the man of action from nedlacafrica scored its highest ever economic freedom ranking in the economic...

TRANSCRIPT

© 2018 C Divaris/The Electronic Publishing Corp CC Postnet Suite 72 Private Bag X87 BRYANSTON 2021 Phone 011-234-2434 Fax 086-515-0955 [email protected].

To subscribe (free), e-mail ‘subscribe’ to [email protected]. By supplying your e-mail address, you agree to receive e-mail notifications of forthcoming seminars and related offers from Bsp Seminars®. You can unsubscribe at any time by e-mailing ‘unsubscribe’ to the same address.

—An irreverent newsletter designed to keep you up to date—

&

The Man Of Action From Nedlac Synchronized breathing comes to the Union Buildings.

MONTHLY LISTING Latest Legislation & Legislative Material To Emerge Or To Be Found Since Issue #180

This is a free publication devoted to unearthing what is going on in the SA tax field. If it isn’t here, it never happened.

Unless otherwise indicated (‘§’), every document listed is cumulatively included in the Tax Shock, Horror Database, which is available monthly, quarterly or even individually, on DVDs, by post, for R260 a month inclusive of VAT at 15%.

This is perhaps the only newsletter in the world with its own stylebook (also free), by Costa Divaris & Duncan McAllister (2015 ed). Bsp Seminars® publications—tax and tax-related acts, books, databases and newsletters by and compiled by Costa Divaris.

All past issues from 2009 to date. All cases listed in this section from 2006 to date. Visit our website.

Act 09 May 1980: Deeds Registries Amendment Act 44 of 1980. Act 06 November 1981: Income Tax Act 96 of 1981. Act 06 November 1981: Revenue Laws Amendment Act 99 of 1981. Act 06 November 1981: Customs & Excise Amendment Act 114 of 1981. Act 17 March 1982: Deeds Registries Amendment Act 27 of 1982. Act 16 June 1982: Customs & Excise Amendment Act 86 of 1982. Act 16 June 1982: Revenue Laws Amendment Act 87 of 1982. Act 23 June 1982: Income Tax Act 91 of 1982. Act 02 March 1983: Perishable Products Export Control Act 9 of 1983. Act 06 July 1983: Customs & Excise Amendment Act 89 of 1983. Act 13 July 1983: Revenue Laws Amendment Act 92 of 1983. Act 13 July 1983: Income Tax Act 94 of 1983. Act 01 March 1984: Income Tax Amendment Act 30 of 1984. Act 25 July 1984: Matrimonial Property Act 88 of 1984. Act 13 June 1986: Customs & Excise Amendment Act 52 of 1986. Act 04 July 1986: Income Tax Act 65 of 1986. Act 04 July 1986: Revenue Laws Amendment Act 71 of 1986. Act 19 September 1986: Taxation Laws Amendment Act 108 of 1986. Act 11 March 1987: Currency & Exchanges Amendment Act 23 of 1987. Act 14 October 1987: Intestate Succession Act 81 of 1987. Act 14 October 1987: Customs & Excise Amendment Act 84 of 1987. Act 14 October 1987: Income Tax Act 85 of 1987. Act 14 October 1987: Taxation Laws Amendment Act 86 of 1987. Act 29 April 1988: Currency & Exchanges Amendment Act 48 of 1988. Act 29 June 1988: Customs & Excise Amendment Act 69 of 1988. Act 13 July 1988: Taxation Laws Amendment Act 87 of 1988. Act 15 July 1988: Income Tax Act 90 of 1988. Act 30 September 1988: Income Tax Amendment Act 99 of 1988. Act 23 March 1989: Deeds Registries Amendment Act 24 of 1989. Act 21 June 1989: Customs & Excise Amendment Act 68 of 1989. On these items 21 June 1989: Acts in the Tax Shock, Horror Database improved. Missing notice 2017: I cannot find the annual notice to furnish normal tax returns for 2017. High Court case 26 May 2017: Carte Blanche Marketing CC and Others v CSARS (26244/2015)

[2017] ZAGPPHC 253 (171, 172 TSH 2017). See 26, 27, 28 TAW 2017. FIC annual report 28 September 2017: Financial Intelligence Centre annual report 2016/16. FIC publications 05 February 2018: Online scams. Tax court case 13 February 2018: TC IT 13726. SARS attacks yet another ‘Gentleman Farmer’,

or so it thought. But the judgment is screwy, purporting to reach a substantive outcome, under an interlocutory application! Even the assessor got it wrong.

Issue: 181 Tax Shock Horror Database—18 683 items (5,77 GB)—3 291 subscribers April 2018

181 Tax Shock, Horror 2018—April—2

—An irreverent newsletter designed to keep you up to date—

See 17, 18 TAW 2018.* FIC release 26 February 2018: Outcomes of the February 2018 meeting of the FATF. SARS presentation March 2018: Health promotion levy—sugary beverages levy (SBL)—customs. SARS presentation March 2018: Health promotion levy—sugary beverages levy (SBL)—excise. FIC notice 08 March 2018: Updated guidance on the mode of communication regarding

ss 27, 32, 34 & 35 of the Financial Intelligence Centre Act. On PCC 38A. FIC PCC 38A 08 March 2018: PCC 38A. FIC publication 09 March 2018: Money laundering typologies & indicators. Hardly. Looks more

like instances of common fraud. SARS EM 12 March 2018: Explanatory memorandum on the health promotion levy—

amendment of part 7A of Schedule no 1, Schedule nos 4, 5 & 6 of the C&EA. SARS practitioners 15 March 2018: Last payment date for March 2018 (180 TSH 2018). It’s

pathetic. The ‘authority’ for this unlawful declaration by SARS was perhaps seen as being s 245 of the Tax Administration Act. Small problems: it’s a power vested in the Minister, not the Commissioner, & it may be exercised only by way of a ‘public notice’, that is, what we used to call the Government Gazette.

IRBA release 18 March 2018: IRBA Act amendments will strengthen oversight powers. And pigs will fly.

GN R 341 GG 41515 23 March 2018: Amendment of rules (DAR 172). Under ss 54F, 54J & 120 of the Customs & Excise Act. (Health promotion levies, or SBL.)*

Treasury release 23 March 2018: Publication for comment of the draft amendments to the regulations to be made in terms of the Long-Term Insurance Act of 1998 & Short-Term Insurance Act of 1998.

SCA case 27 March 2018: Lion Match Company (Pty) Ltd v CSARS (301/2017) [2018] ZASCA 36 (180 TSH 2018). See 15 TAW 2018.

SCA case 28 March 2018: CSARS v Danwet (399/2017) [2018] ZASCA 38 (180 TSH 2018). See 16 TAW 2018.

SCA case 28 March 2018: CSARS v The Executors of Estate Late Sidney Ellerine (142/2017) [2018] ZASCA 39. Now picked up in the SARS ‘What’s New’ page.*

FIC notice 28 March 2018: Updated guidance on registration with the FIC in terms of s 43B of FICA by accountable & reporting institutions & acquisition of login credentials by any other business with a reporting obligation under the act. On the draft PCC 05C.

FIC draft PCC 28 March 2018: Draft PCC 05C. GN 396 GG 41544 28 April 2018: Cross-border Road Transport Act: permit tariff fee regulations,

2018. The crazy transport policies of the Apartheid era endure.§ DTC report 29 March 2018: Closing report on the work done by the Davis Tax Committee. DTC report 29 March 2018: Feasibility of a wealth tax in SA. DTC report 29 March 2018: Final report on VAT for the minister of finance. DTC report 29 March 2018: Report on the PBO & the tax system for the MOF. fin24 29 March 2018: Did SARS Gupta VAT refund break financial law?§ AGSA website April: We’ve revamped! I certainly hope so. I am hardly ever able to find

anything on this site. (Nothing much seems to have changed.) SAICA website April: A new website entirely. fin24 01 April 2018: SARS accuses Guptas of lying.§ Business Day 02 April 2018: Former SARS trio to state their case to NPA—they wanted the

charges stayed pending a review of the decision to prosecute.§ Treasury speech 03 April 2018: Launch of the prudential authority. By this week’s MOF. Treasury speech 03 April 2018: Minister’s speech at the SARS 2017/18 preliminary revenue

outcome announcement. Ditto. SARS release 03 April 2018: SARS announces R1 216,6 billion preliminary revenue outcome:

Every year SARS implements comprehensive initiatives to optimize revenue collections. The short-term Special Voluntary Disclosure Program, initiated to offer taxpayers the opportunity to declare off shore wealth raised R2,9 billion in taxes in the financial year from 827 processed SVDP applications from the 2 024 applications received. The ongoing Voluntary Disclosure Program continues to perform well and has realized R10,8 billion since 2012 when the VDP was launched.

SARS collected more than R0,8 billion from the national Prominent Business Individuals project. This initiative was developed to ensure an end-to-end view of a taxpayer’s business profile and hence tax liability.

Invoking paragraph 19(3) of the Fourth Schedule of the Income Tax Act, SARS may request additional payments from provisional taxpayers based on the latest estimates of financial performance. This year SARS collected R10,7 billion from Paragraph 19(3) interventions.

