report no. 7438-ph philippines: toward sustaining the...

TRANSCRIPT

Report No. 7438-PH

Philippines: Toward Sustaining the EconomicRecoveryCountry Economic MemorandumJInuary 30,1989

Country Operations DivisionAsia Country Department II

FOR OFFICIAL USE ONLY

Document of the World Bank

This document has a restricted distribution and may be used by recipientsonly in the performance of their official duties. Its contents may not otherwisebe disclosed without World Bank authorization.

Pub

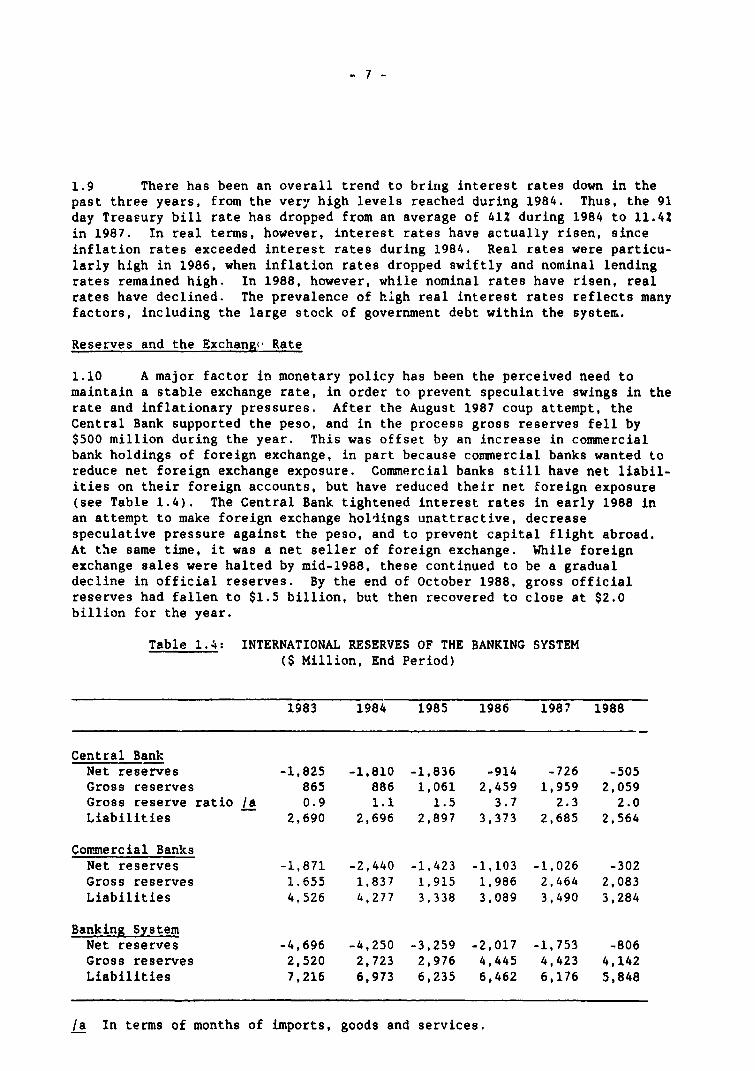

lic D

iscl

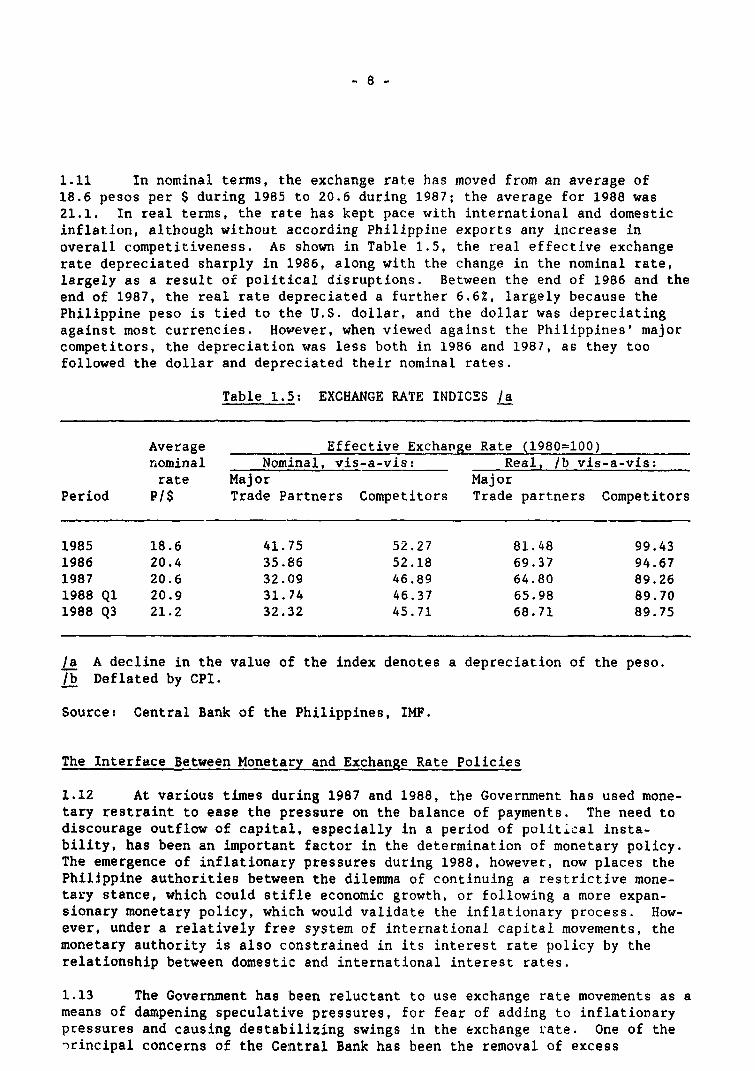

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

Average 1988 - US$1.0 - 21.1- P1.0 0.047

Average 1987 - US$1.0 = 20.6- P1.0 0.049

Average 1986 - US$1.0 = 20.4- P1.0 - 0.049

Average 1985 - US$1.0 - 18.6- P1.0 0.054

ACRONYMS

APT - Asset Privatization TrustBOI - Board of InvestmentsCB - Central BankCARP - Comprehensive Agarian Reform ProgramCPI - Consumer Price IndexDA - Department of AgricultureDAR - Department of Agarian ReformDBP - Development Bank of the PhilippinesDENR - Department of Environment

DPWH - Department of Public Works and High aysDTI - Department of Trade and IndustryEPR - Effective Protection RateGDP - Gross Domestic ProductGFI - Government Financial Institutiongnfs - Goods and non-factor servicesGNP - Gross National ProduccGRT - Gross Receipts Taxha - hectareHYV - High Yielding VarietiesICOR - Incremental Capital Output RatioIGLF - Industrial Guarantee & Loan FundIMF - International Monetary FundLBP - Land Band of the PhilippinesLIBOR - London Inter-Bank Offer RateMRR - Manila Reference RateMT - metric tonsNEDA - National Economic and Development AuthorityNFA - National Food AuthorityNIA - National Irrigation AdministrationNPA - Non-performing AccountsNPC - National Power CorporationO&M - Operation and MaintenancePCA - Philippine National BankPNOC - Philippine National Oil CompanyWPI - Wholesale Price Index

FOR OFmFCIAL USE ONLY

Preface

This report presents the work of a mission which visited thePhilippines in May/June 1988. The mission members included Norman Hicks(leader), Thanos Catsambas (macro), Zdenek Drabek (industry), Guillermo Hakim(balance of payments), Judy Lu (statistics, projections), Gerry Sicat (publicfinance), and Tom Wiens (agriculture, natural resources). The report wassubsequently updated during a mission which visited the Philippines inNovember/December 1988. In addition, the report draws on recent economic andsector work of other Bank missions, including "Philippines: The Challenge ofPoverty" Report No. 7144-PH (October, 1988), "Transport Sector Review" ReportNo. 7098-PH, (March 1988), "Selected Issues in Public Rescu:ce Management"Report No. 6887-PH (April, 1988), "Financial Sector Study", Report No. 7177-PH(August, 1988), and "Forestry, Fisheries, and Agricultural kes!urce ManagementStudy" Report No. 7388-PH (January 1989).

The mission would like to express its appreciation for the coopera-tion received from various government departments and agencies, including theNational Economic and Development Authority, the Central Bank the Office ofBudget and Management, and the Departments of Trade and Industry, Agricul-ture, Natural Resources, Finance, and Labo,r and Employment.

This document has a restricted distribution and may be used by recipients only in the performance |of their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

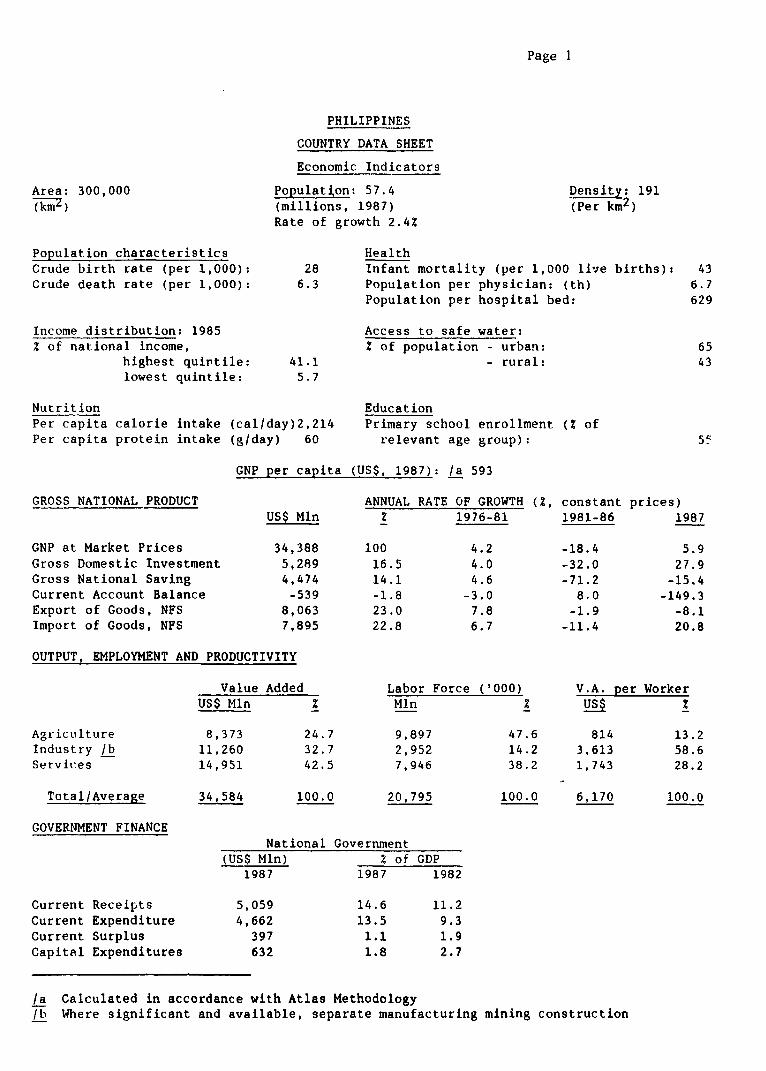

Page 1

PHILIPPINES

COUNTRY DATA SHEET

Economic Indicators

Area: 300,000 Population: 57.4 Density: 191

(kmZ) (millions, 1987) (Per km2)

Rate of growth 2.4Z

Population characteristics HealthCrude birth rate (per 1,000): 28 Infant mortality (per 1,000 live births): 43

Crude death rate (per 1,000): 6.3 Population per physician: (th) 6.7Population per hospital bed: 629

Income distribution: 1985 Access to safe water:Z of national income, Z of population - urban: 65

highest quintile: 41.1 - rural: 43lowest quintile: 5.7

Nutrition EducationPer capita calorie intake (cal/day)2,214 Primary school enrollment (Z ofPer capita protein intake (g/day) 60 relevant age group): 55

GNP per capita (US$, 1987): /a 593

GROSS NATIONAL PRODUCT ANNUAL RATE OF GROWTH (%, constant prices)US$ Mln Z 1976-81 1981-86 1987

GNP at Market Prices 34,388 100 4.2 -18.4 5.9

Gross Domestic Investment 5,289 16.5 4.0 -32.0 27.9

Gross National Saving 4,474 14.1 4.6 -71.2 -15.4

Current Account Balance -539 -1.8 -3.0 8.0 -149.3

Export of Goods, NFS 8,063 23.0 7.8 -1.9 -8.1

Import of Goods, NFS 7,895 22.8 6.7 -11.4 20.8

OUTPUT, EMPLOYMENT AND PRODUCTIVITY

Value Added Labor Force ('000) V.A. per Worker

US$ Mln Z Mln z US$ z

Agricutlture 8,373 24.7 9,897 47.6 814 13.2

Industry /b 11,260 32.7 2,952 14.2 3,613 58.6

Services 14,951 42.5 7,946 38.2 1,743 28.2

Total/Average 34,584 100.0 20,795 100.0 6,170 100.0

GOVERNMENT FINANCENational Government

CUS$ Mln) % of GDP1987 1987 1982

Current Receipts 5,059 14.6 11.2Current Expenditure 4,662 13.5 9.3

Current Surplus 397 1.1 1.9Capital Expenditures 632 1.8 2.7

/a Calculated in accordance with Atlas Methodology/b Where significant and available, separate manufacturing mining construction

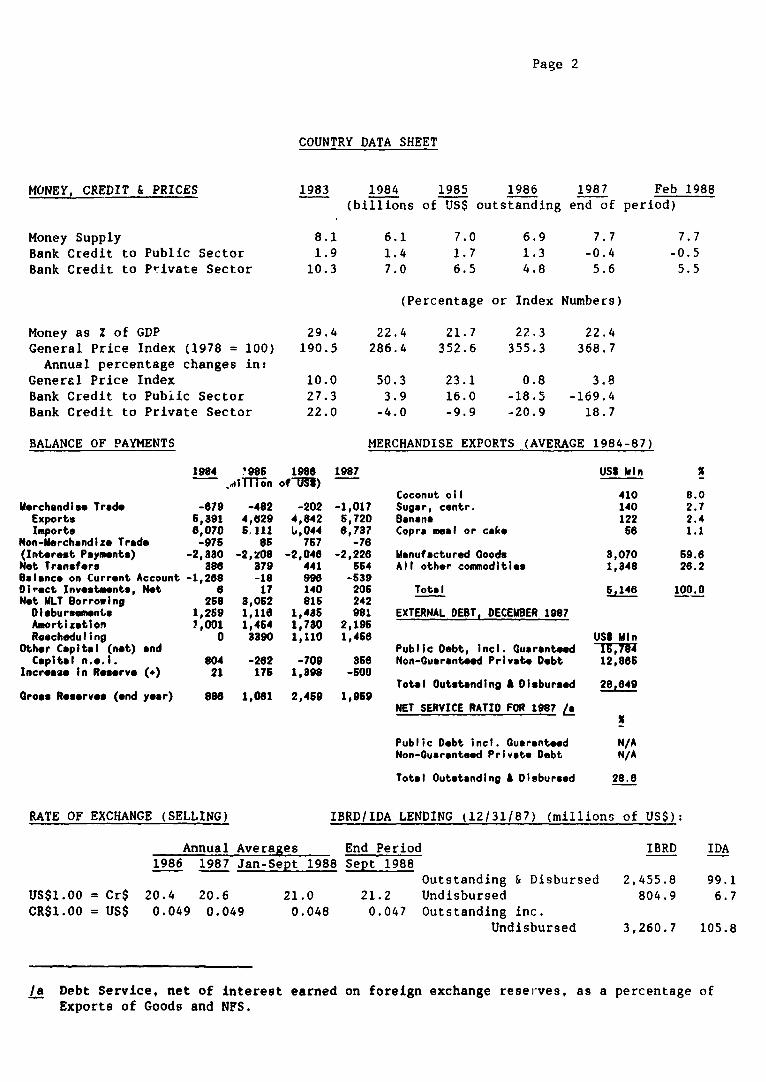

Page 2

COUNTRY DATA SHEET

MONEY, CREDIT & PRICES 1983 1984 1985 1986 1987 Feb 1988(billions of US$ outstanding end of period)

Money Supply 8.1 6.1 7.0 6.9 7.7 7.7Bank Credit to Public Sector 1.9 1.4 1.7 1.3 -0.4 -0.5Bank Credit to Private Sector 10.3 7.0 6.5 4.8 5.6 5.5

(Percentage or Index Numbers)

Money as Z of GDP 29.4 22.4 21.7 22.3 22.4General Price Index (1978 = 100) 190.5 286.4 352.6 355.3 368.7Annual percentage changes in:

General Price Index 10.0 50.3 23.1 0.8 3.8Bank Credit to Pubiic Sector 27.3 3.9 16.0 -18.5 -169.4Bank Credit to Private Sector 22.0 -4.0 -9.9 -20.9 18.7

BALANCE OF PAYMENTS MERCHANDISE EXPORTS (AVERAGE 1984-87)

1984 1985 1986 1987 USS Pun.,1ilTTin of U-U)

Coconut oil 410 8.0Merchandi.e Trade -679 -482 -202 -1,017 Sugar, centr. 140 2.7Exports 5,391 4,629 4,842 6,720 Banana 122 2.4Imports 6,070 65111 6,044 6,787 Copra meal or cake 66 1.1

Non-Merchandize Trade -976 86 767 -76(Interest Payments) -2,380 -2,Z0O -2,046 -2,228 Manufactured Goods 3,070 59.6Net Transfers asf 379 441 564 All other commodities 1,348 28.2Balance on Current Account -1,268 -18 996 -639Direct Investments, Net 6 17 140 206 Total 6,146 100.0Net MLT Borrowing 268 3,062 815 242Disbursements 1,269 1,118 1,436 981 EXTERNAL DEBT, DECESBER 1987Amortization 1,001 1,464 1,780 2,196Rescheduling 0 8390 1,110 1,468 USt MIn

Other Capital (not) and Public Debt, incl. Guaranteed IK,7IlCapital n.e.i. 804 -262 -709 ase Non-Guaranteed Private Debt 12,886

Increase in Roserve (.) 21 176 1,398 -600Total Outstanding A Disbursed 28,649

Gross R.serves (end year) 886 1,081 2,459 1,959NET SERVICE RATIO FOR 1987 L

Public Debt incl. Guaranteed N/ANon-Guaranteed Private Debt N/A

Total Outstanding A Disbursed 28.8

RATE OF EXCHANGE (SELLING) IBRD/IDA LENDING (12/31/87) (millions of US$):

Annual Averages End Period IBRD IDA1986 1987 Jan-Sept 1988 Sept 1988

Outstanding & Disbursed 2,455.8 99.1US$1.00 = Cr$ 20.4 20.6 21.0 21.2 Undisbursed 804.9 6.7CR$1.00 = US$ 0.049 0.049 0.048 0.047 Outstanding inc.

