r3 summit handout - bkd

TRANSCRIPT

3/10/2021

1

Housekeeping Items• Small Group Discussions

• Breaks – Stay Logged in for the Entire Day

• Questions – Chat Questions & Unmute During Small Group Discussions

1

2

3/10/2021

2

Packed Agenda

• Economic Update & Higher Education Outlook

• Tax & Accounting Update

• Strategic Options for Managing Challenging Financial Circumstances

• Tips for Leadership in Crisis

• & More!

Economic UpdateMoody’s – Michael Osborn

3

4

3/10/2021

3

What Is Next for Higher Education?2021 Annual Higher Education OutlookAbsorbing Chaos, Giving Back Calm, Providing Hope

What’s Next?New U.S. Presidential Administration & Congressional Majority

5

6

3/10/2021

4

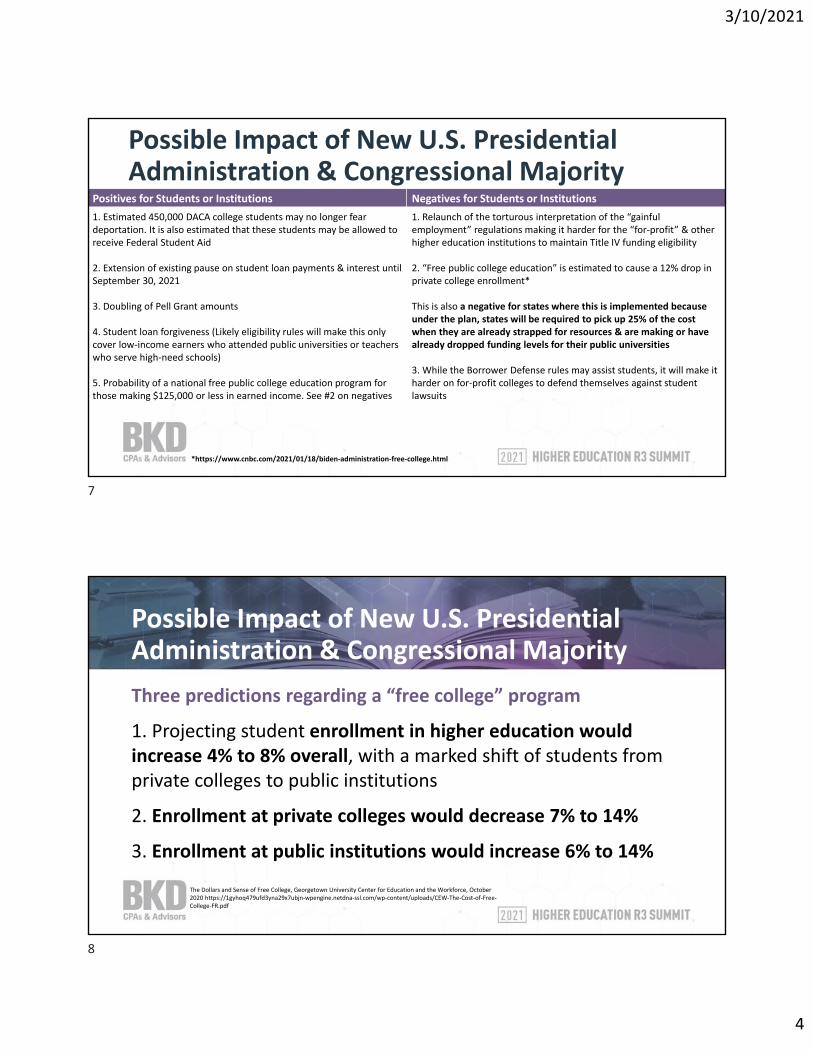

Possible Impact of New U.S. Presidential Administration & Congressional Majority

Positives for Students or Institutions Negatives for Students or Institutions

1. Estimated 450,000 DACA college students may no longer fear deportation. It is also estimated that these students may be allowed to receive Federal Student Aid

2. Extension of existing pause on student loan payments & interest until September 30, 2021

3. Doubling of Pell Grant amounts

4. Student loan forgiveness (Likely eligibility rules will make this only cover low‐income earners who attended public universities or teachers who serve high‐need schools)

5. Probability of a national free public college education program for those making $125,000 or less in earned income. See #2 on negatives

1. Relaunch of the torturous interpretation of the “gainful employment” regulations making it harder for the “for‐profit” & other higher education institutions to maintain Title IV funding eligibility

2. “Free public college education” is estimated to cause a 12% drop in private college enrollment*

This is also a negative for states where this is implemented because under the plan, states will be required to pick up 25% of the cost when they are already strapped for resources & are making or have already dropped funding levels for their public universities

3. While the Borrower Defense rules may assist students, it will make it harder on for‐profit colleges to defend themselves against student lawsuits

*https://www.cnbc.com/2021/01/18/biden‐administration‐free‐college.html

Possible Impact of New U.S. Presidential Administration & Congressional Majority

Three predictions regarding a “free college” program

1. Projecting student enrollment in higher education would increase 4% to 8% overall, with a marked shift of students from private colleges to public institutions

2. Enrollment at private colleges would decrease 7% to 14%

3. Enrollment at public institutions would increase 6% to 14%

The Dollars and Sense of Free College, Georgetown University Center for Education and the Workforce, October 2020 https://1gyhoq479ufd3yna29x7ubjn‐wpengine.netdna‐ssl.com/wp‐content/uploads/CEW‐The‐Cost‐of‐Free‐College‐FR.pdf

7

8

3/10/2021

5

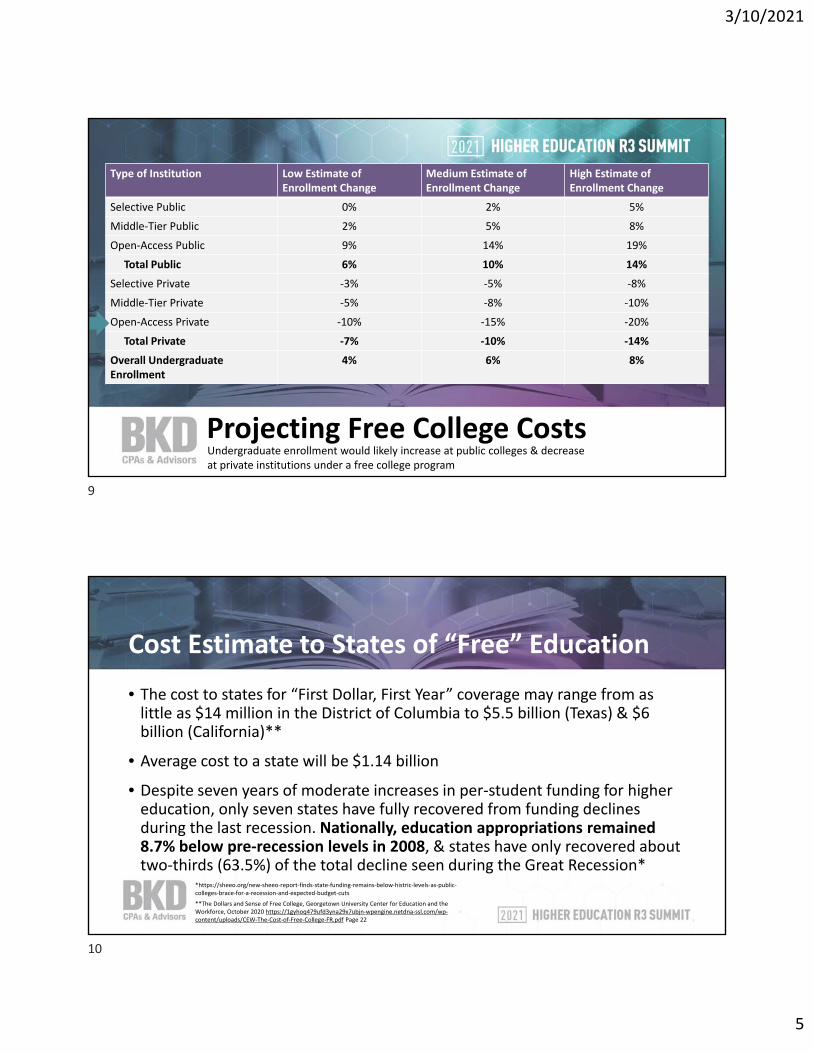

Projecting Free College Costs

Type of Institution Low Estimate of Enrollment Change

Medium Estimate of Enrollment Change

High Estimate of Enrollment Change

Selective Public 0% 2% 5%

Middle‐Tier Public 2% 5% 8%

Open‐Access Public 9% 14% 19%

Total Public 6% 10% 14%

Selective Private ‐3% ‐5% ‐8%

Middle‐Tier Private ‐5% ‐8% ‐10%

Open‐Access Private ‐10% ‐15% ‐20%

Total Private ‐7% ‐10% ‐14%

Overall Undergraduate Enrollment

4% 6% 8%

Projecting Free College CostsUndergraduate enrollment would likely increase at public colleges & decrease at private institutions under a free college program

Cost Estimate to States of “Free” Education

• The cost to states for “First Dollar, First Year” coverage may range from as little as $14 million in the District of Columbia to $5.5 billion (Texas) & $6 billion (California)**

• Average cost to a state will be $1.14 billion• Despite seven years of moderate increases in per‐student funding for higher education, only seven states have fully recovered from funding declines during the last recession. Nationally, education appropriations remained 8.7% below pre‐recession levels in 2008, & states have only recovered about two‐thirds (63.5%) of the total decline seen during the Great Recession*

*https://sheeo.org/new‐sheeo‐report‐finds‐state‐funding‐remains‐below‐histric‐levels‐as‐public‐colleges‐brace‐for‐a‐recession‐and‐expected‐budget‐cuts

**The Dollars and Sense of Free College, Georgetown University Center for Education and the Workforce, October 2020 https://1gyhoq479ufd3yna29x7ubjn‐wpengine.netdna‐ssl.com/wp‐content/uploads/CEW‐The‐Cost‐of‐Free‐College‐FR.pdf Page 22

9

10

3/10/2021

6

Cost Estimate to States of “Free” Education

$‐

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

$5,000

$5,500

$6,000

$6,500

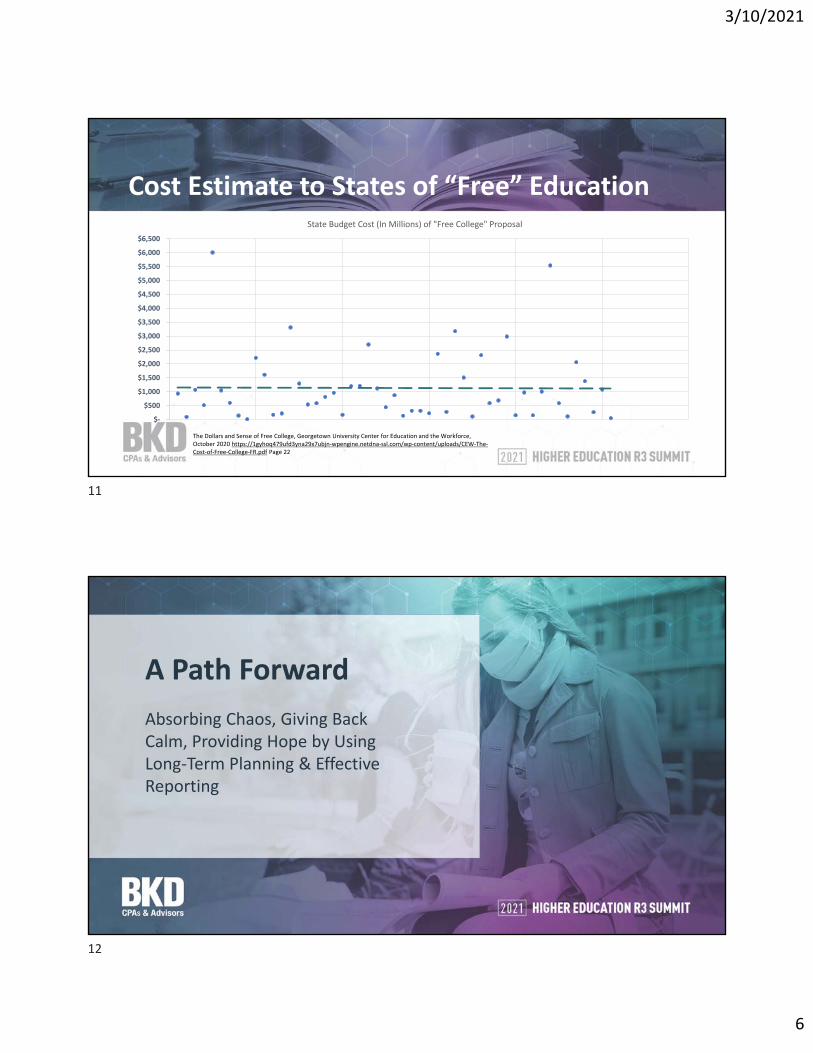

State Budget Cost (In Millions) of "Free College" Proposal

The Dollars and Sense of Free College, Georgetown University Center for Education and the Workforce, October 2020 https://1gyhoq479ufd3yna29x7ubjn‐wpengine.netdna‐ssl.com/wp‐content/uploads/CEW‐The‐Cost‐of‐Free‐College‐FR.pdf Page 22

A Path Forward

Absorbing Chaos, Giving Back Calm, Providing Hope by Using Long‐Term Planning & Effective Reporting

11

12

3/10/2021

7

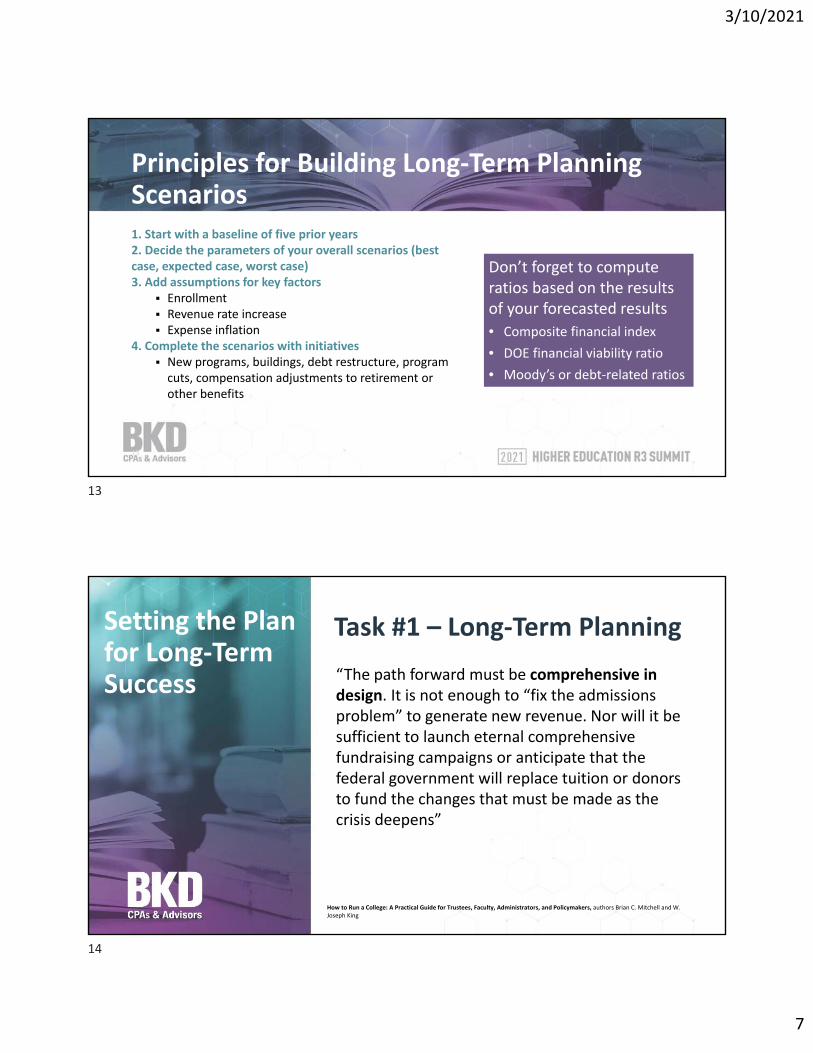

Principles for Building Long‐Term Planning Scenarios1. Start with a baseline of five prior years2. Decide the parameters of your overall scenarios (best case, expected case, worst case)3. Add assumptions for key factors

Enrollment Revenue rate increase Expense inflation

4. Complete the scenarios with initiatives New programs, buildings, debt restructure, program cuts, compensation adjustments to retirement or other benefits

13

Don’t forget to compute ratios based on the results of your forecasted results

• Composite financial index

• DOE financial viability ratio

• Moody’s or debt‐related ratios

Setting the plan for long term success“The path forward must be comprehensive in design. It is not enough to “fix the admissions problem” to generate new revenue. Nor will it be sufficient to launch eternal comprehensive fundraising campaigns or anticipate that the federal government will replace tuition or donors to fund the changes that must be made as the crisis deepens”

How to Run a College: A Practical Guide for Trustees, Faculty, Administrators, and Policymakers, authors Brian C. Mitchell and W. Joseph King

