supporting the corporate growth bringing a fresh

TRANSCRIPT

Citi Perspectives | Q1/Q2 | 2015

Citi PERSPECTIVES

04Treasury Priorities

Supporting the corporate growth agenda by expecting the unexpected, being prepared for anything

10Eye on Cash Management

Bringing a fresh perspective to the corporate balance sheet by applying smart cash management practices

30The Middle East

Why centralizing treasury operations there is hot

Citi Perspectives | Q1/Q2 2015 1

CONTENTS

02 WELCOME

Naveed Sultan Michael Guralnick

10 HOW SMART CASH MANAGEMENT COULD SAVE YOUR BALANCE SHEET

Ebru Pakcan

26 SMARTER, BETTER OUTCOMES FOR CORPORATES DRIVING SSC ADOPTION IN EMEA

Steve Elms

GLOBAL REGULATORY OUTLOOK: WHAT CORPORATE LEADERS NEED TO KNOW IN 2015

Ruth Wandhöfer

30 THE BEATING HEART: WHY MULTINATIONALS ARE CENTRALIZING TREASURY IN THE MIDDLE EAST

Dave Aldred

14

EXPORT CREDIT AGENCIES SUPPORT THE VOLATILE ENERGY INDUSTRY

Valentino Gallo

04 TREASURY PRIORITIES: SUPPORTING GROWTH, MANAGING CONTINGENCIES

Ron Chakravarti Declan McGivern

OPTIMIZING LIQUIDITY IN A SHIFTING WORLD

Amit Agarwal

22

18

Treasury and Trade Solutions2

While economic conditions show steady signs of improvement in the U.S., in the rest of the world, challenges related to economic, regulatory and the geopolitical environment remain an ever-present concern. In many regions, particularly the eurozone, political instability and sovereign debt issues are seen as the top risk to global growth. Even in the economic juggernaut of China, there is a prevailing pessimistic sentiment about current and future conditions on the home front. Latin America shares a similar view, which stands in stark contrast to India, where domestic conditions are seen as overwhelmingly positive.

Beyond concerns in their home regions, multinational corporates are focused on global risks such as increased economic volatility, potential sovereign-debt defaults, low consumer demand and rising volatility of exchange rates worldwide. In light of these factors, the importance of building a modern treasury function, well-integrated with wider business areas (not just being seen as a cash management hub) is increasingly being seen as a critical element in support of a clear and defined growth strategy.

Citi’s unparalleled global footprint, extensive local expertise and industry-leading technology (such as CitiDirect BESM Tablet, which brings business intelligence and global banking to your fingertips) are helping treasurers to re-engineer their processes to more effectively manage risk, improve visibility and control, enhance flexibility and increase efficiency. And when it comes to delivering the very best client experience, we spare no effort.

SUCCEEDING IN TODAY’S COMPLEX BUSINESS ENVIRONMENT

On the following pages of this issue of Perspectives, we will delve into a number of topics that are on the minds of treasury professionals, along with trends and innovations that are impacting structures and processes in today’s complex economic, financial and regulatory environment.

As indications of a U.S.-led global economic recovery are tempered by geopolitical shifts, supporting revenue growth and managing contingencies have become the leading focus for treasury. And, we will examine the top treasury priorities for 2015 that are shaping the agenda of corporate treasury professionals.

WELCOME

Naveed Sultan

Global Head, Treasury and Trade Solutions, Citi

Michael Guralnick

Global Head, Corporate & Public Sector Sales and Global Marketing, Treasury and Trade Solutions, Citi

Citi Perspectives | Q1/Q2 2015 3

With an eye toward improving the balance sheet, companies are increasingly looking at their cash management operations, conducting benchmarking assessments to address financial pressures that influence current-state decisions in order to better shape strategies and priorities going forward.

In this issue, we also look more deeply at new regulatory changes that directly affect corporates, as well as those that indirectly impact them by targeting the banks they work with, influencing the availability of certain types of financing or products. We will examine two recent regulatory initiatives that have significant implications for corporates.

Also in this issue, we will examine the role of energy in the global economy and how changes in energy prices are impacting exploration and associated activities. We will explore the flexibility of trade finance solutions and its ability to support a wide range of energy-related projects in a dynamic sector.

Furthermore, we will review the drivers behind the adoption of shared service centers (SSCs) in EMEA and why the competition for talent is steadily raising hiring expenses, which over time will diminish cost benefits leading companies to shift to either new low cost locations to take advantage of the cost arbitrage or add higher value-added services into the SSC’s to drive a higher return on investment. We will delve into the reasons corporates must look beyond short-term personnel cost savings and instead focus more on the efficiencies that result from centralization and automation and how to bring more services into the SSCs.

As you review the articles in this edition of Perspectives, we hope you will find them both informative and thought-provoking. We remain committed to sharing insights into trends and innovation that we believe can bring value to your business. In order to continue meeting the needs of our clients, we rely on your input, and we invite you to let us know how we can better support your goals.

We remain committed to sharing insights into trends and innovation that we believe can bring value to your business.

Treasury and Trade Solutions4

Citi’s forecasts call for a gradually improving global economy during 2015. However, the outlook is marked with increasing divergence across countries and regions and consequent uncertainties for corporate top-line growth. Meanwhile, investors remain unforgiving of earnings surprises in an environment with elevated political and market risks.

Against this backdrop, treasury teams are working to support their company’s growth, while standing ready to “expect the unexpected” in planning scenarios.

TREASURY PRIORITIES: SUPPORTING GROWTH, MANAGING CONTINGENCIESWith signs of a U.S.-led global economic recovery tempered by geopolitical shifts, treasurers are leading the way by supporting revenue growth and managing contingencies.

Risk remains a critical factor For many treasurers, a top-of-mind issue is dealing with volatility as global markets adjust to divergent economic growth prospects, fluctuating commodity prices, and rate-increase decisions by the Fed, while quantitative easing spreads in Europe. With international sales representing over a third of revenue for the median S&P 500 corporate, and prospects for continued USD appreciation, treasury teams are focused on risk management strategies to protect cash and provide more stability for corporate earnings.

Ron Chakravarti

Managing Director, Global Head of Treasury Advisory Group, Treasury and Trade Solutions, Citi

Figure 1: FX Risk Drives Earnings Volatility*

R-squared (%) of Index Volatilities with Earnings Volatility

*Factset, Bloomberg.

Declan McGivern

Director, EMEA Head of Treasury Advisory Group, Treasury and Trade Solutions, Citi

63%

FX

40%

Commodities

37%

Interest Rates

5Citi Perspectives | Q1/Q2 2015

Treasury and Trade Solutions6

In a recent survey of multinational risk management practices,1 two key trends stood out:

• There was a consensus on the risks created by continued appreciation of the dollar, but many had taken limited mitigating action. Among the considerations currently playing out is whether FX management should be focused on protecting the plan rate or on helping to smooth earnings. Hedging approaches such as layering vs. rolling can help achieve one goal, but potentially conflict with the other. If smoothing earnings is desired, a rolling approach with longer duration can help achieve the objective with long-dated options used to maintain flexibility.

• In a surprising number of cases, subsidiary funding and associated decisions (sources of funding, currency and risk mitigation) were made on an ad-hoc basis or under local finance discretion. At a time of high currency volatility, keeping these activities, and associated currency and interest-rate hedging, within the scope of central treasury and tax decision making is advisable given the potential for earnings impacts, running into thin capitalization rules, and other issues that may arise.

