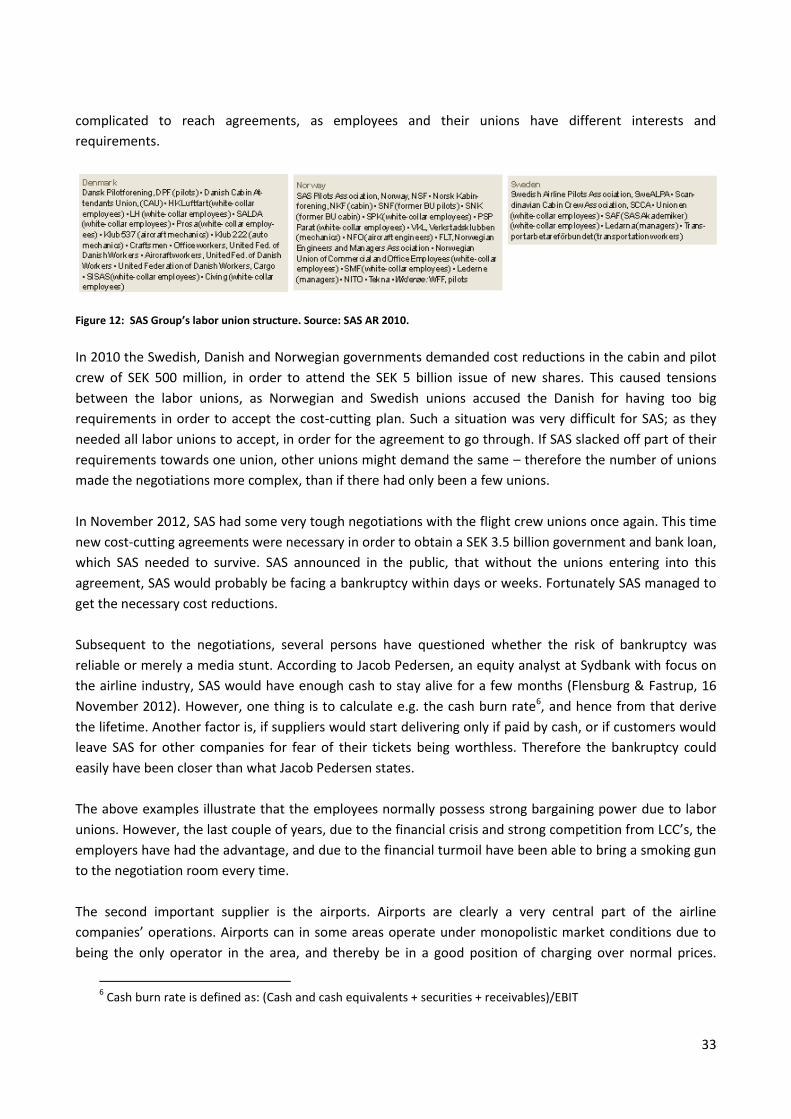

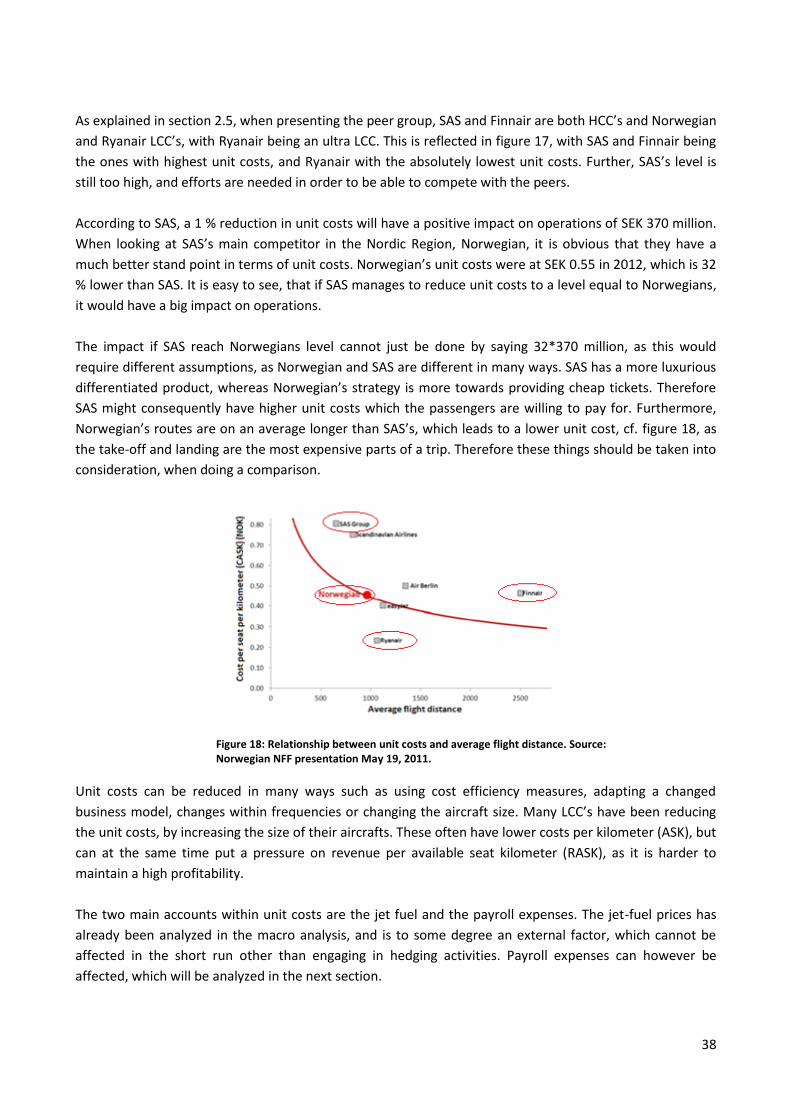

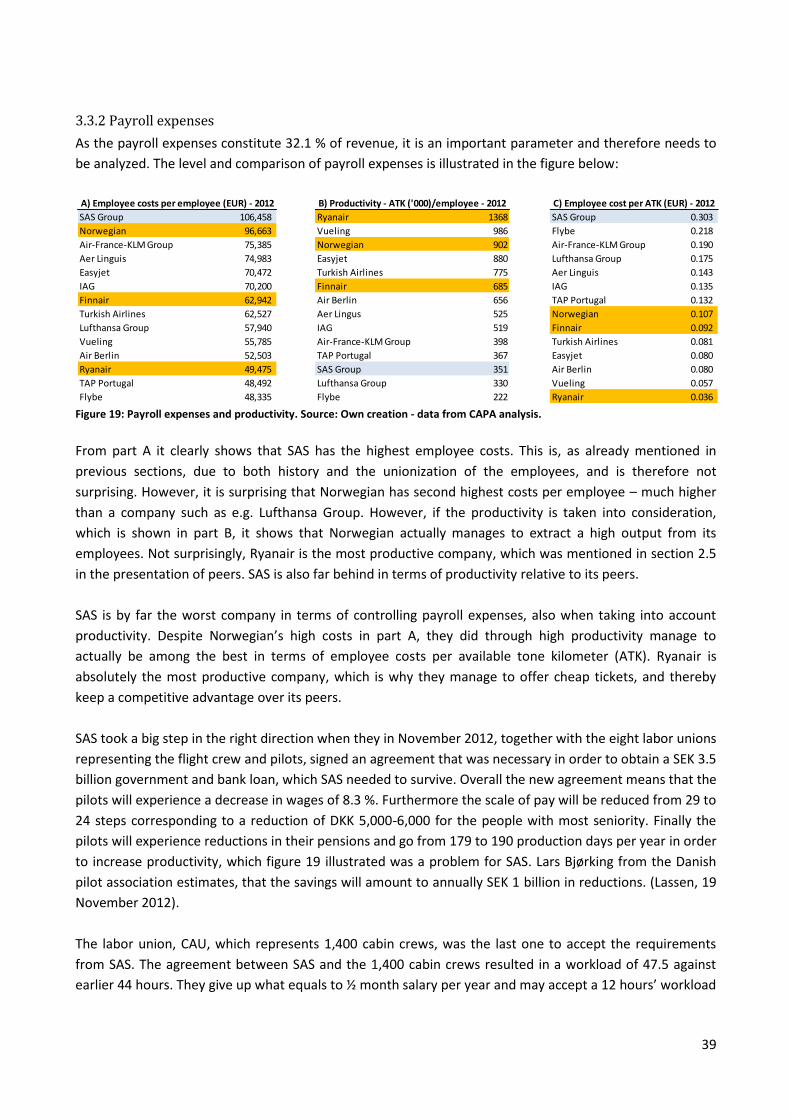

strategic analysis and valuation of scandinavian airlines

TRANSCRIPT

Master of Science in Economics and Business Administration

Accounting, Strategy and Control (ASC)

Strategic Analysis and Valuation of Scandinavian Airlines - A company in financial turmoil

Master’s Thesis

11 September 2013

Mikkel Allen Kjærsgaard

Supervisor: External Associate Professor Daniel Probst 80 pages and 183.561 characters

Copenhagen Business School 2013

2

3

Executive Summary

The central objective of the thesis has been to determine which models were most suitable in order to

carry out a valuation of Scandinavian Airlines (SAS) as per 1 May 2013. The decision of which model is the

most optimal to apply, does among other things depend on, whether SAS is assumed to continue as going

concern or not - which have been analyzed thoroughly.

Before being able to conduct the valuation, a strategic and financial analysis was conducted, in order to

understand the historical performance, and to estimate future financial performance of SAS, which

obviously lays the foundation for the value creation in a company.

Through the strategic analysis it has been concluded that the airline industry is characterized by high

competition among the different operators. Specifically after the 00’s with the IPO of Norwegian in 2003,

SAS has experienced an increasingly competition, which have resulted in a loss of market share of 7

percentage points from 2008 to 2012. This negative trend is assumed to continue in the realistic scenario,

unless something dramatic happens in SAS.

Among the important initiatives that SAS has in their strategy, is to decrease the level of unit costs. These

are of big importance in the industry, as they decide the competitiveness of the company, in terms of e.g.

offering cheap tickets to passengers. Unfortunately SAS has the highest unit costs in their peer group, 47 %

higher than Norwegian, its biggest competitor.

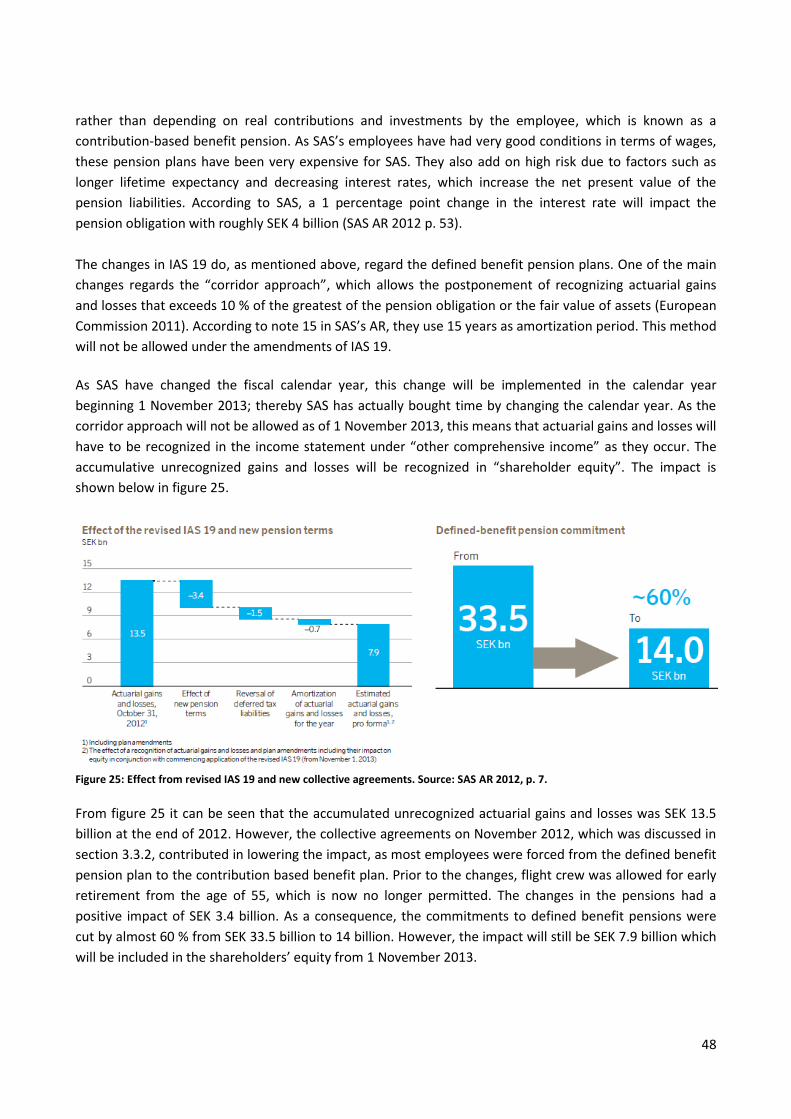

As of 1 November 2013, SAS has to adapt to new changes to IAS 19, regarding actuarial losses/gains from

future discounted pension obligations. This will cause a loss of SEK 7.9 billion on shareholders’ equity from

next year, which corresponds to a loss of 70.1% of SAS’s equity. As a consequence SAS will likely be forced

to raise additional capital – which may be a difficult task after having asked investors for additional capital

in both 2009 and 2010.

After defining three different scenarios for SAS’s future performance, the share price was determined. The

optimistic and realistic scenarios were based on going concern and were valued by applying the DCF model.

The worst case scenario was liquidation, which was supported by Altman’s Z-score, indicating a high

probability of default within the next 12 months. Also credit default swaps with different maturities

indicated high probability of default. The price was determined to SEK 11.26 against a price of SEK 12.10

observed in the market.

In order to test the valuation methods, a sensitivity analysis was carried out. It clearly indicated that the

share price is very sensitive to the different input factors, such as changes in the assumptions to the

development in e.g. payroll expenses, different levels of the growth rate in the terminal period and the

WACC. Hence, the valuation should be evaluated with prudence.

In order for SAS to continue as going concern, management has, as a minimum, to succeed with the current

strategy, otherwise liquidation may be just around the corner, and the company which we have all known

for years, will suddenly belong to the past.

4

Table of content

Part 1: Introduction .................................................................................................................................... 7

1.1 Motivation ......................................................................................................................................... 7

1.2 Problem statement ........................................................................................................................... 8

1.3 Methodology ..................................................................................................................................... 8

1.3.1 Delimitation ............................................................................................................................... 8

1.3.2 Research approach and quality evaluation ................................................................................ 9

1.3.3 Structure of project .................................................................................................................... 9

1.3.4 Discussion of main theories ..................................................................................................... 11

Part 2: Presentation of SAS ...................................................................................................................... 13

2.1 History ............................................................................................................................................. 13

2.2 Strategy ........................................................................................................................................... 14

2.3 SAS’s markets .................................................................................................................................. 15

2.4 Management, ownership and operational structure ..................................................................... 16

2.5 Peer group ....................................................................................................................................... 17

2.5.1 Norwegian Air Shuttle .............................................................................................................. 17

2.5.2 Ryanair ..................................................................................................................................... 18

2.5.3 Finnair ...................................................................................................................................... 18

Part 3: Strategic analysis .......................................................................................................................... 20

3.1. Analysis of the macro environment ............................................................................................... 20

3.1.1 Political factors ......................................................................................................................... 20

3.1.2 Economic factors ...................................................................................................................... 22

3.1.3 Social factors ............................................................................................................................ 26

3.1.4 Technical factors ...................................................................................................................... 27

3.1.5. Conclusion of PEST analysis .................................................................................................... 28

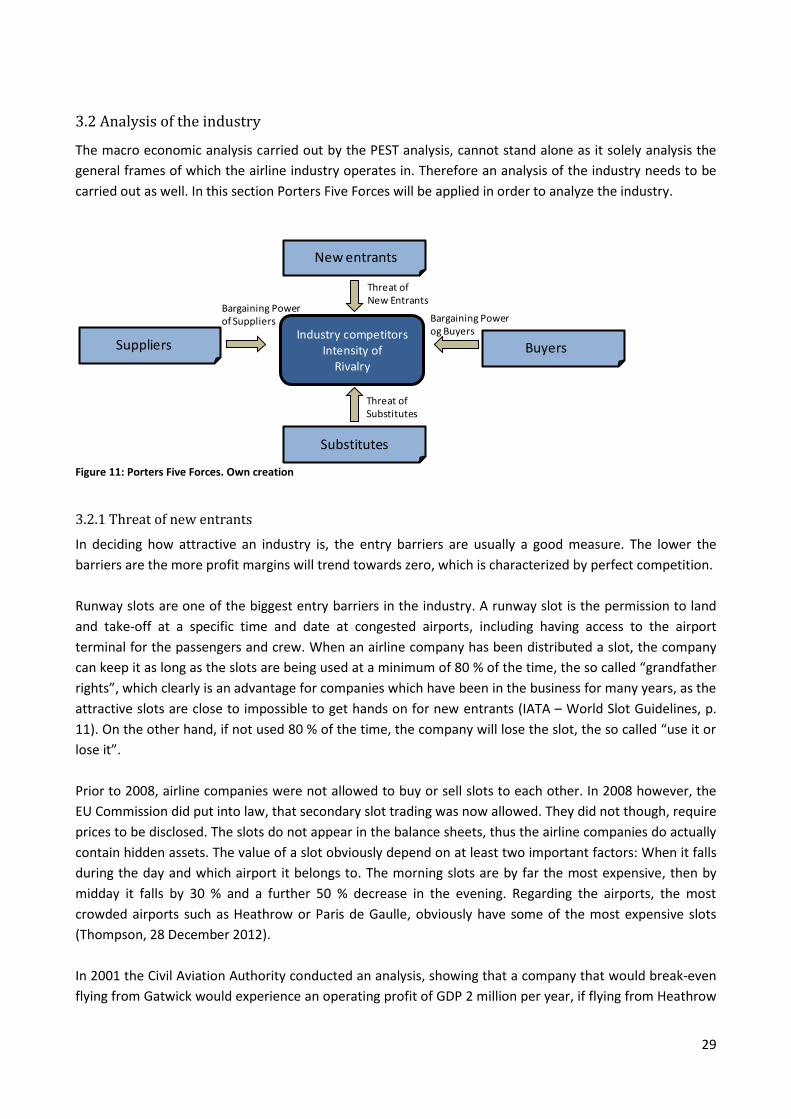

3.2 Analysis of the industry ................................................................................................................... 29

3.2.1 Threat of new entrants ............................................................................................................ 29

3.2.2 Threat of substitute products or services ................................................................................ 30

3.2.3 Buyers bargaining power ......................................................................................................... 32

3.2.4 Suppliers bargaining power ..................................................................................................... 32

3.2.5 The competition in the industry .............................................................................................. 34

3.2.6 Conclusion of the industry analysis .......................................................................................... 36

3.3 Internal analysis of SAS ................................................................................................................... 37

