risk management for enterprises and individuals chapter 21 employment-based and individual longevity...

TRANSCRIPT

RISK MANAGEMENT FOR ENTERPRISESAND INDIVIDUALS

Chapter 21Employment-Based and

Individual Longevity RiskManagement

1 - 2© 2010 Flat World Knowledge, Inc. 21 - 2© 2010 Flat World Knowledge, Inc.

Learning Objectives

In this chapter, we elaborate on the following:Distinguishing aspects of qualified retirement plansVarious qualified plans available through employers or

on an individual basisKey features of annuitiesEmployer’s pension plan funding options

1 - 3© 2010 Flat World Knowledge, Inc. 21 - 3© 2010 Flat World Knowledge, Inc.

The Nature of Qualified Pension Plans

Qualified plan: Type of retirement plan whereEmployer contributions to an employee’s pension

during the employee’s working years are deductible as a business expense and not taxable income to the employee until they are received as benefits.

Investment earnings on funds held by the trustee for the plan are not subject to income taxes as they are earned.

1 - 4© 2010 Flat World Knowledge, Inc. 21 - 4© 2010 Flat World Knowledge, Inc.

The Nature of Qualified Pension Plans

Nonqualified planDoes not allow employer funding contributions to be

deducted as business expenses unless classified as compensation to the employee

Investment fund earnings are also subject to taxationRetirement benefits are deductible business expenses

when paid to the employee (if not previously classified as compensation)

1 - 5© 2010 Flat World Knowledge, Inc. 21 - 5© 2010 Flat World Knowledge, Inc.

ERISA Requirements for Qualified Pension Plans

To be qualified, a plan must fulfill specific requirements enforced by the United States Internal Revenue Service, the United States Department of Labor, and the Pension Benefit Guaranty Corporation (PBGC).

1 - 6© 2010 Flat World Knowledge, Inc. 21 - 6© 2010 Flat World Knowledge, Inc.

ERISA Requirements for Qualified Pension Plans

The main items covered by ERISA and subsequent laws and amendments are:Employee rightsReporting and disclosure rulesParticipation coverageVesting; FundingFiduciary responsibilitiesAmounts contributed or withdrawnNondiscriminationTax penalties

1 - 7© 2010 Flat World Knowledge, Inc. 21 - 7© 2010 Flat World Knowledge, Inc.

Eligibility and Coverage Requirements

Under ERISA, the minimum eligibility requirements are the attainment of age 21 and one year of service.

The Age Discrimination in Employment Act eliminates all maximum age limits for eligibility.

ERISA has coverage requirements that are designed to improve participation by nonhighly compensated employees.

1 - 8© 2010 Flat World Knowledge, Inc. 21 - 8© 2010 Flat World Knowledge, Inc.

Retirement Age Limits

Normal retirement age: The age at which full retirement benefits become available to retirees; age 65 in most private retirement plans.

Early retirement may be allowed, but that option must be specified in the pension plan description.

1 - 9© 2010 Flat World Knowledge, Inc. 21 - 9© 2010 Flat World Knowledge, Inc.

Vesting Provisions

Vesting specifies the extent of employee’s right to benefits for which the employer has made contributions, subject to ERISA, EGTRRA 2001, TRA86, and other federal requirements.

Vesting schedules for defined contribution and defined benefit plans are cliff vesting and graded vesting.

1 - 10© 2010 Flat World Knowledge, Inc. 21 - 10© 2010 Flat World Knowledge, Inc.

Nondiscrimination Tests

The employer’s plan must meet one of the following coverage requirements:Percentage ratio testAverage benefit test

1 - 11© 2010 Flat World Knowledge, Inc. 21 - 11© 2010 Flat World Knowledge, Inc.

Distributions

Distributions are benefits paid out to participants or their beneficiaries, usually at retirement.

Tax penalties are imposed on plan participants who receive distributions (except for disability benefits) prior to age 59½.

The longest time period over which benefits may extend is the participant’s life expectancy.

ERISA requires that pension plan design make spousal benefits available through preretirement survivor annuity and joint and survivor annuity.

1 - 12© 2010 Flat World Knowledge, Inc. 21 - 12© 2010 Flat World Knowledge, Inc.

Loans

The loan provisions require that an employee can take only up to 50 percent of the vested account balance for not more than $50,000.

The number of loans is not limited as long as the total amount is within the required limits.

1 - 13© 2010 Flat World Knowledge, Inc. 21 - 13© 2010 Flat World Knowledge, Inc.

