the future of the world car fleet the road ahead bbva research · the future of world car fleet:...

TRANSCRIPT

The Future of World Car Fleet: The Road Ahead(A BBVA Research model for long-term automobile projections)

November, 2012

Cross-Country Emerging Markets Unit

A BBVA Research model for long-term automobile projections

2

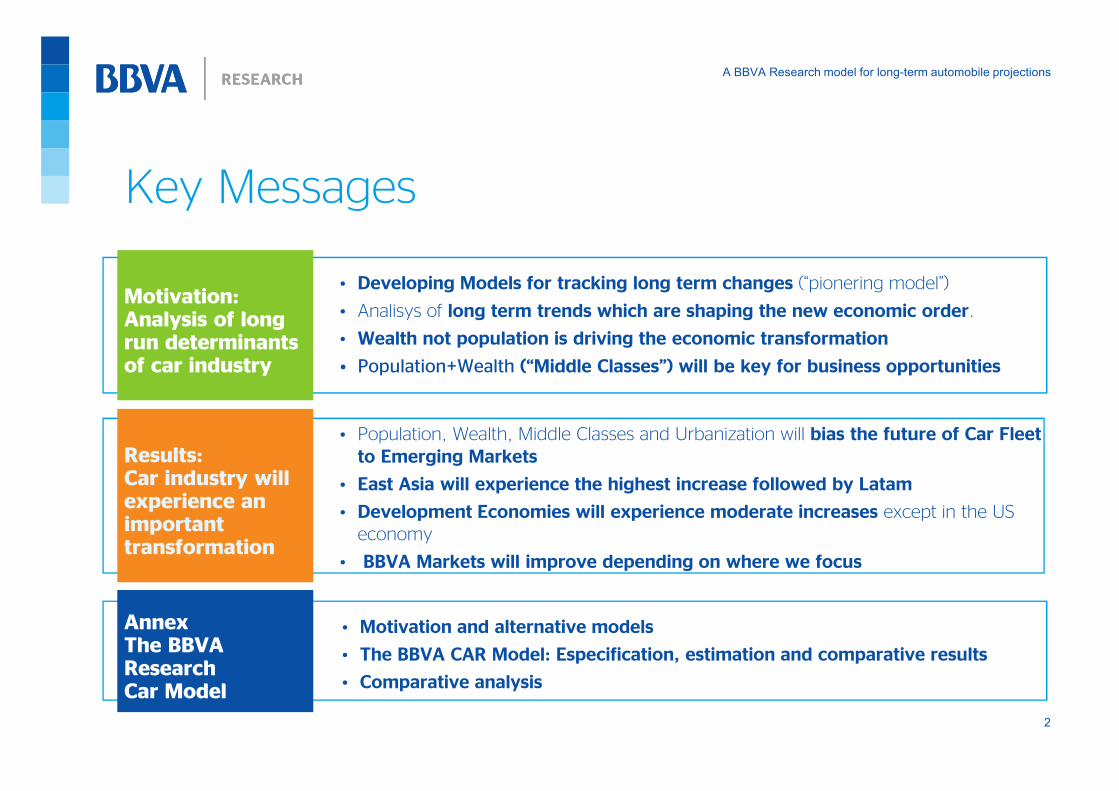

• Population, Wealth, Middle Classes and Urbanization will bias the future of Car Fleet

to Emerging Markets

• East Asia will experience the highest increase followed by Latam

• Development Economies will experience moderate increases except in the US

economy

• BBVA Markets will improve depending on where we focus

Key Messages

• Motivation and alternative models

• The BBVA CAR Model: Especification, estimation and comparative results

• Comparative analysis

Results:Car industry willexperience animportanttransformation

AnnexThe BBVA ResearchCar Model

• Developing Models for tracking long term changes (“pionering model”)

• Analisys of long term trends which are shaping the new economic order.

• Wealth not population is driving the economic transformation

• Population+Wealth (“Middle Classes”) will be key for business opportunities

Motivation:Analysis of longrun determinantsof car industry

A BBVA Research model for long-term automobile projections

3

Contents

Analysis of long run determinants of Car Industry

Global results

Annex: The BBVA Research CAR Model

A BBVA Research model for long-term automobile projections

4

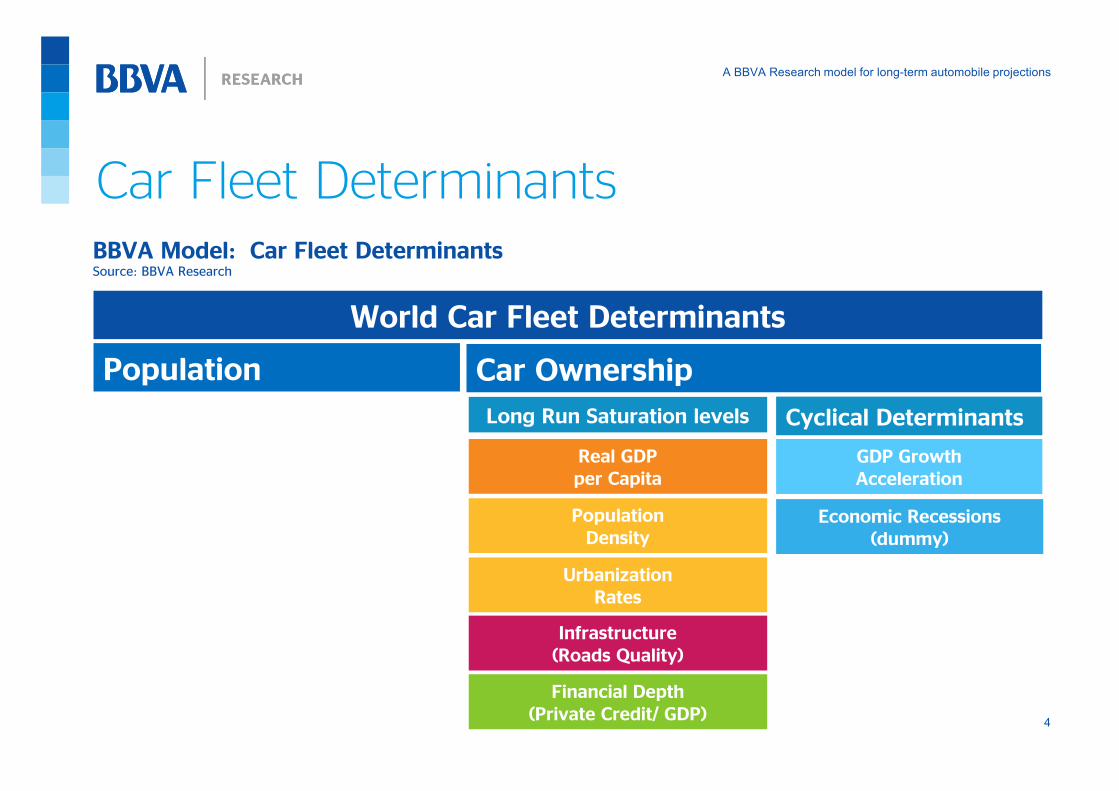

Car Fleet Determinants

Car Ownership

Long Run Saturation levels Cyclical Determinants

Real GDP

per Capita

Population

Density

Urbanization

Rates

Infrastructure

(Roads Quality)

Financial Depth

(Private Credit/ GDP)

GDP Growth

Acceleration

Economic Recessions

(dummy)