Change to improving return on invested capital Mindful of investor focus on returns, CEOs continue to attend to capital deployment decisions, with treasurers helping to create financial capacity to execute on these choices.

Consider:

• Is the company positioned with the liquidity needed to complete strategic transactions the Board may decide on?

• How should hurdle rates be adjusted for countries likely to impose capital controls and FX restrictions, so that CapEx decisions take this into account?

• And, as growth in new markets creates more working capital funding needs, are there ways to shore up the balance sheet?

Among the areas where treasury teams are directly making an impact is in Return on Invested Capital (ROIC). Working capital solutions, such as global cash management centralization and trade finance solutions help lower invested capital and enhance ROIC. Global cash pooling shrinks net working capital at the consolidated level by netting subsidiary level bank cash and short-term debt positions, allowing the company to run with less operating cash. Similarly, centralization of financial operations into Shared Service Centers provides treasury

Working capital solutions, such as global cash management centralization and trade finance solutions, help lower invested capital and enhance ROIC.

1 Citi Treasury Diagnostics and The NeuGroup Assistant Treasurers Group of Thirty, Risk Management Survey, March 2015.

7Citi Perspectives | Q1/Q2 2015

teams with more control over the levers to change Days Sales Outstanding and Days Payables Outstanding, improving cash conversion cycles. When payment terms are extended, supply chain financing provides support to vendors, who may be smaller and more credit-challenged than their multinational corporate buyers. It is clear that more companies are deploying these approaches:

In Citi’s Treasury Diagnostics benchmarking survey, 34% of large corporates surveyed are using supplier financing solutions today, compared with only 21% five years ago.2

By taking these actions, treasurers can free cash trapped in the balance sheet and deliver tangible shareholder value.

Integrating regulatory changes into treasury structuresCountry capital controls drive whether and how local markets’ cash and funding activity can be integrated into the company’s global treasury structure. China especially stands out with regard to opportunity. Despite the recent slowdown, it will continue to be a major growth market for many multinationals. Meanwhile, regulatory reforms and the internationalization of the renminbi have fundamentally altered what companies can achieve in treasury management. Multinationals can now centralize nationwide payments and collections processes in China, concentrate domestic cash and link this to their global liquidity pools, and use netting and reinvoicing structures to centralize FX risk management into their global in-house banks.

2Citi Treasury Diagnostics 2015.

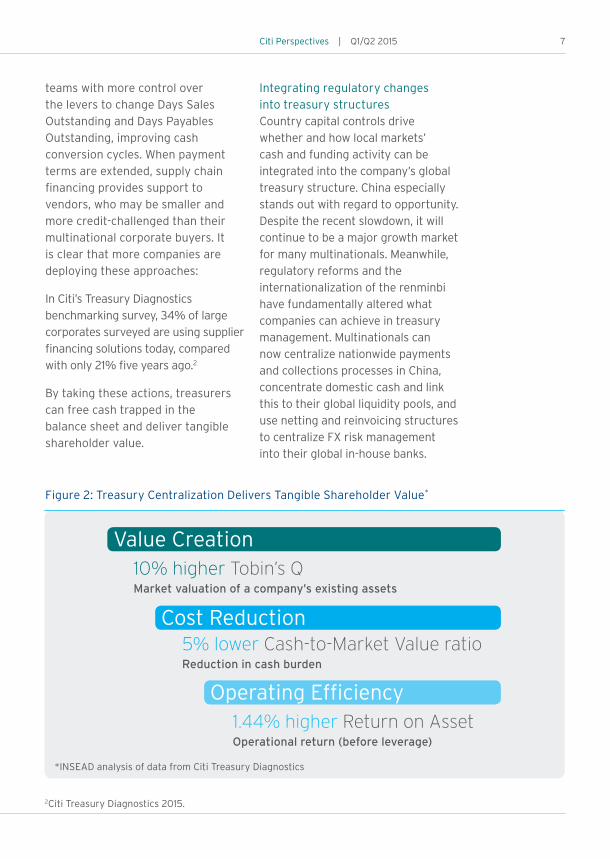

Figure 2: Treasury Centralization Delivers Tangible Shareholder Value*

10% higher Tobin’s QMarket valuation of a company’s existing assets

Value Creation

Cost Reduction5% lower Cash-to-Market Value ratioReduction in cash burden

Operating Efficiency1.44% higher Return on AssetOperational return (before leverage)

*INSEAD analysis of data from Citi Treasury Diagnostics

Treasury and Trade Solutions8

Consolidating more transaction activity at a bank makes balances more likely to be classified as operating.

Next, as banks adjust to Basel and other regulations, the value ascribed to lines of business and client relationships continues to evolve. While most corporates are aware that regulation has made operating cash management business more attractive to banks, it is worth understanding the nuances. For example, large banks generally analyze client accounts using actual operating activity and tenor profiles to determine how much of a client’s balances receive more attractive regulatory liquidity treatment. Even under full regulatory oversight and disclosure, analytical methodologies vary between banks. But, in general, consolidating more transaction activity at a bank makes balances more likely to be classified as operating. There is also a debate around whether Basel makes cash pooling structures a less attractive offer for banks. While Citi’s methodology means that cash pools linked to operating cash management structures remain both attractive and a core client offer, appetites vary between banks.

It is important for companies to recognize that these results drive how banks value client relationships and should be incorporated into bank relationship management discussions and wallet allocation decisions. Treasury teams will need to continue to stay up to date as other changes occur. For example, other Basel rules are still being

implemented. Ring-fencing of bank balance sheets by national regulators (to favor local depositors in case of a failure) impacts how companies can utilize global liquidity management services. And coming money fund regulation in the U.S. and Europe will drive changes in short-term investment and funding practices.

Additionally, the OECD Base Erosion and Profit Shifting (BEPS) action plan is taking firmer shape. The objective of tax authorities is to restrict transfer pricing mechanisms being used to generate profits in tax-favorable jurisdictions at the risk of lower tax revenue in the country of trade origin. The outcome of BEPS is expected to impact many commonly used corporate trading models. This will have consequent implications for treasury vehicles (such as in-house banks) and liquidity management structures. Multinational treasury departments should assess the implications and get ready for changes.

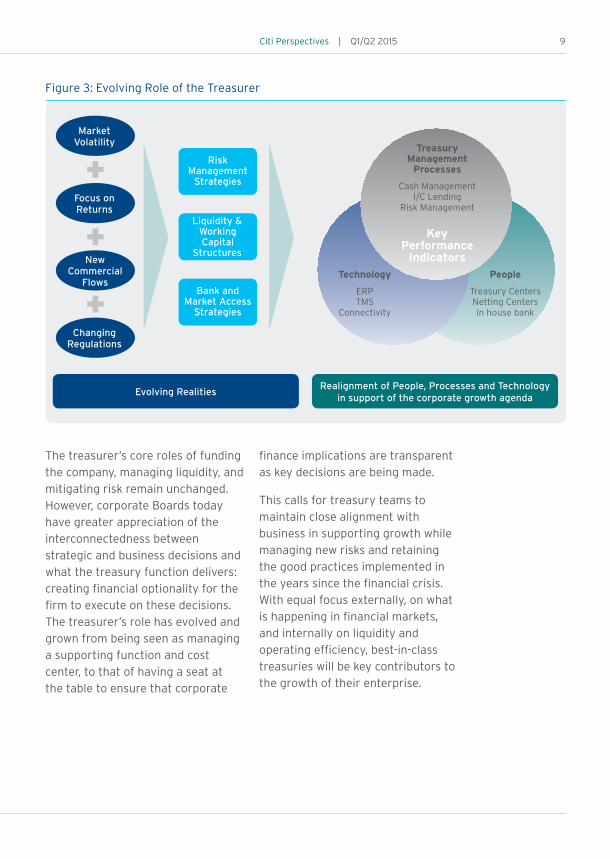

Evolving role of the treasurer Evolving commercial and market realities are making many legacy treasury practices sub-optimal. Companies should continually reassess opportunities for refinement and extension of treasury organizational structures and processes to reduce carrying costs and risks.

