tain stoc - lse home

TRANSCRIPT

Taking stockKath Scanlon, Christine Whitehead and Peter Williams. LSE London.

Understanding the effects of recent policy measures on the private rented sector and Buy-to-Let

EXECUTIVE SUMMARY

PAGE 3

1. Thisreportclarifiestheroleoftheprivaterentedsector(PRS)intheUKandthecontributionmadetoitbytheBuy-to-Letsubsector.ItexploresrecentchangesingovernmentpolicyandhowtheymightaffectthePRS,andmakessuggestionsabouttherolethesectormightbeexpectedtoplayinthefuture.

The Private Rented Sector now 2. The size of the PRS hasmore than doubled in the last 15 years and now accounts for almost one-fifth of all

dwellingsintheUK.Despitepolicyinitiativestoencourageinstitutionalinvestmentthebulkoflandlordsareprivateindividuals,manyowningjustoneunit.Dataaboutlandlordsandtheirfinancialmodelsarepatchyandcontradictory,althoughit isclearthatthosewhomakeaconsciousdecisiontoinvest(andnotalldo)oftendosoasaformof pensionprovision.

3. ThelargestnumbersandhighestproportionsofPRShousingarefoundincentralcitiesandespeciallyinLondon.Tenantsaremorelikelytobeyoung,workingand/ormigrants,althoughincreasingnumbersoffamilieswithchildrenareinthePRS.Largenumbersoflowincomehouseholdsliveinthesector,includingstudentsandhouseholdswhoareoutsidethelabourforceaswellaslowpaidworkers.OveraquarterofPRStenantsareinreceiptoftheLocalHousingAllowance.

4. Atthemomentlandlordsaretaxedattheirmarginaltaxrateontheirrentalincomenetofexpenses,whichincludesinterestpaidonBuy-to-Letloansaswellaswear-and-tearforfurnishedaccommodation.TheUKtreatslandlordsfortaxpurposesratherlessfavourablythanmanyotherdevelopedcountriesintwoways:itdoesnotallowdepreciationnorcanrental lossesbeoffsetagainstothertypesof income.However, therehavebeensignificanttaxchangesrecentlywhichmaymateriallyimpactinvestmentlevelsinthePRSinthefuture.

UK housing tenures 1980-2013

Private rented Social rentedOwner occupied

1981 2013201120092007200520032001199919971995199319911989198719851983

Source:DCLGLiveTable101

The PRS now accounts for almost one-fifth of all dwellings in the UK

PAGE 4

Growth and change 5. ThePRShadbeenindeclinefornearlyacenturywhenitbegantogrowagainveryslowlyfromaround1990.The

necessarypreconditionwasthe1988HousingActwhichputinplacefullderegulationofrentsandtenancies.Thedownturninthehousingmarketandhomeownershiparound1990alsohadsomeeffect.

6. Significantexpansiondidnotoccuruntilthemid-1990sandcanbedatedtoaroundtheintroductionoftheBuy-to-Letmortgageinthemid-1990s.Supplygrewmainlythroughthetransferofdwellingsfrombothowner-occupationandsocialhousing(mainlyviaRighttoBuy),ratherthanthroughnewbuild.Some,althoughbynomeansalltheseadditionalPRSdwellings,werefundedbythenewmortgages.Noneofthegovernmentschemesintendedtoboostinstitutionalinvestmenthadamajorimpactonthesectorasawhole,despitepocketsofinterest.

7. Especiallysincetheturnofthecentury,demandhasgrownrapidly,reflectingtheincreaseinthe‘naturalmarket’forPRS (students,migrants, itinerantprofessionalsandyoungerpeoplemoregenerally).But increaseddemandhasalsocomefromreducedaccesstoowner-occupation(mainlyforaffordabilityanddepositreasons);increasedeconomicuncertainty,especiallyinthelabourmarket;higherdebtamongpotentialfirst-timebuyers;theimpactoftheglobalfinancialmarket;andworseningaccesstosocialrentingforhouseholdswhoarenotinpriorityneed.

8. GiventheincreasesinpopulationandhouseholdsthatareprojectedintheUK,itisalmostcertainthatthedemandforprivatelyrentedaccommodationwillcontinuetogrowoverthenextdecades.TomeetthisdemandthereneedstobecontinuedgrowthininvestmentinthePRS.Assessingtheeffectsofpolicychangerequiresanunderstandingnotjustofdemandbutalsoofthevarioustypesoflandlordinvolvedandtheirdifferentincentivestoinvestinthesector.Theevidencebase is thin. Itsuggeststhatamongprivate landlords,whileBuy-to-Let funding is themostcommonacquisitionmodel,asignificantproportionoflandlordsbuytheirpropertiesoutrightoruseothersourcesoffunding,sometimesinadditiontoBuy-to-Letmortgages.

9. Buy-to-Let lending increased rapidly from its introduction until the financial crisis of 2008/9. In the periodimmediatelybeforethatcrisistherewerelargeincreasesnotonlyintotallendingbutalsointheproportionofBuy-to-Letfinancewhichwasintheformofre-mortgaging.Thiswasalsothecaseformortgagesforhousepurchase.Afterthecrisismortgagecreditofalltypeswasinshortsupplyandotherformsoffinance-includinginparticularowners’equity-supportedtheexpansionofthesector.Buy-to-Letfundinghasnowrevived(althoughnotasmuchasthatforfirst-timebuyers)andre-mortgaginggrewrapidlyin2015,possiblyreflectingdebtmanagementwithin growingportfolios.

New UK Buy-to-Let loans for purchase and re-mortgaging and change in stock of PRS dwellings, 2002-2013

For purchase For re-mortgage Change in PRS stockTotal new loans

2002 2015201420132012201120102009200820072006200520042003

Source:CMLTableMM17andDCLGLiveTable101

PAGE5

Addressing the government’s concerns 10. Overthelastyearthegovernmenthasintroducedanumberofpolicychangesspecifictothesector.Theyinclude

anadditionalpropertyStampDuty(SDLT),areductioninthewearandtearallowancefor landlordsoffurnishedtenanciesandphasedchangesintherateatwhichtaxreliefcanbeclaimedonmortgageinterest,plusamodificationinhowtaxliabilityisassessedandwhencapitalgainsmustbepaid.

11. ThegovernmenthasassertedthatBuy-to-Letinvestorscompeteunfairlywithfirst-timebuyers.Therehasalsobeenalong-termpreferenceamongpolicymakersforarentedsectorownedandmanagedbyinstitutionsratherthanprivateindividualsasameansofbothprovidingfinanceandofprofessionalisingthesector.

12. TheauthoritiesareconcernedaboutthestronggrowthoftheBuy-to-Letmarket,whichisnotregulatedbytheFCA,althoughthedataonthismarketarelimited.Theworrythatlandlordsmightsellpropertiesduringacrisisdoesnotreflecttheexperiencetodateoflandlords’behaviour–duringthelastfinancialcrisiswedidnotseeamasssell-offofproperty.TheconcernsoftheBankofEngland,whowillverylikelybegrantedpowersovertheBuy-to-Letmarket,seemoverdone.

13. WhilethereisclearlysomecompetitionbetweendemandfromBuy-to-Letlandlordsandfirst-timebuyers,theextentofsuchcompetitionvariesenormouslyacross thecountryaswellasbetweenproperty types.The (very limited)researchintodirectcompetitionbetweeninvestorsandputativeowner-occupiershasfoundthatnationwideonlyaminorityofsalesto landlords involvedbidsfrombothtypesofbuyer. Inmanymarketsthere isnomeaningfulcompetition and first-time buyers on modest incomes can readily afford homes. In others—mainly in centralcityareasand innerLondon inparticular—there isstrongdemandfromboth landlordsandprospectiveowner-occupiersespeciallyforoneandtwo-bedflats;elsewherethereislittleevidenceofdirectcompetitionbetweenthesetwoformsofhousingtenure.

14. EveryyearsinceBuy-to-Letmortgageswereintroducedmoreloanshavegonetofirst-timebuyersthanBuy-to-Letinvestorsinallregions,includingLondon.Landlordscanaccessinterest-onlymortgageswhicharemoredifficultforowner-occupierstoobtain.LTVsforinvestorsarelowerthanforfirst-timebuyersandthetermsforwhichtheyareissuedareshorter.Moreover,higherLTVloansforfirst-timebuyersarenowmorecommonandthereisamodestrevivalintheinterest-onlyloanmarket,aswellasafairlysignificantincreaseindemandforlong-termmortgageswhich,inpartseektocreateasyntheticinterest-onlyrepaymentprofile.

15. Theargumentsaboutlandlordbehaviourinadownturnhavebeenbasedonlimitedsurveyevidenceandapparentlywithoutlookingbackatpreviousevents.TheNMGsurveyusedbytheBankofEnglandisageneralhouseholdsurveywhichappearstoincludeadisproportionatenumberofyoungerlandlords.Inmoretargetedsurveyslandlordstendtosaytheyaremorelikelytobuythantosell,whateverthestateofthemarket.InthatsensewejudgethelikelylandlordcontributiontofinancialinstabilityinadownturntobelessthansuggestedbytheBankandthegovernment.Similarly, although institutional investment will help boost the sector and potentially assist professionalisationandhigherstandards, it is importantnottooverstatethecontribution itmightmakerelativetothescaleof the sectoroverall.

The worry that landlords might sell properties during a crisis does not reflect the experience to date of landlords’ behaviour – during the last financial crisis we did not see a mass sell-off of property. The concerns of the Bank of England, who will very likely be granted powers over the Buy-to-Let market, seem overdone.

PAGE 6

Changing the landscape for Buy-to-Let 16. IncreasesinSDLTcanbeexpectedtoreducelandlordpurchasesandturnover.Mortgagetaxchangeswillreduce

returnsformanylandlordsbutarenotexpectedtocausethemtosellupenmasse.Decisionsabouttheroleofresidentialpropertyinoverallportfolioswilldependonreturnsonotherassetclasses,andanyrebalancingwilltakeplaceoveranumberofyears.

17. ThefutureofthePRSwillbedeterminednotjustbyfiscalandregulatorymeasuresbutratherbymanyotherfactors,includingthepromotionofhomeownership(drawinginsomepotentialtenants)andtherelativereturnsfromotherinvestmentsaswellasincreasingpopulationandrealincomegrowth.

18. ThemortgagetaxchangesannouncedwillmostlyimpactprivateindividualinvestorswithsmallportfoliosandBuy-to-Letloans.Thosewhocurrentlypayhigheroradditionalratetaxwillclearlybeaffected.Thewaythatthetaxiscalculatedalsomeanssomelandlordswillbepushedintohighertaxratesand/orloseincome-relatedbenefits.

19. Together thechanges tomortgagetaxreliefandSDLT (andthereduction incapitalgains tax forother typesofinvestmentannouncedintheBudget)willmodifytheincentivestructureforlandlordsbutthescaleoftheimpactonlandlordbehaviourisunclear.Theevidencesuggeststhat,inadditiontonormalturnover,somewillsellanumberorevenalloftheirproperties;somewillreducegearing;somewillpostponeorforegofurtherinvestmentinthesector.Butothersmayfeel it isagoodtimetoenterthemarketorexpandportfoliosasotherlandlordssell.Sothemagnitudeandtimingoftheseimpacts isunknown.Moreover,theeffectonsupplywilldependasmuchonwidermarketandeconomicconditions,includingreturnsavailableelsewhere,asonspecificchangestothetaxation oflandlords.

