung der Steuergesetze mit negativer Auswirkung auf die Konzernerträge;

● Erdbeben, die sich auf das Geschäft und die Betriebsergebnisse auswirken.

4.2 Darüber hinaus unterliegt der Konzern diversen finanziellen Risiken, die sich aus den ihm zugrunde liegenden Betrieben und betrieblichen finanziellen Aktivitäten ergeben wie z.B.:

● Wechselkursrisiken;

● Zinsrisiko;

● Marktrisiko für finanzielle Vermögenswerte;

● Kreditrisiko;

● Liquiditätsrisiko.

4.3 Zudem bestehen für den Konzern Risiken im Zusammenhang mit dem geplanten Erwerb aller ausstehenden Aktien von Genentech wie z.B.

• eine Einschränkung der Handlungsmöglichkeiten des Konzerns aufgrund einer erheblichen Kreditaufnahme des Konzerns im Zusammenhang mit dem geplanten Erwerb aller ausstehenden Aktien von Genentech;

• eine mögliche Herabstufung des Kreditrating von Roche;

• das Risiko, dass die Kosten und Aufwendungen für den Erwerb sehr viel höher ausfallen als erwartet;

• das Risiko, dass der erwartete Nutzen der Akquisition sich aufgrund Intergrations- oder sonstiger Schwierigkeiten nicht realisiert.

Page 16

4.4 Des Weiteren bestehen Risiken insbesondere im Zusammenhang mit den Genussscheinen und dem Connect Programm:

● der Marktpreis der Genussscheine kann Schwankungen unterliegen;

● Inhaber von Genussscheinen in Ländern mit anderen Währungen als Schweizer Franken sind auf Grund von Wechselkursschwankungen einem weiteren Anlagerisiko ausgesetzt;

● Inhaber von Genussscheinen sind im Allgemeinen zu einer dreijährigen Teilnahme am Connect Programm verpflichtet;

● Inhaber von Genussscheinen können nicht bei Generalversammlungen abstimmen;

● mit Zeichnung verpflichten sich die Teilnehmer des Connect Planes zu zukünftigen Anlagen in Genussscheine.

5. AUSGEWÄHLTE FINANZINFORMATIONEN

Die nachfolgenden ausgewählten Finanzinformationen stellen einen Auszug aus den geprüften Konzernabschlüssen dar und sind gemäß International Financial Reporting Standards erstellt worden:

Zum Jahresende /Stand 31. Dezember 2006 2007 2008

Gewinn- und Verlustrechnung des Konzerns in Millionen CHF

Verkäufe 42,041 46,133 45,617 Betriebsgewinn 11,730 14,468 13,896 Inhabern von Roche-Inhaberaktien und Genussscheinen zuzurechnende Nettoerträge

7,880 9,761 8,969

Forschung und Entwicklung 6,589 8,385 8,845

Konzernbilanz in Millionen CHF

Anlagevermögen 33,519 35,349 37,485 Umlaufvermögen 40,895 42,834 38,604 Gesamtvermögen 74,414 78,183 76,089 Langfristige Verbindlichkeiten (14,908) (10,422) (10,163) Kurzfristige Verbindlichkeiten (12,692) (14,454) (12,104) Gesamtverbindlichkeiten (27,600) (24,876) (22,267) Nettovermögen insgesamt 46,814 53,307 53,822 Inhabern von Roche-Inhaberaktien und Genussscheinen zuzurechnendes Kapital und Rücklagen

39,444 45,347 44,479

Nicht-beherrschende Anteile

7,370 7,960 9,343

Wesentliche Kennzahlen

Inhabern von Roche-Inhaberaktien und Genussscheinen zuzurechnender Konzerngewinn in % der Verkäufe

19 21 20

Inhabern von Roche-Inhaberaktien und Genussscheinen zuzurechnender Konzerngewinn in % des den Inhabern von Roche-Inhaberaktien und Genussscheinen zuzurechnenden Kapitals und Rücklagen

20 22 20

Forschung und Entwicklung in % der Verkäufe 16 18 19 Current ratio in % 322 296 319 Eigene Mittel und nicht-beherrschende Anteile in % des Gesamtvermögens

