the u.s.-republic of korea free trade agreement and its ......subsequently balassa distinguishes...

TRANSCRIPT

The U.S.-Republic of Korea Free Trade Agreement

and its Impact on Latin America

Diploma Thesis

Anja Breuer

International Degree Course in Economics University of Applied Sciences Bremen

1. Examiner: Prof. Dr. Hans H. Bass, University of Applied Sciences Bremen

2. Examiner: Raquel Artecona, UN Economic Commission for Latin America and the Caribbean

August 2008

iii

Contents

List of Figures and Tables..............................................................................iv

List of Abbreviations and Acronyms.............................................................vi

1 Preferential Trade Arrangements: Forms, Development and Implications ......................................................................................................1

1.1 Forms of Preferential Trade Arrangements .............................................................2

1.2 The Recent Proliferation of Preferential Trade Arrangements................................5

1.3 The Economic Impact of Free Trade Agreements in Theory..................................8

2 The KorUS FTA and its Impact on Latin American Exports to the U.S. and Korea........................................................................................................17

2.1 History and Basic Facts of the KorUS FTA..........................................................18

2.2 The Impact of the KorUS FTA on the Member Countries....................................20

2.2.1 Current U.S.-Korea Trade and Its Development .............................................21

2.2.2 Estimated Effects on Trade and Welfare for the U.S. and Korea....................25

2.3 The Impact of the KorUS FTA on Latin American Exports .................................31

2.3.1 A Short Literature Review on Trade and Welfare Effects ..............................33

2.3.2 Current Latin American Trade with Korea and the U.S. and its Dynamics ....35

2.3.3 Composition of Latin American Exports.........................................................42

2.3.4 Comparison of Export Structures ....................................................................49

2.3.5 Competitiveness of Latin American Exports...................................................60

2.3.6 Conclusions .....................................................................................................66

3 The Nature of International Trade Relations Under Construction ........71

3.1 Is There a Superior Construction Plan?.................................................................72

3.2 PTAs: Building Blocks or Stumbling Blocks?......................................................78

3.3 Changing the Design? An Assessment of Policy Options.....................................83

References......................................................................................................87

iv

List of Figures and Tables

Figure 1: Main forms of economic integration.................................................................4

Figure 2: Preferential Trade Arrangements Notified to the WTO....................................6

Figure 3: Static Partial Equilibrium Analysis of a Free Trade Area ..............................10

Figure 4: U.S. Commodity Trade with South Korea......................................................21

Figure 5: Shares of Total U.S. Commodity Trade..........................................................22

Figure 6: Shares of Total Korean Commodity Trade.....................................................22

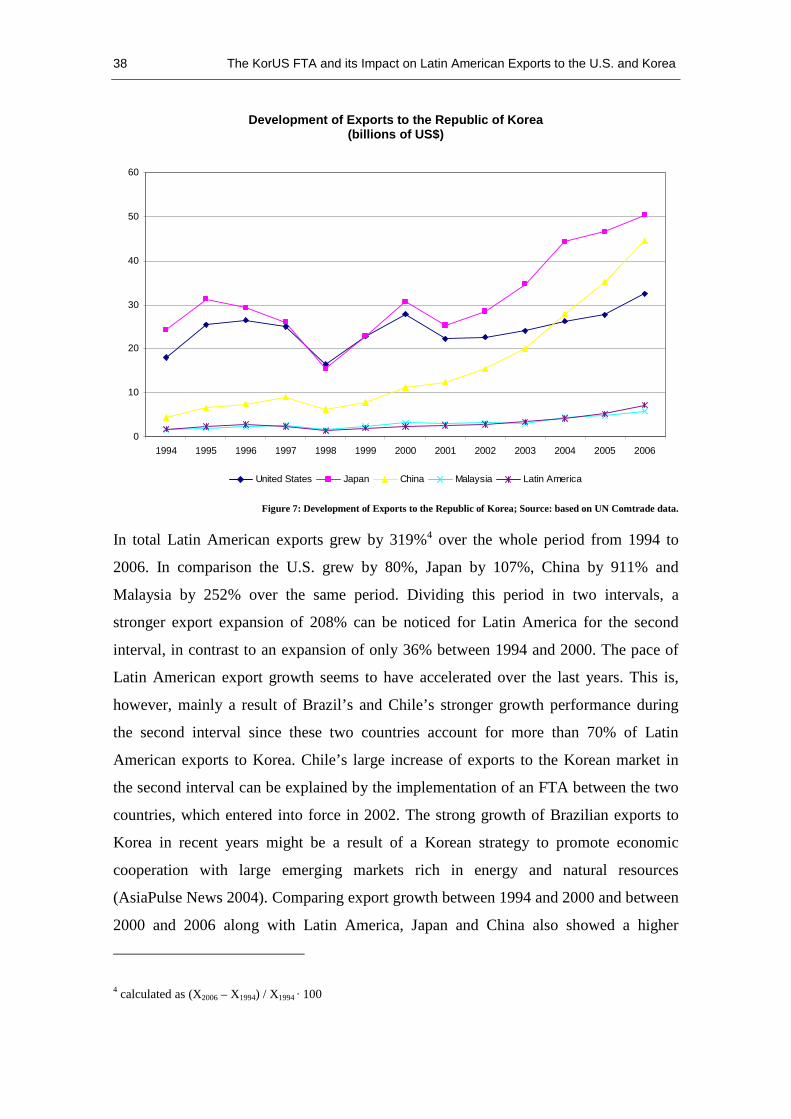

Figure 7: Development of Exports to the Republic of Korea.........................................38

Figure 8: Development of Exports to the United States.................................................41

Figure 9: ESI and WESI Values for the Korean Market................................................51

Figure 10: ESI and WESI Values for the U.S. Market...................................................55

Figure 11: Static Impact and Dynamic Time-Paths of Regionalism..............................79

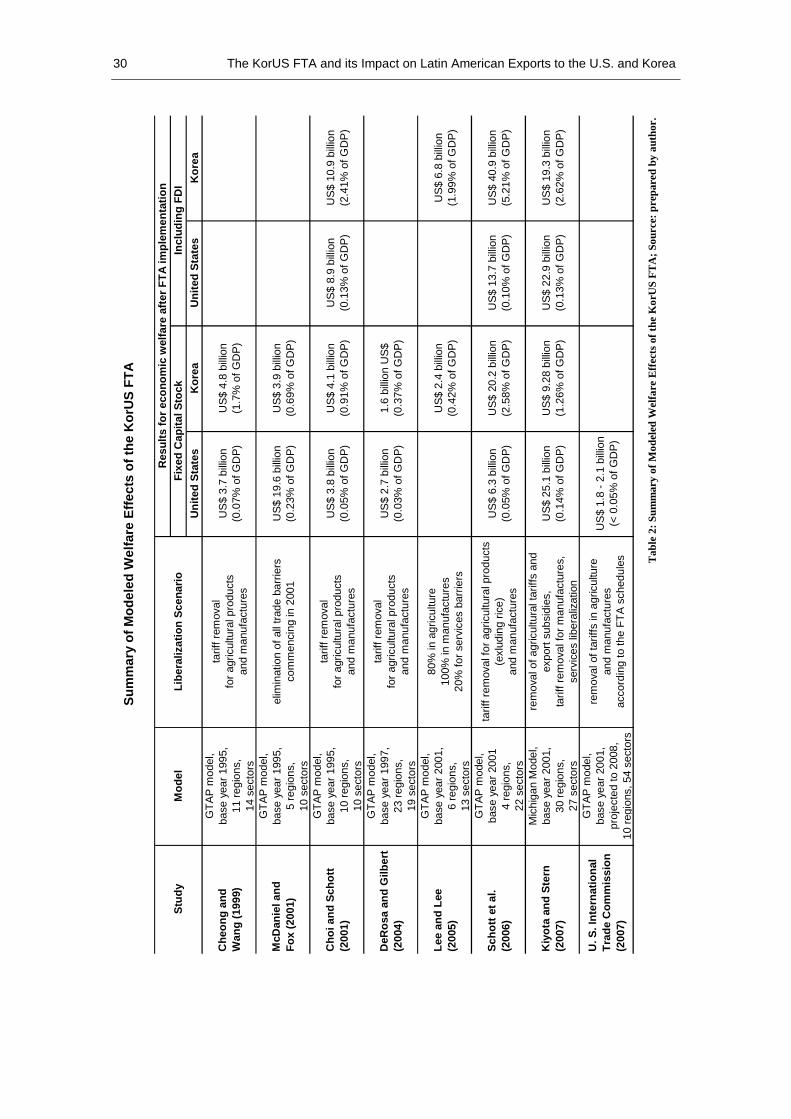

Table 1: Summary of Modeled Sectoral Output Effects of the KorUS FTA .................28

Table 2: Summary of Modeled Welfare Effects of the KorUS FTA..............................30

