risk management in payments processing. cheque fraud solutions for banking banking & mobile...

TRANSCRIPT

RISK MANAGEMENT IN PAYMENTS PROCESSING.

Cheque Fraud Solutions for Banking

Banking & Mobile Money West Africa 1

Topics1. Business Considerations2. Payments “Line of Business”4. Fraud Prevention Solutions• UV Detection• Fraud Buster • Positive Pay • Signature Verification• Web Review• Customer Information Verification5. Summary & Conclusion

Banking & Mobile Money West Africa 2

Business Considerations

Attracting New and Retaining Existing Customers

Maintaining and Improving Competitive Positioning

Managing, Limiting & Mitigating Risks

(Security)

Positioning to adopt, or adapt to, future changes

(Agility)

ReducingCost-to-Income Ratio

(Efficiency)

Strategic Business Drivers in Banking Today

(Effectiveness)

EffectivenessEfficiency

The big challenge for any bank is to achieve ‘Efficiency’ while retaining ‘Effectiveness’, ‘Security’ and ‘Agility’ – a balancing act!Banking & Mobile Money West Africa 3

Tower Group: Global Payments Top 10 Technology Initiatives for 2011

Banking & Mobile Money West Africa 6

“Now regulation and a business case furthering the evolution of payments from a product to a line of business are driving changes.

In this period of increased regulation, banks have the opportunity to grow their payments capabilities and improve operating efficiency as well as provide relief to parts of the bank that face reduced fee income or increased capital requirements.”

to CEO’s, COO’s and CIO’sEfficiency Improvement?

Fraud Risk is elevated due to limited scrutiny levels within current system

Processing Costs high due to manual paper content and not meeting current & proposed clearing regulations.

Customer Service Levels are constrained by manual and paper-based records

Value-Add Service Offerings also constrained by what is possible given your banks paper-based records

Effectiveness Improvement?

Compliance Risk – lack industry standard functionality & support for image processing technology & applications

Competitive New Offerings –image based initiatives by other banks can erode your client-base

Competitive Cost Reduction -lower service fees by the same banks will see your bank disadvantaged in local market

Competitive Window of Advantage created by new regulations could pose a threat to your bank – one of erosion of income due to erosion of client-base

Improving both Efficiency and Effectiveness makes for a compelling argument for Banks to act – and act soon!

Banking & Mobile Money West Africa 7

8

Customer makes deposit at Bank Branch

Teller Captures Image of Cheque and Deposit Slip Transaction Proofed @ Teller, in real-time in back office or over Network using advanced software tools (ICR, CAR, LAR) and/or human operators

Once captured, proofed and archivedphysical items are destroyed

Electronic data transferred to:1. Regional Office2. Branch Office3. Head Office4. Electronic Clearing House5. Payee Bank & onward

All subsequent processes are performed using data and image using suitable workflow software and

transaction based processes to feed legacy systemsBanking & Mobile Money West Africa

