state of retail real estate in india

DESCRIPTION

State of Retail Real Estate in IndiaTRANSCRIPT

State of the Retail Real Estate in India Market Trends and Outlook

May 2012 Himadri Mayank AVP-Research and REIS

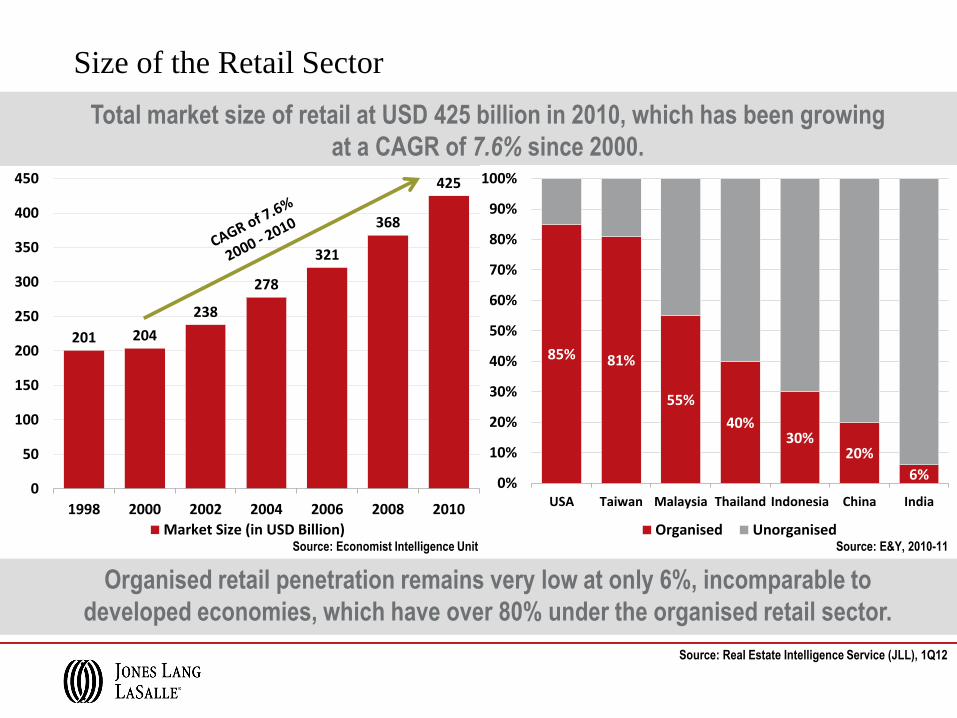

201 204

238

278

321

368

425

0

50

100

150

200

250

300

350

400

450

1998 2000 2002 2004 2006 2008 2010

Market Size (in USD Billion)

Source: Real Estate Intelligence Service (JLL), 1Q12

Size of the Retail Sector

Total market size of retail at USD 425 billion in 2010, which has been growing

at a CAGR of 7.6% since 2000.

85% 81%

55%

40%30%

20%

6%0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

USA Taiwan Malaysia Thailand Indonesia China India

Organised Unorganised

Organised retail penetration remains very low at only 6%, incomparable to

developed economies, which have over 80% under the organised retail sector.

Source: Economist Intelligence Unit Source: E&Y, 2010-11

India - Growth of Organised Retail

Easy Access to

Credit

Rapid

Urbanisation

Expected

Economic

Growth

7-8%

Young

Demographics

with Rising

Income

Rise in Brand

Consciousness

Pressing need

to improve

supply-chain

efficiencies

Hypermarkets

to dominate

organised

retail sector

Relaxation in

Policy to

Support

Investments

Share of organised retail slated to grow from 6% in 2010 to 9% by 2015 and to

20% by 2020

Source: Real Estate Intelligence Service (JLL), 1Q12

The Growth of Retail Malls

The Growth of Retail Malls

As of December 2008, there were 173 malls expected to become operational

during 2009-2011 in the top seven cities @ 1 mall per week!

Source: Real Estate Intelligence Service (JLL), 1Q12

Note: Figures represent the top seven cities of India – Mumbai, NCR-Delhi, Bangalore, Chennai, Pune, Hyderabad and Kolkata.

Rationalisation of Mall Supply (2008)

As of December 2008, there were 173 malls expected to become operational

during 2009-2011 in the top seven cities @ 1 mall per week!