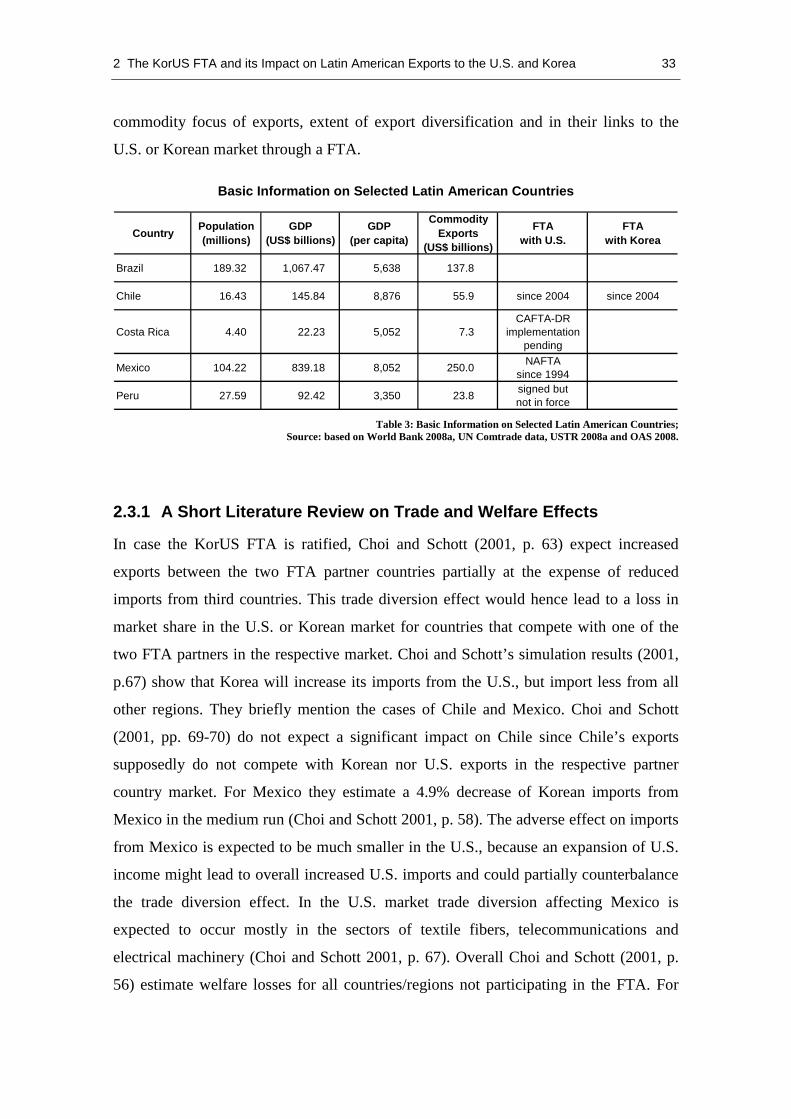

Table 3: Basic Information on Selected Latin American Countries...............................33

Table 4: Welfare Effects of the KorUS FTA on Latin America ....................................34

Table 5: Changes in Latin American Exports due to the KorUS FTA...........................34

v

Table 6: Trade with the Republic of Korea in 2006.......................................................36

Table 7: Trade with the United States in 2006 ...............................................................40

Table 8: Import Shares in the Korean Market in 2006...................................................43

Table 9: Import Shares in the U.S. Market in 2006........................................................44

Table 10: Product Penetration in the Korean Market in 2006........................................45

Table 11: Product Penetration in the U.S. Market in 2006.............................................46

Table 12: Top 5 Exports to the Korean Market in 2006.................................................47

Table 13: Top 5 Exports to the U.S. Market in 2006 .....................................................48

Table 14: Decomposition of ESI Values for the Korean Market ...................................52

Table 15: Decomposition of WESI Values for the Korean Market ...............................53

Table 16: Decomposition of ESI Values for the U.S. Market........................................56

Table 17: Decomposition of WESI Values for the U.S. Market ....................................57

Table 18: Highest Latin American RCAs in the Korean Market ...................................62

Table 19: RCAs Shared by the U.S. and Latin American Countries in the Korean Market.............................................................................................................................63

Table 20: Highest Latin American RCAs in the U.S. Market........................................64

Table 21: RCAs Shared by Korea and Latin American Countries in the U.S. Market ..65

vi

List of Abbreviations and Acronyms

APEC Asia-Pacific Economic Cooperation

CGE computable general equilibrium

CU customs union

ESI export similarity index

FDI foreign direct investment

FTA free trade agreement

GATS General Agreement on Trade in Services

GATT General Agreement on Tariffs and Trade

GDP gross domestic product

GTAP Global Trade Analysis Project

KorUS FTA United States - Republic of Korea free trade agreement

LA Latin America

MFN most-favored-nation

NAFTA North American Free Trade Agreement

n.e.s. not elsewhere specified

PTA preferential trade arrangement

RCA revealed comparative advantage

SITC Rev.3 Standard International Trade Classification, Revision 3

vii

UN Comtrade United Nations Commodity Trade Statistics Database

USITC United States International Trade Commission

WESI weighted export similarity index

WTO World Trade Organization

1 Preferential Trade Arrangements: Forms, Development and Implications

The world economy has changed considerably over the last few decades. The world

grew together in many ways experiencing an improvement of transportation networks,

an expansion of information and communication networks, the liberalization of

financial markets and an increase in world trade. The last decade, however, is

particularly marked by a new development:

“The growth of regional trade blocs has been one of the major developments in international relations in recent years. Virtually all countries are members of a bloc, and many belong to more than one. Over a third of world trade takes place within such agreements.” (Schiff and Winters 2003, p. 1)

There is a long list of reasons given by different stakeholders on why countries seek

economic integration. Jovanović (2006, p. 192) mentions e.g. the reduction in the cost

of trade through the elimination of trade barriers, technological advances and downward

pressure on prices through increased competition, the exploitation of economies of scale

in larger markets, improved efficiencies and a strengthened bargaining position with

external partners. This new aspect of the current economic reality also leaves the world

with many questions. What are the characteristics and determinants of the recent

proliferation of preferential trade arrangements1 (PTAs)? How will this new trend

influence the economic landscape? What impact of a preferential trade agreement can

be expected by member countries and by the rest of the world not party to the

agreement? Will there be winners and losers in the race towards trade blocs? How will

1 The term ‘preferential trade arrangements’ is used as an umbrella term for all discriminatory forms of economic integration in the context of this thesis.

2 Preferential Trade Arrangements: Forms, Development and Implications

the expansion of bilateral (or in a few cases plurilateral) trade negotiations as a trade

policy instrument change the way countries negotiate multilaterally?

In the light of the recent developments this paper tries to answer these complex

questions making use of relevant literature and analyzing trade data. In the first chapter

the paper explores the framework surrounding preferential trade arrangements giving an

introduction to basic theoretic concepts and highlighting recent trends concerning PTAs.

The second chapter analyzes the economic impact of a specific preferential trade

agreement. For this purpose the proposed free trade agreement (FTA) between the U.S.

and the Republic of Korea has been chosen, because it would be the United States’

“most commercially significant FTA in over a decade” (USTR 2007) and a FTA is the

form of economic integration most often chosen by countries negotiating bilaterally (see

section 1.2). A special emphasis of the second chapter lies on the impact that the FTA,

upon entering into force, might have on Latin American exports to the FTA member

countries and is performed with the help of case studies of Brazilian, Chilean, Costa

Rican, Mexican and Peruvian exports. The competitiveness of Latin American countries

in the U.S. and in the Korean market is of substantial interest as the U.S. is a traditional

export market for Latin America and the South Korean market could provide Latin

America with a valuable option for a diversification of export markets. Therefore the

impact of the proposed FTA on this region of the world seems especially relevant, but

has, so far, not been analyzed thoroughly in recent studies. Finally, the third chapter

addresses the influence of the recent spread of PTAs on the multilateral trading system

and its future as discussed in the respective literature.

1.1 Forms of Preferential Trade Arrangements

Countries have many options for structuring their trade relations with other nations. They

can pursue a multilateral approach seeking and granting market access via multilateral

negotiations on the rules of trade within the framework of the World Trade Organization

(WTO). One of the guiding principles of the WTO is the most-favored-nation (MFN)

principle according to which in general all countries have to receive equal treatment (WTO

2007, p. 10). Alternatively, countries can pursue strategies that are based on preferential

market access between two partner countries or among a group of several partner countries.

