state of the industry report -...

TRANSCRIPT

Implications for Foodservice

Equipment & Supplies Manufacturers

September 2014

State of the Industry Report

1

Perspective

The 2014 State of the Industry Report, powered by research and information gleaned from

industry-leading research organization, Technomic, delves into issues impacting foodservice

operations, and, the implications of such on equipment and supplies purchases.

What consumer behaviors and attitudes impact menu and culinary trends? What are the

implications for equipment and supplies manufacturers? Read on for ideas, information and

opportunities.

2

Today’s Consumer

The success of the foodservice industry is ultimately driven by the consumer. Consumer

financial well-being is critical to understanding the broader trends and issues impacting the

industry as a whole, and the equipment and supplies manufacturer in particular.

According to the Conference Board, consumer confidence stood at 90.9 in July, up four points

from June. Sentiment is holding more or less steady, and is well above the doldrums during

and after the great recession. However, while consumers appear to be getting more

confidence in the overall situation and that of the broader economy, today’s numbers are not

those typical of an expansionary period. This indicates consumers do not fully believe that the

economy has recovered and are constraining their spending as a result.

Base: 1985 = 100

Source: Conference Board

Jul '07111.9

Jul '1490.9

0

20

40

60

80

100

120

Jan '06 Jan '07 Jan '08 Jan '09 Jan '10 Jan '11 Jan '12 Jan '13 Jan '14

Consumer Confidence – U.S. Index

3

Today’s Consumer

Over time, Technomic has found that the growth in disposable personal income provides the strongest correlation to overall foodservice industry growth. Disposable personal income, inflation, and an increase in food prices all impact consumer confidence. Disposable personal income was up 1.9 percent in May 2014 over May 2013. The average disposable income growth has been less than 1 percent over the past several years, which strongly correlates to sluggish industry growth.

Technomic keeps a close eye on both the unemployment and the under-employment rate since the level of employment is key to understanding broader consumer financial health and the ability to spend money on dining out. While the unemployment rate dropped to 6.1 percent in June, its lowest since July 2008, under-employment remained a concern. In June, the under-employment rate, with under-employment defined as individuals working in positions insufficient in the level of skill required, hours worked or level of compensation, stood at 12.1 percent. Under-employment compresses disposable personal income.

-4%

-2%

0%

2%

4%

6%

8%

May

'06

May

'07

May

'08

May

'09

May

'10

May

'11

May

'12

May

'13

May

'14

Disposable Income % Real Change vs. Prior Year

4

Today’s Consumer

Since spring, jobs have been growing and production has been on the upswing. Although core

inflation remains low, “non-core” inflation – for energy and food – has been rising. Consumers

are slow to regain confidence. Nearly 45 percent of all consumers surveyed report eating away-

from-home more than once a week, with another 22 percent reporting they have eaten out at

least once a week. Only 14 percent eat away-from-home once a month or less, and consumers

remain very cautious.

While foodservice has become ingrained in many consumers’ daily activities, many have not

increased spending and even more are spending less. Additionally, the recovery has not been

uniform. Higher-income consumers have recovered much more quickly than low-income

consumers, which has had an impact on the growth of various foodservice channels.