Banking & Mobile Money West Africa 10

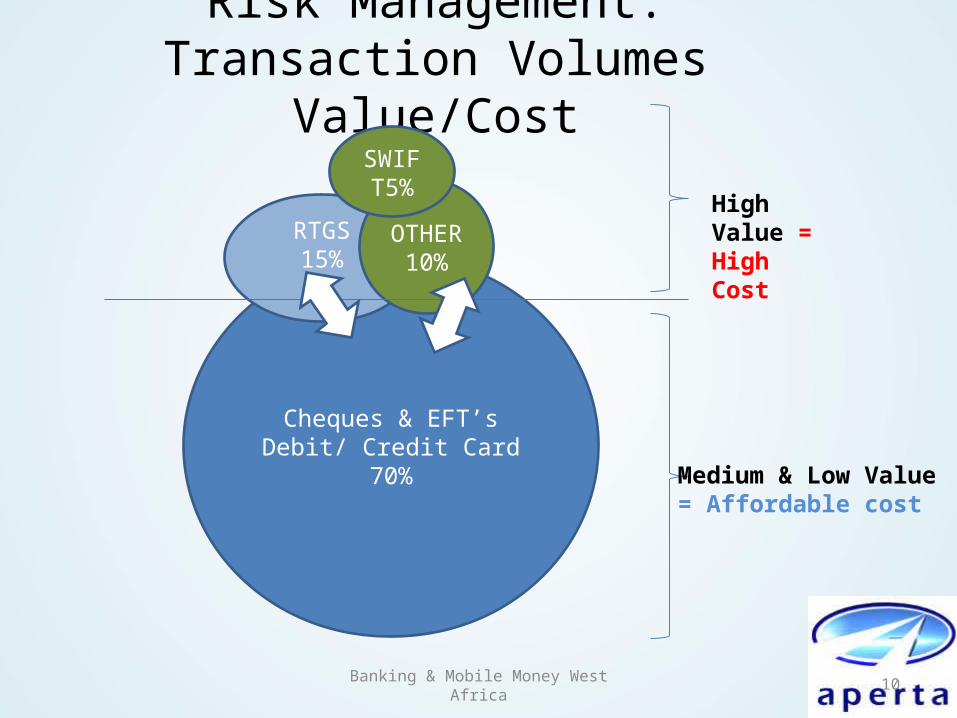

Risk Management: Transaction Volumes Value/Cost

Cheques & EFT’sDebit/ Credit Card

70%

RTGS15%

OTHER10%

SWIFT5%

Medium & Low Value = Affordable cost

High Value = High Cost

Cheque Fraud – US survey

Even as cheque volumes fall cheque fraud increases

Cheque Fraud Facts (AFP)• 71% of organizations experienced attempted or actual

payments fraud in 2010.• Cheques were the payment format most frequently

targeted for fraud, with 93% of attacked organizations reporting that their checks were involved.

• Among the most widely used techniques to commit payments fraud were counterfeit checks using the organization’s MICR line data (68 percent), alteration of payee names on checks issued by the organization (56 percent), and alteration of dollar amount on checks issued (35 percent).

Cheque Fraud Facts (AFP)• Checks were the payment method subject to

the greatest financial loss resulting from fraud in 2010 for surveyed organizations.

• Fourteen percent of organizations that were victims of at least one attempt of check fraud during 2010 suffered a financial loss resulting from the fraud.

• Checks are still the most widely used payment instrument for B2B payments.

Banking & Mobile Money West Africa 13

Typical Defences• High quality cheque stock

– Relies on teller and back office staff vigilance– Most methods are not image survivable

• Imaged inward items from other banks

• Signature Verification– Visual verification based on signature cards– Time consuming – only higher value cheques verified

• Bad account lists• Analytics

BackgroundTraditional protection is based on secure paper and ink technology i.e.;

• Watermark• Prismatic Printing• Chemically Reactive Paper/ink• High-resolution Borders• Micro printing

All of the above are not “image survivable”

Cheque Fraud Solutions:

1. “Active UV”

Leverage you LOB (truncation) infrastructure

“Active UV”• Ultra-Violet light• Invisible spectrum• Image survivable feature• Automatic detection at point of capture• Protects fields of interest, if UV ink is present• Deters Counterfeiting of checks, if invisible UV logo is

printed• Print and auto-read secure code/number with UV ink• Existing workflow unaffected

Banking & Mobile Money West Africa 17

APERTA UV LOGO DETECTION

Banking & Mobile Money West Africa 18

APERTA UV CHANGE DETECTION

Banking & Mobile Money West Africa 19

2. “Active Positive Pay”

Secure Corporate/ Government Payments

Overview• Bank receives details of customers issued cheques• When cheque presented for encashment details

received are compared with cheque details• Any differences detected• Customer asked to make pay/no pay decision

Benefits

• Minimise risk and improve cash management• Make pay /no pay decisions online in real time

– Helps customer to return items on time• Option to automatically accept/reject all suspect items

– Alerts to suspect fraud• Reduce potential for fraud loss• Customer controls check disbursement activity• Can be extended to EFT

How Positive Pay WorksCompare•Amount•Payee•MICR •Date

Positive Pay

Reverse Positive PayReversePositive Pay

“Active Positive Pay”

“The majority of the (check fraud) losses were due to;• a failure to use some type of positive pay or

“post no checks” service, • failure to perform a timely review of positive pay

or account reconciliation, or • not returning a check in the legally mandated

time frame.”

