theme watcher navigating a thematic investing …...2 thematic investing 09 january 2015 contents...

TRANSCRIPT

>> Employed by a non-US affiliate of MLPF&S and is not registered/qualified as a research analyst under the FINRA rules. Refer to "Other Important Disclosures" for information on certain BofA Merrill Lynch entities that take responsibility for this report in particular jurisdictions. BofA Merrill Lynch does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Refer to important disclosures on page 86 to 88. Analyst Certification on Page 85. 11469307

Thematic Investing Thematic Investing

Theme Watcher – Navigating a thematic investing landscape

Equity | Global | Thematic Investing 09 January 2015

Beijia Ma >> Equity Strategist MLI (UK)

Sarbjit Nahal >> Equity Strategist MLI (UK)

Manish Kabra, CFA >> Equity & Quant Strategist MLI (UK)

Click the image above to watch the video.

A Transforming World

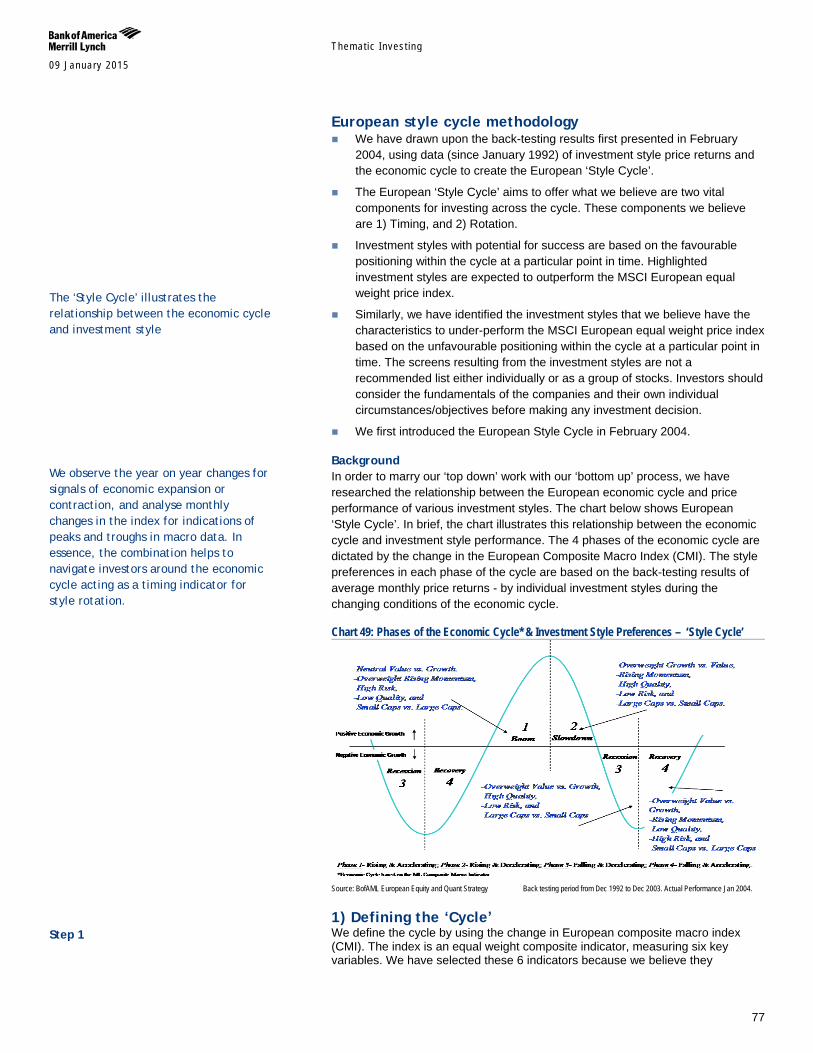

