russia’s economy: after transformation, before …vid-1.rian.ru/ig/valdai/russian economy after...

TRANSCRIPT

Russia’s Economy: after Transformation, before Modernization

Valdai Discussion Club

Analytical Report

Moscow, January 2013

valdaiclub.com

Russia’s Economy: after Transformation, before Modernization

Valdai Discussion Club Analytical Report

Moscow, January 2013valdaiclub.com

Russia’s Economy: after Transformation, before Modernization

This report was prepared after discussions at the Valdai Discussion Club Summit held on Octo-ber 21–22, 2012.

The authors express gratitude to all the participants in the Valdai Club Summit and the situ-ational analysis discussions held on July 26, 2012, for contributing valuable ideas. Our special acknowledgements go to Pami Aalto, Director of the Jean Monnet Centre, University of Tam-pere; Pavel Andreev, Executive Director, RIA Novosti; Sergey Alexashenko, Director for Mac-roeconomic Research, National Research University Higher School of Economics; M.K. Bhad-rakumar, former ambassador of India to Turkey and Uzbekistan; Evgeny Gavrilenkov, Manag-ing Director and Chief Economist, Sberbank CIB; Sergei Glaziev, Advisor to the President of Russia; Charles Grant, Director, Centre for European Reform; Yuri Danilov, Director, Stock Market Development Center Foundation under the Federal Financial Markets Service of Rus-sia; Mikhail Delyagin, Director, Institute of Globalization Problems; Sergey Dubinin, Chair-man of the Supervisory Board, VTB-Bank; Piotr Dutkiewicz, Director, Center for Governance and Public Management, Carleton University, Ottawa; Natalya Zubarevich, Regional Program Director of the Independent Institute for Social Policy; Andrey Klepach, Deputy Minister of Economic Development of Russia; Yaroslav Lisovolik, Chief Economist and Head of the Analytical Department, Deutsche Bank Russia; Fyodor Lukyanov, Editor-in-Chief, Russia in Global Affairs journal; Józef Oleksy, Dean of the International Relations Department, Acad-emy of Finance (Warsaw); John Peet, Europe Editor, The Economist; Vladimir Popov, Inter-regional Advisor, UN Department of Economic and Social Affairs; Boris Porfiryev, Deputy Director, Institute for Economic Forecasting, Russian Academy of Sciences; Alexander Rahr, Advisor to the President, German-Russian Chamber of Commerce; Jean-François Rischard, ex-Vice President, World Bank; Jacques Sapir, Director of Studies, Paris School for Advanced Studies in the Social Sciences (EHESS); Kirill Rogov, Senior Research Fellow, Gaidar Institute for Economic Policy; Partha Sen, Professor of Economics, South Asia University; Boris Titov, Presidential Commissioner for Entrepreneurs’ Rights; Feng Shaolei, Dean of the Institute for Advanced International and Regional Studies, East China Normal University, Shanghai; Yu Hongjun, Director, Research Office, International Department of the Communist Party of China Central Committee; Igor Yurgens, Chairman of the Board of the Institute of Contem-porary Development. The authors express their special thanks to Full Member of the Russian Academy of Sciences and President of the New Economic Association Victor Polterovich. In the course of the preparation of the report, the authors studied and summarized all major programs and proposals on the economic policy made in the last three years.

The main author of the report is Professor Leonid Grigoriev, Head of the World Economy Department, World Economy and International Affairs Faculty, National Research University – Higher School of Economics. Other key contributors to the report are: Evsei Gurvich, Head, Economic Expert Group; and Igor Makarov along with Ekaterina Makarova, post-graduate stu-dents of the National Research University–Higher School of Economics.

The authors express sincere gratitude to Sergei Karaganov, Chairman of the Valdai Discussion Club, for his most valuable conceptual contribution and help in editing this paper.

This report incorporates many of the conclusions on Russia’s political development contained in the 2011 Valdai report “Russia Should Not Miss Its Chance: Development Scenarios” (http://valdaiclub.com/publication/35120.html).

Valdai Discussion Club wishes to express its gratitude to its partners from Strategic Foresight, World Economic Forum – Kristel van der Elst, Director and Head; Stephan Mergenthaler, Asso-ciate Director; Andrew Bishop, Project Manager, for effective cooperation while working on this report and the report of World Economic Forum “Scenarios for the Russian Federation”.

4

7

11

14

20

30

38

Contents

1. Summary

2. Transformation Completed, Objectives not Achieved

3. Russia 2030 — Setting Goals

4. The World in a Generation

5. Russia’s Resources

6. What Should Be Done?

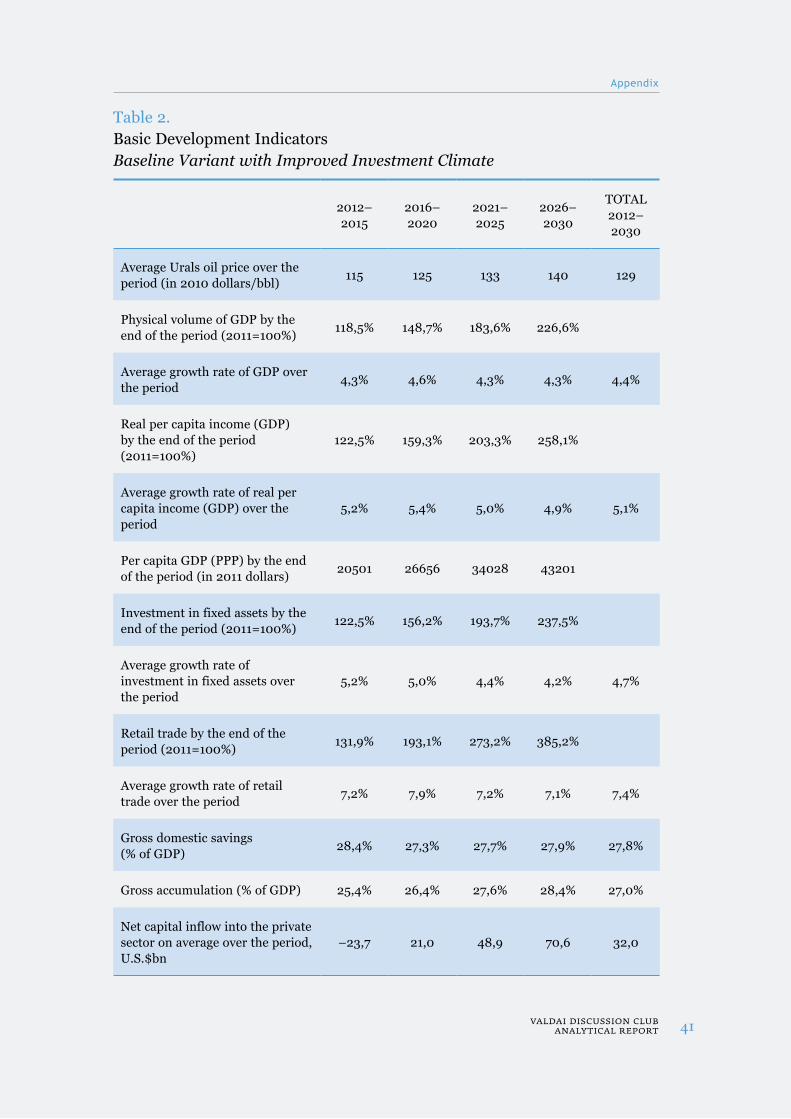

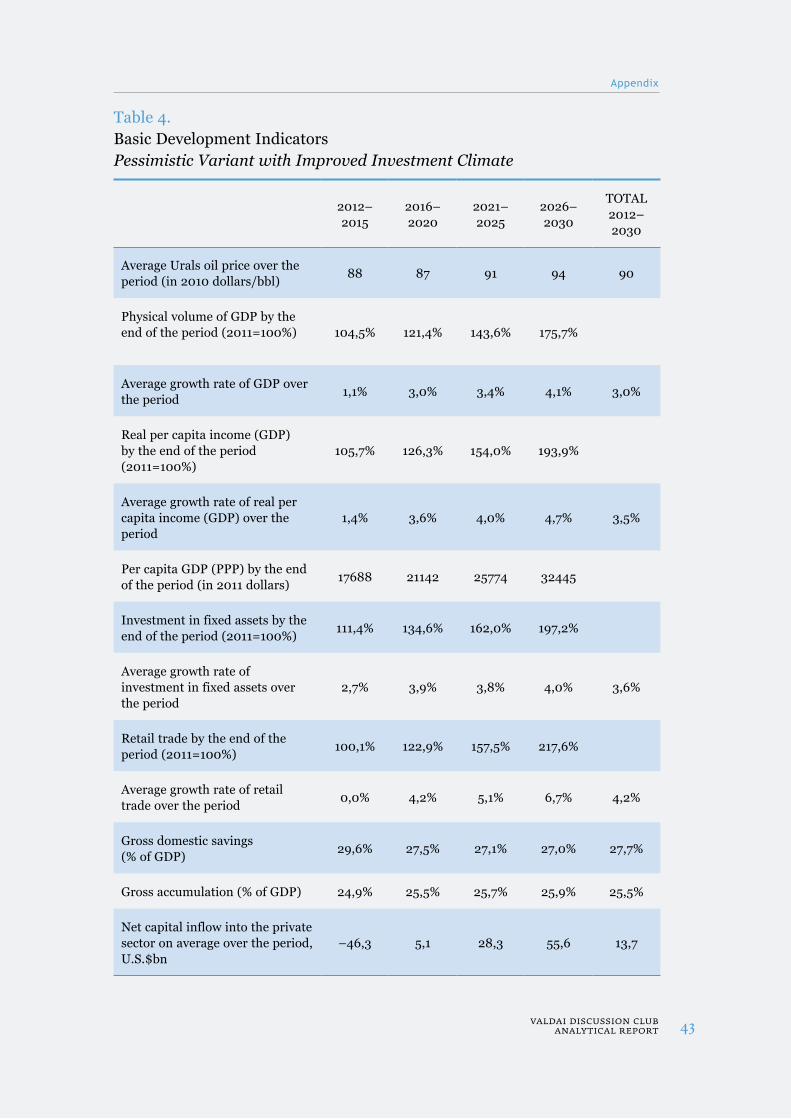

Appendix. Scenarios for Russian Economic Development until 2030 — Quantitative Approach

Russia’s Economy: after Transformation, before Modernization

4 Moscow, JAnuAry 2013

Russia’s economic development up to 2030 – and this is the time span covered in this report – will embrace three presidential terms. The external factors (oil prices and world financial turmoil) are largely predictable for the next three to five years, while longer-term

forecasts are highly tentative. Easily predict-able are climate change, a growth in the short-age of fresh water and food, and demographic changes.