The para 19(3) people at SARS are the Provisional Tax Mafia. They are lawless.*

181 Tax Shock, Horror 2018—April—3

—An irreverent newsletter designed to keep you up to date—

Mail & Guardian 03 April 2018: Scorpio: The Moyane Dossier, Part 2—Gupta VAT payments unpacked—Six red flags Moyane & Mokoena chose to ignore.§

SARS table updated 04 April 2018: Interest rates—Table 3.* Moneyweb 04 April 2018: Bobroffs score sequestration victory—a clear misjoinder of the

two respondents—judge.§ FMF 04 April 2018: SA is not capitalist, but needs to be. By Martin van Staden:

In the late 1980s, and especially after the first democratic election in 1994, South Africa did embrace a freer market. This continued up to the year 2000, when South Africa scored its highest ever economic freedom ranking in the Economic Freedom of the World index, published by the Canada-based Fraser Institute. Prosperity was within grasp, yet evading us because of draconian labour legislation that adopted Apartheid logic almost verbatim.§

news24 04 April 2018: SARS ‘rogue unit’ officials to appear in court, after withdrawing urgent application.§

SARS website 05 April 2018: Customs & Excise Act: The Tariff Amendment Notice, scheduled for publication in the Government Gazette, relates to the amendments to— Part 1 of Schedule No 1, by the substitution of tariff subheadings 1001.91 and

1001.99 as well as 1101.00.10 and 1101.00.90 to reduce the rate of customs duty on wheat and wheaten flour from 71,63c/kg and 107,45c/kg to 39,49c/kg and 59,23c/kg respectively, in terms of the existing variable tariff formula—Minute 01/2018.*§

Moneyweb 05 April 2018: Concern about non-compliant tax practitioners. SARS measures ‘noncompliance’ by what its records show about outstanding returns & payments. It is clueless about real noncompliance. Not so tax practitioners.§

Treasury release 06 April 2018: The launch of Twin Peaks. Treasury speech 06 April 2018: Address to staff at launch of the Financial Sector Conduct

Authority (née FSB). By this week’s MOF. SARS website 06 April 2018: Customs & Excise Act:

Publication details for Tariff Amendment Notice R 422, as published in Government Gazette 41564, are now available.*§

SARS release 06 April 2018: SARS’s stance on the tax treatment of cryptocurrencies. How can you exclude the VAT system, even if temporarily?*

GN 177 GG 41567 09 April 2018: Notice & order of forfeiture. Ukwakha Building & Construction (Pty) Ltd loses $625 081,36 under the EXCON regulations.

GN 178 GG 41567 09 April 2018: Notice & order of forfeiture. Insephe Construction Services (Pty) Ltd loses $398 444,32 under the EXCON regulations.

Business Day 09 April 2018: Former SARS trio to appear in court.§ BusinessReport 09 April 2018: Former SARS executives say they were vilified.§ news24 09 April 2018: Former SARS officials accused of spying on Scorpions.§ Treasury release 10 April 2018: Appointment of Mr Monale Ratsoma as NDB Director-General.

This is the BRICS New Development Bank. Business Day 10 April 2018: Suspended SARS boss Tom Moyane key witness in ‘rogue unit’

trial.§ Daily Maverick 10 April 2018: The case against the NPA’s case against Pillay, van

Loggerenberg & Janse van Rensburg.§ DTC report 11 April 2018: The efficiency of SA’s corporate income tax system. SARS release 11 April 2018: SARS to host BRICS heads of customs authorities.* DTC release 12 April 2018: The Davis Tax Committee concludes its work within 5 years. DTC note 12 April 2018: Davis Tax Committee note on territorial taxation. DTC tsatske 12 April 2018: An extract from a book published by Juta.§ On these items 12 April 2018: I remain committed to studying all of this stuff as soon as I’ve

read the last report of the Katz Commission, which I continue eagerly to await. Eyewitness News 12 April 2018: KPMG suspends top exec over VBS liquidity crisis—the SARB has

red-flagged the bank, saying that nearly R1 billion cannot be accounted for.§ fin24 12 April 2018: Manuel: I am no suspect in SARS spy case.§ SARB release 13 April 2018: SARB commissions forensic investigation into VBS Mutual Bank.

Spilt milk. How about investigating why the SARB failed to see VBS coming? GN 179 GG 41571 13 April 2018: Imposition of levy on perishable products. Under s 17(1) of the

Perishable Products Export Control Act.§ SARS release 13 April 2018: Drugs valued at over R30 million bust at OR Tambo this week.* BusinessReport 13 April 2018: Trevor Manuel: I am a witness, not a suspect in SARS case.§ Moneyweb 13 April 2018: Taxpayer rights get boost from the courts. By Amanda Visser,

who really should try & get hold of a copy of 17 TAW 2018, on TC IT 13726.§ Daily Maverick 13 April 2018: amaBhungane: Nkonki CEO resigns after we expose Gupta

181 Tax Shock, Horror 2018—April—4

—An irreverent newsletter designed to keep you up to date—

fronting deal.§ CIPC Notice 15 14 April 2018: B-BBEE applications via e-services. Business Insider 14 April 2018: Two KPMG partners with a combined 26-year history at the firm

have quit amid the growing VBS Mutual Bank scandal.§ CIPC Notice 16 16 April 2018: Finally deregistered companies & close corporations which fails

[sic] to file annual returns within 30 business days after the [successful] processing of application for re-instatement of deregistered company (form COR 40.5).

Treasury release 16 April 2018: Government’s response to the rating action of Rating & Investment Information, Inc (R&I):

Government notes and welcomes R&I’s decision to affirm South Africa’s long term foreign currency debt rating at ‘BBB’ and local currency debt rating at ‘BBB+’ and to also revise the outlook to stable from negative.

Brimming with bullshit. I reckon these rating agencies are mega-dumb. SARS release 16 April 2018: SARS, NPA to prosecute taxpayers for outstanding returns. Much

as I love him, the current Commissioner has as little understanding of the rule of law as his (recent) predecessors. It is not a criminal offence to fail to submit a return. That is merely a shorthand expression for a more complex idea.*

AGSA release 17 April 2018: Auditor-General of South Africa terminates its auditing contracts with audit firms, KPMG & Nkonki Inc:

[Auditor-General] Makwetu says recent media reports relating to the external audit of VBS Mutual Bank and the conduct of KPMG audit partners are some of the reasons that prompted the decision to withdraw all KPMG audit mandates with immediate effect.

On the termination of Nkonki Inc’s contract, Makwetu said recent media reports on matters arising from the shareholder transactions involving the firm were of ‘grave concern and pose significant risk on the reputation of my office through the statutory audits contracted’ to Nkonki Inc.

DTC letter 17 April 2018: Subject: article on the Davis Tax Committee’s wealth tax report. Letter to the editor of Business Day. (I hope that Davis AJA does not read the Tax Administration Weekly, where I have recently pointed out some of his blunders.) Having enjoyed all the time in the world to write a judgment or report, a judge, I think, should take his or her lumps, with silent fortitude.

dti release 17 April 2018: More companies are fronting their workers—BEE Commissioner Ntuli:

The Commissioner of the Broad-Based Black Economic Empowerment (BBBEE) Commission, Ms Zodwa Ntuli says more and more companies are fronting their employees through trusts. Ntuli was speaking in Parliament today where she briefed Members of Parliament belonging to the Select Committee on Trade and International Relations on the work of the Commission since its inception in 2016.

I have never, ever seen one of these trusts that works. They are all rubbish, in trust law. Nor have I ever met anyone who checked whether they work for BEE.

dti release 17 April 2018: the dti agrees to delink the Y.E.S & the bursary target of 2,5%: [T]he dti is inviting members of the public to participate in a public commentary process on the proposed amendments to the B-BBEE Codes of Good Practice on or before 29 May 2018. The proposed amendments aim to promote innovative ways to increase the participation of black South Africans and in particular black youth in the economy. Key to these amendments is the Youth Employment Service (Y.E.S) initiative and the introduction of a ring-fenced Point indicator on the skills development Scorecard for 2,5% spend target on Bursaries for Black Students attending Higher Education Institutions.

Dr Red Rob must surely have the most-fun job in the land, spending other peoples’ money with abandon, yet he appears these days to be highly stressed.

SARB release 17 April 2018: SARB & the Bank of England agree to co-operate: The South African Reserve Bank (SARB) has agreed to cooperate with the Bank of England (BoE) on training and technical assistance as part of a pilot project funded by the UK Department for International Development (DFID) aimed at providing assistance to central banks in selected African countries.

FMF 17 April 2018: SA should follow winners, not losers. By Leon Louw & Martin van Staden:

Nationalization of property, inefficient State-owned enterprises, raising the legal drinking age from 18 to 21, and higher taxes in a low-growth environment. These ideas have all been tried elsewhere. And they have failed consistently, with few exceptions. The opposite of these ideas: strong protections for private property, an active and entrepreneurial private sector, personal freedom, and low taxes, have also

181 Tax Shock, Horror 2018—April—5

—An irreverent newsletter designed to keep you up to date—

been tried quite widely, and, essentially, everywhere they have been tried, they have worked. Why, then, does South Africa insist on following the losers and not the winners?§

SARS guide updated 18 April 2018: Guide to understatement penalties (Issue 2). I very much doubt it, even if they bring it out monthly (180 TSH 2018).*

SARB speech 19 April 2018: The fintech phenomenon: five emerging habits that may influence effective fintech regulation. By Francois Groepe.