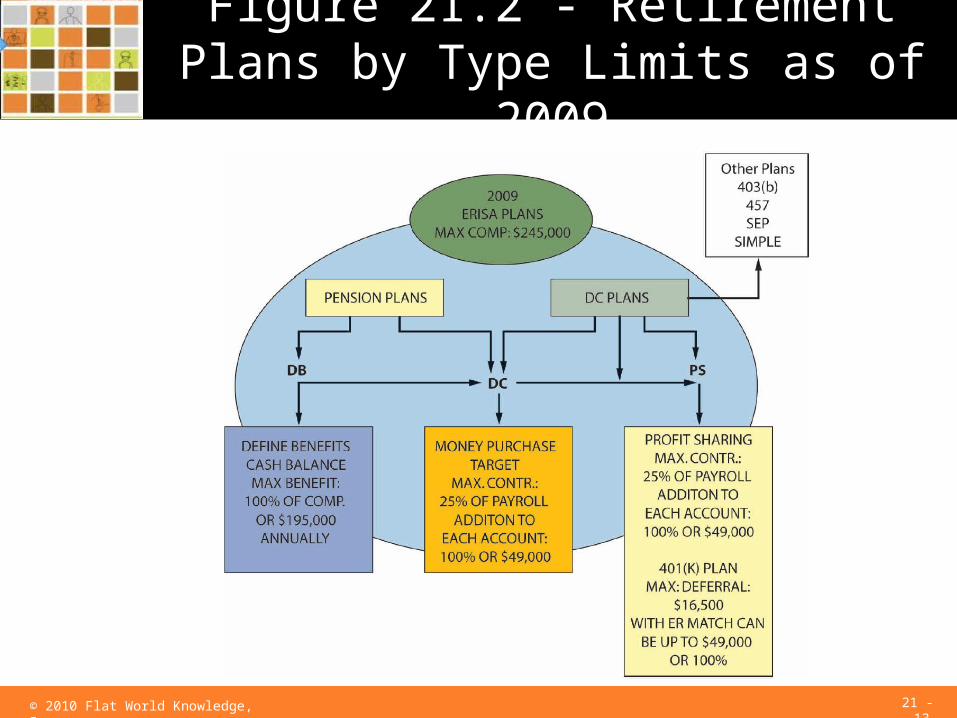

Figure 21.2 - Retirement Plans by Type Limits as of 2009

1 - 14© 2010 Flat World Knowledge, Inc. 21 - 14© 2010 Flat World Knowledge, Inc.

Defined Benefit Plans

Type of pension plan that assures employees of a certain amount at retirement, leaving all risk to the employer to meet the specified commitment; accumulated funds for all participants are managed in one account.Traditional defined benefit planCash balance plan

1 - 15© 2010 Flat World Knowledge, Inc. 21 - 15© 2010 Flat World Knowledge, Inc.

Features of defined benefit plansAll defined benefit plans may provide for adjustments

to account for inflation during the retirement years.Many plans integrate the retirement benefit with Social

Security benefits.

Defined benefit cost factorsNormal costsSupplemental costs

Defined Benefit Plans

1 - 16© 2010 Flat World Knowledge, Inc. 21 - 16© 2010 Flat World Knowledge, Inc.

Defined Contribution Plans

A defined contribution (DC) plan is a qualified pension plan in which the contribution amount is defined but the benefit amount available at retirement varies.

The most common type of defined contribution plan is the money purchase plan.

Other Qualified Defined Contribution PlansProfit sharing plans401(k) Plans

1 - 17© 2010 Flat World Knowledge, Inc. 21 - 17© 2010 Flat World Knowledge, Inc.

403(b) and 457 plansKeogh plansSimplified employee pension plansSimple plansTraditional IRA and Roth IRARoth 401(k) and Roth 403(b) plans

Other Qualified Plans

1 - 18© 2010 Flat World Knowledge, Inc. 21 - 18© 2010 Flat World Knowledge, Inc.

Annuities

Life annuity: Contract in which the duration of payment from an annuity depends upon the expected length of a life or lives.

1 - 19© 2010 Flat World Knowledge, Inc. 21 - 19© 2010 Flat World Knowledge, Inc.

Parties to an Annuity

Owner: The person or entity that purchases an annuity.

Annuitant: The person on whose life expectancy payments are based.

Beneficiary: The person or entity who receives any death benefits due at the death of the annuitant.

