the future of social security amy rehder harris tax research and program analysis section iowa...

TRANSCRIPT

The Future of Social Security

Amy Rehder HarrisTax Research and Program Analysis Section

Iowa Department of Revenue

(formerly of the Long Term Modeling Group, Congressional Budget Office, Washington, D.C)

History of Social Security Social Security (OASDI) is mandatory

public insurance to alleviate poverty in old-age Old-Age Insurance established 1935 Expanded to include Survivors and Spouses in

1939 Disability Insurance introduced 1956

Hospital Insurance (Medicare) began 1965

Old-Age Eligibility Must work at least 10 years While working, pay 6.2% (12.4%) payroll tax on

earnings up to taxable maximum $106,800 in 2011 During 2011 – employee pays 2% less – TRA 2010

Upon retirement, benefits a function of AIME: highest 35 years of earnings (indexed for inflation) PIA: progressive formula – higher replacement for lower

lifetime income NRA: rising from 65 to 67 for birth years 1960+ Age at claim (Claim at EEA of 62 = 30% reduction; Claim

at 70 with DRC = 24% increase)

Primary Insurance Amount

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$0 $12,000 $24,000 $36,000 $48,000 $60,000 $72,000 $84,000

Average Annual Earnings

An

nu

al B

enef

it a

t N

RA

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

90 percent replacement up to $8,988

32 percent replacementthrough $54,204

15 percent replacement up to maximum

Old-Age Benefits Retired Workers

32.3 million beneficiaries in Dec. 2008 Average annual benefit was $13,800 in

2008 Auxiliary Beneficiaries

Spouses: 2.4 million Survivors: 4.4 million Children: 2.4 million Also mother/father or parents

Spouse Benefits Established in era of one-earner household

Married to a worker at retirement Married for 10 years or more if divorced Receive benefit equal to 50 percent of PIA Reduced based on claim age of spouse

Average annual benefit was $6,800 in 2008

For two-earner household, spouse with lower earnings could receive no additional benefit even though paid tax of 12.4% on every dollar earned

Survivor Benefits Established in era of one-earner household

Married to a worker at death Married to deceased worker for 10 years or

more if divorced Receive benefit equal to 100 percent of worker

benefit Reduced based on claim age of survivor

Average annual benefit was $13,300 in 2008

Survivor in retired household faces up to 1/3 benefit reduction at death of spouse

Annual Cost-of-Living Adjustment 1973 a COLA created to account for

impact of inflation on current beneficiaries Prior to then, required act of Congress

COLA is linked to consumer price index Flat (and falling) prices from late 2008

through 2010 lead to two years of no cost-of-living increases

Cry for “relief” $250 checks sent out in 2009 ($13 B) Nothing equivalent for 2010 or 2011 planned

Disability Insurance Eligible if worked 5 of previous 10 years

Benefit is function of earnings divided by years worked prior to disability (minus lowest 5 years)

7.4 million beneficiaries in 2008 with average annual benefit of $12,800

Auxiliary beneficiaries: 1.8 million Large growth in beneficiaries

Recent expansion to mental illness and back pain Concerns about incentives to claim DI rather than OAI

when nearing EEA (no benefit reduction) Spike in claims during current recession among

unemployed

Iowa’s Aging Population

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

24%

2000 2005 2010 2015 2020 2025 20300%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

24%

Iowa Share 65+

Iowa Share 75+

Iowa Share 85+

US Share 65+

US Share 75+

US Share 85+

Population Pyramid or Tower?

2010

Figure 2. Iowa Population Pyramid Projections, 2010 and 2030

2030Percent of Total Population

5 4 3 2 1 0 1 2 3 4 55 4 3 2 1 0 1 2 3 4 5

0 - 4 5 - 910 - 1415 - 1920 - 2425 - 2930 - 3435 - 3940 - 4445 - 4950 - 5455 - 5960 - 6465 - 6970 - 7475 - 7980 - 84 85+

Male FemaleMale Female

Impact of Aging Population Worker-Beneficiary Ratio

Iowa and US: 3.0 falling to 2.0 Manifested through deteriorating tax

bases OASDI: Wages Income Taxes: Pensions and investment

earnings often receive preferential tax treatment, additional exempt earnings by age