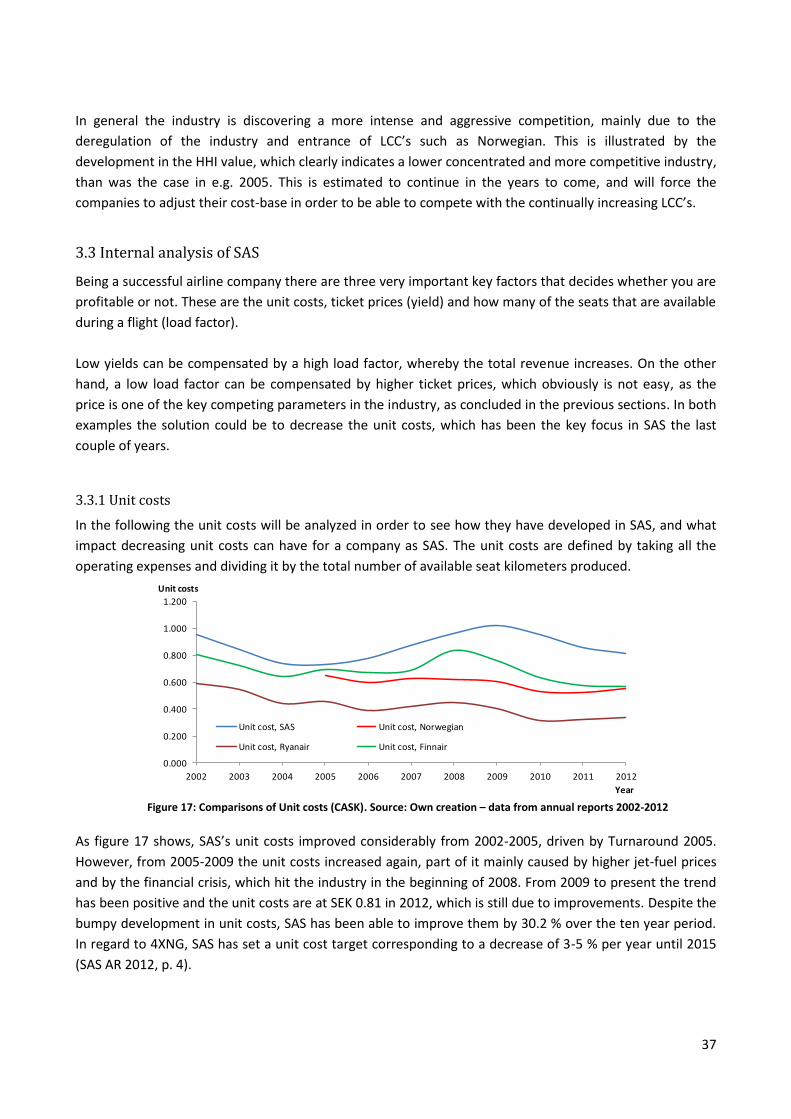

3.3.1 Unit costs.................................................................................................................................. 37

3.3.2 Payroll expenses ....................................................................................................................... 39

3.3.3 Yield and load factor ................................................................................................................ 40

5

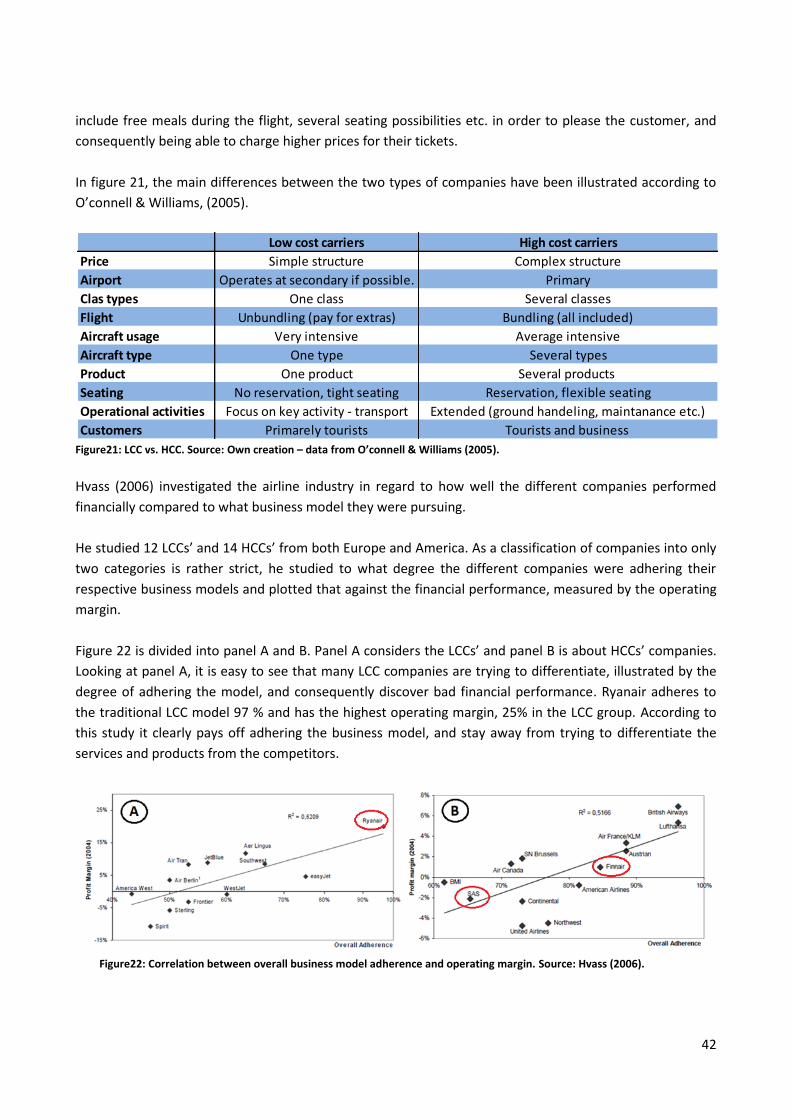

3.3.4 Optimal business model ........................................................................................................... 41

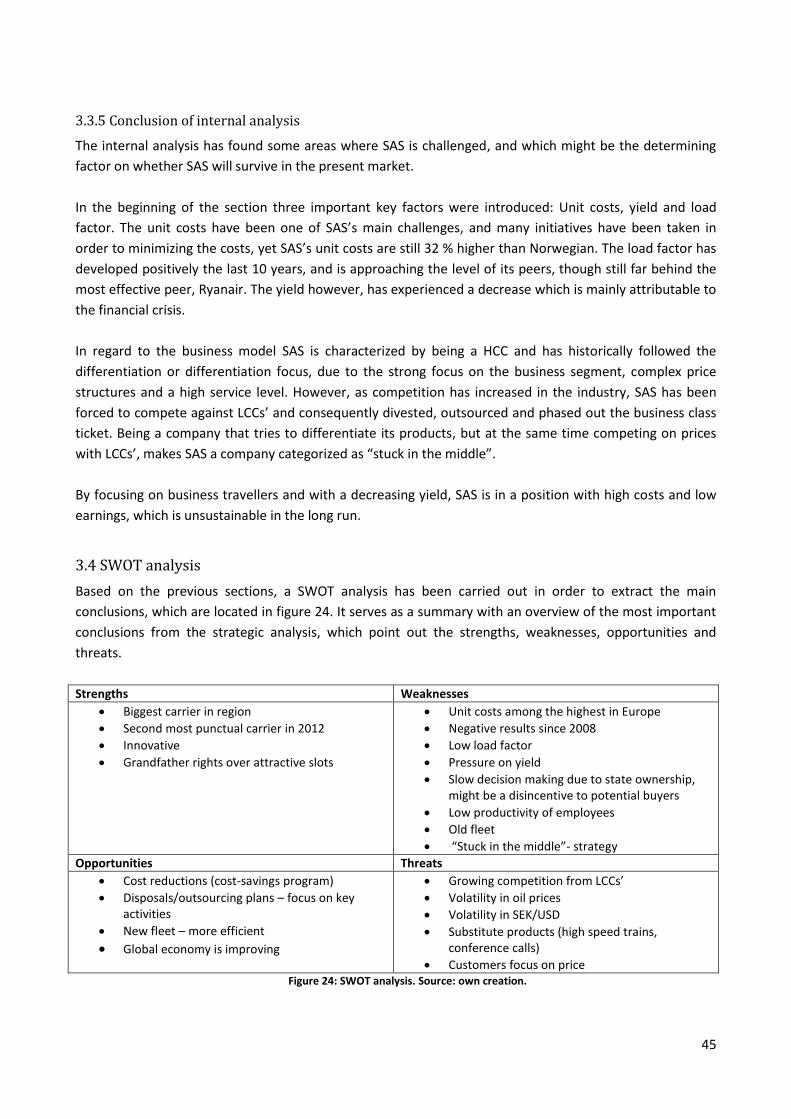

3.3.5 Conclusion of internal analysis................................................................................................. 45

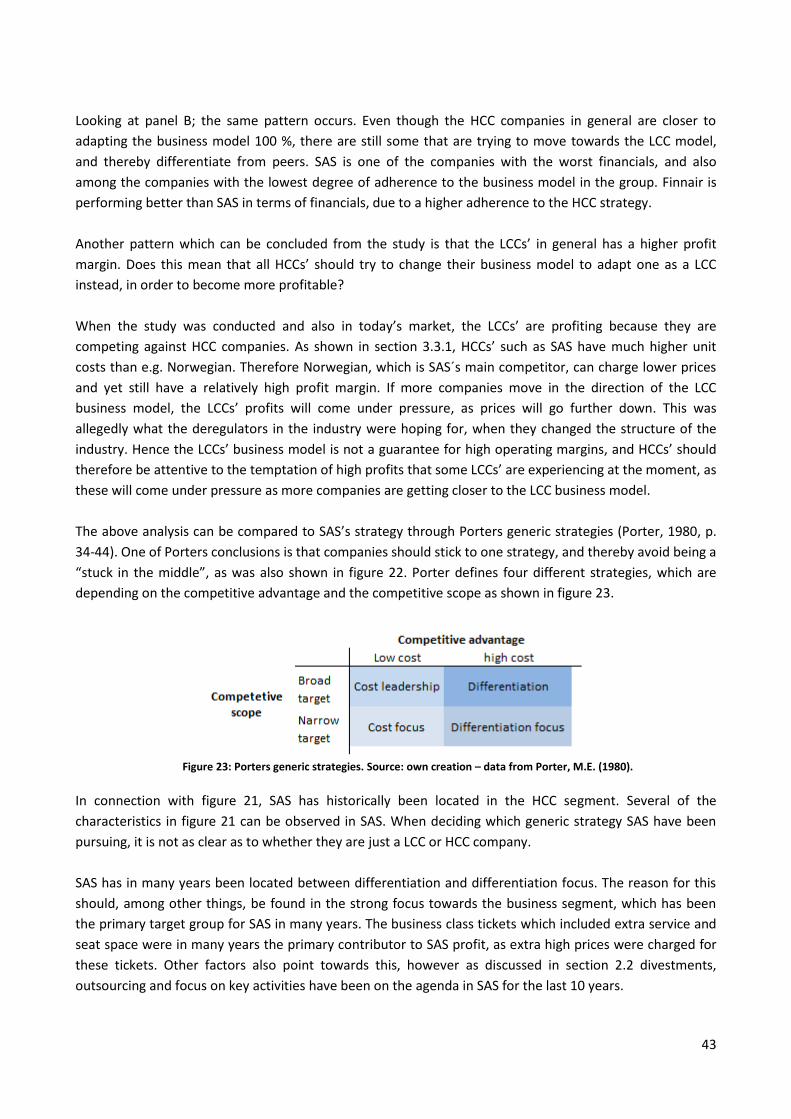

3.4 SWOT analysis ................................................................................................................................. 45

Part 4: Financial Statement Analysis ....................................................................................................... 47

4.1. Accounting policies ........................................................................................................................ 47

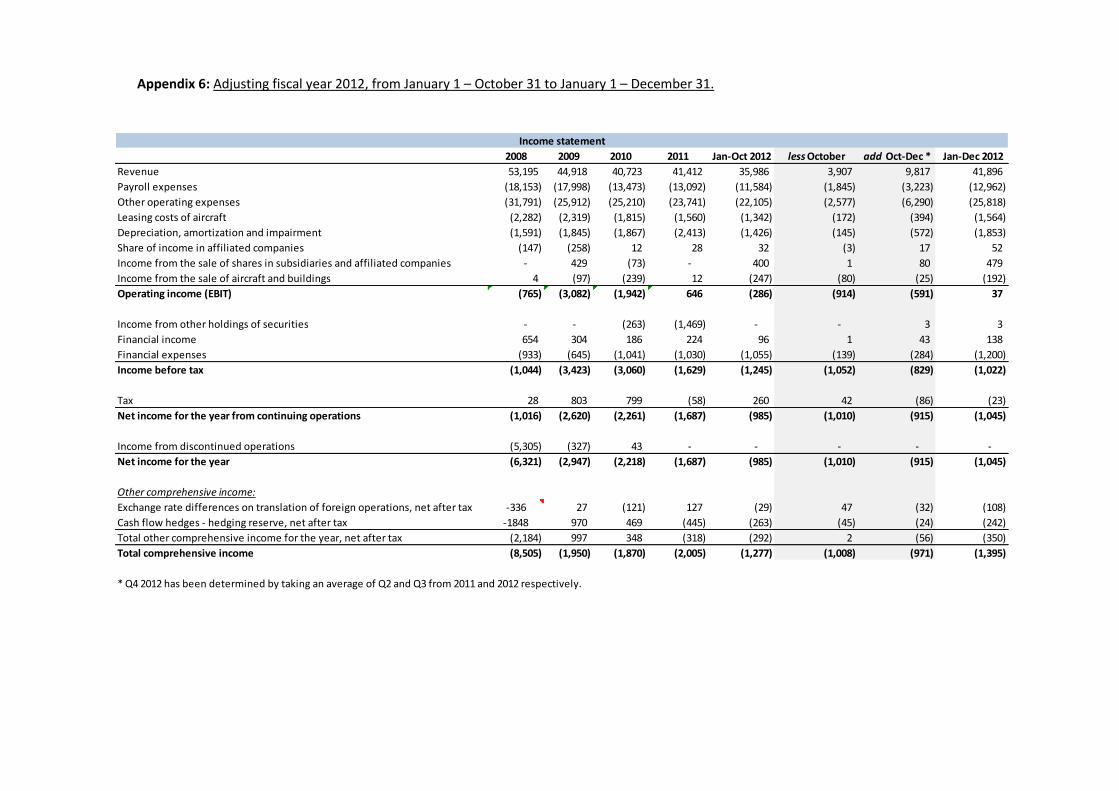

4.2. SAS’s new calendar year – due to IAS 19? ..................................................................................... 47

4.3 Preparing analytical income statement .......................................................................................... 49

4.4 Preparing analytical balance sheet ................................................................................................. 51

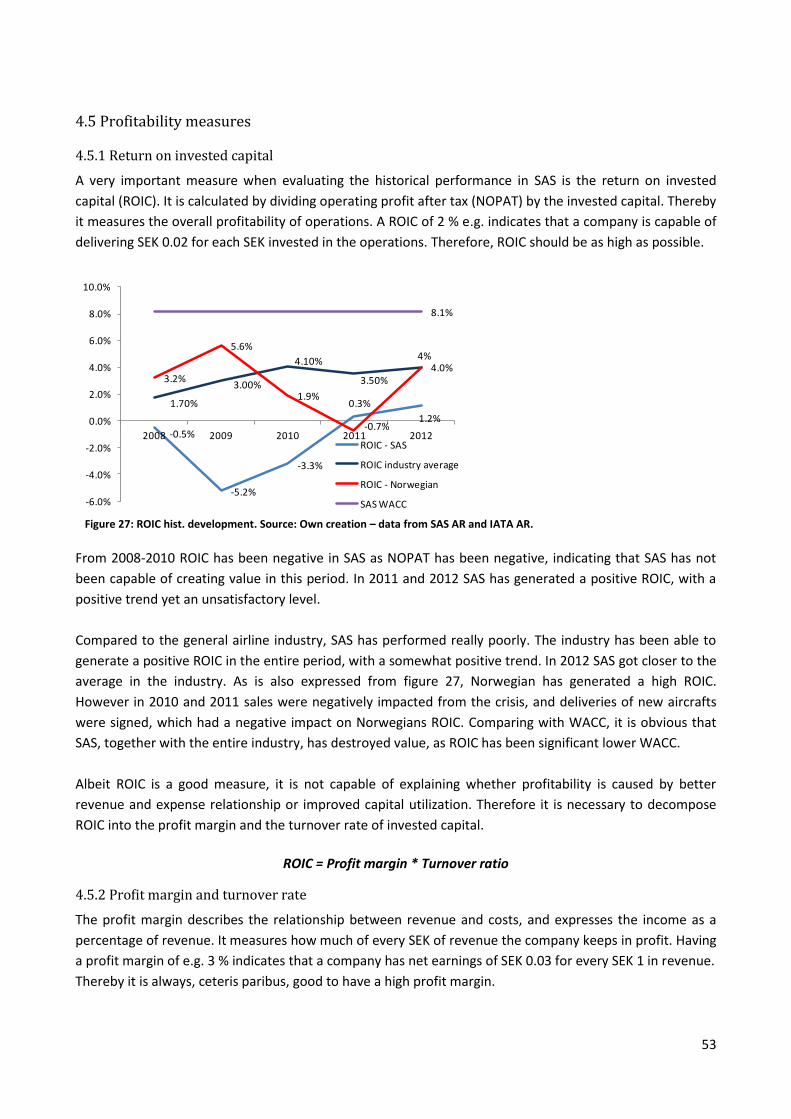

4.5 Profitability measures ..................................................................................................................... 53

4.5.1 Return on invested capital ....................................................................................................... 53

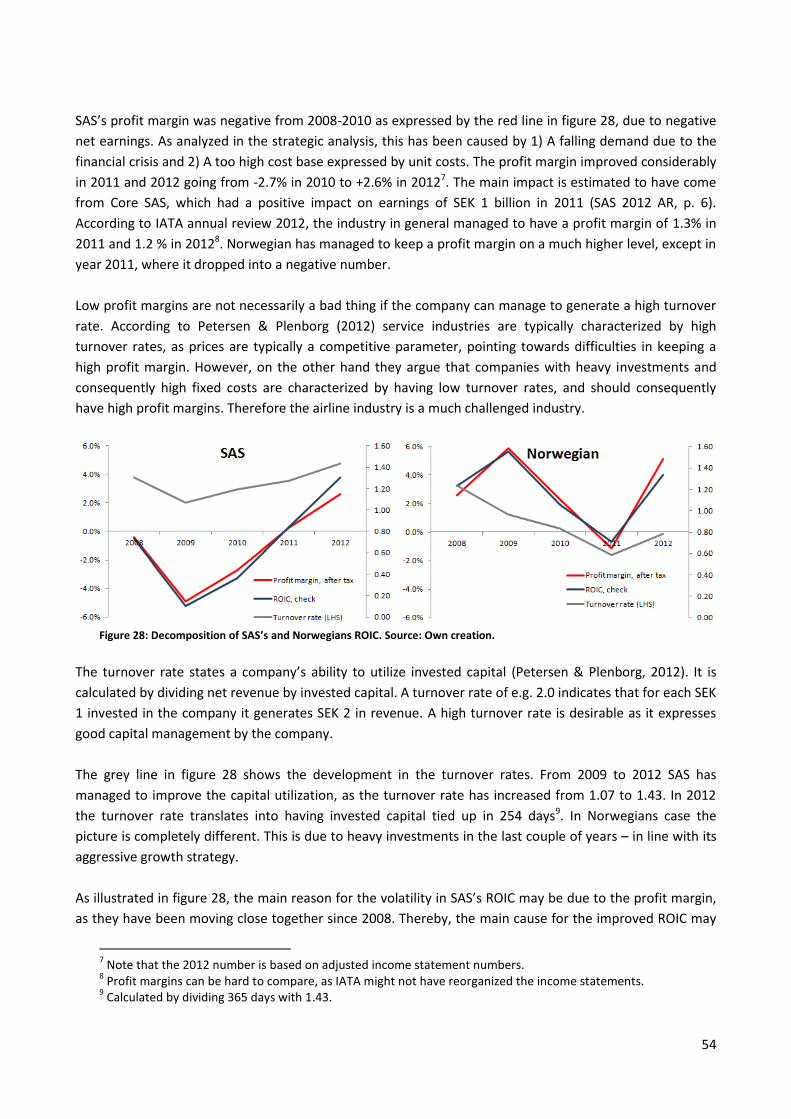

4.5.2 Profit margin and turnover rate ............................................................................................... 53