FORECAST

Source: Real Estate Intelligence Service (JLL), 1Q12

Note: Figures represent the top seven cities of India – Mumbai, NCR-Delhi, Bangalore, Chennai, Pune, Hyderabad and Kolkata.

3.4 3.8 3.7

9.48.5

6.3

17.3

13.9

20.0

0

5

10

15

20

25

30

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

(mill

ion

sq

ft)

Supply as of End-2009

Rationalisation of Mall Supply (2009)

Only 25% of the projected supply in 2009 became operational. Several malls

were delayed, while some in initial stages were shelved or converted.

FORECAST

Source: Real Estate Intelligence Service (JLL), 1Q12

Note: Figures represent the top seven cities of India – Mumbai, NCR-Delhi, Bangalore, Chennai, Pune, Hyderabad and Kolkata.

3.4 3.8 3.7

9.48.5

6.3 6.9

19.3

13.812.3

0

5

10

15

20

25

30

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

(mill

ion

sq

ft)

Supply as of End-2010

Rationalisation of Mall Supply (2010)

As retail became the last to recover among the real estate sectors, 60% of the

projected supply of 2010 was also delayed to 2011.

FORECAST

Source: Real Estate Intelligence Service (JLL), 1Q12

Note: Figures represent the top seven cities of India – Mumbai, NCR-Delhi, Bangalore, Chennai, Pune, Hyderabad and Kolkata.

3.4 3.8 3.7

9.48.5

6.3 6.9

13.812.0

9.5

17.2

0

5

10

15

20

25

30

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

(mill

ion

sq

ft)

Supply as of End-2011

Rationalisation of Mall Supply (2011)

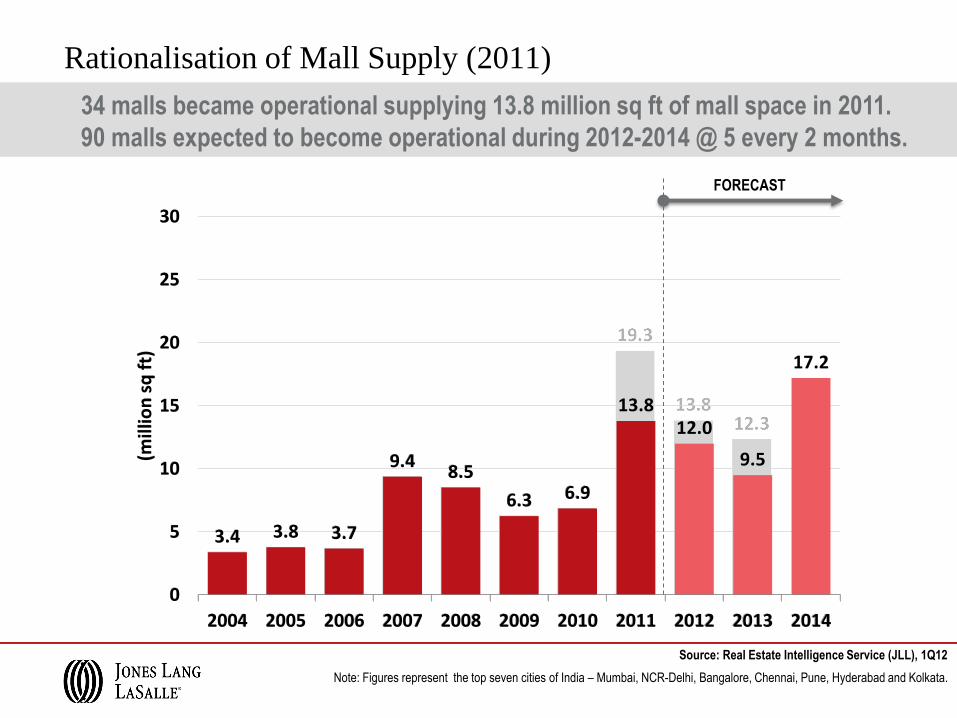

34 malls became operational supplying 13.8 million sq ft of mall space in 2011.

90 malls expected to become operational during 2012-2014 @ 5 every 2 months.

FORECAST

Source: Real Estate Intelligence Service (JLL), 1Q12

Note: Figures represent the top seven cities of India – Mumbai, NCR-Delhi, Bangalore, Chennai, Pune, Hyderabad and Kolkata.

