shaking energy landscape - applied physics laboratory · shaking energy landscape ... 1990 1995...

TRANSCRIPT

JHS/APL Rethinking Seminar Series:

Rethinking U.S. Enduring Strengths, Challenges, and Opportunities

December 17, 2014

Shaking Energy Landscape Edward C. Chow

Senior Fellow

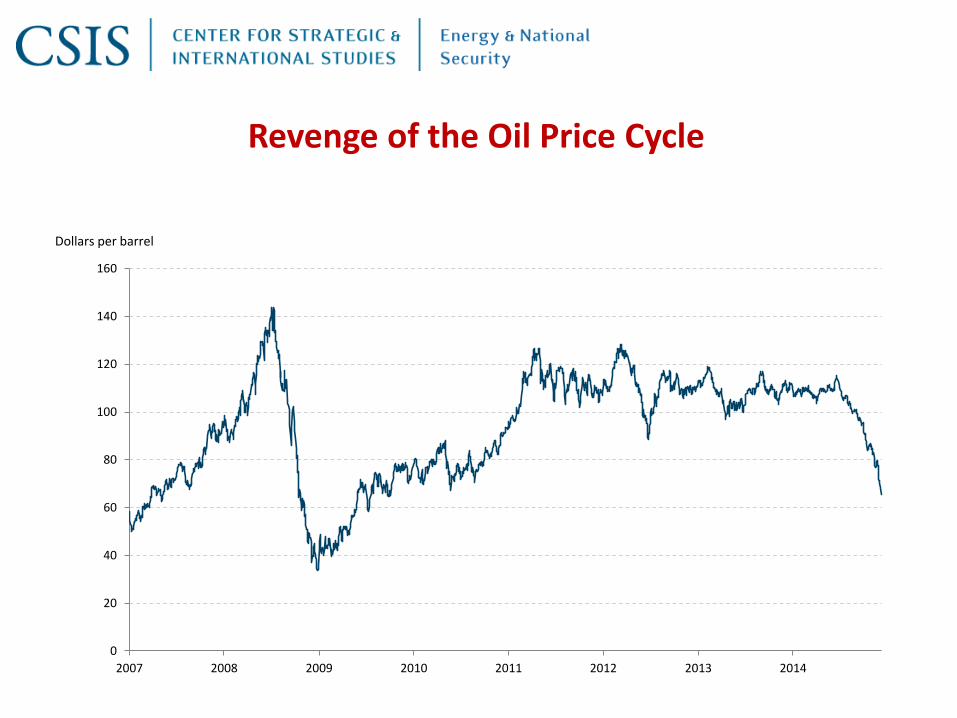

Dollars per barrel

Revenge of the Oil Price Cycle

0

20

40

60

80

100

120

140

160

2007 2008 2009 2010 2011 2012 2013 2014

American Innovation: R&D and Entrepreneurship

3

4

5

6

7

8

9

2008 2014M

mb

/d

0.6

0.7

0.8

0.9

1

1.1

1.2

1.3

1.4

1.5

1.6

2008 2014

Mm

b/d

45

50

55

60

65

70

75

2008 2014

Bcf

/d

Source: Source: U.S. Energy Information Administration; LPG = Propane and Butane; Crude oil includes lease condensate

Back to the

level of 1985

+29% +90% +67%

50% of

Worldwide

LNG Market

50% of

International

LPG Market

Dry gas production LPG production Crude oil production

US Production and Global Market

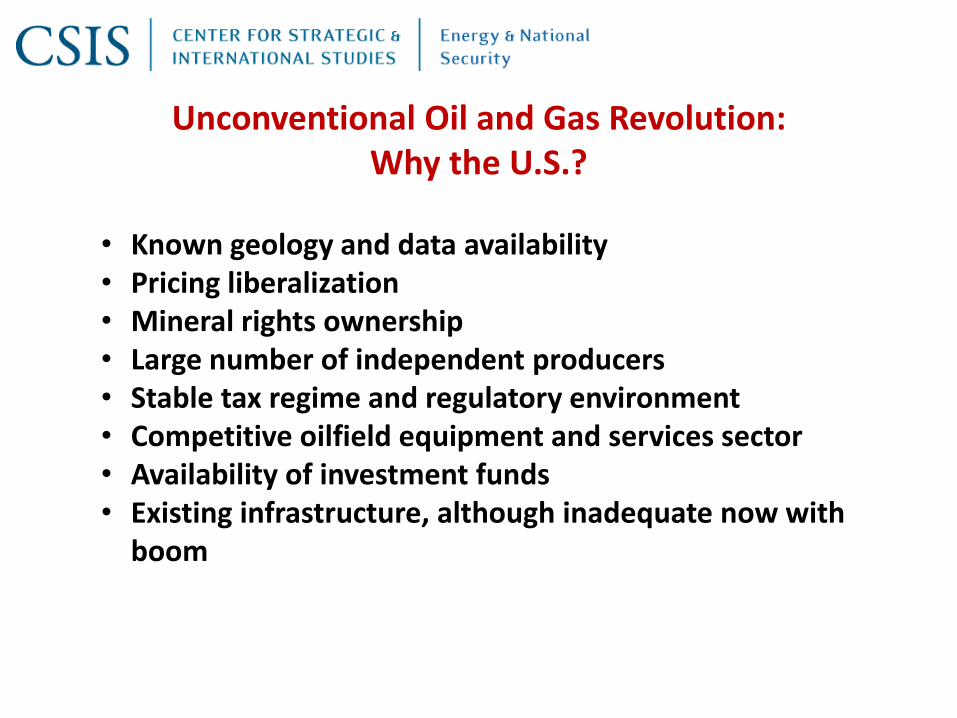

Unconventional Oil and Gas Revolution:Why the U.S.?

• Known geology and data availability• Pricing liberalization• Mineral rights ownership• Large number of independent producers• Stable tax regime and regulatory environment• Competitive oilfield equipment and services sector• Availability of investment funds• Existing infrastructure, although inadequate now with

boom

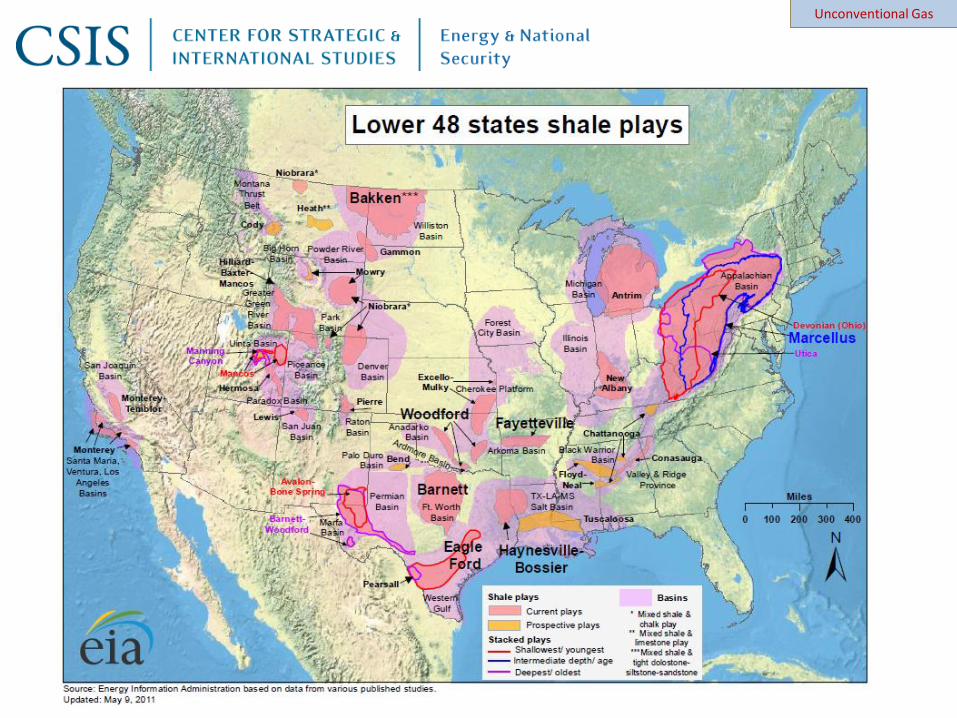

U.S. Shale Gas Resources

Unconventional Gas

These seven regions accounted for 95% of U.S. oil production growth and all U.S. natural gas production growth from 2011-2013