Population

World Car Fleet Determinants

BBVA Model: Car Fleet DeterminantsSource: BBVA Research

A BBVA Research model for long-term automobile projections

5

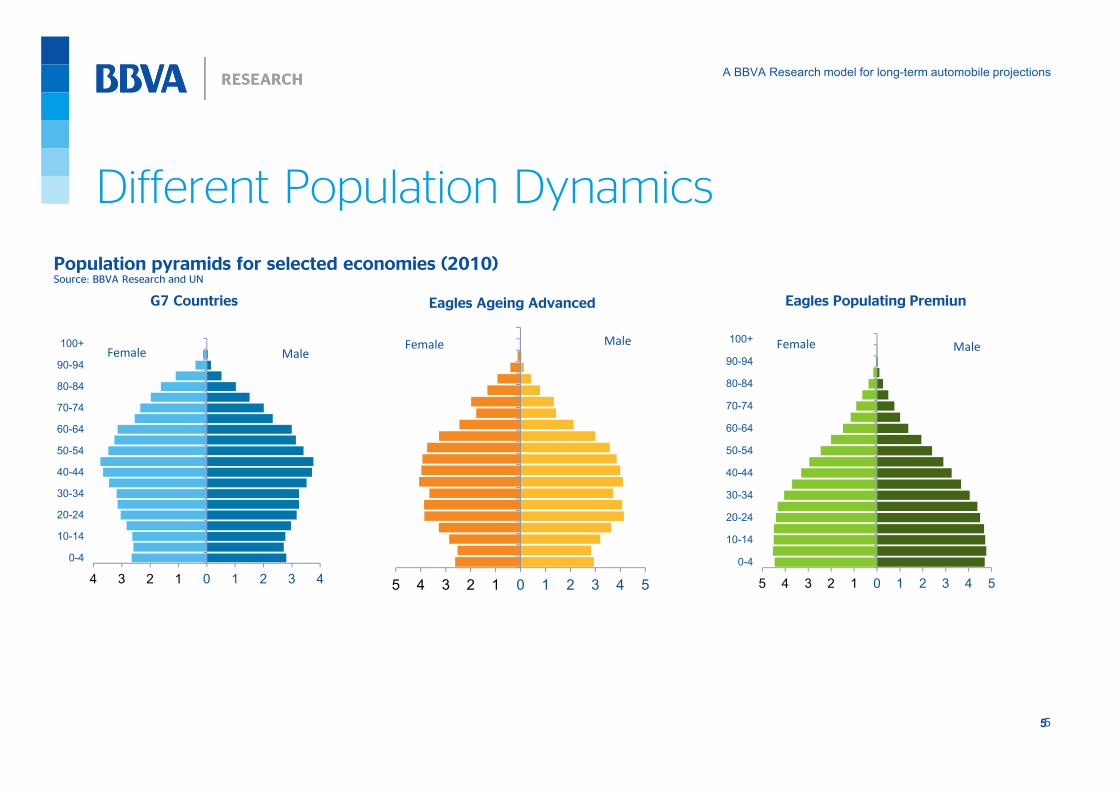

Different Population Dynamics

5

Population pyramids for selected economies (2010)Source: BBVA Research and UN

G7 Countries

4 3 2 1 0 1 2 3 4

0-4

10-14

20-24

30-34

40-44

50-54

60-64

70-74

80-84

90-94

100+Female Male

5 4 3 2 1 0 1 2 3 4 5

Female Male

Eagles Ageing Advanced Eagles Populating Premiun

5 4 3 2 1 0 1 2 3 4 5

0-4

10-14

20-24

30-34

40-44

50-54

60-64

70-74

80-84

90-94

100+Female Male

A BBVA Research model for long-term automobile projections

6

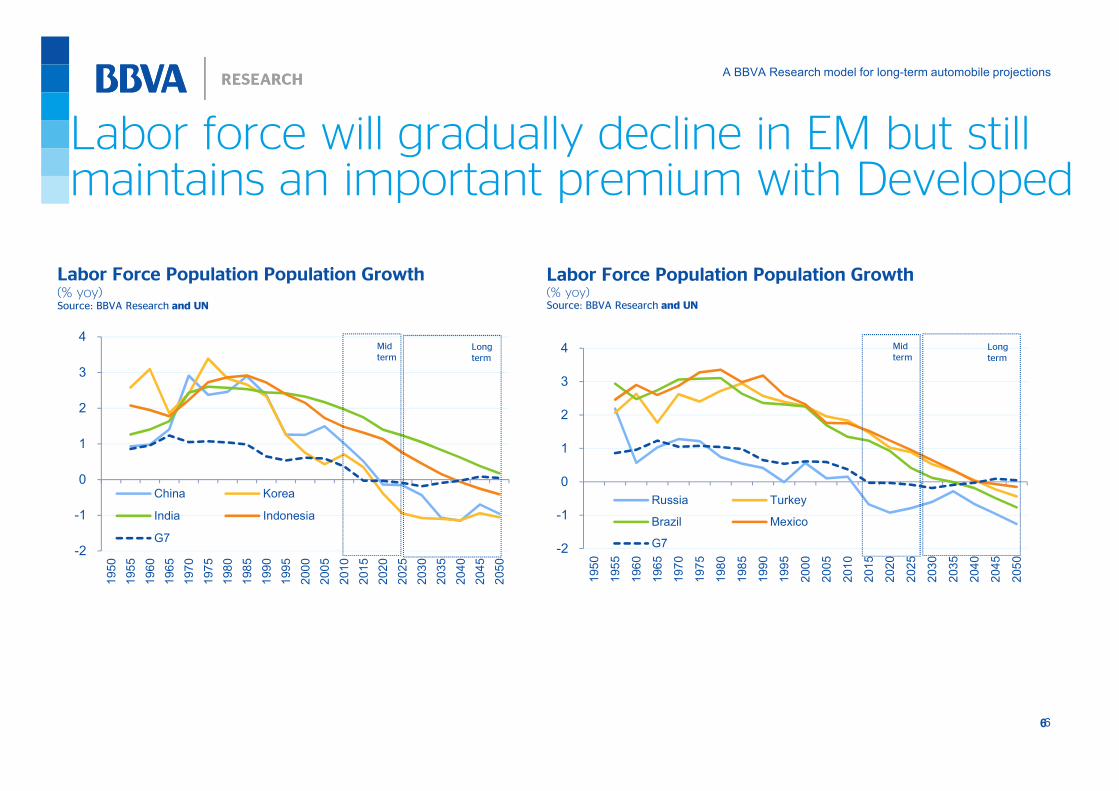

Labor force will gradually decline in EM but stillmaintains an important premium with Developed

6

-2

-1

0

1

2

3

4

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

China Korea

India Indonesia

G7-2

-1

0

1

2

3

4

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

Russia Turkey

Brazil Mexico

G7

Labor Force Population Population Growth(% yoy)Source: BBVA Research and UN

Labor Force Population Population Growth(% yoy)Source: BBVA Research and UN

Mid

term

Long

term

Mid

term

Long

term

A BBVA Research model for long-term automobile projections

7

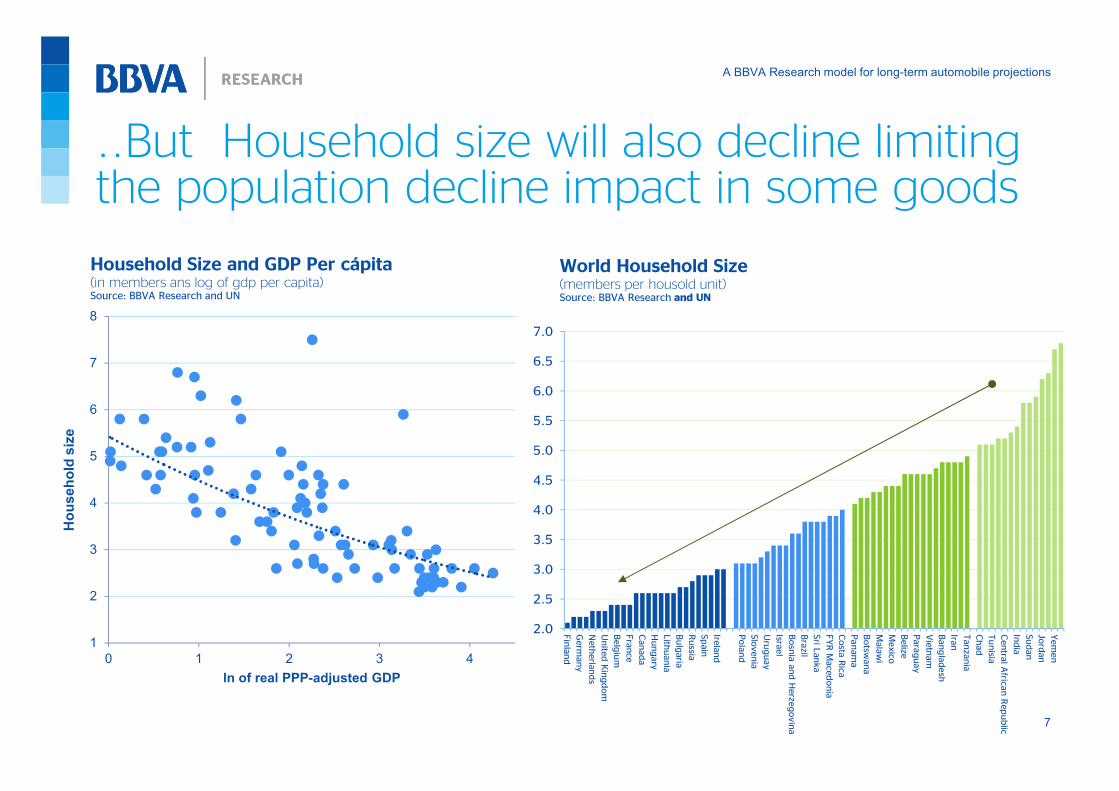

..But Household size will also decline limitingthe population decline impact in some goods

1

2

3

4

5

6

7

8

0 1 2 3 4

Household size

ln of real PPP-adjusted GDP

Household Size and GDP Per cápita(in members ans log of gdp per capita)Source: BBVA Research and UN

World Household Size(members per housold unit)Source: BBVA Research and UN

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

Finland

Germ

any

Netherlands

United Kingdom

Belgium

France

Canada

Hungary

Lithuania

Bulgaria

Russia

Spain

Ireland

Poland

Slovenia

Uruguay

Israel

Bosnia and Herzegovina

Brazil

Sri L

anka

FYR Macedonia

Costa

Rica

Panama

Botsw

ana

Malawi

Mexico

Belize

Paraguay

Vietnam

Bangladesh

Iran

Tanzania

Chad

Tunisia

Centra

l Afric

an Republic

India

Sudan

Jordan

Yemen

A BBVA Research model for long-term automobile projections

8

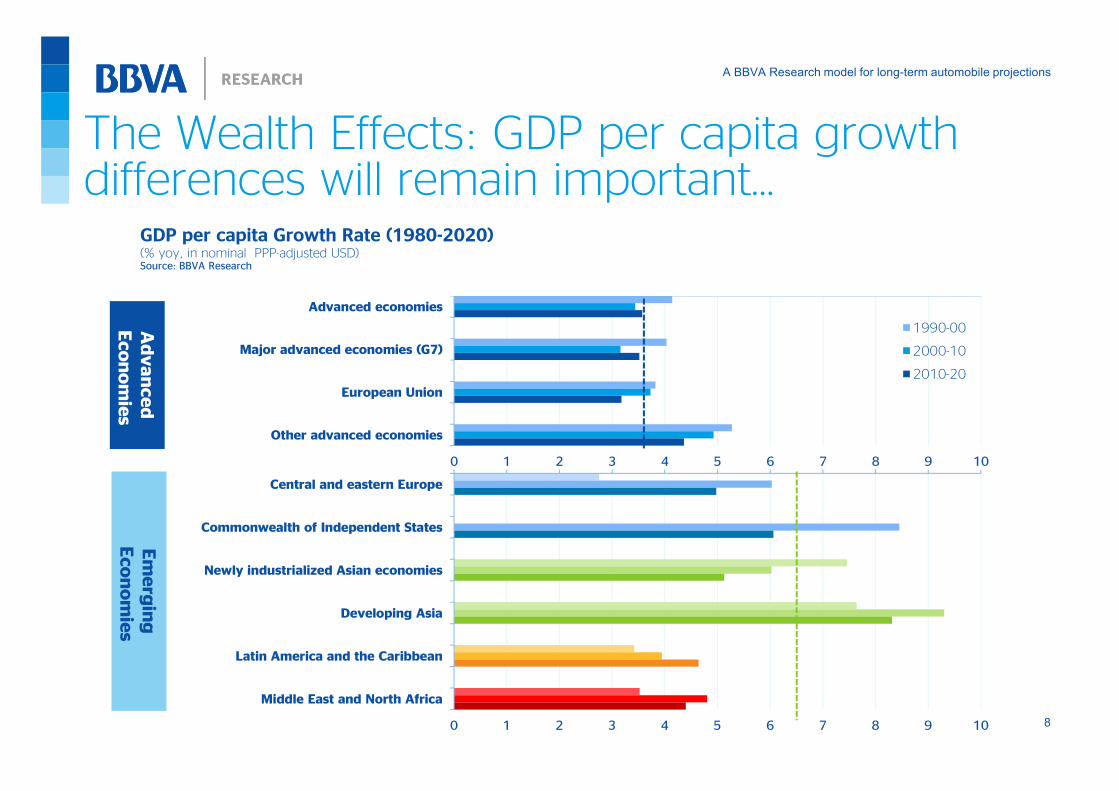

The Wealth Effects: GDP per capita growthdifferences will remain important…

0 1 2 3 4 5 6 7 8 9 10

Central and eastern Europe

Commonwealth of Independent States

Newly industrialized Asian economies

Developing Asia

Latin America and the Caribbean

Middle East and North Africa

0 1 2 3 4 5 6 7 8 9 10

Advanced economies

Major advanced economies (G7)

European Union

Other advanced economies

1990-00

2000-10

2010-20

GDP per capita Growth Rate (1980-2020)(% yoy, in nominal PPP-adjusted USD)Source: BBVA Research