Although the pursuit of strategies giving preferential access to some countries seems to be

an apparent contradiction to the WTO’s MFN principle, there are provisions within the

1 Preferential Trade Arrangements: Forms, Development and Implications 3

General Agreement on Tariffs and Trade (GATT) and the General Agreement on Trade in

Services (GATS) that allow for certain exceptions (WTO 2007, p. 64). GATT article 24 and

GATS article 5 give permission to set up preferential trade arrangements provided that

certain criteria are met (WTO 2008b; WTO 2008d). They specify that “barriers should be

reduced or removed on substantially all sectors of trade in the group” and that barriers for

the outside world should not be raised. Under the so-called Enabling Clause (WTO 2008c)

there are also exceptions provided for developing countries that wish to reduce or eliminate

trade barriers among themselves. Since these possibilities for exceptions to the MFN

principle have become widely used over the last decades in the following an overview of

different forms of economic integration is given and the extent of commitments that these

forms of preferential trade arrangements entail is explained.

According to Balassa (1961, p. 4) economic integration can be defined “as a process and

as a state of affairs”. With regard to the definition as a process, the analysis of economic

integration is concerned with the “measures leading to the suppression of

discrimination” between different national states. Understood as a state of affairs,

economic integration results in “forms of economic integration” that “can be

characterized by the absence of discrimination in various areas” (Balassa 1961, p. 5).

Subsequently Balassa distinguishes five forms of economic integration each

characterized by varying degrees of integration.

The first of the five forms of economic integration mentioned by Balassa (1961, pp. 5-

6) is the free trade area, which is characterized by the abolition of tariffs and

quantitative restrictions in trade between the participating countries. The second form

introduced is the customs union, which in addition to the provisions of a free trade area

also requires the establishment of a common external tariff towards non-member

countries. The next higher form of integration is represented by a common market,

characterized by the elimination of not only trade restrictions but also restrictions

concerning factor movements. An economic union as the fourth form of economic

integration according to Balassa goes even further in its requirements and calls for the

“harmonization of economic, monetary, fiscal, social, and countercyclical policies.” The

highest form of integration is total economic integration. It is achieved by the

unification of all policies and the setting up of a supranational authority whose decisions

are binding for all member-countries. Figure 1 illustrates the first four forms (by other

4 Preferential Trade Arrangements: Forms, Development and Implications

authors also called ´types´, ´tiers´ or ´stages´) of economic integration of Balassa’s

concept matching each form with the corresponding areas that are characterized by the

absence of discrimination.

Figure 1: Main Forms of Economic Integration; Source: based on Blank et al. 1998, p. 35.

When comparing economic integration initiatives in real life with Balassa’s theoretic

categorization, it is noticeable that the distinctions between the different forms of

integration are not always as clear cut as Balassa’s concept might suggest. Nevertheless,

Balassa’s categorization is generally accepted and adopted by the relevant literature.

Some authors, however, do not include the last form (total economic integration)

because it is not viewed as a form of strictly economic integration but rather as political

integration (compare e.g. Blank et al. 1998, p. 34; Das 2004, p. 15). Others include this

stage of integration and express their differing view by adjusting the form’s name. It is,

e.g., termed ´complete political integration´ by El-Agraa (1989, p. 2) and ´political

union´ by Kaiser (2003, p. 28).

Furthermore, some authors add additional stages to the scheme that are embedded at a

degree of integration inferior to that of a free trade area. Jovanović (2006, p. 22), Das

(2004, p. 15) and Kaiser (2003, p. 27) e.g. include preferential trade (or tariff)

agreements, which eliminate tariffs on a specified number of commodities only or lower

tariffs among member countries relative to third parties without eliminating tariffs

completely. Jovanović also mentions the form of partial customs unions, which retain

their initial tariffs for trade among the member countries, but establish a common

external tariff on trade with the rest of the world.

In his contribution Das (2004, p. 15) distinguishes between shallow and deep stages of

integration grouping preferential trade (tariff) agreements, free trade areas and customs

unions as forms of shallow integration and common markets and economic unions as

Characteristics

Form

Free Trade Area

Customs Union

Common Market

Economic Union

harmonization/unification

of economic policy

free tradebetween members

common external tariff

full mobility offactors of production

1 Preferential Trade Arrangements: Forms, Development and Implications 5

forms of deep integration. Regardless of where you chose to draw the line between

shallow and deep integration, however, it is important to observe that economic

integration is not necessarily a gradual process in which countries continuously advance

from one stage of integration to the next higher form (Jovanović 2006, pp. 22-23).

According to their wishes and needs countries can negotiate to start at the degree of

integration that best fits their interests, they can remain at the same stage, advance

slowly, skip stages or they can cancel existing integration agreements. Furthermore, in

practice many agreements do not enter into force entailing immediate elimination or

reduction of tariffs, but are ´phased in´ lowering tariffs in various steps over a specified

period of time.

1.2 The Recent Proliferation of Preferential Trade Arrangements

Much has been talked and written about the ´new regionalism´ since the 1990s and

“´proliferation´of RTAs [regional trade arrangements] has become a common term, in

the press and relevant literature, to account for the increasing number of RTAs being

recorded in recent years” (Fiorentino et al. 2006, p. 2). But is regionalism (understood

as the spread of preferential trade arrangements) really a new phenomenon? In short:

yes and no.

Regionalism is, in fact, not a new phenomenon in itself. In 1664 e.g. a customs union of

the provinces of France was proposed and in 1834 the German Zollverein was

established as one of the earlier examples of a customs union (compare Schiff and

Winters 2003, p. 4; Jovanović 2006, p. 16; Blank et al. 1998, pp. 43-44). Furthermore,

according to Kaiser (2003, p. 20) multilateralism and regionalism have co-existed since

the multilateral trading system was established in form of the General Agreement on

Tariffs and Trade (GATT) in 1947. As she notes, however, in the past for most

countries multilateral negotiations were the dominant approach for arranging

international economic relations, whereas the massive proliferation of regional

arrangements within the last decade has definitely changed the current weighting of the

two approaches. Looking back at the last century two waves of regionalism can be

identified of which the first appears starting with the establishment of the European

Economic Community in 1957 and the second wave of regionalism dates to the 1990s

(Das 2004, p. 10; Kaiser 2003, p. 30).

6 Preferential Trade Arrangements: Forms, Development and Implications

Figure 2: Preferential Trade Arrangements Notified to the WTO according to GATT Art. 24, GATS Art. 5 and Enabling Clause; Source: based on WTO data (WTO 2008a).

As figure 2 shows the number of PTAs notified to the GATT increased slowly over time

and until into the mid-1970s there were still less than 50 notified agreements. Only in

the 1990s the number of notifications increased substantially and by now almost 400

PTAs have been notified to the GATT and the WTO. Therefore, first of all, a significant

quantitative change concerning PTAs can be observed. Nevertheless, it is important to

note, that out of the almost 400 PTAs notified only slightly more than 200 are actually

active. Additionally, it has to be mentioned that the WTO figures overstate the physical

number of agreements as countries have to submit a notification in case of accession to

an existing agreement and, since 1995, have to submit separate notifications for an

agreement containing provisions on trade and services (Fiorentino et al. 2006, p. 2). In

spite of methodological limitations, however, the increasing number of notifications

received by the WTO is still a valuable indicator for the spread of PTAs. In addition, the

percentage of world trade conducted under such agreements gives an impression of the

importance of regionalism in the modern world: According to direct communication

with the WTO’s Economic Research and Statistics Division the share of exports among

partners of PTAs (excluding the overlap of PTAs) in world exports was slightly over

40% in 2005 and 2006.

Preferential Trade Arrangements Notified to the WTO

0

5

10

15

20

25

30

35

1948

1951

1954

1957

1960

1963

1966

1969

1972

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

2005

2008

0

50

100

150

200

250

300

350

400

450

notif ications(left-hand scale)

notif ied(cumulative)

notif ied and active(cumulative)

1 Preferential Trade Arrangements: Forms, Development and Implications 7

There is not only a quantitative change regarding the spread of PTAs, there is also a

qualitative change. Whereas the old wave of PTAs consisted mostly of agreements

among neighboring countries, the new wave of regionalism is first and foremost

characterized by an ever increasing number of cross-regional alliances with a diverse

range of partners (Das 2004, p. 17). While in 2006 only 12% of the PTAs notified and

in force were cross-regional, among the agreements signed but not yet notified and

those still under negotiation 43% were of a cross-regional nature (Fiorentino et al. 2007,

p. 9). This steep increase in cross-regional alliances in combination with the trend to

rely increasingly on bilateral2, not plurilateral, negotiations is, according to Fiorentino et

al. (2007, p. 8), evidence for the new focus on strategic market access that guides

modern trade policy in most countries. Since most countries are members of various

PTAs simultaneously, in fact, some members are party to more than 20 different PTAs

(WTO 2008), an ever more complex net of preferential trade relationships is created

(see also chapter 3).

Yet another distinguishing characteristic of the recent development of PTAs is the

increase in alliances between developing/emerging-market economies and industrialized

countries (Das 2004, p. 64). As of December 2006 among the PTAs in goods notified to

the WTO 27% are between a partner from a developed and a partner from a developing

country. Among the agreements in services notified to the WTO 44% fall within this

category (Fiorentino et al. 2007, p 11).