Taxation of Social Security “Contributions” taxed as income when

earned by federal and state governments Benefits paid at retirement non-taxable

until 1983 If other income above $32,000/$25,000, up to

50% taxable Revenue to OASDI Trust Fund Attempting to improve system finances in

preparation for baby boomers 1993 up to 85%, money to Medicare

Taxation of Social Security in Iowa Followed federal rules by taxing 50% of

benefits for seniors with other income Fear that encouraging high-income elderly

to move out of state at retirement 2006 change – phase-out of taxation on

benefits by 2014 (67% of taxable benefits exempt in 2011)

Evidence suggests elderly move to warmer climates, not non-tax states

Social Security Long Run Finances Social Security currently running surpluses

– saved in OASDI Trust Fund Taxes > Benefits

Projections show future will have large deficits

How are those projections made? What can Congress do to prevent the

system from going broke?

CBO Projected Outlays and Revenues 1985-2084

0

1

2

3

4

5

6

7

8

9

10

1985 1995 2005 2015 2025 2035 2045 2055 2065 2075

Sh

are

of

GD

P

0

1

2

3

4

5

6

7

8

9

10

Outlays

Revenues

Impact of the Great Recession- Revenues Minus Outlays

Social Security Administration Social Security is administered by SSA, an

executive branch agency SSA produces an Annual Trustees report

about the future of the system Short-run (10 years) Long-run (75 years)http://www.ssa.gov/OACT/TR/2010/tr2010.pdf

CBO produces long-term projections http://www.cbo.gov/ftpdocs/119xx/doc11943/10-22-SocialSecurity_chartbook.pdf

