the rise and risks of lending to non-depository financial institutions

TRANSCRIPT

Enterprise Risk · Credit Risk · Market Risk · Operational Risk · Regulatory Compliance · Securities Lending

1

JOIN. ENGAGE. LEAD.

THE RISE AND RISKS OF LENDING

TO NON-DEPOSITORY FINANCIAL

INSTITUTIONS

An Excerpt from “2017 Industry Insights:

Perspectives from the Front Line”

by RMA’s Credit Risk Council

Enterprise Risk · Credit Risk · Market Risk · Operational Risk · Regulatory Compliance · Securities Lending

2

JOIN. ENGAGE. LEAD.

Private equity

investments in

financial technology

(fintech) firms

exceeded $10

billion across more

than 500

companies.

2016

Nonbank mortgage

lenders accounted

for more than half of

mortgage loans; 6

of the top 10

mortgage lenders

were nonbanks.

Late 2016

In the wealth

management

sector, digital and

automated robo-

advising is growing

and threatening

traditional business

models.

2016

The OCC’s

semiannual Risk

Perspective, states

that loans to non-

depository institutions

were up 150% in

three years,

becoming the fourth

largest commercial

loan category.

Fall 2016

THE RISE OF NON-DEPOSITORY FINANCIAL INSTITUTIONS

Enterprise Risk · Credit Risk · Market Risk · Operational Risk · Regulatory Compliance · Securities Lending

3

JOIN. ENGAGE. LEAD.

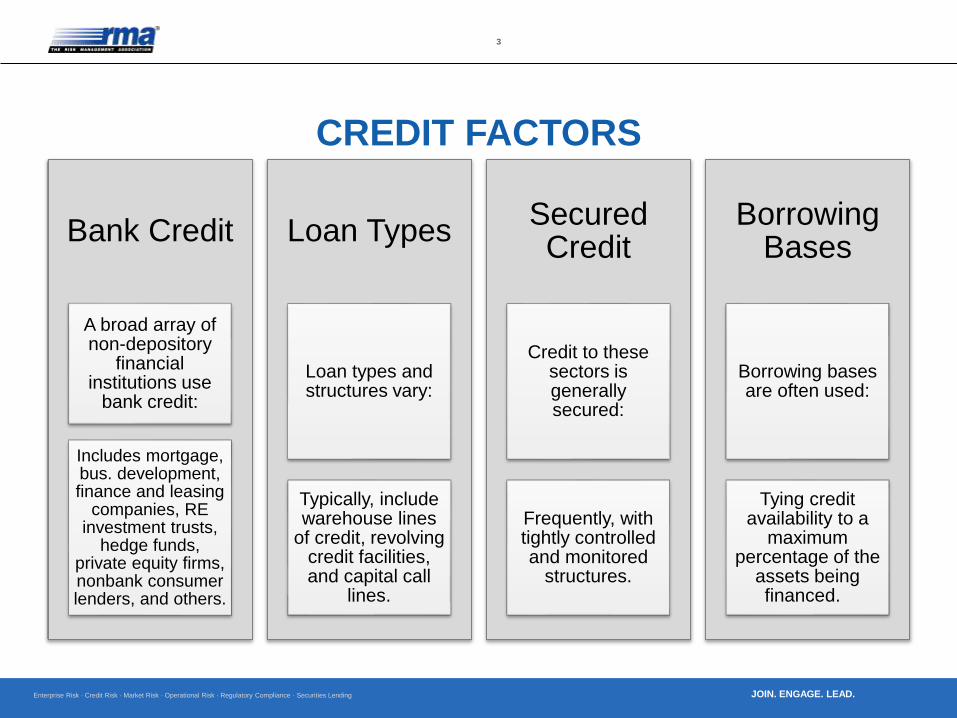

CREDIT FACTORS

Bank Credit

A broad array of non-depository

financial institutions use

bank credit:

Includes mortgage, bus. development, finance and leasing

companies, RE investment trusts,

hedge funds, private equity firms, nonbank consumer lenders, and others.

Loan Types

Loan types and structures vary:

Typically, include warehouse lines

of credit, revolving credit facilities, and capital call

lines.

Secured Credit

Credit to these sectors is generally secured:

Frequently, with tightly controlled and monitored

structures.

Borrowing Bases

Borrowing bases are often used:

Tying credit availability to a

maximum percentage of the

assets being financed.

Enterprise Risk · Credit Risk · Market Risk · Operational Risk · Regulatory Compliance · Securities Lending

4

JOIN. ENGAGE. LEAD.

IMPACT

There is an increasing

importance of nonbanks to all

facets of the financial services

industry, including the

competitive threats they present

to traditional banks.

Enterprise Risk · Credit Risk · Market Risk · Operational Risk · Regulatory Compliance · Securities Lending

5

JOIN. ENGAGE. LEAD.

IMPACT (CONT.)

While many of these nonbank

sectors provide investing,

partnership, and financing

opportunities for traditional banks,

they also create numerous risks,

including credit risk.

Enterprise Risk · Credit Risk · Market Risk · Operational Risk · Regulatory Compliance · Securities Lending

6

JOIN. ENGAGE. LEAD.

Lending to non-depository

financial institution comes with

credit risks that can be

substantial and can arise from

various factors.

Enterprise Risk · Credit Risk · Market Risk · Operational Risk · Regulatory Compliance · Securities Lending

7

JOIN. ENGAGE. LEAD.

THE RISK:

ASSET EVALUATION

Failing to properly evaluate asset quality in the borrower’s

portfolio poses risk.