The statistics also reveal that there is a strong tendency towards forming a free trade

area (FTA) instead of a customs union (CU). As of December 2006 84% of notified

PTAs in force were intended to be FTAs, 8% CUs and 8% partial scope agreements.

Among the PTAs signed, under negotiation and proposed as of December 2006 the

share of FTAs rises to 92%, whereas the share of partial scope agreements remains

almost unchanged at 7% and the share of customs unions drops to only 1% (Fiorentino

et al. 2007, p. 6). Schiff and Winters (2003, pp. 78-82) believes the current tendency

towards the creation of FTAs is due to the fact that CUs require common external

tariffs, that can be hard to agree on, and after their establishment more ongoing

2 Bilateral in this context means that the negotiations take place between two parties. One or both of the parties can, however, be a trade bloc consisting of more than one country.

8 Preferential Trade Arrangements: Forms, Development and Implications

coordination in all areas of trade policy thereby limiting the members’ sovereignty. He

points out that in order to reap the benefits of absent customs inspections for all goods

at intra-area borders in a CU trade policy has to be harmonized not only with regard to

tariffs but also with regard to non-tariff barriers. Fiorentino et al. (2007, p. 5) attribute

the increasing popularity of FTAs among the forms of economic integration to three

characteristics of this form: Fist, FTAs usually allow for faster negotiations. Second,

they offer more flexibility regarding the scope of the agreement and the choice of

partners. And third, they provide higher selectivity by allowing member countries to

agree to ambitious preferential concession while, at the same time, safeguarding each

member’s sovereignty over its trade policy. He concludes that the FTA is the form of

economic integration that best fits the modern world’s trade policy needs and

objectives.

Although the quantitative and qualitative changes regarding PTAs have been recorded

and continue to be monitored closely, the underlying reasons for the proliferation of

PTAs over the last decade are hard to single out. Kaiser (2003, pp. 31-32) e.g. identifies

several determinants leading to a more intense second wave of PTAs such as a changed

economic environment with better integration of world markets through the successive

liberalizations of trade under the GATT, financial liberalization and better information,

communication and transportation networks. She also points to a greater willingness of

developing countries to open up their economies and the changed attitude of the U.S.

towards bilateral trade agreements as likely causes for the recent proliferation of PTAs.

1.3 The Economic Impact of Free Trade Agreements in Theory

“The decision about entering into a customs union or any other type of integration has always been primarily political, but economic considerations usually play a very important role.” (Jovanović 2006, p. 23)

Not surprisingly, therefore the analysis of the economic impact of CUs, although with

small variations in the focus of analysis, is a frequent subject in introductory books to

economic integration and trade policy (compare e.g. Robson 1998, pp. 18-19;

Zimmermann 1999, p. 10; Jovanović 2006, p. 40; Schiff and Winters 2003, p. 55). A

partial equilibrium analysis of a FTA, however, is much harder to find in the relevant

literature. This might reflect the view that FTAs and CUs are similar forms of

preferential trade arrangements (for definitions see section 1.1) and thus the analysis of

1 Preferential Trade Arrangements: Forms, Development and Implications 9

one form is sufficient to shed light on the effects of both forms of economic integration

(Kreinin and Plummer 2002, p. 5). However, there are also essential differences

between customs unions and free trade areas regarding their operation and economic

impact, which should attract the observer’s attention (Robson 1998, p. 28). Taking into

account the special role of FTAs in the proliferation of PTAs this section will focus

particularly on the economic impact of FTAs. In the following a theoretical analysis of

the economic impact of free trade areas in a comparative static partial equilibrium

setting is presented and rounded off with further explanations.

The main observation and the main concern of the so-called traditional customs union

theory, starting with Viner’s famous contribution (Viner 1950), is summed up by Schiff

and Winters (2003, p. 31) with the following words:

“A trade bloc usually increases trade between its members. An important issue, however, is whether it “creates” trade […] or “diverts” it.”

To illustrate the concepts of trade creation and trade diversion and their economic and

welfare impact on a free trade area this section uses an example given by Robson (1998,

pp. 30-35). With the help of the model we can observe how trade in a certain good

between two FTA member countries and the rest of the world is affected by the entering

into force of the FTA. Being a comparative static partial equilibrium model Robson’s

example is subject to the typical but rather restrictive assumptions of homogeneous

goods, perfect competition in goods and factor markets, increasing marginal costs, the

absence of transportation costs and production factors that are mobile on a national level

but immobile across national borders.

Robson’s example (figure 3) shows a country (country H) forming a free trade area with

a partner country (P) and their respective domestic demand (Dh, Dp) and supply curves

(Sh, Sp). Whereas demand conditions are similar in both countries for the good in

question, the partner country is a more efficient producer with a relatively elastic supply

curve (Sp). The world supply price is given by Pw for both countries with world supply

assumed to be perfectly elastic. Before the free trade area is formed the home country

applies a tariff to all imports represented by the difference between Pw (the world

supply price) and Th (the tariff-inclusive price for imports in H). Before the entering

into force of the FTA H’s market is supplied by domestic production up to the quantity

10 Preferential Trade Arrangements: Forms, Development and Implications

L and the quantity LN is imported at the tariff-inclusive price of Th from the rest of the

world. The partner country (P) applies a prohibitive tariff to imports from the rest of the

world meaning that at the tariff-inclusive price of Tp demand in P is satisfied by

domestic production only.

Figure 3: Static Partial Equilibrium Analysis of a Free Trade Area; Source: Robson 1998, p. 31.

When a free trade area is formed between H and P the two countries eliminate all tariffs

on imports from the member countries but continue to apply their respective tariffs to

the imports from the rest of the world. In order to avoid that imports from the rest of the

world enter the free trade area through the country with the lowest tariff and are

subsequently distributed duty-free to the different FTA member countries (which would

be termed ‘trade deflection’) most FTAs establish rules of origin (Robson 1998, p. 28).

Rules of origin that determine which products are sought to have originated within the

free trade area and are therefore eligible for duty-free treatment have been created using

different criteria. Frequently used rules of origin are e.g. that a commodity needs to

have changed tariff classifications between import and export by a FTA member

country, that a specified percentage of the commodity’s sales price must consist of value

added in a member country or that a specified percentage of a commodity’s parts and

components must be purchased from member countries (Krueger 1999, p. 263).

Although rules of origin are essential for protecting the effectiveness of the external

tariffs of the individual member countries (Zimmermann 1999, p. 16), they can also

give rise to “exported” protectionism and distortions in trade flows as producers within

1 Preferential Trade Arrangements: Forms, Development and Implications 11

the free trade area might be forced to import more expensive within-area inputs to fulfill

the requirements for duty-free exports to other member countries (Schiff and Winters

2003, p. 79; Carlowitz 2003, p. 116)

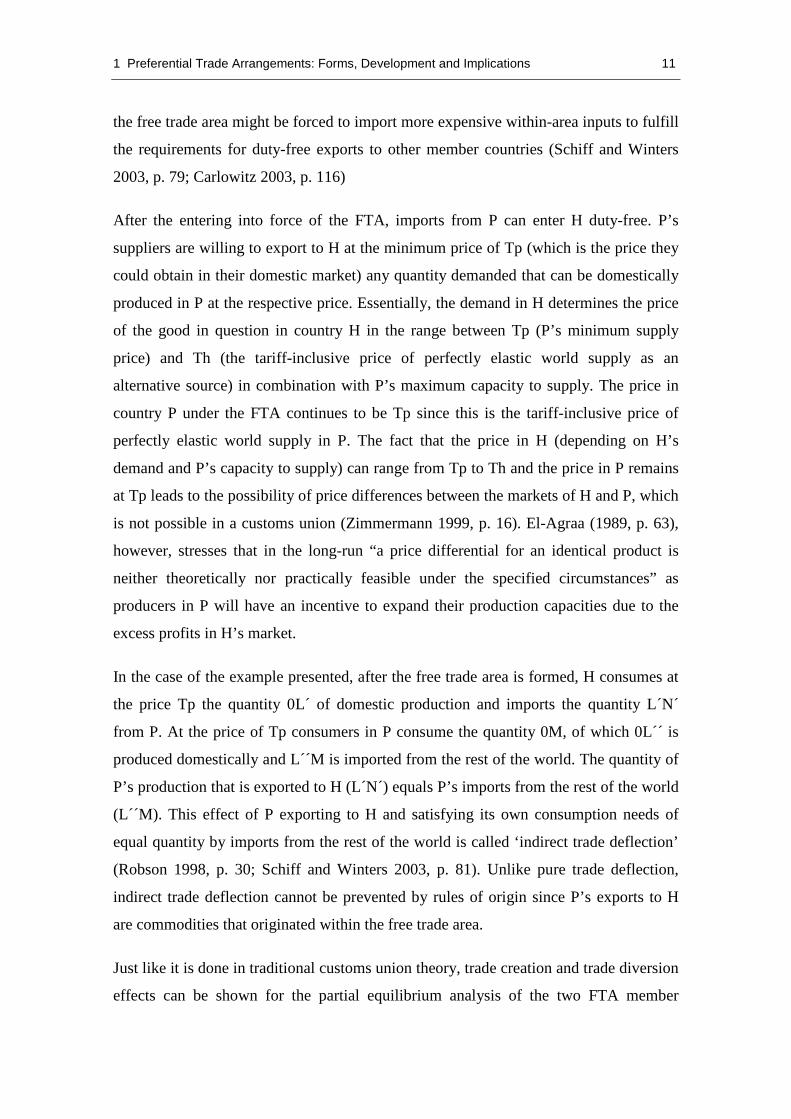

After the entering into force of the FTA, imports from P can enter H duty-free. P’s

