sthree nidhi credit co-operative federation ltd. nidhi... · message stree nidhi credit cooperative...

TRANSCRIPT

Sthree Nidhi Credit Co-operative Federation Ltd.Regd. No. TFD No. 002/2014

Rural Development DepartmentGovernment of Telangana

AANNNNUUAALLRREEPPOORRTT

22001155--1166

MESSAGE

It gives me immense pleasure to note that Sthree Nidhi Credit Cooperative Federation Ltd.,

has been providing affordable and timely credit for the last few years and emerged as an

alternative to prevent high cost borrowings by the poor SHG members. Adoption of

technology not only enabled it to reach the poor effectively but also made it cost effective

and demonstrated how the organisations serving the poor can be self-sustainable with

innovative approaches. Stree Nidhi has emerged financially stronger and thus is in a

position to assist the poor and vulnerable effectively by meeting increased credit needs of

the poor for livelihoods.

Any SHG member in need of credit today prefers to approach Stree due to quick and hassle

free credit delivery where SHGs and their federations play a pivotal role. I am confident that

Stree Nidhi with new initiatives, aggressive posture towards financing livelihoods and

extending financial, Meeseva, and e-Panchayat services through One Stop Shop would

emerge as a household name in the service to poor. The role and involvement of

community and with its unique features of functioning made it possible for Stree Nidhi to

become a role model in the country. I also appreciate the efforts made by the community;

all the staff of Stree Nidhi, SERP and MEPMA for the active role played them in moulding the

institution to deliver services to the poor effectively.

On this occasion, I wish Stree Nidhi a success in providing hassle free financial services to

the poor which would enable it to scale greater heights and play a key role in expanding

outreach aimed at poverty alleviation.

Jupally Krishna Rao

Shri Jupally Krishna Rao, Hon’ble Minister, Panchayat Raj &Rural Development,Government of Telangana

Annual Report 2015-16 iii

MESSAGE

Stree Nidhi Credit Cooperative Federation Limited., has created niche space in the sphere

of microfinance in the country with its low cost credit delivery model and unique features.

Through its focus on the poorest of the poor it is able to ensure credit flow to the most

neglected sections of the society for alleviation of poverty.

Adopting technology and proper systems it is able to deliver credit within 48 hours from

the time loan is requested for, which is crucial for the poor. Stree Nidhi has been diversifying

and foraying into new services like insurance, business correspondents to facilitate financial

inclusion and to provide banking, Meseva and e-Panchayat services at the door step of

people. Its focus on livelihood financing is laudable as such an approach only would

mitigate poverty.

It is a self- sustainable, vibrant and dynamic community owned institution. It has grown

from strength to strength achieving a robust growth under all its business parameters year

after year emerging as a financially strong institution. It is a matter of great pride that Stree

Nidhi has been appreciated by NITI Aayog and is recognised by National Rural Livelihoods

Mission as a National Support Organisation to guide other states in establishment of

institutions on the lines of Stree Nidhi.

I congratulate all associated with the working of Stree Nidhi including SHG community for

their laudable role for positioning Stree Nidhi to help Self Help movement. On this occasion,

I wish Stree Nidhi all success in its endeavours to reach out to the poor and in their efforts

to reduce poverty.

S.P. Singh

Shri S.P. Singh, IASSpecial Chief Secretary, PR & RD

Government of Telangana

Annual Report 2015-16 v

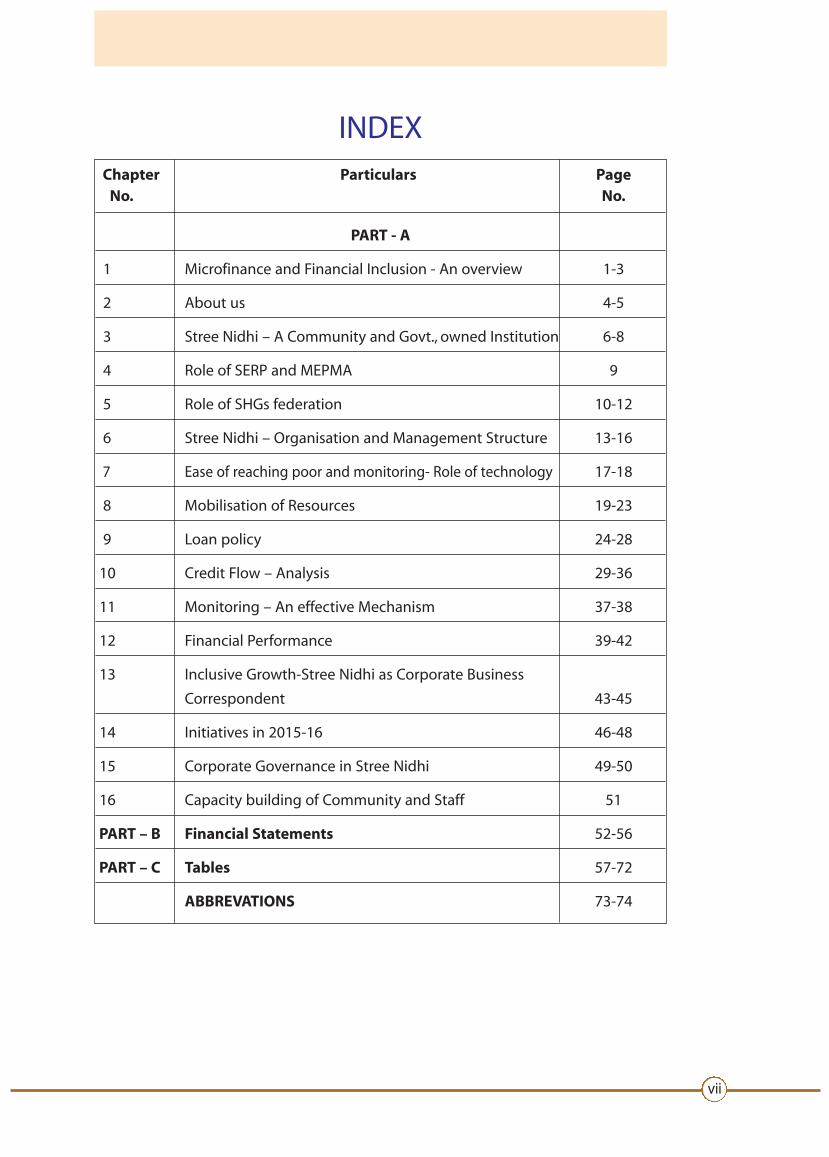

INDEXChapter Particulars Page No. No.

PART - A

1 Microfinance and Financial Inclusion - An overview 1-3

2 About us 4-5

3 Stree Nidhi – A Community and Govt., owned Institution 6-8

4 Role of SERP and MEPMA 9

5 Role of SHGs federation 10-12

6 Stree Nidhi – Organisation and Management Structure 13-16

7 Ease of reaching poor and monitoring- Role of technology 17-18

8 Mobilisation of Resources 19-23

9 Loan policy 24-28

10 Credit Flow – Analysis 29-36

11 Monitoring – An effective Mechanism 37-38

12 Financial Performance 39-42

13 Inclusive Growth-Stree Nidhi as Corporate Business

Correspondent 43-45

14 Initiatives in 2015-16 46-48

15 Corporate Governance in Stree Nidhi 49-50

16 Capacity building of Community and Staff 51

PART – B Financial Statements 52-56

PART – C Tables 57-72

ABBREVATIONS 73-74

Annual Report 2015-16 vii

Annual Report 2015-16 1

Chapter 1

M icrofinance and FinancialInclusion-An overview

Equitable growth, a core element of development economics is critical for long-termsustainability of economic prosperity and social development and micro finance hasan enormous role in this sphere.Micro finance would enable them to augment incomeand to emerge as the most effective way of reaching the poor.

The Govt. of India and Reserve Bank of India (RBI) have been taking measures tofacilitate financial services to the poor for inclusive development. While the PrimeMinister’s Jan Dhan Yogana (PMJDY) has enabled opening of bank accounts for thepoor for DBT purposes, RBI has ushered in a new set of reforms by giving licenses toSmall Finance Banks and Payment banks in addition to NBFC-MFI, creating an enablingenvironment to deliver services in niche areas.This multi-pronged approach is likely toinduce competition in expanding outreach and is expected to benefit the segment ofthe population, which require small loans and services.

With such a wide canvass for delivery of financial services whether the poor will getfinancial services, particularly micro financial services is an aspect to be watched withkeen attention. In all these endeavors, technology would play a paramount role asincrease in outreach to massive numbers and their monitoring hinges on use of costeffective and efficient technology. The Govt. of India as also State Governments havebeen laying emphasis on Digital India focusing on digital literacy and on providinginternet services to nook and corners of the country. Availability of information andknowledge would play a critical role in ameliorating the lives of the poor.

While disruptive technologies continue to emerge for the benefit of communityincluding mobile banking, internet banking, UPI, bio metric based payment system,linking with Aadhar for facilitating transactions etc., some element of human touch willbe of great relevance in respect of the poor as credit plus approach requiresunderstanding of the conditions of the poor and appropriate solutions. Moreorganized efforts in convergence with Govt. are considered necessary in this direction

Sustainable development Goals provide for ending poverty in all its form fromeverywhere and empowerment of women by 2030. The 17 Sustainable DevelopmentGoals, inter alia, include poverty reduction, empowerment of women, gender equalityetc., It is agreed to reduce at least by half the proportion of men, women and childrenof all ages living in poverty in all its dimensions. Progressively, we have to strive toachieve sustainable income growth of the bottom 40 per cent of the population at arate higher than the national average.

Implementation of appropriate social protection systems, achieving substantialcoverage of the poor and the vulnerable with appropriate financial services, includingmicrofinance is expected to build resilience of the poor and vulnerable to face

Sthree Nidhi2

economic, social,environmental shocks and disasters.Environment degradation affectsthe poor more than anybody else as they lose livelihoods. SDG envisages doubling theagricultural productivity and incomes of small-scale food producers, in particularwomen, provide skills and financial services, markets and opportunities for valueaddition and for non-farm employment.

Microfinance is a powerful tool to achieve the above objectives as it has been playingan important role in helping the poor to meet their exigent, working capital andinvestment needs for taking up livelihoods. However, more important aspects aretimely, adequate and affordable credit delivery, which are basic tenets of any efficientcredit delivery system. It is a paradox that poor who need low cost credit pay high rateof interest on loans accessed either frommoney lenders or MFIs while the other well todo segment get loans even for consumption at low interest rates on the asumptionthat the former are more risky. The notion that poor need small amount of credit andtherefore they are interest rate insensitive needs to be looked at afresh as "Interestsaved is money earned” which not only makes activities viable but also is need of thehour for poor segment of the society.

Reaching out banking services to the poor at their door step is imperative eitherthrough technology directly or with the help of business correspondent as anintermediary. While movement towards digital banking by the poor would take somemore time, extension of these services through Business correspondent assumessignificant importance as it would reduce real cost of transaction and also facilitatecredit and saving services to the poor expeditiously.

SHG bank linkage

Self Help Group- Bank linkage programme in the country which is the largestmicrofinance programme in the world, has an outreach of 10.1 cr householdsorganised into 79 lakh SHGs. The increase in loan disbursement by banks to SHGs,during the year 2015-16 was 35% taking it to Rs.37,287 crore as compared to Rs.27,582crore during the previous year. The average loan disbursement per group during2015-16 was Rs 2.03 lakh which showed a healthy increase of 20% from Rs 1.69 lakhduring 2014-15. The Gross NPAs as on 31 March 2016 were Rs. 3686.2 crore, whichwitnessed a decline from Rs. 3814.7 crore a year back. The gross NPAs in bank loans toSHGs declined from 7.4% in 2014-15 to 6.4% in 2015-16.

In the State of Telangana, there are about 5 lakh SHGs both in rural and urban area,covering about 60 lakh poor women. The credit flow from banks to these SHGs wasabout Rs 7000 cr in 2015-16 while loan outstanding was about Rs. 9000 cr. It isestimated that credit demand from these members would be about Rs. 30000 crleaving a huge gap to be met.

Despite spectacular progress under SHG Bank linkage Programme, a large section ofthe poor population still remain excluded and those who are covered are not able toget adequate credit to take up sustainable livelihoods and this is the biggest challengemaking it imperative for micro finance institutions to play a role particularly those whopurvey credit and other financial services cost effectively.

Annual Report 2015-16 3

MFI disbursements

It has been reported that annual growth in the credit disbursed by MFIs in the lastthree years was about 50%, which increased from Rs. 23682 cr in 2013-14 to Rs. 61860cr in 2015-16. Of this amount, the 8 SFB licensees account for a portfolio of Rs. 23,553cr.The provisional estimate of clients served by MFIs as the end of March 2016 was 476lakhs, out of which nearly 135 lakhs are being served by already licensed SFBs. Thisleaves huge space for expansion of MFIs. The growth witnessed by MFI sector since2010 is an indication of the absorption capacity and potential for such type of lendingproviding opportunity for not-for profit MFIs, i.e. NGO-MFIs,Mutuals/Cooperatives andSection 8 Companies which have high level of operational efficiency. It is pertinent tomention that microfinance services in one form or other exist even in advancedcountries as poverty is relative.

Need to support institutions like Stree Nidhi

Stree Nidhi model facilitates low cost, timely and affordable credit to the poor. It is acommunity driven model, where SHG federations are stake holders along with theState Govt., and the former provide last mile connectivity and play an important role inmanaging operations of Stree Nidhi. SHG federations and SHGs themselves decide theeligibility as per the loan terms and conditions stipulated by Stree Nidhi throughparticipatory approach. It is also helping in strengthening the SHGs and theirfederations. Stree Nidhi is focussing on promotion of livelihoods and is supplementingthe efforts of SERP in financing Farmers Producers Groups/Activity Groups, which takeadvantage of collective action.

Stree Nidhi has unique model of credit delivery in the country where banking sectoralso plays a supporting role. Technology is a major plank facilitating ease of reachingthe poor and monitoring. Considering the strengths of Stree Nidhi, NRLM/GOI haveappointed Stree Nidhi as a National Support Organisation for providing support inimplementation of appropriate credit delivery model on the lines of Stree Nidhi in fivestates of the country.This speaks volumes of theway the institution evolved itself in thelast few years rendering service to the poor.

Stree Nidhi has a major role in alleviation of poverty in the State of Telangana andwould make earnest efforts in this direction by bringing innovations and customizingloan products and services. It will also associate with implementation of Govt.programmes like NREGA promoted LIFE and also with line departments for financinglivelihoods including those aimed at soil and moisture conservation, ecologicalbalance, animal husbandry and other farm and non-farm activities. Stree Nidhi wouldalso focus on financing Farmers’ Producers Groups for livelihoods. It will adopt Villagesfor development through credit.

Along side, it will also endeavor to foray into micro insurance services to the poor,promote financial inclusion and delivery of financial services through BusinessCorrespondent channel.The focus will also be on use of technology, e- KYC,mobile andother digital platforms to make the delivery of financial services more efficient andtransparent.

Sthree Nidhi4

Chapter 2

About us

2.1. Stree Nidhi Credit Co-operative Federation Ltd., is an apex society at state levelestablished on 07.09.2011,promoted jointly by the federations of SHGs namelyMandalSamakhyas and Town Level Federations and the State Government. Later on, as per A.PState Reorganisation Act’ 2014 Stree Nidhi, Telangana was registered on 26.05.2014 asa separate institution and functioning as a separate entity in Telangana State from02.06.2014.

2.2. Stree Nidhi is a community owned financial institution actively engaged inproviding financial services viz. credit, savings and banking services as BusinessCorrespondent to the poor in the state. Stree Nidhi laid a strong foundation to extendrequired credit in time for micro enterprises taken up by the poor, at an affordable rateof interest without any hassles to enhance their income earning capacities. This ispossible with the active support of State Govt., Society for Elimination of Rural Poverty(SERP) and Mission for Elimination of Poverty in Municipal Areas (MEPMA) working forelimination of poverty in rural and urban areas respectively.