Most Consumers Use Foodservice at Least Once a Week

5

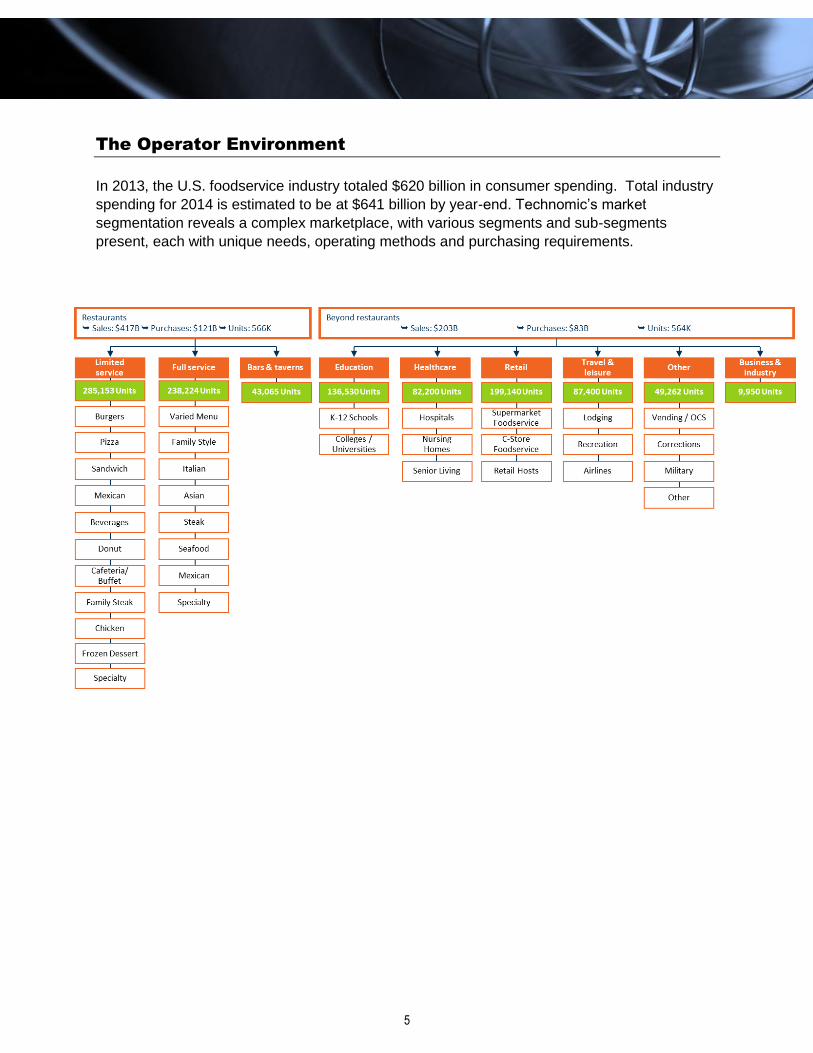

The Operator Environment

In 2013, the U.S. foodservice industry totaled $620 billion in consumer spending. Total industry

spending for 2014 is estimated to be at $641 billion by year-end. Technomic’s market

segmentation reveals a complex marketplace, with various segments and sub-segments

present, each with unique needs, operating methods and purchasing requirements.

6

The Operator Environment

Chains continue to dominate the industry in the restaurant sector. In 2013, the current year for

which Technomic has full-year data, the top 100 limited- and full-service chains controlled 49

percent of the $448 billion restaurant business. Further, the top 500 chains experienced a less

severe decline than independents, weathering the recession better than other foodservice

outlets. And while chains have been growing faster than the broader restaurant industry,

franchising has been the preferred source of growth, since it’s less risky for the corporate

parent.

The top 500 chains by U.S. sales account for almost $6.00 out of every $10.00 taken in

nationally, although they represent only four out of 10 restaurant locations. The limited-service

sector, dominated by large chains, comprises 83 percent of limited-service sales and 65 percent

of unit locations. Full service is still led by independent restaurants and regional companies,

with big chains accounting for only 33 percent of sales and 17 percent of locations.

.

Total 2013 Restaurant

Industry: $448 billion Sales Growth vs. Previous Year

Share of Restaurant Sales Share of Restaurant Units

7

The Operator Environment

Growth for the top 10 largest chains, for both full- and limited-service restaurants – especially

full service – has been hampered by strong economic headwinds and a consumer desire for a

differentiated experience. As a result, much of the growth has occurred in small chains and

independents.

For years, same-store sales growth in limited-service restaurants has almost always beat that in

full service, indicating a general consumer demand for low-cost menu options and some

“trade down” effect. It’s also true that full-service restaurants, specifically casual dining, suffered

from a poor value equation, with consumers finding a lack of differentiation among many of the

larger chains.