1 - 20© 2010 Flat World Knowledge, Inc. 21 - 20© 2010 Flat World Knowledge, Inc.

Mechanics of Annuities

Accumulation Versus LiquidationFixed-dollar annuityVariable annuity

Premium PaymentsCommencement of Benefits

Immediate annuityDeferred annuity

Level of Benefits

1 - 21© 2010 Flat World Knowledge, Inc. 21 - 21© 2010 Flat World Knowledge, Inc.

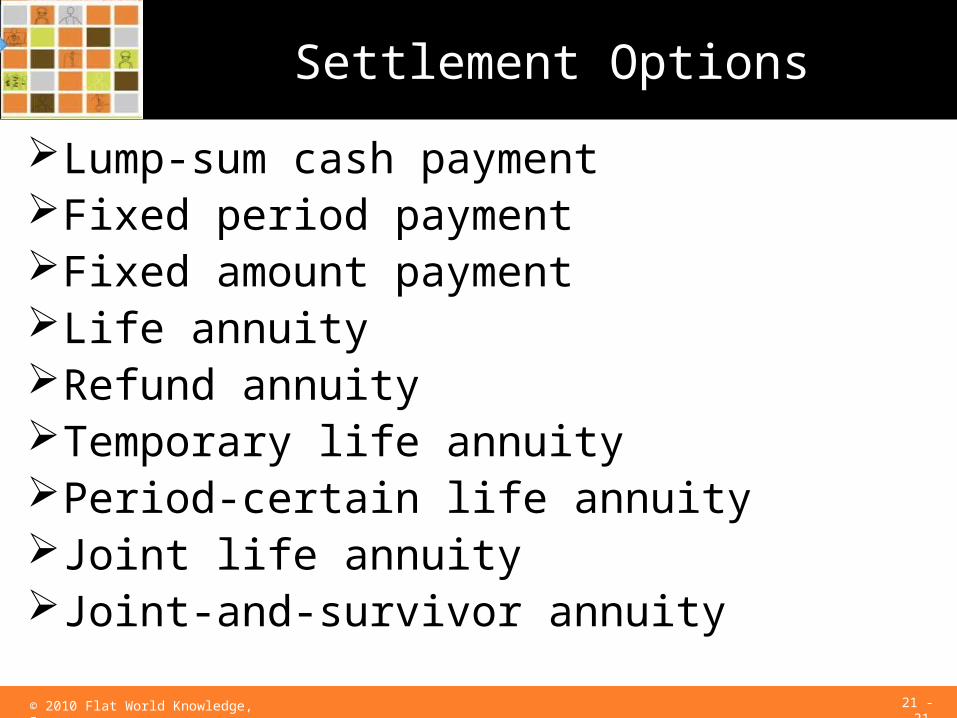

Settlement Options

Lump-sum cash paymentFixed period paymentFixed amount paymentLife annuityRefund annuityTemporary life annuityPeriod-certain life annuityJoint life annuityJoint-and-survivor annuity

1 - 22© 2010 Flat World Knowledge, Inc. 21 - 22© 2010 Flat World Knowledge, Inc.