• Example: lending to a finance or business development

company with heavy exposure to highly leveraged

businesses.

• Example: Financing a real estate investment or

mortgage firm with excessive geographic

concentrations in declining markets.

Enterprise Risk · Credit Risk · Market Risk · Operational Risk · Regulatory Compliance · Securities Lending

8

JOIN. ENGAGE. LEAD.

THE RISK:

AGGRESSIVE UNDERWRITING

Underwriting aggressively and

outside of industry norms can be

problematic.

• Example: using advance rates

that exceed generally accepted

levels or financing asset types that

other banks normally exclude.

Enterprise Risk · Credit Risk · Market Risk · Operational Risk · Regulatory Compliance · Securities Lending

9

JOIN. ENGAGE. LEAD.

THE RISK:

ASSESSING THE BORROWER

Financing borrowers with very high leverage and little

absolute capital, because you are comfortable with their

track record and cash flow stability can be risky.

• It’s critical to understand the ability of such borrowers to

operate under stressed conditions.

Using looser credit structures for borrowers who appear to

be well capitalized when their underlying portfolios are

highly risky and subject to large losses can cause

repayment problems.

Enterprise Risk · Credit Risk · Market Risk · Operational Risk · Regulatory Compliance · Securities Lending

10

JOIN. ENGAGE. LEAD.

THE RISK:

ASSESSING OPERATIONAL CONTROLS

You should properly assess the

operational controls of

borrowers and their ability to

manage complex portfolios and

business models.

• How good is the borrower’s own

credit reporting and how well

does it monitor its clients?

• Does the borrower track and

share early warning indicators?

Enterprise Risk · Credit Risk · Market Risk · Operational Risk · Regulatory Compliance · Securities Lending

11

JOIN. ENGAGE. LEAD.

THE RISK:

ASSESSING THE INVESTORS

You must properly assess the quality

and quantity of investors when

providing capital call facilities backed

by committed capital.

Enterprise Risk · Credit Risk · Market Risk · Operational Risk · Regulatory Compliance · Securities Lending

12

JOIN. ENGAGE. LEAD.

THE RISK:

UNDERSTANDING THE BORROWER

You should understand the

borrower’s own credit policies,

underwriting standards, and

exception trends.

Enterprise Risk · Credit Risk · Market Risk · Operational Risk · Regulatory Compliance · Securities Lending

13

JOIN. ENGAGE. LEAD.

THE RISK:

COLLATERAL VALUES

In secured facilities,

overestimating collateral values

and not adjusting advance rates to

market conditions is risky.

Enterprise Risk · Credit Risk · Market Risk · Operational Risk · Regulatory Compliance · Securities Lending

14

JOIN. ENGAGE. LEAD.

THE RISK:

CONCENTRATION RISK

You must recognize and/or

structure around significant

concentration risk in the

borrower’s business, which could

be any combination of single

obligor, sector, geographic, or

asset type.

Enterprise Risk · Credit Risk · Market Risk · Operational Risk · Regulatory Compliance · Securities Lending

15

JOIN. ENGAGE. LEAD.

THE RISK:

REPUTATION RISK

If the borrower is financing risky clients, this

could create reputation risk for the bank

involved, particularly in a workout situation.

It’s important to understand the sectors and

specific clients being financed.

A good rule of thumb is if a bank would not lend

directly to the end borrowers, then it should think

twice about lending to the entity directly.

Enterprise Risk · Credit Risk · Market Risk · Operational Risk · Regulatory Compliance · Securities Lending

16

JOIN. ENGAGE. LEAD.

CREDIT RISK FACTORS

The list of risk factors outlines some of the principle risks and demonstrates that successful lending to this broad sector requires:

Industry

knowledge

Effective

underwriting

standards.

Significant due

diligence

Ongoing

monitoring.

There are undoubtedly other credit risks not indicated in this presentation.

Enterprise Risk · Credit Risk · Market Risk · Operational Risk · Regulatory Compliance · Securities Lending

17

JOIN. ENGAGE. LEAD.

CREDIT RISK FACTORS (CONT.)

Consistent with broader trends during

recent years, banks have enjoyed strong

credit quality in these sectors, but that could

change, and understanding these key credit

risks is important to any institution with

exposure to these industries.

Enterprise Risk · Credit Risk · Market Risk · Operational Risk · Regulatory Compliance · Securities Lending

18

JOIN. ENGAGE. LEAD.

The Credit Risk Council supports

professionals who are responsible for

establishing, maintaining, or carrying

out credit risk management policies.

The council focuses on funded and

off-balance-sheet risk management,

including capital markets activity, and

other forms of credit intermediation

and risk mitigation.

ABOUT RMA’S CREDIT RISK COUNCIL

Enterprise Risk · Credit Risk · Market Risk · Operational Risk · Regulatory Compliance · Securities Lending

19

JOIN. ENGAGE. LEAD.

For additional information about

credit risk management,

visit

www.rmahq.org/credit-risk/

LEARN MORE

Enterprise Risk · Credit Risk · Market Risk · Operational Risk · Regulatory Compliance · Securities Lending

20

JOIN. ENGAGE. LEAD.

Share This Presentation

Visit http://www.rmahq.org for information on risk management.

RMA is a member-driven professional association whose sole

purpose is to advance sound risk principles in the financial services

industry.

RMA helps its members use sound risk principles to improve

institutional performance and financial stability, and enhance the risk

competency of individuals through information, education, peer

sharing, and networking.

Become a member today.