staying ahead of the curve revenue cycle change

DESCRIPTION

Staying Ahead of the Curve Revenue Cycle Change. Joseph J. Fifer, FHFMA, CPA. President and CEO, HFMA. 2014 MAHAP-MPAA-HFMA Michigan Revenue Cycle Conference. September 18, 2014. Key Trends Affecting Revenue Cycle Leaders. Intensifying regulatory scrutiny (RACs, etc). Preparing for ICD-10 - PowerPoint PPT PresentationTRANSCRIPT

Staying Ahead of the CurveRevenue Cycle Change

Joseph J. Fifer, FHFMA, CPAPresident and CEO, HFMA

2014 MAHAP-MPAA-HFMA Michigan Revenue Cycle ConferenceSeptember 18, 2014

1

2

Key Trends Affecting Revenue Cycle Leaders

1. Intensifying regulatory scrutiny (RACs, etc).

2. Preparing for ICD-10

3. Adapting to emerging payment models

4. Integrating with physicians and affiliated providers

5. Reducing costs

6. Impact of the Affordable Care Act

7. Adopting a patient-centered approach

3

RAC Denials and Medical Record Requests Continue to Increase

4

CMS RAC Settlement Offer

• Situation: CMS backlog of up to 800,000 cases has resulted in hospitals waiting up to 18 months to resolve a case.

• CMS is offering 68% of the net payable sum that most hospitals had appealed or planned to appeal of patient status claim denials.

• CMS’s stated goal is to “quickly reduce the volume of patient status claim denials pending in the appeals process.”

• HFMA Analysis: Each qualifying organization should evaluate the offer in the context of its case mix & historical success rate with appeals.

• Solving the backlog without addressing the root problem is only a Band-Aid solution. This offer does not address higher costs beneficiaries face when a RAC denies stay that would have otherwise qualified a patient for medically necessary skilled nursing care.

5

ICD-10 Readiness Still Low

Source: Reader/CHIME survey reveals 12 ICD-10 delay surprises. SearchHealthIT. http://searchhealthit.techtarget.com/news/2240228031/Reader-CHIME-survey-reveals-12-ICD-10-delay-surprises

Only 11 percent of respondents to a survey conducted in summer 2014 reported that they are ready for ICD-10.

6

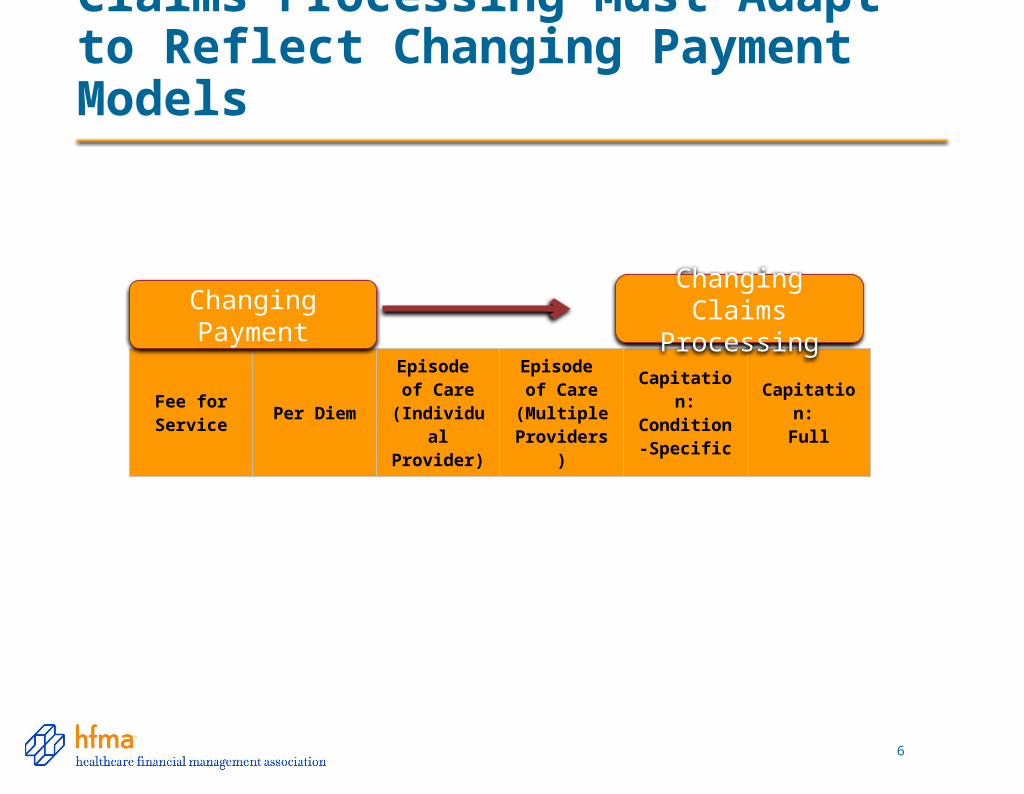

Claims Processing Must Adapt to Reflect Changing Payment Models

Fee for Service Per DiemEpisode of Care

(Individual Provider)