Advanced

Economies

Emerging

Economies

A BBVA Research model for long-term automobile projections

9

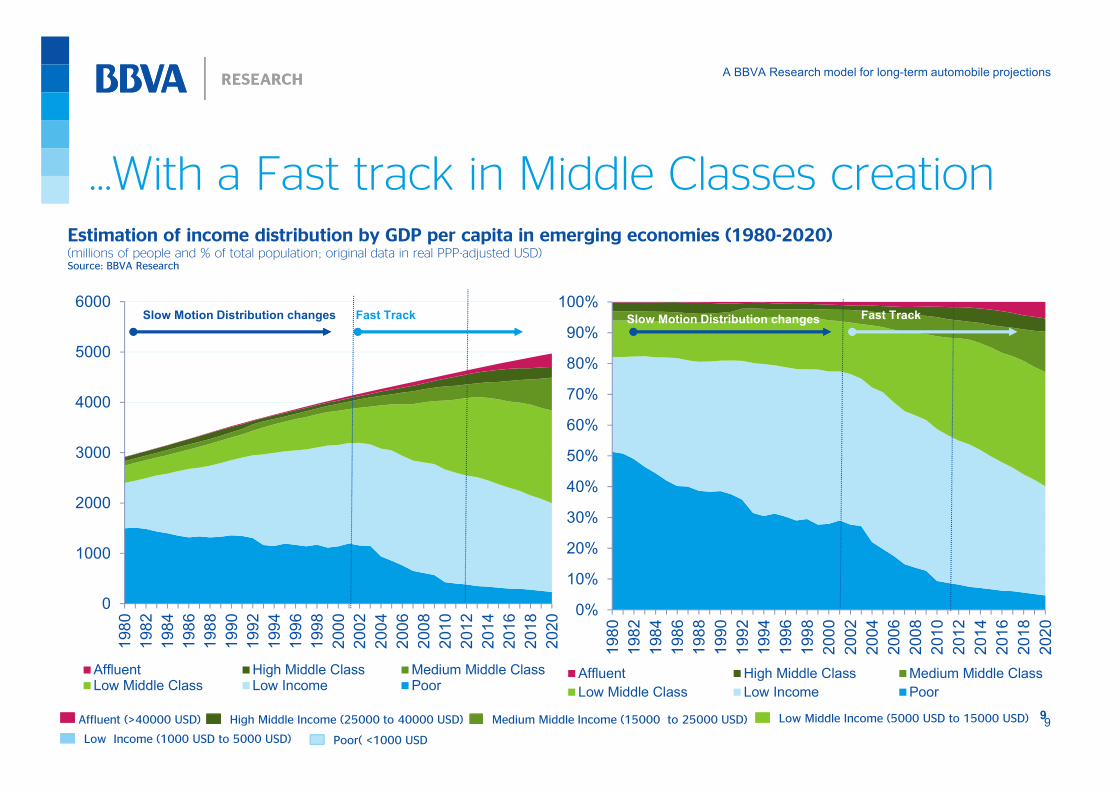

…With a Fast track in Middle Classes creation

0

1000

2000

3000

4000

5000

6000

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

Affluent High Middle Class Medium Middle ClassLow Middle Class Low Income Poor

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

Affluent High Middle Class Medium Middle Class

Low Middle Class Low Income Poor

9

Estimation of income distribution by GDP per capita in emerging economies (1980-2020)(millions of people and % of total population; original data in real PPP-adjusted USD)Source: BBVA Research

Slow Motion Distribution changes Fast Track Slow Motion Distribution changes Fast Track

Affluent (>40000 USD) High Middle Income (25000 to 40000 USD) Medium Middle Income (15000 to 25000 USD) Low Middle Income (5000 USD to 15000 USD)

Low Income (1000 USD to 5000 USD) Poor( <1000 USD

A BBVA Research model for long-term automobile projections

10

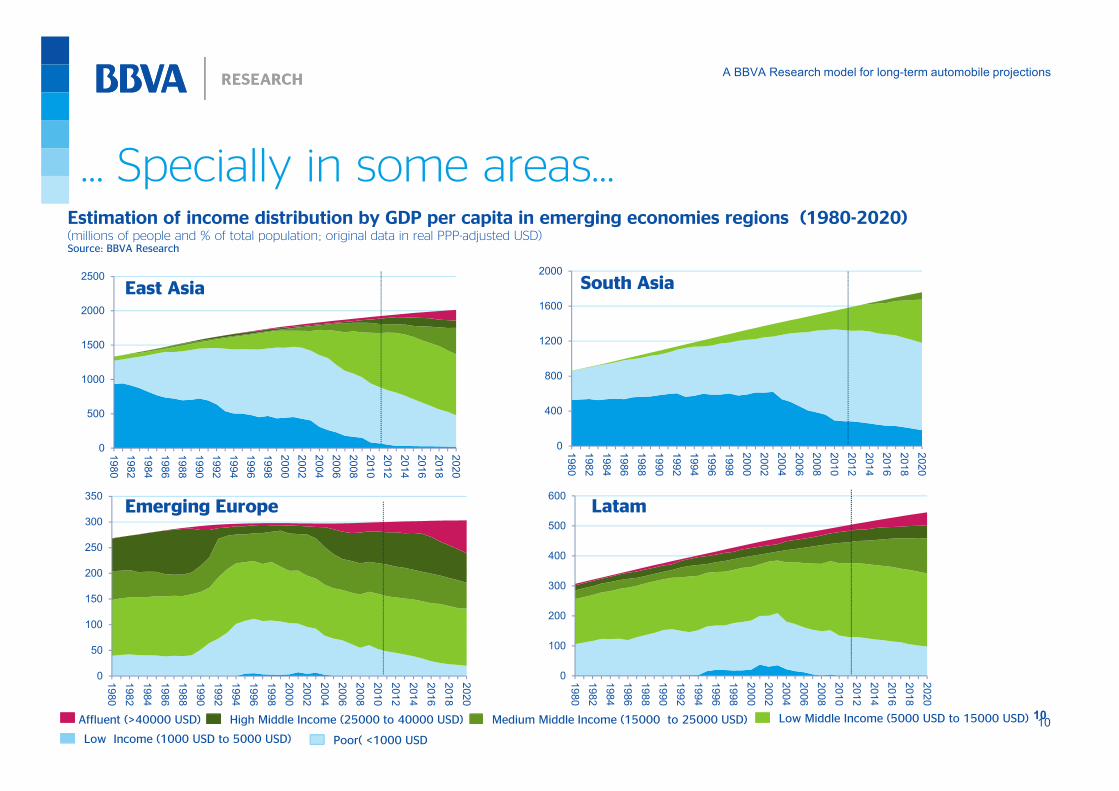

… Specially in some areas…

0

500

1000

1500

2000

2500

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

0

100

200

300

400

500

600

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

Estimation of income distribution by GDP per capita in emerging economies regions (1980-2020)(millions of people and % of total population; original data in real PPP-adjusted USD)Source: BBVA Research

0

50

100

150

200

250

300

350

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

0

400

800

1200

1600

2000

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

10Affluent (>40000 USD) High Middle Income (25000 to 40000 USD) Medium Middle Income (15000 to 25000 USD) Low Middle Income (5000 USD to 15000 USD)

Low Income (1000 USD to 5000 USD) Poor( <1000 USD

East Asia South Asia

Emerging Europe Latam

A BBVA Research model for long-term automobile projections

11

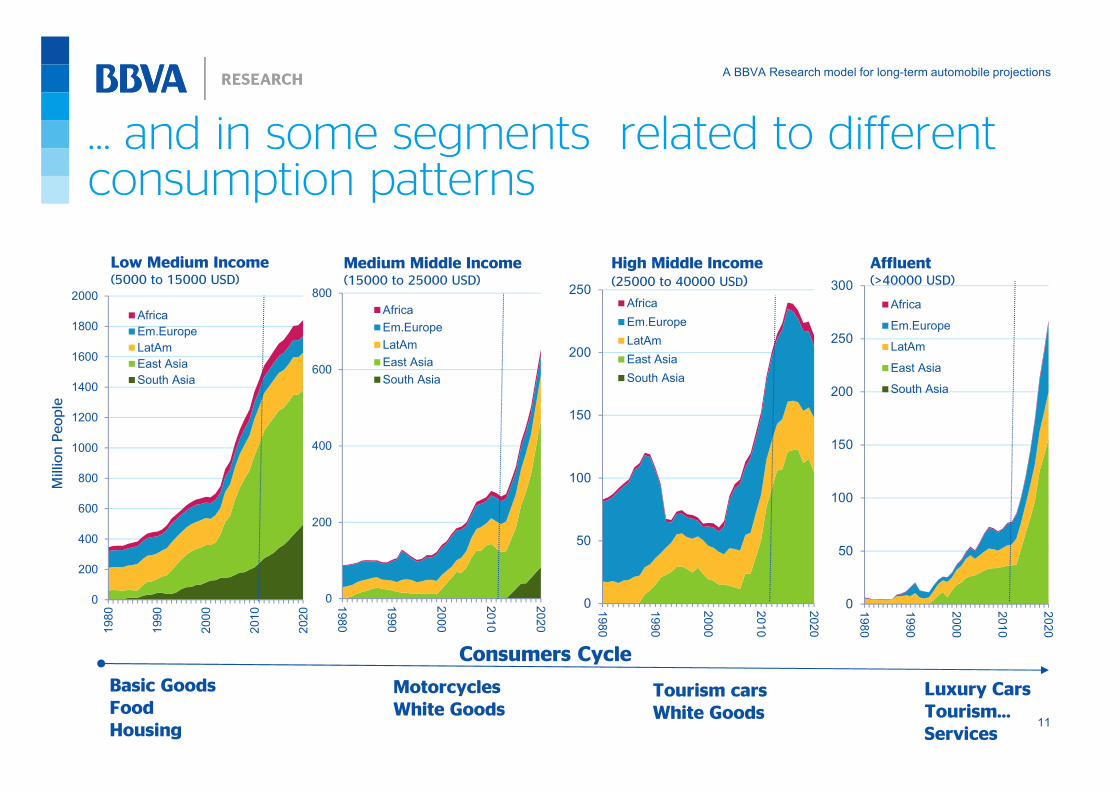

… and in some segments related to differentconsumption patterns

0

200

400

600

800

1000

1200

1400

1600

1800

2000

1980

1990

2000

2010

2020

Africa

Em.Europe

LatAm

East Asia

South Asia

0

200

400

600

800

1980

1990

2000

2010

2020

Africa

Em.Europe

LatAm

East Asia

South Asia

0

50

100

150

200

250

1980

1990

2000

2010

2020Africa

Em.Europe

LatAm

East Asia

South Asia

0

50

100

150

200

250

300

1980

1990

2000

2010

2020

Africa

Em.Europe

LatAm

East Asia

South Asia

Low Medium Income(5000 to 15000 USD)

Medium Middle Income(15000 to 25000 USD)

High Middle Income(25000 to 40000 USD)

Affluent(>40000 USD)

MillionPeople

Basic Goods

Food

Housing

Luxury Cars

Tourism…

Services

Motorcycles

White Goods

Consumers Cycle

Tourism cars

White Goods

A BBVA Research model for long-term automobile projections

12

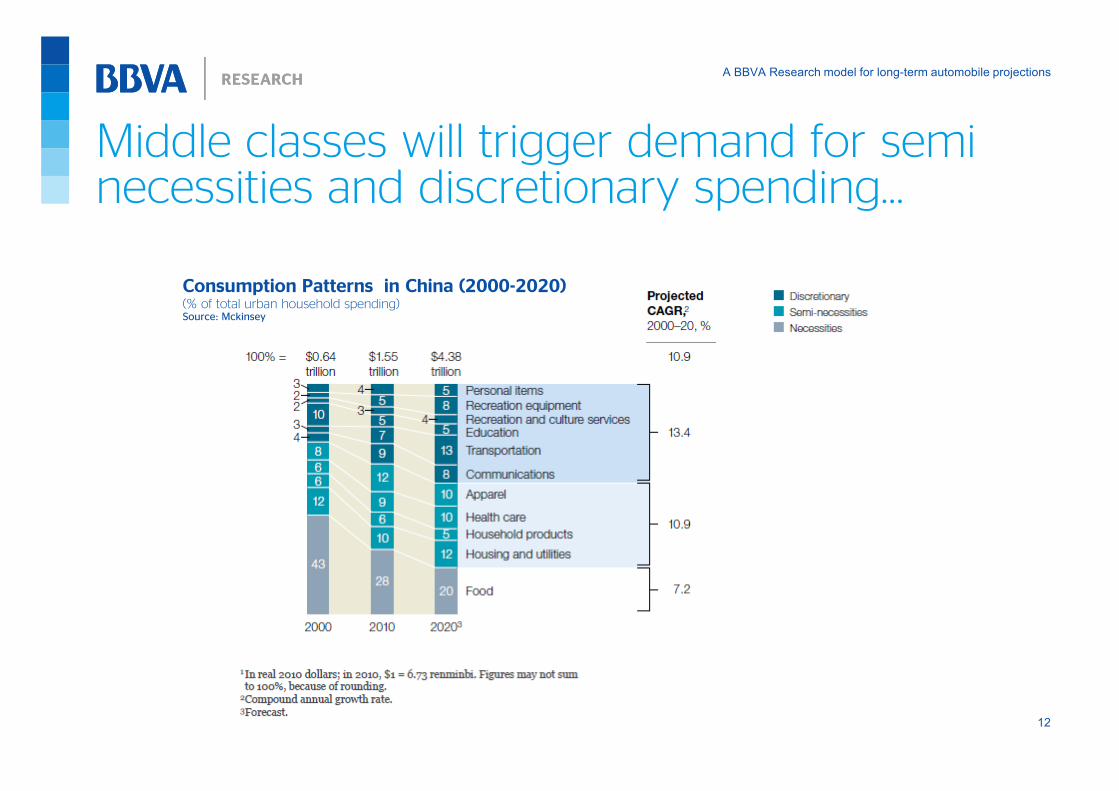

Middle classes will trigger demand for seminecessities and discretionary spending…