Source: EIA, Drilling Productivity Report

U.S

. dry

nat

ura

l gas

pro

du

ctio

n

trill

ion

cu

bic

fee

t

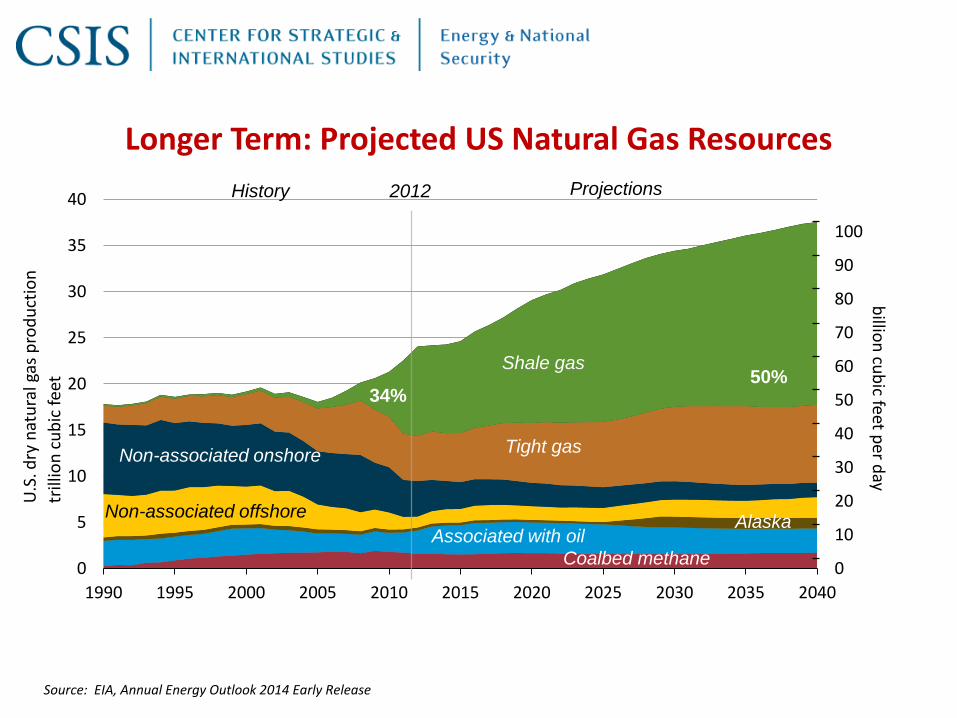

Source: EIA, Annual Energy Outlook 2014 Early Release

0

10

20

30

40

50

60

70

80

90

100

0

5

10

15

20

25

30

35

40

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040

Associated with oil

Coalbed methane

Tight gas

Shale gas

AlaskaNon-associated offshore

Non-associated onshore

ProjectionsHistory 2012

billio

n cu

bic feet p

er day

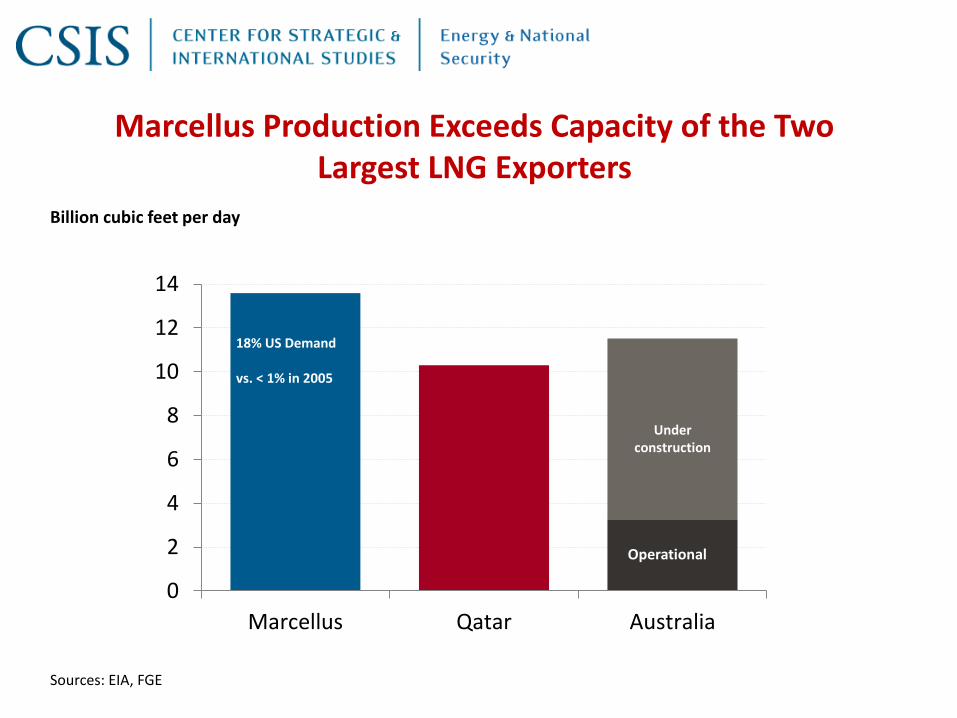

Longer Term: Projected US Natural Gas Resources

34%50%

Operational

Underconstruction

Billion cubic feet per day

Sources: EIA, FGE

Marcellus Production Exceeds Capacity of the Two Largest LNG Exporters

0

2

4

6

8

10

12

14

Marcellus Qatar Australia

Operational

Underconstruction

18% US Demand

vs. < 1% in 2005

Source: U.S. Energy Information Administration, Annual Energy Outlook 2014, May 7, 2014

Henry Hub spot Prices (2012 dollars per million Btu)

Increased production allows U.S. to transition from net importer to net exporter of natural gas

U.S. dry gas production, trillion cubic feet per year

0

5

10

15

20

25

30

0.0

10.0

20.0

30.0

40.0

50.0

60.0

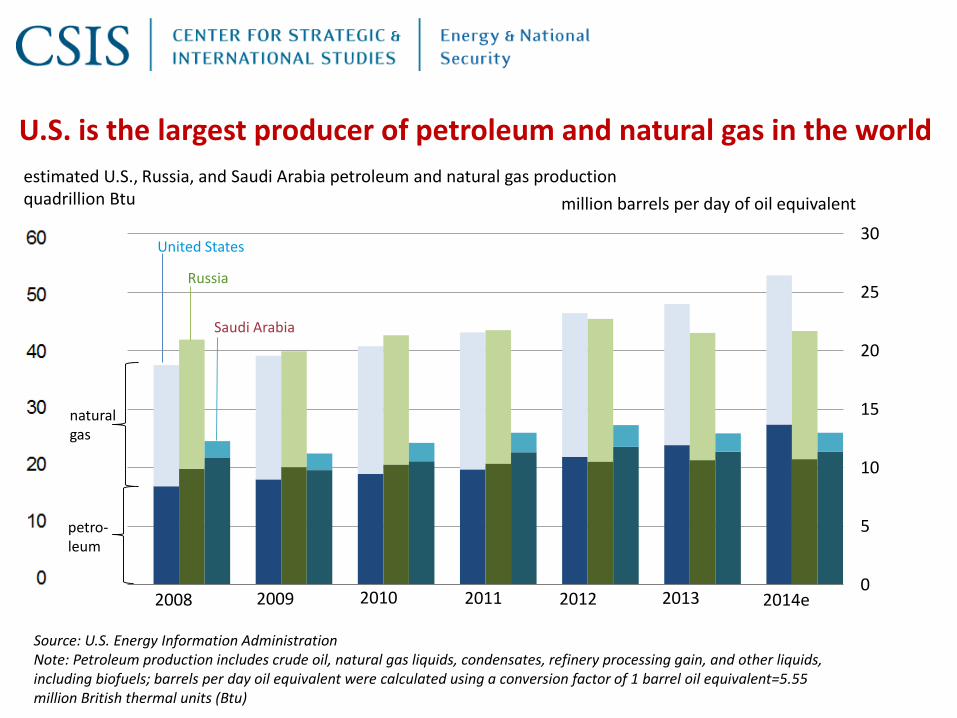

U.S. is the largest producer of petroleum and natural gas in the world

estimated U.S., Russia, and Saudi Arabia petroleum and natural gas productionquadrillion Btu million barrels per day of oil equivalent

United States

Russia

Saudi Arabia

petro-leum

naturalgas

2008 2009 2010 2011 2012 2013 2014e

Source: U.S. Energy Information AdministrationNote: Petroleum production includes crude oil, natural gas liquids, condensates, refinery processing gain, and other liquids,including biofuels; barrels per day oil equivalent were calculated using a conversion factor of 1 barrel oil equivalent=5.55 million British thermal units (Btu)

