ryan nabil final draft 2

TRANSCRIPT

Ryan Nabil

“What are the Characteristics and Determinants of U.S. and Chinese Foreign Direct

Investment in Africa?”

May 9, 2015

Nabil 1

1. Introduction

If a company wants to serve a foreign market, it essentially has three options: it can

produce goods domestically and export them to the foreign market, produce goods in the

foreign market using a foreign firm, or produce in the foreign market by buying majority

shares of a local company. This last option is called Foreign Direct Investment (FDI). FDI is

defined formally as “cross-border investment by a resident entity in one economy with the

objective of obtaining a lasting interest in an enterprise resident in another economy” (OECD

Library, 2012). FDI occurs when a company purchases 10 or more percent of the outstanding

shares of an enterprise, allowing the company to have the controlling share of the entity.1 For

instance, if an American entity buy stocks of an African enterprise, the American company

will have the controlling share of the company and can introduce new techniques of

production and management in the company.

There are two main types of FDI: horizontal FDI and vertical FDI. Horizontal FDI

occurs when firms replicate identical production techniques in multiple countries. For

instance, when Pepsi Cola establishes a production facility in Lagos, Nigeria to produce

beverages, it employs the same production technique as it uses in its headquarters in New

York. Pepsi Cola’s investment to acquire a firm in Nigeria to serve domestic customers there

is an example of horizontal FDI. On the other hand, vertical FDI occurs when firms locate

different stages of operation in different countries. For instance, in the production process of

MacBook laptops, Apple produces the processors in California, but assembles them in China

because of lower labour cost in China. Apple’s investment to purchase an assembly factory in

China is an example of vertical FDI. Both horizontal and vertical FDI bring host countries a

number of benefits, including higher capital stock and output, increased employment, tax

1 However, if a company purchases less than 10 percent of outstanding shares, it does not have the controlling

share of the entity. This investment is referred to as Foreign Portfolio Investment (FPI).

Nabil 2

revenues, and exports. Lastly, as Apple and other foreign companies train their local

employees, they improve the host country’s human capital stock. As these employees leave

the multinational companies and join local companies, they bring their improved managerial

and technical skills to the local companies. Thus, FDI can have significant spill over effects

in the local economy.

Because of increase in capital stock and human capital, FDI is important to Africa’s

development, but as a continent, it receives only a minority of the world’s FDI flows: for

instance, in 2000-2005, it received only 2.2 percent of the global FDI flows (UNCTAD,

FDI/TNC Database). Some economists think that in order for Africa to grow at the same rate

as Southeast Asia did in the 1980s, Africa needs more FDI and the increase in physical and

human capital training that accompanies it (UNCTAD). Apart from the European Union, the

United States and China are the two main development partners of Africa.2 In this paper, I

will compare American and Chinese FDI patterns in Africa. I will also investigate their

determinants. This investigation is important because if American and Chinese FDI in Africa

are functions of certain policies such as lower tax rates or stronger protection of intellectual

property rights, then African governments can attract more FDI by changing those policy

variables.

This brings me to the second part of my motivation for this paper: the popular media

has been sceptical of the Chinese involvement in Africa. For instance, with the increase in

Chinese FDI, particularly in the natural resources sector, Chinese involvement in Africa has

been called “neo-colonialist,” and “neo-imperialist” (Okeowo, 2013). It has been suggested

that the Chinese investors are interested in Africa to exploit their natural resources and are

2 The other main development partner of Africa is the European Union. Since the EU consists of 27 states, it

would be more difficult to generalise about the European FDI determinants in Africa (for instance, France and

the UK have different colonial legacies and are more interested in certain countries than others). On the other

hands, southern and Eastern European countries might also have their own FDI objectives. Therefore, I find

China and US to be a more interesting comparison.

Nabil 3

more likely than other investors to support states with poor human rights records. As a part of

my investigation, I will also explore if Chinese investors are more likely than American

investors to invest in countries that have high concentrations of natural resources.

2. Historical Overview

2.1 The United States in Africa

The United States has been involved significantly with Africa since the early modern

times. Unlike that of China, the U.S. involvement in Africa has been intertwined with its

history of slavery. The United States Africa Command provides a useful summary of

historical U.S. exchanges with Africa in “Fact Sheet: U.S.-Africa Relations Chronology”: in

1619, the first group of African slaves arrived in Florida in what was then the English Colony

of Jamestown, Virginia (the United States Africa Command, 2008).3 In 1777 Morocco

became the first country in the world to recognise the United States as a nation following its

War of Independence with Britain. Between 1798 and 1808, the United States imported

approximately 200,000 African slaves, which was the highest number of slave imports to the

United States in its history. In 1808 the Congress outlawed slavery, but it did not come to

effect until 1820, when the Congress equated slave trade with piracy and makes its imports

punishable by death. In 1822 the United States establishes the first African-American

settlements, which leads to the creation of Liberia.

In the next few decades, when European nations began exploring and colonising

Africa, the United States assumed a reluctant role. For instance, when German Chancellor

Otto Von Bismarck hosts the 1884-85 Berlin Conference, which marked the beginning of the

European colonisation of Africa, the United States sent a representative, but did not act as a

major player in the talks. In fact, over the years, the United States remained anti-imperialist:

3 The exact country of origin of these slaves are unknown.

Nabil 4

during the 1899-1902 Boer War, the American popular support sways in favour of the Boers

as the “anti-imperialist yeomen fighters” (the U.S. Africa Command, 2008). During and after

the Second World War, the United States became involved in emancipating several African

countries. In the 1942 Operation Torch, American and British troops drove the Axis forces

out of Africa by defeating them in Vichy French-Morocco, Algeria, and Tunisia.

Furthermore, during the 1956 Suez Canal, the United States and USSR pressured Israel,

Britain, and France into leaving Egypt, which bolstered the United States’ image as an anti-

imperial force in Africa.

However, American publicity in Africa suffered during the Cold War era, as

American interests at times did not align with those of Soviet-backed African leaders. For

instance, in 1961, the Kennedy Administration backed Belgium and the presence of Belgian

peacekeeping forces in Congo, which was deemed as the better alternative to pro-Soviet

Congo. Furthermore, American complicity and suspicions of its involvement in the death of

Patrice Lumumba, pro-Soviet Congolese independence leader and the first democratically

elected Congolese Prime Minister, deteriorated African perceptions of the United States.

Furthermore, fear of Soviet-led government in Angola led the United States to support the

minority National Liberal Front of Angola (NLF), which lengthened its civil war between

NLF and pro-Soviet groups. Such proxy-wars bolstered the idea that the United States was

interested in Africa to maintain its hegemony against the Soviet Union.

