real estate vs stock market: approaching the required rate of return through the treynor and black...

TRANSCRIPT

Real Estate vs Stock Market: approaching the required rate of return through the Treynor

and Black model

Joan Montllor-Serrats(Universitat Autònoma de Barcelona)

Anna-Maria Panosa-Gubau (Universitat de Girona)

Summary of the paper

• Study of the properties of real estate combined with financial assets in an optimal portfolio– Application of Treynor and Black Model

• Effects of the indivisibility– Relationship with value and bubbles

• Analysis of bubbles based on exchange options

RealEstate is outside the financial market

Combining Real Estate with the Market Index of financial assets

Real Estate will be included in a portfolio if provides an alpha that compensates this drawbacks

Incentives to combine: - Low correlation with

financial assets- Way to create value

Drawbacks:

- Low liquidity- high transaction costs

Combining Real Estate with the Market Index of financial assets

Treynor and Black Model (1973)

portfolio combining :- portfolio of

undervalued assets

- market index

This work:enlarged portfolio

portfolio combining : real estate assets

+market index

Central difference

undervalued assets short run

real estate long run

(stable portfolio)

Combining Real Estate with the Market Index of financial assets

Enlarged portfolio

M

R

RE

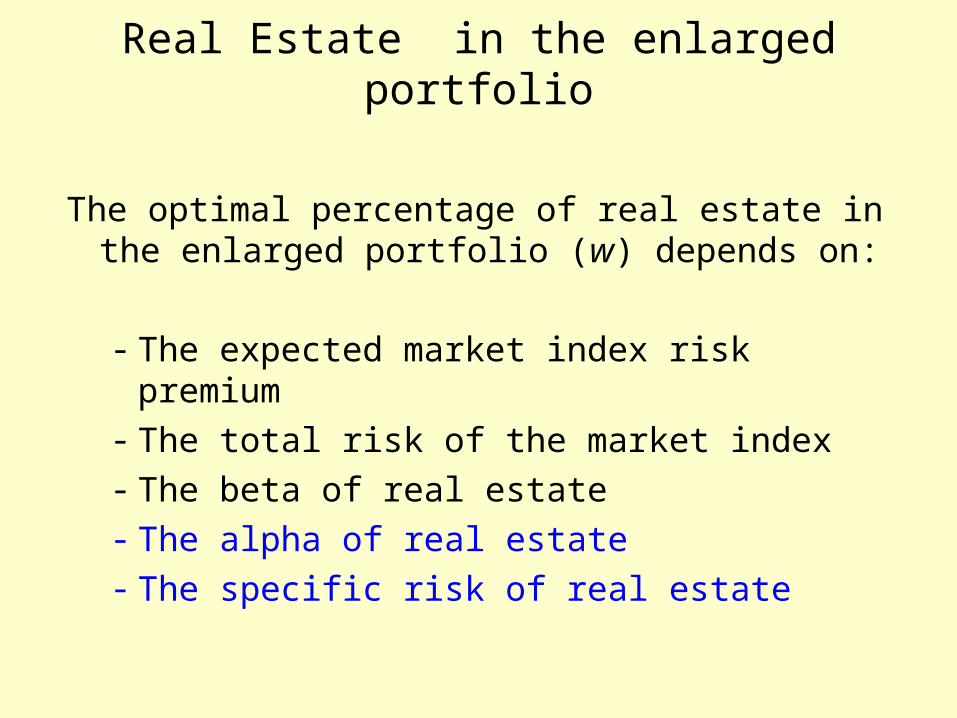

The optimal percentage of real estate in the enlarged portfolio (w) depends on:

- The expected market index risk premium- The total risk of the market index- The beta of real estate- The alpha of real estate- The specific risk of real estate

