reputation survey 30aug2010

TRANSCRIPT

Reputation and the Invisible Hand: A Review of Empirical Research

For

The Oxford Academic Symposium on Reputation

September 15-17, 2010

and

The Handbook of Corporate Reputation

Jonathan M. Karpoff

First draft: 30 August 2010

This is a first draft. Please do not quote or cite without the author’s permission.

1

Reputation and the Invisible Hand: A Review of Empirical Research

“[Each person] generally, indeed, neither intends to promote the public interest, nor knows how much he is promoting it … he intends only his own security; and by directing [his] industry in such a manner as its produce may be of the greatest value, he intends only his own gain, and he is in this, as in many other cases, led by an invisible hand to promote an end which was no part of his intention. Nor is it always the worse for the society that it was not part of it. By pursuing his own interest he frequently promotes that of the society more effectually than when he really intends to promote it.” – Adam Smith, The Wealth of Nations (IV.ii.6-9, page 456 of the 1776 Glasgow Edition of Smith’s works; vol. IV, ch. 2, p. 477 of 1776 U. of Chicago Edition.)

I. The economic problem

Adam Smith’s “invisible hand” is perhaps the most important idea in the history of

economic thought. It captures one of the great discoveries of social science, that the pursuit of

self-interest can promote social welfare. But note that, in coining the term, Smith inserts a

qualifier. The pursuit of self-interest does not always promote society’s interest. Rather, it

frequently does so.

In the 234 years since The Wealth of Nations, economic philosophers have worked to

understand the conditions and processes by which the invisible hand works to promote social

good, and also to understand the conditions and processes in which it does not. So far, we have

three broad answers for why it might not: Self-interest can decrease the social pie when

monopoly is involved, when the costs of externalities are sufficiently high, or when market

outcomes are deemed undesirable for equity reasons.

This essay considers another category of economic activity in which the pursuit of self-

interest does not, in general, serve to promote social welfare. This is when economic actors lie,

2

cheat, and steal.1 It is widely acknowledged that opportunistic behavior impedes value creation

and that a culture of corruption tends to be inversely related to economic development.2

Economists also understand how trust is fundamental to exchange. In Akerlof’s (1970) lemons

problem, buyers demand discounts to compensate for their risk of being ripped off by sellers who

have an informational advantage about the quality of the good to be exchanged. Sellers who

stand ready to sell in the face of such discounts signal that their products are relatively inferior,

causing buyers to demand even larger discounts. In the end, trade breaks down, as buyers infer

that only sellers of the lowest quality products remain in the market at low, discounted prices that

buyers are willing to pay.

Akerlof’s problem is pervasive, in that information is costly and sellers typically know

more than buyers about the quality of what they are trying to sell. The problem goes the other

way, too, as buyers can opportunistically take advantage of sellers. In theory, one could get

around the lemons problem by writing contracts that protect opportunistic buyers and sellers

from each other. The problem, of course, is that contracts are costly to write and to enforce, and

therefore will always be incomplete.

Despite the pervasiveness of the lemons problem, buyers and sellers do get together –

millions of times each day. When you think about it, it is a bit of a miracle: millions of trades

occur every day in all parts of the world, despite the ever-present risk that sellers could cheat

buyers or buyers could cheat sellers. How does that happen? What holds the whole economic

process together? Why is fraud not running rampant in the streets? Fraud does occur, but why is

it the exception rather than the norm?

1 I do not take a strong position that this constitutes a fourth category of exceptions to Smith’s invisible hand theory. It is possible to frame misconduct and opportunistic behavior as a type of externality problem. The Coase Theorem implies that the costs of opportunistic behavior arise because the information and transaction costs to fix the problem are prohibitive. 2 A search for “corruption and economic development” on ssrn.com obtains 289 matches.

3

Of course, some people do not cheat others because their personal, moral, or religious

codes discourage cheating. Some types of opportunistic behavior are illegal, and the threat of

legal sanctions deters many people from behaving badly. Personal ethics and the law no doubt

are important. But even in an amoral society with no legal enforcement of contracts, there would

remain a powerful inducement to honest dealing: the prospect that your counterparty will do

business with you again in the future. By performing as promised, individuals and firms can

develop reputations for honest dealing. Such reputations are valuable because they yield

favorable terms of contract with customers, employees, suppliers, and investors.

Klein and Leffler (1981), Shapiro (1983), and others have developed models in which

reputation – and reputation alone – encourages good behavior and disciplines bad behavior. The

upshot is that people and businesses can invest in reputation, just as they might invest in

machinery, R&D, or human capital. Viewed this way, reputation is a valuable asset. It is the

present value of the improvement in net cash flow and lower cost of capital that arises when the

firm’s counterparties trust that the firm will uphold its explicit and implicit contracts, and will

not act opportunistically to their detriment.

Reputational capital is not transparent on a firm’s balance sheet, but circumstantial

evidence suggests that it is important. For example, Beatty, Bunsis, and Hand (1998) find that

investment banks with high reputation obtain higher fees for their services. And Resnick et al.

(2002) find that high-reputation sellers on eBay get higher prices than others, even for the same

goods. Nonetheless, measuring the size of a firm’s reputational capital is difficult, and we have

little direct evidence on its size for most firms. To get around the measurement problem,

researchers have used a different kind of experiment to infer the importance of reputation to

firms. This experiment examines the counterexamples – i.e., instances in which people or firms

4

lose reputation by lying, cheating, or stealing. To the extent that such losses are large, we can

infer whether, and where, reputation matters.

In this essay I survey the empirical research on the costs to firms from misconduct that

affects investors, customers, employees, suppliers, and the community at large. Section II

examines financial misconduct. The prototypical case is Enron, which during 1997-2002

inflated its reported earnings – and its stock price – by underreporting expenses, exaggerating

revenues, and lying about its financial leverage. The results from 32 studies show that firms lose

a significant amount of market capitalization when their financial misconduct is revealed,

although point estimates of the loss range widely.

Evidence of share price losses does not necessarily imply that firms suffer reputational

losses, because share prices can decline for other reasons as well. Section III reports on an

attempt to partition firms’ share value losses into components that reflect regulatory fines, class

action settlements, price deflation due to new information about the firm’s financial position, as

well as reputation. For financial misconduct, reputational loss explains the largest portion of

firms’ total losses. This inference is corroborated by evidence that the cost of equity and debt

financing both increase after investors learn that a firm’s books were in error.

Section IV surveys the empirical evidence regarding firms’ losses for many other types of

misconduct, including frauds of related parties, product recalls, air safety disasters, and

environmental violations. Here the evidence is mixed. Some types of misconduct, such as fraud,

are associated with significant share value and reputational losses. For other types, including

environmental violations and misconduct that affects unrelated parties, there is no systematic

evidence of reputational loss. Even when share values decline because of an environmental

5

violation, the decline reflects the legal penalties imposed on the violating firms, not any

reputational effect.

Section V proposes an explanation for these mixed results. Reputational capital – what

Klein and Leffler (1981) refer to as the quasi-rent stream from delivering the level of quality that

is promised – works to encourage honest dealing among counterparties. It is not a panacea that

discourages all types of misconduct. It has force when the firm’s actions undermine its trust with

its counterparties, but not when it harms unrelated parties. So firms that defraud consumers lose

future sales, and firms that cook their financial books face less favorable terms from investors

and creditors. But, while firms that pollute a river impose harms on downstream users, the

harmed parties typically are not the ones with whom the firm does business.

Thus, the role of reputation is more complex than a bland admonition to “follow the

Golden Rule,” or to “do well by doing right.” The evidence indicates that reputation, and the

threat of losing it, plays a more important role for some types of misconduct than others. As I

discuss in Section V, even firms in the same industry invest in different levels of reputational, so

the size of the reputational capital at stake differs even across otherwise similar firms. This

implies that vendors offer customers, suppliers, and investors different levels of reputational

guarantee, just like they offer different product, price, delivery, payment, and service. Where the

reputation at stake is larger, the likelihood that the firm will act opportunistically is smaller.