SARB release 19 April 2018: South African Reserve Bank notes recent KPMG developments: The South African Reserve Bank (SARB) has noted the recent developments regarding KPMG and in particular its audit of VBS Mutual Bank. The SARB continues to engage with KPMG as well as with banks that use KPMG as their auditors.

SARS release 19 April 2018: BRICS members to strengthen customs co-operation. They certainly need to find something they can keep themselves busy with.*

GN 435 GG 41581 20 April 2018: Prescribed rate of interest (s 1 of the Prescribed Rate of Interest Act). For the purposes of s 1(1), the rate of interest is set at 10% pa as from 1 May 2018. See the Lost & Found section.

SAGNA release 20 April 2018: President makes swift return amid Mahikeng protests: President Cyril Ramaphosa has cut his trip short to the Commonwealth Heads of Government Meeting (CHOGM) in London to attend to the protests that have engulfed Mahikeng in the North West province.

SARB release 20 April 2018: Notice of the resignation of the curator of Residual Debt Services Limited & appointment of a new curator:

As per the African Bank website, RDS is the same legal entity as the former African Bank Limited. It was renamed on 4 April 2016, when the old African Bank surrendered its banking license under the Bank Act, 94 of 1990.

GN R 429 GG 41577 20 April 2018: Amendment of rules (DAR 175). Under ss 8 & 120 of the Customs & Excise Act. (Section 8 matters.)*

GN R 430 GG 41577 20 April 2018: Amendment of rules (DAR 173). Under ss 64E & 120 of the Customs & Excise Act. (Accredited client status.)*

GN R 431 GG 41577 20 April 2018: Amendment of rules (DAR 174). Under ss 47(9)(a)(iv)(ff) & 120 of the Customs & Excise Act. (Alcoholic beverages.)*

On these items 20 April 2018: I am missing DAR 171. Or SARS is. GN 451 GG 41583 20 April 2018: Notice & order of forfeiture. Ukuzuza Trading (Pty) Ltd loses

R31 300 602,36 under the EXCON regulations. SARS BPR 301 20 April 2018: Taxation of dividends received by a borrower under a securities

lending arrangement. Duh. Good grief, man! Couldn’t you just look it up?* SARS release 20 April 2018: New electronic reporting requirements for customs clients.* PPSA tsatske 21 April 2018: Op ed. What politics does Mpumelelo analyse? By Sibusiso

Nyembe, seemingly a special adviser to the public protector, defending the boss. Like almost everything to do with the PPSA, really, really weird.§

SAGNA release 21 April 2018: President asks for more time to resolve Mahikeng protests. DAFF release 23 April 2018: Suspended director-general resumes his duties today:

After the Director-General approached the high court again in November 2017 the matter was struck off the urgent court roll for lack of urgency. According to the order of the High Court it was declared that: 1. the Minister lacked the authority to suspend the Director-General 2. the suspension was unlawful, invalid and of no force and effect 3. the precautionary suspension of the Director-General was set aside with

immediate effect 4. the Minister lacked the authority to institute disciplinary proceedings against the

Director-General and such proceedings were unlawful, invalid and were set aside 5. the Minister is to allow the Director-General to resume his duties with immediate

effect 6. the Minister is called upon to show cause on affidavit on or before 15 May 2018

why a. he should not be joined in his personal capacity and b. he should not pay the costs of the application from his own pocket.

Today the suspended Director-General Mr Michael Mlengana has reported for duty. Some valuable lessons in law here. AGSA release 25 April 2018: Auditor-General of South Africa (AGSA) sets the record straight on

the termination of contracts with audit firms KPMG & Nkonki Inc: [Auditor-General] Makwetu says, contrary to these misleading statements that seek to project his office’s decision to terminate these contracts as irrational and unsympathetic, his office had given the affected audit firms ample time to explain the matters that were raised with them on the slew of unflattering governance issues

181 Tax Shock, Horror 2018—April—6

—An irreverent newsletter designed to keep you up to date—

raised against them. The acting CEO & ‘leadership’ of Nkonki Inc ‘did not know of & were not involved

in all the transactions that took place in 2016, including the payments that were made between the buyer & sellers’. The firm’s ISQC 1 (don’t ask) report ‘was not forthcoming’. Section 38 of the Audit Professions Act ‘was not adhered to’, on the issue of the supposedly restricted ownership of registered auditing firms (I’ve been wondering when someone would raise that issue). As for KPMG, there was no sign that the IRBA & SAICA ‘sponsored investigations would be concluded ahead of our statutory audit sign-off dates’:

This was also compounded by the findings that were made on the VBS Mutual Bank, which also triggered other actions that were widely publicized.

CASAC release 25 April 2018: CASAC [Council for the Advancement of the SA Constitution] seeks personal costs order against Public Protector (read on):

CASAC is a seeking a punitive personal costs order against Public Protector, Adv Busisiwe Mkhwebane, in its application to review and set aside the Report on the Vrede Dairy Farm.§

SARB review 25 April 2018: Financial stability review. First edition 2018.§ SARB speech 25 April 2018: At financial stability forum. By Francois Groepe:

Overall, despite some headwinds from a moderate economic growth scenario and some remaining fiscal challenges, the South African financial sector is assessed as strong and stable. The sector is characterised by well-regulated, highly capitalized, liquid and profitable financial institutions, supported by a robust regulatory and financial infrastructure.

SARB paper 25 April 2018: Aggregate public-private remuneration patterns in SA.§ Treasury review 25 April 2018: Terms of reference for the independent panel of experts for the

review of current list of VAT zero-rated food items. Times Select 25 April 2018: Revealed: Guptas claimed another R89 m in VAT.§ Business Day 25 April 2018: Parliament told there are other options to help the poor than VAT

zero-rating—Judge Dennis Davis says the rich benefit disproportionately from the zero-rated items. Yet costs do not determine prices.§

SARS website 26 April 2018: Customs & Excise Act: The Tariff Amendment Notice, scheduled for publication in the Government Gazette, relates to the amendments to— General Notes to Schedule No 1, by the substitution of Table 1 in paragraph 3.1 to

Note IJ to implement the SACU allocation of cheese tariff rate quota under the EPA agreement between the EU and SADC EPA states.*§

SARS FAQs 25 April 2018: FAQs: increase in the VAT rate (issue 4).* GN 459 GG 41593 26 April 2018: Administration of estates: amendment regulations. Under s 103

of the Administration of Estates Act. SAGNA release 26 April 2018: Government intervenes to stabilize North West:

Government has approved two immediate interventions to restore order and stability in communities of the North West province. One of the interventions includes a task team of Ministers, which will be dispatched to visit the North West to establish the facts on the ground.… Another intervention that government has introduced is the invoking of Section 100(1)(b) of the Constitution to address the apparent crisis, particularly in the health sector.

That’s a national intervention in provincial administration. Real action stuff—a ministerial excursion, & a procedure not yet known to make any difference.

GN 208 GG 41593 26 April 2018: Rate of interest on government loans. Under s 80(1)(a) & (b) of the Public Finance Management Act, the Standard Interest Rate is fixed at 10%, as 1 May 2018. See the Lost & Found section.

BN 53 GG 41593 26 April 2018: Adjustment of statutory limit on claims for loss of income & loss of support. Under s 17(4)(c) of the Road Accident Fund Act, to R270 285 (R266 200) as from 30 April 2018. (TSHD ‘Thresholds’ schedule updated.)

SARS website 26 April 2018: Customs & Excise Act: Publication details for Tariff Amendment Notice R 462, as published in Government Gazette 41599, are now available.*§

SARS BPR 302 26 April 2018: Corporate restructuring & unbundling of listed shares. SAGNA release 27 April 2017: SA dealing decisively with corruption:

South Africa is fixing itself by addressing corruption and maladministration. Wow! Further excerpts:

‘We must remember that the introduction of the National Minimum Wage will increase the income of over six million working South Africans. A wage increase of that size and extent is unprecedented in our history, and we must celebrate it.’ ….

With regards to land, President Ramaphosa said economic freedom means that the

181 Tax Shock, Horror 2018—April—7

—An irreverent newsletter designed to keep you up to date—

land that was taken from black South Africans needs to be returned. He committed to accelerating the redistribution of land, both in urban and rural areas, to ensure that poor South Africans are able to own land and have the means to work it. He said government will land expropriation without compensation where it is necessary and justified. ‘We call on all South Africans to be part of the broad process of consultation on how we should implement this decision in a way that makes redistribution meaningful and which contributes to a stronger economy, greater agricultural production and improved food security.’ The move is aimed at extending property rights to all South Africans.

Who would have thought we’d come to miss the other chap, & so soon? PPSA release 30 April 2018: Adv Mkhwebane rejects CASAC’s claims:

Public Protector Adv Busisiwe Mkhwebane has noted with concern and disappointment the claims [levelled] against her by the Council for the Advancement of the South African Constitution (CASAC) in a widely publicized media statement dated 25 April 2018. Although the matter is before the courts, and therefore sub-judice, Adv Mkhwebane is of the strong view that letting the allegations concerned go without a challenge will have dire implications for her office in the eyes of the public. She, accordingly and without going deep into the merits, wishes to set the record straight.

