structured settlement annuities in special needs settlement planning jack meligan, cssc, bcfe...

TRANSCRIPT

Structured Settlement Annuities in Special Needs

Settlement Planning

Jack Meligan, CSSC, BCFEMichele Whitmore, CSSC, CFP®

• Settlement Planning is a profession that helps recipients of settlement proceeds use those proceeds to achieve their post-loss goals and transition successfully into their post-settlement financial lives.

What is Settlement Planning?

Settlement Planning

Financial Planning

Litigation

What is Settlement Planning?

Structured Settlement Annuity

• Issued by an insurance company• Payments are fixed and cannot be

changed (SPIA)• Lump-sums allowed (No need to be

“substantially equal”)• Interest included in payments is not

taxable

Structured Settlement Annuity

• IRC 104(a)(2) – excluded whether paid as lump sum or periodic payments

• IRC Sec. 130 – Qualified Assignment – allows defendant to transfer liability to a third party

• Actual and constructive receipt issues

Are Structured Settlements Bad?

A fairly dumb question

Which is the Best Tool?

• Hammer• Pliers• Screwdriver• Ratchet• Saw• Wrench

Which is the Best Tool?

• Ridiculous question• Depends on the job

at hand• Some tools more

useful than others• No BAD tools

unless used incorrectly or for wrong job

Best Settlement Planning Tool?

• Structured settlement annuity

• Mutual fund• Exchange traded fund• Supplemental needs

trust• Settlement

preservation trust• Money market fund

Are Structured Settlements Bad?

• Bad question• Depends on job• Structured

settlement can be a wonderful tool when used correctly by a professional

• Structures sometimes get a bad reputation

Hacks with Dollar Signs in Their Eyes

• Nasty defense tactics• Unqualified hacks• Over-structuring

When All You Have is a Hammer….

• Your professional should use a comprehensive approach to settlement planning

• Don’t work with a one trick pony annuity hawker

How to Recognize Professional?

• Credentials• Loyalty to

plaintiffs• Planning

approach• Professional• Experience

How Much to Structure?

If appropriate to structure any

To Structure or Not to Structure

• What’s the proper amount to structure, if any?– Needs analysis– Liquidity analysis– Life care plan analysis– Meet baseline needs and

not a penny more– FedEx money- absolutely,

positively has to be there

Advantages of Structured Settlements

• Can’t get at the money• Rated ages• Tax-exempt income• Lifetime payments• Fixed, guaranteed

return• Match fixed cash flows• Secure• No need to manage• Low dissipation risk

• Medical underwriting• Bad is good – not just injury related• Full market survey• Adds substantially to payout• Baby who got rated age of 79 – took

cash at recommendation of trust officer, money exhausted, everyone sued

Rated Ages

SNT

SSAnnuity

InvestmentAccount Cash

FlexibilityFlexibility

Risk of LosingRisk of Losing

Tools of Settlement Planning

• Predictable, ongoing needs can best be met with annuity

• Structured settlement annuities are flexible in design.– Lifetime payments– Period certain

payments– Lump sum payments

Square Pegs and What to Structure

Predictable Medical Expenses

• Attendant care• Predictable

medical expenses

• Equipment replacement

• Regular transportation upgrades

• Medications

Do NOT Structure…

• Expenses projected for next 5 years (except attendant care)

• Examples:– Home renovations for

accessibility and safety purposes

– Vehicle modifications– Emergency reserve for

unexpected expenses

Diversification

• Multiple annuity companies

• Methods of payment (i.e. monthly vs. lump sums)