20. OnthenearhorizonarefurtherregulatorychangessuchasincreasedcontrolsonBuy-to-Letlendingandperhapsthestabilisationofrentincreases,at leastinsomecitiesalongwithanewcapitalweightingsregimeunderBasel3.On29MarchthePrudentialRegulationAuthorityreleasedaconsultationpaperonunderwritingstandardsforBuy-to-Letmortgages.ThiswasimmediatelywelcomedbytheFinancialPolicyCommittee(FPC)whichismonitoringdevelopments in thismarket. The industry still awaits theoutcomeof thecurrentHMTreasuryconsultationonpowersofdeterminationoverbuyto-letmortgagelendingthoughitisassumedthesewillcomeintobeing.TheFPCwillprepareastatementofitspolicyfortheuseofpowersofdirectionaheadofanysuchpowersbeingapproved byParliament.

21. MostimmediatelythereisthefouryearfreezeontheLocalHousingAllowance(27%ofprivatetenantsclaimLHA);theintroductionofacaponwhatcanbepaidoutwhichisnowbitingininnerLondon;andmeasurestoreducethesupplyofsocialhousingatleastintheshortterm.

22. Effortstoencourageinstitutionalinvestmentarebearingfruitand,subjecttothefinalisationofforthcomingchangesin regulationsand taxation,willprobablynotaffect largecompanyorcorporate landlords.At themoment theirincentivetoexpandisthereforeunchanged.However,evenifthissubsectorweretogrowasrapidlyasoptimistssuggest,itwouldstillaccountforonlyasmallproportionofthePRSstock.Ontheotherhandtherewillbesignificantincentives to reduce investment among Buy-to-Let landlords. Given the potential increases in demand forprivatelyrentedhousingfromcontinuedin-migrationandpopulationgrowththiswillfurtherincreasepressuresin themarket.

23. Government initiatives to facilitateowner-occupationcould inprincipleadduptoasmanyas100,000unitsperannumtothestockinthattenure.Notallwillbegenuinely‘additional’,assomeofthehouseholdswhobenefitwouldhaveboughtanyway,butevensotherewillbeanimpactondemandforrentedproperty.Thevariousmeasures,togetherwithwidereconomicanddemographictrends,canbeexpectedtoslowtherateofgrowthofthePRSbutnottoreversetheupwardtrend.

PAGE 7

Renting, owning and policy 24. Willprivaterentingcontinuetogrowatasimilarpaceoverthenextdecades?Thisdependsnotonlyontheeffectsof

fiscalmeasuresandgovernmentpolicytowardsthePRSmoregenerallybutondevelopmentsinothertenuresandinwiderinvestmentmarkets.

25. Private individualsareandwill continue tobe thebulkof landlords,even if institutionsmassively increase theirinvolvement.Theexamplesetbyinstitutions,coupledwithlargerindividualportfoliosandtenantdemand,willtendtoresultinincreasedprofessionalismmoregenerally.

Portfolio size by type of landlord

1 2 - 4 5 - 9 10 - 24 25 - 100 100+

Private individuals Companies Other organisations

Source:PrivateLandlordsSurvey2010

26. Whiletherearereasonstoexpectowner-occupationtogrowat leastamongmaturetraditionalhouseholds it isourviewthatitishighlyunlikelythatyoungerhouseholdswillenterowner-occupationtotheextentthattheydidinearlierdecades.Suchascenarioimpliesthattheproportionofowner-occupationinEnglandcouldgrowtobetween64%and66%ofthetotalstockoverthenextfewyearsandstabiliseataroundthatlevel.

27. Equally, socialhousingmightundersome,perhapsunlikely, circumstances remainat roughly its currentsizeashousingassociationsrespondtothechallengetoexpandwithoutdirectsubsidy.However,itisfarmoreprobablethat itwill decline, especially ifpartialownership starts to takea larger role inaffordablehousingprovision.Anestimatemightbethatitwouldfalloverthenextfewyearstounder15%ofthetotalstock.Indeed,overtime,unlessthere isapolicyreversal, forexample,asaresultofachangeingovernment, itcoulddeclinefurther,toas little as10%.

28. Taken together, these scenarioswould suggest aPRS in the rangeof 20%and22%within thisparliament andperhaps25%asthelongertermequilibriumlevel.Thesearesignificantincreasesespeciallyinabsoluteterms,eventhoughtheyarelowerthanmanyotherprojections.Theyreflectcurrentgovernmentpolicyandanassumptionthattheeconomycontinuestoimprove.Iftheoutlookismorenegative,theproportioninprivaterentingwillbehigher.Butifrealhouseholdincomesrisemorerapidlytheproportioninowneroccupationcouldbehigher,moreinlinewithmatureNorthernEuropeanmarketsthatstillfavourthatsector.Ifso,manyyoungerhouseholdswillcontinuetorent,butthevastmajorityofstableworkinghouseholdswillbeowner-occupiers.

PAGE8

Conclusions 29. Insummary,privaterentingplaysandwillplayakeyroleintheUK’shousingsystem.Itkeepspressureoffthehome

ownershipsectorbyofferinghouseholdsaclearalternativewhetherfortheshortorlongterm.Italsoplaysaroleasanalternativetotheprovisionofsocialhousing.

30. ThecontinuingflowofregulatoryandtaxationchangesbeingintroducedandconsideredwillslowtheexpansionofthePRSatatimewhentherearelimitedalternatives.However,oncurrenttrendsdemandforprivaterentingisalmostcertainlygoingtocontinuetoriseinbothabsoluteandproportionalterms.Thekeyconcerniswhethertherewillbesufficientlandlordstocontinuetomeetthecontinuinggrowthintenantdemand.Anyslowdownintheexpansioninsupplyofprivatelyrentedhousingarisingfromchangesintaxationandregulationwillputpressureonrentsandhouseholdbudgets.

31. Evenifinstitutionalinvestorsenthusiasticallyenterthemarket,individuallandlordswillremaindominant–astheyareacrossEurope.Shrinkingthesectorthereforedoesnotseemasensiblewayforwardgivenwhatweknowaboutunmetdemandandneed.

32. Inanidealworldwecouldidentifythegoalsofpolicychanges,establishabaselineandmonitoroutcomestoseeifthesegoalsweremet.Inthiscasehowever,thegovernment’sgoalsaremultipleandsometimesinconsistentandpoordatamakehighqualitymonitoringdifficultifnotimpossible.Ifwearetounderstandandmanagethesectorbetter,weneedtoimprovethedataasquicklyaspossible.

Chapter 1: Introduction PAGE10

Chapter 2: The private rented sector today PAGE 12

Chapter 3: Growth and change in the private rented sector PAGE 32

Chapter 4: Addressing the government’s concerns PAGE 42

Chapter 5: Changing the landscape for Buy-to-Let? PAGE52

Chapter 6: Where are we going: renting, owning and policy PAGE60

References PAGE 64

Annex 1: How many landlords are there in the UK? PAGE70

Annex 2: Comparing renting and owning PAGE 72

CONTENTS

PAGE9

CHAP

TER

1INTRODUCTION

This report clarifies the role of the private rented sector (PRS) in the UK and the contribution to it through the Buy-to-Let subsector. It explores recent changes in government policy and how they will affect the PRS, and makes suggestions about how the sector can play an effective role in the UK housing system. This chapter clarifies the objectives of the research, the reasons for addressing these issues and the position of the Buy-to-Let market within the overall total rented sector.

InJanuary2016,ParagonGroupcommissionedtheauthorstowriteanindependentreviewofpolicydevelopmentsintheprivaterentedsector(PRS)ingeneralandtheBuy-to-Letmarketinparticular.Theobjectivesofthisstudy,undertakenfrommid-Januarytotheend-February,were:

• first, to clarify the roleplayedby thePRS in theUK (notably England) andhow that rolehasevolvedsincethePRSstartedtogrowinthe1990s;

• second, to identify to the extent possible theBuy-to-Let segmentwithin the broader privaterentalmarket;

• third,tounderstandthedirectandindirectimpactsofgovernmentpolicyinitiativesonthehealthoftheBuy-to-LetmarketandthesustainabilityofthePRSasawhole;

• fourth, tosuggestwhat the implicationsof thesepoliciesare for the futureofBuy-to-Letandprivaterentingmoregenerally;and

• finally, to draw conclusions about what is necessary for the PRS to play an effective role in housingprovision.

The backgroundTheimmediatereasonsforundertakingthisstudyarethechangesintaxationandregulationthatthegovernmenthasannouncedoverthe lastyearandthechangingattitudestoprivaterenting,particularly with respect to Buy-to-Let among policy makers and those responsible for macro-stabilisationandregulation.

AmorefundamentalreasonlieswiththerapidgrowthofthePRSacrosstheUKwhichhasmorethandoubledsincetheturnofthecenturysupportedbytheexpansionoftheBuy-to-Letmarket.MuchofourunderstandingofhowthesectoroperatesisbasedondataandanalysiswhichrefersbacktoearlierinthecenturyandevenfurtherandthesectorhasnotbeenfullytestedinthenewpostGlobalFinancialCrisisenvironment.Thisresearchaimstobringtogetherthebestavailabledatatoclarifyboththecurrentpositionofprivaterenting;itsroleintheoverallhousingmarket;andwhereitmightbeheading.

PAGE 11

Defining private renting and Buy-to-Let Itisimportanttobeclearaboutdefinitionsandtoclarifytheterminologyusedinthisreport.MostpeoplebelievetheyunderstandwhatthePRSis,butforstatisticalpurposesitisoftensimplydefinedasallhousingthatisnotowner-occupiedorsocialrented.Thetermcancoverontheonehandveryshort-termletsandroomslettolodgers,andontheother,propertiesinwhichthesamehouseholdshavelivedfordecadesundercontrolledconditions.SomewoulddefinethePRSasdwellingsletatmarketrents,butthesectorincludesmanypropertieswhererentsarenowherenearmarketlevels--indeedsomePRShousingisrent-free(propertiesprovidedbyparentsfortheirchildren,forexample).Moreover,whilethevastmajorityoflandlordsareindividuals,corporateentities,localcouncilsandhousingassociationsmayalsoownprivaterentedproperty.Thatsaid,themajorityofPRSlandlordsandtenantsarewillingbuyersandsellerswhocontractonthebasisofAssuredShortholdTenancyarrangementswithaminimumsecurityofsixmonths.

TheideaofBuy-to-Letmaysimplybeaboutmotivationamongindividualsandsmallcompanies.Butinpracticethetermcanbedefinedinanumberofdifferentways.Buy-to-Letisoftenusedtorefertoallpropertiespurchasedtoletoutonthemarketbyindividuallandlords,whetherusingequityordebt.Thisdefinitionincludesowner-occupierswho(re)mortgagetheirprincipalhomestobuyarentalproperty,aswellasthosewhohavepaidofftheirmortgage(whateverformittook).Butinthefinancialcontext,andinthecontextoftheissuesgovernmentiscurrentlyconcernedabout,Buy-to-Letreferstoaparticularformofmortgageintroducedinthemid-1990sandbasedonrentalreturns,whichmaybetakenupbyindividualsorcompanies.Inthemainpolicysectionsofthisreport,‘Buy-to-Let’referstothatpartofthemarketcurrentlyfinancedbysuchmortgagesandtothosebuyingandsellingpropertieswithinthissubsector.Originallyabrandname,thetermisnowusedgenerically.

