public fraud & theft in the workplace. economic downsizing in local governments

TRANSCRIPT

THE PERFECT STORM

Public Fraud & TheftIn the Workplace

Why The Perfect Storm?

Economic Downsizing in Local Governments

Why The Perfect Storm?

Employee Wage Freezes, Furloughs, and Reduced Benefits

Why The Perfect Storm?

Economic Hardships on Individual EmployeesLoss of Dual IncomesLoss of Investments or Home ValuesIncreased Expenses or Medical CostsLooming Retirement Date

Why The Perfect Storm?

Justification/Anger Due To “Wall Street” Bailout or Actual/Perception City Management not Sharing the Cutting Pain

Why The Perfect Storm?

Rapid Changes in Financial Systems; including speed, volume, and complexity of transactions

and

Improvements to technology and improved access to personal information.

Why The Perfect Storm?

Changing Societal Values

Symantec Smart Phone Honey Stick ProjectPlanted 50 “lost” phones and tracked their movement, return rates, and pilferage of personal data 89% Accessed Personal Data 72% Accessed Personal Pictures 57% Accessed Password Folders 43% Tried to Access Banking Apps Less than 50% tried to return the phone

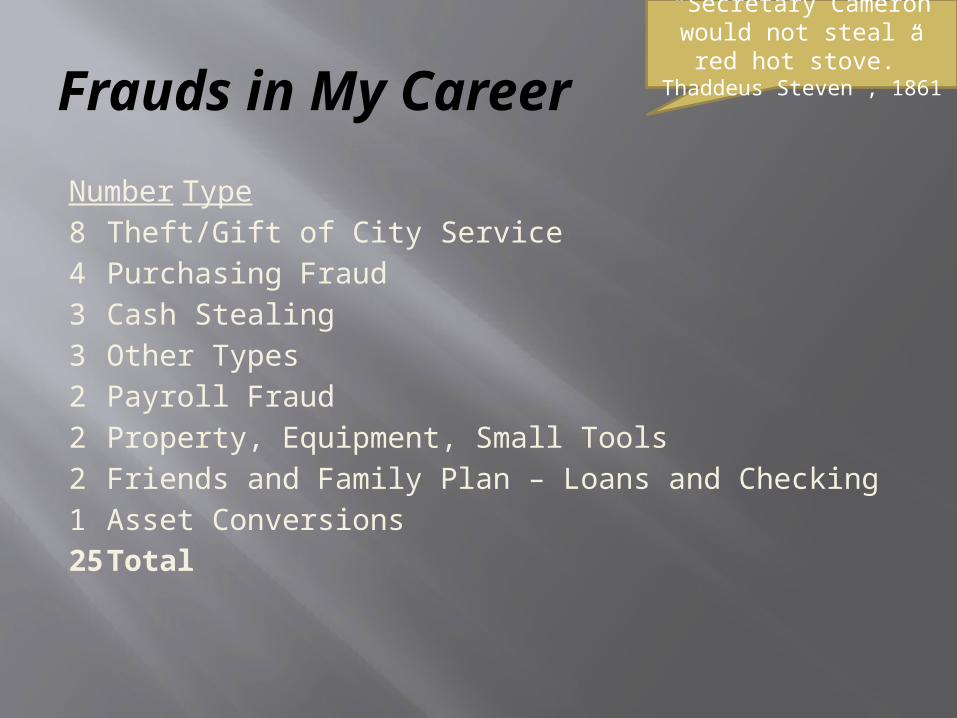

Frauds in My Career

Number Type8 Theft/Gift of City Service4 Purchasing Fraud3 Cash Stealing3 Other Types2 Payroll Fraud2 Property, Equipment, Small Tools2 Friends and Family Plan – Loans and Checking1 Asset Conversions25 Total

