school of accounting seminar series - unsw business …€¦ · · 2014-04-29school of accounting...

TRANSCRIPT

School of Accounting Seminar Series Semester 2, 2013

Field evidence on auditors’ and investors’ views on audit quality

Brant Christensen

Texas A&M University

Date: Friday 25th October 2013

Time: 3.00pm – 4.30pm

Venue: ASB 216

Australian School of Business School of Accounting

Field Evidence on Auditors’ and Investors’ Views on Audit Quality

Brant E. Christensen

Mays Business School

Texas A&M University

Steven M. Glover

School of Accountancy

Brigham Young University

Thomas C. Omer

School of Accountancy

University of Nebraska-Lincoln

Marjorie K. Shelley

School of Accountancy

University of Nebraska-Lincoln

October 2013

Acknowledgements: We thank the six participating audit firms and the Center for Audit Quality’s

Research Advisory Board for helping refine our study materials and for funding this project. We

also thank Tara Voskamp for assistance in identifying investor participants. We are grateful for

helpful comments from Brian Fitzgerald, James Flagg, Andrew McMartin, Stevie Neuman, Nate

Sharp, Kecia Smith, Frances Tice, Chris Wolfe, and workshop participants at Texas A&M

University and the 2013 Texas A&M FDS Conference. Brant Christensen acknowledges funding

from the Deloitte Foundation, Steven Glover acknowledges funding from the Driggs Endowed

Professorship in Accounting, and Thomas Omer acknowledges funding from the Delmar

Lienemann Sr. Chair of Accounting at the University of Nebraska-Lincoln. The views expressed

in this article and its content are those of the authors alone and not those of the Center for Audit

Quality or the participating firms.

Field Evidence on Auditors’ and Investors’ Views on Audit Quality

Abstract: We obtain and analyze responses from audit partners, senior managers, and investors

on their views, definitions, and potential measures of audit quality. We find important similarities

and differences with respect to how the two stakeholder groups define audit quality, how they view

the factors that contribute to or detract from audit quality, and how they suggest users can identify

low audit quality using publicly available information. Key findings include: support for some

commonly used measures of audit quality in archival research; differences in the definition of audit

quality between audit professionals (GAAS compliance) and investors (individual auditor

competence); agreement among stakeholder groups that audit team characteristics are among the

most important determinants of audit quality; different views on the importance of audit

committees between audit professionals (increases audit quality) and investors (has no effect);

different views among stakeholder groups on the association between PCAOB inspections and

audit firm quality; agreement among stakeholder groups that high estimation uncertainty threatens

audit quality; and agreement that although not a perfect signal, restatements may be the best

publicly available signal of low audit quality. We employ factor analysis to organize our findings

into discrete key indicators of audit quality.

Keywords: Audit quality, audit quality indicators, PCAOB inspections, estimation uncertainty

Data Availability: Contact the authors.

1

I. INTRODUCTION

Auditing standards require auditors to plan and perform audits to obtain reasonable

assurance about whether or not the financial statements are free of material misstatements and to

express an opinion about the accuracy of the financial statements (PCAOB 2010a).1 The degree

to which financial statement users can rely on an audit opinion depends on the quality of the

audit performed. Despite the importance of audit quality to the stability of the capital markets,

and the large body of research investigating the topic, regulators, investors, and researchers

continue to debate the definition, composition, and measurement of audit quality (Francis 2011;

Knechel et al. 2013). Furthermore, projects seeking to define, measure, and evaluate audit quality

are on the agendas of the International Auditing and Assurance Standards Board (IAASB 2013),

the U.S. Department of the Treasury (2008), the Public Company Accounting Oversight Board

(PCAOB 2012a, 2013), and the Center for Audit Quality (CAQ 2012, 2013), as well as audit

firms themselves (KPMG 2011). In a recent speech, PCAOB board member Jeanette Franzel

listed the task of assessing and tracking audit quality as the Board’s first priority (Franzel 2013).

Given the increased interest in audit quality, this study seeks the insights into audit quality of two

key stakeholders in the financial reporting process: auditors and investors.2

The PCAOB provides information regarding the quality of the audit process through the

release of Parts 1 and 2 of its inspection reports, as well as instructions to audit committee

members regarding discussion of these reports with the auditor (PCAOB 2012b). In order to

create a well-rounded view of audit quality, it is critical to obtain input from the auditors who

1 The PCAOB has defined “reasonable assurance” as “high” assurance (PCAOB 2004a). 2 We use the term “auditors or “audit professionals” throughout the paper to describe both partner and senior

manager participants; over 80 percent of our survey responses are from partners. Untabulated analysis indicates that

the two groups’ responses are not statistically different (p > 0.10 in all comparisons). Further, we use the term

“investors” throughout the paper to describe our investor participants. While these participants are not professional

investors, their educational background and reported investing experience suggests they are experienced and

knowledgeable investors. See Section III for additional details.

2

attest to, and investors who rely on, the financial reports directly affected by audit quality. We

use a survey to obtain audit professionals’ and investors’ insights into audit quality by asking

participants to define and measure audit quality; evaluate the association with audit quality of

various engagement-, team-, and entity-specific characteristics; evaluate the association between

PCAOB inspection findings and the quality of the audit firm as a whole; assess the impact of

estimation uncertainty on perceived audit quality; and identify publicly available signals of low

audit quality. Prior archival studies use a variety of proxies for audit quality, including client

restatements, audit fees, going concern opinions, lawsuits filed against auditors, client

bankruptcies, level of abnormal accruals, and SEC enforcement actions (e.g., Carcello and Nagy

2004; Francis et al. 1999; Francis and Michas 2012; Lambert et al. 2011; Lennox 1999; Palmrose

1998; Stanley and DeZoort 2007). Further, the PCAOB has initiated its own project to define and

measure audit quality (PCAOB 2013). Our results seek to inform efforts to define and measure

audit quality by providing evidence on audit professionals’ and investors’ perceptions,

definitions, and measurements of audit quality.

Surveys serve a critical role in understanding and gaining insight into theoretical

constructs that are often unobservable and, when studied archivally, subject to measurement

error and omitted correlated variables biases (Dichev et al. 2013; Nelson et al. 2002). Auditors

have been surveyed on topics such as earnings management (Nelson et al. 2002), the effect of

auditor behavior on audit quality (Herrbach 2001), the effect of budget time-pressure on audit

quality (Coram et al. 2003), in-person versus electronic review (Agoglia et al. 2010), and auditor

identification of fraud risks (Graham and Bedard 2003), but research on the definition and

determinants of audit quality is more limited. Previous studies used surveys of auditors (e.g.,

Carcello et al. 1992; Schroeder et al. 1986), financial statement users, and preparers to rank

3

various audit characteristics (e.g., industry specialization, auditor independence, provision of

non-audit services, etc.) with respect to their importance in determining audit quality. Similarly,

Duff (2004) conducted a survey of U.K. auditors, finance directors, and fund managers to rank

the importance of characteristics identified in the audit quality literature as determinants of audit

quality. However, none of the studies solicited auditors’ opinions on audit quality beyond the

pre-determined characteristics presented in the survey, and previous surveys were conducted

before the Sarbanes-Oxley Act of 2002 (SOX) and the creation of the PCAOB, which

fundamentally changed the audit industry. This study examines audit quality in the current

regulatory and inspection environment.

In addition to professional auditors’ views of audit quality, prior research has

documented an “expectations gap” between what auditors and investors expect of the audit

function (Church et al. 2008; Maijoor et al. 2002; Mock et al. 2012). Because the PCAOB has

initiated a discussion that is likely to influence expectations about audit quality and because an

expectations gap may lead to differing views on audit quality, our study compares responses

between audit professionals and investors, extending the current literature on audit quality.