THEPRIVATERENTEDSECTORTODAY

This chapter profiles the private rented sector (PRS) in the UK. Its size has more than doubled in the last 25 years and the sector now accounts for about one-fifth of all dwellings. Despite policy initiatives to encourage corporate investment the bulk of landlords are private individuals, many owning just one unit. Data about landlords and their financial models are patchy and contradictory, though it is clear that those who deliberately invested (and not all did) often did so as a form of pension provision.

The highest proportions of PRS housing are found in cities, especially London. Tenants are more likely to be young, working and/or migrants, though increasing numbers of families with children are in the PRS. The decline in the number of social rented units means many low-income households live in the sector, and about a quarter of PRS tenants receive housing benefit.

Landlords are taxed at their marginal rate on their rental income net of expenses, which at the moment includes interest paid on Buy-to-let Loans. The UK treats landlords for tax purposes rather less favourably than many developed countries in two ways: it does not allow depreciation nor can rental losses be offset against other types of income.

CHAP

TER

2

What is private renting?Theprivate rented sector (PRS) is defined inUK statistics as all renteddwellings not ownedbylocalauthoritiesorhousingassociations.Thusitcomprisesdwellingsownedbyprivateindividualsorcompaniesandrented,generallyatmarketrents,tootherhouseholds.Accordingtothelatestfigures,thePRSmakesup19.6%ofdwellingsinEngland(DCLGLiveTable104).ThePRShouses19%ofhouseholds(DCLG:EnglishHousingSurvey2014/15).ThismakesEnglandbroadlytypicalofEuropeannations(Table2.1)althoughthereisawidespreadoftenurepatterns:GermanyandSwitzerlandhavemuchlargerprivaterentedsectors,whileinSpainandtheNetherlandsthesectorsaremuchsmaller2.

Table 2.1: Private rented sector as proportion of dwelling stock in European countries

Country % of stock Year

Germany 49 2010

France 21 2011

Ireland 19 2011

England 18 2011

Denmark 17 2011

Austria 16 2012

Scotland 12 2011

Spain 11 2011

Netherlands 9 2010

Source:SocialHousinginEurope(Scanlon,WhiteheadandFernandez,eds)

1 Whererelevantinthisdiscussionweexcluderesidentlandlords,asresearchhasfoundthattheydiffersignificantlyintermsofmotivationandbusinessmodelfromotherlandlords(CrookandKemp,2011).

2HoweveritshouldbenotedthatthedefinitionofthePRSvariesconsiderablybetweencountriesanditisoftenaresidualfigure.

PAGE 13

Who is housed in the PRS?Onthewhole,householdsinthePRSaremorelikelytobe

• Young–35%areaged25to34

• Singlesorcouples(althoughtheproportionoffamilieswithchildrenisgrowing)

• Onlower-than-averageincomes

• Migrantsfromothercountries.

Table2.2summarisessomeofthemoreimportantattributesofthesector.Inparticular,itshowsthatprivaterentingis for thoseofworkingageandmainly for thosewhoare inwork. Itplaysa key role inaccommodatinghouseholdscoming into the country from abroad and thosemoving around the country, particularly for job-related purposes.The vast majority of international migrants entering the country move into privately rented accommodation: 74%of thosewhohavebeen in thecountry for less thanfiveyears live in thePRS.Thisonlydrops tobelow50%amongthose who have been here for more than ten years. Overall, 39% of foreign born households are private tenants (Vargas-Silva,2015).

ThePRSalsoplaysanimportantroleinaccommodatingthose,includinghomelessfamilies,whoareunabletoaccesssocialhousing.Suchhouseholdsarenormallyoutsidethelabourforceanddependonhousingbenefittopaytheirrent(Wilcoxetal,2015).

Table 2.2: Characteristics of private tenants in England, 2014/15

Private tenants

Social tenants

Owner occupiers

% % %

Gross weekly household income under £300* 30 58 18

Economic status of head of household

fullorpart-timework 71 38 61 otherinactive 9 22 3 retired 9 30 35 full-timeeducation 5 9 1 unemployed 7 1 0

Household type

couple,nodependentchild(ren) 23 16 44 couplewithdependentchild(ren) 23 16 23 onepersonunder60 20 17 9 othermulti-personhouseholds 14 11 6 loneparentwithdependentchild(ren) 13 17 2 onepersonaged60orover 7 24 16

Ethnicity: Head of household not British or Irish* 23 7 3

Source:EnglishHousingSurvey2013/14;EnglishHousingSurveyHeadlineReport2014/15.*latestavailabledata2013/14.

PAGE 14

Withrespecttotheroleofprivaterentinginmobilitymoregenerally,theEnglishHousingSurveyshowsthataroundone-thirdofprivatetenantshavemovedinthepastyearasagainst11%ofallhouseholds,whiletwo-thirdsofprivatetenantshavebeen in their currentaccommodation for fewer than threeyears. In2014-15,57%ofprivate tenantssaid theyexpectedtobuy—afallfrom61%theyearbefore.However,overthelongertermtheratewasnotsignificantlydifferentfromthe59%ofprivaterenterswhoexpectedtobuyin2008-09(DCLG,2016).

What do they pay?LikesomuchoftheinformationaboutthePRS,thedataaboutprivaterentsareincomplete.Oneofficialsourcegivesanaverage(mean)privaterentinEnglandin2014/15of£775(EnglishHousingSurvey,2014/15).Anothersays£625wasthemedianprivaterentforthesameyear(ValuationOfficeAgency),suggestingthattheaveragefiguresintheEnglishHousingSurveyarepulledupbysomeveryhighrents.

TheEnglishHousingSurveygivesdistributionofrentsbyhouseholdtype.In2013/14(themostrecentyearforwhichthisbreakdownwasavailable)theaveragePRSmonthlyrentforallhouseholdtypesinEnglandwas£763(Table2.3).Multi-personhouseholds(generallysinglepeoplesharing)paidthemost,atanaverageof£1135,whilesinglepersonspaidonaverageabouthalfthat(£563).

Table 2.3: Average monthly rents by household type, all England

2013 / 14 2014 / 15

£ £

Household type

othermulti-personhouseholds 1135

couplewithdependentchild(ren) 797

couple,nodependentchild(ren) 719

loneparentwithdependentchild(ren) 715

one person 563

All private renters 763 775

Source:EnglishHousingSurvey2013/14AnnexTable4.3;2014/15AnnexTable

PAGE15

Thereislargeregionalvariationinrents.ThehighestlevelsarefoundininnerLondon,andthelowestinthenorthofEngland. Table2.4presentsdata forEngland from theValuationOfficeAgency, and forEnglandandWales fromanestate-agencysurveybasedon20,000properties.

Table 2.4: Median and lower-quartile monthly rents by English region

VOA Oct 2014 – Sept 2015

Your Move/Reed Rains December 2015

Area Lower Quartile Median Average

£ £ £

ENGLAND 625

ENGLAND AND WALES 1135 794

London 1,100 1,400 1,251

Inner London 1,300 1,625 -

OuterLondon 995 1,250 -

SouthEast 650 800 766

East 550 656 831

SouthWest 545 650 669

West Midlands 450 550 593

NorthWest 425 525 599

East Midlands 430 525 608

YorkshireandtheHumber 425 498 556

NorthEast 400 475 517

Wales - - 560

Source:ValuationOfficeAgencyPrivateRentalMarketSummaryStatistics2014-15;YourMove/ReedsRainsBuy-to-LetIndexDecember2015

PAGE 16

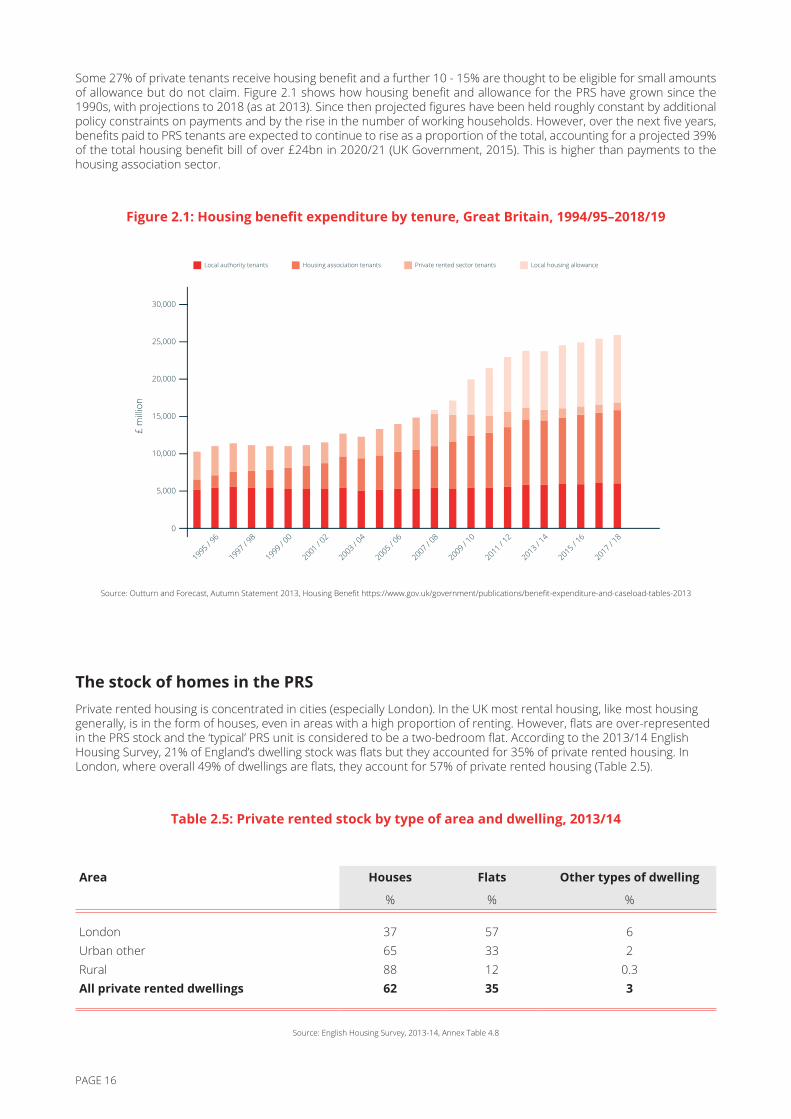

Some27%ofprivatetenantsreceivehousingbenefitandafurther10-15%arethoughttobeeligibleforsmallamountsofallowancebutdonotclaim.Figure2.1showshowhousingbenefitandallowanceforthePRShavegrownsincethe1990s,withprojectionsto2018(asat2013).Sincethenprojectedfigureshavebeenheldroughlyconstantbyadditionalpolicyconstraintsonpaymentsandbytheriseinthenumberofworkinghouseholds.However,overthenextfiveyears,benefitspaidtoPRStenantsareexpectedtocontinuetoriseasaproportionofthetotal,accountingforaprojected39%ofthetotalhousingbenefitbillofover£24bnin2020/21(UKGovernment,2015).Thisishigherthanpaymentstothehousingassociationsector.