9Citi Perspectives | Q1/Q2 2015

The treasurer’s core roles of funding the company, managing liquidity, and mitigating risk remain unchanged. However, corporate Boards today have greater appreciation of the interconnectedness between strategic and business decisions and what the treasury function delivers: creating financial optionality for the firm to execute on these decisions. The treasurer’s role has evolved and grown from being seen as managing a supporting function and cost center, to that of having a seat at the table to ensure that corporate

finance implications are transparent as key decisions are being made.

This calls for treasury teams to maintain close alignment with business in supporting growth while managing new risks and retaining the good practices implemented in the years since the financial crisis. With equal focus externally, on what is happening in financial markets, and internally on liquidity and operating efficiency, best-in-class treasuries will be key contributors to the growth of their enterprise.

Market Volatility

Focus on Returns

Changing Regulations

New Commercial

Flows

Risk Management

Strategies

Liquidity & Working Capital

Structures

Bank and Market Access

Strategies

Evolving Realities Realignment of People, Processes and Technology in support of the corporate growth agenda

Treasury Management

Processes

Cash Management I/C Lending

Risk Management

Technology

ERP TMS

Connectivity

People

Treasury Centers Netting Centers in house bank

Key Performance

Indicators

Figure 3: Evolving Role of the Treasurer

Treasury and Trade Solutions10

HOW SMART CASH MANAGEMENT COULD SAVE YOUR BALANCE SHEETMore often than not, finding ways to improve a company’s balance sheet requires looking at cash management operations through a different set of lenses. Just as an eye care professional can offer remedies that improve eyesight, cash management experts assist with cash flow and cash management processes that can lead to stronger financial health.

Ebru Pakcan

Global Head of Payments and Receivables, Treasury and Trade Solutions, Citi

Top cash management providers deploy their own methodology for analyzing treasury and financial operations, and then deliver intelligence on root causes of various problems and prescriptions for fixing them. Toward this end, they conduct their examinations through a number of lenses. One of their most critical focal points is an organization’s financial position, where a thorough assessment of financial pressures that drive current-state decisions can help shape strategies and priorities going forward.

Perspectives on these pressures are found in the company’s balance sheet and income statement, which represent its wealth and its health, respectively. These statements provide insights into financial drivers that cascade through product development, distribution, sales cycles and market expansion. They also house information that is critical

to unlocking solutions for improving working capital management, in addition to risks and controls.

Looking through the financial lens Since financial statement characteristics and drivers can vary from industry to industry, a company’s cash management partner must ask the right questions to understand business and financial priorities. If, for example, the company is a new entrant to an industry or is deploying a new product line under a new subsidiary, it may be focusing on shortening receivables and avoiding sales reversals. A stronger, longer-term player in the same industry may be concentrating on its liquidity position to support acquisition activities. An enterprise with a wide geographic sales footprint may want to have an optimization play across multiple balance sheets, and in turn, may set up a re-invoicing or shared

11Citi Perspectives | Q1/Q2 2015

service center arrangement, where it may benefit from tax efficiencies by making its receivables “cross-border.” A fully global company may be under competitive pressure to drastically innovate and overhaul its product line, distribution and sales model. This situation could impact its legal and account structures, payment and collection channels, and its payment methods. In the end, it comes down to asking the right questions.

Process improvementsOverall, improvements to payments and receivables processes can yield numerous benefits. Potential benefits include a reduction in expenses, as well as improved cash flows and working capital management.

Efficient accounts payable processes can lower operating, interest and foreign exchange costs, and also increase days payables outstanding (DPO). The later money can go out, the longer it can be used internally to support business activities, reducing both borrowing needs and the amount of debt on a company’s balance sheet. Plus, having the ability to accurately monitor and shorten payables cycles increases the availability of working capital and enhances overall liquidity positions.

On the accounts receivable side, reducing the risk of outstanding payments is a common priority among companies looking to improve cash flows. Efficient receivables management can reduce operational expenses, collapse days sales outstanding (DSO) and increase control. The faster money comes in, the faster it can be reallocated or converted to cash, which effectively increases assets on the balance sheet. Mitigating receivables risks can drastically impact financial standing.

Ensuring liquidity is essential Another point of focus in any assessment of treasury operations is centralization. Centralizing the management of cash, generally speaking, fuels liquidity optimization and investment performance, as well as strategic and daily working capital operations.

Many large multinationals maintain very sophisticated investment policies that stipulate “qualified” instruments, investment limits for different obligors (government, bank and other institutions) as well as the credit rating limits for instruments and certain financial ratio requirements. Depending on its treasury management philosophy, a corporation may

Treasury and Trade Solutions12

maintain comprehensive worldwide policies that consist of different parameters for domestic and overseas operations, and include defined levels of approval for certain overseas activities.

The sophistication and risk appetite of the company will often drive the level of detail in its investment policies. Regardless of how detailed the policies are, it is critical for a company’s cash management consultants to thoroughly understand its investment policies in the context of its treasury and working capital management processes and goals.

No matter how young or mature a treasury operation may be, or how complex or geographically dispersed its activities are, an operational and policy check-up by a trusted provider offers the potential to unlock opportunities for improvement.

Citi’s treasury and cash management experts have a proven track record in refining and improving treasury setups and operations while bringing new levels of working capital optimization to help foster ideal financial positioning.

Many large multinationals maintain very sophisticated investment policies that stipulate “qualified” instruments, investment limits for different obligors (government, bank and other institutions) as well as the credit rating limits for instruments and certain financial ratio requirements.

13Citi Perspectives | Q1/Q2 2015

Treasury and Trade Solutions14

Ruth Wandhöfer

Global Head, Regulatory and Market Strategy, Treasury and Trade Solutions, Citi

Corporates rightfully spend most of their time focused on their operational strategy and goals while constantly assessing the impact of the changing macro-economic environment on their business. Treasury’s role is to respond to the needs of the business and use its knowledge and tools to manage risk, enable the company to fund itself and operate efficiently, and help the business to achieve growth in a sustainable way.

Necessarily, economic and geopolitical conditions also play a major part in treasury planning. Similarly, a third factor — regulation — has always been an important consideration in treasury management. However, in the post-crisis period, regulation has become ever more crucial. A large part of treasury resources at many corporates is now focused on keeping up to date with the evolution of regulations.

The nature of regulatory change is twofold: Some new rules directly affect corporates; others impact them indirectly by targeting the banks they work with, which can affect the availability of certain types of financing or products. To compound the challenges faced by corporates seeking to understand regulatory change, while many new regulations are global in nature, their implementation remains but should

be implemented on a national level. In some cases there is significant divergence in how regulations are framed. In the following section, we address aspects of two recent regulatory initiatives that have significant implications for corporates.