Russia has just emerged from the gravest transitional crisis of the 1990s (when the GDP

slumped by 43%), undergone painful transfor-mations, dropped the meaningless and costly global confrontation, and avoided the risk of a civil war and the collapse of statehood. The GDP has just recently exceeded the level of the year 1989, but with a new quality – its per-

sonal consumption component is greater than in 1989, while pub-lic (especially military) spending are lower. This is seen as relative improvement of the condition of the society, which has manifest-ed itself in at least a dual way – a decline in the rate of suicides and heavy crime (murders), and the emergence of public protest against corruption and ineffec-tive governance – as well as oth-

er factors characteristic of civil society worthy of a European country.

By the second half of the 2000s, Russia by and large ended the post-Soviet period of its history, and started to develop. This is quite an achievement in itself. But after a while

1. Summary

By the second half of the 2000s, Russia by and large ended the post-Soviet period of its history, and started to develop. But after a while the country marked time again

Russia’s Economy: after Transformation, before Modernization

5Valdai discussion club analytical report

the country marked time again, enjoying the redistribution of the oil rent and a level of consumption unheard of in the past hundred years. Signs of stagnation became increasingly visible. The elite developed new division lines.

Our search for ways of the country’s advancing into the future uses as a point the desirable and possible visions of Russia in 2030 which have been developing by the authorities and by the civil society. The report also takes into

account the realities of the competition-ruled world, the country’s actual condition at the moment, and the available resources. This implies formulating and proposing for soci-ety’s consideration a “Concept of the Country’s Future 2030.” For Russia to achieve the mean-ingful progress by 2030, it must have a mean-ingful goal, accepted and supported by society, and consistent efforts to translate it into life. The key reforms must be set in motion within several years.

Russia’s resources – human, material and financial – are diversified and relatively large. In this report they are regarded as the basis for effective functioning of the economy and society’s existence, which does not require a detailed description. We proceed from the understanding that the capabilities of many sectors of the economy and half of the budget

depend on the external oil rent. Alongside the influx of capital from outside and the reinvest-ment of huge national savings, which depend on the legal and social climate in the country, the rent determines the government’s freedom of maneuver and the dynamics of this major budget source. We do not narrow the mean-ing of “resources” to that of “rent,” but further on often use the term ‘rent’ as a synonym of access to resources.

This report is by and large eco-nomic, as it focuses on econom-ic policy assumptions. But its authors and most experts who contributed to the discussion arrived at the following unequiv-ocal conclusion: Russia needs a new round of comprehensive reform. Economic measures,

even super-reasonable ones, will be insuf-ficient. Political reforms – irrespective of whether they may be liberal or anti-liberal – will be not enough, either.

In preparing this report we used a multi-scenario approach, briefly outlined in the following paragraph (also see Appendix). We do not focus on them in the main text not to confuse with “Scenarios for the Russian Federation” – a parallel report by the World Economic Forum, which was produced in cooperation with the working group of the Valdai Club report. At the end of our report we offer a list of measures, which include both those proposed previously in various strategies, and also relatively new ones. We strongly believe that these measures are cru-cial for the country’s successful development as they can reverse the growing stagnation-

Russia needs a new round of comprehensive reform. Economic measures, will be insufficient

Russia’s Economy: after Transformation, before Modernization

6 Moscow, JAnuAry 2013

bound trend that may eventually bring it to degradation.

In case of successful reforms combined with a high oil rent (the scenario that we termed “sanguine”), the Russian economy will outpace the world economy in terms of the average growth rate. An absence of both factors will hinder Russia’s economic growth consider-ably (the “melancholic” scenario). Successful reforms without a high rent (the “phlegmatic”

option) will secure roughly similar economic growth as in the case of a high rent without reforms (the “choleric” option). The report does not consider the possibility of an eco-nomic crisis in the country following a slump in oil prices (generally possible), say, to under $80 per barrel.

A decline of high-tech industries, de-intellec-tualization of life, degradation of the people’s culture and public morals, massive capital flight and emigration of talented young peo-ple – these are factors of the main catastrophic option Russia should steer clear of by all

means. The political effects of such a scenario would entail, in the least, a loss of the great power status and part of the regained sover-eignty and, in the worst case, a resumption of the trend towards the country’s breakup.

For a country with tremendous imbalances stemming from its history, geography and the nature of recent development, the socio-economic issues are particularly important as a factor of economic development. Hence the

report foresees the possibility of a surge of discontent among the educated middle class (Discon-tent 1) – even in case of a high rent, and also discontent among the poor strata (Discontent 2), which will manifest itself very acutely if the rent slumps. The maximum possible consent of the elites and the development of civil society are undoubtedly

essential for the modernization of the state and the economy. But the present level of the country’s development inevitably implies reliance on certain elements of “authoritar-ian modernization” – not on authoritarianism without modernization, though.

In this brief report we do not propose a detailed strategy of Russia’s economic development up to 2030 – that is the business of the whole of society, the elites and the authorities. But we shall try to identify its critically important aspects that are missing in the existing pro-grams.

The present level of the country’s development inevitably implies reliance on certain elements of “authoritarian modernization” - not on authoritarianism without modernization, though

Russia’s Economy: after Transformation, before Modernization

7Valdai discussion club analytical report

2. Transformation Completed, Objectives not Achieved

Over the 20 years of reforms Russia has not achieved the desirable objective – to become a great power with a medium-developed economy and European-type democracy. It has undergone three transformations: of the ideology and the political system of the state; of the economy; and of the country’s ethnic

and geographic composition. History shows that such transformations usually result in an utter collapse of the state. Russia and its elite may take pride in their unique success of preserving the core of the state – at a rela-tively low cost.

Russia has created a very peculiar market – not the type everybody hoped for in the early days of the reforms twenty years ago. The elites, civil society, the people in general and external onlookers are rather unhappy with the condition of the country’s market economy, state governance and society. After

a certain level of well-being has been achieved (largely at the expense of the high oil rent) dis-content over the state of affairs has come back – but along far stricter criteria.

The global economic crisis was negotiated without any major upheavals, and the 2012 GDP will be above the 2008 level, but only few points above the 1989

level. Personal consumption is way above the level of 1989, but the “investment depression” of the 1990s has not been overcome yet, capi-tal investment in the manufacturing industries and in science remains far below the Soviet level. During the recent crisis the structure of

The elites, civil society, the people in general and external onlookers are rather unhappy with the condition of the country’s market economy, state governance and society

Russia’s Economy: after Transformation, before Modernization

8 Moscow, JAnuAry 2013

production and export became increasingly narrow.

Reliance on redistribution of the unstable external rent is harmful not only for the government but the country in general. It causes stagnation of sophisticated businesses, immobilizes initiative, and turns the state leaders into “cowpunchers” – the people wait for instructions, subsidies and career promo-tions from the superiors. Uncertainty about the future breeds disappointment, apathy and discontent in society. Moreover, and that is still worse, it causes the flight of intellectuals and capital, while these are the main assets

in the 21st century. The country has got in the so-called Middle Income Trap. It badly needs to break away from the GDP level of $16,6 thousand per capita.

The level of education has grown over the past ten years: among 100 million Russians (aged over 15), 25% have higher education and over 60% have tertiary edu-

cation. That is above the level of most devel-oped countries, but it must be matched by high-standard policies, state governance, and civil society development. However, social inequality has grown and social lifts have weakened. The modernization of the economy and development of innovations are not a nor-mal, self-sustaining process. It is not society and business that generate innovations in the country and self-modernize, it is the state that is spreading paternalism “from pensioners to innovations.” The greater the bureaucratiza-tion, the heavier the load on the country’s leadership. Being forced to push the develop-

Uncertainty about the future breeds disappointment, apathy and discontent in society. Moreover it causes the flight of intellectuals and capital, while these are the main assets in the 21st century

Russia’s Economy: after Transformation, before Modernization

9Valdai discussion club analytical report

ment processes from above, the government has found itself in a difficult situation where it is just unable to cope with the overwhelm-ing task.

The pace of socio-economic changes in the country has slowed down, the adjustment of the existing institutions is extremely tough-going, primarily due to the resistance from the existing interest groups. There is a great problem with transition from the market institutions that took shape amid the chaos of the transitional period of the 1990s to the rule of law. In principle, the latter is to be the indicator a successful completion of the transformation. Social institutions – above

all, the rule of law, the protection of prop-erty rights, and the reliability of the judicial system, are the most important develop-ment factor. Political scientists, economists and businessmen are unanimous in that it is the institutional obstructions that hinder the modernization of the Russian economy. How-ever, number one institutional problem – political and moral one – is the illegitimacy of large private property. The struggle for prop-erty is possibly one of the main reasons why Russia still lacks a long-term development strategy. Also, it is an obstruction to steady onward development.

The debate over whether the oil rent is good or bad for development is fruitless. The rent in combination with good institutions is a devel-opment resource. The rent without adequate institutions is a risk of stagnation. The use of the rent without adequate market institutions in Russia clearly failed to give an impetus to modernization. Instead, a number of manage-rial functions in business began to be regu-lated by the state, and government companies started to grow and get bureaucratized. This policy addressed three tasks: meeting the interests (resource-oriented) of high-ranking officials; consolidating resources; and produc-ing an impression of active efforts to resolve the country’s problems.

The time factor is a major prob-lem for the country. The educat-ed generation of Soviet intellec-tuals with their solid knowledge and certain principles is about to go, the Soviet-era bureaucrats are quitting the stage. Many new intellectuals are leaving the coun-try or packing their suitcases.

Infrastructural problems and the wear of fixed assets are aggravating (hence the growing rate of accidents) and urgently require huge investment for the overhaul of not only the infrastructure, but of the extracting industries, transport and urban utilities, too.

