sostenibilidad de deuda en guatemala

TRANSCRIPT

Institutional and management fundamentals of the debt sustainability in Guatemala, a

micro approach

Fredy Gómez, MGPP, ME*, MFPublic Credit Directorate

Ministry of Finance

Outline

• Sustainability literature• Public debt situation, aspects to manage• Sustainability management under institutional

and management fundamentals• Perspectives

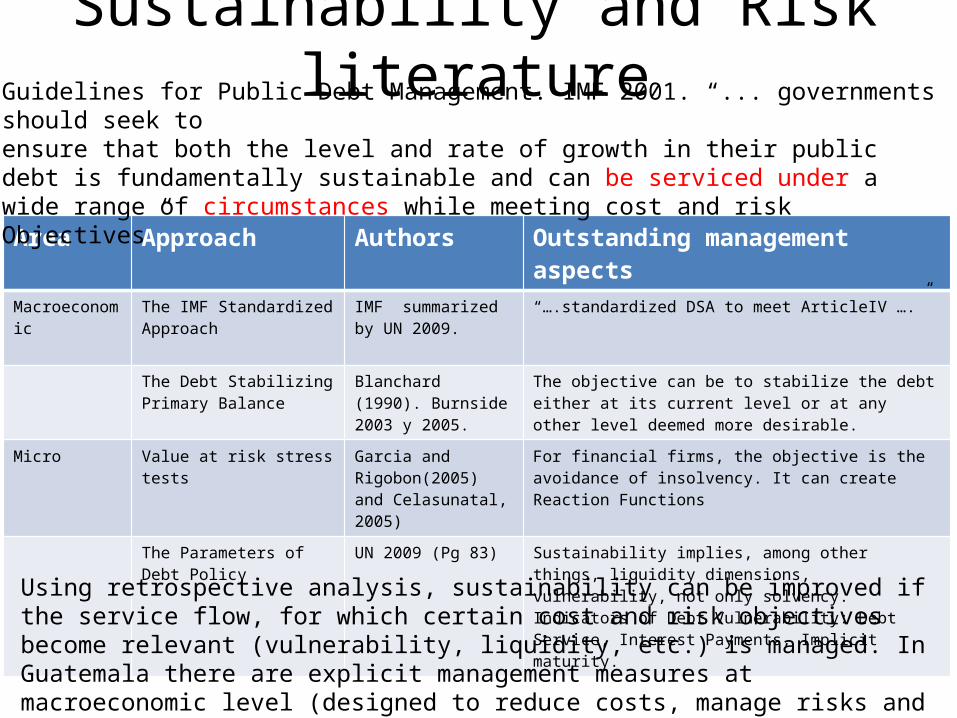

Sustainability and Risk literature

Area Approach Authors Outstanding management aspectsMacroeconomic The IMF Standardized

ApproachIMF summarized by UN 2009.

“….standardized DSA to meet ArticleIV ….”

The Debt Stabilizing Primary Balance

Blanchard (1990). Burnside 2003 y 2005.

The objective can be to stabilize the debt either at its current level or at any other level deemed more desirable.

Micro Value at risk stress tests Garcia and Rigobon(2005) and Celasunatal, 2005)

For financial firms, the objective is the avoidance of insolvency. It can create Reaction Functions

The Parameters of Debt Policy

UN 2009 (Pg 83) Sustainability implies, among other things, liquidity dimensions, vulnerability, not only solvency. Indicators of Debt Vulnerability: Debt Service, Interest Payments, Implicit maturity.

Using retrospective analysis, sustainability can be improved if the service flow, for which certain cost and risk objectives become relevant (vulnerability, liquidity, etc.) is managed. In Guatemala there are explicit management measures at macroeconomic level (designed to reduce costs, manage risks and ensure payment, which contribute to sustainability).

Guidelines for Public Debt Management. IMF 2001. “... governments should seek to ensure that both the level and rate of growth in their public debt is fundamentally sustainable and can be serviced under a wide range of circumstances while meeting cost and risk Objectives”