An unintelligible communication. The dire implications must therefore ensue. SARS release 30 April 2018: Trade statistics for March 2018 (surplus of R9,47 billion).* Huffington Post 30 April 2018: Disciplinary steps go ahead as Moyane’s settlement talks with

SARS fall flat—three attempts to settle with Tom Moyane have reportedly failed.§ Sunday Times 30 April 2018: Law firms revolt over SARS non-payments.§ news24 30 April 2018: Exclusive: controversial attorney & alleged spy Belinda Walter

was a consultant for senior KPMG manager.§ news24 01 May 2018: SA’s ‘extremely clever’ former finance minister Derek Keys dies.§ * Found or to be found on the SARS website. Concurrently on the SARS ‘What’s new’ page. § Not included in Tax Shock, Horror Database.

LOST & FOUND TSHD This month 125 items were added to the Tax Shock, Horror Database. Land subdivision Since 16 September 1998, the President has failed to proclaim the Subdivision

of Agricultural Land Act Repeal Act 64 of 1998. Michael Hellens 05 November 2017: I await, indefinitely, if necessary, confirmation of the

‘Mazzotte donation’ or a denial from acting judge Adv Hellens. From the original Sunday Times report, this was, as I see it, a remuneratory donation (126 TSH 2013). As such, it would be exempt from donations tax under s 56(1)(k) of the Income Tax Act (because included in gross income).

Repo rate 29 March 2018: Reduced to 6,5%—MPC (180 TSH 2018). Official rate 01 April 2018: Reduced to 7,5%—ITA (repo plus 1%)) (see the Monthly Listing). Standard Rate 01 May 2018: Reduced to 10%—PFMA (repo plus 3,5%) (see Monthly Listing). Prescribed rate 01 May 2018: Reduced to 10—TAA (= SIR) (see the Monthly Listing). Take on the month So much misguided optimism, doomed to be smashed on the rocks of the

upcoming, desperate election. And how, Oh how, is it to be financed?

MONTHLY NOTEBOOK All past entries from 2007 to date. All words & phrases from 2009 to date.

Overpaying SARS and mora interest A little finger trouble results in the overpayment of PAYE by a listed company of a staggeringly huge amount. It successfully secures a refund, and then thinks about interest. Without seeking any advice, it starts bugging SARS for interest.

Seven months later SARS replies, by way of a brilliant letter, saying, essentially: ‘Tough luck! You never claimed mora interest, under the Prescribed Rate of Interest Act (156 TSH 2016).’

Well done, SARS!

VAT increase (1): statutory fees and charges Still within the bounds of intelligibility (like s 67(1); 180 TSH 2018) is s 67(3) of the Value-Added Tax Act.

As far is presently relevant, it applies to an increase in the standard rate for which a vendor is accountable, under s 7(1), on the supply of goods or services subject to a fee, charge or

other amount prescribed by or determined pursuant to an act, a regulation or a measure having the force of law. It applies whether the consideration demanded is a fixed, maximum or minimum fee. It message is simple:

that fee, charge or other amount may be

181 Tax Shock, Horror 2018—April—8

—An irreverent newsletter designed to keep you up to date—

increased…by the amount of tax or additional tax charged or chargeable.

Then there are the inevitable exclusions:

The rule does not apply if the relevant legislation already caters for the increase.

And it also does not apply if the consideration

demanded is calculated as a percentage or fraction of the amount representing the consideration in money for a taxable supply of goods or services.

The second exclusion does not apply when it is irrelevant, that is, when the taxable supply is zero-rated or when the supply is exempt.

How SARS makes those collections Here is a tiny example of how SARS behaves. I have seen it do the same thing with millions of rand, and without even notifying the taxpayer:

Kindly be advised that you have an unallocated amount of R 6 233, 97. This is as a result of your payment of R47 918,70 Dated 29/02/2016 for tax period 01/2016 and credits from previous periods have been allocated to 01/2016 and this resulted to the overpayment.

Please provide us with proof of payment (bank statement) for the original amount R47 918,70 for

the R6 233,97 to be refunded. If no response is received within 21 working

days, an assessment will be raised to absorb your credit.

The lesser insult to the taxpayer’s rights is to ask for proof of the very payment that is the subject-matter of the communication. The unlawful, and possibly criminal, action is to threaten to raise an assessment for purposes other than the administration of a tax Act. It is this type of assessment I deal with daily.

Did your response to s 7C invalidate your trust? The introduction of s 7C of the Income Tax Act (cheap related-party loans to a trust are subject to donations tax) caused some consternation among the fraternity of clients and advisers either using trusts for nefarious purposes or simply not being in the league for whom trusts are appropriate.

So here’s this client, worried about his interest-free loans to his stable of trusts. He emails his advisers, pretty late in the day, in fact, after the February 2018 year-end. What to do?

No problemo, comes the reply, we will put through interest on all the loans and so avoid donations tax, and show the interest in your personal returns, which are due only much later. Then we’ll think what to do about the 2019 year.

Not a word about the effect of the extra interest income on the client’s second provisional tax payment for 2018, and possible, swingeing penalties, or the need for a top-up payment.

No concern expressed about the deductibility or otherwise of the interest charge to the

trusts, despite the inevitable taxation of that interest in the client’s hands.

Not even a blush at the thought that interest is being charged non-contractually and ex post facto, rendering a deduction by the trusts in any event unlawful, ab initio.

No professional qualms about unilaterally making the necessary entries without authority from the client.

No shame in revealing that the so-called trustees are stooges, and bloody fools, to boot, being saddled with interest charges they never agreed to, and exposing them to delictual claims by the beneficiaries, and, plausibly, even creditors. Yet they will meekly sign the financials.

Clearly, even if the trusts were properly constituted (even though not a betting man, I would bet against it), they are being administered as if the trust property is in the ownership of the client and under the thumb of the advisers. Their response to s 7C did not of itself bring about the invalidity of the trusts—it merely made their invalidity apparent.

VAT increase (2): goods, services, rentals, successive supplies Now for the difficult stuff—s 67A of the Value-Added Tax Act. The principal rule, laid down by s 67A(1), does not apply to the ‘sale’ of ‘fixed property’. And, insanely, it is made subject to anomalous time-when-provided rules. Only in three other instances has some incautious draftsperson conjured with goods and services ‘provided’, when the gold-standard verb of the act is ‘supplied’ (s 1(1) sv ‘domestic goods and services’; s 11(2)(h)(ii) zero-rating for qualifying international transport services; and

s 54(6)(b)(ii) agency rule for qualifying shipping and aviation services).

Apply the old rate Section 67A(1)(i) allows you to apply the old rate, as long as you pull two triggers. In relation to the supply of goods, these are:

The goods must be provided before the date of the increase.

The supply of the goods must be deemed by

181 Tax Shock, Horror 2018—April—9

—An irreverent newsletter designed to keep you up to date—

s 9 to be made on or after the date of the increase.

In relation to goods provided under a rental agreement (s 9(3)(a)) or as progressive supplies (s 9(3)(b)), the two triggers are:

The goods must be provided during a period beginning before and ending before the date of the increase.

The supply of the goods must be deemed by s 9 to be made on or after the date of the increase.

And, in relation to services, the two triggers are:

The services must be performed during a period beginning before and ending before the date of the increase.

The supply of the services must be deemed by s 9 to be made on or after the date of the increase.

Apportion between old and new rate Section 67A(1)(ii) calls for a fair and reasonable apportionment of the value of supply, as between the period before the date of the increase and the period thereafter. The old rate must be applied to the first period, and the new rate to the second. Again, two triggers must be pulled.

In relation to goods provided under a rental

agreement (s 9(3)(a)) or as progressive supplies (s 9(3)(b)), they are:

The goods must be provided during a period beginning before and ending on or after the date of the increase.

The supply of the goods must be deemed by s 9 to be made on or after the date of the increase.

And, in relation to services, they are:

The services must be performed during a period beginning before and ending on or after the date of the increase.

The supply of the services must be deemed by s 9 to be made on or after the date of the increase.

What ‘provided’ means Under s 67A(3), goods are deemed to be provided by their supplier when they are delivered to the recipient, while goods supplied under a rental agreement are deemed to be provided to the recipient when the recipient takes possession or occupation of them.

Special rules Section 67A(4) caters for a pre-existing agreement fixing the price of the construction by a vendor carrying on a construction enterprise of a new dwelling; s 67A(5) for lay-by agreements.

KPMG and PRECCA In 2016, KPMG Viewpoint (which I happened to come across recently, while considering whether to report one of the Big 3½ audit firms to IRBA, for grossly unprofessional conduct, incredibly damaging to the client concerned, yet groundless and stupid, having to do with this very subject) carried an item entitled ‘Section 34—The Duty to Report Corrupt Transactions’, purporting to cover s 34 of the Prevention and Combatting of Corrupt Activities Act.

What KPMG says Under the heading ‘Duty to report’ this claims that:

Section 34 of PRECCA places a duty on certain persons to report certain offences. Failure to report is a criminal offence.