There remain many questions about how and in what settings reputation works to

facilitate Adam Smith’s invisible hand. Section VI concludes with a list of ten questions for

further empirical research.

6

II. Market value losses when financial misconduct is revealed

News that a firm’s financial reports are in error can affect the firm’s share values in three

ways. First, the news indicates that the financial information used by many investors to help

value the company is in error. Share values usually are inflated by the misleading financial

information, and they decrease as investors reassess the firm’s value in light of financial data that

provide a more accurate picture of the firm’s earnings. Second, the news suggests that the firm

may face legal penalties in the form of regulatory sanctions, fines, or shareholder lawsuits. And

third, the news can change the company’s real operations or cost of capital. The fact that the

firm’s officers furnished misleading financial information indicates that the company has poor

internal controls, managers who behave opportunistically, or both. As we will see, such

information causes the firm’s investors and other stakeholders to change the terms with which

they are willing to do business with the firm. Lenders, for example, change higher interest rates

to firms whose financial reports or internal controls are suspect.

In this survey I refer to these three effects as (i) share deflation, (ii) legal penalties, and

(iii) impaired operations and reputation. In theory, each of these effects serves to decrease share

values, so news of financial misconduct should be associated with a decrease in share values.

This is exactly what empirical research has documented. Table 1 summarizes the results of 30

studies that examine the share price reactions to news of error in a firm’s financial reports. The

table is organized by the five primary methods that researchers have used to identify financial

misconduct. Panel A reports on four studies that use key word searches from media reports to

identify instances of financial misconduct. Panel B summarizes the results of nine studies that

examine share price reactions for samples of firms that restated earnings. Panel C reports the

results of seven studies that examine the effects of private lawsuits, typically securities class

7

action lawsuits that allege that the firm violated SEC Rule 10b-5. Panel D reports the results of

four papers that use SEC Accounting and Auditing Enforcement Releases (AAERs) to identify

financial misconduct, and Panel E reports the results of two papers that use SEC enforcement

actions to identify such misconduct.

In a few cases I report weighted averages of a combination of smaller subsample results.

But in most cases I report the results as the authors report them. I focus on results from the event

window that the authors emphasize, or absent any such emphasis, the results from a window that

appears most comparable to the other papers in the table. My summary focuses on abnormal

stock returns, which are calculated as the difference between the raw return and a benchmark. In

many studies the benchmark is estimated from a one-factor market model, with estimation

periods that vary across studies. Several papers use alternate benchmarks, such as a simple

market return. A critical review of several individual papers’ empirical procedures could raise

doubts about their particular conclusions. But I believe that these papers’ overall conclusions –

and the inferences I draw from them – do not depend on the particular empirical methods

deployed.

II.A. Media key word searches

Early attempts to examine the share price impacts of business misconduct used data

collected from media sources, usually The Wall Street Journal. Several of these include

subsamples involving financial misreporting. Karpoff and Lott (1993) report an average two-day

abnormal return of -4.66% upon the initial press announcement for a small subsample of

financial reporting violations. Davidson, Worrell, and Lee (1994) report a three-day abnormal

stock return of -2.80% for a slightly larger sample of such violations. Gerety and Lehn (1997)

8

identify 37 instances of financial disclosure violations from SEC, and identify the first public

announcements of the SEC’s actions in The Wall Street Journal. The average three day

abnormal stock return is -3.05% and is marginally significant. To date, few studies investigate

the share price effects of business misconduct outside of North America. An exception is

Tanimura and Okamoto (2010), who examine corporate scandals in Japan, including 40 cases of

financial reporting frauds. Although the events are from a different country and time period than

the other events summarized in Panel A, the average abnormal stock return is similar, -5.99%.

II.B. Studies based on earnings restatements

Several researchers have examined how firm value is affected by news that a firm has to

restate earnings. Using a hand-collected dataset on 286 earnings restatements, Palmrose,

Richardson, and Scholz (2004) find that a restatement announcement is associated with a share

value decline of 9.2%, on average. Anderson and Yohn (2002), Akhigbe, Kudla, and Madura

(2005), and Agrawal and Chadha (2005) collect restatement samples using such media-based

databases as Lexis-Nexis. They also find negative stock price reactions to news of a restatement,

although their point estimates are smaller in magnitude. Several teams of researchers use

restatement data compiled by the Government Accountability Office (GAO 2003). Using the

GAO data, Hribar and Jenkins (2004), Arthaud-Day, Certo, Dalton, and Dalton (2006), Burns

and Kedia (2006), and Desai, Hogan, and Wilkins (2006) estimate the loss at 9-11%. Using the

same database, however, Kravet and Shevlin’s (2010) obtain an estimate of -5.4%.

The differences in point estimates illustrate a potential problem in using the GAO data to

identify instances of misconduct. Hennes, Leone, and Miller (2008) point out that the GAO

database includes both intentional and unintentional restatements. By their estimate, fully 73%

9

of the GAO restatements are unintentional or technical restatements, or what they call “errors.”

Hennes et al. measure the average abnormal stock return for 69 such “error” restatements as -

1.93%. In contrast, the average abnormal stock return for events that reflect intentional

misstatements, or what they call “irregularities,” is -13.64%. This implies that the consequences

to intentional misrepresentation are much larger than they are for minor accounting errors.

Researchers who use the GAO database must decide whether a restatement event

corresponds to a material case of financial misconduct. The fact that different researchers obtain

different point estimates of the share value loss reflects, in part, different choices on which

restatements to include in their analyses.

Karpoff, Lee, and Martin (2008a) point out another potential problem from using

restatements to measure the loss from financial misconduct. In some cases investors first learn

of the misconduct when the firm announces a restatement. In many other cases, however, a

restatement is made many weeks or months after the first disclosure of misconduct. For

example, HealthSouth Corp. engaged in a financial fraud from 1996 until March 2003. The firm

restated some previous years’ earnings in 2005. But investors first learned of the misconduct in

late 2002 and early 2003 through a series of press releases and federal regulatory

announcements. Clearly, by the time of the 2005 restatement, the firm’s misconduct was old

news. Karpoff, Lee, and Martin (2008b) report that restatement announcements coincide with

the first public revelation for only 14% (53 out of 371) of the misconduct cases in their sample.

This implies that restatement data will provide low power tests of the hypothesis that news of

financial misconduct affects stock prices. Despite such power issues, the evidence clearly

indicates that share prices decline by a large and statistically significant amount when firms

announce an earnings restatement.

10

II.C. Studies based on securities class action lawsuits

Several studies use lawsuits as indications of financial misconduct. Most examine

securities class action lawsuits filed under SEC Rule 10b-5. Rule 10b-5 prohibits any “untrue

statement or a material fact or to omit to state a material fact … in connection with the purchase

or sale of any security.” Plaintiffs can sue for damages if they can show that managers willfully

released inaccurate financial information. In a 1964 case, the U.S. Supreme Court referred to

private lawsuits using Rule 10b-5 as acting like “private attorneys general,” helping to enforce

securities laws and promote accurate financial reporting.

As reported in Panel B of Table 1, most studies examine the share impacts around either

or both of two key events in a securities class action lawsuit: the public disclosure that prompts

the lawsuit, and the filing of the lawsuit itself. In an early investigation, Kellogg (1984) finds

that the initial discovery of financial misrepresentation that leads to a lawsuit is associated with

an average share price decline of 3.9%. Subsequent investigations, however, find that the public

disclosure is associated with much larger losses. Francis, Philbrick, and Schipper (1994) find

that the initial adverse earnings disclosure that subsequently prompts a class action lawsuit is

associated with a stock price decline of 17.16%. Using the lawsuit complaints to identify the

initial public revelation of financial fraud, Ferris and Pritchard (2001) find that the average three-

day abnormal return is -24.99%. They argue that such a large reaction is consistent with the

notion that plaintiffs’ lawyers select cases with large share price declines and a larger likelihood

of recovery. Using a large sample of 2,133 lawsuits from 1990 – 2001, Griffin, Grundfest, and

Perino (2004) measure a three-day average abnormal return of -16.60%.