Undisbursed 3,260.7 105.8

/a Debt Service, net of interest earned on foreign exchange reserves, as a percentage ofExports of Goods and NFS.

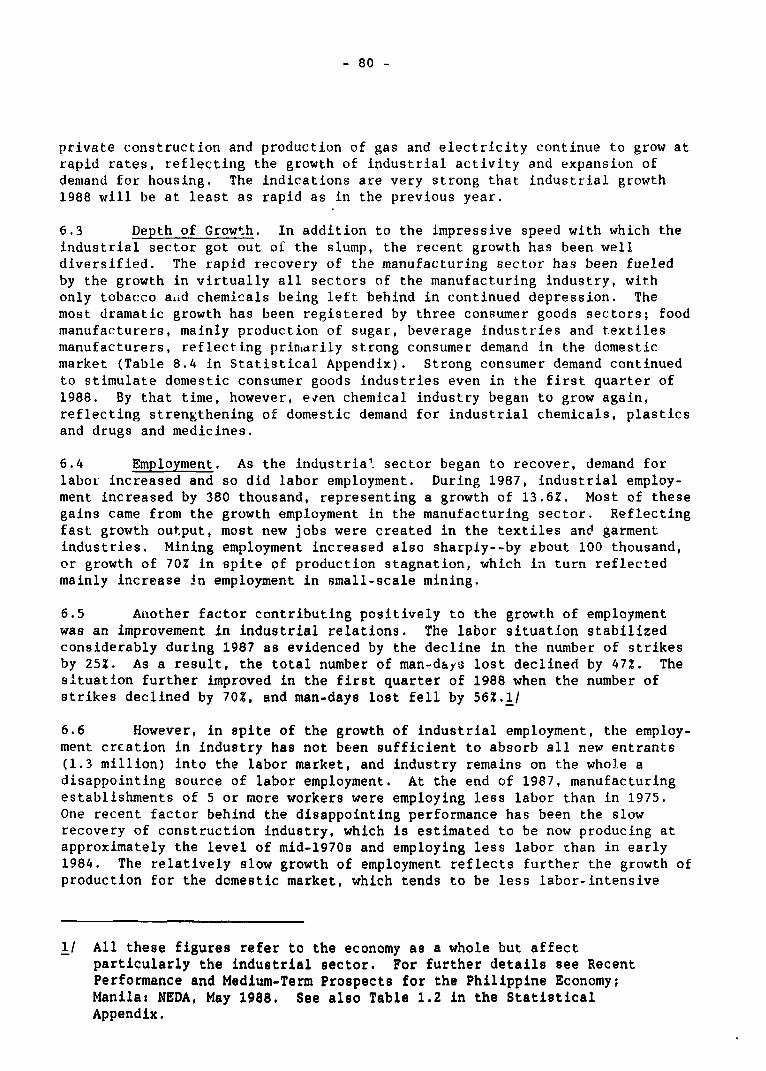

PHILIPPINES: TOWARD SUSTAINING THE ECONOMIC RECOVERY

COUNTRY ECONOMIC MEMORANDUM

Table of Contents

Page No.

PREFACE

EXECUTIVE SUMMARY ...................................................... i-xi

INTRODUCTION ........................................................... 1

Chapter I: Recent Performance and Issues in Macro-Management ....... 3A. Recent Economic Performance ................................ 3

Savings and Investment ..................................... 4Monetary Policy and Interest Rates ......................... 6Reserves and the Exchange Rates ............................ 7The Interface Between Monetary and Exchange

Rate Policies ........................................... 8The Banking Sector ......................................... 9

B. Balance of Payments ........................................ 10The Trade Balance .......................................... 11Merchandise Imports ........................................ 12Terms of Trade ............................................. 13The Balance of Payments .................................... 14Debt Relief ................................................ 15Reserves ................................................... 16

Chapter II: The Public Sector ...................................... 18A. Tax and Revenue Effort ..................................... 18

The Tax Reform Package of 1n86-87 .......................... 20B. Public Expenditure ......................................... 22

Expenditures ............................................... 22Public Debt ................................................ 23Personnel Services ......................................... 24Public Investment .......................................... 25Administrative Improvements ................................ 26Future Public Investment ................................... 27Public Non-Financial Corporations .......................... 29The Public Sector Fiscal Deficit ........................... 32Decentralization and Regional Development .................. 33Conclusion ................................................. 34Annex - The Value Added Tax ................................ 35

Chapter III: Growth Debt and Aid Requirements ...................... 40Background ................................................. 40Constraints on Growth ...................................... 40Growth Scenarios ........................................... 41Capital Flows .............................................. 45Alternative Scena-ios ..................................... 46The Debt Problem ........................................... 47Aid Issues ................................................. 49

Chapter IV: Poverty and Unemployment ............................... 52The Nature of Poverty .................... 52The Causes of Poverty .................... ...... 53Income Distribution ........................................ 57Toward a Poverty Alleviation Strategy ...................... 57Annex - Progress in Land Reform ............................ 61

Chapter V: Agricultural and Natural Resources ...................... 64Recent Performance ................ 64Future Prospects ........................................... 68Credit: REform and Rehabilitation ......................... 69Public Services: Decentralization, Reform and

Redeployment ............................................ 71Natural Resource Management ................................ 74

Chapter VI: Issues in the Industrial Sector ........................... 79A. Industry's Competitiveness ................................. 82B. Industrial Policies ........................................ 87

Omnibus Investment Code .................................... 87Development Programs ....................................... 89Restructuring of Private Firms ............................. 91

C. Trade Policies ............................................. 92External Trade Barriers .................................... 98Participation in the Uruguay Round Negotiation ............. 100

Economic Indicators..................................................... 102

Statistical Appendix................................................... 105

Map i

SUMMARY AND CONCLUSIONS

Recent Progress

In recent years, the Philippines has undergone a traumatic adjustmentprocess, which has fundamentally altered many parts of the economy. The patternof development followed prior to 1983 had resulted in an economy with a dis-torted incentive structure, an inefficient pattern of investment, and a heavydependence on foreign resources. As a result, the ecot.viny did not adjust well

to external shocks, and could not sustain the momentum of development.

Since 1983, and particularly since the change of government in early1986, a series of reforms have been undertaken which have eliminated most ofthe major distortions, and reduced the fundamental imbalances in the foreignaccounts. As a result, the exchange rate has been brought more in line withmarket conditions, interest rates are competitively determined, and a largenumber of import restrictions have been eliminated. Monopolistic marketingarrangements for agricultural outputs and inputs have been eliminated, andexport taxes on agricultural goods abolished. The major government banks,which were often a convenient conduit for easy credit to weak projects, have

been restructured and put on a sound financial and managerial basis. Thepublic investment program has been reduced in scope, and refocused on priorityitems in infrastructure and the social sectors. The tax system has beensimplified and made more efficient and equitable.

As a result of these reforms, and of prudent fiscal and monetarymanagement, the economy has staged a remarkable recovery. The growth rate fGDP, which had been negative in 1984 and 1985, reached 4.7% in 1987 despitepoor performance in agriculture. Growth in 1988 is estimated to have been

about to 6.6%. The balance of payments current account has shown only a smalldeficit in 1987, and public sector deficits have been held to about 3-4% ofGNP, compared to 8-9% in the past. Inflation, which hit 50% in 1984, was lessthan 4% in 1987 and while increasing, is still running on the order of 7-9%.In general, the pattern of recovery, and the focus of reform efforts, has beenconsistent with the expectations of previous Bank reports which focused on theneed for a major economic reorientation and recovery.!/

This report provides an update of progress made in the recovery effort

to date on a variety of fronts. Its particular focus is to provide an overviewof the outstanding problems that remain to be tackled, and the requirements forexternal assistance.

Remaining Problems

The Government needs to be given maximum credit for undertaking a

series of politically difficult reforms in recent years. However, despiterecent progress, the economy is still encumbered by many problems that limitthe sustainability of the recovery effort, and prevent the economy from

/ "The Philippines: An Agenda for Adjustment and Growth," Report No. 5258PH (November 1984) and "The Philippines: A Framework for EconomicRecovery," Report No. 6350 PH (November 1986).

- ii -

sustainability of the recovery effort, and prevent the economy from reachingits full potential. The remaining problems go beyond the simple removal ofcontrols and policies that distort factor and commodity prices, or the disman-tling of inefficient or restrictive government entities. The task bei-ore theGovernment is one of reforming basic institutions and structures, and tacklingfundamental problems, some of which have plagued the growth process fordecades.

The overall goal must be to increase the overall efficiency of theeconomy, i.a agriculture, industry and the publi- sectors, while ensuring thatthe benefits from growth are distributed more 1,jitably within the populationand among regions. The distorted price and investment incentives of the pasthave produced an economy marked by a low level of productivity in many sectors.AS the economy expands, new investments will hopefully respond to a morerational set of incentives which should produce a more efficient pattern ofinvestment, and one that provides for greater output and generates moreemployment. Some additional reforms of the incentive system are r.eeded whichwill help this process. At the same time, the Government is faced with majorchallenges of overall macro-economic management, including a growing publicsector deficit, a heavy external debt burden, and the need to keep realinterest rates within tolerable limits. The high levels of poverty,unemployment, and rapid population growth are concrete obstacles to raisingliving levels and achieving social stability.

Thus, the focus of future Government efforts should be on:

- finding ways to improve the external debt position andrestoring creditworthiness;

- increasing the level and productivity of private investment, aswell as the level of domestic savings;

- increasing the efficiency of the public sector, both in terms ofraising revenues and improving its capacity to provide essentialinfrastructure and services;

- addressing in a meaningful way the deep-seated problems ofpoverty, population growth, and unemployment, including thedevelopment of expanded programs for the social sectors, and aneffective program of family planning; and

- improving efficiency in agriculture and indust.y, both to serveas a basis for exports and for increased labor incomes.

These issues are clearly of concern to the Government. The recentlyissued Updated Development Plan places particular emphasis on decentralizationand regionalization efforts as a means of improving local participation andGovernment effectiveness in the implementation of programs. 2/ In addition,much emphasis is given to expanding social sector programs and land reform as ameans of addressing the poverty problem.

2/ National Economic and Development Authority, "Highlights of the UpdatedPhilippine Development Plan, 1988-89", July 1988.

- iii-

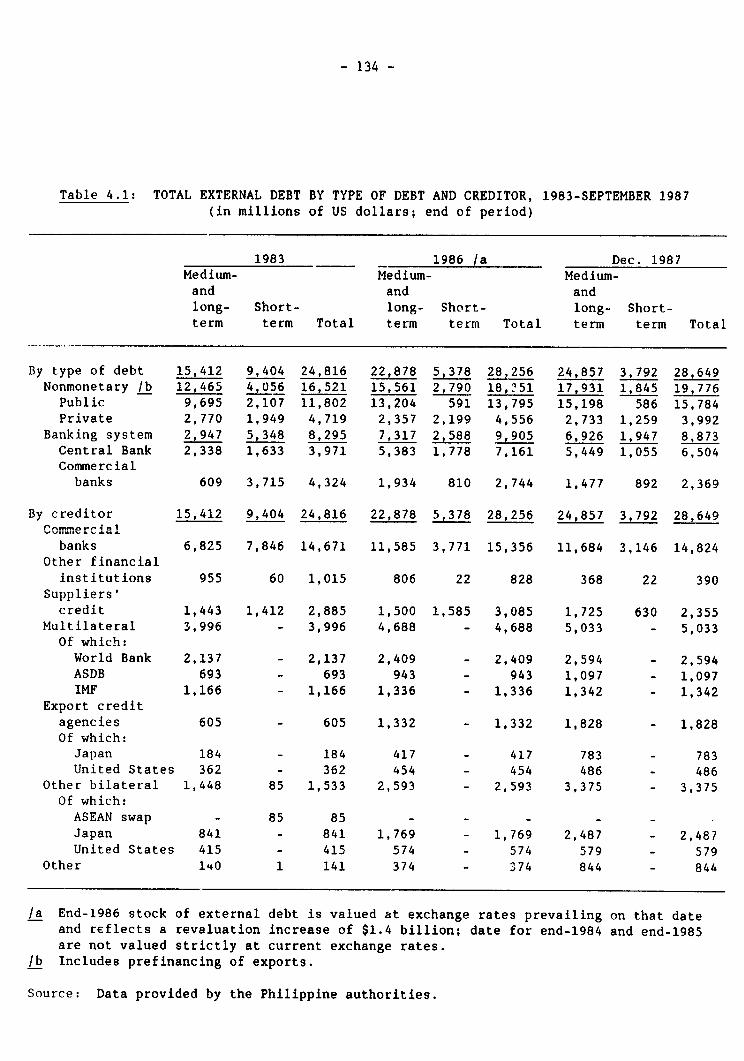

Debt and Creditworthiness

The Philippines is one of the world's most heavily indebted developingcountries with a total debt of over $28 billion. The restoration of credit-worthiness remains a critical goal for the future, if sustainable growth is tobe achieved. While past reschedulings have reduced amortization payments inthe immediate future, they do not represent a permanent solution to theproblem. Interest on the external debt will average about $2.6 billion a yearover the next four years, or about 19% of exports of goods and services. Thetotal debt service ratio is projected to be only about 28% over the sameperiod, largely because most of the payments on private and commercial debthave been rescheduled and fall due during the period after 1992. The countrywill not be creditworthy so long as the external debt problem remainsunresolved, and there are requirements for additional reschedulings and newborrowings.

There is no panacea for the debt problem. At best, growth will reducethevelative burden over time. However, there are a number of steps that car,be taken which can move the country toward a solution.

The Exchange Rate. Rapid growth of output and exports will befundamental to both reducing the relative burden of the debt andproviding the foreign exchange for debt service and criticalimport needs for the recovery. The maintenance of a viableexchange rate will be essential to any attempt to accelerateexport growth. In the past year, the Government reduced reservesand tightened monetary policy in order to discourage capital o, t-flows and thereby support the exchange rate. The result has beena dwindling level of reserves and, at times, an overly tightmonetary policy. Foreign exchange reserves of the Central Bankhave dropped to less than two months of imports. The Governmentneeds to build a more adequate level of reserves and ensure thatthe exchange rate remains competitive, in order to avoid under-mining the recovery.