Figure 2.1: Housing benefit expenditure by tenure, Great Britain, 1994/95–2018/19

2015 / 16

2013 / 14

2011 / 12

2009 / 10

2007 / 08

2005 / 06

2003 / 04

2001 / 02

1999 / 00

1997 / 98

1995 / 96

2017 / 18

Local housing allowanceHousing association tenants Private rented sector tenantsLocal authority tenants

Source:OutturnandForecast,AutumnStatement2013,HousingBenefithttps://www.gov.uk/government/publications/benefit-expenditure-and-caseload-tables-2013

The stock of homes in the PRS Privaterentedhousingisconcentratedincities(especiallyLondon).IntheUKmostrentalhousing,likemosthousinggenerally,isintheformofhouses,eveninareaswithahighproportionofrenting.However,flatsareover-representedinthePRSstockandthe‘typical’PRSunitisconsideredtobeatwo-bedroomflat.Accordingtothe2013/14EnglishHousingSurvey,21%ofEngland’sdwellingstockwasflatsbuttheyaccountedfor35%ofprivaterentedhousing.InLondon,whereoverall49%ofdwellingsareflats,theyaccountfor57%ofprivaterentedhousing(Table2.5).

Table 2.5: Private rented stock by type of area and dwelling, 2013/14

Area Houses Flats Other types of dwelling

% % %

London 37 57 6Urbanother 65 33 2Rural 88 12 0.3All private rented dwellings 62 35 3

Source:EnglishHousingSurvey,2013-14,AnnexTable4.8

PAGE 17

AccordingtothePrivateLandlordsSurveyaboutthree-fifthsofthedwellingsownedbyprivateindividuallandlordsarehouses(59%)andjustoveraquarterarepurpose-builtflats(Table2.6).Companylandlordsownahigherproportionofflatsbutevenso,overhalftheirdwellingsarehouses.(Itshouldbenotedhoweverthatthesamplesizesforcompaniesandotherorganisationsweresmall—136and131respondentsrespectively.)

Table 2.6: Types of private rented dwelling owned by landlord type (dwelling weighted)

Types of landlord

Dwelling type Private individuals Companies Other organisations

% % %

Terracedhouse 35 23 19

Semi-detachedhouse 14 17 25

Detachedhouse 10 11 28

Purpose-builtflat 27 32 18

Convertedflat 14 17 10

Total 100 100 100

Source:PrivateLandlordsSurvey2010,AnnexTable3.2

Newerunits,especiallyinLondon,areofteninhigh-riseblocks,buttheseareoutnumberedbyconversionsofVictorianhouses.Overall32%ofthePRSinEnglandwasbuiltbefore1919ascomparedto20%ofthetotalstock.EvensotheproportionofPRSunitswhichwerebuiltin1990orlaterishigherthanaverage;theserecentlybuilthomesaccountfor18%ofPRSunitsascomparedto15%oftheoverallstock.Importantlynearly50%ofhousinginEnglishcentralcityareasisprivatelyrented,asis31%ofthestockinthesecentralareastogetherwithotherurbancentres.Thusprivaterentingisfarmoreconcentratedthanothertenuresinareasthatareeasilyaccessibletoworkandleisureactivities.Intheseareasprivaterentingmakesupasignificantproportion,sometimesthemajority,oftransactionsinnewlybuiltstock(ScanlonandWalmsley,2016).

IntheUK,dwellingsaregenerallyownedbyindividualsandsmallcompanieswithasmallnumberofunits,sothateveninahigh-riseblockthatismostlyrentedtherewillbemanydifferentlandlords.Thispresentsaclearcontrasttoothercountries(e.g.,USAandDenmark)wherethetypicaltransactionunitistheentirebuilding.

PAGE18

Who are the landlords?Ingeneralthereisnorequirementforpermissiontobecomealandlord,or(inmostofEngland)toregisteradwellingasrented.Thismeansthatourunderstandingaboutthecharacteristicsoflandlords,orevenhowmanythereare,isrelativelypoor.Extrapolatingfromthe2010privatelandlordssurvey(seebelow)andotherevidencesuggeststhatthemostlikelyfigureisbetween1.5and2million–seeAnnex1.

Thereareanumberofsourcesofdatathatdoprovideindicationsoflandlords’characteristics,attitudesandbusinessmodels,butthedataarefarfromcomprehensive.ThewidelycitedPrivateLandlordsSurveycommissionedbyDCLGeveryfewyearsisinprinciplearepresentativesurvey,butcoversEnglandonly,andlasttime(2010)thesamplesizewaslessthan600.Mostoftheothersurveys(whichoftenemploysimpleonlinesurveytechniques)areconductedbyassociationsoflandlordsoragentsorbylenders,sothereareclearissuesofsamplebias.Table2.7describesthemajorrecentsurveysofEnglishorUKlandlords.

Table 2.7: Characteristics of surveys of landlords

NameDate of

most recent

Frequency Method Coverage Carried out by

Number of responents Comments Regional

breakdown

CouncilofMortgageLenders Buy-to-Letsurvey

2004 One-off Papersurveydistributedtocustomersof12buy-to-letlenders

UK Industrybody 1340 Coveredonlythoselandlordswithamortgage

•

DCLGPrivateLandlords Survey

2010 Periodically(aboutevery4or5years)

Face-to-faceand telephone interviewswithlandlordsandagentsoftenantsfromEHS

England Commissioned bygovernmentdepartment

1051overallo/w599landlords (remainderagents)

Designedtoberepresentativeandstatisticallyvalid,butsmallsample size

BDRCContinental /NLA

December2015–January2016

Quarterly OnlinesurveyofNLAmembers+telephone interviewsofclientcustomers

UK Marketresearchfirm

1364 Contains usefuldetailonbusinessmodels and portfolios

•

ARLA SurveyofResidential Landlords

Autumn2014

Quarterlyfrom2004butnowceased

OnlinesurveyofvisitorstoARLAwebsite

UK Trade association

1016 Canbeusedtotrackmarketsentiment 2004-2014

•

HomeLet October2015

Notstated Notstated UK Onlineestateagency

1882 Focusesonlandlords’relationship withtenants

PropertyAcademyLandlord and Tenants

2015 Annual OnlinesurveyofvisitorstoPropertyAcademywebsite

Notstated Trainingandeventorganisersforpropertyindustry

2313 Focusesonlandlord/agentrelationship

YourMove/Reed Rains

September2015

Quarterly Notstated Estateagencygroup

1192

Mintel Buy-to-LetMortgages2015*

Annual n/a n/a Marketresearchfirm

Cost£1750

*Notpubliclyavailable--forpurchase

PAGE19

AsTable2.7suggests,mostsurveysoflandlordsarenotstatisticallyrobust.Theonlyauthoritative,statisticallyrigorousandrepresentativesurveyoflandlordsistheDCLGPrivateLandlordsSurveyalreadyreferredto.Thishasusefulinformationaboutwholandlordsareintermsofwhethertheyareindividualsorcompaniesandthecharacteristicsoftheirportfolios.However,itwaslastcarriedoutin2010soisnowoutofdate(thesectorinEnglandhasgrownby17%between2010and2014).Thesamplesizewassmall(only599landlords,asopposedtoagents)anditcoversEnglandonly,soitcannotbeusedforanalysisataUKlevelorforregionalbreakdowns.Finally,itcoversahugerangeoftopicsofinteresttothegovernment(e.g.willingnesstolettotenantsonHousingBenefit;useofEnergyPerformanceCertificates)butcontainsrelativelylittleaboutlandlords’financialmodels—therewereonlytwoquestionsaboutmortgages,andBuy-to-Letmortgagesarenotspecificallyidentified.

Theothersurveysmostlyrelyonself-selectionbylandlordswhovisitaparticularwebsiteorusetheservicesofanagencyorassociation,andtheirsamplesarethereforealmostcertainlybiased.TheBDRCsurveysmembersoftheNationalLandlordsAssociationthroughitsso-called‘LandlordPanel’,althoughitisnotclearfromthepublishedmethodologywhetherthisisagenuinepanel(i.e.thesameindividualsquestionedeverytime).

Thebestsourceofdetailedinformationaboutlandlords’financialmodelsandspecificallytheiruseofbuy-to-letmortgagesremainsthe2004CMLstudy(ScanlonandWhitehead,2005).ThiscoversEngland,WalesandScotland.However,itisnowverymuchoutofdate.Itfocusesonthemotivations,businessmodelsandfinancialarrangementsofbuy-to-letlandlords.Welookatthemostrelevantfindingsbelow.Butthisresearchalsohadshortcomings:forinstance,thewordingofthequestionnairedidnotallowusaccuratelytodeterminewhatproportionofeachlandlord’sportfoliowasbackedbyamortgage.

PAGE20

Table 2.8: Findings from surveys of landlords

Name/Date

% owning a single

property

Business modelAverage portfolio (number of units)

Funding method for

next property purchase

% of properties

backed by a mortgage

Reaction to mortgage tax

changes

Main business

(%)

Investment but not

main business

(%)

CML/2004 27 11 89 4 Atleast25%ownedsomeproperties outrightandothersbackedbyamortgage.

DCLGPrivateLandlords Survey/2010

78 56%ofpropertypurchasedbackedbymortgage

ARLA SurveyofResidential Landlords/4Q2014

18

BDRCContinental/NLA/late2015

14 26 57 8.2 BTLmortgage60%Buyoutright29%Releaseequity24%

BTL44%Ownedoutright30%PartBTL/partoutright26%

5%ofrespondentswillreduceportfolio;28%notincrease.Thosewithbiggestportfoliosmostlikelytosell

HomeLet/Oct2015

55 56.5%havemortgagedproperty;43.5%unmortgaged

PropertyAcademy/2015

58 7 52

YourMove/ReedRains/Sept2015

4.5%ofrespondents said decrease inmortgagetaxreliefwouldbeareason to sell

Sources:pertable

PAGE 21

Type of ownerMostprivatelandlordsinEnglandareprivateindividualsorcouples.TheDCLGPrivateLandlordsSurveyisoneofthefewsourcesthatcoverstheentiresectorratherthanfocusingonprivateindividuals.Itshowedthat89%oflandlordswereprivateindividuals,5%companiesand6%otherorganisations(PrivateLandlordsSurvey,2010).

TheWealthandAssetsSurvey (WAS)providesdetailsofhouseholdassets, includingprivaterentalproperty, inGreatBritain.Thesurveyisrunintwo-yearwaves;themostrecent(Wave4)coveredtheperiod2012-2014,andpreliminaryresultswerereleasedinDecember2015(ONS,2015).However,thisgeneralpublicationcontainslittleinformationaboutlandlords,sayingonlythat4%ofthe20,000householdssurveyedownedaBuy-to-Letproperty.

Thereissomeusefulinformationina2013reportbasedonthesecondwave(2008-2010),althoughinevitablyitisnowsomewhatoutofdate(Lordetal,2013).Therewere1274privatelandlordsamongsttheWave2respondents.Thisreportfoundthat72%ofthemownedasingleproperty.HouseholdswithPRSlandlordshadgreaterfinancialwealththanthegeneralpopulationevenexcludingthevalueoftheirrentedproperties,tendedtoliveinlarger-than-averagehomes,andweremorepositiveabouttheiroverallfinancialsituations.Threeinfivethoughtinvestinginpropertywasthesafestwaytomakemoney,andabouthalfthoughtitwasthebestwaytosaveforretirement.Mostlandlords(about60%)saidtheyearnedmoremoneyfromtheirjobsthanfromrentalincome.TheWASquestionnaireasksonlyaboutmortgagesonthehousehold’sprincipalresidence,sothesurveyprovidesnoinformationaboutrespondents’useofBuy-to-Letmortgages.