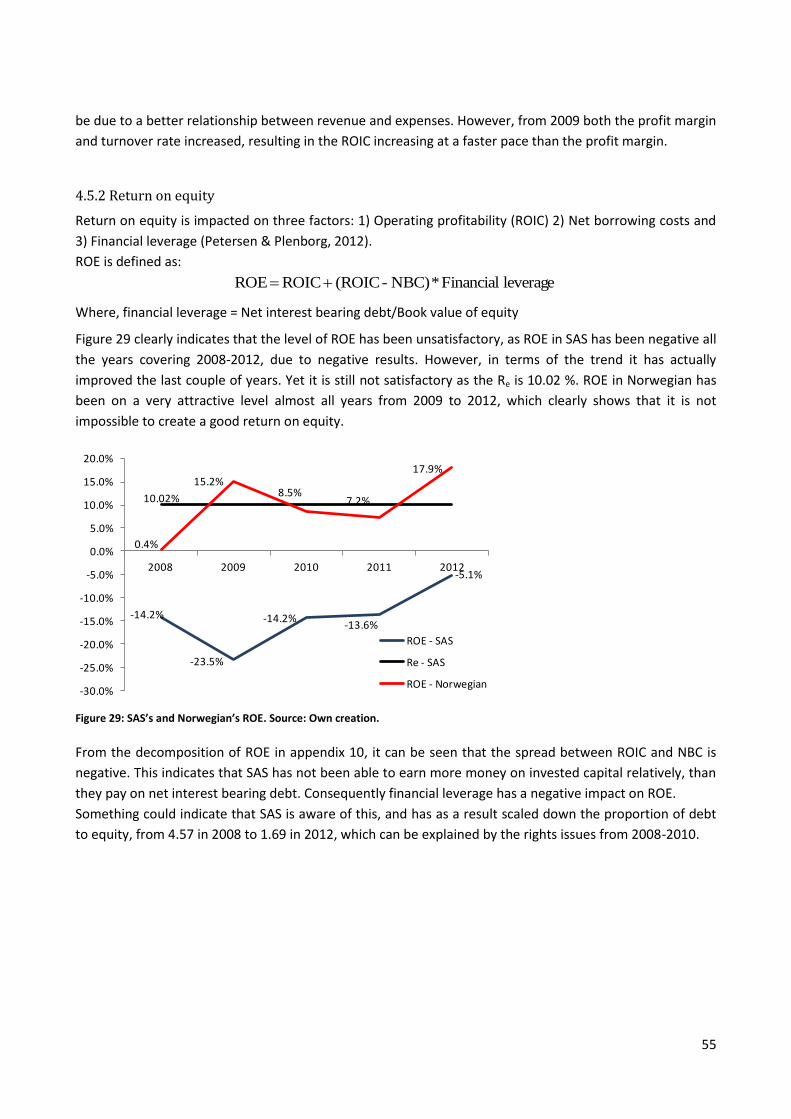

4.5.2 Return on equity ...................................................................................................................... 55

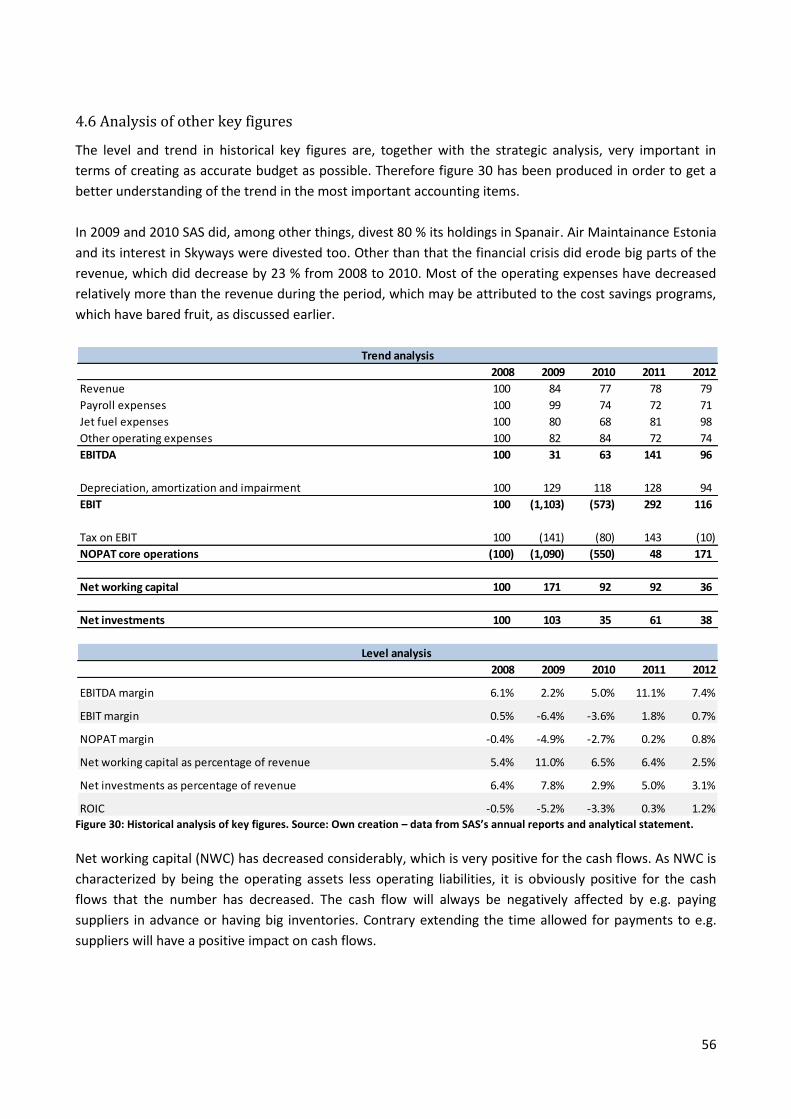

4.6 Analysis of other key figures ........................................................................................................... 56

4.7 Conclusion of financial statement analysis ..................................................................................... 57

Part 5: Budgeting ...................................................................................................................................... 58

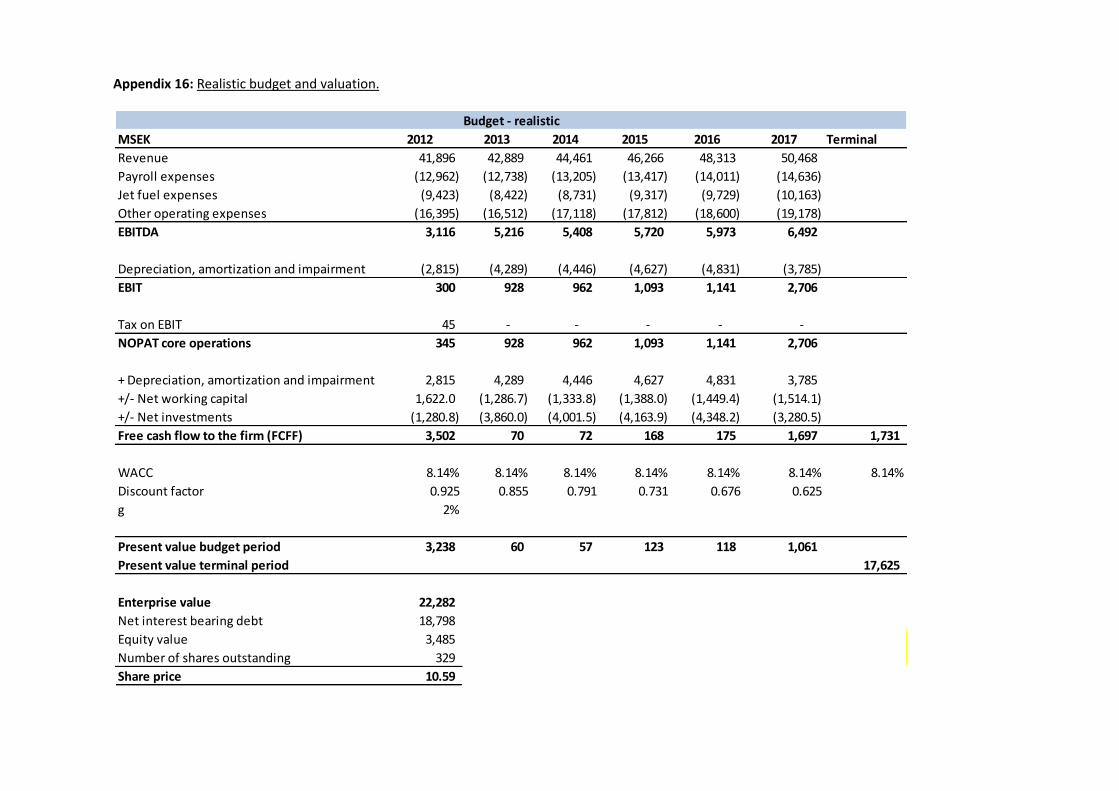

5.1 Realistic scenario ............................................................................................................................. 58

5.1.1 Revenue ................................................................................................................................... 58

5.1.2 Payroll expenses ....................................................................................................................... 60

5.1.3 Jet-fuel expenses ...................................................................................................................... 60

5.1.4 Other operating expenses ........................................................................................................ 61

5.1.5 Depreciation, amortization and impairment (DAI) .................................................................. 61

5.1.6 Net working capital .................................................................................................................. 62

5.1.7 Net investments ....................................................................................................................... 62

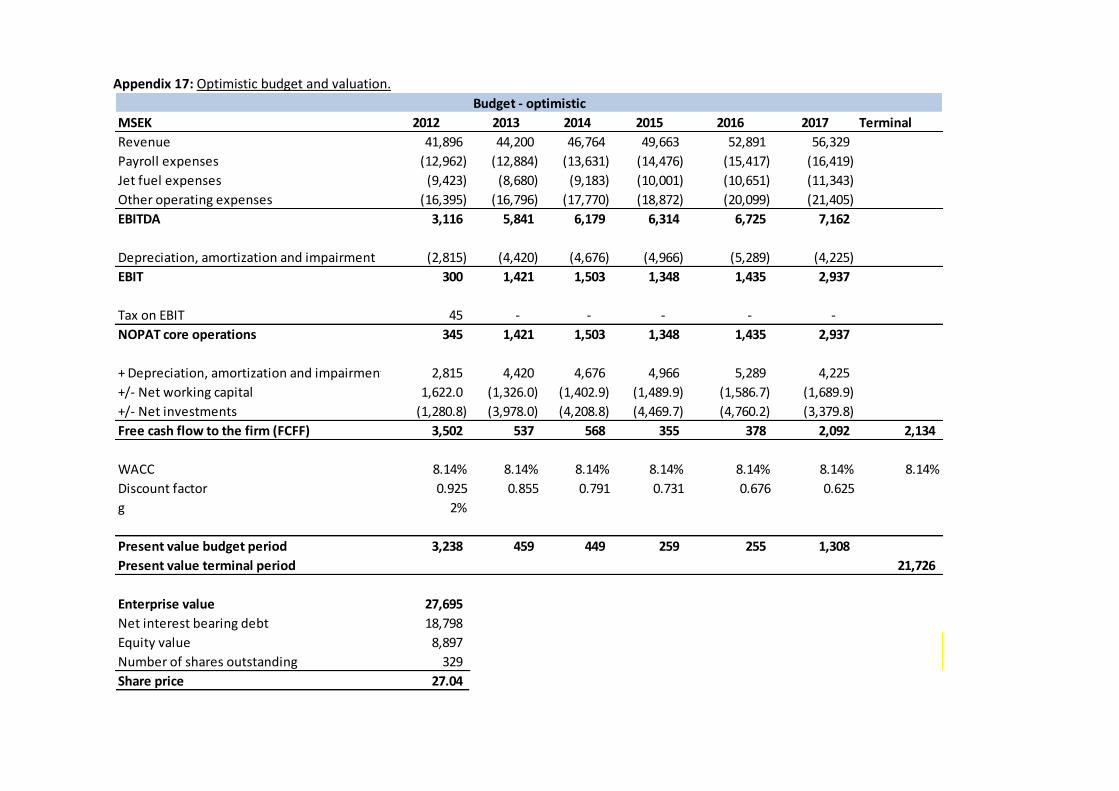

5.2 Optimistic scenario ......................................................................................................................... 62

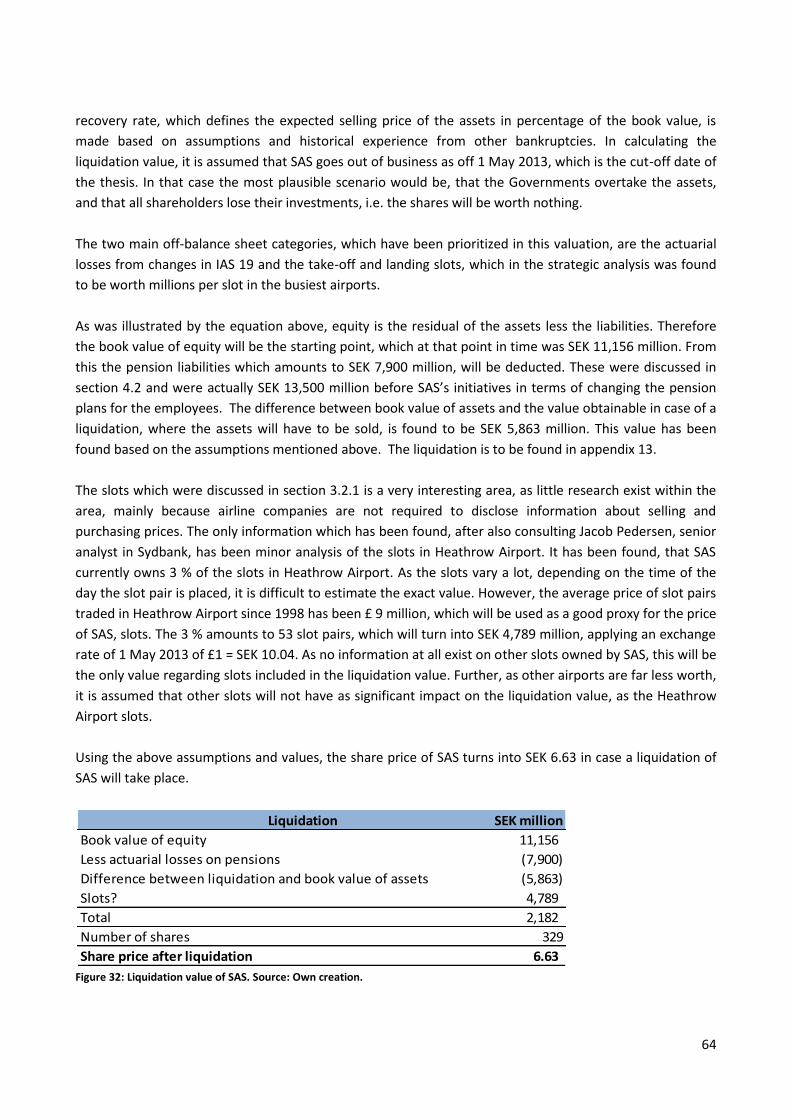

5.3 Non-going concern scenario - liquidation ....................................................................................... 63

Part 6: Cost of capital & Valuation .......................................................................................................... 65

6.1 Required rate of return on equity ................................................................................................... 65

6.1.1 Risk free interest rate ............................................................................................................... 65

6.1.2 Systematic risk – Beta .............................................................................................................. 66

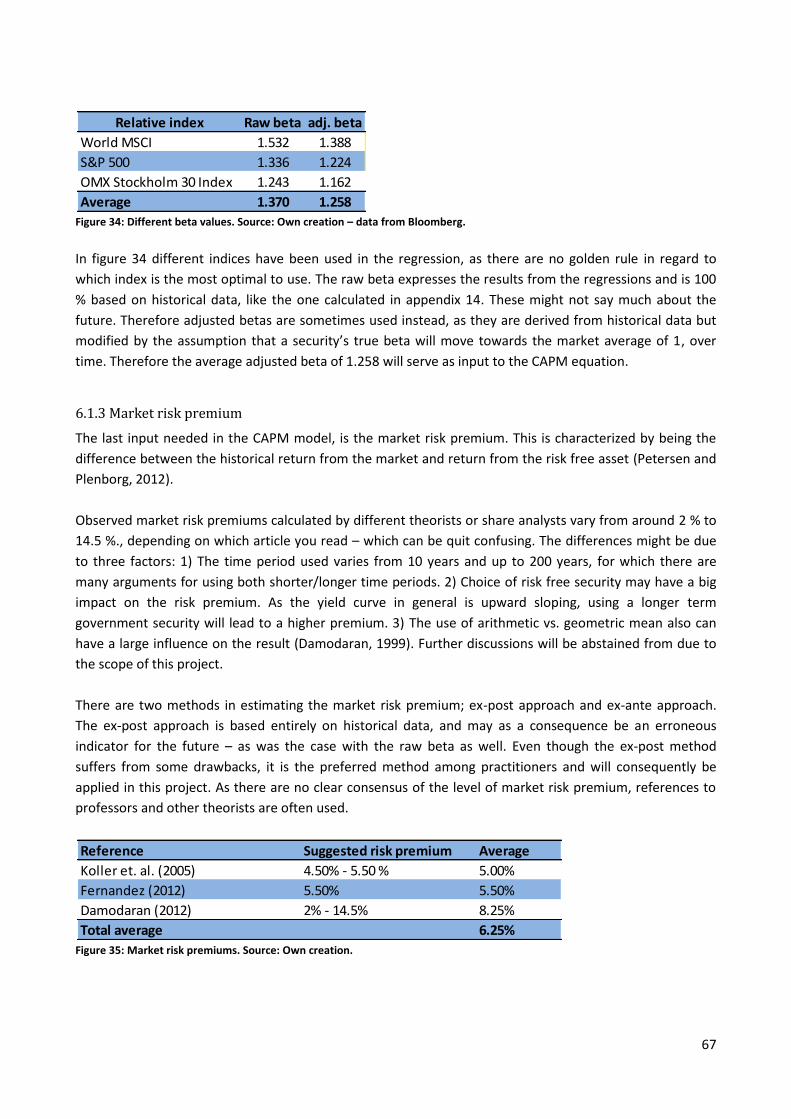

6.1.3 Market risk premium ............................................................................................................... 67

6.1.4 Calculating required rate of return on equity .......................................................................... 68

6.2 Cost of debt ..................................................................................................................................... 68