Basel III: The net stable funding ratioBasel III is perhaps the most significant post-crisis regulatory change affecting the banking industry (and indirectly, corporates). The most recently published element of Basel III (in October 2014) is the Net Stable Funding Ratio (NSFR), which is the long-term liquidity pillar of Basel III. The other principal liquidity standard is the Liquidity Coverage Ratio (LCR), which is intended to ensure that banks can withstand a 30-day stress scenario by requiring them to hold a sufficiently large buffer composed

GLOBAL REGULATORY OUTLOOK: WHAT CORPORATE LEADERS NEED TO KNOW IN 2015

15Citi Perspectives | Q1/Q2 2015

GLOBAL REGULATORY OUTLOOK: WHAT CORPORATE LEADERS NEED TO KNOW IN 2015

of eligible liquid assets. The LCR was enforced by many jurisdictions in 2015 (e.g., by the U.S. agencies in September 2014) and its impact has already been widely discussed.

The NSFR aims to support banks’ long-term stability and resilience by creating a framework for them to hold long-term stable funding in relation to their assets to ensure that funding risk is significantly reduced. The stability of liabilities under the NSFR is determined by the funding tenor, where long term liabilities are assumed to be more stable, and the funding type and counterparty, where retail and small- and medium-sized enterprise deposits are assumed to be behaviorally more stable than wholesale funding from other counterparties, such as corporates and financial institutions. Consequently, it has some significant repercussions for corporates.

At a high level, the NSFR will — like LCR — contribute to phenomena, such as reduced bank lending; falling bank profitability; increased financial disintermediation; continued bank capitalization exercises; less bank trading activity and associated reductions of liquidity in the market; increased exposure of banks to sovereigns; limited ability of banks to redistribute financial risk and potential concentration in some asset classes; reduced support for financing international trade; and ultimately a transformation of banks’ role in the broader economy.

The NSFR is a complex calculation which comprises an Available Stable Funding Factor (ASF), which is the portion of capital and liabilities that is expected to be reliable over the one-year time horizon of the NSFR; and a Required Stable Funding Factor (RSF), which is the amount of stable funding that will be required over the one-year horizon. However, while complicated in detail, the practical implications of these factors on corporates are fairly straightforward.

For the ASF side, corporate funding with residual maturity of less than one year, as well as operational deposits (from transaction banking-related activities) receive a 50% ASF factor and will become less sought after by banks. Other liabilities with a maturity of over one year receive a 100% ASF and will become very attractive to banks in relation to their NSFR compliance. On the RSF side, corporate loans extended for a period of less than one year require 50% long-term funding, and will become more expensive to banks. Banks will be dis-incentivized to lend to corporates beyond one year as it will require a 100% RSF.

Other implications of the NSFR include the potential for derivatives transactions to become more expensive, given the tighter requirements around netting and collateralization. Another issue for corporates to consider is that the RSF factor, which describes how much is required over the one-year

Treasury and Trade Solutions16

horizon and which is determined by the liquidity characteristics and residual maturities of the assets held by the bank, including off-balance sheet exposures, will be applied to the portion of undrawn irrevocable and conditionally revocable credit/liquidity facilities. This will add an element of additional funding cost. National variations on implementing the RSF factors for other contingent funding, such as trade finance guarantees and letters of credit, may also add an element of fragmentation between markets with varying associated cost implications for corporates.

However, the Basel timetable foresees the NSFR to be in force only by 2019, which still leaves some time for the industry to adjust.

MMF reformOne important focus of regulators in the post-crisis period has been Money Market Funds (MMFs), which are an important element of many corporates’ investment strategy. In September 2013, the European Commission proposed a European framework designed to make MMFs more resilient to future financial crisis and, at the same time, secure their financing role for the economy. The European framework continues to evolve, with the European Parliament due to consider the MMF Regulation during a plenary session in late April 2015, but the broad shape of the regulation is known.

The proposed MMF Regulation requires levels of daily/weekly liquidity for the MMF to be able to satisfy investor redemptions (MMFs are obliged to hold at least 10% of their assets in instruments that mature on a daily basis and an additional 20% of assets that mature within a week). It also requires clear labelling on whether the fund is a short-term MMF or a standard one (short-term MMFs hold assets with a residual maturity not exceeding 397 days while the corresponding maturity limit for standard MMFs is two years).

One important aspect of the regulation, a capital cushion (the 3% buffer) for constant net asset value (CNAV) funds to support stable redemptions in times of decreasing value of the MMFs’ investment assets, was dropped by the European Parliament in early April. A CNAV fund seeks to maintain a stable €1 per share when investors redeem or purchase shares. In February, the ECON committee of the European Parliament voted in favor of requiring every CNAV MMF to become an “EU Public Debt CNAV MMF,” a “Retail CNAV MMF” or a “Low Volatility NAV MMF.” Low Volatility NAV MMFs would be permitted to display a constant NAV when certain conditions are fulfilled, but are subject to a five-year ‘sunset’ clause.

Other reform measures include a requirement to implement customer profiling policies to help

One important focus of regulators in the post-crisis period has been Money Market Funds (MMFs), which are an important element of many corporates’ investment strategy.

17Citi Perspectives | Q1/Q2 2015

anticipate large redemptions. In addition, MMF managers will have to do some internal credit risk assessment to avoid overreliance on external ratings. The proposed rules would apply to all funds that invest in money market instruments — regardless of whether the basic parameters of the fund are governed by the Undertakings for Collective Investment in Transferable Securities rules or whether the MMF operates as an alternative investment fund according to Alternative Investment Fund Managers Directive.

The European approach seeks to align with the international work on shadow banking, mainly with the recommendations formulated by the Financial Stability Board and the European Systemic Risk Board. On most issues, such as the liquidity rules, issuer diversification and customer profiling, the EU proposals seek to mirror the rules already applicable in the U.S. Differences in approach result from the fact that the current European market is structured differently from other jurisdictions. The U.S. is more advanced in its reform of MMFs than Europe. In July 2014, the SEC

passed new regulations that will be implemented over a two-year period through to 2016. The rules have two main components: First, a floating NAV for institutional prime/commercial paper (CP) MMFs. Second, liquidity fees and redemption gates for all institutional MMFs (if liquid assets drop below certain thresholds and subject to the discretion of the MMF’s board).

These changes have prompted investor concerns regarding issues such as liquidity access, principal preservation, tax (capital gain/loss) and accounting (MMFs may potentially no longer be considered a cash equivalent). The industry also remains concerned that a floating NAV could severely impair short-term corporate and financial institutional funding markets, given their reliance on MMFs as a conduit for financing, and also push CP rates higher (corporates may compensate by issuing more CP directly to investors). Liquidity fees and redemption gates provide funds with the flexibility to manage/mitigate potential heavy redemptions during times of stress, but ultimately restrict investors’ liquidity.

Treasury and Trade Solutions18

Valentino Gallo

Global Head, Export and Agency Finance, Treasury and Trade Solutions, Citi

The sharp decline in the oil price since June 2014 — it more than halved in just six months — has focused attention on the role of energy in the global economy. Changes in energy prices have affected the viability of oil and gas exploration and some facilities have been mothballed: A steep fall in investment is anticipated.

For many oil and gas exploration projects longer-term factors — such as energy security — play an important role in determining whether they go ahead. Some countries have made increasing renewable sources of energy a political priority. While falls in oil prices may require governments to fine-tune the support offered to renewables, backing will not evaporate.

Moreover, the flexibility of trade finance solutions should ensure that a wide variety of energy-related projects continue to progress. Increased volatility will reduce the appetite of some investors for energy-related trade finance. However, export credit agencies (ECAs) are likely to step into the breach and increase their support for energy projects.