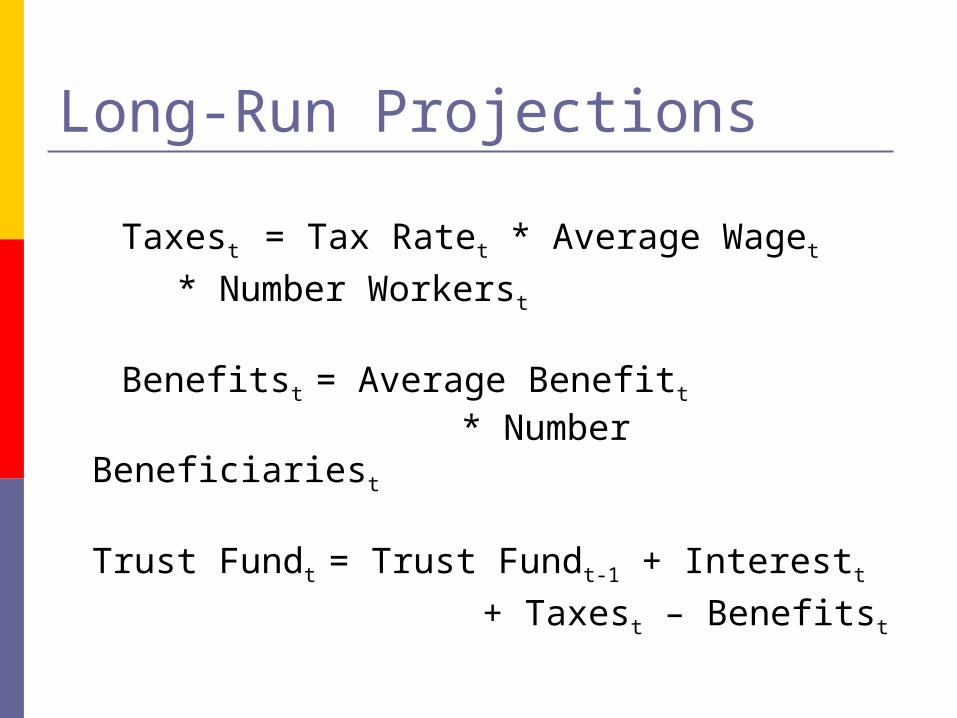

Long-Run Projections

Taxest = Tax Ratet * Average Waget

* Number Workerst

Benefitst = Average Benefitt

* Number Beneficiariest

Trust Fundt = Trust Fundt-1 + Interestt

+ Taxest – Benefitst

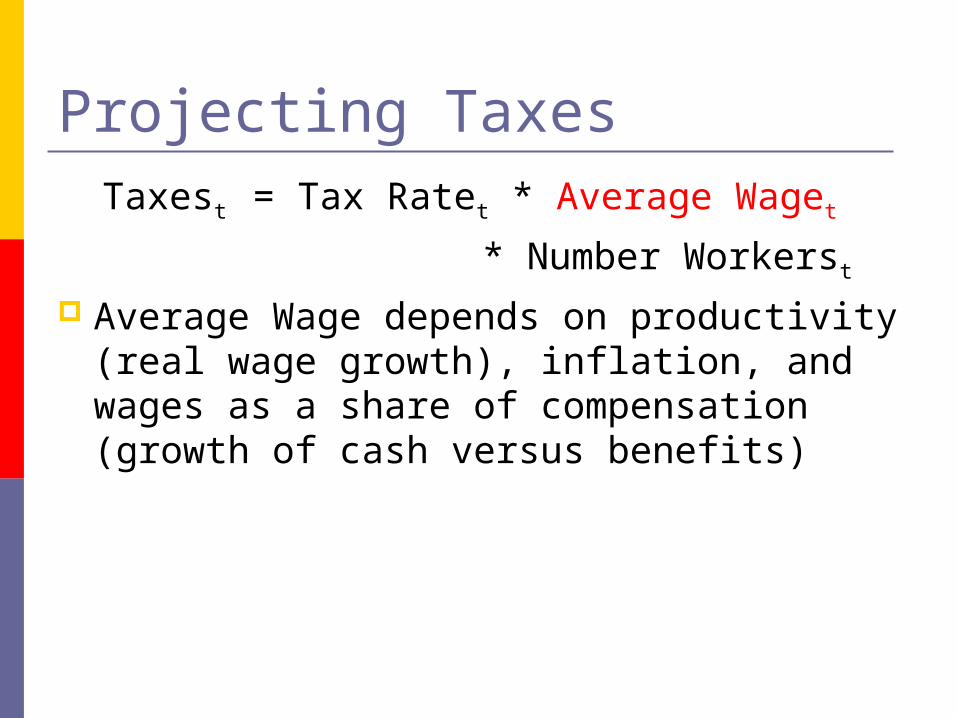

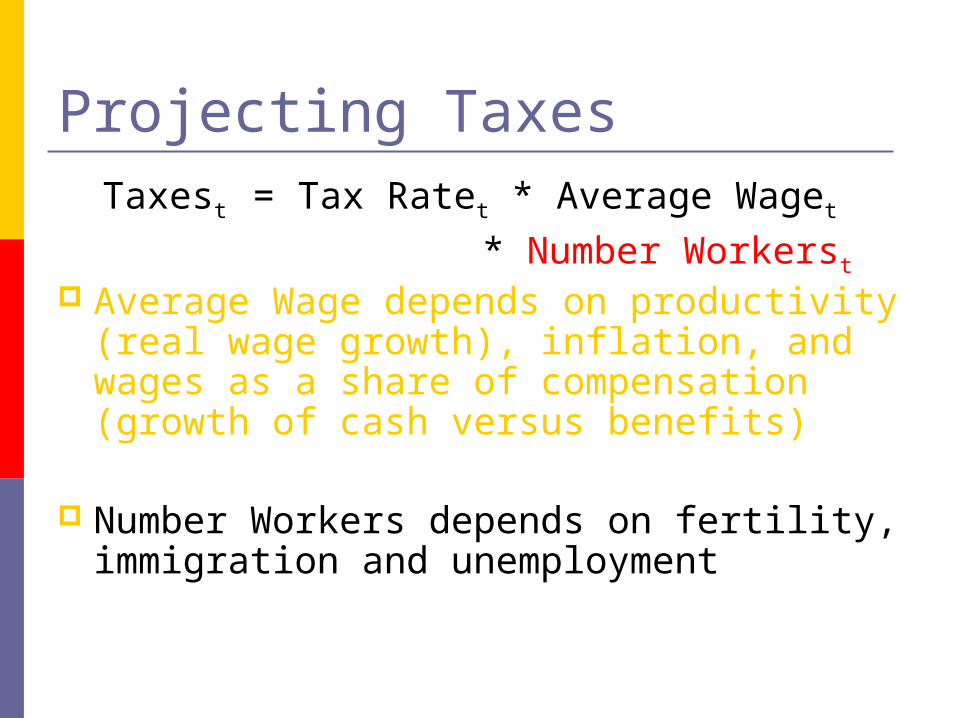

Projecting Taxes Taxest = Tax Ratet * Average Waget

* Number Workerst

Average Wage depends on productivity (real wage growth), inflation, and wages as a share of compensation (growth of cash versus benefits)

Projecting Taxes Taxest = Tax Ratet * Average Waget

* Number Workerst

Average Wage depends on productivity (real wage growth), inflation, and wages as a share of compensation (growth of cash versus benefits)

Number Workers depends on fertility, immigration and unemployment

Projecting Benefits

Benefitst = Average Benefitt

* Number Beneficiariest

Average Benefit depends on past wages and inflation (along with all of the policy rules)

Projecting Benefits

Benefitst = Average Benefitt

* Number Beneficiariest

Average Benefit depends on past wages and inflation (along with all of the policy rules)

