the future of queensland's gas sector

TRANSCRIPT

Sunrise Seminar The Future of QLD’s Gas Sector

Thursday 28 July 2016

The Future of QLD”s Gas Sector © Deloitte Touche Tohmatsu 2016 1

“We acknowledge the traditional owners of the land on which we meet, and their continuing connection to the land and community” “We pay respect to them and their culture, and the elders past, present and future”

The Future of QLD”s Gas Sector © Deloitte Touche Tohmatsu 2016 2

Follow up for more insight

• National Director, Oil and Gas, Deloitte Brisbane

• Blog: www.geoffreycann.com

• Twitter: @geoffreycann

• Email: [email protected]

• Phone: 0447-366-333

2

The Future of QLD”s Gas Sector © Deloitte Touche Tohmatsu 2016 3

Queensland’s gas sector has a bright future, if you squint

• The pain is real and the patient is unwell

• Demand is still strong but supply growth stronger

• Australian projects shifting to ops

• Global sector conditions favour price upturn

• Watch a few indicators

The Future of QLD”s Gas Sector © Deloitte Touche Tohmatsu 2016 4

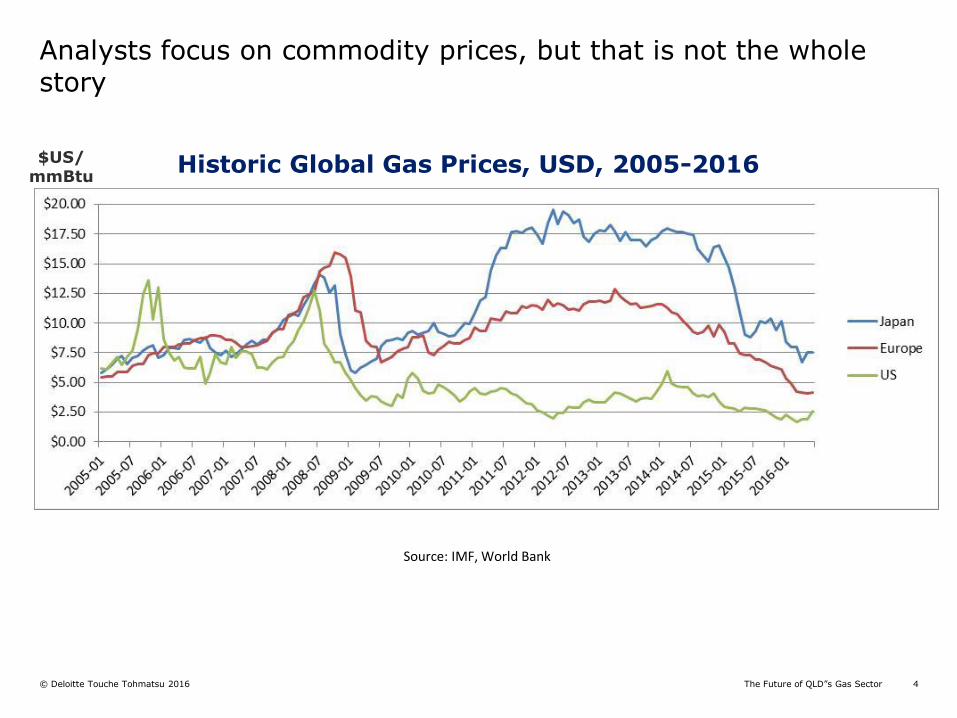

Analysts focus on commodity prices, but that is not the whole story

Source: IMF, World Bank

$US/ mmBtu

Historic Global Gas Prices, USD, 2005-2016

The Future of QLD”s Gas Sector © Deloitte Touche Tohmatsu 2016 5

Demand is rising 4.5% CAGR from 2015-2035, but LNG capacity is ahead. US gas will really pressure the field

Source: Deloitte MarketPoint

Liquefaction Capacity and LNG Demand, 2011-2035

The Future of QLD”s Gas Sector © Deloitte Touche Tohmatsu 2016 6

Future industry growth strongly favours US geologic productivity, liquids rich, deep supply base, free trade in oil and gas