Navigating a Transforming World, introducing Theme Watcher

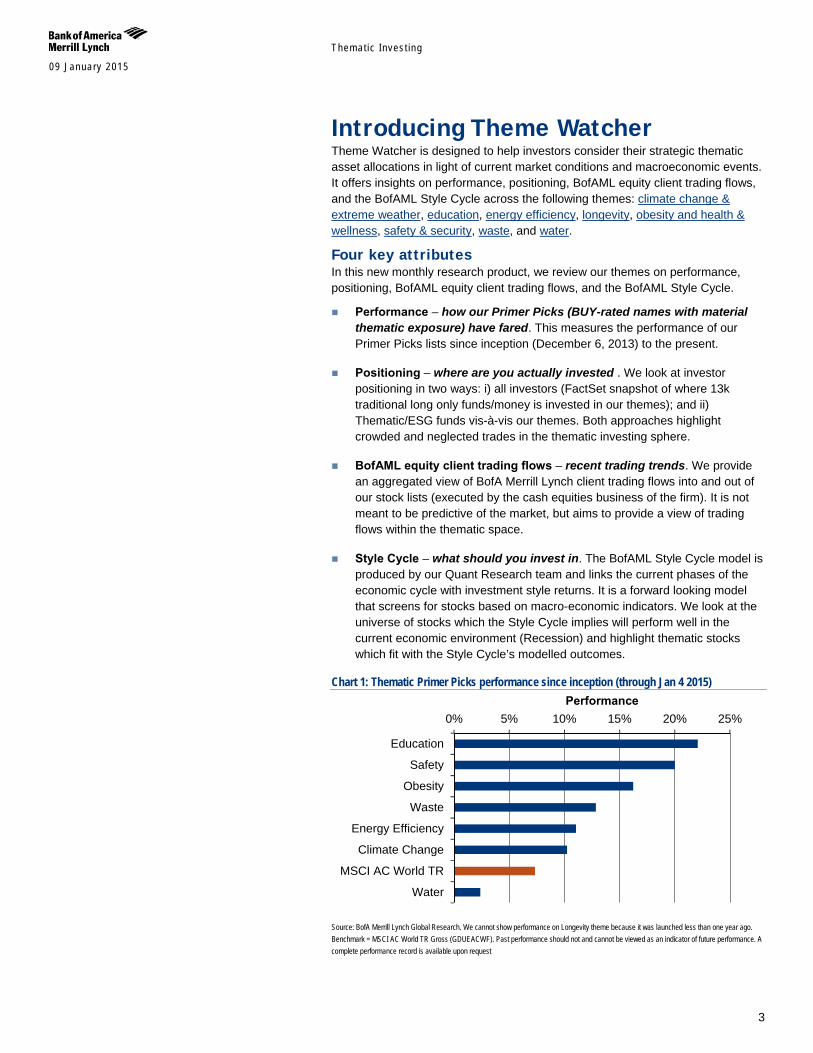

As part of our work on A Transforming World, and as discussed in our 2015 year ahead, we continue to believe that thematic investing should outperform in the brave, new, post-QE world – and that investors should position for lower expected returns from financial markets by concentrating portfolios in assets related to our long-term themes. In this report we introduce Theme Watcher, a new monthly report that is designed to help investors consider their strategic thematic asset allocations in light of current market conditions and macroeconomic events. It offers insights on performance, positioning, BofAML equity client trading flows, and the BofAML Style Cycle across the following themes: climate change & extreme weather, education, energy efficiency, longevity, obesity and health & wellness, safety & security, waste, and water.