2.1 China in Africa

While China has not been as involved in African politics like the United States,

Chinese involvement in Africa is not a modern phenomenon; in fact, it dates back to the

Ming Dynasty, when the Chinese imperial sailor Zheng He made four trips to the coast of

Africa between 1405 and 1433 (Wade, 2004). However, in the next few centuries following

Nabil 5

Zheng He’s explorations, China would pursue protectionist and inward-looking foreign

policy. Modern-day exchanges between Africa and China dates back to the 1950s, when

China looked towards Africa to counterbalance the Soviet hegemony after its relationship

with the Soviet Union deteriorated (Ayodele and Sotola, 2014). In fact, African countries

provided important support to China in the United Nations, especially as China dealt with its

disputes over Taiwan. During the next two decades, China provided foreign aid to thirty

African countries. However, during the 1980s, as China focused on inward economic

development, its relationship with Africa suffered. The 1990s saw the Chinese re-emergence

in the continent, with increased focus not just on direct foreign aid, but also on investment,

technology transfer, development assistance, and trade.

Since its re-emergence in Africa in the 1990s, China has become an important

economic partner for Africa: between 2000 and 2012, trade between China and Africa

increased from $9 billion to $166 billion, making China the largest trading partner of Africa

(U.N. Comtrade, 2014). In the same time period, Chinese FDI to Africa increased from $200

million to $2.9 billion (UNCTAD, 2013). While U.S. FDI to Africa is still slightly greater

than Chinese FDI to Africa, China is now the largest developing country trading partner of

Africa, making Chinese involvement in Africa an interesting counterpart to American

involvement in the region.4 Furthermore, China, unlike the United States, improved its

poverty rate from 84 percent in 1981 to 15.9 percent in 2005, which makes the Chinese

model of development relatable to many Africans (Zheng, 2010: 273).

4 See Chart 1a and 1b at the end of the paper for distribution of American, European and Chinese FDI in Africa.

Nabil 6

3. Theory

3.1 Investment Theory

In the history of FDI literature, there have been two major theories: capital or

investment theory, and OLI theory. Until the 1950s, investment theory was the main theory in

understanding FDI patterns. Investment theory predicted that capital should flow to countries

with lower capital stock and higher returns. This theory was bolstered by empirical evidence

on American investment in Europe, which was the major source of FDI in the world at that

time. During the 1950s, American investment in Europe indeed earned higher returns than

American investment at home (Mundell, 1957). However, in the 1960s and 1970s, when

returns to American investment in Europe became lower, investment theory did not fully

explain why capital did not flow as much to African countries, which had much lower capital

stock and higher returns than European countries. After investment theory came OLI theory,

which is the framework I use for the majority of my paper.

3.2 OLI Framework

Among the different theories put forward by economists regarding FDI, the “eclectic

approach” or the “OLI” framework is helpful in understanding why multinational

corporations (MNCs) invest in certain countries. OLI stands for ownership, location, and

internalisation advantages. “World Economy FDI: the OLI Framework” provides a useful

summary of these advantages (Neary, 2015). Ownerships advantages refer to the specific

capabilities of a firm for which it wishes to enter a foreign market. Ownerships advantages

include factors such as large amounts of asset, patent, technology, and production techniques.

Such advantages often make a multinational company more competitive than domestic firms.

For instance, local entrepreneurs in Kenya might not possess the technology or infrastructure

Nabil 7

to extract oil. However, British Petroleum has the technological expertise and equipment with

which to extract oil. Consequently, when British Petroleum operates in Kenya, it is able to

compete there because of its superior assets and technical knowhow, that is, because of its

ownership advantage.

Locational advantages, on the other hand, explain factors about a particular country

for which firms wants to invest there. Such advantages can include factors such as the size of

the economy (as measured by real GDP) or population, which make the host country

attractive to investors. For instance, Coca Cola is more likely to invest in Nigeria, Egypt, and

South Africa, the three largest economies in Africa, rather than Somalia, Gambia, and

Comoros, the three smallest ones, since the larger economies have more purchasing power

than the smaller ones.

Lastly, internalisation advantages explain why a firm finds it more advantageous to

produce goods itself, rather than letting a domestic firm license its technology and produce on

its behalf. Licensing makes it difficult for a firm to keep its technology secret, and makes it

more likely that other firms will steal its technology. Consequently, if a firm wants to protect

its technology against risk of imitation and other opportunistic behaviour, it may decide not

to issue a license. For instance, if Apple issues a license to a local firm, in the absence of

strong property rights, the local firm may steal Apple’s technology. Therefore, Apple has an

incentive to run its own firm to protect its technology against imitation. Internalisation

advantage refers to the benefit that Apple gets when it runs its own firm rather than licensing

its technology.

4. Literature Review on Determinants of Foreign Direct Investment

There has been little empirical research comparing U.S. and Chinese FDI in Africa,

but there has been a number of empirical studies concerning the global determinants of FDI.

Nabil 8

Previous research found GDP per capita, GDP, and market size to be the most important

determinants of FDI flow (Kravis and Lipsey (1982), Wheeler and Mody (1992), and

Billington (1993)). This is not surprising since GDP and market size are reflective of a

country’s locational advantages, while lower GDP per capita often signals lower wages and

attracts vertical FDI (see empirical strategy for further discussion on how these variables

relate to the OLI framework). Furthermore, in their research about FDI, James P. Walsh and

Jiangan Yu find openness, average inflation, and GDP per capita to be key determinants

(Walsh and Yu, 2010). The other important determinants of FDI include trade openness, host

country tax rate, and human capital. I include all of these variables in my regression.

Whilst there has not been as much research regarding the determinants of U.S. or

Chinese FDI in Africa, there has been a substantial body of research regarding the

determinants of U.S. FDI in Europe. Previous studies by Lunn (1980) and Culem (1988)

found market size and growth to be important determinants of U.S. FDI in the European

Union area; however, to what extent these determinants are true of U.S. FDI in Africa

remains unclear. I include GDP growth rate in my regression to investigate if GDP growth

rate is an important indicator of U.S. FDI in Africa as well as Europe.

5. Data Analysis

Before discussing empirical strategy, I would like to discuss the general trends in my

dataset. The data on FDI flows between 2006 and 2012 is available from the United Nations

Conference on Trade and Development (UNCTAD). There are several countries for which

FDI data are not reported for the years 2006 and 2007. In order to maximise the number of

countries in my sample, I take the average FDI flows between the years 2008 and 2012

Nabil 9

The dataset contains 31 of the 53 countries of the African continent (see footnote for

the 31 countries).5 It contains all the major economies of Africa, including South Africa,

Egypt, Mauritius, and Angola. The countries in the dataset are geographically diverse: for

instance, while South Africa is at the southernmost point of Africa, Morocco and Algeria are

in North Africa, and Mauritius is in the Indian Ocean about 1,200 miles off the southeast

coast of Africa. However, this dataset does not include a few small islands such as Cape

Verde, Reunion (France) and Saint Helena, Ascension and Tristan da Cunha (UK). It also

does not contain certain war-torn countries such as Sierra Leone, newly independent nations

such as South Sudan, or disputed territories such as the Western Sahara. Nonetheless, since

most of these nations receive little to no FDI, their omission from the dataset is not likely to

significantly impact my results.