11

Although news of the misconduct is associated with the largest share price declines, the

filing of a lawsuit also is associated with a decline in share values. The estimates range from -

2.71% (Bhagat, Bizjak, and Coles 1998, reporting on “SEC-type Suits”) to -4.66% (Gande and

Lewis 2009). These results suggest that, even after the public learns of the misconduct, news of

the filing conveys additional and unfavorable information about the eventual cost of the

misconduct to the firm.

II.D. Studies based on AAERs

A large accounting literature examines the quality of firms’ reported earnings (see

Dechow, Ge, and Schrand (2010) for an excellent survey). Several papers in this literature use

AAERs to identify instances of financial misconduct. As described in the first AAER issued in

1982, an AAER is a designation that the SEC attaches to an enforcement release when it

involves an accountant. The idea is that “…[I]nterested persons will be able to easily distinguish

enforcement releases involving accountants from releases in which the Commission announces

the adoption or revision of rules related to financial reporting or discusses its interpretive views

on financial reporting matters” (page 1).3

Feroz, Park, and Pastena (1991) first introduced the idea of using AAERs to identify

instances of financial misconduct. For 58 firms that subsequently were the subjects of AAERs,

the public disclosure of misconduct is associated with a two-day average abnormal stock return

of -12.9%. Dechow, Hutton, and Sloan (1996) report a one-day average abnormal stock return

of -8.8% for 92 firms that were the subjects of AAERs. Beneish (1999) uses AAERs to identify

50 firms that overstated earnings. Most likely because these firms’ misconduct was particularly

3 Accounting and Auditing Enforcement Release No. AAER-1, 1982 SEC LEXIS 2565, May 17, 1982; Accounting and Auditing Enforcement Release No. AAER-1, 1982 SEC Act Rel No. 6396, Exch Act Rel No. 18649 / April 15, 1982.

12

egregious, the 3-day abnormal stock return for the initial disclosure is relatively large at -20.2%.

Bonner, Palmrose, and Young (1998) also use AAERs to identify a sample of misconduct firms.

They do not report an event study, but report that the average abnormal return over the 12-month

period centered on the end of a firm’s violation period is -24%. Karpoff and Lou (2010) report

that the end of the violation period is on average 2 months before the initial public revelation of

the misconduct, so this result likely reflects, in part, the share price decline that accompanies

such revelations. Finally, Miller (2006) reports an average abnormal return of -6.3% upon

publication of the first press article for a sample of firms that attracted enforcement releases

receiving an AAER designation.

In addition to these results, Feroz, Park, and Pastena (1991) examined share price

reactions to related events. The initiation of an SEC investigation that leads to an AAER is

associated with a share price decline of 7.5%, on average. Feroz et al. find no significant share

price reaction to the announcement of a settlement of an SEC action.

All of these studies conclude that news of financial misconduct reduces share values.

The point estimates of the loss, however, vary widely. As with most studies, some of the

discrepancy can be attributed to differences in the specific measure of abnormal returns and

sample selection. Below, however, I argue that much of the variation is due to differences in the

power of the tests. Some samples yield powerful tests of the hypothesis that news of misconduct

is associated with share value losses because they correctly identify the earliest public release of

information about cases that actually involve misconduct. Other samples, in contrast, tend to

capture neutral events, or events that occur well after the initial release of information about the

misconduct.

13

II.E. Studies based on SEC enforcement actions

Karpoff, Lee, and Martin (2008b) (hereafter, KLM) measure the impact on share values

of SEC enforcement actions for financial misrepresentation from 1978 through September 2006.

They claim that their sample is the universe of federal enforcement actions for violations of

provisions that require firms to keep accurate books and records (15 U.S.C. §§ 78m(b)(2)(A))

and to maintain a system of internal accounting controls (15 U.S.C. §§ 78m(b)(2)(B)).

Figure 1 illustrates the sequence of events that constitute a typical SEC enforcement

action. Most enforcement actions follow a conspicuous trigger event that publicizes the potential

for misconduct and attracts the SEC’s scrutiny. Trigger events include self-disclosures of

malfeasance, restatements, auditor departures, unusual trading, and whistle-blower lawsuits.

KLM report that the average one-day market-adjusted share return on such trigger dates is

–25.24%. Using an updated version of the KLM data, Karpoff and Lou (2010) report an average

abnormal return of -18.2% on the trigger date. These results are similar in magnitude to those

from studies, such as those in Panel C of Table 1, that focus on the initial disclosure of

misconduct.

KLM (2008b) report results that help to clarify the discrepancies in many of the results in

Table 1. When the trigger event is an earnings restatement announcement, the average abnormal

return is -24%. This is much larger than the averages in Panel B, but this is because many of the

restatements in prior studies are preceded by prior public revelation of the misconduct. That is,

most samples of earnings restatement announcements include many events that convey relatively

little new information about the misconduct.

14

KLM also report that the initial filing of a securities class action lawsuit, which typically

occurs after the trigger date, is associated with an average share price decline of -7.0%. This is

larger than the results for filing dates reported in Panel B. This reflects the fact that lawsuits in

the KLM sample are related to relatively egregious or costly types of financial misconduct,

because they are accompanied by SEC sanctions. The lawsuits investigated by the papers in

Panel B, in contrast, include a broader range of events, including relatively small lawsuits that

impose little cost on shareholders.

Following a trigger event, the SEC gathers information through an informal inquiry that

may develop into a formal investigation of financial misconduct. As illustrated in Figure 1, the

announcement of a formal investigation is associated with an average share price decline of

13.7%.

The SEC releases its findings and penalties in its Administrative Releases and Litigation

Releases, some – but not all – of which also receive a designation as an AAER. (KLM (2008a)

report that 63% of the regulatory releases in their sample also were assigned an AAER number.)

If the SEC proceeds and imposes sanctions, the news of its initial regulatory action is associated

with a further 9.6% decline. Subsequent releases that indicate that the matter is resolved are

associated with an average decline of 4.2%. These are the events that are captured in the AAER-

based samples summarized in Panel D. Notice that most researchers who use AAERs to infer

financial misconduct backfill their data to identify the first disclosure of the misconduct. So the

results in Panel D most likely reflect a combination of trigger events and regulatory releases as

illustrated in Figure 1.

The events illustrated in Figure 1 typically take several years to play out. Karpoff and

Lou (2010) report that in their sample of enforcement events, the median length of the violation

15

period is 24 months, and the median length from the beginning of the violation until its initial

public revelation is 26 months. From the initial public revelation until the end of the

enforcement action takes an additional 41 months.

III. Reputational losses for financial misconduct

The research summarized in Table 1 clearly establishes that share values fall upon news

of financial misconduct. Some authors interpret such losses as a type of penalty that deters

misconduct (e.g., see Gunthorpe 1997). This, however, confuses the source with the measure of

firm losses. In reasonably efficient markets, share prices reflect investors’ expected values of

future cash flows to equity. They change when such expectations change. That is, changes in

share values are not the source of penalties, but rather, a measure of investors’ expectations of

the penalties. The sources of penalties include the regulatory fines, class action settlements,

higher cost of capital, and impaired operations that result from the discovery of misconduct. In

addition, share values decline as investors realize they had been relying on incorrect financial

information to forecast the firm’s future cash flows.