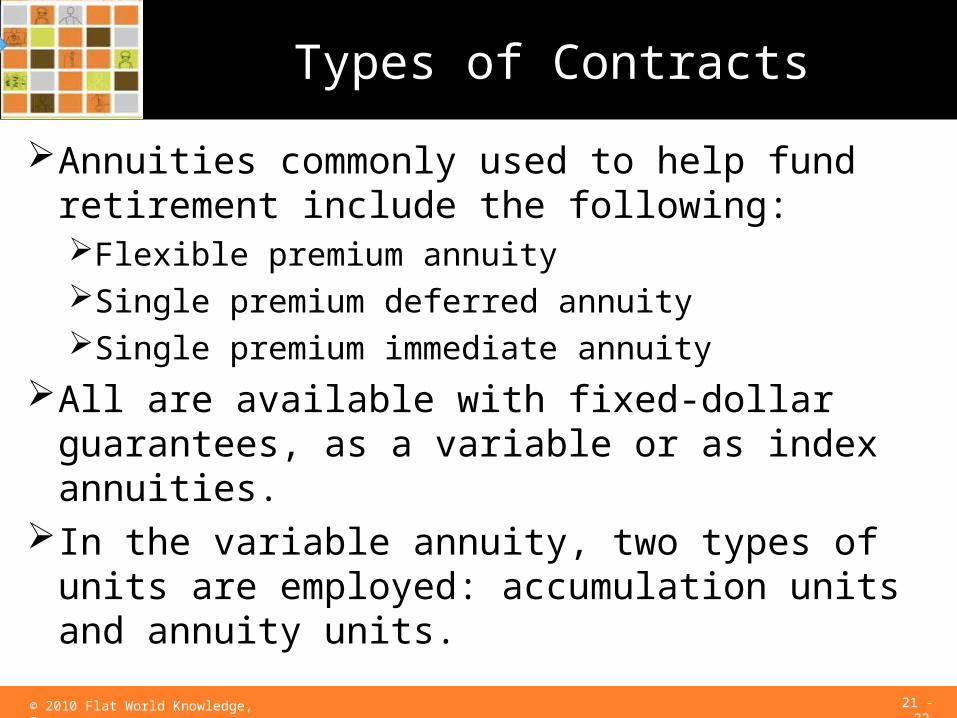

Types of Contracts

Annuities commonly used to help fund retirement include the following:Flexible premium annuitySingle premium deferred annuitySingle premium immediate annuity

All are available with fixed-dollar guarantees, as a variable or as index annuities.

In the variable annuity, two types of units are employed: accumulation units and annuity units.

1 - 23© 2010 Flat World Knowledge, Inc. 21 - 23© 2010 Flat World Knowledge, Inc.

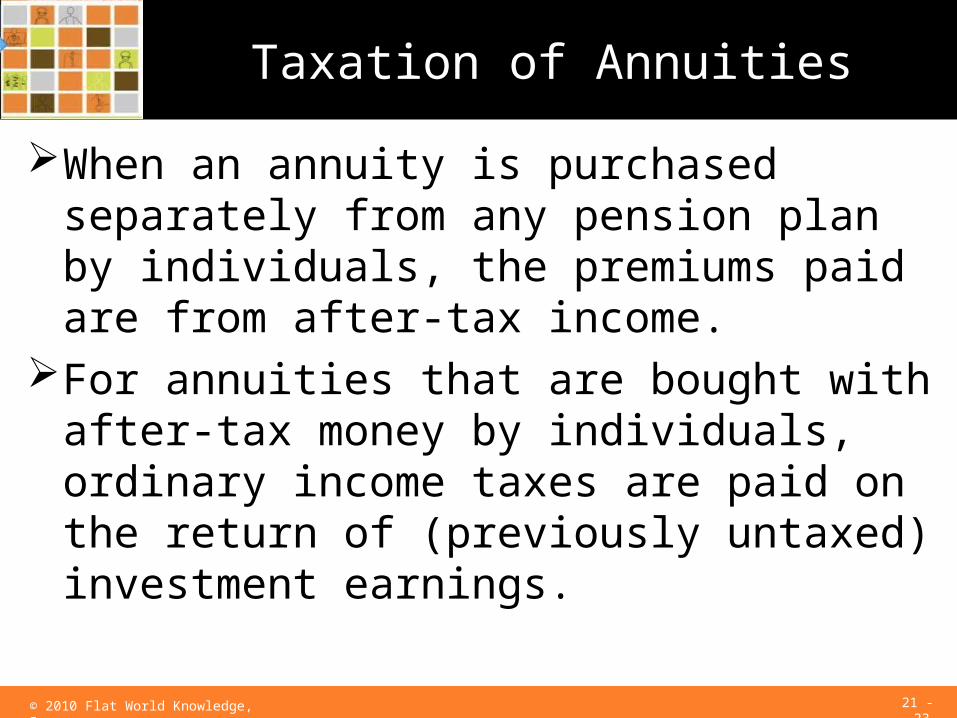

Taxation of Annuities

When an annuity is purchased separately from any pension plan by individuals, the premiums paid are from after-tax income.

For annuities that are bought with after-tax money by individuals, ordinary income taxes are paid on the return of (previously untaxed) investment earnings.

1 - 24© 2010 Flat World Knowledge, Inc. 21 - 24© 2010 Flat World Knowledge, Inc.

Taxation of Annuities

Exclusion ratio: Expression of annuity payments during distribution as taxable and nontaxable portions and calculated as: investment in contract divided by expected return.

1 - 25© 2010 Flat World Knowledge, Inc. 21 - 25© 2010 Flat World Knowledge, Inc.