Gathering and analyzing audit professionals’ and investors’ opinions about the factors that

compose audit quality, along with in-depth interviews with audit partners, contributes to the

public debate on audit quality and may help regulators, standard setters, practitioners, and

researchers develop common understanding and measures of audit quality.

We present five categories of response analyses. The first category is the definition and

measurement of audit quality; the second category relates to the association between various

audit engagement-, team-, and entity-specific characteristics and audit quality. Our third and

fourth categories relate to the association between PCAOB inspection findings and the quality of

4

the audit firm as a whole and to the effect of estimation uncertainty on audit quality. Our final

category relates to publicly available signals of lower audit quality.

We find that audit professionals define audit quality primarily in terms of compliance

with professional standards, whereas investors rely more on the individual characteristics of the

auditors and audit teams who perform the audit. Other definitions of audit quality mentioned by

participants include an audit that results in financial statements consisting of accurate, reliable

information that the investing public can rely upon as evidenced by hindsight; a well-planned

engagement that addresses the significant risks of the company; and an engagement performed

by independent, skeptical auditors. In terms of engagement-specific characteristics of audit

quality, we find that both audit professionals and investors perceive characteristics of the audit

opinion, outcomes from the review process and the payment of reasonable audit fees as pertinent

to determining audit quality. When examining characteristics at the engagement team level, we

find almost unanimous agreement that individual auditor characteristics impact audit quality.

Additionally, we find evidence that input from parties outside the core engagement team such as

the national office and engagement review partners is an important component of audit quality.

We also find evidence that client-specific characteristics such as restatements, SEC enforcement

actions, and the frequency of committee meetings are significant attributes of audit quality. A

factor analysis of these characteristics and their associations with audit quality identified nine

(six) distinct factors of audit quality based on responses from audit professionals (investors) that

may prove useful for identifying the underlying dimensions of audit quality.

We also find evidence of a negative impact on audit quality of estimation uncertainty and

of an unintended interpretation of PCAOB inspection reports. Finally, we find evidence that

auditors and investors view financial statement restatements as one of the strongest publicly

5

available indicators of low audit quality. We believe the insights reported from audit

professionals and investors add to the public discussion of audit quality and highlight the

similarities and differences between professional auditors’ and investors’ views and expectations

of financial statement audit quality.

The remainder of this paper is organized as follows. Section II discusses the survey

instrument design and the data collection process, and Section III describes our survey

participants. Sections IV through VII discuss our audit quality findings, Section VIII discusses

supplemental analyses, and Section IX concludes.

II. RESEARCH DESIGN AND DATA COLLECTION

Research Questions

Standard setters, regulators, and academics are currently undertaking efforts to define,

measure, and evaluate audit quality. The eventual definition and measurement of audit quality

could influence decisions made by regulators, standard setters, audit firms and investors. The

PCAOB’s efforts to define audit quality may change both auditors’ and investors’ views of audit

quality as well as the differences in their perceptions of audit quality that were observed prior to

SOX and the formation of the PCAOB (Church et al. 2008; Maijoor et al. 2002; Mock et al.

2012). Therefore, our study compares responses between these two key stakeholders—audit

professionals and investors—in the current regulatory climate, extending the current literature on

audit quality and informing the discussion regarding the definition and measurement of audit

quality. Specifically, auditors and investors responses address the following five research

questions:

RQ 1) What is the definition of audit quality, and how can it be measured?

RQ 2) What factors contribute to or detract from audit quality?

6

RQ 3) What is the association between findings in PCAOB inspection reports and firm-

wide quality?

RQ 4) How does estimation uncertainty in reported values impact audit quality?

RQ 5) What publicly available information signals lower audit quality?

To address these research questions, auditors (investors) responded to 29 (23) queries

regarding audit quality.3

Survey Design

Feedback on the survey design and valuable insights into different perspectives on audit

quality were provided by senior members of the participating firms and the CAQ’s Research

Advisory Board improved the clarity of the survey questions. The survey instrument was pilot

tested by the participating firms and subsequently revised. The final version of the survey was

then distributed to the participating firms.

Due to differences between audit professionals’ and investors’ professional experience,

understanding, and exposure to the terminology and concepts associated with financial statement

audits, some of the language in the survey had to be tailored to each group. For example, while

audit professionals clearly understand terms such as going concern, engagement team structure,

and the PCAOB inspection reports and processes, slight re-wording of a few questions was

necessary to clarify those concepts for investor participants. To ensure that responses from the

participant groups could be meaningfully compared, care was taken to keep the fundamental

3 The length of our survey is equal to, or shorter than, other contemporaneous surveys (e.g., Dichev et al. 2013;

Nelson et al. 2002). We also note that the order of the questions presented to participants was not randomized. This

was done primarily because questions were presented in meaningful orders and topical groupings that were

generally confirmed using factor analysis. While order effects cannot be ruled out, participants’ responses to scale-

based questions are generally consistent with open-ended questions (e.g., lack of restatements is positively

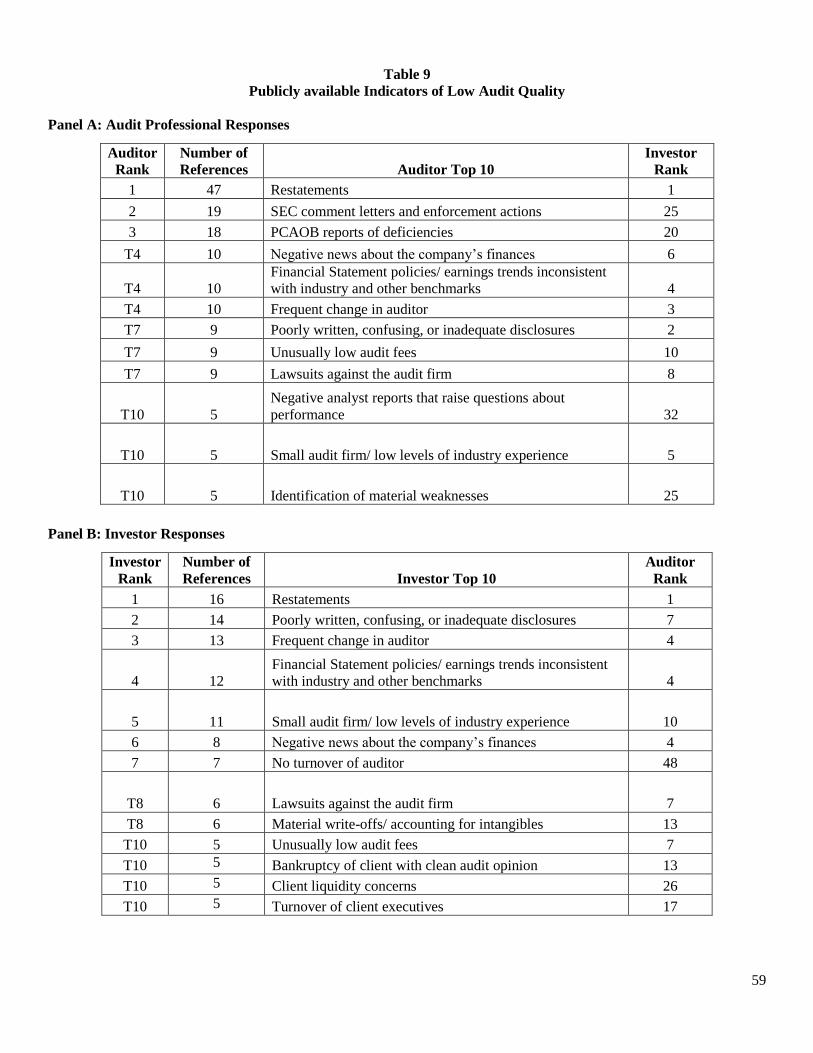

associated with audit quality in question 6.2, and open-ended responses in Table 9 indicate that the presence of

restatements is an indicator of lower quality), thus indicating that the order of question presentation did not drive

results.