Vision:

2.3.To ensure economic empowerment of the poor and emerge as a one stop shop atvillage / slum level for providing a wide spectrum of financial and other services intime, at an affordable cost with emphasis on livelihoods to augment incomes of thepoor.

Mission:

2.4. To reach out to members of SHGs and their families in need of credit and otherfinancial services, with focus on livelihoods, minimise reliance of community on highcost borrowing and strengthening SHGs and their federations leveraging technology.

Business Mix

Annual Report 2015-16 5

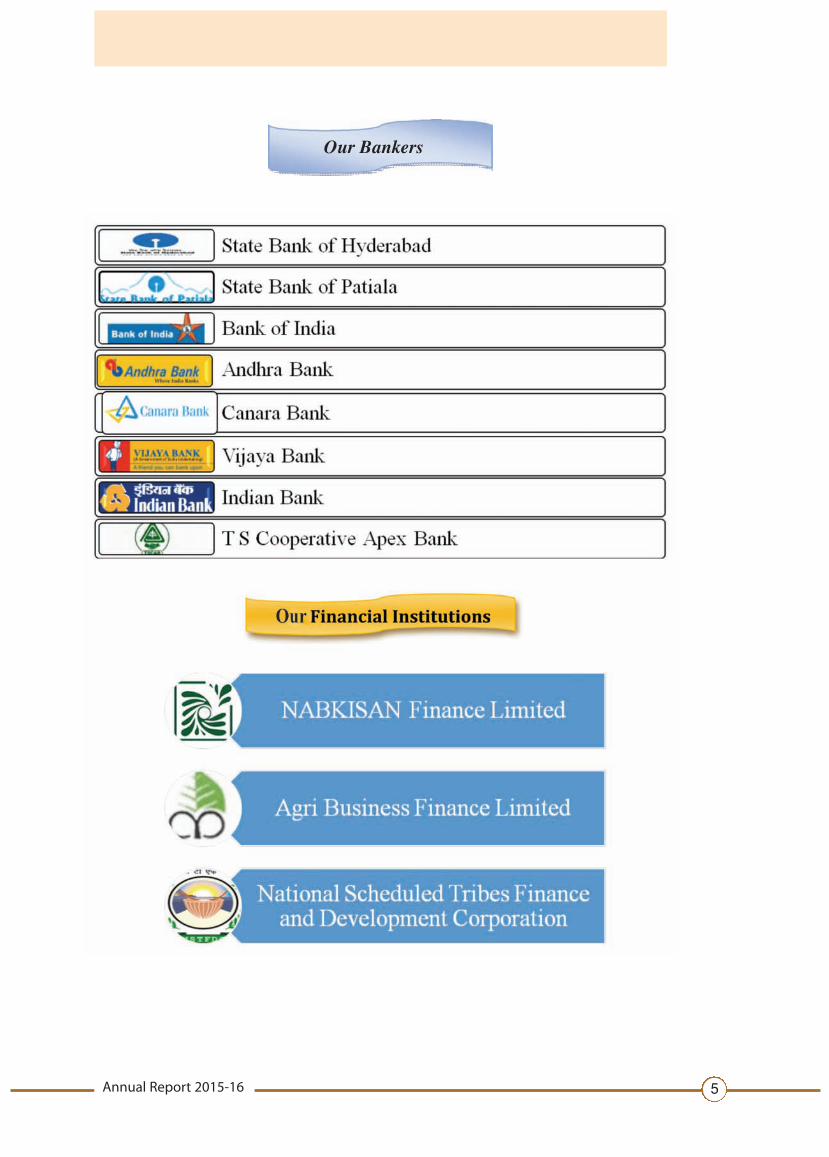

Our Bankers

Sthree Nidhi6

Chapter 3

Stree Nidhi- Jointly owned bycommunity and Govt.

3.1. The MFIs in the erstwhile state of Andhra Pradesh had exploited the vulnerabilityof the poor pumping credit and such irresponsible lending at usurious rates of interestresulted in debt trap and to recover such dues and unethical practices were adoptedaffecting their self-respect driving some of them to commit suicide. To put a halt tosuch practices of MFIs, the State Govt. regulated the operations of MFIs through anordinance in October 2010,which has resulted in stoppage of their lending operationsin the State.

3.2. Poor require low cost credit, in time and in a hassle free manner. However, in theabsence of such an arrangement they resort to high cost borrowings from moneylenders and others. Real cost of borrowing and inadequate credit flow from bankingsector is a cause of concern. A need therefore, was felt to create a suitable financialinstitution to provide required credit to poor with low operational cost by adoption ofappropriate technology.

3.3. In order to fill the credit gap and to ensure availability of timely and affordablecredit to poor individuals and households, whose access to credit has been affecteddue to cessation of lending byMFIs in the State, theMandal Samakhyas andTown LevelFederations in association with the State Government have promoted Stree NidhiCredit Co-operative Federations Ltd.,

Objectives:

3.4.The main objectives of Stree Nidhi are as under:

a. To provide low cost credit to the SHG members expeditiously using technologyand supplement credit flow from banking sector

b. To promote and finance livelihoods to generate income and alleviate poverty.

c. To work for the socio economic upliftment of the members of Self Help Groups inRural and Urban area.

Non-Availbility of Timelyand adequate credit

Usurious interest rates frommoney lenders and MFIs andCoercive methods of recovery

Credit to meet recurringcredit needs of the poor

not available

Providing low costcredit

Emergence of Stree Nidhi

Annual Report 2015-16 7

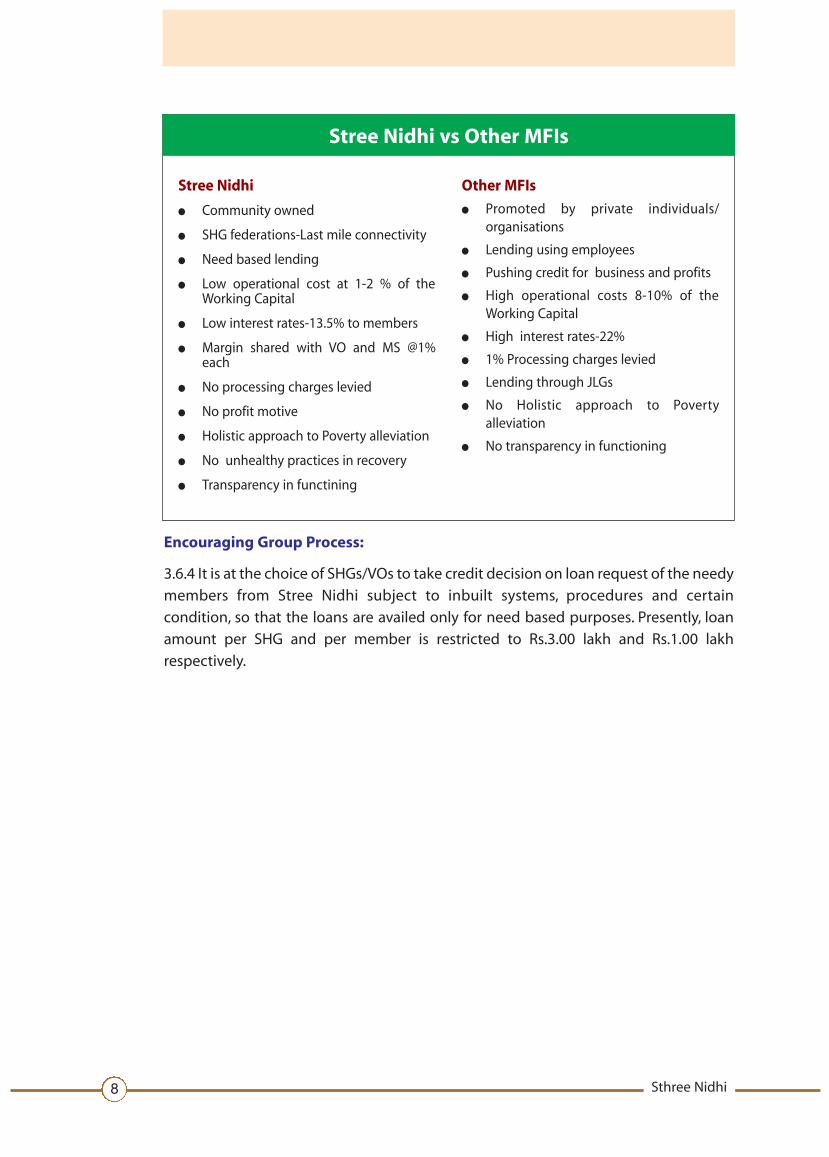

Stree Nidhi is different from other MFIs:

3.6.1. Stree Nidhi is owned by community as the federations of SHGs namely MS andTLF having contributed to Share Capital along with State Government. Community isrepresented on the Board and participate in decision making.The focus is not on profitmaking but on working for the poor.

Low operational cost:

3.6.2. Leveraging technology in operations enables Stree Nidhi to keep the operationalcost at low level unlike carrying out operations through brick & mortar branches. StreeNidhi uses the presence of VO/MS and SLF/TLFs nurtured by SERP and MEPMArespectively for providing last mile connectivity, by paying service charges. Theyfacilitate the members/SHGs in accessing credit either through mobile or web basedapplications. The operational cost is less than 1% of working funds as against 8-10% incase of other MFIs.

Affordable rate of Interest:

3.6.3. Being a cost effective financial institution, interest rate charged to SHG members

is presently at 13.5% per annum. Further, out of the above interest realised at this rate,

1.25% is passed on to VOs, SLFs and 1% to MSs, TLFs to compensate their services

towards monitoring operations of Stree Nidhi and for strengthening the federations.

Thus, the effective rate of interest charged by Stree Nidhi is less than that of RRBs in the

State and is comparable to the rates charged by the commercial banks under SHG-

Bank linkage programme. The burden of interest is low to the borrower as compared

to the interest charged by private MFIs, which is around 21-22%.

Communityowned and

managed financialinstitution

Use oftechnology for

speedy delivery ofservices and realtime monitoring

Making SHGFederations aspartners in

development

Creditdisbursementin 48 hours

Householdlevel planning toestablish incomegenerating Microand tiny activities

Providingsourcing ofavenues tothe poor

Specificallocation of creditto the poorest of

the poor

Riskmitigation and

insurance

Enforcing creditdiscipline andresponsiblelendering

Financialinclusion through

BusinessCorrespondent

StreeNidhi

3.5. Unique features of Stree Nidhi

Sthree Nidhi8

Encouraging Group Process:

3.6.4 It is at the choice of SHGs/VOs to take credit decision on loan request of the needy

members from Stree Nidhi subject to inbuilt systems, procedures and certain

condition, so that the loans are availed only for need based purposes. Presently, loan

amount per SHG and per member is restricted to Rs.3.00 lakh and Rs.1.00 lakh

respectively.

Stree Nidhi

� Community owned

� SHG federations-Last mile connectivity

� Need based lending

� Low operational cost at 1-2 % of theWorking Capital

� Low interest rates-13.5% to members

� Margin shared with VO and MS @1%each

� No processing charges levied

� No profit motive

� Holistic approach to Poverty alleviation

� No unhealthy practices in recovery

� Transparency in functining

Other MFIs

� Promoted by private individuals/organisations

� Lending using employees

� Pushing credit for business and profits

� High operational costs 8-10% of theWorking Capital

� High interest rates-22%

� 1% Processing charges levied

� Lending through JLGs

� No Holistic approach to Povertyalleviation

� No transparency in functioning

Stree Nidhi vs Other MFIs

Annual Report 2015-16 9

Chapter 4

Role of SERP and MEPMASociety for Elimination of Rural Poverty (SERP)

4.1 SERP is an autonomous society, promoted by the State Government and registeredunder Societies Act, headed by an IAS officer. SERP evolves and implements multi-dimensional poverty alleviation strategy by extending sensitive support to theinstitutions of the poor in rural area. SERP focusses on creation and strengthening ofstrong network of SHGs and their federations of poor viz. Village Organisations atvillage level, Mandal Samakhyas at Mandal level and Zilla Samakhyas at District level.SERP has about 4000 staff positioned in the field and striving hard to alleviate ruralpoverty by facilitating credit flow under SHG Bank linkage programme.They play a keyrole in motivating the SHGs to take up livelihoods which generate incremental incomeon a sustainable basis and provide safety nets and entitlements. SERP also plays a keyrole in various activities for promotion of livelihoods both under farm and non-farmsector including promotion of producers organisations, implementation of flagshipprogrammes of the State Govt. like Aasara Pension, Haritha Haram, Swatcha BharathMission,Abhaya Hastham,etc., SERP through SHG federations also procures agricultureproduce from farmers and helps in better market price through transparent systems.SERP implements economic support schemes for the benefit of the poor like SCSP,TSP,IWMP, NRLM with Stree Nidhi as a Channelising agency and also extends insurancefacilities to cattle through Call centers at Zilla Samakhyas.

4.2. SERP is instrumental and playing a major role and provides back support to StreeNidhi in mobilising savings from SHGs, facilitating required credit flow and monitoringthereof. They not only help in credit flow for taking up micro and tiny enterprises butalso assist in grading of institutions,prompt repayment of loans in coordination withstaff of Stree Nidhi.

Mission for Elimination of Poverty in Municipal Areas (MEPMA)

4.3. Stree Nidhi extends financial services to SHGs promoted by MEPMA. For evolvingsuitable strategies to alleviate poverty in urban area,and to implement the same, theGovernment has established a Mission for Elimination of Poverty in Municipal Areasheaded by an IAS officer.MEPMA is facilitating poor in urban areas in formation of SHGsand their organisation into federations at Slum level and Town level. It is playing a keyrole in implementation of SHG- Bank linkage programme in urban areas through theirstaff under the leadership of Project Directors located at District Head Quarters. TheStaff are actively involved in ensuring delivery of financial services of Stree Nidhi. Theyextend support in effective monitoring of credit flow and repayment of loans.

4.4. Stree Nidhi is working in tandem with SERP and MEPMA, to provide financialservices along with other services in an integrated manner to have synergetic effect.

Sthree Nidhi10

Chapter 5

Role of SHGs federations5.1. In the State of Telangana, 4.41 lakh SHGs were promoted and nurtured by SERP inrural area and 0.93 lakh SHGs were promoted in municipal and urban areas by MEPMAexcluding SHGs in GHMC area. In rural area, about 20-30 SHGs have federated intoVillage Oraganisation (VO) and likewise in urban area into Slum Level Federations(SLF). About 20-30 VOs and SLFs are federated at Mandal Level as Mandal Samakhyas(MSs) and at town level as Town Level Federations (TLFs) respectively. These are legalentities registered under Mutually Aided Co-operative Societies Act (MACS Act)’1995.

5.2. The VOs and SLFs play a key role in providing last mile connectivity, facilitatingmembers to avail the services of Stree Nidhi, monitoring performance and implementall other activities of Stree Nidhi and thus function like branches of Stree Nidhi atvillage and town level. District wise data relating to no. of members, SHGs,VOs/SLFs &MS/TLFs are furnished in Table no.1 & 2 of part-C appended to this report.

Pattern of affiliation of SHGs to their federations

5.3. The no. of SHGs affiliated to each VO/SLF varies. The following is the pattern of

affiliation of SHGs in VOs/SLFs.

