secondary debt tradi ng documentation (par and …

TRANSCRIPT

For the avoidance of doubt, this guide and the documents referred to in this guide are in a non-binding, recommended form. Their intention is to be used as a starting point for negotiation only. Individual parties are free to depart from their terms and should always satisfy themselves of the regulatory implications of their use.

SECONDARY DEBT TRADING DOCUMENTATION (PAR AND DISTRESSED)

20 April 2016

USERS GUIDE

LMA Users Guide 20 April 2016

CONTENTS

Section Page

1. Important Notice ............................................................................................................ 2

2. Introduction .................................................................................................................... 6

3. Anatomy of a Trade ....................................................................................................... 9

4. Confidentiality Letter ................................................................................................... 15

5. Trade Confirmation ...................................................................................................... 19

6. Standard Terms and Conditions ................................................................................... 30

7. Assignment and Transfer Agreement .......................................................................... 76

8. Funded/Risk Participation Agreements ....................................................................... 82

9. Termination and Transfer Agreements ........................................................................ 97

10. Netting Agreements ................................................................................................... 104

11. Taxation ..................................................................................................................... 113

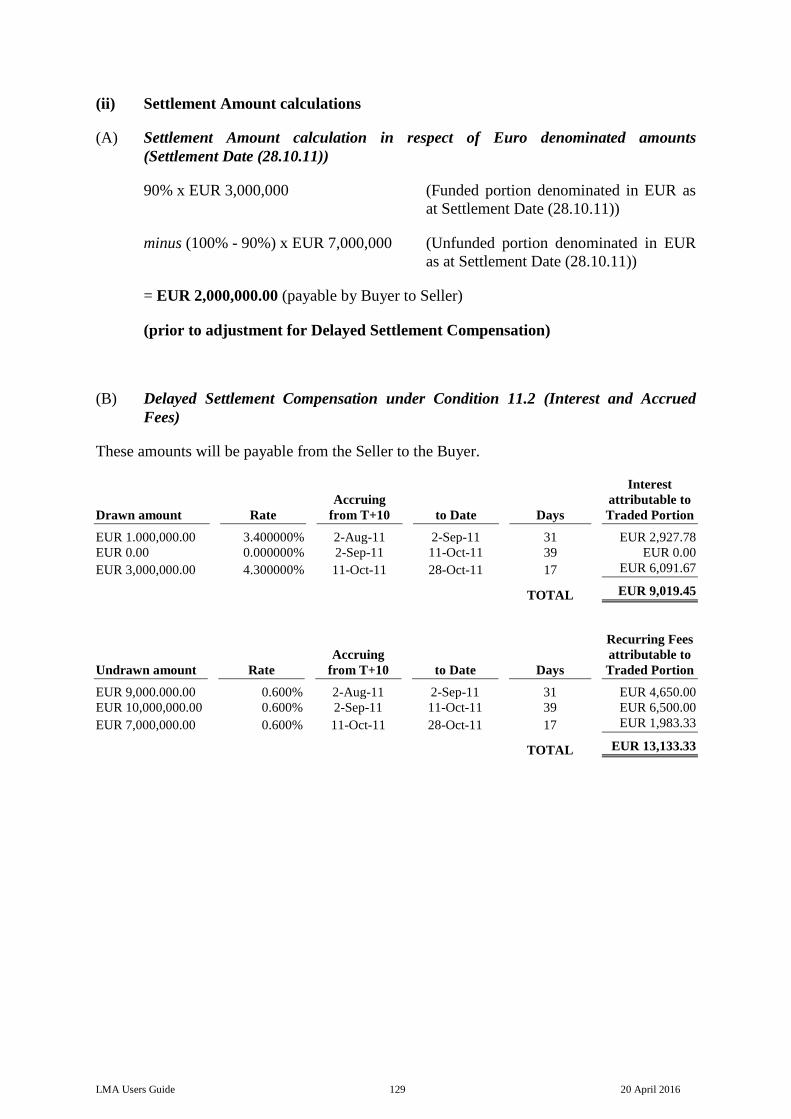

Schedule 1 Example Settlement Amount Calculations ......................................................... 122

LMA Users Guide 20 April 2016

DISCLAIMER

This Users Guide has been prepared for the Loan Market Association ("LMA"). Whilst every care has been taken in the preparation of this Users Guide, neither the LMA nor Clifford Chance LLP gives any representation or warranty as to the suitability of any of the documents in the Package for any particular transaction, or that the documents in the Package will cover every or any eventuality, or as to the accuracy or completeness of the contents of this Users Guide. Any person utilising the documents in the Package or entering into a transaction whether on the basis of the documents in the Package or otherwise must obtain and rely upon its own legal advice as to the suitability, validity and enforceability of the documents in the Package and the terms of such transaction and may not rely upon the contents of this Users Guide. Neither the LMA nor Clifford Chance LLP can be liable for any losses suffered by contracting on the terms of the documents in the Package or arising from the presence of any errors or omissions in this Users Guide.

LMA Users Guide 1 20 April 2016

1. IMPORTANT NOTICE

For the avoidance of doubt, this guide and the documents referred to in this guide are in a non-binding, recommended form. Their intention is to be used as a starting point for negotiation only. Individual parties are free to depart from their terms, and should always satisfy themselves of the regulatory implications of their use.

Users of the documentation referred to in this guide should satisfy themselves as to the taxation and accounting implications of its use.

In particular, but while stressing that these are not the only issues affecting sales of loan assets, the following should be noted:

1.1 Nature of Asset

The standard form documentation has been designed to be as flexible as possible. However, this should not be seen as implying that it is appropriate to use it in relation to all types of asset (for example, where the asset is subject to the laws of a jurisdiction other than England) and users should carry out their own diligence in each case.

1.2 Taxation

A number of taxation issues arise in the context of the buying and selling of interests in loans including, but not limited to:

• whether any amounts payable - by borrower, seller or buyer - are or become subject to a withholding liability on the payer;

• whether, in the case of a participation, there is any reason why the Grantor is not entitled to a tax deduction for its payments to the Participant; and

• whether any stamp duty and/or stamp duty reserve tax may be payable on the sale.

Users should note that Condition 29.1 (Tax) of the Standard Terms and Conditions states that the Buyer is responsible for making its own independent tax analysis of all Credit Documentation and each transaction. This is particularly relevant in the case of participations, since the standard form documentation does not provide for the gross-up of payments made by the Grantor (Seller) to the Participant (Buyer). It should also be noted that if, after a payment has been made without a withholding, HM Revenue & Customs ("HMRC") (or another jurisdiction's tax authority) determines that tax should have been withheld and retrospectively claims the amount of tax due from the Grantor, the standard form documentation does not provide for the Grantor to recover this from the Participant.

Users should therefore ensure that they take appropriate advice in relation to the circumstances of each transaction.

Certain tax issues which may be of particular interest to users and in respect of which there have been recent developments are dealt with in outline in Section 10

LMA Users Guide 2 20 April 2016

(Taxation). In addition, there are complex rules for Banks within the UK tax net which may require consideration when such a Bank holds, acquires or disposes of distressed debt (such rules relate to recognition and timing of any losses arising in respect of such debt and the tax and accounting treatment of such debt, or any assets other than debt instruments received in respect of such debt). An outline of some of the main considerations is set out in the HMRC Corporate Finance Manual at CFM 21670.

1.3 The Contracts (Rights of Third Parties) Act 1999 (the "Third Parties Act")

The Third Parties Act entitles persons who are not parties to a contract to enforce contractual terms where a contract expressly provides or the term confers a benefit on that party. The provisions of the Third Parties Act apply unless expressly excluded. An exclusion of the Third Parties Act has therefore been included in the standard form documentation except in the case of:

(a) the Standard Terms and Conditions which grant exclusions of liability to the LMA, the LMA Pricing Panel and the Determination Agent in connection with the Buy-in/Sell-out provisions; and

(b) the Confidentiality Undertakings which grant certain rights to third parties including the Borrower.

It should however be noted that the Third Parties Act supplements any rights that a third party would otherwise have under existing law.

1.4 Rome II

The governing law and jurisdiction clauses in the standard form documentation cover non-contractual obligations. This is to reflect that Regulation EC No 864/2007 ("Rome II") became effective in all EU member states (other than Denmark) from 11 January 2009. In broad summary, Rome II provides that, where it applies, parties pursuing a "commercial activity" can, in a "freely negotiated" agreement, agree the law which will govern any non-contractual dispute that may arise between them.