Winners and losersLower oil prices have a different effect on oil importing and exporting countries. Economies in oil-importing

countries, such as China and India, and — in the developed world, Europe and Japan, have been boosted by lower oil prices, with falling inflation, improvements in their balance of payments and the freedom to maintain expansionary monetary policies.

By driving growth, lower fuel costs should increase tax revenues and may offer an opportunity to reduce fuel subsidies, which are often a sizeable part of government spending in emerging markets. Oil importers should therefore have additional resources to invest in infrastructure, which should increase demand for trade finance solutions.

In contrast, lower oil prices will weaken oil-exporting countries’ current account balances and public finances and reduce growth. For some large oil exporters, especially in Gulf Cooperation Council (GCC) countries, significant buffers and available financing should minimize cuts in government spending.

EXPORT CREDIT AGENCIES SUPPORT THE VOLATILE ENERGY INDUSTRY

Lower fuel costs should increase tax revenues and may offer an opportunity to reduce fuel subsidies, which are often a sizeable part of government spending in emerging markets.

19Citi Perspectives | Q1/Q2 2015

EXPORT CREDIT AGENCIES SUPPORT THE VOLATILE ENERGY INDUSTRY

Treasury and Trade Solutions20

However, most oil exporters will have to reduce infrastructure spending to balance their budgets.

For emerging market countries, whether they are oil importers or exporters, the fall in energy prices — reinforced by an expected rise in interest rates by the Federal Reserve in the coming months — has the potential to increase market volatility. As a result, all energy projects in emerging markets could become more reliant on ECA funding.

Financing alternative sources of energyThe unstable geopolitical environment has made energy security a major priority for both emerging and developed market countries. Consequently, many governments have adopted policies to promote alternative sources of energy, including renewable sources, such as solar and wind power, and non-traditional sources of carbon-based fuels, such as liquefied natural gas (LNG).

In Latin America, for example, renewable energy has gained increasing government support in recent years. Unlike the U.S. and Europe, where renewable energy is usually subsidized to encourage production, renewable energy in Latin America is competitive with conventional sources of power because of high domestic energy costs.

The bulk of the cost of a renewables project is equipment. ECAs from the country where equipment is manufactured usually provide approximately 50% of the financing for a renewable project; commercial banks (such as Citi) provide around 30%, and the developer typically contributes equity representing 20% of the project value.

Citi is a leader in Latin American renewables financing and acted as advisor and loan arranger for Abengoa’s Palmatir wind project in Tacuarembó, Uruguay. The $153.5 million two tranche loan (from Export-Import (Ex-Im) Bank of the United States and the Inter-American Development Bank) financed the purchase of equipment made in the U.S. by Spanish wind turbine-maker Gamesa.

One growing alternative source of energy is LNG. Most LNG tankers are built in Asia and their purchase by international shipping companies is often facilitated by Asian ECAs. In the last quarter of 2014, Citi completed a $1.34 billion senior secured vessel financing for the Angelicoussis Shipping Group Limited. The financing supported the purchase of eight new build LNG carriers to be built by the South Korean shipyards Hyundai Samho Heavy Industries, and Daewoo Shipbuilding and Marine Engineering. The financing includes a $908.5 million tranche, which is 95% covered by K-Sure, the

21Citi Perspectives | Q1/Q2 2015

South Korean Export Credit Agency, as well as a $427.5 million commercial tranche.

In Africa, ECAs play an important role in the energy sector. Most African sovereigns cannot borrow at the tenors necessary for energy infrastructure investment: an ECA guarantee is therefore necessary. Citi acted as advisor and co-arranger for a 15-year, $101.3 million term facility for the Government of Ghana that was 100%-guaranteed by the Export Credit Insurance Corporation of South Africa. The deal, the first of its type in Ghana, financed electricity transmission lines for 532 towns and villages.

For emerging market countries, whether they are oil importers or exporters, the fall in energy prices — reinforced by an expected rise in interest rates by the Federal Reserve in the coming months — has the potential to increase market volatility.

Energy investment in the region has recently been boosted by Power Africa, a $7 billion partnership between the U.S. government ($5 billion from Ex-Im Bank), several African governments, and other public and private sector entities that aims to double access to electricity. Citi, which last August pledged to source $2.5 billion in incremental support for the initiative, will also leverage its renewable energy financing expertise to assist the program.

Treasury and Trade Solutions22

With ongoing speculation around the future of the eurozone and crisis-driven regulation still being implemented across the financial sector, any casual observer could be forgiven for thinking that little has changed in the macro business environment over the last five years. But as any treasurer will tell you, nothing could be further from the truth.

The first and perhaps hardest hitting change — at least for those in the corporate treasury profession — is the introduction of negative interest rates. Whilst interest rates have been extremely low across Europe and the U.S. in recent years, the move by the European Central Bank (ECB) in June 2014 to lower the deposit rate from zero to -0.1% took us into a new phase in the interest rate cycle.

This triggered a domino effect of rate cuts across Europe with the Danish, Swedish and Swiss National Banks all choosing to follow suit in an effort to protect their currencies and reduce market volatility. For treasurers, the impact of these changes in monetary policy is wide-reaching. We are

entering new territory when it comes to the traditional treasury priorities of security, liquidity and yield. Liquidity is being challenged by regulations such as Basel III, and yields on investments and currencies are scarce, but capital preservation is even trickier.

Take investment policies, for example. These typically dictate that treasurers must retain capital and maintain the value of that capital, but doing so in a world where deposit rates are suddenly negative poses a real challenge. As a result, many treasurers are left questioning the validity of their investment policies and priorities, as well as their accounting practices.

Treasurers are also still wondering where interest rates will go next, as they do not appear to have bottomed out yet. As Steven Elms, Head of Industrials Sector Sales, Treasury and Trade Solutions, Citi, observes, “this uncertainty around rates is a genuine challenge for corporates trying to navigate the new business environment. Not only are they trying to understand where the policy moves are heading but also as to how banks

OPTIMIZING LIQUIDITY IN A SHIFTING WORLD From negative interest rates to significant currency volatility and geopolitical risk, today’s treasurers are operating in largely uncharted territory. Exploring and exploiting this new liquidity landscape will require skillful navigation — and an open mind.

Amit Agarwal

EMEA Head of Liquidity Management Services, Treasury and Trade Solutions, Citi

23Citi Perspectives | Q1/Q2 2015

are responding and how this will impact their deposits, investments and wider currency market movements.”

Against this backdrop of uncertainty, there is one safe bet, says Elms, namely that this new territory for interest and FX rates is here to stay, for the foreseeable future at least. “This is the new normal — and it is this environment that treasurers and banks need to be comfortable operating in.”

Adapting to changeWhat this means is that while it is important to continue to build on the best practices that have been honed within treasury departments in recent years, forward-looking treasurers must also examine ways to adapt and optimize their liquidity structures accordingly.

“One very noticeable trend that we are observing among leading treasuries is the conscious decision to exclude certain pockets of

The first and perhaps hardest hitting change — at least for those in the corporate treasury profession — is the introduction of negative interest rates.

Treasury and Trade Solutions24

daily liquidity from global liquidity structures in response to the lower rate environment,” says Elms. After all, why should a company move balances away from a jurisdiction and incur an FX cost, only to be impacted by the negative rate environment?

