ss machines ltd bbp final

TRANSCRIPT

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 1/55

2012

SS MACHINES LTD

BUSINESS BLUEPRINT

Project Name: SAP FICO Implementation

Created by: SAPR19FICO101ERP Project Team

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 2/55

Business Blueprint

SS Machines Project Page 2

This document describes the parameters for SS Machines LTD business Blue print. It includes theactivities, events and deliverables compiled as a result of the output from the business requirements

gathered outlining the strategy of how SS Machines are to be mapped into the SAP systems.

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 3/55

Business Blueprint

SS Machines Project Page 3

Table of Contents

Table of Contents Page0.0 BUSINESS PROCESS CONFIGURATION SETTINGS……………………………………… 6

1.0. ORGANISATION STRUCTURE .……………….………………………………………………. 6

1.1. Client……………….…….…………………………………………………………………………. 7

1.2. Company….…………………………………………………………………………………………. 7

1.3. Company Code.……………….…………………………………………………………………….. 7

1.4. Chart of Accounts…..……….………………………………………………………………………. 7

15 1.5 Group Chart of Accounts (GCOA) ………………………………………………….…………. 8

1.6. Chart of Depreciation..……………………………………………………………………………… 8

1.7. Controlling Area….………………………………………………………………………………… 8

1.8. Cost Centre………………………………………………………………………………………… 9

1.9 Profit Centers ……………………………………………………………………………………… 9

2.0. GENERAL LEDGER…………………………………………………………………………….. 10

2.1. Chart Of Accounts…………………………………………………………………………………. 10

2.2. Master Data………………………………………………………………………………………… 10

2.3. Integration ….……………….………………………………….…………………………………. 11

2.4. Company Code Segment……………………………………….………………………………….. 11

2.5. Currency..………………………………………………………………………………………….. 11

2.6. Asset Master.………………………………………………………….…………………………… 11

2.7. Fiscal Year and Fiscal Year Variance ………………………………..…………………………… 11

2.8. Document Type………………………………………..…………………………………………... 13

2.9. Posting Key ………………………………………………..…………………………………..….. 13

2.10. Accounts Group………………………………………………..…………………………………... 15

3.0. ACCOUNTS PAYABLE………………………………………………………………………… 17

3.1. Vendor Master Data .……………………………………………………………………………… 17

3.2. Vendor Accounts Group…………………………………………………………………………… 19

3.3. Payment methods…………..……………………………………………………………………… 19

3.4. Vendor Tolerance Group………………………………………………………………………...... 20

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 4/55

Business Blueprint

SS Machines Project Page 4

3.5. Vendor Reconciliation Account………………………………………………………………....... 20

3.6. Taxes…..………………………………………………………………………………………….. 20

3.7. Payment Block..…………………………………………………………………………………… 20

3.8. Automatic Payment Program.……………………………………………………………………. 21

3.9. House Bank Definition ………………………………………………………………………..….. 22

4.0. ACCOUNTS RECEIVABLES……………………………………………………………..….. 23

4.1. Master Data ……………………………………………………………………………………….. 23

4.2. Reconciliation Account…………………………………………………………………………… 25

4.3. Description of Improvement…………………………………………………………………….. 26

4.4. Special GL Accounts……………………………………………………………………………… 27

4.5. Dunning…………………………………………………………………………………………….. 29

4.6. Customer/Vendor…………………………………………………………………………………… 30

4.7. Process Control ……………………………………………………………………………………. 30

4.8. Functional Gaps ……………………………………………………………………………………. 31

5.0. BANK ACCOUNTING……………………………………………………………………………..32

5.1. Bank Master Data ….…………………………………………………………..…………………… 32

5.2. General Ledger Account…………………………………………………………………………….. 33

5.3. House Bank and House Bank Creation………………………………………………………………33

5.4. Check Management Process.…………………………………………………………………………34

5.5. Manual Bank Reconciliation……….………….………………………………………….……. 35

5.6. Description of Improvement…………..…………..…………………………………….……….….. 35

5.7. Petty Cash Management ……………………………………………………………………………..36

5.8. Description of Functional Deficit …………….…………………………………………………….. 36

6.0.TAXES………………………………………………………………………………………………

37

6.1. rror not defined..……………………………………………………………………………………38

6.2. ………………………………………………………………………………………………………..38

6.3. ………………………………………………………………………………………………………..38

7.0. ASSET ACCOUNTING.………………………………………………………………………….. 39

7.1. Asset Classes….……………………………………………………………………………………. 41

7.2. Chart of Depreciation ……………………………………………………………………………… 41

7.3. Posting Depreciation ……...………………………….……………………………………………. 41

7.4. Acquisition of an Asset …..…………………………..…………………………………………… 41

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 5/55

Business Blueprint

SS Machines Project Page 5

7.5. Intercompany Transfers……………………….………..……………………………………….... 43

7.6. Asset Retirement ………………………………………………………………………………….. 43

7.7. Asset Under Construction……………………..……….………………………………………..... 45

7.8. Fiscal Year Change ……………………….………….……………………..…………………….. 46

8.0. COST CENTER ACCOUNTING……………………………………………………………….. 47

8.1. Cost Centres……..………………………………………………………………………………….. 47

8.2. Assessments of Cost Centres……………………………………………………………………….. 48

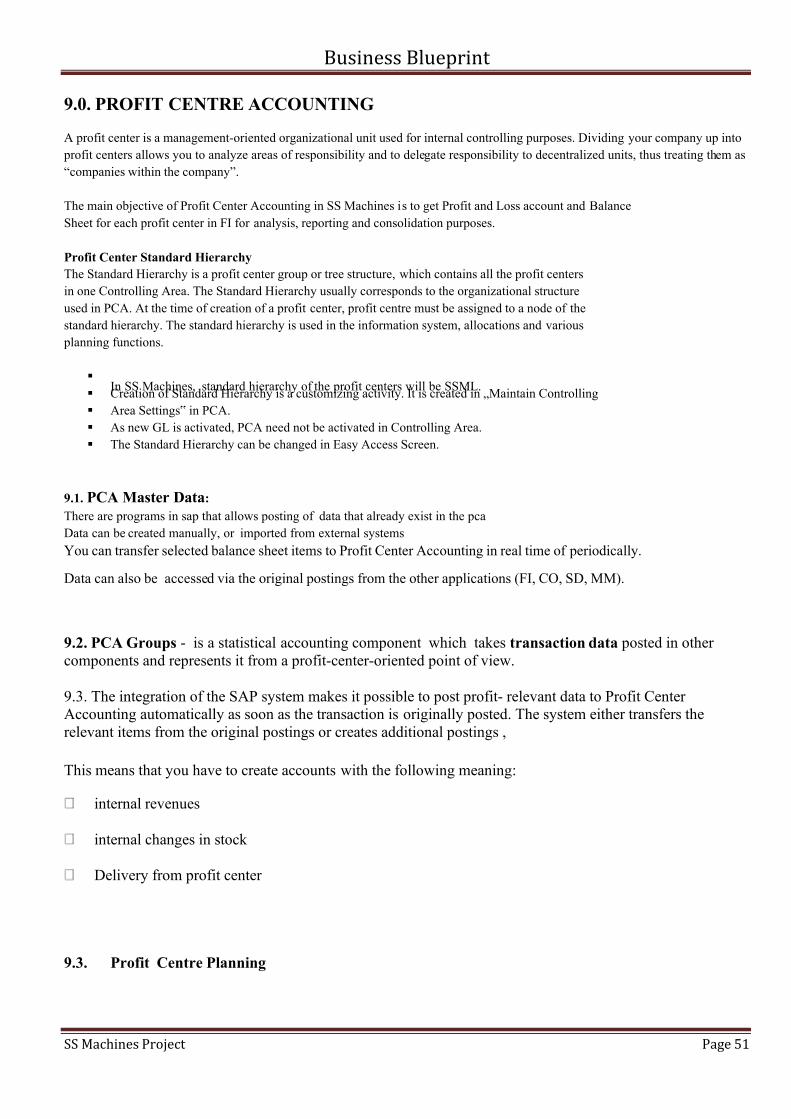

8.3. Period End Closing in Cost Centres…………………….……………………………………………49

9.0. PROFIT CENTER ACCOUNTING……………………………………………………………. 51

9.1. Profit Centres Master Data……..………………………………..…..…………………………….. 51

9.2. Profit Centres Group………………………………………………….……………………..…….. 51

9.2 Profit Centres planning………………………………………….………………………………… 52

10.0. MASTER DATA………………………………………………………………………………….. 53

10.1. General Ledger Master.……………………………..………………………………………………..53

10.2. Customer Master ……..………………………..……………………..……………………………. 54

10.3. Vendor Master ………………………………..…………………………………………………… 54

10.4. Asset Master ……………………………..……………………………………………..……………55

10.5. Bank Master ………..………………………..……………………………………………………….55

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 6/55

Business Blueprint

SS Machines Project Page 6

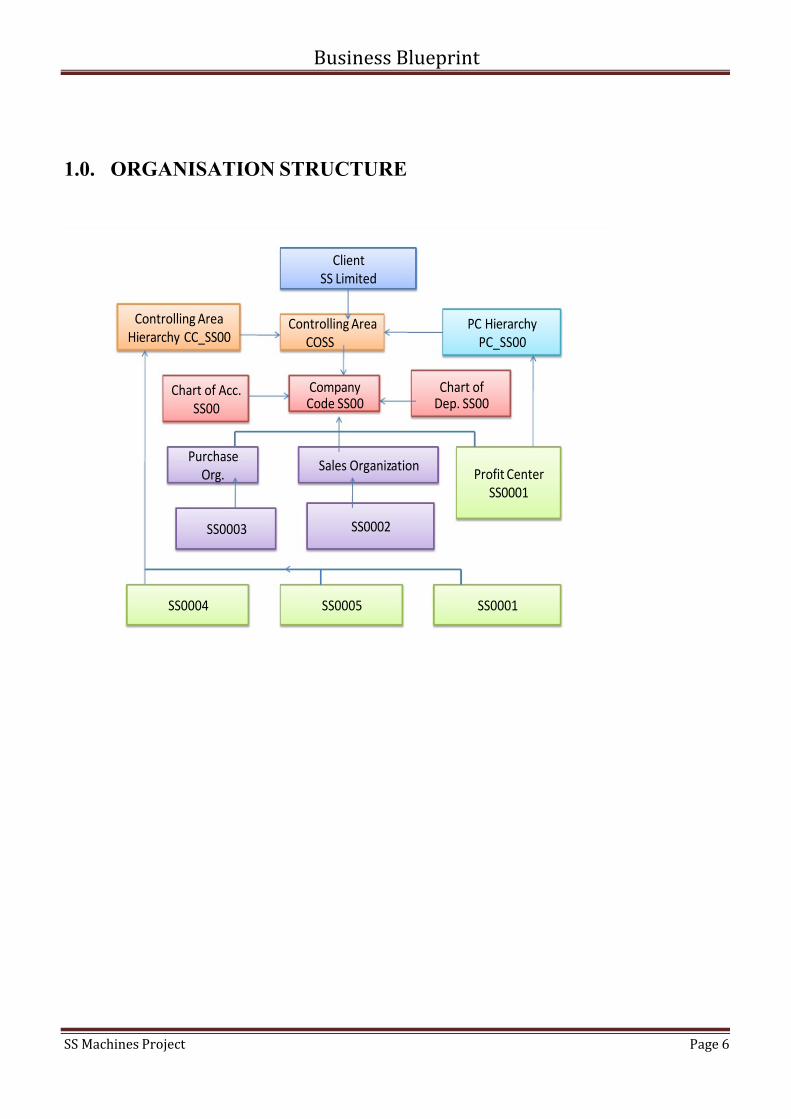

1.0. ORGANISATION STRUCTURE

Client

SS Limited

Controlling Area

COSS

Chart of Acc.

SS00

CompanyCode SS00

Purchase

Org.Sales Organization

Profit Center

SS0001

Controlling Area

Hierarchy CC_SS00

Chart of Dep. SS00

SS0003 SS0002

SS0001

PC Hierarchy

PC_SS00

SS0005SS0004

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 7/55

Business Blueprint

SS Machines Project Page 7

1.1 Client

Client is the highest level in the SAP hierarchy.

Specifications or data which will be valid for all organizational units in all SAP applications are entered at

the client level, eliminating the need to enter this information more than once (e.g. exchange rates).

Each client is a self-contained unit which has separate master records and a complete set of tables and data.

A client key is used automatically in all master records in background, which ensures that they are stored per

client.

Users must enter a client key and have a user master record in the client in order to log on to the system.

The Enterprise Structure in SAP Finance module consists of the following entities under Client:

Company

Company Code

Chart of Accounts

Chart of Depreciation

There will be one Client (SS01) for SS Machines.

1.2 Company

A Company represents a group of entities (one or more Company codes) in SAP. This entity is used for

consolidation of accounts of multiple entities (Company Codes). All company codes within a company can use the

same operational Chart of Accounts and the same Fiscal Year breakdown. However, the company code currencies

can be different.

1.3 Company Code

A Company Code represents an independent legal accounting entity in SAP. Balance Sheets and Profit/Lossstatements required will be created at the Company Code level. In other words, a company code is an organizational

unit for which a complete self-contained set of accounts can be drawn up for external reporting purpose. The process

of external reporting involves recording all relevant transactions and generating all supporting documents required

for financial statements.

Company Code Company Code Description

SS00 SS Machines Limited

1.4 Chart of Accounts (COA)