1.5 Financial Accounting Standards Board Statement ASC 860 Transfers and Servicing ("ASC 860")

ASC 860 is relevant to entities which report, or whose groups report, under US GAAP.

One of the implications of ASC 860 is that, in order to achieve off-balance sheet treatment for sales of loan assets, the buyer of the asset must not be subject to credit risk on the seller, even in the event of the seller's insolvency.

This is primarily a concern in the case of Participations, where the Euromarket standard is that the rights of the Participant (in this context the Buyer of the asset) are purely contractual against the Grantor of the participation (the Seller), and the Participant is exposed to credit risk on the Grantor.

LMA Users Guide 3 20 April 2016

This issue can prove to be somewhat intractable and a Grantor which is subject to US GAAP should take its own legal, tax and accounting advice if it wishes to obtain off balance sheet treatment under ASC 860 in respect of Participations.

1.6 International Accounting Standard 39 (Financial Instruments : Recognition and Measurement) ("IAS 39")1

Under IAS 39 a financial asset may be derecognised when:

(a) the contractual rights to the cash flows from the asset expire; or

(b) the transferor has transferred a financial asset and the transfer qualifies for derecognition.

The transfer of an asset for derecognition purposes occurs only if the transferor either:

(i) retains the contractual rights to receive the cash flows of the financial asset but assumes a contractual obligation to pay those cash flows to one or more recipients in an arrangement that meets the following three specified conditions:

(A) the transferor has no obligation to pay amounts to the eventual recipients unless it collects equivalent amounts from the original asset;

(B) the transferor is prohibited by the terms of the transfer contract from selling or pledging the original asset other than as security to the eventual recipients for the obligation to pay them cash flows; and

(C) the transferor has an obligation to remit any cash flows it collects on behalf of the eventual recipients without material delay. In addition the transferor is not entitled to reinvest such cash flows, except for investments in cash or cash equivalents during the short settlement period from the collection date to the date of required remittance to the eventual recipients, and interest earned on such investments is passed to the eventual recipients; or

(ii) transfers the contractual rights to receive the cash flows of a financial asset.

The standard forms of LMA Funded Participation contain provisions that reflect these requirements. However advice should be taken from auditors as to whether or not on

1 IFRS 9 Financial Instruments issued on 24 July 2014 is the IASB's replacement of IAS 39 Financial Instruments: Recognition and Measurement. IFRS 9 Financial Instruments carries over (without amendments) from IAS 39 the requirements for derecognition of financial assets and financial liabilities. The version of IFRS 9 issued in 2014 supersedes all previous versions and is mandatorily effective for periods beginning on or after 1 January 2018 with early adoption permitted (subject to local endorsement requirements).

LMA Users Guide 4 20 April 2016

any specific transaction, the participation agreement contains the requisite elements for derecognition for the purposes of IAS 39.

On the transfer of an asset, IAS 39 requires an assessment by the seller of whether it has transferred substantially all the risks and rewards of ownership of the transferred asset. If it has retained substantially all such risks and rewards it continues to recognise the transferred asset. If it has transferred all such risks and rewards it derecognises the transferred asset. If it has neither transferred nor retained substantially all the risks and rewards of ownership of the transferred asset an assessment of control is required. If it has retained control the seller continues to recognise the transferred asset to the extent of its continuing involvement in the transferred asset. If it has not retained control the seller derecognises the transferred asset.

IAS 39 provides guidance on how to apply the concepts of risks and rewards and of control.

1.7 The Dodd-Frank Wall Street Reform and Consumer Protection Act 2010 ("Dodd-Frank")

Dodd-Frank establishes, amongst other things, a comprehensive new regulatory framework for "swaps" and "security-based swaps" in the US. The stated aim of Dodd-Frank is to reduce risk, increase transparency and promote market integrity within the US financial system.

The US regulators, in the release accompanying the final definition of "swap" under Dodd-Frank, state that, a loan participation will not be considered a swap or a security-based swap if the loan participation represents "a current or future direct or indirect ownership interest in the loan or commitment that is the subject of the loan participation". The regulatory release sets out the following four characteristics that must be present to distinguish a loan participation from a swap or security-based swap:

1. the Grantor must be a lender of record or a participant or sub-participant;

2. the participation must not exceed the principal amount of the loan and/or commitment held by the Grantor;

3. the entire purchase price for the loan participation must be paid in full at the outset; and

4. the participant must acquire all of the economic benefit and risk of the loan/commitment.

It is clear from the above that funded participations documented on LMA terms would be excluded from the Dodd-Frank definition of "swap" and "security-based swap" and would not therefore fall within the new Dodd-Frank regulatory regime in the US. However, in the case of risk participations the position is unclear and therefore advice should be sought on the effect of Dodd-Frank on risk participations involving US counterparties. For an explanation of the differences between a funded participation and a risk participation, see Section 8 (Funded/Risk Participation Agreements).

LMA Users Guide 5 20 April 2016

2. INTRODUCTION

The purpose of this guide is to assist users in their use of the package of standard form documentation (the "Package") for secondary debt trading which was distributed to users in January 2010.

The Package has been designed for use for documenting both par and distressed trades and replaces the separate set of documentation designed for par trades and the separate set of documentation designed for distressed trades that were previously published by the LMA.

2.1 The Package

The Package consists of the following:

• Confidentiality Letter (Seller)

• Confidentiality Letter (Purchaser)

• Confidentiality Letter (Seller's agent/broker)

• Confidentiality Letter (Purchaser's agent/broker)

• Master Confidentiality Undertaking

• Confidentiality Letter for Administration/Settlement Services Providers

• Trade Confirmation (Bank Debt)

• Trade Confirmation (Risk Participation)

• Trade Confirmation (Claims)

• Standard Terms and Conditions

• Termination Notice

• Early Termination Amount Statement

• Buy-in/Sell-out Notice

• Purchase Price Notice

• Price Dispute Notice

• Funded Participation (par/distressed)

• Funded Participation (Distressed/Claims)

• Risk Participation (par)

• Funded/Risk Participation (par)

LMA Users Guide 6 20 April 2016

• Risk to Funded Participation (par)

• Master Funded Participation (par/distressed)

• Master Risk Participation (par)

• Multilateral Termination and Transfer Agreement (Bank Debt/Novation)

• Bilateral Termination and Transfer Agreement (Bank Debt/Novation)

• Termination Agreement

• Assignment (Bank Debt)

• Assignment (Claims)

• Transfer Agreement

• Multilateral Netting Agreement (Bank Debt/Novation)

• Bilateral Netting Agreement (Bank Debt)

In addition to the Package, the LMA has produced this Users Guide for Secondary Debt Trading Documentation (Par and Distressed). The LMA has also produced a paper discussing the credit risk taken by the participant on the grantor in funded participations, a Pricing Panel Methodology, a checklist of issues to be considered prior to/immediately after a trade, a comparison of LMA and LSTA terms for debt trading, a note on the relevance of the use of so called Proceeds Letters in conjunction with the Package and a Guide to Secondary Loan Market Transactions.

On 30 June 2010 the Multilateral Netting Agreement (Bank Debt/Novation), the Bilateral Netting Agreement (Bank Debt), the Bilateral Termination and Transfer Agreement and the Termination Agreement became available on the LMA Website. At the same time the previously published Termination and Transfer Agreement (Novation) was amended to conform to those documents and was renamed as the Multilateral Termination and Transfer Agreement (Bank Debt/Novation).

On 24 March 2011, revised versions of the LMA forms of confidentiality letter, trade confirmation, standard terms and conditions, assignment agreement and participation agreement were published by the LMA. This followed a review of those documents by the LMA Secondary Documentation Committee. The changes made to those documents were largely to address clarificatory issues that had arisen on the documents since their publication in January 2010.

On 27 June 2011, the Funded Participation (Distressed/Claims) was published on the LMA Website together with revised forms of the Trade Confirmation (Claims), the Standard Terms and Conditions and the Users Guide to take account of the publication of the new form of funded participation for claims trades.

On 3 March 2014, a revised version of the Standard Terms and Conditions was published by the LMA. This followed a project to rewrite the Standard Terms and

LMA Users Guide 7 20 April 2016

Conditions in a plainer English style. The intention of the project was to express concepts more clearly thereby improving the accessibility of the Standard Terms and Conditions particularly for newcomers to the secondary loan market and to those for whom English is not the first language. Importantly, this did not result in any changes of substance to the Standard Terms and Conditions.

On 12 November 2014 a revised version of the Confidentiality Letter for Administration/Settlement Services Providers was published by the LMA to take into account changes made to the LMA's recommended forms of facility documentation.