“Secretary Cameron would not steal a red

hot stove.”Thaddeus Steven , 1861

Recent Frauds in the News

$1.6 (m) – Franklin CountyPublic Works ManagerAccused - Payables FraudTook Over Bankrupt Company IDCreated Quasi Bank AccountApproved Invoices payable to Company8 years

“Where do people steal the money? They steal it on the

way in and the way out.Joe Derives, SAO

Recent Frauds in the News

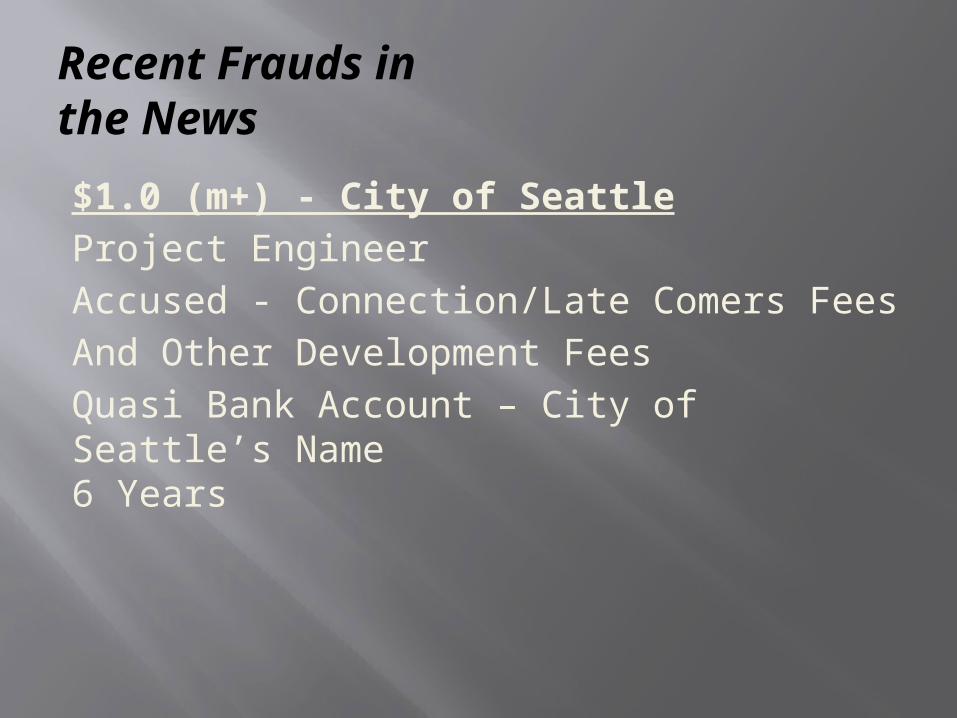

$1.0 (m+) - City of SeattleProject EngineerAccused - Connection/Late Comers FeesAnd Other Development FeesQuasi Bank Account – City of Seattle’s Name6 Years

Recent Frauds in the News

$468(k) – Birch Bay WSDFinance ManagerCredit Cards, Payables, Travel Fund, Quasi Bank Account 8 Years

Recent Frauds in the News

$1.3 (m) – City of ArlingtonFinance Accounting ClerkAccounts Payable - Manual WarrantsQuasi Bank Account8 Years

Recent Frauds in the News

$151(k) – City of Lakewood Police GuildPolice Officer Accused - Donations for Memorial Trust FundQuasi Bank Account2 Years ?

Internal Controls

Strong internal controls will not stop fraud!

“Ability is nothing without opportunity.

Napoleon Bonaparte

Internal Controls

Strong internal controls will decrease the likelihood of fraud; and,

Internal Controls

Strong internal controls will decrease the likelihood of fraud; and,

Increase the speed in which the fraud is identified; and,

Internal Controls

Strong internal controls will decrease the likelihood of fraud; and,

Increase the speed in which the fraud is identified; and,

Create a better record trail to identify and determine who committed the fraud, its duration, and the amount.