III.A. Legal penalties for financial misconduct

One reason share values decrease is that investors anticipate that the firm will face

monetary or non-monetary sanctions from the SEC and other regulators, or lawsuits related to

the misconduct. Consider, for example, the array of legal penalties described by KLM (2009)

imposed on WorldCom related to its 1999-2002 accounting fraud:

On June 27, 2002, the U.S. Securities and Exchange Commission (SEC) filed a complaint alleging that WorldCom Inc. misreported its earnings from January 1999 through March 2002 by a cumulative amount of $11 billion. In subsequent actions, the SEC halted trading in WorldCom stock for two days, barred four WorldCom executives from serving

16

as officers or directors of publicly held companies, suspended five directors and employees who were CPAs from appearing or practicing before the Commission as accountants, and fined the company $2.25 billion (an amount reduced in bankruptcy and district court negotiations to $750 million). The Department of Justice (DOJ) fined the company $27 million, ordered the firm to provide an additional $670,000 in communication services, and prosecuted CEO Bernie Ebbers, CFO Scott Sullivan, and four others for financial fraud, culminating in combined sentences of 32.4 years in jail and $49.2 million in restitution. In a parallel class action lawsuit, the firm and its officers paid a total of $6.8 billion to investors.

KLM (2008b) report that the SEC imposed an average of 1.4 non-monetary sanctions for

each of the 585 firms in their sample. Most (90.6%) were cease-and-desist orders or permanent

injunctions – actions that appear to impose extremely small penalties. Monetary penalties are

less common. Only 47, or 8%, of the 585 firms were assessed monetary penalties by regulatory

agencies. The mean fine was $106.98 million, but this is affected by WorldCom, which is an

outlier. Excluding the WorldCom case, the mean fine is only $59.8 million. In recent years the

SEC has imposed larger fines in high-profile enforcement actions involving such firms as Qwest

Communications International ($250 million), Bristol-Myers Squibb Co. ($100 million), and the

Royal Dutch/Shell Group ($100 million).

Monetary penalties from shareholder class action lawsuits are much more common than

fines from regulators. KLM report that 39% of the firms in their sample paid class action

settlements, with a mean settlement of $37.7 million.

Although legal penalties sometimes are large, they are much smaller than firms’ share

value declines when their misconduct is revealed. Using the KLM (2008b) data, the mean legal

penalty equals only 3.1% of the total loss in the market values of the targeted companies. Class

action settlements account for an additional 5.4% of the loss. Together, these legal penalties

equal only 8.8% of the total dollar loss associated with the enforcement actions.

17

III.B. Share deflation to correct to full-information value

Another reason that news about financial misconduct decreases share values is that

investors learn that the firm’s accounting statements contain bad information. So the stock price

must be revalued using information that the firm previously was cooking its books. This can

affect investors’ view of the firm’s cash flow from operations or the growth in such flows. Here

is an example:

Suppose the Bunda Company is an all-equity firm with a book value of assets of $100 and a market-to-book ratio of 1.5. The market value of the firm's assets, and its stock, is therefore $150. But then assume that Bunda issues a misleading financial statement that overstates its asset values by $10. If the firm's market-to-book ratio stays the same, its share values will increase temporarily by ($10 x 1.5) to $165. But when the financial misrepresentation is discovered, Bunda's book values will adjust back to $100. And if there is no other impact, the share value will fall back to $150. That is, Bunda's shares will drop in value from their inflated value of $165 to their "correct" value of $150.

Things get more complicated if the market-to-book ratio depends on the firm’s reported assets,

as would be the case if investors’ views of the firm’s long-term growth depends on reported

financials.

Figure 2 illustrates the share price inflation for an actual firm. In early 1997 Xerox began

to inflate its reported earnings by accelerating its recognition of revenue on its equipment lease

contracts. Rather than recognizing revenue when lease payments were made, it booked the full

stream of expected lease payments when the lease agreement was made. The effect was to

increase near-term revenue and earnings. As illustrated in Figure 2, this reporting strategy

helped to boost Xerox’s share price for over two years. The only way such revenue-acceleration

schemes work is if the company generates sufficiently high real growth in sales to make up for,

and to cover up, the eventual shortfall in future periods. Xerox was unable to generate such high

18

sales growth, and eventually it had to recognize that it would not be able to cover up its

aggressive reporting practice. On October 8, 1999, the firm announced that its third quarter

earnings would not meet projections. Investors, inferring that the announcement was only the tip

of a larger problem, lowered their values of the company and the stock price fell immediately. In

the ensuing months, Xerox made additional disclosures of earnings problems, the SEC launched

an investigation of its reporting practices, and the firm eventually was penalized for

misrepresenting its financial statements.

Clearly, Xerox’s share price was artificially inflated during the period that its books were

in error. The share price decline, as investors found out about Xerox’s misconduct, was due in

part to the price returning to the level it would have been had Xerox never misrepresented its

financials in the first place. Measuring this share inflation – and deflation – is a central point of

argument in many securities class action lawsuits. I am aware, however, of only one published

attempt to develop a systematic estimate of the share price inflation. KLM (2008b) use a

multiple of the firm’s asset write-offs in the period after its misrepresentation is uncovered. The

multiple, in turn, is the median market-to-book ratio of firms in its 2-digit SIC industry.

Using this method, KLM estimate that, on average, 28.8% of the drop in share values is

due to this correction in firms’ artificially inflated share values. This is the amount by which

firms’ share values decline when their financial misconduct is discovered because investors have

more accurate information about the firm’s financial performance.4

4 In dollar terms, the 28.8% effect equals $54 million for the average firm. This indicates that, on average, share values were falsely inflated $54 million by the misrepresentation. The correction amount is based on the firm’s largest asset write downs during the total period the firm was under suspicion or investigation for financial misrepresentation. Many write downs are legitimate and unrelated to any cooking of the financial books. So the 28.8% figure is an overstatement of the correction amount. Nonetheless, even with such an overstatement our main observation – that the impaired operations and reputation slice of the pie is very large – is apparent.

19

In Figure 3 I apply the KLM method to illustrate the size of the share inflation and

deflation for Xerox. During the period Xerox was misrepresenting its revenues and earnings, its

share values increased. This is illustrated in stylized form by the green line. Immediately before

Xerox announced that third quarter 1999 earnings would be less than previously forecast, the

firm’s market capitalization was $16.864 billion. The cumulated loss in market cap, measured

over the sequence of events by which investors learned of the misconduct, was $5 billion,

leaving the company with a market cap (adjusted for market-wide movements) of $11.864

billion.

Of the $5 billion loss, the KLM method implies that $1.15 billion, or 23%, is the

deflation effect. This represents share values returning the level at which they hypothetically

would have been if no misrepresentation had occurred. An additional $0.523 billion of the loss

can be attributed to amounts Xerox paid in fines and to settle a class action lawsuit. The rest of

the loss – $3.3 billion – is due to something else. The most plausible explanation is that much,

even all, of the $3.3 billion is due to impaired operations and lost reputation – which I abbreviate

to simply “the reputational loss.”

III.C. The reputational loss from financial misconduct

The discovery of financial misconduct can impair the firm’s operations if its managers

are indicted, lose their jobs, or divert time and energy to the investigation rather than attending to

company business. The investigation also could force the firm to adopt new monitoring and

control policies that increase its cost of operations. Such higher costs of operation will lower the

firm's future earnings and result in a lower current value. In addition, the firm suffers a loss in

reputation that also lowers firm value.

20

The term “reputation” has many colloquial meanings. Merriam-Webster.com defines

“reputation” as:

1 a : overall quality or character as seen or judged by people in general

b : recognition by other people of some characteristic or ability

2: a place in public esteem or regard : good name

Here, I define reputation as the present value of the cash flows earned when an individual or firm

eschews opportunism and performs as promised on explicit and implicit contracts. It is the value

of the quasi-rent stream when accrues when counterparties offer favorable terms of contract as

insurance against being cheated.5

It is well established that firms that restate earnings or have financial reporting problems

face a higher cost of capital (e.g., see Hribar and Jenkins 2004, or Kravet and Shevlin 2010).