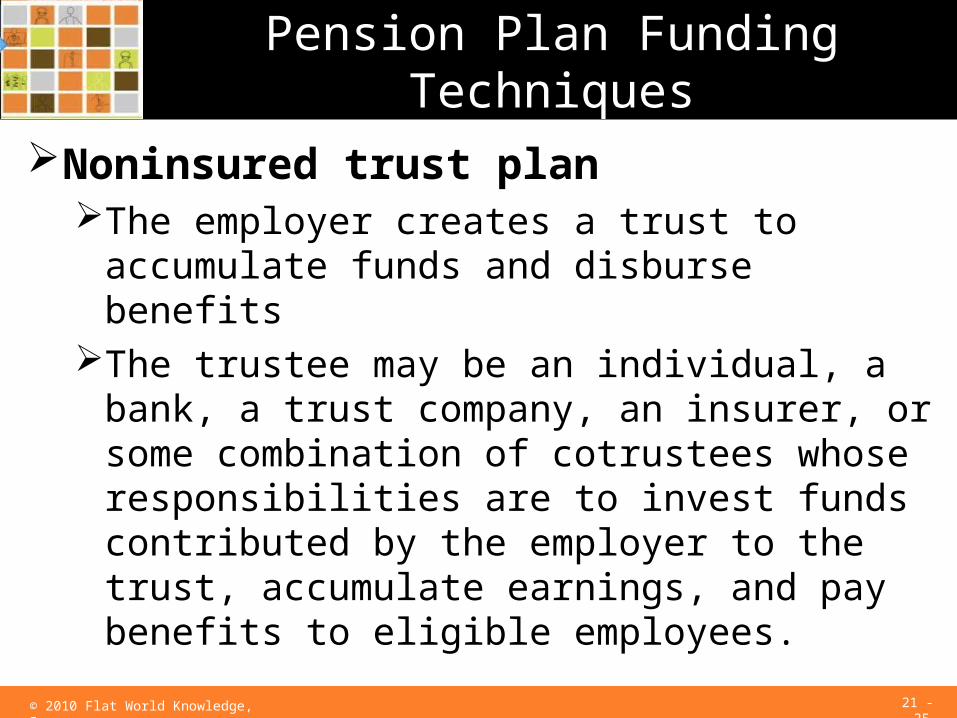

Pension Plan Funding Techniques

Noninsured trust planThe employer creates a trust to accumulate funds and

disburse benefitsThe trustee may be an individual, a bank, a trust

company, an insurer, or some combination of cotrustees whose responsibilities are to invest funds contributed by the employer to the trust, accumulate earnings, and pay benefits to eligible employees.

1 - 26© 2010 Flat World Knowledge, Inc. 21 - 26© 2010 Flat World Knowledge, Inc.

Insured Plans

Group deferred annuity: Contract between insurer and employer to provide for the purchase of specified amounts of deferred annuity for employees each year.

Deposit administration: Requires the employer to make regular payments (as determined by actuaries) to the insurance company on behalf of employees, and these contributions accumulate at interest.

1 - 27© 2010 Flat World Knowledge, Inc. 21 - 27© 2010 Flat World Knowledge, Inc.

Insured Plans

Immediate participation guarantee (IPG) contract: A form of deposit administration whereby the employer makes regular deposits to a fund managed by the insurance company and the insurer receives deposits and makes investments.

Separate account plans: Designed to give the insurer greater investment flexibility; contributions are not commingled with the insurer’s other assets and not subject to the same investment limitations.

1 - 28© 2010 Flat World Knowledge, Inc. 21 - 28© 2010 Flat World Knowledge, Inc.

Insured Plans

Guaranteed investment contracts (GICs): Insured pension funding arrangements used by insurers to guarantee competitive rates of return on large, lump-sum transfers (usually $100,000 or more) of pension funds, usually from another type of funding instrument.

1 - 29© 2010 Flat World Knowledge, Inc. 21 - 29© 2010 Flat World Knowledge, Inc.

Summary

Qualified employee retirement plans allow tax-deductible contributions for employees and tax deferral for employees.

Defined benefit plans require the greatest degree of employer commitment by guaranteeing specified retirement benefits for employees.

Defined contribution plans require less employer commitment by guaranteeing only contribution amounts toward employees’ retirement accounts.

1 - 30© 2010 Flat World Knowledge, Inc. 21 - 30© 2010 Flat World Knowledge, Inc.

Summary

Other qualified plans allowing tax-deferred contributions include 403(b), Section 457, Keogh, SEP, and SIMPLE.

There are different types of annuities, which act as retirement investment and distribution vehicles.

Funding of pension plans can be insured through several options.