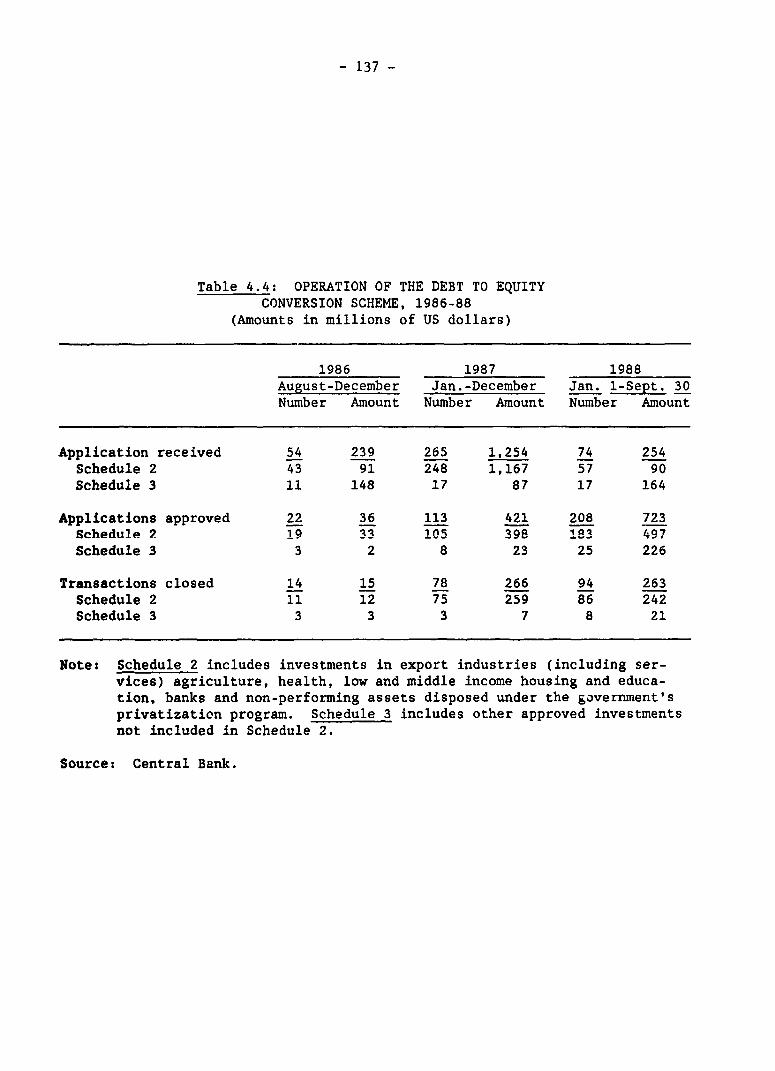

Debt Management. More needs to be done to encourage privatepurchases of debt and transfers to the Philippines, in order totake advantage of the fact that Philippine external debt sells ata discount of 45-50% in the market. The present debt-equityprogram has been limited by the Central Bank because of itsmonetary implications. The Central Bank should investigate theviability of other schemes that could be instrumental in reducingdebt through conversion to some form of domestic financial or realasset, provided the monetary impact can be kept under control.The guidelines for the use of the present debt-equity programshould be clarified.

Investment and Savings

While investment has grown in recent months, the overall investmentrate of the economy is low, about 18% of GNP in 1988. Sustainable real percapita income growth will necessitate an investment rate on the order of 22-25%of GNP, however, even given an improvement in investment efficiency. With a

- iv -

rapidly growing population (2.4% per year), ;2 the need to make up for pastdeclines in per capita consumption, the ability to raise domestic savings islimited. For its part, the public sector tends to run deficits which aregreater than its investment rate, meaning that it is a net dissaver; it isusing private savings to fund public sector investment and part of publicsector consumption. On the other hand, the ability of the private sector tomobilize private savings and direct them through the financial system toinvestors is also weak. The banking L.ector is still recovering from theexcesses and trauma of past events, and remains very cautious. If publicsector deficits remain large, and private sector investment continues to grow,there will be competition for available funds that will cause interest rates torise, limit growth, and crowd out efficient private sector investment. Giventhe current external debt position, however, the country has only limitedaccess to foreign capital to finance investment. For the future, therefore,attention must be paid to certain key areas.

Public Deficit. The public sector deficit must be reduced sothere is a net generation of savings from the public sector. Sinceexpenditures for critical programs will probably have to increase,this means major emphasis must be given to increasing revenues,particularly through improved tax collection and enforcement, andmaking public corporations self-sufficient through better pricingand collection policies.

Long Term Credit. There is a general shortage of long-term creditavailable for industry, particularly for small and medium scalefirms. A strong institution is needed that can tap available lcngterm funds (e.g insurance, social security), and channel these tothe private sector for investment. The Development Bank of thePhilippines has undergone an extensive rehabilitation program andis the most likely candidate for this role. Current programs nowadministered by the Central Bank should be turned over to DBP.

Financial Sector Reforms. A number of taxes and other distortionsthat prevent the financial sector from operating efficiently andtend to reduce savings. The gross receipts tax on banks should beeliminated and restrictions on branch banking relaxed. Interestrates on long term loans from foreign sources need to be set atmarket rates, so that concessional foreign loans do not distortthe structure of local interest rates.

Public Sector Efficiency

Past reforms have made major improvement in public sector effective-ness. A tax reform has unified corporate and personal income taxes, raisedexemption levels to eliminate taxation of the poor, dropped export taxes, andintroduced a value-added tax. As a result of both tax reform and a growth inthe tax base, tax revenues have risen from 10% to 12% of GNP between 1986 and198-/. The introduction of the VAT in 1988 was expected to raise this ratiofurther. However, poor collection and enforcement efforts have resulted in adecline in the tax effort to 11% of GNP. On the expenditure side, maintenanceand operating expenditures have been increased in real terms over the past twoyears, making up for past years of budgetary cuts which had adverse effects on

road maintenance, and the performance of the school and health system.Salaries of government workers have also been increased to compensate for pastinflation. A major effort has Laen made to redesign the public investmentprogram to eliminate projects having low economic rates of return, or which canbe better undertaken by the private sector. A program for the disposal orprivatization of over 200 public corporations has been launched, and improvedcontrols over the remaining public corporations have been established.

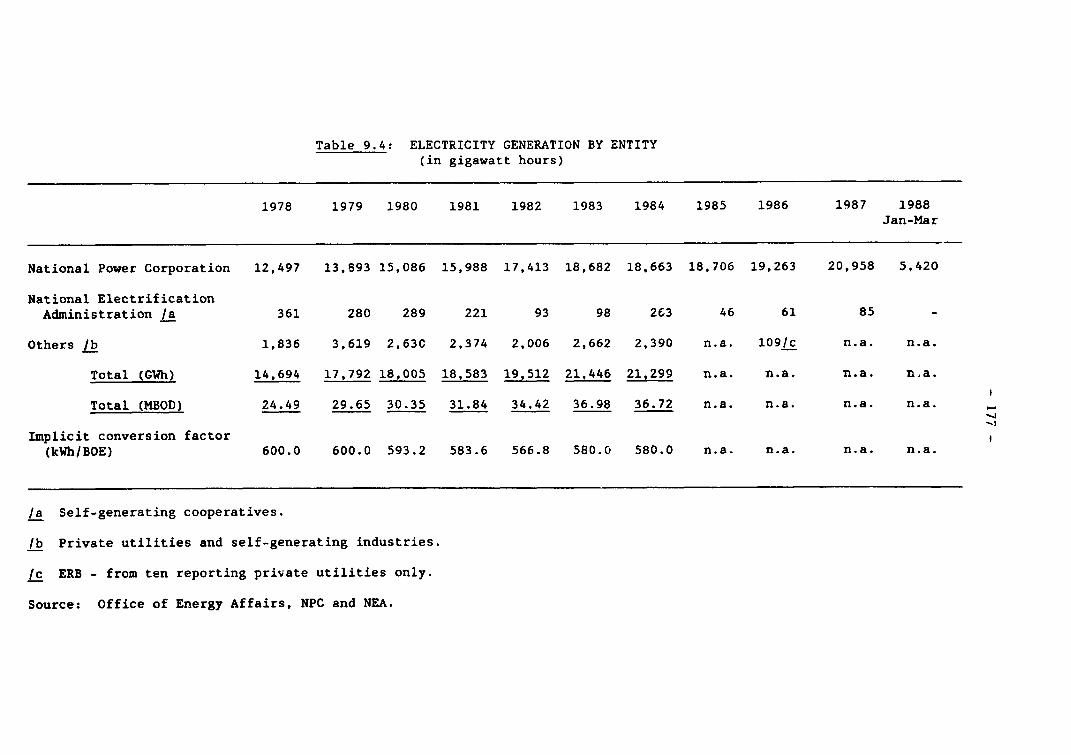

Despite progress on many fronts, many problems remain. These particu-larly affect the level and composition of the public investment program, andthe Government'J implementation capacity. While the Government's Medium-TermPublic Investment Program calls for an average rate of public investment of5.5% of GNP, the actual rate in 1987 was about 3.2%. While steps have beentaken to improve budget, contract and auditing processes, and to provide moreoversight of project implementation, there has been little improvement in per-formance. As a result, the Philippines' ability to utilize its pipeline ofofficial aid is also lagging, and there is growing evidence of imbalances incritical infrastructure that coula affect the pace of the recovery. Electricpower consumption is growing quickly, and outpacing the capacity build-up ofthe National Power Corporation. In part, this reflects the decision not tooperate the nuclear power plant, which would have provided a considerable addi-tion to total capacity. There is an urgent need to bolster rural infrastruc-ture which will reduce poverty and help raise agricultural productivity.

An additional constraint is the large size of the domestic debt. Alarge element in government current expenditures constitutes interest paymentson public debt. Because of the liabilities assumed in the restructuring of thetwo large government banks, public sector debt has increased by 40% since 1985,and now represents the equivalent of 107% of GNP. For the national government,interest payments now constitute over 30% of total expenditures. The highlevel of domestic debt makes the coordination of monetary and fiscal policydifficult. A one percent irc:rease in interest rates will produce a 20%increase in the budget deficit of the national government. Since over 60% ofthe public debt is externally held, the budgetary debt service burden is alsoaffected by changes in exchange rates and foreign interest rates.

For the future, the Government will need to focus on a number ofcritical areas which will improve public sector efficiency:

Tax Reform. The existing tax system could generate much more thanits present level of revenue. Rather than increase tax rates,more attention needs to be devoted to increasing compliance andenforcement. Eventually, the tax system should move away from itshigh reliance on indirect taxes on trade and energy products, andto a higher degree cof direct income taxation. The presentbalance, however, reflects the comparatively better collectionperformance of indirect taxes. A movement away from indirecttaxes will also reduce the regressivity of the present system,wherein the poor pay a higher share of their income in taxes thanthe rich.

Public Investment. Ihe current level of public investment is toolow to sustain the recovery. Efforts need to be made to raise the

- vi -

investment rate closer to the Plan target of 5.5% of GNP, byspeeding up the implementation of existing projects and identifi-cation and preparation of new projects. A strong publicinvestment program will be essential for a rapid utilization ofexisting aid commitments.

Operating and Maintenance Expenditures. While O&M have beenincreased in recent years, the present level is still only about85% of the real level of 1982. Increases are particularly neededin the social sectors, to provide reliable and effective programsin health, education and nutritiox.

Public Corporations. The operating efficiency of public corpora-tionts is low in many cases, resulting in high cost public servicesin critical areas (power, water supply). These, in turn, raisecosts and reduce competitiveness of industrial and agriculturaloutput. Further steps need to be taken to improve collectionperformance, reduce technical losses, and restructure prices toeliminate cross-subsidies and other distortions.

Decentralization. Efforts have been made to decentralize centralgovernment functions to the regions, in an attempt to make govern-ment more responsive to local needs, and to increase the power ofthe regions over the planning and control of programs. Controlover most resources still rests with the center, however, andlittle effective power has devolved to the regions. While theGovernment needs to move forward with its decentralization/regionalization efforts, progress may be limited by the ability ofmany local governments to assume greater responsibility. Programsneed to be developed that build staff administrative capacity atthe local level, and improve local tax collection efforts.

Poverty and Unemplovment3/

The Philippines continues to be a country with a substantial amount ofpoverty, and high levels of under- and unemployment. At the same time, popula-tion growth remains high (2.4% per year). As the population grows, the pres-sure on rural land mounts, and poor farm families migrate to new upland loca-tions or to the cities, in an attempt to find more remunerative occupations.The result is both a rising level of underemployment in urban centers, and adeterioration of upland forests, as migrants settle land unsuitable for conven-tional farming techniques. The failure of modern sector employment to grow inrecent years reflects the bias of the past incentive system which favoredcapital-intensive, import substituting industries, and the general slow growthof the economy in recent years.

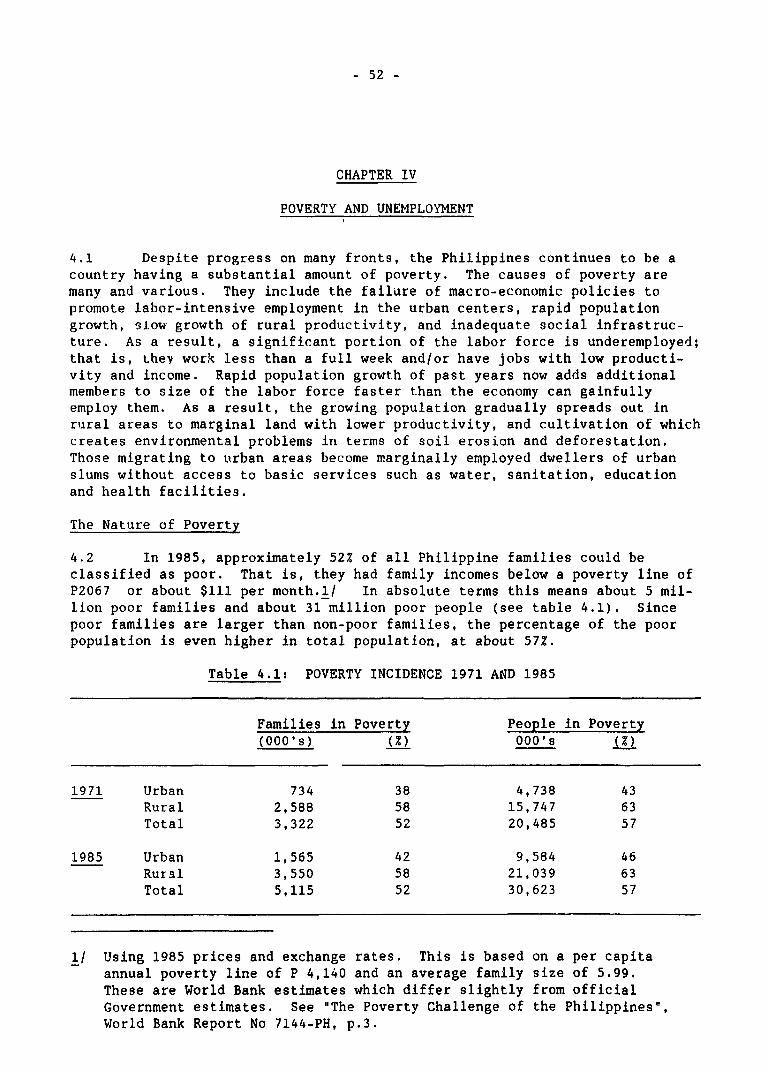

While estimates of poverty are necessarily fragile, in general about52% of all families in the Philippines were classified as "poor" in 1985. Thisis about the same level as that prevailing in 1971. During the interveningyears, it appears that poverty was reduced during the high growth years of the

3/ A fuller treatment of this subject is contained in "Philippines: TheChallenge of Poverty." Report No. 7144-PH (September 1988).

- vii -

1970s, but then increased during the recession and adjustment years up to 1985.Income distribution remains highly skewed; the top 10% of the population has anaverage income 15 times that of the lower 10%. On top of this, there has beena very rapid growth of the labor force. Since 1980, the labor force has grownat an average rate of 4.5% per year. The result has been downward pressure onreal wages and a falling level of output per worker.

While growth is necessary to provide the economic progress so essen-tial to maintaining stability, it is not by itself sufficient. The structureof growth must be oriented to reducing poverty and increasing employment; thebenefits of growth must be spread widely through the population and geograph-ically throughout the country. While reducing poverty is a long term goal, abeginning must be made as soon as possible. Areas of focus include:

Land Reform. Land reform is a high priority, because of itsequity and social stability effects. The recently signed Compre-hensive Agrarian Reform Program (CARP) extends the existing landreform program to crops other than rice and corn, which werecovered under the 1972 legislation. The Government has alreadybegun to expedite transfers in rice and corn areas; it needs tomove faster on other categories of land, including lands whichhave been taken over by foreclose and abandonment, and publiclands in upland areas. The new legislation holds out the promiseof a major change in economic relationships in tha countryside.The Government needs to move quickly to organize itself to carryout the program, which is a massive undertaking.

Pogulation/Family Planning. Rapid growth of population is clearlyoutstripping the country's natural resource base and ability toprovide productive employment. Poor families lack access tofamily planning services, and have higher fertility rates than thegeneral population. Existing programs in family planning need tobe expanded, the level of expenditures significantly increased,and the delivery of services made more effective, and integratedwith health care and nutrition services.