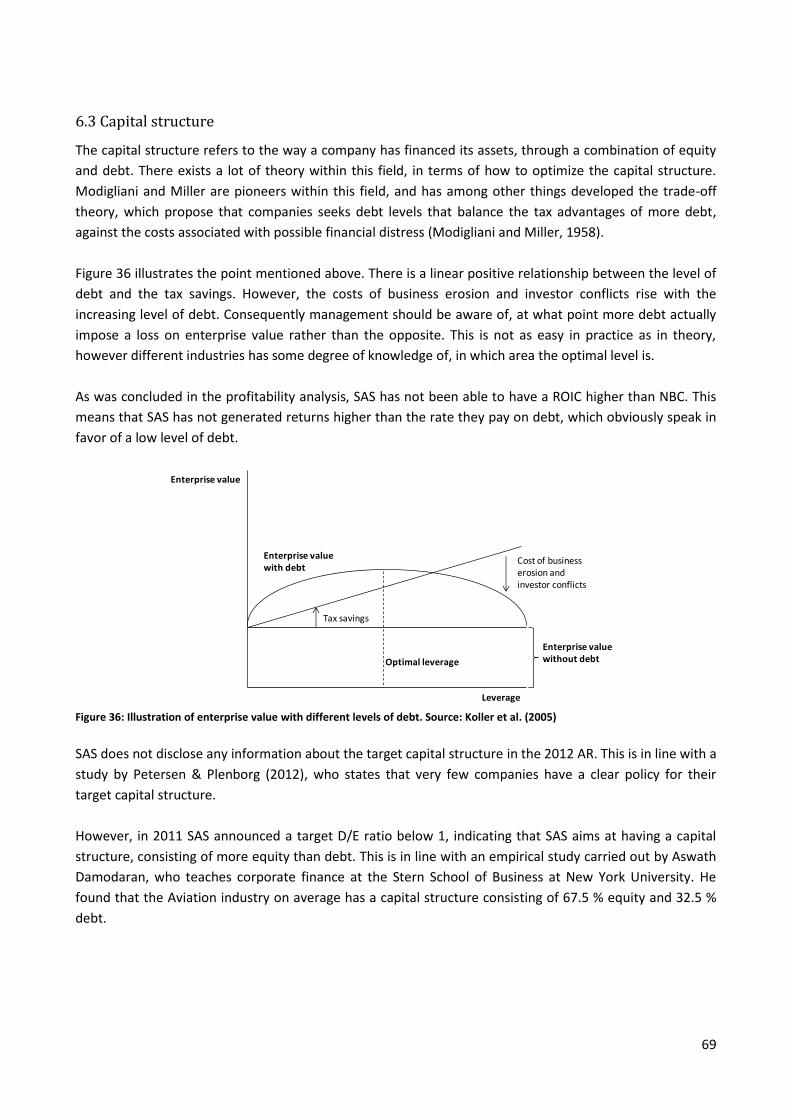

6.3 Capital structure .............................................................................................................................. 69

6.4 Weighted Average Cost of Capital (WACC) ..................................................................................... 70

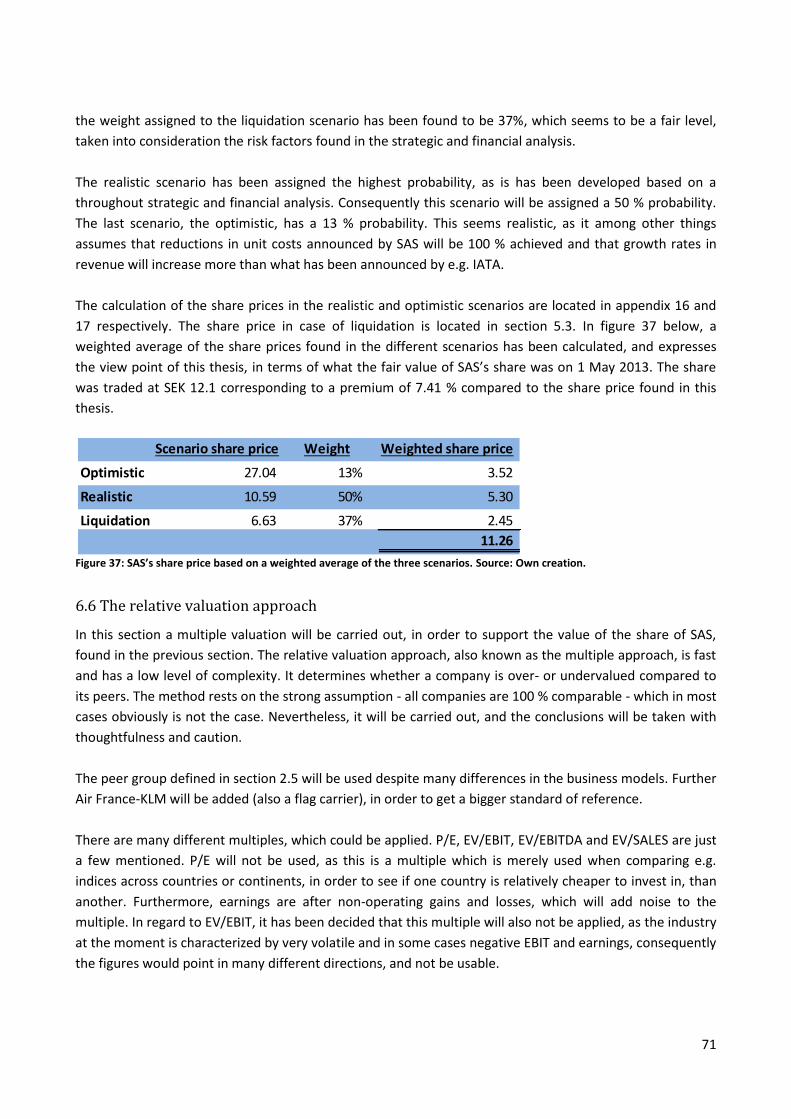

6.5 Valuation ......................................................................................................................................... 70

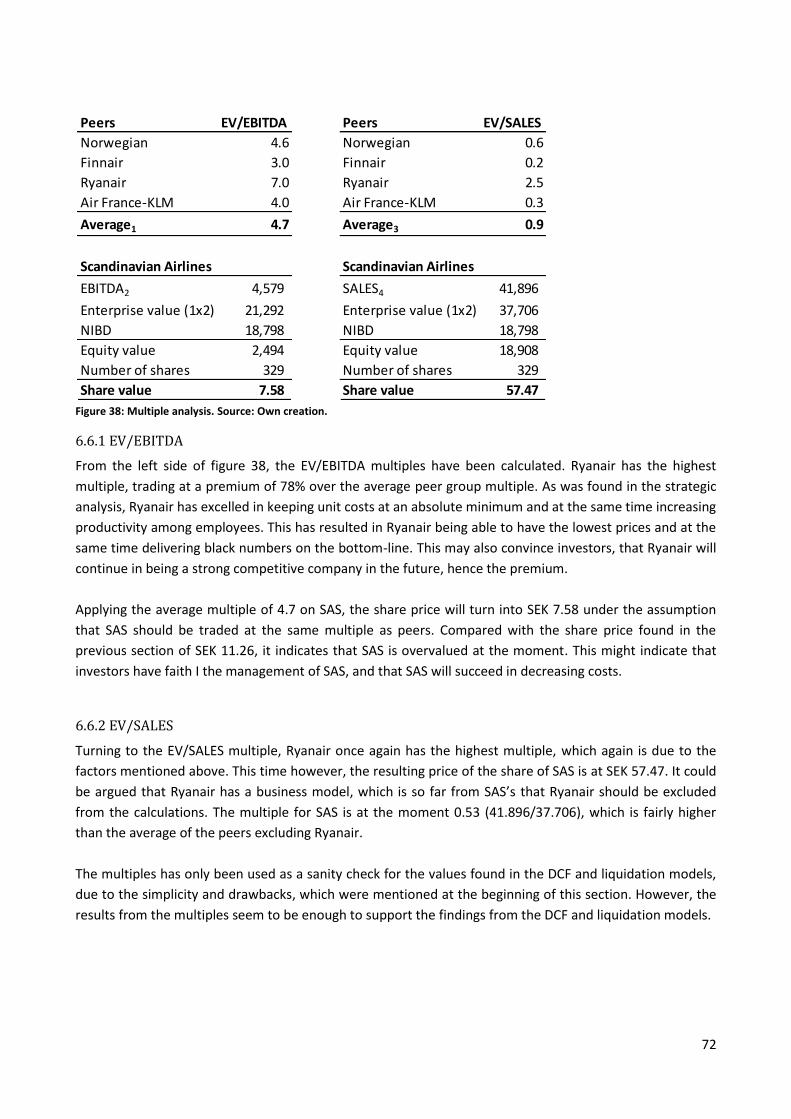

6.6 The relative valuation approach ..................................................................................................... 71

6

6.6.1 EV/EBITDA ................................................................................................................................ 72

6.6.2 EV/SALES .................................................................................................................................. 72

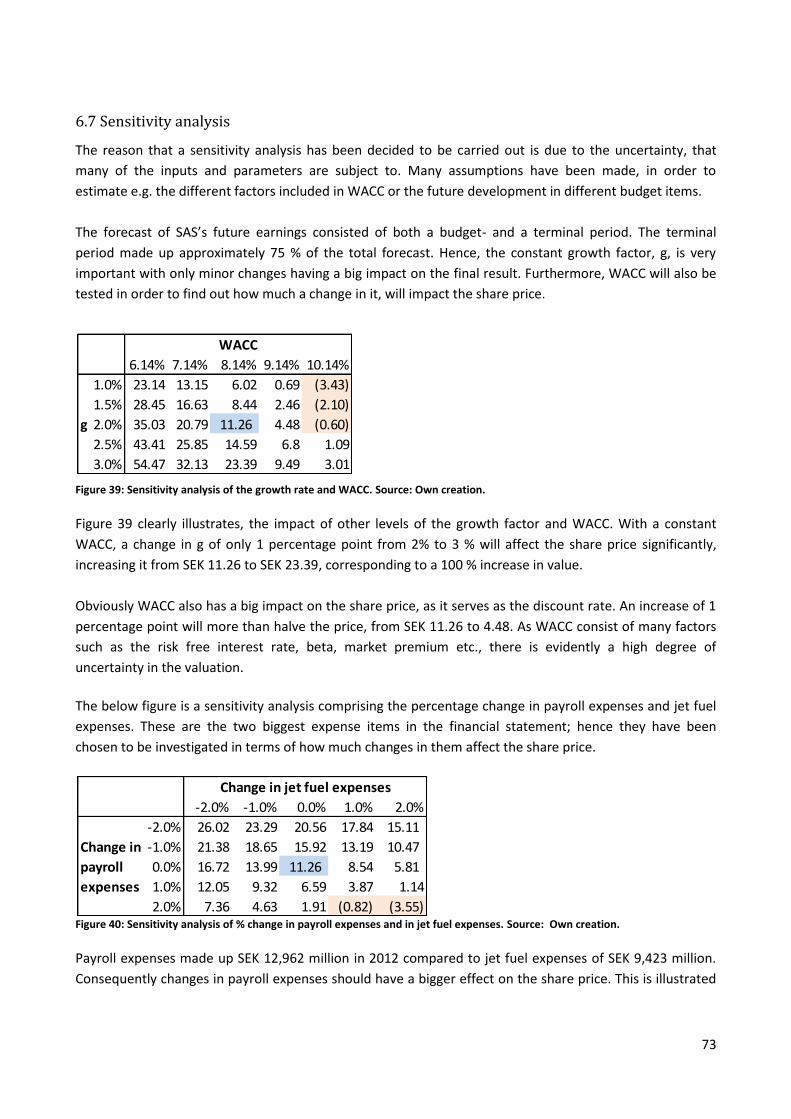

6.7 Sensitivity analysis .......................................................................................................................... 73

Part 7: Conclusion ..................................................................................................................................... 75

7.1 Conclusion ....................................................................................................................................... 75

7.2 The future of SAS ............................................................................................................................ 76

Bibliography .............................................................................................................................................. 77

Appendix ................................................................................................................................................... 81

7

Part 1: Introduction

1.1 Motivation

Scandinavian Airlines (SAS) has in many years been a very respected and prestigious company. Prior to the

beginning of the 1990s, where EU initiated their deregulation of the aviation industry, SAS benefited from

the monopolistic conditions in Scandinavia, where they had monopoly on different very profitable routes,

which meant poor competition and consequently higher prices and no focus on the cost side (Horn &

Willumsen, 2006)

The growing competition in the industry with low cost carriers (LCC), such as Norwegian, entering the

market, let SAS to losses of market shares and forced SAS into implementing different cost savings

programs such as Turnaround 2005, Profit 08, Strategy 2011, 4Excellence and the latest 4Excellence New

Generation (4XNG), which all have had the purpose of restructuring SAS into being less cost-intensive and

to focus on key competencies, which means divesting areas that is not considered as so. 4XNG is expected

to have an impact of SEK 5.2 billion of which SEK 2.6 million is expected to come from divesting SAS Ground

Handling and the aviation company Widerøe (Annual Report (AR) 2012, p. 9).

On top of this the financial crisis, which stroke Europe in 2008, has impacted the business traveler segment

- a key segment to SAS - and consequently affected SAS negatively. As SAS has a reputation of very high

fixed costs in terms of e.g. payroll expenses, the crisis hit SAS very hard relatively to its peers. This is one of

the reasons that SAS was very aggressive in their collective bargaining in November 2012, where SAS got

through with savings on wages and salaries equal to one monthly salary per year for pilots and half a month

per year for the cabin crew. Despite this, SAS still suffers from very high unit costs compared to its peers.

The financial markets have also reacted to SAS’s financial problems. In February 2012 Standard & Poor’s

(S&P), downgraded SAS from B- to CCC+, which both are “non-investment” grades, meaning that investing

in SAS is regarded as a speculative investment (AR 2012, p. 27).

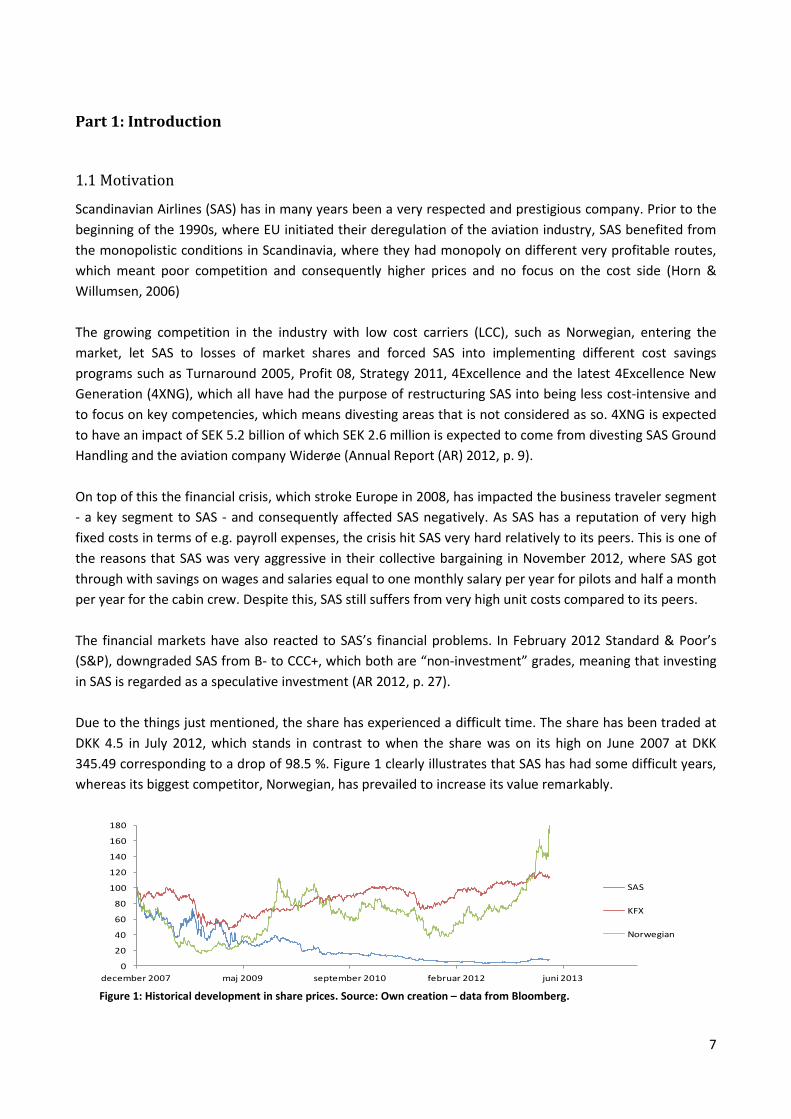

Due to the things just mentioned, the share has experienced a difficult time. The share has been traded at

DKK 4.5 in July 2012, which stands in contrast to when the share was on its high on June 2007 at DKK

345.49 corresponding to a drop of 98.5 %. Figure 1 clearly illustrates that SAS has had some difficult years,

whereas its biggest competitor, Norwegian, has prevailed to increase its value remarkably.

Figure 1: Historical development in share prices. Source: Own creation – data from Bloomberg.

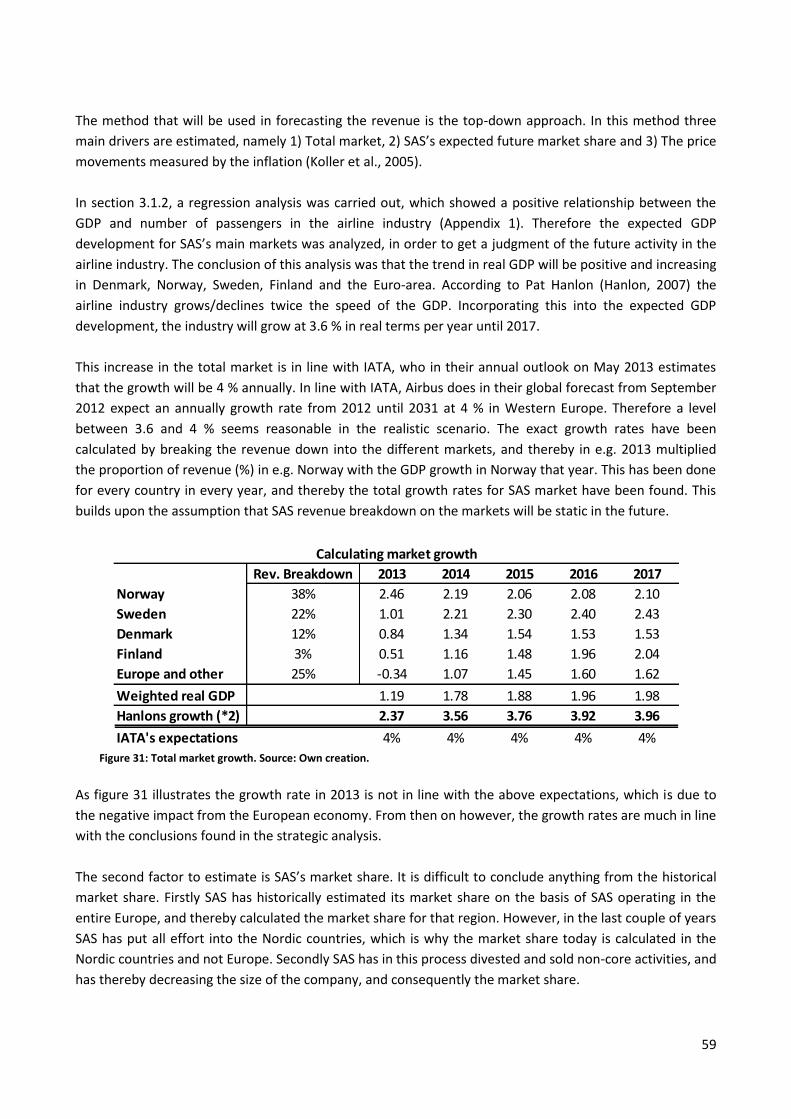

0

20

40

60

80

100

120

140

160

180

december 2007 maj 2009 september 2010 februar 2012 juni 2013

SAS

KFX

Norwegian

8

Based on the critical situation SAS finds itself in, it isinteresting to look at how SAS will perform in the

future. Will the cost saving programs, which have been characterizing SAS in the last couple of years, be

enough to ensure black numbers on the bottom line and thereby make sure that SAS will continue as a

going concern? Or will SAS be forced to enter into a liquidation process?