Under the heading ‘What to report’ it lists corruption, theft, fraud, extortion, forgery, and uttering of a forged document.

These excerpts, not qualified in any way in the rest of the editorial portion of the document, struck me as not being in accordance with my early examination of the act, some years ago, and in conjunction with a colleague, from the point of view of being professionals in the advice business. So I took a second, even more careful look at s 34.

First, I canvassed all the case reports in SALR on PRECCA, noting, in passing, that the only person seemingly ever prosecuted and found guilty under the act was one Selebi (S v Selebi 2012 (1) SA 487 (SCA)).

What PRECCA says Since there is no guidance there, one is required to interpret s 34 of the basis of its terms, read within the context of the act, read as a whole:

Duty to report corrupt transactions 34. (1) Any person who holds a position of authority and who knows or ought reasonably to have known or suspected that any other person has committed— (a) an offence under Part 1, 2, 3 or 4, or

section 20 or 21 (in so far as it relates to the aforementioned offences) of Chapter 2; or

(b) the offence of theft, fraud, extortion, forgery or uttering a forged document,

involving an amount of R100 000 or more, must report such knowledge or suspicion or cause such knowledge or suspicion to be reported to the police official in the Directorate for Priority Crime Investigation referred to in section 17C of the South African Police Service Act, 1995, (Act 68 of 1995).

Clearly, Viewpoint cannot be dealing with

181 Tax Shock, Horror 2018—April—10

—An irreverent newsletter designed to keep you up to date—

s 34(1)(a), since every offence to which that provision refers involves the giving or acceptance of a ‘gratification’ (s 1 sv ‘gratification’), a term that does not appear even once in the editorial portion.

It follows that Viewpoint takes the, well, view that s 34(1)(b), in covering theft, fraud, extortion, forgery or uttering a forged document, is a substantive, stand-alone provision.

In my view, by contrast, despite the apparent construction of s 34(1) in the form of a disjunctive (‘or’) list, a reading of the entire act suggests that ‘the offence of theft, fraud, extortion, forgery or uttering a forged document’ must be linked in some way with the giving or acceptance of a gratification, otherwise a huge number of people, especially in government and in commerce, and in law and, particularly, auditing firms, would be guilty of an offence, under s 34(2), read with s 26(1)(b).

The clue to the proper interpretation of s 34(1) lies, I believe, in the preamble to the act,

which includes this line:

AND WHEREAS there are links between corrupt activities and other forms of crime, in particular organized crime and economic crime, including money-laundering;

The ‘corrupt activities’ referred to all involve the giving or acceptance of ‘any gratification’. Section 34(1)(b) therefore looks to ‘the offence of theft, fraud, extortion, forgery or uttering a forged document’ linked to the giving or receiving of a gratification.

In other words, s 34(1) is not to be read as an ordinary disjunctive (‘or’) list. Nor is to be read as if ‘or’ means ‘and’, in a conjunctive (‘and’) list (see, on this possibility, Mthembu v Letsela and Another 2000 (3) SA 867 (SCA); 178 TSH 2018), since that would restrict the deliberately widely cast net of s 34(1)(a).

It must, I submit, be read as if some linking words have been omitted by the legislature.

Wills: witness cannot be executor Thanks to s 4A(1) of the Wills Act, ‘a witness to a will is prohibited from being appointed executor of the deceased estate concerned’ (per Van Heerden JA in Henriques v Giles NO 2010 (6) SA 51 (SCA)). Section 4A(1) reads like this:

4A. (1) Any person who attests and signs a will as a

witness, or who signs a will in the presence and by direction of the testator, or who writes out the will or any part thereof in his own handwriting, and the person who is the spouse of such person at the time of the execution of the will, shall be disqualified from receiving any benefit from that will.

VAT increase (3): supplies hit by the new rate Subject to an even wider set of time-when-provided rules is s 67A(2) of the Value-Added Tax Act. It applies, by implication, even to the ‘sale’ of ‘fixed property’. It creates a deemed time of supply of the date of the increase in the rate for:

Goods deemed by s 9 to be supplied at a time falling between the date of the announcement of the increase in the rate (Budget day, 21 February 2018) and the day before the increase becomes effective (31 March 2018), and deemed to be provided on or after the twenty-second day after the date of the increase.

Services deemed by s 9 to be supplied at a time falling between the date of the announcement of the increase in the rate (Budget day, 21 February 2018) and the day before the increase becomes effective (31 March 2018), and performed on or after the date of the increase.

Customary payments Excluded are supplies ‘taking place’ (what the hell does that mean?)

in consequence of any payments customarily made or becoming due or invoices customarily issued, when made, becoming due or issued at regular

intervals for the provision of goods or the performance of services still to be provided or performed….

I have no idea what is intended.

What ‘provided’ means Under s 67A(3), again:

Goods are deemed to be provided by their supplier when they are delivered to the recipient.

Goods supplied under a rental agreement are deemed to be provided to the recipient when the recipient takes possession or occupation of them.

But, in this context, there is an additional rule affecting fixed property:

Goods consisting of fixed property supplied by way of a sale, to be transferred by registration in a deeds registry, are deemed to be delivered to the recipient upon registration.

Special rules Again s 67A(4) caters for pre-existing agreements affecting the sale of fixed property and the commercial construction of a dwelling.

181 Tax Shock, Horror 2018—April—11

—An irreverent newsletter designed to keep you up to date—

VAT increase (4): why these dumb rules cannot work I clearly remember making the same point back in 1993 when s 67A was introduced. It was written by someone with what I used to call a ‘shoebox’ view of VAT systems, referring to the shoebox in which a corner café or spaza shop might keep its incoming and outgoing vouchers.

Other businesses rely upon more sophisticated systems to maintain their accounting systems, which, I assure you, are, at the best of times, if I am to be very polite,

imperfectly adapted to accounting for the VAT law. But even under the most favourable circumstances, you could not possibly adapt a sophisticated system, on the fly, to s 67A. And even if, miraculously, you are running a properly integrated accounting and VAT system, you would never have expected s 67A to survive any future change in rates. Thus even the best-run businesses could not possibly have been ready for the increase. As for SARS….

Municipal rates: 99-year lease Who is liable for municipal rates on a property subject to 99-year lease? The leaseholder.

‘Property’ is defined in s 1(1) of the Local Government: Municipal Rates Act primarily as ‘immovable property registered in the name of a person’. If it is property on which a municipality may levy a rate under s 2, it qualifies as ‘rateable property’, as also defined in s 1(1). Section 7(1) requires a municipality to levy rates on all rateable property in its area ‘levy rates on

all rateable property in its area’, subject to its power under s 7(2) not to levy a rate.

‘Immovable property’ is defined in s 102 of the Deeds Registries Act as including a registered right of lease hold.

Being a real right in land, under s 16 of the Deeds Registries Act, leasehold can be transferred only by registration by a registrar of deeds. Thus the leasehold will be registered in the name of the leaseholder.

VCCs: more Lucid on hotel v ‘hotel’? I do not fully follow the paper trail or the corporate structure but, it seems, the Lucid Hotel Company (Pty) Ltd recently made a private placement of its shares. It claims to be a venture capital company under s 12J of the Income Tax Act. I quote selectively but nevertheless verbatim (including spelling errors) from Addendum 1 to the offer:

REGULATORY: Section 12J registered FSB, VCC number vcc—0072, SARS tax certificate issued.

INVESTMENT STRATEGY: The Lucid Hotel Fund is a low risk, Section 12J tax efficient investment vehicle that will purchase a portfolio of high-end residential apartments in South Africa’s highest growth areas, with a primary focus on Cape Town, and will operate an apartment style hotel business.

Tax Advisor—Werksmens Attorneys, Johannesburg

The following selected extracts come from the ‘pitch’, a document headed ‘Lucid Hotel Fund’:

The Lucid Hotel Fund Is a low risk, 12J tax efficient Investment vehicle that will gather a portfolio of quality apartments In SA's highest growth areas. primarily Cape Town, and operate a high end Apartment Hotel business.

Investors in the Lucid Hotel Fund will get priority booking as well as a discount on accommodation at the Lucid portfolio of apartment hotels (subject to terms and conditions and a fair usage policy).

Included is a table apparently explaining what is

an ‘apartment hotel’. It gives the ‘legal structure’ as a sectional title unit; the ‘typical room size’ as 50 sqm; the ‘in-room service’ as fridge, dishwater, kitchenette, laundry; the ’hotel facilities’ as concierge, coffee shop, deli; the ‘staff complement’ as limited; the ‘building’ as mixed with residential; and the ‘channels’ as website, tour operators, online channels eg booking.com.

Podcast Finally, there is a transcript of a sponsored podcast on BizNews, including the following passage:

…. The one specific inclusion in 12J is ‘hotelkeeping’ or hospitality. The opportunity that we identified was that we could buy high-end residential units and create a hotel offering within that complex. One of the factors that drove it was that from a tourist or corporate traveller’s perspective there’s a growing demand for accommodation which is slightly more apartment-style. In other words, accommodation where one has a bigger unit, self-catering facilities, you have a little kitchenette that you can do your own cooking if you so choose. You can do some washing if you want within the apartment. And the building itself doesn’t have extensive hotel facilities like a big dining hall with a breakfast buffet for example. It would be much more reliant on the area that it’s in. These are typically in high-demand areas where there’s transportation available, where there’s good restaurants and coffee shops close by, as well as perhaps a Virgin Active gym. So that’s really what we’ve identified as a big global not only a

181 Tax Shock, Horror 2018—April—12

—An irreverent newsletter designed to keep you up to date—

local trend. It’s also a really nice match-up with 12J, as it’s a hospitality business with a strong property underpin supporting one of South Africa’s key industries—tourism.