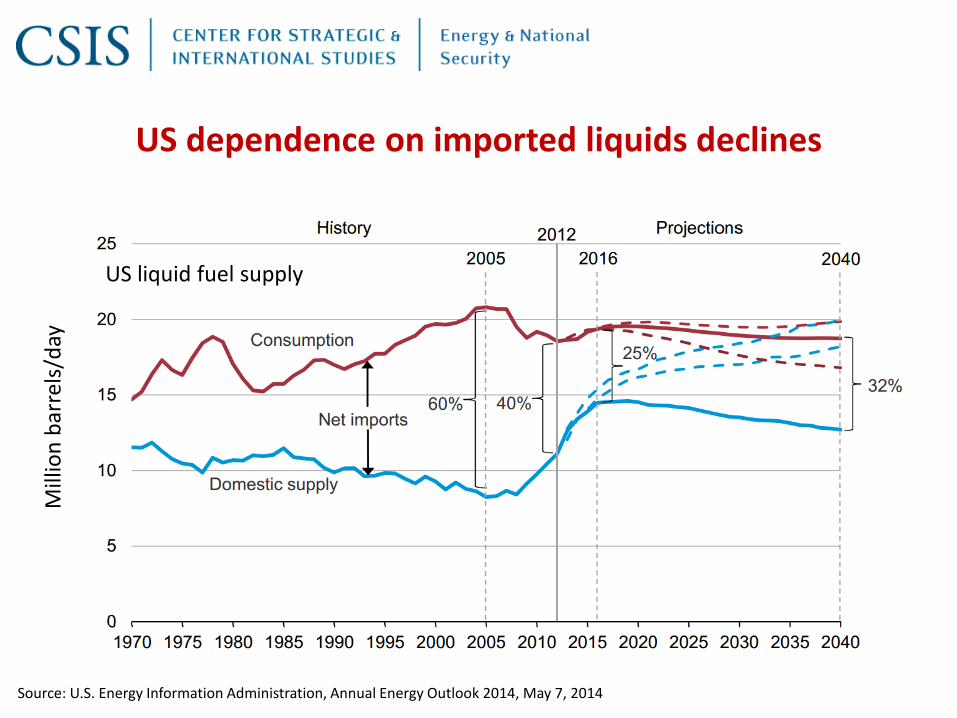

US dependence on imported liquids declines

US liquid fuel supply

Mill

ion

bar

rels

/day

Source: U.S. Energy Information Administration, Annual Energy Outlook 2014, May 7, 2014

Million barrels per day

Source: U.S. Energy Information Administration; 2014 includes data through September

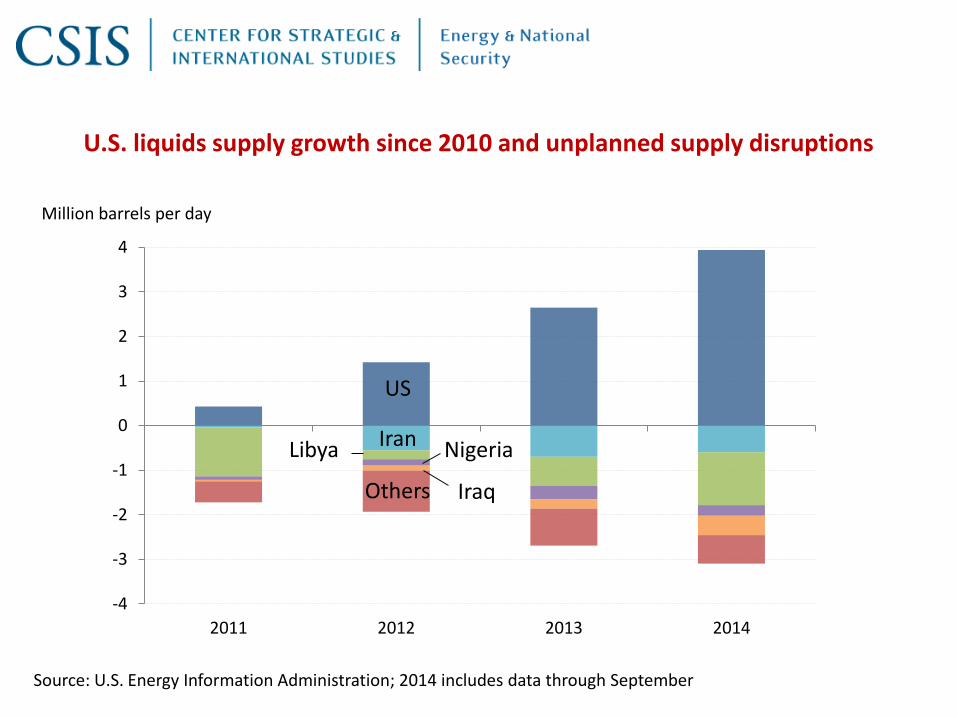

U.S. liquids supply growth since 2010 and unplanned supply disruptions

-4

-3

-2

-1

0

1

2

3

4

2011 2012 2013 2014

US

IranLibya Nigeria

IraqOthers

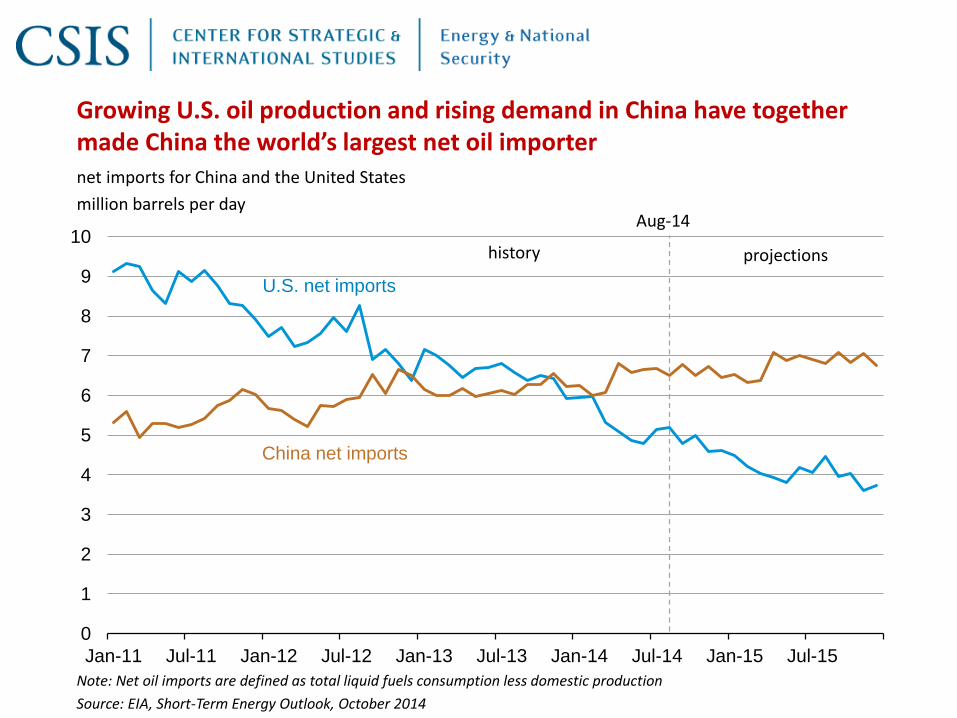

Growing U.S. oil production and rising demand in China have together made China the world’s largest net oil importer

0

1

2

3

4

5

6

7

8

9

10

Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15

U.S. net imports

China net imports

net imports for China and the United States

million barrels per day

Note: Net oil imports are defined as total liquid fuels consumption less domestic production

Source: EIA, Short-Term Energy Outlook, October 2014

projectionshistory

Aug-14

Natural gas demand outlook by region

The main regions pushing global gas demand higher are China – which overtakes the EU as a gas consumer around 2035 – and the Middle East

