quebec government bodies round table laurette saade, rq david girard boucher, rq pierre morin, csst...

TRANSCRIPT

Quebec Government Bodies Round TableLaurette Saade, RQ

David Girard Boucher, RQPierre Morin, CSST

Robert Dicaire, R2D1 Inc.Marie Lyne Dion, STM

CSST Sub-Contractors and Volunteers

• Employers responsible for ensuring sub-contractors and volunteers are covered by the CSST.

• If not, employer to pay remittances by March 15 without penalty or interest.

Safe Maternity Experience program

• For the five working days following her temporary withdrawal from work, the worker is paid her regular salary by her employer; this amount is not refunded by the CSST.

• For the 14 calendar days following this initial five-day period, the employer pays the worker 90% of her net salary. This amount is refunded to the employerby the CSST.

…Province of taxation•If a non-Quebec resident works at the employer’s establishment in Quebec: •QPP instead of CPP•EI at the Quebec rate•Deduct QPIP•Federal income tax (Quebec table) •Quebec income tax•All employer contributions:

–CSST – Commission de la santé et de la sécurité du travail – QWCB –QHSF – Quebec Health Services Fund –CNT – Commission des normes du travail – QLS–WSDRF – Workforce Skills Development and Recognition Fund

•T4 and R1•Inform your insurance carrier that the employee lives in Ontario and that sales tax should be at 8%•Remove any Quebec only taxable benefits

QPP

• No maximum age limit:• You are over 18, you work, you pay!

• Successive employers:• No work interruption, consider previous contributions –

CRA is now following the same rules… well almost… unless you change your status!

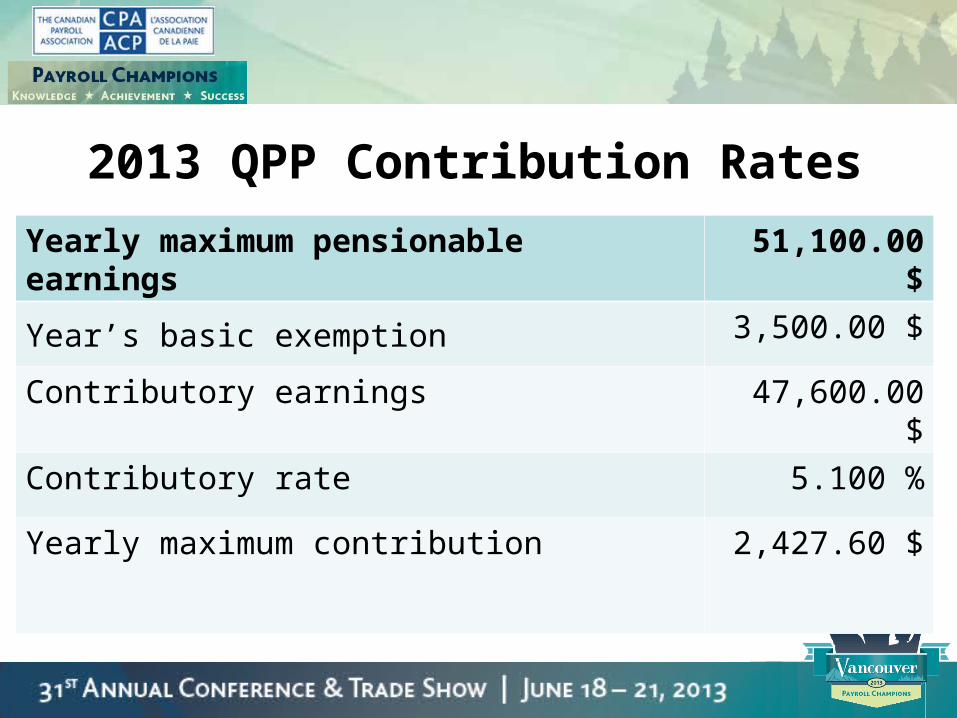

2013 QPP Contribution Rates

Yearly maximum pensionable earnings 51,100.00 $

Year’s basic exemption 3,500.00 $

Contributory earnings 47,600.00 $

Contributory rate 5.100 %

Yearly maximum contribution 2,427.60 $

Parental insurance

• What is the Quebec Parental Insurance Plan (QPIP)?– Government plan provides an income replacement

for eligible workers during a maternity, paternity, parental and adoption leave which are different from those available under EI in a number of ways.

Parental insurance

• Eligibility Criteria:• Employee or self-employed person with a minimum

annual income of $ 2000,• Being a Quebec resident or, for a self-employed, being a

Quebec resident on December 31 of the year prior to receiving the benefits.