5.1 Recipients of FDI

The average U.S. FDI flow to 31 countries in the sample was $176.71 million,

whereas the average Chinese flow was $78.81 million. In absolute terms, the highest five and

lowest three recipients of U.S. and Chinese FDI flows are as follows:

Country US FDI Flow (2008-

2012) ($million)

Country Chinese FDI Flow

(2008-2012)

($million)

Egypt 1655.00

South Africa 886.31

Nigeria 1251.20

Nigeria 209.96

Mauritius 755.80

Congo, Dem. 181.34

Angola 688.40 Sudan 112.93

South Africa 643.40 Algeria 163.45

Eq Guinea -143.40 Eritrea 1.54

Tunisia -144.00 Tunisia 0.36

5 Algeria, Angola, Botswana, Cameroon, Congo, the Democratic Republic of Congo, Cote d’Ivoire, Egypt,

Equatorial Guinea, Eritrea, Gabon, Ghana, Kenya, Liberia, Madagascar, Malawi, Mali, Mauritania, Mauriitus,

Morocco, Mozambique, Niger, Nigeria, Rwanda, Senegal, Seychelles, South Africa, Sudan, Tunisia, Uganda,

and the United Republic of Tanzania.

Nabil 10

Gabon -154.50 Cote d’Ivoire -1.21

Here are two charts showing U.S. and Chinese FDI flows to Africa, followed by a map of

Africa by FDI recipients:

0.00

200.00

400.00

600.00

800.00

1000.00

Sou

th A

fric

aC

on

go,…

Alg

eria

Mau

riti

us

Egyp

tK

enya

Un

ited

Re

p. o

f…C

on

goB

ots

wan

aG

abo

nSe

ych

elle

sM

auri

tan

iaU

gan

da

Cam

ero

on

Mal

awi

Tun

isia

Ch

ines

e FD

I Flo

w (

in M

illio

ns

of

USD

)

Countries

Chinese FDI Flow (2008-2012) by Destination

-500.00

0.00

500.00

1000.00

1500.00

2000.00

Egyp

t

Mau

riti

us

Sou

th A

fric

a

Gh

ana

Mo

rocc

o

Bo

tsw

ana

Mo

zam

biq

ue

Sud

an

Mau

rita

nia

Nig

er

Erit

rea

Sen

ega

l

Cam

ero

on

Co

ngo

Equ

ato

rial

…

Gab

on

US

FDI F

low

(in

Mill

ion

s o

f U

SD)

Countries

U.S. FDI Flow (2008-2012) by Destination

Recipients of U.S. and

Chinese FDI in Africa

(Brookings, 2012)

Nabil 11

We see a few key trends here: several countries, such as South Africa, Egypt, Nigeria,

and Mauritius monopolise FDI flows into Africa. These four countries account for 78% and

52% of 2008-2012 U.S. and Chinese FDI flows to Africa. Apart from the Democratic

Republic of Congo, there is a strong overlap between the major recipient of U.S. and Chinese

FDI: South Africa, Nigeria, and Mauritius are in the top 5 recipients for both countries. The

large discrepancy between U.S. and Chinese FDI in the Democratic Republic of Congo is due

to the 2008 $9 billion deal between China and Congo, of which $6 billion is to be invested in

infrastructure and $2 billion in mining operations (The China Monitor, 2008).

Secondly, apart from South Africa, which is the largest recipient of Chinese FDI to

Africa, Chinese FDI flows are more evenly distributed, with the lowest FDI recipient being

Gabon, with a net FDI inflow of -1.21 million. This means that between 2008 and 2012,

Chinese investors pulled out $1.21 million out of Gabon. However, while the U.S. has, on

average, higher FDI flow into Africa, they are highly concentrated in Egypt, Mauritius, South

Africa, and Ghana. Furthermore, the U.S. investors have been pulling out substantial sums of

money from Gabon, Tunisia, and Equatorial Guinea. Between 2008 and 2012, it pulled out an

average of $154.50 million dollar out of Gabon. In fact, the magnitudes of U.S. FDI flows

tend to be higher in both extremes: U.S. FDI flow (to Egypt) is 86% higher than the highest

Chinese FDI flow (to South Africa). At the same time, the U.S. also pulled out money from

risky countries faster than China did. For instance, consider Tunisia, a country that was 2nd

lowest FDI recipient for both countries. While Chinese investors invested added a meagre

$360,000 per year in the period 2008-2012, the US investors pulled out an average of $144

million per year on average during the same time period.

The main reason why both the United States and Chinese investors decreased their

investment in Tunisia is due to the political transition following the Arab Revolution, as

investors became wary of the transitioning political system and the new business policies (the

Nabil 12

Dubai National, 2012). However, it seems that U.S. investors are more sensitive to political

volatility than Chinese investors. In addition to the above example of American investment

fleeing Tunisia, consider the cases of Congo, Gabon, and Equatorial Guinea, three countries

that have been strife with political violence over the last few years.6 American investment

decreased in Cote d’Ivoire by $56.40 million per year between 2008 and 2012, whereas

Chinese investment in Cote d’Ivoire decreased only by $1.2 million per year during the same

time period. Similarly, in Congo, 2008-2012 Chinese FDI flow averaged $35 million, while

U.S. FDI flow averaged $29 million (UNCTAD data).

5.2 Sectors of FDI

Both the U.S. and China invest heavily in Egypt, Mauritius, South Africa, and Ghana:

apart from Mauritius, the other three are large economies with have copious amounts of

natural resources. 7 Natural resource share of GDP for these three countries average 26%,

which is higher than the African average of 21% (UNCTAD). However, to what extent are

the U.S. and China engaged in different industries? While the UNCTAD dataset which I use

does not report sectoral composition of U.S. and Chinese investments, the Brookings

Institution used the Chinese White Paper on Economic Cooperation (2013) and a 2012 CRS

paper “U.S. Trade and Investment Relations with sub-Saharan Africa and the African Growth

and Opportunity Act” to analyse the composition of U.S. and Chinese FDI stocks and here is

a summary of their findings: 8

6 For instance, Congo saw two civil wars in the last ten years, the latter of which ended in 2011. 7 Mauritius is the top recipient of both American and Chinese FDI flows, but this largely reflects the pro-trade

policies of the Mauritian government, in addition to the bilingual work force and political stability, which

encourages foreign investment (the IMF, 2002). Furthermore, Mauritius is used as a conduit to invest into India

because of their Double Taxation Avoidance Argument (DTAA): last year for instance, Mauritius was the

highest source of FDI to India, accounting for 25 percent of India’s total FDI flows in 2012 (the Economic

Times, 2014). 8 No such data on FDI flow is available.

Nabil 13

Sector Percentage of U.S.

FDI Stock

Percentage of

Chinese FDI Stock

Mining and Extractive Industries 58.0% 30.6%

Financial Services 12.0% 19.5%

Construction 0% 16.4%

Manufacturing 5.0% 15.3%

Technological Services and Geological

Prospecting

25.8% 18.2%

Total 100.0% 100.0%

This data provides no evidence to suggest that China invests more in mining and

extractive industries than the United States; in fact, it seems to be the other way around, with

Chinese FDI stock in mining being 30.6% of its total investment as opposed to 58.0% for

U.S. FDI stock. Another sector which stands out is the construction industry, where the

Chinese invest 16.4%, but the Americans do not invest at all. China’s involvement in African

construction breeds the perception that China is a development partner in Africa and an

alternative to institutions such as the International Monetary Fund and the World Bank

(Zheng, 2010: 271). In fact, building infrastructure is an important part of Chinese

involvement with Africa: in 2006, there were 800 Chinese construction companies operating

in Africa (He, 2006).