200

400

600

800

1 000bcm0.7%

2.0%5.5 %

0.6%0.2%

3.2%

4.6%

Additionalto 2040

2012

% = CAAGR 2012-2040

UnitedStates

MiddleEast

China EuropeanUnion

Russia Africa IndiaLatin America

2.4%

Source: IEA World Energy Outlook 2014

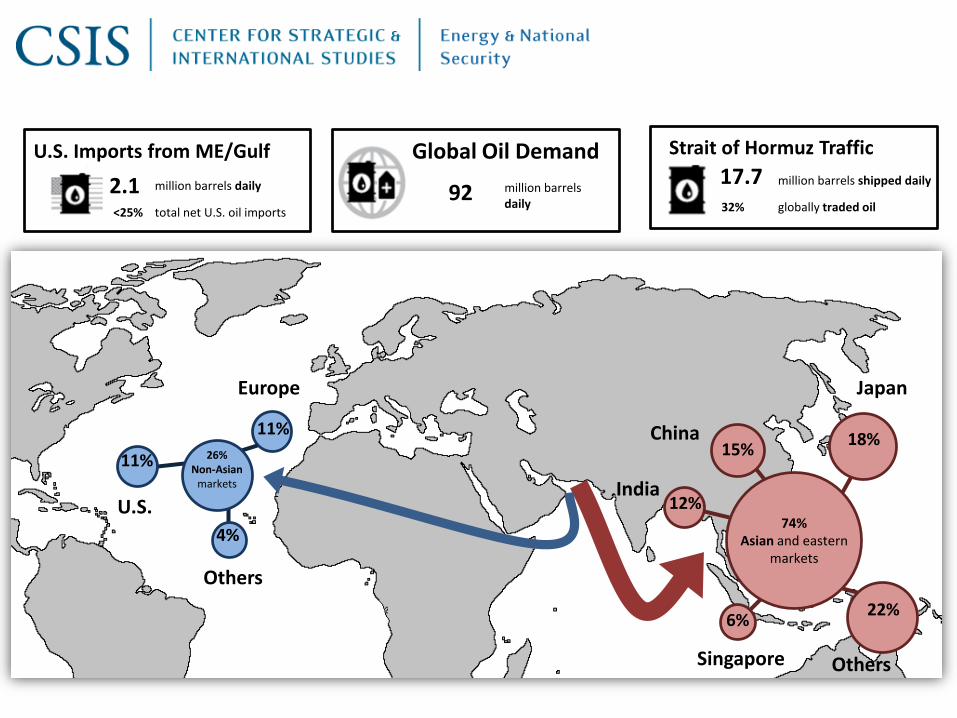

74%Asian and eastern

markets

12%

18%15%

22%6%

4%

11%

11%

26%Non-Asian

markets

U.S.

Others

OthersSingapore

India

China

JapanEurope

2.1<25%

million barrels daily

total net U.S. oil imports

U.S. Imports from ME/Gulf

globally traded oil

Strait of Hormuz Traffic

17.732%

million barrels shipped daily92 million barrels

daily

Global Oil Demand

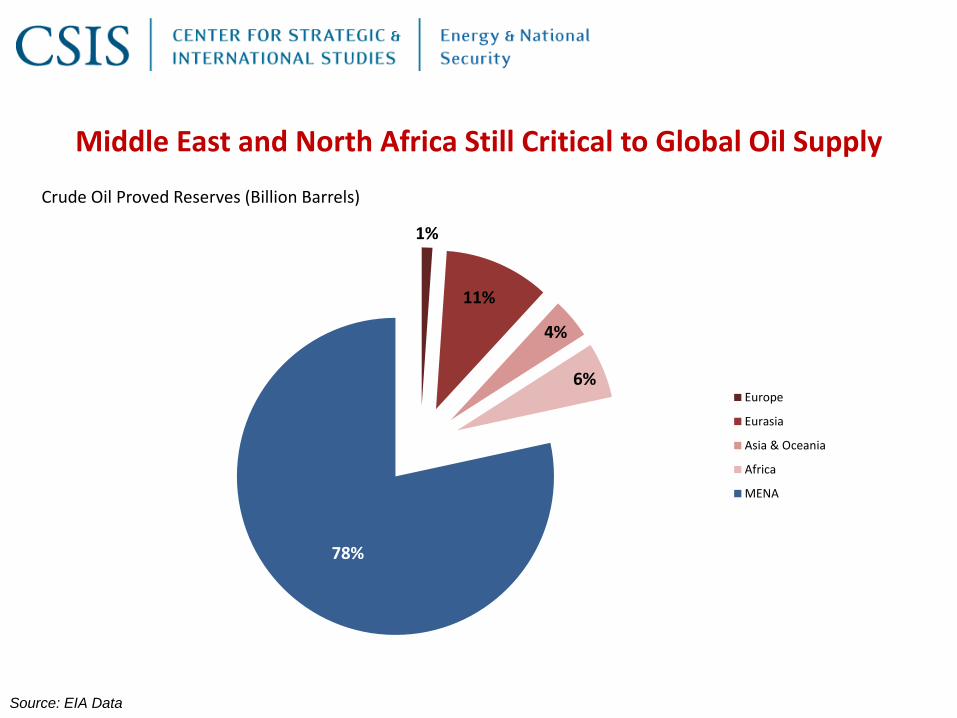

Middle East and North Africa Still Critical to Global Oil Supply

Source: EIA Data

1%

11%

4%

6%

78%

Europe

Eurasia

Asia & Oceania

Africa

MENA

Crude Oil Proved Reserves (Billion Barrels)

2013 2020 2030 20402015

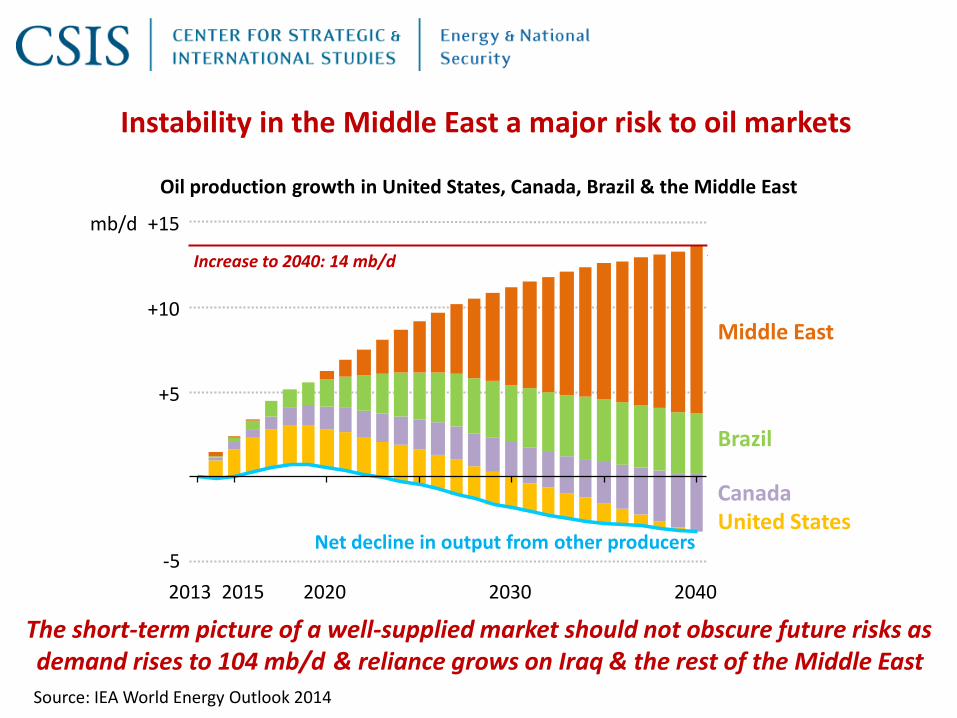

Instability in the Middle East a major risk to oil markets

Oil production growth in United States, Canada, Brazil & the Middle East

The short-term picture of a well-supplied market should not obscure future risks as demand rises to 104 mb/d & reliance grows on Iraq & the rest of the Middle East