Episode of Care

(Multiple Providers)

Capitation: Condition-

SpecificCapitation:

Full

Changing Payment

Changing Claims Processing

Insurance exchanges – plansNarrow networksHigh deductibles

501(r) requirements

7

Fee-For Service Still Dominant. . . What Is the Tipping Point?

• Catalyst for Payment Reform found that only about 11 percent of all hospital payments were “value-oriented” in 2013.

• But even that may be high, because for 43 percent of these, providers were not at risk for their financial performance.

• We haven’t reached the tipping point yet, and it’s not clear what it will be.

• When that tipping point comes, revenue cycle must be ready.

8

Realignment Is Erasing Traditional Healthcare Boundaries

Driven by demands for care transformation, the healthcare industry is realigning at an an unprecedented pace.

The Triple Aim framework was developed by the Institute for Healthcare Improvement in Cambridge, Mass. (www.ihi.org).

SHARED GOAL

9

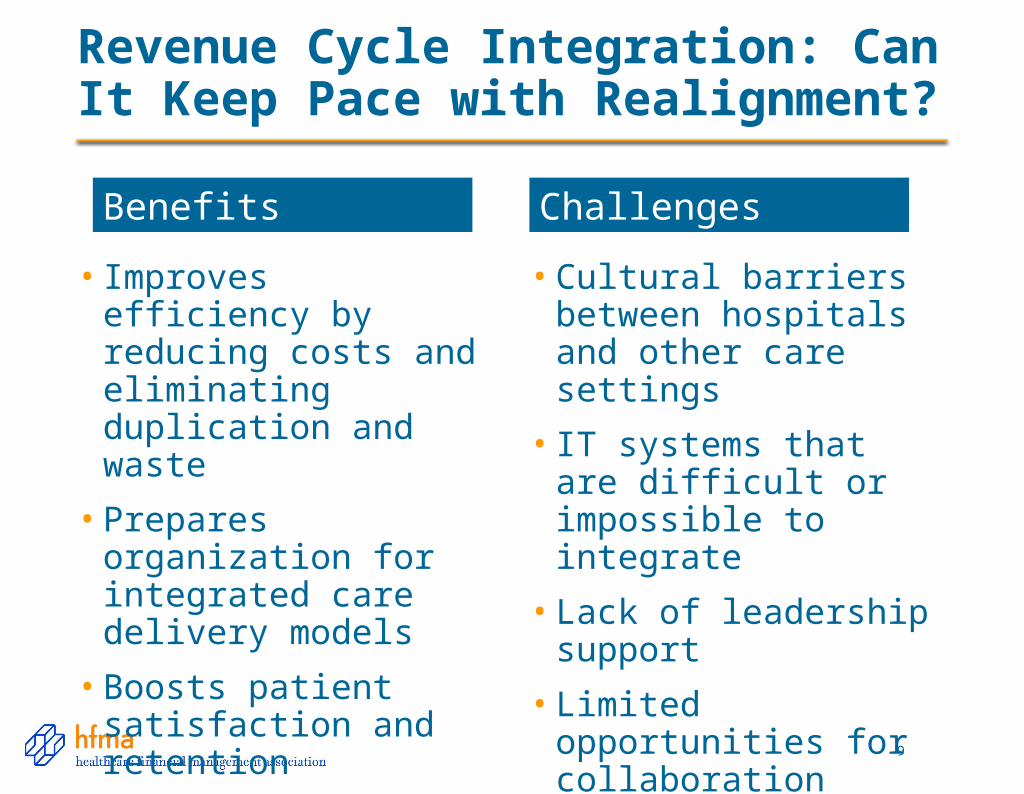

Revenue Cycle Integration: Can It Keep Pace with Realignment?