1.2 Problem statement

The main objective of this thesis is to give an investor a better basis for decision making in regard to

whether he should be buying or selling shares in SAS. As stated in section 1.1, SAS has been challenged

financially due to excessively high unit costs and by the increasing competition from LCC’s. Therefore this

project will focus on answering the following main question:

1. With the current crisis in SAS, what methods and models will be suitable in order to carry out a valuation

– both if considered as a going concern and if liquidated - and what factors should be taken into account

when conducting the valuation?

In order to answer the above mentioned question, SAS will be investigated and analyzed based on different

methods and models. In this process towards the valuation the following secondary questions will be

answered:

1. What is SAS’s strategy, and what is the estimated impact on the performance?

2. How is SAS’s position compared to its peers?

3. What market and industry factors affect SAS’s important value and cost drivers?

4. What has the level and trend in key financial value and cost drivers been historically?

5. What is a realistic budget for SAS?

6. What is an appropriate risk profile for SAS and the corresponding WACC?

7. Should SAS be trading at a premium or discount relatively to its peers?

8. What is the estimated value of SAS applying different models such as DCF, liquidation model and

multiples?

1.3 Methodology

1.3.1 Delimitation

In this thesis it is assumed that the reader has a general economic understanding and consequently has a

basic knowledge of the different theories and models within valuation, accordingly there will not be carried

out a separate presentation of theories and models. However there will be a discussion of the main

theories and models applied in this report, as the ones applied are not indisputable albeit applied by the

majority of the M&A and share analysts.

The thesis will exclude the possibility of trying to get hands on primary data, e.g. by directly contacting the

company. Consequently only secondary public available information will be applied in pursuing a fair value

of the company. This has been decided, as investors normally do not have the possibility of contacting the

9

management of the company they consider to invest in, and thereby only uses information available in the

markets as basis for their investment decisions.

In terms of analyzing the performance of SAS historically, it is estimated that going back five years is

sufficient, as this is the consensus among analysts. This means that the historic performance by SAS, which

will also be part of the basis for the budget, will be analyzed back from 2008 and up until today.

The period of the budget period will be limited to five years, meaning going to and including 2017 from

which the terminal period will be growing with a constant growth rate. The reason that there will not be

budgeted further than five years, is due to the risk associated with it, in terms of unpredictability of the

factors that influence the earnings in SAS.

The cut-off date for including new information and consequently the date of valuation will be set at 1 May

2013.

1.3.2 Research approach and quality evaluation

The research approach will take its starting point in the deductive approach, meaning that well-known

theories and models will be applied on the collected empirical data. This is in contrast to the inductive

method, which starts by collecting empirical knowledge and then from that deduces new theories and

models.

The data used in the project will be qualitative as well as quantitative data. The data will be coming from

annual reports, press releases, newspapers etc. but also from financial data providers such as Bloomberg,

which provides lots of reliable and valid up-to-date financial data. Furthermore organizations such as

International Air Transportation Association (IATA), which provides publications on market developments

and outlooks such as traffic forecasts, will be consulted during the writing of this project.

It is, of course, very important to check the sources, reliability and validity of the empirical data in order not

to get any wrong data but also to leave out subjectivity from the date being used. When conducting a

valuation, as with any other types of projects, it is important to be aware that different stakeholders have

different agendas. SAS do, ceteris paribus, have an interest in presenting the company as being as healthy

and strong as possible, and will of course do that within the legal boundaries. Therefore it is the author of

this project’s job to go beyond these potential “beautifications” and create the most realistic picture of the

company as possible.

1.3.3 Structure of project

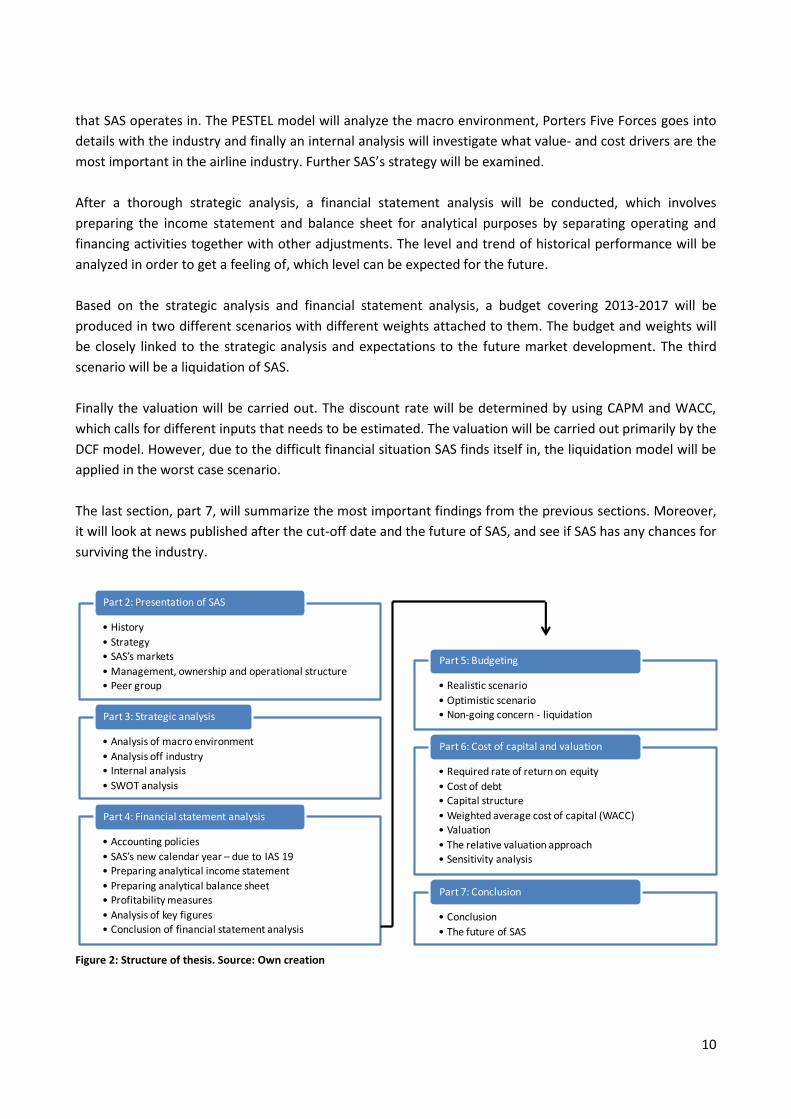

The thesis takes its form as a classical fundamental analysis, hence a strategic analysis together with a

financial statement analysis constitute the inputs to the budget and valuation models.

Figure 2 gives an overview of how the valuation will be approached. After the introduction and

presentation of SAS, it starts out by conducting a strategic analysis, which will be analyzing the environment

10

that SAS operates in. The PESTEL model will analyze the macro environment, Porters Five Forces goes into

details with the industry and finally an internal analysis will investigate what value- and cost drivers are the

most important in the airline industry. Further SAS’s strategy will be examined.

After a thorough strategic analysis, a financial statement analysis will be conducted, which involves

preparing the income statement and balance sheet for analytical purposes by separating operating and

financing activities together with other adjustments. The level and trend of historical performance will be

analyzed in order to get a feeling of, which level can be expected for the future.

Based on the strategic analysis and financial statement analysis, a budget covering 2013-2017 will be

produced in two different scenarios with different weights attached to them. The budget and weights will

be closely linked to the strategic analysis and expectations to the future market development. The third

scenario will be a liquidation of SAS.

Finally the valuation will be carried out. The discount rate will be determined by using CAPM and WACC,

which calls for different inputs that needs to be estimated. The valuation will be carried out primarily by the

DCF model. However, due to the difficult financial situation SAS finds itself in, the liquidation model will be

applied in the worst case scenario.

The last section, part 7, will summarize the most important findings from the previous sections. Moreover,

it will look at news published after the cut-off date and the future of SAS, and see if SAS has any chances for

surviving the industry.

Figure 2: Structure of thesis. Source: Own creation

• History

• Strategy

• SAS’s markets

• Management, ownership and operational structure• Peer group

Part 2: Presentation of SAS

• Analysis of macro environment

• Analysis off industry

• Internal analysis

• SWOT analysis

Part 3: Strategic analysis

• Accounting policies

• SAS’s new calendar year – due to IAS 19• Preparing analytical income statement

• Preparing analytical balance sheet• Profitability measures

• Analysis of key figures• Conclusion of financial statement analysis

Part 4: Financial statement analysis

• Realistic scenario

• Optimistic scenario• Non-going concern - liquidation

Part 5: Budgeting

• Required rate of return on equity

• Cost of debt• Capital structure

• Weighted average cost of capital (WACC)

• Valuation

• The relative valuation approach• Sensitivity analysis

Part 6: Cost of capital and valuation

• Conclusion

• The future of SAS

Part 7: Conclusion

11

1.3.4 Discussion of main theories

In the following section the most important theories applied in the thesis will be discussed. The chosen

theories are the best available and the most popular among share analysts and other professionals

conducting valuations. Although they are the most popular theories and models, they are not perfect. It is

therefore very important to be aware of the drawbacks of the theories, as it could have a big impact if the

theories are not applied properly or the drawbacks are not being taken into account.

Even though the method and assumptions underlying the Capital Asset Pricing Model (CAPM) have been

criticized by many theorists, it is still a very powerful tool for people within the financial industry to

calculate required rates of return by investors. The reason that it is so popular despite the drawbacks

pointed out, is that is simple and easy to apply, and generates a relationship between required rate and

specific risk.

Some of the drawbacks of the model are due to the strong assumptions it relies on, of which the most

important are:

1. Investors can borrow and lend at the risk free rate

2. Investors hold diversified portfolios, i.e. no unsystematic risk

3. Investors have homogeneous expectations, i.e. they estimate identical probability distribution for

the future rates of return

4. All investors have same one-period time horizons

5. There are no taxes or transaction costs

6. There is no inflation or change in interest rates

7. Capital markets are in equilibrium, i.e. they are properly priced

It is obvious that the above assumptions are questionable. In regard to the first assumption, it is reasonable

to assume that investors can lend at the risk free rate, however it is questionable whether investors can

borrow at the risk free rate. Obviously as noted by Brennan (1969), the borrowing portfolios are not as

profitable when it is not possible to borrow at the risk free, as assumed by the CAPM, which is one reason

why the results by CAPM can be faulty.

As the CAPM only takes systematic risk, measured by the beta coefficient (β), into account it indirectly

assumes that investors hold diversified portfolios, which in many cases are not the case. However, the

development of the financial markets and new products such as Exchange Traded Funds (ETF) has made it

easier for small investors to more closely “track” the stock markets.

Obviously the capital markets are not perfect as transaction costs, taxes etc. exists, and therefore the rest

of the assumptions likewise seem to be too strong to image the real world, which as noted earlier is the

reason for the criticism raised against the CAPM.

Fama & French (1992) came up with an alternative to the traditional CAPM. In their study they found that

the average stock returns were not positively related to the market betas, which is what CAPM state. Fame

& French concluded that equity returns were inversely related to the size of the company and positively

related to the company’s book value to its market value of equity. Even though it seems more accurate as it

incorporates more factors, it has never really grown as popular as the CAPM, which is still the most popular

and used model among financial professionals (Levy, Giorgi & Hens, 2011).

12

Determining the discount rate not only involves the CAPM – it only determines the required rate of return.

After having found the required rate of return, the Weighted Average Cost of Capital (WACC) needs to be

determined, which is the return that providers of the company´s capital require. WACC can be used as a

hurdle rate for investment decisions but also act as a measure to be minimized, in order to find the optimal

capital structure for the company.

WACC has been criticized for being too static in regard to the capital structure of the target firm. The

reason for that is, that firms in their start-up phase do have a lot of debt and as the firm gets more mature

and profitable it does in most cases gradually replace some of the debt with equity. Due to this, the WACC

can potentially result in erroneous values. Further, as firm value is very sensitive to the level of WACC, it is

of course important to bear in mind that one of the inputs into the model comes from the CAPM, which

also has drawbacks as already mentioned above.

There exist many valuation methods in the world of finance. Overall there are two main methods: Cash

flow based or accrual based methods. Koller et al. (2005) argued in favor of the cash flow based method as

it is unaffected by the accounting methods applied. On the other hand Penman & Sougiannis (1998)

concluded in their research that the residual income method (RI), which is an accrual based valuation

method, is more precise than the discounted cash flow model (DCF), which is based on a company’s cash

flows. However, as both methods are based on the dividend discount model (DDM) introduced by Milller &

Modigliani (1961), they should both yield the same value if applied properly.

The main valuation method applied in this thesis will be the DCF model. Therefore it is important to be

attentive of its drawbacks. The biggest problem with the DCF model is that is does not match cash inflows

with cash outflows. In the example of SAS, attention should therefore be drawn towards big investments in

some periods (cash outflows) and significant cash inflows in the following periods. The cash flow can also

be manipulated by the company, by for example taking out a big loan, which will increase the cash flows.

The above have only concerned theories within the valuation section of this thesis. The reason they have

been subject to discussion, is that they are all based on math, equations and a lot of assumptions. This gives

rise to a lot of criticism and theorists testing them by conducting different studies, in order to improve or

finding new methods.

Other theories applied such as the PESTEL, Porters Five Forces, Porters Value Chain etc. will not be

discussed in details in this section. The reason for this is, that the author does not regard them as theories

as such, but merely guidelines of which factors that might be relevant to consider, when analyzing things

such as the industry or the macro environment. They will of course still be critically applied in the analysis

of SAS.

13

Part 2: Presentation of SAS

In part 2 a brief presentation of SAS will be carried out. In order to give a potential investor an introduction

to SAS, the section will include SAS’s history, as this is needed to understand the ownership structure and

the way that SAS has developed. SAS’s strategy is another important aspect to know about. The different

strategies from 2002 up until today will be presented, as they give a good picture of the direction that SAS

has been trying to follow, and where SAS wants to be in the future in terms of markets, financials etc.

The markets that SAS is operating in will be mentioned, and the last section of part 2 will deal with the

SAS’s peer group, as they are very important to know off when conducting benchmarks.

2.1 History

The history of SAS dates back to 1946 as Det Danske Luftfartsselskab (DDL), Det Norske Luftfartsselskab

(DNL) and Svensk Interkontinental Lufttrafik AB (SILA) merged, and created what would be known as SAS.

From the 1960’s – 1980’s SAS grew and expanded into new business areas. In 1960 SAS opened its first

hotel – SAS Royal Hotel Copenhagen and did from then on open hotels in many other countries, the first

one in 1980 in Kuwait named SAS Kuwait Hotel. In 1982 and 1984 SAS won prices for the “most precise

aviation company” and for “Airline of the year” respectively. In 1986 Spanair was founded as a joint venture

between SAS and Viajes Marsans, Consequently SAS expanded into new markets. In 1981 Jan Carlzon

became the CEO of SAS, and held that position for 12 consecutive years. He introduced the strategy “The

Businessman’s Airline” which focused on the businessmen, who was characterized by willing to pay a

higher price and thereby increasing the profit per flight seat. Further it was under management of Jan

Carlzon that the payroll expenses really took off, which gave him the nickname “the world’s best Carlzon”

and “the world’s most expensive Carlson”. Carlzon focused on customers and employee satisfaction which

meant increasing payroll, pension and other operating costs. However, as SAS operated in a monopoly the

solution was to raise prices (Ussing 6 April 2013). This was laying the ground for the SAS we have known for

many years, characterized by a high service level and a continuing battle with high fixed costs.

From 1992 and onwards SAS entered a more turbulent period in its history. The period was characterized

by SAS entering into new markets by acquiring competitors such as Air Botnia (1998) and Widerøe (1999).

However, other areas of the business were divested, such as the majority holding in Intercontinental Hotels

Group in 1992. Jen Reinås who took seat as CEO in 1993 got the task to build a leaner SAS and focus more

on the key activity – aviation. However, as Jan Stenberg became CEO in 1994, he forgot all about cost

savings and focused instead on Total Quality Management. Under management of Stenberg 1,600 people

were hired in 1996 and 1450 more in 1997, which meant a more cost-intensive SAS (Horn & Willumsen,

2006).

Shifting management and cost-cutting plans continued into the new millennium, and culminated in 2001

where theorists attached the World Trade Centers, which affected the aviation industry worldwide. From

then on SAS had to do something drastic in order to survive. The next section will touch upon the strategies

that SAS has been implementing the last decade.

14

2.2 Strategy

As mentioned in section 2.1, SAS needed to do something after the 9/11 attack in order to stay

competitive, as demand had gone down and competition from LCC such ad Norwegian really had increased,

especially after the initial public offering (IPO) of Norwegian in 2003.

In 2002 SAS initiated the “Turnaround 2005” program which aimed at improving the competitiveness and

profitability. The program was rather ambitious and was designed to make cost reductions of SEK 14 billion

within 2005. In 2005 the program was fully implemented and structural cost reductions ended at SEK 14.2

billion, corresponding to unit cost reductions of 30 %, adjusted for currency and fuel effects, and with

reductions in staff of approximately 5,500 full time employees (AR 2005, p. 6).

In 2006 SAS kicked off a new strategic plan, “Strategy 2011”. The new strategy had a clear focus on

customers and employees, and aimed at being better at focusing on the key competence, namely aviation.

The overall aim was to ensure that SAS could ensure a passenger growth of 20 % in 2011.

In 2008 Strategy 2011 had saved costs of SEK 4 billion. However, due to the changed market conditions

primarily caused by the financial crisis, the strategy was not enough. Therefore a new strategy, “Core SAS”,

was launched in 2009. SAS management wanted a more simple structure, meaning that companies that

were outside of the Nordic home market, which was not considered as part of SAS’s core business, would

be divested or outsourced. Core SAS was fully implemented in 2011 with total cost reductions of SEK 7.6

billion and reduction in unit costs of 23 % compared to 2008 (AR 2011 p. 7).