The country and society will be changing with the change of generations in the elite and the middle class. The minimum degree of wealth and of freedom of information and travel (and of the right to emigration) all gained since 1991, satisfied those who lived most of their lives in the USSR, with its shopping lines

The rent in combination with good institutions is a development resource. The rent without adequate institutions is a risk of stagnation

Russia’s Economy: after Transformation, before Modernization

10 Moscow, JAnuAry 2013

and no end of restrictions. The recent fast growth of bureaucracy and corruption cause sincere and quite patriotic annoyance of civil society – however weak it may be. The new norm for the well-off and educated part of the society is high-quality governance with-out corruption (“democracy”), an independent judicial system and personal safety; for busi-nesses – the possibility to invest without the fear of losing property rights and protection against racketeering; for the poor – stability of the real incomes and absence of arbitrariness (“justice”); for young people – opportunities for taking part in social processes and vertical mobility in their own country, not elsewhere.

Apparently, only a milder ver-sion of the well-known formula “the upper classes can no long-er live the old way and the low-er classes no longer wish to live the old way” is applicable for these days. The upper classes are unable to ensure an inno-vative way of economic devel-opment without the freedom of social innovations, protection of property rights, personal safety of innovative businesses from racketeering and crimi-nalization. The upper classes are unable to generate inten-sive development even through

the obviously needed large-scale prestigious infrastructural projects. The development of the Transbaikal Region is clearly stalled. At the same time, the upper classes can no long-er afford to postpone modernization indefi-nitely and depend on the unstable foreign market of oil to finance most important state programs. The educated classes have unam-biguously expressed their discontent on the streets and through massive frondeuring by the middle class. Protest potential among the poorest strata has been growing against “injustice,” which traditionally encompasses everything in Russia – from social inequality to “bad nobility.”

The new norm is high-quality governance without corruption (“democracy”), an independent judicial system and personal safety; the possibility to invest without the fear of losing property rights and protection against racketeering; stability of the real incomes and absence of arbitrariness (“justice”); opportunities for taking part in social processes and vertical mobility in their own country, not elsewhere

Russia’s Economy: after Transformation, before Modernization

11Valdai discussion club analytical report

3. Russia 2030 — Setting Goals

The goal of the country’s development up to 2030 cannot be confined to guarantees of well-being, pension insurance, and socio-political stability. The program must set posi-tive objectives for the main sectors of society: in fact, the issue of optimal combination of objectives and ways to achieve them is irrel-

evant without account for the subject – the country’s citizens. And they all are very differ-ent and tend to change their demands once the previous objectives had been met.

The vision of Russia in 2030 is sort of a prag-matic dream, an achievable goal for the most

active citizens of the country, compatriots abroad, and sympathizing on-lookers. The wishes of university students or of the parents of university students are of major relevance here. So far according to opinion polls, about 68% of Russians with incomes above the national average would like to see their chil-

dren study and work abroad, and 37% want their children to set-tle abroad permanently. Elderly people (75%) see the president as the “father of the nation” (only 20% are against this), and young people aged 18–24 are split evenly: 48% share this approach and 48% are against it. These attitudes embody a direct way towards stagnation and eventual

degradation. Society needs a positive objective and solid proof that the government is deter-mined to move towards its real implementa-tion, and not just indulge in fine rhetoric.

The country’s ruling and intellectual elites are facing the challenge of proving their ability for

Society needs a positive objective and solid proof that the government is determined to move towards its real implementation, and not just indulge in fine rhetoric

Russia’s Economy: after Transformation, before Modernization

12 Moscow, JAnuAry 2013

compromise and staying united for the sake of the country’s development. There must be genuine (not simulated) dialogue among the elites, the authorities and the intellectuals over what sort of country they would like to have. The authorities feel insulted and alien-ate intellectuals, while a considerable part of the intellectuals have turned their backs on the authorities.

Three presidencies up to 2030 will be able to “feed” the poor. But Russia has Argentinean

parameters of distribution of the (visible) deciles incomes, which in the context of high education and egalitarian traditions is a very inconvenient combination for maintaining socio-political stability. A drastic reduction in inequality is hardly possible. The world trends point to the opposite. But then the authorities must have at least the active part of society – the new middle class and the intellectuals – on its side. Otherwise, in case of any slump in the oil rent Discontent 1 and 2 may merge with great chances of a social explosion.

What Russia will have besides raw materials, semi-finished product and assembly shops in 2030 is no longer a problem of just tech-nocratic decisions as to where to channel

the resources of businesses and investment, but a problem of society’s preparedness to work and sacrifice its efforts for the sake of the future? The priority economic sec-tors in state programs – energy production, nuclear power engineering, aircraft-build-ing, pharmacology and other capital-intense industries – will be unable to substitute for the diversity of research-intensive consum-er businesses and services, where business innovations must be the key factor in mod-ernizing the country.

If the industrial de-moderniza-tion trend persists, but no condi-tions for innovation are created, upgrading the national defense will be impossible.

The most important questions are: Will people feel comfort-able at home? Will young peo-

ple return home after studying abroad? Will business be investing inside the country? Will judges be impartial? What shall be we proud of? What should the intellectuals and the upper middle class do in this country? Servic-ing (and discussing) the bureaucracy or push-ing ahead with innovations? The democratic choice of the intellectuals and the middle class in Russia is by and large not to be doubted, but the success of modernization hinges on the balance of forces in society and the adap-tation of the ruling elite. Joining the group of advanced democratic market economies will require tremendous effort from Russia, both material and institutional – the moderniza-tion of society and the state, even though by authoritarian methods at first.

Joining the group of advanced democratic market economies will require tremendous effort from Russia, both material and institutional

Russia’s Economy: after Transformation, before Modernization

13Valdai discussion club analytical report

The country is longing for a real reduction of corruption and for control of the civil serv-ants by the civil society and the mass media. In relation to the market economy the main institutional requirements look obvious by and large, but they are to be discussed with society and businesses: independent courts; respect for property rights; restrictions on state interference in the economy to a sensible level of correcting “market failures”; promo-tion of competition; society’s (mass media’s) control of the civil servants; promotion of diversified types of property (the problem of state capitalism); and creation of incen-

tives for the regions’ independ-ent effective development.

A strategy of the country’s long-term development up to 2030 must become an attractive guideline for the society, for the people, and not a list of “check parameters” for the agencies to

meet. The country’s future position incor-porates the state of minds, an opportunity to rely not only on history, but also on the achievements of the coming decades. Rus-sia’s new image of an advanced democracy, of a country of great culture and science, a country of educated people looking into the future, who have broken off with the grave legacy of the Communist past but take pride in the achievements of their compatriots of all times, and of a strong and independent great power will serve as a tremendous posi-tive factor for drawing investments – both internal and external.

A strategy of the country’s long-term development up to 2030 must become an attractive guideline for the society and not a list of “check parameters” for the agencies to meet

Russia’s Economy: after Transformation, before Modernization

14 Moscow, JAnuAry 2013

4. The World in a Generation

The state of the external world also requires boosting development and overcoming the tendency towards stagnation. Along with chal-lenges, there come opportunities. Currently, most governments see post-crisis efforts as

their main priority tasks. They include: sus-taining growth while reducing unemployment and overcoming macroeconomic imbalances; reducing huge budget deficits; and preventing inflation. There is a threat that the recovery phase may fail at the very start of the period under review and that the world may go over from the Great Recession to the second Great Depression. The crisis has shaken the world economy, and there are neither simple meth-

ods, nor an appropriate theory to explain the changes, nor “handy” recipes to achieve fast growth.

Global rivalry for investment is increasing and becoming a major driving force of world processes. Russia will have to make huge efforts in order to keep up with the world progress and, all the more so, to modernize itself and take the lead over other countries. Russia should be proactive in advancing towards the world whose con-tours are gradually showing up,

rather than prepare for the “previous” (and lost) economic wars.

Overall global growth rates in the foreseeable future will apparently be lower than in the 2000s. The years 2012–2030 will be a transi-tion period in the world’s development. In the next few decades, advanced (yet already used globally) technologies will grow fast through

Russia will have to make huge efforts in order to keep up with the world progress and, all the more so, to modernize itself and take the lead over other countries

Russia’s Economy: after Transformation, before Modernization

15Valdai discussion club analytical report

new investment, replacing the old physical capital.

World economic growth will most likely pro-ceed in two different dimensions: the OECD countries, on the one hand, and China, India and part of the developing world, on the other. Other countries will address their problems in a tough competition with flows of cheap goods from fast-developing yet still poor countries, and sophisticated and expensive technologies from developed countries. The first prevents new industrialization of moderately developed countries, and the second stands in the way of

post-industrial development based on coun-tries’ own production of sophisticated tech-nologies and services. Both challenges apply to Russia and require unconventional economic specialization, rather than just a new industri-alization or a “post-industrial breakthrough.”

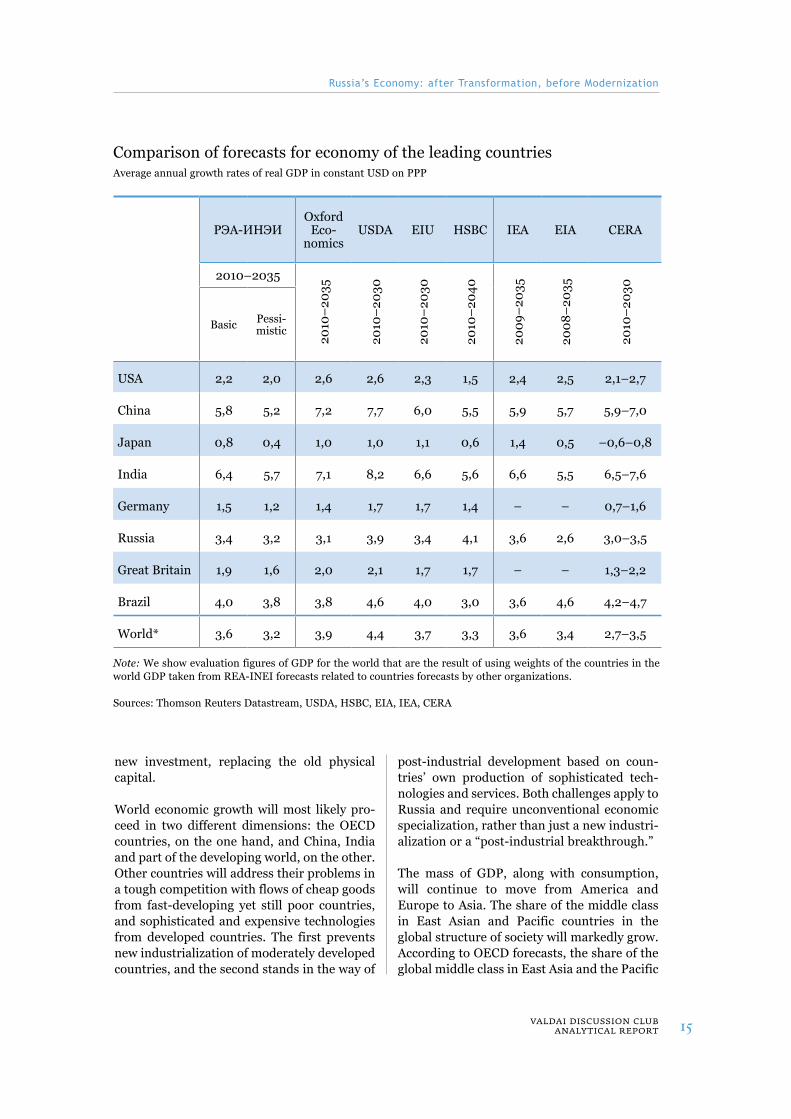

The mass of GDP, along with consumption, will continue to move from America and Europe to Asia. The share of the middle class in East Asian and Pacific countries in the global structure of society will markedly grow. According to OECD forecasts, the share of the global middle class in East Asia and the Pacific