Furthermore, differences in U.S. and Chinese investment in Africa are indicative of

their relative OLI advantages. The 27.4 percentage point difference between the U.S. and

Chinese investment in mining and extractive industries and the 7.6 percentage point

difference in technological services and geological prospecting reflects the ownership

advantage that the American companies might possess. For instance, American companies

might have better machinery, technical knowledge, and asset than their Chinese counterparts,

which is why they are overrepresented in for mining and extractive industries.

Financial services reflect both ownership and locational advantages: for instances,

accounting and auditing services require strong financial knowledge, which indicate the

Nabil 14

financial firms’ ownership advantages. On the other hand, financial firms are also more likely

to start businesses in countries with stronger locational advantages such as South Africa and

Egypt, which are two of the largest economies in Africa. Lastly, Chinese investment is

slightly higher than American investment in manufacturing, which is suggestive of vertical

FDI in those countries, as countries with lower wages will have comparative advantage in

labour-intensive manufacturing industries. Chinese investment in manufacturing also reflects

the increasing cost pressure in the Chinese textile and electronics industries, particularly in

the coastal industrial zones. In fact, this increase in cost is in fact leading many Chinese

companies to shift manufacturing jobs to countries with countries with lower labour cost,

such as Vietnam, Mexico, and South Africa (Goodman, 2015).

5. Empirical Strategy

I use an OLS regression to investigate the determinants of U.S. and Chinese FDI in

Africa. Here is the regression equation:

𝑃𝑒𝑟𝑐𝑒𝑛𝑡𝑎𝑔𝑒 𝑜𝑓 𝐹𝐷𝐼 𝐹𝑙𝑜𝑤 𝑡𝑜 𝑇𝑜𝑡𝑎𝑙 𝐺𝐷𝑃

= 𝛼 + 𝛽1 ∗ 𝑇𝑜𝑡𝑎𝑙 𝐺𝐷𝑃 + 𝛽2 ∗ 𝐺𝐷𝑃 𝐺𝑟𝑜𝑤𝑡ℎ + 𝛽3 ∗ 𝐺𝐷𝑃 𝑝𝑒𝑟 𝐶𝑎𝑝𝑖𝑡𝑎 + 𝛽4 ∗ 𝐼𝑛𝑓𝑙𝑎𝑡𝑖𝑜𝑛 + 𝛽5

∗ 𝑃𝑜𝑝𝑢𝑙𝑎𝑡𝑖𝑜𝑛 + 𝛽6 ∗ 𝑁𝑎𝑡𝑢𝑟𝑎𝑙 𝑅𝑒𝑠𝑜𝑢𝑟𝑐𝑒𝑠 + 𝛽4 ∗ 𝑂𝑝𝑒𝑛𝑛𝑒𝑠𝑠 + 𝛽5 ∗ 𝐸𝑎𝑠𝑒 𝑜𝑓 𝐵𝑢𝑠𝑖𝑛𝑒𝑠𝑠 + 𝛽6

∗ 𝐵𝑢𝑠𝑖𝑛𝑒𝑠𝑠 𝑇𝑎𝑥 + 𝛽7 ∗ 𝐻𝑢𝑚𝑎𝑛 𝐶𝑎𝑝𝑖𝑡𝑎𝑙 + 𝛽8 ∗ 𝐵𝑖𝑙𝑎𝑡𝑒𝑟𝑎𝑙 𝑇𝑟𝑒𝑎𝑡𝑦 + 𝛽9 ∗ 𝑃𝑜𝑙𝑖𝑡𝑖𝑐𝑎𝑙 𝑅𝑖𝑔ℎ𝑡𝑠 𝐼𝑛𝑑𝑒𝑥

+ 𝛽10 ∗ 𝐼𝑛𝑡𝑒𝑙𝑙𝑒𝑐𝑡𝑢𝑎𝑙 𝑃𝑟𝑜𝑝𝑒𝑟𝑡𝑦 𝑅𝑖𝑔ℎ𝑡𝑠 + 𝜀

The dependent variable of this regression is the percentage of FDI flow (from the

U.S./China to the total GDP of a country.) 9 Data on FDI flow is available from the United

Nation Conference on Trade and Development (UNCTAD), which lists flows of FDI by

country in terms of million US dollars. I divide the average inward FDI flow between 2008

and 2012 by the average of 2008-2012 nominal GDP per capita (in current US$) to obtain

9 I use fraction of FDI flow to Total GDP as opposed total flows in FDI to control for the size of economy.

Nabil 15

this variable (see Appendix A for a summary of variables). I do this to control for the size of

the country, as measured by its GDP. (See Appendix A: Data and Sources.)

The mean percentage of U.S. FDI flow to GDP is 0.30%, with a standard deviation of

1/76%, whereas those values are 0.25% and 0.27% respectively for Chinese FDI flow to

GDP. The mean percentage of U.S. FDI flow to GDP to African countries is higher than that

for Chinese FDI, which is consistent with the findings from the previous section. The

countries with the highest percentage of U.S. FDI to GDP are Mauritius, Liberia, and Egypt,

while those with the highest percentage of Chinese FDI to GDP are Seychelles, Mauritius,

and Liberia. Chinese FDI flow accounted for only 1.1% of the GDP of Seychelles, whereas

American FDI flow represented 6.6% of Mauritius’ GDP.

Both OLI framework and investment theory inform my choice of variables in the

regression. For instance, total GDP and market size, as measured by the total population of a

country, reflect the locational advantages that a firm can obtain by serving the market in the

host country. Therefore, if coefficients 𝛽1 and 𝛽5 are positive for a host country, it will

indicate the country’s locational advantages.

On the other hand, the share of natural resources of rent in GDP is likely to be

associated with ownership advantages. For instance, if a country is well endowed with natural

resources, it will attract investment from global mining and extraction firms, whose physical,

technological, and managerial skill reflect strong ownership advantages. In that case, I expect

𝛽6 to be positive. Share of natural resources is also likely to attract more vertical or resource

seeking FDI, who will want to exploit the natural resources of the country.

The coefficient on GDP per capita 𝛽3 is trickier to interpret as it can reflect either the

advantages of vertical relative to horizontal FDI or locational advantages. For instance, if 𝛽3

is negative, it may mean that a higher FDI flow to GDP percentage is associated with

Nabil 16

countries with lower GDP per capita and consequently lower wages. A negative 𝛽3 therefore

suggests that a country is more likely to attract vertical FDI, which seeks to exploit cheap

labour. On the other hand, if 𝛽3 is positive, higher FDI flow to GDP percentage is likely to

be associated with higher GDP per capita, suggesting that the higher income of countries

attract horizontal FDI. Since horizontal FDI seeks to replicate the same model of production

technique abroad, locational advantages such as higher GDP per capita are likely to induce

more horizontal FDI. Furthermore, 𝛽3 might also reflect support investment theory: if

investment theory is correct, 𝛽3 is likely to be negative, since more FDI should flow to

countries with higher returns, which according to the neoclassical theory, are the countries

with lower capital stock and lower GDP per capita.