Consumption Patterns in China (2000-2020)(% of total urban household spending)Source: Mckinsey

A BBVA Research model for long-term automobile projections

13

…Urbanization will increase very fast in some of the regions…

0

10

20

30

40

50

60

70

80

90

West Europe N.América

East Europe Asia

Latam Africa-0.1

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025

West Europe N.América East Europe

Asia Latam Africa

World Urbanization Rates(1980-2020)(Urban population as a % of total)Source: United Nations

World Urbanization Rates(1980-2020)(Annual Change in Urbanization Rates)Source: United Nations

A BBVA Research model for long-term automobile projections

14

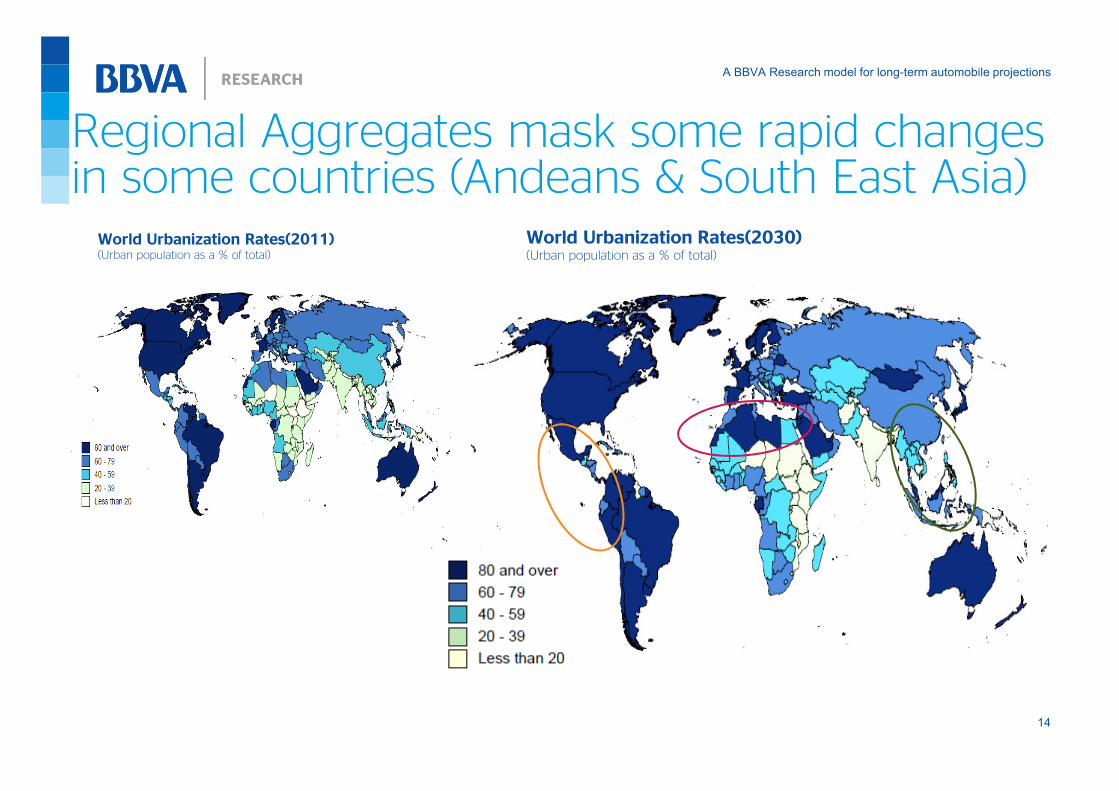

Regional Aggregates mask some rapid changesin some countries (Andeans & South East Asia)

World Urbanization Rates(2011)(Urban population as a % of total)Source: United Nations

World Urbanization Rates(2030)(Urban population as a % of total)Source: United Nations

A BBVA Research model for long-term automobile projections

15

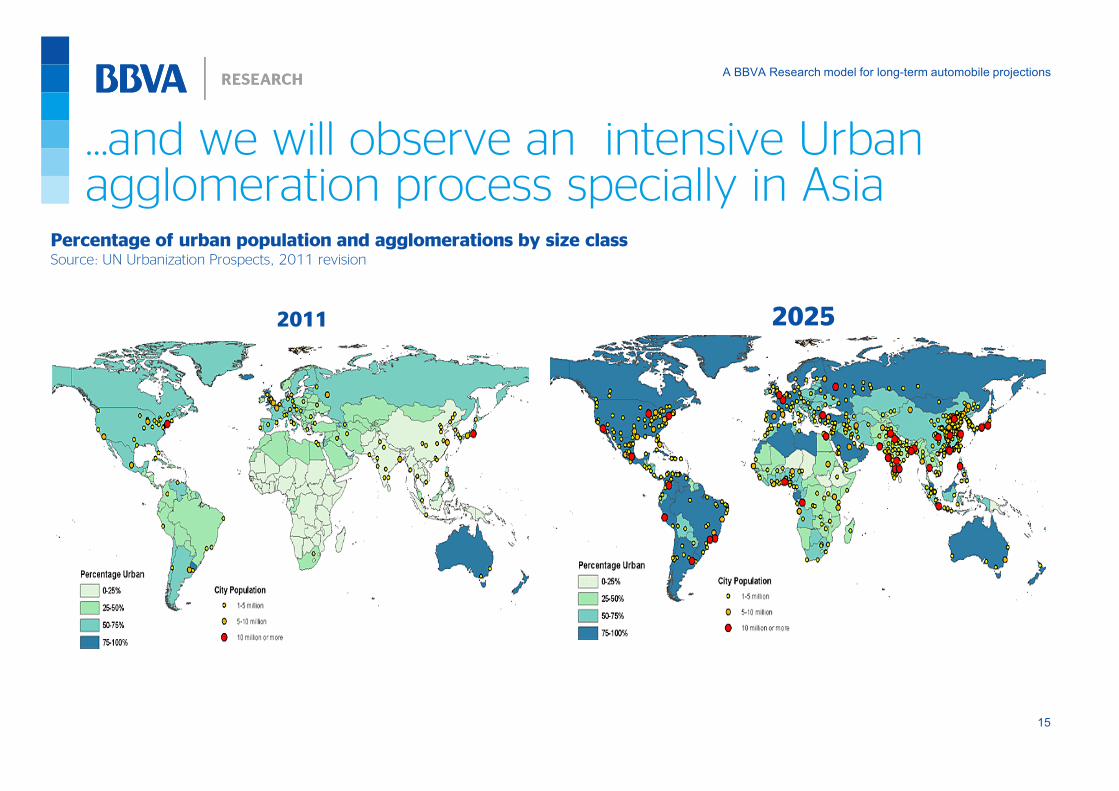

…and we will observe an intensive Urbanagglomeration process specially in Asia

Percentage of urban population and agglomerations by size classSource: UN Urbanization Prospects, 2011 revision

2011 2025

A BBVA Research model for long-term automobile projections

16

… But Emerging Markets still lags in transportinfrastructure …

Paved Road World Map(% of total roads, from 0=lighter to 100= Darker)Source:World Bank Development Indicators

Road Density World Map(Sinthetic indicator, from -1=lighter to 1= Darker)Source:World Bankand BBVA Research

A BBVA Research model for long-term automobile projections

17

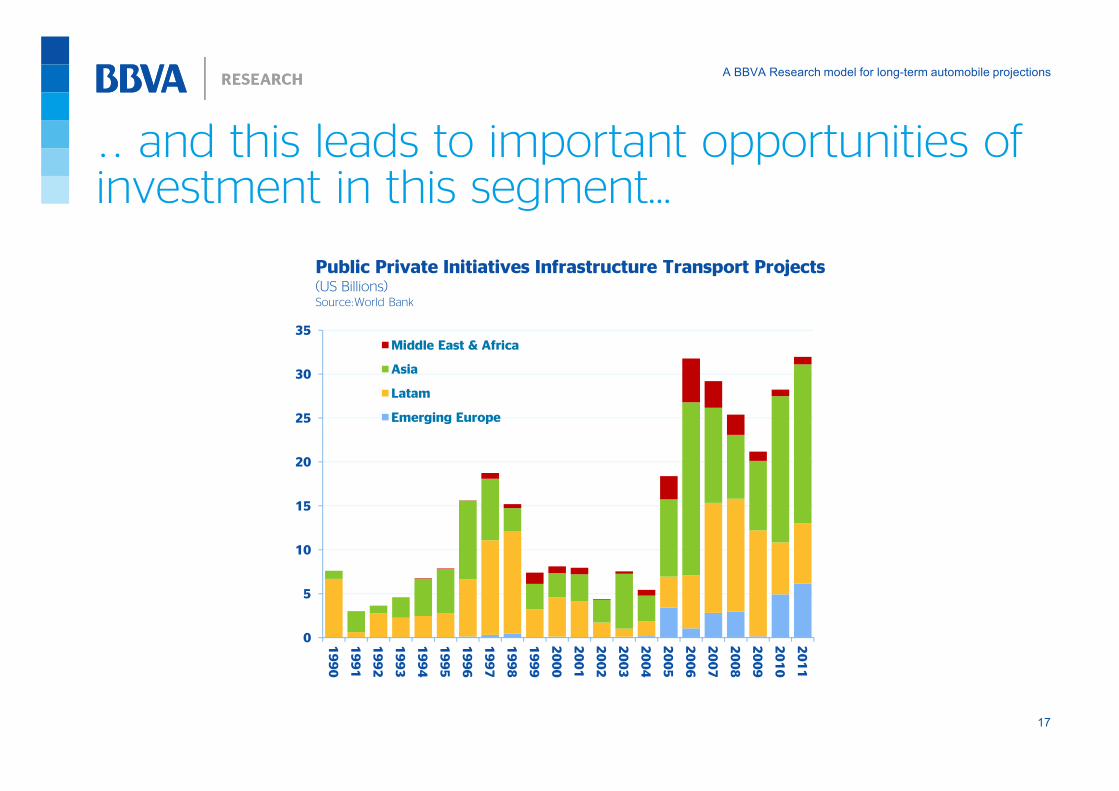

.. and this leads to important opportunities of investment in this segment…

0

5

10

15

20

25

30

35

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Middle East & Africa

Asia

Latam

Emerging Europe

Public Private Initiatives Infrastructure Transport Projects(US Billions)Source:World Bank