+5

+10

+15

-5

2013 2020 2030 20402015

Net decline in output from other producers

Increase to 2040: 14 mb/d

mb/d

Increase to 2040:14 mb/d

Middle East

Brazil

CanadaUnited States

& reliance grows on Iraq & the rest of the Middle East

Source: IEA World Energy Outlook 2014

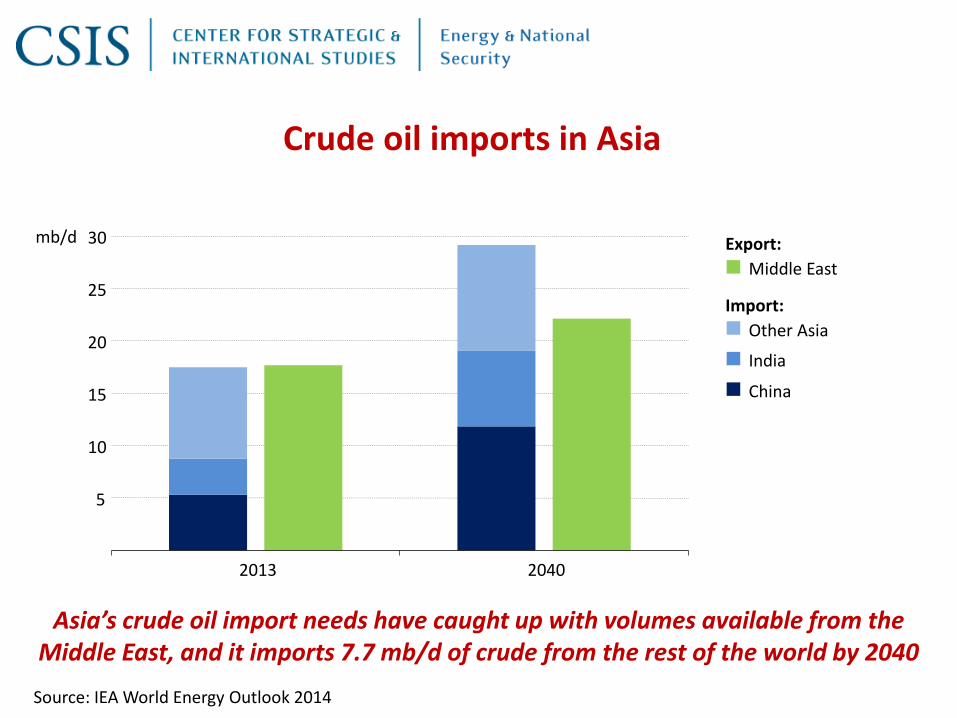

Crude oil imports in Asia

Asia’s crude oil import needs have caught up with volumes available from the Middle East, and it imports 7.7 mb/d of crude from the rest of the world by 2040

5

10

15

20

25

30mb/d

2013 2040

Middle East

Other Asia

India

China

Export:

Import:

Source: IEA World Energy Outlook 2014

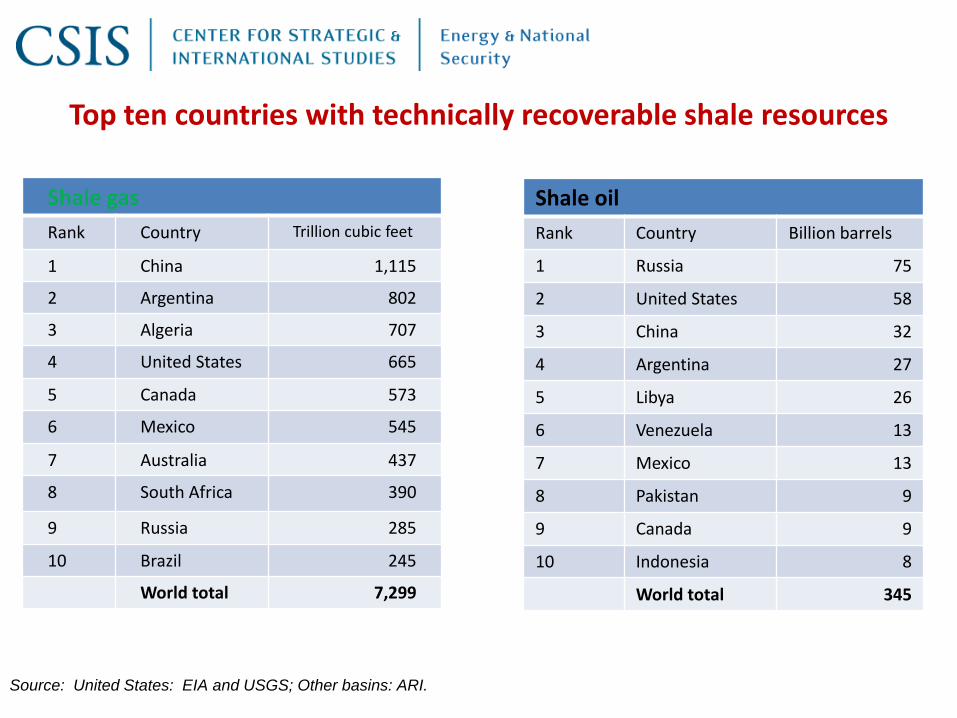

Top ten countries with technically recoverable shale resources

Shale gas

Rank Country Trillion cubic feet

1 China 1,115

2 Argentina 802

3 Algeria 707

4 United States 665

5 Canada 573

6 Mexico 545

7 Australia 437

8 South Africa 390

9 Russia 285

10 Brazil 245

World total 7,299

Shale oil

Rank Country Billion barrels

1 Russia 75

2 United States 58

3 China 32

4 Argentina 27

5 Libya 26

6 Venezuela 13

7 Mexico 13

8 Pakistan 9

9 Canada 9

10 Indonesia 8

World total 345

Source: United States: EIA and USGS; Other basins: ARI.

•Source: United States basins from EIA and United States Geological Survey, other basins from ARI based on data from various published studies