Classification SERP MEPMA

of SHGs (No of VOs) (No of SLFs)

up to 4 SHGs 129 80

5-10 SHGs 1602 233

11-15 SHGs 2448 430

16-20 SHGs 3046 851

21-25 SHGs 3619 802

26-30 SHGs 3270 575

31-35 SHGs 2153 278

36-40 SHGs 1155 119

41 above SHGs 1092 60

Total: 18514 3428

Annual Report 2015-16 11

Grading of SHG Federations:

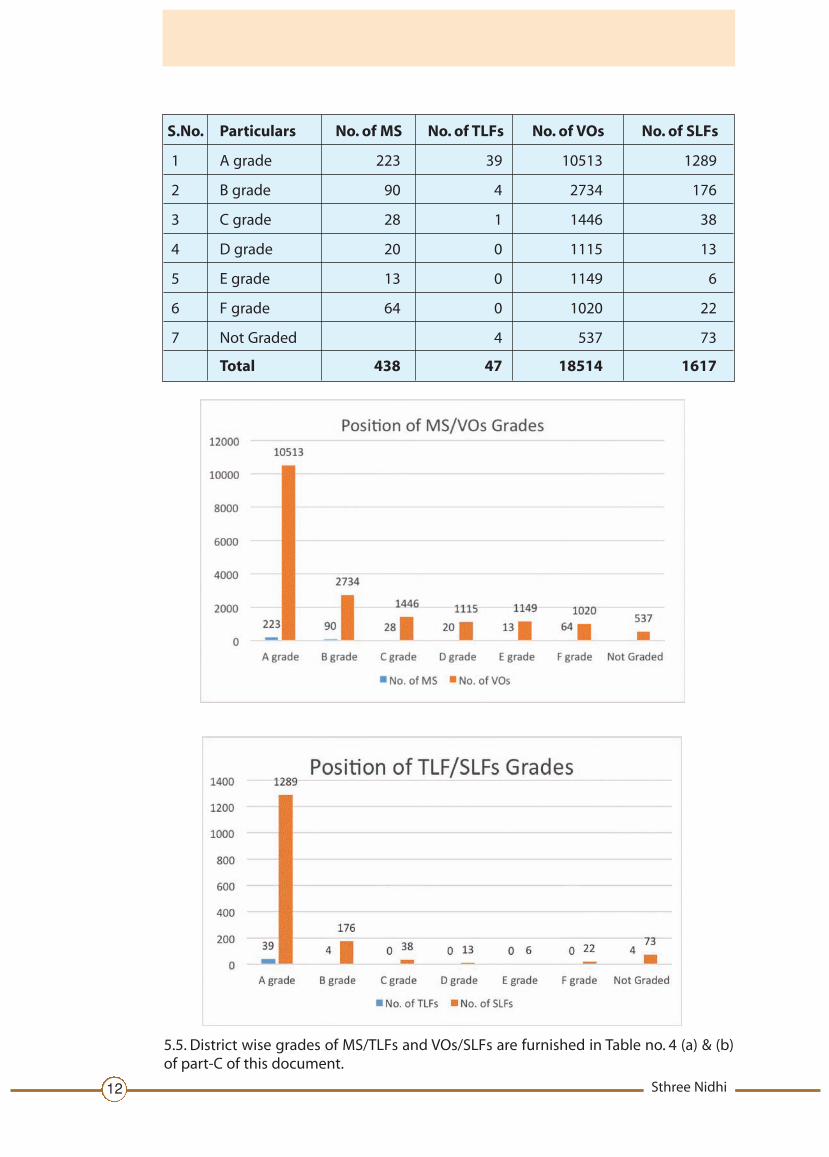

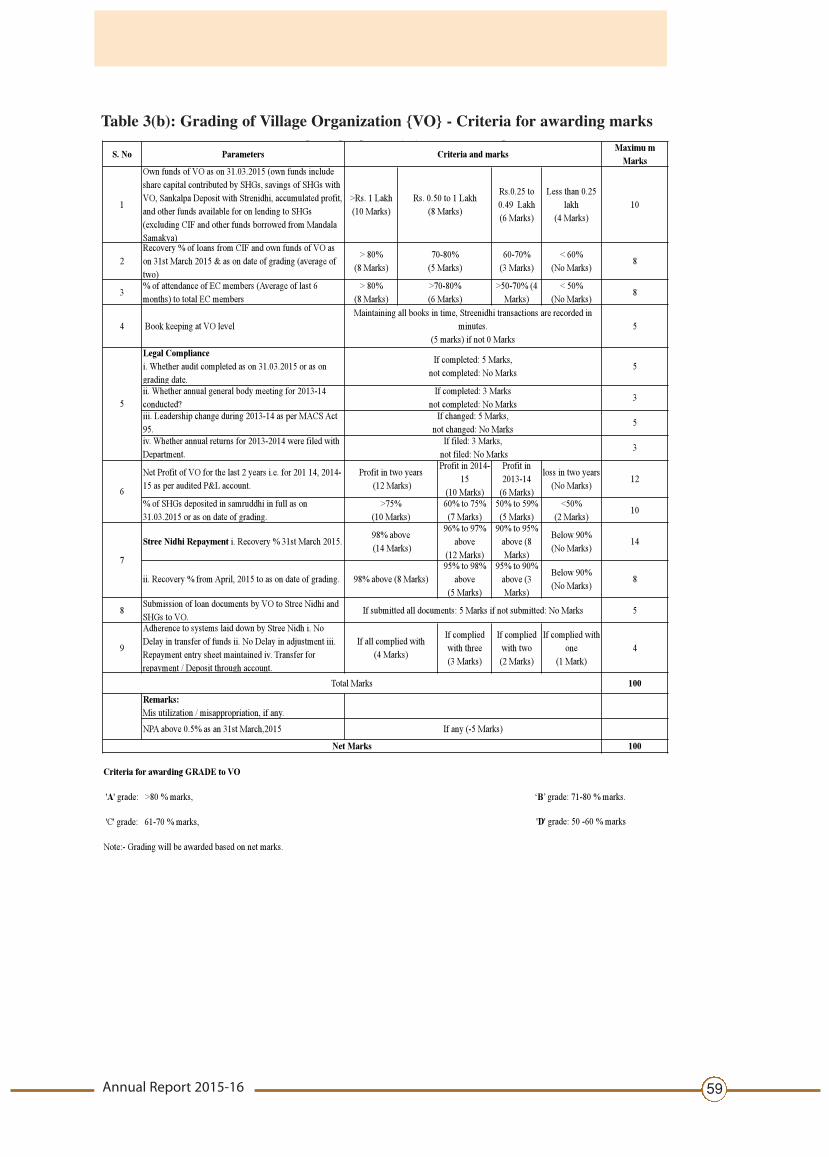

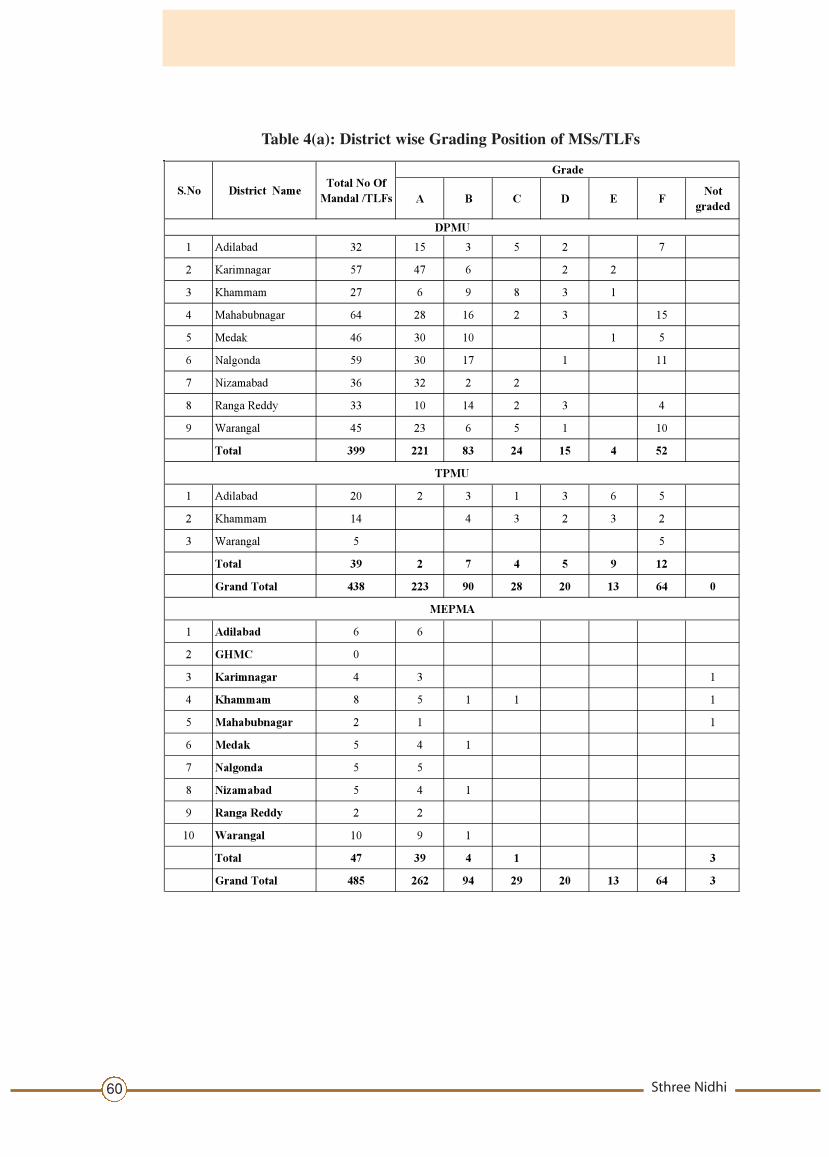

5.4. Stree Nidhi is allocating credit limits to VOs/SLFs, depending on rating secured bythem. The federations namely VOs/SLFs/MSs/ TLFs are subjected to grading processannually on completion of their yearly audit. While grading, the performance isassessed under key parameters namely owned funds, net profit earned, legalcompliance,percentage of attendance in the ECmeetings, recovery performance,bookkeeping, etc., The criteria followed for grading purpose are given in Table 3(a) & 3(b) ofPart-C of this report. Based on the scoring, the institutions are graded in to A, B, C, D , Eand F category. The status of grades of MSs/TLFs and VOs/SLFs as on 31.03.2015 is asunder.

Sthree Nidhi12

S.No. Particulars No. of MS No. of TLFs No. of VOs No. of SLFs

1 A grade 223 39 10513 1289

2 B grade 90 4 2734 176

3 C grade 28 1 1446 38

4 D grade 20 0 1115 13

5 E grade 13 0 1149 6

6 F grade 64 0 1020 22

7 Not Graded 4 537 73

Total 438 47 18514 1617

5.5. District wise grades of MS/TLFs and VOs/SLFs are furnished in Table no. 4 (a) & (b)of part-C of this document.

Annual Report 2015-16 13

Chapter 6

Stree Nidhi – Organisation andManagement Structure

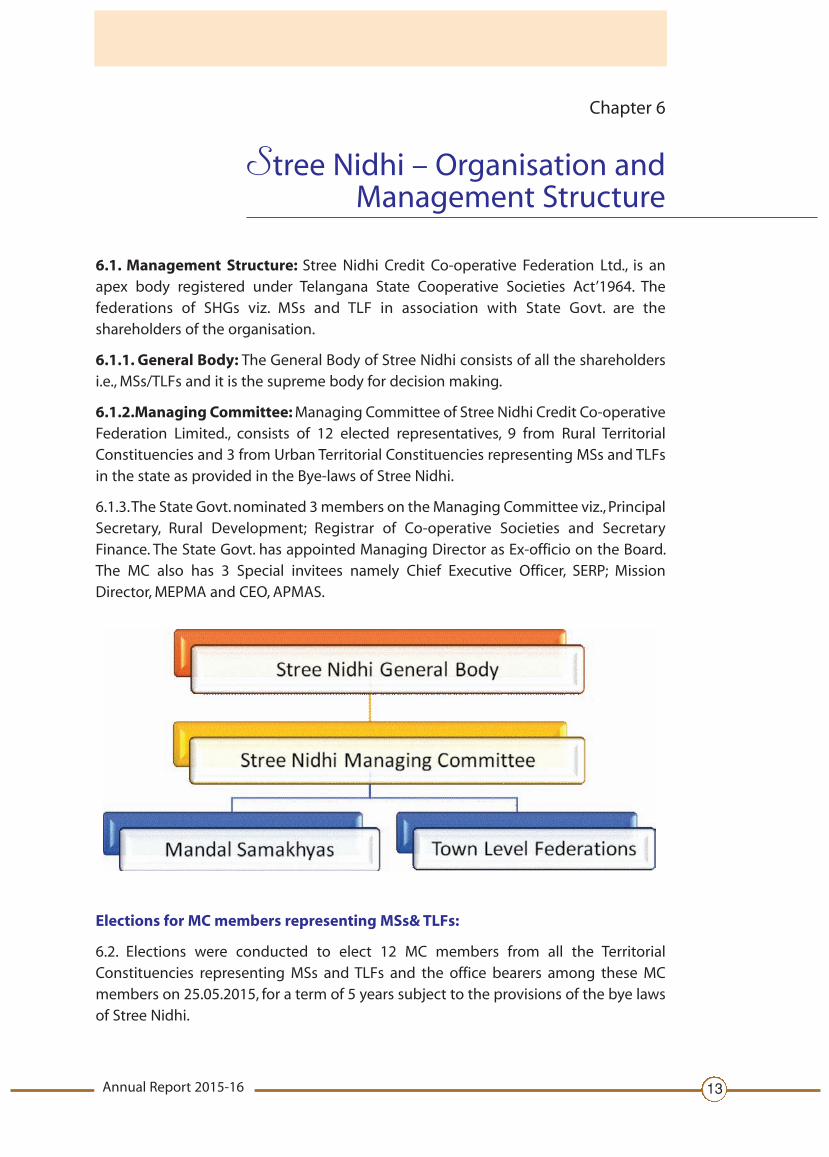

6.1. Management Structure: Stree Nidhi Credit Co-operative Federation Ltd., is anapex body registered under Telangana State Cooperative Societies Act’1964. Thefederations of SHGs viz. MSs and TLF in association with State Govt. are theshareholders of the organisation.

6.1.1. General Body: The General Body of Stree Nidhi consists of all the shareholdersi.e., MSs/TLFs and it is the supreme body for decision making.

6.1.2.Managing Committee:Managing Committee of Stree Nidhi Credit Co-operativeFederation Limited., consists of 12 elected representatives, 9 from Rural TerritorialConstituencies and 3 from Urban Territorial Constituencies representing MSs and TLFsin the state as provided in the Bye-laws of Stree Nidhi.

6.1.3.The State Govt.nominated 3members on theManaging Committee viz., PrincipalSecretary, Rural Development; Registrar of Co-operative Societies and SecretaryFinance. The State Govt. has appointed Managing Director as Ex-officio on the Board.The MC also has 3 Special invitees namely Chief Executive Officer, SERP; MissionDirector,MEPMA and CEO, APMAS.

Elections for MC members representing MSs& TLFs:

6.2. Elections were conducted to elect 12 MC members from all the TerritorialConstituencies representing MSs and TLFs and the office bearers among these MCmembers on 25.05.2015, for a term of 5 years subject to the provisions of the bye lawsof Stree Nidhi.