Number Beneficiaries depends on fertility (60 years earlier), mortality, and disability rates

Projecting Trust Fund Balances

Trust Fundt = Trust Fundt-1 + Interestt

+ Taxest – Benefitst

Interest rates on government bonds (IOU’s to ourselves)

Ten Key Assumptions Five Economics Assumptions:

Future earnings(1) Real wage growth (2) Inflation(3) Unemployment(4) Wage as a Share of Compensation

Future benefits paid to retirees, the disabled, spouses and survivors

Earnings on the existing Trust Fund(5) Interest rate

Ten Key Assumptions (cont) Five Demographics Assumptions:

How many people will be paying taxes and receiving benefits

(6) Mortality(7) Fertility(8) Immigration(9 & 10) Disability Incidence and Termination

2009 changes to mortality assumptions worsened finances

2010 changes to mortality data improved finances

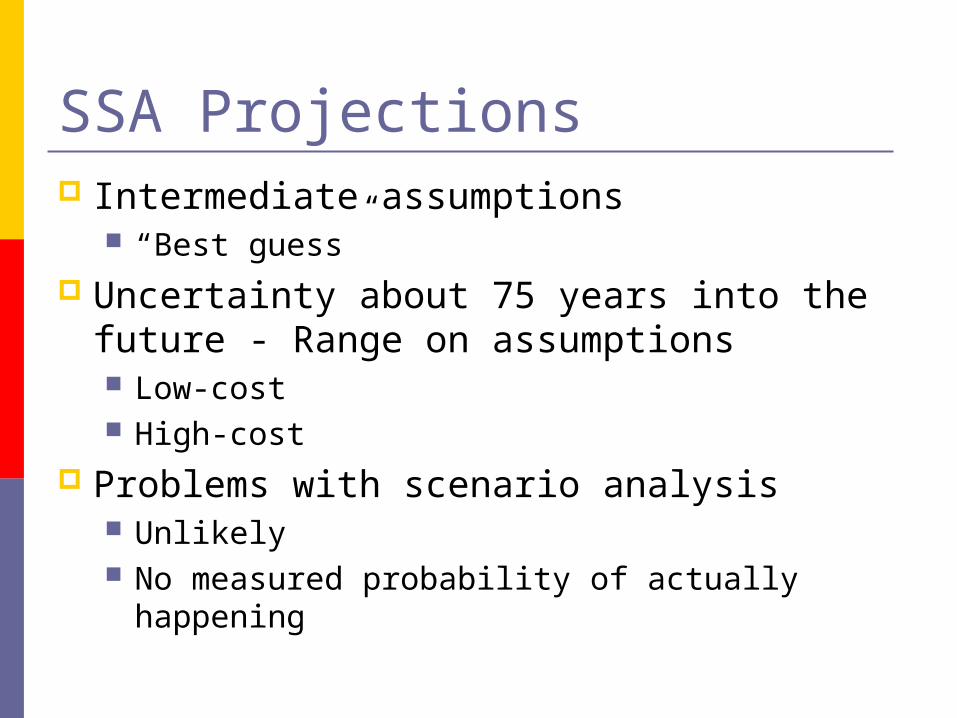

SSA Projections Intermediate assumptions

“Best guess” Uncertainty about 75 years into the future

- Range on assumptions Low-cost High-cost

Problems with scenario analysis Unlikely No measured probability of actually happening