Comparison of forecasts for economy of the leading countriesAverage annual growth rates of real GDP in constant USD on PPP

РЭА-ИНЭИOxford

Eco-nomics

USDA EIU HSBC IEA EIA CERA

2010–2035

2010

–20

35

2010

–20

30

2010

–20

30

2010

–20

40

2009

–20

35

2008

–20

35

2010

–20

30

Basic Pessi-mistic

USA 2,2 2,0 2,6 2,6 2,3 1,5 2,4 2,5 2,1–2,7

China 5,8 5,2 7,2 7,7 6,0 5,5 5,9 5,7 5,9–7,0

Japan 0,8 0,4 1,0 1,0 1,1 0,6 1,4 0,5 –0,6–0,8

India 6,4 5,7 7,1 8,2 6,6 5,6 6,6 5,5 6,5–7,6

Germany 1,5 1,2 1,4 1,7 1,7 1,4 – – 0,7–1,6

Russia 3,4 3,2 3,1 3,9 3,4 4,1 3,6 2,6 3,0–3,5

Great Britain 1,9 1,6 2,0 2,1 1,7 1,7 – – 1,3–2,2

Brazil 4,0 3,8 3,8 4,6 4,0 3,0 3,6 4,6 4,2–4,7

World* 3,6 3,2 3,9 4,4 3,7 3,3 3,6 3,4 2,7–3,5

Note: We show evaluation figures of GDP for the world that are the result of using weights of the countries in the world GDP taken from REA-INEI forecasts related to countries forecasts by other organizations.

Sources: Thomson Reuters Datastream, USDA, HSBC, EIA, IEA, CERA

Russia’s Economy: after Transformation, before Modernization

16 Moscow, JAnuAry 2013

will increase from 18% to 66% in the period from 2009 to 2030. China and India will account for more than 59% of all consumption by the global middle class.

The share of developing countries in the world GDP growth rate will continue to increase, so the definition of a “developed” country may change. The structure of the world economy will gradually change towards the develop-ment and introduction of energy-saving tech-nologies, economical housing and transport, the recycling of materials and waste, the intro-duction of more services and standards to meet the requirements of social justice in developed countries, and the growth of education and demand for new standards of living in devel-oping countries. It would be safe to predict a

steady growth of the demand for food and of food prices.

The global problems remain unresolved and will pose a poten-tial threat to social and political stability for some countries and regions and – in the long term – the whole of mankind. Poverty, climate change and the environ-mental challenges, relative short-

ages of food and many kinds of raw materials, development disparities among countries and regions, the population explosion in some regions and the aging of the population in oth-ers, and limited resources (especially intellec-tual and financial ones) create an urgent need for more concerted and coordinated efforts by the international community. A mere listing of problems now facing the international com-munity is enough to doubt mankind’s ability to solve them within the coming years.

The collision between development tasks, global problems and the decline of global governability will be in the center of the inter-national agenda. Russia will have to look for a position of its own, which would link the

GDP Growth Rate by Groups of Countries over the Given Period, %

1981–1990 1991–2000 2001–2008 2009–2011

World 38,7 36,9 36,4 8,7

Developed economies: 38,1 32,0 18,0 1,0

— including EU 17,5 17,1 13,8 1,0

— including US 37,5 40,1 17,4 1,2

Developing economies: 39,9 46,4 66,2 17,4

— including China 143,0 169,6 124,7 31,6

Russia – –27,4 66,5 0,3

Source: IMF

The global problems remain unresolved and will pose a potential threat to social and political stability for some countries and regions and – in the long term – the whole of mankind

Russia’s Economy: after Transformation, before Modernization

17Valdai discussion club analytical report

interests of its development and promotion of the solution of a wide range of global prob-lems. Russia can contribute to their solution, but resource limitations are highly significant. This suggests a cautious approach and the integration of such goals into a national devel-opment strategy. At the same time, some glob-al problems – climate change, food insecurity, a sharp deterioration of the environmental

situation regarding, in particu-lar, the quality and quantity of fresh water in Asia – may cre-ate new competitive advantages for Russia.

Estimates of future Russian exports and revenues are based on the assumption that the physical volume of Rus-

sian hydrocarbons, metals and other prod-ucts will be in demand, despite programs to reduce global energy intensity. But we do not know exactly what the oil price will be in the future in the conditions of revolu-tionary changes in the global energy sector, which have already begun. Rational behavior as regards budget projections would be to

Russia will have to look for a position of its own, which would link the interests of its development and promotion of the solution of a wide range of global problems

Russia’s Economy: after Transformation, before Modernization

18 Moscow, JAnuAry 2013

Military Expenditures: Years 1988, 2000, 2010$bn year 2009 and % of GDP

$ bn 2010 % GDP

1988 2000 2010 1988 2000 2010

USA 540 382 698 5,7 3,0 4,8

Great Britain 54 44 58 4,1 2,4 2,6

France 65 58 59 3,6 2,5 2,3

Germany 64 47 45 2,9 1,5 1,4

Japan 46 55 55 1,0 1,0 1,0

China 17 33 121 2,5 1,9 2,1

India 17 26 46 3,6 3,1 2,7

Brazil 20 22 34 2,1 1,8 1,6

Russia 331* 29 59 15,8 3,7 3,9

Israel 13 13 14 15,6 8,0 6,5

Saudi Arabia 20 26 45 15,2 10,6 10,1

Source: SIPRI* USSR

abide by conservative estimates concerning oil prices. Energy efficiency, as a major vec-tor of the development of the energy industry relying on new technological opportunities, is acquiring increasing importance. As the world approaches the 2020s, one should be

very careful, as the oil price may fall to U.S. $80 per barrel.

The decline in global defense spending from 1988 to 2000 (the “peace dividend”) has given way to its growth (above all, in developing countries). The world (except for Europe) is obviously rearming. Security areas now include ever more spheres of life, such as energy, information,

cyber threats, etc. It has turned out that in the 21st century there is no bloc confrontation but there still remain economic interests of coun-tries and financial elites, lasting preferences of political elites, and historical phantom aches. In addition, the world is facing terrorism and

In the 21st century there is no bloc confrontation but there still remain economic interests of countries and financial elites, lasting preferences of political elites, and historical phantom aches

Russia’s Economy: after Transformation, before Modernization

19Valdai discussion club analytical report

changes in the balance of power. The struggle for resources is coming back, along with the old geopolitics in a new appearance.

After the post-Cold War “unfreezing” of con-flicts (Yugoslavia, the Caucasus), there has begun the second “unfreezing” era marked by the rise of nation states, fast redistribution of power, and the decline of Western domination (hence the growth of tensions in East Asia, and conflicts in the Middle East). This era of conflicts is only unfolding. Military power is

returning into the center of world politics, which apparently requires an adequate mili-tary buildup from Russia.

An analysis of links among economy, politics and defense spending is beyond the scope of this report. But we should warn here that Russia will inevitability face the chal-lenge of choosing between increased defense spending and a lack of investment in human capital, and this will require serious internal discourse.

Russia’s Economy: after Transformation, before Modernization

20 Moscow, JAnuAry 2013

5. Russia’s Resources

The country’s modernization in the context of such external challenges will be possible only if it taps tremendous intellectual and financial resources and effectively uses the available assets to address four tasks: ensure the well-being of the citizens; maintain and modernize the physical and social infra-structures; restore and realize the innova-tive development potential; and ensure an adequate defense capability. All these efforts will require a high degree of unity of the elites and society around a common national idea.

The profound transitional crisis of the 1990s has been overcome only in some respects. The investment slump in the infrastructural industries and the emigration of intellectuals against a backdrop of axed spending on sci-ence and education have created ground for the country’s de-industrialization and pose a threat to innovative development. Shrink-ing population and the flight of financial and human capital require raising the effective-ness of the latter.

In the coming decades Russia will remain in a precarious position between two groups of countries both enjoying various compet-itive edges. The criteria of the success of Russian modernization programs will be not GDP growth rates, and not even the current consumption, but the effectiveness of capi-tal investment, proper identification and use of competitive advantages, dynamic business and high-quality jobs for the graduates of Rus-sian universities.