63 68 71

Page 17

Zum Jahresende /Stand 31. Dezember 2006 2007 2008

Angaben zu Aktien und Genussscheinen

Dividenden insgesamt in Millionen CHF 2,933 3,968 4,313 Erträge je Aktie und Genussschein (verwässert) in CHF

9.05 11.16 10,23

Dividenden je Aktie und Genussschein in CHF

3.40 4.60 5,00

Die in dieser Tabelle enthaltenen Informationen basieren auf den Angaben zum Zeitpunkt des Berichts. Änderungen der Rechnungslegungsgrundsätze auf Grund von Änderungen der International Financial Reporting Standards - IFRS (Internationale Standards zur Rechnungslegung) finden keine rückwirkende Anwendung.

6. ZUSAMMENFASSUNG DES CONNECT PLANS

Einleitung

6.1 Der Connect Plan (der „Plan”) soll bestimmten Mitarbeitern eines Unternehmens des Konzerns (ein Mitarbeiter von irgendeinem Unternehmen von Roche ein "Mitarbeiter) Gelegenheit verschaffen, an den Ergebnissen von Roche teilzuhaben, indem diesen eine passende Möglichkeit zum regelmäßigen und systematischen Erwerb von Genussscheinen (siehe unten) geboten wird, wodurch Roche besser in der Lage ist, Mitarbeiter zu gewinnen, zu motivieren und an sich zu binden.

6.2 „Genussscheine” sind nicht stimmberechtigte Eigenkapitalwertpapiere von Roche, die an der Schweizer Börse SIX Swiss Exchange (vormals SWX) notiert und auch zum Handel an dem im Vereinigten Königreich regulierten Marktsegment der SWX Europe (vormals virt-x Exchange) in London zugelassen sind. Die ISIN der Genussscheine lautet CH0012032048.

Teilnahmeberechtigung

6.3 Alle Mitarbeiter, die auf der Gehaltsliste eines Konzernunternehmens stehen, das von dem Exekutivausschuss der Gesellschaft als teilnehmendes Unternehmen („teilnehmendes Unternehmen”) vorgesehen ist und die bei jenem teilnehmenden Unternehmen angestellt sind, sind vorbehaltlich gewisser Ausnahmen zur Teilnahme an dem Plan berechtigt, mit der Maßgabe, dass sie eine Mindestdienstzeit vollendet haben, die Voraussetzung zur Teilnahme in dem jeweiligen Land ist.

6.4 Das Angebot für Genussscheine und das Recht zum Erwerb von Genussscheinen gemäß dem Connect Plan, das durch diesen Prospekt unterbreitet wird, ergeht ausschließlich an Mitarbeiter von teilnehmenden Unternehmen mit Sitz in Deutschland und in jenen Mitgliedstaaten des Europäischen Wirtschaftsraums, in denen die Bundesanstalt für Finanzdienstleistungsaufsicht gemäß Artikel 18 der Prospektrichtlinie (2003/71/EG) der entsprechenden zuständigen Behörde eine Benachrichtigung zugesandt hat. Derzeit wird davon ausgegangen, dass es sich bei diesen Mitgliedstaaten des Europäischen Wirtschaftsraums um Österreich, Belgien, die Tschechische Republik, Dänemark, Finnland, Griechenland, Italien, die Niederlande, Norwegen, Polen, Portugal, Spanien, Schweden und das Vereinigte Königreich handeln wird. Durch diesen Prospekt ergeht kein Angebot an andere Personen in einer anderen Rechtsordnung.

Beitritt zum Connect Plan

6.5 Mitarbeiter, die zur Teilnahme an dem Plan berechtigt sind, wird ein Beitrittsformular zugesandt, welches Einzelheiten zu dem Verwalter des Plans („Verwalter des Plans“) enthält, an den das betreffende Beitrittsformular zurückgeschickt werden muss. Zur Teilnahme an dem Connect Plan berechtigte Mitarbeiter müssen in der Zeit vom 27. April 2009 bis 15. Mai 2009 bei dem hierin angegebenen Verwalter des Plans ein Beitrittsformular einreichen (die „Beitrittsfrist”). Der betreffende Verwalter des Plans kann in seinem alleinigen Ermessen (ohne jedoch hierzu verpflichtet zu sein) Beitrittsformulare, die außerhalb der Beitrittsfrist eingereicht werden, annehmen.