Rural Development. The infrastructure needs in the rural areasshould be expanded. Of particular importance are the developmentof rural roads, rural electrification, and agricultural credit andextension services that reach poor and smaller farmers.

Social Services. Programs in the social sectors need to beaugmented, made more effective and targetted on the poor, andhigh-risk groups within the poor. Health care particularly needsto be expanded in rural areas, integrated with nutrition services,and emphasize preventative as well as curative care. Feestructures need to be adjusted so that the non-poor pay themarginal cost of providing services, reducing the overall cost ofthe program and permitting free services for the poor. In educa-tion, the quality of education in poor and rural areas is low, anddropout rates are high. Steps need to be taken to increase expen-ditures for supplies and teacher training in schools in poor andrural areas.

- viii -

Agriculture

Since 1980, there has been a genieral decline in the growth of agricul-tural productivity. The fertilizer-seed-irrigation technology innovations ofthe 1970s allowed for a rapid growth in rice and corn output. By 1982, thegains from this technology began to be exhausted, and since then total agricul-tural growth has averaged only 1.8% per year, less than population growth.Part of this low growth was due to very adverse weather conditions. However,yields in traditional crops remain low even with good weather, and there is aneed to diversify wherever profitable into minor crops that have betterprospects. In the past few years, the growth of crops such as shrimp andprawns, bananas, coffee, rubber and vegetables has been strong. Governmentresearch efforts, however, have largely concentrated on traditional crops,particularly rice. Another factor affecting farmer productivity is the shortageof agricultural credit, particularly for small farmers. The formal marketsupplies only about one third of the credit needs of the sector, with the restcoming from the informal system (commercial middlemen, landlords, friends,moneylenders). Poor farmers generally lack access to any kind of credit,particularly if they do not have title to their land.

Agricultural productivity is also affected by the gradual deteriora-tion of soil and forest resources, as a result of rapid population growth inupland areas, and weak public sector management. Shifting cultivation inupland areas and poor soil management techniques leads to erosion which reducesfarm productivity and causes siltation of streams, rivers and coral reefs,which also affects the productivity of coastal fishermen. Poor management offorest resources has resulted in over extraction of prime species withoutadequate replanting for future production.

During the past year, the Government has made a major effort to reor-ganize and decentralize agricultural services. Nevertheless, governmentservices remain fragmented over a variety of organizations, many of which donot come under the Department of Agriculture. In addition, government servicestend to be stronger in the lowland areas, and very sparse in upland areasinhabited by the poorer farmers. For the future, programs in agriculture willneed to focus on:

Agricultural Credit. The Government is presently engaged in aprogram to revitalize the rural banking system, which will helpraise the level of formal credit in the sector. There are anumber of regulatory steps that need to be taken to induce morecompetition in rural credit. These include the elimination of therequirement that rural banks retain 75% of their deposits in thearea received; the elimination of the required lending foragriculture and agrarian reform (Agri/Agra); and a more liberalpolicy allowing branch banking in rural areas.

Research! Extension. There is a general need to diversify theresearch effort, and to strengthen the extension service. Whilethe existing service is large relative to the farm population, itis relatively ineffective. The Government needs Lo raise salariesof extension workers, increase limited operating funds, increasetraining of extension workers and establish clear priorities fortheir work.

- ix -

Resource Management. The Government needs to intensify itsmanagement of protected areas; parks, watersheds, wildernessareas, etc. For the rest, incentives should be put in place forbetter local and/or private management. This would includeproviding secure tenure for upland farmers in the form of titleswith conservation-oriented land use restrictions, recognizingcollective land tenure rights, and the organization of commonproperty management schemes at the community level. A majordistortion that should be corrected ic the low prices set by theGovernment for resource extraction, particularly timber. Loggingconcessionaires now pay about 50% of potential economic rent infees, and formerly paid only 10%. Fees based on total volumeremoved also contributes to selective cutting of high valuespecies and large amounts of waste left on the forest floor.

Industry

Rapid growth in the industrial sector is essential for substantialgrowth in the economy, and significant urban employment creation. ThePhilippiiLes is well-positioned to begin a period of significant industrialgrowth for a number oL reasons. It has a large, well-educated and skilledEnglish-speaking labor force, and a large group of modern entrepreneurs whichcan organize and manage industrial activities. Wages are relatively lowcompared to other East Asian countries, and labor-intensive industries movingfrom Japan and other countries should find the Philippines an attractive alter-native. Recent Government actions have liberalized trade, and reducedGovernment interventions in the sector. A new Omnibus Investment Code hasclarified the system of incentives, which are comparable to those of otherASEAN countries. The tax reform has lowered the corporate tax rate to 35%,which is also on a par with other countries. Labor productivity, however, isalso low which offsets the advantages of low wages. Past investments wereoften undertaken under a regime of high protection, and are consequently not ata scale that can compete internationally. In addition, the lack of new invest-ment in recent years means that much of existing industrial capacity is tech-nologically out of date and needs to be replaced. Industrial restructuring isalso needed because of financial reasons; firms often carry an excessive levelof debt which makes it impossible to borrow for productivity enhancing improve-ments. Industrial efficiency is also limited by weak infrastructure, and inef-ficiencies in the delivery of public and publicly regulated services, includingwater, power an' telecommunications. The key areas for improvement are:

Infrastructure. Shortages of power are becoming a major impedi-ment to rapid industrial growth. In addition, electricity pricestend to be extremely high compared with other countries. In partthis is due to system inefficiencies and a policy of cross-subsi-dization which provides households with electricity below cost, atthe expense of industrial users. High distribution losses, and

low collection rates, also add to the costs of paying customers.The Government needs to move ahead with its plans to revise powertariffs and to improve the operating efficiencies of the NationalPower Corporation and Meralco. More investment should be madefor supporting infrastructure, particularly in rural areas. Thisincludes particularly reliable power supplies, adequate road and

- x -

port infrastructure. Deregulation of inter-island shipping, andrationalization of port charges, should be undertaken in order toreduce shipping costs internally.

Trade Policy. Significant progress has been made in recent yearsin reducing the level of quantitative import restrictions. Thisprocess needs to be sustained, and combined with a review oftariff protection. The remaining quantitative restrictions shouldbe removed and replaced by tariffs, which would give theGovernment the revenue benefits of protection. In general, thereshould be an attempt to make effective protection more evenbetween industries. However, future trade reforms need to beconsidered within a program of industrial restructuring thatconsiders all the problems facing the industry, and providesadequate time for industries to undertake necessary adjustments.

Foreign Investment. For foreign investors, the new OmnibusInvestment Code provides a system of incentives which are compar-able to other ASEAN countries. However, the requirement that non-export industries can only be 40% foreign owned is more restric-tive than requirements in other countries, and discourages invest-ment in many sectors. This limit should be raised to allow major-ity control with gradual reduction over time to minority control.The existing debt-equity conversion scheme was designed to attractforeign investment, but the need to limit monetary expansion hasforced the Central Bank to impose administrative restrictions onits use. The present arrangement, therefore, actually impedesprivate investment, since investors queue up, hoping to transferinvestment funds through the scheme rather than proceeding withtheir projects. The operation of the scheme should be made moretransparent and procedures for its use clarified, so that it doesnot become a disincentive to investors.

Growth Prospects and Aid Reguirements

The Bank's projection of future growth is based on an assumption of acontinuation of good policy performance, and assumes an average growth rate of5.9% per annum during the 1988-92 period, based on a 3.5% growth rate foragriculture and 8% for industry. Under these assumptions, the average invest-ment rate would be about 22%, and the current account deficit would average2.8% of GNP. By comparison, the Government's revised plan calls for an averagegrowth rate of 6.5%, an investment rate of 21%, and a current account deficitequal to 2.6% of GNP for the same period.

Under the Bank's projection, the total external debt would rise from$29 billion at the end of 1988 to $34 billion by the end of 1992, but relativegrowth of the debt would be less than GNP growth. Thus, the ratio of debt toGNP would fall from 71% in 1988 to 56% by the end of 1992, and the debt serviceratio would average 28% during the period. The projection assumes, however, alevel of capital inflow from official source of about $1.5 billion per yearduring the period. At this level, there remains a gap to be filled by newmoney from official and private sources of $4.1 billion, or about $1.0 billionper year. Without this additional inflow, it is estimated that the growth rate

- xi -

of the economy would fall from the original estimate of 5.9% to an average ofabout 4%. Because domestic savings would have to increase to finance invest-ment requirements, there would be little scope for consumption increase, and inper capita terms consumption levels would fall.

Conclusion

The Philippines has made considerable progress in recent years inrestructuring its economy and eliminating distortions and abuses. Among thehighly indebted countries, its record is one of the best. The Governmentshould be given full credit for undertaking many difficult reforms. Despitethe considerable progress made so far, there remain many impediments tosustained, long term growth. The external debt burden represents a continuingproblem and a significant drag on the economy. Inefficiencies in industry andagriculture lower output potential, worker productivity and growth. Povertyand unemployment remain critical problems. Public sector revenue performanceis problematic, and as result, the public sector is unable to provide adequateservices to support the recovery or address the poverty problem. It iscritical, therefore, that the Government move forward with a new agenda ofreforms that deals with fundamental structural and institutional issues thataffect the overall efficiency of the economy. At the same time, it must resistpressures to backslide on actions already taken to reduce trade and pricedistortions. Future growth will be sustainable only if it is based on anefficient use of resources, and provides for an equitable distribution ofbenefits within the country.

- 1 -

PHILIPPINES

COUNTRY ECONOMIC MEMORANDUM: TOWARD SUSTAINING THE ECONOMIC RECOVERY

Introduction

1. The Philippines has experienced a remarkable turnaround in economicperformance during the past two years. After a period of declining outputduring 1983-85, output grew by 5Z in 1987, and by over 6Z in 1988.Furthermore, there has been a fundamental restructuring of many institutionsand removal of distortions which limited growth in the past. It seemspossible that the Philippines is on the verge of a period of rapid andsustained growth, based on an economy that has undergone some fundamentalrestructuring during the past few years.

2. Since February, 1986, an impressive number of reforms which have beenput in place, which when combined with those undertaken since 1983, provide anew orientation to the economy. These reforms have reduced or eliminated anumber of distortions in commodity and factor markets, and/or reduced thelevel of public sector control over the economy. Specifically.

- a major tax reform has been introduced, including a value-added tax;- monopolistic marketing arrangements have been eliminated for coconut

products and sugar;- import controls have been reduced or eliminated on a wide variety of

industrial raw materials and capital goods;- price controls and export taxes on agricultural products have been

eliminated;- the two largest government financial institutions, which were

previously bankrupt, have been reorganized, restructured, and reducedin scope;

- the exchange rate remains determined by market conditions, anreflects the opportunity cost of foreign exchange;

- interest rates are market determined;- the public investment program has been restructured, reduced in

scope, and focused on high priority projects designed to provideessential infrastructure;

- a significant number of assets taken over from the two banks havebeen sold, as have a number of taken-over commercial banks;

- the Government has commenced a program for the privatization of over100 public corporations, and has created mechanisms to bring theremaining under better control.

3. These structural changes in the economy have contributed to the paceof economic recovery by reducing price and resource distortions, lowering thegovernment budget deficit, and eliminating much unnecessary governmentintervention in the economy. While much has been done, there remain severalimportant issues yet to be tackled. The issue is not entirely one of "gettingthe prices right," although there are still a number of items that should beaddressed in this area, including further reforms of the trade system andagriculture. With the current system of incentives there is every reason to

- 2-

believe that future growth will be more export-oriented, more labor-intensiveand more efficient than the past. The Government must guard against back-tracking on past reforms, including giving in to special interests that seekprotective barriers, subsidized credit, or the reestablishment of monopolistictrading positions.

4. Overall, the focus must now shift to issues of the management ofeconomy. With adjustment by and large accor ished, attention should shiftfrom short term adjustment policies to the deep-seated structural issues thatare more complex and difficult to resolve.

S. Of prime importance is the issue of general macro-economicmanagement, to insure that the recovery continues into the future at a stablepace, without the recurrence of excessive inflation. Restoring productivegrowth in agriculture and industry remains a substantial challenge. The issueof the outstanding debt, and the need to have adequate access to foreigncredits will continue to be an issue for some time. Finally, the longer-termissues of poverty, population growth and unemployment continue to plague theeconomy, and must be resolved if growti is to be achieved without beingarrested by social and political instability.

6. While the government remains the focal point of actions that willshape future growth, it faces serious impediments. As a new democracy, thereare the inevitable growing pains associated wit1a executive-legislative branchtussles and inter-departmental frictions. What makes these activities socostly, is the absolute necessity for the Philippines to make up lost ground.In this context, lapses between intentions and plans on the one hand andactual implementation on the other are an important issue, impinging on suchdiverse activities as tax collection, investment plans, or industrialregulation. In part, the Government has already recognized these problems andis taking steps. Recent actions to raise government wages and salaries willimprove the level of the civil service, even though they merely restore realwages to 1987 levels. Plans are being made to decentralize Governmentprograms to the regions, in order to make Government more responsive to localneeds. The Updated Plan emphasizes the decentralization of budgetaryfunctions to local government units, and the increased participation of localunits in the implementation of programs and policies. Nevertheless, the issueremains serious, particularly since there is a danger of raising falseexpectations if the Government cannot deliver on announced programs andpolicies.

7. This report is designed to provide a review of the economic recoveryas well as the longer term structural problems that remain. The first threechapters discuss current issues in resource management and monetary policies,public finance, the balance of payments, growth prospects and aidrequirements. The balance of the report looks at the longer-term structuralissues in industry and agriculture, along with the issues in poverty,employment and natural resource management.

CHAPTER I

Recent Performance and Issues in Macro-management

A. Recent Economic Performance

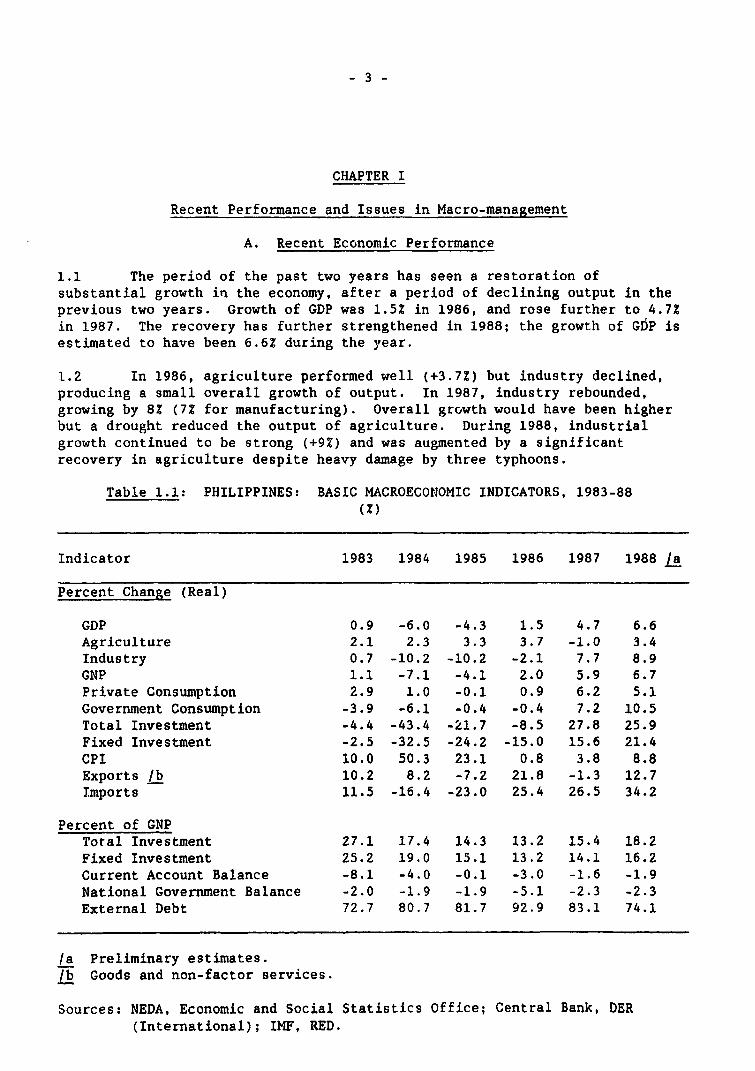

1.1 The period of the past two years has seen a restoration ofsubstantial growth in the economy, after a period of declining output in theprevious two years. Growth of GDP was 1.52 in 1986, and rose further to 4.7Zin 1987. The recovery has further strengthened in 1988; the growth of GDP isestimated to have been 6.6Z during the year.

1.2 In 1986, agriculture performed well (+3.7Z) but industry declined,producing a small overall growth of output. In 1987, industry rebounded,growing by 8Z (72 for manufacturing). Overall growth would have been higherbut a drought reduced the output of agriculture. During 1988, industrialgrowth continued to be strong (+9Z) and was augmented by a significantrecovery in agriculture despite heavy damage by three typhoons.