In order to investigate the effect of internalisation advantage on FDI, I include an

intellectual property rights variable. The World Intellectual Property Forum publishes yearly

data on the total number of trademarks filed according to the country of origin. I divide the

weighted 2011/2012 average by 2011-2012 population (in millions) average to construct the

number of trademarks filed by country of origin per million people, which I use as a proxy

for intellectual property rights.10 If firms have strong internalisation advantage and want to

protect their technology, they are more likely to invest in countries with stronger intellectual

property rights. If that is the case, then the coefficient on IPR should be positive, as countries

with stronger property rights will have higher FDI flow to GDP percentages.

I also include inflation, growth rate, trade openness, and tax rates in my regression

since previous research found them to be important determinants of FDI. I use secondary

school enrolment rate as proxy for human capital and the number of days required to start a

10 The other variable that the World Intellectual Property Forum publishes is the World Intellectual Property

Index, which assigns scores almost exclusively to the developed countries: it assigned an index to only six

African countries.

Nabil 17

new business as proxy for ease of doing business. Lastly, several countries in the UNCTAD

sample have bilateral trade treaties with the United States and China, I create bilateral treaty

dummies for U.S. and Chinese FDI flows.11

Variable

No. of

Observati

on

Mean Standard

Deviation

Minimum Maximu

m

Unit

Percentage of Chinese

FDI/ GDP

31 .25 .27 -0.04 1.11 Percentage

Percentage of US

FDI/GDP

31 .30 1.76 -3.67 6.61 Percentage

Real GDP 31 127.72 222.61 1.82 804.26 Billion USD,

PPP (current

international

USD)

Real GDP Growth 31 4.50 2.40 -0.74 10.92 Percentage

Inflation 31 7.89 4.50 1.58 19.66 Percentage

Population 31 26.00 31.41 0.088 159.86 Current

Share of National

Resources in GDP

31 21.64 19.93 24.50 72.89 Percentage

Share of Exports and

Imports in GDP

31 38.05 21.88 4.80 92.80 Percentage

Days Required to Open a

New Business

31 24.52 26.33 5 135 Days

Secondary School

Enrolment Rate

31 58.13 27.16 16 100 Percentage

Business Tax Rate 31 43.37 12.55 24.5 72.8 Percentage

China Treaty Dummy 31 0.29 0.46 0 1 Number

US Treaty Dummy 31 0.13 0.34 0 1 Number

Political Rights Index 31 3.89 1.74 0.75 6.25 Number

Number of Trademark

Application

Filed/Million People

26 2823.31 6985.575 1 29661 Number/Million

11 China has enforced bilateral treaties (BIT) with 7 countries in our sample: Algeria, Ethiopia, Madagascar,

Mali, Mauritius, Morocco, and Zambia. In the dummy variable that I create, I assign a value of one if a country

has bilateral treaty in force.

The United States also has BITs with five countries in our sample: Rwanda, the Democratic Republic of Congo,

Equatorial Guinea, South Africa, and Zambia. I expect bilateral treaties to be positively correlated with FDI

flows into the country

Summary Statistics

Nabil 18

7. Regression Results12

12 *** Significant at 1% level, ** significant at 5% level, * significant at 10% level. Absolute value of t-

statistics provided in parentheses.

Countries in regressions 1 and 2: Algeria, Angola, Botswana, Cameroon, Congo, the Democratic Republic of

Congo, Cote d’Ivoire, Egypt, Equatorial Guinea, Eritrea, Gabon, Ghana, Kenya, Liberia, Madagascar, Malawi,

Mali, Mauritania, Mauritius, Morocco, Mozambique, Niger, Nigeria, Rwanda, Senegal, Seychelles, South

Africa, Sudan, Tunisia, Uganda, and the United Republic of Tanzania.

Countries in regressions 3 and 4: all countries in regressions 1 and 2 except the Democratic Republic of Congo,

Eritrea, Rwanda, Uganda, and the United Republic of Tanzania. Apart from the Democratic Republic of Congo,

to which Chinese FDI averaged $181 million, Chinese and American FDI flows to these countries averaged only

$16.80 and -$3.24 million per annum.

(1) (2) (3) (4)

Variable Share of US FDI to

Total GDP

Share of Chinese

FDI to Total GDP

Share of US FDI to

Total GDP

Share of Chinese

FDI to Total FDI

Real GDP (in

billions USD)

-.0055

(1.61)

-.0011**

(2.31)

-.01**

(2.64)

-.0010

(1.47)

GDP Growth .11

(0.62)

-.0146

(0.50)

.10

(0.51)

.004

(0.12)

GDP per Capita (in

USD)

.000054

(0.68)

.000022*

(1.78)

.00000

(0.62)

.000000

(0.59)

Inflation .034

(0.40)

.029**

(2.30)

-0.09

(1.33)

.001

(0.87)

Population .027*

(1.32)

.0041

(1.34)

.014

(0.78)

.00010

(0.31)

Share of Natural

Resource Rent in

GDP

.010***

(3.48)

.00087*

(1.87)

.013***

(5.54)

.00046

(0.88)

Share of Exports and

Imports in GDP

-.0039

(1.50)

.00026624

(0.64)

-0.0061

(1.24)

.000050

(0.14)

Days Required to

Open a New

Business

-.0055***

(2.91)

-.0011***

(3.63)

-.003*

(1.76)

-.00075**

(2.23)

Business Tax Rate -.0091***

(3.82)

-.0011***

(3.04)

-.0075***

(3.88)

-.0010*

(1.73)

Secondary School

Enrolment Rate

.0035**

(2.24)

.000094

(0.41)

.003

(1.55)

-.000065

(0.22)

US Treaty Dummy .17

(0.18)

0.86

(0.78)

Chinese Treaty

Dummy

-.045

(0.38)

-.00072

(0.22)

Political Rights

Index

.60 **

(2.19)

.042

(1.11)

.22

(1.23)

.017

(0.41)

Intellectual Property

Rights

.00018**

(2.47)

.000015*

(1.70)

Constant -.55

(0.33)

.24

(0.93)

0.30

(0.08)

-.072

(0.21)