Companyandorganisationallandlordstendtohavelargerportfolios(Figure2.2),andtogetherown29%ofthestock.Still,thevastmajorityofthestock,71%,isownedbyprivateindividuallandlords.ThePrivateLandlordsSurveyfoundthatthegreatmajorityofprivateindividuallandlordsownedonlyasingleproperty,and97%ownedfewerthanfivedwellings(Figure2.3).Othersurveysshowed lowerproportionsof landlordsowningasingledwelling (Table2.8), ranging from18%to58%,whichmayreflectthegrowthofthesectoroverthelastfewyears.Thisrangeoffiguresdemonstratestheunreliableandpatchynatureofthedataaboutprivatelandlords.

Figure 2.2: Type of landlord by portfolio size

Private individuals Companies Other organisations

10 - 24 Dwellings 25 - 100 Dwellings 100+ Dwellings2 - 4 Dwellings 5 - 9 Dwellings1 Dwelling

Source:PrivateLandlordsSurvey2010

PAGE 22

Figure 2.3: Types of landlord by portfolio size

1 2 - 4 5 - 9 10 - 24 25 - 100 100+

Private individuals Companies Other organisations

Source:PrivateLandlordsSurvey2010

It is difficult to determine howmany large corporate landlords are in the sector, because the statistics are brokendownonlybyprivateindividualsandcompanies,anditisrelativelycommonforevensmalllandlordstoownpropertiesthroughacompany.Thebreakdownoftypesoflandlordbyportfoliosize(Figure2.2)showsthatcompaniesandotherorganisationsaremuchmorelikelythanprivateindividualstohaveportfoliosofmorethan100units.However,itisclearthattherearefewerlargecorporatelandlordsinEnglandthaninsomecountries(USA,Germany).GraingeristhelargestPRSspecialistfirmintheUK,managingabout3600units.

InLondoninparticulartherearemanyforeign,non-residentlandlords.Thenew-buildblocksalongtheThamesinLondonandinlocationslikeGreenwichandCroydonhaveprovedattractivetooverseasbuyers,particularlyfromtheFarEast3. Theytypicallybuyoneormoreunitswithintheblockoff-planthenrentthemoutoncompletion,usinglocalagentstomanagethem.

Formany yearsgovernmentpolicyhasbeen toattract institutional investors to the sector, theargumentbeing thattheywouldprovidemoreefficientandprofessionalmanagementandbetter-qualityaccommodationthaneithersmallerlandlords or professional agents. A small number of institutions have entered themarket,mainly in London. TheseincludeinvestorsfromothercountriessuchasGermanyandtheUSA(e.g.theWashingtonStatePensionFund)morefamiliarwithpurpose-builtrentaldevelopments(knownintheUKas‘buildtorent’).Increasingly,domesticinstitutionsareenteringthemarket(AddleshawGoddardandBPF,2016);MandGforexampleisworkinginpartnershipwithbuildersCrestNicholson,providingupfrontfinancinginreturnforbuild-to-rentproduct.Someanalystssaythat‘awallofmoney’iswaitingto invest inpurpose-builtprivaterentedhousingonceriskandviability issuescanbesorted.However, it isacceptedthatmostwillonlywishtopurchasewholecompletedbuildingsandthereisashortageofsuchinvestmentsavailableespeciallygivenpre-sales.

3Thepreponderanceofforeignbuyersinthesedevelopmentshasgeneratedpoliticalcontroversy,andsomedevelopersnowmarketproductsfirstintheUK.Howeverthelengthoftimebetweenagreeinganoff-planpurchaseandreceivingkeystothedwellingcanbeproblematicforUKbuyerswhorequireamortgage,asmortgageoffersforowneroccupierslastamaximumofsixmonthsbeforetheyrequirereconsideration.OverseascashbuyersdonothavethisproblemnordoUKcashbuyers!

PAGE 23

Age of individual private landlordsLandlords tend tobemiddle-agedandolder,although thesourcesgivedifferentfiguresas to thedistribution;ARLAsurveyfoundveryfewundertheageof35,whiletheWealthandAssetsSurveyshowed16%oflandlordstobeintheyoungercohorts(Table2.9).TheNMGConsultinghouseholdsurveyfortheBankofEngland(seeChapter4)containedresponsesfor342landlords.Theirageprofilewasstrikinglydifferent,with37%oflandlordsagedunder35.Thisseemsimplausibleasarepresentativesampleofthesector,apointwereturntointhatchapter.

Table 2.9: Percentages of individual landlord by age category

ARLA4Q2014

(964 responses)

Wealth and Assets Survey Wave 22008-10

(1274 landlord responses)

NMG household survey for Bank of England

September 2015(342 landlord responses)

Under 26 0.4 1 (18-24yearsold)18

26to35 2.4 15 (25-34)19

36to45 11.7 24 (35-44)18

46to55 27.9 27 (45-54)13

56to65 34.8 22 (55-64)14

Over65 22.8 12 (65orover)18

Source:CareyJones2014;Lordetal2013;NMG2015

Landlord business models

The degree of ‘professionalism’ amongst small private landlords is a topic of some interest given that one of thegovernment’slong-standinggoalsistoincreaseprofessionalisminthesector.TheforthcomingchangestoStampDutyLandTax(seeChapter4)wereoriginallyexpectednottoapplytocompanylandlordswithportfoliosofatleast15units,implicitlysuggestingadefinitionofprofessionalism(althoughintheeventitwasdecidedthatalllandlords,eventhosewithlargeportfolios,wouldpaytheadditionaltax).Butalthoughseveralofthesurveysaddressthisquestiontheyalluseslightlydifferentconcepts:someaskwhetherlandlordsthemselvesconsiderthemselvestobeprofessionals;someaskwhetherbeingalandlordisapart-timeorfull-timejob;someaskhowmuchresidentialrentcontributestolandlords’householdincome;andsomeaskwhatthelandlord’smotivationforbeinginthesectoris.TheARLAsurveyfoundthat70%ofrespondentsconsideredthemselves‘professional’landlords(CareyJones,2014).ScanlonandWhiteheaddefinedprofessionalsasthosewhoreceivedrentalincomeequaltoatleastthenationalaverageincomeandcouldliveofftheirincomewithoutsellingproperties to realisecapitalgains.Applying thismethod to theCMLsurveydata theydefined20.5%ofrespondentsasprofessionals(ScanlonandWhitehead,2005).

PAGE 24

Asnoted,landlordshavemanydifferentreasonsforbeinginthesector.Althoughinvestmentreasonsdominatebynomeansallofthesereasonsrelatetofinancialgain(Figure2.4).

Figure 2.4: Purpose of owning rented dwellings by landlord type

An investment pension

Future home for self / family

Future home for relative / friend

A property I'd like to sell but can't

Other

Incidental to another activity

My current home

Somewhere to housean employee

Somewhere to housepeople in need

Other organisations Companies Private individuals

% of dwellings owned by each landlord type

Source:PrivateLandlordsSurvey2010

Some21%ofthedwellingsownedbyindividuallandlordsarepropertieswherethelandlordthemselvesusedtolive,andthelandlordstill lives in2%of individual-ownedPRSdwellings(PrivateLandlordsSurvey2010).Althoughgovernmentpolicyseemstobepredicatedontheideathatcorporatelandlordsaremorebusiness-likethanindividuals,companiesandotherorganisationsoftendidnotconsidertheirPRSholdingstobeabusinessandhadothermotivationsforbeinginthesector,inparticulartohouseemployees(Figure2.4).Smallprivatelandlordsaremostlikelytoviewtheirdwellingsasinvestmentsorcontributionstopensionprovision.

‘Other organisation’ landlords were more likely to be interested in taking an income out of their properties, whilecompaniesandprivateindividualswerelookingforacombinationofincomeandcapitalgrowth.Thoseinterestedonlyincapitalgrowthweremuchmorelikelytobeprivateindividualsthanothertypesoflandlord(Figure2.5).TheARLAsurveysuggestedthatalmostallrespondentshadfinancialmotivationsforbeingalandlord.Some45%wereseekingcombinedrentalincomeandcapitalappreciationfromtheirresidentialinvestments,32%wereseekinglong-termcapitalgainsand13%werelookingmainlyforarentalyield.

PAGE25

Figure 2.5: Type of return sought by landlord type

Both

Income only

Capital appreciation only

Other organisations Companies Private individuals

% of dwellings owned by each landlord type

Source:PrivateLandlordsSurvey2010

Figure 2.6: Will be in the sector in…

Private individuals Companies Other organisations

Two years’ time Five years’ time Ten years’ time

Source:PrivateLandlordsSurvey2010

Privatelandlordsinthemainhavearelativelylong-termcommitmenttothesector(Figure2.6).Aboutfouroutoffivecompaniesandotherorganisationsexpecttobe inthesector intenyears’ time,andevenforprivate individualsthefigurewascloseto60%.Thisisnodoubtdueinparttotheilliquidnatureofpropertyinvestments,andtothehigh(andincreasing)transactionscostsassociatedwithsale.Arguably,however,itisbecauseformanythereasonforinvolvementinproperty(usuallyinadditiontoowner-occupation)isthattheyarelookingtohelppayfortheiroldage.

PAGE 26

There isevidencethatahighproportionofprivate landlords invest inrentedpropertypartlyorentirelyasa formofpensionprovision—eithertoprovideanincomestreaminretirementorwiththeintentionof ‘cashingin’ theunitstoprovideacapitalsum.Suchinvestmentreflectstheperceivedsafetyandhighreturnsfrompropertyinvestmentand(inrecentyears)thefreeingupofpensionsavingsforinvestmentandthereductioninthecaponstandardpensionsavings.

Reasons for investing in property as pension

TheWealthandAssetssurveyhasconsistentlyshownthatrespondentsviewpropertyinvestmentasthesecondsafestwaytosaveforretirement,afteremployerpensions.In2014/15about40%ofrespondentsthoughtemployerpensionswere safest, while 27% chose property (Figure 2.7). The shares for other asset classes including stocks and shares,personalpensionsandISAswerewellunderhalfthefigureforproperty.

Figure 2.7: Which option do you think would be the safest way to save for retirement? Great Britain, 2010 to 2015

Employer pension

Personal pension

Stocks and shares

Property Savings account

ISA Premium bonds

Other

July 2008 to June 2010 July 2010 to June 2012 July 2012 to Dec 2012 Jan 2013 to June 2013

July 2013 to Dec 2013 Jan 2014 to June 2014 July 2012 to June 2014

Source:WealthandAssetsSurvey,OfficeforNationalStatistics

Whilerespondentsthoughtemployerpensionswerethesafestwaytosaveforretirement,theyexpectedthehighestreturnsfromproperty.In2014/15nearly45%ofrespondentsexpectedthatpropertyinvestmentwouldmakethemostoftheirmoney,comparedto25%foremployerpensions.Fewerthan10%ofrespondentsthoughtotherassetclasseswouldprovidethebestreturns(Figure2.8).

PAGE 27

Figure 2.8: Which do you think would make the most of your money? Great Britain, 2010 to 2015

Employer pension

Personal pension

Stocks and shares

Property Savings account

ISA Premium bonds

Other

July 2008 to June 2010 July 2010 to June 2012 July 2012 to Dec 2012 Jan 2013 to June 2013

July 2013 to Dec 2013 Jan 2014 to June 2014 July 2012 to June 2014

Source:WealthandAssetsSurvey,OfficeforNationalStatistics

Recentchangesinthepensionsystemitselfhaveresultedinincreasedopportunitiesforover-55stoinvestinproperty,aswellascreatingincentivesformiddle-tohigher-incomeindividualsofallagestodoso.TheApril2015changesthatallowedsaversaged55oroverfullaccesstotheirpensionspermittedthere-allocationofthesesavingstoproperty.Itwaswidelyforecastatthetimethatthiswouldresultinamini-boomofBuy-to-Letinvestmentbypensioners,althoughwelackthedatatodeterminetheextentofthis.Inaddition,thereductioninthelifetimecaponoverallpensionsavingsto£1millionfrom2016willaffectnotonlyhighearnersbutalsomanyindividualsonrelativelymodestincomes.Propertyinvestmentisoneofthetwomainalternativesforthosewhowanttoincreasetheirpensionprovisionbutareaffectedbythecap(theotherbeingstocksandshares,whetherheldinISAsornot).