For that last word, I was expecting not ‘tourism’ but ‘property plays’.

Clearly, Werksmans does not share my concerns about ‘hotel’ (180 TSH 2018).

Wills: statutory renunciations, patrimonial and fiscal outcomes Section 2C(1) and (2) of the Wills Act allow for privileged renunciations by qualifying beneficiaries, with preordained distributive consequences, overriding the Intestate Succession Act (under the principles of lex posterior priori derogat—160 TSH 2016—and generalia specialibus non derogant—162 TSH 2016).

2C. (1) If any descendant of a testator, excluding a minor or a mentally ill descendant, who, together with the surviving spouse of the testator, is entitled to a benefit in terms of a will renounces his right to receive such a benefit, such benefit shall vest in the surviving spouse. (2) If a descendant of the testator, whether as a member of a class or otherwise, would have been entitled to a benefit in terms of the provisions of a will if he had been alive at the time of death of the testator, or had not been disqualified from inheriting, or had not after the testator’s death renounced his right to receive such a benefit, the descendants of that descendant shall, subject to the provisions of [s 2C(1)], per stirpes be entitled to the benefit, unless the context of the will otherwise indicates.

The designated beneficiary must be ‘entitled to a benefit’ under a will. Thus a distinction must be made as between a beneficiary entitled to a benefit under a will and a beneficiary enjoying a

real right to property, as a result of the liquidation and distribution of the estate. Such a real right arises, under s 35(12) of the Administration of Estates Act, when to use, in part, the convenient language of the courts, the estate accounts have been confirmed and the executor ‘forthwith’ pays the creditors and distributes the estate among the heirs.

Downstream of such a distribution, it is too late to engage s 2C(1) and (2), and any patrimonial events at that stage as between the designated beneficiary and other beneficiaries or family members will have their own fiscal consequences.

As I read s 2C(1) and (2), they would still apply at the moment after confirmation but before distribution. Alas, the designated beneficiary would, at that moment, enjoy a personal right against the executor for delivery of the estate property concerned, and would thus be forgoing it, even if by operation of law. Thus the fiscal consequences would be the same as if the designated beneficiary owned a real right in the property.

The upshot is that a designated beneficiary should act under s 2C(1) or (2) at some time between the moment of death and the moment before the estate accounts are confirmed.

The corresponding provisions of the Intestate Succession Act are s 1(6) and (7), where the same principle applies.

VAT increase (5): natural and deemed times of supply A rate-increase focusses attention upon the time of supplies of goods and services.

Natural time of supply The natural time of supply is fixed by the definition of ‘supply’ in s 1(1) of the Value-Added Tax Act, which requires so-call complete performance by the supplier (94 TSH 2011). Any deemed time of supply cannot apply ahead of the natural time of supply. These are aspects of the VAT law ignored by almost everyone, and, perhaps, forgivably.

Deemed time of supply What cannot be so easily forgiven, by contrast, is the widespread misapprehension of the complex nature of s 9, which is misleadingly headed ‘Time of supply’. As I showed in 171 TSH 2017, s 9 deems things to happen over and above deeming times of supply to come into existence:

There are several ‘deemed-supply’ rules (not

to be confused with ‘deemed-time-of-supply’ rules), which override the definition of ‘supply’ and thus render performance irrelevant.

There is a specific rule governing rental agreements, which celebrates the concept of reciprocal performance (82 TSH 2010) by the parties.

There is a rule governing instalment credit agreements, which, to the extent it relies upon payment, appears unworkable.

There is the invoice/payment rule governing the sale of goods and the provision of services, which cannot mean exactly what it says.

A subscriber asked me how the increase in the rate would affect, say, an advocate rendering an account for work done. Here is how I wish my actual reply read (at the time I could still not re-figure out the meaning of s 67A):

First there must be a ‘supply’. In relation to a

181 Tax Shock, Horror 2018—April—13

—An irreverent newsletter designed to keep you up to date—

supply of services, this requires so-called complete performance by the supplier. For example, if a fee charged by a supplier is agreed upon on a time basis, there is performance hourly or daily; if it is agreed upon on the basis of the completion of the work, there is performance upon its completion.

Then there is a deemed time of supply, in these circumstances, under s 9(1), triggered by the issue of an ‘invoice’ (s 1(1)) or payment (in the common law sense) of the ‘consideration’, whichever is sooner.

An invoice or payment preceding a ‘supply’ is void, as far the application of s 9(1) is concerned. But an invoice or payment following upon a ‘supply’ establishes a deemed time of supply for the actual ‘supply’, overriding the time of performance. A tax invoice is issued when it is delivered (in the common law sense, coloured by the word ‘issue’) by the supplier to the recipient.

Thus, for a supply of services performed before 1 April 2018, the appropriate rate of tax will seemingly depend upon the date of issue of an invoice. But s 67A(1)(i) provides that an invoice issued or payment made on or after 1 April relating to a supply performed before that date attracts the old rate. On the other hand, a ‘supply’ of services performed on or after 1 April 2018 will attract the new rate, under s 67A(2), even if, thanks to the earlier issue of an invoice or a payment, s 9(1) deems the supply to have been made between 21 February 2018 (Budget day) and 31 March 2018.

In supplies between registered vendors, SARS will, I am sure, be indifferent whether the 14% or the 15% rate is applied, since there will be no loss to the fiscus. Most Vat and accounting systems will issue March invoices at the 14% rate and April invoices at 15%, and to hell with the rules.

Words & phrases: ‘any’ In CIR v Ocean Manufacturing Ltd 1990 (3) SA 610 (AD), Nicholas AJA (as he then was) said:

In an alternative argument, Mr Swersky submitted that on a proper interpretation, the expression ‘any agreement affecting any company’ in s 103(2) ‘is restricted to an agreement which affects the control of the company or one which affects any person's right to participate in the profits or dividends of the company’.

In my opinion there is nothing to warrant that interpretation. Any is ‘a word of wide and unqualified generality. It may be restricted by the subject-matter or the context, but prima facie it is unlimited.’ (Per Innes CJ in R v Hugo 1926 AD 268 at 271.) ‘In its natural and ordinary sense, any—unless restricted by the context—is an indefinite term which includes all of the things to which it relates.’ (Per Innes JA in Hayne & Co v Kaffrarian Steam Mill Co Ltd 1914 AD 363 at 371.)

In regard to the subject-matter there is nothing in s 103(2) to suggest that the word any was used in a limited sense. Section 103(2) does not impose a tax, but relates to agreements designed for the

avoidance of tax liability. It should be construed in such a way as to advance the remedy provided by the subsection and suppress the mischief against which it is directed. The Commissioner’s powers should not be restricted unnecessarily by interpretation. (See Glen Anil Development Corporation Ltd v Secretary for Inland Revenue 1975 (4) SA 715 (A) at 727H–728A.) In regard to the context, s 103(2) related to ‘any agreement affecting any company or any change in the shareholding in any company…’. In using the words I have italicized, the Legislature has provided for the sort of case referred to by counsel; it is unlikely that it could have intended that it should be covered also by the earlier words.

Counsel sought to rely on the eiusdem generis rule. A single species (in this case ‘any agreement affecting any change in the shareholding in any company’) does not constitute a genus. (See Craies on Statute Law 7th ed at 181. ‘Unless you can find a category’, said Farwell LJ in Tillmans & Co v SS Knutsford [1908] 2 KB 385 at 403, ‘there is no room for the application of the eiusdem generis doctrine.’)

Normal tax: CGT creep The capital gains tax is one of the greatest legislative cockups of all time, and I very much doubt whether there are as many as six people in the entire country who understand it. I certainly do not pretend to.

It was bad enough when it was largely confined to the Eighth Schedule to the Income Tax Act, barring the notorious s 26A, which, to this day, confuses even clever people, mixing in the wrong company, about how the CGT is integrated into the rest of the act. Over the years, however, more and more CGT law has crept into the main body of the act, making the subject ever more dangerous for the rest of us.

What follows is an attempt at identifying these interlopers. Miss them, and your career, as you

know it, might be over.

The obvious First, provisions obviously directly pertinent to the CGT:

s 1(1)—Definitions: aggregate capital gain, aggregate capital loss, assessed capital loss, capital gain, capital loss, depreciable asset, taxable capital gain.

s 9H—Change of residence, ceasing to be controlled foreign company or becoming headquarter company.

s 9HA—Disposal by deceased person. s 26A—Inclusion of taxable capital gain in

taxable income.

181 Tax Shock, Horror 2018—April—14

—An irreverent newsletter designed to keep you up to date—

s 68—Income and capital gain of married persons and minor children.