Adjusted R-Squared 0.46 0.53 0.59 0.62

Observations 31 31 25 25

Nabil 19

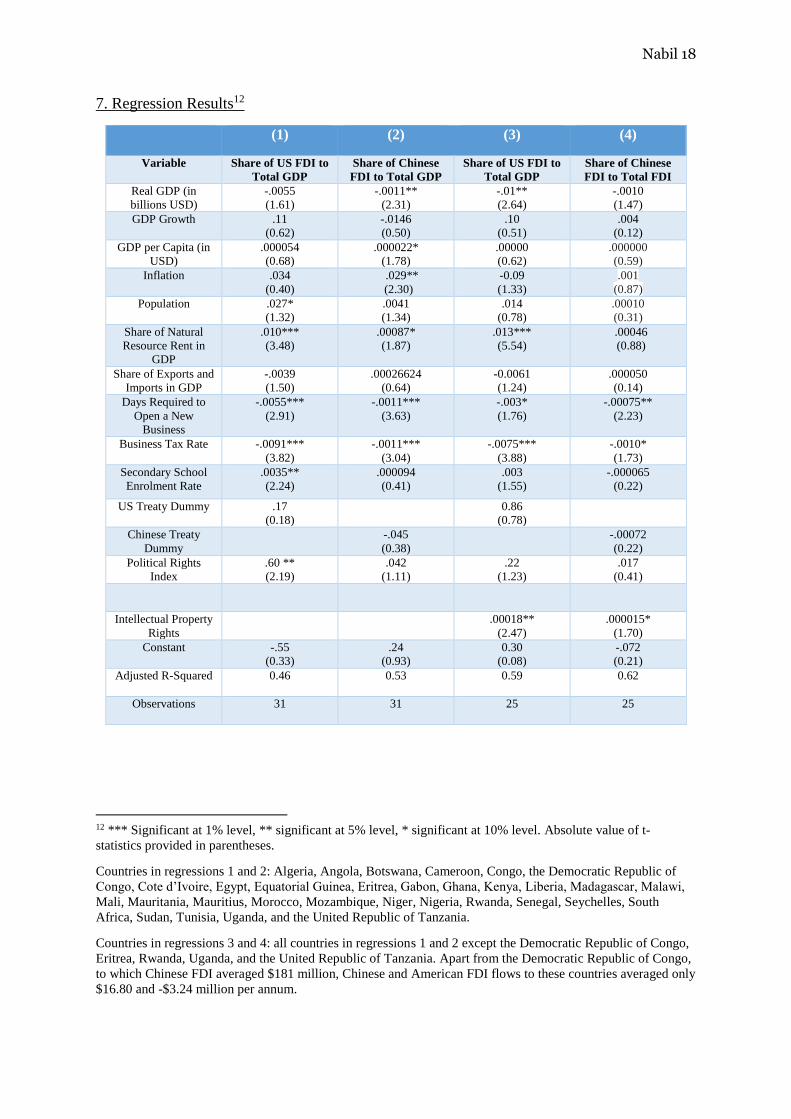

Regressions (1) and (2), included in columns (1) and (2), do not control for

intellectual property rights (IPR), but regressions (3) and (4) do. As seen in column (1),

population, share of natural resource rent, days required to open a new business, tax rate,

secondary school enrolment rate, and political rights index are statistically significant

variables for U.S. investments. On the other hand, real GDP, GDP per capita, inflation, share

of natural resources, days required to open a new business, and tax rates are statistically

significant variables for Chinese FDI.

After controlling for IPR in regressions (3) and (4), real GDP, share of natural

resource rent in GDP, days required to open a new business, tax rate, secondary school

enrolment, and IPR are statistically significant variables for U.S FDI. On the other hand, days

required to open a new business, tax rate, and IPR are statistically significant variables for

Chinese FDI. However, that the magnitude of all of the statistically significant coefficients

are higher for American investment than for Chinese investment, suggesting that American

investment is more sensitive to these variables than Chinese investment.

It is interesting to note that, after controlling for IPR, the share of natural resources is

statistically significant for U.S. FDI, but not for Chinese FDI. This is consistent with the

observation in section 5 that the U.S. invests roughly 60% of its FDI stocks in mining and

extractive services, compared to only 30% by China. This overrepresentation of U.S. FDI in

mining and extractive industries suggest the superior ownership advantages of U.S.

companies, as ownership advantages are important in an capital-intensive field such as

mining and extractive industries. If a country’s natural resource as a share of its GDP

increases by 5 percentage points, this is on average associated with an increase in U.S. FDI

flow by 0.065 percentage points, which represents a 21.7 percent increase in the U.S. FDI

flow/GDP ratio.

Nabil 20

The number of days required to open a business and business tax rates are statistically

significant for both U.S. and Chinese investment; however, the magnitude of these

coefficients are higher for U.S. investment than for its Chinese counterpart, suggesting that

U.S. FDI flow is much more sensitive than Chinese FDI flow. For instance, a 10 percentage

point decrease in business tax rate is on average associated with an increase of U.S FDI flow

by 0.075 percentage points, which represents a 25% increase in U.S. FDI flow/GDP ratio.

However, a corresponding decrease in tax rate is associated with an increase in Chinese FDI

flow by only 0.01 percentage points and an increase in Chinese FDI flow/GDP share by only

4 percent.

Similarly, if the number of business days required to open a business is reduced by a

month, this is on average associated with an increase in U.S. FDI flow by 0.09 percentage

point, which translates into a 30 percent increase in U.S. FDI flow/GDP ratio for that country.

However, this reduction in number of days required to open a business is associated with an

increase in Chinese FDI flow by 0.02 percentage points, which is roughly a 10 percent

increase in Chinese FDI flow/GDP ratio for that country. This suggests that Chinese investors

are significantly less sensitive to changes in ease of doing business than American investors.

To a certain extent, this difference in sensitivity to changes in ease of doing business and tax

rates reflects the underlying differences in American and Chinese FDI decision making. For

instance, whereas American FDI decisions are largely made by privately held multinational

corporations, more than half of Chinese FDI in Africa are controlled by state-owned

enterprises (SOEs) (the Business Insider, 2012). FDI by these SOEs are often a part of

broader governmental policies, which are motivated by a mixture of commercial incentives

and political incentives such as acquiring strategic assets or establishing diplomatic ties. Thus

FDI conducted by Chinese state-owned enterprises are more likely to be less sensitive to

Nabil 21

fluctuations in tax rate and ease of doing business than enterprises with purely commercial

objectives.

Furthermore, IPR is statistically significant for both U.S. and Chinese FDI flows,

suggesting that internalisation advantage is key in considering FDI decisions. However, U.S.

FDI has higher correlation with IPR than Chinese FDI: if trademarks registered per a million

people increases by 500, this is associated with an increase in American FDI flow to GDP

ratio to that country by about 60%, but with an increase Chinese FDI flow to GDP ratio by a

meagre 5%. This should not be surprising, given that U.S. investors tend to have stronger

ownership advantages than Chinese investors, and tend to invest more in technology-heavy

sectors such as geological prospecting, mining and extractive industries, where internalisation

advantages are much more important than in industries such as construction.

Lastly, after controlling for IPR, the size of the economy is strongly inversely

correlated with U.S. FDI/GDP ratio, whereas the correlation is weaker and statistically

insignificant for Chinese FDI/GDP ratio. Real GDP is a strong indicator of locational

advantage of a country. Locational advantages are particularly important to horizontal or

market-seeking firms, which wish to earn profit by serving a local market. It seems that U.S.

FDI in Africa is not driven primarily by locational advantages. Consequently, U.S. FDI tends

to go towards mining and extractive industries, which are industries associated with vertical

FDI more so than horizontal FDI.