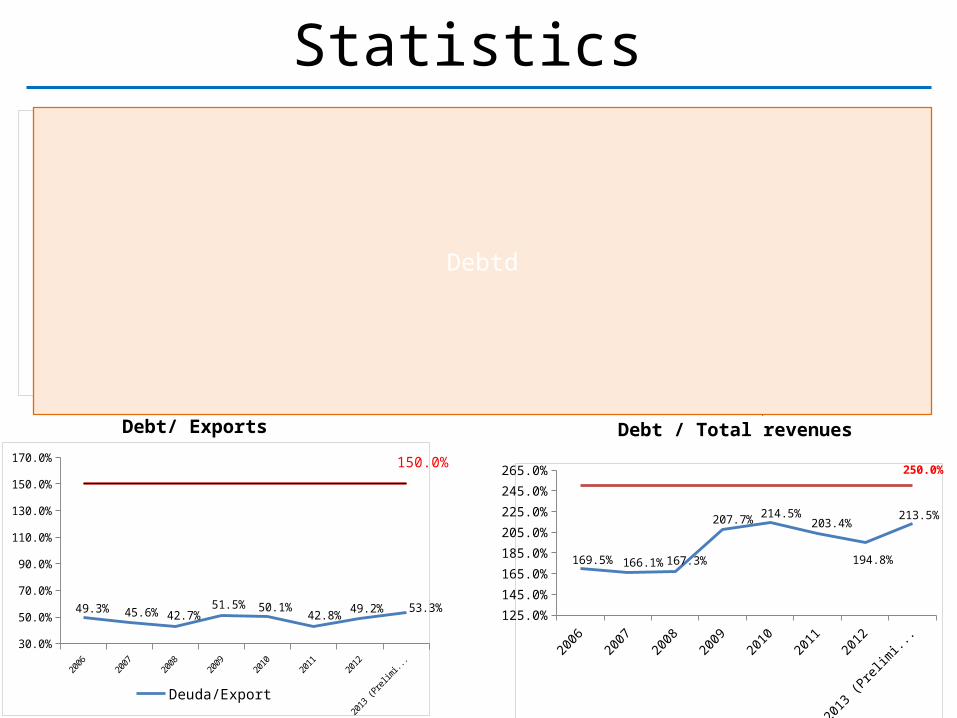

Statistics

2006 2007 2008 2009 2010 2011 2012 2013 (Preliminar)

30.0%

50.0%

70.0%

90.0%

110.0%

130.0%

150.0%

170.0%

49.3% 45.6% 42.7%51.5% 50.1%

42.8% 49.2% 53.3%

150.0%

Deuda/Export Techo

125.0%

145.0%

165.0%

185.0%

205.0%

225.0%

245.0%

265.0%

169.5% 166.1% 167.3%

207.7% 214.5%203.4%

194.8%

213.5%

250.0%

Deuda/Ingresos Techo

2006 2007 2008 2009 2010 2011 2012 2013 (Preliminar)15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

21.8% 21.6%20.0%

23.0%24.6% 24.1% 24.6% 24.7%

40.0%

Deuda/PIB TechoDebt/ Exports

Deuda / PIB

Debt / Total revenues

Debtd

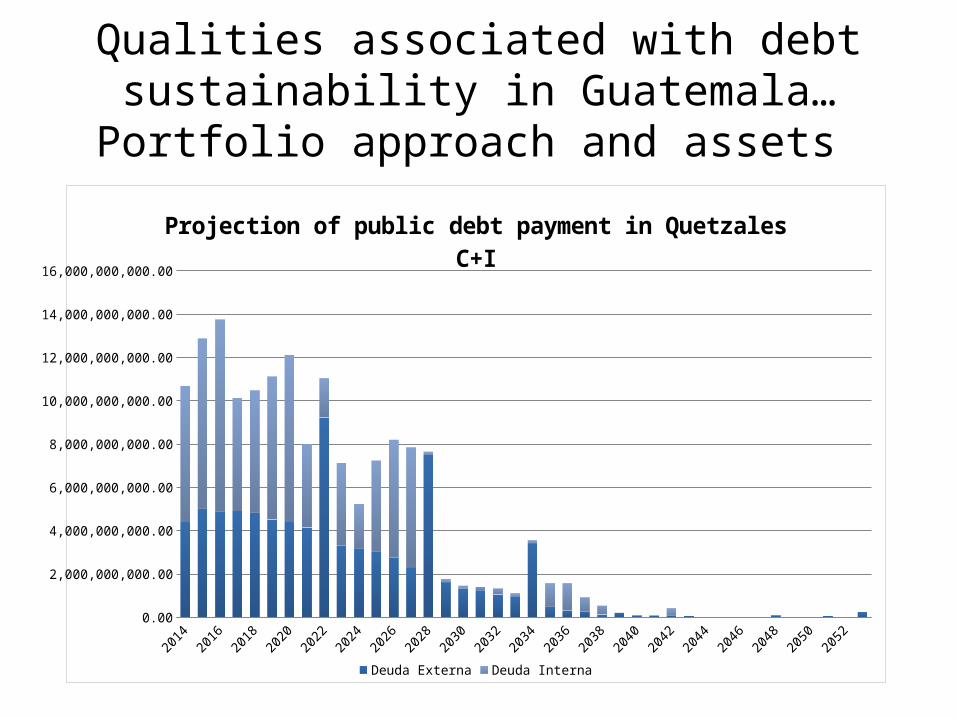

Qualities associated with debt sustainability in Guatemala…Portfolio approach and assets