7

meaning of the revised questions the same between groups.4 We also did not ask investors

questions that were specific to the audit process itself (e.g., timeliness of audit planning). The

investor version of the survey was distributed to a small pilot sample of investors for feedback

and revised accordingly before final distribution.

Data Collection

The CAQ’s Research Advisory Board coordinated with the six participating audit firms

(including all four Big 4 firms) to identify auditor participants. The only restriction we placed on

participants was that they have experience servicing public company clients subject to PCAOB

inspection. Upon identification of potential auditor participants, the survey was provided to the

firms by the CAQ. Most firms used the web-based survey administered by Qualtrics.com; the

alternative administration was paper-based. Of the 109 auditor participants who started the

survey, we received usable responses from 93, for a completion rate of 85 percent.5

Investor participants are knowledgeable, nonprofessional investors. To restrict the

participant pool to individuals with a fundamental understanding of financial statements, we

required that all participants have a business degree from a large U.S. university.6 To increase the

likelihood that participants had the necessary financial capital to make investment decisions on

their own behalf, we required that participants be at least ten years beyond graduation. By setting

these restrictions, we believe we identified a pool of participants with the knowledge, ability and

experience to make reasonable decisions as investors. In coordination with the University’s

Alumni Association, a randomly selected subset of alumni from the pool, described above, were

4 For example, whereas the audit professionals were asked about the association between audit quality and “the

entity being audited by a large U.S. audit firm with a strong global network,” investors were asked about “the audit

being performed by a large U.S. audit firm with a strong global network.” 5 Completion rate of individual firms ranged from a low of 70% (one firm) to 100% (three firms). 6 As detailed in Table 2, many participants did not stop their education with an undergraduate degree. As such, many

participants received various additional degrees.

8

sent e-mail invitations to participate in the web-based survey administered by Qualtrics.com. The

University’s Alumni Association sent two reminder e-mails after the initial mailing. Of the 243

participants who initiated the survey, we obtained usable responses from 102, for a completion

rate of approximately 42 percent.7

Follow-Up Interviews

To add additional insight into partners’ perceptions of audit quality and to obtain

reactions to the survey findings, we performed follow-up interviews with six audit partners from

the participating firms. Our interview protocol consisted of seven questions that would elicit

partners’ reactions to our survey results. The protocol was reviewed by the CAQ, after which

phone interviews were organized with the partners. Quotes from the interviews were transcribed

by the authors and then verified with the interviewee for accuracy. We note that individual

quotes do not necessarily represent the opinion of the Center for Audit Quality, its Research

Advisory Board, or the participating audit firms.

III. PARTICIPANTS

Audit Professionals

Descriptive statistics for our auditor sample are detailed in Table 1.8 Seventy-three

partners and 17 senior managers completed the survey. On average, partners and senior

managers had held their current title for just over 11 and 3 years and had worked in public

accounting for over 23 and 11 years, respectively.

<insert Table 1 here>

7 For both auditors and investors, we included any responses in which the participant had responded to at least half

of the survey questions. Of the 93 auditor responses used, 90 completed the entire survey (97%). Of the 102 investor

responses used, 98 completed the entire survey (96%). 8 Demographic information from audit professionals was limited to questions approved by the participating firms. In

the case of one firm, demographic information was provided only at an aggregate level.

9

Auditors reported that, on average, two-thirds of their client portfolio is composed of

companies that are publicly traded. Participants were asked to indicate industries in which they

deemed themselves to be experts; the two industries most frequently indicated were

Manufacturing and Banking/Finance/Insurance (approximately 32 percent each). Our participant

pool also reported expertise in the Retail/Wholesale (22 percent), Technology (22 percent),

Transportation/Energy (17 percent) and Service/Consulting (11 percent) industries. The

remaining industries had expertise levels under 10 percent. Based on the data in Table 1,

participants have experience performing audits in a wide range of industries, consistent with a

recent survey of CFOs (Dichev et al. 2013).

Investors

Table 2 contains descriptive statistics for our sample of investors. Approximately 77

percent of participants are between the ages of 41 and 60, an age range consistent with Dichev et

al. (2013). All participants have undergraduate business degrees and 48 percent have advanced

degrees. On average, participants had worked a total of 24 years and were employed in a variety

of industries, with no single industry being selected by more than 15.8 percent of participants.9

<Insert Table 2 here>

Because education alone does not necessarily equate to investing experience, we asked a

series of questions about actual investing knowledge and experience. On average, our

participants read the business press (e.g., The Wall Street Journal or Bloomberg) approximately

weekly and a high proportion of participants currently invest in a retirement account such as a

401(k) or IRA (93.9 percent), individual mutual funds (86.6 percent), and/or individual stocks

9 We note that investors were only asked to select one industry (the industry that best matches their current job)

while auditors were able to select multiple areas of expertise. The different phrasing of the question is due to the

inherent difference between professionals in industry versus public company auditors who may have expertise

across industries.

10

(84.1 percent).10 Approximately 89 percent of participants have used financial statement

information to evaluate at least one company in the past five years and 93 percent report a total

portfolio value of at least $50,000. Taken together, demographic data from Table 2 indicates that

our investor participants are knowledgeable, nonprofessional investors with reasonable investing

experience.

IV. DEFINITIONS AND MEASURES OF AUDIT QUALITY

The definition and measurement of audit quality can differ markedly from one observer

to the next. Because a respondent’s reference point can affect her/his definition of audit quality,

several recent academic papers have opted to develop frameworks that discuss components of

audit quality, rather than a single overarching construct. A recent review of the audit quality

literature (Knechel et al. 2013) focuses on four dimensions of audit quality: audit inputs (e.g.,

expertise), audit process (e.g., auditor judgment and work performed), outcomes (e.g.,

restatements) and context (e.g., auditor tenure). Similarly, Francis (2011) proposes a framework

that includes inputs, processes, the audit firms themselves (e.g., firm industry expertise), the

audit industry and market (e.g., market competition), institutions (e.g., the PCAOB), and

economic consequences of audit outcomes (e.g., types of opinions issued). In addition to these

academic frameworks, the CAQ, PCAOB, IAASB, and KPMG have proposed their own audit

quality frameworks referencing components similar to those listed above (CAQ 2013; IAASB

2013; KPMG 2011; PCAOB 2013). In this study, we asked participants to provide their own

definition(s) of audit quality and to assess the validity of audit quality indicators suggested in

10 It is possible that investor responses differ based on actual investing experience. We use MANOVA to compare

all responses from investors who use individual stock as a primary investment tool versus those who do not;

responses are not significantly different (MANOVA F-statistic = 1.19, p = 0.29), indicating that the two investor

groups can be analyzed together. Further, when we compare all responses of auditors and only experienced

investors, we continue to find evidence of fundamental differences between auditors and investors (MANOVA F-

statistic = 10.22, p < 0.01).

11

prior research. These insights provided by audit professionals and investors add context and

substance to the proposed theoretical frameworks.

An open-ended question asked participants to provide up to four definitions of audit

quality, as well as how each definition could be practically measured. We received 181

individual responses. After reviewing the responses, the author team created 18 categories for

definitions of audit quality into which two PhD students acting as independent raters categorized

all responses. The Cohen’s Kappa measure was 0.64, an agreement level that is significantly

different from zero (p < 0.001) and that indicates a significant level of inter-rater agreement

above and beyond random chance. The raters later resolved all coding differences; the results

reported in Table 3 represent the consensus of the two independent raters.