• Improves efficiency by reducing costs and eliminating duplication and waste

• Prepares organization for integrated care delivery models

• Boosts patient satisfaction and retention

• Cultural barriers between hospitals and other care settings

• IT systems that are difficult or impossible to integrate

• Lack of leadership support

• Limited opportunities for collaboration between hospitals and payers

ChallengesBenefits

10

A Perspective on the Long-Term Revenue Cycle Cost Imperative

“Health care is the only industry that has a revenue cycle with a designated subsector of companies that manage it. It costs 20 to 30 cents on the dollar to cross a trade in health care – to take the money from the buyer of health care, the self-insured employer, and put it into the pockets of the providers. If any other industry had a revenue cycle like that, we'd all be living like the Amish. Wall Street crosses a trade for fractions of a penny. There's an enormous opportunity to take costs out of the process by actually fixing the revenue cycle. And by fixing I don't mean by incremental process improvements. I mean blowing it up. And really rethinking the process of how we go about getting doctors and hospitals paid.“

-Sean Wieland, Managing Director and Senior Research Analyst, Piper Jaffray

“Revenue Cycle Ripe for Radical Change,” Healthcare IT News, Dec. 9, 2013

http://www.healthcareitnews.com/news/revenue-cycle-ripe-radical-change

"

11

Why a Patient-Centered Approach Matters Now

• Patients are paying more of their health care out-of-pocket, due to increase in HDHPs and cost-sharing

• As a result, receivables are shifting from third-party payers to patients

• This shift

– Puts more pressure on revenue cycle processes

– Raises concerns for patients –and patients’ expectations of providers

• Big picture: we see a shift toward a more patient-centric industry

12

ACA Enrollees Choose Lower Premiums Now & Higher Patient Share Later

Source: American Action Forum. May 15, 2014.Late ACA Enrollment Dominated by Bronze and Silver Plans.http://americanactionforum.org/uploads/files/serialized_products/Weekly_Checkup_20140515.pdf

Avg. Silver Plan Deductibles:

$2,907 Individual; $6,078 Family% Covered: 70%

ACA Enrollees Are Opting for High-Deductible Plans

13

ACA Discourages Out-of-Network Care—But Patients May Not Understand That

• ACA regulations cap a patient’s annual out-of-pocket expense for in-network care.

• But the patient’s responsibility—and the hospital’s exposure—is unlimited for care delivered out-of-network.

• And nearly 4 in 10 non-group insurance enrollees (37%) in a recent study didn’t know the amount of their deductible.

• Source: Kaiser Family Foundation. Survey of Non-Group Health Insurance Enrollees. June 19, 2014. http://kff.org/health-reform/report/survey-of-non-group-health-insurance-enrollees/

14

Many Newly Insured Don’t Understand Basic Insurance Terms

Source: Public Understanding of Basic Health Insurance Concepts on the Eve of Reform. Urban Institute. Dec. 2013.http://hrms.urban.org/briefs/hrms_literacy.html

15

What Is OUR Responsibility,

Given the Patient-Centric Trend?

16

Hospitals Have a Role in Educating Newly Insured Patients

17

• * Estimate is statistically different from estimate for the previous year shown (p<.05). • NOTE: These estimates include workers enrolled in HDHP/SO and other plan types. Average general annual health plan deductibles for PPOs, POS• plans, and HDHP/SOs are for in-network services. • SOURCE: Kaiser/HRET Survey of Employer-Sponsored Health Benefits, 2006-2013.

Employees Are Also Sharing More Costs; Not Necessarily by Choice

Percentage of covered workers enrolled in a plan with a general annual deductible of $1,000 or more for single coverage, by firm size, 2006-2013

18

Even at higher income levels, collection yields on balances after insurance drop precipitously as balances increase

Balance: $0 - $250 Balance: $250 - $500 Balance: > $500FPL < 200% 200- 400% > 400%

FPL < 200% 200- 400% > 400%

FPL < 200% 200- 400% > 400%

60 Day 29.1% 38.0% 44.7% 22.9% 31.7% 38.9% 5.6% 9.6% 15.6%120 Day 37.2% 46.7% 54.1% 30.4% 40.4% 49.0% 7.5% 12.5% 19.9%180 Day 39.8% 49.2% 56.6% 33.9% 43.8% 52.6% 8.6% 14.0% 21.9%

360 Day 41.9% 51.4% 58.5% 37.5% 47.3% 56.2% 10.2% 16.0% 24.5%

75% Decline

Source: David Franklin; Connance; Patient Pay Collectability Data Study Review; March 14, 2014

Providers’ Collection Yields Fall as Balance After Insurance Increases

19

Dissatisfied Patients Are Less Likely to Pay

Source: Steve Levin, “What to Expect in Round Two of the Health Insurance Exchanges.” HFMA Revenue Cycle Strategist, Sept. 2014. http://www.hfma.org/Content.aspx?id=24697