• Cash, investments and structured settlement annuities

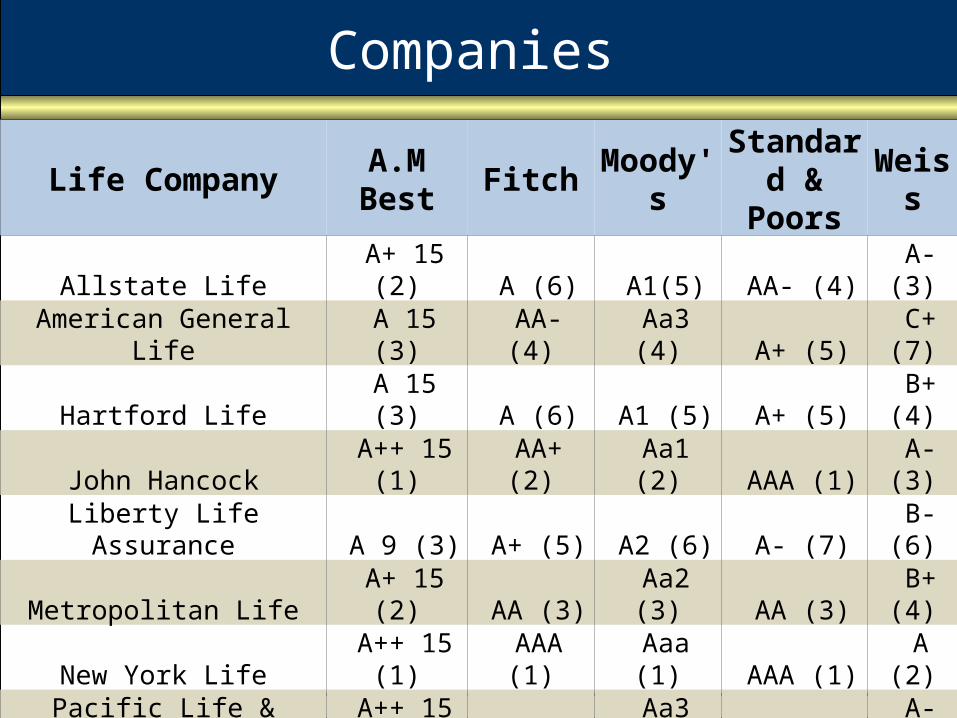

Companies

Life Company A.M Best Fitch Moody's Standard & Poors Weiss

Allstate Life A+ 15 (2) A (6) A1(5) AA- (4) A- (3)

American General Life A 15 (3) AA- (4) Aa3 (4) A+ (5) C+ (7)

Hartford Life A 15 (3) A (6) A1 (5) A+ (5) B+ (4)

John Hancock A++ 15 (1) AA+ (2) Aa1 (2) AAA (1) A- (3)

Liberty Life Assurance A 9 (3) A+ (5) A2 (6) A- (7) B- (6)

Metropolitan Life A+ 15 (2) AA (3) Aa2 (3) AA (3) B+ (4)

New York Life A++ 15 (1) AAA (1) Aaa (1) AAA (1) A (2)

Pacific Life & Annuity A++ 15 (1) AA (3) Aa3 (4) AA (3) A- (3)

Prudential A+ 15 (2) AA-(4) Aa3 (4) AA (3) B (5)

Symetra Life A 12 (3) A+ (5) A2 (6) A (6) B (5)

Case Study - Jackie

• 12 year old little girl• Catastrophic brain

injury• Rated age of 45• Annuity

– $10,000/mo.– 3% COLA– Lifetime payments– $3,000,000 cost

Jackie - Alternatives

• SNT needed• Life care plan –

needs $10,000/mo. in FedEx money

• Trustee recommending portfolio

• How does this stand up?