As reported in Table 3, Panel A, the most frequently mentioned definition of audit quality

by audit professionals is an audit performed in accordance with GAAS that obtains reasonable

assurance that the financial statements are fairly stated in all material respects.11 This definition

is consistent with the process portion of the audit quality frameworks discussed earlier. To

measure this definition, audit professionals recommend using results of internal and external

review; lack of future restatements; and individual auditor expertise. Auditors’ second most

frequently mentioned definition is an audit that results in financial statements with accurate,

reliable information that the investing public can rely upon as evidenced by hindsight (e.g., lack

of subsequent financial statement restatement). This definition is consistent with the output

portion of the prior frameworks and can be measured by restatements and/or SEC action in

subsequent years. Auditor’s third most frequently mentioned definition is a well-planned

11 Regarding the notion of reasonable versus absolute assurance, one partner responded: “[even] though the audit

standards state and everybody knows that the audit does not provide absolute assurance, when you have one audit

that did not have the right opinion, all of that is of virtually no help. At that point, that notion that the audit is not

designed to be perfect is of almost no help.”

12

engagement that addresses the significant risks of the company, as measured by the results of

internal and external inspection.

<insert Table 3 here>

We present investor responses in Table 3, Panel B. The most frequently mentioned

investor definition of audit quality is one performed by well-trained, competent auditors as

measured by auditor experience, inspection results, and the size of the audit firm. This response

is consistent with the input portion of prior audit quality frameworks and provides evidence that

investors view individual auditor characteristics as an important determinant of audit quality and

provides some support for disclosure of engagement team characteristics (Knechel et al. 2013).

In response to this finding, one partner we interviewed stated, “investors don’t want to hear

auditors talk about GAAS, compliance, etc. because in some respects that’s seen as a curtain

auditors can hide behind. Investors and audit committee members want to know who is on the

team? Do we have the right team? Do they have the right experience? Don’t tell me about

GAAS, tell me about the team.” Another partner, however, expressed skepticism about this

investor viewpoint, and stated that “you can have the right staffing levels, training and expertise,

but I’m not convinced that automatically translates into audit quality.” This partner went on to

state that “[you] have to combine [those team characteristics] with performing the audit in

accordance with GAAS. Compliance with GAAS is the minimum requirement, but then the

quality of the audit can be improved upon by increasing the quality of the staff through

additional training, expertise, etc.” Several partners expressed the opinion that the different

definitions between the two groups is understandable given their different points of view, but

that the investors’ definition can be viewed as a subset of the auditors’ definition because GAAS

explicitly requires engagement teams to be adequately staffed and trained.

13

Like audit professionals, investors defined a quality audit as a well-planned engagement

that addresses significant client risks (investor ranking #2; auditor ranking #3); an audit

performed in accordance with standards (investor ranking #4; auditor ranking #1); and an audit

that results in reliable financial statements (investor ranking #4; auditor ranking #2). However,

unlike audit professionals, investors also mentioned the need for a quality audit to be performed

by independent, skeptical auditors (investor ranking #3), which they suggested could be

measured by non-audit fees and auditor rotation. This explicit reference to auditor independence

is consistent with concerns recently voiced by regulators (Franzel 2012).

V. ATTRIBUTES OF AUDIT QUALITY

Tables 4, 5 and 6 report audit professionals’ and investors’ responses regarding how the

quality of a specific audit engagement is impacted by a given characteristic. Based on

consultation with audit professionals and based on our understanding of the audit function, the

characteristics listed were sorted into three groups, each of which relates to a different aspect of

the audit: 1) the audit engagement; 2) resources available to the audit team; and 3) the audited

entity. Participants were asked to evaluate the extent to which the quality of an audit engagement

is affected by the given characteristic by marking their response on an 11-point Likert scale

bounded by “Lower Audit Quality” (1) and “Higher Audit Quality” (11) with a midpoint of “No

Association with Audit Quality” (6).12 We compare auditor and investor responses using

12 As with any analysis using a Likert scale, there is the potential that some individual participants will

misunderstand the question and respond on the opposite end of the scale from the rest of the group. As shown in

subsequent tables, it appears that several individual participants did misunderstand certain questions; their responses

were reversed relative to the majority of participants. Upon review of the data, there did not appear to be an

identifiable group of participants who misinterpreted all questions; rather, the reversals appeared to be randomly

distributed across participants. Using factor analysis, we found that 95 percent of auditors and 96 percent of

investors treated the Likert scales in the same manner, providing evidence that the scales were not broadly

misinterpreted.

14

ANOVA and compare each group’s mean response to the midpoint using t-tests.13

Characteristics of the Audit Engagement: Audit Firm Size

Question 1 in Table 4 (Question 4.1) asks participants to indicate the extent to which

being audited by a U.S. audit firm with a strong global network affects audit quality. Audit

professionals indicated that audit firms with this characteristic are strongly associated with

higher audit quality, (mean score of 9.40 on the 11-point scale; different from midpoint at p <

0.01). Investors also associated larger audit firms with higher audit quality (mean score of 7.47;

different from midpoint at p < 0.01), but investors’ perceptions of the association between a

larger audit firm size and audit quality is significantly weaker than that of audit professionals (p

< 0.01). Responses of both audit professionals and investors indicate a positive association

between audit firm size and higher audit quality, generally supporting academics’ use of audit

firm size as a proxy for audit quality (e.g., Francis et al. 1999; Kim et al. 2003). One partner

suggested “by definition the firm would have to be large to perform a quality audit of a large

organization…because only a few firms can actually have the resources and ability to audit the

largest companies that are located in multiple jurisdictions.” However, several partners also

cautioned that a large firm does not automatically perform higher quality audits than a smaller

firm, especially in the case of smaller clients and in certain industries.

<insert Table 4 here>

Characteristics of the Audit Engagement: The Audit Report

Questions 4.2-4.4 investigate the extent to which characteristics of the audit report are

associated with audit quality. Question 4.2 addresses unqualified, or “clean,” audit opinions. In

13 Due to the skewness inherent in testing means between groups, we augment our analysis by testing median

responses for each question between auditors and investors. Inferences are robust to these alternative

(nonparametric) tests.

15

Table 4, we report that 30.1 percent of audit professionals and 50.0 percent of investors associate

an unqualified audit opinion with higher audit quality. Both groups provide a mean response that

is significantly different from the midpoint (p < 0.01), with investors indicating a stronger

association than auditors (p = 0.06). This response by investors is consistent with analysts’ views

on the role of the auditor. In a recent survey, analysts stated that they “take the financial

statements at face value” and that “the underlying assumption…is that the company is audited,

they’re compliant, and they’re doing things the right and proper way” (Brown et al. 2013). The

fact that investors associate an unqualified opinion with high audit quality highlights a potential

misunderstanding within the investing public as to the meaning of the audit report and the level

of assurance auditors provide. SEC filing regulations rarely accept financial statements that are

accompanied by a qualified audit report, resulting in the vast majority of opinions being

unqualified (SEC 2013). Therefore, investor responses from our survey would indicate that

virtually all audits are of high quality, which is not necessarily the case. Audit professionals, on

average, indicate a similar misunderstanding, albeit to a lesser extent (approximately 70 percent

indicate that an unqualified opinion in and of itself is not associated with audit quality).

Questions 4.3 and 4.4 relate to going concern opinions and the association between the

audit report’s accuracy in predicting a client’s future solvency and audit quality. Prior research

has used audit opinion accuracy as a proxy for audit quality. For example, Lennox (1999)

characterizes an audit report as accurate (and thus ostensibly of higher quality) if client

bankruptcies are preceded by the inclusion of a going concern paragraph and, conversely, if

those clients who do not go bankrupt receive an unqualified audit opinion. Despite the fact that

the rate of going concern opinions is less than 10 percent of all audits and that there are relatively

high levels of both Type 1 and Type 2 errors made in identifying going concerns (see Francis

16

2011), research shows that going concern reports are associated with negative stock price

reactions, indicating that investors deem the going concern opinion as informative (Menon and

Williams 2010).