A BBVA Research model for long-term automobile projections

18

Contents

Analysis of long run determinants of Car Industry

Global results

Annex: The BBVA Research CAR Model

A BBVA Research model for long-term automobile projections

19

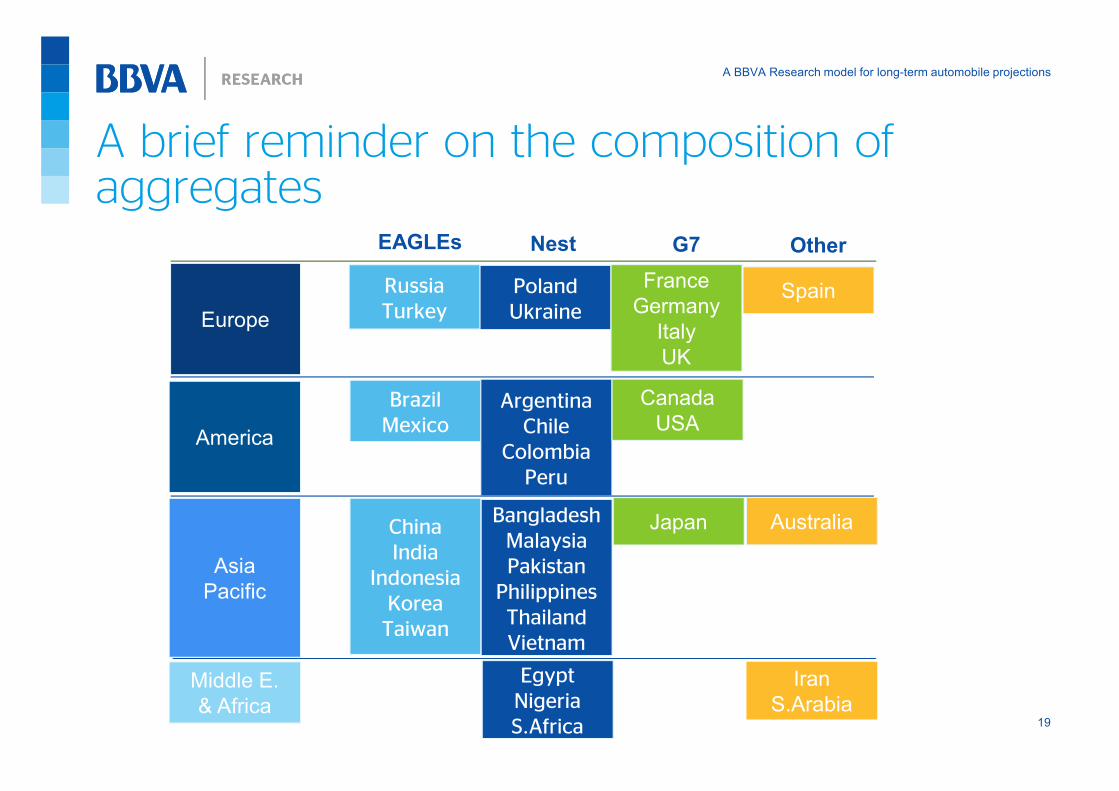

A brief reminder on the composition of aggregates

EAGLEs

China

India

Indonesia

Korea

Taiwan

Brazil

Mexico

Russia

Turkey

Nest

Bangladesh

Malaysia

Pakistan

Philippines

Thailand

Vietnam

Argentina

Chile

Colombia

Peru

Poland

Ukraine

Egypt

Nigeria

S.Africa

Asia

Pacific

America

Europe

Middle E.

& Africa

G7

Japan

Canada

USA

France

Germany

Italy

UK

Other

Australia

Spain

Iran

S.Arabia

A BBVA Research model for long-term automobile projections

20

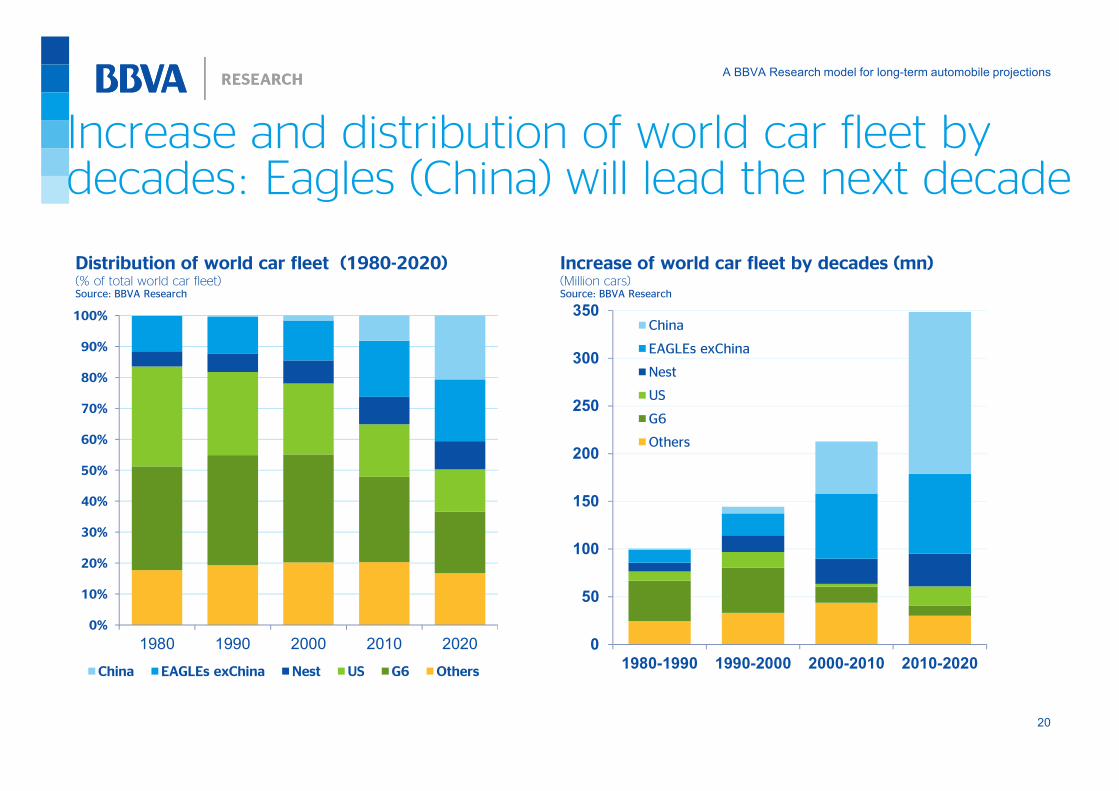

Increase and distribution of world car fleet by decades: Eagles (China) will lead the next decade

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1980 1990 2000 2010 2020

China EAGLEs exChina Nest US G6 Others

0

50

100

150

200

250

300

350

1980-1990 1990-2000 2000-2010 2010-2020

China

EAGLEs exChina

Nest

US

G6

Others

Distribution of world car fleet (1980-2020)(% of total world car fleet)Source: BBVA Research

Increase of world car fleet by decades (mn) (Million cars)Source: BBVA Research

A BBVA Research model for long-term automobile projections

21

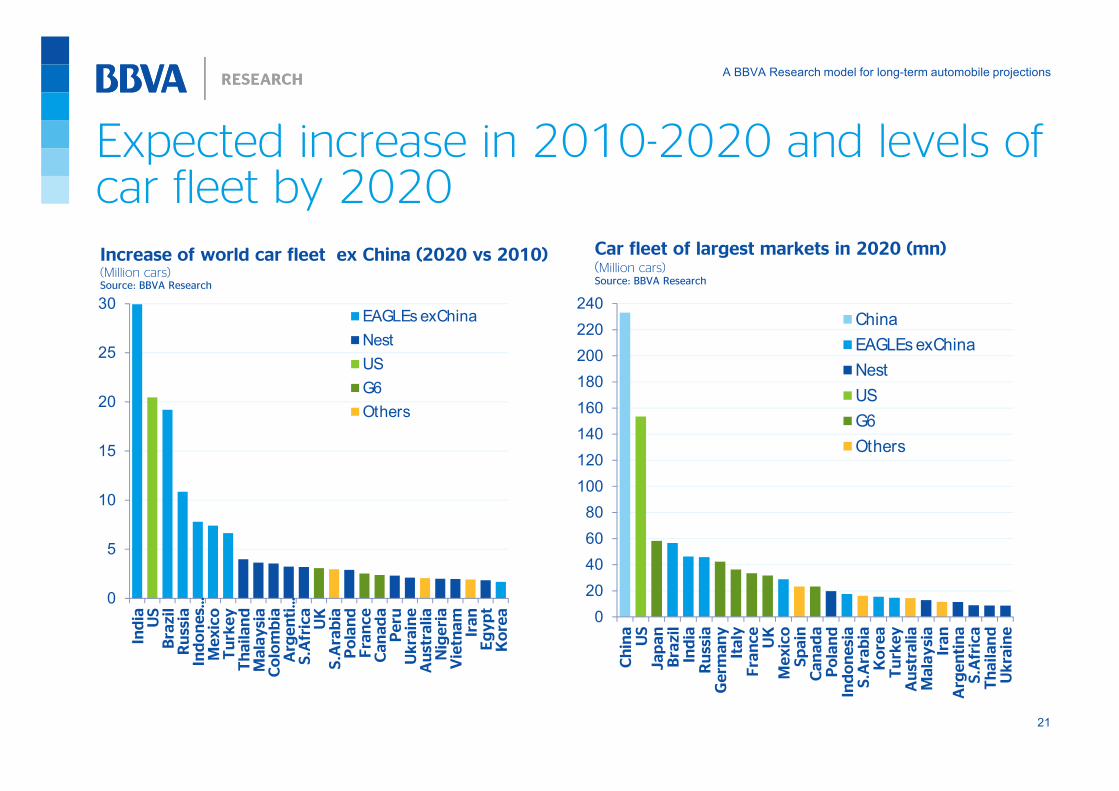

Expected increase in 2010-2020 and levels of car fleet by 2020

0

5

10

15

20

25

30

India US

Brazil

Russia

Indones…

Mexico

Turkey

Thailand

Malaysia

Colombia

Argenti…

S.Africa

UK

S.Arabia

Poland

France

Canada

Peru

Ukraine

Australia

Nigeria

Vietnam

Iran

Egypt

Korea

China

EAGLEs exChina

Nest

US

G6

Others

0

20

40

60

80

100

120

140

160

180

200

220

240

China

US

Japan

Brazil

India

Russia

Germ

any

Italy

France

UK

Mexico

Spain

Canada

Poland

Indonesia

S.Arabia

Korea

Turkey

Australia

Malaysia

Iran

Argentina

S.Africa

Thailand

Ukraine

China

EAGLEs exChina

Nest

US

G6

Others

Car fleet of largest markets in 2020 (mn)(Million cars)Source: BBVA Research

Increase of world car fleet ex China (2020 vs 2010)(Million cars)Source: BBVA Research