The condition of Russia’s economy in 2012 is not a theme for debate by and large. Eve-rybody seems to have got used to, if not “reconciled oneself with” an expected growth rate of 3%–4%, or even less. Regrettably, the structure of production is fixed and frozen: the GDP and incomes from the export grow mainly with the production and prices of oil, gas, metals, chemistry products, timber and grain. The accumulation rate during the boom of 2000–2007 remained at a very low level of 20%. The export of savings (debt pay-ments, the export of capital and the creation of

Russia’s Economy: after Transformation, before Modernization

21Valdai discussion club analytical report

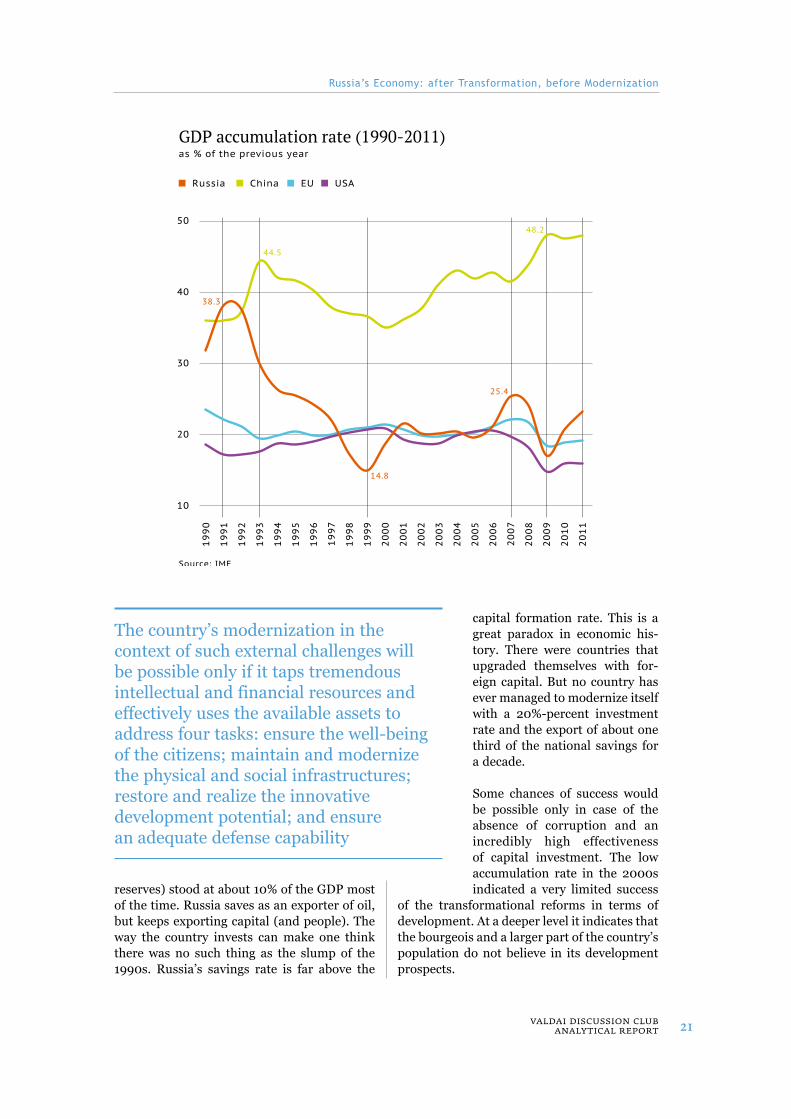

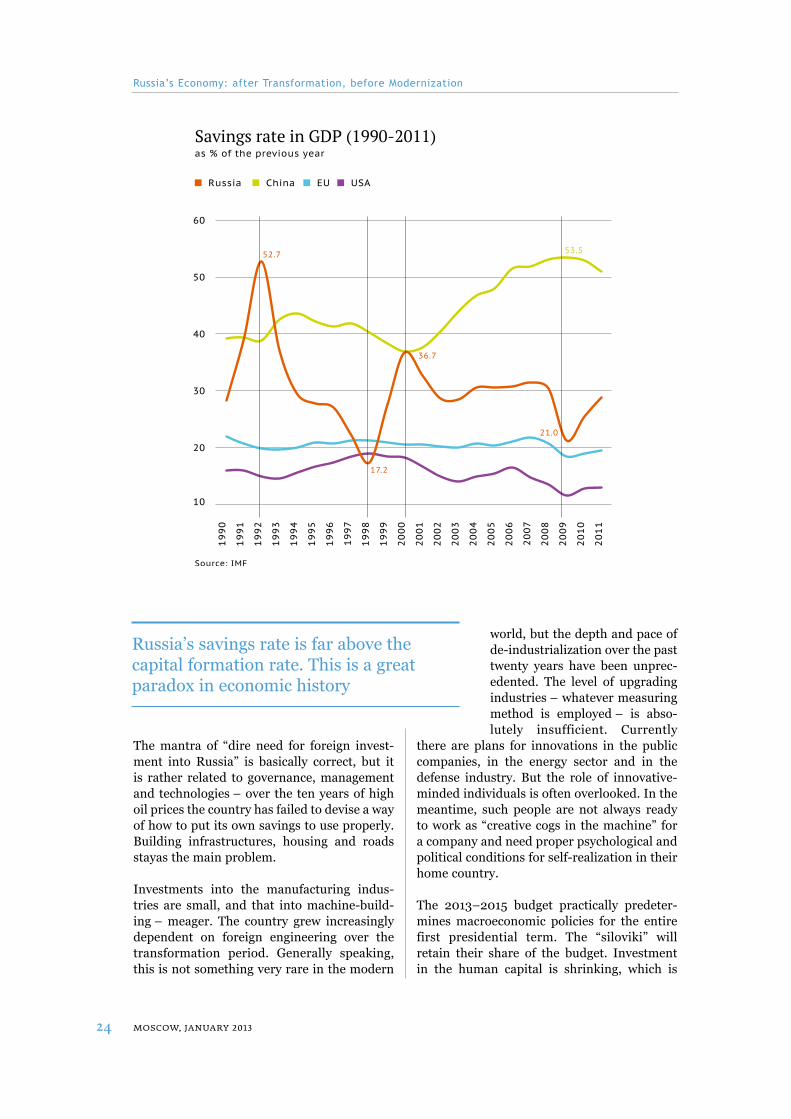

reserves) stood at about 10% of the GDP most of the time. Russia saves as an exporter of oil, but keeps exporting capital (and people). The way the country invests can make one think there was no such thing as the slump of the 1990s. Russia’s savings rate is far above the

capital formation rate. This is a great paradox in economic his-tory. There were countries that upgraded themselves with for-eign capital. But no country has ever managed to modernize itself with a 20%-percent investment rate and the export of about one third of the national savings for a decade.

Some chances of success would be possible only in case of the absence of corruption and an incredibly high effectiveness of capital investment. The low accumulation rate in the 2000s indicated a very limited success

of the transformational reforms in terms of development. At a deeper level it indicates that the bourgeois and a larger part of the country’s population do not believe in its development prospects.

The country’s modernization in the context of such external challenges will be possible only if it taps tremendous intellectual and financial resources and effectively uses the available assets to address four tasks: ensure the well-being of the citizens; maintain and modernize the physical and social infrastructures; restore and realize the innovative development potential; and ensure an adequate defense capability

Russia’s Economy: after Transformation, before Modernization

22 Moscow, JAnuAry 2013

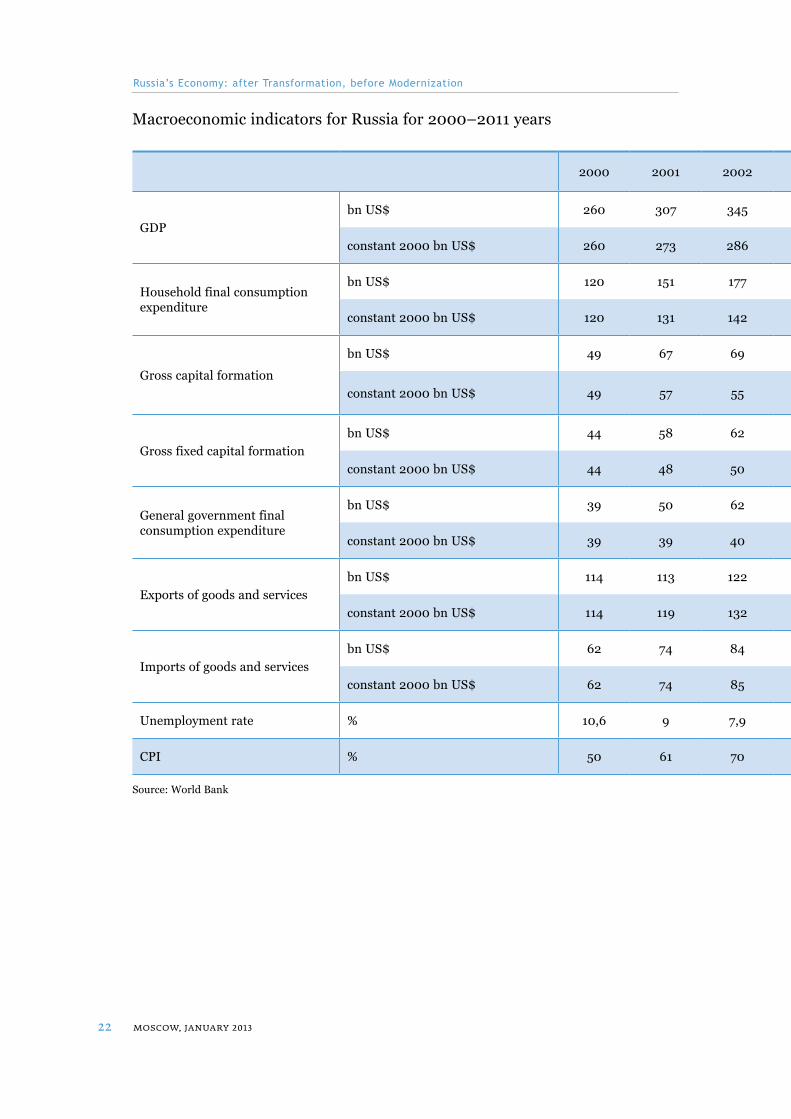

Macroeconomic indicators for Russia for 2000–2011 years

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

GDPbn US$ 260 307 345 430 591 764 990 1300 1661 1223 1488 1858

constant 2000 bn US$ 260 273 286 307 329 350 378 411 432 398 415 433

Household final consumption expenditure

bn US$ 120 151 177 218 298 382 483 634 812 668 768 908

constant 2000 bn US$ 120 131 142 153 171 191 214 245 270 257 265 344

Gross capital formation

bn US$ 49 67 69 90 124 153 210 314 424 231 338 457

constant 2000 bn US$ 49 57 55 63 71 77 91 111 123 73 93 101

Gross fixed capital formationbn US$ 44 58 62 79 109 136 183 273 370 269 324 430

constant 2000 bn US$ 44 48 50 57 64 70 83 100 111 95 101 106

General government final consumption expenditure

bn US$ 39 50 62 77 100 129 172 225 296 257 288 315

constant 2000 bn US$ 39 39 40 41 42 42 43 44 46 46 47 40

Exports of goods and servicesbn US$ 114 113 122 152 203 269 334 392 520 343 445 514