This occurs as investors charge a premium for their increased risk of investing in firms with poor

internal controls and/or managers who have displayed a willingness to behave opportunistically.

Graham, Li, and Qiu (2008) also show that lenders also charge higher rates to firms that have

restated earnings. And Murphy, Shrieves, and Tibbs (2009) show that misconduct firms also

have lower cash flows from operations.

Collectively, this evidence indicates that firms that misreport their financials lose

investors’ trust, pay a higher cost of capital, and may even experience lower cash flows from

operations. This is because at least some of these firm’s investors and counterparties do not want

to do business with a company that lied in its financial statements. Banks are reluctant to lend

the company money if they cannot trust the firm's financial statements. Existing lenders increase

their scrutiny of the company and become less flexible with their terms of credit. Suppliers tend

5 Klein and Leffler (1981) do not use the term “reputation.” Nonetheless, the reputation loss equals W2 in their model.

21

to be reluctant to offer the firm trade credit and could require that the firm pay cash for its

supplies. The firm's customers could even be affected, if the firm's bad publicity causes them to

doubt the firm's products and guarantees. For example, customers might place less faith in the

firm's guarantees to support warranties or to supply compatible services or parts in the future.

The sum total of all of these effects is what I call the firm’s reputational loss. The

reputational loss is the present value of the higher costs and/or lower revenues when firms are

discovered to have cheated their investors, suppliers, employees, or customers. It occurs because

of direct impairments to the firm’s ongoing operations, and also because counterparties alter the

terms with which they are willing to continue to do business with the firm.

But how costly are such effects? One measure is the portion of the firm’s total loss that

cannot be explained by other factors. By this measure, Xerox’s reputational loss was $3.33

billion, or 67% of its total loss. This is illustrated in Figure 3.

The Xerox example is close to the average from a large sample of firms that were

revealed to have cooked their books. Using a sample of 384 firms that faced SEC sanctions for

financial misrepresentation, KLM (2008b) estimate that 8.8% of these firms’ total losses were

due to legal penalties, 24.5% to share deflation, and 66.6% to lost reputation. This breakdown is

illustrated in Figure 4. Using median rather than mean values, limiting the sample to firms that

survived the enforcement process, or using alternate measures of the share deflation all yielded

similar or larger measures of the reputation loss.

Stated differently, KLM’s results indicate that firms can temporarily increase their share

values by misrepresenting their earnings and assets. When the misrepresentation is detected,

however, firm value decreases by more than the original inflation. For every dollar of inflated

value during the period that the firm’s books are in error, the firm loses that dollar when its

22

misrepresentation is uncovered. In addition, the firm loses an additional $3.08. Some of this

additional loss – 36¢ – is due to the legal penalties these firm’s incur. Most – $2.71 – is due to

lost reputation.

These results support the argument that financial reporting violations carry large

penalties. The largest penalties are not from regulators or private lawsuits. Rather, they are from

the firm’s investors and other counterparties. It is unlikely that investors and firm counterparties

intend, or even are aware, that they impose penalties on the offending firm. Rather, they simply

are protecting their own interests, requiring a premium to do business with firms that are less

trustworthy than they previously believed.

IV. Market value losses for other types of business misconduct

A large amount of research also has investigated whether there are significant share price

reactions to other types of business misconduct. The results are summarized in Table 2.

Here, the results are not as straightforward as for financial misconduct. Panel A reports

on eight studies that examine illegal corporate activities, including fraud, bribery, breach of

contract, securities fraud, patent infringement, environmental violations, price fixing, illegal

campaign contributions, tax evasion, and OSHA violations. Some find evidence of negative

stock price effects. Davidson and Worrell (1988), for example, report an average abnormal

return of -3.48% for a sample of 96 announcements of “corporate illegalities.” Reichart, Lockett,

and Rao (1996) and Bhagat, Bizjak, and Coles (1998) report statistically negative stock returns to

announcements of indictments or lawsuits for firm misbehavior. Overall, however, the size of

the share value losses are much smaller than reported in Table 1 for financial misconduct. Two

studies even report that the average share price reactions are not statistically significant.

23

A drawback of the results in Panel A is that they are drawn from samples that combine

different types of misconduct. Several studies, in contrast, examine only one type of misconduct,

or provide results on isolated types of misconduct. Panel B, for example, reports on four studies

that examine track the share price reaction to news that a firm defrauded or failed to perform as

contracted with a counterparty. As an example, during the 1980s BeechNut Corp. sold bogus

apple juice for babies(!). Labeled "100%" apple juice for infants, the product actually was a

concoction of water, sugar, artificial flavors, and food coloring. Eventually the fraud was

discovered and the company's President and V-P for operations were sentenced to jail. All four

of the studies in Panel B find that news of such misconduct is associated with share price

declines that range from 1-5%.

Panel C reports on studies that examine frauds of government. As an example, in the

1990s Rohr Inc. falsified test reports for the parts and adhesive materials used to attach the wings

onto two military aircraft, the Air Force C-5 transport plane and the Navy F-14 Tomcat fighter.

The prospect of wings falling off planes was too much for the Department of Defense, and Rohr

Inc. eventually pleaded guilty to eight counts of making false statements.6 Again, the results of

these studies indicate that news of such misconduct is associated with small but statistically

significant share price declines.

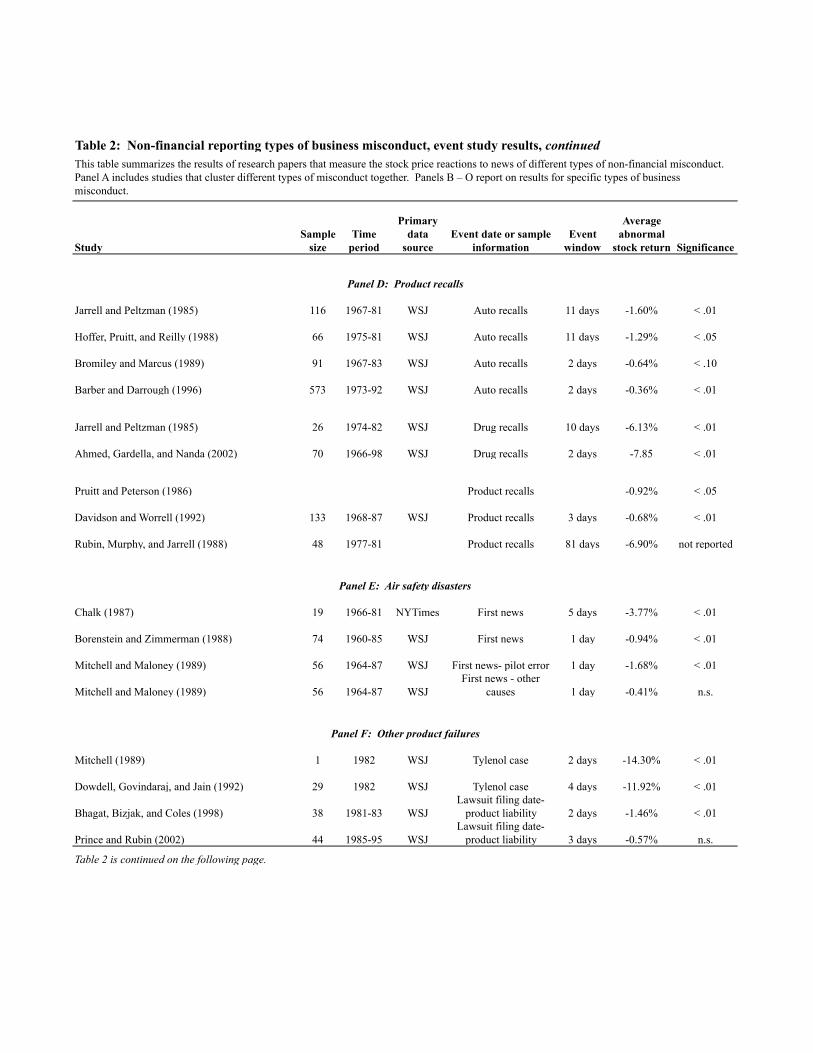

Several papers have examined product recalls. While not necessarily the result of

intentional misconduct, a product recall represents at least some degree of failure by the firm to

deliver on its explicit or implicit guarantee to provide a safe and reliable product. Recalls in the

automobile industry are associated with small stock price declines. The point estimate from

Barber and Darrough (1996), who examine the largest sample of the papers in this group, is -

6 In a similar case in 1991, General Motors' Hughes Aircraft division falsified tests of the electronic circuits used in aircraft and missile guidance systems. This raises horrible images of missiles going to the wrong targets because of an error in the guidance system!