Source: Real Estate Intelligence Service (JLL), 1Q12

Absorption of retail space more than doubled to reach 10.7 million sq ft. Supply in 2012 is near

completion, while half of the supply of 2013 and most in 2014 have high construction risks.

Note: Figures represent the top seven cities of India – Mumbai, NCR-Delhi, Bangalore, Chennai, Pune, Hyderabad and Kolkata.

Supply and Demand of Retail Mall Space 3

.8 4.1

9.4

8.5

6.3 6

.9

13

.8

12

.0

8.4

14

.2

2.8

3.7

9.6

6.6

4.0 4.0

10

.7

8.1

7.1

10

.1

0%

4%

8%

12%

16%

20%

24%

28%

32%

0

2

4

6

8

10

12

14

16

2005 2006 2007 2008 2009 2010 2011 2012F 2013F 2014F

New Completions Net Absorption Vacancy

FORECAST

Completed

Ready for Fit-Outs

50%-100% Structure

Ready

Less than 50%

Structure Ready

Excavation / Upto

Plinth

Proposed

Source: Real Estate Intelligence Service (JLL), 1Q12

Hyderabad and NCR-Delhi have several malls under construction, but a significant

portion is under initial stages. Mumbai, Pune, Chennai and Bangalore have few malls in

the supply pipeline. Thus, there is a severe crunch of suitable mall space for retailers.

Status of Construction of Upcoming Retail Malls

NCR-Delhi

Mumbai

Bangalore

Chennai

PuneHyderabad Kolkata

0

5

10

15

20

25

30

0% 5% 10% 15% 20% 25% 30% 35% 40%

Sto

ck (

mill

ion

sq

ft)

Vacancy (%)

NCR-Delhi and Mumbai lead

others by a huge margin in

terms of operational retail

stock; have high vacancies in

secondary districts. Kolkata, Hyderabad, Chennai

and Bangalore have relatively

low stock and low vacancy.

These cities have considerable

activity on high streets.

NCR-Delhi and Mumbai constitute two-thirds of pan India retail mall space.

Considerable retail activity remains on the traditional high streets of India.

1Q12 4Q13F

Source: Real Estate Intelligence Service (JLL), 1Q12

Retail Trends: Stock vs Vacancy 1Q12

PA

N-I

ND

IA

VA

CA

NC

Y

NCR-Delhi

Mumbai

Bangalore

Chennai

Pune

Hyderabad

Kolkata

0

5

10

15

20

25

30

0% 5% 10% 15% 20% 25% 30% 35% 40%

Sto

ck (

mill

ion

sq

ft)

Vacancy (%)

Note: 4Q13F values for stock and vacancy rate are REIS forecasted values

Source: Real Estate Intelligence Service (JLL), 1Q12

NCR-Delhi expected to remain dominant with over 25 million sq ft of operational mall

space by end-2013. Vacancies are expected to increase in the short term due to supply-

absorption mismatch.

1Q12 4Q13F

Malls expected to

become operational

in 2012 and 2013

will increase stock in

Mumbai and NCR

3.3 million sq ft of

expected supply till

2013 in Chennai

Retail Trends: Stock vs Vacancy 4Q13F

PA

N-I

ND

IA

VA

CA

NC

Y

Source: Real Estate Intelligence Service (JLL), 1Q12

Good quality malls enjoy high occupancy levels while poor quality malls continue to

struggle with high vacancy as they fail to garner retailer interest.

Retail Trends: Polarisation of Demand

• Success chases success. Retailers are

interested in taking spaces in only through

those malls that attract higher footfalls and

have a healthy footfall-to-sales conversion

ratio.

• Superior Grade Malls offer

good location

lease-only model

experienced developer profile

professional mall management

active tenant mix management

Superior

Grade

Average

Grade

Poor

GradeAll

NCR-Delhi 6% 28% 40% 25%

Mumbai 10% 34% 47% 23%

Bangalore 2% 17% 33% 9%

Chennai 0% 29% NA 14%

Pune 17% 18% 21% 18%

Hyderabad 4% 6% 12% 6%

Kolkata 6% 28% 45% 21%

India 7% 26% 39% 20%

Vacancy in Operational Malls

Source: Real Estate Intelligence Service (JLL), 1Q12

After declining sharply in 2009, rents remained stable for most parts of 2010. They have since

recovered gradually in several markets, but remain near cyclical lows.