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 8/55

Business Blueprint

SS Machines Project Page 8

A Chart of Accounts is a classification consisting of a group of General Ledger (G/L) accounts under a

Client.

It provides a framework for the recording of values, in order to ensure an orderly rendering of accounting

data.

The chart of accounts contains the definitions of all G/L accounts in an ordered form.

The definitions consist mainly of the account number, account name, and the type of G/L account, that is,

whether the account is a P&L type account or a BS type account.

One or more Chart of Accounts can be created for the same Client

A Chart of Accounts can be used by one or more Company Codes.

The following COA will be maintained at company code level.

1.5 Group Chart of Accounts (GCOA)

The group Chart of Accounts contains the G/L accounts that are used by the entire corporate group. This allows the

company to provide reports for the entire corporate group.

There would be one group COA at SS01 (Client Level) and all other COA would be mapped to group COA for the

purpose of consolidation.

One group Chart of Accounts can be assigned to different charts of accounts as shown below:

1.6 Chart of Depreciation

A Chart of Depreciation is a list of depreciation areas like book depreciation as per The Companies Act of the

Kingdom of Bhutan, 2000. Chart of Depreciation is created in order to manage various statutory requirements for the

depreciation and valuation of assets. These Charts of Depreciation are usually country-specific and are defined

independently of the other organizational units. A Chart of Depreciation, for example, can be used for all the

company codes in a given country. A single Chart of Depreciation will be assigned to the company code SS00 and

the Chart of Depreciation will consists of the following depreciation areas:

01- Book Depreciation as per Income Tax Act of the United States of America, 2001.

10- Depreciation as per Company Policy.

15- Depreciation as U.S A, Tariff Determination Regulation, 2007.

20- Depreciation as per IFRS.

1.7 Controlling Area

The controlling area is the business unit where cost accounting is carried out. Controlling Area delimits the

company‟s managerial accounting operations. Organization structure is replicated in the controlling system. The

company code and controlling area uses identical chart of accounts, currency & business area. Cost centers, internal

orders, profit centers are used to classify the controlling area. All inter organizational allocations refers to objects

within the same controlling area.

SS Machines will have SS01 as its Controlling Area.

The following are the cost centers

SS0001 Administration

SS0002 Sales

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 9/55

Business Blueprint

SS Machines Project Page 9

SS0003 Production

SS0004 Management

SS0005 Miscellaneous

1.8 Cost Centers

Cost Center in SAP is an organizational unit within a company that is used to track where costs occurred within the

organization (i.e., as a cost collector).In other words, Cost Centers are responsibility areas for costs within the

organization. Cost Centers are logical units or functional areas or locations of a company.

Before cost center is created, a hierarchical structure (called Standard Hierarchy) is set up and assigned to the

controlling area. Once created, it cannot be deleted or changed in Controlling Area.

The Cost Center is the lowest node of the hierarchical structure.

A standard hierarchy (SS01) is to be assigned to the controlling area SSS0 and cost centers are created consideringthe company‟s overall operational structure.

1.9 Profit Centers

Profit Centers represent separate areas of operation/locations within an organization and can be used across

company codes.

They are balancing entities which are able to create their own set of financial statements for internal purposes.

Movements in value entered in Financial Accounting are assigned to Profit Centers. This entity is used for segmental

reporting by drawing P&L statement and Balance Sheet for a segment (typically a line of business or geographical

location).

Following are the Profit Centers

for SS01, Profit Center

Description

SSDUMMY Dummy Profit Center

SS0001 Profit Center Major

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 10/55

Business Blueprint

SS Machines Project Page 10

2.0. GENERAL LEDGERS

Definition:

A general ledger is a primary accounting record used by a business to keep track of all the financialtransactions the company makes. Debits and credits, are recorded, or "posted," in the general ledger,

regardless of whether or not they also post to a subsidiary ledger (sub-ledger), such as accounts receivable or

cash. These values can provide the information used to generate all of a company's financial statements. The

central task of G/L accounting is to provide a comprehensive picture for external reporting and accounting.

Recording is done for all business transactions (primary postings as well as settlements from internal

accounting) in a software system that is fully integrated with all the other operational areas of SS machines

ensuring that the accounting data is always complete and accurate. Accounts Payable, Accounts Receivable,

Asset etc., will be categorized as subsidiary ledgers.

The SAP General Ledger module provides the following functions for SS machines:

2.1 CHART OF ACCOUNTS (COA)

A Chart of Accounts is a classification consisting of a group of General Ledger (G/L) accounts under a Client.

Only one COA will be configured in SAP for Ss Machines, which is SS00 and it will perform the following:

Provide a framework for the recording of values, in order to ensure an orderly rendering of accounting

data.

The chart of accounts contains the definitions of all G/L accounts in an ordered form.

The definitions consist mainly of the account number, account name, and the type of G/L account, that

is, whether the account is a P&L type account or a BS type account.

One or more Chart of Accounts can be created for the same Client

A Chart of Accounts can be used by one or more Company Codes.

2.2 MASTER DATA

2.2.1 Definition

G/L account master records contain the data that is always needed by the General Ledger to determine the

account's function. The G/L account master records control the posting of accounting transactions to G/L

accounts and the processing of the posting data.

2.2.2 Use

Before you can make postings to a G/L account, you have to create a master record in the system for the

account.

2.2.3 Structure

G/L account master records are divided into two areas so that company codes with the same chart of accounts

can use the same G/L accounts.

· Chart of accounts area

The chart of accounts area contains the data that is valid for all company codes, such as the

account number.

· Company code specific area

The company code specific area contains data that may vary from one company code to another,

such as the currency in which the account may be posted.

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 11/55

Business Blueprint

SS Machines Project Page 11

2.2.4 Structure for SS machines

General Ledger master contains the following:

GL Naming Conventions

GL Number Ranges

Types of Accounts

Description and

Control Data

2.2.5 General Ledger Naming Convention

In SS machines, the naming convention of GL Accounts is done in such a way that the user can identify

whether the GL A/c is Asset or Liability or Income etc. as shown below:

1. 1000000000: Asset

2. 2000000000: Liabilities

3. 3000000000: Owners‟ Equity

4. 4000000000: Income

5. 5000000000: Expenses

6. 6000000000: Clearing Accounts

7. 9000000000: Initial Uploads

Points to be considered with respect to G/L accounts are:

Master records for each G/L account will be created and maintained at each company code level.