Table 1.1: PHILIPPINES: BASIC MACROECONOMIC INDICATORS, 1983-88(Z)

Indicator 1983 1984 1985 1986 1987 1988 /a

Percent Change (Real)

GDP 0.9 -6.0 -4.3 1.5 4.7 6.6Agriculture 2.1 2.3 3.3 3.7 -1.0 3.4Industry 0.7 -10.2 -10.2 -2.1 7.7 8.9GNP 1.1 -7.1 -4.1 2.0 5.9 6.7Private Consumption 2.9 1.0 -0.1 0.9 6.2 5.1Government Consumption -3.9 -6.1 -0.4 -0.4 7.2 10.5Total Investment -4.4 -43.4 -21.7 -8.5 27.8 25.9Fixed Investment -2.5 -32.5 -24.2 -15.0 15.6 21.4CPI 10.0 50.3 23.1 0.8 3.8 8.8Exports lb 10.2 8.2 -7.2 21.8 -1.3 12.7Imports 11.5 -16.4 -23.0 25.4 26.5 34.2

Percent of GNPTotal Investment 27.1 17.4 14.3 13.2 15.4 18.2Fixed Investment 25.2 19.0 15.1 13.2 14.1 16.2Current Account Balance -8.1 -4.0 -0.1 -3.0 -1.6 -1.9National Government Balance -2.0 -1.9 -1.9 -5.1 -2.3 -2.3External Debt 72.7 80.7 81.7 92.9 83.1 74.1

/a Preliminary estimates.lb Goods and non-factor services.

Sources: NEDA, Economic and Social Statistics Office; Central Bank, DER(International); IMF, RED.

-4-

1.3 During the period, tight monetary and fiscal policies, and decliningoil prices, have helped keep inflation under control. Consumer pricesincreased on average only .8X in 1986 and 3.8Z In 1987. During 1988 the ratehas accelerated somewhat to about 9Z, although this may reflect such factorsas the introduction of the value added tax in January 1988, and the drought in1987 which raised prices of agricultural commodities. Another factor has beenthe increases required in government wages in 1987 and 1988 to offset theerosion caused by inflation in the past, and to make public sector wagescompetitive with the private sector. In addition, minimum wage levels for theprivate sector were raised by about 18% in December 1987, although it is notclear how much this affected overall wage levels.

1.4 While the recovery has been characterized as "consumption led," infact investment growth has been strong, and more rapid than consumptiongrowth. Private consumption increased by 6% in 1987 and an estimated 5% in1988. Public consumption rose even faster, growing at 72 and 11% in 1987 and1988, respectively. This rapid growth reflects increased public sector wagesas well as greater allocations for necessary operating and maintenanceexpenditures. Investment, on the other hand, rose by 28% in 1987 and 26% in1988. Nevertheless, investment remains low; fixed investment was 15% of GNPin 1987 and 18% in 1988. The low levels of current investment reflect boththe decline in aggregate demand in recent years, and the accumulation of astock of existing capital, much of which is underutilized. With excesscapacity in many industries, it is logical that investment will remain lowuntil excess capacity is eliminated. Those industries, such as foodprocessing, which suffered least during the recent recession, are already ator over full capacity and are undertaking new investments. The fact that thePhilippines can grow with a low level of investment allows this growth to betranslated into increased consumption levels. Even with this recovery,however, per capita personal consumption in 1987 in real terms was 3% lowerthan it was in 1983. Translated using current exchange rates, per capitaconsumption is about $435 per person per year.

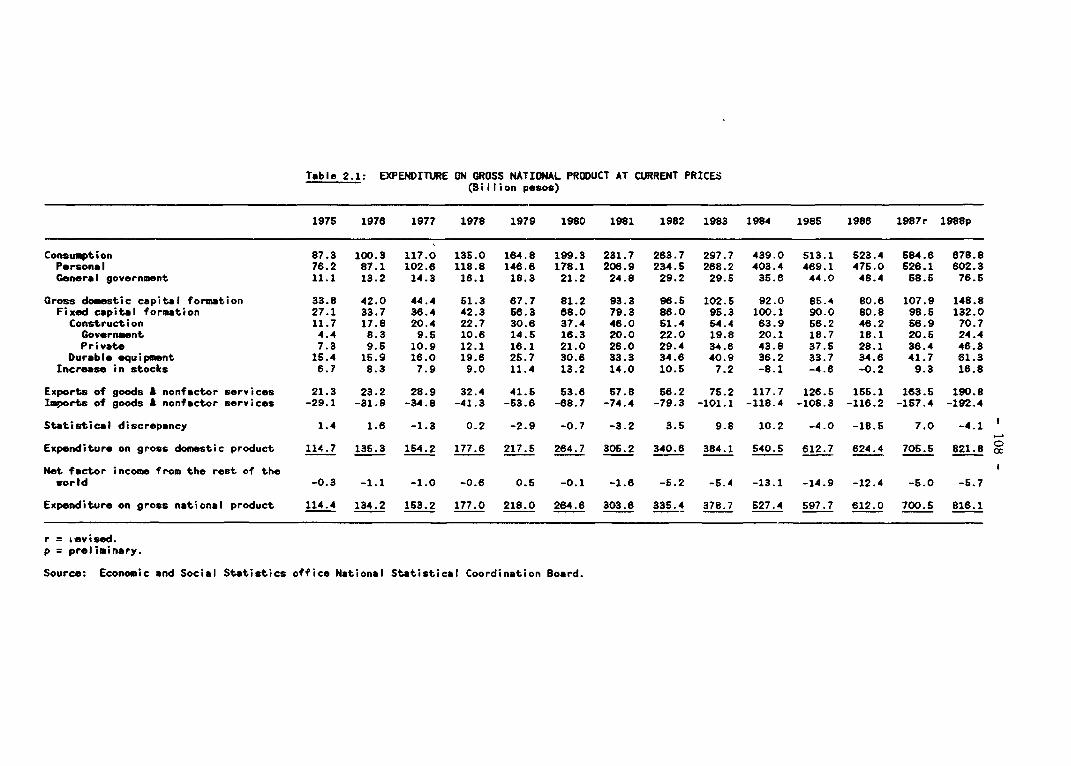

Savings and Investment

1.5 While the country has enjoyed rapid growth despite low investmentrates, once excess capacities are fully exhausted it will be necessary toraise the investment rate to a level sufficient to maintain the planned rateof growth. To sustain future growth of 6% will require an overall investmentrate of 22-25% of GNP. To raise the overall investment rate to this level,however, will require a substantial increase in domestic savings, since only asmall part of this investment could be expected to be financed through thebalance of payments.

- 5 -

Table 1.2: SAVINGS AND INVESTMENT, 1983-88(Z of GNP)

19881983 1984 1985 1986 1987 (est.)

National GovernmentSavings 0.5 -0.8 -0.3 -3.2 -1.0 -1.3Investment 2.5 1.1 1.5 1.9 1.8 1.8Net Balance -2.0 -1.9 -1.9 -5.1 -2.8 -3.1

Corporations /aSavings -0.9 0.9 0.6 0.0 0.7 0.7Investment 3.3 3.0 1.9 1.1 1.2 1.3Net Balance -4.2 -2 1 -1.3 -1.1 -0.5 -0.6

Total Public Sector /bSavings -2.8 -3.7 -2.2 -2.5 0.4 -1.3Investment 6.2 4.5 3.7 3.1 3.2 3.2Net Balance -9.0 -8.2 -5.9 -5.4" -2.8 '-4.5

Private SectorSavings 19.9 18.8 17.2 18.2 13.4 17.6Investment 19.0 14.6 11.4 9.8 12.2 15.0Net Balance 0.9 4.2 5.8 8.4 1.2 2.6

Current Account Balance -8.1 -4.0 -0.1 <.0 -1.6 -1.9

/a Covers 14 major public sector corporations./b Includes local governments, social security, and government financial

institutions, including the Central Bank.

Source: NEDA, Central Bank and staff estimates.

1.6 Raising the savings rate may be difficult, particularly in light ofthe need to undo past declines in private consumption and provide for somereal improvement in living levels. In the past, and despite the recession,the private sector has had a substantial savings rate. During the 1983-87period, private sector savings averaged about 17.5% of GNP (see Table 1.2).The public sector, however, was a net dissaver, with an average rate of -6.32.At the same time, public sectcr investment averaged only 4.1Z of GNP, so thatthe public sector was tapping private savings to finance public consumption.Preliminary estimates indicate that these trends continued into 1988, withprivate savings rising to 17.6% of GNP, but private investment equal to only15Z. This strategy may have made sense during the recession years, whenagareaate demand was falling, the private sector was reluctant to invest, anda pubiic sector stimulus was LequiEed. With the reLovery now in progress,however, there will be substantial competition between the public and pri7atesectors for investment funds. Unless the public sector does a better job of

- 6 -

mobilizing its own resources the competition for investible funds will resultin high interest rates, a crowding out of the private sector, and a constrainton future private sector investments.

1.7 In fact, between 1983 and 1987 there has been substantial progress inreducing the overall public sector deficit from 9Z of GNP to 3.22; in 1987 thedeficit was smaller than public sector investment for the first time in fouryears. The major factor behind the smaller deficit was a substantial increasein the tax ratio and lower than planned investment expenditures. The taxeffort in 1987 rose nearly 2 percentage points to 12.2Z of GNP as a result ofbcth the 1986 tax reform package and an expansion of the tax base, particu-larly imports. In 1988, however, the public sector deficit appears to haverisen to 4.5? of GNP, and the tax effort declined to 11? of GNP.

Monetary Policy and Interest Rates

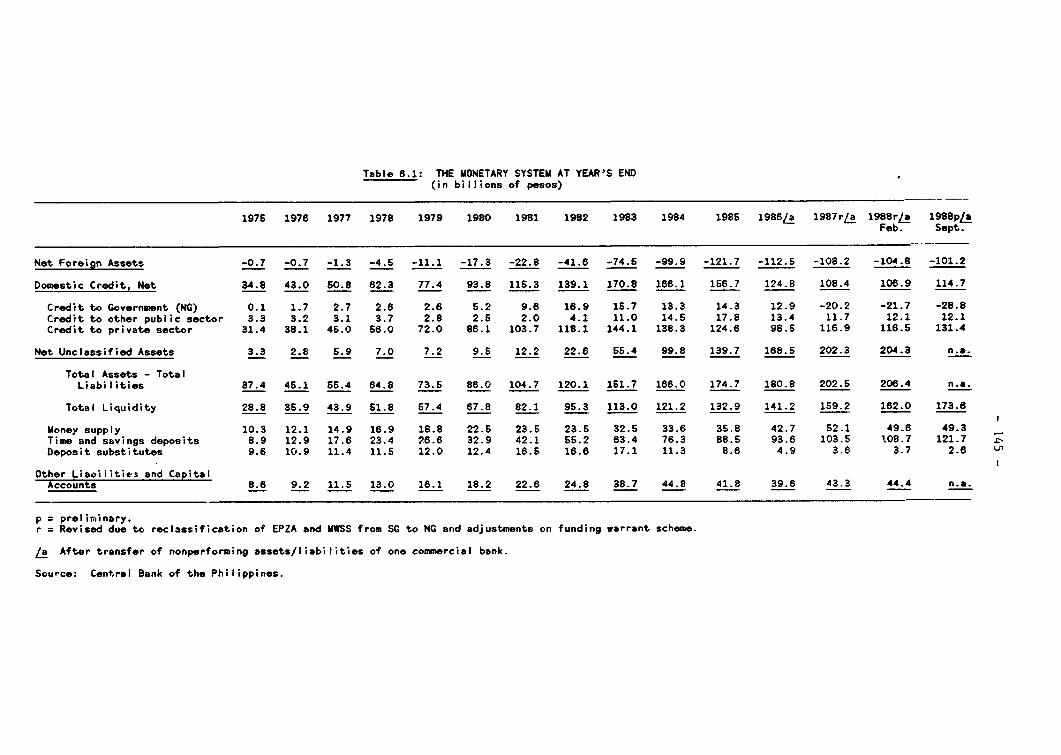

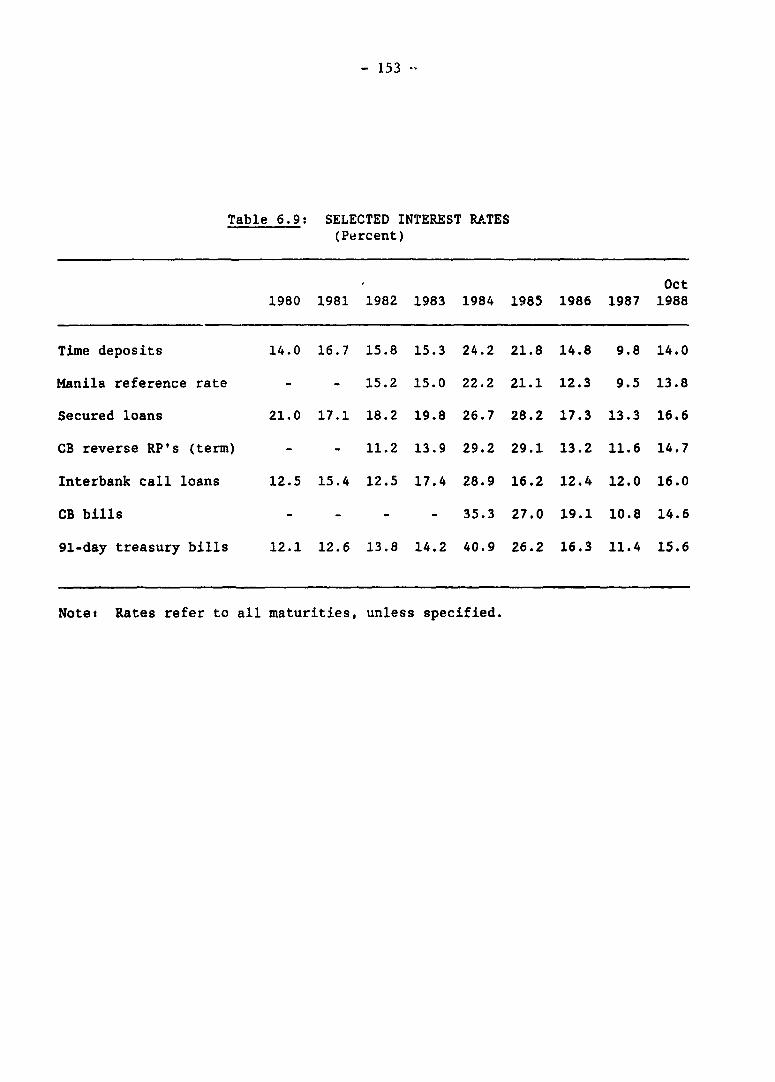

1.8 Monetary policy has been conducted cautiously, with the money supply(M3) growing by 12? in both 1986 and 1987. Political uncertainties andinstability have made monetary management difficult in recent years. Thesefactors have resulted in the public preferring to hold cash and governmentsecurities to bank deposits. Thus, the currency-deposit ratio at the end of1987 reached a historical high level of 272 (see Table 1.3). The presentincrease in inflationary pressures may reflect a return to more normal condi-tions, and an attempt by the public to decrease cash holdings. InOctober 1986, the monetary authorities suspended the sale of new central bankbills and the National Government deficit was covered by issuing treasurysecurities. The emergence of these close substitutes for quasi-money holdingsis related to the relatively slow rate of growth of deposits (9.92 in 1987),as government securities substitute for bank deposits.

Table 1.3: MONEY SUPPLY AND INTEREST RATES

1983 1984 1985 1986 1987 1988(Sept.)

Money Supply (P Billion)M3 113.0 121.2 132.9 149.3 167.3 184.8Currency 19.6 21.8 24.1 29.3 35.4 31.8Deposits 93.4 99.4 108.8 120.0 1 1.9 153.1

Currency-Deposit Ratio (Z) 21.0 21.9 22.2 24.4 27.0 20.8

Interest Rates (2)Time deposits 15.3 24.2 21.8 14.8 9.8 13.2 /aAverage lending rate 19.3 26.7 28.2 17.3 13.3 15.8 /a91-day treasury bills 14.2 40.9 26.2 16.3 11.4 15.7 /a

Inflation 10.0 50.3 23.1 0.8 3.8 8.8

/a December 1988.

Source: Philippine authorities.

1.9 There has been an overall trend to bring interest rates down in thepast three years, from the very high levels reached during 1984. Thus, the 91day Treaeury bill rate has dropped from an average of 412 during 1984 to 11.42in 1987. In real terms, however, interest rates have actually risen, sinceinflation rates exceeded interest rates during 1984. Real rates were particu-larly high in 1986, when inflation rates dropped swiftly and nominal lendingrates remained high. In 1988, however, while nominal rates have risen, realrates have declined. The prevalence of high real interest rates reflects manyfactors, including the large stock of government debt within the system.