Movement of Rental Values (1Q08 – 1Q12)

Simple Average of % Q-o-Q Change in Rental Values of Constituent Micro-Markets

Rental

Movement

1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2012 2013 2014 1Q08-4Q14F

NCR-Delhi 0.0% -3.0% -9.8% -21.1% -12.1% -8.4% -8.7% -5.8% -3.9% 0.0% 0.0% 0.7% 1.6% 1.3% 0.9% 0.0% 1.7% 5.0% 6.4% 6.3%

Mumbai 1.1% 0.0% -14.5% -15.3% -12.2% -5.4% -3.0% 0.0% 0.0% 0.0% 0.0% 0.0% 2.4% 1.8% 2.9% 0.4% 1.4% 4.3% 6.0% 7.1%

Bangalore 0.0% 0.0% -2.6% -8.0% -7.6% -5.8% -2.7% -1.5% 0.0% 0.0% 0.0% 0.0% 3.5% 1.3% 0.0% 0.0% 1.4% 4.4% 6.4% 6.7%

Pune 0.0% 0.0% -16.6% -7.9% -5.6% 0.0% 0.0% 0.0% 0.0% 0.0% 2.4% 0.9% 1.3% 1.6% 1.1% 0.0% 1.9% 5.4% 6.6% 7.2%

Hyderabad 0.0% 0.0% -11.3% -13.9% 0.0% -6.5% 0.0% 0.0% 0.0% 0.0% 0.0% 0.8% 0.0% 0.0% 0.0% 0.0% 1.0% 2.9% 3.9% 4.8%

Kolkata 2.6% 1.9% -8.2% -12.7% -10.9% -2.6% -1.9% 0.0% 0.0% 0.8% 0.0% 0.9% 0.7% 0.6% 2.4% 3.5% 1.2% 4.0% 5.8% 4.0%

ANNUAL FORECASTGROWTH

SLOWING

RENTS

DECLINING

RENTS

RISING

DECLINE

SLOWING

The Recipe for Success

Source: Real Estate Intelligence Service (JLL), 1Q12

Average size of a shopping mall in India has been increasing due to developers focusing on

larger shopping malls. Success of a mall does depend on its size, as superior grade malls are

nearly double the size of average grade malls.

Average Size of Shopping Mall

Note: Figures represent the top seven cities of India – Mumbai, NCR-Delhi, Bangalore, Chennai, Pune, Hyderabad and Kolkata.

-

2,00,000

4,00,000

6,00,000

8,00,000

10,00,000

12,00,000

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

(Ave

rage

Siz

e in

sq

ft)

-

1,00,000

2,00,000

3,00,000

4,00,000

5,00,000

6,00,000

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

(Ave

rage

Siz

e in

sq

ft)

For Malls

Becoming

Operational

in a

Particular

Year

For All

Operational

Malls

Crosses 200,000 sq ft

in 2007

Expected to cross

300,000 sq ft by 2014

200,000

2001 - 2006

300,000

2007 - 2010

400,000

2011 - 2013

700,000?

2014 - 2017

Superior Grade

440,000 sq ft

Average Grade

190,000 sq ft

Poor Grade

150,000 sq ft

Average Size of

What makes a mall successful in India?

Leasable

Area

Vacancy

Prime locations, but

not necessarily at the

centre of the city

Location

50% of the malls have at least

one anchor store with area

greater than 60,000 sq ft

Anchor Store

Professional Mall

Management Services Adequate Parking

Multiplex essential to

ensure sufficient foot-

falls

Entertainment

Ample Mall Amenities

From the analysis of 20 successful malls across major Indian cities

| Ambi Mall, Vasant Kunj, Delhi | Ambience Mall, Gurgaon | City Centre, Kolkata | DLF Emporio, Delhi | Express Avenue, Chennai |

Forum Mall, Bangalore | GVK One, Hyderabad | High Street Phoenix, Mumbai | Inorbit, Hyderabad | Inorbit, Malad, Mumbai | Inorbit,

Vashi, Mumbai | Korum Mall, Thane | Mantri Square, Bangalore | MGF Metropolitan, Gurgaon | Oberoi Mall, Mumbai | Pacific Mall,

Delhi | R-City Mall, Mumbai | Select City Walk, Delhi | South City Mall, Kolkata | The Great India Place, Noida |