20

How to Adopt a Patient-Centered Approach to Revenue Cycle

• Before (or at) the time of service

– Help patients understand what they will be expected to pay

• After the time of service

– Ensure that patients with unresolved accounts are treated fairly

• Throughout the time that patients are interacting with you

– Treat patients with empathy and respect

21

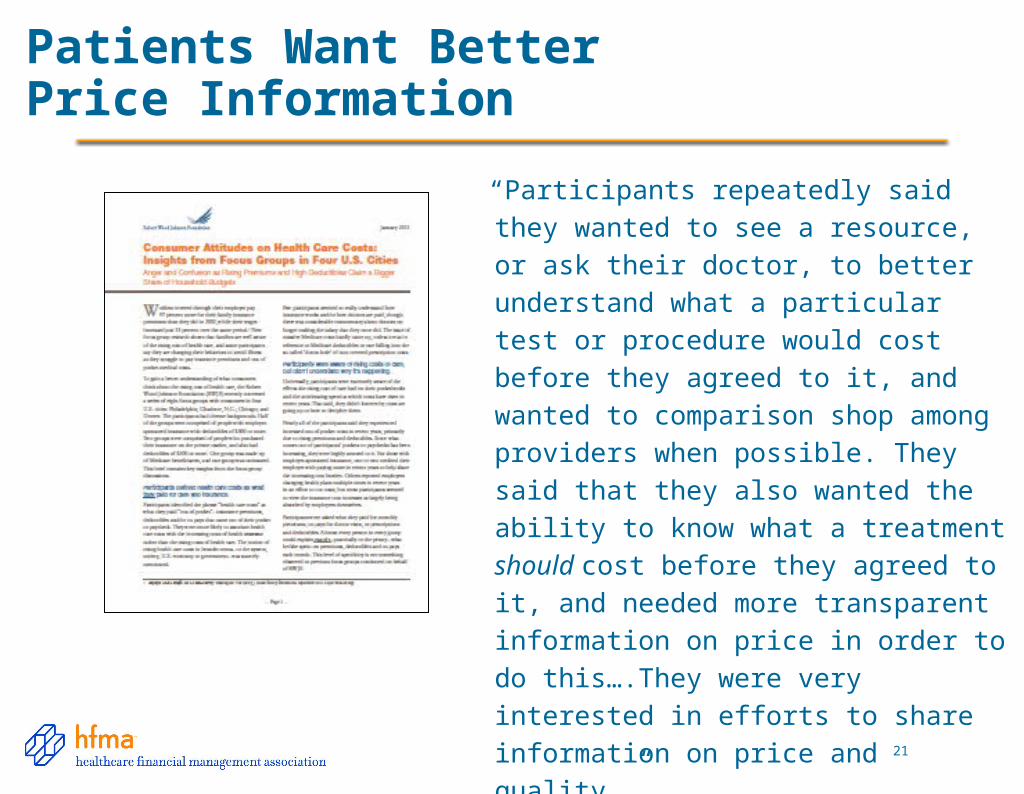

Patients Want Better Price Information

“Participants repeatedly said they wanted to

see a resource, or ask their doctor, to

better understand what a particular test or

procedure would cost before they agreed

to it, and wanted to comparison shop

among providers when possible. They said

that they also wanted the ability to know

what a treatment should cost before they

agreed to it, and needed more transparent

information on price in order to do

this….They were very interested in efforts

to share information on price and quality.”• Source: Robert Wood Johnson Foundation. Consumer Attitudes on Healthcare Costs: Insights from

Focus Groups in Four U.S. Cities. January 2013. http://www.rwjf.org/en/research-publications/find-rwjf-research/2013/01/consumer-attitudes-on-health-care-costs--insights-from-focus-gro.html

22

Our Payment System Was Not Designed for Price Transparency

• Historically, prices have served a wholesale function

• Only recently have prices been viewed as retail

• Without transparency, neither consumers nor hospitals could compare hospital prices

• With thousands of items, the chargemaster is not “transparency-friendly”—and not reflective of “price”

23

Would this be a reasonable pricing system for buying a truck? Yet , that is the system hospitals and doctors are REQUIRED to use

The Time Is Right for Price Transparency

In a system where. . .

– Charges are primarily used as a factor in a payment calculation

– Actual prices are essentially invisible to the consumer, and…

– Charges have little relationship to the service being acquired

. . . change is inevitable!

We all contributed to this situation—hospitals, physicians, payers, the business community, and even patients.

We all need to work together to fix it!