The master record contains information and controlling parameters which control the entry and

processing of business transactions in that G/L account.

G/L accounts will also be used for posting transactions from other modules of SAP.( MM / HCM/ SD,

Etc)

2.3 INTEGRATION

In the standard system, all business transactions that are posted to G/L accounts are updated in the general

ledger. Additionally, you can define further ledgers to which data can also be posted. To do this, you must

implement the Special Purpose Ledger [Ext.].

Chart of accounts SS00

Account number: 10000

Short text: Petty cash

USA

Company code: SS00

Currency: USD

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 12/55

Business Blueprint

SS Machines Project Page 12

2.4 COMPANY CODE SEGMENT The information, which is specific to a particular company, is maintained in the Company Code segment of

the General Ledger Master record. This data controls how one enters and processes business transaction data

in the appropriate account as well as how the account is managed within a Company Code. The company codeto be used for SS machines configuration is SS00

The following are some of the specifications which will be made for each G/L account:

Currency - account currency (USD)

Reconciliation Account for Account Type - to specify the control accounts for the sub ledgers.

Open Item Management - will be maintained for an account that requires open item management. Eg.Bank sub-accounts, GR/IR Clearing account, etc., are maintained in Open Item Management.

Line Item Display - will be retained for accounts for which line items are to be stored separately. Eg.

Bank main accounts, all expense accounts, all balance sheet accounts, excepting accounts which are of

the nature of reconciliation accounts

2.5 CURRENCY

For each Company Code, a currency must be specified. Accounts are managed in the Company Code

currency. All other currencies are indicated as foreign currency. The system converts the amounts

posted in a foreign currency into the Company Code (Local) currency. The currency defined in the

Company Code is known as the local currency within SAP. USD currency will be used for SS

machines.

2.6 ASSET MASTER

The Asset Accounting module contains master records that control how business transactions arerecorded and posted to the account. The Asset master record also contains all the data required to

manage company‟s Fixed Assets. Standard asset class will be used to configure SS machines

Following details will be maintained in the Asset Master for SS machines:

General Master Data

This part of the master record contains concrete information about the fixed asset.

The following field groups exist:

General information (description, quantity, etc.)

Posting information (for example capitalization date etc.)

Time-dependent assignments (for example cost center, custodian, etc)

Information on the origins of the asset

Insurance data

Depreciation areas [Each asset class is maintained with different depreciation areas as required for SSmachines.

2.7 Fiscal Year and Fiscal year Variant

To separate business transactions into different periods, a fiscal year with posting periods has to bedefined.

The fiscal year is defined as a variant which is assigned to the Company Code. Standard fiscal year variants are already defined in the system and can be used as templates. The fiscal year variant

contains the definition of posting periods and special periods.

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 13/55

Business Blueprint

SS Machines Project Page 13

Special periods are used for postings which are not assigned to time periods, but to the process of year-

end closing.

The fiscal year will consist of maximum of 12 posting and 4 special periods.

A fiscal year is defined as fiscal year variant which is then assigned to Company Code. One fiscal year

variant can be used by several Company Codes. The following are the available options for defining

fiscal year variants:

Fiscal year same as calendar year.

Fiscal year differs from calendar year (non-calendar fiscal year). The posting periods can also bedifferent to the calendar months.

The fiscal year variant that would be used by SS machines will be V3 (April to March)

2.8 Document Types

The document type controls the document header and is used to differentiate the business transactions to be

posted, e.g. Customer invoice, Vendor payments, etc. Standard document type will be used for SS machinesconfiguration.

Document types are required in SAP to create and post financial documents (e.g. Bank Payment

Voucher, Receipt Voucher etc.).

Document types are defined at the client level and are therefore valid for all company codes.

The standard system is delivered with document types which can be used, changed, or copied.

SAP has the standard Document Types, which will be adopted by SS machines.

The document number range defines the allowable range in which a document number must be

positioned and cannot overlap. SAP standard number range will be used by SS machines

The document number range has to be defined for the year in which it is used.

The system stores the last used document number from the number range in the field “current number”and takes the subsequent number for the next document.

2.9 Posting Key

Posting Key controls Debit or Credit account indicator for each line item.

The posting key also describes the type of transaction that is entered in a line item and allowable

account type, which will be entered for the respective line item.

SAP provides certain predefined posting keys. These predefined posting keys will be used wherever

applicable. For every posting key, properties control the entry of the line item.

For each Posting Key, a reversal-posting key may be defined. The reversal-posting key is used toreverse a document posted in Financial Accounting.

Posting keys Transaction Debit/Credit Account Types Reversal01 Invoice Dr D 12

02 Reverse Credit

Memo

Dr D 11

09 Special G/L

Debit

Dr D 19

11 Credit Memo Cr D 02

19 Special G/L

Credit

Cr D 09

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 14/55

Business Blueprint

SS Machines Project Page 14

21 Credit Memos Dr K 32

29 Special G/L

Debit

Dr K 39

31 Invoice Cr K 22

32 Reverse Credit

Memo

Cr K 21

39 Special G/L

Credit

Cr K 29

40 Debit Entry Dr S 50

50 Credit Entry Cr S 40

70 Assets Debit Dr A 75

75 Assets Credit CR A 70 Standard Account Types in SAP are as follows:

71 S-General Ledger

72 A-Assets73 K-Vendors

74 D- Customers

75 M- Materials

SS machines will use the Standard Posting Keys and the Account Types wherever applicable.

2.9.1 General Ledger Postings

The General Ledger forms the backbone of all the financial systems. General ledger is the main

accounting record of a business which uses double-entry bookkeeping. It captures all businesstransactions in FI and through integration with other operational areas of the company ensures that

accounting data is always complete and accurate.

General ledger is a comprehensive financial management solution that enhances financials controls,

data collection, information access and financial reporting. It is the central repository of all the

accounting information of the organization as on date. Most of the transactions will be handled in

respective sub-ledgers (Accounts Payable, Accounts Receivable, Assets) and subsequently

consolidated and posted to General Ledger. However, the module shall provide specific functions of

passing journal entries (Manual, Provisional, Recurring and Reversal Journals) and posting them,

which will be purely rectification and provisional in nature.

Essentially, the general ledger serves as a complete record of all business transactions of SS machines business. Actual individual transactions can be checked at any time in real-time processing by

displaying the original documents, line items, and transaction figures at various levels.

Features of GL Accounting

GL Account maintenance

Open item clearing

Foreign currency valuation

Recurring journal entry

Accrual/ reversal posting

2.9.2 Posting with Clearing

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 15/55

Business Blueprint

SS Machines Project Page 15

There are some GL accounts that need to be maintained as open item. Examples of GL Account to be

managed in open items are-

- Bank clearing accounts,

- Clearing accounts for goods receipt/invoice receipt

- Salary clearing accounts.

By posting with clearing, system clears the open item in the account.

2.9.3 Document ReversalIt is possible for a user to make an input error. As a result, the document created will contain incorrect

information. In order to provide an audit of the correction, the user must first reverse the document in error,

and then capture the document correctly.

The system provides a function to reverse G/L, A/R and A/P documents both individually or in mass.

When reversing a document, a reversal reason code must be entered to explain the reason for reversal.

The reason code also controls if the reversal date is allowed to be different from the original posting

date.

SS machines can use standard reversal reasons or can define its reasons.

Documents with cleared items cannot be reversed. The document must first be reset.

Some standard Reversal Reasons;01 - Reversal in current period

02 - Reversal in closed period

05 - Accrual

06 - Asset transactions reversal

07 - Incorrect document date

However, it needs to be noted that reversal of any document will affect the allocation cycles in case if these processes are completed. It will be required to re-run all these cycles once again after reversing the document.

2.10 Accounts Groups

The account group is a summary of accounts based on criteria that effects how master records are created.

The account group determines:

The number interval from which the account number is selected when a G/L account is created.

Use:

When you create a G/L account in the chart of accounts area, you must specify an account group.

Liabilities – 100000 series

Assets – 200000 series

Owner‟s equity 300000 series

Income – 400000 series

Expenditure – 500000 series

Clearing – 600000 series

Initial Uploads – 900000 series

The above sub-modules are integrated to FI-G/L via the “field reconciliation for account type” in thecompany – code specific segment of GL master. With this indicator, the G/L account can only be

posted via respective sub-ledger in SAP. Different indicators for „reconciliation for account type‟ are:

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 16/55

Business Blueprint

SS Machines Project Page 16

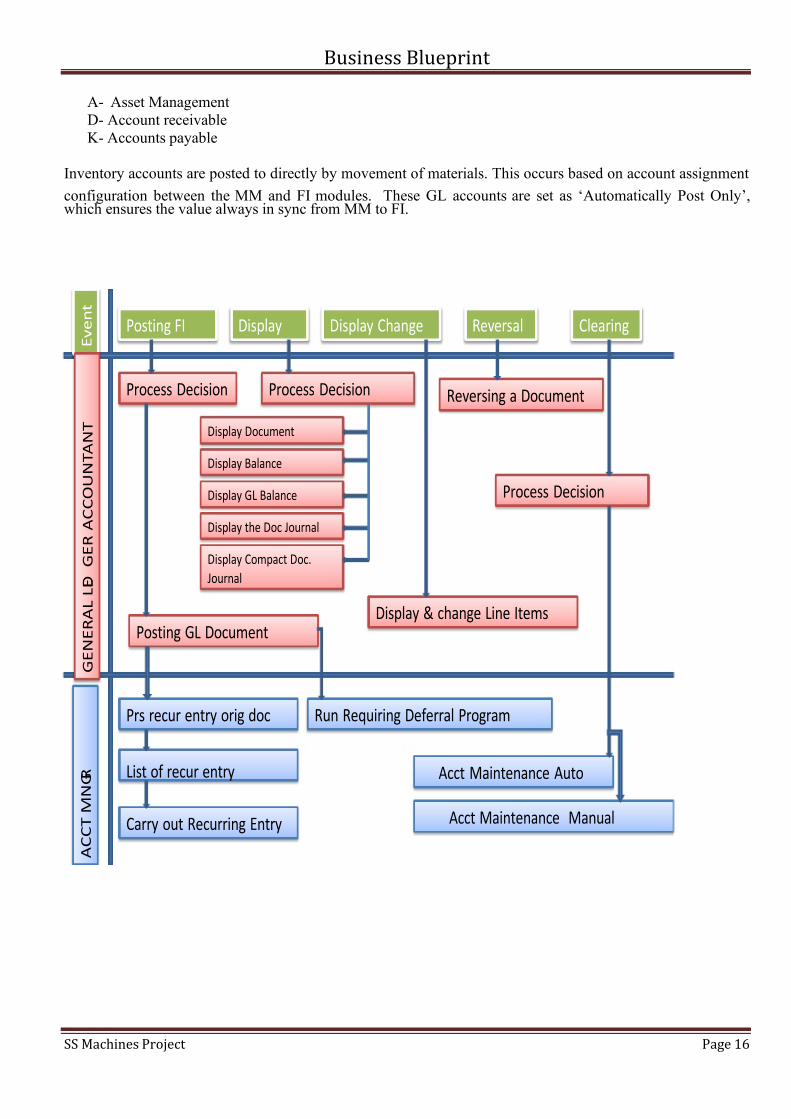

A- Asset Management

D- Account receivable

K- Accounts payable

Inventory accounts are posted to directly by movement of materials. This occurs based on account assignment

configuration between the MM and FI modules. These GL accounts are set as „Automatically Post Only‟,which ensures the value always in sync from MM to FI.

E v e n t

G E N E R A L L E D

G E R A C C O U N T A N T

A C C T M N G R

Posting FI Display Display Change Reversal Clearing

Process Decision

Posting GL Document

Prs recur entry orig doc

List of recur entry

Carry out Recurring Entry

Process Decision

Display Balance

Display GL Balance

Display & change Line Items

Reversing a Document

Process Decision

Acct Maintenance Auto

Acct Maintenance Manual

Run Requiring Deferral Program

Display Document

Display Compact Doc.

Journal

Display the Doc Journal

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 17/55

Business Blueprint

SS Machines Project Page 17

3.0. ACCOUNTS PAYABLES

“Accounts Payable” , a sub module under Financial Accounting (FI) , takes care of Vendor related transactions as the module is

tightly integrated with the purchasing transactions arising from the „ procurement Cycle.‟

Based on the nature of different transactions involved like payables and down payments etc., different GL accounts will be affected.

For open items in Account payables, the system contains due date forecasts and other standard reports that can be used to monitor

open items.

Features of Accounts Payable

Vendor master maintenance

Advance payment tracking & settlement

Non- P.O Invoice Processing

Credit/Debit memo processing

Automatic & manual payment program

Open Item * GR/IR Clearing.

Balance confirmations, accounts statements, and other forms of reports to suit requirements in business correspondence

with vendors.

Vendor- Customer Cross adjustments.

The relationship between Customer and Vendor Accounts

3.1. Vendor Master Data

The accounting department uses some data (customer/vendor) that remains unchanged for long periods of time & that is often

referred to by other data. That is called Master Data.

The AP component contains Vendor master records that control how business transactions are recorded & posted to the account.

The master record is used not only in Accounting but also in Materials Management.

3.1.1 General Data:

This data is contained at the client level and can be accessed throughout the whole organization. This data applied to whole purchase

organization in the company. The general data includes example of customer‟s name, address, language, telephone, payments

transactions etc.

3.1.2 Company Code Data:

It is created at the CC level. Any Cc that wishes to do business with that Vendor has to create a CC segment for that vendor. The

data includes , for example , the reconciliation account number and terms of payments, Correspondence, insurance information etc.

3.1.3. Purchase Organization Data:

This data is relevant to the purchase organizations and distribution channels of the company. Data that is stored in this area includes,

for example, data on order processing, shipping, & billing.

General Data ( Client level)

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 18/55

Business Blueprint

SS Machines Project Page 18

Following CC details are maintained by Finance for SS Limited ( CC SS00)

General Details Name, Address etc.

Reconciliation Account for Vendors This Reconciliation Account is the General ledger for the Accounts

Payable sub - ledger

Withholding Tax Details TDS details of Vendors are maintained here.

Payments Terms Terms of Payment (

House Bank If vendor is always paid through the same same Bank, this field needs to

be maintained.

Customer Code If the Vendor is also a Customer

Payment Terms/ method The mode of Payment through which Vendor will be paid.

Payment Block It prevents you from paying “ Open Items” . It is usually maintained in

the “payment Block” field in a Vendor Master record or directly in the

open line item.

Tolerance for Vendors It is group that deals with the differences arising out of accounting

transactions and to instruct the system on how to proceed further. Once

defined, each vendor/ customer is assigned o once of these groups. We

can also define “ permitted payment differences”

3.2 Vendor Accounts Groups

A vendor account group is used to group together vendors by some criteria. E.G. a business may have different account groups for

international, domestic and one-time vendors. Similar settings can then be defined once and used for all the vendors in the same

vendor account group.

The account group is a classifying feature within vendor master records. The account group determines: the number

interval for the account number of the vendor,

whether the number is assigned by the user or by the system,

Which specifications are necessary and/or possible in the master record?

Vendor Account Group

Account Groups Number range

Regular vendors( SSRV)

100000 to 149999

One Time Vendors

(SSOT)

1500000 to 199999

Company Code

data Segment

Purchase

Organization

Data Segment

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 19/55

Business Blueprint

SS Machines Project Page 19

Customer Accounts/

vendor Customers

(SSVC)

2000000 to 249999

3.2.1 Number range for Vendors:

Number Ranges for Vendor Account Groups Definition: Identifies a number range interval within an object or sub object.

A unique number is assigned to each business partner master record. You can use this number to access the master record,

or to refer to the business partner when processing business transactions.

A number range can be valid for more than one account group. You can use the number range to assign different numbers

to a head office and subsidiaries.

The number for a business partner master record can be assigned in one of the following ways:

I. Externally: You assign the number. In this case, you define a number range that allows for alphanumerical number

assignment. The system checks whether the number you enter are unique and within the number range defined by the

account group.

II. Internally: The system assigns a consecutive number automatically from a number range defined by the account group.

SS Machines: Standard SAP Internal Number range

3.3. Payment methods:

Payment methods have 2 parts: country specific settings and firm code specific settings. This section particulars the essential

requirements and specs for payment strategies for each country.

Within the type knowledge area, specify the name of the SAPScript type for payment media

Bank Advice

Dd/TT

Check

E- Payment

Cash/LC etc.

3.3.1. Payment terms:

Key for defining payment terms composed of cash discount percentages and payment periods. It is used in sales orders,

purchase orders, and invoices. Terms of payment provide information for: “Cash management”, “ Dunning procedures”,

and “Payment transactions”.

Terms of payment can be defined for each vendor which will be updated in each Vendor Master and defaulted in the P.O.

Terms of payment will define the credit period, due date and cash discount, if applicable. The due date will calculated from

the baseline date as per payment terms, which will be either of following dates:

Document date

Posting Date

SS Limited Payment terms:

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 20/55

Business Blueprint

SS Machines Project Page 20

1. 30 Days 2. 45 Days 3. 60 Days 4.120 Days.

3.4. Vendor Tolerance Group:

Freely definable group code for customers and vendors, or G/L accounts. Tolerance groups are unique within a company

code. Each tolerance group contains settings that affect cash discount and payment difference processing. These settings

become effective during payment entry.

You can use the tolerance level to set a percentage or absolute tolerated difference between the transmitted value and the

open value. If the difference exceeds the tolerance limit, a new open item is created.

The system compares the value transmitted with the value that is still open in the internal invoice for the delivery. You can

set tolerance limits at delivery and/or item level (material.) If the tolerance limit is not violated, no new open item is

created.

SS Limited Tolerance for Vendors:

Max- 999999 USD 10%

3.5. Vendor Reconciliation Accounts:

The reconciliation account ensures the integration of a Sub ledger account into the general ledger. When you post items to a

subsidiary ledger, the system automatically posts the same data to the general ledger. Each subsidiary ledger has one or

more reconciliation accounts in the general ledger. We can‟t use reconciliation account for direct posting.

3.5.1. Alternative Reconciliation Accounts:

The reconciliation account in G/L accounting is the account which is updated parallel to the sub ledger account for normal

postings (for example, invoice or payment).

For special postings (for example, down payment or bill of exchange), this account is replaced by another account (for

example, 'down payments received' instead of 'receivables'). The replacement takes place due to the special G/L indicator

which you must specify for these types of postings.

3.6. Taxes

SAP allows the consideration of fol taxes:

a. Tax on sales and purchases b. US sales tax

c. Additional taxes(country-specific, for example, investment tax in Norway, clearing tax in

Belgium)

d. Withholding tax

Tax on Sales and Purchases

Tax on sales and purchases is the balance of two: Output tax & Input Tax

I. Output tax: levied on net value of goods sold and is billed to customer; It‟s a liability of CC to tax authorities.

II. Input Tax: levied on net invoice amount billed by vendor; It‟s a receivable which CC claims from tax authority.

3.7. Payment Block:

Some invoices can have pymt block.