EIA / ARI assessed shale oil and shale gas resources 2013

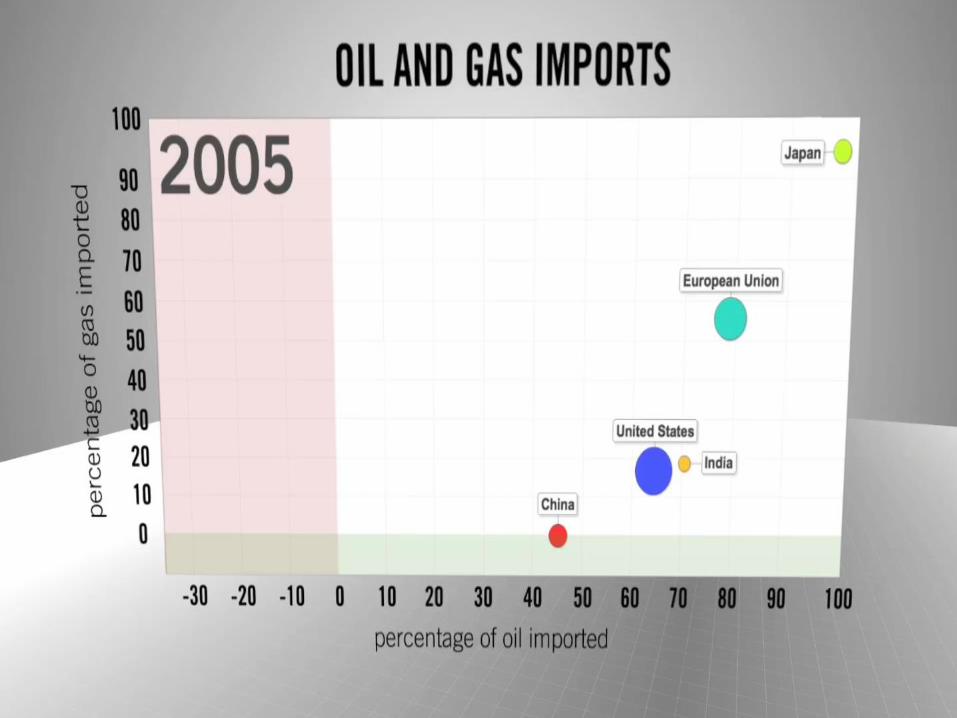

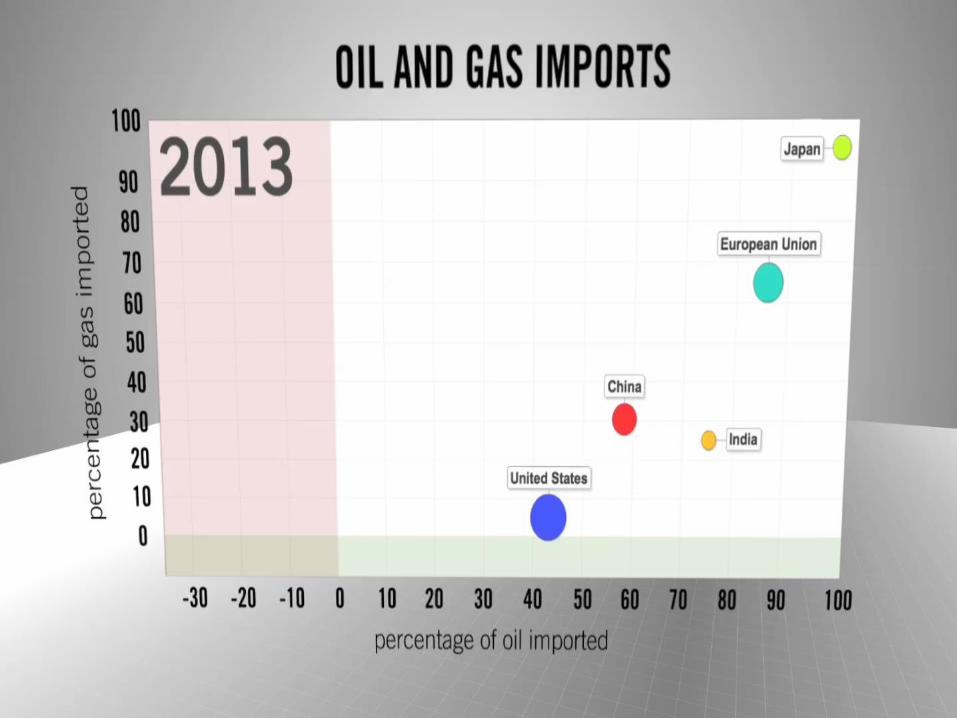

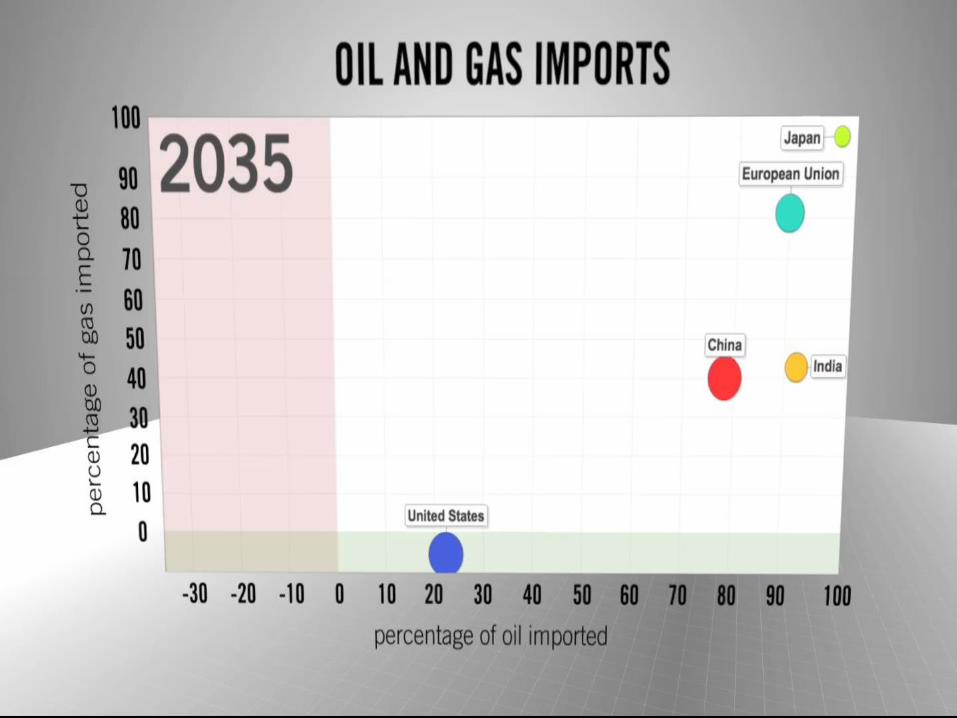

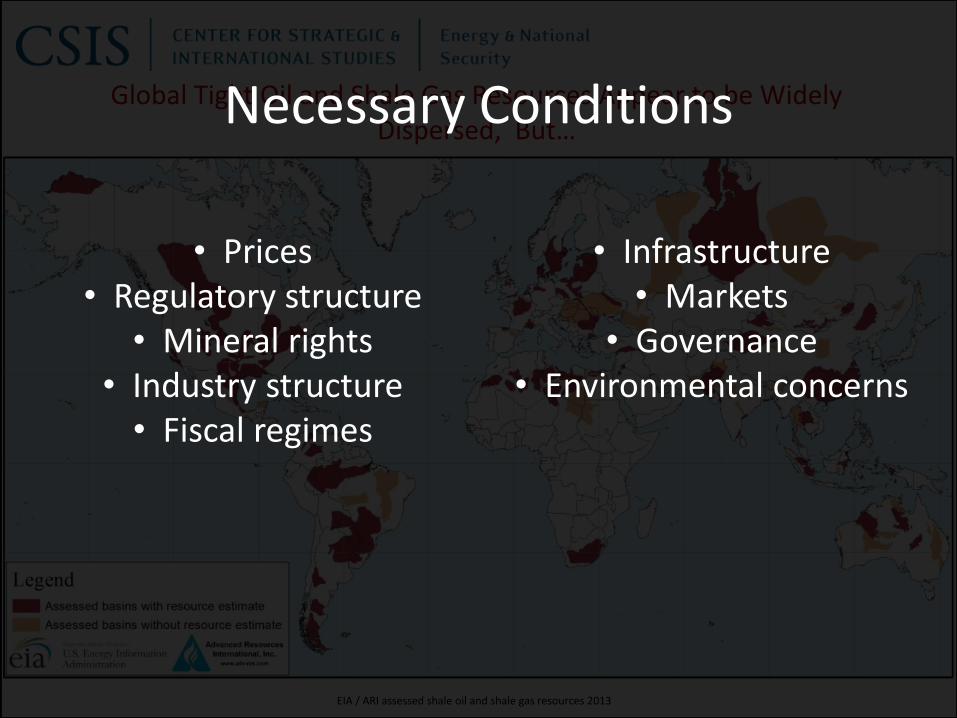

Global Tight Oil and Shale Gas Resources Appear to be Widely Dispersed, But…

• Prices• Regulatory structure

• Mineral rights• Industry structure• Fiscal regimes

• Infrastructure• Markets

• Governance• Environmental concerns

Necessary Conditions

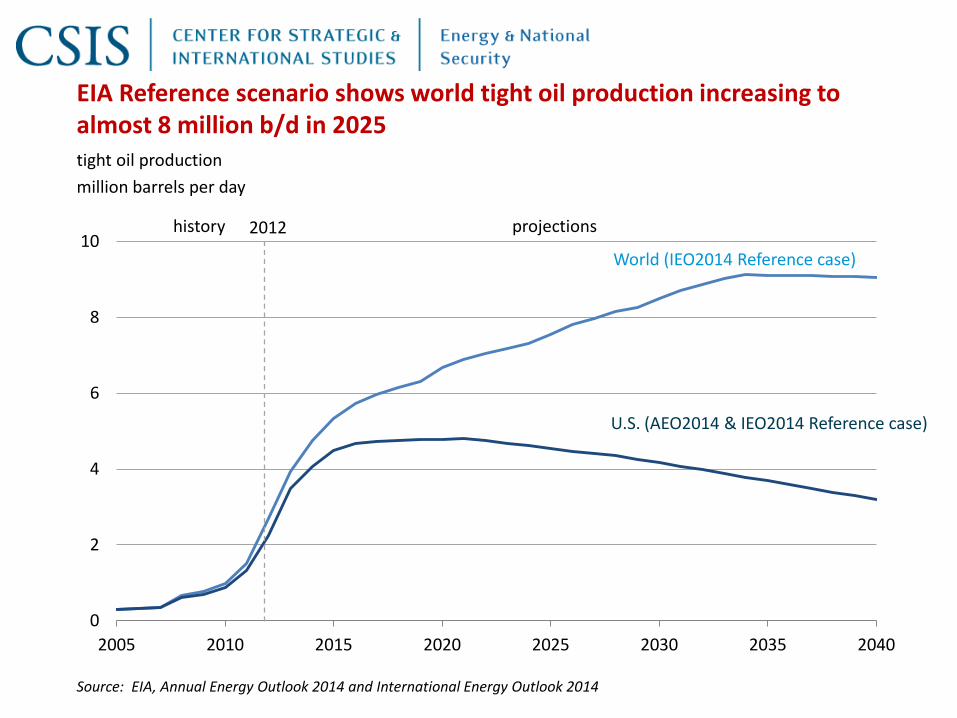

EIA Reference scenario shows world tight oil production increasing to almost 8 million b/d in 2025