Jackie – Testing Alternatives

• Structured settlements– No taxes– No trust fees apply

• Non-structure alternatives– Stocks– T-Bonds– 50%/50%

• Back tested using actual returns going backwards

Jackie – Testing Alternatives

• Structured Settlement

• Stocks• T-Bonds• 50%/50%

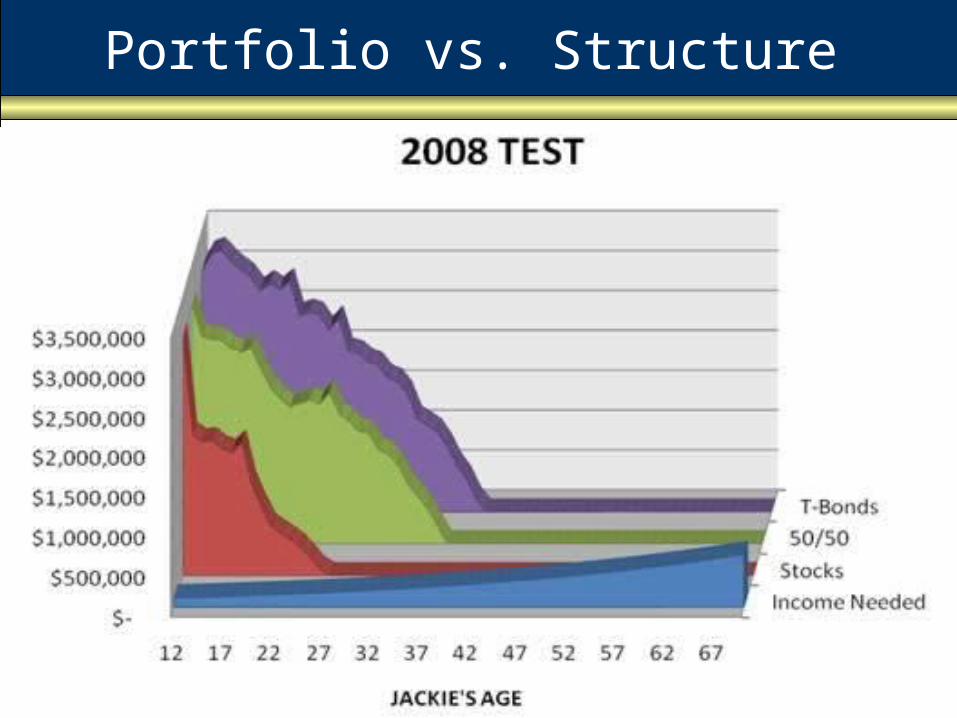

Portfolio vs. Structure

Portfolio vs. Structure

Portfolio vs. Structure

Portfolio vs. Structure

What if Things Change

Stuff Happens!

What if the Situation Changes?

• Life comes at you fast

• What can change?– Death– Miraculous

recovery– Further injury– Family misfortune– Opportunity– Etc.

What if Claimant Dies?

• Accelerated payment of the annuity at death (commutation rider)

• Family needs?• Estate Tax (IRC Sec.

2039(a) – The gross estate shall include the value of an annuity or other payment …)

Commutation Riders

• If the claimant dies after the purchase of a structured settlement annuity by the Assignee, and there are any remaining and unpaid guaranteed payments under this structured settlement annuity, a percentage of such payments will be commuted and paid to the designated beneficiary (or to the claimant’s estate) in a single sum.

• The amount of the commuted payment will be calculated using 95% of its annuity purchase rates in effect at the time of claimant’s death, for the same or similar certificate.

Factoring

Working the “Factoring” Market

• Rarely recommended• Companies are

overly aggressive• Settlement planners

can provide guidance to protect the client

• Hint: Don’t call 1-800-CASH NOW

IRC Sec. 5891, which became effective January 23, 2002, allows for certain future payments to be “factored” to a lump sum with court approval.

Factoring Structured Settlements

• Court will consider “best interest” of payee and payee’s dependents

• Unapproved factoring transactions subject to 40% federal tax

Settlement Language Pitfalls

Settlement Documents

• Settlement Agreement and Release

• Qualified Assignment

• Court Order Approving Settlement

Process: Required Documents

Settlement Agreement & Release

• Settlement agreement should never state that plaintiff or SNT Trustee will purchase annuity

• Signals constructive receipt

• Defendant or its casualty insurer send check directly to annuity company

Settlement Agreement & Release

• Settlement agreement should not state “receipt and sufficiency is hereby acknowledged”

• Sufficiency is okay, but not receipt (since future payments have not yet been received)

• Settlement agreement should never put injury in doubt

Settlement Agreement & Release

INCORRECT: “Plaintiff claims that he sustained personal physical injuries, all as a result of the incidents…”CORRECT: “Plaintiff sustained personal physical injuries, that he claims are as a result of…”

Qualified Assignment

• “Qualified assignment” assigns obligation to pay future payments from defense or its liability insurer to assignment company

• Assignment company purchases and owns the annuity

• Take care not to allow secured creditor status

Court Order Approving Settlement

• Court must approve if minor or incompetent adult

• Court orders payment made directly to assignment co.