Real Estate in the enlarged portfolio

Introducing the appraisal ratio or information ratio

p

ppAR

Real Estate in the portfolio

Introducing the appraisal ratio

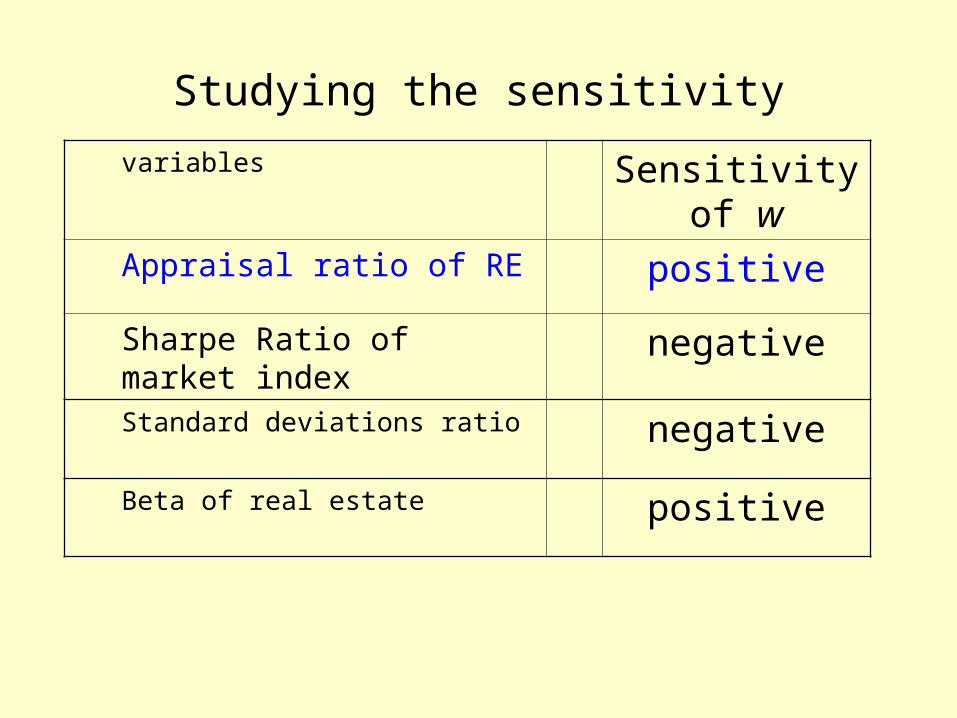

The optimal percentage (w) depends on:

- A variable that only depends on real estate its appraisal ratio

- A variable that only depends on financial assets the Sharpe ratio of its market index

- Two variables that depend on real estate and financial assets at the same time

The coefficient beta of real estate The ratio between the specific risk of real estate and the specific

risk of market index

Real Estate in the portfolio

Studying the sensitivity

variables Sensitivity of wAppraisal ratio of RE positive

Sharpe Ratio of market index negative

Standard deviations ratio negative

Beta of real estate positive

The Sharpe ratio of the enlarged portfolio

from Bodie, Kane and Marcus (2002):

On this basis:

Real Estate in the portfolio

Increase in the expected risk premium for the volatility assumed by the investor:

The increase in the risk premium depends on a sole variable connected with real estate:

its appraisal ratio

R r SM

1AR

p2

SM2 1

2 2m M pS S AR

Real Estate in the portfolio

From the value of a portfolio at one year horizon

increase in value:

The increase in value depends on the same variables as the increase in the risk premium, encapsulated on the appraisal ratio

1

1

m

m

M

M

R rr

VR r

r

V

SM 1

ARp2

SM2 1

1 r SM

Importance of this analysis for the agents:

• They have to pay attention to the Appraisal ratio (alpha and the specific risk of the real estate) not only to the risk premium.

Real Estate in the portfolio

Effects of Indivisibility

Indivisibility (real assets)

minimum budget in Real Estate

Minimum investor’s budget (total)

minP

minmin

PB

w

(w =optimal % of RE in the enlarged portfolio)

Effects of Indivisibility

Investor (CML) who whishes

higher minimum budget (for the volatility required)

i minB B

i m

minmin

mi

i i

BB B

x

( )i i mx

Investor needs higher budged to have lower volatility than

the enlarged portfolio

Enlarged portfolio

M

CML

mi

imR

iMR

Is the lose for an investor with insufficient budget who wants lower volatility than the volatility of the enlarged portfolio