Setting the Plan for Long‐Term Success

Task #1 – Long‐Term Planning

13

14

3/10/2021

8

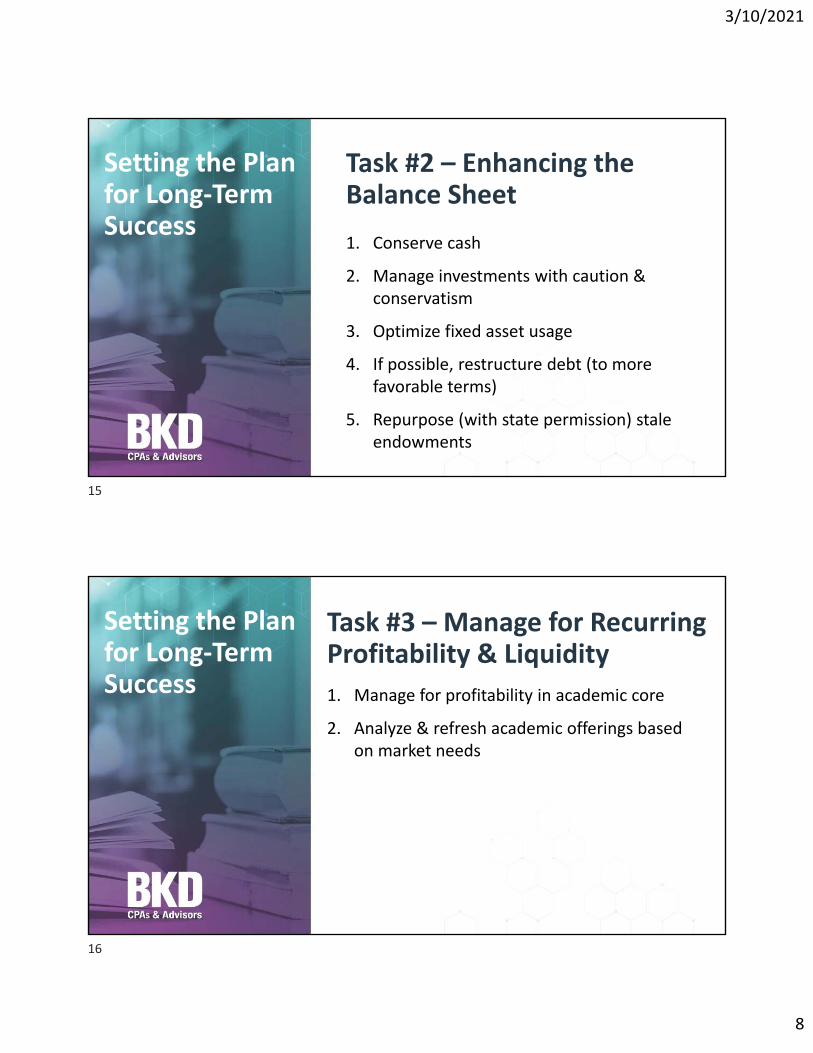

Task #2 – Enhancing the Balance Sheet

1. Conserve cash

2. Manage investments with caution & conservatism

3. Optimize fixed asset usage

4. If possible, restructure debt (to more favorable terms)

5. Repurpose (with state permission) stale endowments

Setting the Plan for Long‐Term Success

Task #3 – Manage for Recurring Profitability & Liquidity

1. Manage for profitability in academic core

2. Analyze & refresh academic offerings based on market needs

Setting the Plan for Long‐Term Success

15

16

3/10/2021

9

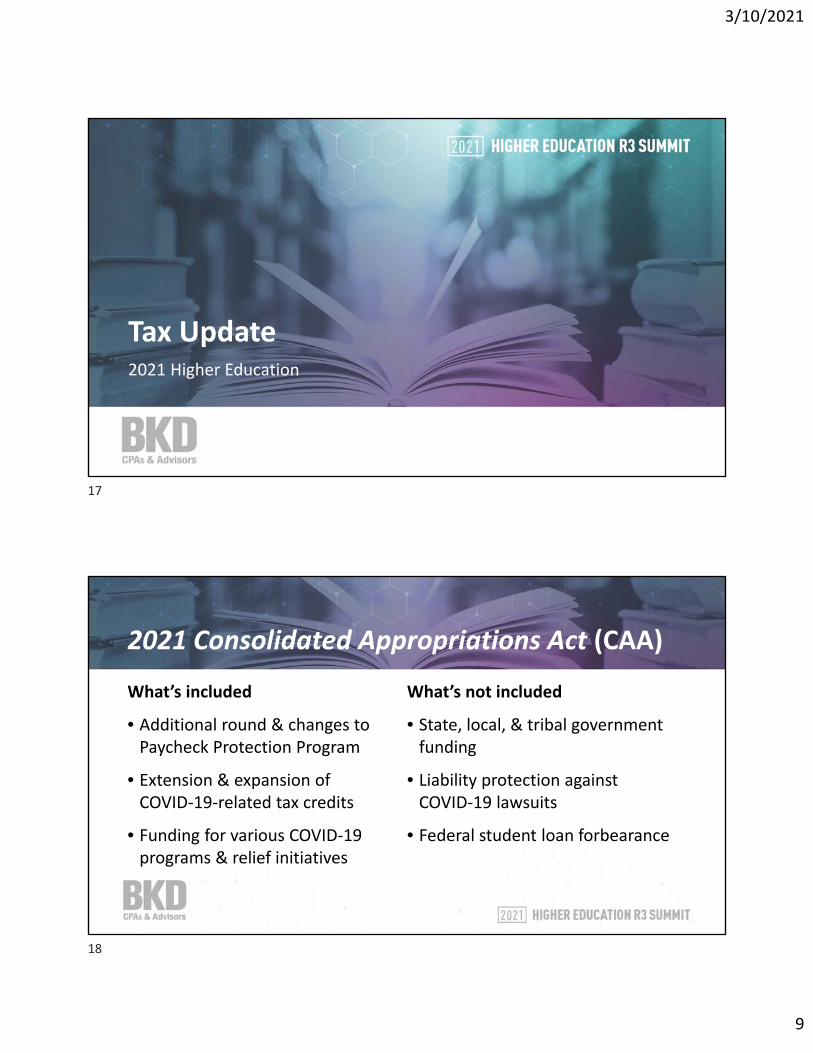

Tax Update2021 Higher Education

2021 Consolidated Appropriations Act (CAA)

What’s included

• Additional round & changes to Paycheck Protection Program

• Extension & expansion of COVID‐19‐related tax credits

• Funding for various COVID‐19 programs & relief initiatives

What’s not included

• State, local, & tribal government funding

• Liability protection against COVID‐19 lawsuits

• Federal student loan forbearance

17

18

3/10/2021

10

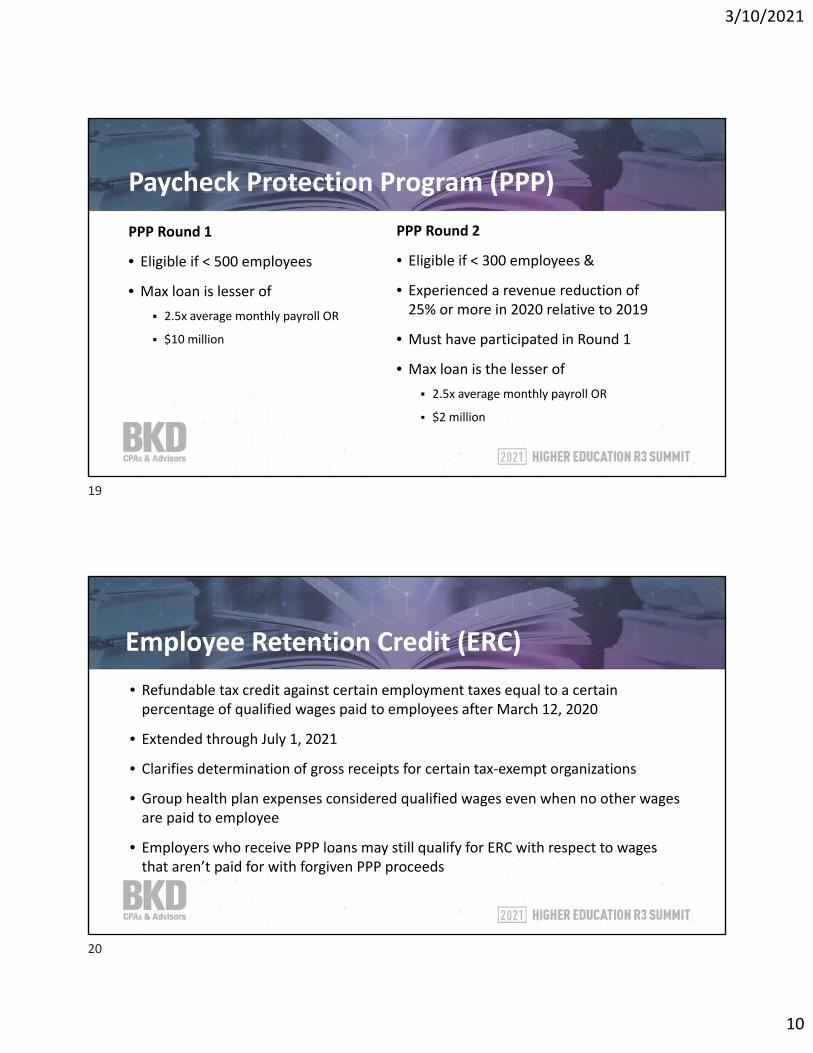

Paycheck Protection Program (PPP)

PPP Round 1

• Eligible if < 500 employees

• Max loan is lesser of

2.5x average monthly payroll OR

$10 million

PPP Round 2

• Eligible if < 300 employees &

• Experienced a revenue reduction of 25% or more in 2020 relative to 2019

• Must have participated in Round 1

• Max loan is the lesser of

2.5x average monthly payroll OR

$2 million

Employee Retention Credit (ERC)

• Refundable tax credit against certain employment taxes equal to a certain percentage of qualified wages paid to employees after March 12, 2020

• Extended through July 1, 2021

• Clarifies determination of gross receipts for certain tax‐exempt organizations

• Group health plan expenses considered qualified wages even when no other wages are paid to employee

• Employers who receive PPP loans may still qualify for ERC with respect to wages that aren’t paid for with forgiven PPP proceeds

19

20

3/10/2021

11

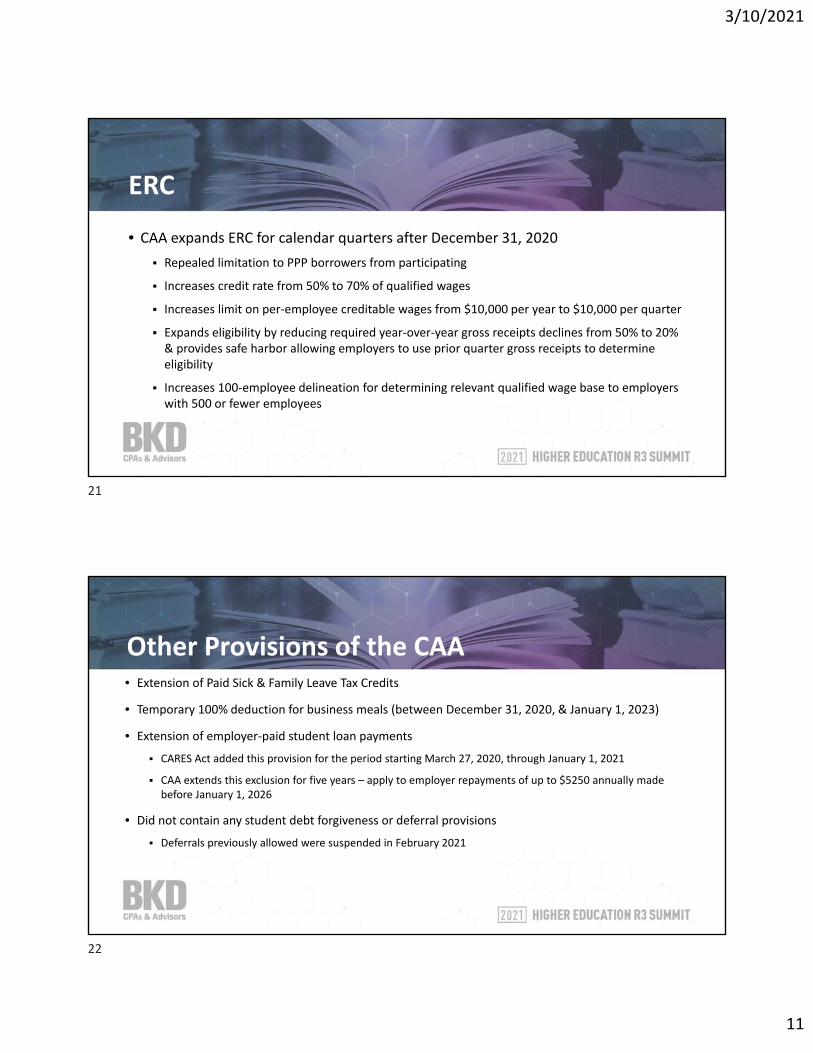

ERC

• CAA expands ERC for calendar quarters after December 31, 2020

Repealed limitation to PPP borrowers from participating

Increases credit rate from 50% to 70% of qualified wages

Increases limit on per‐employee creditable wages from $10,000 per year to $10,000 per quarter

Expands eligibility by reducing required year‐over‐year gross receipts declines from 50% to 20% & provides safe harbor allowing employers to use prior quarter gross receipts to determine eligibility

Increases 100‐employee delineation for determining relevant qualified wage base to employers with 500 or fewer employees

Other Provisions of the CAA• Extension of Paid Sick & Family Leave Tax Credits

• Temporary 100% deduction for business meals (between December 31, 2020, & January 1, 2023)

• Extension of employer‐paid student loan payments

CARES Act added this provision for the period starting March 27, 2020, through January 1, 2021

CAA extends this exclusion for five years – apply to employer repayments of up to $5250 annually made before January 1, 2026

• Did not contain any student debt forgiveness or deferral provisions

Deferrals previously allowed were suspended in February 2021

21

22

3/10/2021

12

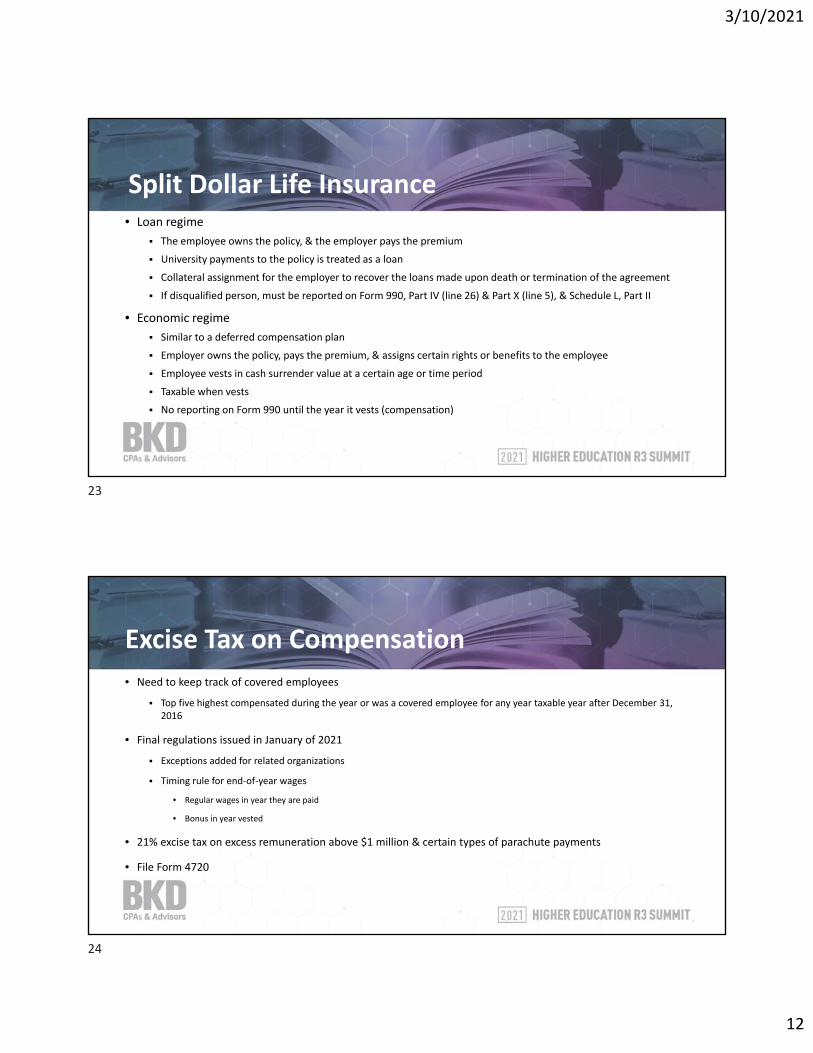

Split Dollar Life Insurance• Loan regime

The employee owns the policy, & the employer pays the premium

University payments to the policy is treated as a loan

Collateral assignment for the employer to recover the loans made upon death or termination of the agreement

If disqualified person, must be reported on Form 990, Part IV (line 26) & Part X (line 5), & Schedule L, Part II

• Economic regime

Similar to a deferred compensation plan

Employer owns the policy, pays the premium, & assigns certain rights or benefits to the employee

Employee vests in cash surrender value at a certain age or time period

Taxable when vests

No reporting on Form 990 until the year it vests (compensation)

Excise Tax on Compensation

• Need to keep track of covered employees

Top five highest compensated during the year or was a covered employee for any year taxable year after December 31, 2016

• Final regulations issued in January of 2021

Exceptions added for related organizations

Timing rule for end‐of‐year wages

• Regular wages in year they are paid

• Bonus in year vested

• 21% excise tax on excess remuneration above $1 million & certain types of parachute payments

• File Form 4720

23

24

3/10/2021

13

Sunsetting Academic ProgramsWhy, When, & How?

Why sunset academic programs?

When to sunset a program

How do we move forward?