24

0.36%. The effects of a drug recall announcement is larger, averaging from 6%-8% (see Jarrell

and Peltzman 1985; Ahmed, Gardella, and Nanda 2002).

Three papers in Panel E examine a variety of product recalls. Pruitt and Peterson (1986)

and Davidson and Worrell (1992) conclude that the average stock price reaction is negative but

less than 1% in magnitude. Using a long event window, Rubin, Murphy, and Jarrell (1988)

report an average stock price reaction of -6.9%.

An airplane crash represents an extreme abrogation of the firm’s guarantee to provide a

safe product or service. Three studies listed in Panel F measure airlines’ loss in value when a

plane crashes. Chalk (1987) and Borenstein and Zimmerman (1988) find that share values

decline. Mitchell and Maloney (1989) show that the loss depends on the cause. When pilot error

is to blame, the airline suffers a statistically significant loss of 1.68%. When external factors are

blamed for the crash, such as the weather, the stock price change is statistically insignificant.

Panel G summarizes the results of other types of product failures. Mitchell (1989) and

Dowdell et al. (1992) examine a 1982 case of product tampering, in which capsules of Tylenol

were laced with cyanide and seven people died. This case is noteworthy because both customers

and the manufacturer, Johnson & Johnson, were victimized by the perpetrator. Even though it

was not directly responsible, however, Johnson & Johnson experienced a significant decline in

share values.

Bhagat, Bizjak, and Coles (1998) and Prince and Rubin (2002) measure the stock price

reactions to announcements that lawsuits have been filed seeking damages for product liability.

The reactions are negative and small in magnitude, and are statistically significant only in the

Bhagat et al. sample.

25

Another example of a product failure is a breach of security among software and database

providers. Such breaches can result in the public dissemination of clients’ and customers’

personal information. As shown in Panel I, most studies find that security breaches result in

small or statistically insignificant stock price reactions. Breaches that expose confidential

information, in contrast, are more likely to result in significant share price declines for the

offending firm.

Panels K through O of Table 2 report findings for employee-related misconduct, false

advertising, investigations of IPO underwriters, punitive damage-seeking lawsuits, antitrust

violations, and price fixing. All are associated with statistically significant declines in share

values.

The results in Panels H and I, however, are mixed. Panel H reports the results of seven

investigations of environmental violations. A typical example of such violations is a case

involving Tyco International, Inc. From 1999 to 2001, employees of a Tyco subsidiary dumped

wastewater containing high levels of lead, copper, oil, and other chemicals into the public water

treatment systems of two cities in Connecticut. In an attempt to cover up its pollution, company

employees altered wastewater samples and falsified reports to the U.S. Department of

Environment Protection. In several papers, news of such violations is associated with negative

share price reactions. But other researchers conclude that the average share price reaction is

statistically insignificant.

Panel I reports on investigations into violations or frauds that affect unrelated parties, i.e.,

not parties with whom the firm does business. Examples include violations for check kiting or

failure to report currency transactions.

26

V. Reputational losses for other types of business misconduct

The results in Table 2 indicate that, frequently, news that a firm had engaged in some

type of misconduct is associated with a decline in its share values. This indicates that investors

regard such news as costly for most firms. But what is the source of the cost? Firms that

defraud customers, for example, are likely to face regulatory penalties and class action lawsuits.

In fact, the sizes of such legal penalties can be substantial. Murphy, Shrieves, and Tibbs (2009)

report that the mean legal fine for firms that commit frauds that affect related parties (as in Panel

B of Table 2) is $18.79 million. For violations that affect third parties (Panel K), the mean fine

is $32.87 million. Karpoff, Lee, and Vendrzyk (1999) report that defense procurement frauds

triggered fines that average $8.0 million plus required restitution of $4.4 million. Not all legal

penalties are as large. Cohen (1992) reports that the penalties for antitrust violations, for

example, average $0.3 million in fines plus an additional $0.1 million in restitution.

To tease out the importance of reputational losses, it is essential to examine whether the

share value losses can be explained by such legal penalties, or other losses that occur when a

firm’s misconduct is revealed. Other losses include any losses from having to abandon the

activities that were revealed. For example, Van den Broek, Kemp, Verschoor, and de Vries

(2010) consider the effect on the firms’ conspiracy-related profits when estimating the

reputational loss from antitrust actions.

Many of the researchers cited in Table 2 have made attempts to distinguish between share

value losses and the different types of penalties that they reflect. Table 3 summarizes the

qualitative assessments made by authors who have sought to shed light on the size of any

reputational loss. The estimates of reputational loss are positive for frauds of related parties,

some frauds of government, false advertising, product recalls, air safety disasters, other product

27

failures, employee discrimination or safety problems, punitive damage awards, and antitrust

violations. Researchers have concluded that reputational losses do not arise, however, for

environmental violations, security breaches, and regulatory violations or frauds affecting

unrelated parties.

To illustrate the nature of such conclusions, consider environmental violations. Jones and

Rubin (2001) find that, among a sample of public utility companies, news of an environmental

violation is not associated with a decline in share values, on average. They conclude that there

must be very little reputational loss for these companies. Karpoff, Lott, and Wehrly (2005), in

contrast, find that the average share price reaction is negative in their broader sample of

environmental violations. However, they also find that the legal penalties for the firms in their

sample are of similar magnitude to the share value losses. Violations affecting air quality during

the 1980s and 1990s, for example, resulted in an average fine of $31.7 million (in constant 2002

dollars). In addition, the guilty companies were required to incur costs averaging $123 million to

comply with air quality rules or to remediate the damage of their pollution. Firms that were

responsible for contaminated sites faced an average penalty of $11.0 million and a clean-up cost

of $108 million. While firms that are caught contaminating air, water, or land resources face

significant costs, these costs are all those imposed by regulators and the courts. Since these costs

fully explain the defendant firms’ losses in share values, they conclude that the reputational loss

from violating environmental rules is negligible, on average.

A number of researchers have made quantitative assessments of the importance of

reputational losses. These results are summarized in Figure 5. When more than one set of

researchers provides information from which a reputational loss can be estimated, I present the

average of the loss estimates.

28

Averaging over the estimates from three studies, 70% of firms’ losses from financial

misrepresentation can be attributed to lost reputation. Reputational losses also explain large

portions of the losses that accrue from several other types of misconduct. The largest

reputational loss component is for punitive damage lawsuits. I note, however, that such lawsuits

include many different types of misconduct, from fraud to business negligence to defective

products. So there is some overlap between the events in the punitive lawsuit category and other

types of misconduct. For these types of wrongdoing, the penalties imposed through legal fines,

penalties, and damage awards are dwarfed by the huge reputational losses these firms

experience. For security breaches, environmental violations, and unrelated party violations, in

contrast, reputation plays a negligible role.