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 21/55

Business Blueprint

SS Machines Project Page 21

payment items can be temporarily blocked in the proposal by manually assigning a payment block .The doc incl in the payment

run have been locked against any other posting like paid manually or in another payment run.

If the problem arises during I nvoice Verif ication process , the invoice is usually blocked for pymt. If there is a reason why a

Vendor shouldn‟t be paid, you can create a pymt block in in the master data. When an AP invoice is enters it can be blocked f or

pmt.

The type of pymt block determines whether it can be removed during the pymt proposal.We can define additional pymt block in the system.

User can also specify whether the pymt block can be removed when pymts are processed.

SS Machines Ltd uses these Codes for Payment Block:

A Blocked for Payment

B Blocked for Payment

N Post process inc. Payment

P Payment request

R Invoice Verification

S Other reasons(1)

V Payment Clearing

3.8. Automatic Payment program:

The payment program is designed so that both outgoing and incoming payments can be processed. These functions are

supported for payment transactions with vendors and customers and between bank accounts.

All the common payment procedures are in the standard system or can be set up within Customizing. All default values used in

the payment program are required in the following.

The payment program processes domestic and foreign payments for vendors, customers and between bank accounts. It

generates the payment program and provides the data for the payment medium programs. These ABAP programs print a

payment list, payment forms (e.g. checks) or generate data media such as magnetic tape or disk. A further possibility is the

distribution of payment data to a central system via ALE.

3.8.1. There are 4 steps to the cost process:

1. Parameters : In this step, the next questions are requested and answered:

Who is going to be paid?

What fee methods will seemingly be used?

When will they be paid?

Which company codes will be thought-about?

How are they going to be paid?

1. Proposal: Once the parameters have been specified, the proposal run is scheduled and it produces a listing of business

companions and open invoice es which would possibly be due for payment. Invoices might be blocked or unblocked for

payment.

2. Program: As quickly as the payment list has been verified, the cost run is scheduled. A cost doc is created and the overall ledger

and sub-ledger accounts are updated.

3. Print: The accounting capabilities are accomplished and a separate print program is scheduled to generate the payment media.

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 22/55

Business Blueprint

SS Machines Project Page 22

The main payment program configuration menu has push buttons for each area. To be sure that the configuration is complete,

work from left to proper by every push button. The primary three areas would require minimal configuration changes. Thestandard system incorporates the frequent payment strategies and their corresponding varieties, which have been definedseparately for each country.

3.9 House Bank Definition

Checks supplied by a bank or a printing shop are usually divided into lots, since they may be written (issued) or printed at various

different locations. In the SAP System, a check number range represents a batch (lot) of numbered checks.

In the Financial Accounting Configuration menu, you must define check lots (number ranges) that correspond to the actual check

lots (in the printer, the safe, or your employees' desks). The print program uses this number range to link the check with the

payment.

SS Limited Bank: Citi bank

Accounts Account Number

Bank Account 1 123457893Bank Account 2 234568975

Bank Account 3 568975698

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 23/55

Business Blueprint

SS Machines Project Page 23

4.0. ACCOUNTS RECEIVABLES

The Accounts Receivable SAP FI sub module records and manages accounting data of all customers. It is an integral part of sales

and distribution management. All postings in Accounts Receivable are recorded directly in the General Ledger and updated in

different General Ledger accounts based on the transactions involved - i.e advance receipts, bank guarantees and down payments

etc.

There are a range of tools available for documenting the transactions that occur in Accounts Receivable, including account balance

lists, journals, balance audit trails, and other standard reports.

In an organization, FI- AR and SD use the customer master records. The customer master records are stored and updated centrally to

reduce inconsistency and maintain data integrity.

Features of Account Receivables

Customer master maintenance

Customer down payment processing

Dunning, Balance confirmation etc

Clearing of incoming payment against Customer invoice

There are also a range of tools that can be used to monitor open items, such as account analyses, due date lists etc.

4.1. Customer Master Data

The Customer Master data is the core data that contains all the information essential for carrying out business transaction with a

customer.

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 24/55

Business Blueprint

SS Machines Project Page 24

The customer master data structure map

The customer Master Data comprises of three main sections:

General DataThe general data includes - the customer's name, address, language and telephone data. This is the general data that applies to every

sales organisation in a company.

Company Code Data

This is data that is specific to an individual Company Code. The information stored in this area includes - Accounting clerk, the

reconciliation account number, terms of payment and dunning procedure.

Sales Area Data

This is data relevant to the sales organizations and distribution channels of a company. Data that is stored in this area includes -sales order processing, shipping and billing, terms of payments.

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 25/55

Business Blueprint

SS Machines Project Page 25

4.2. Customer Accounts Groups

Customer account group is a classification or grouping of customers based on the characteristics of the groupings. A customer

account must be assigned to an account group. The account group ensures that only the relevant screens and fields are displayed andready for input for each of the customer‟s different functions. For example, the address, communication, and bank data fields are

omitted for the account group for one-time accounts.

The customers are classified into two categories based on the data requirement & maintenance:

Customers for sale of Products and services the customers who buy products and service from SS Machines company will

be created in S&D module.

Other Customers: These are one time, occasional customers for sale of SS Machines products, parts and miscellaneous

sales.

Following details will be maintained by SS Machines Finance Department

General Details Name, Address, Tel contact etc.

Reconciliation Account for the Customer Reconciliation Account No. for Customer.

Withholding Tax Details Tax sales details for the Customer

Payment Terms Terms of Payment

Account Group One time, Domestic & Foreign Customers

Vendor Code Customer is also a Vendor

SS Machines company will use the following account Groups:

Group Customer Groups names

0001 Domestic Customers

0002 Foreign Customers

0003 One Time Customers

0004 Customer is also a vendor

4.3. Payment terms

The following Payment Terms exist currently in legacy and will be created in SAP.

PlantPTC BPC

SS Machines Plant45 days 30 days

60 days 30 days

120 days 30 days

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 26/55

Business Blueprint

SS Machines Project Page 26

4.3.1. Numbering Master Records

The customer master record number will be assigned internally the system and the system ensures that the numbers assigned are

always unique. With internal assignment, the system selects the next number from the interval and therefore, no duplication of

numbers. With external assignment, the system prevents entering the same number twice. A customer identification key will besame in all Company Codes.

SS Machines company will use the following account Groups number ranges:

Group Customer Groups names Number Ranges Number Assignment

0001 Local Customers – Sold to 0000001000 - 0000001999 Internal

0002 Foreign Customers Receivables- Ship to 0000002000 - 0000002999 Internal

0003 Customer/Vendor - Bill to 0000003000 - 0000003999 Internal

0004 Inter Company Receivables - Payer 0000004000 - 0000004999 Internal

0005 One time Customer – OTC – Tax Refundable 0000005000 - 0000005999 Internal

4.3.2. Reconciliation Accounts

A reconciliation account must be specified in the master record so that all postings made to a subsidiary ledger are also posted to the

general ledger.

Currently SS Machines is billing to foreign and domestic customers. In SAP, the processes related to sales are routed through Salesand Distribution Model (SD). The GL accounts for foreign customer and domestic customer is maintained in SD module using

pricing condition. Whenever billing happens from SD, revenue accounts and customer accounts are determined automatically and

posted to FI.

The FI module is integrated with the SD module by defining the account determinations in the SAP system. Sales activities

leading to financial implications automatically update the respective Customer & G/L accounts.

Asset / Material disposal will be routed through SD module and corresponding accounting entry will be posted in FI. If the

disposal is with the Customer, customer master will be created. Sales order will be created in SD for the selected customers

against approved materials.

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 27/55

Business Blueprint

SS Machines Project Page 27

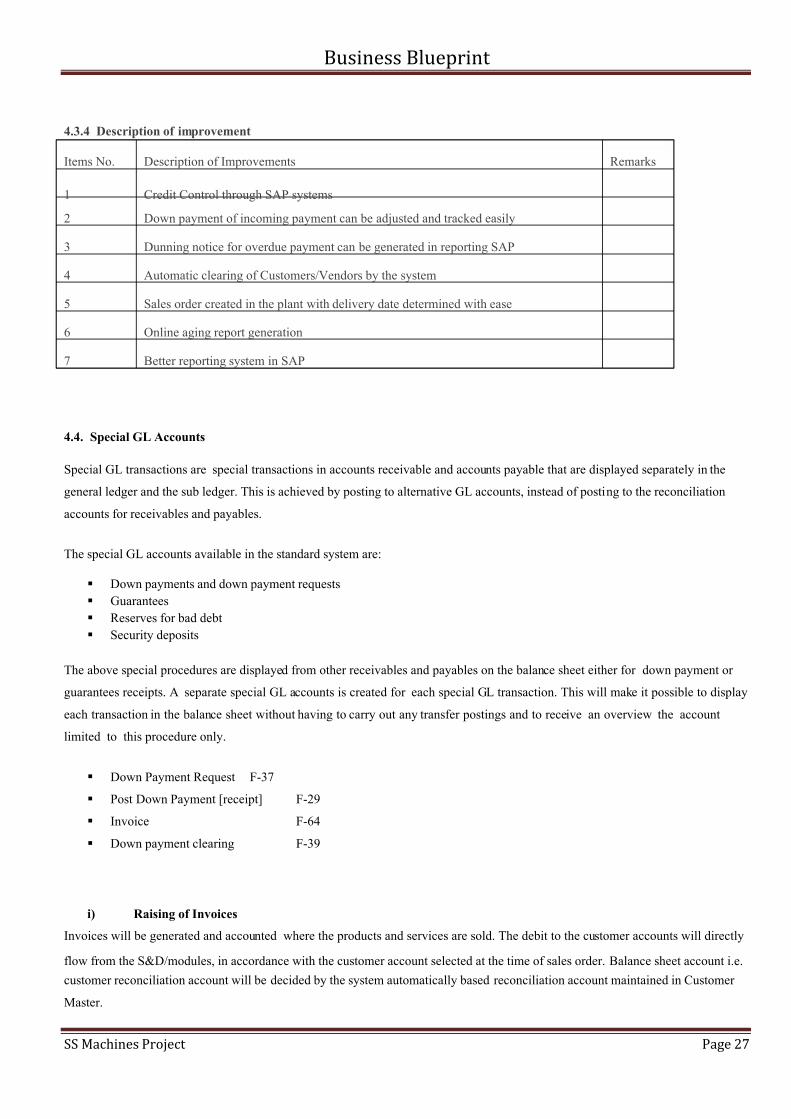

4.3.4 Description of improvement

Items No. Description of Improvements Remarks

1 Credit Control through SAP systems

2 Down payment of incoming payment can be adjusted and tracked easily

3 Dunning notice for overdue payment can be generated in reporting SAP

4 Automatic clearing of Customers/Vendors by the system

5 Sales order created in the plant with delivery date determined with ease

6 Online aging report generation

7 Better reporting system in SAP

4.4. Special GL Accounts

Special GL transactions are special transactions in accounts receivable and accounts payable that are displayed separately in the

general ledger and the sub ledger. This is achieved by posting to alternative GL accounts, instead of posting to the reconciliation

accounts for receivables and payables.