8. Limitation

One of the main issues with OLS regression is reverse causality, to which the

regression used in this paper is no exception. For instance, reverse causality is likely to be a

significant problem for the IPR variable. On one hand, countries with strong intellectual

property rights are likely to attract more foreign direct investment; however, on the other

Nabil 22

hand, countries with more foreign direct investment are also more likely to develop stronger

intellectual property rights as a result of the presence of multinational companies and their

internalisation practices. Because of reverse causality, the regression in this paper implies

correlation but not causation.

9. Conclusion

To summarize, it seems that both American and Chinese FDI tend to go towards

countries such as South Africa, Egypt, and Algeria, which are large African economics rich

in natural resources. However, while the U.S. and China both invest heavily in mining and

extractive industries, Chinese investment in Africa is significantly more diversified than its

American counterpart. Indeed, American investment in Africa is associated with higher

percentage of natural resource revenue as a part of total output, indicating the ownership

advantages of American companies. There is therefore little evidence to suggest that China’s

FDI in Africa is dominated by natural resources and ownership advantages; in fact, it is U.S.

investment in Africa that is more strongly associated with the presence of natural resources

and ownership advantages.

Secondly, there are some major differences between the American and Chinese

investment in Africa: American investment hardly goes towards the construction sector,

whereas construction is an important part of China’s involvement in Africa. Chinese

investment is also much less sensitive to variables such as ease of doing business and tax

rates, and internalisation advantages. This diminished sensitivity of Chinese investment, to a

certain extent, is reflective of the mixture of commercial and political incentives of the

Chinese state-owned enterprises.

Given that U.S. investment is more likely to go towards natural resources and mining,

and Chinese investment towards construction and mining, it seems that U.S. and Chinese

Nabil 23

investment are not necessarily in direct competition with one another. The U.S. firms tend to

have stronger ownership and internalisation advantages, and consequently they invest more in

capital-intensive industries such as mining. On the other hand, Chinese firms are more

interested in investing in Africa’s infrastructure and outsourcing China’s labour-intensive

technological and textile manufacturing to lower cost countries such as South Africa.

Because of these factors, the roles that the United States and China play in Africa are

different, and, in some ways, complementary.

Nabil 24

Chart 1: Share of African FDI by Country of Origin (Brookings Institution, 2013).

Chart 1a: Share of FDI stocks

in Africa by country of origin

Chart 1b: Share of FDI flows

in Africa by country of origin

Nabil 25

Appendix A: Data and Sources

Variable Description Source

Fraction of

FDI to GDP

Constructed for country i during year t by dividing the average

2008-2012 FDI inflows (in current US$) by average 2008-2012

nominal GDP (in current US$).

UNCTAD

(2008-2012)

and World

Bank (2008-

2012)

Real GDP Average GDP, PPP (real US$, PPP) between 2008 and 2012 World Bank

Development

Indicator

(2008-2012)

Real GDP

Growth

Annual percentage growth rate of GDP at market prices based

on constant local currency. I use the 2008-2012 average.

World Bank

Development

Indicators

(2008-2012)

Real GDP per

Capita

Average GDP, PPP (real US$, PPP) between 2008 and 2012 World Bank

Development

Indicators

(2008-2012)

Inflation Average of CPI inflation between 2008 and 2012. Inflation is

measured by the Consumer Price Index (CPI), which reflects the

annual percentage change in the average basket of goods and

services that may be fixed or changed at specific intervals, such

as years.

World Bank

Development

Indicators

(2008-2012)

Total

Population

The World Bank uses the de facto definition of citizenship,

which is “the total count of all residents regardless of legal

status or citizenship, except for refugees not permanently settled

in the country of asylum, who are considered part of the

population of the country of their origin.” Total populations are

midyear estimates. Constructed using the average of 2008-2012

populations.

World Bank

Development

Indicators

(2008-2012

Share of

National

Resources in

GDP

Total natural resource rent are the sum of oil rents, natural gas

rents, coal (hard and soft) rents mineral rents, and forest rents

(World Bank, 2011a) . Constructed using the average of 2008-

2012 shares.

World Bank

Development

Indicators

(2008-2012)

Share of

Exports and

Imports in

GDP

Constructed by the World Bank using the World Bank and

OECD national accounts data. I use the 2008-2012 average.

World Bank

Development

Indicators

(2008-2012)

Days

Required to

Open a New

Business

The number of calendar days needed to complete the procedure

to legally operate a business. If a procedure can be speeded up at

an additional cost, the fastest procedure, independent of cost has

been taken (World Bank, 2011b). Once again, I use 2010 data

(since number of days required to open a business tend to stay

the same over the years).

World Bank

Development

Indicators

(2010)

Business Tax

Rate

Business Tax Rate is the percentage of commercial profits that is

paid in taxes. Taxes withheld, for instance personal income tax,

value added tax, or sales taxes are excluded. I use the 2010 data

since tax rates tend to stay constant over time.

World Bank

Development

Indicators

(2010)

Nabil 26

Secondary

School

Enrolment

Rate

Total enrolment in secondary education, expressed as a

percentage of the population of the official secondary age. It can

exceed 100% percent because of early/later school entrance and

grade repetition. I use the 2010 data since this rate does not vary

significantly in our data range.

World Bank

Development

Indicators

(2010)

Chinese

Treaty

Dummy

Dummy variable, where countries are assigned a score of 1 if it

has a bilateral investment treaty (BIT) in force with China. If a

country has a BIT that has been signed, but is not in force, it

receives 0. Similarly, if a country does not have BIT signed with

China, it also gets 0.

African

Growth and

Opportunity

Act Data

Centre (2015)

American

Treaty

Dummy

Dummy variable, where countries are assigned a score of 1 if it

has a bilateral investment treaty (BIT) in force with the United

States. If a country has a BIT that has been signed, but is not in

force, it receives 0. Similarly, if a country does not have BIT

signed with United States, it also gets 0.

Office of the

United States

Trade

Representative

(2015).

Political

Rights Index

CIRI Human Rights Data publishes Physical Integrity Index,

where a country receives a score 0 for terrible human rights

records and 8 for stellar human rights record. This index takes

extrajudicial killings, disappearances, assassinations, freedom of

speech, and freedom of movement into account. Since 2012 data

is not available, I use the 2008-2011 average.

CIRI Human

Rights Index

(2011)

Intellectual

Property

Rights (IPR)

Variable

The World Intellectual Property Indicators list the total number

of trademark applications filed by country of origin. I divide the

2011-12 weighted average share of trademark applications by

the 2011-12 average population to construct the IPR variable.

The World

Intellectual

Property

Indicators

(2012)

Nabil 27

Reference

African Growth and Opportunity Data Center. “Country Trade Profiles.” Accessed online at:

http://agoa.info/profiles.html.

Aykut, Dick. Ratha, Dilip. “South-South FDI Flows: How Big Are They?” United Nations

Conference on Trade and Development (UNCTAD). Transnational Corporations, vol. 13, no.

1. April 2003.

Ayodele, Thompson; Sotola, Olusegun. “China in Africa: an Evaluation of Chinese Involvement in

Africa.” Institute for Public Policy Analysis Working Paper Series. 2014.

Beseda, Hany. Wang, Yang. Whalley, John. “China’s Growing Economic Activity in Africa.”

National Bureau of Economic Research. Working Paper 14024.