0

2

4

6

8

10

2005 2010 2015 2020 2025 2030 2035 2040

tight oil production

million barrels per day

Source: EIA, Annual Energy Outlook 2014 and International Energy Outlook 2014

projectionshistory 2012

U.S. (AEO2014 & IEO2014 Reference case)

World (IEO2014 Reference case)

Outlook for tight oil

Tight oil production remains focused in the United States, but is joined increasingly by other players

1 2 3 4 5 6 7

2013

2025

2040

mb/d

United States Russia Argentina Mexico China Canada Rest of world

Source: IEA World Energy Outlook 2014

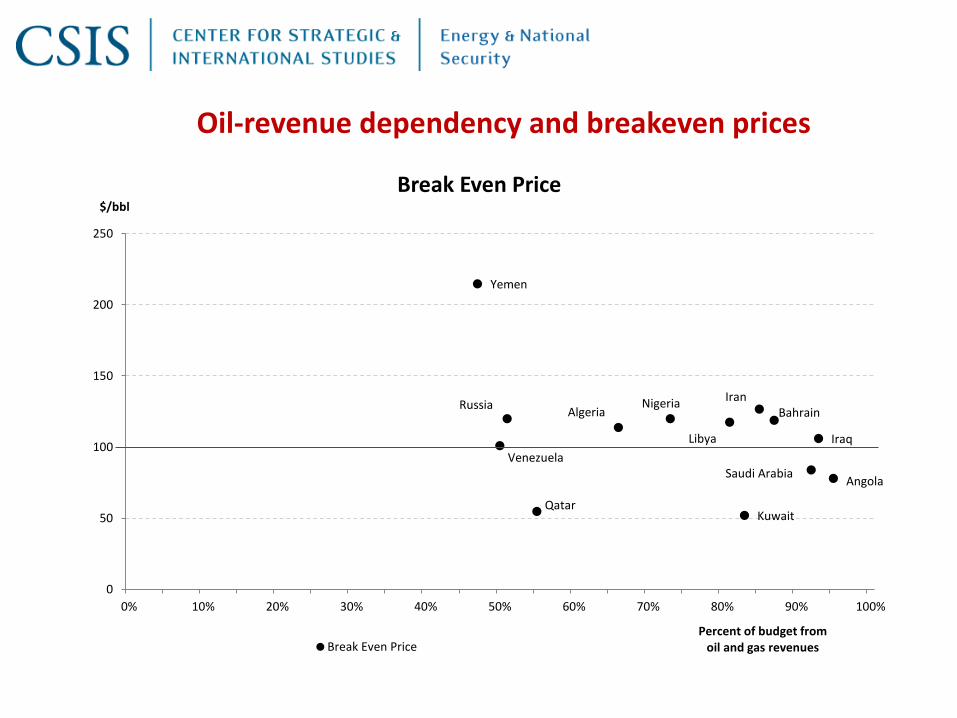

Yemen

Venezuela

Qatar

AlgeriaNigeria

Libya

Kuwait

IranBahrain

Saudi Arabia

Iraq

Angola

0

50

100

150

200

250

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

$/bbl

Percent of budget from oil and gas revenues

Break Even Price

Break Even Price

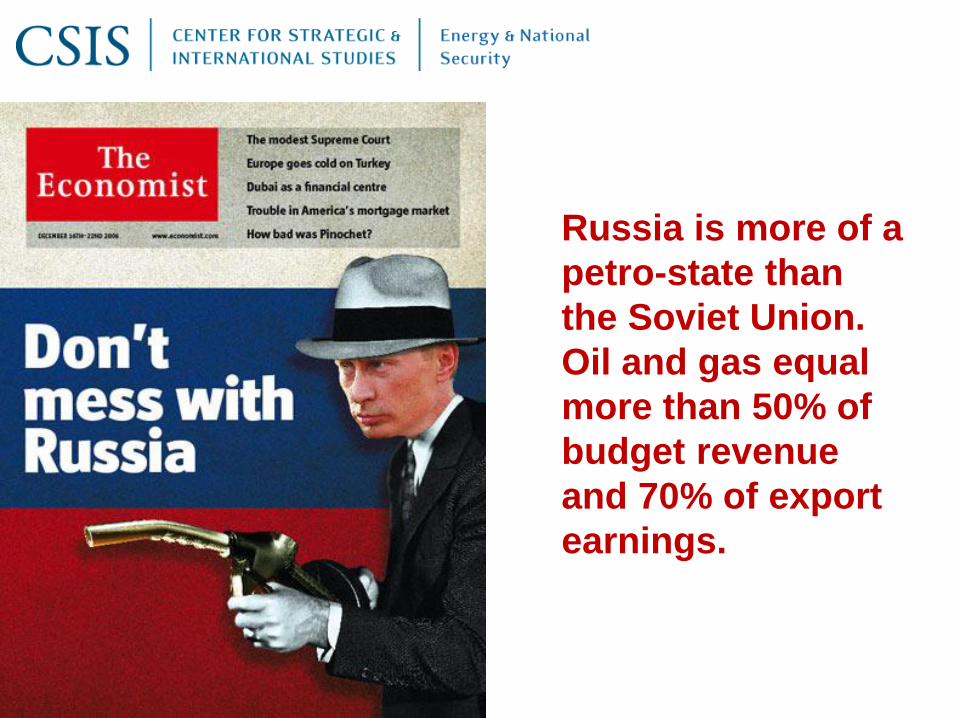

Russia

Oil-revenue dependency and breakeven prices

Russia is more of a

petro-state than

the Soviet Union.

Oil and gas equal

more than 50% of

budget revenue

and 70% of export

earnings.

31

Shanghai Cooperation Organization SummitSeptember 2014 in Dushanbe

32

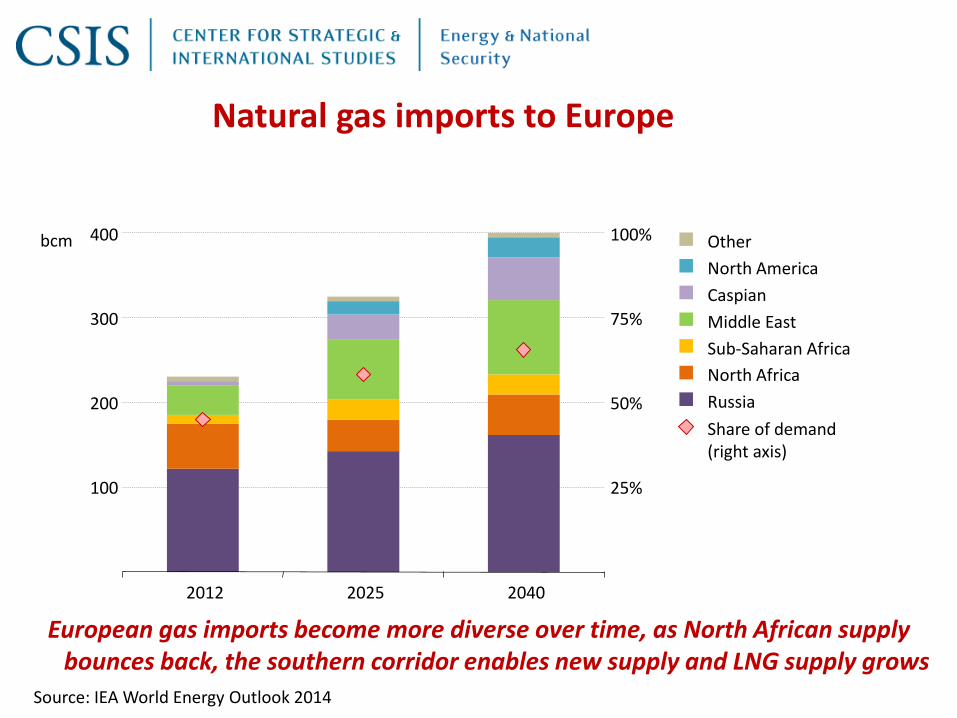

Natural gas imports to Europe

European gas imports become more diverse over time, as North African supply bounces back, the southern corridor enables new supply and LNG supply grows

100

200

300

400

2012 2025 2040

bcm

25%

50%

75%

100% Other

North America

Caspian

Middle East

Sub-Saharan Africa

North Africa

Russia

Share of demand(right axis)