HFMA Resources to Help You Improve the Billing and Payment Experience for Patients

25

hfma.org/dollars

26

HFMA Price Transparency Task Force

27

HFMA Price Transparency Task Force Report

• Clarifies basic definitions that are often misused

• Sets forth guiding principles

• Establishes roles for payers, providers, others

• Reflects consensus of key stakeholders

hfma.org/dollars

Cost, charge, and price should not be used as interchangeable terms.

• Cost varies by the party incurring the expense.

• Charge is the dollar amount a provider sets for services rendered before negotiating any discounts.

• Price is the total amount a provider expects to be paid by payers and patients for healthcare services.

Definitions of Key Terms

28

Care Purchaser

• Individual or entity that contributes to the purchase of healthcare services.

Payer

• An organization that negotiates or sets rates for provider services, collects revenue through premium payments or tax dollars, processes provider claims for service, and pays provider claims using collected premium or tax revenues.

Provider

• An entity, organization, or individual that furnishes a healthcare service.

Definitions of Parties to a Transaction

29

An Actionable Definition of Price Transparency

Readily available information on the price of

healthcare services, that, together with other

information, helps define the value of those services

and enables patients and other care purchasers to

identify, compare, and choose providers that offer

the desired level of value.

30

Guiding Principles

Price transparency information should:

• Empower patients and other care purchasers to make meaningful price comparisons

• Be easy to use and easy to communicate

• Be paired with other information that defines the value of services for the care purchaser

• Enable patients to understand the total price of their care and what is included in that price

And price transparency will require the commitment and active participation of all stakeholders.

31

32

Roles for Key Stakeholders

• Health plans should serve as the principal source of price information for their members

• Providers should be the principal source of information for uninsured patients and out-of-network care

• Referring clinicians should use price information to benefit patients

• All stakeholders can offer a price information resource to consumers

33

• Health plans should serve as the principal source of price information for their members.

• Tools for insured patients should include:

– The total estimated price of the service

– A clear indication of whether a particular provider is in the health plan’s network

– A clear statement of the patient’s estimated out-of-pocket payment responsibility

– Other relevant information on the provider or service sought

Health Plan Role

34

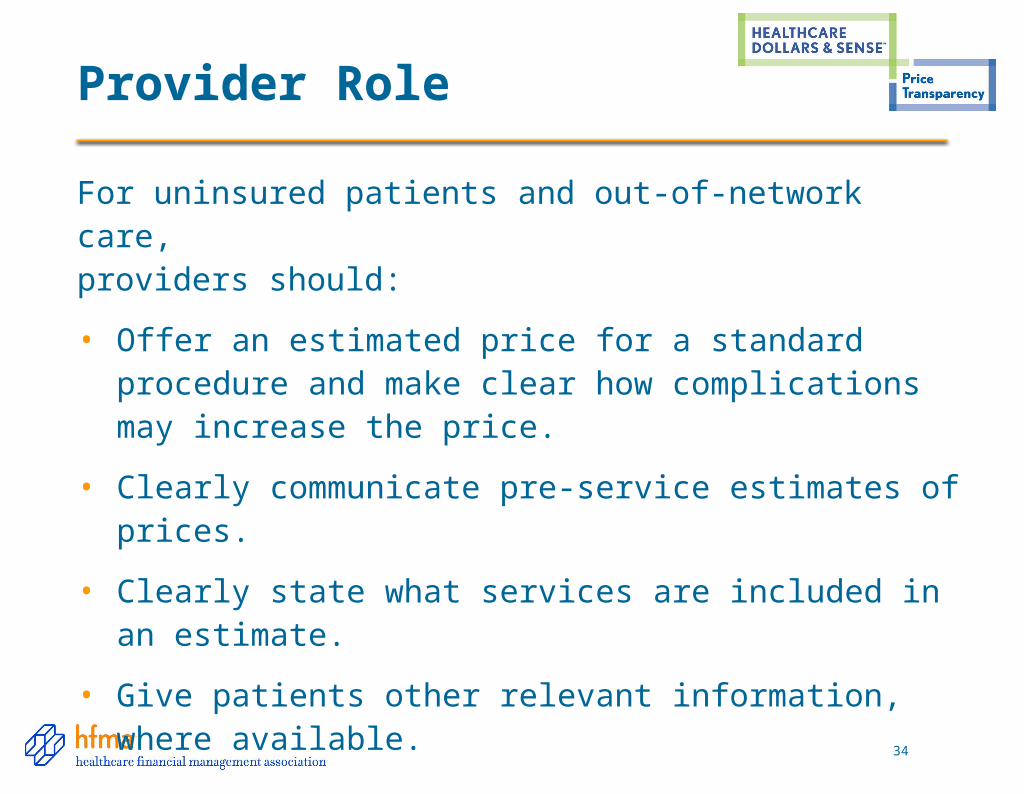

Provider Role

For uninsured patients and out-of-network care, providers should:

• Offer an estimated price for a standard procedure and make clear how complications may increase the price.