suppliers are willing to export to H at the minimum price of Tp (which is the price they

could obtain in their domestic market) any quantity demanded that can be domestically

produced in P at the respective price. Essentially, the demand in H determines the price

of the good in question in country H in the range between Tp (P’s minimum supply

price) and Th (the tariff-inclusive price of perfectly elastic world supply as an

alternative source) in combination with P’s maximum capacity to supply. The price in

country P under the FTA continues to be Tp since this is the tariff-inclusive price of

perfectly elastic world supply in P. The fact that the price in H (depending on H’s

demand and P’s capacity to supply) can range from Tp to Th and the price in P remains

at Tp leads to the possibility of price differences between the markets of H and P, which

is not possible in a customs union (Zimmermann 1999, p. 16). El-Agraa (1989, p. 63),

however, stresses that in the long-run “a price differential for an identical product is

neither theoretically nor practically feasible under the specified circumstances” as

producers in P will have an incentive to expand their production capacities due to the

excess profits in H’s market.

In the case of the example presented, after the free trade area is formed, H consumes at

the price Tp the quantity 0L´ of domestic production and imports the quantity L´N´

from P. At the price of Tp consumers in P consume the quantity 0M, of which 0L´´ is

produced domestically and L´´M is imported from the rest of the world. The quantity of

P’s production that is exported to H (L´N´) equals P’s imports from the rest of the world

(L´´M). This effect of P exporting to H and satisfying its own consumption needs of

equal quantity by imports from the rest of the world is called ‘indirect trade deflection’

(Robson 1998, p. 30; Schiff and Winters 2003, p. 81). Unlike pure trade deflection,

indirect trade deflection cannot be prevented by rules of origin since P’s exports to H

are commodities that originated within the free trade area.

Just like it is done in traditional customs union theory, trade creation and trade diversion

effects can be shown for the partial equilibrium analysis of the two FTA member

12 Preferential Trade Arrangements: Forms, Development and Implications

countries in figure 3. Trade creation refers to the positive effect on resource allocation

from a shift from higher-cost domestic products to lower-cost partner country products.

Trade diversion refers to the negative resource allocation effect from a shift from lower-

cost imports from the rest of the world to higher-cost imports from the partner country

(Johnson 1960, p. 68.). The overall welfare effect induced by economic integration

depends on the balance between trade creation and trade diversion (Zimmermann 1999,

p. 11; Schiff and Winters 2003, p. 35).

Due to the lower prevailing price of Tp in H after the FTA consumers in H enjoy an

increased consumer surplus constituted by the area between Th and Tp to the left of the

demand curve (Dh) in figure 3. The decreased domestic production of 0L´ leads to a

decreased producer surplus equal to the area between Th and Tp to the left of the supply

curve (Sh). Since H does not import from the rest of the world anymore the government

in H will face a loss of tariff revenue shown by the area b and the rectangle above b.

The trade creation for H is therefore represented by the triangles a and c. Trade

diversion is shown by the rectangle b in figure 3. Since in our example the triangles a

and c are larger than the rectangle b the home country experiences a net welfare gain

after the free trade area is formed.

In country P the price remains unchanged at Tp after the FTA enters into force and

consequentially there are no changes in consumer or producer surplus. As P starts to

import from the rest of the world when the free trade area is formed P’s government

receives tariff revenue represented by the rectangle between Tp and Pw between L´´ and

M. Due to the effect of indirect trade deflection the partner country enjoys a net welfare

gain. The FTA would also lead to an improved position for the rest of the world as

exports to the newly formed free trade area increase due to indirect trade deflection and

make up for the loss in H’s market (L´´M > LN).

Within the scope of comparative static partial equilibrium analysis the main difference

between the effects of a tariff-averaging customs union and a free trade area lies in the

existence of indirect trade deflection. Due to trade diversion when a free trade area is

formed the rest of the world can face decreased exports to the FTA member countries

with higher tariffs for a certain good. Through the effect of indirect trade deflection,

however, imports from the rest of the world enter the free trade area at the more

1 Preferential Trade Arrangements: Forms, Development and Implications 13

efficiently producing countries (with assumed lower tariffs) making up for the shortfall

in domestic products in these countries due to their increased intra-FTA exports. Unlike

in the case of a tariff-averaging customs union with a common external tariff in a free

trade area imports from the rest of the world cannot be diverted completely (assuming

that the rest of the world is in fact the least-cost source for imports and that the partner

countries supply is not perfectly elastic). In fact, in the setting of a static partial

equilibrium model the rest of the world can gain from the creation of the free trade area

through the effect of indirect trade deflection (Zimmermann 1999, p. 18).

A glance at the theoretical structure of international trade and the directions of trade

flows, however, reveals that in real life the outcomes of the model cannot be observed

with the accuracy suggested by traditional customs union theory. The static partial

equilibrium model and the effect of indirect trade deflection e.g. suggest that for a given

commodity one of the following two scenarios should hold true:

Scenario A: The quantity produced in P is sufficient to satisfy H’s demand for

imports. Therefore the prevailing price in H’s market is lower than Th and P is

the exclusive source of imports in H.

Scenario B: The quantity produced in P is not sufficient to satisfy H’s demand

for imports. Therefore the prevailing price of the commodity in H is Th and H

imports from the partner country up to its maximum capacity to supply and

imports the remaining quantity from the rest of the world. Consequently, P’s

entire production is sold to H.

In the real world though we can observe that usually countries do not import from one

exclusive source only and that countries do not tend to sell their entire domestic

production abroad either. The reason for the incongruence of the model’s suggestions

with our observations may well lie in the model’s assumptions.

According to Schiff and Winters (2003, p. 31) the static partial equilibrium analysis is

“based on a view of the world in which intercountry trade is driven entirely by

differences in productivity and factor endowments.” Parting with the assumption of

homogeneous goods and assuming product differentiation instead allows for the

existence of intra-industry trade, which makes up a good part of actual international

14 Preferential Trade Arrangements: Forms, Development and Implications

trade. Allowing for product differentiation might lead to monopoly power or imperfect

competition among the producers, which would contradict the assumption of perfect

competition. Whereas the model assumes constant returns to scale there are many

products for which economies of scale can be exploited during the production process.

In fact, reaping economies of scale in production is often seen as one of the main

benefits of the access to an expanded market through economic integration (Kreinin and

Plummer 2002, p. 24; Robson 1998, pp. 37-38). Another point often stressed is that

economic integration increases competition and therefore leads to the elimination of

internal inefficiencies increasing productivity levels (Schiff and Winters 2003, p. 50). In

the world depicted by a static partial equilibrium model, however, this would not be

feasible since it is assumed that all factors of production at all times are used optimally

so that there are no inefficiencies to be eliminated. Furthermore the existence of

transport costs in the real world is not taken into account by static partial equilibrium

models either and might help to explain why there must be limits to the effect of

indirect trade deflection.

Being static in nature the model presented also disregards some dynamic effects that are

key elements within the forces that affect economic activity, such as technological

advances and decisions concerning the location of investment and its rate of growth

(Robson 1998, p. 37). In fact, regional integration might induce changes in investment

behavior and frequently leads to a temporary investment boom in the newly integrated

area (Kreinin and Plummer 2002, p. 28; Schiff and Winters 2003, pp. 220-221).

Investment opportunities in the partner country might be perceived as more attractive

due to strategic decisions to locate new production facilities in the partner country

market and, possibly, due to a more clearly defined investment environment after the

implementation of a PTA. Assuming international mobility of capital and a finite

volume of investable funds investments may be made within the economic integration

area that otherwise would have been more efficiently made outside the integration area.