25

26

3/10/2021

14

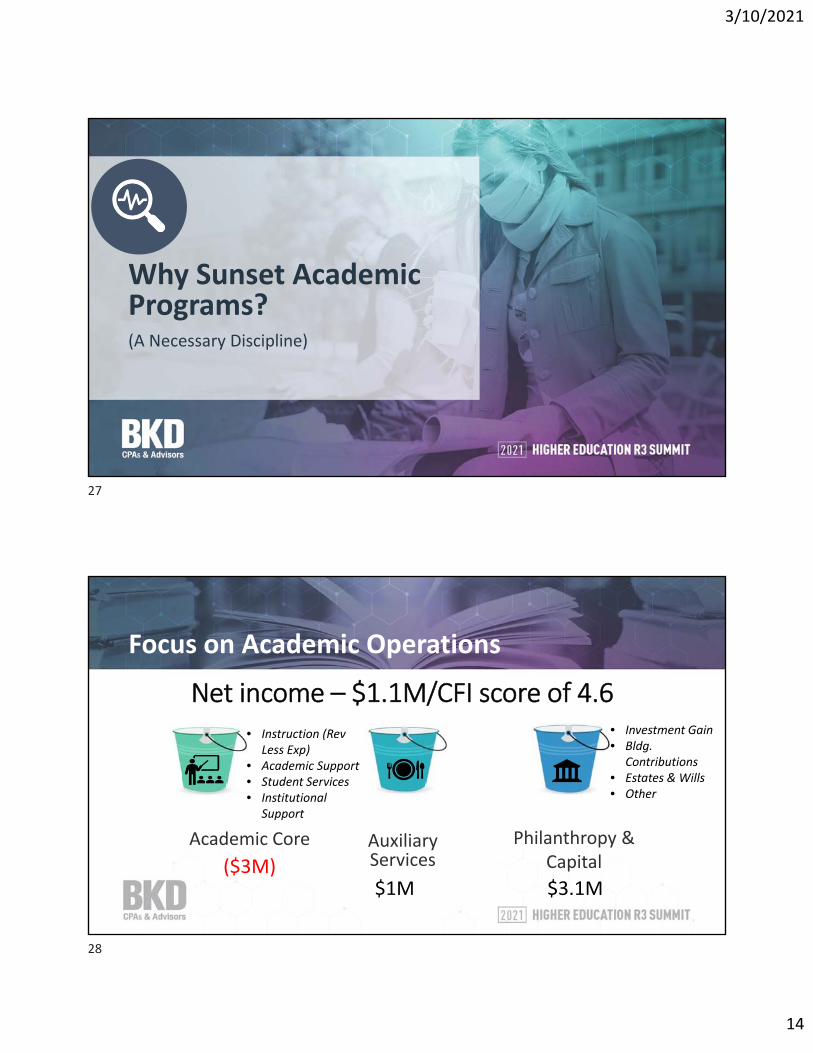

Why Sunset Academic Programs?(A Necessary Discipline)

Focus on Academic Operations

Net income – $1.1M/CFI score of 4.6

Academic Core Auxiliary Services

Philanthropy & Capital($3M)

$1M $3.1M

• Investment Gain• Bldg.

Contributions• Estates & Wills• Other

• Instruction (Rev Less Exp)

• Academic Support• Student Services• Institutional

Support

27

28

3/10/2021

15

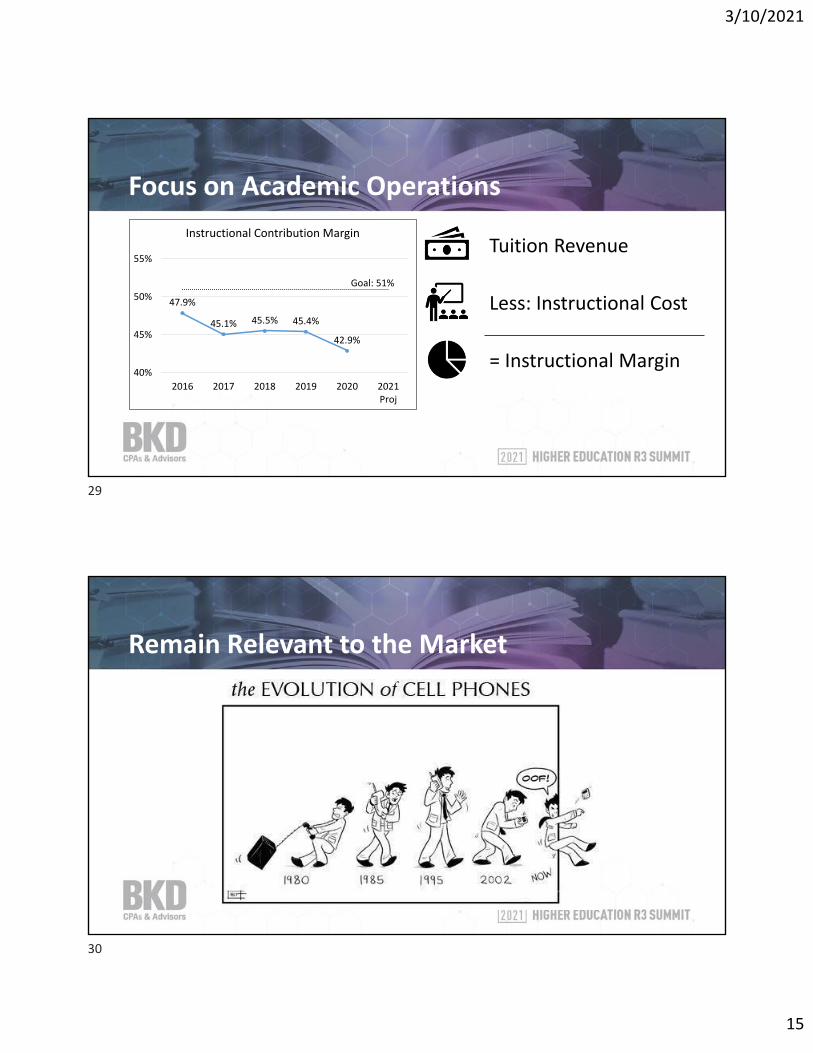

Focus on Academic Operations

47.9%

45.1% 45.5% 45.4%

42.9%

40%

45%

50%

55%

2016 2017 2018 2019 2020 2021Proj

Instructional Contribution Margin

Goal: 51%

Tuition Revenue

Less: Instructional Cost

= Instructional Margin

Remain Relevant to the Market

29

30

3/10/2021

16

Remain Relevant to the Market

• Higher education has changed Traditionally: University was viewed to produce good citizens

Shifting V=view: “A careerist assumption has taken over”

“… it is a primarily economic decision that needs to deliver returns”

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$700,000$710,000$720,000$730,000$740,000$750,000$760,000$770,000

Net Present Value & Median Debt

Impact of COVID on Higher Education

Moody’s Investors Service: Issued a negative outlook• Operating revenue decline by 5% to 10%

60% of public 75% of private

• High fixed costs

S&P Global Ratings: Maintaining a negative outlook• Fourth straight year• Short‐term challenges related to COVID‐19

Enrollment & operating margin struggle even before COVID

• Weak demand & weak financials mean less operating flexibility

31

32

3/10/2021

17

Changing Demographics

• Enrollment changes are leading to tough decisions

• 6.6 million loss of future 18‐year‐olds

• Enrollment pressure remains for the long run

Limited Resources

33

34

3/10/2021

18

Limited Resources

• Not all programs in the academic portfolio are helping the institution move forward

• Some programs are high producers & others may be slowing the institution down by ‘draining resources’ through a poor ROI

When to Sunset a Program(Making a Data‐Informed Decision)

35

36

3/10/2021

19

A Difficult Decision

Programs are important to the faculty who teach them, the students enrolled in them, the graduates who began careers & lives, & institutional stakeholders

A data‐informed process is critical – without it, indiscriminate closure/defunding violates institutional norms & can trigger protests & problems

37

38

3/10/2021

20

How Do You Know When It Is Time?

• Low attendance

• Low retention

• Low margins

• Poor evaluations

Is it a value problem or a marketing problem?

Gather Relevant Data

• Critical points to consider Enrollment trends

Market demand

Margin performance

Mission fit

39

40

3/10/2021

21

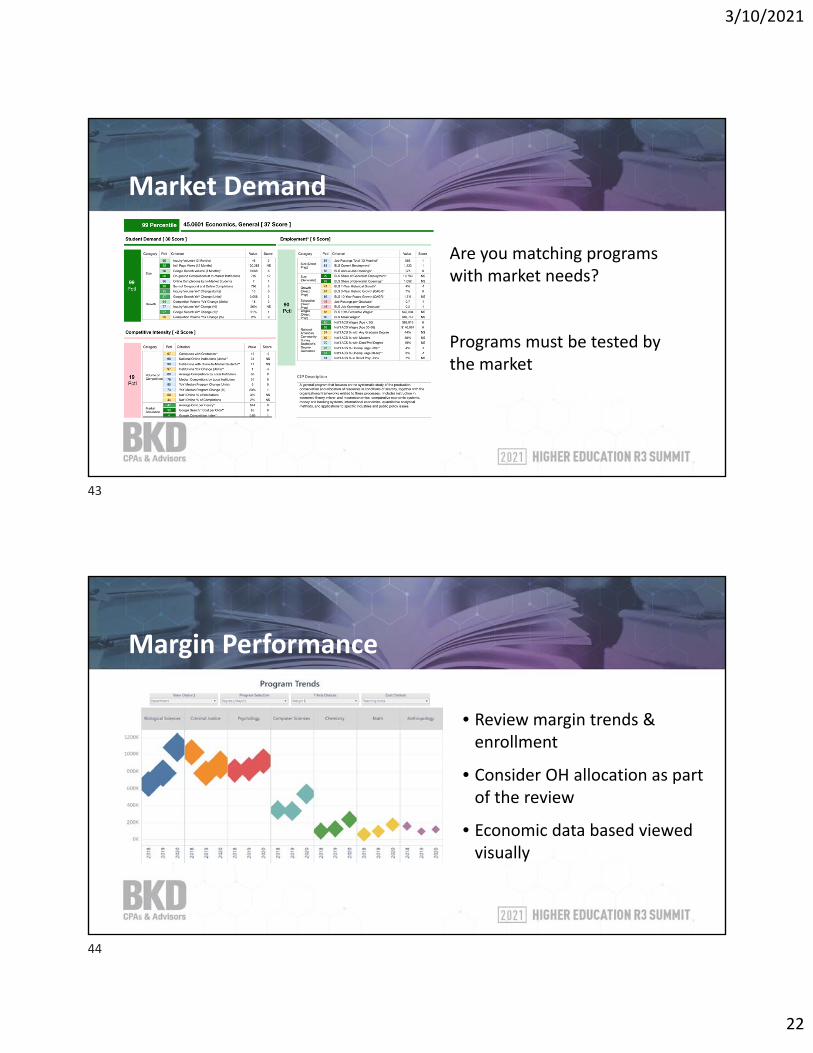

Enrollment Trends

• The customer has spoken …

After five years – two out of five* new programs had no graduates in 2018!

Just because faculty like it does not mean it is valued by the ‘customers’

Any program evaluation must include the enrollment management leader

*Burning Glass examined more than 10,500 new programs with first graduates in 2013 – half had fewer than five graduates in 2018

Enrollment Trends

Annual Enrollment Review by ProgramTarget FTE enrollment: __20__Actual FTE enrollment (5‐year average): __14__Change from previous: __0___Target degrees conferred: __5___Actual conferred (5‐year average): __4___Change from previous: _+1___Target student credit hours: _1000_Actual credit hours (5‐year average): __820_Change from previous: _‐135_

Missing targets• Enrollment•Graduates• Credit HoursBased on five‐year averages & trend data, this program should move through the next review phase process

41

42

3/10/2021

22

Market Demand

Are you matching programs with market needs?

Programs must be tested by the market

Margin Performance

• Review margin trends & enrollment

• Consider OH allocation as part of the review

• Economic data based viewed visually

43

44

3/10/2021

23

Margin Performance

Benchmarking economic performance by program helps identify possible issues

‐20%

‐10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Program Margin Benchmarking

University Peer Average

Mission Fit

• Everything funded by the university must supports its mission

• Mission is an “institutional value proposition”

• Develop a rubric to measure mission & evaluate academic programs

45

46

3/10/2021

24

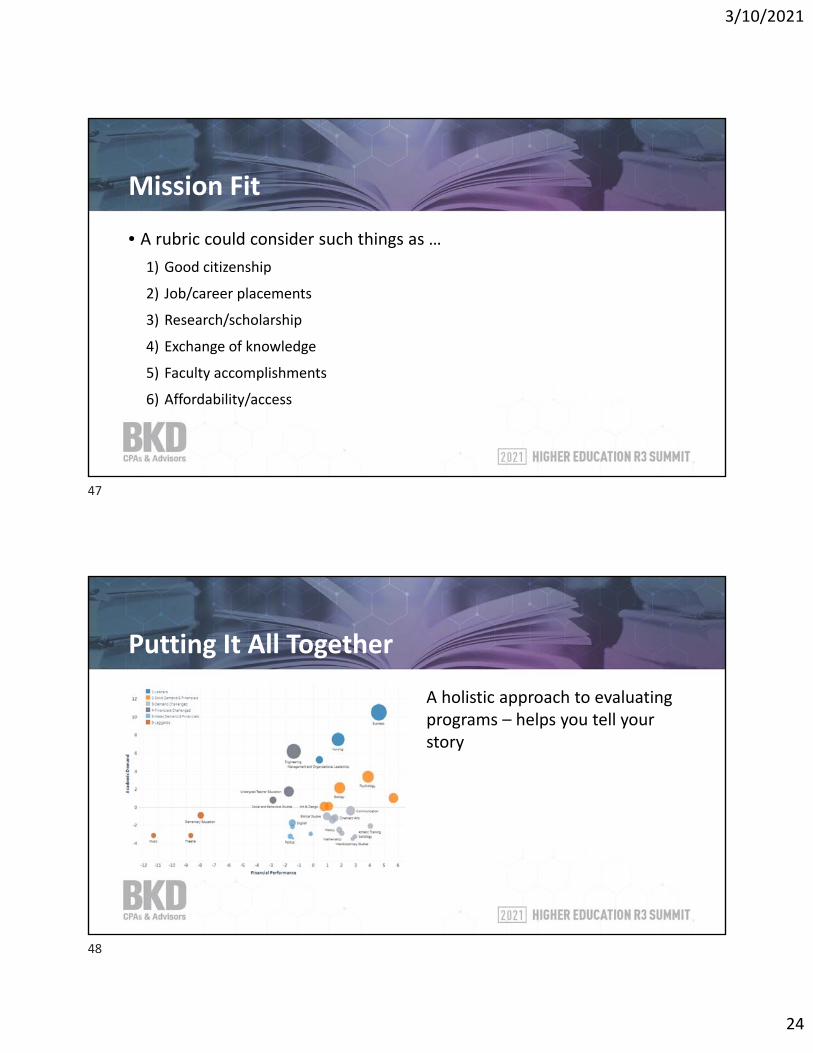

Mission Fit

• A rubric could consider such things as …1) Good citizenship

2) Job/career placements

3) Research/scholarship

4) Exchange of knowledge

5) Faculty accomplishments

6) Affordability/access

Putting It All Together

A holistic approach to evaluating programs – helps you tell your story

47

48

3/10/2021

25

How Do We Move Forward?(Process & Communication)

Review Process

• Establish a review process cycle (if not already in the faculty handbook)• Review process should consider

Value to students (enrollment trends)

Value to market (workplace needs/prospective students)

Margin (revenue less expense)• Remember: Nonprofit is a tax status, not a strategy

• Margin supports critical initiatives to further the institution

Alignment with mission• Are current resources taking away from strategic goals & mission?