The special GL accounts available in the standard system are:

Down payments and down payment requests

Guarantees

Reserves for bad debt

Security deposits

The above special procedures are displayed from other receivables and payables on the balance sheet either for down payment or

guarantees receipts. A separate special GL accounts is created for each special GL transaction. This will make it possible to display

each transaction in the balance sheet without having to carry out any transfer postings and to receive an overview the account

limited to this procedure only.

Down Payment Request F-37

Post Down Payment [receipt] F-29

Invoice F-64

Down payment clearing F-39

i) Raising of Invoices

Invoices will be generated and accounted where the products and services are sold. The debit to the customer accounts will directly

flow from the S&D/modules, in accordance with the customer account selected at the time of sales order. Balance sheet account i.e.

customer reconciliation account will be decided by the system automatically based reconciliation account maintained in Customer

Master.

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 28/55

Business Blueprint

SS Machines Project Page 28

ii) Sales Accounting

Accounting documents for all customer transactions originating from SD and other receivables will be generated automatically in

the system in all cases.

iii) Delivery

Based on the customer sales order, delivery is created in Sales. The last step in shipping is posting of goods issue, which results in a

material document and an accounting document being created in the background. Apart from reduction in the quantity, it reduces the

inventory and debits the Cost of Goods Sold account.

Dr. Cost of Goods sold

Cr. Inventory

iv) Invoices

With reference to the delivery, a sales invoice will be created in SD, which will be posted to FI as follows:

Dr. Customer Account

Dr. Discounts (if applicable)

Cr. Sales Revenue Account

Cr Accrual commissions (Collection commission)

The customer reconciliation account is derived from the customer master as explained in the previous chapter.

v) Advance Invoices- will be handled as a Performa invoice with no effect in the customer account balance, and the

payment for this invoice will be handled as a down payment. This down payment will be cleared against the actual

invoices.

Advance invoices will be linked to the actual delivery and the actual invoice, to be able to know the remaining amount from those

invoices, and a customized report will be generated to show the history for them.

V1) Posting a Credit Memo with Reference to the Invoice

Posting a Credit Memo will be processed with Reference to the Invoice in Sales and Distribution if the Sales and Distribution (SD)

component is in scope. This ensures full integration of the sales and distribution and accounting/controlling functionality.

Posting of sales returns credit memo from SD will cause the following entries:

Dr. Sales Revenue

Dr. Accrued interest

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 29/55

Business Blueprint

SS Machines Project Page 29

Cr. Customer Account

Cr. Discount (If Applicable)

4.5. Dunning Notice (Reminder letter)

The credit department will process a complete and continuous follow-up of outstanding debts for business whenever customer payments are not fulfilled, after the delivery of goods and services or drawn automatically using direct debit.

4.5.1. Correspondence with customers

The dunning system in SAP enables you to handle the process from, for outstanding customer accounts that have not been settled.

4.5.2. Credit Limit

SS Machines will use the credit management component to set the desired credit limit for their customers and the customer will be

blocked automatically if they exceed their credit limit amount only. Accounts Team can also block customer manually.There will

be credit check, in quotations, sales order , delivery , billing .

4.5.3. Customer Payment

Different payment methods exist in SAP. The customer payments can be processed using the following different methods:

C = Incoming Check

T = Bank Transfer in

Cash Deposit

4.6. Customer is also a Supplier/ Vendor

If a customer is also a vendor, or vice versa, there can be the payment program and the dunning program to offset the customer and

vendor open items against each other. For this, Customer Vs Vendor relation will be maintained if required and the incoming and

outgoing payments will be automatically adjusted by the systems.

User can also select the vendor line items at the time of display of the customer/vendor line items for this account. Before clearing

items between a vendor and customer account, it is a requirement to:

Create a customer master record for the vendor that is also a customer

Enter the vendor account number in the Vendor field in the control section of the general data

in the customer master record.

Enter the customer account number in the Customer field in the control section of the general

data in the vendor master record.

Choose Clearing with vendor and clearing with customer in the company code data in

both the customer and vendor master records. In this way, each company code can decide

separately whether it needs to offset the customer against the vendor.

4.6.1. Clearance - Customer Vendor Cross Clearing Transactions

For customer/vendor processing a clearing transaction for incoming/outgoing payment or account maintenance, the system will

select the open vendor items automatically, provided that the vendor number is entered in the customer master record and the

clearing with Vendor indicator has been set. The same rule applies for a vendor that is also a customer during a clearing transaction.

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 30/55

Business Blueprint

SS Machines Project Page 30

There are two options for clearing available -

Automatic clearing program

Manual clearing

Automatic Clearing of Open Items in Customer Accounts

The company can periodically clear open customer account items if credit memos have been created for invoices.

Manual Clearing of Open Items in Customer Accounts

Clearing of open customer items. If the balance of the items to be cleared is not 0, a residual items can be created, for example for

overpayments/underpayments.

The main processes under account Receivables are:

Sales Order receipt

Invoice

Incoming payment from customers

billing Report

4.7. Accounts Receivable Business Process in SS Machines

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 31/55

Business Blueprint

SS Machines Project Page 31

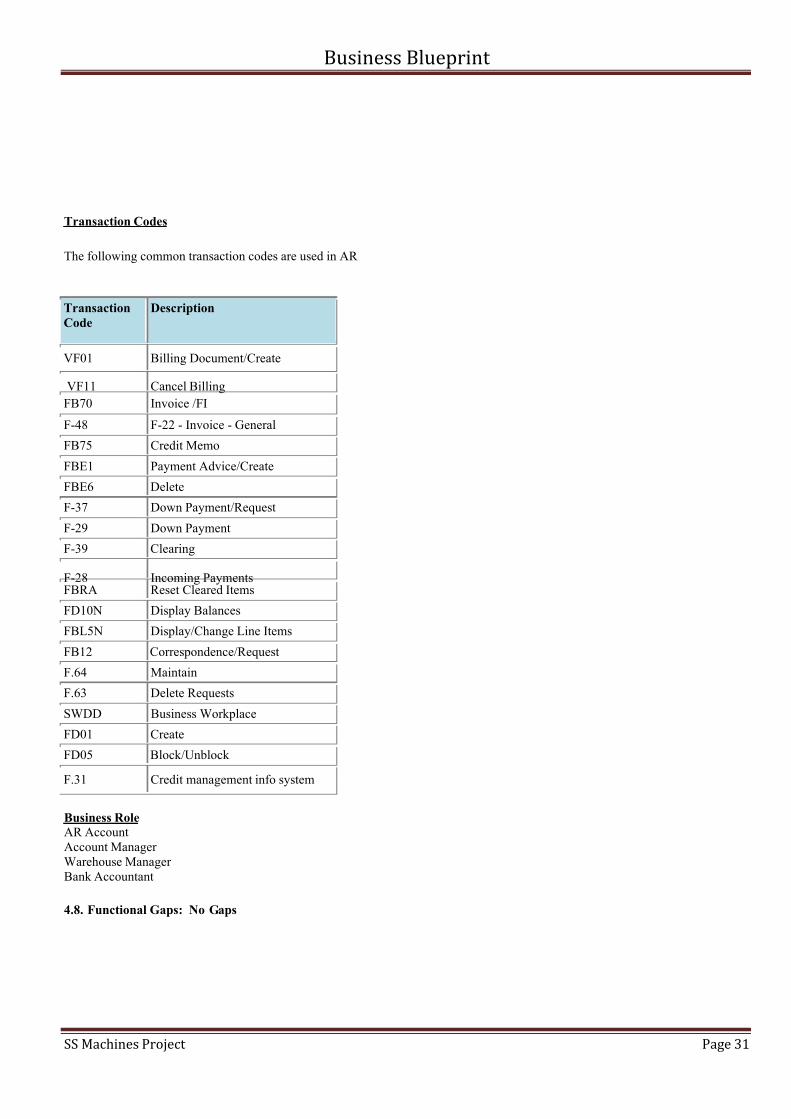

Transaction Codes

The following common transaction codes are used in AR

Transaction

Code

Description

VF01 Billing Document/Create

VF11 Cancel Billing

FB70 Invoice /FI

F-48 F-22 - Invoice - General

FB75 Credit Memo

FBE1 Payment Advice/Create

FBE6 Delete

F-37 Down Payment/Request

F-29 Down Payment

F-39 Clearing

F-28 Incoming PaymentsFBRA Reset Cleared Items

FD10N Display Balances

FBL5N Display/Change Line Items

FB12 Correspondence/Request

F.64 Maintain

F.63 Delete Requests

SWDD Business Workplace

FD01 Create

FD05 Block/Unblock

F.31 Credit management info system

Business Role

AR Account

Account Manager

Warehouse Manager

Bank Accountant

4.8. Functional Gaps: No Gaps

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 32/55

Business Blueprint

SS Machines Project Page 32

5.0. BANK ACCOUNTING

It includes the management of bank master data; cash balance management, and the creation and processing of incoming and

outgoing payments. Bank Accounting is part of FI but master data related to bank are taken from Cash Management. The Cash