CBO Projections Stochastic projections (500 runs)

Median Uncertainty about 75 years into the future

- Range on outcomes 90th percentile 10th percentile

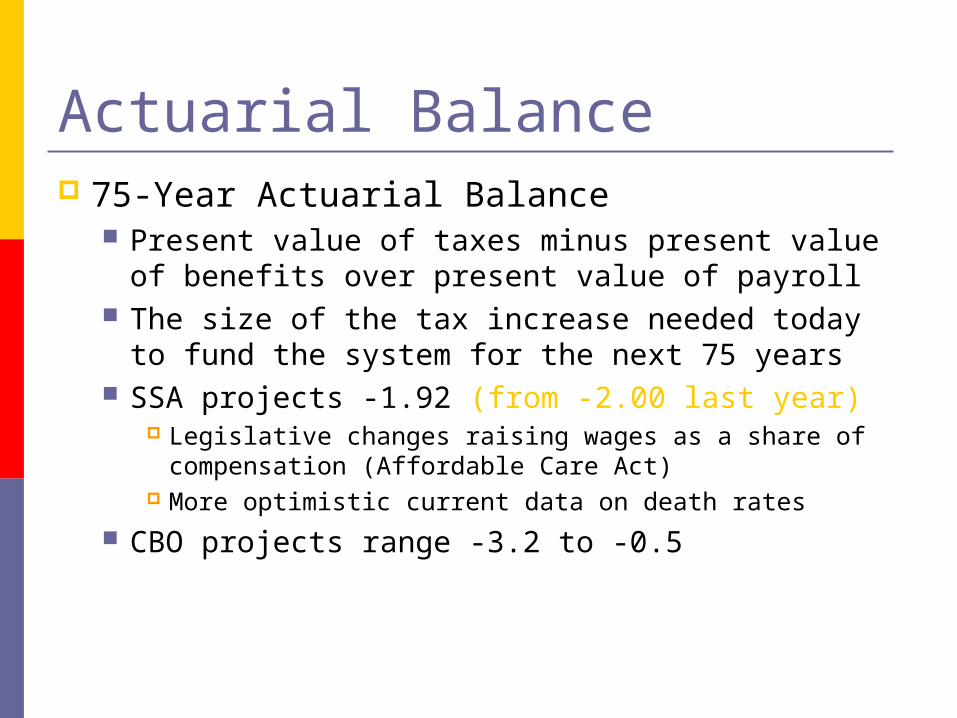

Actuarial Balance 75-Year Actuarial Balance

Present value of taxes minus present value of benefits over present value of payroll

The size of the tax increase needed today to fund the system for the next 75 years

SSA projects -1.92 (from -2.00 last year) Legislative changes raising wages as a share of

compensation (Affordable Care Act) More optimistic current data on death rates

CBO projects range -3.2 to -0.5

Income and Cost Rates Income Rate/Revenues

Payroll taxes as percent of GDP 2009: 4.9 2084: 4.8-5.2

Cost Rate/Outlays Benefits as percent of GDP 2009: 4.8 2084: 5.1-8.8

CBO Projected Outlays and Revenues 1985-2084

0

1

2

3

4

5

6

7

8

9

10

1985 1995 2005 2015 2025 2035 2045 2055 2065 2075

Sh

are

of

GD

P

0

1

2

3

4

5

6

7

8

9

10

Outlays

Revenues

Trust Fund Ratio Trust fund assets over annual

expenditures Measures if the system can pay benefits Currently large surplus Source of touted “Exhaustion Date” SSA projects the system will “go broke” in

2037 (same as last year) CBO projects between 2032 to 2058 However, current outlays exceed revenues –

living on interest and soon trust fund assets will be “redeemed”