49

50

3/10/2021

26

Transparency

• An open & data‐informed process

• A rushed process leads to lack of transparency Most examples of sunset processes that gain traction in the media occurred too quickly

Key stakeholders do not feel heard or included in the process

• Cross‐discipline working group (faculty & employees) The deans are in the best position to lead their program faculty through this process & submit recommendations

• Follow established academic policies

• Avoid surprises

Recent Examples

Guilford College – 1,600 students/budget $45M 15 programs, 27 faculty, & 8 additional staff (reduced 47 in spring)

University of Vermont, College of Arts & Sciences – 4,500 students 12 majors & 11 minors

• Geology, German, Greek, Asian Studies, Religion, Classical Civilization

College of St. Rose – 3,800 students/budget $71M 16 bachelor majors & 6 master’s degrees, 41 faculty

• Art (4), Music (3) Math (2), Science/Tech (5), Business (2)

Adrian College – 1,730 students/budget $48M 4 programs & 22 teaching positions

• History, Theater, Religion/Philosophy, & Leadership

51

52

3/10/2021

27

Recent Examples

University of Evansville – 2,300 students/budget $73M 17 majors, 3 departments & 35 faculty

• Philosophy, Religion, Music, Electrical Engineering, & Computer Science

Concordia University (Chicago) – 6,500 students/budget $74M 15 programs & 51 faculty & staff

• Graphic Arts, Theater, Chemistry, Women’s & Gender Studies, & Business Communications

Hardin Simmons – 2,200 students/budget $53M 35 programs & 47 teaching positions & 14 staff

• Environmental Science (1), Geology (13), Medical Illustration (0), Philosophy (5), Physics (3), Political Science (23), Sociology (3), Spanish (8), & Bachelor of Music in Performance (6)

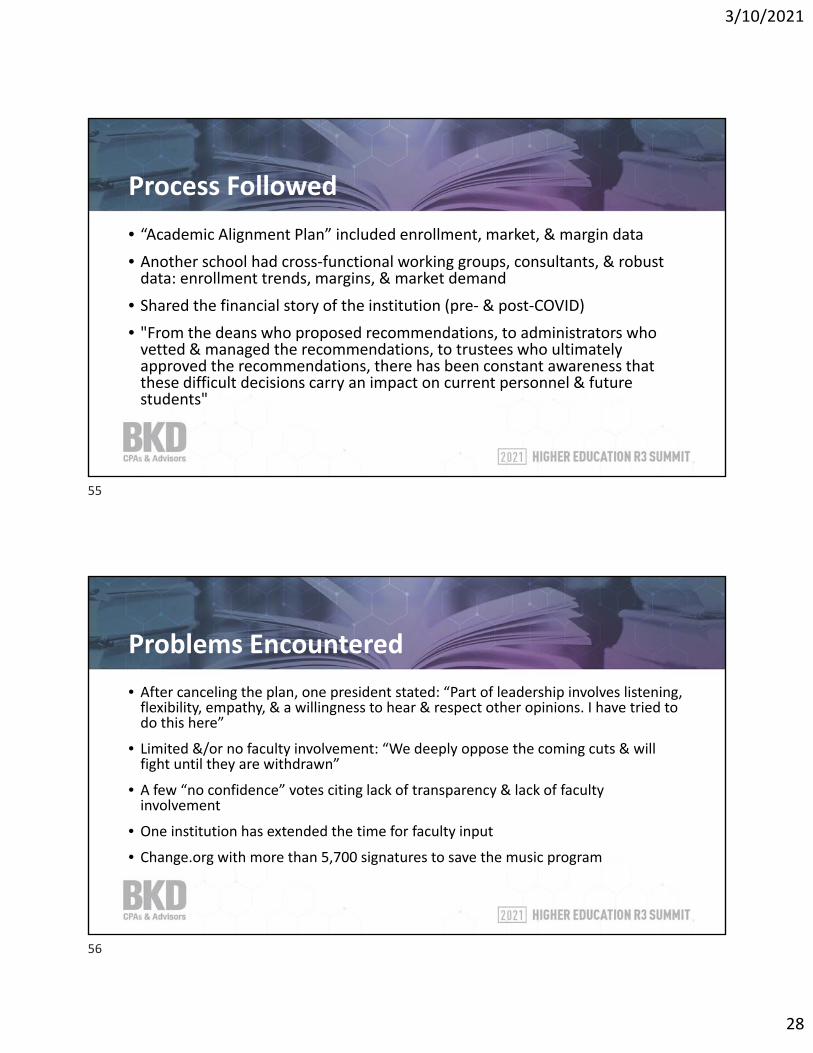

Process Followed

Reasons Cited “We need to build a stronger base – one where operating expenses & revenue align”

Duration of Program Review Two months, several months, & up to two years

Tenure – a few institutions suspended tenure due to COVIDPersonnel Involved

Cross‐functional teams – reporting to dean – reporting to provost – reporting to president/board

Cabinet & board

Dean proposed without faculty or student input

Administration working with a “representative committee” of faculty

53

54

3/10/2021

28

Process Followed

• “Academic Alignment Plan” included enrollment, market, & margin data

• Another school had cross‐functional working groups, consultants, & robust data: enrollment trends, margins, & market demand

• Shared the financial story of the institution (pre‐ & post‐COVID)• "From the deans who proposed recommendations, to administrators who vetted & managed the recommendations, to trustees who ultimately approved the recommendations, there has been constant awareness that these difficult decisions carry an impact on current personnel & future students"

Problems Encountered

• After canceling the plan, one president stated: “Part of leadership involves listening, flexibility, empathy, & a willingness to hear & respect other opinions. I have tried to do this here”

• Limited &/or no faculty involvement: “We deeply oppose the coming cuts & will fight until they are withdrawn”

• A few “no confidence” votes citing lack of transparency & lack of faculty involvement

• One institution has extended the time for faculty input

• Change.org with more than 5,700 signatures to save the music program

55

56

3/10/2021

29

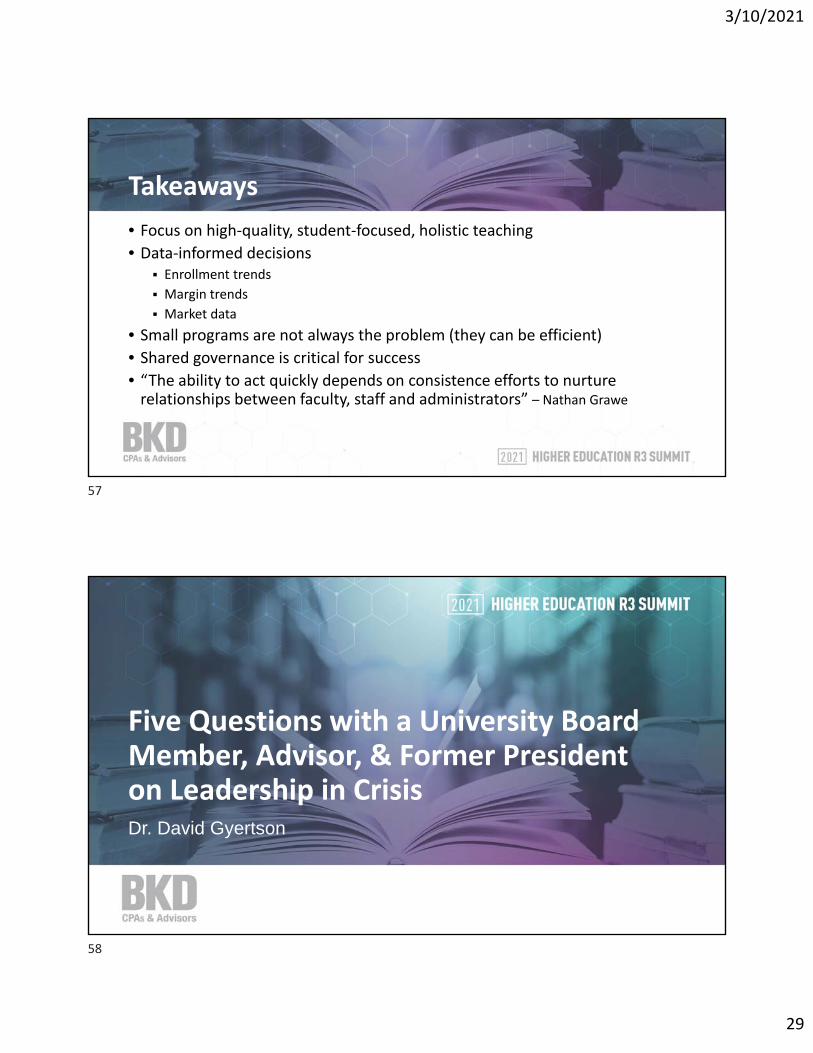

Takeaways

• Focus on high‐quality, student‐focused, holistic teaching• Data‐informed decisions

Enrollment trends

Margin trends

Market data

• Small programs are not always the problem (they can be efficient)

• Shared governance is critical for success• “The ability to act quickly depends on consistence efforts to nurture relationships between faculty, staff and administrators” – Nathan Grawe

Five Questions with a University Board Member, Advisor, & Former President on Leadership in CrisisDr. David Gyertson

57

58

3/10/2021

30

Managing Fraud & Technology in a Remote World

Agenda

• Increase in Fraud Risk – COVID‐19

• COVID‐19 Benchmarking Report

• Higher Education Fraud

• Technology Tips

59

60

3/10/2021

31

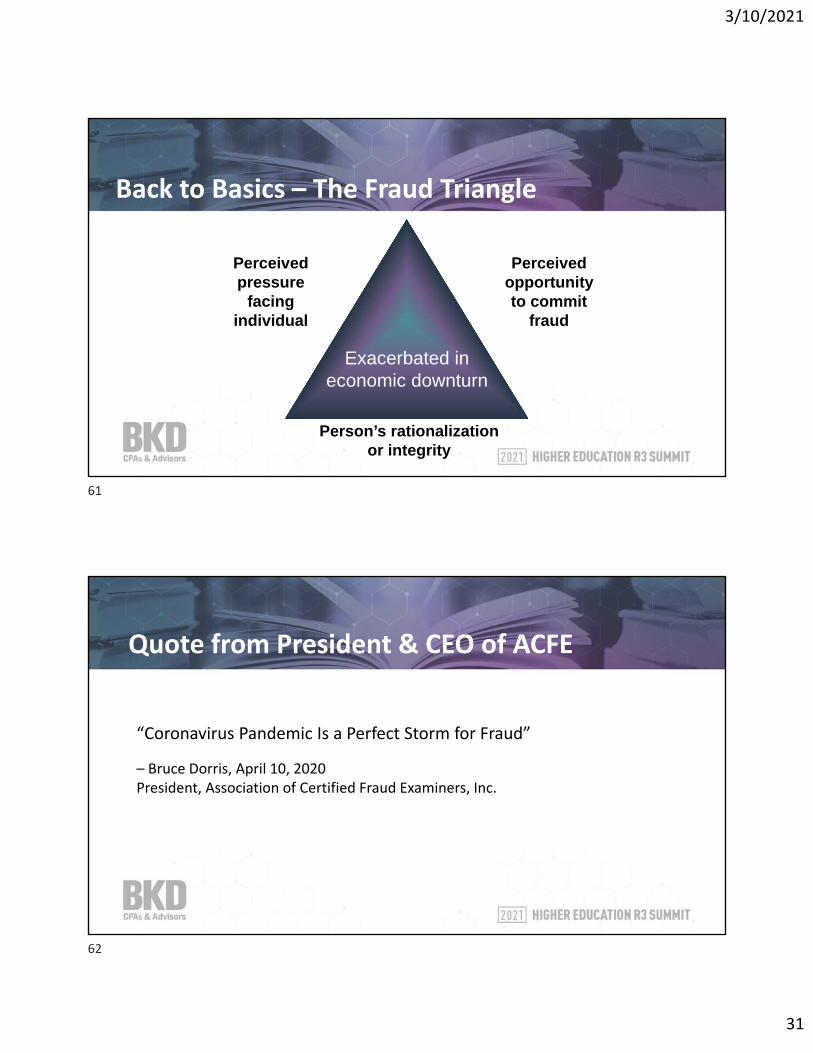

Back to Basics – The Fraud Triangle

Exacerbated ineconomic downturn

Perceived pressure

facing individual

Perceived opportunity to commit

fraud

Person’s rationalization or integrity

Quote from President & CEO of ACFE

“Coronavirus Pandemic Is a Perfect Storm for Fraud”

– Bruce Dorris, April 10, 2020President, Association of Certified Fraud Examiners, Inc.

61

62

3/10/2021

32

©2020 Association of Certified Fraud Examiners, Inc.

©2020 Association of Certified Fraud Examiners, Inc.

63

64

3/10/2021

33

©2020 Association of Certified Fraud Examiners, Inc.

©2020 Association of Certified Fraud Examiners, Inc.

65

66

3/10/2021

34

Why Do Employees Steal?

• Legitimate financial need is rare anymore

• Other basic reasons employees steal

Low morale

Feel employer has mistreated or “wronged” them

Feel underpaid &/or under appreciated

Consequences of theft are minimal

Lack of preventive measures

Profile of a Fraudster

• No prior criminal history

• Well liked by co‐workers

• Likes to give gifts/compulsive shopper

• Gambling problems not unusual

• Long‐term employee

• Rationalizes, starts small, or “borrows”

• Lifestyle clues©2020 Association of Certified Fraud Examiners, Inc.

67

68

3/10/2021

35

Who Looks Suspicious?

Petty Cash Fraud: $116,000

• Tyler Liddle, a former Idaho State University employee charged with embezzlement, used fake invoices & receipts to steal $116,000 from the university over a period of about four years, according to police reports

• During an internal audit, investigators reviewed student petty cash reimbursement forms, receipts, invoices, & correspondence from the student clubs & determined that the misappropriation of funds was carried out through a series of fake invoices & payments made to fictitious students, vendors, & inactive student groups

• Auditors were unable to find supporting documentation for 401 petty cash reimbursements & 199 of those were deemed fraudulent. The investigation also uncovered reimbursement for Costco receipts containing Liddle’s membership number but allegedly paid to other individuals. Templates used to create fake invoices & receipts were also found on Liddle’s work computer

69

70

3/10/2021

36

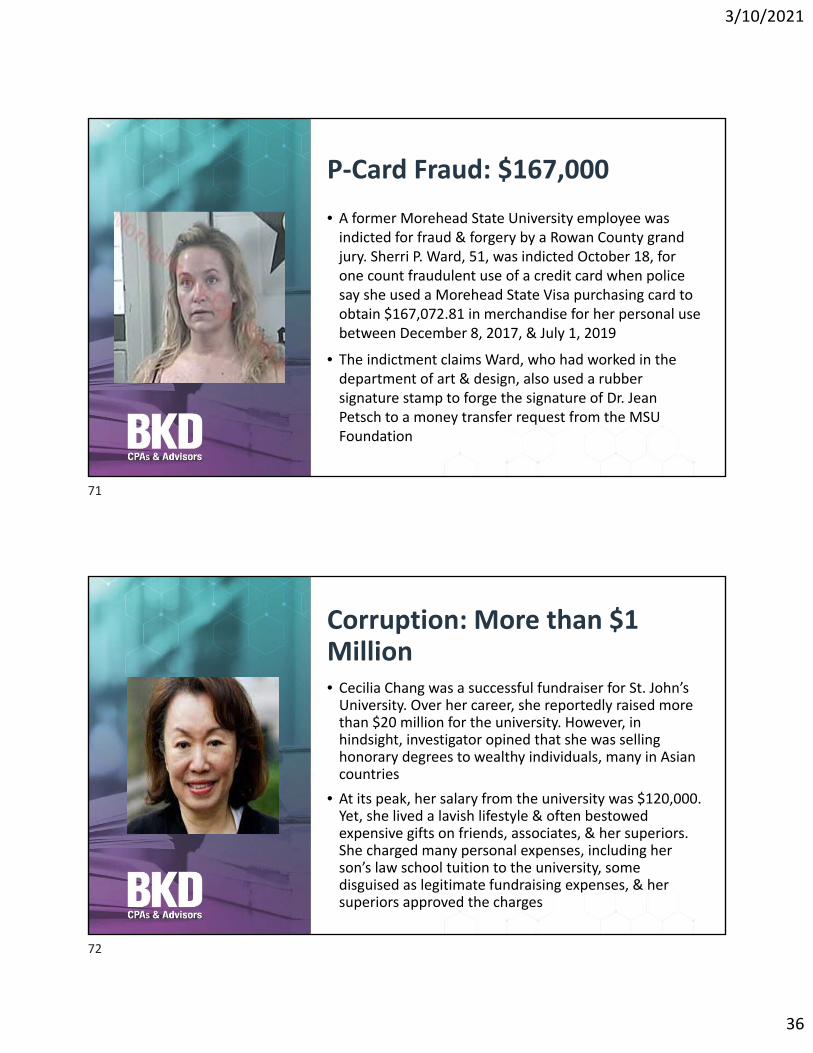

P‐Card Fraud: $167,000

• A former Morehead State University employee was indicted for fraud & forgery by a Rowan County grand jury. Sherri P. Ward, 51, was indicted October 18, for one count fraudulent use of a credit card when police say she used a Morehead State Visa purchasing card to obtain $167,072.81 in merchandise for her personal use between December 8, 2017, & July 1, 2019

• The indictment claims Ward, who had worked in the department of art & design, also used a rubber signature stamp to forge the signature of Dr. Jean Petsch to a money transfer request from the MSU Foundation

Corruption: More than $1 Million• Cecilia Chang was a successful fundraiser for St. John’s University. Over her career, she reportedly raised more than $20 million for the university. However, in hindsight, investigator opined that she was selling honorary degrees to wealthy individuals, many in Asian countries

• At its peak, her salary from the university was $120,000. Yet, she lived a lavish lifestyle & often bestowed expensive gifts on friends, associates, & her superiors. She charged many personal expenses, including her son’s law school tuition to the university, some disguised as legitimate fundraising expenses, & her superiors approved the charges

71

72

3/10/2021

37

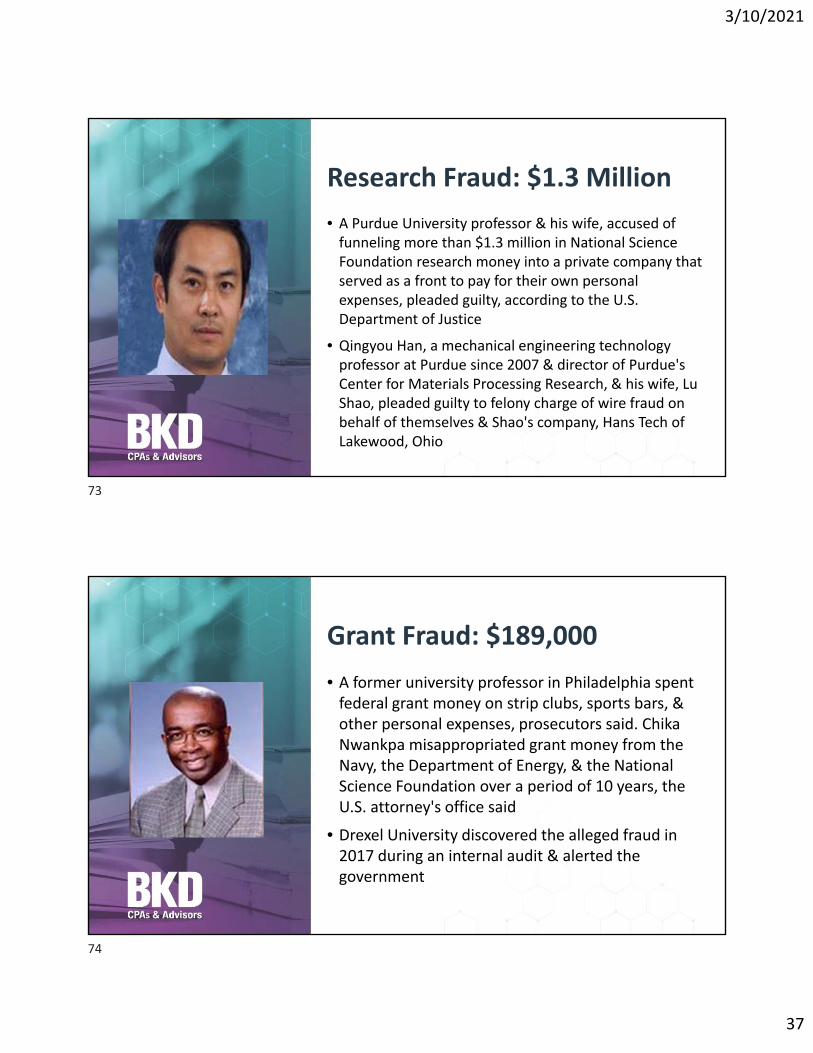

• A Purdue University professor & his wife, accused of funneling more than $1.3 million in National Science Foundation research money into a private company that served as a front to pay for their own personal expenses, pleaded guilty, according to the U.S. Department of Justice