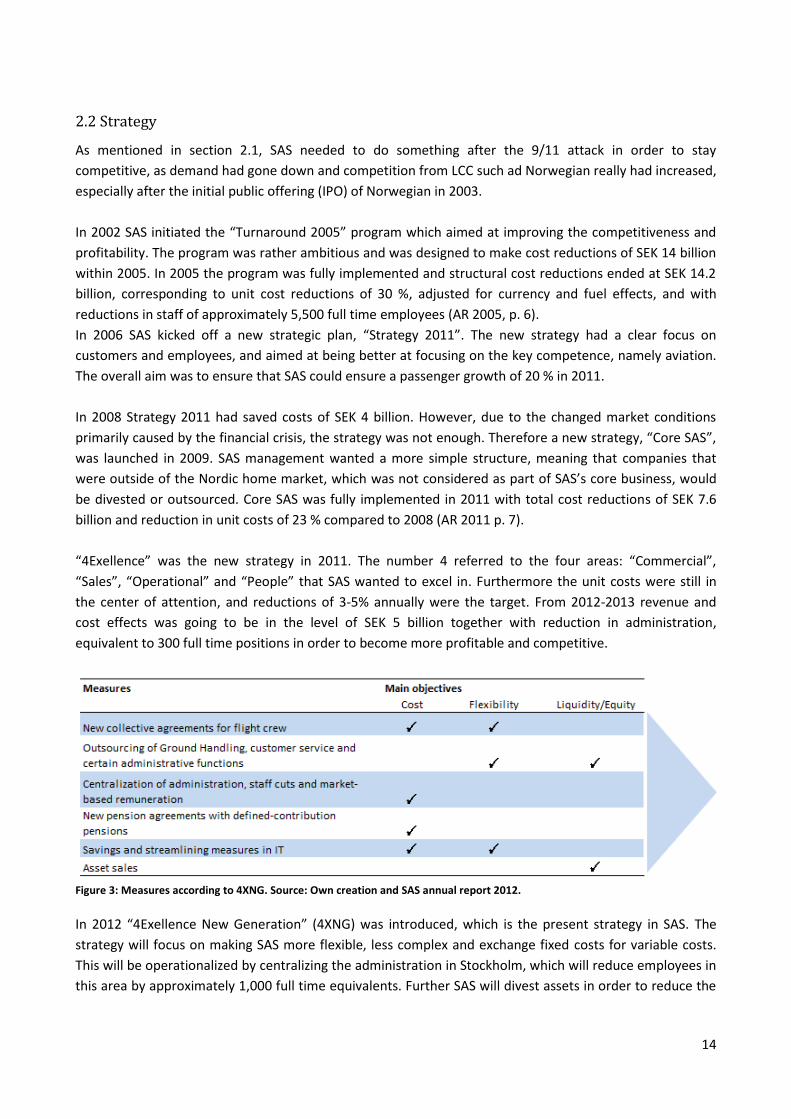

“4Exellence” was the new strategy in 2011. The number 4 referred to the four areas: “Commercial”,

“Sales”, “Operational” and “People” that SAS wanted to excel in. Furthermore the unit costs were still in

the center of attention, and reductions of 3-5% annually were the target. From 2012-2013 revenue and

cost effects was going to be in the level of SEK 5 billion together with reduction in administration,

equivalent to 300 full time positions in order to become more profitable and competitive.

Figure 3: Measures according to 4XNG. Source: Own creation and SAS annual report 2012.

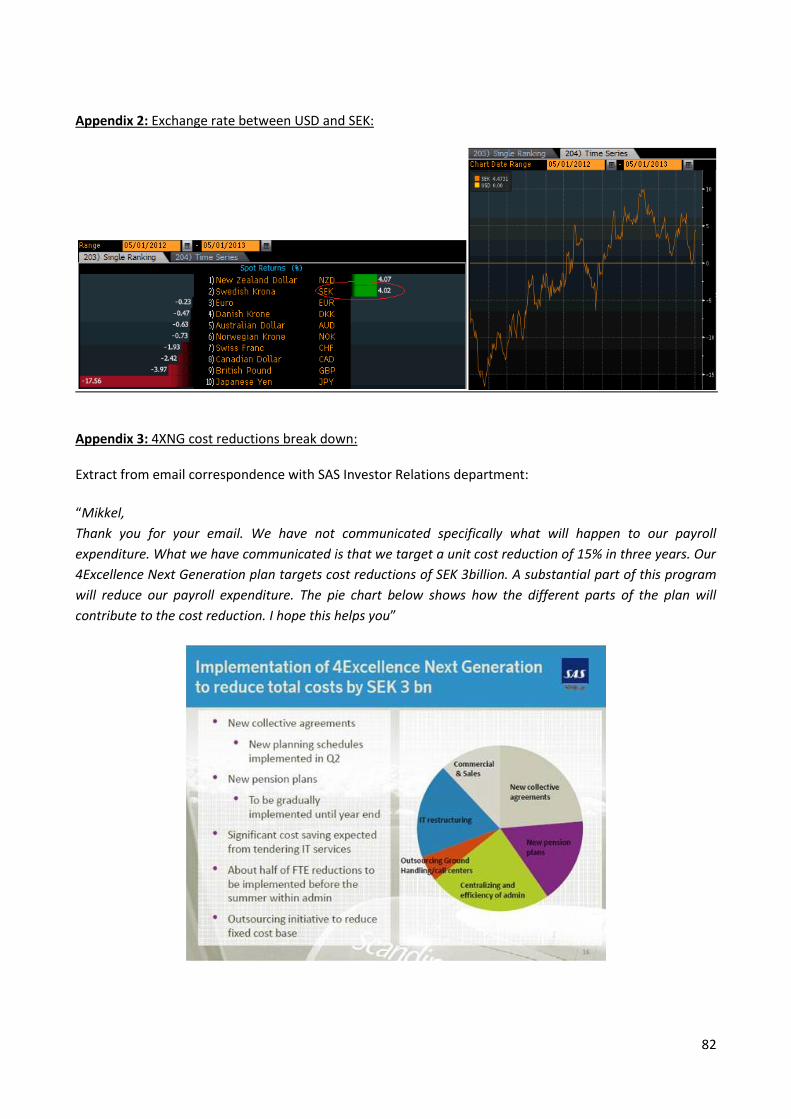

In 2012 “4Exellence New Generation” (4XNG) was introduced, which is the present strategy in SAS. The

strategy will focus on making SAS more flexible, less complex and exchange fixed costs for variable costs.

This will be operationalized by centralizing the administration in Stockholm, which will reduce employees in

this area by approximately 1,000 full time equivalents. Further SAS will divest assets in order to reduce the

15

dependence on external funding. Potential divestments include Widerøe, Airport-related real estate,

Ground handling and Aircraft engines as illustrated in figure 3. The overall aim is to secure cost reductions

of SEK 3 billion in 2012 and 2013 and to divest assets with an effect on liquidity of around SEK 3 billion (AR

2012 p. 5-12).

According to the Q1 12/13 interim report, SAS outsourced the Ground Handling operations to Swissport.

Furthermore the centralization of administration is progressing and staff has been reduced by 30 %. Finally

the call center has been outsourced to a third-party and a sale and leaseback agreement has been signed

regarding reserve engines, which correspond to a liquidity effect of SEK 700 million during the second

quarter. This is all in line with the strategy and SAS is about to become a more streamlined profitable

company with the main focus on its core competency, aviation.

In conjunction with the introduction of 4XNG, SAS has also set new financial targets. The most important

one is the profitability in terms of the EBIT margin. SAS aims at improving the EBIT margin, so that a level of

8 % will be set as target. SAS believe that it is realistic to reach the target EBIT margin in 2014/2015.

2.3 SAS’s markets

SAS’s main market has always been in the Nordic Countries, which consists of Norway, Sweden, Finland and

Denmark. During the history SAS has bought and expanded to new routes and markets. However, Core SAS

had, as one of the objectives, to focus the attention on the home market – the Nordic Market. This is also

known as de-diversifying, which is usually a phenomenon in hard financial times, where a company has

difficulties in creating profit, and therefore start focusing on what they are best at. This is the case in SAS at

the moment cf. section 2.2.

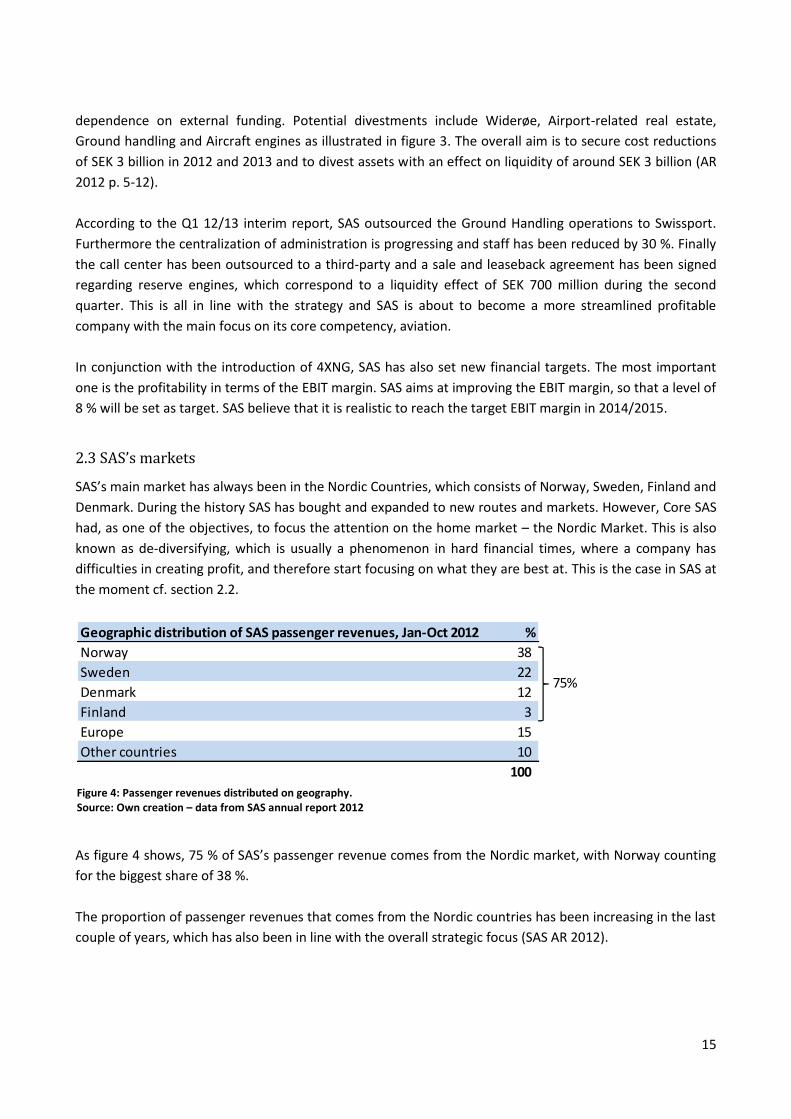

As figure 4 shows, 75 % of SAS’s passenger revenue comes from the Nordic market, with Norway counting

for the biggest share of 38 %.

The proportion of passenger revenues that comes from the Nordic countries has been increasing in the last

couple of years, which has also been in line with the overall strategic focus (SAS AR 2012).

Geographic distribution of SAS passenger revenues, Jan-Oct 2012 %

Norway 38

Sweden 22

Denmark 12

Finland 3

Europe 15

Other countries 10

100

75%

Figure 4: Passenger revenues distributed on geography. Source: Own creation – data from SAS annual report 2012

16

0 5 10 15 20 25 30

SAS group

Norwegian

Ryanair

Finnair

AirFrance/KLM

Widerøe

British Airways

AirBerlin

Easyjet

%

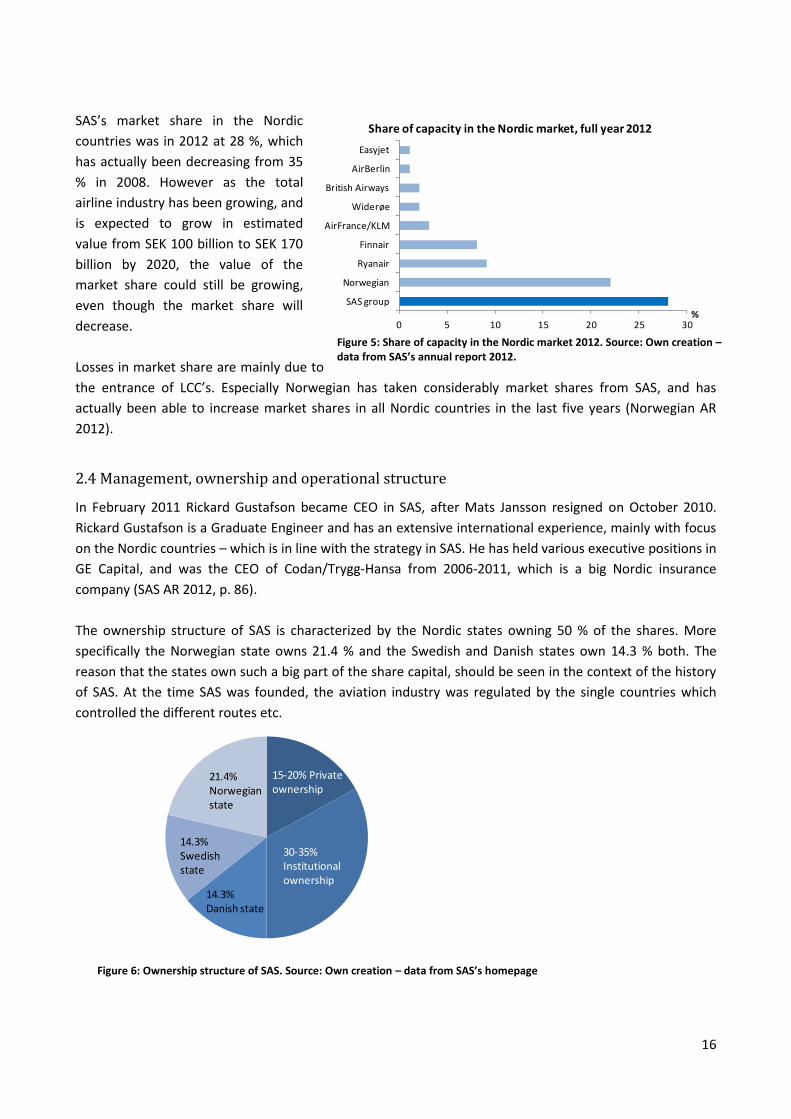

Share of capacity in the Nordic market, full year 2012SAS’s market share in the Nordic

countries was in 2012 at 28 %, which

has actually been decreasing from 35

% in 2008. However as the total

airline industry has been growing, and

is expected to grow in estimated

value from SEK 100 billion to SEK 170

billion by 2020, the value of the

market share could still be growing,

even though the market share will

decrease.

Losses in market share are mainly due to

the entrance of LCC’s. Especially Norwegian has taken considerably market shares from SAS, and has

actually been able to increase market shares in all Nordic countries in the last five years (Norwegian AR

2012).

2.4 Management, ownership and operational structure

In February 2011 Rickard Gustafson became CEO in SAS, after Mats Jansson resigned on October 2010.

Rickard Gustafson is a Graduate Engineer and has an extensive international experience, mainly with focus

on the Nordic countries – which is in line with the strategy in SAS. He has held various executive positions in

GE Capital, and was the CEO of Codan/Trygg-Hansa from 2006-2011, which is a big Nordic insurance

company (SAS AR 2012, p. 86).

The ownership structure of SAS is characterized by the Nordic states owning 50 % of the shares. More

specifically the Norwegian state owns 21.4 % and the Swedish and Danish states own 14.3 % both. The

reason that the states own such a big part of the share capital, should be seen in the context of the history

of SAS. At the time SAS was founded, the aviation industry was regulated by the single countries which

controlled the different routes etc.

30-35% Institutional ownership

15-20% Private ownership

21.4%Norwegian state

14.3%Danish state

14.3%Swedish state

Figure 5: Share of capacity in the Nordic market 2012. Source: Own creation – data from SAS’s annual report 2012.

Figure 6: Ownership structure of SAS. Source: Own creation – data from SAS’s homepage

17

It has often been debated whether the states should give up their ownership stakes in SAS. Proponents of

SAS being a 100 % privately held company argues, that one of the reasons that SAS has got into financial

troubles is, that SAS has been focusing more on keeping and creating jobs, disregarding the profitability,

than on creating a healthy and profitable company, where non-profitable units are divested or excess

workers are laid off.

SAS group consists today only of two companies: Scandinavian Airlines and Widerøe. During 2012 Blue 1, a

Finnish airline company, owned by SAS group, which up until 2012 was an independent unit under SAS

group, was integrated into Scandinavian Airlines’ operations. The majority of Blue 1’s European routes were

closed, in order to secure a more streamlined SAS - in line with 4XNG.

Scandinavian Airlines, which stands for 91 % of the revenue (2012), is the biggest airline company in the

Nordic region with 156 aircrafts in service carrying more than 21 million passengers in 2012. SAS was

recently given the title as the “world’s third most punctual airline” in 2012 by the independent American

flight statistics and analysis source “Flightstats”. The punctuality was according to Flightstats at 87.91 %,

meaning that all flights landed on time in 2012. SAS was also named Europe’s most punctual airline

company from 2009 to 2011 also by Flightstats.

Widerøe is a subsidiary based in Norway. Widerøe operates both domestically and international with 39

operating aircrafts carrying 2.3 million passengers in 2012. Widerøe’s revenue, in percentage of the total

revenue in SAS group, was 9 % in 2012.

2.5 Peer group

This section serves the purpose of presenting a relevant peer group than can act as a benchmark in the

strategic and financial analysis of SAS. In an ideal world the peer group should consist of companies that are

comparable to SAS in all areas of the business, which of course is not possible, as some might pursue the

strategy as LCC and another as HCC. Further, there may be differences in strategies, internal processes,

capital structures etc. which undoubtedly will make noise when comparing the companies.

As figure 5 illustrated, SAS’s biggest peers in the Nordic countries are Norwegian, Ryanair and Finnair, as

they have the biggest market shares after SAS. Consequently these have been chosen as peer group in the

remainder part of this project. In addition, SAS have made it clear, that the Nordic market will be the focus

area for SAS in the future, which is why companies operating outside the Nordic countries have not been

considered as useful peers.

2.5.1 Norwegian Air Shuttle

Norwegian is a LCC based in Oslo, Norway. It has 75 aircrafts and operates 382 routes to 121 destinations in

Europe, North Africa, Middle East, Thailand and USA. Norwegian’s strategy is to operate as a LCC, offering

discount tickets to passengers, which are both leisure and business travelers. The home market for

Norwegian is Europe, with much of the routes located in the Nordic countries.

18

In 2012 Norwegian had 2,705 full time employees (FTE) and the company transported almost 18 million

passengers. This is 25% less than SAS’s 24 million passengers, which is only from 1 January - 31 October,

due to changes in SAS’s financial year. However, Norwegian is growing aggressively at the moment, and has

between 2005 and 2012 had a compounded annual growth rate of 21% (Norwegian AR 2012).

Norwegian had revenues of NOK 12.8 billion in 2012 compared to 10.5 the year before, corresponding to a

revenue growth of 22%.

Norwegian is by far the biggest competitor in SAS’s home market at the moment, which can also be

concluded from the market shares between the two. In 2008 SAS’s market share in the Nordic countries

was 35% against Norwegians 11%. In 2012 these numbers were 28 % and 22 % respectively, as expressed in

figure 5.

2.5.2 Ryanair

As with Norwegian, Ryanair is a LCC. The main base is Stanstead Airport together with 57 other bases all

over the world. Ryanair operates 1,600 routes and has a fleet consisting of 305 aircrafts. Ryanair is an ultra

LCC compared to e.g. Norwegian, as the main objective is to offer the lowest ticket prices on the market.

This is done by use of surcharges, which by other companies are normally included in the price. In 2010

Ryanair considered to install pay toilets, in order to lower prices even further. However, this was never

realized, and was leaved undone in 2011.

9,127 FTE’s were employed in Ryanair in 2012, which is about 40 % less than the 15,000 in SAS. This is in

contrast to the 79 million transported passengers, which is almost three times the number of transported

passengers in SAS.