VI. How reputation encourages greater quality assurance

VI.A. How reputational capital discourages opportunism

To understand why reputational losses are large for some types of misconduct and not for

others, it is important to understand how and why reputational losses occur at all. Consider the

following questions:

• When you travel, do you dine at local eateries or well-known chain restaurants?

• When did you last buy a car? Did you go to a new-car dealer or a used-car dealer? Did

you buy through a newspaper ad?

• When you buy over-the-counter medicines (say, acetaminophen), do you buy brand name

products like Tylenol™, or generic products?

• When you buy acetaminophen for an infant child, do you buy brand name products or

generic products?

29

The fact that peoples’ answers differ illustrates how reputation works and why reputational

losses can occur when companies behave opportunistically.

Consider consumers’ choices of restaurants when they travel. Adventurous travelers who

eat at a local Joe's Diner might experience a gastronomic delight – or they might get Ptomaine

poisoning. That is, without local knowledge the traveler faces a high-variance outcome. To

avoid such uncertainty, many travelers prefer to eat at a chain restaurant – say, McDonalds.

McDonalds and other chain restaurants sell not only hamburgers and fries, but also a high level

of quality assurance. Note that high quality assurance is not the same thing as high quality.

Rather, it is a high level of certainty about what the buyer is going to receive. People who eat at

McDonalds know with a high degree of certainty what they are going to get, even if they are not

in their hometowns.

Not surprisingly, McDonalds has invested heavily to provide its customers a high level of

certainty in their products. Through its training and franchising procedures, the company works

to assure that its dining experience meets a certain standard and that its customers will not be

surprised. In return, the company is rewarded with customers who return again and again.

Notice that McDonalds could decide to cut corners and sell its customers poorer fare than it has

promised. But to do so would be to alienate its customers and see its sales dry up. In other

words, McDonalds has high reputational capital, just like other firms have high physical capital.

If McDonalds were to cheat its customers its reputational capital would depreciate. That is, the

firm would suffer a reputational loss, as it would lose future sales and the profits that come with

them.7

7 The literature on franchising emphasizes the role that the franchise contract plays in discouraging franchisees from free-riding on the brand name, and in encouraging a standardized product (e.g., see Klein 1995).

30

Similar concerns explain why some people buy automobiles through established car

dealers, while others purchase through newspaper ads. One difference between a car dealer and

a private seller is the degree of reputation at stake. Car dealers who sell lemons risk losing future

sales. For a private seller using a newspaper ad, in contrast, little reputation is at risk. People

who buy from a private person through a newspaper ad prefer not to pay the price premium that

accompanies a dealer's higher reputation – the quasi-rent that Klein and Leffler (1981) show

serves as incentive to not cheat. Such buyers might have automotive skills that allow them to

assess the car's quality without having to rely on a dealer's reputation. Or, since quality

assurance is an income-normal good, consumers who buy from low-reputation outlets might

simply have low incomes and low demands for quality assurance.

We observe similar differences in the sale and purchase of acetaminophen. Some

consumers like the higher level of certainty that comes from buying a brand name like

Tylenol™. They know, or at least intuit, that Tylenol™ has more to lose if it screws up and

delivers poor quality acetaminophen. Sellers of generic acetaminophen, in contrast, face smaller

reputational losses if they do not deliver the promised quality.

From sales figures, we can see that some people buy generic acetaminophen for

themselves but brand-name acetaminophen for their children. These consumers apparently place

a lower value on certainty when buying acetaminophen for themselves than when they buy

acetaminophen for their children. They know, at least implicitly, that brand-name sellers like

Tylenol™ would suffer large reputational losses if there are problems with their products, so

they are likely to control their production and distribution procedures with more care. Some

buyers are willing to pay a bit more for the extra quality assurance.

31

VI.B. Cross-sectional differences in reputational losses

These examples illustrate why different sellers face different reputational losses if they do

not deliver the products they promise to deliver. Similarly, some types of misconduct expose

companies to greater reputational losses than others. Lying to investors by misrepresenting

financial statements triggers large reputational losses. So does defrauding customers, as with the

incident in which BeechNut sold fake juice that was labeled "100% pure" apple juice. In such

incidents, the perpetrator reveals itself to be untrustworthy. Companies that defraud customers

therefore tend to lose sales. Those that cheat employees or other suppliers face higher input

costs or lost trade credit. And those that lie to their investors face higher financing costs.

Reputational losses are not uniformly high, however. As indicated in Figure 5, they are

negligible, on average, for firms that violate environmental laws. For these types of misconduct,

firms' losses in share values are attributable wholly to their legal penalties.

This is most apparent from the empirical results regarding environmental violations. In

theory, firms that violate environmental rules could suffer reputational losses, if consumers and

suppliers refuse to do business with environmentally unfriendly firms. After the 1989 Exxon

Valdez oil spill, for example, some consumers cut up their Exxon credit cards and vowed to buy

gasoline from other vendors. The data, however, show that, on average, any reputational loss

from harming the environment is negligible. Jones and Rubin (2001) and Karpoff, Lott, and

Wehrly (2005) argue that this is because firms who violate environmental rules do not impose

costs on parties with whom they do business. As an example, downstream fishermen are

damaged if an electroplating company dumps toxic chemicals into a municipal storm sewer. But

the fishermen do no business with the firm, and the firm’s customers have no direct incentive to

32

lower their demands for the firm’s products if the dumping does not affect the quality of those

products. As a result, the polluting electroplating company experiences no reputational costs.

A similar argument holds for frauds of unrelated parties. Although such actions as check

kiting are against the law, it is not evident that any of the parties with whom the firm does

business are harmed by the activity. As a result, when firms are caught violating these types of

rules they may face legal penalties. But since they do not directly harm their customers,

investors, or suppliers, they do not suffer a reputational loss. That is, investors do not expect

them to lose sales or face higher operating costs.

V.C. How reputational losses show up in firms' operations

The evidence implies that firms engaging in many types of misconduct incur large

reputational losses. This evidence is based, however, on observations that share prices decline

when investors find out about the misconduct. But are investors correct? That is, do reputational

losses actually show up in firms' subsequent performance? Do these firms subsequently lose

business, incur higher costs, or experience a higher cost of capital?

The research on this question is still developing. But a number of findings are consistent

with the event study results. For example, Karpoff and Lott (1993) find that firms charged with

defrauding customers and other stakeholders do in fact have lower operating earnings over the

following five years. Alexander (1999) reports that 57% of such firms experience termination or

suspension of specific contracts. However, such business losses occur only following frauds of

parties with whom the firm does business. Offenses against other parties with whom the firm

does not do business, in contrast, do not lead to a high rate of lost sales. Similarly, Murphy,

33

Shrieves, and Tibbs (2009) find that allegations of illegal acts are accompanied by a significant

decrease in firms' earnings and an increase in uncertainty over future earnings.

There is fairly strong evidence that financial misconduct results in a higher cost of capital

for the firm. Hribar and Jenkins (2004), Kravet and Shevlin (2010), and others show that the

cost of equity capital increases for firms that restate earnings. And Graham, Li, and Qiu (2008)

show that bank lender rates increase for restating firms.

Several papers document direct evidence of reputational losses. Beatty, Bunsis, and

Hand (1998) find direct evidence of operating losses for investment bankers that are investigated

by the SEC for problems in bringing IPO firms to the public market. These firms experience

sharp decreases in their shares of the IPO underwriting market after they are targeted by an SEC

investigation. The share prices of these firms' client companies also decline, indicating that the

decrease in the investment banker's reputation affects its clients as well.