• Clearly communicate pre-service estimates of prices.

• Clearly state what services are included in an estimate.

• Give patients other relevant information, where available.

Referring Clinician Role

Physicians and other referring clinicians should

• Help patients make informed decisions about treatment plans

• Recognize the needs of price-sensitive patients

• Help patients identify providers that offer the best value

35

Employer Role

• Employers should continue to use and expand transparency tools that help their employees identify higher-value providers

• Self-funded employers should identify data that will help them

– Shape benefit design

– Understand their healthcare spending

– Provide transparency tools to employees

36

37

Pricing Resource for Consumers

• Describes how to request price

estimates, step by step

• Clarifies what estimates may or

may not include

• Explains in-network and

out-of-network care

• Defines key terms

• Available for posting on your

website at no charge

• Hardcopies available for purchase

in bulk at a nominal price through

AHA’s online storehfma.org/transparencyahaonlinestore.org

38

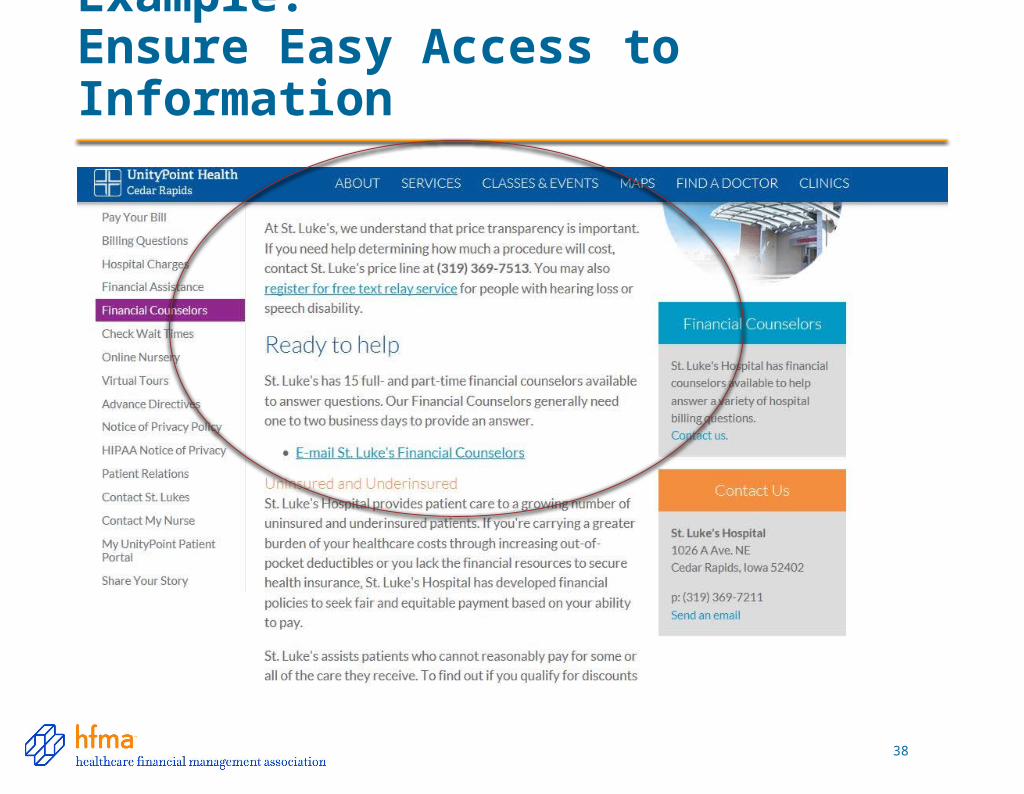

Example:Ensure Easy Access to Information

Example: Allow Patients to Search for Providers in Their Area

39

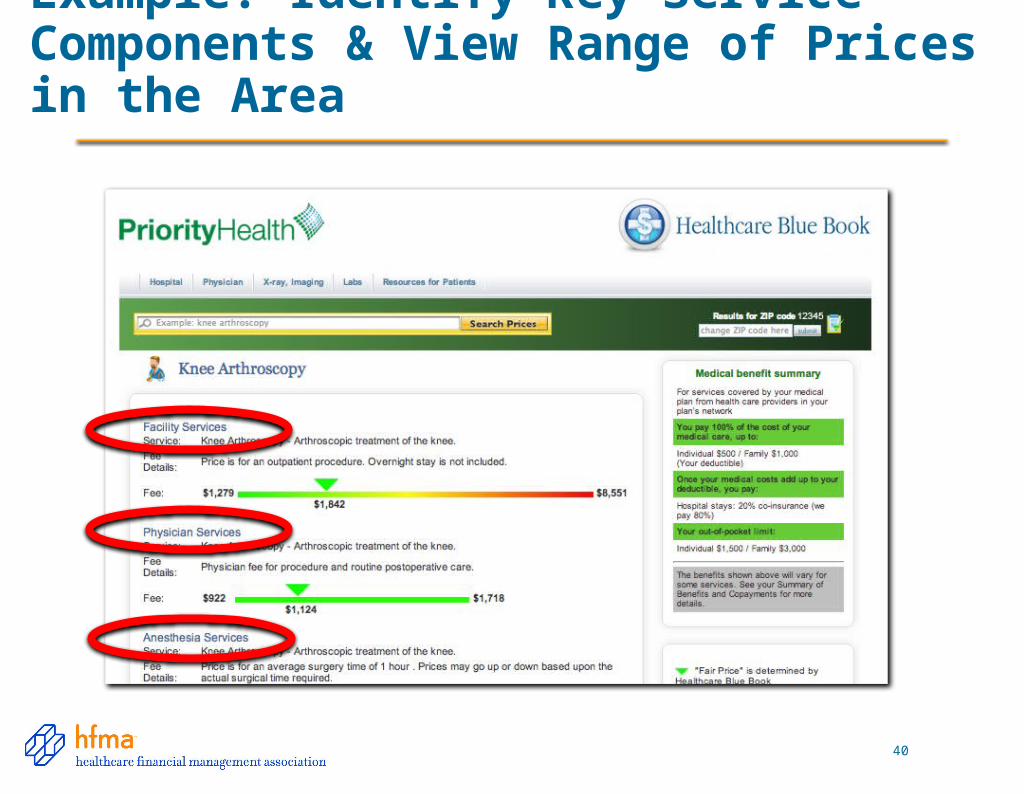

Example: Identify Key Service Components & View Range of Prices in the Area

40

Example: See List of Area Providers Ranked, Based on Relative Price

41

Example: Provide Simple, Clear Estimates for Self-Pay Patients

42

• Determining effect of transparency on prices

– For consumers, more transparency is better.

– But in the B2B marketplace, the jury is still out.

• Surfacing issues with out-of-network balance billing

– Inadvertent out-of-network use (e.g., anesthesiologists, pathologists)

– Emergency care

• Reassessing hospital chargemasters

– It is time for change!

Transparency Issues Yet to Be Addressed

43

Identify a reasonable starting point