CBO Projected Trust Fund Ratio, 1985-2084

-25

-20

-15

-10

-5

0

5

10

1985 1995 2005 2015 2025 2035 2045 2055 2065 2075

Ra

tio

of

Tru

st

Fu

nd

Ba

lan

ce

to

An

nu

al

Ou

tla

ys

-25

-20

-15

-10

-5

0

5

10

Hope under Current Law? Taxest = Tax Ratet * Average Waget

* Number Workerst

Benefitst = Average Benefitt

* Number Beneficiariest

Trust Fundt = Trust Fundt-1 + Interestt

+ Taxest – Benefitst

Hope with Changes to Current Law? Taxest = Tax Ratet * Average Waget

* Number Workerst

Benefitst = Average Benefitt

* Number Beneficiariest

Trust Fundt = Trust Fundt-1 + Interestt

+ Taxest – Benefitst

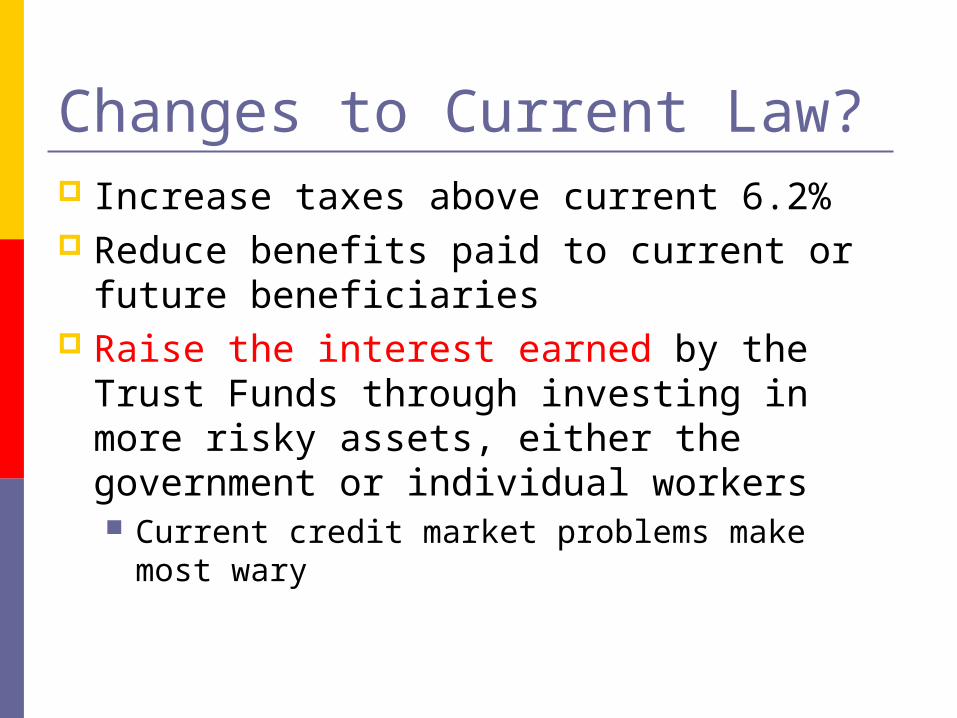

Changes to Current Law? Increase taxes above current 6.2%

Regressive tax Raise taxable maximum with no benefit

increase? Risk of doing nothing – required tax increases

(1.9 percentage points today, to 14.3 percent, good for next 75 years ONLY)

Future workers pay (much higher if wait longer)

Changes to Current Law? Increase taxes above current 6.2% Reduce benefits paid to current or future

beneficiaries Raise NRA further? Risk of doing nothing – about 2040 when

system no longer takes in enough resources not all of promised benefits can be paid

Across-the-board benefit cuts? (estimated 22 percent cut in benefits for all)

Future beneficiaries pay (much higher if only new beneficiaries affected)

Changes to Current Law? Increase taxes above current 6.2% Reduce benefits paid to current or future

beneficiaries Raise the interest earned by the Trust

Funds through investing in more risky assets, either the government or individual workers Current credit market problems make most

wary

Risks of Government Investing Bad stock returns could harm new retirees

(35% of the time – lose money) Only 5% chance better off in all years over

next 75 Public control over private assets creates

conflicts “Social Investing”