On 17 February 2015, the Standard Terms and Conditions were republished by the LMA. The definitions of LIBOR and EURIBOR were updated to reflect the changes to the administrators of each of these rates. Mechanics for calculating a benchmark rate for trades which settle in Australian dollars, New Zealand dollars, Canadian dollars, Danish Krone and Swedish Krona (all of which are no longer LIBOR currencies) was also included. Rates for any other currencies are to be agreed by the parties.

On 16 December 2015, a further set of amendments to the Standard Terms and Conditions were published. The main changes made included clarifying the Non-Cash Distribution provisions and adding a new Condition to allow the parties to agree at the time of trade the allocation of responsibility for payment of any notional fees payable in connectin with the transaction. Other clarificatory changes were made to Condition 15.9 (Allocation of Interest and Recurring Fees/Non-Recurring Fees) following the Tael One Case (Tael One Partners Limited (Appellant) v Morgan Stanley & Co International PLC (Respondent [2015] UK SC 12).

2.2 Users Guide

The following sections of the guide are structured so as to follow a trade from its inception to its completion. This will therefore involve dealing in some detail with the confirmation (bank debt, risk participation or claims), the associated terms and conditions (Sections 5 and 6) and the Forms of Purchase (Sections 7 and 8). Examples of Settlement Amount calculations are given in Schedule 1 (Example Settlement Amount Calculations).

It is understood that forms of Confirmation may be formatted by individual users to suit their own particular requirements, systems and procedures and that this formatting may include the addition of non-standard additional terms that a user may require to be negotiated at the time of trade, the choice of typical options and the insertion of contact details into the form of confirmation. However, it is not expected that the Standard Terms and Conditions will themselves be amended. If there are any changes to be made these should be agreed at the time of the trade and subsequently set out in the Confirmation. Users must ensure that any proposed changes made to any of the standard forms are clearly highlighted to their counterparty before the trade is entered into, otherwise they will be bound by the default positions adopted in the standard (i.e. unamended) forms. It is envisaged that individual users may wish to produce checklists of changes that they may seek to the default positions adopted in the standard forms for use within their individual institutions.

LMA Users Guide 8 20 April 2016

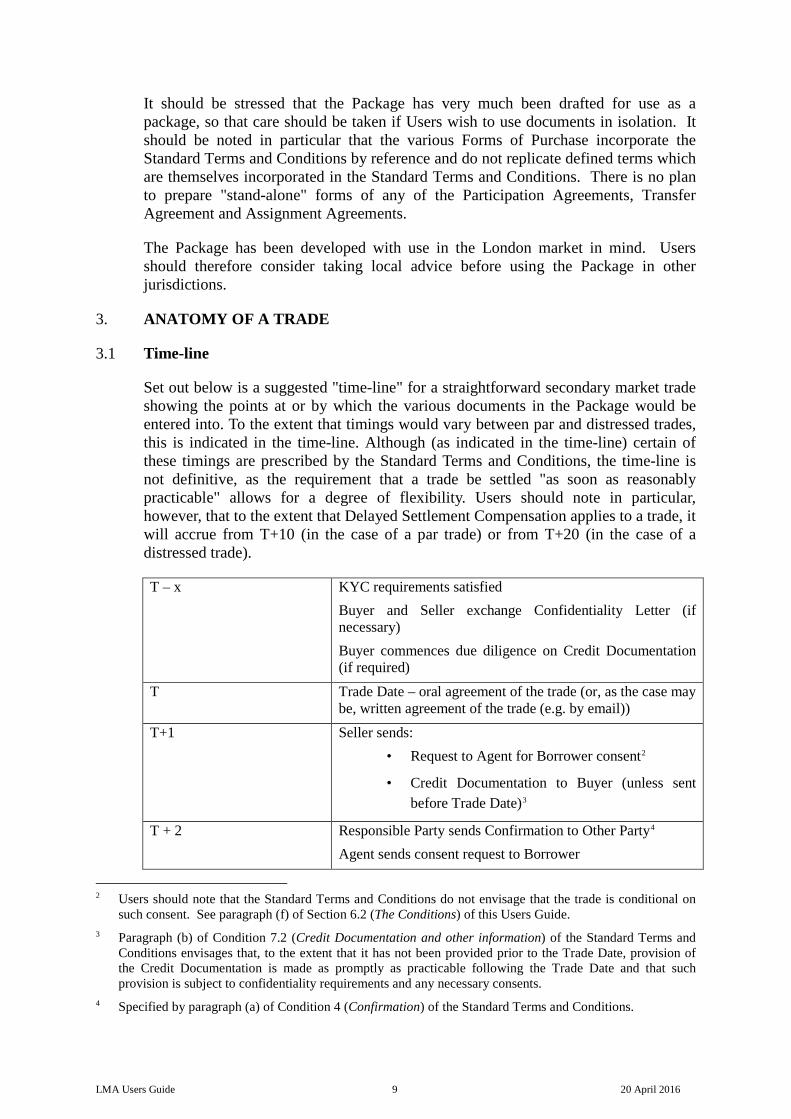

It should be stressed that the Package has very much been drafted for use as a package, so that care should be taken if Users wish to use documents in isolation. It should be noted in particular that the various Forms of Purchase incorporate the Standard Terms and Conditions by reference and do not replicate defined terms which are themselves incorporated in the Standard Terms and Conditions. There is no plan to prepare "stand-alone" forms of any of the Participation Agreements, Transfer Agreement and Assignment Agreements.

The Package has been developed with use in the London market in mind. Users should therefore consider taking local advice before using the Package in other jurisdictions.

3. ANATOMY OF A TRADE

3.1 Time-line

Set out below is a suggested "time-line" for a straightforward secondary market trade showing the points at or by which the various documents in the Package would be entered into. To the extent that timings would vary between par and distressed trades, this is indicated in the time-line. Although (as indicated in the time-line) certain of these timings are prescribed by the Standard Terms and Conditions, the time-line is not definitive, as the requirement that a trade be settled "as soon as reasonably practicable" allows for a degree of flexibility. Users should note in particular, however, that to the extent that Delayed Settlement Compensation applies to a trade, it will accrue from T+10 (in the case of a par trade) or from T+20 (in the case of a distressed trade).

T – x KYC requirements satisfied Buyer and Seller exchange Confidentiality Letter (if necessary) Buyer commences due diligence on Credit Documentation (if required)

T Trade Date – oral agreement of the trade (or, as the case may be, written agreement of the trade (e.g. by email))

T+1 Seller sends: • Request to Agent for Borrower consent2

• Credit Documentation to Buyer (unless sent before Trade Date)3

T + 2 Responsible Party sends Confirmation to Other Party4 Agent sends consent request to Borrower

2 Users should note that the Standard Terms and Conditions do not envisage that the trade is conditional on such consent. See paragraph (f) of Section 6.2 (The Conditions) of this Users Guide.

3 Paragraph (b) of Condition 7.2 (Credit Documentation and other information) of the Standard Terms and Conditions envisages that, to the extent that it has not been provided prior to the Trade Date, provision of the Credit Documentation is made as promptly as practicable following the Trade Date and that such provision is subject to confidentiality requirements and any necessary consents.

4 Specified by paragraph (a) of Condition 4 (Confirmation) of the Standard Terms and Conditions.

LMA Users Guide 9 20 April 2016

T + 4 Other Party returns Confirmation to Responsible Party5. T + 5 Responsible Party sends Transaction Documentation to

Other Party.6 T + 7 Borrower's approval of trade7 T + 7 (Par Trade) T + 15 (Distressed Trade)

Both parties sign Transaction Documentation – deliver to the Agent.8

T + as soon as reasonably practicable

Settlement Date9

T + 10 (Par Trade) T + 20 (Distressed Trade)

If applicable, delayed settlement compensation starts to accrue.10

T + 60 (Par Trade only) Buy-in/Sell-out applies if one party fails to perform its Settlement Delivery Obligations.11

N.B.

T = Trade Date

T+/-(number) = Number of Business Days after/before Trade Date.

3.2 Stages of a trade

Assuming that a trade commences, for these purposes, when either a prospective Seller decides that it has an asset which it wants to sell or, conversely, a potential Buyer decides that it wishes to buy a particular loan asset, a trade breaks down into a number of relatively well-defined stages.