• Court orders payee of annuity is SNT Trustee

• No beneficiary other than SNT Trustee (to protect Medicaid’s interest)

Deficit Reduction Act of 2005

• Requires disclosure of any interest an applicant has in an annuity

• Disclosure required even if an annuity is irrevocable or not treated as an asset

• Insufficient disclosure may result in denial or termination of Medicaid eligibility

Does SNT Beneficiary Have Interest?

• Remember scenario for structure:– SA requires future payments paid by defense– Defense assigns obligation to make future

payments to assignment company– Assignment company buys and owns annuity– Court orders payments sent by assignment

company directly to SNT Trustee– Trustee is payee and only party who could

sell future payments

Does SNT Beneficiary have Interest?

• What is SNT beneficiary’s interest in annuity?– Not buyer, owner, payee or beneficiary– Never had receipt (actual or constructive) of

any of the funds– Cannot sell, accelerate, transfer, give away,

alter, receive, encumber, smell, touch or see the contract or any payment from it!!!

– Saleable = Countable (but, SNT beneficiary cannot sell payments, not the payee (Trustee) or owner (Assignment Company)

A Call to Action!

• DRA doesn’t address “Structured Settlement” annuities

• Different states may adopt different policies

• Need clear authority - issuance of POMS• Calling for coalition of ASNP, SSP, NSSTA,

NAELA, The Alliance, AAPD, and others to request clarity from SSA

• Until then, may be risk if you don’t follow the rules in DRA

Safety of Annuity Companies

What if the sky falls?

Have They Seen Worse Times?

• New York Life 1845• MetLife 1863• Pacific Life 1868• Prudential 1875• Amer. General 1900• Liberty Life 1919• Allstate 1931• Symmetra 1957• Hartford 1810• John Hancock 1862

Companies

Life Company A.M Best Fitch Moody's Standard & Poors Weiss

Allstate Life A+ 15 (2) A (6) A1(5) AA- (4) A- (3)

American General Life A 15 (3) AA- (4) Aa3 (4) A+ (5) C+ (7)

Hartford Life A 15 (3) A (6) A1 (5) A+ (5) B+ (4)

John Hancock A++ 15 (1) AA+ (2) Aa1 (2) AAA (1) A- (3)

Liberty Life Assurance A 9 (3) A+ (5) A2 (6) A- (7) B- (6)

Metropolitan Life A+ 15 (2) AA (3) Aa2 (3) AA (3) B+ (4)

New York Life A++ 15 (1) AAA (1) Aaa (1) AAA (1) A (2)

Pacific Life & Annuity A++ 15 (1) AA (3) Aa3 (4) AA (3) A- (3)

Prudential A+ 15 (2) AA-(4) Aa3 (4) AA (3) B (5)

Symetra Life A 12 (3) A+ (5) A2 (6) A (6) B (5)

What if Insurer Goes Broke?

• Only A+ or better insurers should be used

• Even when they go broke, annuitants almost always get something

• Better odds elsewhere?• So far 700,000 insured structured

settlements– About 300 people didn’t get 100% of what

they were promised– 99.95% got everything, .05% got most

after delays and hassle

Are Annuities Safe in the Long Run?

• Fair question in these hard times• Safety begins with proper risk

management• Heavily regulated by state insurance

commissioners• Reserves, Capital, Surplus• Insolvency – does not mean they

can’t pay the bills• State guarantee funds

Where Can This Bite Me?

What to Watch Out For

Watch Out!

• Where can this bite me in the &*#$@?– Not having a qualified settlement

planner on the team….but, wait, isn’t that the plaintiff attorney?

– If SNT attorney takes assignment from plaintiff attorney who has not retained an expert.

– Broker on case who has no duty to protect plaintiff’s interests

Watch Out!

• What about choice of funding vehicle(s)?– Plaintiff attorneys believe SNT attorneys

are experts in all areas– Liabilities:

•Improper coverage of special needs with funding vehicles

•Improper diversification of funding vehicles

Other Potential Problems

• Improper beneficiary designations

• Improper liquidity considerations:– while injury victim

is living– at injury victim’s

death

Questions?