Sthree Nidhi14

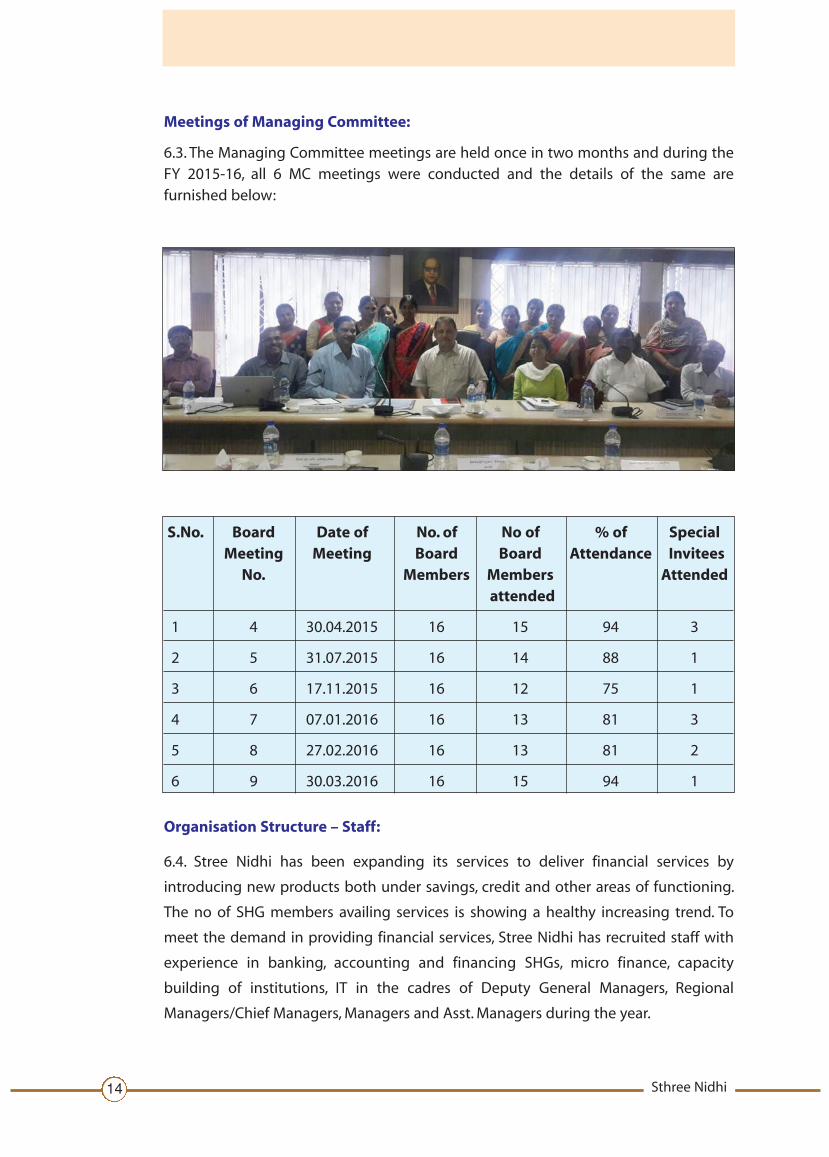

Meetings of Managing Committee:

6.3. The Managing Committee meetings are held once in two months and during theFY 2015-16, all 6 MC meetings were conducted and the details of the same arefurnished below:

S.No. Board Date of No. of No of % of SpecialMeeting Meeting Board Board Attendance Invitees

No. Members Members Attendedattended

1 4 30.04.2015 16 15 94 3

2 5 31.07.2015 16 14 88 1

3 6 17.11.2015 16 12 75 1

4 7 07.01.2016 16 13 81 3

5 8 27.02.2016 16 13 81 2

6 9 30.03.2016 16 15 94 1

Organisation Structure – Staff:

6.4. Stree Nidhi has been expanding its services to deliver financial services by

introducing new products both under savings, credit and other areas of functioning.

The no of SHG members availing services is showing a healthy increasing trend. To

meet the demand in providing financial services, Stree Nidhi has recruited staff with

experience in banking, accounting and financing SHGs, micro finance, capacity

building of institutions, IT in the cadres of Deputy General Managers, Regional

Managers/Chief Managers,Managers and Asst.Managers during the year.

Annual Report 2015-16 15

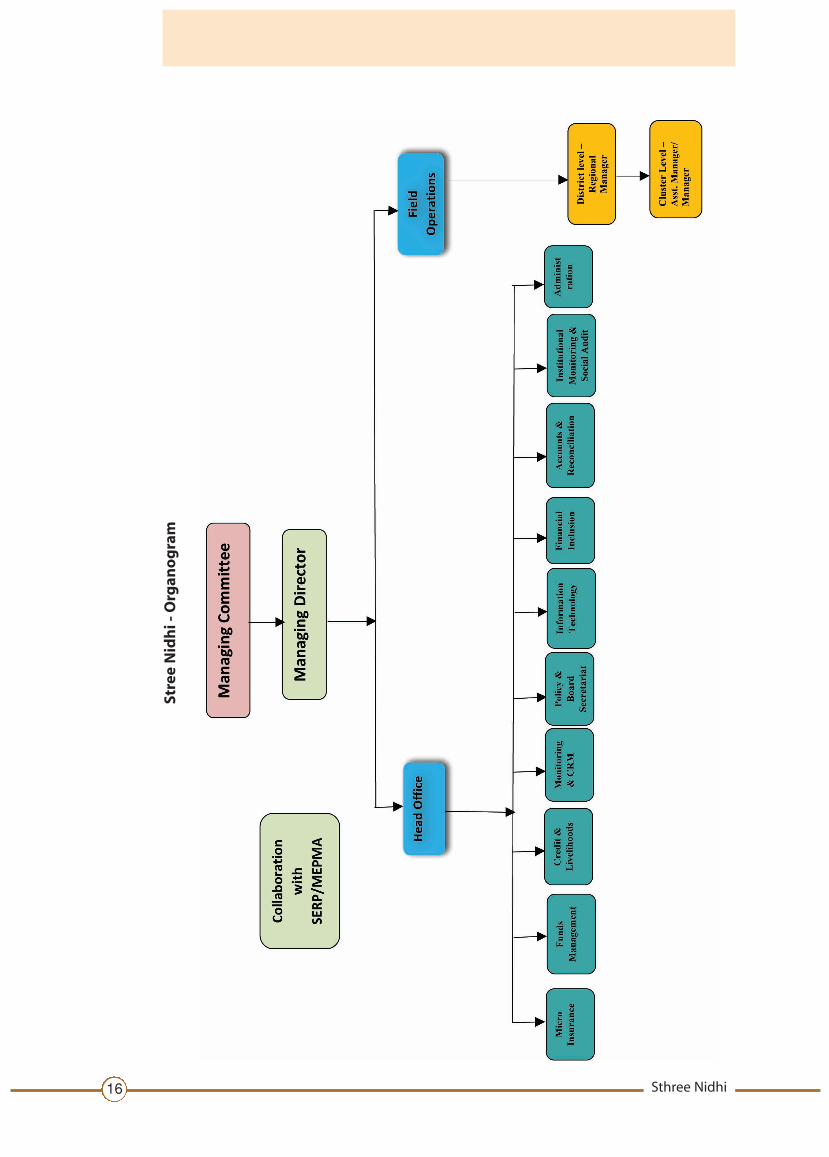

Staffing Pattern:

6.5. For effective monitoring of implementation of Stree Nidhi activities, a three tier

system is followed.

6.5.1.Head Office:under over all administrative control of the Managing Director, the

following verticals have been formed to supervise various functions,which are headed

by DGMs and assisted by Chief Managers,Managers & Asst.Managers.

� Board Secretariat, Policy and MIS

� Monitoring

� General Administration

� Credit and Livelihoods

� Information Technology

� Financial Inclusion

� Funds Management

� Risk Management

� Accounting and Reconcilation

� Institutional Monitoring & Social Audit

Field level functionaries:

6.5.2. To ensure effective implementation of activities and monitoring to achievedesired results, all the districts except Hyderabad are divided in to 3 zones and fewdistricts in the zone are considered as a Region. Each zone is headed by DGM,who willsupervise the performance of the Regions in all the areas. The regions are headed byRegional Managers and they are assisted by Managers, Assistant Managers who areresponsible for overall performance of the regions. In each region, operational areaconsisting of 7-8 mandals is allocated to Asst. Managers/Managers. The RegionalManager has to supervise the functioning of all the Managers and Asst.Managers andthe Managers have to monitor the functioning of Asst. Managers working under theirpurview.

Recruitment of Staff:

6.5.3.Stree Nidhi has increased staff strength from time to time depending on the needin tune with the growth in volume of business and coverage of members. The Staffstrength has increased to 81 as on March 2016.During the year, there was an excellentgrowth in total advances, deposits and improved performance in repayment andreduction in NPAs. The details of staff positioned at HO & field in different cadres aregiven in the table no.5 of part-C of this report and organogram is depicted below.

Sthree Nidhi16

StreeNidhi-

Organ

ogram

Annual Report 2015-16 17

Chapter 7

Ease of reaching poor andmonitoring- Role of technology

7.1. Stree Nidhi has been using I.T. Solutions to the optimum covering all operations todeliver financial services at the doorsteps of the poor members of SHGs in the State.Technology platform adopted has been playing a key role in providing the last mileconnectivity to the poor and in lowering the cost of operations. Entire range ofoperations right from loan request, mobilisation of savings, loan processing,disbursement, repayment and adjustment of amount repaid to loan accounts,monitoring and implementation of BC activities are enabled through technology.Funds transfer is ensured through Electronic Fund Management to reach to SHGs,through banking channel using RTGS, NEFT and intra bank transfers.

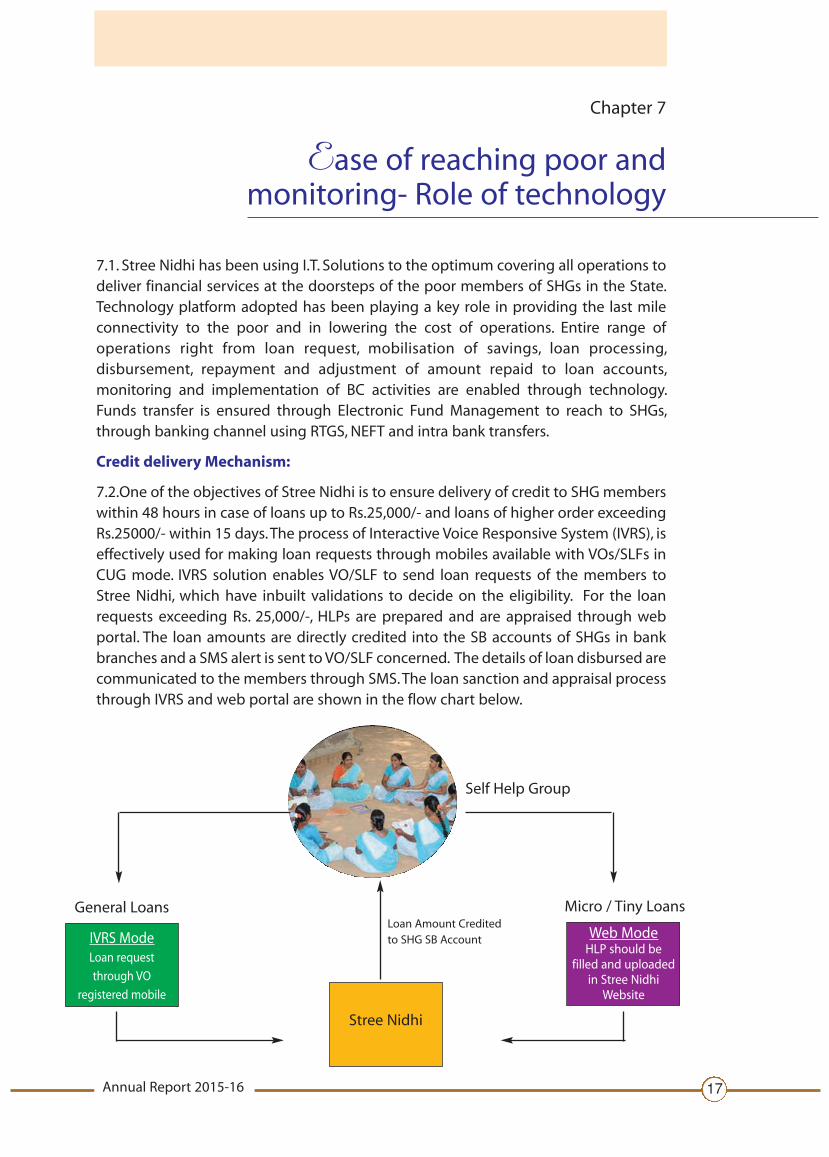

Credit delivery Mechanism:

7.2.One of the objectives of Stree Nidhi is to ensure delivery of credit to SHG memberswithin 48 hours in case of loans up to Rs.25,000/- and loans of higher order exceedingRs.25000/- within 15 days.The process of Interactive Voice Responsive System (IVRS), iseffectively used for making loan requests through mobiles available with VOs/SLFs inCUG mode. IVRS solution enables VO/SLF to send loan requests of the members toStree Nidhi, which have inbuilt validations to decide on the eligibility. For the loanrequests exceeding Rs. 25,000/-, HLPs are prepared and are appraised through webportal. The loan amounts are directly credited into the SB accounts of SHGs in bankbranches and a SMS alert is sent toVO/SLF concerned. The details of loan disbursed arecommunicated to the members through SMS.The loan sanction and appraisal processthrough IVRS and web portal are shown in the flow chart below.

Self Help Group

General Loans Micro / Tiny Loans

Stree Nidhi

Web ModeHLP should be

filled and uploadedin Stree Nidhi

Website

Loan Amount Creditedto SHG SB AccountIVRS Mode

Loan request

through VO

registered mobile

Sthree Nidhi18

Repayment:

7.3. For the loan accounts created, the member wise repayment schedule is generatedand the same is aggregated at SHG,VO/SLF and MS/TLF level for monitoring purpose.The details of amounts to be repaid, due date, interest for delayed payment iscalculated and the information is sent through SMS one week before the due date toall VOs/SLFs. The details of loans and amount to be repaid are also made available inURL specific to the VO/SLF and can be accessed using GPRS enabled in CUG mobile asalso website.

7.4. After the repaid amounts are transferred to Stree Nidhi and on sharing of thedetails by the Banks, these amounts will be reflected in Stree Nidhi was site. TheVOs/SLFs can adjust the member wise repayments through URL provided for thepurpose. Thereafter, the member wise amounts will be accounted for in the loanledgers automatically.The amounts credited are confirmed to VOs/SLFs through SMS.

7.5. Any communication from Stree Nidhi is communicated to VOs/SLFs through voicecalls.

7.6. A robust MIS and monitoring system is evolved to ensure monitoring of theservices rendered, credit and savings portfolio and staff effectively which gets updatedmore or less on a real time basis.

Annual Report 2015-16 19

Chapter 8

Mobilisation of Resources

8.1. There is growing demand for credit from the members of SHGs both in rural andurban areas. On account of various measures taken up by Stree Nidhi in coordinationwith SERP & MEPMA, awareness is gradually spreading on availability of timely,affordable and hassle free credit delivery services from Stree Nidhi. Stree Nidhi isemerging as a dependable financial institution of their own to help them in times ofneed. Stree Nidhi has fine- tuned credit policy from time to time and enhanced creditlimits of VOs/SLFs, SHGs and members. New loan products were introduced totransform Stree Nidhi from Micro financing to Micro enterprises, to enable the needymembers to avail credit for taking up livelihood activities of the higher order.

8.2.To meet resource gap, Stree Nidhi has been availing credit facilities from the banksand other financial institutions. The bye-laws of Stree Nidhi provide for outsideborrowings not exceeding 10 times of owned funds. The bye-laws of Stree Nidhiprovide to mobilise resources from the following sources.

� Share Capital from MSs and TLFs

� Share Capital from State Government

� Savings mobilised from SHGs/VOs/SLFs/ MSs/TLFs and ZSs

� Borrowings from Commercial Banks, NABARD, etc.,

� Deposits from State Government

� Loans from State Government, Govt. of India and Other Government agencies

� Grant in aid and subsidy from Government and Govt. agencies

Own funds of Stree Nidhi

8.3. The owned funds of Stree Nidhi constitute share capital contributed by MSs/TLFs,General reserves, accumulated profits and capital grants from State Govt., Samruddhiand CIF Corpus deposits, which are crore in nature. The total owned funds haveincreased from Rs. 304.31 Cr as on Mar 2015 to Rs. 482.11 cr as on March 2016.

Sthree Nidhi20

Total Resources

(Rs. Cr.)

Share Capital Deposits Grants Reserve Accumulated Bank Others Totalprofit Borrowings

90.89 317.97 55.56 6.46 67.21 824.34 74.72 1437.15

Share Capital

8.4. All 438 Mandal Samakhyas and 47 Town Level Federations have contributed toshare capital of Stree Nidhi.The details of share capital as on 31/03/2016 are furnishedbelow.

(Rs. Cr.)

S.No. Sources of Share Capital 31.03.2016

1 State Government 43.52

2 MS and TLFs 47.37

Total: 90.89

The district wise details of paid up Share capital up to 31.03.2016 are furnished in Tableno. 6 part-C of this report.

Mobilisation of Savings from Community

8.5. To become a self-reliant in resources Stree Nidhi has introduced different depositproducts to tap funds from SHGs and their federations. This not only would improveown resources but also help in achieving broader objective of making the communityown up the institution. Four types of deposit products have been introduced viz.Samruddhi, Bhavitha, Sankalpa and CIF Corpus Deposit scheme.