Beitragszahlungen

6.6 Mit dem Beitrittsformular kann ein Teilnehmer an dem Plan (ein „Teilnehmer”) einen festen Jahressatz für Beitragszahlungen in der Landeswährung auswählen. Im Allgemeinen darf der Jahressatz für Beitragszahlungen nicht weniger als 0,5% des jährlichen Grundgehalts des Teilnehmers betragen und darf 10% des jährlichen

Page 18

Grundgehaltes des Teilnehmers nicht überschreiten. Die auf diesem Jahressatz basierenden Beitragszahlungen werden an jedem Zahltag vom Grundgehalt des Teilnehmers abgezogen und in ein für diesen Teilnehmer geführtes „Barkonto“ eingezahlt. Darüber hinaus werden alle ausgeschütteten Dividenden für Genussscheine, die in einem Depotkonto eines Teilnehmers gehalten werden (siehe unten), werden dem Barkonto dieses Teilnehmers gut geschrieben.

Erwerb von Genussscheinen

6.7 Genussscheine werden einmal im Monat vom Verwalter des Plans für den Teilnehmer unter Verwendung des gesamten, auf dem Barkonto des jeweiligen Teilnehmers befindlichen Guthabens erworben. Die auf diese Weise erworbenen Genussscheine werden auf einem „Depotkonto” verwahrt, das für den Teilnehmer geführt wird.

6.8 Alle für den Plan verwendeten Genussscheine werden von dem Verwalter des Plans im Markt erworben. Teilnehmer zahlen jedoch nicht den Preis, der vom Verwalter des Plans auf dem Markt für Genussscheine, die für sie gekauft wurden, gezahlt wurde. Stattdessen wird der durchschnittliche, vom Verwalter des Plans für alle in einem Monat gekauften Genussscheine am Markt entrichtete Preis verwendet, um den Kaufpreis (der „Kaufpreis”) zu ermitteln, den die Teilnehmer für in ihrem Auftrag erworbene Genussscheine zahlen (und der von ihrem Barkonto abgezogen wird). Im Allgemeinen beträgt der Kaufpreis 80% des vom Verwalter des Plans auf dem Markt für Genussscheine gezahlten durchschnittlichen Preises, außer wenn der Kaufpreis unter Verwendung reinvestierter Dividenden bezahlt wird; in einem solchen Fall beträgt der Kaufpreis 100% des gezahlten durchschnittlichen Preises. Diese Prozentangaben unterliegen auch Abweichungen für Teilnehmer in bestimmten Ländern, wie dies in den jeweiligen Ergänzungen für die betreffenden Länder angegeben ist. Alle Differenzen zwischen dem vom Verwalter des Plans für Genussscheine auf dem Markt bezahlten Preis und dem für Teilnehmer geltenden Kaufpreis werden von Roche übernommen.

6.9 Der Verwalter des Plans kauft gewöhnlich Genussscheine am 18. Tag jedes Monats oder am nächsten auf den 18. folgenden Handelstag, wenn der 18. kein Handelstag ist. Die Teilnehmer werden über den von dem Verwalter des Plans für die ihrem Depotkonto zugeteilten Genussscheine in einem Monat gezahlten durchschnittlichen Marktpreis in dem vierteljährlichen Kontoauszug informiert, auf den im folgenden Absatz eingegangen wird. Die Genussscheine werden fortlaufend öffentliche angeboten und der Kaufpreis wird fortlaufend festgesetzt. Informationen über den anfänglichen Verkaufspreis werden in gedruckter Form zur kostenlosen Ausgabe an das Publikum am 23. Juli 2009 am Sitz von Roche, Grenzacherstrasse 124, 4058 Basel, Schweiz bereitgehalten. Darüber hinaus werden Mitarbeiter von Roche, die an dem Connect Plan teilnehmen können, individuell und fortlaufend über nachfolgende Kaufpreise informiert.