Billington, N. “The Location of Foreign Direct Investment: An Empirical Analysis”, Applied

Economics 31. 1999. pp. 65-76.

Blonginen, Bruce A. “Determinants of Foreign Direct Investment.” National Bureau of Economic

Research. Working Paper 16704.

Borenzstein, E. Gregorio, J. De. Lee, J-W. “How Does Foreign Direct Investment Affect Economic

Growth?” Journal of International Economics, vol. 45. 1998. pp. 115-135.

Brooks, D.H.; Hasan, R.; Lee, J.-W.; Son, H.H.; Zhuang, J. “Closing Development Gaps: Challenges

and Policy Options.” ADB Economics Working Paper Series 209. Manila: Asian

Development Bank. 2010.

The Brookings Institution. “The US-Africa Leaders’ Summit: A Focus on Foreign Direct

Investment.” 11 July 2013. Accessed online at: http://www.brookings.edu/blogs/africa-in-

focus/posts/2014/07/11-foreign-direct-investment-us-africa-leaders-summit.

The Business Insider. “Here’s What’s Driving China’s Investments in Africa.” June 27, 2012.

Central Intelligence Agency (CIA). Population Database. Accessed Online.

The China Monitor. “China and the Democratic Republic of Congo: Partners in Development?”

Centre for Chinese Studies. 2008.

Kravis, I, B; Lipsey, R. E. Location of overseas production and production for exports by US

multinational firms, Journal of International Economics, vol. 12. 1982. pp. 201-223.

Cingranelli, David L; David L. Richards; Clay, Chad. “The CIRI Human Rights Dataset.” 2014.

Available online at: www.humanrightsdata.com

Culem, C. “Direct Investment among Industrialized Countries.” European Economic Review, vol. 32.

1988. pp. 885-904.

Dunning, J. H. “Trade, Location of Economic Activity and the MNE: a Search for an Eclectic

Approach.” In B. Ohlin, P. O. Hesselborn, and P. M. Wijkman. “The International Allocation

of Economic Activity.” London: MacMillan. 1977.

Dunning, J. H. “Towards an Eclecting Theory of International Production: Some Empirical Tests.”

Journal of International Business Studies, vol. 11, issue 1. 1980. pp. 9-31.

Dunning, J. H. The Eclectic Theory of International Production: A case study of the international

Hotel Industry. Managerial and Decision Economics. 1981.

Dunning, J. H. “Multinational Enterprises and the Global Economy.” Wokingham, UK and Reading,

Massachusetts: Addison Wesley. 1993.

Nabil 28

Dunning, J. H. “The Eclectic Paradigm as an Envelope for Economic and Business Theories of MNE

Activity.” International Business Review, vol. 9. 2000. pp. 163-190.

The Economist. The Chinese in Africa: Trying to Pull Together. April 11, 2011. Accessed online at:

http://www.economist.com/node/18586448.

The Economist. Africa Rising: a Hopeful Continent. March 2, 2013. Accessed online at:

http://www.economist.com/news/special-report/21572377-african-lives-have-already-greatly-

improved-over-past-decade-says-oliver-august.

The Economic Times. “Foreign Direct Investment from Mauritius to India Drying Up.” April 13,

2014.

Hymer, Stephen. “The International Operations of National Firms: a Study of Direct Foreign

Investment.” The MIT Press. 1958.

Kravis, I.B. and R.E. Lipsey. “The Location of Overseas Production and Production for Export by

U.S. Multinational Firms.” Journal of International Economics, vol. 12. 1982. pp. 201-223.

Llaudes, Ricardo. Salman, Ferhan. Chivakul, Mali. “The Impact of Great Recession on Emerging

Markets.” IMF Working Paper WP/10/237. October 2010.

Mundell, R. A. “International Trade and Factor Mobility.” American Economic Review, vol. 47.

1957.

Neary, Peter. “World Economy FDI: the OLI Framework.” The University of Oxford and CEPR.

Accessed online at http://users.ox.ac.uk/~econ0211/papers/pdf/fdiprinceton.pdf. Date

accessed: May 8, 2015.

Lunn, J. “Determinants of US Direct Investment in the EEC.” European Economic Review, vol. 13.

pp. 93-101. 1980.

Shatz, H. and A.J. Venables. “The Geography of International Investment”, World Bank Policy

Research Working Paper No. 2338. 2000.

Markusen, J. R. “Multinationals, Multi-Plant Economies, and the Gains from Trade”, Journal of

International Economics, vol. 16 (3-4). 1984. pp. 205-226.

OECD Factbook 2013: Economic, Environmental, and Social Statistics. “Foreign Direct Investment.”

Accessed online at: http://www.oecd-ilibrary.org/sites/factbook-2013-

en/04/02/01/index.html?itemId=/content/chapter/factbook-2013-34-en.

Office of the United States Trade Representative: Executive Office of the President. “Africa.”

Accessed online at: https://ustr.gov/countries-regions/africa.

Okeowo, Alexis. “China in Africa: the New Imperialists?” The New Yorker. June 12, 2013.

Renard, Mary-Francoise. China’s Trade and FDI in Africa. African Development Bank Group

Working Paper.

Wacker, Konstantin. “On the Measurement of Foreign Direct Investment and its Relationship to

Multinational Corporations.” Working Paper Series 1614. European Central Bank. November

2013.

Wade, Geoff. “The Zheng-He Voyages: A Reassessment.” Asia Research Institute, Working Paper

No. 31. National University of Singapore. October 2004.

Walsh, James P. Yu, Jiangan. “Determinants of Foreign Direct Investment: a Sectoral and

Institutional Approach.” IMF Working Paper WP/10/187. July 2010. Accessed online at:

https://www.imf.org/external/pubs/ft/wp/2010/wp10187.pdf.

Nabil 29

Wheeler, D. Mody, A. International investment location decisions: The case of U.S. firms, Journal of

International Economics, vol. 33. 1992. pp. 57-76.

The World Bank. “Development Indicators.” Accessed online at:

http://data.worldbank.org/indicator/SE.SEC.ENRR/countries

The World Intellectual Property Indicators. “Data on Trademarks.” 2012. Available online at:

http://www.wipo.int/edocs/pubdocs/en/intproperty/941/wipo_pub_941_2012.pdf.

The World Trade Organization. India-Africa: South-South. Trade and Investment for Development.

2013.

The United Nations Committee on Trade and Development (UNCTAD). India and China Foreign

Direct Investment Database (2014). Accessed online at:

http://unctad.org/Sections/dite_fdistat/docs/webdiaeia2014d3_CHN.pdf

The United Nations Committee on Trade and Development (UNCTAD) International Trade Statistics

Database (2014). Accessed online at: http://comtrade.un.org/pb/

The United States Africa Command. “Fact Sheet: U.S.-Africa Relations Chronology.” September 26,

2008. Accessed online at:

http://www.africom.mil/newsroom/article/6108/factsheetusafricarelationschronology

Zheng, Liang. “Neo-colonialism, Ideology or Just Business: China’s Perception of Africa” Global

Media and Communication, Vol.6: 3. 2010. pp. 271.