constant 2000 bn US$ 114 119 132 148 166 176 189 201 202 193 207 211

Imports of goods and servicesbn US$ 62 74 84 103 131 164 208 280 367 251 321 396

constant 2000 bn US$ 62 74 85 100 123 143 174 219 252 175 220 264

Unemployment rate % 10,6 9 7,9 8,2 7,8 7,2 7,2 6,1 6,3 8,4 7,5 6,1

CPI % 50 61 70 80 89 100 110 120 136 152 163 176

Source: World Bank

Russia’s Economy: after Transformation, before Modernization

23Valdai discussion club analytical report

Macroeconomic indicators for Russia for 2000–2011 years

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

GDPbn US$ 260 307 345 430 591 764 990 1300 1661 1223 1488 1858

constant 2000 bn US$ 260 273 286 307 329 350 378 411 432 398 415 433

Household final consumption expenditure

bn US$ 120 151 177 218 298 382 483 634 812 668 768 908

constant 2000 bn US$ 120 131 142 153 171 191 214 245 270 257 265 344

Gross capital formation

bn US$ 49 67 69 90 124 153 210 314 424 231 338 457

constant 2000 bn US$ 49 57 55 63 71 77 91 111 123 73 93 101

Gross fixed capital formationbn US$ 44 58 62 79 109 136 183 273 370 269 324 430

constant 2000 bn US$ 44 48 50 57 64 70 83 100 111 95 101 106

General government final consumption expenditure

bn US$ 39 50 62 77 100 129 172 225 296 257 288 315

constant 2000 bn US$ 39 39 40 41 42 42 43 44 46 46 47 40

Exports of goods and servicesbn US$ 114 113 122 152 203 269 334 392 520 343 445 514

constant 2000 bn US$ 114 119 132 148 166 176 189 201 202 193 207 211

Imports of goods and servicesbn US$ 62 74 84 103 131 164 208 280 367 251 321 396

constant 2000 bn US$ 62 74 85 100 123 143 174 219 252 175 220 264

Unemployment rate % 10,6 9 7,9 8,2 7,8 7,2 7,2 6,1 6,3 8,4 7,5 6,1

CPI % 50 61 70 80 89 100 110 120 136 152 163 176

Source: World Bank

Russia’s Economy: after Transformation, before Modernization

24 Moscow, JAnuAry 2013

The mantra of “dire need for foreign invest-ment into Russia” is basically correct, but it is rather related to governance, management and technologies – over the ten years of high oil prices the country has failed to devise a way of how to put its own savings to use properly. Building infrastructures, housing and roads stayas the main problem.

Investments into the manufacturing indus-tries are small, and that into machine-build-ing – meager. The country grew increasingly dependent on foreign engineering over the transformation period. Generally speaking, this is not something very rare in the modern

world, but the depth and pace of de-industrialization over the past twenty years have been unprec-edented. The level of upgrading industries – whatever measuring method is employed – is abso-lutely insufficient. Currently

there are plans for innovations in the public companies, in the energy sector and in the defense industry. But the role of innovative-minded individuals is often overlooked. In the meantime, such people are not always ready to work as “creative cogs in the machine” for a company and need proper psychological and political conditions for self-realization in their home country.

The 2013–2015 budget practically predeter-mines macroeconomic policies for the entire first presidential term. The “siloviki” will retain their share of the budget. Investment in the human capital is shrinking, which is

Russia’s savings rate is far above the capital formation rate. This is a great paradox in economic history

Russia’s Economy: after Transformation, before Modernization

25Valdai discussion club analytical report

extremely unfavorable, although not yet cata-strophic from the standpoint of transition to innovative development. The economy-related ministries will lose a lot. The Finance Minis-try’s role grows to redistributing directly up to half of the budget.

In practice, this budget draft means that any significant increase in investments domesti-cally is possible only in the private sector. The state can merely establish tax discounts or improve “the climate.”

It follows that investment in the development in the next few years will be the matter of commercial companies (includ-ing state-run ones), which will be using their own or borrowed funds. In other words, the oil rent will be used only for addressing social problems and financing the defense. More new

private investment is necessary as no tangi-ble growth of state investment is anywhere in sight: according to the Economic Devel-opment Ministry, government investment in 2005–2008 in the entire budget system was within a range of 3.5%–3.8% of the GDP, and in 2012–2015 it will be within a range of 3.4%–3.5% of the GDP.

The energy sector is left out of all reform pro-grams to remain the elite’s “sacred cow.” We do not share the opinion, which has been pre-

Investment in the development in the next few years will be the matter of commercial companies (including state-run ones), which will be using their own or borrowed funds

Russia’s Economy: after Transformation, before Modernization

26 Moscow, JAnuAry 2013

vailing in the past six to twelve months, that the demand for and prices of Russia’s oil and gas are doomed to slump. However, it is highly probable that new technologies may cause problems on the world markets. Geopolitical destabilization of the Middle East may offset this factor only to a certain extent. Pinning development and well-being most entirely on the energy export will be a highly risky strat-egy already in the medium term.

The financial sector remains weak – by the existing standards even the largest banks are unable to finance truly significant projects. Russia is the sole large country which has an effective law on the blocking packet of shares.

A well-developed internal bond market is still absent, mostly due to the unstable legal environment. The weakness of the private financial sector drops out of sight now and then. As long as it is non-existent, financing an investment boom with national savings without “carouselling” them through foreign gubs will be problematic.

Foreign direct investment will hardly exceed 1%–2% of the GDP, that is, reach one-tenth of the overall annual investment in the country. Currently, Russia has a very unsound model of capital export and import. Direct capital is exported to return only partially and only as foreign one. Capital is largely pumped in

Russian budget projections for 2013 and the longer period extending over 2014–2015

2011 2012 2013 2014 20152015

to 2011,%

Spending (bn. rbls.) 9352 11108 11612 11697 12128 +29,7

%

Defense Ministry 11,2 11,8 11,7 8,9 8,7 +2,5

Interior Ministry 5,4 9,6 9,4 8 7,7 +2,3

Emergencies Ministry 1,6 1,5 1,4 1,4 1,3 –0,3

Security forces combined 18,2 23 22,5 18,3 17,8 –0,4

Ministry of Finance 40,9 39,9 42 48,5 50,5 +9,6

Education, science, healthcare, justice and culture

8,3 7,7 7 6,2 5,8 –2,5

Spending by other agencies on economic development

32,5 29,4 28,5 27 25,8 –7,7

GDP – assessment, bn. rbls.

54369 59750 67360 74086 81761 +50,4

Share of state expenditure in GDP, %

17,2 18,6 17,2 15,8 14,8 –2,4

Source: The Ministry of Finance Source: RBC Daily, 24.09.2012, p. 3

Russia’s Economy: after Transformation, before Modernization

27Valdai discussion club analytical report

through the banking sector and the exchange mechanisms as portfolio capital, where it is prone to conjectural waves. But even if direct capital is drawn into the country – directly into some companies, it is important to under-stand that the potentially needed boom of for-eign investment in Russia would merely work as an amplifier, not as a substitute for own investment and for re-investment of domestic savings.

The population and labor resources, according to demographic forecasts, will be declining. Time is ripe to create conditions for wider

use of foreign workforce and for creating attractive conditions for those who are prepared to live and work in this country.

There is a vast source of national workforce in the spheres con-cerned with people’s personal safety, judiciary and law enforce-

ment. According to the latest estimates, secu-rity firms employ more people (from 800,000 to 1.5 million men of able-bodied age) than there are on active service in the army.

The country’s resources are rather limited by a number of key parameters: employment, available credit, management and technolo-gies. Only foreign revenues from the export of crude (and other raw materials and semi-finished products) are large. All economists adhere to one principal assumption: resources for development must be basically created by businesses and the population within the

Potentially needed boom of foreign investment in Russia would merely work as an amplifier, not as a substitute for own investment and for re-investment of domestic savings

Russia’s Economy: after Transformation, before Modernization

28 Moscow, JAnuAry 2013

framework of a competent government policy. In other words, the country needs not rent sharing, or rent redistribution through the budget, or reliance on future foreign invest-ment (although the latter is important as a

criterion and as a resource), but opportuni-ties for creating and using resources. And this depends on the quality of institutions.

Bureaucratization, the creeping “governmen-talization” of business and increased regula-tory pressure by the state are now major top-ics discussed by the business community and expert society. Three simultaneous process-es are underway – immediate-action laws, which cannot be interpreted unambiguously, are being adopted; businesses are being arti-ficially criminalized under “controversial” articles of the Criminal Code; lawmaking continues non-stop, newly issued or changing instructions put people and businesses in the guilty-by-ignorance position, thereby push-ing up the transaction costs. This situation

and the systemic corruption which it breeds force businesses to transfer part of their assets outside of the country as a safety meas-ure, narrow the horizon for planning and investment, and lower their readiness to take

commercial risks in conditions of illegal takeover of businesses and bureaucratic risks.

The sharp shift in the interests of young people over the past decade from business to civil service (possibly the sole such case in the developed countries) is a clear sign that the innova-tive processes in business and

knowledge are slowing down to give way to bureaucratic innovations. The struggle for the rent – inventing reasons for getting the rent, seizing the rent and keeping the rent – obstructs development. It is characteristic of many levels of the government machinery, including the regional one.

There will be hardly any dramatic change in the coming years related to Russia’s acces-sion to the World Trade Organization, partly because the compromises achieved in con-cluding the agreement practically rule out shocks.

A period of twenty five years, when the risk of the Communism’s comeback played some role in elections and in decision-making is over.