Ryanair managed to report revenue of EUR 4,884 million corresponding to SEK 41,6251 million. This was not

much better than SAS revenue in 2012, which reported revenue of SEK 35,986 from 1 January to 31

October. Ryanair’s market share was 9 % in the Nordic countries in 2012, up from 7 % in 2008 – indicating

that Ryanair is not as aggressive in this region as Norwegian in terms of growing the business.

2.5.3 Finnair

Finnair is the national carrier of Finland, and is majority owned by the Finnish government. The prime base

is Helsinki with 45 aircrafts flying to more than 70 destinations worldwide. Finnair’s strategy is to become

the number one airline in the Nordic countries. In contrast to Norwegian and Ryanair, Finnair is not a LCC,

but merely as SAS focused on providing good service during the flight.

Finnair had 6,368 FTE’s in December 2012 and transported 8.8 million passengers, which makes it the

smallest company in the peer group, measured by transported passengers, and almost three times less

than SAS.

1 Using the exchange rate of EUR 1 = SEK 8.52 which was the rate at the cut-off date 1 May 2012

19

The revenue in 2012 was EUR 2,449 million corresponding to SEK 20,865 million, which was approximately

half the size of SAS’s reported revenue.2 Finnair had a market share in the Nordic countries of 8 % in 2012

down from 11 % in 2008. As in the case with SAS, Finnair has lost market shares, mainly due to the

increasing competition from the LCC’s.

Finnair is probably the competitor reminding most of SAS, as it is also a flag carrier, and has its main

activities in the Nordic countries.

2 Applying the same exchange rate as in note 1.

20

Part 3: Strategic analysis

3.1. Analysis of the macro environment

In part 3 a strategic analysis containing political, economic, social and technological factors, which are of big

importance for the airline industry and more importantly SAS, will be examined. These are all external

factors which are very important to try to control, or at least to be aware of. Consequently they should be

assessed continuously in order to minimize the risks associated herewith. The analysis carried out in this

section, will serve as important inputs to the budgeting of future cash flows.

3.1.1 Political factors

The airline industry has in recent years been characterized by being gradually deregulated. In 1978 the

Airline Deregulation Act was approved, which deregulated the industry in USA. From 1993-1997 the

European Union deregulated the airline industry and phased in the open skies regime, which allowed all

transatlantic routes to be opened up to European and American airline companies. Furthermore, all

restrictions concerning which routes should be operated by whom and the corresponding prices were

removed, and replaced with open competition (Horn & Willumsen, 2006).

As mentioned in section 2.4, the Swedish, Norwegian and Danish states each own 50 % in total of the

shares outstanding in SAS, and consequently have the majority of the shares and thereby the ownership of

the company. This has caused a lot of debate in recent years, especially after the deregulation of the

industry, but in particular after the financial turmoil in SAS took off.

Being a state-owned company can have some unfortunate drawbacks, as the main focus might be on things

other than the profitability i.e. increasing shareholder value. With approximately 15,000 employees in SAS

and even more if suppliers and personal in the airports are included; the politicians obviously have an

interest in keeping SAS alive. Unprofitable units in SAS might have been held alive in order to secure as

many as possible employed, especially in light of the recession that e.g. EU finds itself in at the moment.

Another conflict might be the importance of a modern infrastructure, which is crucial for every western

knowledge-based society that focuses on productivity and increasing wealth. In particular in Norway the

airline industry is important, as other means of transport might not be an alternative. Thus politicians might

have an interest in keeping regional routes open to secure the infrastructure, which might not be

profitable. Keeping unprofitable routes artificially alive creates overcapacity which in the end puts a

downward pressure on the yield, not only for the company itself, but for the entire industry.

21

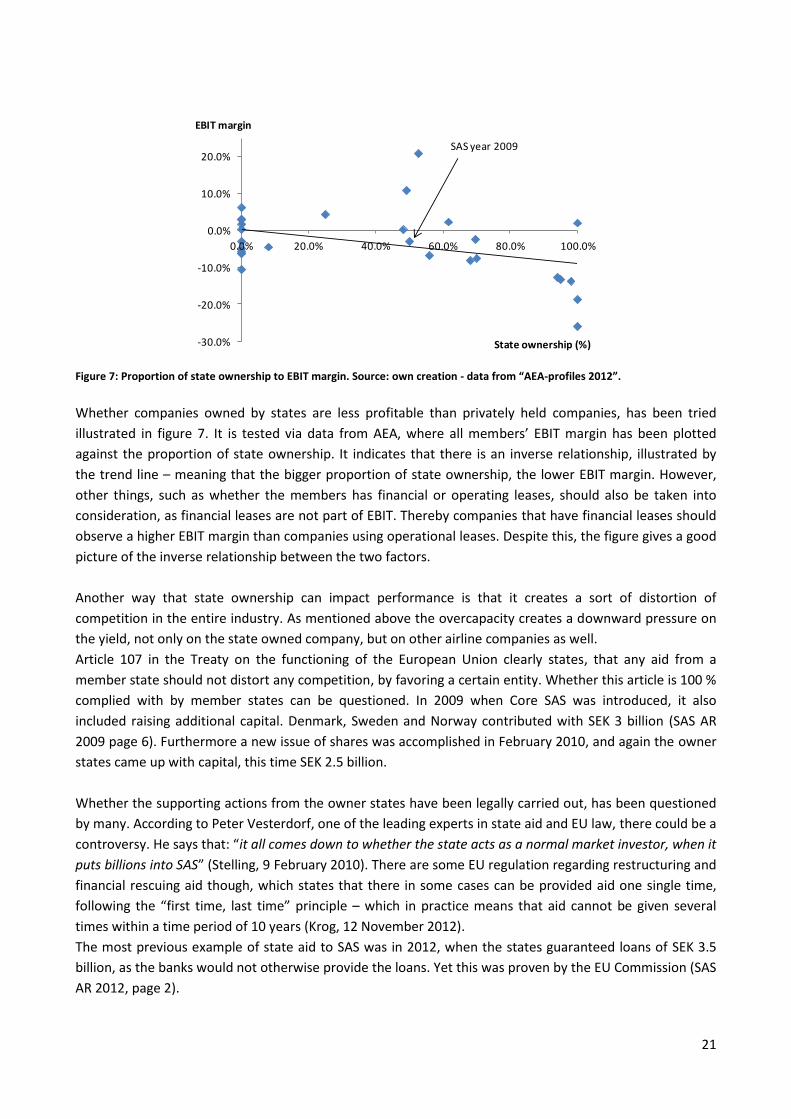

Figure 7: Proportion of state ownership to EBIT margin. Source: own creation - data from “AEA-profiles 2012”.

Whether companies owned by states are less profitable than privately held companies, has been tried

illustrated in figure 7. It is tested via data from AEA, where all members’ EBIT margin has been plotted

against the proportion of state ownership. It indicates that there is an inverse relationship, illustrated by

the trend line – meaning that the bigger proportion of state ownership, the lower EBIT margin. However,

other things, such as whether the members has financial or operating leases, should also be taken into

consideration, as financial leases are not part of EBIT. Thereby companies that have financial leases should

observe a higher EBIT margin than companies using operational leases. Despite this, the figure gives a good

picture of the inverse relationship between the two factors.

Another way that state ownership can impact performance is that it creates a sort of distortion of

competition in the entire industry. As mentioned above the overcapacity creates a downward pressure on

the yield, not only on the state owned company, but on other airline companies as well.

Article 107 in the Treaty on the functioning of the European Union clearly states, that any aid from a

member state should not distort any competition, by favoring a certain entity. Whether this article is 100 %

complied with by member states can be questioned. In 2009 when Core SAS was introduced, it also

included raising additional capital. Denmark, Sweden and Norway contributed with SEK 3 billion (SAS AR

2009 page 6). Furthermore a new issue of shares was accomplished in February 2010, and again the owner

states came up with capital, this time SEK 2.5 billion.

Whether the supporting actions from the owner states have been legally carried out, has been questioned

by many. According to Peter Vesterdorf, one of the leading experts in state aid and EU law, there could be a

controversy. He says that: “it all comes down to whether the state acts as a normal market investor, when it

puts billions into SAS” (Stelling, 9 February 2010). There are some EU regulation regarding restructuring and

financial rescuing aid though, which states that there in some cases can be provided aid one single time,

following the “first time, last time” principle – which in practice means that aid cannot be given several

times within a time period of 10 years (Krog, 12 November 2012).

The most previous example of state aid to SAS was in 2012, when the states guaranteed loans of SEK 3.5

billion, as the banks would not otherwise provide the loans. Yet this was proven by the EU Commission (SAS

AR 2012, page 2).

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

0.0% 20.0% 40.0% 60.0% 80.0% 100.0%

EBIT margin

State ownership (%)

SAS year 2009

22

It is obvious from the above, that the competition in the airline industry cannot be characterized by open

competition, as many European airlines - among those SAS - are still owned partially by states which often

acts in the grey area in terms of financial aid.

Whether SAS will still be kept as a state owned company in the future is hard to predict. However,

politicians in Norway and Denmark have several times mentioned the idea of selling their ownership in SAS.

Whether this should be regarded as a threat of an opportunity for SAS, would probably depend on which

eyes are looking at it. It was probably not bad for SAS, that they were owned by states during the crisis,

where Sweden, Norway and Denmark guaranteed loans of SEK 3.5 billion and put up additional capital of a

total of SEK 5.5 billion. However, as figure 7 illustrated, companies tend to perform better without the

influence from politicians.

Other things that influence the industry are the taxes and duties that airline companies are being charged

for, by the individual countries. Enhedslisten, a Danish left wing party represented in the Parliament, has

proposed a DKK 75 air passenger duty, for every passenger that takes off from a Danish airport (Krog, 29

August 2012). This would presumably affect the number of passengers, as the airline companies would be

forced to pass on the duty to the passengers in terms of higher ticket prices. If this is introduced it will

influence LCC’s more than for example SAS, as the duty would make up a bigger proportion of the ticket

price. This is an everlasting concern in the industry, as for many other industries, yet not easy to influence.

3.1.2 Economic factors

General economic situation and outlook

SAS’s home market is the Nordic Countries, however when assessing the influence from external economic

factors, not only should the home market be taken into consideration, but also the global economy. This is

important as the small open economies in the Nordic countries are very sensitive to the rest of the world,

especially USA and China, as the GDP of those two countries stand for 31.9 % (Bloomberg) of the total

world GDP. Therefore a very briefly description of the state of the economy, including expectations to USA

and China, will be presented in the following.

According to the IMF, the global economic growth is estimated to pick up in 2013-2014, among other things

due to the policy actions in USA and Europe, who are stimulating the economies and keeping interest rates

at an artificially low level (IMF Economic Outlook May 2013 p. 9).

Looking at USA, several factors are indicating that the economy is gaining momentum. The S&P/Case-Shiller

Home Price Index, which shows the change in home-prices in two portfolios consisting of 10 and 20 big US

cities, indicates that the annual home prices increased in February 2013 by 8.6 % and 9.3 % respectively.

Home prices have a big impact on the private consumption and are therefore very important in regard to

growth, as the private consumption make up 70 % of GDP in USA. The growth rates in the home prices will

according to SEB (Nordic Outlook February 2013) have a positive impact on US GDP of 0.3-0.4 percentage

points in 2013. The price increases might also have impacted the consumer confidence which in May 2013

was at a five months high at 68.1.

23

Furthermore, unemployment has started to come down from the top in January 2013 at around 10 % to 7.5

% in May 2013, which indicates that the employers are beginning to hire workers and consequently are

looking more opportunistic at the future.

In regard to the policy actions in USA, the Federal Reserve (FED) has introduced thresholds for

unemployment (6.5%) and inflation (2.5%) that should be reached before increases in interest rates might

be considered, which with the present development will not be reached within the nearest future.

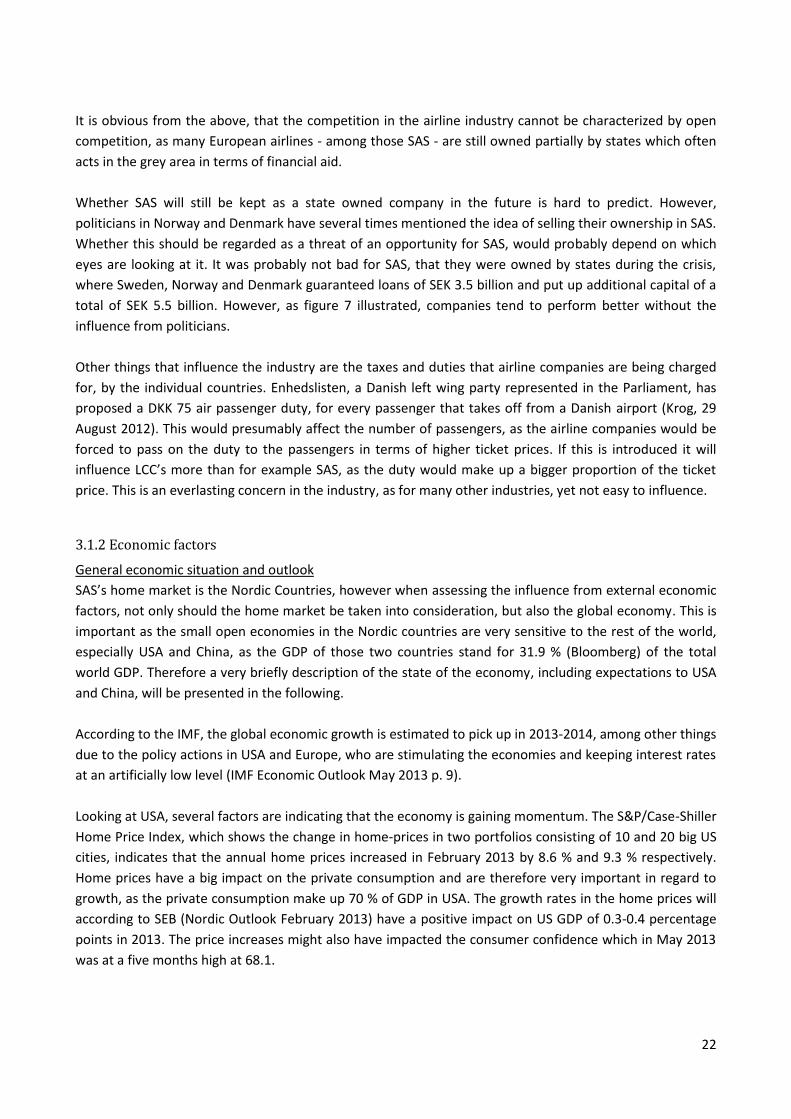

Figure 8: Total GDP in 2012. Source: Own creation – data from Bloomberg.

Looking at China, which has been the real engine of growth during the financial crisis, the economy is still

booming. Even though not growing at the same speed as in 2007, with growth rates of more than 10 %

annually, it was still growing at 7.7 % in May 2013 according to Bloomberg. Due to the strong economic

growth in China, many people are being dragged out of poverty and the middle class are growing. As the

Chinese have never been richer than now they will, as the trend has shown in the last years, start to buy

European goods, as Western luxury brands are associated with life and sophistication, and might thereby

contribute to getting the European economy on the right track again.

Going through the two most important economies at the moment, it indicates that the economy is at a

turning point, which could indicate a budding economy. Other factors such as the stock markets also

indicate a positive development. In Q1 2013 the S&P 500 in USA was growing at 6.2 % and the MSCI world

index, which is a diversified portfolio consisting of indices from more than 70 countries, grew by 7.18 %

(Press release: MSCI Indices Q1 2013 performance results).

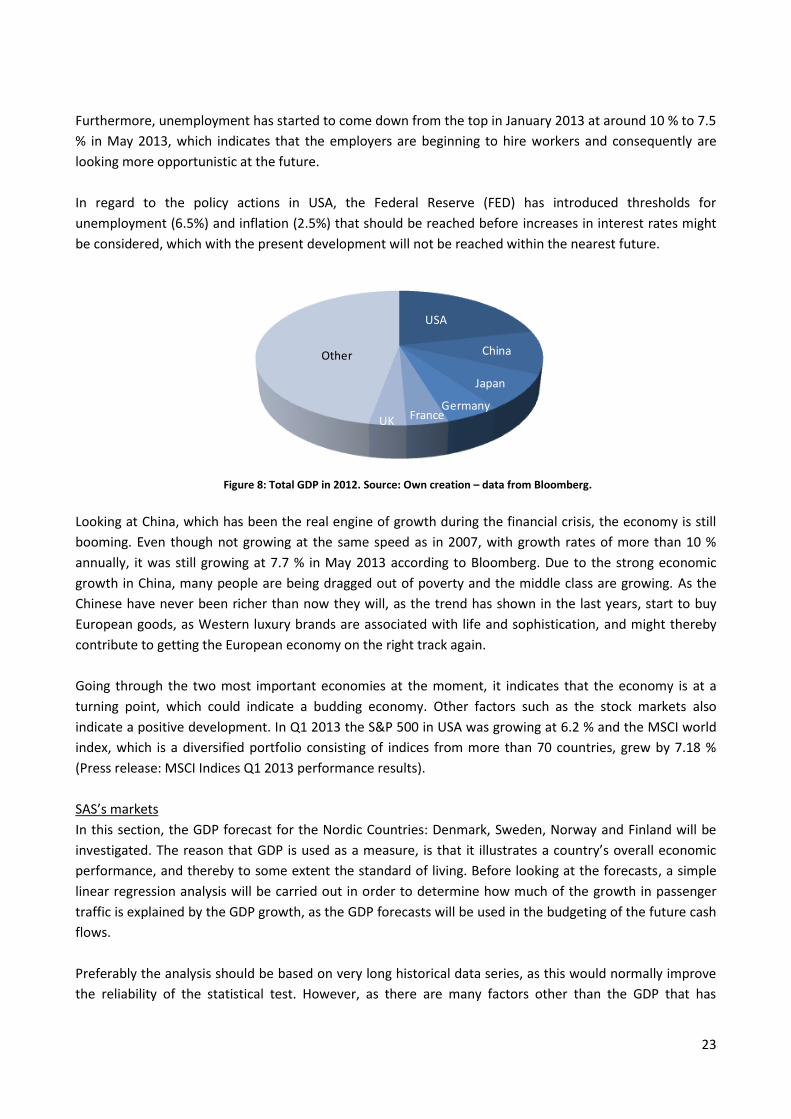

SAS’s markets

In this section, the GDP forecast for the Nordic Countries: Denmark, Sweden, Norway and Finland will be

investigated. The reason that GDP is used as a measure, is that it illustrates a country’s overall economic

performance, and thereby to some extent the standard of living. Before looking at the forecasts, a simple

linear regression analysis will be carried out in order to determine how much of the growth in passenger

traffic is explained by the GDP growth, as the GDP forecasts will be used in the budgeting of the future cash

flows.

Preferably the analysis should be based on very long historical data series, as this would normally improve

the reliability of the statistical test. However, as there are many factors other than the GDP that has

USA

China

Japan

GermanyFranceUK

Other

24

affected the volume in the industry, especially the deregulation of the airline industry in Europe in the 90’s,

it is estimated that using data from before the 00’s will have a negative impact and add noise to the test.

Consequently the test is based on data from the period 2001-2011.