Management deals with Cash Position, Liquidity Forecast and Bank Reconciliation aspect. Currently we are considering Bank

Master Data and Bank Reconciliation for the scope

IMPLEMENTATION SCOPE

Area To Be Process Related R/3 Functions

Bank Accounting Bank Master Data Bank Master Data

Bank Reconciliation Bank Reconciliation

5.1. Bank Master Data

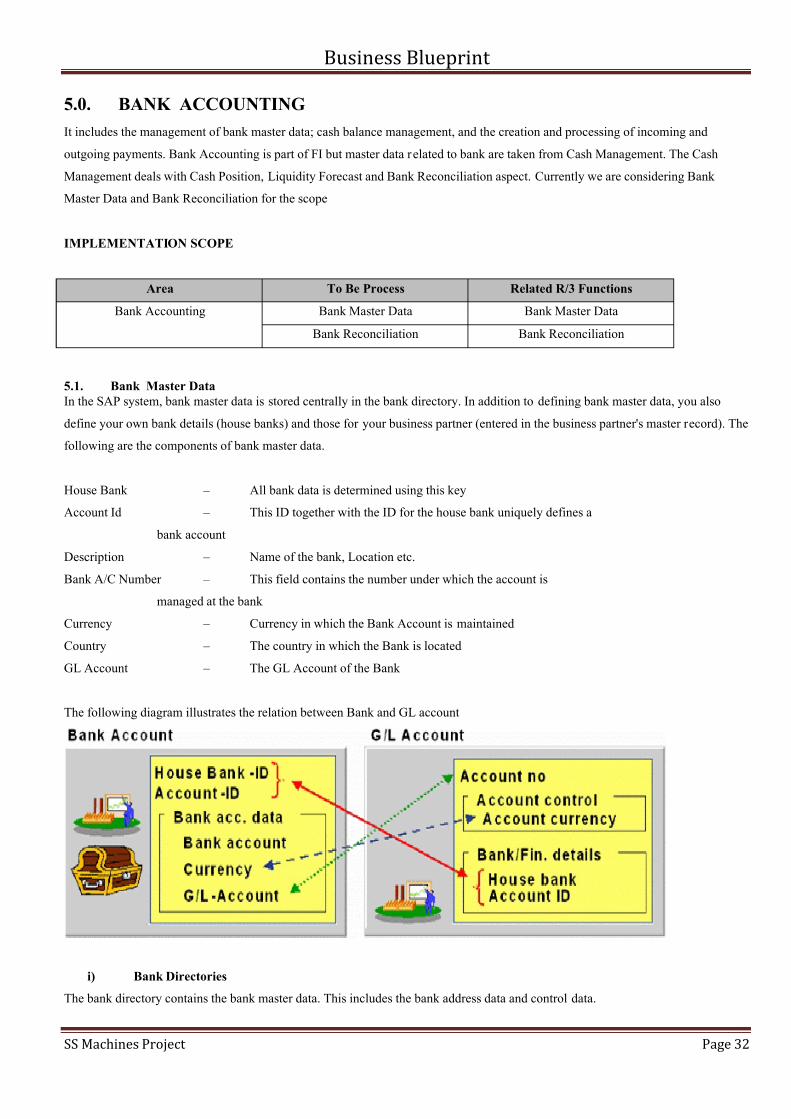

In the SAP system, bank master data is stored centrally in the bank directory. In addition to defining bank master data, you also

define your own bank details (house banks) and those for your business partner (entered in the business partner's master record). The

following are the components of bank master data.

House Bank – All bank data is determined using this key

Account Id – This ID together with the ID for the house bank uniquely defines a

bank account

Description – Name of the bank, Location etc.

Bank A/C Number – This field contains the number under which the account is

managed at the bank

Currency – Currency in which the Bank Account is maintained

Country – The country in which the Bank is located

GL Account – The GL Account of the Bank

The following diagram illustrates the relation between Bank and GL account

i) Bank Directories

The bank directory contains the bank master data. This includes the bank address data and control data.

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 33/55

Business Blueprint

SS Machines Project Page 33

The bank directory must contain the master data for all the banks that you require for payment transactions with your business

partners

ii) Bank Details

To be able to run the payment program, the system requires details on your own bank, and these details must be entered in the

customer and vendor master records. In the company code-specific data of a vendor master record, you could for example enter the

house bank from which payment is to be made to this vendor. If you do not enter a bank in the master record, you must specify the

rules by which the payment program determines the bank. The data that you enter is the same in both cases- an ID code for your

bank.

iii) House Bank

A list of house bank represents the bank in which the company uses for its outgoing and incoming payments. SAP will then refer

to this list maintain in table BNKA for its automatic payment program as well as to forecast bank balances with SAP

treasury function .

These lists are maintained at the company code level and each house banks are given a user defined bank ID that can be

alphanumeric. For this implementation, bank list will be maintained in all company codes, List o f bank o f various

company codes has to be obtained and customized. The house banks will be created for every main and branch bank.

iv) The naming conventions for the bank ID are base on these logics:

Use the first letter of the bank name and the first letter for bank as acronyms which described the house bank. The graph

below illustrates acronyms for Citibank. The last two digit of the house bank will use 00 to denote first bank l isted in the

system. Therefore for Citibank, it can have up to 100 branches entered in the system using the CB convention. It isrecommended to use 00 to identify the main bank of the company.

Example:

CB000 - Citibank Main Branch

CB001 - Citibank New York City

CB002 - Citibank Washington DC

Bank accounts are maintained for every house banks using a unique bank ID. This bank ID is used to enter specification

for bank payment and general ledger master records.

v) Bank Account ID

Each bank ID is unique within a company code. For each bank, enter the bank country, and either the bank number or an

appropriate country-specific key. The system uses this information to identify the correct bank master data .

5.2. GL Account

A G/L master record is created for each bank account. One bank account will have a corresponding two bank clear ing accounts,

i.e. outgoing and incoming payment.

The benefit of having two bank clearing accounts is that it helps to simplify processing of electronic bank statements

5.3. House Bank and Bank Account Creation

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 34/55

Business Blueprint

SS Machines Project Page 34

There are two key master data types in Cash Management, namely the house banks and the bank accounts. The critical information

required to set up these master data include bank name, bank key, bank branch and bank address.

The use of the bank account G/L structure can be seen through the following example.

When the company executes the payment program and makes payments for open payables, the following post ings take place:

Dr

Vendor AP account

Cr

Outgoing clearing account (G/L AccountXXXXXX 02)

This amount will remain in the outgoing clearing account until it clears the bank. Once the outgoing payments clear the bank, the

following postings take place:

Dr

Outgoing clearing account

Cr

Main bank G/L account

5.3.1. Bank Data Accounting Process

Requirement and Expectation

There is need for accounting of all bank related transactions like, vendor payment, customer receipt and any other payments and

receipts through bank. On regular basis bank account is reconciled with bank statement and reconciliation differences areshown to match both the balances

5.3.2. Business Mapping to R3

SAP bank accounting application helps in posting transaction for funds transfer between the banks, and for doing bank

reconciliation. And also Bank Account will impact based on the Receipt from customer or payment to vendor.

Presently SS Machines is having banks accounts at their main office in New York. In SAP House bank and account ID is created for

each of the banks and bank clearing accounts will be used for posting transactions related to payment and receipts. Bank Account

will be created for each of the bank and bank clearing accounts are configured to the respective bank accounts. Presently SS

Machines one bank CITI Bank and 3 accounts.

Three Accounts are

ACCOUNT 1 – General Deposits

ACCOUNT 2 – Payments

ACCOUNT 3 – Payroll

Bank Master and Account ID and bank account is created for each bank and will be mapped to automatic payment program ,

Cheque lots will be maintained form annual check payment and automatic check payment. Bank master data has to be

uploaded at the time of realization

5.4. Cheque Management Process

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 35/55

Business Blueprint

SS Machines Project Page 35

This function is used to enter checks you receive. After the input is complete, you can access the additional functions to fur ther

process the entered checks (see Entering Incoming Checks).

Normal bank payment transactions are happening through Accounts Payable Model.

5.5. Manual Bank ReconciliationPage81of157

There are basically two steps in this method:

1. The transfer-posting screen under G/ L, the users retrieve the open items under incoming bank clearing account and select them if

they appear on the deposit column of the statement. The open items can be sorted by date to ease matching. Upon completion,

post them against the main bank account. The system will generate the accounting entries l ike the followings:

Dr Main bank

Cr bank incoming clearing

2. The transfer-posting screen under G/ L, the users retrieve the open items under outgoing bank clearing

account and select them if they appear on t he withdrawal column of the statement. The open items can be

sorted by date to ease matching. Upon completion, post them against the main bank account. The system will

generate the accounting entries like the following:

Dr Bank outgoing clearing

Cr Main bank

Steps Procedures

1 Received hardcopy of bank statement

2 Identify bank statement items that can be matched withthe line items in the GL bank account

3 Manually post items that exists in bank statement but not

yet captured in the system

4 Manually post and clear the matched items

5 Manually prepare the reconciliation statement

5.6. Description of Improvement

Reconciliation can be done as often as you get the bank statement and will ensure that data is captured on time. This will also

automatically match the bank statement and bank account

It is very obvious that the balance in the bank clearing account is the not reconciled.