Question 4.3 asks participants the extent to which issuing an unqualified audit opinion is

associated with audit quality if the client subsequently files for bankruptcy. A large percentage,

43.3 percent, of audit professionals indicate that such an occurrence has no association with

audit quality, and an almost equal percentage (44.4 percent) of audit professionals associate

issuing an unqualified audit opinion to a client that subsequently goes bankrupt with lower audit

quality (mean score of 5.43; different from midpoint at p < 0.01). The majority of investor

participants (69.6 percent) also associate this situation with lower audit quality (mean score of

4.00; different from midpoint at p < 0.01) and they do so at a significantly higher level than do

auditors (mean scores of 5.43 and 4.00; different at p < 0.01).

While question 4.3 addresses Type 2 going concern misidentification errors, question 4.4

addresses Type 1 misidentification errors, wherein a going concern paragraph is included and the

client does not fail in a subsequent period. On average, both audit professionals (mean score of

6.94; different from midpoint at p < 0.01) and investors (mean score of 7.08; different from

midpoint at p < 0.01) associate this seemingly conservative reporting pattern with higher audit

quality. In summary, responses from questions 4.3 and 4.4 indicate that audit professionals and

investors view the failure to add a going concern paragraph followed by subsequent client

insolvency as an indicator of lower audit quality, whereas adding such a paragraph followed by

no client insolvency is viewed as an indicator of higher audit quality. These responses provide

some support for using going concern opinions (or the lack thereof) as a proxy for audit quality

(Lennox 1999), keeping in mind the low base rate of going concern opinions (Francis 2011).

17

Characteristics of the Audit Engagement: Review and Inspection Results

The most direct evaluation of an audit’s quality occurs during the rigorous, iterative

review process that all audits undergo. The process begins with real-time reviews during the

audit (PCAOB 2004b), continues with internal firm review performed by the engagement review

partner (PCAOB 2009) 14 and possible additional internal quality control review, and concludes

with external reviews by peer firms and the PCAOB. Audit deficiencies identified throughout the

review process would indicate a departure from standards, thus indicating a decrease in the

quality of the audit.

Questions 4.5 through 4.8 examine how participants view the association between the

audit review process and audit quality. In response to question 4.5, 79.5 percent of audit

professionals indicate that finding fewer audit deficiencies during real-time review is associated

with higher audit quality (mean score of 8.33; different from midpoint at p < 0.01), indicating

that auditors acknowledge the importance of rigorous real-time review. Additionally, this

negative association between the number of deficiencies identified and audit quality persists

through various levels of review including internal quality review (question 4.6), peer-review

(question 4.7), and PCAOB review (question 4.8). In all cases, more than 70 percent of audit

professionals associated fewer deficiencies identified by the review function with higher audit

quality, and only in the case of PCAOB reviews did auditors view the association as being

significantly stronger than did investors (p < 0.05).15 One partner interpreted this significant

14 We note that review by the engagement review partner is also a part of “real-time” review, but will be addressed

along with other consultations from parties outside the core engagement team in Table 5. 15 In untabulated within-subjects analysis, we compare the mean scores among the varying levels of review to

determine whether certain types of review are more strongly associated with audit quality than others. We find that

audit professionals indicate that real-time review (mean value 8.33) has the strongest association with audit quality,

although only statistically different from the more formal internal quality review, in which audit engagements are

selected for review by the firm’s national office (mean score 7.97; different at p = 0.04). Among investors, we find

that peer-review has the strongest association with audit quality (mean score of 8.05) and that this association is

significantly stronger than either internal quality review (p < 0.01) or PCAOB review (p < 0.01).

18

difference between partners and investors as meaning that “investors aren’t as concerned about

the PCAOB inspection process as we the partners are.” Another partner suggested that the

difference is because many PCAOB deficiencies relate to documentation only, and that “better

audit documentation is not necessarily consistent with what the investor public desires.”

Regarding PCAOB inspections, one partner stated that because “there aren’t many measuring

sticks available, I’m not surprised [investors] connect PCAOB deficiencies with audit quality. In

some respects…it speaks well of the inspection process” and another agreed with a negative

correlation between individual engagement quality and the number of PCAOB deficiencies.

Along these lines, several partners noted that the firms take the PCAOB inspections very

seriously, with one partner stating that “the PCAOB has and continues to have a lot of impact,

particularly by focusing on the systems of quality control at the firms. I wish [the PCAOB] put

more emphasis on the quality control system at the firms.”

Characteristics of the Audit Engagement: Timeliness of Procedures

Questions 4.9 and 4.10 investigate the association between the timely completion of

various audit procedures and audit quality.16 The PCAOB’s standard on audit planning (2010b)

states that audit planning is not a “discrete” event but rather a process that takes place starting at

the completion of the prior year’s audit through the completion of the current year’s audit (AS

9¶4). The majority of the planning procedures, however, are performed before fieldwork

commences and are adjusted as necessary. As shown in Table 4, audit professionals view

planning procedures as an integral part of audit quality with 94.6 percent indicating that the

timely completion of planning procedures is associated with higher audit quality. Audits planned

on a timely basis signal that the engagement team has analyzed the client’s risks and designed

16 Due to the subject matter, these questions were only posed to audit professionals.

19

audit procedures to appropriately address those risks. Audit firms’ electronic workpapers makes

this information available to audit firms and to the PCAOB. Responses to question 4.9 indicate

that disclosure of such information, either by the firms or by the PCAOB, may provide valuable

information to investors about factors that drive audit quality.

In addition to the timeliness of audit planning, audit quality is affected by the timeliness

of audit fieldwork completion. Failure to complete audit fieldwork in a timely manner results in

additional time and budgetary pressure, reducing audit quality (Agoglia et al. 2010; Coram et al.

2004; Houston 1999; Lopez and Peters 2012; McDaniel 1990). In support of this notion, 89.3

percent of audit professionals associate the timely completion of audit fieldwork with higher

audit quality. Lambert et al. (2011) indirectly investigate the effect of audit completion

timeliness by investigating the impact of accelerated filing dates on audit quality. When filing

dates are accelerated, auditors have less time in which to perform their work and thus encounter

more time pressure, potentially reducing audit quality. The authors find that acceleration of the

audit report date by 15 days or more results in higher discretionary accruals and a greater

likelihood of just meeting or beating analyst forecasts, measures that have been used to proxy for

audit quality in prior literature (e.g., Davis et al. 2009; Myers et al. 2003). One partner we

interviewed specifically mentioned time pressure as an impediment to audit quality, stating that

“[when I speak of time pressure as an impediment to audit quality], I’m talking about the

findings or the need for information that comes right at the end…and there’s a lot of pressure

from management, and with some clients from the audit committee, in my opinion, to go ahead

and sign the audit opinion without getting that evidence.” In summary, responses from audit

professionals to both questions 4.9 and 4.10 indicate a positive association between the timely

completion of audit procedures and audit quality.

20

Characteristics of the Audit Engagement: Other

Question 4.11 investigates the association between the lack of subsequent lawsuits

against the audit firm and the quality of the audit engagement (Palmrose 1998). Responses to

question 4.11 indicate that, on average, audit professionals associate the lack of a lawsuit with

higher audit quality (mean score of 6.60; different from midpoint at p < 0.01). Investors’ views

of this association are similar to auditors’ (mean score 6.86; different from midpoint at p < 0.01).