The country needs not rent sharing, or rent redistribution through the budget, or reliance on future foreign investment, but opportunities for creating and using resources

Foreign investment in Russiabillions of US dollars

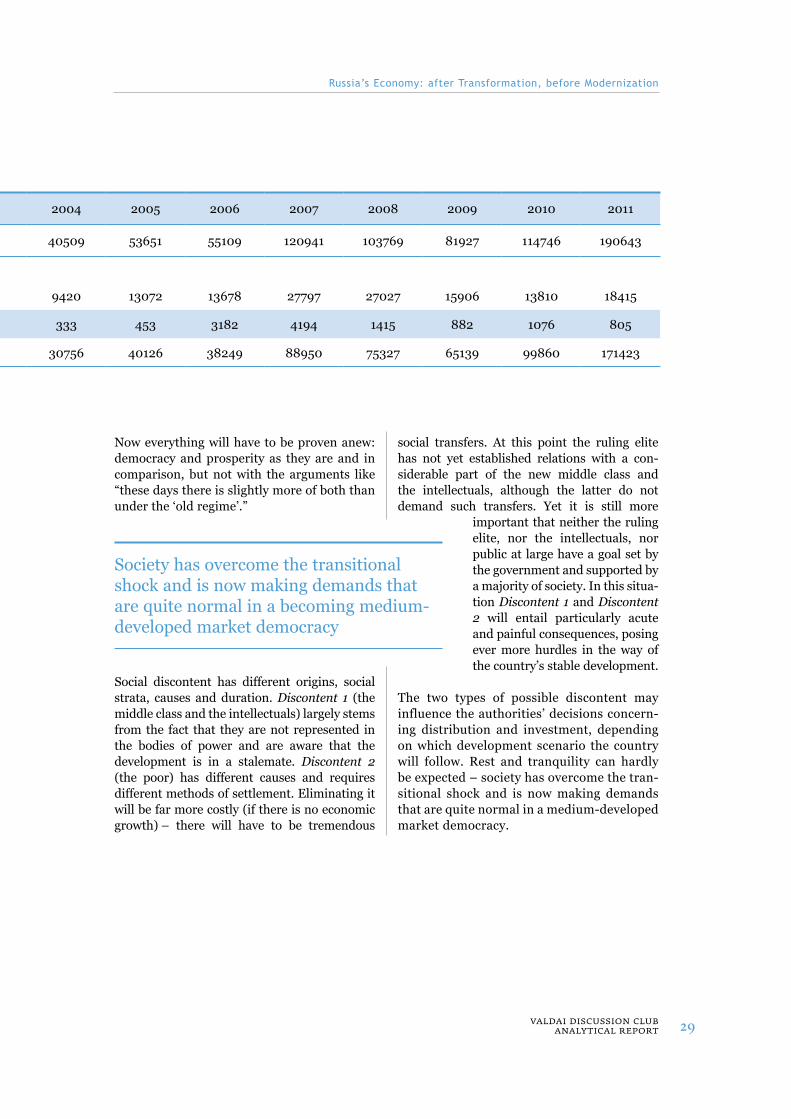

1995 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Total 2983 10958 14258 19780 29699 40509 53651 55109 120941 103769 81927 114746 190643

Including:

Direct investment 2020 4429 3980 4002 6781 9420 13072 13678 27797 27027 15906 13810 18415

Portfolio investment 39 145 451 472 401 333 453 3182 4194 1415 882 1076 805

Other investment 924 6384 9827 15306 22517 30756 40126 38249 88950 75327 65139 99860 171423

Source: Rosstat

Russia’s Economy: after Transformation, before Modernization

29Valdai discussion club analytical report

Foreign investment in Russiabillions of US dollars

1995 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Total 2983 10958 14258 19780 29699 40509 53651 55109 120941 103769 81927 114746 190643

Including:

Direct investment 2020 4429 3980 4002 6781 9420 13072 13678 27797 27027 15906 13810 18415

Portfolio investment 39 145 451 472 401 333 453 3182 4194 1415 882 1076 805

Other investment 924 6384 9827 15306 22517 30756 40126 38249 88950 75327 65139 99860 171423

Source: Rosstat

Now everything will have to be proven anew: democracy and prosperity as they are and in comparison, but not with the arguments like “these days there is slightly more of both than under the ‘old regime’.”

Social discontent has different origins, social strata, causes and duration. Discontent 1 (the middle class and the intellectuals) largely stems from the fact that they are not represented in the bodies of power and are aware that the development is in a stalemate. Discontent 2 (the poor) has different causes and requires different methods of settlement. Eliminating it will be far more costly (if there is no economic growth) – there will have to be tremendous

social transfers. At this point the ruling elite has not yet established relations with a con-siderable part of the new middle class and the intellectuals, although the latter do not demand such transfers. Yet it is still more

important that neither the ruling elite, nor the intellectuals, nor public at large have a goal set by the government and supported by a majority of society. In this situa-tion Discontent 1 and Discontent 2 will entail particularly acute and painful consequences, posing ever more hurdles in the way of the country’s stable development.

The two types of possible discontent may influence the authorities’ decisions concern-ing distribution and investment, depending on which development scenario the country will follow. Rest and tranquility can hardly be expected – society has overcome the tran-sitional shock and is now making demands that are quite normal in a medium-developed market democracy.

Society has overcome the transitional shock and is now making demands that are quite normal in a becoming medium-developed market democracy

Russia’s Economy: after Transformation, before Modernization

30 Moscow, JAnuAry 2013

6. What Should Be Done?

Domestic legal and economic institutions are crucial for an efficient economy, the position of the country, its clout and ability to influence the environment in order to achieve better condi-tions for its transition to innovative develop-ment. Of special importance to Russia is the use of its human capital and business potential to

give up, as soon as possible, its reliance on the natural resource rent, which will become ever more risky in the long term.

This reform implies accelerated innovative development of Russia itself with a view to mak-

ing it more than just a market for its neighbors’ products and more than just an energy exporter. Russia should offer cooperation in engineering, space for development, the traditional Russian cultural openness, and stable legal and econom-ic institutions. Another important strategic goal is to save and strengthen the Russian world as a

great civilization, which has made a huge contribution to the devel-opment of mankind. But this goal requires much more attention to (and investment in) education, culture, and the infrastructure of maintaining traditions. The global competition has covered this area, too: a country with a huge crea-tive potential and ability to create works of science, art and literature

of universal significance increases its capitaliza-tion, creates respective jobs, and receives a rent from its culture.

Success in Russia’s innovative modernization depends on the country’s actual starting basis

Accelerated innovative development of Russia itself with a view to making it more than just a market for its neighbors’ products and more than just an energy exporter

Russia’s Economy: after Transformation, before Modernization

31Valdai discussion club analytical report

and implies its steady movement towards a higher civilizational and cultural level. It is, in fact, the movement to the model of developed democracies (which are close to Russia in cul-ture and values), while maintaining the coun-try’s independence and identity and developing Russian culture.

Naturally, the adoption of many advanced, mostly Western, institutions will not mean following Western foreign policies (which have obviously lost their bearings), or giv-ing up the forced and already belated pro-gram for entering the rising Asian markets through new development of the Transbaikal Region.

Emphasis on institutions presupposes unity and stability within the political and finan-cial elites, and concentration of their efforts on public goals, rather than settlement of internal conflicts and distribution of material benefits typical of the early stages of soci-ety formation. A delay in choosing the type, direction and tools of modernization would mean a loss of time and a failure to reach an important goal for the elites (at least, the intellectual elite) and society: achieving the

status of a great scientific, cultural, political (and military) power with a developed civil society and a high level of personal freedom – in other words, becoming a modern Great Russia.

An overhaul of society and market institu-tions implies maximum unity of the elites and a transition from the short-term horizon to long-term coordinated actions. Elites usually rally together in the face of a common danger, especially when it is close and obvious. It is much harder to rally in order to maximize long-term benefits for the broader constituency and on terms that part of the clans may take as a concession or a

loss. It is important that the elites realize as a threat to themselves not slow growth but the country’s de-intellectualization (brain drain, decrease in the sophisticated products out-put, bureaucratization, etc.) and primitiviza-tion of the economy. A compromise among the elites for the next 15 years would give a chance for them and the nation to ensure the country’s progress and stability of its posi-tions.

The creation of institutions will require extraordinary initiative from the country’s top leaders. At first, this policy will have to be implemented largely in a manual mode, so traditional for Russia.

The change of interests of social strata and groups along with their development and the growth of their identity is an inevitable

A delay in choosing the type, direction and tools of modernization would mean a loss of time and a failure to reach an important goal for the elites and society – becoming a modern Great Russia

Russia’s Economy: after Transformation, before Modernization

32 Moscow, JAnuAry 2013

process. The only question is about forms of manifestation. Street protests in 2011–2012 have improved somewhat the investment cli-mate in Russia, as they showed its normalcy from the standpoint of the European tradi-tion of expressing dissent. Citizens’ readiness for social innovations, their resolve to protect their rights, and their demand for compliance with the law is a natural prerequisite for the country’s transition to the next development stage. This is an important condition for modernizing the country and strengthening its statehood.

Again: a conscious choice of a preferred economic development scenario is possible only when there is a long-term and maxi-mum agreed goal. The first thing that catches the eye in Russia’s official and semi-official economic programs for 2011–2012 is the abundance of applied problems and techni-cal details, parameters and indicators. With all due respect for their authors, they are not programs for the country’s economic trans-formation or the creation of efficient market democracy institutions and foundations to support and develop the status of a modern great power, but a collection of immediate ministerial plans.

Of course, fundamental issues concern-ing macroeconomics and budget spending, including a choice between investment in human capital and the defense-industrial complex, imply a huge institutional load. Strategy 2020 devotes much attention to the pension system, the quality of public services and e-government. We cannot enter into a detailed discussion of ministries’ deci-sions and are not discussing concrete rec-ommendations for specific industries, areas of people’s activities, businesses or public administration. Given below is a list of prob-lems, whose solution is vital, in our opinion,

for creating an efficient econo-my, the foundation of the might and well-being of the country and the people. The more effi-cient and more comprehensive the reform of institutions, the more chances there will be able to launch mechanisms of devel-opment, innovation and invest-ment, which are now blocked by

cumbersome bureaucratic governance sys-tems.