Reserves and the Exchango Rate

1.10 A major factor in monetary policy has been the perceived need tomaintain a stable exchange rate, in order to prevent speculative swings in therate and inflationary pressures. After the August 1987 coup attempt, theCentral Bank supported the peso, and in the process gross reserves fell by$500 million during the year. This was offset by an increase in commercialbank holdings of foreign exchange, in part because commercial banks wanted toreduce net foreign exchange exposure. Commercial banks still have net liabil-ities on their foreign accounts, but have reduced their net foreign exposure(see Table 1.4). The Central Bank tightened interest rates in early 1988 inan attempt to make foreign exchange holdings unattractive, decreasespeculative pressure against the peso, and to prevent capital flight abroad.At the same time, it was a net seller of foreign exchange. While foreignexchange sales were halted by mid-1988, these continued to be a gradualdecline in official reserves. By the end of October 1988, gross officialreserves had fallen to $1.5 billion, but then recovered to close at $2.0billion for the year.

Table 1.4: INTERNATIONAL RESERVES OF THE BANKING SYSTEM($ Million, End Period)

1983 1984 1985 1986 198' 1988

Central BankNet reserves -1,825 -1,810 -1,836 -914 -726 -505Gross reserves 865 886 1,061 2,459 1,959 2,059Gross reserve ratio /a 0.9 1.1 1.5 3.7 2.3 2.0Liabilities 2,690 2,696 2,897 3,373 2,685 2,564

Commercial BanksNet reserves -1,871 -2,440 -1,423 -1,103 -1,026 -302Gross reserves 1.655 1,837 1,915 1,986 2,464 2,083Liabilities 4,526 4,277 3,338 3,089 3,490 3,284

Banking SystemNet reserves -4,696 -4,250 -3,259 -2,017 -1,753 -806Gross reserves 2,520 2,723 2,976 4,445 4,423 4,142Liabilities 7,216 6,973 6,235 6,462 6,176 5,848

/a In terms of months of imports, goods and services.

- 8 -

1.11 In nominal terms, the exchange rate has moved from an average of18.6 pesos per $ during 1985 to 20.6 during 1987; the average for 1988 was21.1. In real terms, the rate has kept pace with international and domesticinflation, although without according Philippine exports any increase inoverall competitiveness. As shown in Table 1.5, the real effective exchangerate depreciated sharply in 1986, along with the change in the nominal rate,largely as a result of political disruptions. Between the end of 1986 and theend of 1987, the real rate depreciated a further 6.6Z, largely because thePhilippine peso is tied to the U.S. dollar, and the dollar was depreciatingagainst most currencies. However, when viewed against the Philippines' majorcompetitors, the depreciation was less both in 1986 and 1987, as they toofollowed the dollar and depreciated their nominal rates.

Table 1.5: EXCHANGE RATE INDICES /a

Average Effective Exchange Rate (1980=100)nominal Nominal, vis-a-vis: Real, /b vis-a-vis:rate Major Major

Period P/$ Trade Partners Competitors Trade partners Competitors

1985 18.6 41.75 52.27 81.48 99.431986 20.4 35.86 52.18 69.37 94.671987 20.6 32.09 46.89 64.80 89.261988 Ql 20.9 31.74 46.37 65.98 89.701988 Q3 21.2 32.32 45.71 68.71 89.75

/a A decline in the value of the index denotes a depreciation of the peso./b Deflated by CPI.

Source: Central Bank of the Philippines, IMF.

The Interface Between Monetary and Exchange Rate Policies

1.12 At various times during 1987 and 1988, the Government has used mone-tary restraint to ease the pressure on the balance of payments. The need todiscourage outflow of capital, especially in a period of politial insta-bility, has been an important factor in the determination of monetary policy.The emergence of inflationary pressures during 1988, however, now places thePhilippine authorities between the dilemma of continuing a restrictive mone-tary stance, which could stifle economic growth, or following a more expan-sionary monetary policy, which would validate the inflationary process. How-ever, under a relatively free system of international capital movements, themonetary authority is also constrained in its interest rate policy by therelationship between domestic and international interest rates.

1.13 The Government has been reluctant to use exchange rate movements as ameans of dampening speculative pressures, for fear of adding to inflationarypressures and causing destabilizing swings in the exchange rate. One of the-rincipal concerns of the Central Bank has been the removal of excess

liquidity from the system in order to control exchange-rate speculation. Onemeans to achieve this has been the use of the so-called "revers repurchaseagreements," whereby the Central Bank effectively borrows at short-term fromcommercial banks. Until January 1988, the "reverse repurchase agreements"were of overnight maturity, but failure to mop up the required amount ofliquidity led the Central Bank to the introduction of a 14-day maturity inFebruary and of a 7-day maturity in April.

1.14 Currently, interest rates remain high in nominal terms, with Treasurybills selling at 15-162. At the same time inflation appears to averagingabout 7-92 so that real interest rates remain quite high. High interest ratesalso have a major impact on the budget deficit, since interest costs alreadyrepresent 242 of national government expenditures. Thus, it could be arguedthat there may have been over-reliance on monetary policy as a means ofmanaging the exchange rate. In general, monetary and fiscal policy should beprimarily used to affect the level of aggregate demand, and not support aparticular exchange rate.

1.15 The gradual loss in reserves during 1988 reflects a continuedstrategy of support for the exchange rate. During the first half of 1988, theCentral Bank was a net seller of foreign exchange. While it became a netpurchaser during the second half, these purchases were less than its foreignexchange requirements, requiring a use of official reserves. As a result,total official reserves have declined to $1.6 billion (September 1988), orless than two months of imports of goods and services, despite a relativelyrestrictive monetary policy. The approach of the authorities is sound, if itpermits a continuous, but smooth, adjustment of the exchange rate to marketconditions. However, the continued loss of reserves by the Central Bank insupport of the exchange rate suggests that the current strategy cannot besustained, and the time may have come for a less restrictive monetary policy,and the accumulation of reserves.

The Banking Sector

1.16 Monetary and fiscal management is made more difficult by the weak-nesses of the commercial banking sector. Since 1980, the banking sector hasundergone a very substantial contraction in real terms, as a result of politi-cal turmoil and economic shocks of that period. During 1980-86, the totalassets of the banking system fell by 44% in real terms; loans to the privatesector contracted by 631. The system is characterized by a large number ofsmall banks, with high operating costs because of their size; many banks arein poor condition. Yet banks in the Philippines operate with very high inter-mediation margins, averaging 7-10X during the 1983-86 period.

1.17 The Central Bank needs to take additional steps to strengthen thesector through consolidation and merger of weak banks, tighter regulation andsupervision, and by permitting more competition through increased branching.Intermediation costs can be reduced by elimination of the gross receipts taxon banks which adds about one percentage point of total spread, and eliminat-ing the Agri-Agra requirements which force banks to hold a certain proportionof low interest bonds in lieu of agricultural lending. In addition, the 20%withholding tax on interest should be eliminated for inter-bank deposits, and

- 10 -

transactions between the CB and the commercial banks. Another possibility isto raise the interest rate paid on required eserves, or lowering the requiredreserve ratio.

1.18 In general, commercial banks do not provide adequate amounts of longterm loans. In part, this reflects their tradition of commercial banking, andthe fact that most sources of funds are short-term. Attempts in the past toencourage long-term lending, such as by reducing reserve requirements on long-term deposits, have not been successful. Central Bank funds (APEX) madeavailable to finance long term loans have been underutilized, as commercialbanks seem inherently unwilling to take on an unfamiliar activity. Outsidethe commercial banks, there are few viable alternative sources of long-termfunds. Equity and bond markets remain underdeveloped and available only tothe biggest corporations with outstanding reputations. As a result, manyentrepreneurs finance long-term investments with short-term credits which areperiodically rolled-over. This is less than a happy solution. Yet theoverall financial system does have sources of long term funds, principally theGovernment's social security system and private life insurance companies.Some system needs to be developed to tap these sources and funnel them throughan institution that is equipped to undertake long term lending, as well as towork with borrowers on other aspects of their financial needs, such as finan-cial restructuring and equity offerings. The reorganized and restructured DBPis the logical choice for this role, as recent reforms have removed thesources of past problems. Long-term funds presently administered by theCentral Bank (APEX, IGLF) should be shifted to DBP, and efforts should be madeto have DBP act as a mobilizer of domestic savings.

B. Balance of Payments

1.19 Despite past progress, the Philippine remains one of the world'smajor high-debt countries. External debts are about $29 billion, or about 74%of GNP. The debt service ratio, even after substantial debt rescheduling,remains at 35% of exports of goods and services. This debt, and the need toservice this debt, remains an important constraint on future growth prospects.Yet in the past few years, the Philippines has taken major steps to strengthenits balance of payments position; the exchange rate has been made morecompetitive, import restrictions have been reduced, and the external debt havebeen renegotiated. In addition, the external environment has improved;interest rates have declined and the terms of trade have moved in thePhilippines favor.

The Trade Balance

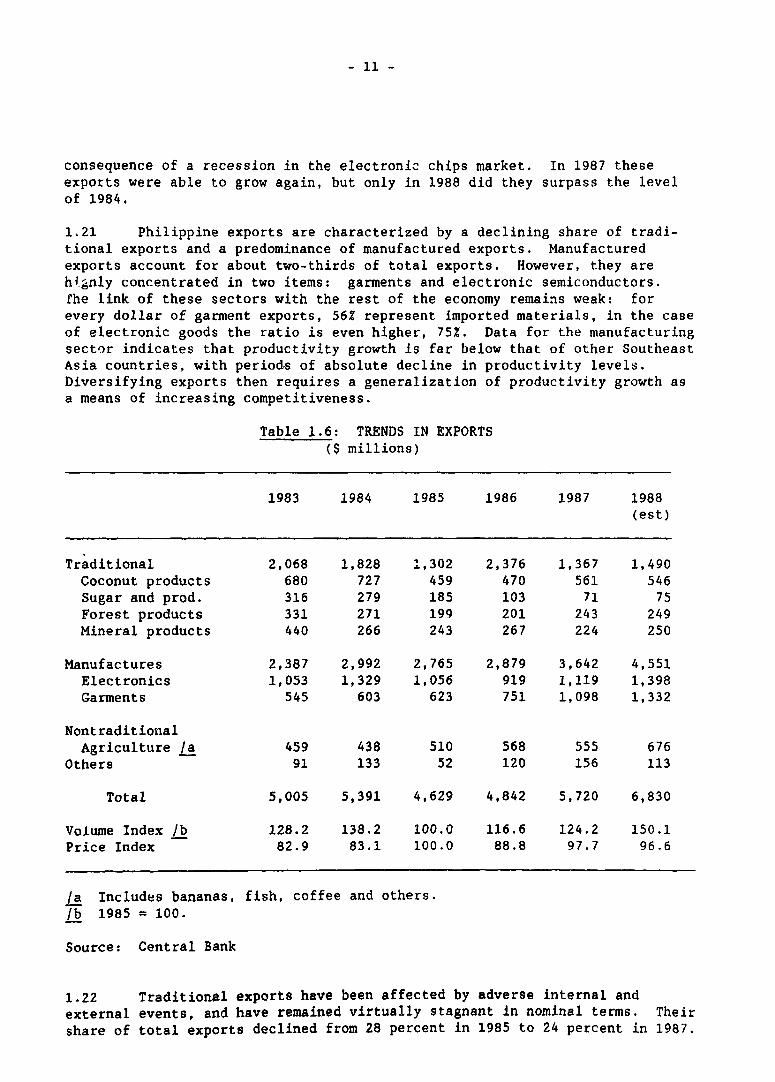

1.20 After small increase in 1986, exports have experienced a substantialrevival in 1987 with an overall growth of 18Z (in nominal terms), and afurther growth of 19% in 1988. In volume terms, exports have increased by 29%in the past twG years (see Table 1.6). The level of exports in 1988 was about$6.8 billion, which exceeded the peak level previously reached in 1980. Lead-ing the recovery have been manufactured exports, especially garments. Inrecent years garment exports have grown at an average rate of 20 percent peryear (in nominal terms) reaching a level of $1.3 billion in 1988, almost asmuch as the electronics exports. The latter have grown at a much more moder-ate rate, and actually declined for two consecutive years in 1985-86 as a

- 11 -

consequence of a recession in the electronic chips market. In 1987 theseexports were able to grow again, but only in 1988 did they surpass the levelof 1984.

1.21 Philippine exports are characterized by a declining share of tradi-tional exports and a predominance of manufactured exports. Manufacturedexports account for about two-thirds of total exports. However, they arehignly concentrated in two items: garments and electronic semiconductors.fhe link of these sectors with the rest of the economy remains weak: forevery dollar of garment exports, 56Z represent imported materials, in the caseof electronic goods the ratio is even higher, 75Z. Data for the manufacturingsector indicates that productivity growth is far below that of other SoutheastAsia countries, with periods of absolute decline in productivity levels.Diversifying exports then requires a generalization of productivity growth asa means of increasing competitiveness.

Table 1.6: TRENDS IN EXPORTS($ millions)

1983 1984 1985 1986 1987 1988(est)

Traditional 2,068 1,828 1,302 2,376 1,367 1,490Coconut products 680 727 459 470 561 546Sugar and prod. 316 279 185 103 71 75Forest products 331 271 199 201 243 249Mineral products 440 266 243 267 224 250

Manufactures 2,387 2,992 2,765 2,879 3,642 4,551Electronics 1,053 1,329 1,056 919 1,119 1,398Garments 545 603 623 751 1,098 1,332

NontraditionalAgriculture /a 459 438 510 568 555 676

Others 91 133 52 120 156 113

Total 5,005 5,391 4,629 4,842 5,720 6,830

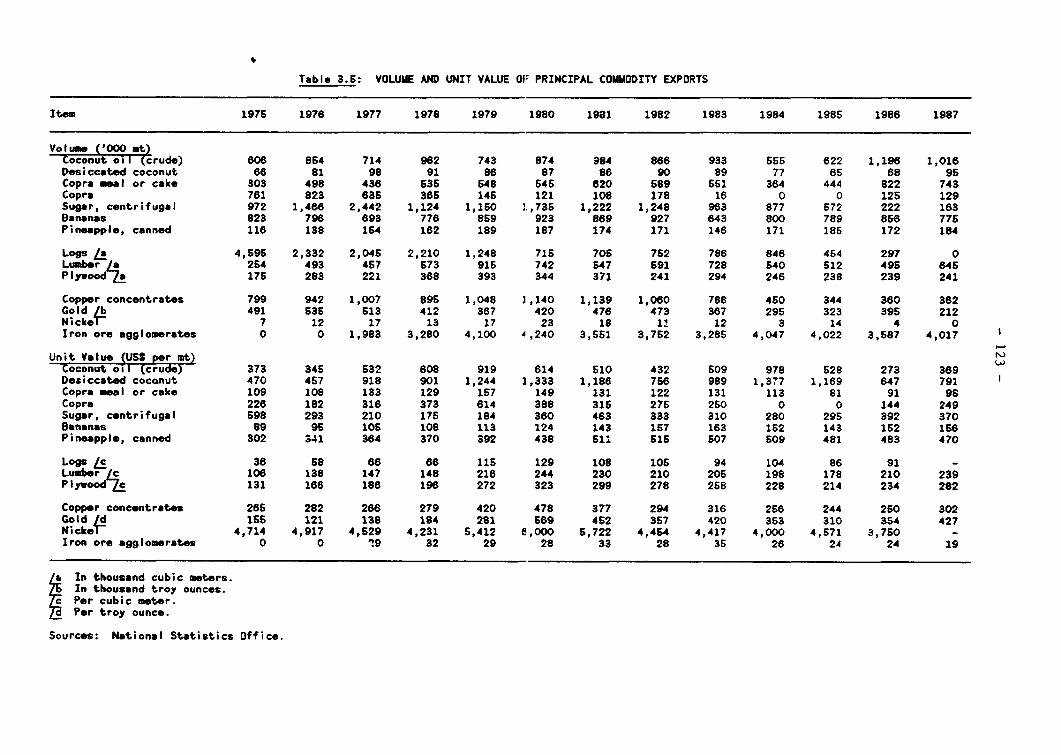

Volume Index /b 128.2 138.2 100.0 116.6 124.2 150.1Price Index 82.9 83.1 100.0 88.8 97.7 96.6

/a Includes bananas, fish, coffee and others./b 1985 = 100.

Source: Central Bank

1.22 Traditional exports have been affected by adverse internal andexternal events, and have remained virtually stagnant in nominal terms. Theirshare of total exports declined from 28 percent in 1985 to 24 percent in 1987.