Same-Store Sales

8

The Operator Environment

Within the top 500 limited-service restaurants, key trends emerged. Fast-casual Asian/noodle

and bakery café sectors were the fastest growing, along with coffee cafes.

Limited-service sales growth, beating that of the full-service restaurant sector, is a bit more

complex. In full service, with demand driven by affluent consumers and business travelers,

expensive steakhouses exceeded all other menu clusters in growth. Varied-menu chains also

beat the segment average.

With that in mind, fast casual ― with concepts such as Qdoba, Panera, Five Guys and Chipotle

― and contemporary casual concepts ― such as Yard House, Maggianos, The Cheesecake

Factory and Seasons 52 ― are best positioned for growth.

9

The Operator Environment

Within the context of this report, it is important to keep in mind that the U.S. foodservice industry

has been in a prolonged period of flat to declining growth. In general, the industry is mature.

Expectations for growth through 2016 suggest that real growth, i.e. case or volume growth, will

be just over 1 percent for the next three years. As with any statistic, certain segments will

outperform this variable.

Given the uncertainties facing operations and consumers, most nominal industry sales growth

comes from inflation, with a return to 1 percent plus real growth in 2015. Sectors beyond

restaurants will do better than the commercial restaurant industry based on changes to the

menu and traffic mix. Limited-service restaurants are likely to see real sales flat in 2014 and up

1 percent in 2015, while full-service restaurant real sales are more likely to contract this year

and bounce back next year.

Total U.S. Foodservice Industry Growth 2001-2014 (P)

Nominal and real percentage

10

Foodservice E&S

As reported in NAFEM’s 2014 Size & Shape of the Industry Study, the overall foodservice

equipment and supplies market for 2013 totaled approximately $9.9 billion, up from $9 billion in

2011 and $8.1 billion in 2009.

From a growth perspective, and compared to 2011 figures, food preparation equipment was the

fastest growing category, up nearly 10 percent over the two-year period. Refrigeration and ice

machines grew 9 percent, while primary cooking equipment was up nearly 6 percent.

Equipment & Supplies Category

2013 sales

($000,000)

Refrigeration & Ice Machines $2,422.6

Primary Cooking Equipment $2,030.0

Serving Equipment $1,162.5

Tabletop & Servingware $1,081.6

Warewashing, Janitorial & Safety

Equipment

$808.1

Storage & Handling Equipment $699.9

Furnishings, Décor & Custom Fabrication $643.0

Smallwares, Cookware & Kitchen Tools $620.2

Food Preparation Equipment $474.5

Total E&S sales ($B)

11

Foodservice E&S

Equipment & Supplies Category

Compound Annual

Growth (2011-2013)

Food Preparation Equipment 9.7%

Refrigeration & Ice Machines 9.0%

Primary Cooking Equipment 5.9%

Furnishings, Décor & Custom

Fabrication

5.4%

Tabletop & Servingware 4.7%

Storage & Handling Equipment 4.6%

Smallwares, Cookware & Kitchen Tools 3.7%

Warewashing, Janitorial & Safety Equip. 1.4%

Serving Equipment 0.9%

While the NAFEM 2014 Size & Shape of the Industry Study provides detailed information by

product category, it is important to place the size of these categories into context.

Technomic continually monitors the broader foodservice industry and has identified eight key

drivers impacting both consumer spending and front- or back-of-the-house foodservice

operations. These macro-level trends also impact how equipment and supplies manufacturers

could respond to customer needs.

Overall, it is important to realize that regardless of the segment, all foodservice operators have

common concerns such as costs, sales and margins. Human-asset issues also are on the rise.

Interestingly, as consumers call for “fresh” and “hand-crafted,” labor issues and costs dictate a

greater need for automated equipment.

Similar issues impact the equipment and supplies world. Rising costs, the need for profitability

enhancement, labor challenges, freshness as a quality driver, customization, an increasing

focus on ethnic foods, continued interest and focus around “health,” and sustainability and

social responsibility, all factor into discussions on equipping foodservice kitchens worldwide.