A BBVA Research model for long-term automobile projections

22

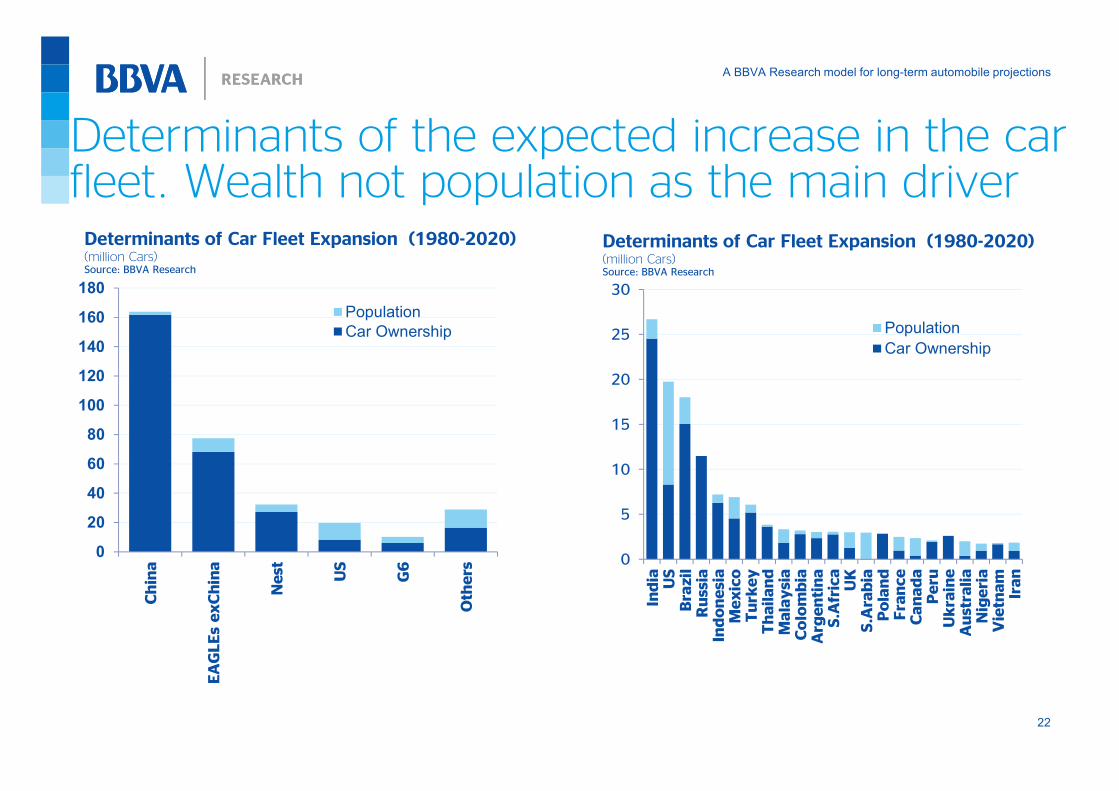

Determinants of the expected increase in the car fleet. Wealth not population as the main driver

0

20

40

60

80

100

120

140

160

180

China

EAGLEs exChina

Nest

US

G6

Others

Population

Car Ownership

0

5

10

15

20

25

30

India US

Brazil

Russia

Indonesia

Mexico

Turkey

Thailand

Malaysia

Colombia

Argentina

S.Africa

UK

S.Arabia

Poland

France

Canada

Peru

Ukraine

Australia

Nigeria

Vietnam

Iran

Population

Car Ownership

Determinants of Car Fleet Expansion (1980-2020)(million Cars)Source: BBVA Research

Determinants of Car Fleet Expansion (1980-2020)(million Cars)Source: BBVA Research

A BBVA Research model for long-term automobile projections

23

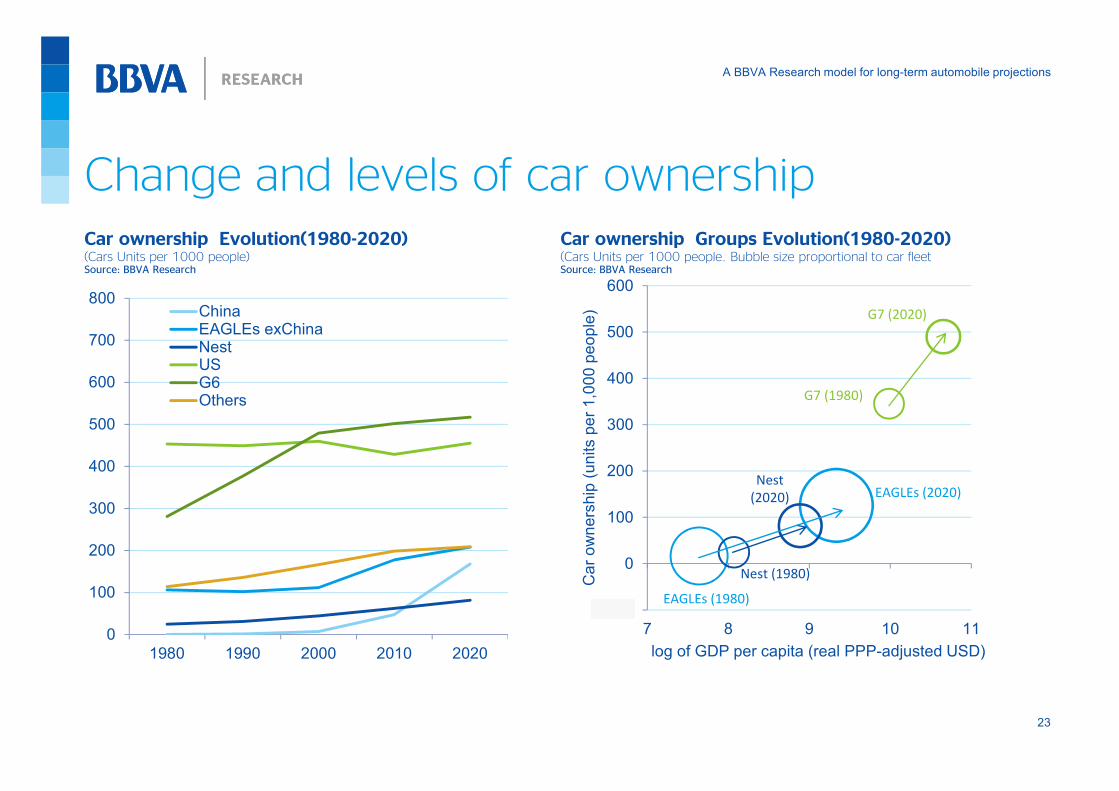

Change and levels of car ownership

0

100

200

300

400

500

600

700

800

1980 1990 2000 2010 2020

ChinaEAGLEs exChinaNestUSG6Others

-100

0

100

200

300

400

500

600

7 8 9 10 11

Car ownership (units per 1,000 people)

log of GDP per capita (real PPP-adjusted USD)

G7 (2020)

G7 (1980)

EAGLEs (2020)

EAGLEs (1980)

Nest (1980)

Nest

(2020)

Car ownership Evolution(1980-2020)(Cars Units per 1000 people)Source: BBVA Research

Car ownership Groups Evolution(1980-2020)(Cars Units per 1000 people. Bubble size proportional to car fleet Source: BBVA Research

A BBVA Research model for long-term automobile projections

24

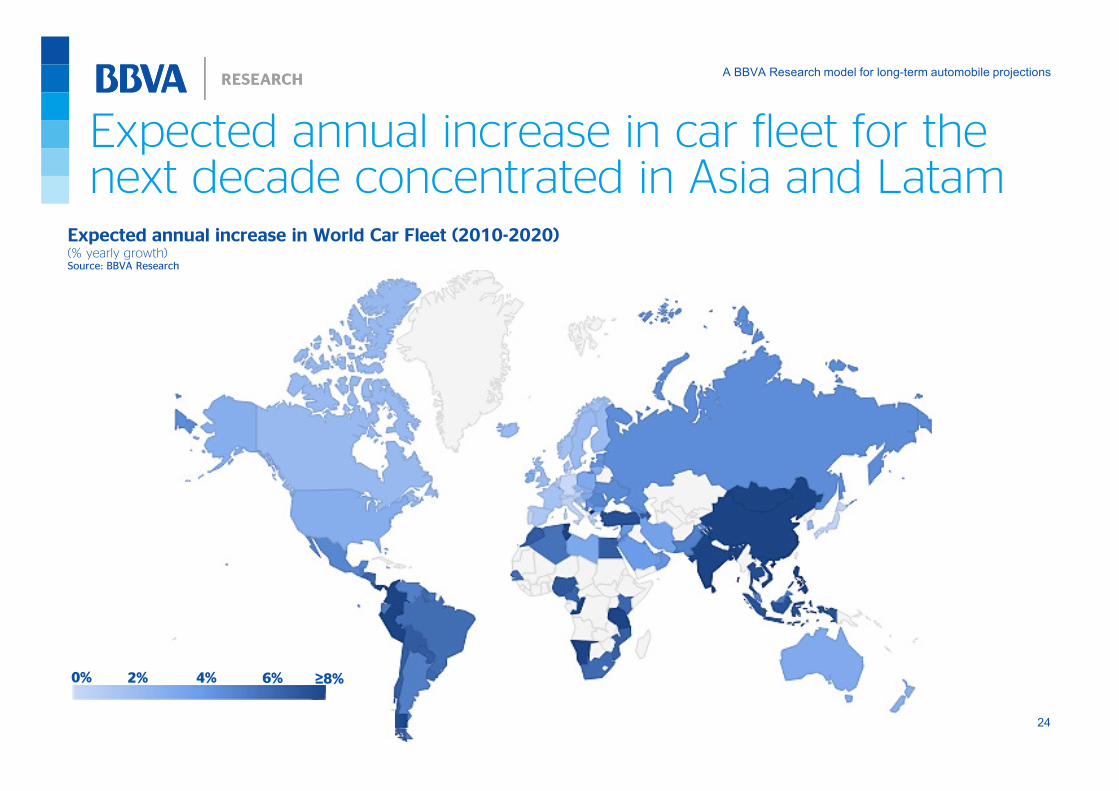

Expected annual increase in car fleet for the next decade concentrated in Asia and Latam

0% ≥8%4%2% 6%

Expected annual increase in World Car Fleet (2010-2020)(% yearly growth)Source: BBVA Research

A BBVA Research model for long-term automobile projections

25

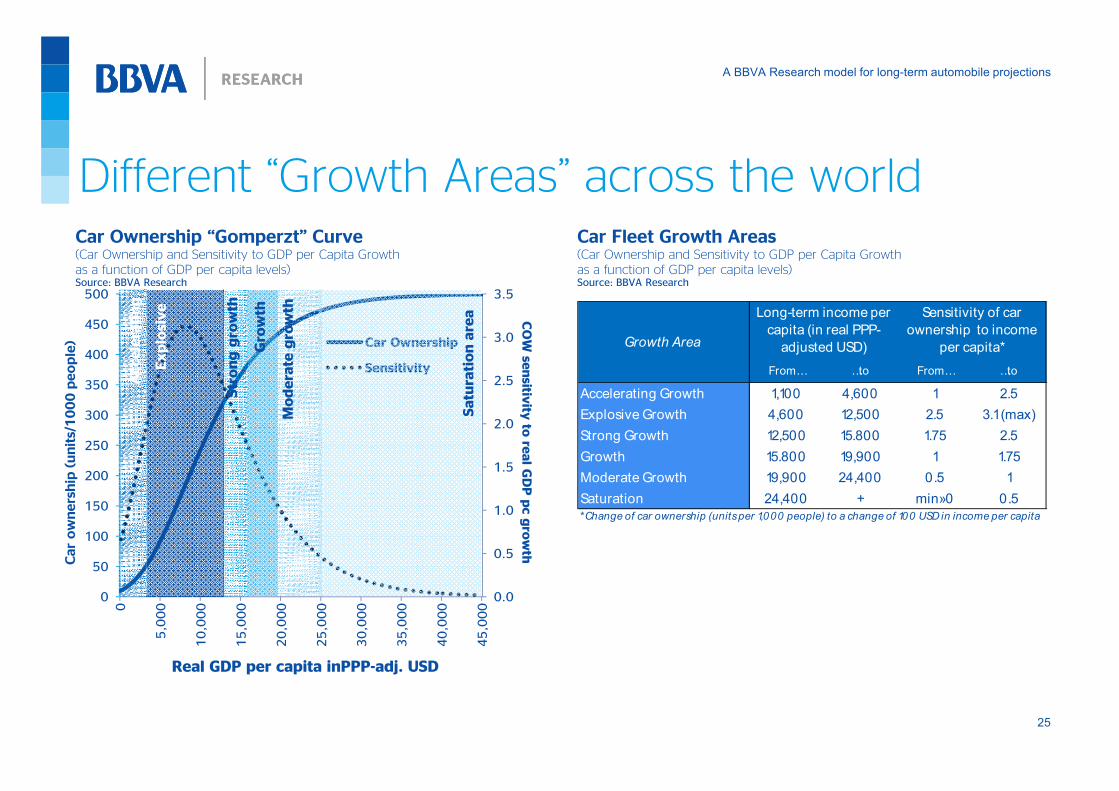

Different “Growth Areas” across the world

From… …to From… …to

Accelerating Growth 1,100 4,600 1 2.5

Explosive Growth 4,600 12,500 2.5 3.1 (max)