• Qingyou Han, a mechanical engineering technology professor at Purdue since 2007 & director of Purdue's Center for Materials Processing Research, & his wife, Lu Shao, pleaded guilty to felony charge of wire fraud on behalf of themselves & Shao's company, Hans Tech of Lakewood, Ohio

Research Fraud: $1.3 Million

• A former university professor in Philadelphia spent federal grant money on strip clubs, sports bars, & other personal expenses, prosecutors said. Chika Nwankpa misappropriated grant money from the Navy, the Department of Energy, & the National Science Foundation over a period of 10 years, the U.S. attorney's office said

• Drexel University discovered the alleged fraud in 2017 during an internal audit & alerted the government

Grant Fraud: $189,000

73

74

3/10/2021

38

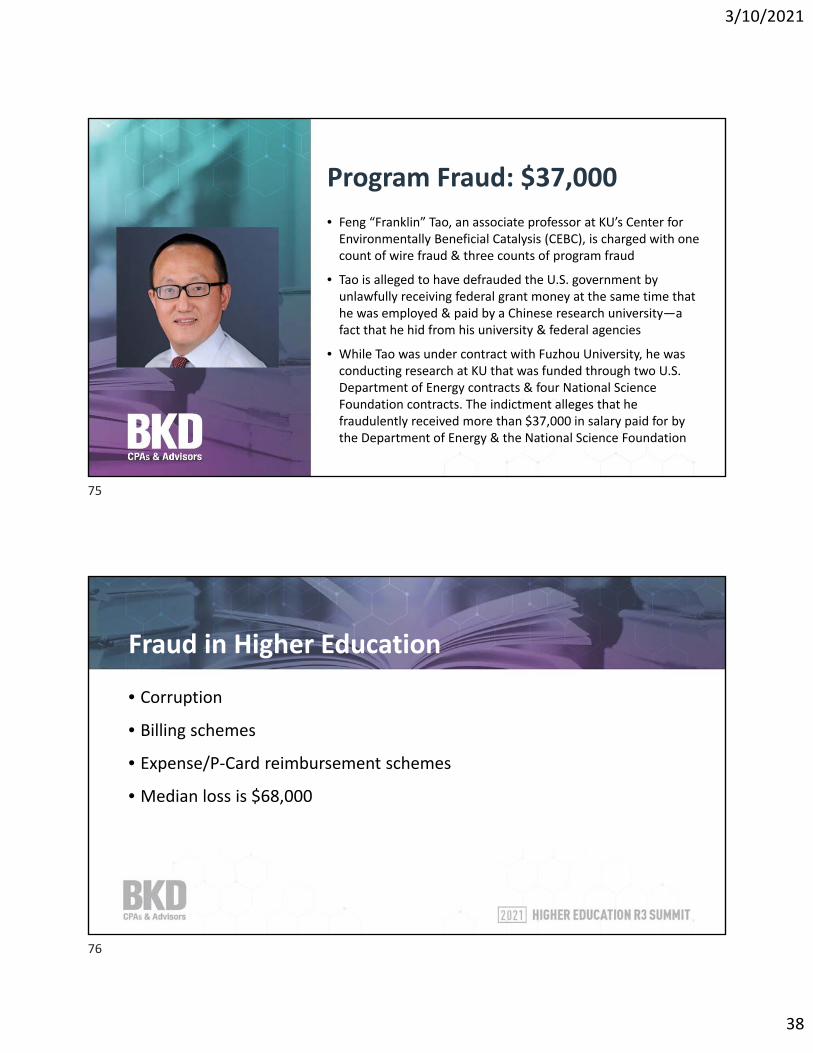

Program Fraud: $37,000

• Feng “Franklin” Tao, an associate professor at KU’s Center for Environmentally Beneficial Catalysis (CEBC), is charged with one count of wire fraud & three counts of program fraud

• Tao is alleged to have defrauded the U.S. government by unlawfully receiving federal grant money at the same time that he was employed & paid by a Chinese research university—a fact that he hid from his university & federal agencies

• While Tao was under contract with Fuzhou University, he was conducting research at KU that was funded through two U.S. Department of Energy contracts & four National Science Foundation contracts. The indictment alleges that he fraudulently received more than $37,000 in salary paid for by the Department of Energy & the National Science Foundation

Fraud in Higher Education

• Corruption

• Billing schemes

• Expense/P‐Card reimbursement schemes

• Median loss is $68,000

75

76

3/10/2021

39

Using Technology to Enhance System Security

• Track data changes – use change tracking in your data to know when data is being changes, who’s changing it, & what changes are being made

• Utilize approval workflows – ensure that records are being created based on approvals

• Utilize the principle of least privilege – don’t give users the keys to the kingdom when they only need a single window to enter data

• Compare pre‐ & post‐changes – ensure data is not being changed after being entered

Using Technology to Mi gate Fraud

• Keep your application updated – newer applications are supported by the publishers & can include updates for compatibility with newer security technology

• Enforce complex passwords – ensure that users have passwords not easily breakable or guessed

• Enable multifactor authentication – utilize MFA to ensure the right users are logging into the system

• Segregation of duties – utilize security reports to ensure the system is set up to support segrega on of du es

77

78

3/10/2021

40

Using Technology to Mitigate Fraud • Clean up user accounts – review user accounts to remove unused logins

• Use single sign‐on – SSO reduces the number of accounts & minimizes the use of simple passwords because users have less accounts to manage

GASB & FASB Update Breakouts

79

80

3/10/2021

41

GASB Update

Agenda

• GASB timeline & COVID-related items

• Statements No. 91-97

• Upcoming projects

81

82

3/10/2021

42

GASB Timeline & Accounting for COVID‐Related Items

Statement No. 95Postponement of the Effective Dates of Certain Authoritative Guidance

83

84

3/10/2021

43

Statement No. 95

• Delayed the effective date of provisions of nine statements & five Implementation Guides

• Most were delayed for one year

• Leases (Statement No. 87) & related Implementation Guide 2019‐3 delayed for eighteen months

Statement No. 84

• Effective for reporting periods beginning after December 15, 2019

• Provides clarification of which activities are fiduciary in nature & how to report them

• Key principle: cannot be a fiduciary for own resources• Implementation guides provide examples of items not likely to be fiduciary activities & administrative involvement

85

86

3/10/2021

44

Statement No. 87

• Effective for fiscal years beginning after June 15, 2021

• Changes accounting for leases, both for lessees & lessors

• Gathering relevant contracts can pose challenges

• Time‐consuming process – don’t delay!

Technical Bulletin No. 2020‐1

Series of questions & answers regarding topics related to the CARES Act

Following items may be of particular interest to institutions of higher education

87

88

3/10/2021

45

If amendments to the CARES Act are enacted after year‐end, but prior to issuance of the financials, should effects of amendments be recognized in the financials?

No, those amendments would be considered a nonrecognized subsequent event (Statement No. 56, paragraphs 8‐12)Do not represent conditions that existed as of the period‐end being reported

Technical Bulletin No. 2020‐1

Should CARES Act resources provided through the following to BTA or enterprise fund be reported as nonoperating revenues

• Provider Relief Fund (US Dept. of HHS)• Higher Education Emergency Relief Fund (U.S. Dept. of Education)• CARES Act Airport Grants (FAA)• Formula Grants for Rural Areas & Urbanized Area Formula Grants programs (FTA)

Yes, except for U.S. Dept. of HHS Provider Relief Fund’s Uninsured Program, the resources are subsidies & should be reported as nonoperatingResources from the Uninsured Program are payment for services provided & should be reported as operating

Technical Bulletin No. 2020‐1

89

90

3/10/2021

46

Should outflows of resources incurred in response to the coronavirus (actions to slow the virus, adjustments in provision of services, implementation of stay‐at‐home orders) be reported as extraordinary or special items?

No type of event being considered is the appearance of a coronavirus diseaseNot infrequent, so not extraordinary itemNot within control of management, so not special item

Technical Bulletin No. 2020‐1

GASB Standards

91

92

3/10/2021

47

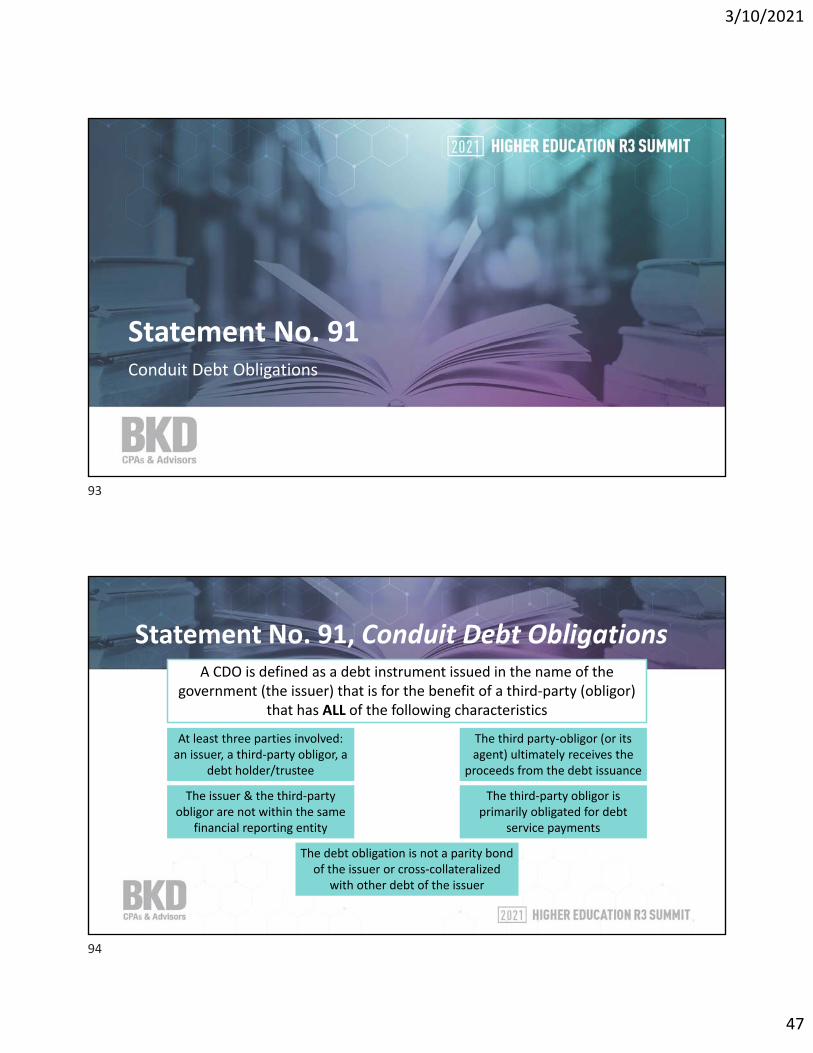

Statement No. 91Conduit Debt Obligations

Statement No. 91, Conduit Debt ObligationsA CDO is defined as a debt instrument issued in the name of the

government (the issuer) that is for the benefit of a third‐party (obligor) that has ALL of the following characteristics

At least three parties involved: an issuer, a third‐party obligor, a

debt holder/trustee

The issuer & the third‐party obligor are not within the same

financial reporting entity

The debt obligation is not a parity bond of the issuer or cross‐collateralized

with other debt of the issuer

The third party‐obligor (or its agent) ultimately receives the

proceeds from the debt issuance

The third‐party obligor is primarily obligated for debt

service payments

93

94

3/10/2021

48

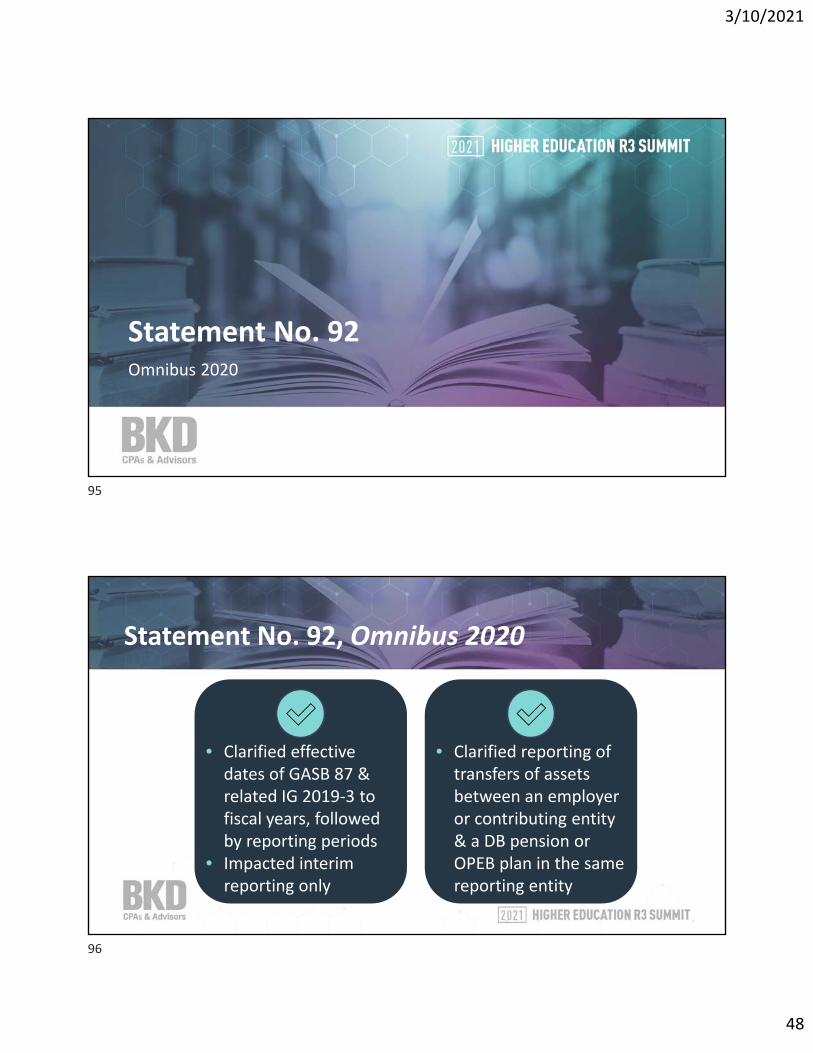

Statement No. 92Omnibus 2020

Statement No. 92, Omnibus 2020

• Clarified effective dates of GASB 87 & related IG 2019‐3 to fiscal years, followed by reporting periods

• Impacted interim reporting only

• Clarified reporting of transfers of assets between an employer or contributing entity & a DB pension or OPEB plan in the same reporting entity

95

96

3/10/2021

49

Statement No. 92, Omnibus 2020

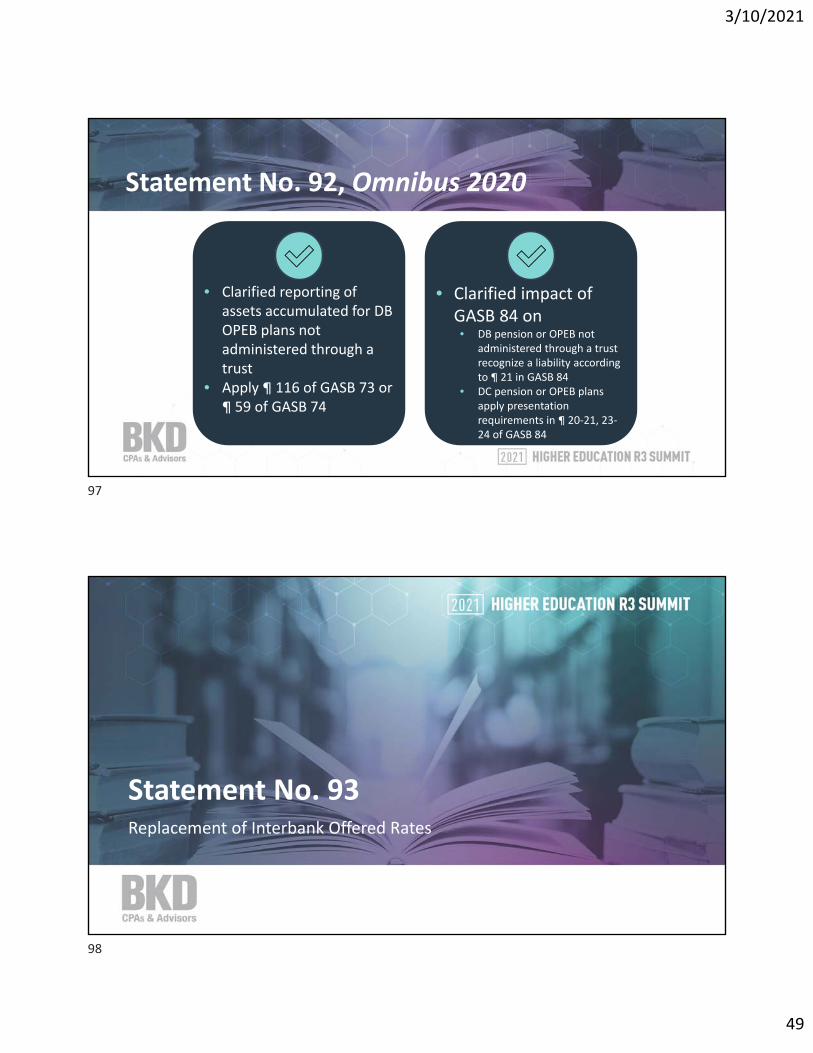

• Clarified reporting of assets accumulated for DB OPEB plans not administered through a trust