Extent of investment in property as pension

RhodesandBevanfoundin2002and2003thatalmostallpart-timelandlordsinterviewedregardedtheirpropertiesasaformofretirementplanning(RhodesandBevan,2003).Theysawrentalpropertyassuperiortotraditionalpensionsbecauseitwasmoreflexibleanddidnotrelyonstock-marketperformance.‘Whilstasmallnumberoflandlordssawthevalueinhavingaspreadofdifferenttypesofinvestment,mostweredisillusionedwithstocksandsharestotheextentthattheyhadeithercompletelydivestedthemselvesofsuchinvestments,orregardedthemasbeinginconsequentialtotheirfutureplans’(RhodesandBevan,2003,p.37).

AccordingtothePrivateLandlordsSurvey2010(p.14),80%ofindividualprivatelandlordsseetheirpropertiesas ‘aninvestment/pension’. This figure was not broken down further, but other surveys have attempted to tease out thedifferences.Theygivewidelyvaryingresults,probablybecauseofthedifficultyofseparatingmoregeneralinvestmentmotivesfromspecificpensionmotives,bothinthewordingofsurveyquestionnairesbutalsoconceptually.The2004CMLsurveyfoundthatthesecondmostcommonmotivationforinvestinginpropertywasasacontributiontopensionprovision,withaboutaquarterofrespondentscitingthisastheirreason.Afurther52%listedmoregeneralinvestmentmotives,whichwouldnotbe inconsistentwith futureuse forpension (ScanlonandWhitehead2005).AndaccordingtotheBDRCLandlordsPanelin2012,81%ofrespondentssaidtheirpropertiesweretheirpensions.Three-fifthssaidtheyplannedtoliveofftherentalincome,whileaquarterplannedtosellsomeoralloftheirpropertiesaspartoftheirretirementplan(Long,undated).

PAGE28

Anumberofone-off surveyshavebeen commissionedon this issuebynewsmediaand rental-property specialists.Theseprovidesomeusefulindicators,althoughtheyshouldbeinterpretedwithcaution.Theevidencetheyprovideismixed:a2015surveybyHomeLet,forexample,foundthat‘pensioninvestment’wasamotiveforonly5%ofrespondents,whileapollcommissionedbyTheObserverreportedin2013thatonepersoninthreeplannedtoreceiveretirementincomefromoneormorebuy-to-letproperties(Wright2013).A2014surveyof500Buy-to-LetinvestorsbyPlatinumPropertyPartnersfoundthatonaveragetheyexpectedayearlyincomeof£19,785fromtheirrentalproperties,whichwouldmakeupmorethanhalfoftheiroverallretirementincome(PlatinumPropertyPartners,2014).

Private landlords: taxation, regulation and supportPrivatelandlordsaresubjecttoincometaxontheirrentalincome,StampDutyLandTaxwhentheypurchaseapropertyandcapitalgainstaxwhentheysell.Theproposedchangesinarrangementsfortwoofthese—incometaxandStampDutyLandTax—aredealtwithinsomedetaillaterinthisreport.

Income tax

Currently,privatelandlordsaretaxedattheirmarginaltaxrateontheirrentalincomenetofanyrelatedexpenses.Eligibleexpensesincluderepairandmaintenance,agencyfeesandmortgageinterestpayments.Incontrasttomanycountriesthereisnodepreciationofrentalproperty,althoughlandlordswhorentfurnishedpropertiesarecurrentlypermittedtodeduct10%oftheannualrentasa ‘wearandtear’allowance,withouthavingtodemonstrateanyexpenditureonrenewals—ineffecta formofdepreciation.Rental lossescanbesetagainstotherrental income,butnotagainst thelandlord’sincomefromothersources.

There are three ratesof income tax: 20% (on taxable incomeup to£31,785 in 2015/16), 40% (on incomebetween£31,786and£150,000)and45%(onincomeover£150,000).Rentalincomeisaddedtolandlord’sincomefromothersources,suchassalariedemployment,toarriveatafigurefortotalincome.Thegovernmenthasannouncedplanstolimitthedeductibilityofmortgageinterestpayments,whichwillhavetheeffectofincreasingtheincome-taxliabilityofBuy-to-Letlandlordswhopayhigheroradditional-ratetax,andofsomebasic-ratetaxpayers.Thewear-and-tearallowancewillalsobelimitedtoreceiptedexpenditures.ThesechangesarediscussedindetailinChapter4.

Table2.10comparesincometaxtreatmentofresidentialrentalincomeintheUKandothermajorcountries.Itshowsthatevenbeforetheforthcomingchanges,landlordsaretreatedlessfavourablyfortaxpurposesintheUK.Themaindifferencesarethat‘negativegearing’(offsettingofrentalincomeagainstincomefromothersources)isnotpermittedintheUK,andthatthereisnoformaldepreciationallowance.

PAGE29

Table 2.10: Income tax treatment of residential rental income in various countries

Mortgage interest

deductible

Lower tax on rental income

Costs deductible

Depreciation allowance

Rental losses offset against other types of

income

UK • * ••

***(wearandtearfurnishedonly)

Australia • ••

newpropertiesonly

•

Belgium • • • •

Denmark • • institutionsonly • •

France•

butcannotlead to loss

• • uptolimit

Germany • • • •

Ireland • 75% • •

NetherlandsBusiness • • • • •Non-business **

Spain • • • •

Switzerland • • • •

USA • • • • withlimits

Colourkey:

TaxtreatmentsimilartoUK

LandlordstreatedmorefavourablythaninUK

LandlordstreatedlessfavourablythaninUK

*Exceptfor‘rent-a-room’allowance **Animputedreturnof4%ofnetwealthistaxedatarateof30%--i.e.effectiveincometaxrateof1.2%ofequity

***Wearandtearallowanceof10%ofnetrentforfullyfurnishedaccommodation

Source:DerivedandupdatedfromKochanandScanlon,2011Table4

Stamp Duty Land Tax

LandlordspurchasingpropertyhaveuntilrecentlypaidthesameStampDutyLandTax(SDLT)asanyotherbuyer;withnodistinctionmadebetweentypesofowner.RatesofSDLTdependedonthevalueofthedwelling.For‘bulk’purchases(say,100unitsinasinglebuilding)thetaxiscalculatedbasedonthemedianpriceperunitratherthanthetotaltransactionvalue(whichwouldsubjectsuchbuyerstothehighesttaxrate).Thegovernmenthasannouncedthatthosepurchasingapropertythatisnotforuseastheirprincipalresidence(thatis,landlordsandsecond-homebuyers)willpayanadditional3%inSDLTfromApril2016.ThisisdiscussedinChapter4.

PAGE30

Capital gains tax

Whenalandlordsellsapropertytheymustpaycapitalgainstaxof28%onthedifferencebetweenthesalevalueandtheoriginalpurchasevalue,adjustedforinflation.Theratedoesnotdependonhowlongthepropertywasheld.

Subsidy

There are no subsidies or incentives offered to small private landlords for investment in or improvement in theirproperties,apartfromthoseavailabletoallpropertyowners(e.g.theutilitycompanies’greencommitment,providingfreeinsulation).Institutionalinvestorshavebeenabletoavailthemselvesofthegovernment’sBuildtoRentfundandtheBuildtoRentguaranteescheme(seeChapter3),designedtosupportthedevelopmentoflarge-scalepurpose-builtrental-onlyblocksinsingleownership.

Rental support

Privatelandlordsreceive£9bnplusofindirectgovernmentsupportthroughLocalHousingAllowance(LHA),thesubsidyforlow-incometenantslivinginthePRS.Thisiscommonlyknownashousingbenefit(HB),althoughstrictlyspeakingHBisthesubsidyforsocialtenants.)LHAsubsidiesarebasedon30thpercentilerentsinthelocalarea,andaresubjecttoanationwidecapthatdependsonthesizeofthedwelling.

Regulation

There isno regulationof rent levelsor rent increases, except indirectly through theoperationof theLocalHousingAllowance.ThestandardformoftenancyisanAssuredShortholdTenancy,whichusuallylastssixortwelvemonths.Thelandlordcanrequirethetenanttoleavewithtwomonths’noticeattheendofthetenancy,oratanytimethereafter,withoutgivingareason.ThereareotherformsoftenancythatgivetenantsmoresecuritybutsomeBuy-to-Letlenderswillnotpermittheirborrowerstousethem—thoughthisischangingundergovernmentandmarketpressure.

OwnersofHouses inMultipleOccupation(generallythreeormoreunrelatedadults living inahouse—althoughlocaldefinitionsvary)mustregisterwiththeirlocalauthorities.ScotlandandWalesrequirealllandlordstoregister,asdoanincreasingnumberoflocalauthoritiesinEngland.ExceptforHMOs,propertiesarenotroutinelyinspectedevenifthereisaregistrationscheme.

Landlordsareobligedtocomplywithanumberofsafetystandardstodowithfireprevention,gassafety,etc.Alsofromthisyearlandlordswillberequiredtoverifytenants’eligibilitytoliveintheUK.

ConclusionsThischapterhasgivenanoverviewofthecurrentpositionofthePRSintermsofwholivesinthesector;whoinvests;howgovernmenttreatshouseholdsandlandlordsinthesectorandtheoutcomesintermsoftypesandlocationsofpropertiesandtherentscharged.Itpointsouthowmuchofthispicturedependsonsurveyswithdifferentpurposesandsamplesizes.Theresultisajigsawwhichsuggestsclearvariationsbetweengroupsinthesector,bothlandlordsandtenants,andbetweenthoseinthePRSascomparedtoothertenures.However,itcanonlybeindicativeofdetailsparticularlyabouthowthesectorischangingasitbecomesthesecondlargesttenure.Inparticulardatarelatingtotherapidriseinthesectoroverthelastfewyearsispatchyatbest,asisdetailedevidenceonlandlordportfolios,indebtednessandlongertermobjectives.

PAGE 31

GROWTHANDCHANGEINTHEPRIVATERENTEDSECTOR

The private rented sector (PRS) had been in decline for nearly a century when it began to grow again in the mid-1990s. The necessary precondition was the 1988 deregulation of tenancies and rents, but the turnaround can be dated to the introduction of the Buy-to-Let mortgage in the mid-1990s. Supply grew mainly through the transfer of dwellings from both owner-occupation and social housing (via Right to Buy), rather than through new build. Some though by no means all PRS dwellings were funded by the new mortgages. None of the government schemes intended to boost institutional investment had a major effect on the sector as a whole, despite pockets of interest.

Demand has grown, reflecting the increase in the ‘natural market’ for PRS (students, migrants, itinerant young professionals) but also reduced access to owner occupation (mainly for affordability reasons) and social housing. Given the increases in population and households that are projected in the UK, it is almost certain the demand for privately rented accommodation will continue to grow over the next decades. To meet this demand there needs to be continued investment in the PRS

Assessing the expected effects of policy changes requires an understanding of the various types of landlord. The evidence base is thin. It appears that while Buy-to-Let funding is the most common acquisition model, a significant proportion of landlords (around one third) own their properties outright or use a mix of funding.