Finally, question 4.12 investigates the association between audit fees and audit quality.

All else held constant, auditors’ compensation must be sufficient to motivate audit effort and

gather sufficient audit evidence to justify the audit opinion (Messier et al. 2010; PCAOB 2010a;

Simunic 1980). In response to question 4.12, 72.0 percent of audit professionals indicate a

positive association between audit fees and audit quality. Additionally, the mean auditor

response is significantly higher than that of investors (p < 0.05), of whom only 52.9 percent

indicate a positive association between audit fees and audit quality. While the payment of higher

audit fees does not always ensure higher audit quality, participants’ responses suggest that higher

fees tend to be associated with higher quality.

In summary, results documented in Table 4 indicate that audit firm size; unqualified,

accurate and conservative audit opinions; fewer identified deficiencies; timely completion of

audit planning and audit fieldwork; lack of litigation; and reasonable audit fees are indicators of

higher audit quality.

Resources Available for the Audit Team: Engagement Team Qualifications

Questions in Table 5 examine the resources available to the audit engagement team.

Questions 5.1 through 5.3 address individual characteristics of the audit team, including adequate

staffing, auditor training, and auditor expertise.

21

<insert Table 5 here>

Question 5.1 investigates the sufficiency of engagement team staffing and audit quality.

In response to this question, 100 percent of audit professionals associate adequate team staffing

with high audit quality; with a mean response of 10.02 on an 11-point scale, auditors consider

this association to be very strong. Investors on average agree with this assessment (mean

response of 8.80), but the strength of the association is significantly lower than audit

professionals’ (p < 0.01). Clearly, both groups indicate that adequate staffing is a prerequisite to

achieving a high-quality audit. Consistent with this result, interview participants emphasized that

current staffing practices at audit firms are very rigorous to ensure that high-quality staff are

assigned to each engagement. Adequately-staffed audit teams can improve audit quality by

allocating audit procedures among more engagement team members, thus decreasing the amount

of work assigned to each individual, as well as by appropriately allocating work to those team

members most qualified for the task (Bonner 1990; Griffin and Ricchiute 2011; Hanson 2013).

Question 5.2 investigates the association between audit quality and having well-trained

auditors. Results reported in Table 5 indicate that 100 percent of both audit professionals (mean

score of 10.14) and investors (mean score of 9.66) associate having well-trained auditors with

higher audit quality. In a similar vein, question 5.3 investigates the association between auditor

expertise (e.g., industry-based or transaction-based) and audit quality. Similar to the previous

question, 100 percent of both audit professionals (mean score of 9.82) and investors (mean score

of 9.88) associate auditor expertise with higher levels of audit quality.

The first three questions in Table 5 relate to individual characteristics of the audit

engagement team and its members. Both stakeholder groups overwhelmingly associate these

individual characteristics with high audit quality. Among survey responses, these three questions

22

receive the three highest average scores among any of the questions focused on audit quality,

supporting findings from prior literature that additional knowledge and expertise leads to higher

audit quality overall (e.g., Bedard 1989; Hammersley 2006; Low 2004; Owhoso et al. 2002;

Taylor 2000;Wright and Wright 1997). This finding is also consistent with recent archival

literature that finds that auditor training is positively associated with accruals-based measures of

audit quality, while staff and partner workload are negatively associated with audit quality (Van

Linden and Willekens 2013). Additionally, these findings are consistent with accounting firms’

recent emphasis on key process inputs, such as auditor expertise and training, as crucial to audit

quality (CAQ 2012; KPMG 2011).

Our results provide evidence that individual auditor characteristics are viewed as an

important determinant of audit quality and provide some support for disclosure of engagement

team characteristics (Knechel et al. 2013). One partner indicated that these indicators could be

“reported without embarrassing anybody” while another said that disclosure of these indicators

would be appropriate as long as the nature of the information disclosed is “predetermined” by

standards. However, most partners we interviewed suggested that making such disclosures

comparable would be difficult. For example, one partner stated, “each engagement really is

unique…and potentially has different staffing needs and requirements. If I look at my practice

with clients of similar size, the staffing models may be different due to individual characteristics

of the clients.” Additionally, another partner mentioned, “the intangibles, the qualitative portion

[of engagement team characteristics], would get lost in disclosing to the public those particular

quantitative factors that are important.” As an alternative, this partner noted that perhaps firms

could disclose “a description of the process by which the sufficiency of an engagement team is

evaluated” by the firm itself and disclose items such as engagement risk, internal control

23

effectiveness, prior year audit concerns, etc. to provide more client-specific information on how

the firm evaluates staffing needs. This is consistent with the firms’ willingness to disclose more

information regarding their own internal quality monitoring programs (PwC 2013).

Regarding team characteristics and audit quality, one partner indicated that while he

agreed that engagement team characteristics such as staffing, training, and expertise are

indicators of audit quality, “they don’t define audit quality.” The partner went on to explain that

regardless of how strong the staff members are, the manager and partner can override them.

Specifically, this partner stated that important potential impediments to audit quality are “the

personality and the personal characteristics of the audit partner and manager as to what is driving

them from a personal standpoint. I think both of these things can dramatically change the

outcome of the audit regardless of the quality of the engagement team inputs.” Another partner

suggested that instead of disclosing information about the entire engagement team, the disclosure

could perhaps be limited to characteristics related to the senior leadership of the audit

engagement team (e.g., partners, senior managers).

Resources Available for the Audit Team: Consultations

Questions 5.4 through 5.7 evaluate how consulting with individuals outside to the day-to-

day operations of the audit team impacts audit quality. Input from sources such as engagement

review partners, national office partners, external experts, and internal audit firm specialists also

play an important role in ensuring audit quality, especially when the engagement team

encounters subjective and complicated accounts and transactions. These advisors can have a

significant impact on audit quality and are therefore important to examine.17

17 Due to the inherently specialized nature of these external advisors, we did not pose these questions to investors.

24

Audit standards require audits to be reviewed by an engagement review partner (ERP),

who has the necessary expertise to understand the client but is not directly responsible for, or

involved in the day-to-day activities of, the audit engagement (PCAOB 2009, AS 7 ¶2). We ask

audit professionals to indicate the extent to which the number of hours billed by an ERP is

associated with audit quality. Responses to question 5.4 indicate that 78.4 percent of audit

professionals associate greater involvement by the ERP with higher audit quality (mean score of

7.63; different from midpoint at p < 0.01).

Engagement teams may also contact the firm’s national office for guidance during the

audit. These national office consultations do not occur during every audit engagement, but rather

only when needed to address difficult technical accounting matters, unusual and material

transactions (e.g., mergers and acquisitions), infrequently encountered audit risks (e.g., material

legal contingencies) or other audit methodology judgments for which an audit engagement team

would prefer to receive counsel from the national office. When asked about the association

between the number of national office consultations and audit quality, 69.9 percent of audit

professionals associate national office consultations with higher audit quality, with 25.8 percent

indicating no association between the number of such consultations and audit quality. With an

average response of 7.14 (different from midpoint at p < 0.01), audit professionals on average

perceive a benefit with respect to audit quality from engaging in national office consultations

when needed.

Questions 5.6 and 5.7 investigate the perceived impact of external experts and internal

specialists, respectively, on audit quality. When asked about the association between audit

quality and the number of consultations with external experts, 59.1 percent of audit professionals

associate input from external experts with higher audit quality. On the other hand, when asked

25

about internal firm specialists and audit quality, 82.9 percent of audit professionals associate

consulting with internal firm specialists with higher audit quality. The mean responses for the

two questions, 6.77 and 7.68 respectively, are significantly different (p < 0.01). Based on these

responses, consulting with internal specialists is preferred to consulting with experts outside of

the firm. This finding may be due, in part, to the fact that accounting firms are typically large

enough to employ most types of specialists, reducing the need to seek counsel from external

specialists. However, relying solely on within-firm guidance potentially discounts the value of

advice from a more independent third-party.