• Apply ¶ 116 of GASB 73 or ¶ 59 of GASB 74

• Clarified impact of GASB 84 on• DB pension or OPEB not

administered through a trust recognize a liability according to ¶ 21 in GASB 84

• DC pension or OPEB plans apply presentation requirements in ¶ 20‐21, 23‐24 of GASB 84

Statement No. 93Replacement of Interbank Offered Rates

97

98

3/10/2021

50

Statement No. 93Replacement of Interbank Offered Rates

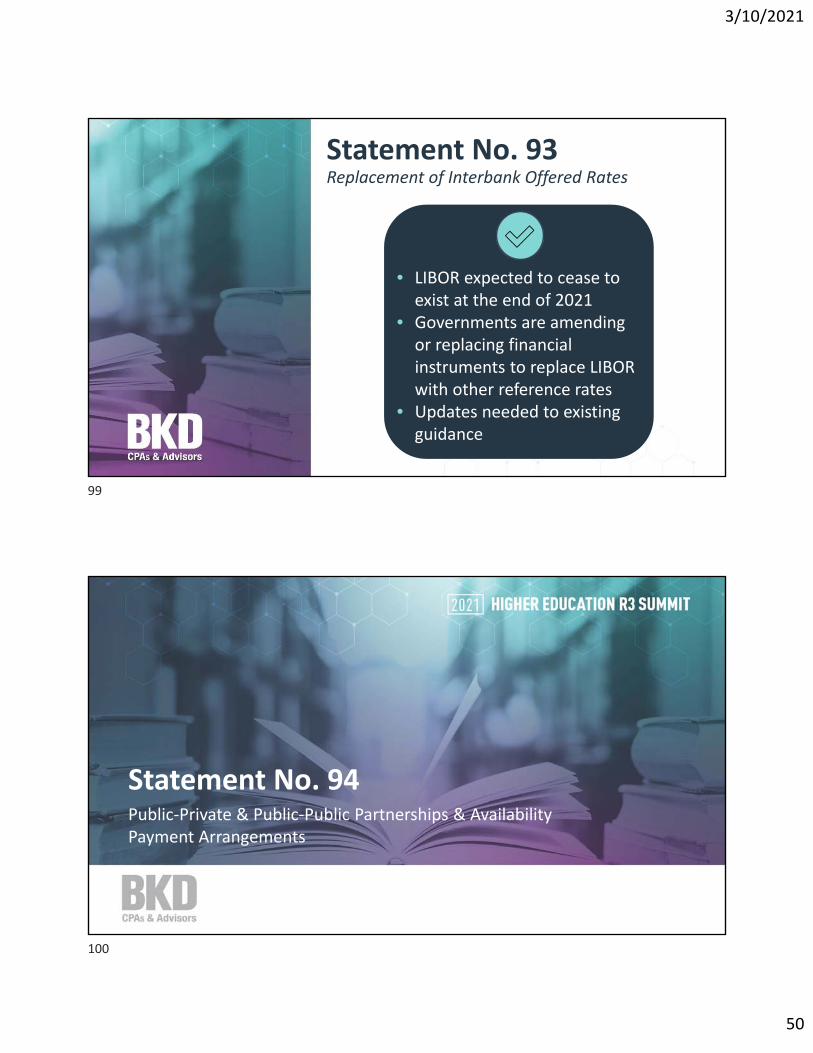

• LIBOR expected to cease to exist at the end of 2021

• Governments are amending or replacing financial instruments to replace LIBOR with other reference rates

• Updates needed to existing guidance

Statement No. 94Public‐Private & Public‐Public Partnerships & Availability Payment Arrangements

99

100

3/10/2021

51

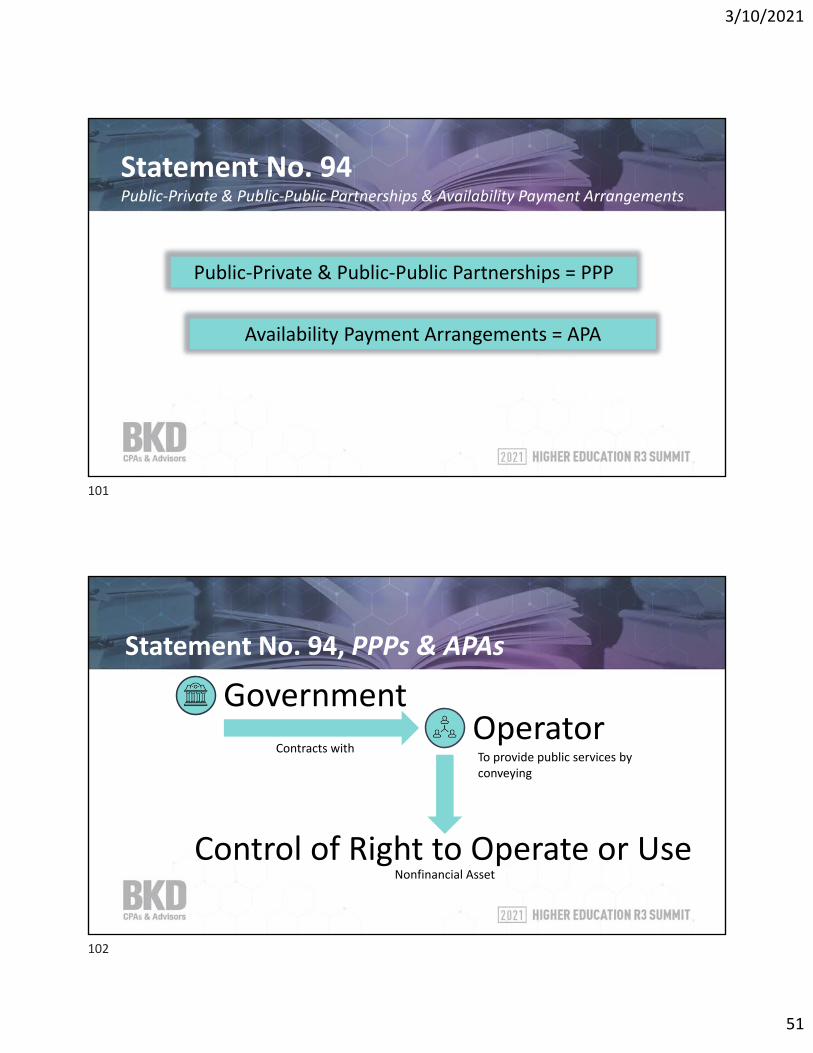

Statement No. 94 Public‐Private & Public‐Public Partnerships & Availability Payment Arrangements

Public‐Private & Public‐Public Partnerships = PPP

Availability Payment Arrangements = APA

Statement No. 94, PPPs & APAs

GovernmentOperator

Control of Right to Operate or Use

Contracts withTo provide public services by conveying

Nonfinancial Asset

101

102

3/10/2021

52

Statement No. 94, PPPs & APAs

• PPP that meets the definition of a lease – use GASB 87

Only underlying PPP assets are existing assets of the transferor that are not required to be improved by the operator as part of the PPP

&

PPP does not meet the definition of a service concession arrangement (SCA)

• PPP that meets the definition of an SCA or not in the scope of GASB 87 – use GASB 94

What about Statement No. 60? Superseded by GASB 94

Statement No. 94, PPPs & APAs

• APAs

Availability payments are regular project payments made from the governmental entity to the private consortium once the piece of infrastructure is “available.” In an availability payment P3, the private consortium typically designs, builds, & finances the construction of the asset. After construction, the private consortium will operate & maintain the asset for the life of the contract, typically around 30 years but in some cases longer

In exchange, the governmental entity may provide milestone &/or completion payments during the construction period, & then pay annual availability payments, which are Availability Payments in either predetermined or based on a predetermined formula, to the contractor once the asset is operational, as long as contractually specified performance standards are met

103

104

3/10/2021

53

Statement No. 96Subscription‐Based Information Technology Arrangements

Statement No. 96 Subscription‐Based Information Technology Arrangements

Contract that conveys control of the right to use another party’s (a SBITA vendor’s) IT software, alone or in combination with tangible capital assets (the underlying IT assets), as specified in the contract for a period of time in an exchange or exchange‐like transaction

105

106

3/10/2021

54

Statement No. 96, Subscription‐Based Information Technology Arrangements

Costs for Activities Associated with SBITA

Preliminary Project Stage

Expensed as Incurred

Initial Implementation Stage

Capitalized

Operation & Additional Implementation Stage

Expensed as Incurred*

*Capitalized if meet specific criteria

Training costs should be expensed, regardless of stage in which incurred.

Statement No. 97Certain Component Unit Criteria, & Section 457 Deferred Compensation Plans

107

108

3/10/2021

55

Statement No. 97Certain Component Unit Criteria, & Section 457 Deferred Compensation Plans

• Is a government financially accountable for a potential component unit in the absence of a governing board?

• Treat the same as appointment of voting majority except

• Defined contribution pension, OPEB, or other employee benefit plan

Statement No. 97Certain Component Unit Criteria, & Section 457 Deferred Compensation Plans

• Paragraph 7 of GASB 84 indicates that pension/OPEB plans administered through a trust impose a financial burden on the PG if that government is legally obligated or has otherwise assumed obligation to make contributions to the pension/OPEB plan

• Only applies to DB plans

109

110

3/10/2021

56

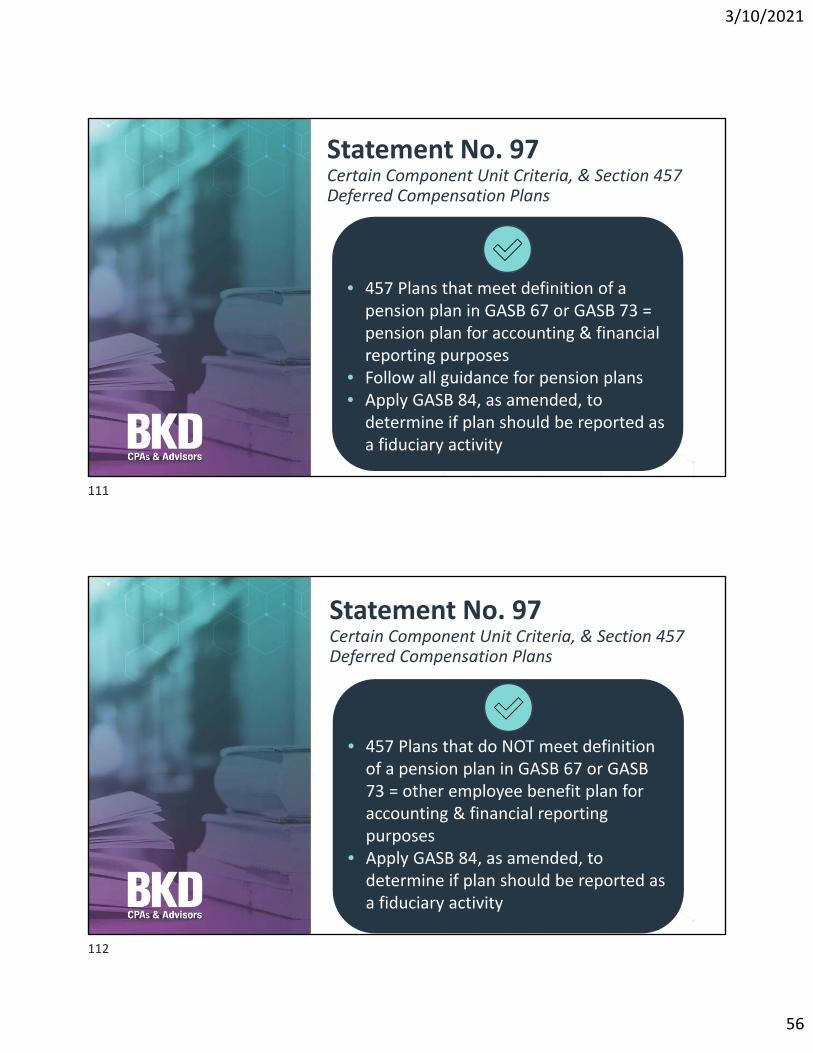

Statement No. 97Certain Component Unit Criteria, & Section 457 Deferred Compensation Plans

• 457 Plans that meet definition of a pension plan in GASB 67 or GASB 73 = pension plan for accounting & financial reporting purposes

• Follow all guidance for pension plans• Apply GASB 84, as amended, to determine if plan should be reported as a fiduciary activity

Statement No. 97Certain Component Unit Criteria, & Section 457 Deferred Compensation Plans

• 457 Plans that do NOT meet definition of a pension plan in GASB 67 or GASB 73 = other employee benefit plan for accounting & financial reporting purposes

• Apply GASB 84, as amended, to determine if plan should be reported as a fiduciary activity

111

112

3/10/2021

57

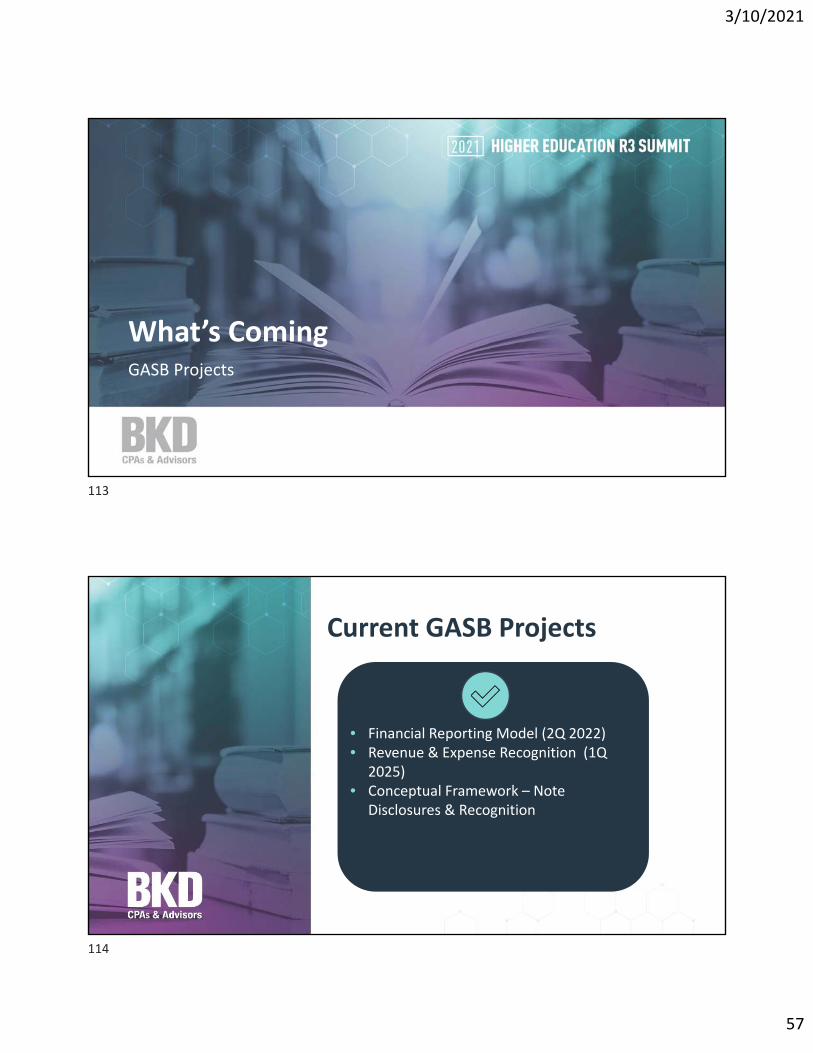

What’s ComingGASB Projects

Current GASB Projects

• Financial Reporting Model (2Q 2022)• Revenue & Expense Recognition (1Q

2025)• Conceptual Framework – Note

Disclosures & Recognition

113

114

3/10/2021

58

Current GASB Projects

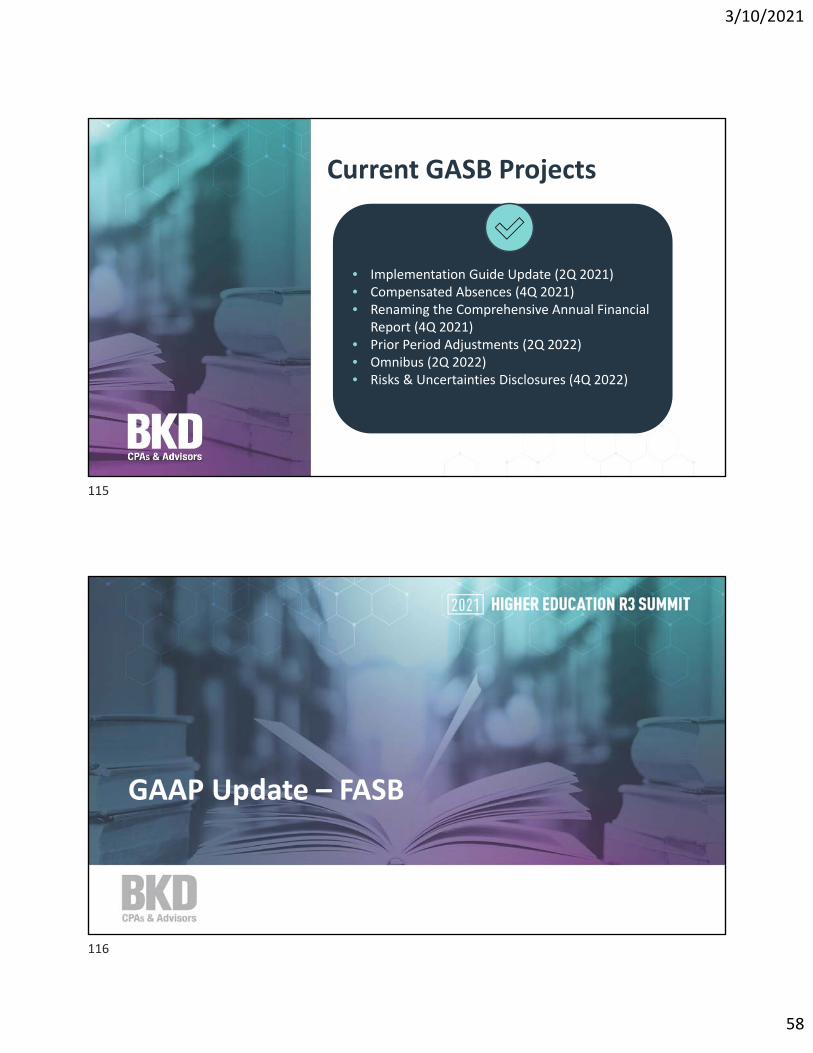

• Implementation Guide Update (2Q 2021)• Compensated Absences (4Q 2021)• Renaming the Comprehensive Annual Financial