The stuff that creeps up on you Then, provisions relying upon substantive references to the CGT:

s 1(1)—Definitions: assessment, listed company, representative taxpayer.

s 3(4)—Decisions subject to objection and appeal.

s 6quat—Rebate or deduction in respect of foreign taxes on income (s 6quat(1)(f)).

s 7C—Loan or credit advanced to trust by a connected person (s 7C(5)(d)).

s 8—Certain amounts to be included in income or taxable income (s 8(4)(e), (eD), (eE)).

s 9—Source of income (s 9(2)(j)). s 9D—Net income of controlled foreign

companies (s 9D(2A), (2A)(e), (f), (k), 9D(9)(fB)).

s 9H—Change of residence, ceasing to be controlled foreign company or becoming headquarter company (s 9H(3)(e), (5)(b)).

s 10—Exemptions (s 10(3)). s 12N—Deductions in respect of

improvements not owned by taxpayer (s 12N(1)).

s 18A—Deduction of donations to certain organizations (s 18A(3A)).

s 19— Concession or compromise in respect of a debt (s 19(6)).

s 22—Amounts to be taken into account in respect of values of trading stock (s 22(3)(a)).

s 23D—Limitation of allowances granted in respect of certain assets (s 23D(2A)(c)).

s 24BA—Transactions where assets are acquired as consideration for shares (s 24BA(3), (4)(b)).

s 25—Taxation of deceased estates (s 25(4)(b)).

s 25BB—Taxation of REITs (s 25BB(5)). s 29A—Taxation of long-term insurers

(s 29A(10), (11)(a), (h), (13B)(d)). s 29B—Mark-to-market taxation in respect of

long-term insurers (s 29B(3)(b)). s 36—Calculation of redemption allowance

and unredeemed balance of capital expenditure in connection with mining operations (s 36(7EA)).

s 37D—Allowance in respect of land conservation in respect of nature reserves or nature parks (s 37D(2)(b)).

s 41—General (s 41(2), (9)). s 42—Asset-for-share transactions

(s 42(2)(a), (b), (c), (5)(b), (6)(a), (b), (7)(a)). s 43—Substitutive share-for-share

transactions (s 43(1A), (2)). s 44—Amalgamation transactions (s 44(2),

(5), (6)). s 45—Intra-group transactions (s 45(2),

(3A)(b), (5)). s 46—Unbundling transactions (s 46(3)(b) sv

‘expenditure’, ‘market value’, (5A)).

s 47—Transaction relating to liquidation, winding-up and deregistration (s 47(2), (4)).

s 90—Persons by whom normal tax payable. s 91—Recovery of tax (s 91(4A)). s 103—Transactions, operations or schemes

for purposes of avoiding or postponing liability for or reducing amounts of taxes on income (s 103(3C), asset).

Tenth Schedule para 7(2).

Definitional indiscipline Finally, provisions using CGT terms:

s 9C—Circumstances in which certain amounts received or accrued from disposal of shares are deemed to be of a capital nature (s 9C(1) sv ‘disposal’).

s 9H—Change of residence, ceasing to be controlled foreign company or becoming headquarter company (s 9H(1) sv ‘asset’).

s 12P—Exemption of amounts received or accrued in respect of government grants (s 12P(1) sv ‘allowance asset’, ‘base cost’).

s 19—Concession or compromise in respect of a debt (s 19(1) sv ‘capital asset’).

s 20A—Ring-fencing of assessed losses of certain trades (s 20A(2)(b): vehicles, aircraft or boats).

s 22—Amounts to be taken into account in respect of values of trading stock (s 22(9)(a)(i), (b)(i), (c)(i), (d)(i): recognized stock exchange).

s 23O—Limitation of deductions by small, medium or micro-sized enterprises in respect of amounts received or accrued from small business funding entities (s 23O(1) sv ‘allowance asset’, ‘base cost’).

s 24BA—Transactions where assets are acquired as consideration for shares (s 24BA(1) sv ‘asset’).

s 29A—Taxation of long-term insurers (s 29A(13B)(d), asset).

s 29B—Mark-to-market taxation in respect of long-term insurers (s 29B(1) sv ‘market value’, recognized exchange, (4) asset).

s 35A—Withholding of amounts from payments to non-resident sellers of immovable property (s 35A(15) sv ‘immovable property’).

s 40CA—Acquisition of assets in exchange for shares or debt issued (asset).

s 41—General (s 41(1) sv ‘asset’, ‘base cost’, ‘capital asset’, ‘date of acquisition’, ‘disposal’).

s 50A—Definitions (s 50A(1) sv ‘listed debt’, recognized exchange).

s 64E—Levy of tax (s 64E(3)(a), recognized exchange).

s 64FA—Exemption from and reduction of tax in respect of dividends in specie (s 64FA(1)(c), disposal, (d), disposal).

s 103—Transactions, operations or schemes for purposes of avoiding or postponing liability for or reducing amounts of taxes on income (s 103(2), asset).

Feature Supplement to 181 Tax Shock Horror 2017

Cases

All past entries from 2006 to date.

April 2018 Winners & Losers In That Other Beautiful Game

Current & Past SATC Case Reports by Julian Ware

© 2018 J Ware ([email protected])

Income tax—legal privilege CIR v Van Der Heever

Supreme Court of Appeal (1999)—61 SATC 321 (judgment delivered by Grosskopf JA; Smalberger JA, Nienaber JA, Plewman JA and Farlam AJA concurring): The Commissioner successfully appealed a declaratory order granted in favour of the taxpayer’s tax adviser, a former practising advocate, that proceedings under s 417 of the Companies Act of 1973 be halted to enable the adviser to launch a further application for a declarator absolving him, under the principle of legal privilege, from being called upon as a witness. Since the client had waived its right to legal privilege, the adviser lacked the necessary locus standi to have brought the application before the court a quo. Legal privilege is for the benefit of a client not an adviser.

Lump sum proceeds—arrear tax recovery Burne NO v CIR & Another

Durban & Coast Local Division (1998)—61 SATC 331 (judgment delivered by Combrinck J): Could the Commissioner recover arrear income tax, PAYE and VAT owed by the deceased taxpayer before his death, from commuted proceeds payable to policy beneficiaries under a retirement annuity fund? Although for tax purposes the proceeds were deemed to have accrued to the deceased immediately before his death, under pension law the funds were not an asset in the deceased’s estate, and they were not available to discharge the deceased’s indebtedness to SARS.

VAT—agency appointment Contract Support Services (Pty) Ltd & Others v CSARS & Others

Witwatersrand Local Division (1998)—61 SATC 338 (judgment delivered by Brett AJ): A shockingly delivered judgment by an acting judge. The nub of the matter? Could SARS appoint a bank as its collecting agent under s 47 of the Value-Added Tax Act as it then read? The taxpayer was unsuccessful in its endeavours to obtain an interim declaratory order to set aside the appointment. Its argument that SARS had not observed the audio alteram partem principle came to naught. Today, s 179(5) of the Tax Administration Act (the ‘final-demand-10-days’ rule) and the Promotion of Administrative Justice Act would be very relevant.

Tax deduction—theft Taxpayer v CIR

ITC 1661 (Gauteng Special Court (1998))—61 SATC 353 (judgment delivered by Kirk-Cohen J): The partners in a dental practice appointed a firm of auditors to perform accounting and managerial functions on their behalves. The firm misappropriated partnership funds, which the partners sought to deduct under s 11(a) of the Income Tax Act. Since the firm was an independent contractor and no master-servant relationship existed between the parties, the loss sustained was not incurred in the production of income.

Trading stock—publications Taxpayer v CSARS

ITC 1662 (Gauteng Special Court (1998))—61 SATC 357 (judgment delivered by Brand J): The tax court’s decision in the AA The Motorist Publications’ case, which was confirmed on appeal to the Cape provincial Division (150 TSH 2015). Pre-production publishing costs did not form part of ‘trading stock’ as defined.

Fringe benefits—salary sacrifice Taxpayer v CSARS

ITC 1663 (Cape Special Court (1999))—61 SATC 363 (judgment delivered by Selikowitz J): A failed salary-sacrifice scheme involving medical aid contributions by a technikon. The court acknowledged that salary-sacrifices might be valid when implemented properly.

Sales tax—liability Taxpayer v COT

ITC 1664 (Zimbabwe Fiscal Appeal Court (1999))—61 SATC 383 (judgment delivered by Smith J): The Commissioner failed to establish that professional services rendered by the taxpayer were liable to sales tax.

t sh

Feature Supplement to 181 Tax Shock Horror 2018

Davey’s Locker

April 2018 Understatement penalties The SARS guide

by Tony Davey © 2018 A H Davey ([email protected] www.daveyvos.co.za)

A tax penalty, described in the Tax Administration Act as the ‘understatement penalty’ is imposed in circumstances dependent upon the taxpayer’s behaviour vis-à-vis an understatement. In essence, an understatement is a default, omission or incorrect statement in a return. The understatement penalty percentage is a graded percentage penalty dependent upon the severity of six listed behaviours in the table comprised by s 223.

But, if the taxpayer’s understatement resulted from ‘a bona fide inadvertent error’, no penalty is imposed under s 222(1).

To date, since the general commencement of the act, on 1 October 2012, which contains no definitions of the six behaviours nor of ‘a bona fide inadvertent error’, tax practitioners have had to reply upon dictionary definitions, comparative foreign jurisdictions and, more recently, a few domestic tax court cases.