im iMR R

Effects of Indivisibility

Investors with insufficient budget

Remain in CML

lose

im iM mm M

iM

M im

R r R rR R S S

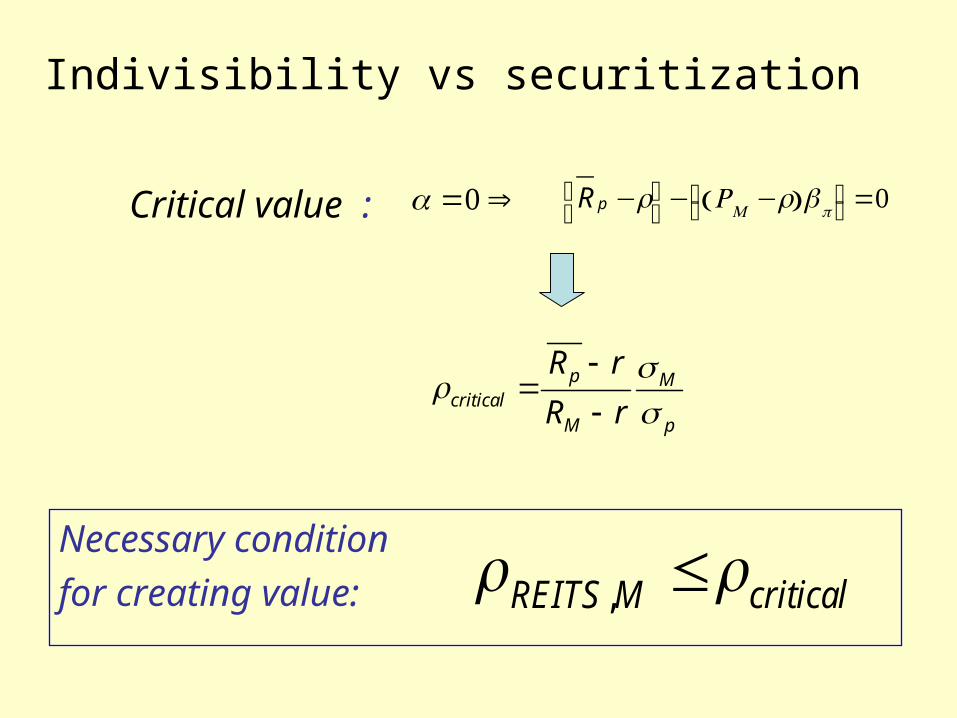

Indivisibility vs securitization

Substituting real estate assets by REITs

consequences :

- Avoid the problem of indivisibility (recoup value)- Increase correlation with market index (lessen value)

Critical value : ⇒ =0

Indivisibility vs securitization

Critical value : =0⇒

p Mcritical

M p

R r

R r

Necessary condition

for creating value: ,REITS M critical

R p −r⎡⎣

⎤⎦− RM −r βp

⎡⎣

⎤⎦0

Indivisibility minmin

PB

w

∂w∂AR

> 0 min 0B

AR

min demand of real estateAR w B AR

Effects of indivisibility

In a bubble

In a crisis

min demand of real estateAR w B AR

(Bubble: overvaluation of a kind of assets)

Securitization: a way of reducing indivisibility effect

Detecting Bubbles

Overvaluation obtain a positive anomalous return (positive Jensen alpha) not justified by facts or change of expectations

( the challenge is to evaluate the weight of the change of expectations)

Proposal:

an indicator of overvaluation through exchange options

Detecting bubbles

Strategy: Option to exchange the market index for real estate

i.e. exchange a final value of 1 € invested in market index for the final value of 1 € invested in real estate

t=0 t=1

Purchase of exchange options -CH0 Max {0, RA-RM)

Credit CH0 - CH0 (1+r)

0 Max {0, RA-RM) - CH0 (1+r)

Detecting bubbles

In this strategy:- The risk premium is embedded in the initial value of the exchange option

- The exchange option is valued according to Margrabe (1978)

This analysis

- Is based on the reliability of option valuation:- is independent of risk attitudes

- enables a direct comparison between the two rates of return under consideration

rCHRRb MA 10

An extra return (b>0) at the end of the period (not due to a change of

expectations or unexpected facts) can indicate a bubble

Detecting bubblesSimulation (not with real data) : Option valued according to

Margrabe (1978)

0 1A M C rR HR

Example: Option to exchange A (we receive real estate) for M (we deliver market index). Free interest rate: 5%. Cost of carry (maintenance costs: 2%)

at the end of the period, an extra return has been obtained if

10,00% 20,00% 25,00%

5,00% 20,00% 10,00%

5,00% 20,00% 5,00%

A M AM

0,08916 0,05 9,36%

0,08964 0,05 9,41%

0,09061 0,05 9,51%

0CH 0 (1 )CH rr

Conclusions (central ideas)- The expected rate of return of RE has to compensate for lack of

liquidity and higher transactions costs (compensatory alpha)

- Investor can create an enlarged portfolio – apply T&B model – combining Real Estate and Market index

- The appraisal ratio is regarded as the driver through wich real estate creates value

- Indivisibility requires a higher budged for a lower volatility (to maintain an optimal position)

- Indivisibility contributes to boost bubbles and to make crisis deeper

- Proposal of an indicator for detecting bubbles through exchange options

Thank you for your attention