In summary, results documented in Table 5 indicate that both stakeholder groups

associate characteristics of the individual audit team such as staffing levels, training, and

expertise with higher audit quality. Additionally, audit professionals generally associate

consulting with individuals outside the core audit engagement team with higher audit quality,

although consulting within the firm (i.e., with internal specialists, the national office and

engagement review partners) is viewed more favorably than consulting outside of the firm.

Characteristics of the Audited Entity: Accruals

In addition to characteristics of the audit engagement and the audit engagement team,

characteristics of the audited entity itself also may be associated with higher or lower audit

quality. These characteristics, such as the entity’s accruals, subsequent outcomes related to the

company’s financial statements, and the entity’s committee meetings are investigated and

reported in Table 6.

<insert Table 6 here>

Question 6.1 investigates the entity’s financial reporting quality as measured by the

conservatism reflected in a company’s accruals. Although an entity’s level of discretionary

26

accruals is a commonly used proxy for earnings quality (see Dechow et al. 2010 for a review), it

has also been associated with audit quality. Studies show that higher discretionary accruals—

which would in theory signal more accounting manipulation by management—is negatively

associated with audits by Big N auditors (Francis et al. 1999; Kim et al. 2003), audit firm office-

specific size (Francis and Yu 2009), audit firm specialization (Balsam et al. 2003), audit firm

tenure (Myers et al. 2003), and is positively associated with past restatements (Francis and

Michas 2012).

We find that 54.8 percent of audit professionals indicate that conservative reserve

balances are associated with higher audit quality. While 37.6 percent of auditors indicate that

there is no association between reserve balances and audit quality, their responses also indicate

that on average audit professionals associate higher quality audits with more conservative

financial reporting by their clients, using accruals levels to represent conservatism (mean score

of 6.89; different from midpoint at p < 0.01). When the same question was posed to investors,

they responded similarly on average (mean score 6.62, different from midpoint at p < 0.01).

Taken together, both stakeholders view conservative accruals as indicating higher audit quality,

providing some support for the use of accruals as a proxy for audit quality.

Characteristics of the Audited Entity: Subsequent Outcomes

Due to data limitations, many studies of audit quality have focused on publicly

observable outcomes related to the audited entity. Questions 6.2 through 6.4 investigate three of

these outcomes: restatements, SEC enforcement actions, and fraud.

Question 6.2 addresses the association between audit quality and the lack of future

restatements by the audited entity related to the period under audit. Restatements are one of the

more visible signals that material information was either omitted or misstated in published

27

financial statements. Restatements have been used as a proxy for lower audit quality under the

assumption that if audit quality had been higher, the auditors would have identified the material

misstatement during the audit process (e.g., Stanley and DeZoort 2007). Consistent with this

notion, 75.3 percent of audit professionals indicate that the lack of future financial statement

restatements is associated with higher audit quality. With a mean response of 7.87 (different

from midpoint at p < 0.01), audit professionals, on average, indicate a positive association

between audit quality and the lack of financial statement restatements. When investors are asked

the same question, 62.8 percent indicate that a lack of future restatements is associated with

higher audit quality, although the perceived association is weaker among investors than auditors

(p = 0.03). In follow-up interviews, partners agreed with these results, stating that using

restatement trends or the lack thereof as an indicator of audit quality “is not 100 percent perfect,

but it’s a fairly good indicator as to whether or not audit quality is improving.” Several partners

we interviewed were surprised that the percentage of investors viewing a lack of restatements as

higher audit quality was not higher than 62.8 percent.

Question 6.3 examines the association between SEC enforcement actions and audit

quality. SEC enforcement actions, as made publicly available through the release of an

Accounting and Auditing Enforcement Release (AAER), are issued as a result of a violation of

the financial reporting requirements in the Securities Exchange Act of 1934 (Dechow et al. 1996;

Pincus et al. 1988). If a company’s SEC filings are the target of an AAER for material

misstatement, users may blame auditors for not identifying and correcting the error before the

release of the financial statements. Accordingly, AAER’s have been used in research to proxy for

low audit quality (e.g., Carcello and Nagy 2004).

28

When we asked audit professionals about the association between audit quality and the

lack of SEC enforcement actions, 70.9 percent of practitioner respondents report that a lack of

SEC enforcement action indicates higher audit quality, consistent with the view expressed

regarding restatements. Similarly, 62.7 percent of investors associate the lack of SEC

enforcement action with higher audit quality. In untabulated results, auditors’ average perceived

association between SEC enforcement actions and audit quality is significantly lower than the

perceived association between restatements and audit quality (p < 0.05), indicating that from the

average audit professional’s perspective, restatements are more strongly associated with audit

quality than are AAERs. One partner explained this significant difference as being “due to the

frequency of occurrence [of the two outcomes]. Very few partners ever deal with an SEC

enforcement action, but almost everyone, at some time in their career, has dealt with a

restatement or two.”

Finally, question 6.4 investigates the association between the lack of future fraud

identification and audit quality. Consistent with responses regarding restatements and SEC

enforcement actions, 62.8 percent of investors associate the lack of future fraud identification

with higher audit quality. The fact that “only” 62 percent of investors view the lack of future

fraud as indicative of high audit quality is somewhat surprising when we take into account

investors’ high expectations of auditors in regard to identifying fraud (Hogan et al. 2008;

McEnroe and Martens 2001).

These external indicators of audit quality are among the most easily observable, but are

also subject to hindsight bias when evaluating the performance of the auditor. One partner stated

the following regarding this bias:

After Pearl Harbor, and after the attacks of 9/11, we do these investigations and we piece

together these things that, looking backward, we can connect these dots, this action or

29

inaction with that one and that one and that one and we can construct all of these things

that led up to this horrible event. And then we can look at the people who were involved

and say ‘my gosh, how could you possibly have not seen this coming?’ Now the problem

with that is that in the real world, we’re always in the beginning of that sequence of

events. Any one of those events by itself, the results are typically benign and yet it’s the

combination over time that eventually causes the problems.

Characteristics of the Audited Entity: Committee Meetings

The final two questions in Table 6 investigate the association between audit quality and

the number of audit committee and board of directors meetings held by the audited entity each

year. Question 6.5 asks participants to indicate the extent to which the number of formally

planned audit committee meetings per year is associated with audit quality. Audit committees are

receiving increasing attention from regulators, researchers, and the financial press (PCAOB

2012b, 2012c; Weil 2012) and audit committee oversight is viewed as an important component

of the audit process. In general, audit professionals agree with this view; 78.2 percent of audit

professionals indicate that the number of audit committee meetings is positively associated with

audit quality (mean score of 7.65; different from midpoint at p < 0.01). When investors are asked

the same question, 56.9 percent of investors see no association between the number of audit

committee meetings and audit quality, and only 31.3 percent indicate a positive association.

Additionally, the mean investor response of 6.19 is not significantly different from the midpoint,

although it is significantly different from auditors’ 7.65 mean response (p < 0.01). As such, there

appear to be significant differences between auditors’ and investors’ views on audit committee

impact on audit quality. We note that potential explanations for the difference are investors’ lack

of familiarity with the role of the audit committee and the lack of ability to observe audit

committee actions and how audit committees impact audit quality.

Question 6.6 addresses the more general board of directors meetings and their association

with audit quality. In this case, the findings are opposite to those related to audit committees.