The SARS ‘Guide to understatement penalties’, published on 29 March 2018, provides some welcome insight into SARS’s approach to penalties. Bear in mind that this publication is not an ‘official publication’, and accordingly does not create a practice generally prevailing, nor is it a binding general ruling; thus it has no authoritative effect and is, at best, only of an indicative nature.

Bona fide inadvertent error No penalty is imposed in the event of such an error. SARS states its position in the Guide, after quoting case law and the English Oxford Dictionary, as follows:

The desire not to punish understatements that result from bona fide inadvertent errors must consequently be understood and the language of the provision given meaning within the context of the regime’s purpose to specifically sanction only the behaviours

listed in rows (i) to (vi) of the understatement penalty table….

A taxpayer who acts in good faith, without the intention to deceive, will escape a penalty, not because the trigger is necessarily a bona fide inadvertent error, but because the regime is designed not to punish such taxpayers….

An inadvertent error is one that does not result from deliberate planning, and a bona fide inadvertent error is one that genuinely does not result from deliberate planning. It is simply a real or genuinely accidental mistake, an honest momentary lapse of reason if you will. What constitutes such an error would depend on the circumstances of the taxpayer and the circumstances under which it was made.…

In future newsletters I hope to cover the six listed behaviours attracting understatement penalties, dependent upon the level of blameworthiness of the taxpayer’s behaviour.

T S H

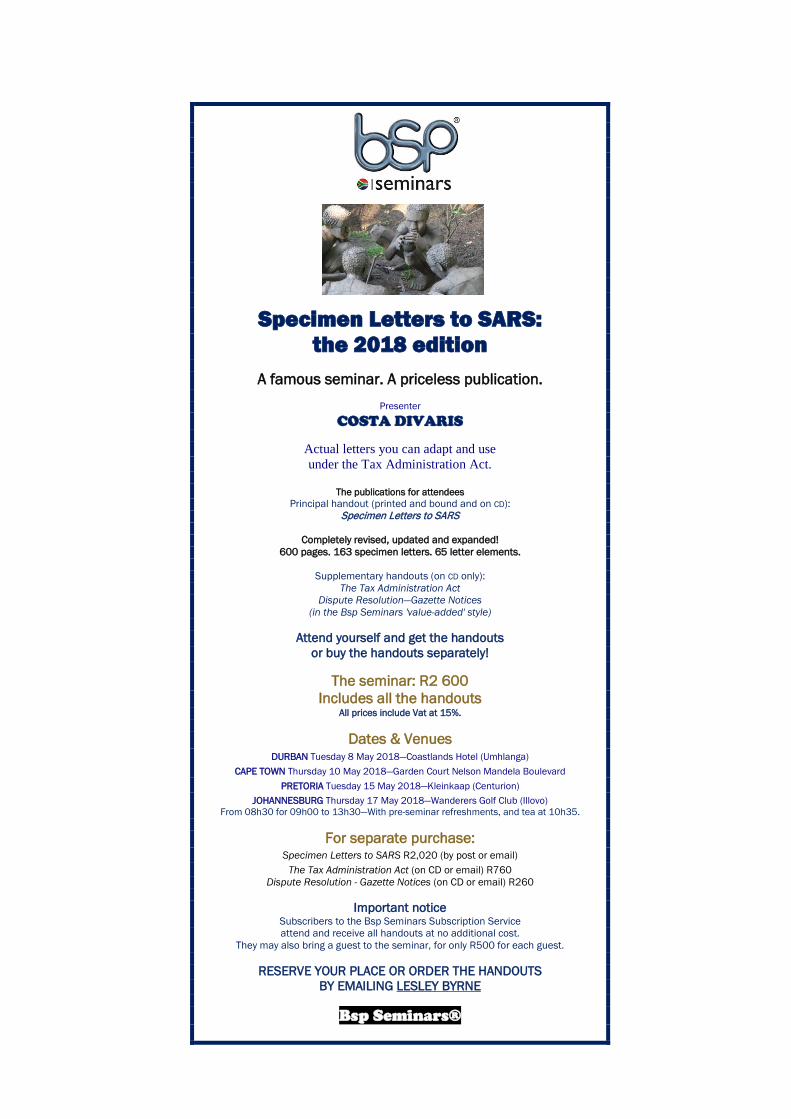

Specimen Letters to SARS: the 2018 edition

A famous seminar. A priceless publication.

Presenter

COSTA DIVARIS

Actual letters you can adapt and use under the Tax Administration Act.

The publications for attendees

Principal handout (printed and bound and on CD): Specimen Letters to SARS

Completely revised, updated and expanded!

600 pages. 163 specimen letters. 65 letter elements.

Supplementary handouts (on CD only): The Tax Administration Act

Dispute Resolution—Gazette Notices (in the Bsp Seminars 'value-added' style)

Attend yourself and get the handouts

or buy the handouts separately!

The seminar: R2 600 Includes all the handouts

All prices include Vat at 15%.

Dates & Venues DURBAN Tuesday 8 May 2018—Coastlands Hotel (Umhlanga)

CAPE TOWN Thursday 10 May 2018—Garden Court Nelson Mandela Boulevard PRETORIA Tuesday 15 May 2018—Kleinkaap (Centurion)

JOHANNESBURG Thursday 17 May 2018—Wanderers Golf Club (Illovo) From 08h30 for 09h00 to 13h30—With pre-seminar refreshments, and tea at 10h35.

For separate purchase:

Specimen Letters to SARS R2,020 (by post or email) The Tax Administration Act (on CD or email) R760

Dispute Resolution - Gazette Notices (on CD or email) R260

Important notice Subscribers to the Bsp Seminars Subscription Service attend and receive all handouts at no additional cost.

They may also bring a guest to the seminar, for only R500 for each guest.

RESERVE YOUR PLACE OR ORDER THE HANDOUTS BY EMAILING LESLEY BYRNE

Bsp Seminars®

Feature Supplement to 181 Tax Shock Horror 2018

\

Shortcut Keys in Word by Duncan S McAllister ©2018

April 2018

Some issues with portable storage devices Two issues I recently experienced when copying files from my PC to a memory stick were:

First, when copying the files from Dropbox I received the following message:

Are you sure you want to copy this file without its properties?

This problem is caused because Dropbox inserts some additional file properties in the file during transfer to its servers. Copying the file without all its additional properties should not affect the functioning of the file, so you can click ‘Yes’ without any concern.

When this problem has arisen when copying from my PC’s hard drive to my USB drive, I have prevented it from happening again by deleting the copy on my PC and replacing it with the copy on the USB drive. That way the problematic properties are eliminated from the copy on my PC’s hard drive. The problem will nevertheless continue if you copy files from Dropbox to a portable storage device without first changing the file system on that device (more on this below).

Secondly, when copying files to my USB disk I came up against a 4 GB size limit. This situation can often occur with large .pst (Outlook) files.

These problems arise because the portable storage device is formatted in the FAT 32 (File Allocation Table) format, as opposed to the

more accommodating and modern NTFS (New Technology File System) format. You can check the Properties of the portable storage device to see what file system has been used by pressing ALT + ENTER on the drive in File Explorer. The file system will be indicated under the General tab.

To change the file system from FAT 32 to NTFS, you will first need to format the portable storage device, which means that all information on that device will be lost. Consequently, do not follow the steps below unless you have backed up all your files on the device. Also bear in mind that FAT 32 will work on all other operating systems and most devices, while NTFS may not.

1. Press WIN + R and type diskmgmt.msc in the text box and hit ENTER.

2. Navigate to the removable storage device you want to format and press the applications key (next to right-hand CTRL Key) and arrow down to Format and hit ENTER.

3. You can then change the Volume Label (eg USB disk) if you so choose. Tab to the File system combo box. Press ALT + down arrow to expand it and select NTFS. Tab to OK and hit ENTER. You will then receive a pop-up:

Formatting this volume will erase all data on it. Back up any data you want to keep before formatting. Do you want to continue?

Click on OK and wait for the storage device to be reformatted.

t sh

Feature Supplement to 181 Tax Shock Horror 2018

April 2018 Evidence Corner—evidence could make a welcome change to tax cases

Evidence: science or art (continued)?

by Andrew Paizes © 2018 A Paizes ([email protected])

In the previous edition of Evidence Corner I raised some very big questions about the nature and philosophical foundations of the law in general and the law of evidence in particular. Is the law ‘out there’ to be discovered, like a distant star, or is it something we invent or create, like a painting or a sculpture?

This debate, which has divided mathematicians exploring the philosophical underpinnings of mathematics, is one which has fascinated me for some time. There is a strong link between the law of evidence and mathematics. This is because evidence deals with such things as proof and probability. The onus of proof in civil cases is described as one that has to be discharged ‘on a preponderance of probabilities’, which requires the onus-bearing party to establish that his or her case is ‘more probable than not’. In theory this requirement means that if he or she persuades the court that his or her case is at least 51% probable, victory will be assured.

Once this mathematical link is accepted, the door is open to questions deriving their validity from mathematics and not necessarily from the law itself. One of these concerns the multiplicative effect of combined probabilities. In mathematics the probability of