Annual Report 2015-16 21

Samruddhi Deposit

8.5.1. Every SHG has to save Rs.100 per month. The amount saved in 12 months alongwith interest will be converted to fixed deposit with a maturity of 5 years. This wouldbe on a continuous basis and at the end of 6th year, the amount saved in the first yearwould be refunded along with interest. The rate of interest paid is equal to the rate ofinterest paid by SBI on term deposits for similar maturity.The rate will be reset as on 1stApril of every year.

Bhavitha Deposit:

8.5.2. SHGs can save their idle/surplus funds in this deposit.The amount will be kept interm deposit for a minimum period of 3 years and rate of interest will be 1% above therate paid by SBI for similar term.The rate will be reset as on 1st April of every year.

Sankalpa Deposit:

8.5.3. Under this deposit scheme, the federations of SHGs i.e., VOs/SLFs, MSs/TLFs andZSs can invest their surplus/idle funds.The period is 3 years and rate of interest paid willbe 1% above the rate paid by SBI at monthly intervals, if the amount of deposit is aboveRs.1.00 lakh and at quarterly intervals if the amount is less than Rs.1.00 lakh.The ratewill be reset as on 1st April of every year.

CIF corpus Deposit:

8.5.4. This deposit scheme is devised exclusively for Mandal Samakhyas so as to placethe CIF available with them as a term deposit with Stree Nidhi on a perpetual basis andtherefore is not refundable. The interest will be paid at monthly intervals and the rateof interest will be 1% above the SBI rate. The rate will be reset as on 1st April of everyyear.

Deposit Mobilisation

8.6. Stree Nidhi has been making relentless efforts to create awareness among the

SHGs and their federations about the importance of savings to be made in Stree Nidhi.

These resources are used not only for onward lending but also serve to increase low

cost resource and financial soundness of the organisation. This would also enable

banks for taking exposure to Stree Nidhi. Stree Nidhi, SERP and MEPMA staff are

monitoring the coverage of SHGs under Samruddhi on a regular basis under the

guidance of the Project Directors, DRDA & MEPMA. Stree Nidhi Resource Persons are

actively involved in motivating SHGs to contribute to Samruddhi deposit and avail

services of Stree Nidhi. The measures adopted in mobilisation of deposits from the

community have yielded good results. The deposits mobilised under different

schemes as on 31.03.2016 were Rs.317.97Cr and the year wise progress achieved is

furnished below.

Sthree Nidhi22

(Rs. lakhs)

S.No. Year Samruddhi ZS- MS- VO- Bhavitha Corpus TotalSankalpa Sankalpa Sankalpa Deposit

1 2013-14 1598.97 600.00 1051.82 537.86 40.47 - 3829.12

2 2014-15 7515.75 965.00 2218.03 1061.29 85.62 4714.59 16560.30

3 2015-16 13061.88 1110.00 2529.74 1851.49 109.41 13134.9 31797.45

During the year 2015-16, there was an increase of Rs.152.90 cr. in total deposits

recording a growth rate of 92.63%. The growth is due to transfer of CIF amount

available with theMandal Samakhyas and increase in Samruddhi deposits.District wise

and scheme wise deposit position is furnished in Table no.7 in Part-C of this report.

Borrowings from Banks and Other Financial Institutions

8.7.To meet growing requirement of resources for onward lending to SHGs, apart from

mobilisation of deposits from community, Stree Nidhi has been borrowing from Banks

and other financial institutions in the form of cash credit limits and term loans.

Keeping in view the robust performance and financial strength of Stree Nidhi, Banks

and Financial Institutions are keen to take exposure to Stree Nidhi.The credit limits and

term loans availed from them are given here under.

Annual Report 2015-16 23

(Rs Crore)

S.No. Name of the Bank Cash Credit Limits Credit Limits

1 Andhra Bank 150

2 State Bank of Hyderabad 200

3 Bank of India 150

4 Canara Bank 50

5 T S Cooperative Apex Bank 150

6 Vijaya Bank 40

7 State Bank of Patiala 50

8 Indian Bank 30

Total Cash Credit Limits: 820

Term Loans

10 ABFL 25

11 NAB Kisan 14

12 T S Cooperative Apex Bank 20

13 NSTFDC term Loan 50

Total Term Loans: 109

Grand Total: 929

8.8.Rating of Stree Nidhi:

Stree Nidhi has been rated by M/S Brick Works with BWRBBB+, out look stable. Thisrating was made for the purpose of availing credit facilities from Banks and otherfinancial instititions.

Sthree Nidhi24

Chapter 9

Loan Policy

9.1. The loan policy of Stree Nidhi is fine-tuned from time to time depending on needso as to enable the members of SHGs to avail credit services from Stree Nidhi withoutany hassles. While devising the policy, the guidelines prescribed by RBI are dulycomplied with by Stree Nidhi.The salient features of the present policy are as under.

No. of members eligible for loan in a SHG

9.2.Depending on the no.of members in an SHG,up to ninemembers can access creditas given in the table below.Themembers can avail credit till they attain age of 60 years.The Maximum borrowing limit per SHG is restricted to Rs.3.00 lakh.

S.No. No. of Total no. of No. of Maximummembers in a members members who loan

SHG who can avail can avail loan availableloans by IVRS (Rs in lakh)

(1) (2) (3) (4) (5)

1 12 and above Up to 9 6 3.00

2 10 – 11 Up to 8 6 2.50

3 9 and below 75% of the members 4 2.00or 6, whichever is high

� A member can borrow up to a maximum of Rs.1.00 lakh

� Ceiling on credit limit of VO is Rs.50.00 lakh

� Of the credit limits allocated to VOs, 35% is allocated to Micro & Tiny loans.

� A member having availed a general loan repaid regularly can also avail micro loanfor livelihood enterprises.

� For availing tiny loans the members loan outstanding under Bank Linkage shall notexceed Rs.25000/-.Themaximum investment cost of activity shall not bemore thanRs.1,20,000/- which includes money mobilised by the borrower.

� In case of loans for the purpose of marriage, the loan will be linked to the amountof loan given by SHG to it’s member. It will be a matching loan from Stree Nidhi.

Allocation of credit limits to VO/SLF and MS/TLF:

9.3.1. Stree Nidhi laid much emphasis on the functioning of federations of SHGs atVillage/Slum level namely Village Organisation and Slum Level Federation and furtherat Mandal/Town level i.e.,Mandal Samakhyas and Town Level Federations. Credit limitsare allocated to VOs/SLFs based on their performance under key parameters reflectedin the rating given. These institutions are rated once in a year based on theperformance as the end of March. The objective is to reward the federations functiongwell with higher credit limits and to thus minimise credit risk. The parameters

Annual Report 2015-16 25

considered for rating are own funds, regularity in conduct of meetings and percentageof attendance, Book keeping, Net profit earned, Legal compliance, Savings, CIFrecovery and Repayment of Stree Nidhi loans.

9.3.2. Higher credit limits are allocated to VOs/SLFs which score higher rating. It is a

revolving credit limit at VO/SLF level. The SHGs can borrow and repay any number of

times subject to the ceiling at the level of SHG andmember which enables coverage of

more no.of SHGs. As there will be regular repayment and such amount repaid by SHGs

in a VO/SLF can be availed by other SHGs there by meeting the demand for credit and

thus high cost borrowing from other sources can be minimized.

Credit limits to VOs in MSs with different ratings:

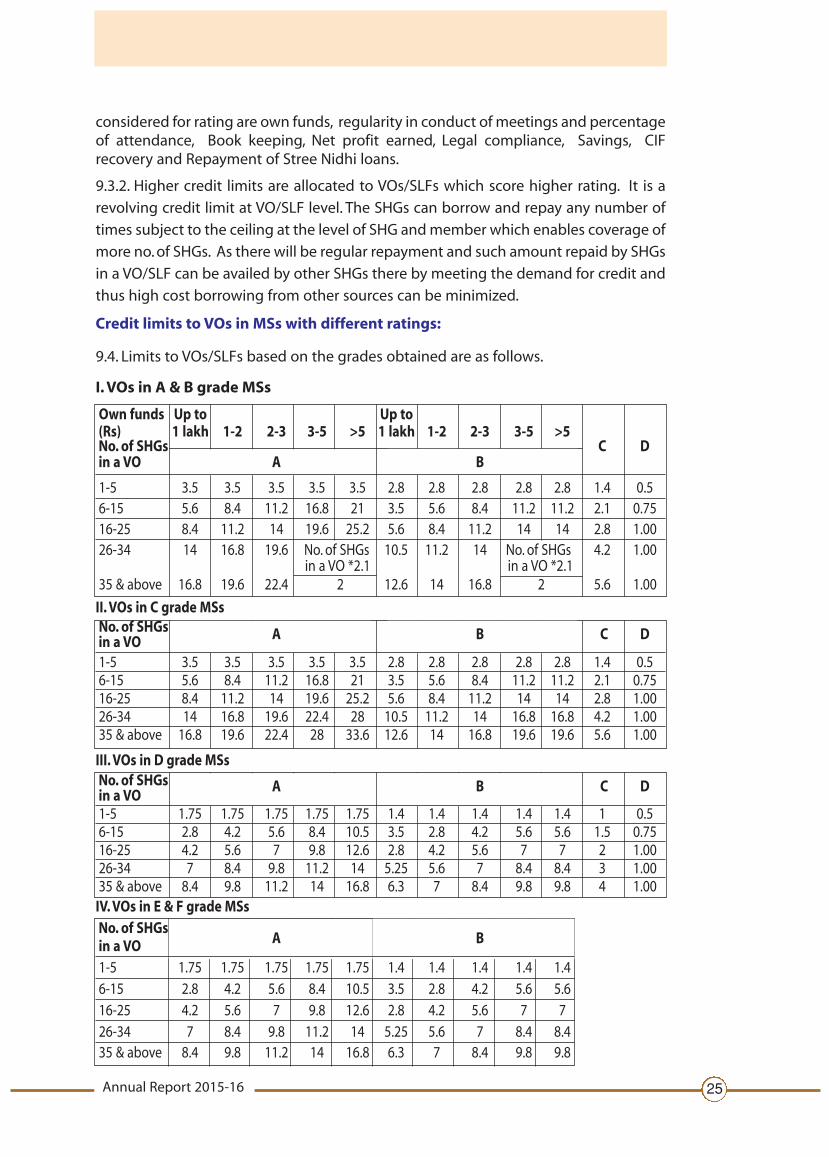

9.4. Limits to VOs/SLFs based on the grades obtained are as follows.

I.VOs in A & B grade MSs

Own funds Up to Up to(Rs) 1 lakh 1-2 2-3 3-5 >5 1 lakh 1-2 2-3 3-5 >5No. of SHGs C Din a VO A B

1-5 3.5 3.5 3.5 3.5 3.5 2.8 2.8 2.8 2.8 2.8 1.4 0.56-15 5.6 8.4 11.2 16.8 21 3.5 5.6 8.4 11.2 11.2 2.1 0.7516-25 8.4 11.2 14 19.6 25.2 5.6 8.4 11.2 14 14 2.8 1.0026-34 14 16.8 19.6 No. of SHGs 10.5 11.2 14 No. of SHGs 4.2 1.00

in a VO *2.1 in a VO *2.135 & above 16.8 19.6 22.4 2 12.6 14 16.8 2 5.6 1.00

II.VOs in C grade MSsNo. of SHGsin a VO A B C D

1-5 3.5 3.5 3.5 3.5 3.5 2.8 2.8 2.8 2.8 2.8 1.4 0.56-15 5.6 8.4 11.2 16.8 21 3.5 5.6 8.4 11.2 11.2 2.1 0.7516-25 8.4 11.2 14 19.6 25.2 5.6 8.4 11.2 14 14 2.8 1.0026-34 14 16.8 19.6 22.4 28 10.5 11.2 14 16.8 16.8 4.2 1.0035 & above 16.8 19.6 22.4 28 33.6 12.6 14 16.8 19.6 19.6 5.6 1.00

III.VOs in D grade MSsNo. of SHGsin a VO

A B C D

1-5 1.75 1.75 1.75 1.75 1.75 1.4 1.4 1.4 1.4 1.4 1 0.56-15 2.8 4.2 5.6 8.4 10.5 3.5 2.8 4.2 5.6 5.6 1.5 0.7516-25 4.2 5.6 7 9.8 12.6 2.8 4.2 5.6 7 7 2 1.0026-34 7 8.4 9.8 11.2 14 5.25 5.6 7 8.4 8.4 3 1.0035 & above 8.4 9.8 11.2 14 16.8 6.3 7 8.4 9.8 9.8 4 1.00IV.VOs in E & F grade MSsNo. of SHGsin a VO A B

1-5 1.75 1.75 1.75 1.75 1.75 1.4 1.4 1.4 1.4 1.46-15 2.8 4.2 5.6 8.4 10.5 3.5 2.8 4.2 5.6 5.616-25 4.2 5.6 7 9.8 12.6 2.8 4.2 5.6 7 726-34 7 8.4 9.8 11.2 14 5.25 5.6 7 8.4 8.435 & above 8.4 9.8 11.2 14 16.8 6.3 7 8.4 9.8 9.8

Sthree Nidhi26

Credit products

9.5.1. Financing microenterprises and livelihoods has been widely adopted as

anti-poverty strategy. Micro enterprises have been playing as an engine of economic

growth, equitable development and encourage self-employment to a large extent.

Availability of financial services is a key to the success of micro enterprises.

9.5.2. Stree Nidhi played a significant role in purveying micro credit to the needy

members of SHGs during the past 4 years. The loan amount initially was limited up to

Rs.25,000 per member depending on the purpose of loan. Keeping the importance of

Micro Enterprises and livelihoods in enhancing income level of the poor, Stree Nidhi

made a paradigm shift to provide credit for these purposes. Keeping in view increased

credit requirements for taking up livelihoods, the loan limit per SHG member was

raised to Rs. 1.0 lakh and this was also enabled by policy relaxation from RBI.

9.5.3.Stree Nidhi has adopted a strategy to promote and financing livelihoods at house

hold level thus focus is laid on House Hold Level planning for extending credit support

for taking up micro enterprise/ livelihoods of families’ choice after necessary due

diligence at SHG and VO/SLF level. It is endeavour of Stree Nidhi to finance livelihood

activities/micro enterprises in a big way and therefore is positioned accordingly to

support poor in

� Expansion of existing income generating activities

� Taking up New activities

� Cluster level activities

Types of Loans:

9.6. Stree Nidhi has introduced the following three types of loans.

I. General loans Amount of loan can be accessed up to Rs.25000

II.Micro loans Where loan amount is >Rs.25,000 to Rs.50,000

III. Tiny loans Loan amount is >Rs.50000 to Rs.1.00 lakh

General loans can be accessed for both livelihoods of lower order and consumptionpurposes in the ratio of 70:30 out of the credit limit allocated. These loans can beaccessed through IVRS .

9.6.1.The credit limits allocated under Micro & Tiny loans can be accessed only forlivelihood purposes and application for loans to be made through web portal. Duediligence and appraisal of house hold level plans is done at SHG/VO level and by staffof SERP and Stree Nidhi. The details regarding the member and her family, proposedactivity, availability of required raw material, skill & knowledge, capital investment,sources of funds, loan amount required, incremental income expected, repaymentcapacity, etc., are looked into, while preparing HLP and appraisal of the proposedactivity. These loans can be availed only for IGA/Livelihoods/Micro enterprises. Themembers in SHGs of VOs with A, B grades in MSs with A, B and C grade are eligible for

Annual Report 2015-16 27

micro and tiny loans. Loanamount is released directly to SBA/C of SHG to which the memberis associated.

9.6.2. In the EC meeting of VO/SLFof all the requests received fromSHGs will be subjected to scrutinywith regard to attendance ofmember in SHG, savings andrepayment history, skills andknowledge in activity, scope forincremental income and loan amount required. Thereafter, VO will take a decisionwhether the member is eligible for loan and on their request the CC concerned willappraise the activity proposed on the basis of HLP. There is a provision to receive theloan requests in the meeting of OBs held one week after each EC meeting and scrutinyof the requests is done on the above lines. The appraisals thus prepared by CC/StreeNidhi staff are placed in the next EC meeting for approval. The VO ensures end use ofthe loan and the same will be recorded in the minutes’ book of VO EC meeting. Theloan applications and documents from SHGs are preserved at VO/MS and documentsobtained from members are kept with the SHGs concerned.