(a) Identify the counterparty: Very little need be said in this document about this, obviously fundamental, part of the process. However, restrictions on the type of person to whom loans can be transferred (by novation) or assigned are often found in the underlying credit documentation and any prospective Seller should establish the position in relation to the particular loan asset in question before identifying possible counterparties. This is, of course, less of an issue

5 Specified by paragraph (a) of Condition 4 (Confirmation) of the Standard Terms and Conditions. (Users should note that the requirement is that the Other Party return the confirmation two Business Days from delivery of the Confirmation by the Responsible Party).

6 Condition 8 (Transaction Documentation) of the Standard Terms and Conditions requires the Responsible Party to endeavour to deliver the Transaction Documentation within five Business Days of the Trade Date.

7 This suggested timing assumes that either (i) the Borrower reverts with its consent within 5 Business Days of receiving the request or (ii) if the Borrower has not responded to the request, that the Credit Agreement contains (as per the LMA recommended forms of Primary Document) a clause deeming the Borrower's consent to have been given 5 Business Days after the relevant request and that the Seller relies on such deemed consent.

8 Users should note that Condition 8 (Transaction Documentation) of the Standard Terms and Conditions requires the Transaction Documentation to be signed and delivered to the Agent as soon as reasonably practicable after the Trade Date.

9 Specified by Condition 10.1 (Settlement date) of the Standard Terms and Conditions. 10 Specified by Condition 11 (Delayed settlement) of the Standard Terms and Conditions. 11 Specified by Condition 23.3 (Buy-in/Sell-out) of the Standard Terms and Conditions.

LMA Users Guide 10 20 April 2016

if the 'sale' is to be by way of participation, although occasionally credit documentation does impose restrictions on participations as well as transfers and assignments.

(b) Confidentiality: Once potential counterparties have been identified the question of confidentiality arises. This will almost invariably be an issue as regards the provision of copies of credit documentation and other information received as a lender, but can in certain instances also extend to the very fact of being a lender. In all cases the provisions of the underlying Credit Documentation should be checked. Where English law applies and the Credit Documentation is silent on the subject of disclosure, the Borrower's consent must be obtained before disclosing any information relating to the Borrower, the Group or the financing received, including copies of the Credit Documentation.

The need to obtain consent where the Credit Documentation is silent on the subject of confidentiality applies whether or not a confidentiality agreement is entered into between the prospective Seller and Buyer.

More commonly, credit documentation will permit the disclosure of information, with or without the need to enter into a confidentiality agreement. Needless to say, if the terms of the Credit Documentation require the recipient of confidential information to enter into a confidentiality agreement then this must be complied with and, if a particular form of confidentiality undertaking is specified, this should be followed. Users should note that it will only be in situations where the Credit Documentation either leaves the form of confidentiality agreement up to the lender in question or stipulates that a LMA standard form of confidentiality agreement may be used that the LMA forms of confidentiality letter described in Section 4 (Confidentiality Letter) should be employed.

As regards the position of a Participant vis à vis the passing of information to third parties, the prudent view is that, in the absence of the Borrower's agreement to the contrary, a Participant must regard any information relating to the Borrower received from the Grantor of the Participation as confidential. Grantors of Participations should ensure that the confidentiality provisions agreed with the Participant are not at odds with any duties of confidentiality owed to the underlying Borrower. The LMA forms of Confidentiality Letter require the Participant to keep confidential all information so received to the extent required by the Credit Documentation.

The Standard Terms and Conditions provide that (subject to confidentiality constraints in the Credit Documentation, by operation of law or under regulation) Buyers may disclose the terms of transactions to potential purchasers provided that they do not disclose any of the pricing arrangements or the identity of the counterparty. However Users should be careful not to breach any duty of confidentiality or other confidentiality obligations they may owe to the Borrower.

(c) Due Diligence: A prospective Buyer is expected to have carried out all necessary due diligence prior to the Trade Date. The Confirmation and

LMA Users Guide 11 20 April 2016

Standard Terms and Conditions do not permit the Buyer's legal due diligence to be a condition precedent to the closing of a trade. Due diligence by a prospective Buyer cannot, of course, start until any required confidentiality agreement has been entered into; once this has been done the Seller can provide the Buyer with the necessary information, including copies of the underlying credit documentation and financial information.

If the Confirmation provides for the credit documentation to be provided, then to the extent that it has not already done so prior to the Trade Date, the Buyer is put under a duty to sign up to a confidentiality agreement (if requested by the Seller) and the Seller is then obliged to provide, if it has not already done so prior to the Trade Date, a complete copy of the credit documentation (that the Agent has made generally available to all the Lenders) as promptly as practicable and a copy of all notices and other documents received after the Trade Date as promptly as practicable following receipt (see Condition 7 (Due Diligence) of the Standard Terms and Conditions).

(d) The Trade: Once the Seller and the Buyer are in a position to carry out a trade, this will normally be done over the phone. Whether a binding contract comes into being at that point will depend on the intention of the parties. (Recent case-law has indicated that even if the parties are silent on whether or not a binding contract has come into being then it may be held that there had.)12 If, however, the parties agree to carry out a trade on LMA terms then, unless they explicitly agree that the Trade is "subject to contract", there should be a binding contract at the time of the oral trade (see Condition 2 (Contract Point) of the Standard Terms and Conditions). Alternatively, parties could agree to the trade being subject to a satisfactory form of Confirmation. It is also recognised that trades may not always be carried out orally. If, for example, a trade is not carried out over the telephone but in writing (by e-mail for example) those written terms will constitute a binding contract pursuant to Condition 2 (Contract Point) of the Standard Terms and Conditions.

(e) The Confirmation: It is envisaged that at the time of the oral (or, as the case may be, written (e.g. by e-mail)) trade the Seller and the Buyer will agree which of them is to prepare the Confirmation. The person charged with that responsibility is referred to in the Standard Terms and Conditions as the "Responsible Party". The Confirmation is to be completed by the Responsible Party and sent to the Other Party within two Business Days of the Trade Date. The Other Party is required to either sign and return the Confirmation to the Responsible Party or to raise any disagreement with any of the terms of such Confirmation, in each case, no later than the end of the second Business Day after delivery of the Confirmation. See Condition 4 (Confirmation).

The form of Confirmation is dealt with in Section 5 (Trade Confirmation); the Standard Terms and Conditions to which trades are subject are discussed in Section 6 (Standard Terms and Conditions).

(f) Third party consents: Consents of third parties (most commonly the Borrower) may be required. If this is the case, the Seller should apply (either directly or

12 Bear Stearns Bank Plc v Forum Global Equity Ltd [2007] EWHC 1576 (Comm).

LMA Users Guide 12 20 April 2016

via the Agent, depending on the terms of the Credit Documentation) for the consent on or as soon as practicable after the Trade Date. (The LMA's suggested time-line envisages that the Seller should apply to the Agent on the first Business Day after the Trade Date with the Agent forwarding that request to the Borrower on the second Business Day after the Trade Date and Condition 6 (Mandatory Settlement Obligations) of the Standard Terms and Conditions requires the Seller to use its reasonable endeavours to obtain any required consents in connection with the transaction). The refusal of any necessary consent will not lead to the transaction being terminated without any liability on either party. Instead, the Seller and the Buyer will be required to settle the proposed transaction by a funded participation or, if the Seller and the Buyer have opted not to be required to settle the proposed transaction by funded participation (by electing "Legal Transfer only" in the Confirmation), by some mutually acceptable alternative means which provides both Seller and Buyer with the economic equivalent of the agreed-upon trade (see Condition 6 (Mandatory Settlement Obligations) of the Standard Terms and Conditions).

(g) Transaction Documentation: The parties choose who is to prepare the documentation required to complete the transaction. Condition 8 (Transaction Documentation) of the Standard Terms and Conditions stipulates that this party (the "Responsible Party") shall endeavour to send the Transaction Documentation to the other (the "Other Party") within five Business Days after the Trade Date, and that the parties should execute the documentation as soon as reasonably practicable after the Trade Date. (The LMA's suggested timeline envisages this being completed within 7 Business Days of the Trade Date on a Par Trade and within 15 Business Days of the Trade Date on a Distressed Trade.) Where a consent is still awaited, or some other condition remains to be satisfied, the execution will need to be conditional on that condition being satisfied. The timing is, however, designed to allow copies of the Transaction Documentation to be provided to the agent bank, if required, giving sufficient time for the trade to complete on a basis of ten Business Days from the Trade Date (in the case of a Par Trade) or twenty Business Days from the Trade Date (in the case of a Distressed Trade). Some credits may impose their own timing requirements for delivery of transfer documentation. The parties should check the Credit Documentation for such requirements and in such scenarios the parties should ensure that the Transaction Documentation is executed and delivered to the Agent Bank taking account of the time frame provided by the Credit Documentation. It is contemplated that, in addition to the forms of Transaction Documentation, there will also be a pricing letter produced in relation to each trade.