Mitteilung über die insgesamt gehaltenen Anlagen und Anzahl der Genussscheine

6.10 Die Teilnehmer erhalten vierteljährlich einen Kontoauszug, in welchem die Gesamtbeträge angegeben sind, die wie folgt angelegt sind: (i) von dem Teilnehmer; (ii) von Roche und (iii) durch Wiederanlage von Dividenden, die für die in dem Depotkonto des Teilnehmers gehaltenen Genussscheine gezahlt wurden, sowie die Gesamtzahl der in dem Depotkonto des Teilnehmers gehaltenen Genussscheine und der von dem Verwalter des Plans für den Erwerb dieser Genussscheine gezahlte Preis.

Übertragbarkeit

6.11 Das Recht auf den Erwerb von Genussscheinen gemäß dem Plan ist nicht handelbar und darf nicht abgetreten, verpfändet oder übertragen werden.

6.12 Genussscheine, die gemäß dem Plan erworben wurden, können während eines „Besitzzeitraums“ von drei Jahren ab dem Zeitpunkt ihres Erwerbs grundsätzlich weder übertragen noch verpfändet werden. Diese Beschränkung wird im Allgemeinen aufgehoben, wenn ein Teilnehmer nicht mehr in einem Angestelltenverhältnis zu Roche steht, gleich aus welchem Grund.

Laufzeit

6.13 Der Plan kann jederzeit von dem Exekutivausschuss durch Mitteilung an die Teilnehmer gekündigt, geändert oder ausgesetzt werden.

Page 19

Länderanhänge

6.14 Es bestehen zusätzliche Bedingungen für Österreich, Belgien, Dänemark, Finnland, Deutschland, Griechenland, Italien, die Niederlanden, Norwegen, Portugal, Spanien, Schweden und das Vereinigte Königreich. Derartige Länderanhänge existieren jedoch nicht für Polen und die Tschechische Republik.

Weitere Informationen

5.15 Mitarbeiter, denen ein Beitrittsformular zugesandt wird, erhalten genaue Kontaktinformationen zu der Person, an die sie sich bei Fragen zu dem Plan wenden können, einschließlich aller länderspezifischen Regeln, die in den oben erwähnten länderspezifischen Ergänzungen enthalten sind.

Page 20

PART 2 RISK FACTORS

Any investment in the Company’s Genussscheine is subject to a number of risks. Prior to investing in the Genussscheine, employees should consider carefully the risks attaching to any investment in the Company’s Genussscheine, the Group’s business and the industry in which it operates, together with all other information contained in this Prospectus including, in particular, the risk factors described below. Additional risks and uncertainties relating to the Group that are not currently known to the Company may also have an adverse effect on the Company’s business, financial condition and operating results. If this occurs the price of the Genussscheine may decline and employees could lose all or part of their investment. Employees should consider carefully whether an investment in the Company’s Genussscheine is suitable for them in light of the information in this Prospectus and their personal circumstances.

Business Risks

Risk that Research & Development will not deliver Commercially Successful New Products

Continued development of commercially viable new products is critical to the Group’s ability to replace sales of older products that decline upon expiration of exclusive rights, and to increase overall sales. Developing new products is a costly, lengthy and uncertain process. A new product candidate can fail at any stage of the process, and one or more late-stage product candidates could fail to receive regulatory approval. New product candidates may appear promising in development but, after significant investments, fail to reach the market or have only limited commercial success for a variety of reasons, e.g. efficacy or safety concerns, inability to obtain necessary regulatory approvals, difficulty or excessive costs to manufacture, infringement of patents or other intellectual property rights of others or inability to differentiate the product adequately from those with which it competes.

Risk of Loss or Expiration of Patents or Marketing Exclusivity

Patent Infringement Litigation

Efforts by generic manufacturers may involve challenges to the validity of a patent or assertions that the alternative compounds do not infringe the Group’s patents. If the Group is not successful during the patent protection or data exclusivity periods in maintaining exclusive rights to market one or more of its major products, the Group’s turnover and margins would be adversely affected.

Generic drug manufacturers may seek to market generic versions of many of the Group’s products, including prior to the expiration of the Group’s patents, and have exhibited a readiness to do so for other products in the future. The risk that Roche’s products are substituted by generic versions also applies to so-called ‘biosimilars’ for which there is a level of uncertainty with regard to the viability and scope of the related patent protection.