9.6.3.A certificate of utilisation has to be uploaded by CC after it is certified by APM andAC within 30 days of loan disbursement. Stree Nidhi staff will verify all the above casesindependently and certify the utilisation of loans within 45 days of disbursement.

Repayment Period

9.7. In order to facilitate the borrowers to repay conveniently, the no. of monthly loaninstalments are fixed depending on the loan amount as follows:

S.No. Loan amount Repaymentperiod in months

1 Rs.25,000/- 24

2 >Rs.2500 to Rs.35,000 36

3 >Rs.3500 to Rs.50,000 42

4 >Rs.5000 to Rs.1,00,000 60

Interest subvention:Vaddi Leni Runalu (VLR)

9.8. The scheme of Vaddi Leni Runalu is aimed at twin objectives of reducing interestburden on loans and encourage promptness in repayment of loans by SHGs.The StateGovt. is implementing interest subvention scheme, where in the amount of interestpaid by the members is reimbursed if the loan instalments (EMIs) is repaid within 30days from due date. The amount of VLR will be credited to the loan accounts of SHGsas and when the amount is received from the Govt.

Sthree Nidhi28

Stree Nidhi as a channelizing Agency:

9.9. Stree Nidhi is functioning as a channelizing agency for releasing credit forimplementation of poverty alleviation programmes viz. SCSP,TSP, IWMP & NRLM. StreeNidhi is managing the funds released by SERP and facilitating disbursement of loans tothe members of low income groups identified by SERP. The loan amount will bereleased to VOs as per the list of the members, activities and loan amount provided bySERP. In turn, the VO will release the funds to SHG members concerned. VOs will takerequired steps to ensure utilisation of funds by the members concerned for thelivelihood activities and to increase their family income. The loans are monitored bySERP. The year wise coverage of members and loans disbursed as channelizing agencyare given in the table below:

(Rs. Cr.)

S.No Year No of AmountMembers Disbursed

1 2013-14 19286 51.15

2 2014-15 30422 74.58

3 2015-16 38363 141.29

Total: 88071 267.02

Annual Report 2015-16 29

Chapter 10

Credit Flow – Analysis

Disbursement of Loans:

10.1. The growth rate achieved in loans disbursed is significant year after year. Duringthe financial year 2015-16, the quantum of loans disbursed was Rs.1148.37cr as againstRs.703.29 cr disbursed in the year 2014-15, recording a growth rate of 63.29% year onyear. The cumulative disbursement of loans since inception was Rs.2597.46 cr as at theend of March 2016.

Coverage of members, SHGs,VOs/SLFs and MS/TLFs

10.2. The efforts made to create awareness among the members through SHGs andtheir federations have enabled increase in outreach and credit. The cumulative no. ofmembers having availed loans has reached 12.27 lakh. There was an addition of 4.54lakh members during the year recording an increase of 41.27% over the previous year.The no. of SHGs covered reached was 2.22 lakh and no. of VOs/SLFs and MS/TLFcovered was 15153 and 473 respectively.

10.2.1.The year wise details of coverage of the members, SHGs,VOs/SLFs and MSs/TLFsin the state of Telangana are as under.

(Rs. lakhs)

S.No. Year No. of No. of No. of No. of SHG AmountMS/TLF VO/SLF SHG Members

1 2011-12 303 2440 7599 25038 3195

2 2012-13 374 7070 47742 181191 29625

3 2013-14 414 8317 62560 229931 41760

4 2014-15 443 9242 88116 336900 70329

5 2015-16 456 12064 126832 454390 114837

Total: 473 15,153 2,22,819 12,27,450 259746

Sthree Nidhi30

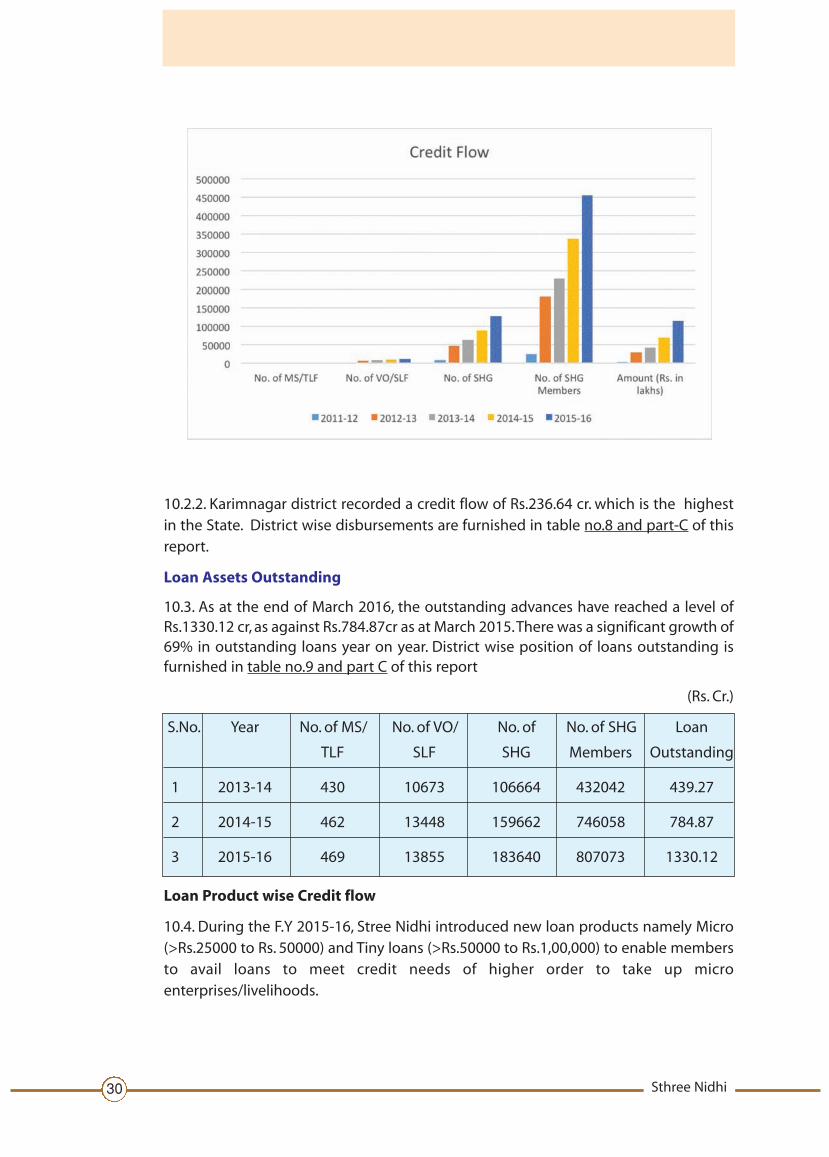

10.2.2. Karimnagar district recorded a credit flow of Rs.236.64 cr. which is the highestin the State. District wise disbursements are furnished in table no.8 and part-C of thisreport.

Loan Assets Outstanding

10.3. As at the end of March 2016, the outstanding advances have reached a level ofRs.1330.12 cr, as against Rs.784.87cr as at March 2015.There was a significant growth of69% in outstanding loans year on year. District wise position of loans outstanding isfurnished in table no.9 and part C of this report

(Rs. Cr.)

S.No. Year No. of MS/ No. of VO/ No. of No. of SHG Loan

TLF SLF SHG Members Outstanding

1 2013-14 430 10673 106664 432042 439.27

2 2014-15 462 13448 159662 746058 784.87

3 2015-16 469 13855 183640 807073 1330.12

Loan Product wise Credit flow

10.4. During the F.Y 2015-16, Stree Nidhi introduced new loan products namely Micro(>Rs.25000 to Rs. 50000) and Tiny loans (>Rs.50000 to Rs.1,00,000) to enable membersto avail loans to meet credit needs of higher order to take up microenterprises/livelihoods.

Annual Report 2015-16 31

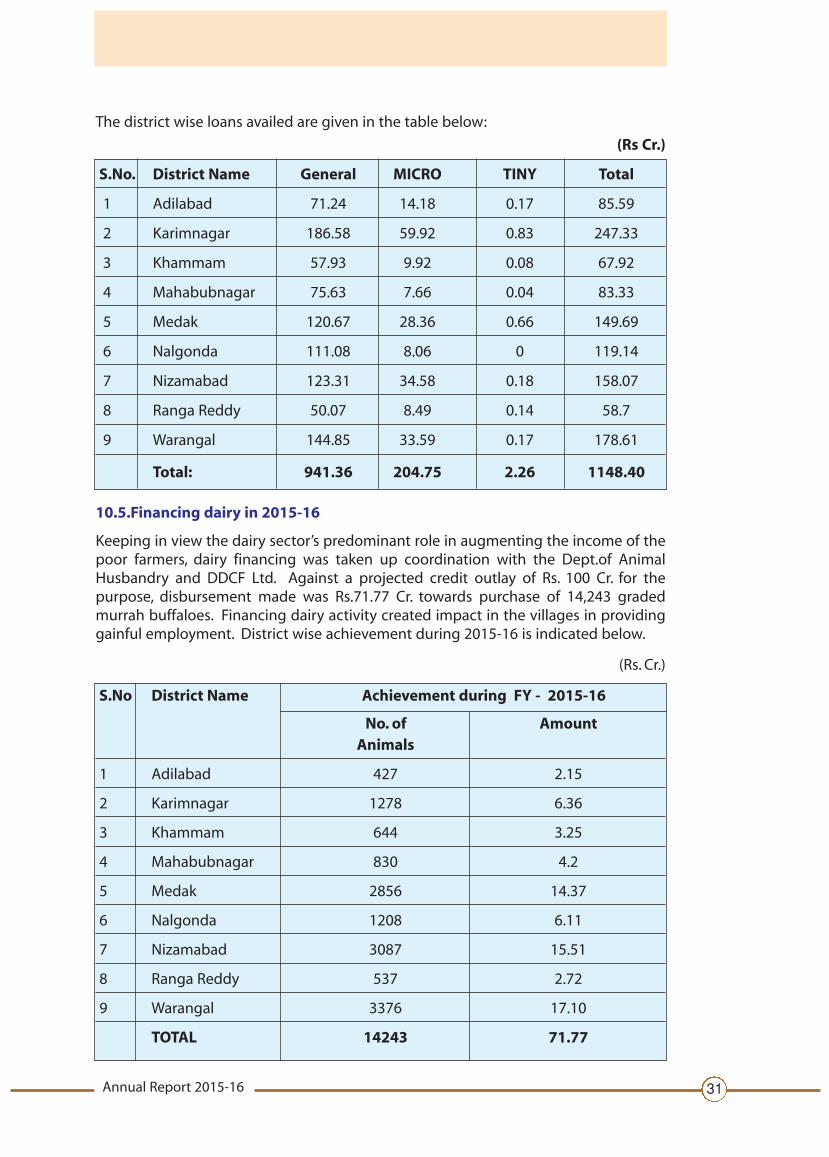

The district wise loans availed are given in the table below:

(Rs Cr.)

S.No. District Name General MICRO TINY Total

1 Adilabad 71.24 14.18 0.17 85.59

2 Karimnagar 186.58 59.92 0.83 247.33

3 Khammam 57.93 9.92 0.08 67.92

4 Mahabubnagar 75.63 7.66 0.04 83.33

5 Medak 120.67 28.36 0.66 149.69

6 Nalgonda 111.08 8.06 0 119.14

7 Nizamabad 123.31 34.58 0.18 158.07

8 Ranga Reddy 50.07 8.49 0.14 58.7

9 Warangal 144.85 33.59 0.17 178.61

Total: 941.36 204.75 2.26 1148.40

10.5.Financing dairy in 2015-16

Keeping in view the dairy sector’s predominant role in augmenting the income of thepoor farmers, dairy financing was taken up coordination with the Dept.of AnimalHusbandry and DDCF Ltd. Against a projected credit outlay of Rs. 100 Cr. for thepurpose, disbursement made was Rs.71.77 Cr. towards purchase of 14,243 gradedmurrah buffaloes. Financing dairy activity created impact in the villages in providinggainful employment. District wise achievement during 2015-16 is indicated below.

(Rs. Cr.)

S.No District Name Achievement during FY - 2015-16

No. of AmountAnimals

1 Adilabad 427 2.15

2 Karimnagar 1278 6.36

3 Khammam 644 3.25

4 Mahabubnagar 830 4.2

5 Medak 2856 14.37

6 Nalgonda 1208 6.11

7 Nizamabad 3087 15.51

8 Ranga Reddy 537 2.72

9 Warangal 3376 17.10

TOTAL 14243 71.77

Sthree Nidhi32

Purpose wise credit flow

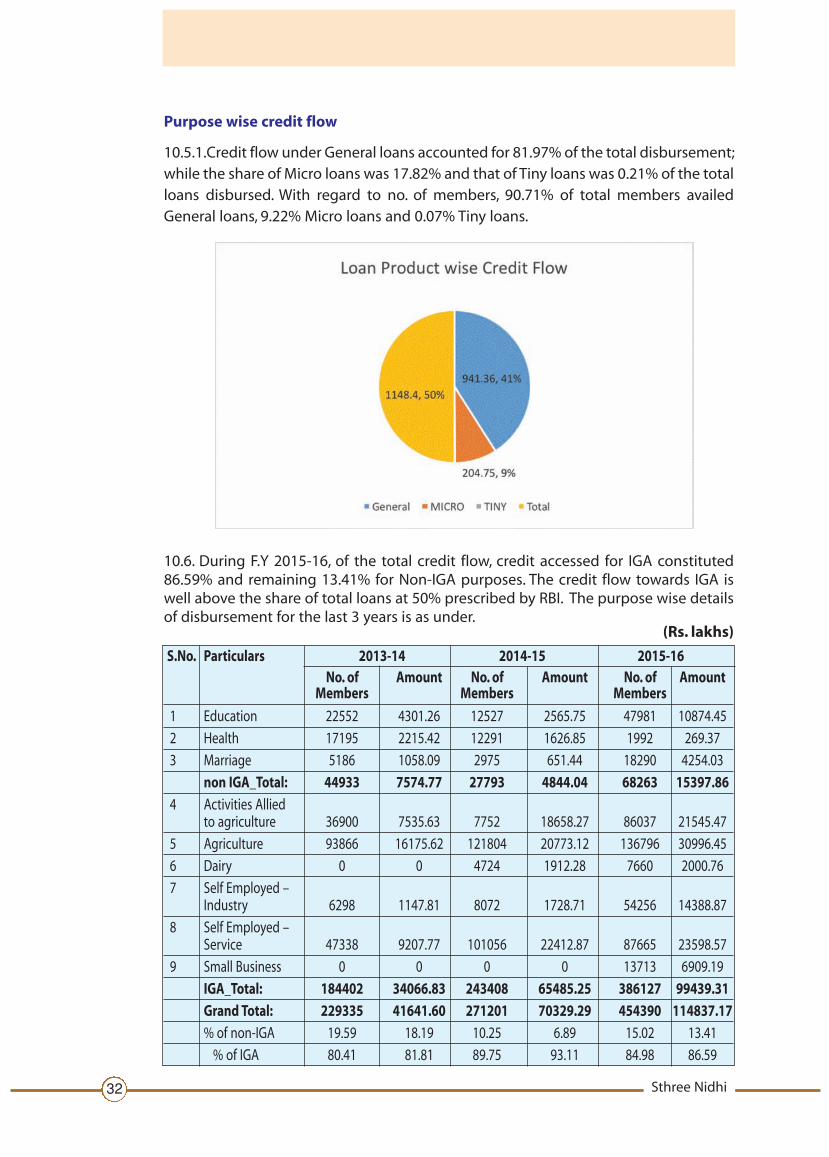

10.5.1.Credit flow under General loans accounted for 81.97% of the total disbursement;while the share of Micro loans was 17.82% and that of Tiny loans was 0.21% of the totalloans disbursed. With regard to no. of members, 90.71% of total members availedGeneral loans, 9.22% Micro loans and 0.07% Tiny loans.