The different forms of Transaction Documentation (or Forms of Purchase) required to implement the trade are discussed in Section 7 (Assignment and Transfer Agreement) and Section 8 (Funded/Risk Participation Agreements).

(h) Settlement Date: On the Settlement Date the trade is legally completed. The asset is transferred to the Buyer and, unless the trade is settling by way of risk participation, the Settlement Amount is required to be paid. Depending on the circumstances and the nature of the asset, the Settlement Amount may be required to be paid by the Buyer to the Seller or by the Seller to the Buyer or,

LMA Users Guide 13 20 April 2016

in some cases, two way payments may be required. The Settlement Amount is adjusted to take account of any Delayed Settlement Compensation.

(i) Post-Settlement Date: Any notices which need to be given (e.g. to the Borrower where the transaction is completed by a notified assignment) or other matters which need to be carried out (e.g. registration of the Buyer as a secured party in certain jurisdictions) should be done as soon as possible after the Settlement Date.

LMA Users Guide 14 20 April 2016

4. CONFIDENTIALITY LETTER

4.1 Confidentiality Generally

Users should read paragraph (b) of Section 3.2 (Stages of a trade) which sets out some of the wider issues related to confidentiality in this context.

4.2 Standard Form Confidentiality Letters

Six forms of confidentiality letter are available. The first is designed to be sent by the Seller to the Purchaser, with the Purchaser returning a signed copy to the Seller. The second is designed to be sent by the Purchaser to the Seller, with the Seller returning a signed copy to the Purchaser. The latter mirrors the terms of the former. In addition, there are two forms designed to be sent by the agent or broker of either the Seller or the Purchaser and which may be addressed to the Seller or Purchaser, as the case may be, or their agent or broker. There is also a master confidentiality undertaking and a confidentiality undertaking for administration/settlement services providers where either the Purchaser or Seller is using an administration and/or settlement service in relation to a transaction and therefore needs to disclose confidential information to it. Some points to note on the Seller and Purchaser forms of confidentiality letter are:

(a) Brief details of the underlying credit agreement should be inserted on the front page of the letter.

(b) The prospective purchaser is permitted to use any information provided only for the purpose of considering and evaluating whether to enter into a trade (or, where the addressee is acting as broker or agent, for the purpose of passing it on to the real purchaser). Once the trade is completed, the permitted purpose restriction ceases to apply because the purchaser may need to use the information it receives for other purposes such as internal audit or regulatory purposes.

(c) The obligations imposed on the prospective purchaser fall away if the trade results in the prospective purchaser becoming a party to the Agreement as a lender of record (the rationale being that the confidentiality provisions of the underlying credit documentation will then apply). In the case of trades that do not result in the prospective purchaser becoming a party to the Agreement as a lender of record (such as a participation), the obligations imposed on the prospective purchaser continue until 12 months after the date on which all of the purchaser's rights and obligations contained in the documentation entered into to implement the trade have terminated (the rationale being that the underlying sale agreement is unlikely to contain confidentiality obligations that directly benefit the Borrower). There is a longstop date of twelve months from the date of final receipt by the prospective purchaser (in whatever manner) of any confidential information in any other case, meaning cases where the trade is not completed (paragraph 5).

(d) If the prospective purchaser does not complete the transaction, the Seller can request that the confidential information be returned or destroyed and that any copies of it be destroyed (save to the extent that the recipient is required to retain any of the information) (paragraph 4).

LMA Users Guide 15 20 April 2016

(e) The recipient of the confidential information is permitted to disclose it to assignees, transferees, sub-participants or those with whom they enter into any other transaction under which payments are or may be made by reference to the Credit Agreement or any Obligor if a confidentiality letter (again in the LMA standard form) is received from that third party. Any disclosure of information within the potential purchaser's organisation, or to its advisers, is only permitted if the recipient is informed in writing of its confidential nature and that some or all of it may be price-sensitive, although no such notification is required where the recipient is either subject to professional obligations to maintain the confidentiality of the information or is otherwise bound by confidentiality requirements. It should also be noted that disclosure to a third party (whether to the potential purchaser where the recipient of the information is the potential purchaser's broker or agent or to a potential assignee, transferee or participant of the potential purchaser) is subject to the requirements of the Credit Documentation which may prohibit such disclosure. In addition, the recipient of the confidential information is permitted to disclose it to the same persons and on the same terms as apply to a lender under the Credit Agreement as if those terms were set out in the letter. This ensures maximum flexibility by allowing disclosure on the equivalent terms to those in the applicable Credit Agreement. In all cases, the terms of the Credit Documentation should always be checked at or prior to any disclosure of confidential information. The confidential information can also be disclosed where required by law or regulation or by the rules of any relevant stock exchange. (paragraph 2).

(f) The signed confidentiality letter and the acknowledgement can be exchanged in counterpart; a hard copy original need only be sent if requested by the other party (see Condition 34 (Counterparts) of the Standard Terms and Conditions).

4.3 The Master Confidentiality Undertaking

The master confidentiality undertaking mirrors the standard form confidentiality letter except that it has been drafted to allow two institutions to sign one master confidentiality undertaking. The master confidentiality undertaking then governs all confidentiality issues which relate to trades carried out between those two institutions (in their respective capacities as both Seller and Purchaser) so long as the underlying loan asset is documented under the LMA Primary Documents. If the underlying Credit Agreement is not in the form of the LMA Primary Document, the terms of the document will need to be reviewed before a master confidentiality undertaking is relied upon. The purpose of the master confidentiality undertaking is to obviate the need for separate confidentiality letters each time two institutions trade. It is however important to note that whilst the master confidentiality undertaking may reduce the amount of paperwork to be signed on any particular trade, it does not obviate the need for the parties to review the disclosure and confidentiality provisions of the underlying Credit Documentation (even if it appears to be in the form of the LMA Primary Document). This is to ensure that, if a form of confidentiality undertaking is required, the use of the master confidentiality undertaking will comply with the terms of the Credit Documentation.

LMA Users Guide 16 20 April 2016

It is also worthy of note that, unlike the LMA forms of Confidentiality Letter, the master confidentiality undertaking does not provide for brokers and agents. It assumes that the signatories will always be acting as principals.

4.4 Which Form to Use?

Users are again reminded that the LMA Standard Forms of Confidentiality Letter will not be appropriate in all circumstances, in particular where another form of confidentiality undertaking is stipulated in the Credit Documentation. In all cases the provisions of the Credit Documentation prevail.

4.5 Master Confidentiality Letter for Administration/Settlement Services Providers

The master confidentiality undertaking for use with administration/settlement services providers mirrors, to the extent relevant, the standard form confidentiality letter.

It is intended to be used by those who have an interest in a credit agreement or any facility thereunder or who wish to acquire some form of interest in a credit agreement or any facility thereunder and wish to appoint a settlement and/or administration services provider in respect of a transaction in relation to such credit agreement or facility thereunder. This would, for example, apply in the case of the seller or the purchaser of a loan who appoints a web based loan settlement services provider or an agent who appoints an administration services provider to take over some of the agent's functions such as in relation to transfer certificates or in relation to primary syndication. The master confidentiality undertaking for use with administration/settlement services providers has been drafted as a master agreement to allow the service provider and the client to sign only one confidentiality undertaking which then governs all transactions for which the service provider provides its services.

The forms of LMA Facility Agreement permit disclosure of confidential information to administration/settlement services providers. In addition, the LMA has published a rider which can be used to amend a credit agreement to include such a permission.

The master confidentiality undertaking for use with administration/settlement services providers applies similar confidentiality restrictions to lenders' funding rates and reference bank quotations. This is because the forms of LMA Facility Agreement restrict the agent's disclosure of these rates. (They permit disclosure to administration and settlement services providers subject to them entering into the master confidentiality agreement for use with administration/settlement services providers.)

Some points to note on the master confidentiality undertaking for use with administration/settlement services providers are as follows:

(a) the Service Provider may only use the information to carry out its administration and/or settlement services and not for any other purpose and, in the case of lenders' funding rates and reference bank quotations, only to the extent that the agent itself is permitted to use the information;

LMA Users Guide 17 20 April 2016

(b) the Client can request the return or destruction of all confidential information and require that all copies are destroyed (save to the extent that the recipient is required to retain any of the information); and

(c) the confidentiality obligations imposed on the Service Provider last for so long as the information remains confidential or, in the case of lenders' funding rates and reference bank quotations, indefinitely.