“As long as there is complete visibility over the cash and at a near-term use of that local liquidity, then leaving it in-country may be the best course of action,” he notes. “That said, it is still fundamentally important that the liquidity structure the company has in place allows the treasurer to move and mobilize that cash when needed — not because of the level of geopolitical unrest today. Trapped cash is a growing concern in politically unstable countries, as is significant FX volatility, so having a flexible and nimble liquidity structure is now more important than ever.”

Offsetting the negativeWhen we overlay all of these challenges — the negative rate, low yield environment; the geopolitical challenges which are creating further FX swings, sovereign and counterparty risk concerns; and of course the liquidity constraints of Basel III, this creates a perfect environment for clients to sit down around the table with their banks and discuss the optimal liquidity structure that brings together the right mix of cash management, investment and the risk management tools, while observing best practice.

A good example of this is the work Citi has been undertaking with clients to help them meet their goal of capital preservation in this era of negative rates. From an investment point of view, we have introduced smart investment options, such as the minimum maturity deposit, which provides enhanced returns over short tenor time deposits with a minimum notice period before funds can be withdrawn.

Elsewhere, multicurrency cash pools — as part of a global liquidity structure — are proving extremely popular among Citi’s clients as a means to gain liquidity and operational efficiencies, while also replacing or at least reducing the need for FX swaps. With a multicurrency pool, it is possible to offset charges in certain low-yielding currencies by changing the mix of the company’s assets and increasing those currencies which have a wider spread. Furthermore, for the day-to-day operating business, rather than having to spend resources and investment dollars executing FX transactions, they can effectively use the multicurrency cash pool as an implicit way of executing their FX swap transactions. With that in mind, we are seeing double-digit growth in the adoption of cash pools, in particular the multicurrency cash pool.

Recently, Flextronics, a leading end-to-end supply chain solutions company, worked with Citi to create

“This is the new normal — and it is this environment that treasurers and banks need to be comfortable operating in.”

25Citi Perspectives | Q1/Q2 2015

a multi-currency pool for its EMEA operations. By automating the FX conversion and draining of pool funds to the U.S., 90% of the cash in Europe is now available to the U.S. — including U.S. dollars in Israel for the first time.

Regulatory change is another driver behind the focus on multicurrency cash pools. According to Elms, a common request is to include the renminbi as part of a multicurrency pool structure, not only because it is an additional currency that can help to offset negative yields, but also because banks such as Citi have grown their capabilities in this currency (since it has been gradually liberalized by the Chinese authorities) to ensure that locally generated liquidity that was previously trapped in-country can now be brought up into a company’s central liquidity structure, even through automated sweeping options.

“Automation is another huge theme in this new liquidity environment,” Elms continues. “We are seeing more and more requests to set up actions that occur without manual intervention when a particular currency — typically a negative yielding one — reaches a specified amount.” Once the level is hit, Citi can then help to push some of that liquidity into a different destination; whether that be a higher yielding account with a longer maturity, or a money market fund, for example.

Embracing the positive“These kinds of innovations are only going to become more popular as people adjust to the new normal,” predicts Elms. And over the last five years, treasurers have already demonstrated great flexibility in their mind-sets, adjusting their investment comfort zones to include instruments such as tri-party repos and secured lending, so thinking outside the box has almost become part of the job description for those at the top of the profession.

Nevertheless, if innovation is to succeed, it must be built on solid foundations — in this case best practice. Now is not the time for treasurers to start undoing all of the hard work they have put in post-crisis, centralizing, rationalizing and automating their liquidity management. Rather, this is the time to examine how external market influences, such as negative interest rates, actually present opportunities for further efficiency.

Treasury and Trade Solutions26

SMARTER, BETTER OUTCOMES FOR CORPORATES DRIVING SSC ADOPTION IN EMEAEMEA is at the forefront of many shared service center (SSC) trends given its favorable regulatory environment, advanced infrastructure and technology, and the availability of relatively low-cost, highly educated individuals in a number of countries within the region. The following are some of the most important trends currently driving SSC adoption in EMEA.

Cost savings Cost continues to be the fundamental driver for SSC adoption in EMEA. Regardless of the economic environment, process efficiency and cost savings are always attractive to corporates. In uncertain times — which still prevail in Europe despite tentative signs of a recovery — the incentive to cut costs is even more pronounced.

SSCs offer numerous opportunities to create savings. When services are provided locally, multiple individuals perform the same function. Usually, they do not have specific expertise — but rather many job functions (possibly in addition to their regular job). Centralizing functions therefore offers an opportunity to improve an individual’s productivity and create a subject matter expert.

Centralizing a function into an SSC improves its efficiency across the region. By bringing multiple processes into a single center of

excellence, economies of scale are available that can facilitate greater automation. Modern communications infrastructure means that there are few geographical limitations on where SSCs are located. As a result, SSCs can be set up in low cost areas.

In EMEA, the success of SSCs has, however, created its own challenges. Where increasing numbers of corporates have opened SSCs in the same location, hiring becomes more expensive and over time the relative cost benefits diminish. Companies have learned that they must look beyond short-term personnel cost savings — important though they are — and instead focus more on the efficiencies that result from centralization and automation.

Moreover, rather than focusing simply on initial cost savings, companies are considering the growth of the business and the opportunity cost of not moving to

Steve Elms

Head of Industrials Sector Sales, Treasury and Trade Solutions, Citi

27Citi Perspectives | Q1/Q2 2015

an SSC model. SSCs offer relatively fixed costs given scalable technology and straight-through-processing: as volumes increase, unit costs continue to fall.

Risk and controlIn an SSC, the person responsible for a task is dedicated to it (unlike in a decentralized model) and can develop a deep understanding of it. They see the process across multiple channels and geographies and, through the use of standardized processes, are well placed to identify anomalies. As a result, risk management is improved.

Centralizing services in an SSC also makes it easier to implement best-in-class processes. Rather than having to inform multiple individuals in multiple locations about process changes, policy can simply be set — and implemented — in a single location.

While centralization is undoubtedly beneficial overall, some flexibility is lost because, unlike at the local level, interaction between the service function and the business is limited: a sales representative cannot simply walk to their Accounts Payable contact and explain how a particular client likes to pay their invoices. More generally, by focusing solely on a specific function, there is a risk that an SSC can lose touch with understanding the nature of the underlying business.

EMEA corporates are realizing that to create a true control environment, it is essential to ensure there is

engagement between the business and an SSC when services are initially transferred and on an ongoing basis.

The increasing use in EMEA of Payment On Behalf Of (POBO) structures, where an in-house bank manages payments on behalf of subsidiaries in a region, delivers efficiency in terms of process, account maintenance and liquidity. However, POBO also places additional responsibilities on the SSC, such as ensuring compliance with anti-money laundering, sanctions and other regulatory requirements. The SSC effectively becomes the gatekeeper for the organization’s integrity.

Only by being connected to the business — through site visits, training and regular contact — can the SSC fulfill these regulatory obligations effectively. One way that the SSC can reinforce its relationship with the business is to be value-accretive. For example, the huge volumes of data it processes can provide insights to the rest of the organization on supplier payment terms, payment instruments and payment costs. More generally, as SSCs assume a wider role as a funnel for the information generated and required by the business, they may need to develop relationships with local banks and regulators in various national markets to ensure they are up-to-date with market developments.

Cyber security is a critical issue for corporates, and SSCs offer a way to reduce the risks associated with multiple individuals accessing

While centralization is undoubtedly beneficial overall, some flexibility is lost because, unlike at the local level, interaction between the service function and the business is limited.