Existing restaurant and foodservice outlets generally are not seeing “organic” sales growth. In

fact, many casual-dining chains actually are watching same-store sales declines. Stagnant

growth conditions mean many foodservice operators are seeing little to no top-line sales growth.

Focusing on maintaining profitability has been critical, which by definition, has meant an

extreme focus on cost containment or reduction.

With a lack of “real” growth and higher traffic counts, operators are discounting to a much

greater degree. While this may or may not provide a traffic lift, it does bring in a much less

profitable guest, leading further to profitability issues.

12

Foodservice E&S

There’s no question that rising costs are the number one concern. Customers are still slow to

spend, and operators are unwilling to raise prices. Maintaining profitability is critical as top-line

sales growth is challenged.

Issue E&S Implications

Rising cost

and need for

profitable

growth

Investment is occurring to keep up with

trends. Being able to show return on

investment including labor savings,

energy efficiency, and more, is critical.

Operators also may delay purchases

on specific types of equipment if it is

not perceived as absolutely necessary.

Labor challenges continue among all foodservice segments, most notably finding and retaining

qualified labor. Of operators surveyed, 64 percent list retention as the most critical issue, with

60 percent citing recruiting a critical concern. Beyond finding and retaining good employees,

many operators are facing a potential cost increase due to legislation such as the Affordable

Care Act and pending action on minimum wage. In Technomic’s 2014 operator survey, half of

restaurateurs and 61 percent of all foodservice operators, including those in on-site sectors,

said a minimum wage increase to $10 an hour would have a negative effect on business.

Issue E&S Industry Implications

Labor

challenges

Provide solutions to reduce labor costs

with a focus on ease of use and simple

maintenance.

Automation can reduce overall labor

costs.

13

Foodservice E&S

More than half the surveyed consumers say customization – allowing the consumer to tailor their meal to their personal taste preferences – is a growing trend. The demand for customization also related to the larger trend of consumers demanding what and how they want it, when they want it. To wit, there’s an increase in all-day snacking, all-day breakfasts, staggered portions, and build-your-own concepts (sandwiches, burritos, pizzas, etc.). Consumers expect to be able to customize their order at the point-of-purchase. Much of the fast-casual marketplace has incorporated customization into their operations. This trend is expected to continue.

Issue E&S Industry Implications

Need for

customization

Equipment that enhances

customization – hot/cold

merchandisers, prep tables, under-

counter refrigeration, etc., – to take

advantage of the trend.

Accelerated cooking equipment is

a natural fit to assist in point-of-

purchase customization.

Food on the go, referred to as grab-n-go, represents a small but critical element of successful

foodservice programs, and growth is expected to outpace that of overall foodservice outlets over

the next three years. Technomic typically defines grab-n-go as pre-packaged, ready-to-eat

prepared food requiring no customer assembly or preparation. These are self-service offerings

sold in heated or chilled merchandisers.

The total grab-n-go market grew 3.6 percent annually between 2010 and 2013, with the concept

in colleges/universities, supermarkets, hotels and mass merchandisers/club stores, outpacing

the overall growth rate.

Issue E&S Implications

Convenience/

grab-n-go

Display and holding equipment, as

well as take-out packaging and

monitoring devices, are all growth

areas for this segment.

14

Foodservice E&S

Flavor also has gained ground. Two thirds of consumers say savory flavors appeal to them,

down slightly from 72 percent of consumers in 2009. All other flavors indicate a slight-to-

moderate increase in consumer interest from 2009, especially salty and smoky flavors. Spicy,

though not seeing as much growth, is the second most appealing flavor, with 52 percent of

consumers now saying they like spicy foods. Operators are incorporating many of these flavors

through cooking and preparation methods such as smoking, marinating, grilling, roasting and

pickling.

Issue E&S Implications

Incorporating

new flavors

Global cuisines create the need for

authentic equipment such as a

vertical spits, smokers, well-

seasoned woks or tortilla presses.

Consumers are trending toward health-halo and looking for healthy food. Nearly 65 percent say

restaurants can offer healthy food that tastes good. A growing number of consumers want

healthy menus, and operators have responded with baked, steamed and other healthful

preparations. However, consumers still see dining out as an indulgence, so operators need

broilers, fryers and panini presses.