Although all issues mentioned above have been discussed in more recent literature on

customs union theory no model has emerged that seems as illustrative as the “classic”

way to show the effects of trade creation, trade diversion and indirect trade deflection

with the help of a static partial equilibrium analysis. El-Agraa (1989, p. 27) concludes

that most of the effects not included in the standard static partial equilibrium analysis

1 Preferential Trade Arrangements: Forms, Development and Implications 15

are long term in nature and, with the exception of internal economies of scale, “cannot

be tackled in orthodox economic terms”. (For examples on the effects of internal

economies of scale in customs unions see El-Agraa 1989, pp. 27-28 or Robson 1998,

pp. 41-48.) Taking into account the various limitations of the assumptions of this

approach, special care has to be taken when interpreting the results of the static partial

equilibrium analysis presented in this section (Jovanović 2006, p. 30). As Robson

(1998, p. 18) puts it: taking into account “the character of modern production and trade

[…] the outcome of customs unions (and other trading blocs) may significantly differ

from the ‘predictions’ of orthodox theory.” It therefore remains up to debate if the

entering into force of a FTA might displace exports of the rest of the world to the free

trade area. Depending on the question if demand for the exports of the rest of the world

changes terms of trade changes would have to be considered as well.

In the case that after the economic integration of two countries the displacement of

exports of the rest of the world occurs, it seems relevant to dedicate a few sentences to

the situation of these third parties. According to orthodox theory a displacement of

exports of the rest of the world does not matter as far as the welfare of the rest of the

world is concerned. The resources used to produce the exports can be redirected to the

production of goods that are consumed domestically and since factors are perfectly

mobile within national borders there will be an immediate and costless adjustment to the

new situation. In the real world in contrast we might find that adjustment processes do

not run quite as smoothly as workers trained for export industries might have to change

workplaces and fixed capital has to be transferred to different industries. Furthermore,

there might be a welfare loss for the rest of the world incurred if the factors used for one

unit of exports create larger welfare as exports than the same factors redirected to

alternative uses. According to Schiff and Winters (2003, p. 214) this might be the case

if exporting generates supernormal profits because of imperfectly competitive export

markets, if the decrease in exports leads to a loss of economies of scale in production or

if exports have positive externalities.

Since no general statement about the economic impact of a free trade agreement can be

derived theoretically the effects on trade patterns and welfare have to be studied on a

case-by-case basis. Using the example of the proposed FTA between the U.S. and the

16 Preferential Trade Arrangements: Forms, Development and Implications

Republic of Korea an analysis of estimated welfare effects and possible changes in trade

flows will be performed in the following chapter.

2 The KorUS FTA and its Impact on Latin American Exports to the U.S. and Korea

The proposed FTA between the U.S. and the Republic of Korea is an interesting

example for the analysis of economic integration for various reasons. First of all, the

economic size and importance of the FTA members draws attention. A FTA between

the world’s largest economy and the world’s 13th largest economy (ranked by GDP in

2006 according to the World Bank’s World Development Indicators database) leads to

the expectation of a sizeable impact of the KorUS FTA on worldwide trade relations. In

fact, the KorUS FTA “would be the largest bilateral accord America has struck since

NAFTA was passed in 1993, as well as the first with a large Asian economy”

(Economist 2007).

Secondly, being a bilateral and cross-regional FTA the agreement between the U.S. and

Korea demonstrates the main characteristics of the form of economic integration most

commonly chosen by trade partners in the recent wave of proliferation of PTAs. In

addition, the U.S. and the Korean market play both interesting as well as differing roles

as a destination for Latin American exports. Whereas the U.S. market is a rather

established destination for Latin American countries’ exports and in many cases is of

vital importance, the Korean market could offer an interesting opportunity for

diversifying export partners and for taking advantage of the Asian economic

development.

In the following this chapter provides some background information on the

development and basic provisions of the KorUS FTA. Subsequently, the expected

effects of the agreement on the member countries are presented starting with an

overview of the state of current U.S.-Korea trade relations and moving on to the

summary of the results of different economic impact studies. As chapter 1 has

18 The KorUS FTA and its Impact on Latin American Exports to the U.S. and Korea

demonstrated FTAs can also have a profound impact on third countries not party to the

FTA since the FTA partners’ preferential market access can lead to increased

competition and altered trade flows. Therefore the chapter closes with an analysis of

current Brazilian, Chilean, Costa Rican, Mexican and Peruvian exports to the U.S. and

the Korean market in order to subsequently draw conclusions on the magnitude and

areas of impact of the entering into force of the KorUS FTA.

2.1 History and Basic Facts of the KorUS FTA

Based on the extensive trade relation between the U.S. and Korea some business groups

as well as single politicians and the academia had been discussing a possible FTA

between the two countries for several years and in late 2004 trade officials started

exploratory trade talks (Schott 2006). Only in February 2006, however, the U.S. and the

Republic of Korea announced that they intended to launch the official negotiation of a

FTA, which was to start in May 2006 (USTR 2006). From there negotiations proceeded

at an accelerated pace and after only ten months and eight rounds of negotiations the

successful conclusion of a FTA was reached on 1 April 2007 (USTR 2007). Due to the

speedy negotiations and the immediate notification of the U.S. Congress the KorUS

FTA became the last U.S. trade agreement still eligible for the so-called “fast-track”

procedures (Schott 2008, p. 83). In order to be eligible for “fast-track” procedures the

U.S. president has to notify Congress 90 days in advance about any trade agreement he

plans to sign and President Bush’s trade promotion authority was to expire the end of

June 2007. The “fast-track” rules require Congress to limit debate and cast a yes or no

vote on a trade agreement without being able to single out any provision of the

agreement (Economist 2007/2007a).

The KorUS FTA was finally signed by the two countries’ representatives on 30 June

2007 (USTR 2007a) and is still awaiting its ratification by the U.S. Congress and the

Korean National Assembly. After the U.S. International Trade Commission had

submitted its required report (USITC 2007) on the FTA the formal legislative process

could have begun in the U.S., but since then things have been moving rather slowly.

Schott (2008, p. 79) sees the ratification of the agreement as “a major challenge for both

governments in 2008.” He points to three main reasons for the slow progress which he

sees in U.S. reservations concerning Korea’s ban of American beef exports, tariff-

2 The KorUS FTA and its Impact on Latin American Exports to the U.S. and Korea 19

structures for automobile exports to Korea and the U.S. presidential primaries (Schott

2008, p. 84).

The campaigning for the U.S. presidential elections makes a passing through Congress

of the KorUS FTA unlikely in the near future as especially the Democratic majority

seems reluctant to support trade agreements (Economist 2007a). Furthermore Korea’s

17th National Assembly has not ratified the KorUS FTA before the elections in April

2008 so that the 18th National Assembly had to start a new debate on the topic, which is

expected to lead to time-consuming disputes (Cheong 2008). However, the Korean

president Lee Myung-bak said that he is “confident that the U.S. Congress will ratify

the Korea-U.S. free trade agreement by the end of this year” after having met President

Bush for consultations in April (Korea.net 2008). Additionally, the Korean government

lifted the ban on imports of U.S. beef (USTR 2008). The recent violent protests in South

Korea, however, cast a shadow on the progress towards the ratification of the KorUS

FTA (Sang-hun 2008, Economist 2008).

If ratified by the two countries’ legislative bodies, the FTA between the U.S. and South

Korea will cover more trade than any other U.S. trade agreement except NAFTA

(Schott et al. 2006, p. 17) and will encompass a wide range of topics. Of the over

10,000 tariff lines of the two countries on commodities currently 38% of U.S. and 13%

of Korean tariff lines are free of duty under MFN treatment. Upon entry into force of

the KorUS FTA an additional 45% of U.S. tariff lines and 67% of Korean tariff lines

will become free of duty immediately for the respective FTA partner country. Over the

five years following the entry into force of the KorUS FTA the total number of duty-

free tariff rates will rise to over 90% for both countries and will eventually reach 99%

for U.S. tariff lines and 98% for Korean tariff lines ten years after the trade agreement’s

implementation (USITC 2007, pp. 1-7 to 1-8). Thereby within the area of industrial and

consumer products almost 95% of bilateral trade will become duty-free within three

years of the KorUS FTA’s entry into force. The U.S. government also estimates that

over 50% of current U.S. agricultural exports will become duty-free immediately while

many of the remaining agricultural products will enjoy two- or five-year tariff phase-

outs (USTR 2007b).

20 The KorUS FTA and its Impact on Latin American Exports to the U.S. and Korea

Furthermore under the KorUS FTA the U.S. and Korea will grant each other market

access to almost all major service sectors and expand the obligations to open

government procurement processes beyond their WTO commitments among each other.

The KorUS FTA will also establish a stronger legal framework and broader protection

for investments among the member countries. Additionally, the FTA includes

provisions promoting greater protection of intellectual property rights and their

enforcement. Through the exchange of comments, the establishment of working groups

and dispute settlement mechanisms the KorUS FTA also seeks to improve transparency

and coordination in the area of regulations and technical barriers to trade.

2.2 The Impact of the KorUS FTA on the Member Countries

Since a possible FTA between the U.S. and the Republic of Korea had been discussed

for several years the effects that can be expected by the member countries upon the

entry into force of such an agreement are well studied. There is a rich set of literature

and economic impact studies on the topic that gives valuable input to the evaluation of

the likely effects of the KorUS FTA on its member countries. Although the impact

studies reviewed part from very different liberalization scenarios and use different

methods, models and database inputs, in the following a short literature summary

presents the most important findings of these contributions.