Report (4Q 2021)• Prior Period Adjustments (2Q 2022)• Omnibus (2Q 2022)• Risks & Uncertainties Disclosures (4Q 2022)

GAAP Update – FASB

115

116

3/10/2021

59

GAAP Update –FASB Agenda

1

2

3

4

Revenue Recognition, Grants (PPP & HEERF)

Leases

Other Recent ASUs

Q&A

Revenue Recognition (Topic 606) & Grants – PPP & HEERF (Subtopic 958‐605)

118

117

118

3/10/2021

60

119

Revenue, Grants, & ContractsEffective Dates

NOTE: “Public” includes NFPs with public debt (conduit or direct)

Revenue From Contracts With Customers –

Topic 606

• CY 2018 (Public Entities)

• CY 2019 (Nonpublic Entities) – Plus one year for COVID relief moves it to CY 2020 or FYE 2021

Contracts Grants & Contracts –ASU 2018-08RecipientsFYE June 2019 & later (Public)

CY 2019 & later (Nonpublic)

Resource ProvidersCY 2019 & later (Public)CY 2020 & later (Nonpublic)

Rev. Rec. – Transition – Topic 606Transition Method

ComparativeYear

Year of Adoption

Footnotes for Year of Adoption

Retrospective(with optional practical

expedients)

Cumulative

catch‐up Report both years under the new standard

Comparative disclosures under the new standard

Cumulative effect

at date of application

No change, report under the legacy guidance

Cumulative

catch‐up Existing

uncompleted & new contracts

under new standard

Existing & new contracts under legacy standard

forYear of adoption to reflect current year

impact

119

120

3/10/2021

61

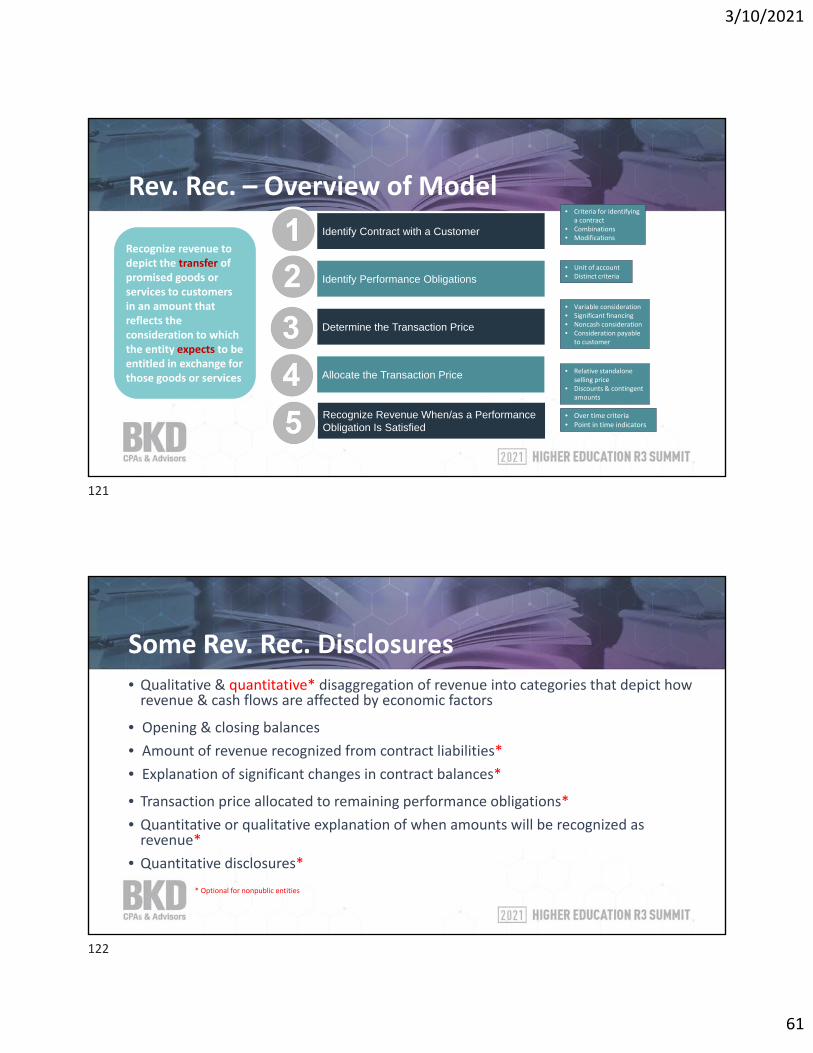

Rev. Rec. – Overview of Model

Recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services

• Unit of account• Distinct criteria

• Variable consideration• Significant financing• Noncash consideration• Consideration payable

to customer

• Criteria for identifying a contract

• Combinations• Modifications

• Relative standalone selling price

• Discounts & contingent amounts

• Over time criteria• Point in time indicators

Identify Contract with a Customer

Identify Performance Obligations

Determine the Transaction Price

Allocate the Transaction Price

Recognize Revenue When/as a Performance Obligation Is Satisfied

Some Rev. Rec. Disclosures

• Qualitative & quantitative* disaggregation of revenue into categories that depict how revenue & cash flows are affected by economic factors

• Opening & closing balances

• Amount of revenue recognized from contract liabilities*

• Explanation of significant changes in contract balances*

• Transaction price allocated to remaining performance obligations*

• Quantitative or qualitative explanation of when amounts will be recognized as revenue*

• Quantitative disclosures*

* Optional for nonpublic entities

121

122

3/10/2021

62

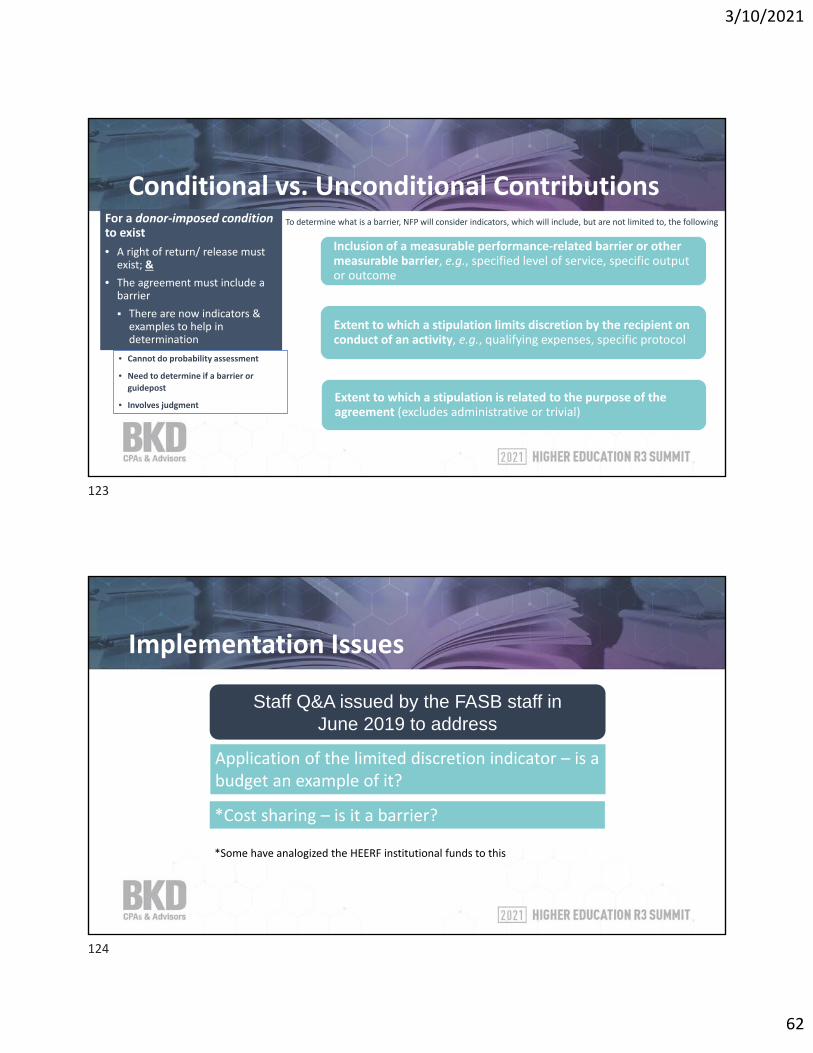

Conditional vs. Unconditional Contributions

• Cannot do probability assessment

• Need to determine if a barrier or

guidepost

• Involves judgment

Inclusion of a measurable performance‐related barrier or other measurable barrier, e.g., specified level of service, specific output or outcome

Extent to which a stipulation limits discretion by the recipient on conduct of an activity, e.g., qualifying expenses, specific protocol

Extent to which a stipulation is related to the purpose of the agreement (excludes administrative or trivial)

For a donor‐imposed conditionto exist

• A right of return/ release must exist; &

• The agreement must include a barrier

There are now indicators & examples to help in determination

To determine what is a barrier, NFP will consider indicators, which will include, but are not limited to, the following

Implementation Issues

Staff Q&A issued by the FASB staff in June 2019 to address

Application of the limited discretion indicator – is a budget an example of it?

*Cost sharing – is it a barrier?

*Some have analogized the HEERF institutional funds to this

123

124

3/10/2021

63

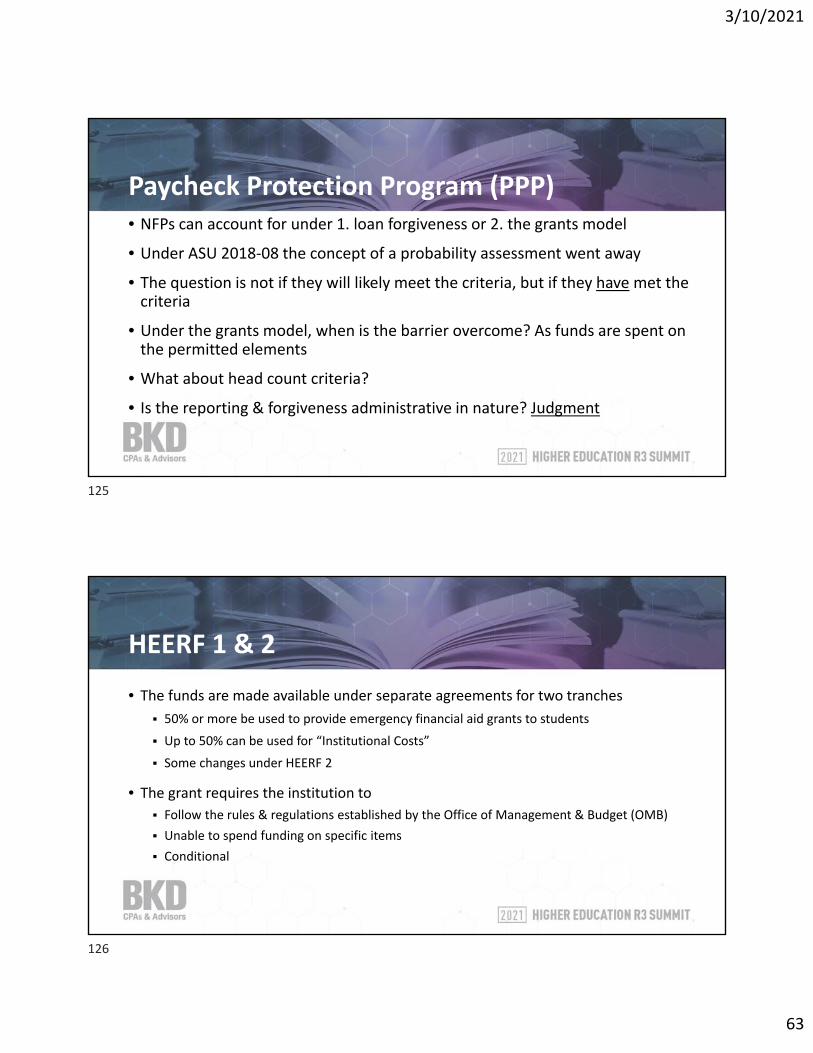

• NFPs can account for under 1. loan forgiveness or 2. the grants model

• Under ASU 2018‐08 the concept of a probability assessment went away

• The question is not if they will likely meet the criteria, but if they have met the criteria

• Under the grants model, when is the barrier overcome? As funds are spent on the permitted elements

• What about head count criteria?

• Is the reporting & forgiveness administrative in nature? Judgment

Paycheck Protection Program (PPP)

HEERF 1 & 2

• The funds are made available under separate agreements for two tranches

50% or more be used to provide emergency financial aid grants to students

Up to 50% can be used for “Institutional Costs”

Some changes under HEERF 2

• The grant requires the institution to

Follow the rules & regulations established by the Office of Management & Budget (OMB)

Unable to spend funding on specific items

Conditional

125

126

3/10/2021

64

LeasesTopic 842

Leases (ASU 2016‐02, etc.; Topic 842)

• A lease contract conveys the right to use an asset (the underlying asset) for a period of time in exchange for consideration

Lessor

Right‐of‐Use Asset

Lease Payments

Lessee

127

128

3/10/2021

65

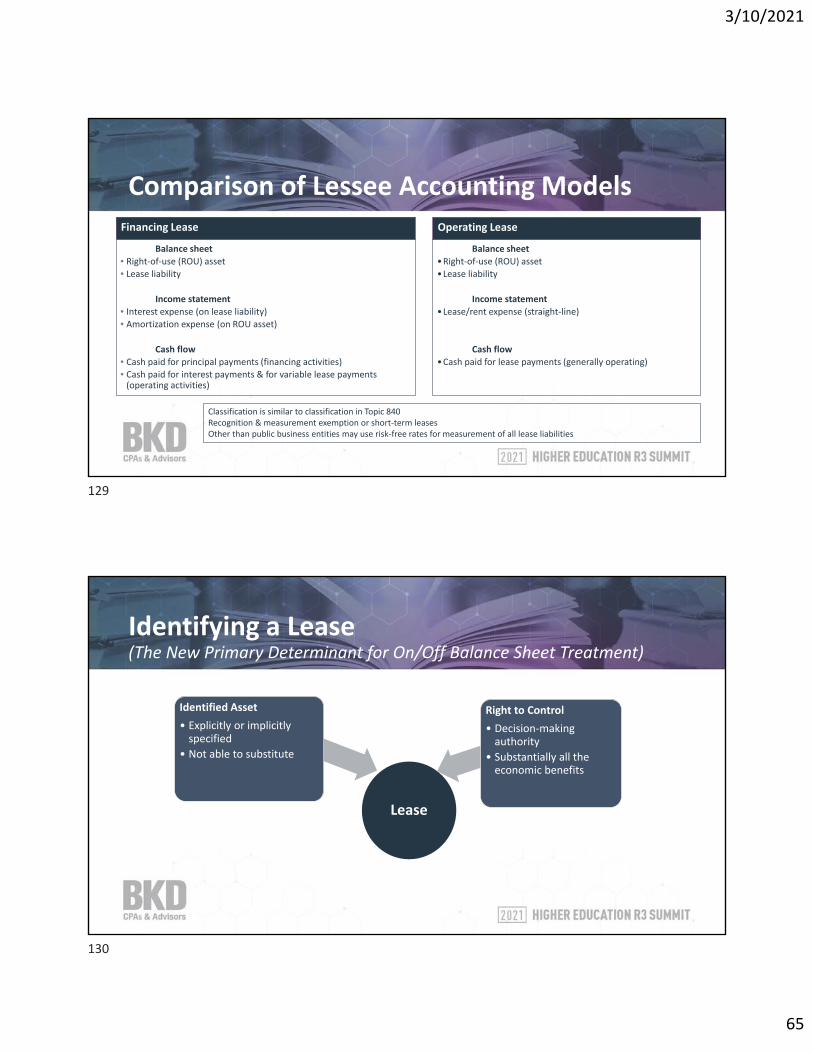

Comparison of Lessee Accounting Models

Balance sheet

• Right‐of‐use (ROU) asset• Lease liability

Income statement

• Interest expense (on lease liability)• Amortization expense (on ROU asset)

Cash flow

• Cash paid for principal payments (financing activities)

• Cash paid for interest payments & for variable lease payments (operating activities)

Balance sheet

•Right‐of‐use (ROU) asset

•Lease liability

Income statement

•Lease/rent expense (straight‐line)

Cash flow

•Cash paid for lease payments (generally operating)

Classification is similar to classification in Topic 840Recognition & measurement exemption or short‐term leasesOther than public business entities may use risk‐free rates for measurement of all lease liabilities

Financing Lease Operating Lease

Identifying a Lease(The New Primary Determinant for On/Off Balance Sheet Treatment)