Assess whether your pricing structure is transparency-ready

Consider how care purchasers will access the information you provide

Identify other information sources that will help patients assess the value of the services you provide.

Work on a collaborative basis with the payers in your market

Be prepared to explain healthcare pricing

Checklist for Preparing for Price Transparency

44

Price Transparency Is Just One Element of a Patient-Centered Approach

45

hfma.org/dollars

46

Every day, healthcare professionals conduct sensitive financial discussions with patients. But there have been no accepted, consistent best practices to guide them in these discussions—until now

hfma.org/dollars

Communication Is Critical Throughout the Process

47

What the Best Practices Cover

Provision of Care

Registration and Insurance

Verification

Financial Counseling

Patient Share

Prior Balances (if applicable)

Balance Resolution

48

Designed for the Most Needed Settings & Purposes

Emergency Department

Time of Service (Outside the

ED)

Advance of Service

Practices for All Settings

Measurement Criteria

Framework

49

Benefit Patients and Providers

• Encourage patients to talk with a financial counselor about any financial concerns

• Identify opportunities to locate additional or alternative insurance coverage

• Determine how accounts will be resolved through conversation

• Identify patients who fall under the 501(r) regulations

• Benefit from the public relations value of a satisfied consumer vs. an unhappy consumer

50

Achieve Recognition as an Adopter

• Recognition demonstrates commitment to best practices

• Based on HFMA review of an application and supporting documentation

• All provider organizations may apply

• Recognition valid for two years

• Adopters may use the phrase “Supporter of the Patient Financial Communications Best Practices” in their marketing materials

Best Practices for Medical Debt

• We want to find solutions that are balanced, fair, and reasonable.