Strong Growth 12,500 15.800 1.75 2.5

Growth 15.800 19,900 1 1.75

Moderate Growth 19,900 24,400 0.5 1

Saturation 24,400 + min»0 0.5

*Change of car ownership (units per 1,000 people) to a change of 100 USD in income per capita

Growth Area

Long-term income per

capita (in real PPP-

adjusted USD)

Sensitivity of car

ownership to income

per capita*

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

0

50

100

150

200

250

300

350

400

450

500

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

COW sensitiv

ity to real GDP pc growth

Car ownership (units/1000 people)

Real GDP per capita inPPP-adj. USD

Car Ownership

Sensitivity

Accelerating

Explosive

Strong growth

Moderate growth

Saturation area

Growth

Car Ownership “Gomperzt” Curve(Car Ownership and Sensitivity to GDP per Capita Growth

as a function of GDP per capita levels)Source: BBVA Research

Car Fleet Growth Areas(Car Ownership and Sensitivity to GDP per Capita Growth

as a function of GDP per capita levels)Source: BBVA Research

A BBVA Research model for long-term automobile projections

26

Explosive and strong growth will be concentrated in Asia, Latam and Turkey

From… …to From… …to

Accelerating Growth 1,100 4,600 1 2.5 Bangladesh, Pakistan, Nigeria, Vietnam, Philippines, India, Cameroon, Kenya

Explosive Growth 4,600 12,500 2.5 3.1 (max) Indonesia, Egypt, Ukraine, Thailand, Colombia, China, S.Africa, Peru, Brazil, Paraguay, Bolivia, Ecuador

Strong Growth 12,500 15.800 1.75 2.5 Turkey, Mexico, Panama, Uruguay, Bulgaria, Romania

Growth 15.800 19,900 1 1.75 Malaysia, Chile, Russia, Argentina, Hungary, Croatia, Lithuania, Latvia

Moderate Growth 19,900 24,400 0.5 1 Poland, Portugal, Slovakia, Saudi Arabia, Greece, Estonia, Oman

Saturation 24,400 + min»0 0.5 Korea, G7, Australia, Spain, Switzerland, Netherlands, Czech Republic, Slovenia, New Zealand

*Change of car ownership (units per 1,000 people) to a change of 100 USD in income per capita

Growth Area

Long-term income

per capita (in real

PPP-adjusted USD)

Sensitivity of car

ownership to

income per capita* Countries and Groups

Car Fleet Growth Areas(Car Ownership and Sensitivity to GDP per Capita Growth as a function of GDP per capita levels)Source: BBVA Research

A BBVA Research model for long-term automobile projections

27

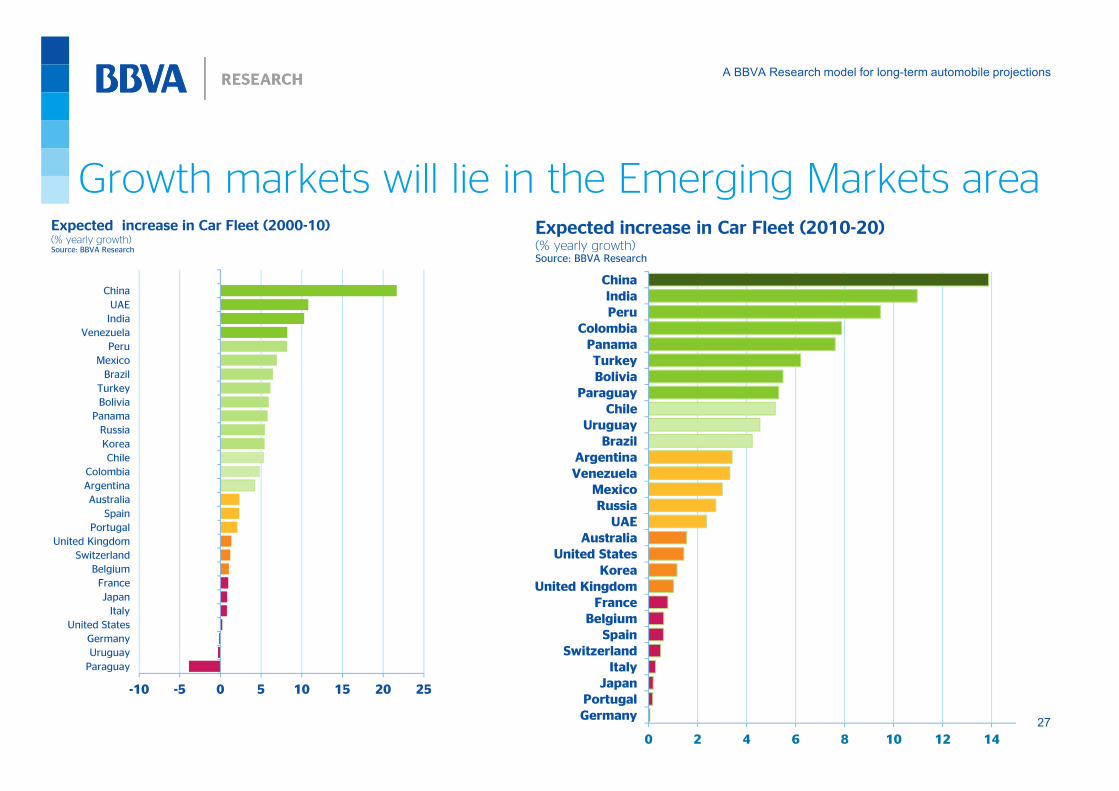

-10 -5 0 5 10 15 20 25

Paraguay

Uruguay

Germany

United States

Italy

Japan

France

Belgium

Switzerland

United Kingdom

Portugal

Spain

Australia

Argentina

Colombia

Chile

Korea

Russia

Panama

Bolivia

Turkey

Brazil

Mexico

Peru

Venezuela

India

UAE

China

0 2 4 6 8 10 12 14

Germany

Portugal

Japan

Italy

Switzerland

Spain

Belgium

France

United Kingdom

Korea

United States

Australia

UAE

Russia

Mexico

Venezuela

Argentina

Brazil

Uruguay

Chile

Paraguay

Bolivia

Turkey

Panama

Colombia

Peru

India

China

Expected increase in Car Fleet (2010-20)(% yearly growth)Source: BBVA Research

Expected increase in Car Fleet (2000-10)(% yearly growth)Source: BBVA Research

Growth markets will lie in the Emerging Markets area

A BBVA Research model for long-term automobile projections

28

Contents

Analysis of long run determinants of Car Industry

Global results

Annex: The BBVA Research CAR Model

A BBVA Research model for long-term automobile projections

29

Literature on car ownership

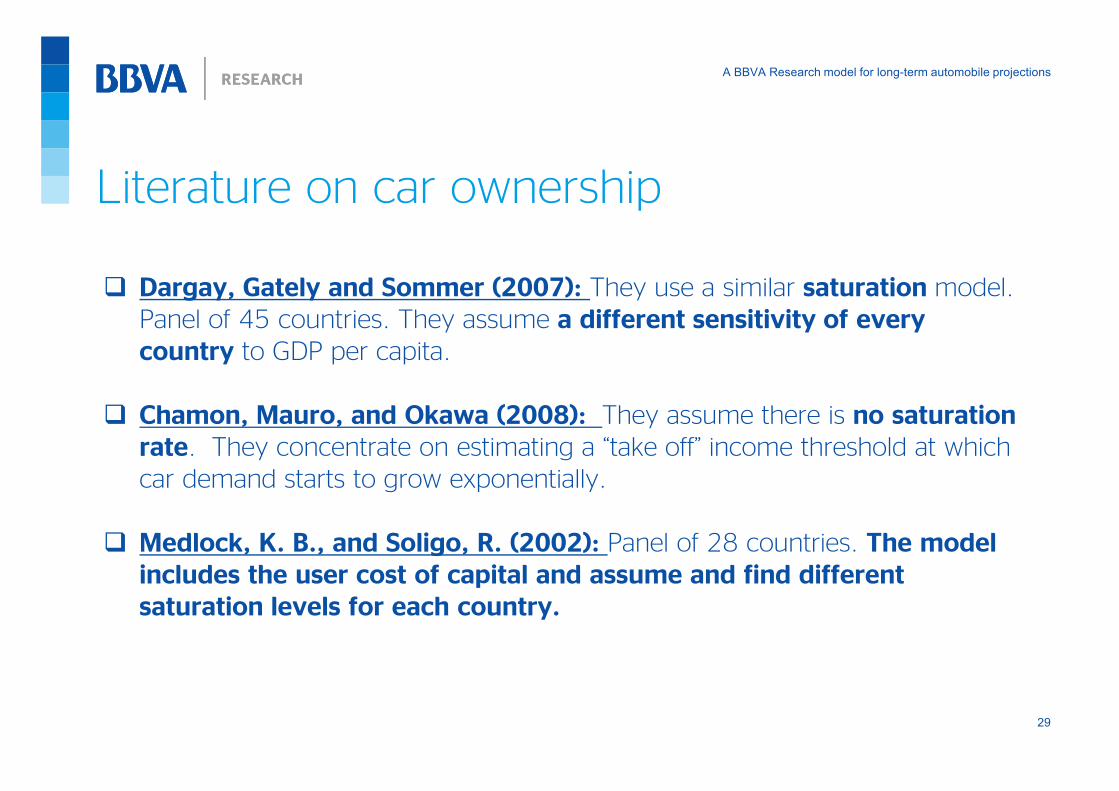

� Dargay, Gately and Sommer (2007): They use a similar saturation model.

Panel of 45 countries. They assume a different sensitivity of every

country to GDP per capita.

� Chamon, Mauro, and Okawa (2008): They assume there is no saturation

rate. They concentrate on estimating a “take off” income threshold at which

car demand starts to grow exponentially.

� Medlock, K. B., and Soligo, R. (2002): Panel of 28 countries. The model

includes the user cost of capital and assume and find different

saturation levels for each country.

A BBVA Research model for long-term automobile projections

30

Enhancements of BBVA Car Model

• We include the level of financial development and an infrastructure

quality indicator as determinants of each country saturation level.

• We associate the saturation level to a long-term or «structural» level of

income instead of the observed GDP per capita.

• We allow short term deviations of income per capita from its

«structural» level to account for short-term variations in car ownership,

instead of relying on the lagged value of the dependent variable to model

short-term dynamics.