Weakness of Intellectual Property Protection in certain Countries

In some of the countries in which the Group operates, patent protection may be significantly weaker than in Switzerland, the USA or the European Union. In addition, in an effort to control public health crises, some developing countries, such as South Africa and Brazil, have considered plans for substantial reductions in the scope of patent protection for products. In particular, these countries could facilitate competition within their markets from generic manufacturers who would otherwise be unable to introduce competing products for a number of years. Any loss of patent protection, including abrogation of patent rights or compulsory licensing, is likely to affect adversely the Group’s operating results in those national markets. Roche has decided not to file patents and will not enforce patent rights in the least developed countries as a matter of its socially responsible management in attempt to increase access to medicine in these countries. Absence of adequate patent protection could limit the opportunity to look to such markets for future sales growth.

Risk of Substantial Adverse Outcome of Litigation and Government Investigations

Unfavourable resolution of proceedings and governmental investigations in which the Group is currently involved and similar future proceedings or investigations may have a material adverse effect on the Group’s results. The Group has made material provisions in 2008, 2007 and 2006 related to legal proceedings and investigations which reduced its earnings. The Group may also make additional significant provisions related to legal proceedings and investigations in the future, which would reduce its earnings.

The Group is selective in taking out insurance for various insurable risks based on an economic assessment of the related insurance cost. If significant risks materialise that are not covered by insurance, then such risks may affect the Group’s business, results or financial condition.

Page 21

Product Safety and Efficacy

Pre-clinical and clinical trials are conducted during the development of potential products to determine the safety and efficacy of products for use by humans following approval by regulatory bodies. Notwithstanding these efforts, when drugs and vaccines are introduced into the marketplace, unanticipated side effects may become evident. Such observations may necessitate change in labelling and marketing or even product withdrawal. Such events may also give rise to litigation against the Group.

Anti-Trust Litigation

In the USA it has become increasingly common that following an adverse outcome in prosecution of patent infringement actions, the defendants and direct and indirect purchasers and other payers initiate anti-trust actions as well. Claims by direct and indirect purchasers and other payers are typically filed as class actions and the relief sought may include treble damages and restitution claims. Damages in adverse anti-trust verdicts are subject to automatic trebling in the USA.

Governmental Investigations

The Group operates globally in complex legal and regulatory environments that often vary among jurisdictions. The failure to comply with applicable laws, rules and regulations in these jurisdictions may result in civil and criminal legal proceedings. Such proceedings may result in trebling of damages awarded or fines in respect of each violation of law. Criminal proceedings may also be initiated against Group companies or individuals.

Risks of Competition and Substitution

The Group operates in highly competitive businesses. In the pharmaceuticals business, it faces competition both from proprietary products of large international manufacturers and producers of generic pharmaceuticals. Significant product innovations and substitution, technical advances or the intensification of price competition by competitors could adversely affect the Group’s operating results. Continued consolidation and co-operation in the pharmaceutical industry could adversely affect the Group’s competitive position, while continued consolidation and co-operation among the Group’s customers may increase pricing pressures.

The diagnostics business is also highly competitive and Roche encounters competition from several international manufacturers.

If any of the Group’s major products were to become subject to a problem such as loss of patent protection, unexpected side effects, regulatory proceedings, publicity affecting doctor or patient confidence or pressure from competitive products, or if a new, more effective product should be introduced, the adverse impact on the Group’s revenues and operating results could be significant.

Generic products often enter the market upon expiration of patents or data exclusivity periods for the Group’s products. Introduction of generic products typically leads to a dramatic loss of sales and reduces the Group’s revenues and margins for its proprietary products.

Pricing and Reimbursement: Governmental and Payer Controls

Pharmaceutical products are subject to price controls or pressures and other restrictions in many markets. Some governments intervene directly in setting prices. In addition, in some markets major purchasers of pharmaceutical products (whether governmental agencies or private health care providers) have the economic power to exert substantial pressure on prices or the terms of access to formularies. The growth in the number of patients covered through large managed care institutions may also increase pricing pressure on the Group’s products. Changes to government reimbursement policies could reduce the funding that healthcare service providers have available for diagnostic and pharmaceutical product expenditures, which could have a material adverse impact on Roche’s sales and/or profit margin.