• Has an income reduction of at least 40%.• Pay premiums under the QPIP

2013 QPIP Rates (within Quebec only)

Yearly maximum insurable earnings 67,500.00 $QPIP premium rate 0.559 %Employee maximum yearly premium 377.33 $Employer premium rate 0.782 %

Employer maximum yearly premium (No reduced rate available)

527.85 $

2013 EI Premium Rate(within Quebec)

Yearly maximum insurable earnings 47,400.00 $

Employment insurance premium rate 1.52 %

Employee maximum yearly premium 720.48 $

Employer maximum yearly premium(Unreduced – 1.4 times employee)

1 008.67 $

HSF – Contribution rate calculation

•Employer’s worldwide annual payroll amount determines the HSF contribution rate:•Payroll less than 1 million: 2.70%•Payroll more than 5 million: 4.26%•Payroll between 1 and 5 million: • 2.31 + (0.39 x S) • Where S = Payroll $ 1 million

HSF

• The total payroll (worldwide) is only used to determine the rate of contribution based on the sum of all payroll value of all associated employers at the end of a calendar year.

HSF – Example 1

• From Jan. to Oct 31 an employer has a total payroll of $ 500.000 – the rate of contribution is 2.7%

• Nov 10 – merger with a company in China and USA• At year-end the WW payroll is more than $ 5 M• The contribution for the ENTIRE year will now be 4.26 %

HSF – Example 2… oups forgot my division in BC

• Employer paid the HSF contribution without taking the associated employer payroll amount into consideration.

• Balance to pay from the RLZ-1.S = $ 12 480 (34 080 - 21 600).• Interest to be paid:

– On 12 480 $ (34 080 $ - 21 600 $) from Feb 28

HSF Contribution

Contribution for 2012 Contribution to be reported on the RLZ-1.S

($ 800 000 x 2,7 %) ($ 800 000 x 4,26 %)

$ 21 600 $ 34 080

Taxability • Insurance paid for Medical, Dental and Visual coverage • Meals and transportation expenses when working

overtime – receipts else TB – no max (17$)• Gifts and rewards (gift certificates is non-monetary) • Professional membership – if required for work… TB• Moving expenses ….see note: http

://www.cra-arc.gc.ca/F/pub/tp/it178r3-consolid/it178r3-consolid-f.pdf

• Payment in lieu of notice

Non-monetary gifts and rewardsFederal

• Separate $ 500 exemption for Long Service Award

• Unlimited number of gifts and awards

• Any amount above $ 500 is taxable

• For any gift or award given in cash, the amount is considered pensionable, insurable, taxable to the employee, subject to all statutory deductions.

Quebec•non-monetary gifts given to an employee for a special occasion (such as Christmas, a birthday, wedding, etc), up to $500 (incl taxes) per year; and•non-monetary rewards given to an employee in recognition of certain accomplishments (such as reaching a certain number of years of service, meeting safety requirements, or achieving objectives), up to $500 (including taxes) per year.•Gift certificates, gift coupons and smart cards that must be used to purchase goods or services from a designated business or list of businesses are not considered to be easily convertible into cash•Unlimited number of gifts and awards•Any amount above $ 500 is taxable

Reminder: Insurance Coverage

Type of coverage Federal Quebec

Life X X

Dependant Life X X

AD&D X X

Medical X

Dental X

Visual X

Health Spending Account * X

Group Insurance – Serious Illness

• Lump sum amount paid to beneficiary that can be used to pay for any expenses during the hardship period

• Any amount paid by the employer for this coverage is a taxable benefit and must be reported in boxes A and L of the RL-1 slip

• The employee can not use this benefits as a credit for medical expenses

Group Insurance – Live / AD&D

• Group insurance paid in full or in part by the employer for: – Life of an employee and / or spouse / dependants – Death or dismemberment

Taxable benefits to be reported in boxes A and L of the RL-1 slip

Group Insurance – Loss of Income

Loss of employment income premiums Contributions Benefits received

Premiums paid by the employee and the employer Non Taxable* Taxable

Premiums only paid by the employer Non Taxable* Taxable

Premiums only paid by the employee Non Taxable Non Taxable

* Premium paid by the employer would be considered a taxable benefit if a lump-sum payment made to the employee instead of periodic payments (considered income under section 43 of the TA).

Health Contribution

• Since Jan 2013, health contribution deductions are included as part of the Quebec income tax– employee may claim an exemption in box 22 of the

TP-1015.3• Employer must remit at the same time as other DAS• Grace period to apply the deduction – March 2013

Professional Membership• Federal

– If you pay professional membership dues on behalf of your employee and the employer is the primary beneficiary of the payment, there is no benefit to the employee

• membership is a condition of employment• The employer is the primary beneficiary

• Quebec– If you pay or reimburse the professional membership dues of an employee,

he or she receives a taxable benefit– It may be considered that such a payment or reimbursement is not a

taxable benefit if the facts show that the payment or reimbursement is entirely or almost entirely for the employer’s benefit (not work related)

Overtime Meals and allowances

FederalNon Taxable if :• The employee works two or more

hours of overtime right before or right after his or her scheduled hours of work.