But before the different studies are presented it is essential to take a look at the status

quo of U.S.-Korea trade relations in order to get an impression of the base that leverage

is to be brought to bear on by the proposed KorUS FTA. Therefore in the following

section the quantity and characteristics of trade between the U.S. and the Republic of

Korea are analyzed. The main focus of analysis is on trade in commodities since trade

data is more readily available and classified in more detail in contrast to trade data in

services. Unless otherwise stated in the following all trade data is obtained from the

United Nations Commodity Trade Statistics Database in the classification of SITC

Rev.3.

2 The KorUS FTA and its Impact on Latin American Exports to the U.S. and Korea 21

2.2.1 Current U.S.-Korea Trade and Its Development

Since the Republic of Korea began its remarkable path of export driven growth in the

1960s it gradually turned into one of the United States’ leading trading partners. U.S.

exports to South Korea were only about US$ 5 billion in 1981, but amounted to over

US$ 32 billion in 2006. The growth in U.S. imports from Korea was even more

impressive: Whereas U.S. imports from Korea were only US$ 5.5 billion in 1981, they

reached US$ 47.5 billion in 2006. For the last twenty years, with the exception of the

years around the Asian financial crisis, the U.S. ran a trade deficit with South Korea.

Figure 4: U.S. Commodity Trade with South Korea; Source: based on UN Comtrade data.

Based on total trade South Korea is the United States’ seventh largest trading partner

(USITC 2007, p. 1-3). Korea’s share of total U.S. commodity trade was, however, only

3% in 2006, compared to a share of 18% for the United States’ neighbor and top trading

partner Canada, 12% for China of 11% for Mexico. Over the last decade Korea’s trade

share has been relatively stable, whereas Japan’s trade share decreased gradually and

China’s trade share has doubled since the year 2000 (see figure 5). In 2006 Korea was

the United States’ seventh largest export market as well as the seventh largest source of

U.S. imports.

U.S. Commodity Trade with South Korea(billions of US$)

0

10

20

30

40

50

60

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Exports Imports

22 The KorUS FTA and its Impact on Latin American Exports to the U.S. and Korea

Figure 5: Shares of Total U.S. Commodity Trade; Source: author’s calculations, based on UN Comtrade data.

Considering total commodity trade the U.S. accounts for about 12% of the trade flows

with Korea thereby taking third place in the list of Korea’s leading trade partners after

China with a share of 19% and Japan with a share of about 12%. Whereas the United

States’ share has been decreasing since 1999 from a former level of about 20%, China’s

share of trade with South Korea has tripled since 1995. In 2006 the U.S. was Korea’s

second largest export market (following China) and its third largest source of imports

(following Japan and China).

Figure 6: Shares of Total Korean Commodity Trade; Source: author’s calculations, based on UN Comtrade data.

Shares of Total U.S. Commodity Trade for Selected Countries(Percentage)

0%

5%

10%

15%

20%

25%

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Canada China Japan Mexico Korea

Shares of Total Korean Commodity Trade for Selected Countries(Percentage)

0%

5%

10%

15%

20%

25%

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

China Japan USA

2 The KorUS FTA and its Impact on Latin American Exports to the U.S. and Korea 23

A measure for the intensity of trade flows between two countries (Michaely 2004, p.

125) sets home country imports from a partner country divided by total home country

imports in relation to the partner country’s share of world exports (which also represents

its share of world imports). A value of one therefore indicates that the partner country’s

share of home country imports equals its average share in worldwide trade flows. A

value above unity indicates a preference of the home country for the partner country’s

exports and a value below unity the contrary. The intensity ratio jointly reflects all

factors that contribute to the bilateral trade flow with the exception of the partner

country’s size. Calculating the respective figures for the U.S. and Korea reveals that

Korea (with a value of 1.09) has a slight preference for importing from the U.S.,

whereas something is constraining U.S. imports from Korea for which the intensity ratio

is only 0.79.

A factor that can influence the intensity of trade flows is the compatibility of the

commodity structure of the home and the partner country’s bilateral trade flows. An

index of compatibility of trade flows can measure if the partner country exports to the

world market are exactly the commodities the home country seeks to import. Such an

index (Michaely 2004, pp. 127-129) can be devised as

Smjxk = 1 - ∑׀mij - xik2 / ׀

where Smjxk = index of compatibility of imports of country j (home) with exports of country k (partner), mij = share of good i in total imports of the home country and xik = share of good i in total exports of the partner country.

The index can range between zero and one. A value of one signals that the structures of

the commodity flows match exactly, whereas a value of zero would imply that there is

no similarity at all between the imports of the home country and the exports of the

partner country. The higher the index value, the stronger is also the potential for a

displacement of imports from the rest of the world by imports from the partner country

in the case that the two countries implement a PTA.

According to calculations based on data on a three digit aggregation level and as a

three-year average of import and export shares between 2004 and 2006 the index

24 The KorUS FTA and its Impact on Latin American Exports to the U.S. and Korea

assumes a value of 0.51 for the compatibility of U.S. imports and Korean exports and a

value of 0.55 for the compatibility of Korean imports and U.S. exports. Thus, the index

shows that there is a significant overlap between the two countries’ exports to the world

market and their respective import demands, although they are far less than a perfect

match. In order to take a more detailed look on the trade relation between the U.S. and

South Korea in the following the composition of the bilateral commodity trade flows is

analyzed.

Looked at on a one-digit aggregation level in 2006 U.S. exports to Korea mainly

consisted of machines and transport equipment (52%), chemicals (13%) and

miscellaneous manufactured articles (11%). Broken down on a two-digit aggregation

level U.S. exports mainly fell into the division of electrical machinery, apparatus and

appliances (20%), other transport equipment (11%), special industries machinery (6%),

organic chemicals (5%) and scientific equipment (5%). Korean exports on a one-digit

aggregation level were mostly concentrated in the area of machines and transport

equipment accounting for 67% of Korean exports to the U.S. in 2006. Manufactured

goods classified chiefly by material ranked second with 13% and mineral fuels and

lubricants and miscellaneous manufactured articles competed for third place with 7%

each. Analyzed on a two-digit level Korea exports to the U.S. mainly consisted of road

vehicles (26%), telecommunications and sound equipment (14%), electrical machinery,

apparatus and appliances (11%), petroleum and petroleum products (7%) and office and

automatic data-processing machines (6%).

According to information of the Economic Research Service of the U.S. Department of

Agriculture (USDA 2008) the U.S. has been one of the main sources of Korean

agricultural imports for decades. In 2006 the U.S. exported US$ 2.85 billion in

agricultural goods to Korea, which made Korea the sixth-largest market for agricultural

exports. Major U.S. agricultural export items were corn, meat, hides, soybeans, milling

wheat and cotton. Growth potential is seen especially in the area of consumer-ready

products (e.g. fruits, nuts, vegetables, meat, preparations thereof), which account for

roughly a third of current U.S. agricultural exports to Korea. Due to a relatively small

arable land area Korea’s agricultural production shows a weak export-focus. In 2006

U.S. agricultural imports from South Korea amounted to only US$ 217 million with the

main export items being ramen instant noodles, pears and bean pastes.

2 The KorUS FTA and its Impact on Latin American Exports to the U.S. and Korea 25

U.S. service exports to Korea in 2007 add up to US$ 13.6 billion according to U.S.

international transactions accounts data (BEA 2008). At an average annual growth rate

of about 9% U.S. service exports to Korea almost doubled between 1999 and 2007.

They currently account for 29% of total U.S. exports of goods and services to Korea, up

from 24% in 1999. In 2007 the biggest subgroup of U.S. service exports was the

subgroup of ‘other private services’ comprising about a third of service exports to

Korea. U.S. services imports from Korea amounted to US$ 8.8 billion in 2007. Their

share of total U.S. imports of goods and services from Korea has remained relatively

stable around 15% since 1999. The annual growth rate of U.S. services imports from

Korea between 1999 and 2007 was 6% on average. The biggest services subgroup in

2007 was ‘other transportation’ with a share of 36% of total U.S. services imports from

Korea.

2.2.2 Estimated Effects on Trade and Welfare for the U.S. and Korea

During the years leading up to the conclusion of negotiations between the U.S. and the

Republic of Korea a range of studies has been prepared concerning the possible effects

of a U.S.-Republic of Korea FTA. The studies simulate the results of trade policy

changes under a bilateral trade agreement in areas such as changes in imports and

exports, sectoral output and welfare. Most studies surveyed made use of the widespread

Global Trade Analysis Project (GTAP) model. Only the study by Kiyota and Stern used

the Michigan model. These two models both belong to the class of computable general

equilibrium (CGE) models and have become the two most commonly used CGE models

over the last years (Piermartini and Teh 2005, pp. 10-11).