Treasury and Trade Solutions28

electronic banking portals in multiple countries. By creating a centralized channel for bank connectivity, control is increased while volumes are consolidated thus facilitating investment in expertise and technology, such as encryption and digital signatures. However, paradoxically, the SSC environment creates potential opportunities for more sophisticated fraud given the high volumes of invoices being

processed. EMEA corporates are therefore mindful of the additional controls and checks required to prevent such fraud.

Operational efficiencyTraditionally, most companies used a lift-and-shift model when transferring functions to an SSC in order to limit the impact on day-to-day business. The expectation was that operational efficiency would be boosted by

29Citi Perspectives | Q1/Q2 2015

centralization and that further efficiencies would be achievable over time. However, regulatory harmonization in EMEA (SEPA) and the pressure to improve control, is spurring corporates to seek greater process efficiencies in the initial stages of the centralization process. This goal is being furthered by the standardization of channels, such as SWIFT to connect to banks, and the increased adoption of standards such as XML. As a result, the SSC is able to achieve operational efficiencies even in regions — most obviously Africa — where there are few regulatory or market similarities.

The drive for operational efficiency is also prompting companies to re-examine previously accepted best-in-class strategies. For example, for many years treasury has sought to centralize FX to eliminate in-country risk and gain control over rates and fees. While these objectives have been achieved, process inefficiencies have not been eliminated — they have simply been centralized.

Increasingly, EMEA corporates are considering using SSCs for low-value, high-volume FX transactions. Provided there is transparency and agreed FX rate terms, the vast majority of transactions can be done at SSC level, dramatically improving efficiency, while still giving treasury the visibility and control it requires. High value transactions can still be processed, with additional scrutiny and interaction with FX providers,

by treasury. Consolidating FX at SSC level provides an opportunity to consolidate account structures. Multiple FX payments can be executed from a single account, achieving further efficiencies.

Companies are also questioning assumptions about the payment instruments they use. Until recently, concentration of payments into SSCs (or payment factories) was seen as an opportunity to create a hierarchy of payment methods, with low-cost ACH payments considered favored, followed by wire payments, and so on. Now EMEA corporates are starting to consider the broader costs to the organization of different payment instruments, rather than simply the payment costs themselves.

The issue has been brought forward by increased adoption of alternative payment instruments in EMEA. Cards are increasingly being used for supplier payments, for example. Cards enable companies to pay as they purchase, eliminating invoicing and the many costly processes and checks associated with reconciliation. As well as lowering processing costs — to a level that better reflects the low value of most corporate payments — cards enable suppliers to be paid quicker (which may encourage them to lower prices). Moreover, by using cards, a corporate can boost working capital as it is able to receive goods before the card bill has to be settled. Payments can therefore effectively become a revenue generator.

The drive for operational efficiency is also prompting companies to re-examine previously accepted best-in-class strategies.

Treasury and Trade Solutions30

THE BEATING HEARTMultinationals expanding in the Middle East and Africa, as well as regional companies growing worldwide, are choosing to centralize treasury activities in the United Arab Emirates.

Dave Aldred

Head of Middle East, North Africa, Turkey and Pakistan, Treasury and Trade Solutions, Citi

The Middle East has long been an attractive destination for investment by international companies, largely in the oil and gas sector. More recently, the focus of exploration has shifted to East and West Africa, with significant discoveries having been made in Uganda, Mozambique, Tanzania, Nigeria and elsewhere. Six of the top ten global discoveries in the oil and gas sector in 2013 were made in Africa.1

Investment opportunities in the Middle East and Africa are no longer restricted to natural resources, however. Over the past decade, opportunities have begun to emerge in new sectors. Countries across the Middle East and Africa have invested heavily in infrastructure, and economies have become more diverse — expanding into chemicals and logistics, for example. At the same time, urban consumers have become more affluent. This has boosted demand for consumer healthcare, technology, media and telecoms, as well as construction services, and prompted investments in agriculture to boost productivity.

As a result, foreign direct investment (FDI) into the Middle East and Africa has increased. According to fDi Intelligence, the global insight wing of the Financial Times, FDI into the Middle East and Africa rose by 24.27% in 2013, compared with 2012. Meanwhile, PwC’s Middle East Capital Projects & Infrastructure Survey, published in June 2014, showed that 75% of respondents expected an increase in spending over the coming 12 months. This is largely driven by major events, including the Dubai Expo 2020 and Qatar World Cup 2022, as well as increased spending on social infrastructure including housing, education and health care.

The region’s companies are also expanding internationally, with significant sums of cash flowing to North America. Outward FDI from the Middle East and Africa grew by 21.81% in 2013, according to fDi Intelligence, with the United Arab Emirates (UAE) taking the lead in the region for outward FDI.2

1 Oil and Gas In Africa: An Early Review of 2014, Ventures Africa, November 24, 2014.2The fDi Report 2014, fDi Intelligence.

31Citi Perspectives | Q1/Q2 2015

Treasury and Trade Solutions32

Greater centralization Historically, the diverse economic, regulatory and political environment in the Middle East and Africa has meant that many companies managed both their operations and treasury on a country-by-country basis. As opportunities in the region have broadened and revenues have risen, however, many corporates have taken a fresh look at their organizational structures.

Increasingly, there is a move towards the greater centralization of activities across the region to improve visibility and control.

It is important to note that while there is a broad trend towards more open economies and financial systems across the Middle East and Africa, reform is occurring at a different pace in each country. Some markets, such as Algeria, Egypt, Morocco and Tunisia, continue to have tough regulatory environments, with restrictive central bank reporting requirements or FX controls that make the movement of cash offshore difficult or impossible while limiting the potential for cash pooling. Meanwhile, Saudi Arabia, Turkey and Jordan have tried to make it easier to do business in recent years. Qatar, Bahrain and the UAE are examples of countries that have more favorable regulatory environments at present.

Naturally, the degree to which a company can centralize treasury in the region varies widely, depending on its operational footprint (as well as its organizational structure elsewhere in the world). At a basic level, companies can establish a center for re-invoicing in order to improve visibility and control, and to keep liquidity out of countries that have regulations or FX controls that limit their flexibility. Alternatively, companies can create a more expansive treasury hub, with responsibility for FX, risk management, import and export trade flows, cash and liquidity management, and working capital management. Some non-treasury activities, such as human resources and procurement, are also being centralized in shared services centers (SSCs).

For all companies — regardless of how operationally decentralized they are — there are considerable benefits to improving the regional visibility of cash positions. It enables FX and risk management to be addressed at group level and improves efficiency and corporate governance while aligning to the company’s overall working capital strategy. Even if local regulations prevent the use of pooling, by improving visibility companies can bring challenges, such as trapped cash, into focus. As a result, alternative solutions can be considered, such as increased capital expenditure (assuming attractive opportunities exist).

Corporates should select banks with local infrastructure and experts on the ground to interpret regulations.

33Citi Perspectives | Q1/Q2 2015

Fortunately, enterprise resource planning and treasury management platforms now make it relatively straightforward to achieve visibility of cash across multiple countries. Such platforms also make it possible to manage regional treasury activity from outside the region, for example, in London. By being physically closer to the markets where they operate, however, treasury professionals can more easily stay in touch with regulatory and market changes. They can also respond more rapidly to them.

Working with the right partnerThe Middle East and Africa offer enormous opportunities. The region remains challenging from a regulatory and market perspective, however. So it is essential that corporates work with a bank that is committed to the region — some have scaled back their presence in recent years. Corporates should select banks with local infrastructure and experts on the ground to interpret regulations (and maintain relationships with regulators) as well as to facilitate control and risk management. Banks’ local knowledge should be combined with global technology, capabilities and connectivity to enable companies to put in place in-house banking arrangements and regional re-invoicing, for example.