Lease

Identified Asset

• Explicitly or implicitly specified

• Not able to substitute

Right to Control

• Decision‐making authority

• Substantially all the economic benefits

129

130

3/10/2021

66

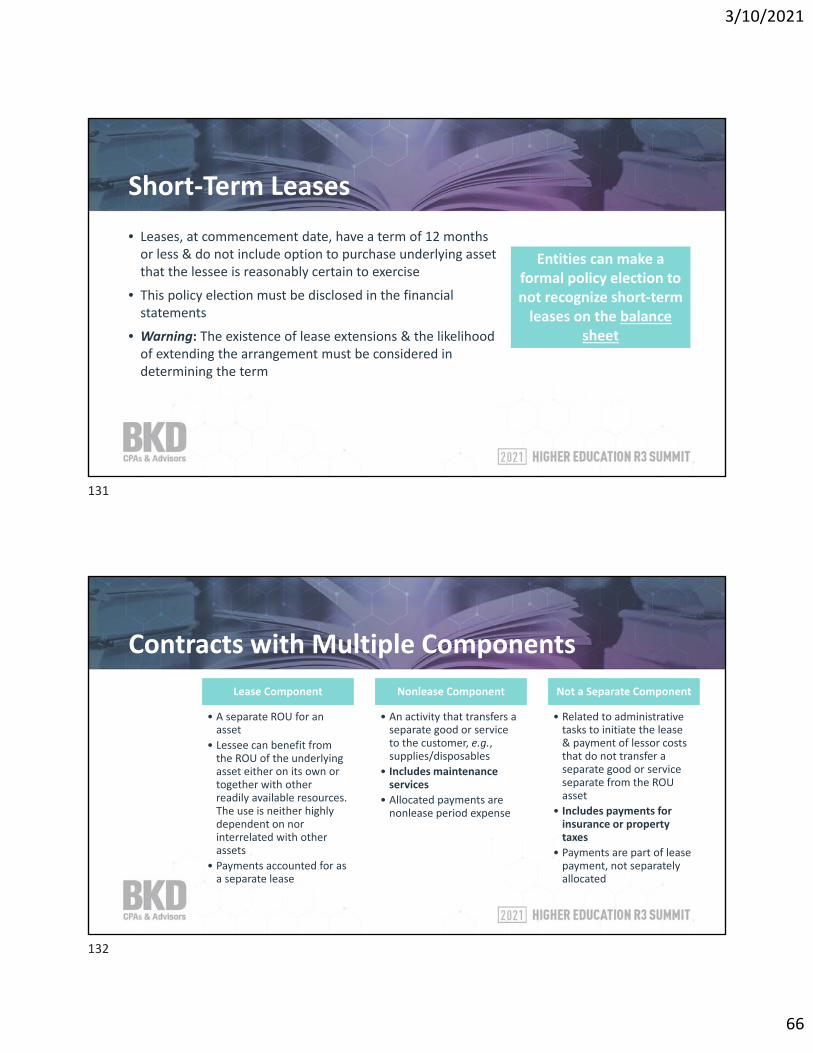

Short‐Term Leases

• Leases, at commencement date, have a term of 12 months or less & do not include option to purchase underlying asset that the lessee is reasonably certain to exercise

• This policy election must be disclosed in the financial statements

• Warning: The existence of lease extensions & the likelihood of extending the arrangement must be considered in determining the term

Entities can make a formal policy election to not recognize short‐term leases on the balance

sheet

Contracts with Multiple Components

Lease Component

• A separate ROU for an asset

• Lessee can benefit from the ROU of the underlying asset either on its own or together with other readily available resources. The use is neither highly dependent on nor interrelated with other assets

• Payments accounted for as a separate lease

Nonlease Component

• An activity that transfers a separate good or service to the customer, e.g., supplies/disposables

• Includes maintenance services

• Allocated payments are nonlease period expense

Not a Separate Component

• Related to administrative tasks to initiate the lease & payment of lessor costs that do not transfer a separate good or service separate from the ROU asset

• Includes payments for insurance or property taxes

• Payments are part of lease payment, not separately allocated

131

132

3/10/2021

67

Finance Lease (Similar to Capital Lease)

Ownership of asset transfers to lessee by end of lease term

Lessee has purchase option that it is reasonably certain to be exercised

Lease term is for major part of economic life of asset (n/a for leases that commence “at or near the end” of the underlying asset’s economic life, e.g., in the final 25% of an asset’s economic life)

PV of minimum lease payments amounts to at least substantially all of fair value of leased asset

NEW: Underlying asset is of such a specialized nature that it is expected to have no alternative use to the lessor at the end of the lease term

Lease Concessions & Covid‐19 Relief

• April 2020 FASB Staff Q&A Discusses implications to lease arrangements as a result of the COVID‐19 pandemic

• Accounting for the deferral of rent payments

• Accounting for lease concessions & consideration of lease modification accounting guidance

133

134

3/10/2021

68

Transition & Effective Date

Public Entities

Years beginning after 12/15/2018

Nonpublic Entities Years beginning after 12/15/2020

COVID‐19 Relief June ASU 2020‐05 issued to provide an additional year to implement

Lease AccountingFY 20X1(comparative

period)

FY 20X2(year of initial adoption)

Original transition method provided in Update 2016‐02

842 842

Additional transition method provided in Update 2018‐11

840 842

TransitionEffective Date

Other Recent ASUs

136

135

136

3/10/2021

69

Not‐for‐Profit Reporting of Gifts‐in‐kind

Increasing transparency about contributed nonfinancial assets through enhancements to presentation & disclosure

Objective

Contributions of nonfinancial assets (fixed assets, use of fixed assets, materials & supplies, intangibles, services)

Scope

Requirements

• Present contributed nonfinancial assets as separate line item in the statement of activities

• Disclose disaggregation by category of nonfinancial asset including if monetized & policy on monetizing

• Disclose a description of donor restrictions associated with nonfinancial asset

• Provide description of the valuation techniques & inputs used to arrive at a fair value measure for contributed nonfinancial assets in accordance with paragraph 820‐10‐50‐2(bbb)(1) of codification for initial recognition

• Disclose principal market (or most advantageous market) used to arrive at fair value measure if it is a market in which the recipient NFP is prohibited by donor restrictions from selling or using the contributed asset

138

Not‐for‐Profit Reporting of Gifts‐in‐Kind

137

138

3/10/2021

70

Not‐for‐Profit Reporting of Gifts‐in‐Kind

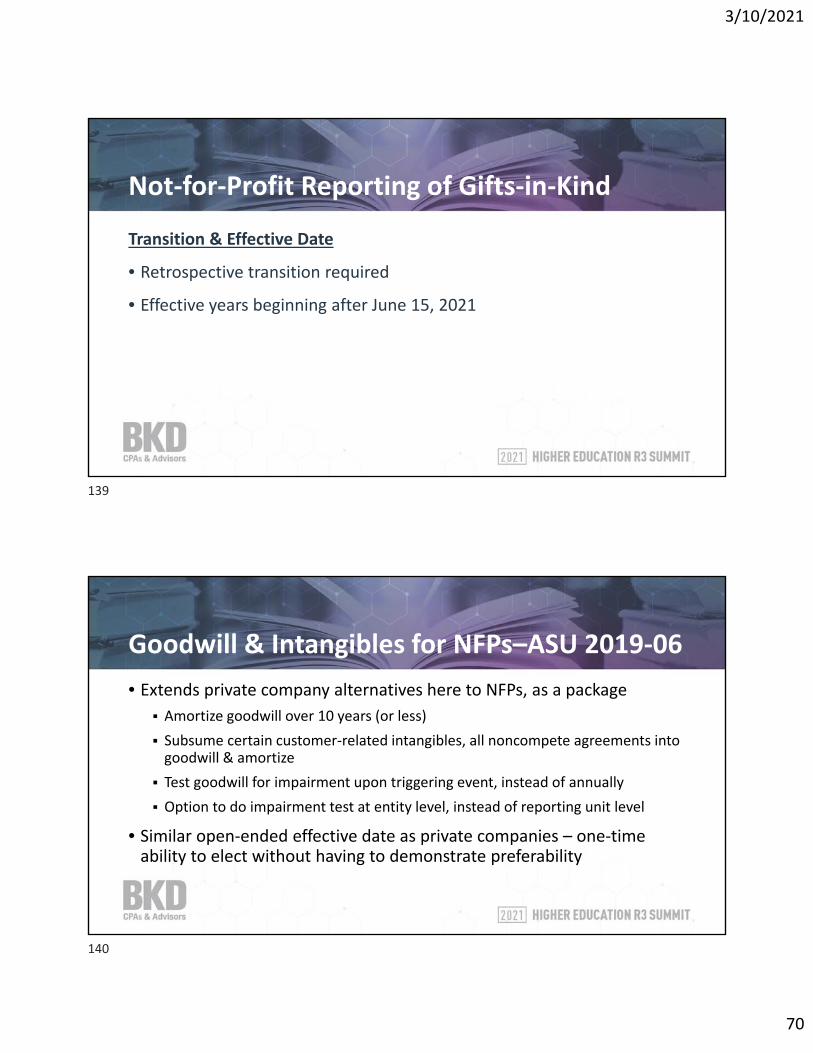

Transition & Effective Date

• Retrospective transition required

• Effective years beginning after June 15, 2021

Goodwill & Intangibles for NFPs–ASU 2019‐06

• Extends private company alternatives here to NFPs, as a package

Amortize goodwill over 10 years (or less)

Subsume certain customer‐related intangibles, all noncompete agreements into goodwill & amortize

Test goodwill for impairment upon triggering event, instead of annually

Option to do impairment test at entity level, instead of reporting unit level

• Similar open‐ended effective date as private companies – one‐time ability to elect without having to demonstrate preferability

139

140

3/10/2021

71

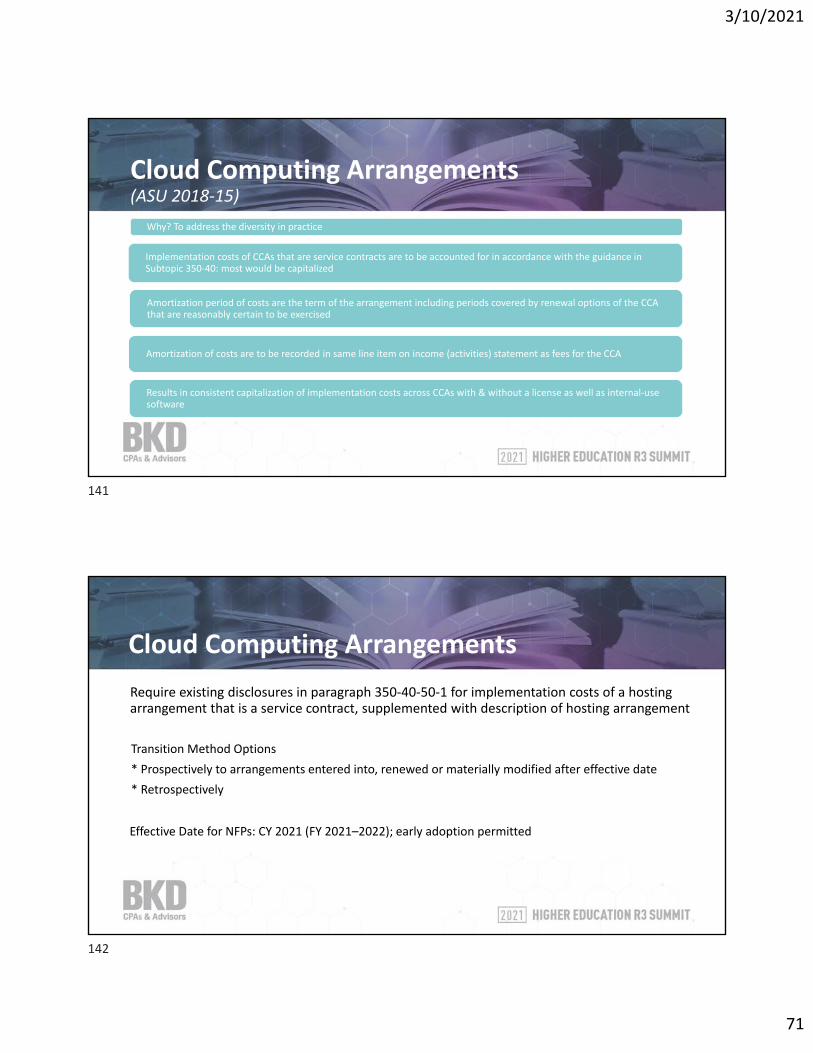

Cloud Computing Arrangements(ASU 2018‐15)

Why? To address the diversity in practice

Implementation costs of CCAs that are service contracts are to be accounted for in accordance with the guidance in Subtopic 350‐40: most would be capitalized

Amortization period of costs are the term of the arrangement including periods covered by renewal options of the CCA that are reasonably certain to be exercised

Amortization of costs are to be recorded in same line item on income (activities) statement as fees for the CCA

Results in consistent capitalization of implementation costs across CCAs with & without a license as well as internal‐use software

Cloud Computing Arrangements

Require existing disclosures in paragraph 350‐40‐50‐1 for implementation costs of a hosting arrangement that is a service contract, supplemented with description of hosting arrangement

Transition Method Options

* Prospectively to arrangements entered into, renewed or materially modified after effective date

* Retrospectively

Effective Date for NFPs: CY 2021 (FY 2021–2022); early adoption permitted

141

142

3/10/2021

72

Reference Rate Reform (ASU 2020‐04)

Current Accounting

High‐volume modifications results in burdensome accounting evaluations

Hedge accounting discontinued when contracts are modified

Hedge accounting discontinued if hedging relationships are not highly effective during the temporary transition period

Optional Relief

Simplified accounting evaluations scaled for high volume of modifications

Hedge accounting preservedwhen contracts are modified

Hedge accounting preservedduring the temporary transition period, with any hedge breakage/ineffectiveness visible in the financial statements

Contract Modifications

Final ASU issued March 2020

Hedge Accounting

TWO AREAS OF FOCUS

Disclosure Framework—Fair Value Measurement (Topic 820)Removals

• Amount of & reasons for transfers between Level 1 & Level 2

• Policy for timing of transfers between levels

• Valuation processes for Level 3• Nonpublic entities only: Unrealized gains & losses in earnings for Level 3 held at period‐end

Modifications

• Net asset value disclosure• Measurement uncertainty disclosure• Nonpublic entities only: Transfers, purchases & issues into or out of Level 3 in lieu of a rollforward

Additions

• Unrealized gains & losses in other comprehensive income for Level 3 held at period end (public entities only)

• Range & weighted average of significant unobservable inputs used to develop Level 3 fair value measurements (public entities only)

ASU 2018‐13 is effective for all entities for CY 2020 (FY 2020–2021). Can early adopt removals & modifications without having to early adopt additions. Public Entities include NFPs that are obligated for publicly‐traded conduit (or direct) debt

143

144

3/10/2021

73

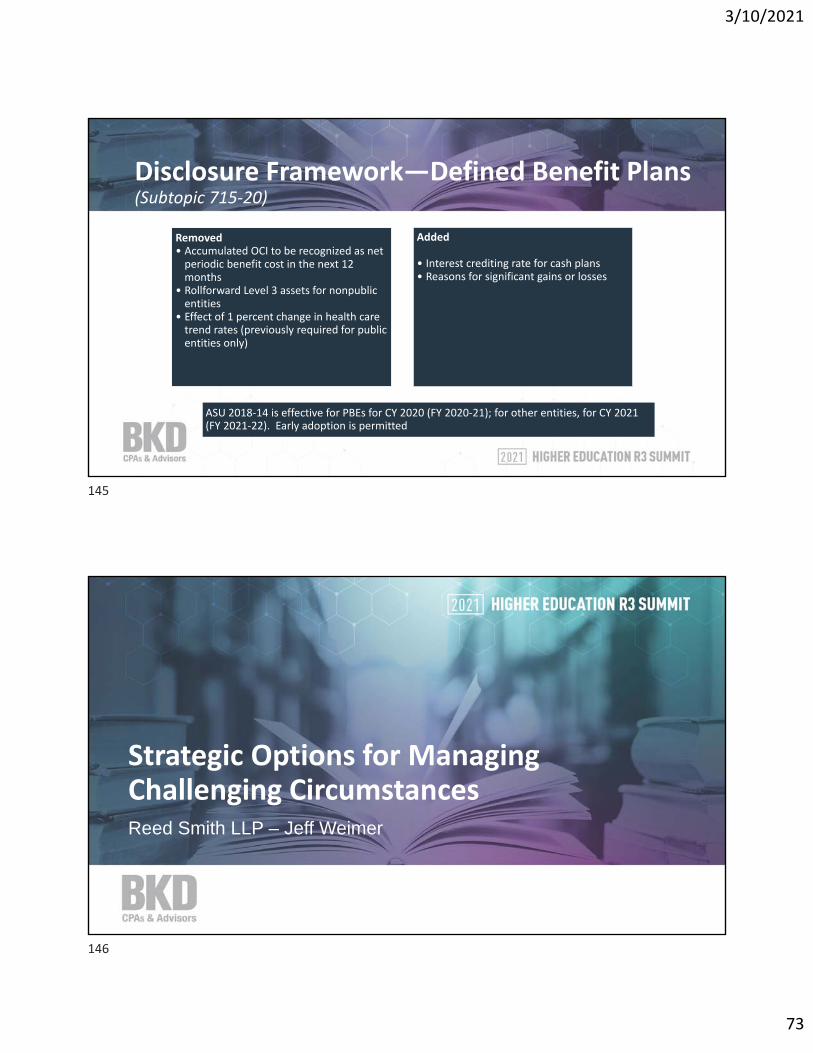

Disclosure Framework—Defined Benefit Plans(Subtopic 715‐20)

Removed• Accumulated OCI to be recognized as net periodic benefit cost in the next 12 months

• Rollforward Level 3 assets for nonpublic entities

• Effect of 1 percent change in health care trend rates (previously required for public entities only)

Added

• Interest crediting rate for cash plans• Reasons for significant gains or losses

ASU 2018‐14 is effective for PBEs for CY 2020 (FY 2020‐21); for other entities, for CY 2021 (FY 2021‐22). Early adoption is permitted

Strategic Options for Managing Challenging CircumstancesReed Smith LLP – Jeff Weimer

145

146

3/10/2021

74

End of Day Closing Comments

147

148

3/10/2021

75

149