A CGE model tries to mirror the functional relations and sectoral linkages of an

economy with the help of a large set of equations solved by a computer. It can thus be

used for the ex-ante evaluation of effects on resource allocation, distribution and

economic welfare induced by a trade policy change represented by the change in the

model’s exogenous variables (Willenbockel 1994, pp. 40-44). A large majority of CGE

models adheres to the assumptions of general equilibrium theory implying perfect

competition in goods and factor markets, market clearing, full employment of factors

and products differentiated only by country of origin. Most CGE models are

comparative static in nature and compare the equilibrium before and after the policy

change without taking into account the timeframe and costs required for the adjustment

26 The KorUS FTA and its Impact on Latin American Exports to the U.S. and Korea

or the evolution of macroeconomic variables. CGE models should therefore not be

regarded as forecasts of economic data such as the change in GDP that will actually

occur in the year following the implementation of an FTA. Instead the numbers

produced by CGE simulations should only be used to give an impression of the order of

magnitude that a trade policy change is expected to induce regarding resource

allocation, trade flows and welfare holding all other things equal (Piermartini and Teh

2005, p. 53).

With the exception of the study of the U.S. International Trade Commission (USITC)

dating from September 2007 all studies taken into account in the following had been

prepared before FTA negotiations between the U.S. and Korea have been concluded or

negotiation results were publicly available. Therefore the surveyed studies part from

different liberalization scenarios according to the authors’ interests at the time of

preparation. Whereas in general the studies analyze the effects of tariff removal for

agricultural products and manufactures, some studies exclude certain agricultural

products or additionally include a partial liberalization of trade in services. But the

studies presented do not only differ in terms of the liberalization scenario assumed, they

also use different models, databases and base years, which can affect their results (see

figure 8). The Kiyota and Stern study e.g. uses the Michigan model which, in contrast to

a typical GTAP model, allows for imperfect competition and product differentiation at

the firm level and thus does not exhibit large terms of trade effects common in the

GTAP model (Kiyota and Stern 2007, p. 6). Furthermore some studies have also

included dynamic simulations in which they allow for capital accumulation in form of

foreign direct investment.

In line with general expectations derived from customs union theory all studies

surveyed estimate a significant increase in bilateral trade flows between the U.S. and

Korea due to the preferential market access granted under the FTA. The USITC (2007,

p. 2-9) e.g. estimates that U.S. exports of goods to Korea increase by US$ 9.7 to 10.9

billion (22.6-25.3%) and U.S. imports of goods from Korea by US$ 6.4 to 6.9 billion

(9.9-10.6%) after the implementation of the KorUS FTA. According to Kiyota and

Stern (2007, p. 44) U.S. exports to Korea increase by US$ 9.2 billion and U.S. imports

from Korea by US$ 6.9 billion. Choi and Schott (2004, p. 185) give an estimate of a

2 The KorUS FTA and its Impact on Latin American Exports to the U.S. and Korea 27

46% increase of U.S. exports to Korea and a 26% increase in U.S. imports from Korea

in the medium run following the implementation of an FTA.

Some of the studies reviewed give simulation results on sectoral effects possibly

induced by a FTA between the U.S. and Korea. The USITC (2007, p. 2.12) e.g. expects

the largest percentage growth in U.S. exports to Korea in agricultural goods (dairy,

bovine and other meat products), wearing apparel and beverages and tobacco. The

largest increase in value of U.S. exports to Korea is expected in chemical, rubber and

plastic products, bovine and other meat products and food products. Schott et al. (2006,

p. 3) are of the opinion that the largest increase in U.S. exports to Korea might occur in

services, especially in financial and knowledge-based sectors, whose liberalization is

not analyzed in many CGE models. U.S. imports from Korea are found to increase the

most in percentage terms for dairy products, wearing apparel, leather products, textiles

and vegetable oils and fats by the USITC. In terms of value imports from Korea are

expected to increase the most in textiles, motor vehicles, wearing apparel, machinery

and equipment, and chemical, rubber and plastic products. Much of the estimated

increase in U.S. imports of Korean textiles and apparel (85% and 91% respectively) and

more than half of the increase in passenger vehicles will, however, be a result of trade

diversion from other sources (USITC 2007, p. 2-12). Overall the different studies found

positive sectoral output effects (see table 1) for the U.S. economy mostly for

agricultural goods and processed foods, whereas negative output effects are estimated

especially for textiles and apparel. Choi and Schott (2004, p. 190) also expect a negative

impact on the U.S. steel and electronics sector. Nevertheless, the output and

employment effects of the KorUS FTA for the U.S. are expected to be negligible

considering the overall size of the U.S. economy relative to the Korean economy

(USITC 2007, p. xvii).

28 The KorUS FTA and its Impact on Latin American Exports to the U.S. and Korea

Un

ited

Sta

tes

So

uth

Ko

rea

Un

ited

Sta

tes

Sou

th K

ore

a

McD

anie

l an

d F

ox

(200

1)ag

ricul

ture

text

iles

and

appa

rel

Ch

oi a

nd

Sch

ott

(200

1)

agric

ultu

re,

fore

stry

and

fish

erie

s,

proc

esse

d fo

od

proc

esse

d fo

od,

text

iles

and

appa

rel,

chem

ical

s, r

ubbe

r, p

last

ics

text

iles

and

appa

rel

agric

ultu

re,

fore

stry

and

fish

erie

s,

dura

ble

man

ufac

ture

s

Lee

and

Lee

(200

5)

garm

ents

and

leat

her,

text

iles,

auto

mob

iles

and

part

s,ch

emic

als,

ser

vice

s

othe

r tr

ansp

ort e

quip

men

t,el

ectr

onic

s,m

achi

nery

Sch

ott

et

al. (

2006

)(f

or v

ersi

on o

f FT

A

excl

udin

g ric

e)ot

her

prim

ary

prod

ucts

text

iles,

app

arel

, lea

ther

,m

etal

s an

d ot

her

low

er-t

echn

olog

y m

anuf

actu

ring

very

sm

all r

educ

tions

fo

r m

ost s

ecto

rs

othe

r pr

imar

y pr

oduc

ts,

dura

ble

man

ufac

ture

s,bu

sine

ss s

ervi

ces

Kiy

ota

an

d S

tern

(200

7)

agric

ultu

re, f

ood,

beve

rage

s, to

bacc

o,ch

emic

als,

nonm

etal

lic m

iner

al p

rodu

cts,

mac

hine

ry a

nd e

quip

men

t,ot

her

man

ufac

ture

s,

othe

r pr

ivat

e se

rvic

es

rice,

whe

at, l

ives

tock

, te

xtile

s an

d ap

pare

l, le

athe

r pr

oduc

ts a

nd fo

otw

ear,

tr

ansp

orta

tion

equi

pmen

t

text

iles

and

appa

rel

othe

r gr

ains

,ve

geta

bles

and

frui

ts,

oil s

eeds

, oth

er c

rops

,ot

her

man

ufac

turin

g,se

rvic

es

U.S

. Int

ern

atio

nal

Tra

de

Co

mm

issi

on(2

007)

smal

l cha

nges

in th

e ag

ricul

tura

l sec

tor

(bov

ine

and

othe

r m

eat p

rodu

cts,

ca

ttle,

cer

eal g

rain

s, d

airy

pr

oduc

ts, o

ther

ani

mal

pro

duct

s),

proc

esse

d fo

ods,

bev

erag

es

smal

l cha

nges

for

padd

y an

dpr

oces

sed

rice,

oils

eeds

,w

heat

, pla

nt-b

ased

fibe

rs,

wea

ring

appa

rel,

text

iles,

man

ufac

ture

s,el

ectr

onic

equ

ipm

ent

Su

mm

ary

of M

od

eled

Sec

tora

l Out

pu

t Eff

ects

of

the

Kor

US

FT

A

Tab

le 1

: Sum

mar

y of

Mod

eled

Sec

tora

l Out

put E

ffect

s of t

he K

orU

S F

TA

; Sou

rce:

pre

pare

d by

aut

hor.

Stu

dy

Po

siti

veN

egat

ive

Ch

ang

es in

Sec

tora

l Ou

tput

2 The KorUS FTA and its Impact on Latin American Exports to the U.S. and Korea 29

Positive output effects for the Korean economy are expected especially for textiles and

apparel as well as for leather products and footwear (see table 1). Some studies see

positive output effects also for chemicals, lower-technology manufacturing and

automobiles and parts. Negative output effects are expected for Korean agriculture and

durable manufactures. In general Choi and Schott (2004, p. 189) expect the heavily

subsidized Korean agricultural sector to be “the biggest loser” from a possible FTA

between the U.S. and Korea. Kiyota and Stern’s model foresees a shift of Korean

employment from the more capital-intensive to the relatively labor-intensive

manufacturing sectors. Depending on the pace of the implementation of the FTA the

arising sectoral changes might be large enough to cause adjustment problems for the