4.6 Who gets the Benefit?

Due to the potentially large numbers of Confidentiality Letters/Undertakings which are likely to be entered into in relation to any particular Credit Agreement, and the consequential administrative burden and likely delay which would arise if Borrowers were required to sign each letter, Borrowers are not parties to these letters/undertakings. Under the current state of the law of confidentiality, which is continuing to develop, a Borrower may be able to obtain an injunction prohibiting any unauthorised disclosure of confidential information and paragraphs 6(b) and 9 of the standard forms (which provide that damages may not be an adequate remedy for breach of the agreement and that Borrowers are intended to take the benefit of the undertakings given by the prospective Buyer or Seller as the case may be) are designed to assist Borrowers in this regard. The Third Parties Act assists Borrowers in this regard. Paragraph 10 of the Confidentiality Letters and Master Confidentiality Undertaking and paragraph 9 of the Confidentiality Letter for Administration/Settlement Services Providers grants Borrowers and each member of the Group rights to enforce the undertakings given in such Confidentiality Letters and as such they will be entitled to the same rights to obtain damages for breach of undertaking, an injunction prohibiting any unauthorised disclosure of confidential information or an order for specific performance of the undertakings as they would have had if they had been a party to such Confidentiality Letter. Paragraph 9 of the master confidentiality undertaking for use with administration/settlement services providers grants similar rights to the providers of lenders' funding rates and reference bank quotations.

LMA Users Guide 18 20 April 2016

5. TRADE CONFIRMATION

5.1 Introduction

The Confirmation is designed to record the terms of the actual trade which takes place on oral (or, as the case may be, written (e.g. by email)) agreement as to its terms. It is therefore expected that users will agree, at the time of such trade, all of those matters which are required to be decided in order to complete the Confirmation. Having the form of Confirmation (together with any checklist of items to be considered and, if necessary agreed with the other party during the course of the trade) to hand (or on screen) and filling in the form of Confirmation during the course of such trade would therefore appear to be the safest option. The Confirmation is intended solely to evidence the terms that were agreed at the time of the trade and is not intended to be subject to negotiation in its own right.

This section should be read in conjunction with Section 6 (Standard Terms and Conditions), which explains the Standard Terms and Conditions to which the trade is subject.

5.2 Choosing which Confirmation to use

The Package includes three types of Confirmation: Bank Debt, Risk Participation and Claims. Users are recommended to use the Bank Debt Confirmation for all trades unless either the asset is being traded by way of risk participation (in which case the Risk Participation Confirmation should be used) or unless the asset being traded represents an unsecured claim of the Seller against a debtor which has entered into a formal insolvency proceeding (e.g. administration or liquidation (sometimes referred to as winding-up)), where it may be more appropriate to use the Claims Confirmation. In this latter scenario, users are recommended to take legal advice as to which form of Confirmation is most appropriate in the specific circumstances, particularly where the relevant claim has not been admitted in the relevant insolvency proceedings at the time of trade. The Bank Debt, Risk Participation and Claims Confirmations contain many of the same provisions and are governed by the same Standard Terms and Conditions.

5.3 Completing the Confirmation

As noted above, the Confirmation is intended to evidence the terms of the actual trade and in most circumstances the standard form of Confirmation should include all the issues which need to be addressed in relation to a trade. However, this will not always be the case (particularly where the parties agree, at the time of the trade, to incorporate additional terms or to disapply or alter any of the Standard Terms and Conditions), and, to the extent that terms agreed at the time of the trade are not addressed in the standard form of Confirmation, additional terms can be included in the "Other Terms of Trade" paragraph in each of the three forms of Confirmation. It is understood that users may produce their own formatted Confirmation, which would include their own preferred standard options and any additional terms and conditions which they would seek to agree with their counterparty at the time of trade (as explained, the Standard Terms and Conditions should not be amended on their face, but only in the Confirmation).

LMA Users Guide 19 20 April 2016

5.4 Confirmation (Bank Debt)

Looking at the Confirmation paragraph by paragraph.

(a) Introductory paragraph: This provides that the transaction is subject to the standard LMA Terms and Conditions as in effect on the Trade Date, and that these are incorporated by reference. Although there is no need to attach the Standard Terms and Conditions to the form of Confirmation, users should send copies to counterparties who have not seen them.

(b) Type of Transaction (paragraph 1): The parties are required to agree at the time of trade whether the transaction is a Par Trade or a Distressed Trade, and that agreement should be specified here. Although in the main a transaction will be subject to the same terms under the Standard Terms and Conditions whether it is a Par Trade or a Distressed Trade, there are areas in which the terms applying to it will differ depending on whether it is a Par Trade or a Distressed Trade. The key terms which apply uniquely to each type of transaction are set out below:

(i) Par Trade

(A) Delayed Settlement Compensation will apply to the trade and will accrue from ten Business Days after the Trade Date unless expressly excluded.

(B) To the extent that the parties so agree, breakfunding compensation may apply to the trade. (Users should note that in the absence of such express agreement the default position adopted in the Standard Terms and Conditions is that breakfunding compensation will not apply to the trade.)

(C) The Seller will give a representation to the effect that no decision has been taken by the Lenders to accelerate or enforce under the Credit Documentation and that no principal or interest is due and unpaid under the Credit Documentation.

(D) The Buy-in / Sell-out provisions (see paragraph (v) of Section 6.2 (The Conditions)) will apply to the trade unless expressly excluded.

(E) To the extent that the trade settles by way of funded participation the Buyer will receive only very limited voting rights under the funded participation. See Section 8.3 (Funded Participation).

(ii) Distressed Trade

(A) Delayed Settlement Compensation will apply to the trade and will accrue from twenty Business Days after the Trade Date unless expressly excluded.

(B) The Seller will give additional representations covering:

LMA Users Guide 20 20 April 2016

(1) Provision of Credit Documentation;

(2) That it is not "connected" with any Obligor for the purposes of the Insolvency Act 1986;

(3) Absence of conduct resulting in the Buyer being treated less favourably and availability of set-off;

(4) No notice of claim impairment or invalidity in respect of Collateral or Credit Documentation;

(5) No obligation to extend credit other than Purchased Obligations and no other liabilities or obligations; and

(6) No Governmental Authority proceedings.

(C) To the extent that the trade settles by way of funded participation, the parties can opt whether or not to give voting rights under the funded participation to the Buyer. (See Section 8.3 (Funded Participation)).

Additionally, various of the timings set out in the recommended time-line (see Section 3.1 (Time-line)) vary depending on whether the transaction is a Par Trade or a Distressed Trade.

(c) Credit Agreement Details (paragraph 2): Sufficient detail should be included to identify the particular Credit Agreement uniquely; care should be taken where a Borrower has outstanding more than one Credit Agreement. If the Credit Agreement has been allocated an ISIN number, this should be used in the Confirmation to identify that Credit Agreement.

(d) Trade Date (paragraph 3): This will usually be the date of the oral (or, as the case may be, written (e.g. by e-mail)) trade. Its relevance is that:

(i) timings for various matters to do with a trade (e.g. preparation and despatch of the Transaction Documentation) run from this date;

(ii) this is the date upon which the Buyer goes "on risk" in relation to the asset being traded;

(iii) where the asset is being "traded flat", this is the date from which the Buyer will be entitled to all accrued and unpaid interest.

(e) Settlement Date (paragraph 4): The Confirmation and the Standard Terms and Conditions prescribe that the Settlement Date will be "as soon as reasonably practicable". Users should note, however, that, unless the Agreed Terms specify otherwise, Delayed Settlement Compensation will apply to the transaction and will begin to accrue 10 Business Days from the Trade Date (in the case of a Par Trade) or 20 Business Days from the Trade Date (in the case of a Distressed Trade).

LMA Users Guide 21 20 April 2016

(f) Seller (paragraph 5): The Seller's name should be inserted. Where the person contracting to sell the asset is acting as an agent, this should be disclosed.

(g) Buyer (paragraph 6): The Buyer's name should be inserted and, as for the description of the Seller, where the person contracting to buy the asset is acting as agent, this should be disclosed.