One reason given for policy changes is to reduce the competition between Buy-to-Let landlords and first-time buyers. The nature and extent of such competition varies enormously across the country. In some markets there is no meaningful competition and first-time buyers on modest incomes can easily afford homes while in others—London particularly—there is strong demand from both landlords and prospective owner-occupiers for particular types of dwelling, especially two-bed flats and houses.

CHAP

TER

3

ThischapterexploresthegrowthofthePRSsincethe1990sandthereasonsforthatgrowth.Itsetstheexpansionofthesectorwithinthecontextofothertenuresandconsidershowthesectorhasrespondedtorisingdemandandstaticsupplyinmanyareas.Itconsidershowvariousfactorshaveshapedthecurrenttenuremixandprovidesindicationsofhowthatmixmightdevelopinfuture,particularlyinlightofgovernmentpolicyinitiatives(towhichweturninChapters5and6).

Startingin1945whenthesectoraccountedformorethan50%ofdwellings,thesizeofthePRSstockintheUKfellconsistentlytoaround8%inthelatterpartofthe1980s.Thesectoratfirstgrewslowlytoaround9%attheturnofthecentury,thenitsexpansionaccelerated.By2013itaccountedfor18.5%ofalldwellings in theUK,2.2 times theproportion in2000andalmost2.5 times theproportionin2008.

PAGE 33

Conditions for growthWecanidentifyfourprincipalsupply-sidedriversofthegrowthofthePRSfromthe1980s.ThefirsttwoweretodowiththePRSitself:theremovalofrentcontrolandlong-termtenuresecurityinthe1980sandthecreation,withtheBuy-to-Letmortgage,ofadedicatedfinancechannelforsmallinvestorsinthelate1990s.Thethirdwasthelong-termimpactoftheRighttoBuyforcounciltenants.Thetransferofdwellingsfromsocialtoprivateownershipreducedthesupplyofcouncilhousingastherateofreplacementdidnotkeepplacewithsales, leadingtoanincreaseindemandforPRShousing.Also,ahighproportionofdwellingssoldundertheRighttoBuyeventuallyendedupinthePRSastheoriginalownerseithermovedelsewhereandrentedthemout,orsoldtoinvestors(Murie2015).Thefourthsourceofsupplyhasthemoveofunitsfromowner-occupationtoprivaterental,insomecasesbecauseowner-occupiersmovedonandkeptthepropertytorentout,andinothersbecauselandlordsoutbidotherpurchasersforexistingdwellings.Sincetheturnofthecenturythenumberofowner-occupiedunitshasincreasedslightly,butasaproportionofdwellingsowner-occupationhasdeclinedfrom69%in2000to63%in2013.Inthesocialsector,absolutenumbersfellbymorethan400,000unitsoverthesameperiodandfrom22%to18%ofthetotalstock(DCLGLiveTable101).

Increased demand for PRS housing has come both from positive reasons (desire for easy-access, short-termaccommodation) andnegativeones (problemsofaffordability andaccess tofinance forowner-occupation, and longwaitinglists,allocationrulesthatfavourprioritygroupsandlackofsupplyinthesocialsector).Figure3.1showsthatinEnglandthenumberofdwellingsinprivaterentaloutstrippedthoseinsocialrentalfromaround2011.InAnnex2FiguresA.2.1andA.2.2givesimilarinformationforhouseholds.

Figure 3.1: UK housing tenures 1980-2013

Private rented Social rentedOwner occupied

1981 2013201120092007200520032001199919971995199319911989198719851983

Source:DCLGLiveTable101

PAGE 34

The1988HousingActmarkedarealstepchangethatprovidedthenecessaryconditionsforgrowth.Themainprovisionswere to introduceanalternative to the indefinite tenancy, and to removeboth controlson initial rents andon rentincreases for existing tenants. The 1988 Act also completely deregulated the PRS in terms of rents and security. Itabolishedrentregulationfornewleasessignedfrom1January1989.Landlordswerepermittedtochargefullmarketrentandtoincreaserentsassetoutintenancyagreementsratherthanbyanamountspecifiedbystatute.However,tenantscouldapplytotheRentAssessmentCommitteeiftheyfeltincreasesweretoohigh.Existingtenanciesbegunbefore15January1989werestill‘regulatedtenancies’(subjectto‘fairrents’).The1988Actalsointroducedtheassuredshortholdtenancy (aminimumsix-month tenancywithno further securityof tenure) and required landlords togive tenantsaminimumoftwomonths’notice.

The government introduced an important short-term tax advantage to the PRS in 1988. It extended the BusinessExpansionScheme,whichgaveincentivestosmallinvestorstogetinvolvedinmoreriskybusinessstart-ups,tolandlordsofnewlyconstructeddwellings letonassuredtenanciesfortheperiod1988-1993.Duringthatperiodsome81,000dwellingswereaddedtothePRSstock,althoughahighproportionoftheunitsprovidedwereonlyavailabletostudents(Crooketal,1995;Hughes,1995).

In1997theassuredshortholdtenancy(AST)becamethedefaultformoftenancyinthePRS.TheASTpermitsthelandlordtoregainthepropertyfromtenantswithtwomonths’noticeattheendofthelease(usually6or12months)oratanytimethereafterwithoutrequiringareason.Nowlandlordshadcertaintythattheycouldchargeamarketrentandgetpropertybackfromtenants,whichsignificantlyreducedtheriskofletting.

TheverylimitedsecurityoftenureintroducedbytheASTtogetherwithincreasingcompetitionamongmortgagelenderscreated theconditions for themortgage industry to lendmoreeasily toprivate landlords.Followinga1994 initiativeby theAssociationofResidentialLettingAgents, theBuy-to-Letmortgagebecameavailable from July1996 toprivatelandlordstopurchasepropertytolet.Theloanswereusuallyinterest-only,basedonprojectedrentalincome,withloan-to-valueratiosofupto85%andinterestrateslittleabovethoseforowner-occupiers(Rhodes,2006;Ball,2004).

In1980thePRSconsistedofsome2.1millionunits,somewhatlessthan12%ofthetotalstock.In1996thenumberofunitswasalmostexactlythesame,butmadeuponlyjustover10%ofthestock.However,intheinterimtherehadbeenfurtherdecline,toaslowas1.8mhomesinthemid-1980s,andthis losswasonlyslowlyoffsetfromtheearly1990s.Eventhen,CrookandKemp(1996)pointedoutthathalfoftheexpansionduringtheearly1990scouldbeexplainedby ‘property slump landlords’ whowere unable or unwilling to sell at that time because of the state of the owner-occupiedhousingmarket.Thusthelargegrowthinthesectorcomesafterthemid-1990swhenBuy-to-Letmortgages becameavailable.

Importantly,anincreaseofonlysome300,000unitsfromthelate1980stotheturnofthecenturydoesnotsuggestthatthesystemwasfunctioningwell.Afterthe1989/90housingcrisisnearlytwomillionhomeownerswereinnegativeequity;owner-occupationratesamonghouseholds intheirtwentiesweredroppingrapidly;andthePRS increasinglyhousedthosewhowouldtraditionallyhavebeeninthesocialsector.ThesefactorsallcontributedtothegrowthofthePRSduringthattime.Butalthoughthetrendshadbecomeclear,theadjustmentprocesswasslow.

Policies to stimulate institutional investmentSincederegulation,amajorfocusofgovernmentpolicyhasbeentostimulatethesupplyofprivaterentaldwellingsbyinstitutionsratherthanindividual investors,eventhoughthelatterdominated–andcontinuetodominate–thePRS.InadditiontotheBESschemementionedabove,HousingInvestmentTrusts(HITs)wereintroducedin1996inordertobringpensionandother long-termfunds intoprivatelyrentedhousing, includingexisting lettings (Crook,etal.,1998;CrookandKemp,2002).However,majorinvestorsdidnotseethemasworthwhileandnoHITshadbeensetupby2010.

Theintroductionin2005oflegislationtoallowUKRealEstateInvestmentTrusts(REITs)basedontheUSmodelmadeitpossibletocreateliquidandpubliclyavailablepropertyinvestmentvehiclesforsaletoawiderangeofinvestors.Theaimwastoencourageinstitutionalandprofessionalinvestmentinbothcommercialrealestateandprivatelyrentedproperty(BallandGlascock,2005).UK-REITshavebeenallowedtooperatesinceJanuary2007.Mostinvest incommercialandretailproperty,althoughasmallnumberalsoinvestinrentalaccommodation.AsyetonlyaveryfewREITsinvestsolelyinresidentialproperty.

PAGE35

Thepolicygoalofattractinginstitutional investmentintoprivaterentalhousingonceagaincametotheforeafterthe2010changeofgovernment.TheMarch2011Budgetcontainedasetofmeasuresaimedatcreatingamoretax-efficientapproachtolargescaleinvestmentthroughREITs(StephensandWilliams,2012).However,ofthemselvesthesechangesdidnot stimulatean incrementalflowof institutional investment intonewhousingbuilt specifically for rent.Afteranindependentreviewofwaystoattractinstitutionalinvestmentintothesector(Montague,2012),thepolicypriorityshiftedtothedevelopmentofanew‘BuildtoRent’scheme.Thistermdescribeslarge-scalepurpose-builtrental-onlyblocksthatareinsingleownership,anindustrymodelcommoninmanyEuropeancountriesbutnotseenintheUKsincethe1930s(PawsonandWilcox,2013;Scanlonetal.,2013).ThefirstgroupofBuildtoRentprojects,announcedon16April2013,willcontainupto10,000newhomes.Inadditionthegovernmentannounceda£10billiondebt-guaranteeschemetosupportnewBuildtoRentdevelopmentsintheUK(Bate,2015).Overall,thesetwomeasuresaimedtoreducethecostsandriskoffinanceatdifferentstagesofdevelopmentandownershipofnewprivaterentaldwellings.

Despitetheseefforts,theroleofinstitutionalinvestorsinthePRSisstillnegligible.Mostoftheinstitutionalinvestmentsinlarge-scalerentedhousingareinLondon.ArecentsurveyofinstitutionalinvestorsbytheInvestmentPropertyForumsuggested that of a total £180 billion in property assets held by 42 institutions, only four per centwas invested inresidential,andofthatlessthanhalfwasinPRSassets(IPF2014).Thiswasanextremelysmallamountcomparedtothetotalestimated£2.7trillionundermanagementbyUKinstitutions(CBI,2013).

Anumberofstudieshave lookedatwhy institutional investorshavenotbecomesignificantplayers in theresidentialpropertymarketandhavegenerallyidentifiedacommonsetoffactors(Daly,2008;HMTreasury2010;Hulletal.,2011;Scanlonetal.,2013):

• thedifficultythatdevelopersofPRS-specificbuildingshavecompetingforlandagainstowner-occupation;

• ashortageofdevelopmentfinance;

• lowrisk-adjustedyields;

• lackofinvestorexperienceinthesectortogetherwithverylimitedperformancedataonwhichtobasedecisions;

• theneedforscale:Savills(2014)commentsthatthedearthoflarge-scalepurpose-builtprivaterentalstockandtheoperationalplatformstorunthemisthemainbarriertoinvestorsinPRS(seealsoMilliganetal.,2013);

• negativeinvestorandlocalgovernmentattitudestothesector:ithasbeensuggestedthatsomelocalauthoritieshavenotadoptedthepro-growthapproachoftheNationalPlanningPolicyFrameworkandhaveblockedthesupplyofnewhousingintheirareas(CBI,2013);

• poorqualityandexpensivemanagement;

• reputationalrisk;and

• uncertaintiesaroundtheregulatoryandtaxationregimes.