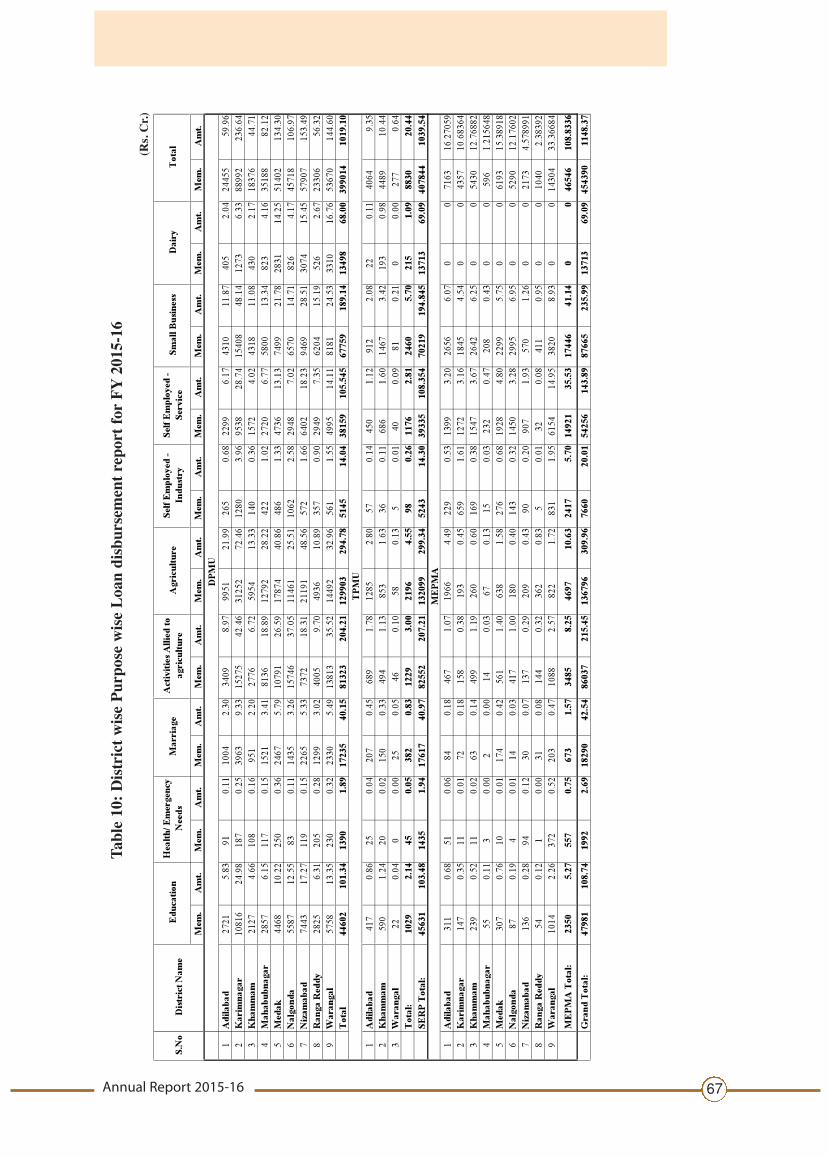

10.6. During F.Y 2015-16, of the total credit flow, credit accessed for IGA constituted86.59% and remaining 13.41% for Non-IGA purposes. The credit flow towards IGA iswell above the share of total loans at 50% prescribed by RBI. The purpose wise detailsof disbursement for the last 3 years is as under.

(Rs. lakhs)

S.No. Particulars 2013-14 2014-15 2015-16No. of Amount No. of Amount No. of Amount

Members Members Members

1 Education 22552 4301.26 12527 2565.75 47981 10874.45

2 Health 17195 2215.42 12291 1626.85 1992 269.37

3 Marriage 5186 1058.09 2975 651.44 18290 4254.03

non IGA_Total: 44933 7574.77 27793 4844.04 68263 15397.86

4 Activities Alliedto agriculture 36900 7535.63 7752 18658.27 86037 21545.47

5 Agriculture 93866 16175.62 121804 20773.12 136796 30996.45

6 Dairy 0 0 4724 1912.28 7660 2000.76

7 Self Employed –Industry 6298 1147.81 8072 1728.71 54256 14388.87

8 Self Employed –Service 47338 9207.77 101056 22412.87 87665 23598.57

9 Small Business 0 0 0 0 13713 6909.19

IGA_Total: 184402 34066.83 243408 65485.25 386127 99439.31

Grand Total: 229335 41641.60 271201 70329.29 454390 114837.17

% of non-IGA 19.59 18.19 10.25 6.89 15.02 13.41

% of IGA 80.41 81.81 89.75 93.11 84.98 86.59

Annual Report 2015-16 33

10.6.1. District wise and purpose wise disbursements are furnished in Table no.10 ofpart-C of this report.

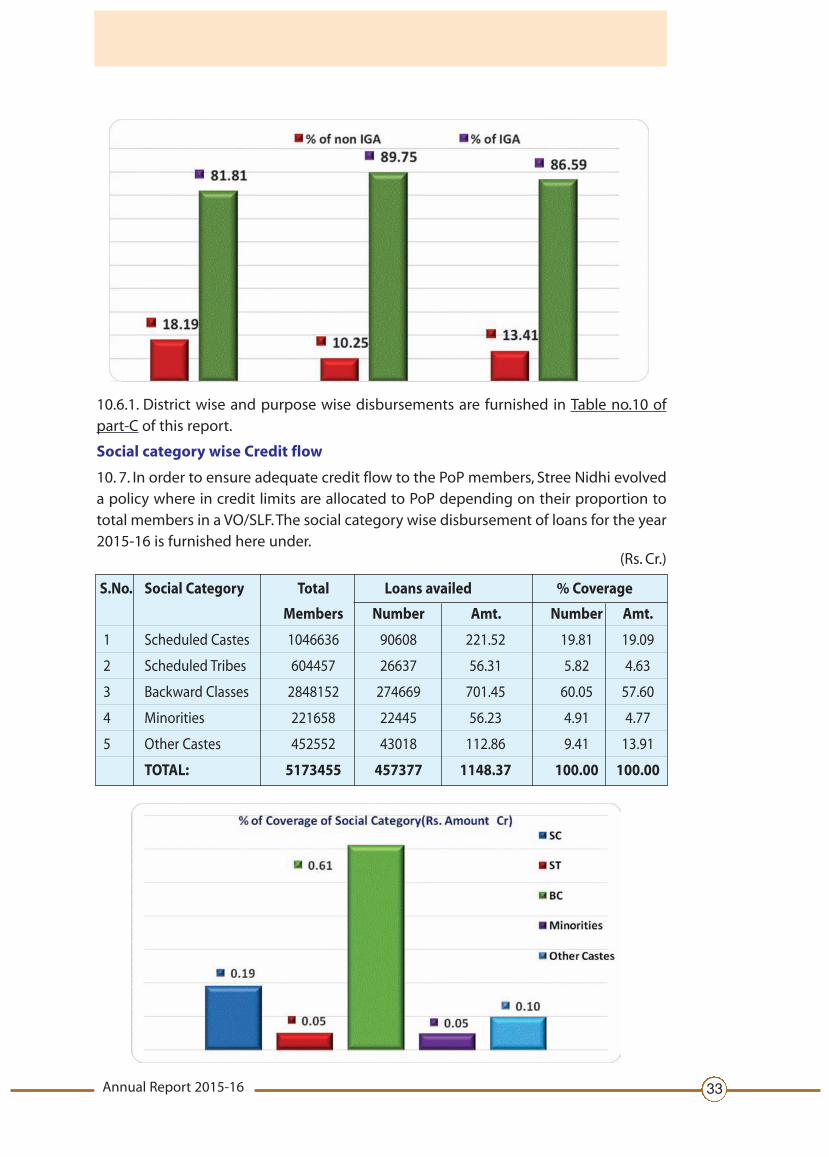

Social category wise Credit flow

10. 7. In order to ensure adequate credit flow to the PoP members, Stree Nidhi evolveda policy where in credit limits are allocated to PoP depending on their proportion tototal members in a VO/SLF.The social category wise disbursement of loans for the year2015-16 is furnished here under.

(Rs. Cr.)

S.No. Social Category Total Loans availed % Coverage

Members Number Amt. Number Amt.

1 Scheduled Castes 1046636 90608 221.52 19.81 19.09

2 Scheduled Tribes 604457 26637 56.31 5.82 4.63

3 Backward Classes 2848152 274669 701.45 60.05 57.60

4 Minorities 221658 22445 56.23 4.91 4.77

5 Other Castes 452552 43018 112.86 9.41 13.91

TOTAL: 5173455 457377 1148.37 100.00 100.00

Sthree Nidhi34

10.7.1. District wise Social Category wise disbursements are furnished in Table no.11part- C of this report.

10.7.2 Disbursement and loan outstanding :

On an average the availment of loan amount and loan outstanding per group wereat Rs 0.91 lakh and Rs 0.72 lakh. The average borrowing members per group are at4.39. The per member average loan availed was Rs 0.25 lakh and per memberoutstanding was at Rs 0.16 lakh. This indicates that still there is a lot of potential toexpand credit protfolio.

(Rs lakh)

S.No Particulars Amount

1 Credit flow per SHG 0.91

2 Loan outstanding per SHG 0.72

3 No.of members having loan per SHG 4.39

4 Credit availed per member 0.25

5 Loan outstanding per member 0.16

Asset Quality:

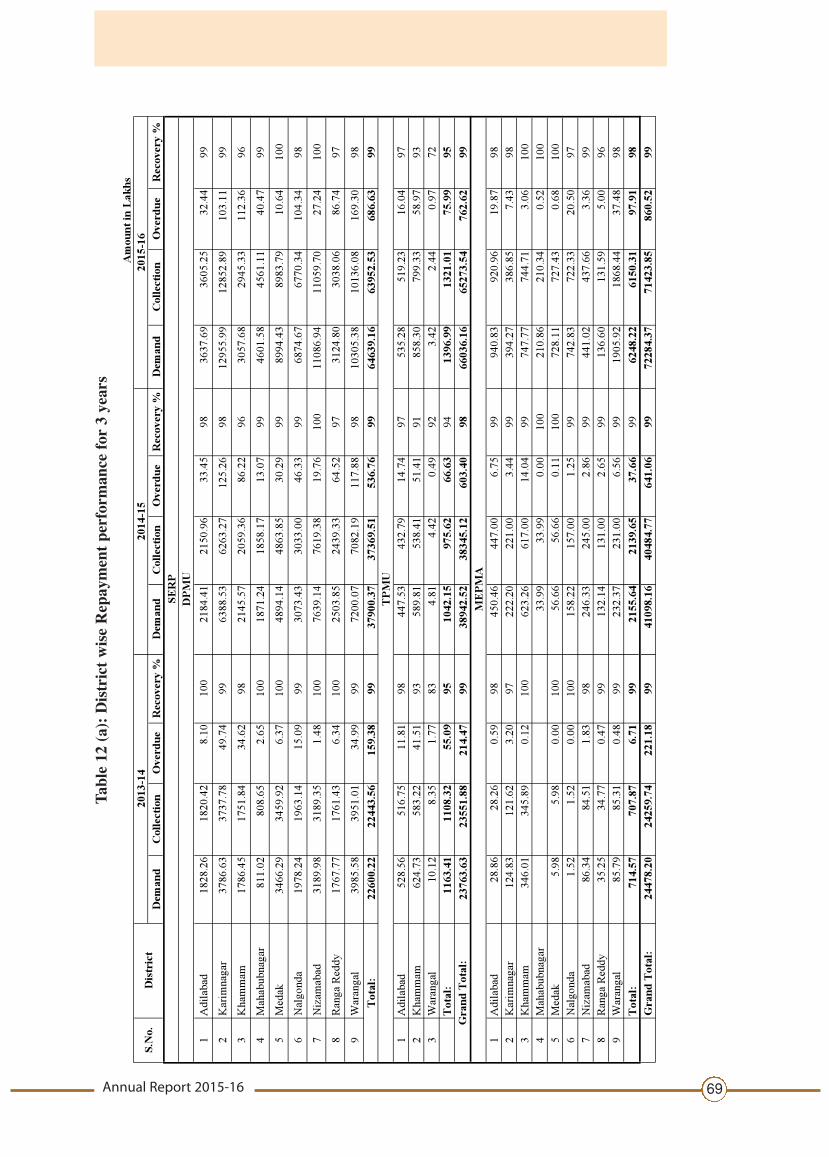

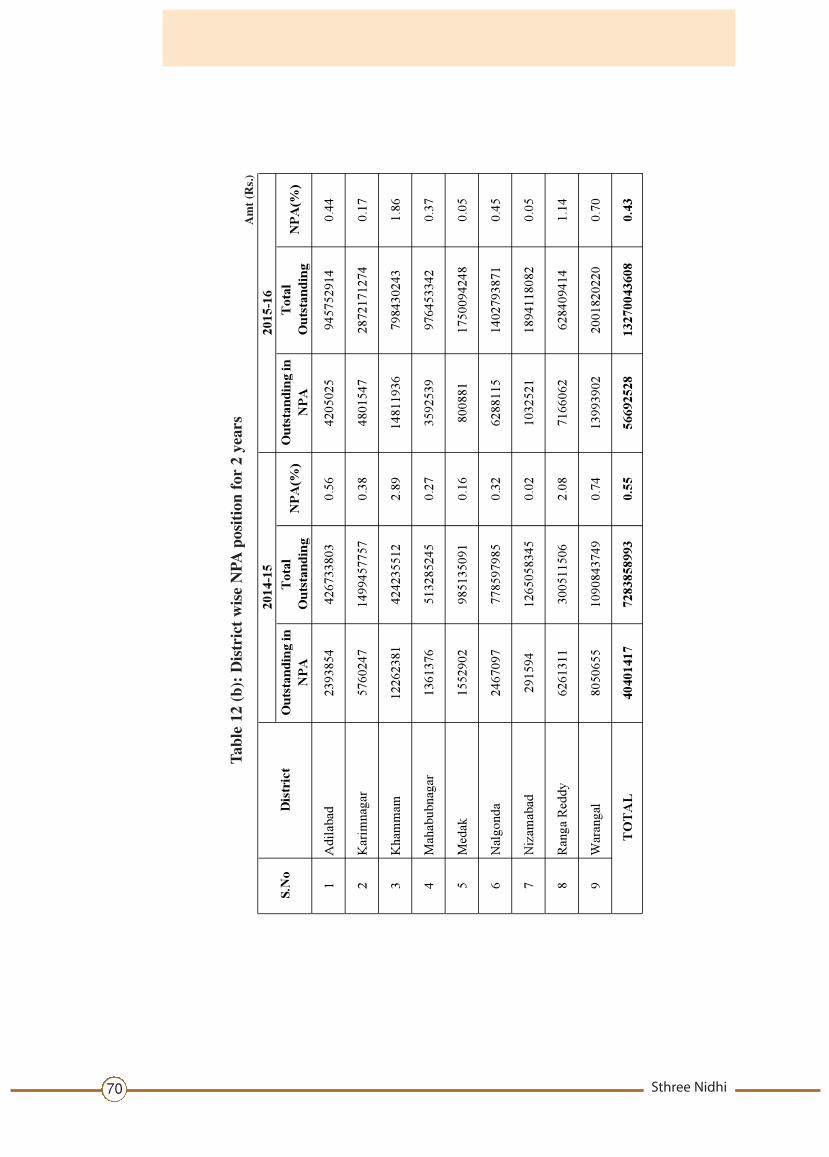

10.8. Stree Nidhi along with robust loan growth ensured quality of assets.As at the endof FY 2015-16, non- performing assets stood at Rs. 5.74 cr. constituting 0.43% of thetotal loans outstanding of Rs. 1330.12 Cr. The provision coverage is 225%. The Net NPAcontinued to be at ZERO as at the end of 31.3.2016. During the year, the repaymentrate of loans was at 98.82% against the demand. District wise details of repaymentperformance and NPA are furnished in Table no. 12(a) & (b) in Part-C of this report.