20142016

20182020

20222024

20262028

20302032

20342036

20382040

20422044

20462048

20502052

0.00

2,000,000,000.00

4,000,000,000.00

6,000,000,000.00

8,000,000,000.00

10,000,000,000.00

12,000,000,000.00

14,000,000,000.00

16,000,000,000.00

Projection of public debt payment in QuetzalesC+I

Deuda Externa Deuda Interna

Qualities associated to debt sustainability in Guatemala… Portfolio approach and assets

Risk Ratings ScaleDescription S&P Moody's Fitch

Highest credit quality

Investment grade

AAA Aaa AAA

High credit qualityAA+ Aa1 AA+AA Aa2 AAAA- Aa3 AA-

Strong payment abilityA+ A1 A+A A2 AA- A3 A-

Adequate payment abilityBBB+ Baa BBB+BBB Baa2 BBBBBB- Baa3 BBB-

Likely to comply with their liabilities, with some uncertainity

Speculative

grade

BB+ Ba1 BB+BB Ba2 BBBB- Ba3 BB-

High credit riskB+ B1 B+B B2 BB- B3 B-

Very high credit riskCCC+ Caa1 CCCCCC Caa2 CCCCC- Caa3 C

Near breach, with recovery possibilitiesCC Ca CC

C

BreachSD C DDDD DD D

Institutional and management fundamentals of debt management

• Funding has continued a deficit path, following the logic of the spending highly bound by constitutional rules

2005 2006 2007 2008 2009 2010 2011 2012 2013-3.5

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

-1.7-1.9

-1.4-1.6

-3.1 -3.3

-2.8

-2.4-2.2

Note: figures of approved budget

Institutional and management fundamentals of debt management

• Rules of operation approval – Loans must be approved one by one by the

Congress, even bond financing– Prior to being sent to this instance, they must

count with the approval of investment directors and the Central Bank.

Management fundamentals, risks

• Which risks faces the service payment, present and future? • Tax resources or debt for debt payment?• Timely payment?• What coverage do we have for risks?

– Price risk (i, E)– Credit and liquidity risk

• Liability and risk management…Focusing on instruments– Who? Reform of the debt office– What do they do? Strategic approach– How? Focusing on management instruments, case of rate. – Results

• Payment reduction for service in time (Eurobond)… exposure increases

• Reduction of concentration risk … Domestic Bond Series…cost, cost increases due to long term

• Exposure reduction.. Domestic placement• Cost reduction

Who?

Proposed organizational structure

Public Credit Directorate

Subdirectorate of Operations

Legal Technical Assistance Unit

Subdirectorate of Management of Public Credit Politics

Department of Treasury Bond Trading and Placement

Department of Negotiation of International Cooperation

Department of Support for the Execution of Foreign Loans

Department of Public Debt Servicing

Department of Registration of Public Debt

Subdirectorate of Operation Negotiation

Department of Liabilities and Risk Management

Department of Research and Innovation

Department of Politics Management

Back Office: Focusing on operations

Middle Office: Focusing on politics

Front Office: Focusing on negotiation

• Better linkage to functions of a modern debt office.• New departments

What do they do?

How? With instruments

* First amount: Q. 400.0 million

* 4 new series, to 7, 10, 12 and 15 years

* Coupon lowerings

Approach for placement1. An amount is “auctioned” , this is a new rule2. Coupons are lowered to reflect the strategy

of cost reduction.

Some results• Results

– Payment reduction for service in time (Eurobond).. Exposure increases

– Reduction of concentration risk … Domestic bond series… cost, cost increases due to long term

– Exposure reduction... Domestic placement

– Cost reduction

Management perspectives

• Relevant interest rate at the market• Prospective studies on service• Contingent liabilities inventories• Rules for the use of provisioning funds• Financial instruments: variable to fixed rate. • Development of the domestic market for low

cost. Standardization.

Institutional and management fundamentals of the debt sustainability

in Guatemala, a micro approach.

Fredy Gómez