Good Internal Controls

Dual Controls, Segregation of Duties, Four Eyes Principle

“Trust, but verify”Ronald Regan

Good Internal Controls

Pre Employment Background Checks? In the Franklin County fraud, the

employee was hired 8 months after being released from Federal prison for creating a fake company to steal from the Federal Government.

Good Internal Controls

Pre Employment Background Checks? A former Deputy City Clerk, arrested for

$7.5 (k), then hired as a bookkeeper for a local roofing company and was later convicted for a $200(k) fraud.

Should be noted that she said stole for a psychological need to help other people by giving them money.

Good Internal Controls

Pre Employment Background Checks! Follow your background checks, and

don’t hire people that do not pass the background.

Good Internal Controls

Daily DepositsDaily Cash CountsCheck and Cash CompositionDual Verification of Deposits and Posting ReportsDaily Verification of All Deposits

Good Internal Controls

Check Issue and RedemptionControl of Check StockInvoice Approval by Non-Check IssuerDetailed Receipts/Invoices for PaymentCheck Redemption by Non-Check IssuerFinal Payments and Invoices Reviewed by Non-Check IssuerPositive Pay with Bank by both Check # and Amount

Good Internal Controls

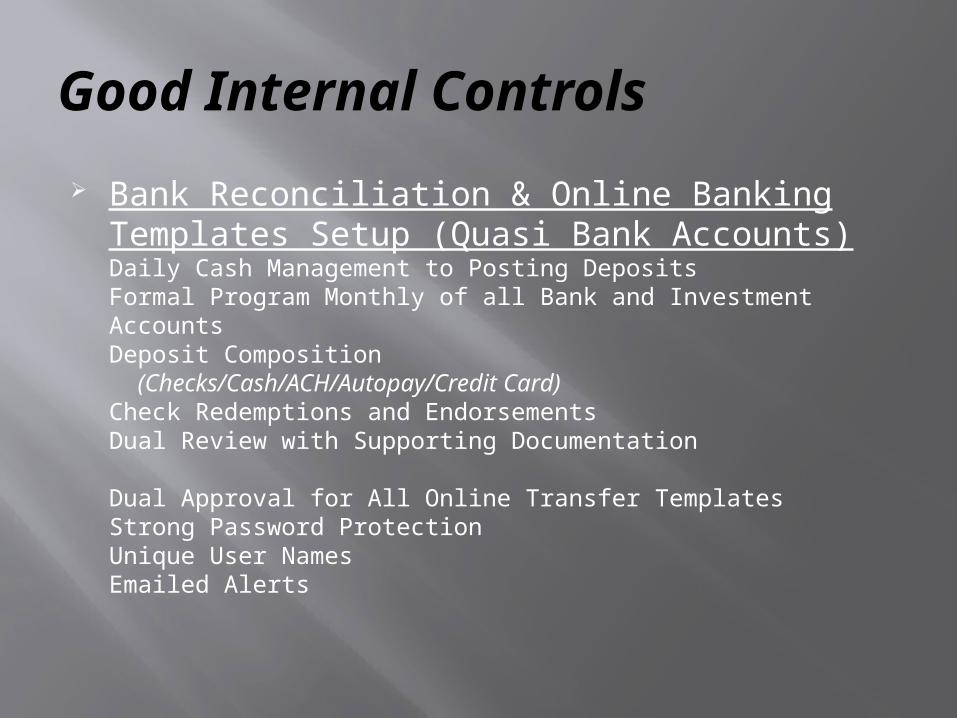

Bank Reconciliation & Online Banking Templates Setup (Quasi Bank Accounts)Daily Cash Management to Posting DepositsFormal Program Monthly of all Bank and Investment AccountsDeposit Composition (Checks/Cash/ACH/Autopay/Credit Card)Check Redemptions and EndorsementsDual Review with Supporting Documentation

Dual Approval for All Online Transfer TemplatesStrong Password ProtectionUnique User NamesEmailed Alerts