One place in which we would expect to see important reputational effects is in online

auctions. Here, buyers deal with sellers they do not know and cannot even see. So we would

expect that sellers with high reputations would charge higher prices than others. Such price

premiums are the amounts that some buyers willingly pay for the guarantee that they will not be

ripped off. And the chance to earn such premiums is sufficient to encourage most high-

reputational sellers to deliver on their promise not to cheat buyers.

Consistent with such expectations, evidence indicates that high-reputation sellers on eBay

do in fact sell at higher prices than others, even for the same items. For example, Resnick,

Zeckhauser, Swanson, and Lockwood (2002) find that the prices of vintage postcards on eBay

average 7.6% higher for sellers with high reputation than for other sellers – even for the exact

same postcards. Dewally and Ederington (2002) find similar results for comic books sold on

34

eBay. The impact of a seller's reputation on price is particularly great when the quality of the

comic book has not been certified by a third party.

Finally, several findings indicate that managers who involve their companies in financial

misconduct end up losing their jobs. Jayaraman, Mulford, and Wedge (2004) find that managers

of firms that are subjects of SEC Accounting and Auditing Enforcement Releases tend to be

displaced at an unusually high rate. Desai, Hogan, and Wilkins (2006) and Agrawal and Cooper

(2007) find that managers of firms that have to restate their earnings share similar fates. KLM

(2008a) report that 92% of managers who the SEC identifies as involved in financial

misrepresentation lose their jobs; 81% lose their jobs even before the SEC imposes any

sanctions.

VII. Ten questions for further research

Opportunistic behavior by buyers and sellers, or its potential, can impede exchange. At

the extreme, it has the potential to cause markets to break down, impeding trade and increasing

poverty. At the beginning of this survey I noted that, when self-interested behavior includes

lying, cheating, stealing, or opportunistic gaming, Adam Smith’s invisible hand might not work

to channel private motivation into social gain.

Economists have long appreciated that repeat contracting has the potential to ameliorate

this problem. In theory, people and firms invest in and develop reputations that encourage others

to trust that they will not be cheated. It is difficult to measure reputation, however, and the

importance of reputation as a guarantor of honest dealing is an empirical matter.

As a way to gain insight into the importance of reputation, a number of researchers have

examined instances in which firms might be expected to lose reputation – that is, when they are

35

discovered to have engaged in illegal or opportunistic activities. The evidence indicates that

firms lose market value when they are caught in many types of misconduct, including financial

misrepresentation and frauds of related parties. A subset of researchers in this area have

attempted to understand the nature of such losses by partitioning them into portions that can be

explained by legal penalties, share price deflation, or lost cheating profits. The portion that

remains unexplained is used as a measure of reputational losses.

Using this approach, the evidence indicates that firms experience significant reputational

losses when their misconduct imposes costs on their counterparties. Firms that cook their

financial books face a higher cost of capital, and firms that cheat customers lose sales. For some

types of misconduct, however, there appear to be few reputational losses. A notable example is

environmental violations. Firms that violate, say Clean Air Act rules about emissions, appear

not to lose sales or face higher financing costs. This implies that reputation and market forces

play a small role in disciplining environmental violations, and that regulations and legal penalties

play a more important role.

To the extent that reputation plays an important role in encouraging honest dealing, it

offers a relatively low-cost solution to the lemons problem and facilitates the operation of Adam

Smith’s invisible hand. As such, understanding whether and how reputation helps to enforce

contractual performance is a vital part of understanding the extent to which markets work or do

not work.

The earliest papers cited in this review are over 20 years old. Nonetheless, the empirical

research on reputational losses has only begun to provide a picture of reputation’s role in

facilitating the development of markets and economic growth. I conclude by offering a list of

ten questions for future research. Work on these questions can begin to fill out the gap between

36

our theoretical understanding of reputation and the way it actually plays different roles in

different markets.

1. How important are reputational penalties around the world? This can help to explain the

extent to which market forces encourage honest dealing and facilitate the working of the

invisible hand.

2. What is the probability of getting caught for different types of misconduct? This can help

to explain the trade-off managers face when considering opportunistic actions. It also can help

guide public policy toward optimal penalties.

3. Given that reputational losses are important for some but not all types of misconduct, do

legal penalties conform to optimality conditions?

4. How do reputational penalties interact with public and private (lawsuit) enforcement of

securities and other laws?

5. How and when do firms rebuild damaged reputation?

6. What explains cross-sectional differences in reputational penalties?

7. Who detects corporate misconduct?

8. How do event-study measures of reputational penalties correspond to lower cash flows or

higher costs?

9. Given the legal and reputational losses from getting caught, why do managers engage in

illegal activity?

10. How does corporate governance affect the likelihood and cost of opportunistic behavior

by corporations?

37

References

Acquisti, Alessandro, Allan Friedman, Rahul Telang, 2006, Is there a cost to privacy breaches? An event study, Proceedings of the International Conference of Information Systems (ICIS) 2006. Agrawal, Anup, and Sahiba Chadha, 2005, Corporate governance and accounting scandals, The Journal of Law and Economics, 48, 371–406. Ahmed, Parvez, John Gardella, and Sudhir Nanda, 2002, Wealth effect of drug withdrawals on firms and their competitors, Financial Management, 31, 21-41. Akhigbe, Aigbe, Ronald J.Kudla, and Jeff Madura, 2005, Why are some corporate earnings restatements more damaging, Applied Financial Economics, 15, 327–336. Alexander, Cindy, 1999, On the nature of the reputational penalty for corporate crime: evidence, The Journal of Law and Economics, 42, 489-526. Anderson, Kirsten L., and Teri Lombardi Yohn, 2002, The effect of 10-K restatements on firm value, information asymmetries, and investors’ reliance on earnings, Working paper, Georgetown University. Arthaud-Day, Marne L.., S. Trevis Certo, Catherine M. Dalton, and Dan R. Dalton, 2006, A changing of the guard: Executive and director turnover following corporate financial restatements, Academy of Management Journal, 49, 1119–1136. Barber, Brad M., and Masako N. Darrough, 1996, Product reliability and firm value: The experience of American and Japanese automakers, 1973-1992, The Journal of Political Economy, 104, 1084-1099. Baucus, Melissa S., and David A. Baucus, 1997, Paying the piper: An empirical examination of longer-term financial consequences of illegal corporate behavior, Academy of Management Journal, 40, 129-151. Beatty, Randolph P., Howard Bunsis, and John R.M. Hand, 1998, The indirect economic penalties in SEC investigations of underwriters, Journal of Financial Economics, 50, 151-186. Beneish, Messod D., 1999, Incentives and Penalties Related to Earnings Overstatements that Violate GAAP, The Accounting Review, 74, 425-457. Bernile, Gennaro, and Gregg A. Jarrell, 2009, The impact of the options backdating scandal on shareholders, Journal of Accounting and Economics, 47, 2-26. Bhagat, Sanjai, and Roberta Romano, 2002, Event studies and the law: Part II: Empirical studies of corporate law, American Law and Economics Review, 4, 380-423. Bhagat, Sanjai, James A. Brickley and Jeffrey L. Coles, 1994, The Costs of Inefficient Bargaining and Financial Distress, Journal of Financial Economics, 35, 221-247. Bhagat, Sanjai, John M. Bizjak, and Jeffrey L. Coles, 1998, The shareholder wealth implications of corporate lawsuits, Financial Management, 27, 5-27. Block, Michael K., 1991, Optimal penalties, criminal law and the control of corporate behavior, Boston University Law Review, 71, 395, 414-415. Bonner, Sarah E., Zoe-Vonna Palmrose, and Susan M. Young, 1998, Fraud type and auditor litigation: an analysis of SEC accounting and auditing enforcement releases, The Accounting Review, 73, 503-532. Borenstein, Severin, and Martin B. Zimmerman, 1988, Market incentives for safe commercial airline operation, American Economic Review, 78, 913-935.

38