Millennials gravitate toward low-calorie, unprocessed, natural items, while Gen Xers want

organic, authentic, homemade creations. Boomers focus on all the lows – fat, salt, cholesterol,

carbohydrates – and premium, homemade dishes.

Issue E&S Implications

Continued

interest in

and focus

around

healthy

Prep cooks with colorful

ingredients at hand need

convenient storage and attractive

servingware.

Fryers, waffle irons, panini

presses, grills and sauté pans still

fit the bill, since dining out is a

consumer indulgence.

15

Foodservice E&S

While freshness is closely linked with the perception of healthy, it also is a critical component

when consumers gauge the overall quality and value of a foodservice establishment. Fresh is

the leading health-halo term, but interest in attributes such as natural and organic has been

increasing.

Issue E&S Implications

Freshness as

a primary

driver for

quality

Operators also need solutions for

storing seasonal ingredients and

displaying freshness.

Perceived freshness is often as

important as true freshness, and

display equipment plays a crucial

role.

With fresh, local and sustainable menu options growing in importance among consumers,

operations are balancing easy-holding frozen items with use-now fresh ingredients. At the

same time, their eco-friendly tactics include sustainable construction materials, energy-saving

equipment and waste-reduction strategies.

Issue E&S Industry Implications

Sustainability

and social

responsibility

Energy-saving and holding

equipment, use of post-consumer

waste, and anything that can be

reduced, reused or recycled, are

growth areas.

16

Conclusions

The foodservice industry remains in a period of challenged growth. The overall industry is

expected to grow by 3.3 percent in 2014 and 3.1 percent in 2015. And, there are a number of

bright spots, including the supermarket, lodging, and college/university segments, that are

expected to outperform the broader industry.

Overall, Technomic sees the following as impacting each NAFEM Size & Shape of the

Industry product category:

Categories Comments/Impact

Refrigeration & Ice Machines

One of the fastest growing E&S categories for the past two years.

Energy efficiency critical to maintain cost control.

With “fresh” positioning causing a shift toward “never frozen,” refrigeration

continues to benefit.

Ice machines can benefit from positive investment and experimentation in new

beverage programs.

Primary Cooking Equipment

On-trend preparation styles include grilling, sautéing, braising; equipment sales

reflecting these trends.

Frying remains a popular preparation technique as consumers still look to indulge.

Serving Equipment

Manufacturers need to demonstrate how serving equipment can positively impact

sales and generate ROI.

Many specific pieces of serving equipment benefit from high growth menu items –

specifically coffee and specialty coffee, next-generation beverages such as teas,

and juices, and the demand to customize at order.

Tabletop & Servingware New unit openings have slowed; operator sales will be generated from

replacement business or as units are “re-concepted.”

Operators may be reluctant to invest here unless there is a proven ROI.

Warewashing, Janitorial & Safety Equipment

Profitability drivers may mean operators try to prolong the life of warewashing

equipment; maintenance is key.

Cleanliness and food safety can often impact consumer attitudes and perceptions

of specific foodservice operations; equipment plays a role.

Storage & Handling Equipment Operator purchases will be driven by replacement, remodels.

Storage solutions that assist in front-of-house prep work can benefit from key

trends.

Furnishings, Décor & Custom Fabrication Much of the growth will be driven by remodels and unit openings.

Smallwares, Cookware & Kitchen Tools Pans, utensils and other items are not likely to outperform the industry.

Sauté pans win on the health trend.

Food Preparation Equipment

Fastest growing category over the past two years; grills, toasters and panini

presses all benefit from trends.

Fryers remain a critical component of a typical kitchen, although long-term trend

indicates frying will fall out of favor.

300 S. Riverside Plaza Suite 1200 Chicago, IL 60606 312-506-3827 [email protected] www.technomic.com

161 N. Clark St. Suite 2020 Chicago, IL 60601 312-821-0201 [email protected] www.nafem.org