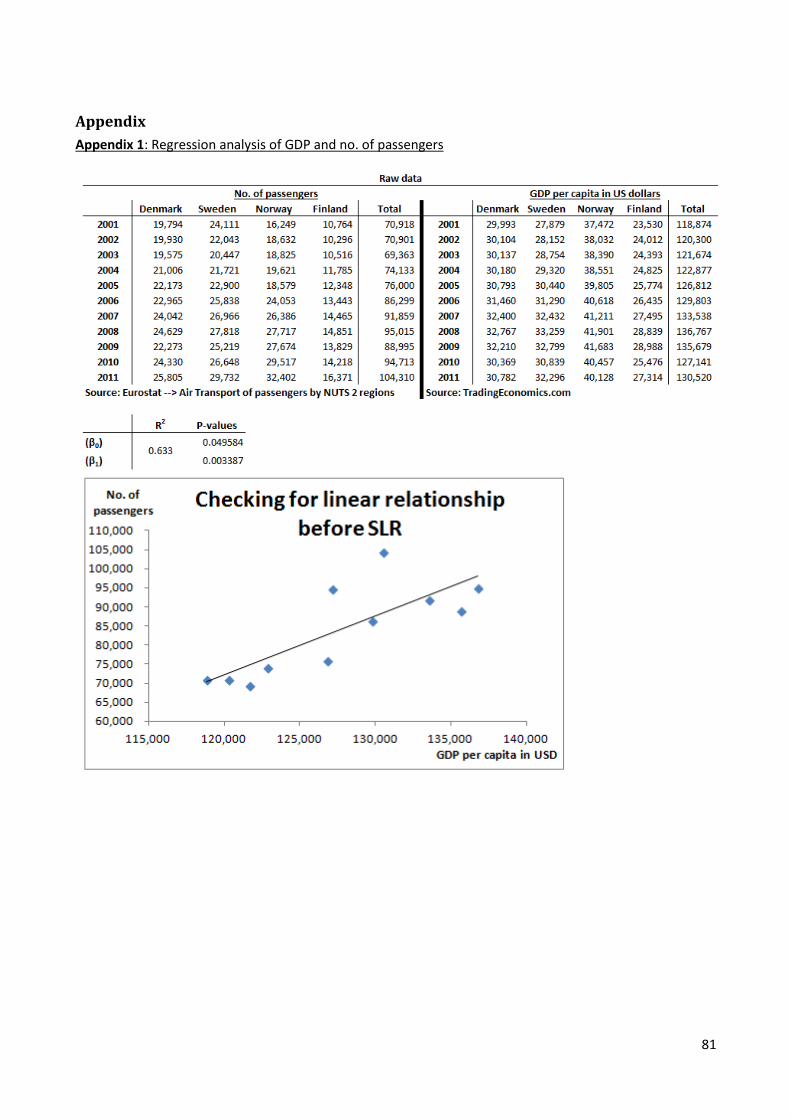

The two hypotheses are, at a 95 % confidence interval:

H0: No relationship between GDP and no. of passengers

H1: Relationship between GDP and no. of passengers3

The regression analysis indicates a positive relationship between the two factors. The P-value for β0 is 4.9 %

which is less than alpha (α) which is 5 %. Even though not significant less than α, it is still less and thereby

the H0 hypothesis, which stated no relationship between the two factors, is rejected.

R-squared (R2) is 63.3 % indicating that GDP growth has explained 63.3 % of the passenger growth in the

last ten years.

Now that it has been concluded that there is a positive relationship between the GDP and no. of

passengers, the GDP forecasts will be taken into consideration, in order to get a view of the future direction

of the airline industry.

Figure 9: Real GDP growth forecast. Source: Own creation - data from IMF.org.

Figure 9 illustrates that real GDP growth in the Nordic Countries and Euro area will move towards a higher

level. As mentioned in section 2.3, 60 % of SAS’s passenger revenues come from Sweden (22%) and Norway

(38%). These markets’ GDP growth will be at 2.13 % (Sweden) and 2.17 % (Norway) respectively.

According to Pat Hanlon (Hanlon, 2007, p. 25) - an American author to several books concerning the airline

industry - the industry has a rule of thumb which approximate that the airline industry, measured by the

revenue passenger kilometers (RPK), grows/declines twice the speed of the GDP. Provided that this is a

realistic assumption, the weighted average GDP growth rate in SAS’s markets will be 1.8 %, which according

to Mr. Hanlon will turn into a growth rate of 3.6 % in real terms.

3 The raw data and the corresponding analysis are in appendix 1.

-0.50

0.00

0.50

1.00

1.50

2.00

2.50

3.00

2013 2014 2015 2016 2017

Dk NoSw FinEU area

Real GDP growth (%)

25

The International Air Transportation Association (IATA) forecasts in their Economic outlook on May 2013,

that the growth in RPK will be at 4 % annually, and Airbus has in their Global Market Forecast in September

2012 (Leahy, 2012) expected a yearly RPK growth from 2012-2031 of 4 % in Western Europe. Therefore a

level of 3.6 - 4 % seems reasonable to assume in the forecasting period.

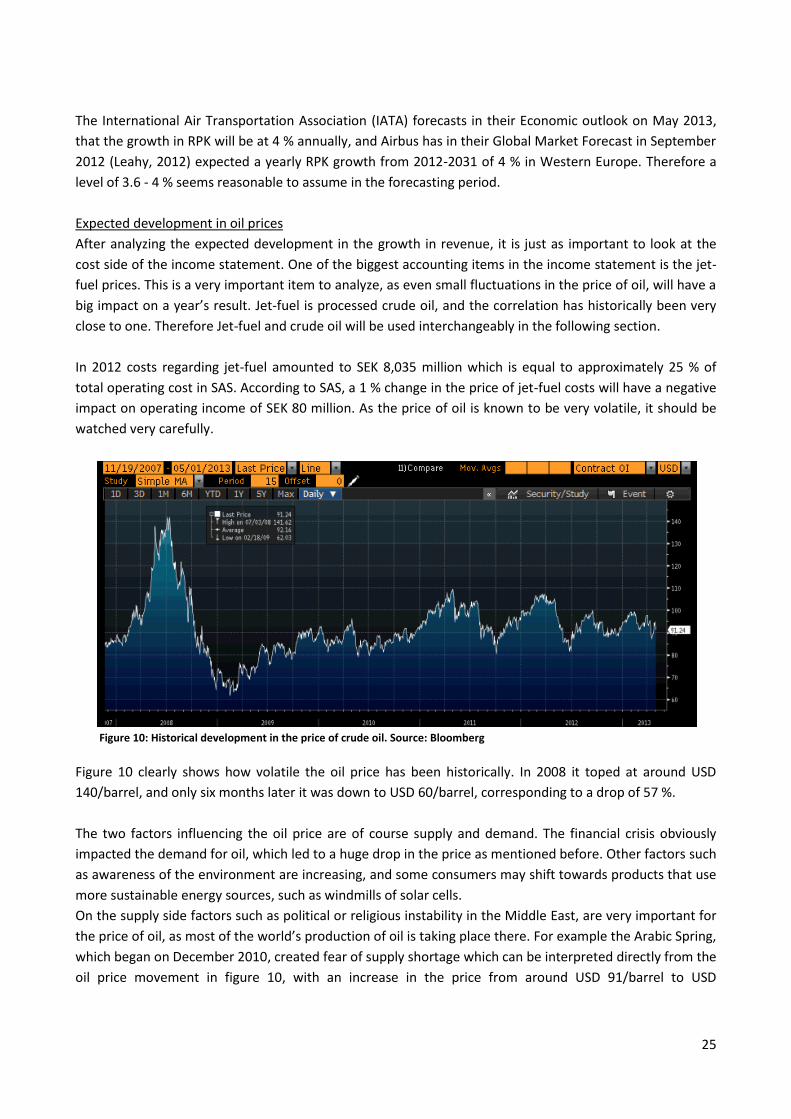

Expected development in oil prices

After analyzing the expected development in the growth in revenue, it is just as important to look at the

cost side of the income statement. One of the biggest accounting items in the income statement is the jet-

fuel prices. This is a very important item to analyze, as even small fluctuations in the price of oil, will have a

big impact on a year’s result. Jet-fuel is processed crude oil, and the correlation has historically been very

close to one. Therefore Jet-fuel and crude oil will be used interchangeably in the following section.

In 2012 costs regarding jet-fuel amounted to SEK 8,035 million which is equal to approximately 25 % of

total operating cost in SAS. According to SAS, a 1 % change in the price of jet-fuel costs will have a negative

impact on operating income of SEK 80 million. As the price of oil is known to be very volatile, it should be

watched very carefully.

Figure 10: Historical development in the price of crude oil. Source: Bloomberg

Figure 10 clearly shows how volatile the oil price has been historically. In 2008 it toped at around USD

140/barrel, and only six months later it was down to USD 60/barrel, corresponding to a drop of 57 %.

The two factors influencing the oil price are of course supply and demand. The financial crisis obviously

impacted the demand for oil, which led to a huge drop in the price as mentioned before. Other factors such

as awareness of the environment are increasing, and some consumers may shift towards products that use

more sustainable energy sources, such as windmills of solar cells.

On the supply side factors such as political or religious instability in the Middle East, are very important for

the price of oil, as most of the world’s production of oil is taking place there. For example the Arabic Spring,

which began on December 2010, created fear of supply shortage which can be interpreted directly from the

oil price movement in figure 10, with an increase in the price from around USD 91/barrel to USD

26

110/barrel. Consequently, as wars are difficult to predict - so are the oil price movement, and only rough

estimates of the future development can be carried out.

The cocktail of being hard to predict and having a big impact on earnings, is of course something that

makes the airline companies very cautious about it. Therefore most airline companies use hedging tools

such as forwards and futures, in order to reducing the short term risks associated with price fluctuations. As

jet-fuel futures do not exists, futures on crude or heating oil must be used instead.

SAS states in their annual report for 2012, that 40-80 % of their oil consumption has already been hedged

for 2013, meaning that the prices have been locked.

Consensus on Bloomberg, which is formed by reported estimates from many of the world major banks,

states an average increase in oil prices until 2017 of 2.8 % annually. This is almost in line with U.S. Energy

Information Administration, who is predicting the oil price to be at USD 117/barrel in 2025 (U.S. EIA Annual

Energy Outlook 2013). Calculating the compounded annual growth rate (CAGR)4 this equals to 2.2 %.

Therefore, a point between 2.2 % and 2.8 % will be used in the budgeting period.

USD/SEK exchange rate

In regard to the costs associated with jet-fuel consumption, the exchange rate between SEK and USD also

have to be taken into consideration. The reason for this is that jet-fuel is being traded in USD. Accordingly

there is a mismatch between cost currency and the revenue currency. Therefore, if the oil price goes down

but the US dollar goes up relatively more against the Swedish currency, the impact on SAS’s earnings will be

negative.

A screen dump from Bloomberg’s currency rating site is visible in appendix 2. This indicates that the SEK is

currently overvalued against the USD by 4.02 %. The SEK has been very volatile in the past, and should

according to Bloomberg decrease in value compared to the dollar, which consequently would drive up the

jet fuel costs.

3.1.3 Social factors

The general tendency in the airline industry the last ten years for the customers, have been to focus more

on price and less on the convenience during the flight, specifically on short haul routes. Especially after

2008, when the financial crisis erupted, passengers started to look after the price more than ever.

Particularly in the business segment, the prices have become an important factor. During the economic

boom, many business passengers had been using first class and were less concerned about the price. This

changed after the financial crisis as many companies, due to their financial troubles, introduced more strict

policies in regard to air travel. According to Henry H. Tarteveldt, an industry analyst and founder of

Atmosphere Research Group: “More businesspeople are traveling, but companies are being tighter with

their budgets” and he continues “Travelers increasingly have to justify their trips, and trips have to be

approved by managers.” (Mouawad, May 2, 2012). The conclusion by Mr. Tarteveldt is also in line with

SAS’s announcements.

4 CAGR = (Ending value/Beginning value)^(1/# of years) - 1

27

Other factors that might contribute to the increasing price consciousness are internet searching tools such

as momondo.dk in Denmark, where customers simply type in date of departure and destination, where

after all available flight tickets on that specific date pups up, in price order starting with the cheapest. This

way of finding a flight ticket, in contrast to 5-10 years ago where the customers had to contact the airline

companies directly, has without doubt impacted the customers towards LLC’s, as they usually offer the

cheapest tickets.

The increasing price consciousness among customers, both in the business and leisure segment, has

obviously impacted SAS. As the trend began, especially with the introduction of LCC’s in the beginning of

the 00’s, SAS had to adapt to the changing market conditions. As mentioned in section 2.2, SAS has worked

hard towards minimizing the unit costs, in order to be able to compete directly with the LCC’s as

Norwegian.

The demography in the Nordic countries is of course another important factor, when looking at the future

market for the airline companies. Due to the baby-boom in the 1950s, large groups of elderly people in the

Nordic countries are expected to be retiring in the nearest future, which might push up the volume in the

leisure segment. Further the proportion of the household income spend on air transport have increased

steadily in the last decade. Using Denmark as an example, there has been an increase from 0.22 % to 0.38

% of the household income spent on air transport (statistikbanken.dk).

3.1.4 Technical factors

One of the main factors influencing the airline industry is the technological development. With the

possibility of ordering and paying tickets, checking-in and comparing prices over the internet, the airlines as

a means of transportation, have become much more convenient and popular than ever, which might also

explain part of the increase in the household economy spend on air transportation mentioned in the

previous section.

Improving the experience of flying is certainly essential in terms of attracting passengers. Hence, being a

first mover within technology is of a great importance. Norwegian was for example one of the first airline

companies to introduce WIFI on their aircrafts, which obviously was a gigantic competitive advantage, as

the internet today is used to everything from checking news to updating Facebook and communicating with

friends, colleagues and family.

SAS has in several cases been a first mover within the field of technology. This has been essential for SAS, as

their strategy has always been to attract the business segment, and on delivering good services during the

flight. SAS has for example been the first mover in regard to introducing the “Smart Pass” where the Near

Field Communication (NFC) technology is used, which is a wireless communication technology (SAS AR

2013, p.13). Initially this has been ruled out for members of loyalty program “EuroBonus”, which makes it

easy to get through the check-in, security control etc. faster than people on a regular economy ticket.

According to plan, SAS are scheduling to have an app ready before the end of 2013, which makes it possible

for passengers to pay, check-in etc. by holding the mobile phone close to a scanner at the entrance.

28

Moreover, the aircrafts are also continuously being developed. Aerodynamics, improved fuel efficiency and

lighter aircrafts are just a few areas that are continuously being improved and researched in. Therefore the

airline companies should constantly be analyzing the fleet in terms of when they should be replaced with

new and more efficient aircrafts, which is always a trade-off between new investments towards improved

unit costs.

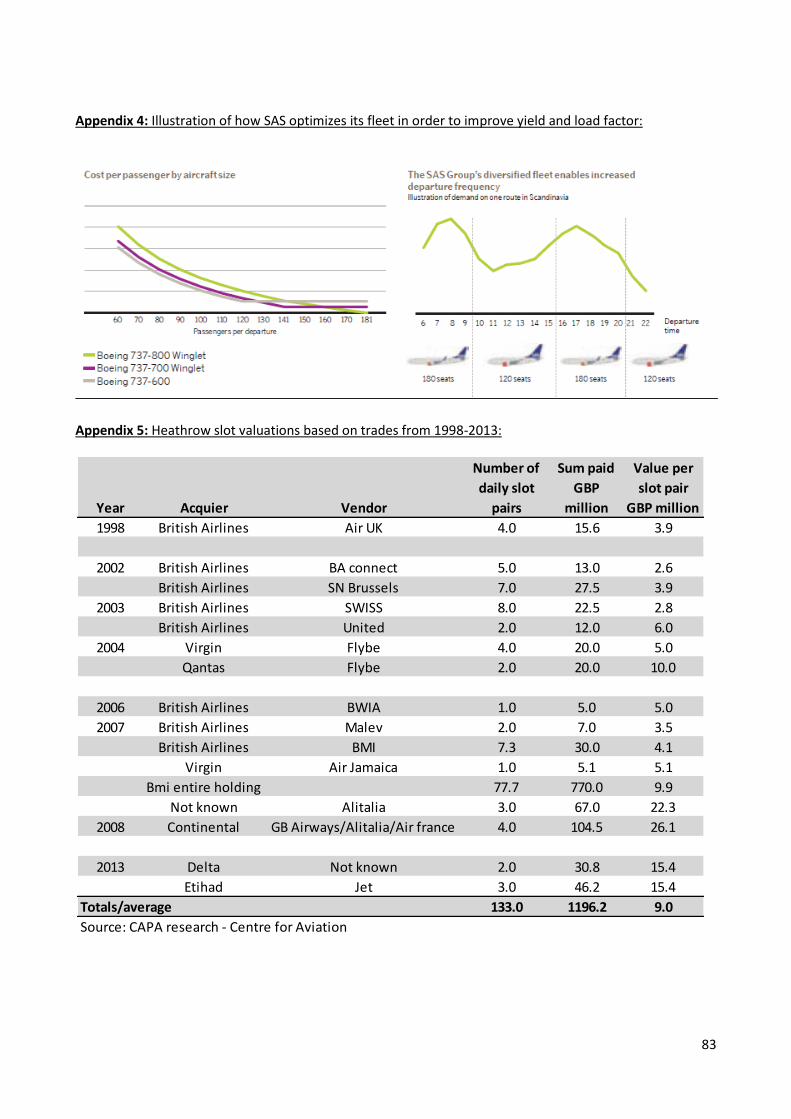

As an example, SAS has signed contracts of 26 new aircrafts as part of the 4XNG strategy, which will reduce

the fuel consumption by 10-15 % compared to the older aircrafts, still with the same number of seats,

which obviously will be included in the forecasts, in terms of decreasing jet-fuel expenses.

3.1.5. Conclusion of PEST analysis

Summing up, the analysis showed a picture of the economic macro environment which is rather attractive

at the moment. Especially the economic conditions which point towards an improvement in the world

economy, with USA gaining momentum and China still delivering solid economic growth rates.

With the GDP forecasts serving as a good indicator for the future activity level in the industry, the growth

rates for SAS’s home markets are also looking to improving from today’s level, with expected growth rates

in the range of 3.6 – 4.0%.

Oil prices which add up to almost 25 % of the total operating costs in SAS, has been very volatility

historically, and are consequently hard to predict in the future. However, a growth rate of around 2.5 % in

the future seems to be the consensus in the market. Taken into consideration the exchange rate between

USD and SEK, it might incur extra costs on SAS, that the SEK is currently overvalued by 4.2 % against the

USD according to Bloomberg.

The industry is to a very high degree affected by political factors as well. The deregulation of the industry

has caused a more free competition, which has allowed LCC’s to enter the market and drive the prices

down and competition up – which obviously has affected SAS negatively, and caused loses in market

shares. Taxes and duties are other things that the politicians have the power to change, and consequently

incur extra risks in the industry.

Consumer preferences have changed in the last decade, making them focusing more on prices than

anything else. This has been a main factor in allowing for LCC’s, and putting pressure on HCC such as SAS.

Finally technology is of a big importance. New improved systems have been invented, aiming at making the

entire process from buying a ticket to when the customer is sitting in the aircraft, more convenient. This

can give a competitive advantage, and therefore it is important in the competition of attracting customers.

Further, being able to offer tickets to competitive prices calls for a modern fleet which is more fuel efficient

and consequently affect the unit costs, which is an important parameter. Therefore, being a first mover

within the field of technology is very important in this industry.

29

3.2 Analysis of the industry