Special configuration consideration

No special configuration required.

Description of Functional Deficit

No deficits

Approaches to covering Functional Deficit

Not Applicable

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 36/55

Business Blueprint

SS Machines Project Page 36

5.7. Petty Cash Management

Requirement and Expectation

There is a need to keep cash and make petty cash transaction at various locations to meet petty cash activity.

5.7.1. Cash Journal

Business Mapping to R3

Cash Journal is a feature in SAP, which permits separate tracking of cash transactions. Each cash journal should be assigned to one

G/ L account, which represents the cash journal in the general ledger. It is however possible, to connect multiple cash journals with

one G/L account. Cash transactions are saved separately in the cash journal and are transferred periodically (for example, daily) to

the general ledger. The Cash Journal also permits generation of daily balance statements for tallying physical cash with the books of

account. Cash journal will not support for making special GL indicator postings. All postings need to be done to vendor or customer

and adjustment entries to be routed separately to special GL indicator.

A separate cash journal and GL account would be maintained for each location handling cash.

Separate cash journals and corresponding GL accounts would also be maintained.

5.8. Description of Improvement

Cash Journal is very effective in SAP, which can track petty cash transaction for each of the locations separately and also will be

tracking balances on daily basis.

Special configuration consideration

No special configuration required.

5.9. Description of Functional Deficit

No deficits

Approaches to covering Functional Deficit

Not Applicable

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 37/55

Business Blueprint

SS Machines Project Page 37

6.0. Taxes

6.1.

6.3

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 38/55

Business Blueprint

SS Machines Project Page 38

6.4

6.5

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 39/55

Business Blueprint

SS Machines Project Page 39

7.0. ASSET ACCOUNTING

The Asset Accounting (FI-AA) component is used for managing and supervising fixed assets with the SAP R/3 System. In SAP R/3

Financial Accounting, it serves as a subsidiary ledger to the FI General Ledger, providing detailed information on transactions

involving fixed assets.

As a result of the integration in the R/3 System, Asset Accounting (FI-AA) transfers data directly to and from other R/3 components.

For example, it is possible to post from the Materials Management (MM) component directly to FI-AA. When an asset is purchased

or produced in-house, you can directly post the invoice receipt or goods receipt, or the withdrawal from the warehouse, to assets in

the Asset Accounting component. At the same time, you can pass on depreciation and interest directly to the Financial Accounting

(FI) and Controlling (CO) components.

The system stores all the values and transaction data per each asset master record. You can differentiate between different types of assets in the FI-AA component. The structure of the master record is identical for all asset main numbers, asset sub-numbers and

group assets. Therefore, the basic procedure for creating any of these objects is essentially the same.

Integration (General)

The FI-AA component is integrated in numerous ways with other R/3 components. The integration of Asset accounting with the FI

(Financial Accounting, including Accounts Payable and Accounts Receivable) component makes it possible to carry out

• Posting of asset acquisitions and retirements that are integrated with accounts payable and accounts receivable.

• Account assignment of down payments to assets when you post down payments in the Financial Accounting (FI) component.

• Posting of depreciation from Asset Accounting to the appropriate general ledger accounts.

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 40/55

Business Blueprint

SS Machines Project Page 40

Asset Accounting-Business Process flow

Asset Master Data

needs to be created

Asset Explorer

Asset Acquisition

Asset Retirements

Intercompany Transfer

Post-Capitalization

Transfer of Reserves

Unplanned Depreciation

Assets under construction

Periodic

Processing

Information

Check

Consistency

EVENT

ASSET

ACCOUNTANT

FINANCE

MANAGER

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 41/55

Business Blueprint

SS Machines Project Page 41

7.1. Asset Classes

Asset classes are the most important means of structuring fixed assets. You can define an unlimited number of asset classes in the

system. You use the asset classes to structure your assets according to the requirements of your enterprise. Asset classes apply in all

company codes. The asset class catalog, therefore, is relevant in all company codes in a client. The preceding is also true when the

company codes have different charts of depreciation and therefore different depreciation areas.

7.2. Chat of Depreciation

Charts of depreciation are used in order to manage various legal requirements for the depreciation and valuation of assets. These

charts of depreciation are usually country-specific and are defined independently of the other organizational units. A chart of

depreciation, for example, can be used for all the company codes in a given country. The chat of Depreciation for company code

SS00 is CDSS.

For SS Machine, there would be monthly posting for Book Depreciation. The depreciation posting cycle is determined by entering

the length of time (in posting periods) between two depreciation-posting runs. This means that a setting of 1 indicates monthly

posting, 3 means quarterly posting, 6 means semi-annual, and 12 means annual (for a fiscal year version with 12 posting periods).

When a depreciation-posting run is started, one has to enter the period for which one wants it to be posted.

7.3. Posting Depreciation

Every asset transaction in the R/3 System FI-AA component immediately causes a change of the forecasted depreciation. However,

it does not immediately cause an update of the depreciation and value adjustment accounts for the balance sheet and profit and loss

statements. The planned depreciation is posted to the general ledger when you run the periodic depreciation posting run. This

posting run uses a batch input session to post the planned depreciation for each posting level for each individual asset as a lump sum

amount.

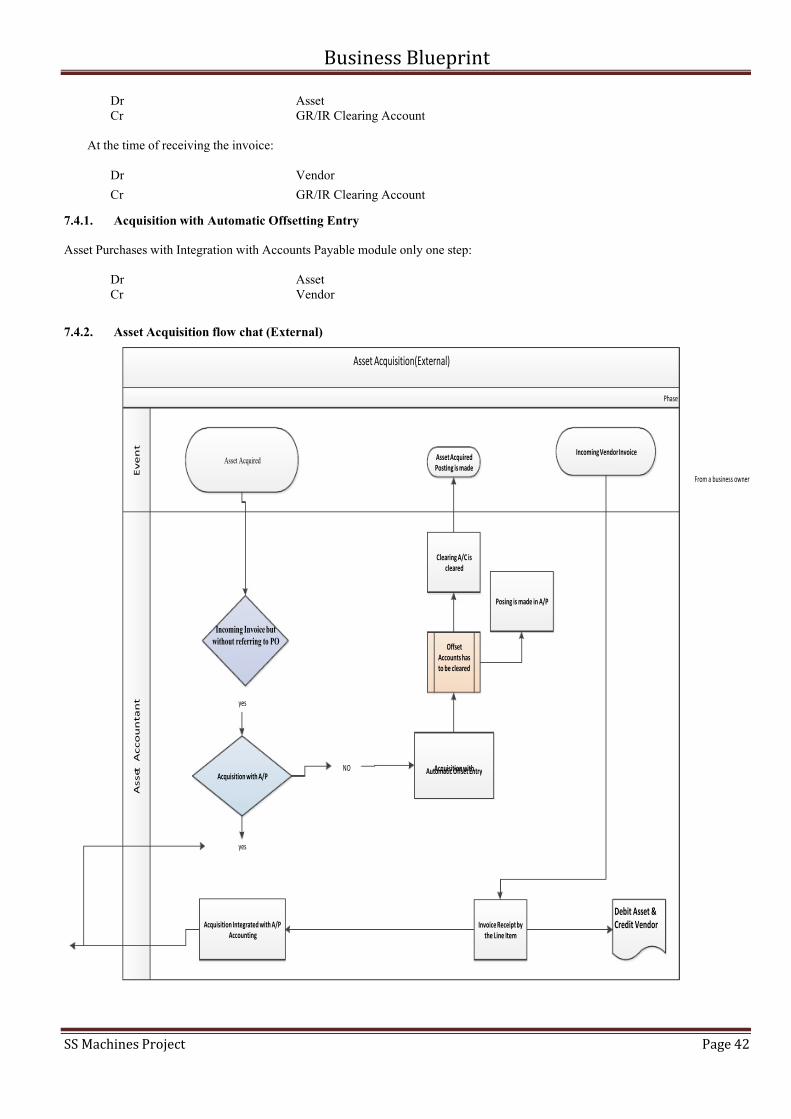

7.4. Acquisition of an Asset

All Asset purchases will be routed through Materials Management route by issuing necessary Purchase order. The transaction is

similar to the other Material Purchases. In SS Limited the Logistic department will process the Asset Receipt through the MM

module. Most of Assets Sales will be handled through MM module.

Unlike most other business transactions, external acquisition using a purchase order requires a sequence of steps to be performed at

separate times:

These are creating the purchase requisition, creating the purchase order, Posting the goods receipt and Posting the invoice r eceipt.

When you use this integrated ordering process, you first have to create an asset master record. You can then post the purchase order

or the purchase requisition with account assignment to the asset. It is also possible to create fixed assets from within the transaction

for creating the purchase order. This means that you can carry out steps, “create asset” and “create purchase order or purchase

requisition,” within one transaction. You enter the most important asset master data information in a dialog box. From this d ialog

box, you can go directly to the actual asset master data transaction. If the asset you create is incomplete because essential asset

master data information is missing, the asset has to be completed later •

At the time of asset receipts:

7/30/2019 Ss Machines Ltd Bbp Final

http://slidepdf.com/reader/full/ss-machines-ltd-bbp-final 42/55

Business Blueprint

SS Machines Project Page 42

Dr Asset

Cr GR/IR Clearing Account

At the time of receiving the invoice:

Dr Vendor

Cr GR/IR Clearing Account

7.4.1. Acquisition with Automatic Offsetting Entry

Asset Purchases with Integration with Accounts Payable module only one step:

Dr Asset

Cr Vendor

7.4.2. Asset Acquisition flow chat (External)

Asset Acquisition(External)

A s s e t

A c c o u n t a n t