- 12 -

Coconut oil exports, responding to the improvements in marketing conditionsinternally, and better weather, increased by 92% in 1986 in volume terms.However, sharply lower world prices resulted in a declined in total earnings.In 1987, drought again reduced production, but higher world prices resulted inan increase in total earnings. Sugar exports continued to contract during theperiod, reflecting a diminishing U.S. quota and the inability of Philippinesugar exports to compete against subsidized sugar export from the EEC. Theban on log exports, and the shortage of adequate timber resources, continue tolimit the level of log and plywood exports. One bright spot has been therapid growth of some of the non-traditional agricultural exports, such asshrimp and prawns, and processed food products.

Merchandise Imports

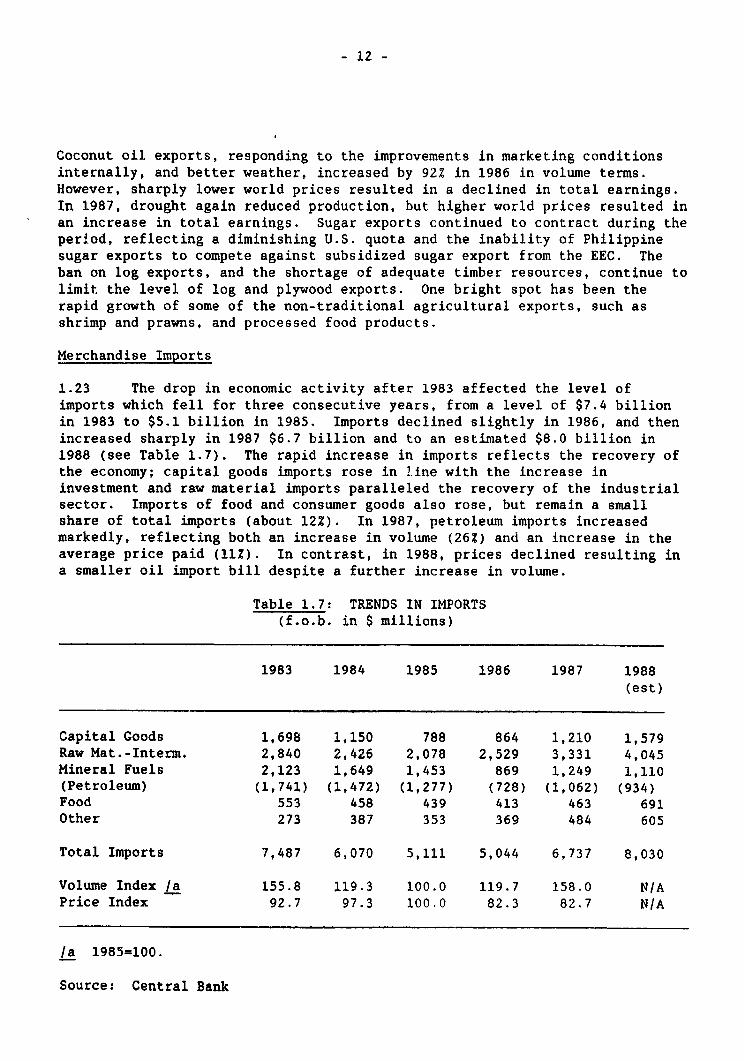

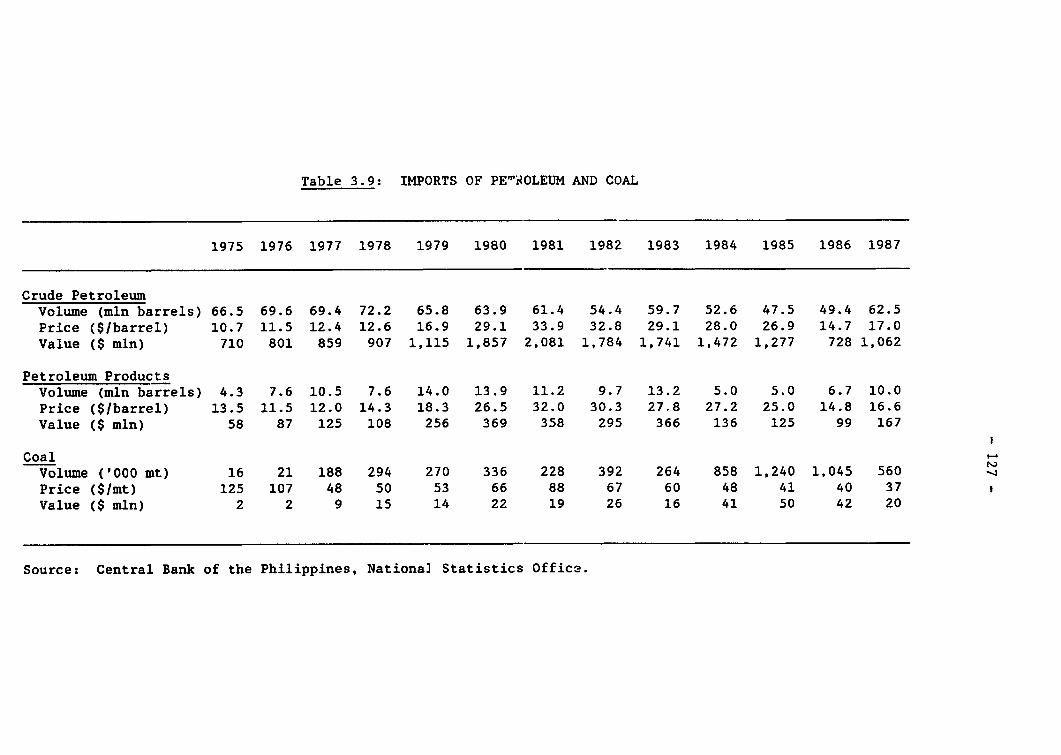

1.23 The drop in economic activity after 1983 affected the level ofimports which fell for three consecutive years, from a level of $7.4 billionin 1983 to $5.1 billion in 1985. Imports declined slightly in 1986, and thenincreased sharply in 1987 $6.7 billion and to an estimated $8.0 billion in1988 (see Table 1.7). The rapid increase in imports reflects the recovery ofthe economy; capital goods imports rose in line with the increase ininvestment and raw material imports paralleled the recovery of the industrialsector. Imports of food and consumer goods also rose, but remain a smallshare of total imports (about 12Z). In 1987, petroleum imports increasedmarkedly, reflecting both an increase in volume (26Z) and an increase in theaverage price paid (11Z). In contrast, in 1988, prices declined resulting ina smaller oil import bill despite a further increase in volume.

Table 1.7: TRENDS IN IMPORTS(f.o.b. in $ millions)

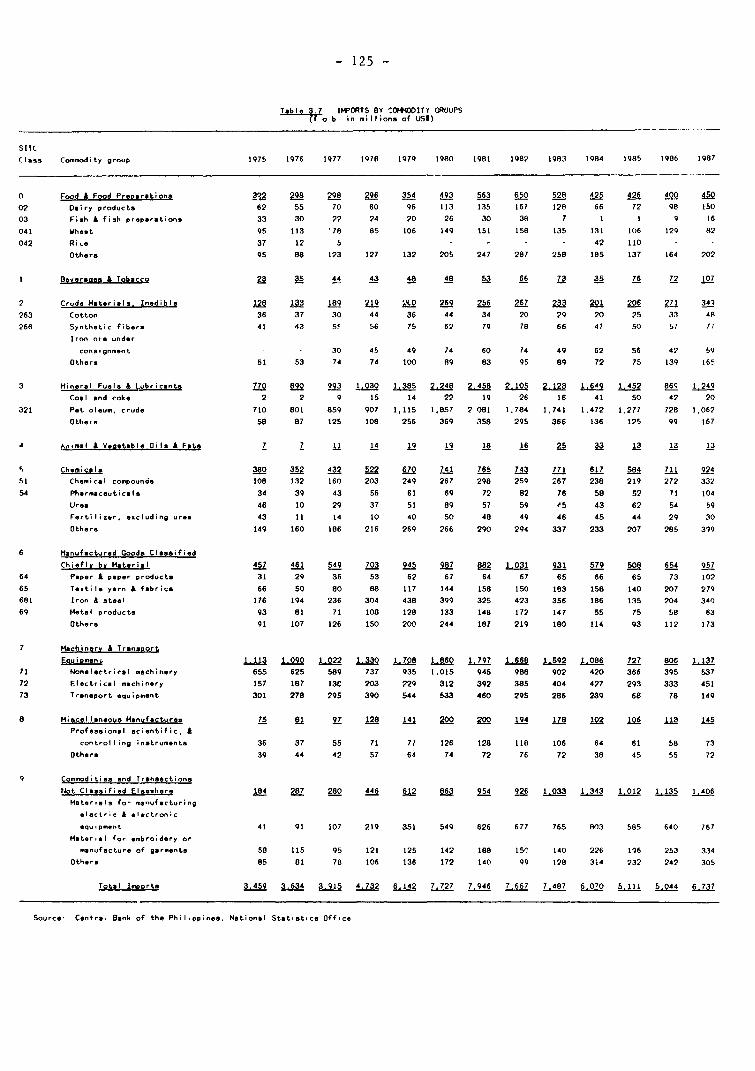

1983 1984 1985 1986 1987 1988(est)

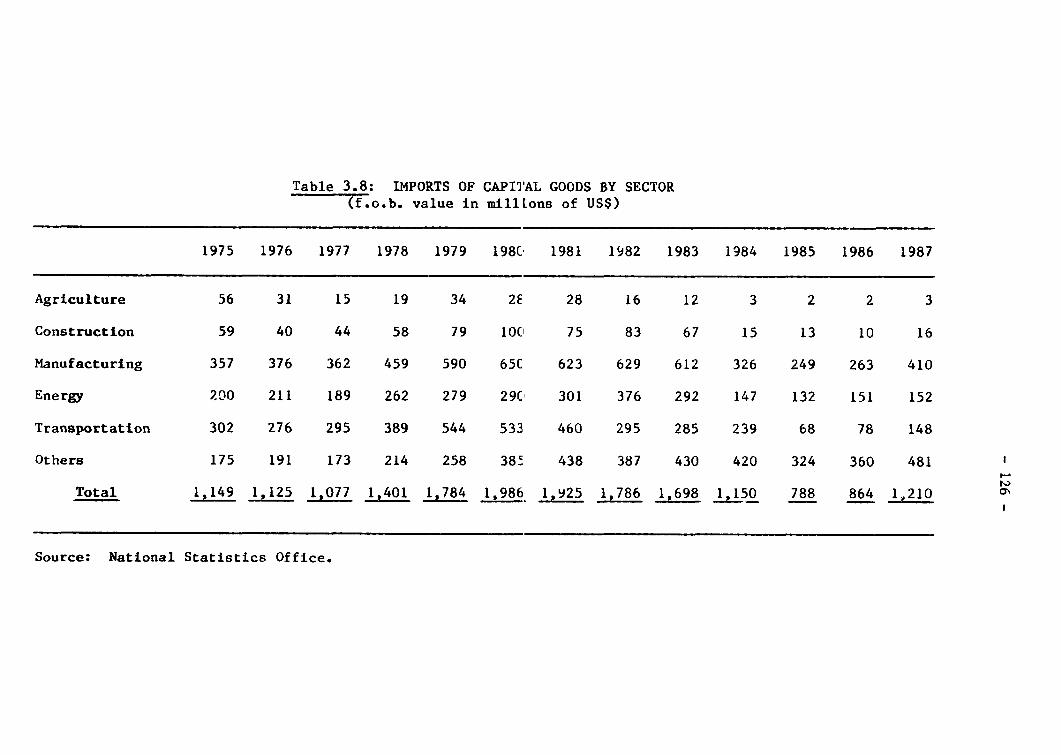

Capital Goods 1,698 1,150 788 864 1,210 1,579Raw Mat.-Interm. 2,840 2,426 2,078 2,529 3,331 4,045Mineral Fuels 2,123 1,649 1,453 869 1,249 1,110(Petroleum) (1,741) (1,472) (1,277) (728) (1,062) (934)Food 553 458 439 413 463 691Other 273 387 353 369 484 605

Total Imports 7,487 6,070 5,111 5,044 6,737 8,030

Volume Index /a 155.8 119.3 100.0 119.7 158.0 N/APrice Index 92.7 97.3 100.0 82.3 82.7 N/A

la 1985=100.

Source: Central Bank

- 13 -

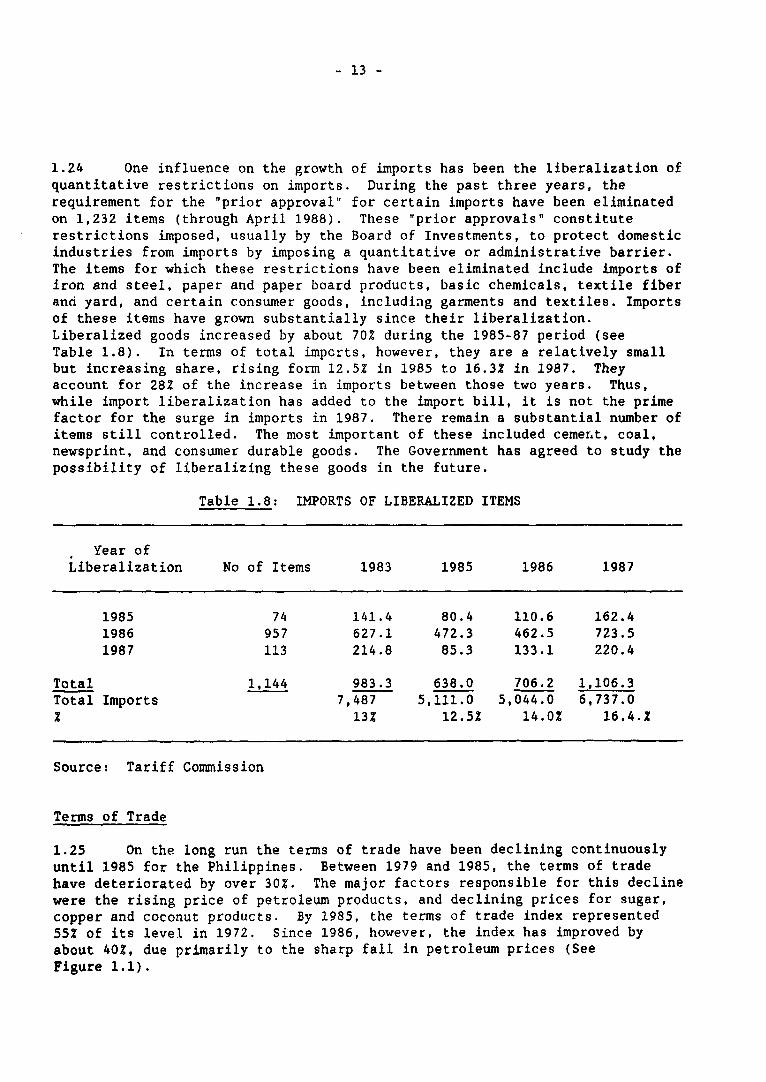

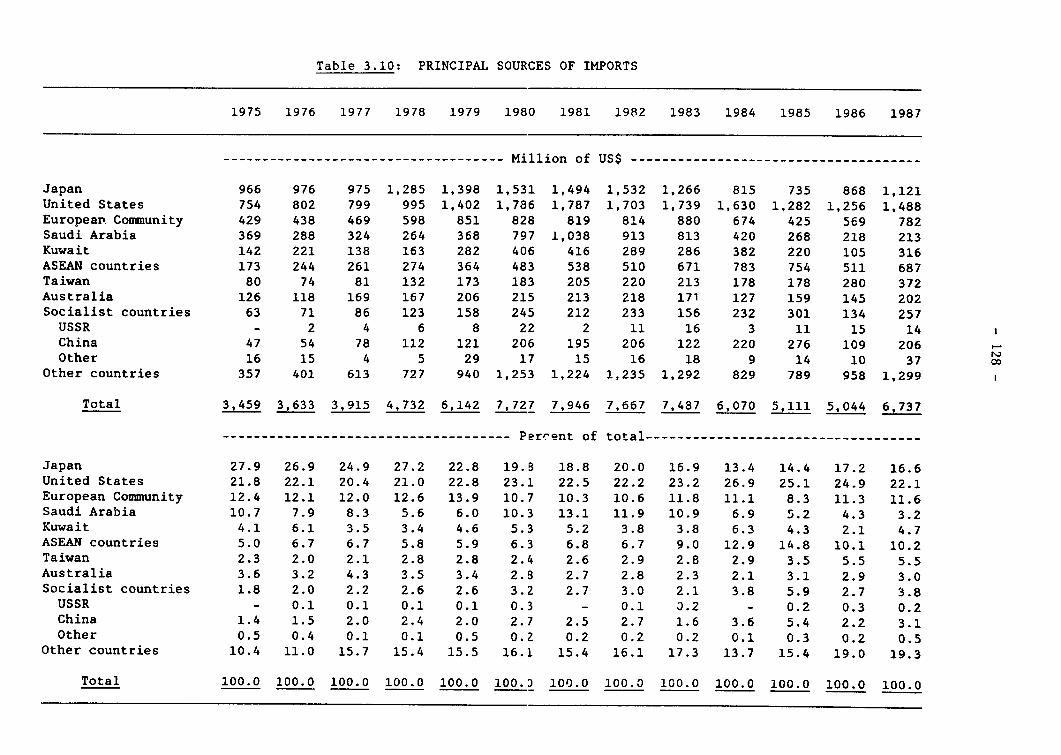

1.24 One influence on the growth of imports has been the liberalization ofquantitative restrictions on imports. During the past three years, therequirement for the "prior approval" for certain imports have been eliminatedon 1,232 items (through April 1988). These "prior approvals" constituterestrictions imposed, usually by the Board of Investments, to protect domesticindustries from imports by imposing a quantitative or administrative barrier.The items for which these restrictions have been eliminated include imports ofiron and steel, paper and paper board products, basic chemicals, textile fiberand yard, and certain consumer goods, including garments and textiles. Importsof these items have grown substantially since their liberalization.Liberalized goods increased by about 70% during the 1985-87 period (seeTable 1.8). In terms of total impcrts, however, they are a relatively smallbut increasing share, rising form 12.5% in 1985 to 16.3% in 1987. Theyaccount for 28% of the increase in imports between those two years. Thus,while import liberalization has added to the import bill, it is not the primefactor for the surge in imports in 1987. There remain a substantial number ofitems still controlled. The most important of these included cement, coal,newsprint, and consumer durable goods. The Government has agreed to study thepossibility of liberalizing these goods in the future.