Continued increasing demand - and how it has been metSowherehasthegrowthfromthemid-1990scomefrom?

RuggandRhodes,ina2008reportforDCLG,identifiedthemostimportantfactorsgeneratingdemandforprivaterenting(RuggandRhodes,2008).Theywere:

• growthinstudentnumbers;

• increasedinwardmigration;

• higherlevelsofrelationshipbreakdown;

• increaseddemandthatwouldotherwisehavebeencateredforinthesocialrentedsector;

• growthinthenumbersofyoungertenantsrentingfor‘lifestyle’reasons;and

• increasingaffordabilityproblemsforthosewantingtoaccesshomeownership.

PAGE 36

Someoftheseelementsofdemandarisefromchoicewhileotherareclearlyconstraintsstoppingpeoplechoosingamore favouredtenure (seeAnnex2 formoredetail)butall leadtohigherdemandforprivaterental.This increasingdemandwasmetinpartfromnewlyconstructeddwellings,butmostlyfromthetransferintoprivaterentalofexistingunitsthathadbeeninthesocialandowner-occupiedsectors.Althoughsome220,000dwellingswerebuiltforthesocialsectorovertheperiod1997-2010,thenumberofunitsinthatsectorfellbynearly500,000astenantsexercisedtheirRighttoBuyandotherunitswerelosttodemolitionandsale.Subsequentstudieshaveshownthatasignificantminorityofunitstransferredintoowner-occupationlatermovedintothePRS(InsideHousing,August2015).

Equally,1.6millionprivateunitswerebuiltbutowner-occupationroseonlybyaroundamillion.InpartthisadjustmentreflectedthegrowingnumberofRighttoBuydwellingsthatmovedintoprivaterenting—itiscurrentlyestimatedthat40%ofallRighttoBuypropertiesarenowletprivately(HouseofCommons2016).Inpart,especiallyaftertheglobalfinancialcrisis,unitsthatcouldnotbesoldbyowner-occupiersinsteadwererentedout.Someproportionoftheincreasecomesfromlandlordswhodonotwishtobeinthesectorforthelongerterm,butmuchreflectsthefactthatexpectedreturnsfromresidentialpropertyexceedthosefromalternativeinvestmentsinaperiodoflowinterestratesandincreasedrisk.Itisalsoclearthatfordevelopers,thereturnsfrombuildingprivaterentedstockusuallycannotcompetewiththereturnsofsaleintoowner-occupation.ThemainsourceofnewPRSsupplyisnotnew-buildbuttheexistingstock.

Overallintheperiod1997-2010thenumberofprivaterentedhomesincreasedbysome85%,andasaproportionofthestockgrewfromjustover10%toabout17%.By2010thereweresome3.9millionprivatelyrentedhomes–afigurelastseeninthemid-1960s.Farmoreoftheseadditionswerenewlybuilthomesthanhadbeenthecasesincethe1930s.Althoughexactnumbersarenotknown,agovernmentanalysis(HMTreasury,2010)basedonasampleofBuy-to-Letmortgages takenoutbetween2004and2007suggested thatBuy-to-Letmighthavecontributed to thepurchaseof35,000unitsayear,oraroundafifthofallnewcompletionsatthattime.However,CMLdatasuggestthatin2015onlyaround6%ofallBuy-to-Letmortgagesweresecuredonnewproperty.Thisimpliesthattheysupportedthepurchaseofjust7,000units,lessthanathirdtheTreasuryestimate(CMLestimate,basedonBuy-to-LetMortgageSurvey).

ThenumberofBuy-to-Letmortgagesincreasedstronglyfromthelate1990s.Figure3.2showsnewloanssince1999,givingthetotalnumber(left-handscale)andvaluein£millions(right-handscale).Thisshowsthedramaticgrowthinthemarket:in1999therewerefewerthan50,000newloansbutby2007thishadgrownbyafactorofsevento346,000.Theincreaseinvalueswasevengreater,withgrossadvancesof£27.4billionin2014–almostninetimesthelevelof1999.

Figure 3.2: Number and value of new Buy-to-Let mortgages, 1999-2014

Value of new loans (£m)Number of new loans

2000 20152011 2012 2013 20142009 20102007 20082005 20062003 20042001 2002

Source:CMLTableMM17

PAGE 37

Therewasaverysharpdropinthewakeoftheglobalfinancialcrisis.Recoveryfromthislowbasebeganin2009andhasbeenacceleratingsince2012,butthenumberandvalueofnewloanshaveyettoregainthelevelsseenin2007 (Figure3.3).

Figure 3.3: Number and value of new Buy-to-Let mortgages, 2007-Q3, 2015

Value of new loans (£m)Number of new loans

20152011 2012 2013 20142009 20102007

Q1 Q1 Q1 Q1 Q1 Q1 Q1 Q1 Q1Q3 Q3 Q3 Q3 Q3 Q3 Q3 Q3 Q3

2008

Source:CMLTableMM17

Loan-to-valueratiosforBuy-to-Letloanshavebeenonadownwardtrendsincethefinancialcrisis,accordingtosurveys,andlandlordsreportedin2014thattheyborrowonaverageabout60%ofthepurchasepriceofproperties.TheaverageLTVofentireportfolioswaslower,asmanylandlordshavesomeun-mortgagedproperties,andhasalsofallensince2007(Carey-Jones2015).

TheDCLGPrivateLandlordsSurvey2010showsthatthevastmajorityofallpropertieswerepurchasedinthemarketplace(Figure3.4).Theproportionsofpropertiesinherited,receivedasgiftsoracquiredinotherwayswhichprobablydidnotinvolvedebtfinanceareallrelativelysmall.Buildingthepropertymighthaveinvolvedexternalfunding,butofadifferentsort.Sothestartingpointisthatperhaps70%ofnewacquisitionsinvolvedamarketpurchase.

PAGE38

Figure 3.4: Method of acquisition by landlord type

Private individuals Companies Other organisations

Bought Inherited Built it Received as a gift Other Acquiried the organisation that owned it

Source:PrivateLandlordsSurvey2010

Figure 3.5: Sources of finance for acquisition by landlord type

Private individuals Companies Other organisations

Mortgage Personal savings Commercial loan Other Other loan Income from other business Income from other rented properties

Source:PrivateLandlordsSurvey2010

Amongprivateindividualsmorethan60%usedamortgagetopurchase(Figure3.5).NotallofthesewouldhavebeenBuy-to-Let,andindeedmanywouldhavebeenacquiredbeforethattypeofmortgageexisted.Afurther10%orsousedother loans.Butthisdoes implythatsome75%ofthestockof investmentproperties in2010hadbeenboughtwith debtfinance.

PAGE39

Among companies theproportion involvingdebt financewasmuch less. Theproportionof companyborrowinghasprobably increased since this survey, because a higher proportion of Buy-to-Let purchasers are now constituted ascompanies.OtherorganisationswouldgenerallynotbeintheBuy-to-Letmarket.

LookingatthetrendsinthenumbersofBuy-to-Letmortgagesweseethatsince2007thenumbersperannumhaverangedfromashighasnearly350,000toalowofunder100,000(Table3.1).

Table 3.1 New Buy-to-Let mortgages (1999-2015) and split between purchase and re-mortgage (2002-2015)

£ millions gross advances Percent for re-mortgageYear Number of loans Total For purchase For re-mortgage

1999 44,400 3,100

2000 48,400 3,900

2001 72,200 6,900

2002 130,000 12,900 8,030 4,130 32

2003 187,600 20,300 11,600 7,460 37

2004 226,000 24,100 14,060 8,490 35

2005 223,100 25,600 12,630 11,670 46

2006 319,200 38,000 19,590 17,120 45

2007 346,000 44,600 23,100 20,640 46

2008 225,300 27,600 12,210 14,610 53

2009 88,400 8,200 4,530 3,390 41

2010 85,200 8,700 4,650 3,960 46

2011 114,900 12,600 6,200 6,400 51

2012 130,200 15,200 7,400 7,600 50

2013 161,000 20,800 9,300 10,700 51

2014 197,700 27,200 12,400 14,500 53

2015 252,200 37,900 15,600 21,900 58

Source:CMLTableMM17

In the period before 2008 the number ofmortgages exceeded the net additions in the final couple of years by aconsiderableamount–in2007by55%(Figure3.6).From2008thenetincreaseinthePRSbegantoexceedthenumberofnewmortgages,initiallybyincreasingamountsandthenasthenumbersofmortgagesgrewagaincamebackcloserto thenet increase.By2013netadditionswerestillabovethenumberofnewmortgagesbyaround30%.However,in2014andparticularlyin2015thegrowthinBuy-to-Letmortgagesjumped–by23%in2014and28%in2015,with re-mortgagingincreasingby28%and38%respectively.Thustosomeextentthepicturepriorto2008isbeingrepeated.

PAGE40

Figure 3.6: New UK Buy-to-Let loans for purchase and re-mortgaging and change in stock of PRS dwellings, 2002-2013

For purchase For re-mortgage Change in PRS stockTotal new loans

2002 2015201420132012201120102009200820072006200520042003

Source:CMLTableMM17andDCLGLiveTable101

Thisdemonstrates thatnotall thegrowth in thePRS isattributable toadditionalBuy-to-Letmortgages. Householdscanletoutpreviouslyowner-occupiedproperties(so-called‘lettobuy’)orfundpurchasesbyincreasingindebtednessontheirowner-occupiedhome. It isalsoclear thata largeproportionofBuy-to-Letmortgages,especiallybefore thecrisis,werere-mortgageswherethemoneywasperhapsusedforotherpurposes.NewBuy-to-LetmortgagesdonotnecessarilygeneratenetadditionalPRSstock;equally,additionalstockcanbegeneratedwithouttheuseofBuy-to-Letmortgages,notonlybecauseasignificantnumberoflandlordsarecashpurchasersbutalsobecausethereareothersourcesofdebtfinance.Whatisalsoclearisthatinstitutionalinvestmenthasremainednegligiblethroughouttheperiodalthoughtherearenowclearsignsofpotentialinterest.

TheBDRCsurveysuggeststhattheroleofBuy-to-Letinfuturepurchasesisexpectedtobeverysimilartothepast-over60%ofthosewithfourpropertiesorfewerexpecttouseaBuy-to-Letmortgage,whileaquarterofalltypesoflandlordexpecttoreleaseequityfromotherpropertiestoenablethenextpurchase.Thesemethodsposeverydifferentrisksandarenotmutuallyexclusive.However,betweenaquarterandathirdofthoselookingtobuyanotherpropertyareexpectingtodosowithoutrecoursetoanyformofdebtfinance.

Locating Buy-to-Let within the PRSAsnotedabove,privatelandlordscanacquiretheirpropertiesinavarietyofways.Manyowndwellingsoutright,havinginheritedthemorpurchasedwithoutusingdebtfinance.Therearethenthosewhoborrowedinitially,eitherwithaBuy-to-Letmortgageorsomeothersource,buthavesincepaidofftheirdebt.Weknownexttonothingaboutthisgroup.ThentherearethosewhocurrentlyhaveoneormoreBuy-to-Letmortgagesandthosewhointendtobuypropertiesusingsuchamortgageinfuture.Itisatthisgroupthatgovernmentpolicyappearstobedirected.