600,000 –

800,000 sq ft

Less than 5%

Future Formats of Retail Real Estate in India

Retail Formats – Ushering an Era of Collaboration

Destination Retailing

Rural Retailing

Mixed Use Formats

Tourism Retailing

Luxury Retailing

Integrated residential

townships

Hotel-and-luxury retail

Office-and-convenience

retail

Lack of luxury malls

Luxury brands

limited to Tier I on

high-streets or Five-

Star Hotels

Recreational

shopping

precincts

Organised retail for

70% of India’s

population

Retail development at

tourist hubs

Partnership with

government

Industry will experiment with several organised retail formats by collaborating with multiple

stakeholders

Source: Real Estate Intelligence Service (JLL)

Source: Real Estate Intelligence Service (JLL)

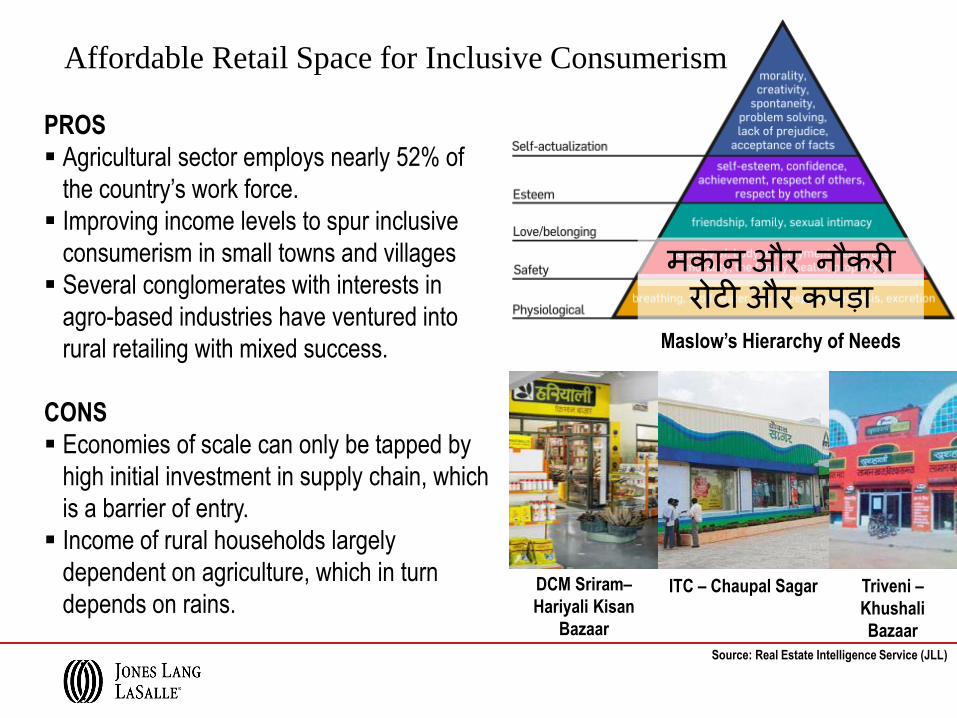

Affordable Retail Space for Inclusive Consumerism

DCM Sriram–

Hariyali Kisan

Bazaar

ITC – Chaupal Sagar Triveni –

Khushali

Bazaar

PROS

Agricultural sector employs nearly 52% of

the country’s work force.

Improving income levels to spur inclusive

consumerism in small towns and villages

Several conglomerates with interests in

agro-based industries have ventured into

rural retailing with mixed success.

CONS

Economies of scale can only be tapped by

high initial investment in supply chain, which

is a barrier of entry.

Income of rural households largely

dependent on agriculture, which in turn

depends on rains.

मकान और नौकरी

Maslow’s Hierarchy of Needs

रोटी और कपडा

Copyright © Jones Lang LaSalle, 2011

Jones Lang LaSalle Research Real Estate Intelligence Service Research Advisory

Leads the industry in India. Drawing on a

wide spectrum of expertise, we provide clients

with best-in-class market insights that allow

you to optimize your real estate strategies and

mitigate risks.

The REIS is a subscription-based service

providing comprehensive market monitoring,

analysis and forecasts across major

institutional-grade real estate markets

throughout the Asia Pacific region.

The Research team offers tailored advisory

services for investors, developers and

occupiers at the local, regional and global

levels.

For more details, contact:

Ashutosh Limaye

Head of Research and Real Estate Intelligence Service

Himadri Mayank

Assistant Vice President, Research and Real Estate Intelligence Service