30

Whereas the majority of audit professionals view the number of board of directors meetings as

having no association with audit quality (53.8 percent), the majority of investors (57.8 percent)

view these meetings as having a positive impact on audit quality; the mean responses of the two

groups are significantly different (p < 0.05). Responses to 6.5 and 6.6 indicate important

differences (or perhaps a knowledge gap) in how audit professionals and investors view the

impact that audit committee and board meetings have on audit quality: while auditors view audit

committee meetings as more important to audit quality, investors view board of directors

meetings as more important.

In summary, results documented in Table 6 indicate that financial statement outcomes are

relevant in evaluating audit quality. Specifically, the lack of future restatements, lack of SEC

enforcement actions, and the number of planned audit committee meetings are among the

outcomes that audit professionals associate with high audit quality. Investors likewise perceive a

positive association between the lack of future restatements, fraud or SEC enforcement actions

and audit quality, although to a lesser extent than auditors. Additionally, investors associate the

number of board of directors meetings with high audit quality, whereas auditors do not.

VI. PCAOB INSPECTIONS AND ESTIMATION UNCERTAINTY

PCAOB Inspections and Audit Firm Quality

The results from Tables 4, 5 and 6 relate to the quality of an individual audit engagement.

Financial statement users, audit committees, and academics are also interested in the quality of

audit firms as a whole. This is difficult to assess because a proper assessment would require

access to the audit firm’s tone at the top, policies, methodologies, training, human resource

management, reward structure, internal inspections, quality control practices, etc. After SOX, the

PCAOB’s board and inspection staff does have access to such information. Perceptions of

31

PCAOB communications about their regulatory oversight, inspection and enforcement processes

and findings, and how such communications relate to audit quality has been the focus of

numerous research studies with mixed results (Abernathy et al. 2013; Canon and Bedard 2013;

Carcello et al. 2011; Church and Shefchick 2012; Defond 2010; Ernst & Young 2011; Fornelli

2012; Glover et al. 2009; Griffith et al. 2013; Lennox and Pittman 2010).

In a release to Audit Committee members on the purpose of PCAOB inspection reports,

the PCAOB states that “the Board…cautions against judging the relative quality of firms’ audit

practices solely on the basis of the number of deficiencies described in the public portions of

inspection reports” (PCAOB 2012b, pg. 3). Thus, the PCAOB contends that the number of

deficiencies reported in their inspection reports should not be used as a statement of overall audit

firm quality. One partner reiterated this in an interview, stating that the sample selected by the

PCAOB “doesn’t start as a representative sample, it doesn’t purport to be a representative

sample, and we know it doesn’t end up as a representative sample.” Another partner stated

similarly that, “it’s very tempting to do a simple deficiency count across Part 1 findings…and in

the absence of other metrics it’s tempting to do that. However, it’s potentially very misleading as

a result of how the inspection process works and how the engagements are selected.”

<insert Table 7 here>

Results reported in Table 7 indicate that in spite of the PCAOB’s warning, 64.5 percent

of audit professionals and 88.1 percent of investors view fewer deficiencies listed in the PCAOB

Part 1 inspection report, the public portion of the report, as being associated with higher audit

quality for the audit firm as a whole.18 In contrast, only 29 percent of audit professionals and

18 PCAOB inspection reports consist of two parts. Part 1, which is released for public viewing upon completion of

the inspection report, lists audit deficiencies identified through inspection of a non-random sample of the firm’s

audits. Part 2 of the report details quality control deficiencies and is not released unless the firm does not adequately

address these deficiencies within one year.

32

10.9 percent of investors indicate that the number of deficiencies has no bearing on firm-wide

audit quality. The mean response for investors (7.90) was significantly higher (p < 0.01) than the

mean response for auditors (6.99), indicating that investors may use a count of deficiencies in

these reports for a purpose not intended by the PCAOB.

Reacting to the difference in perceptions between investors and auditors, one partner

suggested that “partners [responses] are lower [than investors] … because [partners] are delving

into the nature of the deficiencies, whereas investors are just looking at the number [of

deficiencies]. … Sometimes if you get multiple findings in a given area, it’s because the PCAOB

was taking that area and ripping it to shreds. While the [number of deficiencies] may look high,

it’s not as bad as it looks on the surface.” Several other partners expressed concern regarding the

degree to which investors associate the number of PCAOB deficiencies with firm quality. One

partner stated that, “I don’t believe that fewer deficiencies are necessarily indicative of higher

firm quality. … I think it’s a problem for our profession that investors over-rely on something

that might not be a great measure.” Another partner agreed, stating that “it’s an educational

process trying to help users understand what the reports actually mean. The reports try to caveat

that, but at the end of the day the investors take those numbers and look at them and have a

different view regardless of what the PCAOB might say.”

Regarding the 64.5 percent of partners who associate higher firm quality with fewer

PCAOB deficiencies, one partner stated “there’s now a direct connection between personal

inspection results and performance evaluations.” This partner stated that some partners “perceive

Part 1 as being representative of firm quality because everybody else does. They perceive that

academics, analysts, industry specialists and audit committees, for example, perceive it as

important so the partners perceive it as important as well.”

33

Estimation Uncertainty and its Impact on Audit Quality

The length and complexity of financial statement footnotes, the complexity of business

transactions and the general move toward fair-value measurements in financial statements are

just a few of the factors leading to increased financial statement uncertainty. U.S. regulators’

awareness of this trend is evidenced by a 2011 roundtable discussion initiated by the SEC

focusing on uncertainty in financial reporting (SEC 2011). This roundtable acknowledged

“uncertainty exists in financial statements where measurements to a large extent … are based on

estimates, judgments, and models rather than exact depictions” (SEC 2011). Unfortunately,

auditors are required to provide a high level of assurance that the financial statements are

materially correct, regardless of the level of estimation uncertainty (Christensen et al. 2012). This

topic is also receiving attention from researchers (e.g., Cannon and Bedard 2013; Christensen et

al. 2013a; Peecher et al. 2013; White 2013). Thus, we investigate auditors’ and investors’

perceptions of how significant estimation uncertainty affects auditors’ ability to perform their

job. Specifically, participants were asked to evaluate the extent to which the size of the

reasonable range and the number of estimates with significant estimation uncertainty affect the

auditor’s ability to achieve the desired level of assurance for those estimates and the related

financial statements.

<insert Table 8 here>

In Table 8, both audit professionals (75.0 percent) and investors (80.6 percent) indicate

that high levels of estimation uncertainty significantly affect auditors’ ability to provide the

requisite level of assurance. The mean response from both groups is significantly different from

the midpoint (p < 0.01) although not significantly different from each other (p > 0.10). In

conversations with some high-ranking audit regulators, they seem to suggest that regardless of

34

the apparent extreme uncertainty, “better” or “more” auditing will allow auditors to reduce the

reasonable range of uncertainty to within tolerable error. PCAOB inspection reports have cited

firms’ failures to appropriately address uncertainty, despite the existence of substantial

underlying uncertainty (see a discussion of such PCAOB comments in Griffith et al. 2013).

The responses in Table 8 indicate that audit professionals and investors acknowledge the

difficulty of auditing an account whose reasonable range of values exceeds audit materiality. One

partner we interviewed agreed with the findings in Table 8, stating that “these big estimates are

going to be the most difficult areas to audit because of their subjective nature; they’re the most

difficult area to obtain objective evidential matter to support the conclusions.” Another partner

responded that “there are multiple instances where [reducing the reasonable range to within audit

materiality] literally cannot be done. You can have minimal changes in the inputs that result in a

substantial difference.” Finally, one partner reacted to the findings in Table 8 by stating that

these results “prove what I’ve been telling my partners all along: we shouldn’t be held to the

same standard with estimates that we are with verifiable amounts.” Responses suggest that it is

problematic for auditors to provide high assurance associated for a reported point estimate when