• We keep patients informed about payment expectations and time frames.

• The business practices that we—and our business affiliates use—have been approved at the Board level.

51

By following the HFMA Best Practices for Medical Account Resolution, your organization is affirming that. . .

52

Selected Best Practices

• Educate patients and follow best practices for communication

• Make all bills and other communications clear, concise, correct, and patient-friendly

• Establish policies and make sure they are followed internally and by business affiliates

• Be consistent in key aspects of account resolution—from billing disputes to payment application

• Coordinate with business affiliates to avoid duplicative patient contacts

53

Selected Best Practices (cont.)

• Exercise good judgment about the best ways to communicate with patients about bills

• Start the account resolution clock when the first statement is sent to the patient

• Report back to credit bureaus when an account is resolved (in the event that an account is reported to a credit bureau)

• Track all consumer complaints.

• Draw on best practices, principles, and guidelines to inform your organization’s approach

54

hfma.org/dollars

55

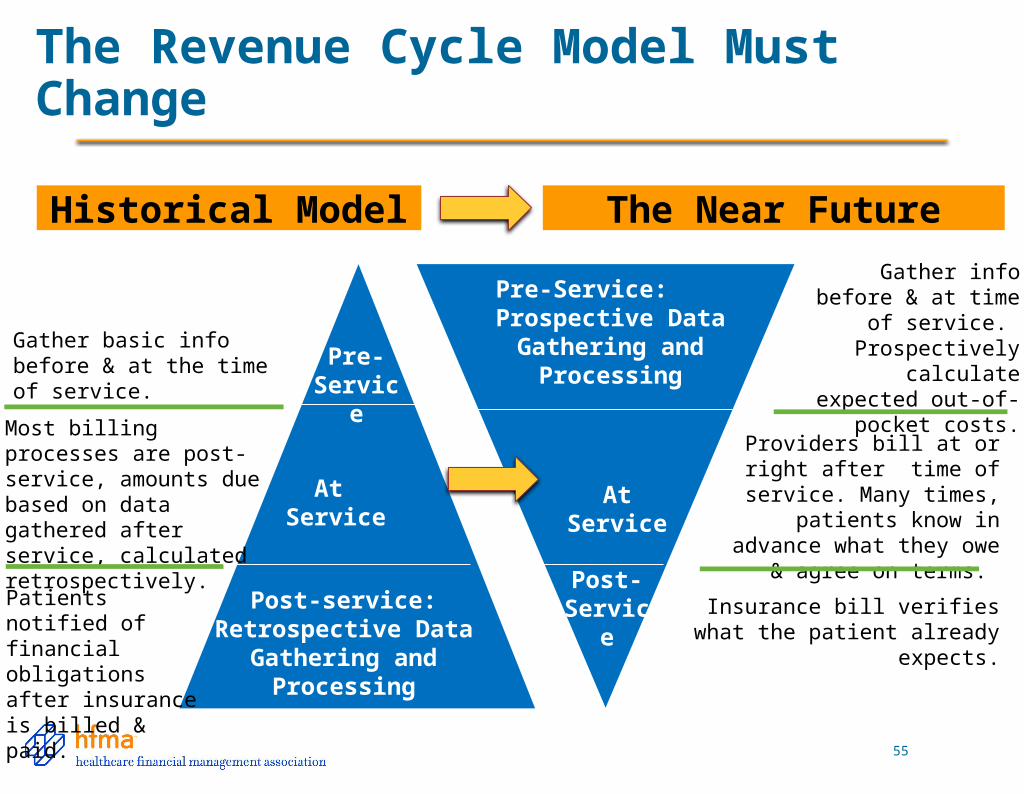

The Revenue Cycle Model Must Change

Historical Model The Near Future

Gather basic info before & at the time of service.

Most billing processes are post-service, amounts due based on data gathered after service, calculated retrospectively.

Patients notified of financial obligations after insurance is billed & paid.

Pre-Service

At Service

Post-service: Retrospective Data

Gathering and Processing

Pre-Service: Prospective Data

Gathering and Processing

At Service

Post-Service

Gather info before & at time of service.

Prospectivelycalculate expected out-

of-pocket costs.

Providers bill at or right after time of service. Many times,

patients know in advance what they owe & agree on

terms.

Insurance bill verifies what the patient already expects.

What we have before us are some breathtaking opportunities disguised as insoluble problems.

John GardnerSecretary, U.S. Department of Health, Education, and Welfare, 1965

• Logic will get you from A to B. Imagination will take you everywhere.

• Albert Einstein