Outstanding NPA - 0.43%

NPA Position

Annual Report 2015-16 35

Credit Risk Mitigation- Stree Nidhi Suraksha

10.9. The SHGmembers are poor and in the event of any untoward incident the familywill be exposed to great risk and difficulties. Keeping this in view Stree Nidhi hasdevised a self- sustainable scheme called “Stree Nidhi Suraksha” to mitigate such riskand has been implementing the same since 01.04.2014 with the following objectives.

a).To protect the family members of a SHG member from financial risks in the event ofuntimely death of member.

b). To safe-guard the institutions of the poor (SHGs) and their federations from theburden of repayment of loan availed by the member in the event of death, therebyprotecting them from becoming defunct and disintegration due to repaymentburden.

c). To improve confidence of SHGs/VOs to face challenges arising on account of deathof members after availing credit from Stree Nidhi.

d). To ensure risk mitigation to Stree Nidhi loan portfolio.

The scheme provides for hassle free settlement of claims and relief to the familymembers of the diseased members.

Salient features of the Stree Nidhi Suraksha Scheme

10.9.1. All the members of SHGs who avail Stree Nidhi loans and the members whoavail loans under Other Stree Nidhi loans are covered. Charges payable are @ Rs.4/- peryear per Rs 1000 loan amount. The total loan availed by the individual member is thesum assured. Coverage commences from the date of availing loan and is valid up tothe due date of last installment.

Settlement of claims

10.9.2. The scheme is being implemented in coordination with Social Security unit,SERP. The claims received through ZS call centres are settled at H.O, Stree Nidhi afterreceiving verification report from the field functionaries.The registration of claims andreceipt of documents will be ensured by ZS call centres and Bhima Mitras. Stree Nidhipays service charges to ZS call centres for the services utilised.The details of thecoverage and claims settled are given in the table.

Coverage of members (Rs. Lakh)

Year No. of members Charges

covered received

2014-15 3,66,886 637.45

2015-16 4,92,753 1256.39

Sthree Nidhi36

Claims settled as on 31.03.2016

No. of Claims registered 837

No. of Claims settled 465

Amount of Claims settled (Rs. lakhs) 100.30

No. of Claims pending 372

10.9.3. Efforts are being made to settle the claims without any delay through

continuous follow up with field functionaries and Zilla Samakhya call centres. Out of

the amount received towards charges under Stree Nidhi Suraksha,a part of the amount

is retained for settlement of claims, and the balance is Rs. 15.47 cr. is invested in the

form term deposits in Banks.

Annual Report 2015-16 37

Chapter 11

Monitoring – An effective Mechanism

11.1. Stree Nidhi has evolved systems and procedures and fine tuned monitoringmechanism from time to time to suit the needs. To facilitate proper implementation,and compliance with the guidelines and to achieve desired goals of the organisation,a five tier monitoring mechanism is put in place as explained below.

Head Office level:

11.2. For monitoring the performance of districts and to take required follow upmeasures on a regular basis, a separate unit has been established at HO being headedby Deputy General Manager. Review meetings are conducted with Zonal Managersand Regional Managers at monthly intervals and with all the staff members atquarterly intervals. An effective and real time MIS is available to monitor progressunder all the key business parameters.For monitoring the functioning of federations ofSHGs i.e,VOs/SLFs a separate unit is established under the supervision of a DGM.

At District level:

11.3. The progress is closely monitored by the Project Director, DRDA and ProjectOfficer, ITDA and Project Director,MEPMA on a regular basis in consultation with ZonalManager and Regional Manager of Stree Nidhi. Regular review meetings areconducted with SERP andMEPMA staff to monitor progress at district level.All the staffincluding PD,DRDAs are given logins to access data base and MIS of their area ofoperations.

At Mandal/TLF level:

11.4.The staff of SERP namely ACs,APM and CCs play a key role in facilitating the needymembers to avail the financial services from Stree Nidhi.Under the close supervision ofAPM/TMC, the activities of Stree Nidhi are implemented effectively at grass root levelin coordination with Cluster Coordinators and other staff. Stree Nidhi has positionedstaff in the cadre of Managers/Asst. Managers for monitoring purpose for every 7-8mandals depending on the volume of business. The staff of Stree Nidhi visit VOs/SLFson a regular basis and take necessary steps to address issues at field level to ensurethat needy get credit and to achieve desired performance at district level under allparameters. All the SERP / MEPMA staff at mandal and TLF level are given logins toaccess data/MIS for regular monitoring.

Stree Nidhi Resource Persons:

11.5. Apart from the supervisory role played by the staff of SERP, MEPMA and StreeNidhi, community is also involved in monitoring the activities of Stree Nidhi. One ortwo suitable SHG members are identified from EC members of VOs/SLFs as Stree Nidhi

Sthree Nidhi38

Resource Persons (SNRP) to monitor operations at MS/TLF level having reasonablevolume of business. The SNRPs visit the VOs/SLF//SHGs and extend hand holdingsupport to ensure credit flow to the needy,ensure documentation,end use, repayment,mobilisation of savings etc. The SNRPs are paid service charges depending on theirperformance on a monthly basis. To update the skills of SNRPs, the Regional Manager,Stree Nidhi of the district conduct review meetings at monthly intervals and providerequired guidance to them to address the issues and to improve performance.

Review of performance of Stree Nidhi in respective Mandal /TLF will be one of theagenda items in themonthly ECmeetings of MS/TLF and suitable resolutions aremadeand to improve performance.

At VO/SLF level:

11.6. These institutions play a vital role in increasing outreach of financial services viz.savings and loans SHGs/Members as also in verification of loan utilisation. In the ECmeetings of VOs/SLFs, performance of Stree Nidhi will be one of the agenda items toreview. VO office bearers are made aware of Stree Nidhi services every year topropagate the same in villages.Close monitoring is done by Office bearers of VOs/SLFs,SNRPs, CCs and Staff of Stree Nidhi to facilitate Stree Nidhi services effectively.

SOCIAL AUDIT

11.7. To ensure transparency and accountability of the financial transactions made atVO/SLF level, these operations are subjected to the process of Social Audit.The servicesof CARPs and TSSAAT are utilised for the purpose. The issues surfaced if any will bediscussed in Gramasabhas and will be dealt suitably.

Annual Report 2015-16 39

Chapter 12

F inancial Performance

12.1.The performance highlights in respect of key parameters for the last two years arementioned in the following table.

(Rs. Cr)

S.No. Particulars 31.03.2015 31.03.2016

1 Share capital 90.49 90.89

2 Grants from Govt. 50.07 55.57

3 Undistributed Profit and Reserves 41.45 73.68

4 Own Funds (Share Capital, Profit,Reserves & Core Deposits) 304.31 482.11

5 Deposits 165.60 317.97

6 Borrowings 457.74 824.34

7 Loan amount outstanding 784.87 1330.12

8 Loan amount disbursed 703.05 1148.35

9 Gross NPA 3.46 5.74

10 Loan loss provisions 7.86 13.33

11 NPA% 0.53 0.43

12 Net NPA 0 0

13 Net profit 18.51 37.25

12.2. The borrowings constitute 51.01% of the average working funds as on 31.3.2016

as against 43.84% as on 31.3.2015.The deposits from SHGs and their federations as on

31st March 2016 were at Rs. 317.97 cr as against Rs. 165.07 cr as on 31st March 2015

showing a growth of Rs.152.90 cr during the year.This is due to increase inmobilisation

of deposits under Samruddhi and CIF Corpus deposit schemes.

Sthree Nidhi40

12.3. Earnings appraisal as on 31 March 2016(Rs. Cr)

S. % to % toNo. Income Amt. total Expenditure Amt. total

Income expenditure

1 Interest on 119.93 96.47 Interest paidAdvances on deposits 20.79 23.88

2 Interest on 1.40 1.13 Interest onInvestments Borrowings 43.53 50.00

3 Other Income 2.99 2.40 OperatingExpenses 17.27 19.84

4 Loan LossProvision 5.47 6.28

Total Income 124.32 TotalExpenditure 87.06

Net Profit 37.25

12.4. Financial Analysis

S.No Particulars 31st March 2015 31st March 2016

1 Total income (Rs. in Cr) 64.82 124.32

2 Total Expenditure (Rs. in Cr) 46.31 87.06

4 Net Profit (Rs. in Cr) 18.53 37.25

5 Cost to Income Ratio (%) 71.44 70.03

6 Operational Self Sufficiency Ratio (%) 139.64 139.97

7 Financial Self Sufficiency Ratio (%) 136.16 143.09

8 Cost of Funds (%) 7.43 7.51

9 Yield on Advances (%) 13.91 13.81

10 Interest Margin (%) 6.48 6.30

11 Net Interest Margin (%) 5.83 5.78

12 Capital to Risk weighted Assets Ratio 33.10 35.44

13 Return on equity (%) 20.92 41.19

14 Return on Assets (%) 3.52 3.84

15 Operational cost to working funds (%) 0.72 1.09

16 Borrowings toWorking Funds (%) 50.01 51.01

17 Debt Equity Ratio (%) 1.44 1.85

18 Per employee loan portfolio outstanding (Rs lakh) 10.90 16.62

Net income

12.5. Total income has increased from Rs. 64.82 cr to Rs.124.32 cr and the expenditurehas increased from Rs. 46.31cr to Rs.87.06 cr in FY 2015-16. The growth in income was

Annual Report 2015-16 41

at 91.79% as compared to growth in expenditure at 87.99%. The increase inexpenditure was on account of increase in borrowings. The net interest incomeincreased from Rs.63.11 cr in 2014-15 to Rs. 121.33 cr in 2015-16 registering a robustgrowth of 92.2 %. This was mainly on account of increase in advances. However,effective management of financial resources and control of operational expenditurehas also resulted in containing the expenditure.

Operating and Net Profit

12.6. The operating profit and net profit were Rs. 42.72 cr and Rs 37.25 cr. respectively

during the year 2015-16 as compared to Rs.21.98 cr and Rs. 18.53 cr. during the year

2014-15 showing a year on year growth of 101% in net profit. This profit is generated

even after making provision of 1% on the total loan outstanding as on 31 March 2016,

which has increased significantly from Rs. 7.86cr as on 31 March 2015 to Rs. 13.33 cr as

on 31.3.2016.

Cost to Income Ratio:

12.7. Cost to Income Ratio has reduced marginally from 71.44 % as on 31.3.2015 to

70.03% as at 31st Mar 2016 indicating the control in cost of operations by ensuring

high repayment against the demand.

Cost of Funds,Yield on Advances and Interest Margin:

12.8. The cost of funds has increased from 7.43 % to 7.51 % for the FY 2015-16 as

compared to previous year mainly on account of increase in the share of borrowings

and deposits in working funds.

12.9.The yield on advances was at 13.81% for the FY 2015-16 which is slightly less than

13.91% for the FY 2014-15.This is due to the sizeable credit flow during second half of

the financial year.

12.10.The interest margin stood at 6.30 % for FY 2015-16 which has reduced from 6.48

% for the year 2014-15.The increase in cost of funds during the current year compared

to last year resulted in a reduction in interest margin.

Net Interest Margin:

12.11. Net interest margin was 5.78% for FY 2015-16 and the same has reduced from

5.83 % for FY 2014-15. The interest paid on deposits and borrowings has increased

during the current year.

OSS and FSS:

12.12.Operational Self Sufficiency Ratio was at 139.97% for FY 2015-16 as compared to

139.64 for the year 2014-15. Financial Self Sufficiency ratio was at 143.09% for FY

2015-16 as against 136.16% for FY 2014-15. These ratios are indicating that the

earnings of Stree Nidhi reflect the strength of the institution in meeting all expenses.

Sthree Nidhi42

Return on Equity /Assets/ Earning Per Share:

12.13. Return on Equity has increased from 20.92% in FY 2014-15 to 41.19 % in FY2015-16.The return on equity has doubled as there is not much increase in equity butprofit has doubled. The earning per share of Rs.1000/ was Rs.205/- as on 31.3.2015which increased to Rs.409 as on 31.3.2016.

12.14. Return on Assets during the year was at 3.84% as compared to 3.52% in FY204-15.This is indicative of efficient liability management and increase in productivity.

Capital Adequacy Ratio:

12.15.Capital Adequacy Ratio has increased to 35.44% in FY 2015-16 from 33.10% in FY2014-15. Though assets under management have increased significantly and eventhough increase in owned funds was not high, the ratio could be maintained more orless at previous year due to accretion of core deposits in the form of CIF -Corpus.

Operational Cost toWorking Funds:

12.16. Operational Cost to Working Funds ratio has increased to 1.09% on 2015-16 ascompared to 0.72% previous year.This is due to higher expenditure on service chargespaid to SERP staff and SNRPs. There is also increase in staff and thus expenditure onsalaries paid to staff. The expenditure is however within the 2% of working funds.

Borrowings toWorking Funds:

12.17. Borrowings to Working Funds ratio has increased from 50.01% in FY 2014-15 to51.01% in FY 2015-16.

Debt Equity Ratio:

12.18. Debt Equity ratio has increased from 1.44 % in FY 2014-15 to 1.85% in FY2015-16 due to increased share of borrowings.

Annual Report 2015-16 43

Chapter 13

Inclusive Growth-Stree Nidhi asCorporate Business Correspondent

13.1. Poverty and exclusion are still predominant in socio and economic front. Many

anti-poverty and employment generation programmes have been implemented for

decades in India. Though Banks have a major role in extending financial services viz.

savings, disbursal of credit, and providing other financial services to the poor, still a

large no of poorer segment of the population is excluded even years after introduction

of inclusive banking initiatives in the country. Though cooperative movement,

nationalization of banks and creation of regional rural banks have yielded some results,

financial inclusion and deepening need to be given major push as the same is

considered essential for inclusive growth and development.

13.2. Financial Inclusion is the “process of ensuring access to appropriate financial

products and services needed by all sections of the society in general and vulnerable

groups such as weaker sections and low income groups in particular, at an affordable

cost in a fair and transparent manner by regulated,mainstream institutional players”.

13.3. To achieve the above objective, in January 2006 the Reserve Bank permitted

banks to utilize the services of intermediaries in providing banking services through

the use of business facilitators and business correspondents. The BC model allows

banks to do ‘cash in – cash out’ transactions at a location much closer to the rural

population, thus addressing the last mile problem. Various models viz., Kiosk, Point of

Service and Mobile models are being tried our by various BCs of Banks.Under business

correspondent model, the scope of activities to be undertaken includes Credit,

Deposits,Withdrawals, Savings, Remittances,Micro insurance and DBTs.

Stree Nidhi as Business Correspondent:

13.4. Stree Nidhi Credit Cooperative Federation Limited., owned jointly by the

Community and Government has established itself firmly in delivering financial

services using technology and electronic payment systems. It has been handling huge

volumes of transactions and reconciliation there of Stree Nidhi forayed into Financial

Inclusion activity seamlessly as there is a well organized structure of SHGs and their

federations, dedicated staff and support of SERP in the field.

13.5.Stree Nidhi has been positioned as a Corporate BC to State Bank of Hyderabad and

Andhra Bank. It has 1156 BC points serving 1150 Gram Panchayats in 320 mandals and

8 districts of Telangana State. These 1156 BC points include 607 BC points allotted

during October 2015 by SBH. Further, Andhra Bank has allotted 116 BC points during

Sthree Nidhi44

October 2015 and SBH has allotted 108 BC points during January 2016 to support the

launch of Palle Samagra Seva Kendralu. Details are furnished in table no. 13 in Part-C

of this report.

13.6. Stree Nidhi is using Kiosk model, taking full advantage of technology that is

preferred by most of the Banks. Apart from banking services, with the help of

Government it has been helping in payments viz. insurance, pension, utility payments,

NREGS wages etc., through ‘branchless banking’ by opening VLE centres as service

delivery points. Stree Nidhi will emerge into a full-fledged payment services centre at

village level thus becoming a gateway to all financial services in villages.