Individual Accounts Allow individuals to take part of payroll tax

and invest in higher returns paid by the stock market

Trade-off is must accept higher risks Stock market is NOT a sure thing

President Obama Opposes any “privatization” Proposed no specific changes in FY 2012

budget, but some reportedly considered: Raising taxable maximum to $180,000 from

current $106,800 (90% of wages, up from 84%)

Change COLA calculation, reduce growth of benefits

Bring uncovered state and local employees into the system (small numbers)

National Commission on Fiscal Responsibility and Reform

Make PIA formula more progressiveRaise taxable maximum to 90% of wagesMake COLA calculation more accurateRaise NRA (69) and EEA (64) by 2075Cover all state and local employees Low-earner benefit at 125% of povertyRaise benefits for very old and long-time disabled (over 20 years)

Improve education of future retirees Increase flexibility for claiming benefits Encourage personal retirement savings

Your future retirement? Social Security benefits are uncertain for

your generation if reforms not instituted soon

Still not a great method of “saving” for retirement

Three-legged stool Public pension (Social Security) Private pension (401k) Personal saving (Roth IRA)

Economics informs us - solution is political

Even Bigger Mess: Medicare Congressional efforts for Social Security

reform ended with 2006 election Current health care reform debate has

shifted focus to Medicare Much bigger financial problem Same concerns about aging with little control

on benefit costs Serves as an example of government-run

health care Considered in Affordable Care Act – mostly as a

source of funds

Medicare defined Medicare is publicly-provided health

insurance for the elderly Medicaid is publicly-provided health insurance

for low income uninsured Four parts

Part A: Hospital Insurance (HI) Part B: Supplemental Medical Insurance (SMI) Part C: Medicare Advantage is alternative to

A&B Part D: Prescription Drugs

Who is covered? Elderly, 65+ (83.6% of beneficiaries)

Everyone automatically covered by HI, must sign up for SMI (95% do)

38.7 million beneficiaries in 2009 Disabled eligible after two years receiving

DI benefits 7.6 million beneficiaries in 2009

End stage renal disease (kidney dialysis)

What is covered? HI covers inpatient hospital care, skilled

nursing facilities, home health services, and hospice care

SMI covers doctor visits, lab tests, and outpatient hospital care

Part D covers prescription drugs (w limits – some removed as part of ACA)

Does NOT cover nursing homes

How is Medicare financed? HI financed through payroll taxes

1.45% (3.9%) on all earnings (HI Trust Fund) SMI and Part D financed through monthly

premiums (25%) and general revenues SMI $96.40-369.10 (2011) each month

means-tested premium Part D varies by plan Deducted from Social Security checks Also co-pays and deductibles

Medicare in financial trouble Dramatic growth in the program

1980: $37 Billion 2009: $502 Billion ($40 Billion 1-yr increase)

Similar to Social Security, Medicare has a bleak financial future Baby boomers start to retire in next 5 years People living longer Health costs rising faster than economy as a

whole

Excess Cost Growth Growth in spending per beneficiary that

exceeds growth in per capita GDP 3.0 percent over 1970-2005 2.1 percent over 1990-2005

Captures both policy changes and “residual” growth

Assumption going forward dramatically alters projections of program growth

Same issues for Medicaid (program for poor jointly funded by the states)

Medicare and Medicaid Spending as Share of GDP: Excess Cost Growth??

0

5

10

15

20

25

30

35

40

1985 1995 2005 2015 2025 2035 2045 2055 2065 2075

0

5

10

15

20

25

30

35

40

Excess Cost Growth of 1 percent

Excess Cost Growth of 2.5 percent

No Excess Cost Growth

CBO Forecast

Percent

…so federal budget in trouble HI Trust Fund, currently in surplus, is

projected to be exhausted in 2029 as costs rise Improved by ACA changes to spending

SMI will squeeze other federal spending as the Part B costs rise – 75% from current taxpayers

Part D cheaper so far, but cries to expand coverage may raise costs Estimated to cost $400 B over 10 years

Your future retirement? Health care diminishing as private

retirement benefit

Reliance on Medicare also uncertain

Health care likely to undergo major changes in next few years as costs rise

Economics informs us – solution is political