(h) Details of Traded Portion (paragraph 7):

(i) name of Tranche/Facility: this should be the description given to the individual tranche or facility within the Credit Agreement, (for example, "Junior Term Facility", "Resettable Facility", "Working Capital Facility"). If the trade involves more than one tranche or facility within the Credit Agreement they should all be specified. If the facility has been allocated an ISIN number, this should be included as a means of identifying the relevant facility;

(ii) nature: this should be completed as "Revolving", "Term", "Acceptances", "Guarantee", "Letter of Credit" or other description as appropriate;

(iii) Traded Portion of Commitment: the amount, in the base currency of the relevant tranche or facility, to be traded should be given.

(i) Pricing (paragraph 8):

(i) Name of Tranche/Facility: this should follow the description given in paragraph 7.

(ii) Purchase Rate: this is a percentage of the nominal principal amount of the relevant credit;

(iii) Upfront Fee: if any upfront fee applies to the transaction this should be stated (preferably as an absolute amount). Provision is made for the parties to specify the amount of the fee, whether it is to be payable on the Settlement Date or some alternative date and whether it is to be payable by the Buyer or the Seller;

(j) Accrued Interest (other than PIK Interest) (paragraph 9): This links into Condition 15 (Interest Payments and Fees) of the Standard Terms and Conditions.

(i) If "Settled Without Accrued Interest" is chosen, then, unless the terms of the Credit Agreement provide for the Agent to distribute interest on a pro rata basis between the Seller and the Buyer, the Buyer will, upon receipt of any Interest or Recurring Fees (other than PIK Interest) accrued to the Settlement Date, pay an amount equal to the amount of such Interest or Recurring Fees to the Seller. If the Buyer makes any payment of such amounts to the Seller but such amount received is clawed back by the Agent the Buyer is entitled to reclaim such amounts from the Seller.

LMA Users Guide 22 20 April 2016

However, the interest treatment will automatically be altered to a "Trades Flat" basis such that these amounts will instead be for the account of the Buyer if they are paid by the relevant Obligor after:

(A) a payment default in respect of those amounts; or

(B) any payment default generally under the Credit Documentation (regardless of any remedy or waiver).

Where an asset is non-performing as regards payment obligations, the Buyer is thereby relieved from having to account to the Seller for its portion of Interest and Recurring Fees for the Seller's period of ownership if and when paid.

(ii) "If Paid on Settlement Date" is chosen, then unless the terms of the Credit Agreement provide for the Agent to distribute interest on a pro rata basis between the Seller and the Buyer, the Buyer pays the Seller on the Settlement Date an amount equal to Interest or Recurring Fees (other than PIK Interest) accrued to the Settlement Date. It should be noted that the Buyer has no recourse to the Seller if the Buyer does not receive the Interest or Recurring Fees from the Borrower in due course. This option is similar to that applying in the bond markets.

(iii) If "Paid on Settlement Date and Discounted from next payment date" is chosen, then the same treatment as described in paragraph (ii) above applies but Interest or Recurring Fees accrued up to the Settlement Date which are not payable under the Credit Documentation until the next payment date are discounted from that payment date back to the Settlement Date.

(iv) If "Trades Flat" is chosen then all accrued and unpaid Interest, Recurring Fees or other fees paid by any Obligor on or after the Trade Date will be for the account of the Buyer for no additional consideration.

(k) Form of Purchase (paragraph 10):

(i) Legal Transfer: This should be selected if the Seller and Buyer have agreed that the trade will settle by way of Legal Transfer. It envisages that the parties will settle the transaction by using the relevant Credit Agreement's prescribed form of transfer (e.g. a transfer certificate or assignment agreement) but that if the Credit Agreement does not provide a form of transfer that the parties will transfer the asset by using either the LMA's standard form of Transfer Agreement or the LMA's standard form of Assignment Agreement. If Legal Transfer is selected and as at the proposed Settlement Date for the relevant trade, a required third party consent (or any transaction specific condition) remains outstanding the parties agree that the trade will be settled by funded participation and if settlement cannot be effected by funded participation or the parties are unable to agree the form of funded participation, it will settle by some mutually acceptable alternative

LMA Users Guide 23 20 April 2016

means which provides the Seller and the Buyer with the economic equivalent of the agreed-upon trade. See paragraph (f) of Section 6.2 (The Conditions).

(ii) Legal Transfer only: This should be selected in addition to selecting "Legal Transfer" if the Seller and Buyer have agreed that the trade will be settled by way of Legal Transfer as for paragraph (i) above but have agreed that they do not wish to settle the transaction by a funded participation if, as at the proposed Settlement Date for the relevant trade, a required third party consent (or any transaction specific condition) remains outstanding. If "Legal Transfer" and "Legal Transfer only" are selected and such a consent or condition is outstanding as at the proposed Settlement Date, the parties will be required to settle the transaction by some mutually acceptable alternative means which provides the Seller and the Buyer with the economic equivalent of the agreed-upon trade. See paragraph (f) of Section 6.2 (The Conditions).

(iii) Funded Participation: This should be selected if the asset is to be traded by way of funded participation and envisages that the parties will settle the transaction by using the LMA standard form of funded participation. If this form of purchase is selected and as at the proposed Settlement Date for the relevant trade a required third party consent (or any transaction specific condition) remains outstanding, the parties agree that the trade will be settled by some mutually acceptable alternative means which provides the Seller and the Buyer with the economic equivalent of the agreed-upon trade. See paragraph (f) of Section 6.2 (The Conditions).

In the case of a transaction settling by Funded Participation (including when the parties agree that "Legal Transfer" applies such that the trade will settle by funded participation if a legal transfer cannot be effected because a required third party consent (or any transaction specific condition) cannot be obtained), the Confirmation requires the parties to provide whether the form of Funded Participation will specify collateral for undrawn commitment or grant information rights. If the transaction is a Distressed Trade and is settling by Funded Participation the parties are also required to provide whether the form of Funded Participation will grant voting rights under the participation to the Participant from the Settlement Date.

(l) Transaction Documentation (paragraph 11): The options are for this to be prepared by the Seller or the Buyer. In either event, the responsible party must endeavour to prepare and deliver the transaction documentation to the other party within five business days after the Trade Date (see Condition 8 (Transaction Documentation) of the Standard Terms and Conditions).

(m) Credit Documentation to be provided by Seller (paragraph 12): Two alternatives (yes or no) are given. See paragraph (c) of Section 3.2 (Stages of a trade). If the Seller is to provide the Buyer with the Credit Documentation and the transaction is a Distressed Trade, the Seller will give a representation

LMA Users Guide 24 20 April 2016

to the Buyer as to the completeness of the Credit Documentation provided. (See paragraph (u)(ii)(F)(1) of Section 6.2 (The Conditions)).

(n) Process Agents (paragraph 14): A process agent will not be required for a party which is incorporated in the UK. Where there is a non-UK party to the transaction, whether a process agent will be required will depend on the circumstances, but where service on that party within the UK is not possible the potential implications of not appointing a process agent for that party are that permission may need to be obtained from the English Courts to serve process on that party outside the UK and that any service of process made outside the UK may, in practical terms, involve significant delay. Accordingly, best practice would suggest that, in all cases where a counterparty is not UK-incorporated, an English incorporated company (either an associate of the foreign company or some third party company) should be appointed as process agent, or some other means found to allow service to be effected in the UK.

(o) Other Terms of Trade (paragraph 15): If, at the time of the trade, additional terms are agreed or the parties wish to disapply or alter any of the Standard Terms and Conditions, those additional terms or disapplications / alterations should be specified here. Areas included as explicit options are as follows:

(i) Transaction to incorporate additional representations: The Standard Terms and Conditions include a number of representations (see paragraph (u) of Section 6.2 (The Conditions)). If, however, the parties agree at the time of trade that the transaction is to incorporate additional representations, this box should be ticked and those other representations should be annexed to the Confirmation.

(ii) Buy-in/sell-out damages do not apply: If the transaction is a Par Trade the Buy-in / Sell-out provisions (see paragraph (v)(vii) of Section 6.2 (The Conditions)) will apply unless it is agreed at the time of trade that they are to be excluded. If it is agreed that the Buy-in / Sell-out provisions will not apply to a transaction, this box should be ticked.

(iii) Breakfunding compensation: Breakfunding compensation will not apply to a transaction unless it is agreed at the time of trade that it will apply. If it is agreed that breakfunding compensation will apply this box should be ticked and the basis on which such compensation is to be calculated should be specified. Users should note that this option, and the Standard Terms and Conditions, assume that the possibility of agreeing breakfunding compensation as a trade specific term would be relevant only if the transaction is a Par Trade.