Good Internal Controls

Accounts Receivables Utility Billing RegistersOff Book ReceivablesConnection, Latecomer, and ULID PaymentsReconciliation between Payments and Services

Good Internal Controls

Payroll Written Documentation and Approval of Pay Rates and BenefitsReview of Check IssuesReconciliation of Taxes PaidReview of Key Employee Payroll and Paid Time Off ReportsRandom Review of Time Reporting RecordsVerification of Checks Issued to Actual Employees

Inside a Fraud

All fraud is based on deception 1. Most frauds are larger than initially thought;

“All war is deception”

Sun Tzu

Inside a Fraud

All fraud is based on deception1. Most frauds are larger than initially thought;2. Not uncommon to have “stumbled” on the fraud

prior to detection;

Inside a Fraud

All fraud is based on deception1. Most frauds are larger than initially thought;2. Not uncommon to have “stumbled” on the fraud

prior to detection;3. Fraud will have a civil element and may have a

separate criminal element;

Inside a Fraud

All fraud is based on deception1. Most frauds are larger than initially thought;2. Not uncommon to have “stumbled” on the fraud

prior to detection;3. Fraud will have a civil element and may have a

separate criminal element;4. Fraud auditing and resolution take a significant

amount of time;

Inside a Fraud

All fraud is based on deception1. Most frauds are larger than initially thought;2. Not uncommon to have “stumbled” on the fraud

prior to detection;3. Fraud will have a civil element and may have a

separate criminal element;4. Fraud auditing and resolution take a significant

amount of time;5. Rare that a person doing fraud will admit to the

fraud.

Inside a Fraud

Expect Counter Claims to Arise Americans with Disabilities Act

Inside a Fraud

Expect Counter Claims to Arise Americans with Disabilities Act Hostile Work Environment and Sexual

Harassment

Inside a Fraud

Expect Counter Claims to Arise Americans with Disabilities Act Hostile Work Environment and Sexual

Harassment Washington State Whistleblowers

Inside a Fraud

Expect Counter Claims to Arise Americans with Disabilities Act Hostile Work Environment and Sexual

Harassment Washington State Whistleblowers The Everyone Else is Doing Theory

Your Protections When Fraud is Up the Chain

Washington State WhistleblowersR.C.W. 42.40.030 protects State employees when they file a whistleblower complaint

R.C.W. 42.41 Local Government Whistleblower Act Protection for Counties, Cities, and Special Purpose Districts is their own Agency’s Whistleblowers Policy, or the County Prosecutor’s Officer if the agency has not adopted a Whistleblower Policy

“By failing to prepare, you are preparing for

failure”Benjamin Franklin

Reporting Requirements

R.C.W. 43.09.185 – Requires state and local agencies to report immediately to the State Auditor’s Office known or suspected loss of funds or assets or other illegal activities.

Reporting Requirements

R.C.W. 43.09.185 – Requires state and local agencies to report immediately to the State Auditor’s Office known or suspected loss of funds or assets or other illegal activities.

Management Representation Letter – Chief Executive Officer and Chief Financial Officer are fiduciary responsible to disclose any loss of funds, or assets or other illegal activities.

Special Note – On Settlements

R.C.W. 43.09.260 (7)– Requires any compromise or settlement of any claim arising from malfeasance, misfeasance, or nonfeasance, or by any action therefore, or for any court to enter upon a compromise or settlement of such action without the written approval of the attorney general and the state auditor.

Internal Fraud Team

City Manager or Chief Executive OfficerPolice Chief or SheriffCity AttorneyHuman ResourcesState Auditor’s OfficeWCIA (Pre-Defense Review on Personnel Action)Colleagues (with reservations)

Final Thoughts

The cost of fraud is not only measured in the in the lost dollars. Stress Time Consuming Emotionally Demanding and Draining Divisive Tarnishes the reputation of the agency and all

the other hard working honest employees

All Public Employees Carry Each Other’s Honor