• The overtime is infrequent and occasional in nature (usually, less than three times a week)

• The allowance, or the cost of the meal, is reasonable ( a value of up to $17)

QuebecNon Taxable if :• The meal expenses incurred by the

employee are reimbursed (in whole or in part) upon presentation of receipts.

• The reimbursed amount / the value of the meal provided by the employer is reasonable.

• At least 3 hours of overtime • Infrequent

Indemnity for damagesTaxable or not?

An amount received in respect of a loss of an office or employment as damages or pursuant to an order or judgment of a competent tribunal constitute: •Retiring allowance if the employee does not return to work•Employment income when an employee reintegrates his employment

An amount that is received as an indemnity for physical, mental or moral damages due to bodily injury or death, and that is awarded by a court of competentjurisdiction or from an out-of-court settlement is generally not taxable if it covers: •Reimbursement of medical or hospital expenses•Compensation for pain and suffering, the accrued or future loss of income, the loss of enjoyment of life and longevity, the impairment or loss of earning capacity, or the loss of the family provider

Clothing Employer provided clothing to employees is not taxable to the employees when it is required to wear as part of their functions if: •Distinctive clothing i.e.: inappropriate outside of the work environment •The value is reasonable

Lieu of notice

• Federal– Lieu of notice is considers by CRA as employment

income – Subject to CPP and EI– Bonus tax calculation method can be used

• Quebec– Amount paid is considered as Retiring Allowance

(Lump Sum rate)

A Retiring Allowance may include…

• Unused sick bank• Year of Service recognition• Severance payment• Amount paid to end an employment including

damage and interest (unjustified termination)• Damage and interest due to a court decision• Lieu of notice (Quebec only)

Taxation and reporting SummaryPayment Federal Québec

CPP EI Tax Reporting QPP QPIP Tax Reporting

Legislated payment

Worked Notice

Yes Yes Yes Regular

T4 Box 14 Yes Yes Yes Regular

Relevé 1 Box A

Lieu of Notice

Yes Yes Yes Bonus

T4 Box 14 Non Yes Yes Lump Sum

Relevé 1 Box O Code RJ

Severance Pay ON & Federal

Non Non Yes Lump Sum

T4 Box 66 and/or 67

Non Non Yes Lump Sum

Relevé 1 Box O Code RJ

Additional payment

Retiring Allowances

Non Non Yes Lump Sum

T4 Box 66 and/or 67

Non Non Yes Lump Sum

Relevé 1 Box O Code RJ

Employee / employer relationship

Salary continuance

Yes Yes Yes Regular

T4 Box 14 Yes Yes Yes Regular

Relevé 1 Box A

Progressive Retirement

Program that allows and employee to continue his contributions to QPP on his full salary while progressively reducing his worked hoursExample:

Reporting: Box A Box U

(presumed salary)Box G

$ 36, 800 $ 9, 200 $ 46, 000

Employee full salary $ 46,000

Work reduction 20% $ 9,200

Progressive RetirementConditions

• Employee is between 55 and 70• Must have contributed to QPP the previous year• Can not receive retirement or invalid benefits from QPP• Income must be greater than $3500• Must be the same employer as the previous year if not the new employer

must consent to the conditions• The employee/employer relationship must never be broken between the time

the employee was full time and his progressive retirement • Both employee and employer contributions must be done• The employee and the employer must agree to the conditions• The agreement must be approved by QPP

Contributions to Normes du travail

• Employers who have employees working in Quebec must contribute to the financing of the Quebec Labour Standards – this contribution covers the cost of administering the law.

• The contribution is calculated at a universal rate of 0.08% ($ 0.80 per $1 000). The contribution stops when an employee exceeds the salary of $ 67,500 (for 2013)

• 4% paid every pay period

Pay slip

• Name of employer • Employee’s first and last

name• Job title• Pay Period and pay dates• Paid hours and rate of

pay • Overtime hours and rate

of pay

• Premium, allowances, indemnities and commissions

• Wage rate or Salary• Gross earnings• Deductions (name and

amount)• Tips• Net Pay

WSDRF• For employers with annual payroll over

$ 1 million• Employers must train their employees for a

minimum of 1 % of their payroll, otherwise they must contribute to the fund when submitting their Summary (RLZ-1.S)

• Employer must complete the form «Déclaration des activités de formation de la Commission des partenaire du marché du travail »

Relevé 17Remuneration for employment outside Canada

The amount entered in box B of the RL-17 slip must include the aggregate of salaries or wages, and allowances paid during the year for employment outside of Canada. This amount must also be entered in box A of the RL-1 slip. Deductions for employment income earned outside of Canada based on Box A of the RL 17:

Contract or agreement signed before Jan 1, 2013

Contract or agreement signed after Decembre 31, 2012

2013 2014 2015 2016

100 % 100 % 100 % 0 %

2013 2014 2015 2016

75 % 50 % 25 % 0 %