(iv) Delayed Settlement Compensation: Delayed Settlement Compensation will apply to a transaction unless it is agreed at the time of trade that it will not apply. The provisions relating to Delayed Settlement Compensation in the Standard Terms and Conditions will apply to the transaction and will begin to accrue 10 Business Days from the Trade Date (in the case of a Par Trade) or 20 Business Days from the Trade Date (in the case of a Distressed Trade). The methodology of the calculation is the same whether the trade is a Par Trade or a Distressed

LMA Users Guide 25 20 April 2016

Trade (see paragraph (j) of Section 6.2 (The Conditions)). If, however, the parties agree at the time of trade that Delayed Settlement Compensation will not apply to the transaction, this box should be ticked and the exclusion expressly noted on the Confirmation.

(v) Transfer Fee: The Standard Terms and Conditions (see Condition 18.1 (Transfer fees)) provide that the Buyer and the Seller each have to pay in equal shares any recordation, processing, transfer or similar fee payable to the Agent under the Credit Documentation in connection with a transaction. If, however, the parties agree at the time of trade that either the Buyer or the Seller will pay the whole of that fee or that payment of transfer fees should be allocated other than on an equal basis, the parties should tick this box and specify which party will be making the payment or, as the case may be, what the allocation between the Seller and the Buyer should be.

(vi) Relevant Benchmark Rate: The Standard Terms and Conditions provide various benchmark rates for the purposes of calculating the Relevant Rate in respect of the cost of carry element of Delayed Settlement Compensation (see paragraph (k) of Section 6.2 (The Conditions)) and the sell-out element of the buy-in/sell-out provisions (see paragraph (w)(vii) of Section 6.2 (The Conditions)). If any sum is denominated in a currency which does not have a Relevant Benchmark Rate, the parties are required to agree the applicable rate at the time of trade. In such a case, this box should be ticked and the applicable rate specified. If the parties do not agree such a rate at the time of trade, the rate for that currency will be as specified by the Seller (acting reasonably).

(vii) Other: The parties are free to include other terms of the transaction. These may include, for example the allocation of interest or fees where the Credit Agreement contains an unusual pricing structure or granting the Participant additional control over the Grantor's voting rights under the Credit Documentation. The details of any such terms should be recorded.

(p) Mechanics: The Confirmation is to be sent (by fax, email or other electronic means agreed between the parties) by the Responsible Party to the Other Party no later than the second Business Day following the Trade Date. The Other Party is obliged to either raise any disagreement with the terms of the Confirmation or return the Confirmation countersigned, no later than the second Business Day following delivery of the Confirmation (where there is any disagreement, best practice is for this to be raised with the Responsible Party as soon as possible by phone). In addition, contact details should be inserted at the foot of the Confirmation. MEI or other identification numbers for the Seller and/or the Buyer should also be included in the contact details.

5.5 Confirmation (Risk Participation)

The structure and content of this Confirmation is very similar to the Bank Debt Confirmation. Where the provisions are the same, no further comment is made.

LMA Users Guide 26 20 April 2016

(a) The Standard Terms and Conditions assume that any transaction evidenced by the Risk Participation Confirmation will be a Par Trade, accordingly, there is no tick-box provided for the parties to evidence whether the transaction was agreed to be a Par Trade or a Distressed Trade.

(b) Details of Traded Portion (paragraph 6):

(i) Final Maturity: The final maturity date for each individual tranche or facility should be given;

(ii) On risk until: This should state the period for which the Buyer will be on risk under the Risk Participation.

(c) Accrued Interest (other than PIK Interest) (paragraph 8): This does not envisage "Trades Flat" as an option.

(d) No tick-box is provided for Transfer Costs as it is assumed that Transfer Costs will not be relevant for a transaction settling by way of risk participation.

(e) Form of Purchase (paragraph 9): The Risk Participation Confirmation should be used for a transaction which is to settle by way of:

(i) Funded / Risk Participation;

(ii) Risk Participation; or

(iii) Risk to Funded Participation.

The parties are required to specify whether the form of participation will specify collateral for undrawn commitment only if the transaction settles by way of Funded / Risk Participation or Risk to Funded Participation because collateral for undrawn commitment is relevant only to the funded aspect of those participations.

(f) Other Terms of Trade (paragraph 13):

(i) Breakfunding compensation: No provision is made to specify breakfunding compensation as this is unlikely to be relevant in the case of a transaction settling by way of risk participation.

(ii) Delayed Settlement Compensation: Unless otherwise agreed by the parties at the time of trade, Delayed Settlement Compensation will apply to a transaction and will begin to accrue 10 Business Days from the Trade Date. If, however, the parties agree at the time of trade that Delayed Settlement Compensation will not apply to the transaction, the parties should tick this box and expressly note the exclusion in the Confirmation.

(iii) Relevant Benchmark Rate: The Standard Terms and Conditions provide various benchmark rates for the purposes of calculating the Relevant Rate in respect of the cost of carry element of Delayed Settlement Compensation (see paragraph (k) of Section 6.2 (The

LMA Users Guide 27 20 April 2016

Conditions)) and the sell-out element of the buy-in/sell-out provision, (see paragraph (w)(vii) of Section 6.2 (The Conditions)). If any sum is denominated in a currency which does not have a Relevant Benchmark Rate, the parties are required to agree the applicable rate at the time of trade. In such a case, this box should be ticked and the applicable rate specified. If the parties do not agree such a rate at the time of trade, the rate for that currency will be as specified by the Seller (acting reasonably).

(iv) Other: The parties are free to include other terms of the transaction. These may include, for example the allocation of interest or fees where the Credit Agreement contains an unusual pricing structure or granting the Participant additional control over the Grantor's voting rights under the Credit Documentation. The details of any such terms should be recorded.

5.6 Confirmation (Claims)

The structure and content of this Confirmation is very similar to the Bank Debt Confirmation. Where the provisions are the same, no further comment is made.

(a) The Standard Terms and Conditions assume that any transaction evidenced by the Claims Confirmation will be a Distressed Trade, accordingly, there is no tick-box provided for the parties to evidence whether the transaction was agreed to be a Par Trade or a Distressed Trade.

(b) Details of Traded Portion (paragraph 6): The traded portion of the Claim Amount is required to be specified.

(c) Pricing (paragraph 7): This is a percentage of the nominal principal amount of the claim.

(d) The Standard Terms and Conditions assume that claims will be traded on a "Trades Flat" basis, accordingly, no tick-box relating to interest treatment is provided in the Confirmation.

(e) Form of Purchase (paragraph 9): The Claims Confirmation envisages that the purchase is completed by way of an assignment or a participation.

(f) Other Terms of Trade (paragraph 12):

(i) Buy-in/sell-out and breakfunding compensation: As the Standard Terms and Conditions assume that any transaction evidenced by the Claims Confirmation is a Distressed Trade, the Claims Confirmation does not provide explicit options to evidence the exclusion of the Buy-in / Sell-out provisions from, or the inclusion of breakfunding compensation to, the transaction.

(ii) Delayed Settlement Compensation: Unless otherwise agreed by the parties at the time of trade, Delayed Settlement Compensation will apply to a transaction and will begin to accrue 20 Business Days from the Trade Date. If, however, the parties agree at the time of trade that

LMA Users Guide 28 20 April 2016

Delayed Settlement Compensation will not apply to the transaction, the parties should tick this box and expressly note the exclusion in the Confirmation.

(iii) Transfer costs: The Standard Terms and Conditions (see Condition 18 (Transfer Costs)) provide that the Buyer and the Seller each have to pay in equal shares any recordation, processing, transfer or similar fee payable to the Agent under the Credit Documentation in connection with a transaction. If, however, the parties agree at the time of trade that either the Buyer or the Seller will pay the whole of that fee or that payment of transfer fees should be allocated other than on an equal basis, the parties should tick this box and specify which party will be making the payment or, as the case may be, what the allocation between the Seller and the Buyer should be.

(iv) Relevant Benchmark Rate: The Standard Terms and Conditions provide various benchmark rates for the purposes of calculating the Relevant Rate in respect of the cost of carry element of Delayed Settlement Compensation (see paragraph (k) of Section 6.2 (The Conditions)) and the sell-out element of the buy-in/sell-out provision, (see paragraph (w)(vii) of Section 6.2 (The Conditions)). If any sum is denominated in a currency which does not have a Relevant Benchmark Rate, the parties are required to agree the applicable rate at the time of trade. In such a case, this box should be ticked and the applicable rate specified. If the parties do not agree the rate at the time of trade, the rate for that currency will be as specified by the Seller (acting reasonably).