The Group cannot predict whether existing controls will increase or new controls will be introduced that will reduce the Group’s margins or affect adversely its ability to introduce new products profitably. Changes in the healthcare market could also force Roche to alter Roche’s approach to selling, marketing, distributing and servicing Roche’s customer base.

Regulatory Controls

The Group must comply with a broad range of regulatory controls on the testing, approval, manufacturing and marketing of many of its pharmaceutical and diagnostic products, particularly in the USA and countries of the European Union, that affect not only the cost of product development but also the time required to reach the market and the uncertainty of successfully doing so.

Page 22

Stricter regulatory controls also heighten the risk of withdrawal by regulators of approvals previously granted, which would reduce revenues and can result in product recalls and product liability lawsuits. In addition, in some cases the Group may voluntarily cease marketing a product or face declining sales based on concerns about efficacy or safety, whether or not scientifically justified, even in the absence of regulatory action. The development of the post-approval adverse event profile for a product or the product class may have a major impact on the marketing and sale of the product.

Risk of Interruption of Product Supply

The products Roche market, distribute and sell are either manufactured at Roche’s own dedicated manufacturing facilities, or through toll manufacturing arrangements or supply agreements with third parties. Since many of Roche’s products are the result of technically complex manufacturing processes, and are sometimes dependent on highly specialised raw materials or regulatory approval, Roche can provide no assurances that supply sources will not be interrupted. In addition, for these same reasons, the volume of production of any product cannot be rapidly altered. As a result, if Roche should fail to accurately predict market demand for any of Roche’s products then Roche may not be able to produce enough of the product to meet that demand, or may produce too much of the product, either of which could affect Roche’s business and operating results.

The manufacture of pharmaceutical products and their constituent materials requires compliance with good manufacturing practice regulations. The Group’s manufacturing sites are subject to review and approval by the U.S. Food and Drug Administration (“FDA”) and other regulatory agencies. Compliance failure by suppliers of key materials or the Group’s own manufacturing facilities could lead to product recalls and seizures, interruption of production and delays in the approvals of new products pending resolution of manufacturing issues. Non-compliance can also result in fines and disgorgement of profits. Any interruption of supply or fines or disgorgement remedy could materially and adversely affect the Group’s financial results. While the Group undertakes business continuity planning, single sourcing for certain components, bulk active materials and finished products creates a risk of failure of supply in the event of regulatory non-compliance or physical disruption at the manufacturing sites.

Risks from the Handling of Hazardous Materials, and Environmental Damage and Waste could negatively impact Roche’s Operating Results

Roche’s operations are subject to the operating risks associated with pharmaceutical and chemical manufacturing, including the related risks associated with processing, storage and transportation of raw materials, products and wastes. These risks include, among other things, the following hazards:

● pipeline and storage tank leaks and ruptures;

● fires and explosions;

● injuries and damage to Roche’s employees’ health;

● malfunction and operational failure; and

● releases, discharges or disposal of toxic and/or hazardous substances resulting from these or other causes.

These operating risks have the potential to cause personal injury (including to Roche’s employees), property damage and environmental contamination, which may result in the shutdown of affected facilities, loss of or restrictions to operating licences, business interruption, the imposition of criminal penalties and civil liabilities in respect of employees’ health/injuries (including by way of class action) and environmental damage, and generally may negatively impact the reputation of the Company. The occurrence of any of these events may significantly reduce the productivity and profitability of the affected manufacturing facility and harm Roche’s operating results. Furthermore, Roche’s property damage, business interruption and casualty insurance policies may not be adequate to cover fully all potential hazards incidental to Roche’s business.

The environmental laws of many jurisdictions impose actual and potential obligations on Roche to remediate contaminated sites. These obligations may relate to sites:

● that Roche acquire, own or operate;

● that Roche formerly owned or operated;

● where waste from Roche’s operations was disposed; or

Page 23

● that are affected by Roche’s operations (for example by contamination of soil, air or water).

These environmental remediation obligations could significantly reduce Roche’s operating results. In particular, Roche’s financial accruals for these obligations may be insufficient if the assumptions underlying the accruals — including Roche’s assumptions regarding the portion of the waste at a site for which Roche is responsible-prove incorrect, or if Roche is held responsible for additional contamination.