Table 1.8: IMPORTS OF LIBERALIZED ITEMS

Year ofLiberalization No of Items 1983 1985 1986 1987

1985 74 141.4 80.4 110.6 162.41986 957 627.1 472.3 462.5 723.51987 113 214.8 85.3 133.1 220.4

Total 1,144 983.3 638.0 706.2 1,106.3Total Imports 7,487 5,111.0 5,044.0 6,737.0X 13% 12.52 14.0% 16.4.X

Source: Tariff Commission

Terms of Trade

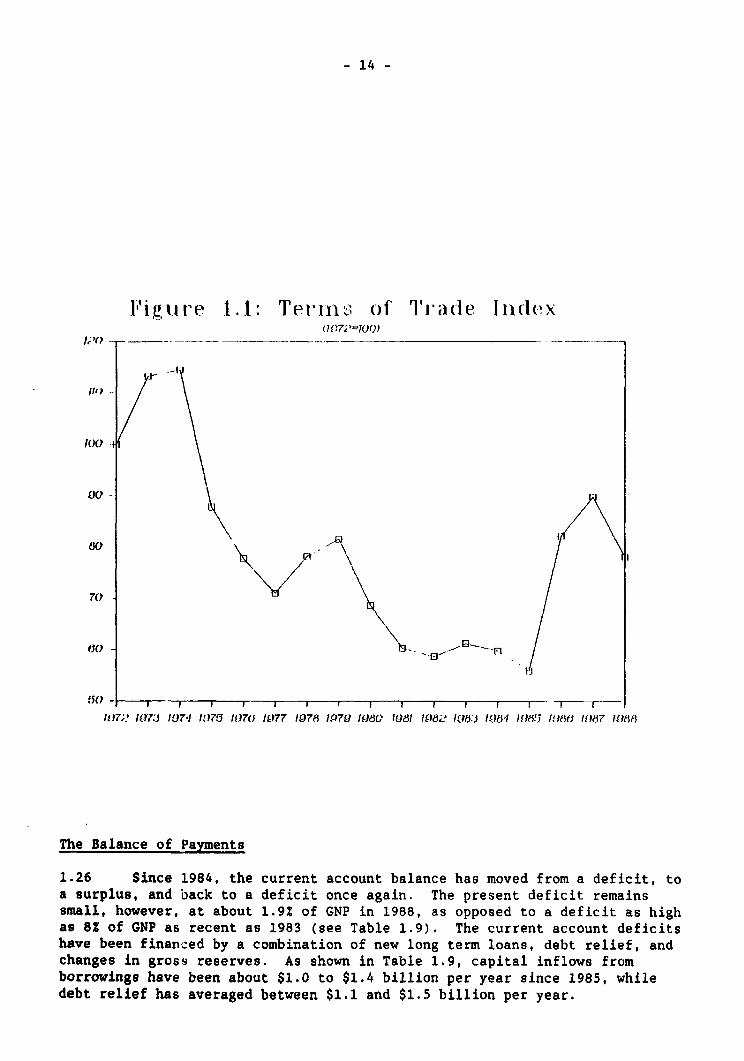

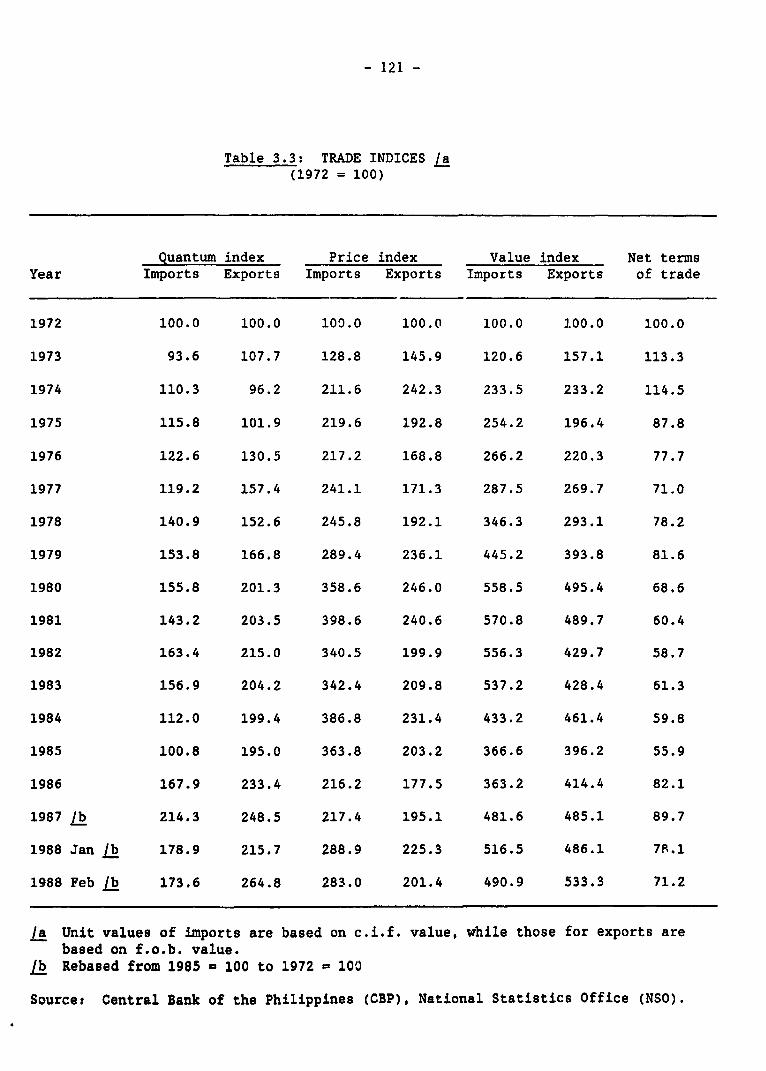

1.25 On the long run the terms of trade have been declining continuouslyuntil 1985 for the Philippines. Between 1979 and 1985, the terms of tradehave deteriorated by over 30%. The major factors responsible for this declinewere the rising price of petroleum products, and declining prices for sugar,copper and coconut products. By 1985, the terms of trade index represented55% of its level in 1972. Since 1986, however, the index has improved byabout 40%, due primarily to the sharp fall in petroleum prices (SeeFigure 1.1).

- 14 -

I'igu re 1.1: Terrn,; of T'i acle I11(lex1?OP

100 1100

'°I k

60 - t,

/lO;? ID7:J 10741 1175 /1076 l077 /978 1.47910 lW1 81 1986 1016:J 10614 1118!5 HOW15 10187 10188

The Balance of Payments

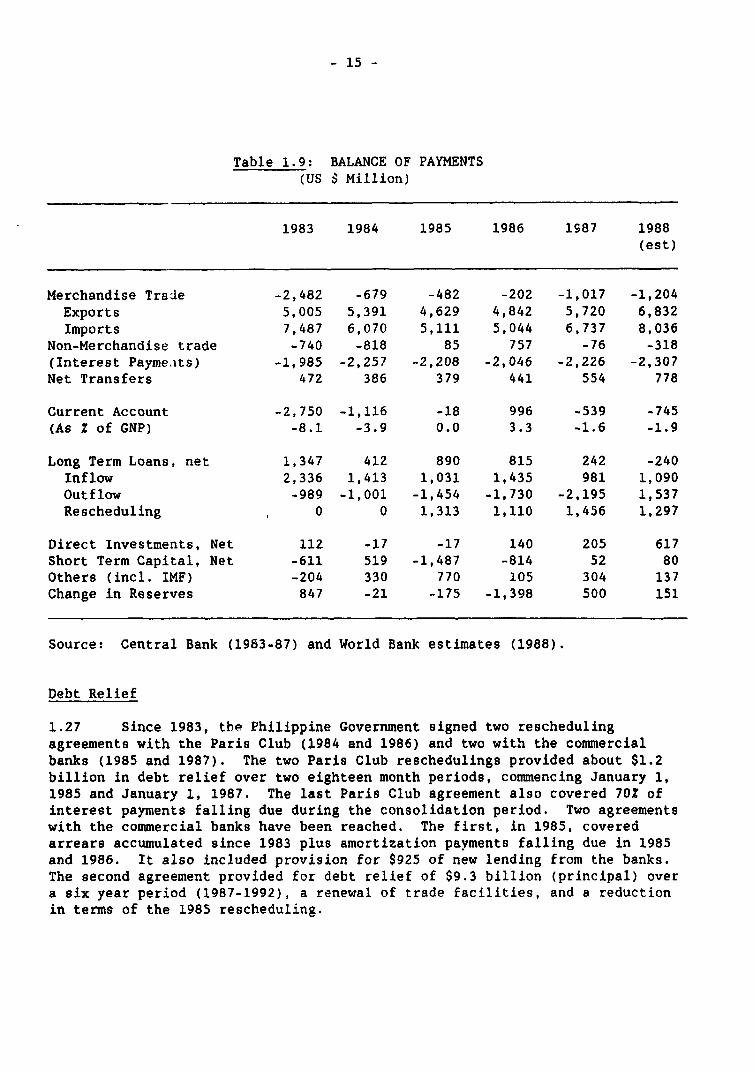

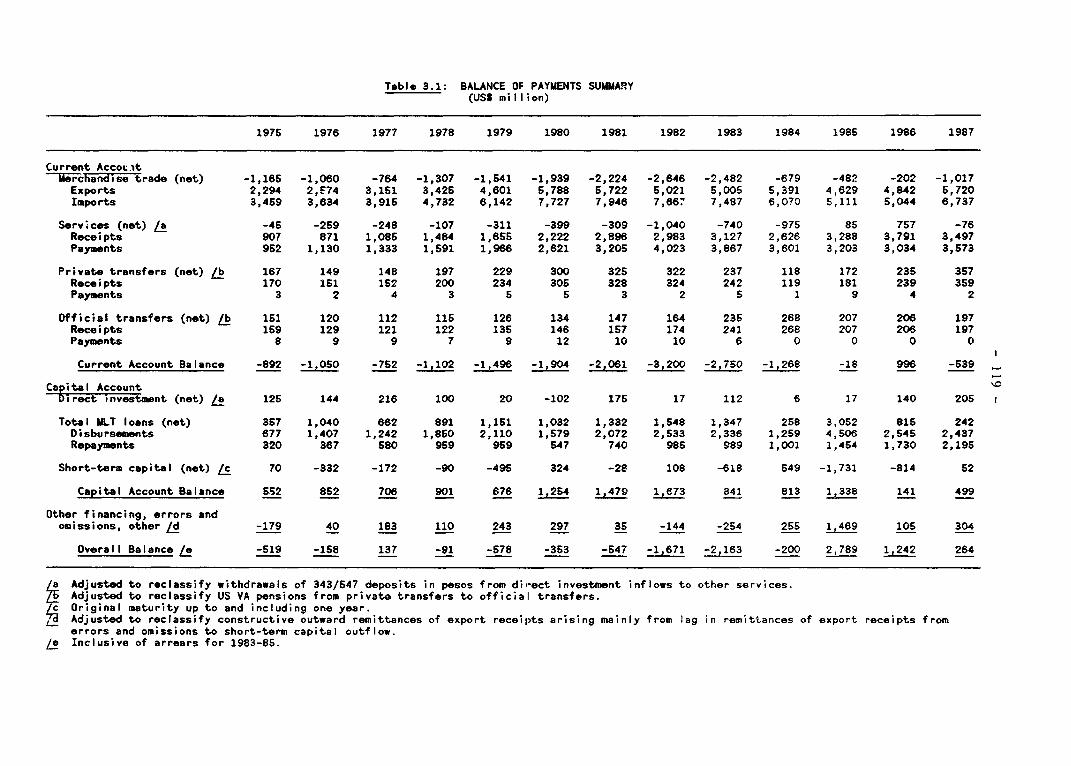

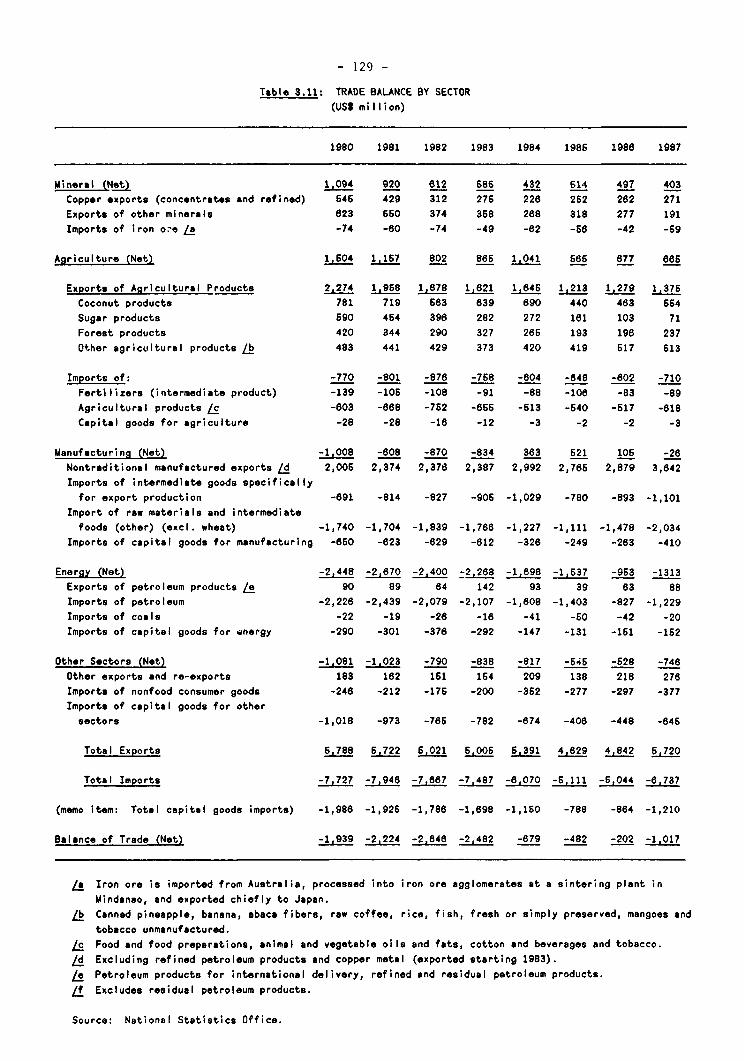

1.26 Since 1984, the current account balance has moved from a deficit, toa surplus, and back to a deficit once again. The present deficit remainssmall, however, at about 1.9% of GNP in 1988, as opposed to a deficit as highas 8Z of GNP as recent as 1983 (see Table 1.9). The current account deficitshave been financed by a combination of new long term loans, debt relief, andchanges in gross reserves. As shown in Table 1.9, capital inflows fromborrowings have been about $1.0 to $1.4 billion per year since 1985, whiledebt relief has averaged between $1.1 and $1.5 billion per year.

- 15 -

Table 1.9: BALANCE OF PAYMENTS(US $ Million)

1983 1984 1985 1986 1987 1988(est)

Merchandise Trade -2,482 -679 -482 -202 -1,017 -1,204Exports 5,005 5,391 4,629 4,842 5,720 6,832Imports 7,487 6,070 5,111 5,044 6,737 8,036