Not the silver bullet but AFP 2010 Survey concludes......

3. “Active Fraud Buster”

Encrypted Barcode print

Background

Payee name

Date

Amount

MICR

Protected fields

AFB+

AFB

AFB Process

AFB+ Process

Features• Fully automated process• High-density image survivable barcode• Cost effective• Fully controlled by the bank

Process and encryption• AFB - Protects all cheques• AFB+ - Effectively provides positive pay on

the cheque for high volume cheque customers Removes the need for issued item files Machine readable information

4. “Active Signature Verification”

OverviewTwo stage process:

1. Capture - reference signature images and data for each account• Image signature cards • Extract signature snippets from signature cards• Extract signatures from validated/paid cheques• Use existing CBS signatures

2. Review - Verify reference image with deposited cheque image• Visually• Semi-automatically• Fully automatic• Technical checks from image

Banking & Mobile Money West Africa 33

5. “Active “

other “Active Solutions”

6. Non MICR code line on cheque• Automatic detection during capture at teller or

back office• Whole code line or fields

7. Duplicate item detection• Detects if same cheque presented more than

once for payment within last x days

“Active” Solutions for FraudCommercial All Clients

Types of Fraud PositivePay

AFB+(Secure

Barcode)

Signature Verification

AFB Duplicate Detection

MICR UV DerogLists

Forged signatures √

Copied cheques √ √ √ √ √

Altered MICR √ √ √ √ √

Altered amount √ √ √

Altered payee √ √ √

Stolen cheque - blank

√ √ √ √

Forged endorsement

√

Links with Analytics √ √ √

Positive Pay & Signature Verification resolves most cheque fraud issues as does AFB + & Signature Verification.

8. “Active Web Review”Pulling it all together

• Consolidated view of all exceptions including fraud

• Allows branches to verify original paper versions of suspect cheques

• Final pay/no pay decision

• Browser interface allowing easy branch access

• Filtering of items by branch, type of exception etc

SummaryManage Risk and become compliant;• Leverage LOB truncation infrastructure

– UV read

• Innovate with efficiency in mind– Positive Pay– Fraud Buster– Verification of signatures, KYC profiles and

payments information at point of entry via Web Review

•Become Agile with Mobile!Banking & Mobile Money West Africa 37

Banking & Mobile Money West Africa 38

Conclusion• The Aperta solution suite is highly configurable and

can be focused to specific needs to help detect and prevent fraud, detect and warn of approaching processing boundaries and limits, to manage risk effectively, and prevent financial loss

• Reduce business risk by creating a secure and simple operating LOB environment which is automatically audited.

• Control financial limits and thresholds and provide associated alert mechanisms when they are approached.

Banking & Mobile Money West Africa 39

Conclusion• Provide a secure LOB operating environment with

automated failover and business process continuity (disaster recovery).

• Improve automated reporting by providing comprehensive audit trails, consolidated and specific reports, and comprehensive management reports.

• Improve regulatory compliance, such as meeting Payment Card Industry (PCI) requirements.

• Prevent fraud using positive pay, signature verification, image-survivable features such as UV markings, secure barcodes, and other anti-fraud solutions.

AiDPS Overview

40Banking & Mobile Money West Africa

Transaction Generation, Customer Verification & Fraud

Prevention

Payments Processing,

Document Archiving & Management

Contact details:• Marius Krige

– [email protected] – +27 12 259 0493– Aperta Africa, PO Box 533, Ifafi, South Africa, 0260

• Martin Wylupek– [email protected]– +44 1236 733300 – Aperta, 12 Mollins Court, Westfield Park, Cumbernauld,

UK, G68 9HP

Banking & Mobile Money West Africa 41