Russia also needs a new image, formulated by its leadership in a dialogue with society and constantly adjusted: the Vision of Rus-sia-2030 – Great Russia, which the majority of society is ready to seek. At the same time, it should be declared what the country should relinquish in order not to fail. Discussing ways to form this image is beyond the scope of this report. Yet it is already obvious that in order to become prosperous, free and strong, Rus-sia, its elites and people should set themselves the following economic and social goals:

It is important that the elites realize as a threat to themselves not slow growth but the country’s de-intellectualization and primitivization of the economy

Russia’s Economy: after Transformation, before Modernization

33Valdai discussion club analytical report

A. Institutional Issues: • Transformation of society in the spheres of

values and morals; the adoption of public-good attitudes as a norm.

• Formation of national identity, fundamen-tally, based on the key role of Russian cul-ture and the preservation and development of the Russian language, on the one hand, and proud and successful history of the struggle for independence and sovereignty, on the other.

• Shaping public attitudes in favor of innova-tions, entrepreneurship instead of reliance on the resource rent.

• The Rule of Law is the key point of the new identity.

• The key institutional reform – the judicial reform – must ensure independence of courts and give citizens, Russian and foreign investors confidence that the administration of justice will be fair for all.

• Improving laws and law enforcement prac-tices, in particular, changing economic clauses in the Criminal Code in order to rid businesses of the threat of artificial crimi-nalization.

• Radically separating public administration and business, in particular, on the regional and municipal levels.

• Reducing state interference in the economy, curbing the bureaucratization of economic life, and modernizing the state apparatus, which should not be confined to e-govern-ment only.

• Preventing corruption from becoming a norm of life at all levels, not as a one-time campaign but as a national task for the

authorities and the civil society. Anti-corruption struggle must become “the national idea” for the years to come.•Human resources policy based

on the principles of meritoc-racy, competence and decency, rather than servility or clan-nishness.

•Astrongbutcompactandpro-fessional army.

B. Social Issues:• Setting a goal of preserving and developing

the nation and safeguarding people’s rights.• Taking care of the main factors in creating

human capital – families and teachers. • Setting a goal of building up the middle

class for social stability. The post-transition (Latin America-style) inequality should be gradually overcome – not through redis-tribution but by releasing market forces, developing entrepreneurship, and support-ing mechanisms of vertical mobility in the society.

• Introducing social innovations and devel-oping civil society as a vehicle of progress.

Russia also needs a new image, formulated by its leadership in a dialogue with society and constantly adjusted: the Vision of Russia-2030 – Great Russia, which the majority of society is ready to seek

Russia’s Economy: after Transformation, before Modernization

34 Moscow, JAnuAry 2013

Achieving clarity as regards the lifestyle of the majority of people, and understanding as to what a family can hope to achieve over its lifetime without emigrating to another country.

• Achieving mutual understanding and unity of the elites as regards the goals of the country’s development and methods of problem-solving. The elites and the politi-cal class should demonstrate their respon-sible behavior towards the state, property and family. The elites should be ready to cooperate among themselves, as well as with foreign elites and civil society. The

change of the generation in the elites in the future should reflect the need for a steady, sustainable approach to government – the transitional period of illegal takeovers must become a thing of the past.

• The environmental policy, the preserva-tion of natural diversity, and participation in international cooperation in addressing global problems (climate change, food and water shortages, poverty) should take center stage, as in the rest of the world.

• The demographic and employment policies should be aimed at improving the quality of life in cities and creating conditions for enlarging families. Mortality from unnatural causes should be reduced. Support should be given to educated mothers who hand down knowledge to their children at home

much more efficiently than pre-school insti-tutions and who help shape national iden-tity, culture and worker morale in families.

• Ensuring personal safety of citizens and property. Reducing superfluous personnel in security companies.

• Combating poverty in cities and poor regions – searching for models to ensure employment. Creating jobs for highly edu-cated young people.

• Migration policy – ensuring a normal life-style for immigrants; normalizing their legal status; and creating conditions for their adaptation, naturalization and effective work.

•Russia should not avoid (inconditions of peaceful devel-opment)the realistic step of increasing the retirement age to 63–65 years both for men and women, and the sooner, the better. This necessary and

inevitable social shock should be compen-sated for by sharply raising pensions which are now at a humiliating level for the major-ity of pensioners, barely dependent on peo-ple’s contributions to pension funds, and which in essence currently bare characteris-tics of a kind of social aid.

C. Property Issues:• Supporting diverse forms of ownership.

Resolutely combating illegal takeovers of businesses and vestiges of communism. Any property, except that whose criminal origin has been proved, should be declared sacred.

• Protecting property rights, in particular by courts, including in conflicts of businesses or citizens with government agencies.

The Rule of Law is the key point of the new identity

Russia’s Economy: after Transformation, before Modernization

35Valdai discussion club analytical report

• Creating a large class of owners (in the mid-dle class) of stocks, houses and businesses is an important but recently forgotten problem of the transformation. Privatization should be aimed at not so much to increase budget revenues as to ensure efficient management.

• Ensuring real, not formal, completion of the separation of management and owner-ship. Combating bureaucratization which is evolving into managerial “nationalization.”

D. Finance and Investment:• Creating conditions for transforming domes-

tic savings into investments to re-invest domestic savings without dealing through foreign financial centers. Developing an industrial bond market, without which ade-quate funding of large domestic projects is impossible.

• Repealing the blocking stake law.• Increasing the capitalization and competi-

tion of banks – there are too few big banks for such an economy.

• The mega-regulator problem: its creation is now being considered. This issue should be addressed in cooperation with market players.

• Introducing more programs to support small and medium businesses (reducing red tape and taxes for science-intensive busi-nesses, and providing such businesses with premises and loans).

• Working out and implementing a set of measures to bring the economy out of the offshore shadows, specifically by concluding agreements with offshore companies on tax information exchanges.

•It is worth returning to lim-ited borrowing in international financial markets. One must account for such borrowing – it is more efficient than budget investment.

E. Industries and Regions:•Thelaunchofseverallargeeco-

nomic projects in industries and regions will require not only funds of major (state-owned)

companies but also organizational and fis-cal stimulation of small and medium busi-nesses.

• It is necessary to stimulate regions’ initiative and a municipal reform. Federal efforts to redistribute funds should cause regions to move away from parasitic attitudes and start developing.

• The development of South Russia and, especially, the Russian Far East and the Transbaikal Region requires consistent and efficient investment by the state. The idea to increase the country’s economic clout and acquire new development resources through “opening into Asia” is critically important. Meanwhile, activity in the Rus-

The post-transition inequality should be gradually overcome – not through redistribution but by releasing market forces, developing entrepreneurship, and supporting mechanisms of vertical mobility in the society

Russia’s Economy: after Transformation, before Modernization

36 Moscow, JAnuAry 2013

sian Far East has sharply decreased after the APEC Forum. The “Corporation” for Siberia and the Far East, whatever its organiza-tional form, does not exist. The situation is serious – transport barriers and continued migration to the West pose serious obstacles to economic development and geopolitical problems.

• A program is needed to revive Central Russia and the historical Muscovy center, where the bulk of the country’s population lives.

• One needs to understand changes in the sec-toral policy under the WTO conditions. Agri-culture could become one of the main driv-

ers of economic growth, but this requires huge managerial and institutional efforts.

• The defense, nuclear and space industries could help solve technological problems faced by the Russian economy. The most promising technologies (nano-, bio-, and “green” energy) need massive targeted, above all fiscal, support. But a total “new industrialization” is an impractical, if not harmful, myth.

• The transport strategy should become one of the main development drivers by bringing the periphery nearer to the center, develop-ing links among the provinces, and reliev-ing the center of the transportation load.

It should also be linked to the national recreation system, another development resource. Task number one is eliminat-ing bottlenecks in the Transbaikal Region, which can block any growth.

F. Energy and Security:• Updating the country’s energy strategy, tak-

ing account of new tendencies in the world and the need to increase energy efficiency. Existing programs should be brought out of their mutual isolation to link domes-tic demand for energy, competition among various types of fuel, growth in energy effi-

ciency, and export needs.•Careful analysis of the pros-

pects of the industry, which accounts for 4.5% of GDP for capital formation and half of national budget revenues, is needed.. Russia produces 10% and exports about 5% of global

(“primary”) energy, which is a huge contribution to world energy secu-rity. This factor requires fulfilling impor-tant tasks, among them increasing energy efficiency and mitigating climate change in the country (especially in permafrost areas).

• Integrating the factors of energy efficiency, small-scale energy and the use of renew-able fuels into regional strategies in order to avoid inefficient investments in infrastruc-ture.

• In the CIS and, especially in the Eurasian Union, emphasis should be made on energy cooperation, in particular to produce higher value added products.

Any property, except that whose criminal origin has been proved, should be declared sacred

Russia’s Economy: after Transformation, before Modernization

37Valdai discussion club analytical report

* * *A picture of the country’s future in 2030 pro-vides a good opportunity for dialogue with citizens and business. One should take into account the different motivations of the main groups of interests in the long term, create such motivations and determine the limits of pos-sible growth in well-being and freedom in order to avoid excessive expectations. This is a task for

five years of presidency, which must be solved to ensure the country’s sustainable development, achieve and maintain the status of a modern great power, and increase its political, cultural, economic and defense competitiveness.

P.S. Theoretically, there are options of a mobilization break-through based on the use of state indicative planning. These vari-ants were discussed by the Valdai Club and were also presented by some members. Our preferred or optimal scenario (section “What Should Be Done?”) has included some elements of these propos-

als. At the same time, like the overwhelming majority of participants in the discussions, we believe that Russia still has a chance for fast and quality development through creating systems of modern economic and social institutions, strengthening the legiti-macy of ownership, and improving the qual-ity of human capital. Creating a subject for the mobilization variant of enhanced plan-

ning is even more difficult than for the institutional-innovative scenario. The state apparatus is too corrupt and enjoys too little trust among the active part of society for that.

However, it may happen that the mobilization scenarios will have

to be implemented if continued degradation tendencies are coupled with a sharp and last-ing fall in energy prices, which may put the country in a difficult situation of a financial shock.

It is necessary to stimulate regions’ initiative and a municipal reform. Federal efforts to redistribute funds should cause regions to move away from parasitic attitudes and start developing

A picture of the country’s future in 2030 provides a good opportunity for dialogue with citizens and business

Russia’s Economy: after Transformation, before Modernization

38 Moscow, JAnuAry 2013

Appendix.

Scenarios for Russian Economic Development until 2030 — Quantitative ApproachBy Evsei T. Gurvich