A BBVA Research model for long-term automobile projections

31

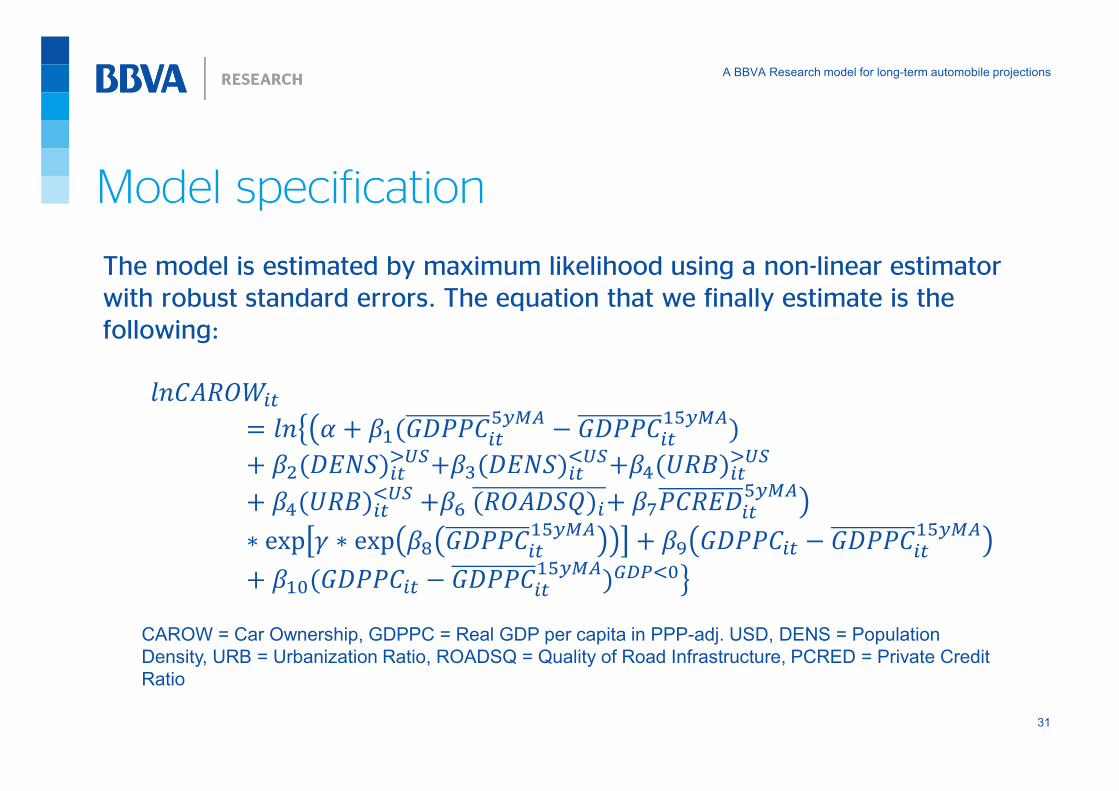

Model specification

The model is estimated by maximum likelihood using a non-linear estimator

with robust standard errors. The equation that we finally estimate is the

following:

�������� ���� � ���������

���� � ������������

� ���������� !��"�������

# !��$�%�&��� !

� �$�%�&��# ! ��' ������(��� �)������

����*∗ exp / ∗ exp �0 ������

����� � �1 ������ � �����������

� ��2������� � ������������345#26

CAROW = Car Ownership, GDPPC = Real GDP per capita in PPP-adj. USD, DENS = Population

Density, URB = Urbanization Ratio, ROADSQ = Quality of Road Infrastructure, PCRED = Private Credit

Ratio

A BBVA Research model for long-term automobile projections

32

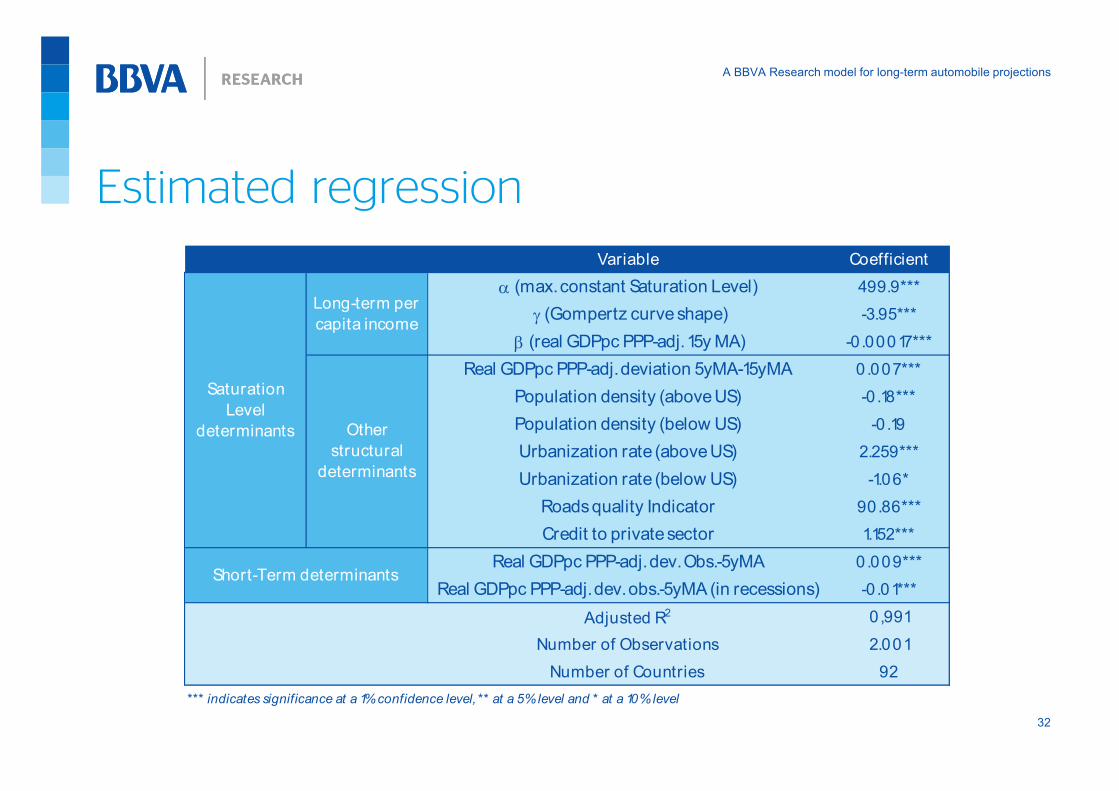

Estimated regression

Variable Coefficient

α (max. constant Saturation Level) 499.9***

γ (Gompertz curve shape) -3.95***

β (real GDPpc PPP-adj. 15y MA) -0 .00017***

Real GDPpc PPP-adj. deviation 5yMA-15yMA 0.007***

Population density (above US) -0 .18***

Population density (below US) -0 .19

Urbanization rate (above US) 2.259***

Urbanization rate (below US) -1.06*

Roads quality Indicator 90.86***

Credit to private sector 1.152***

Real GDPpc PPP-adj. dev. Obs.-5yMA 0.009***

Real GDPpc PPP-adj. dev. obs.-5yMA (in recessions) -0 .01***

Adjusted R2 0,991

Number of Observations 2.001

Number of Countries 92

*** indicates significance at a 1% confidence level, ** at a 5% level and * at a 10% level

Other

structural

determinants

Long-term per

capita income

Short-Term determinants

Saturation

Level

determinants

A BBVA Research model for long-term automobile projections

33

BBVA Research forecasts (2012) compared with previous IMF work (2008)

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

WORLD Advanced Emerging USA* India China

BBVA Research (2012)

IMF (2008)

*BBVA Research uses only passenger cars and not light trucks

0

100

200

300

400

500

600

700

800

900

1000

1100

1200

WORLD Advanced Emerging USA* India China

BBVA Research (2012)

IMF (2008)

Car fleet of largest markets in 2020 (Million cars)Source: BBVA Research

Growth of Car fleet (2010-2020) (average % yoy)Source: BBVA Research

A BBVA Research model for long-term automobile projections

34

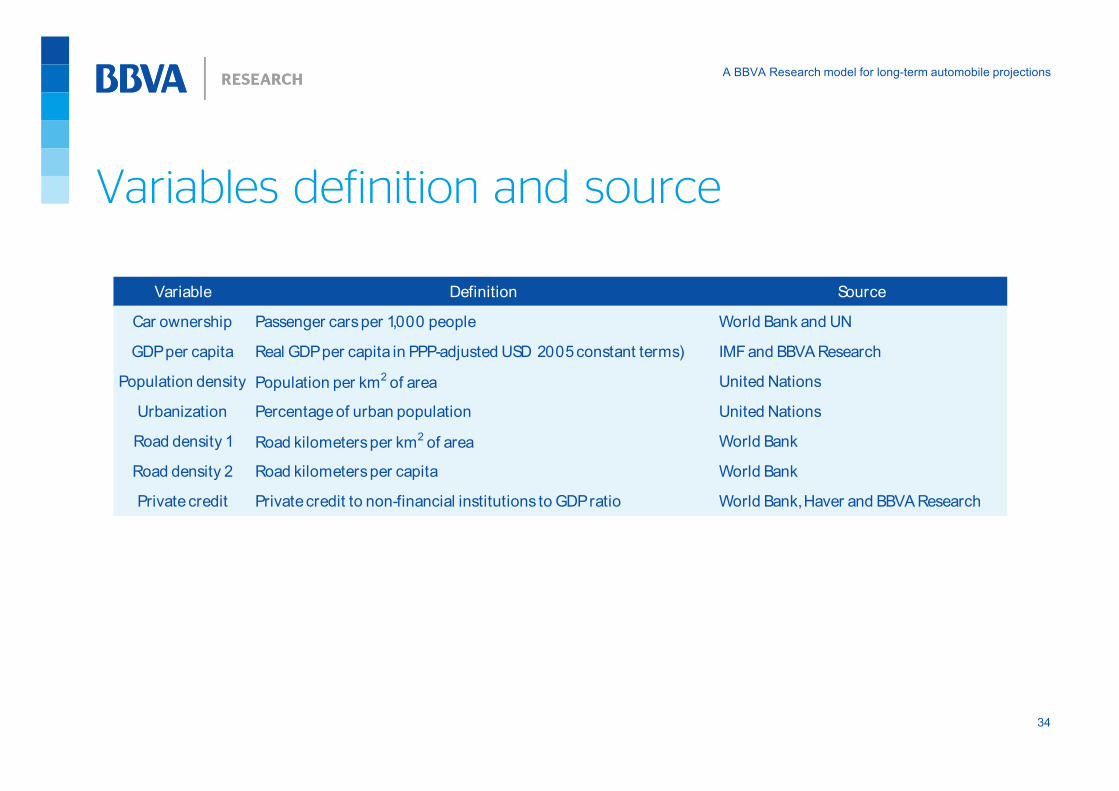

Variables definition and source

Variable Definition Source

Car ownership Passenger cars per 1,000 people World Bank and UN

GDP per capita Real GDP per capita in PPP-adjusted USD 2005 constant terms) IMF and BBVA Research

Population density Population per km2 of area United Nations

Urbanization Percentage of urban population United Nations

Road density 1 Road kilometers per km2 of area World Bank

Road density 2 Road kilometers per capita World Bank

Private credit Private credit to non-financial institutions to GDP ratio World Bank, Haver and BBVA Research

A BBVA Research model for long-term automobile projections

35

Cross-country emerging markets analysis unit

Chief Economist

Álvaro Ortiz [email protected] +34 630144485 Ext 51933

Senior Economist

David Martínez Turé[email protected]+34 690 845 429

SeniorEconomist

Alfonso Ugarte [email protected]+34 91 3743530