Many corporates in the region have high capital expenditure requirements so effective cash and liquidity management capabilities are also important to optimize working capital. Similarly, supplier finance capabilities with robust local onboarding can give companies operating in the region a competitive advantage.

By working with a global bank, corporates can ensure that regional structures are integrated at a global level and that consistent platforms and solutions are used worldwide. Global banks have the technology budgets to develop technology that meets treasury’s needs, including smartphone and tablet apps for treasury management or commercial cards, for example. Similarly, banks with an international presence are better placed to support local companies as they expand globally.

Treasury and Trade Solutions34

Destination of Choice The United Arab Emirates (UAE), which consists of Abu Dhabi and Dubai as well as five other emirates, is the first-choice location for companies seeking to centralize their treasury activities in the Middle East, Africa and even parts of Asia, for myriad reasons. The World Bank’s Doing Business 2015 report ranks the UAE as the 22nd best location worldwide to set up a business, based on a range of measures — from ease of establishing a company and paying taxes to protection for minority investment and access to infrastructure. This is up from 25th place in 2014.

In a region that has witnessed significant change over the decades, the UAE is a beacon of political stability. Its domestic economy is growing rapidly, with growth of 5.2% in 2013,1 while the lessons of Dubai’s 2008 economic collapse appear to have been learned. Crucially, the UAE also has a favorable regulatory environment by regional standards. Furthermore, it has an attractive tax environment, with low personal and business tax and — importantly from a treasury perspective — tax treaties with other countries in the region to facilitate easy movement of funds.

The UAE has a well-educated workforce, with a strong local education system and a large, highly-skilled expatriate community. The UAE’s infrastructure is impressive. Transportation — as well as tourism and logistics, which depend on transportation — is the lynchpin of its economic strategy. Aviation contributes almost 27% of Dubai’s GDP, compared with a global average of just a few percent; by 2020, it is expected to account for 37.5% of GDP.2

Flag carriers Emirates and Etihad are recognized as two of the world’s leading airlines, and it is possible to reach almost anywhere in the world with ease from either Dubai or Abu Dhabi. Passengers can connect from Dubai to 81% of global cities with populations of over 10 million people. It also has direct passenger flight connections to 149 cities with populations of over 1 million people. This represents potential export markets of more than 916 million people, or 13% of the world’s population.3

1 United Arab Emirates National Bureau of Statistics, 6 November, 2014.2Quantifying the Economic Impact of Aviation in Dubai, Oxford Economics, November 2014.3Quantifying the Economic Impact of Aviation in Dubai, Oxford Economics, November 2014.

35Citi Perspectives | Q1/Q2 2015

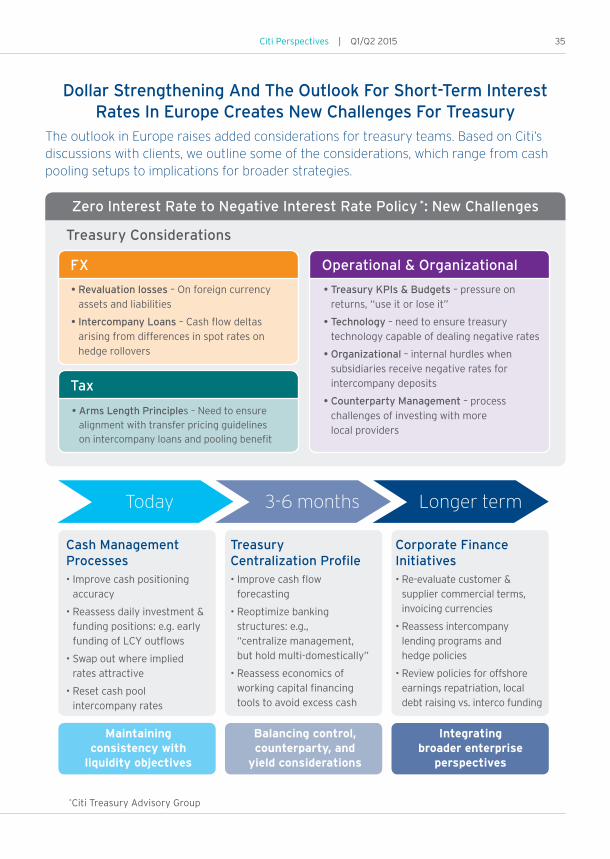

Dollar Strengthening And The Outlook For Short-Term Interest Rates In Europe Creates New Challenges For Treasury

The outlook in Europe raises added considerations for treasury teams. Based on Citi’s discussions with clients, we outline some of the considerations, which range from cash pooling setups to implications for broader strategies.

Treasury Considerations

• Arms Length Principles – Need to ensure alignment with transfer pricing guidelines on intercompany loans and pooling benefit

Tax

• Revaluation losses – On foreign currency assets and liabilities

• Intercompany Loans – Cash flow deltas arising from differences in spot rates on hedge rollovers

FX

Corporate Finance Initiatives•Re-evaluatecustomer&

supplier commercial terms, invoicing currencies

•Reassessintercompany lending programs and hedge policies

•Reviewpoliciesforoffshoreearnings repatriation, local debt raising vs. interco funding

Integrating broader enterprise

perspectives

Today 3-6 months Longer term

Maintaining consistency with

liquidity objectives

Cash Management Processes•Improvecashpositioning

accuracy

•Reassessdailyinvestment&funding positions: e.g. early funding of LCY outflows

•Swapoutwhereimplied rates attractive

•Resetcashpool intercompany rates

Balancing control, counterparty, and

yield considerations

Treasury Centralization Profile•Improvecashflow

forecasting

•Reoptimizebanking structures: e.g., “centralize management, but hold multi-domestically”

•Reassesseconomicsof working capital financing tools to avoid excess cash

*Citi Treasury Advisory Group

Operational & Organizational

• Treasury KPIs & Budgets – pressure on returns, “use it or lose it”

• Technology – need to ensure treasury technology capable of dealing negative rates

• Organizational – internal hurdles when subsidiaries receive negative rates for intercompany deposits

• Counterparty Management – process challenges of investing with more local providers

Zero Interest Rate to Negative Interest Rate Policy *: New Challenges

Treasury and Trade Solutions citi.com/treasuryandtradesolutions

© 2015 Citibank, N.A. All rights reserved. Citi and Arc Design, CitiConnect and CitiDirect are trademarks and service marks of Citigroup Inc. or its affiliates, used and registered throughout the world. The information and materials contained in these pages, and the terms, conditions, and descriptions that appear, are subject to change. The information contained in these pages is not intended as legal or tax advice and we advise our readers to contact their own advisers. Not all products and services are available in all geographic areas. Your eligibility for particular products and services is subject to final determination by Citi and/or its affiliates. Any unauthorized use, duplication or disclosure is prohibited by law and may result in prosecution. Citibank, N.A. is incorporated with limited liability under the National Bank Act of the U.S.A. and has its head office at 399 Park Avenue, New York, NY 10043, U.S.A. Citibank, N.A. London branch is registered in the UK at Citigroup Centre, Canada Square, Canary Wharf, London E14 5LB, under No. BR001018, and is authorized and regulated by the Financial Services Authority. VAT No. GB 429 6256 29. Ultimately owned by Citi Inc., New York, U.S.A.

1309106 GTS26488 04/15