Source: IEA World Energy Outlook 2014

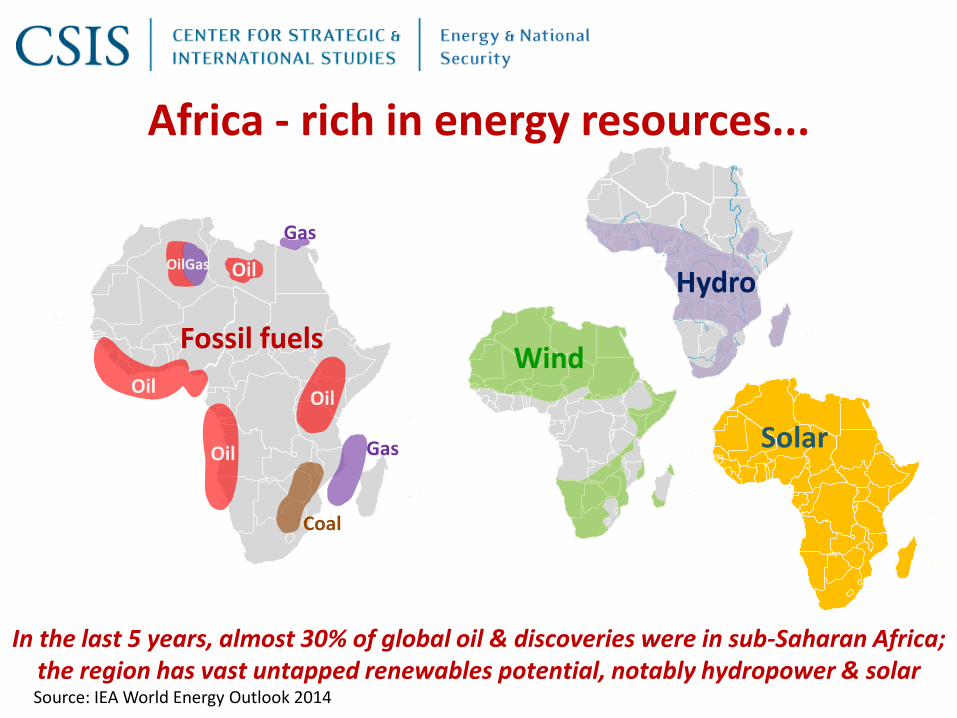

Africa - rich in energy resources...

In the last 5 years, almost 30% of global oil & discoveries were in sub-Saharan Africa;

Hydro

WindOil

Oil

Oil

OilGas

Gas

Oil

Coal

Gas

Fossil fuels

Solar

the region has vast untapped renewables potential, notably hydropower & solar Source: IEA World Energy Outlook 2014

In sub-Saharan Africa, 620 million people – two-thirds of the population – live without electricity. Only a handful of countries have electrification rates above 50%

Less than 50%

More than 50%

Share of population withaccess to electricity:

...but poor in energy supply

Source: IEA World Energy Outlook 2014

A changing balance to oil production

Oil production in sub-Saharan Africa

The region remains a major global supplier, although regulatory uncertainty, unrest & oil theft in Nigeria make Angola the main producer of crude oil until the 2020s

Other

Angola

Nigeria

Production:

1

2

3

4

5

6

7

2000 2013 2020 2030 2040

mb/d

Source: IEA World Energy Outlook 2014

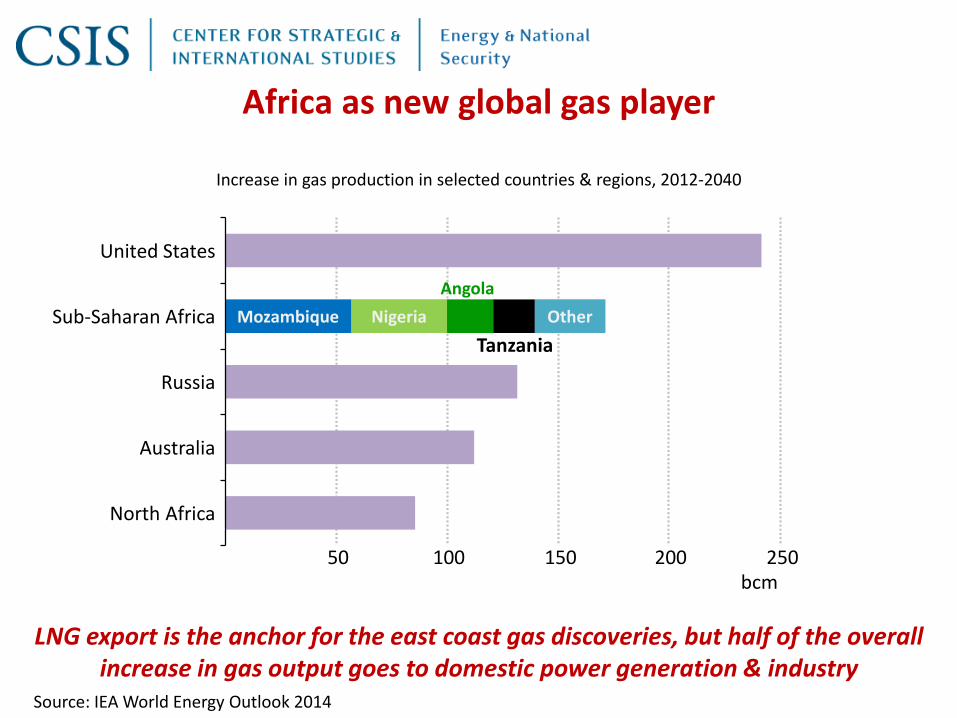

Africa as new global gas player

Increase in gas production in selected countries & regions, 2012-2040

LNG export is the anchor for the east coast gas discoveries, but half of the overall increase in gas output goes to domestic power generation & industry

50 100 150 200 250

North Africa

Australia

Russia

Sub-Saharan Africa

United States

bcm

Mozambique Nigeria Other

Angola

Tanzania

Source: IEA World Energy Outlook 2014

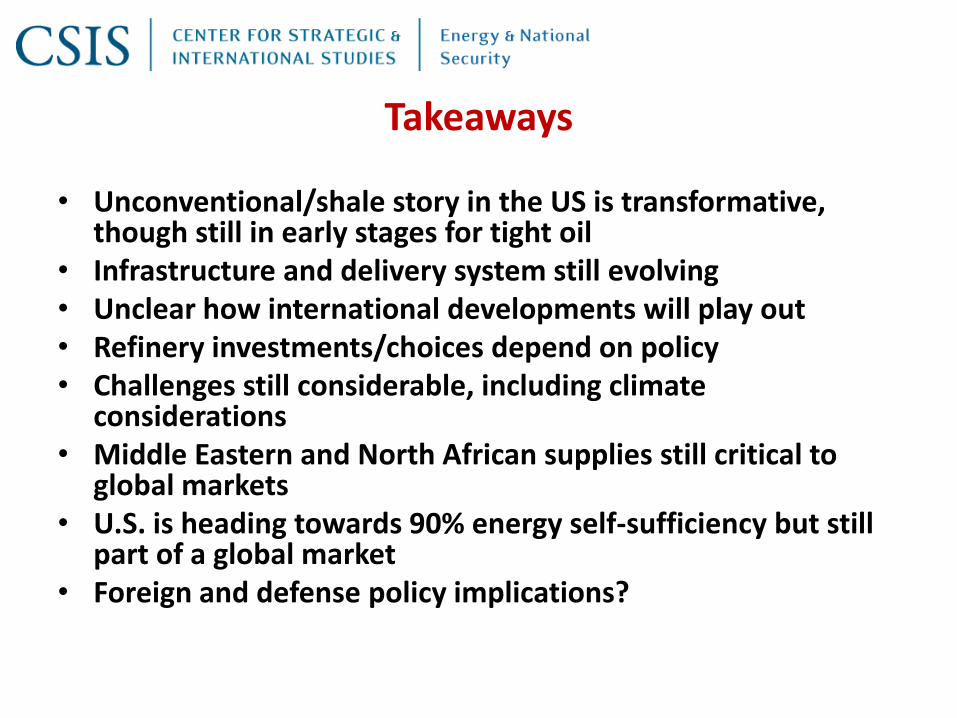

Takeaways

• Unconventional/shale story in the US is transformative, though still in early stages for tight oil

• Infrastructure and delivery system still evolving• Unclear how international developments will play out• Refinery investments/choices depend on policy• Challenges still considerable, including climate

considerations• Middle Eastern and North African supplies still critical to

global markets• U.S. is heading towards 90% energy self-sufficiency but still

part of a global market• Foreign and defense policy implications?