Stricter environmental, safety and health laws and enforcement policies could result in substantial costs and liabilities to Roche, and could subject Roche’s handling, manufacture, use, reuse or disposal of substances or pollutants to more rigorous scrutiny than is currently the case. Consequently, compliance with these laws could result in significant capital expenditures as well as other costs and liabilities, thereby harming Roche’s business and operating results.

Human Resources

The Group has more than 80,000 employees around the world and is subject to laws and regulations concerning its employees — including discrimination and harassment, personal privacy, labour relations and working conditions — that vary significantly from jurisdiction to jurisdiction. Changes in such laws and regulations can increase compliance costs and failure to comply with applicable requirements could have a significant adverse affect on the Group. To sustain growth and innovation, the Group is dependent on there being sufficient employees with adequate skills available in the labour market. Unfavourable developments in the labour market could adversely affect the Group.

Public Pressure on the Pharmaceuticals Industry could affect Roche’s Business and Results of Operations.

There is considerable public sentiment against the pharmaceutical industry, and the industry is under the close scrutiny of the public and the media. In addition there is significant pressure on Roche’s industry from certain disadvantaged nations and non-governmental groups to make Roche’s products available to their people at drastically lower costs. Any increase in such negative public sentiment or increase in public scrutiny or pressure from such disadvantaged nations could lead, among other things, to changes in legislation, to changes in the demand for Roche’s products, additional pricing pressures with respect to Roche’s products, or increased efforts to undercut intellectual property protections. Such changes could affect Roche’s business and results of operations.

Reliance on Information Technology

The Group is increasingly dependent on information technology systems, including Internet-based systems, for internal communication as well as communication with customers and suppliers. Any significant disruption of these systems, whether due to computer viruses or other outside incursions, could materially and adversely affect the Group’s operations.

Changes in Global Economic Conditions and Politics could affect the Group’s Business and Results of Operations.

Roche’s future results could be affected by global economic and political changes. The ongoing global economic crisis and related recessionary conditions in many countries where the Group does business could affect sales of the Group’s pharmaceuticals and diagnostics in those markets, as the ability of patients and payors (such as health insurance plans) to pay for these products could be adversely impacted. These and other effects of recent global economic conditions could adversely affect the Group’s business and financial performance.

In the recent past, terrorist attacks have had an impact on global economic conditions. Any additional terrorist attacks which may occur in the future, and any significant military activity around the world, could have a similar impact, which could affect adversely the Group’s business and results of operations.

Changes in Tax Laws could adversely affect the Group’s Earnings.

Changes in the tax laws of the countries in which Roche does significant business, as well as changes in Roche’s effective tax rate for the fiscal year caused by other factors, including changes in the interpretation of tax law by local tax officials, could affect Roche’s net income. It is not possible to predict the impact on Roche’s results of any tax legislation which may be enacted in the future.

Earthquakes could affect Roche’s Business and Results of Operations.

Roche’s corporate headquarters and certain of Roche’s major production facilities are located near major earthquake fault lines in Basel, Switzerland, San Francisco, USA and Tokyo, Japan. In the event of a major

Page 24

earthquake, Roche could experience business interruptions, destruction of facilities and/or loss of life, all of which could materially adversely affect Roche.

Financial Risks

The Group is exposed to various financial risks arising from its underlying operations and finance activities. The Group’s financial risk exposures are predominantly related to changes in foreign exchange rates, interest rates and equity prices as well as the creditworthiness and the solvency of the Group’s counter-parties.

The Group actively measures, monitors and manages its financial risk exposures by various functions pursuant to segregation of duties principles and in accordance with its financial policies. Failure in compliance or in managing these risks in the dynamics of the financial markets may have an adverse effect on the financial results or condition of the Group.

Foreign Exchange Risk

The Group operates across the world and is exposed to movements in foreign currencies affecting its net income and financial position, as expressed in Swiss francs.

Transaction Exposure arises because the amount of local currency paid or received for transactions denominated in foreign currencies may vary due to changes in exchange rates. For many Group companies revenues and operating expenses are primarily in the local currency. Similarly, transaction exposure arises on net balances of monetary assets held in foreign currencies. This may have an adverse effect on net income and/or net assets.

Translation Exposure arises from the consolidation of the foreign currency denominated financial statements of the Group’s foreign subsidiaries.