Source: EIA (2016), Drilling Productivity Report

US Gas Rig Productivity 2007-2016

The Future of QLD”s Gas Sector © Deloitte Touche Tohmatsu 2016 7

As Australia’s king tide recedes, ops and maintenance take over

Source: Deutsche Bank, Project Websites

FEED FID Production

39.5 53.2 20+ 8+

2 years 2 years 4-5 years 20 years

PROD 2015

PROD 2016

PROD 2017

TBD

PROD 2016

PROD 2017

PROD 2015

PROD 2017

PROD 2012

STALLED

PROD 2014

TBD

TBD

PROD 1989

PROD 2006

92.7 $25B

STALLED

STALLED

Location Project Pre-FEED MTPA CAPEX

WA NWS 16.5

NT Darwin LNG 3.6

WA Pluto-1 4.3

PNG PNG LNG 6.6

QLD QCLNG 8.5 $10B

QLD GLNG 7.8 $5B

QLD APLNG 9.0 $10B

WA Gorgon 15.0

WA Wheatstone 8.9

NT Ichthys 8.9

WA Prelude 3.6

WA Pluto-2 4.3 $10B

WA Pluto-3 TBD $10.4B

WA Browse 12 $44B

NT Sunrise 4 $13.2B

QLD Arrow LNG 8 $20B+

NT Bonaparte LNG TBD TBD

Operate Construct Design

The Future of QLD”s Gas Sector © Deloitte Touche Tohmatsu 2016 8

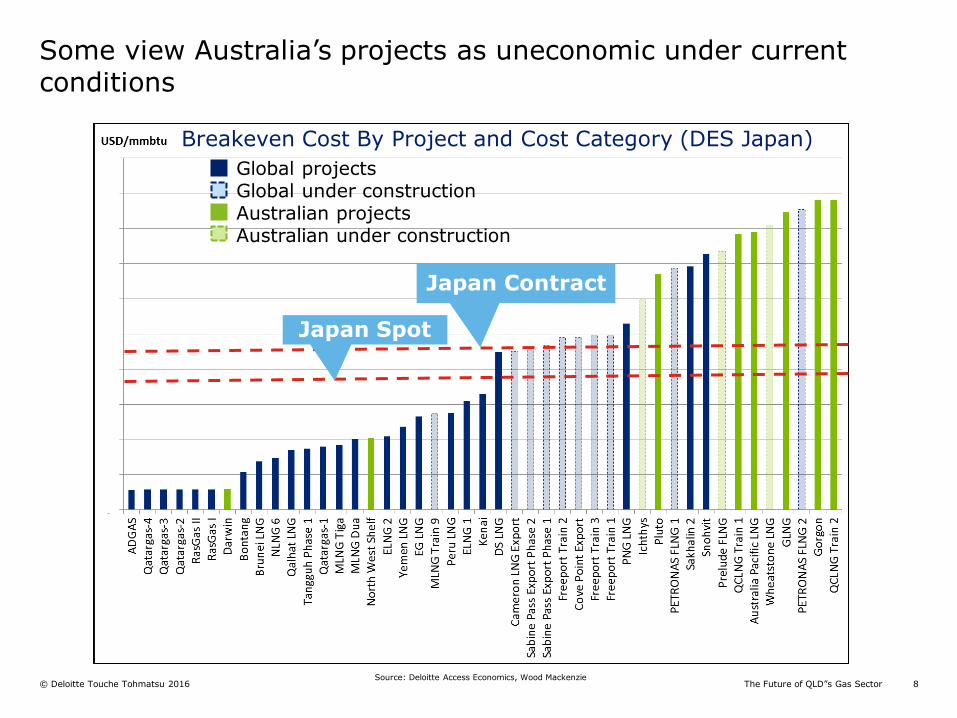

Some view Australia’s projects as uneconomic under current conditions

Source: Deloitte Access Economics, Wood Mackenzie

Japan Contract

Japan Spot

Global projects Global under construction Australian projects Australian under construction

Breakeven Cost By Project and Cost Category (DES Japan)

The Future of QLD”s Gas Sector © Deloitte Touche Tohmatsu 2016 9

Since plant capex is sunk, attention now swings to managing upstream capex, opex and transport (trading)

Japan Contract

Japan Spot

Breakeven Cost By Project and Cost Category (DES Japan)

Source: Deloitte Access Economics, Wood Mackenzie

The Future of QLD”s Gas Sector © Deloitte Touche Tohmatsu 2016 10

Capital spend in oil and gas globally has dropped below levels required to provide for growth and sustain volumes

Global Upstream Spending, ex MENA, $B

The Future of QLD”s Gas Sector © Deloitte Touche Tohmatsu 2016 11

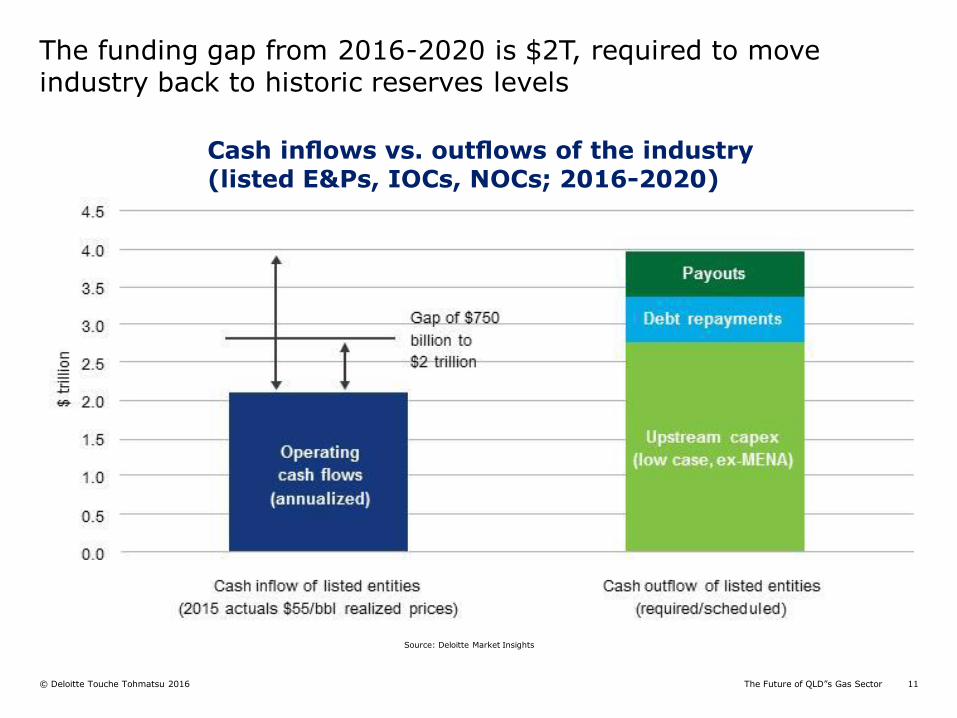

The funding gap from 2016-2020 is $2T, required to move industry back to historic reserves levels

Cash inflows vs. outflows of the industry (listed E&Ps, IOCs, NOCs; 2016-2020)

Source: Deloitte Market Insights

The Future of QLD”s Gas Sector © Deloitte Touche Tohmatsu 2016 12

Even as reserves fell, debt levels have doubled since 2008. Dividend payouts are still robust

The Future of QLD”s Gas Sector © Deloitte Touche Tohmatsu 2016 13

Queensland’s exploration well program shows the same pattern

Source: GSQ, Blue Energy

The Future of QLD”s Gas Sector © Deloitte Touche Tohmatsu 2016 14

Keep an eye on a few market indicators

• OPEC’s growth strategy

• Pre-productive capital

• Oil inventory build up

• Capital intensity and costs

• Shift in demand

• Market developments

• Brexit impacts

• Drilling programs

• Transactions

• Supplier retrenchment

• Creative contracting

• Balance sheet transformation

• Policy actions

International Domestic

The Future of QLD”s Gas Sector © Deloitte Touche Tohmatsu 2016 15

• Oversupply will endure for years

• The US steps up

• New markets emerging quickly

• QLD focus will be on reducing upstream capex and opex

• Capital constraints set scene for rapid price escalation

• Market shake out creates opportunities

Fundamentals for the gas sector are still strong, but capex and opex pressures are relentless

General information only

This presentation contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively the

“Deloitte Network”) is, by means of this presentation, rendering professional advice or services. Before making any decision or taking any action that may affect

your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte Network shall be responsible for any loss whatsoever

sustained by any person who relies on this presentation.

About Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its network of member firms, each of which

is a legally separate and independent entity. Please see www.deloitte.com/au/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu

Limited and its member firms.

Deloitte provides audit, tax, consulting, and financial advisory services to public and private clients spanning multiple industries. With a globally connected

network of member firms in more than 150 countries, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need

to address their most complex business challenges. Deloitte has in the region of 225,000 professionals, all committed to becoming the standard of excellence.

About Deloitte Australia

In Australia, the member firm is the Australian partnership of Deloitte Touche Tohmatsu. As one of Australia’s leading professional services firms. Deloitte Touche

Tohmatsu and its affiliates provide audit, tax, consulting, and financial advisory services through approximately 6,000 people across the country. Focused on the

creation of value and growth, and known as an employer of choice for innovative human resources programs, we are dedicated to helping our clients and our

people excel. For more information, please visit our web site at www.deloitte.com.au.

Liability limited by a scheme approved under Professional Standards Legislation.

Member of Deloitte Touche Tohmatsu Limited