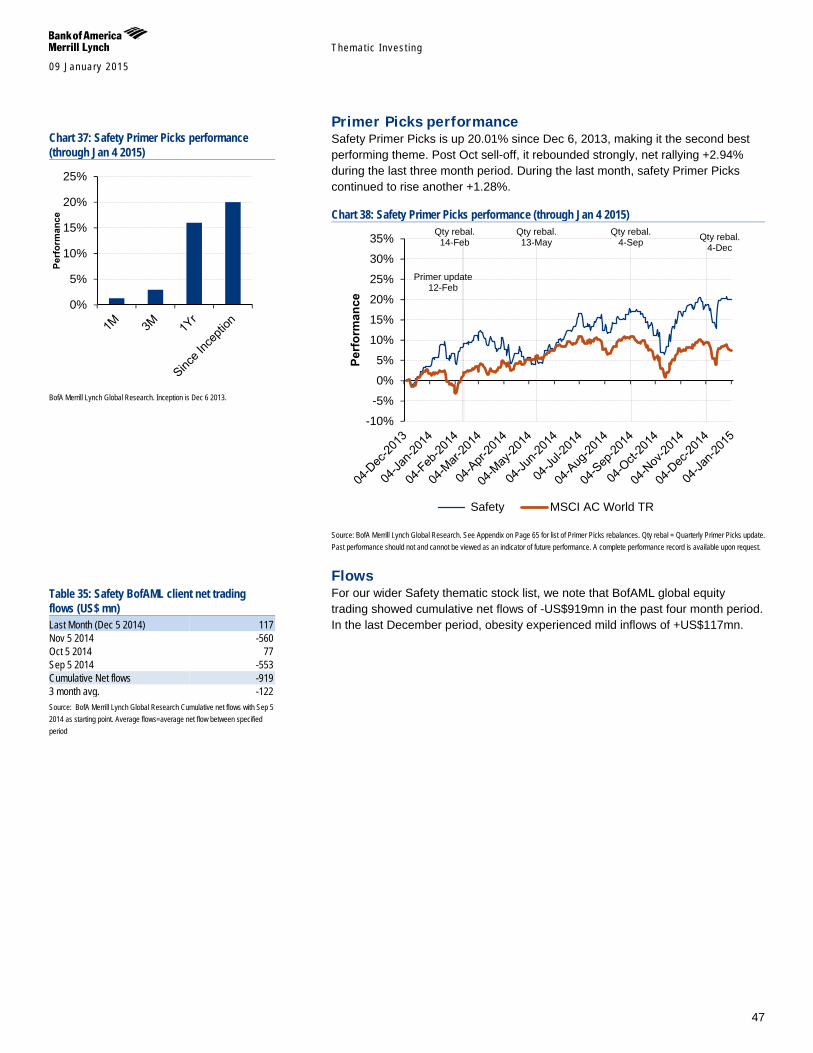

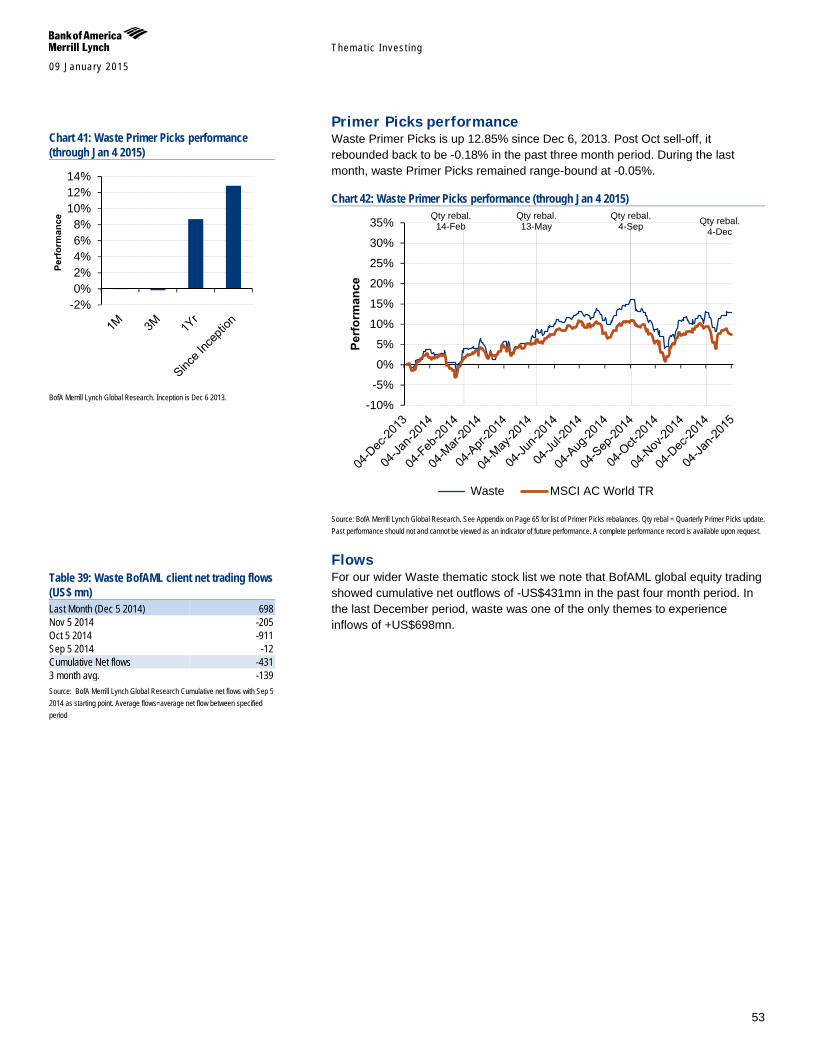

Performance results: education & safety up 20%+ We have measured our thematic Primer Picks (Buy-rated names with material exposure) against the benchmark MSCI AC World since inception on 6 December 2013. Our education and safety & security themes have been the best performers since inception, up 22.1% and 20.0% respectively (vs. +7.3% for MSCI AC World). The Globesity and health & wellness Primer Picks increased +16.2%, Waste +12.9%, Energy efficiency +11.0%, and Climate change +10.2%. Water was the sole underperformer relative to MSCI AC World, up only 2.4%. We have not included our Longevity Primer Picks list as we have <12 months data.

Weightings: investors are overweight energy efficiency & ICT We have analysed publicly disclosed fund holdings globally for 13k+ investment funds and assessed the overweights/underweights across our themes, sub-themes, and stocks. Energy efficiency was the biggest overweight globally, with water the biggest underweight. Specifically, investors are concentrated in ICT-related sub-themes and stocks including ICT, cybersecurity, and edtech. In contrast, the biggest underweights were in engineering & construction-related sub-themes such as water infrastructure and equipment, as well as retail.

Water: the theme most favoured by thematic & ESG investors Our Thematic & ESG Consensus model measures the most favoured stocks and sectors of long-term thematic and ESG (environmental, social, governance) funds. Applying its findings to our themes, the most commonly held theme is water, followed by climate change.

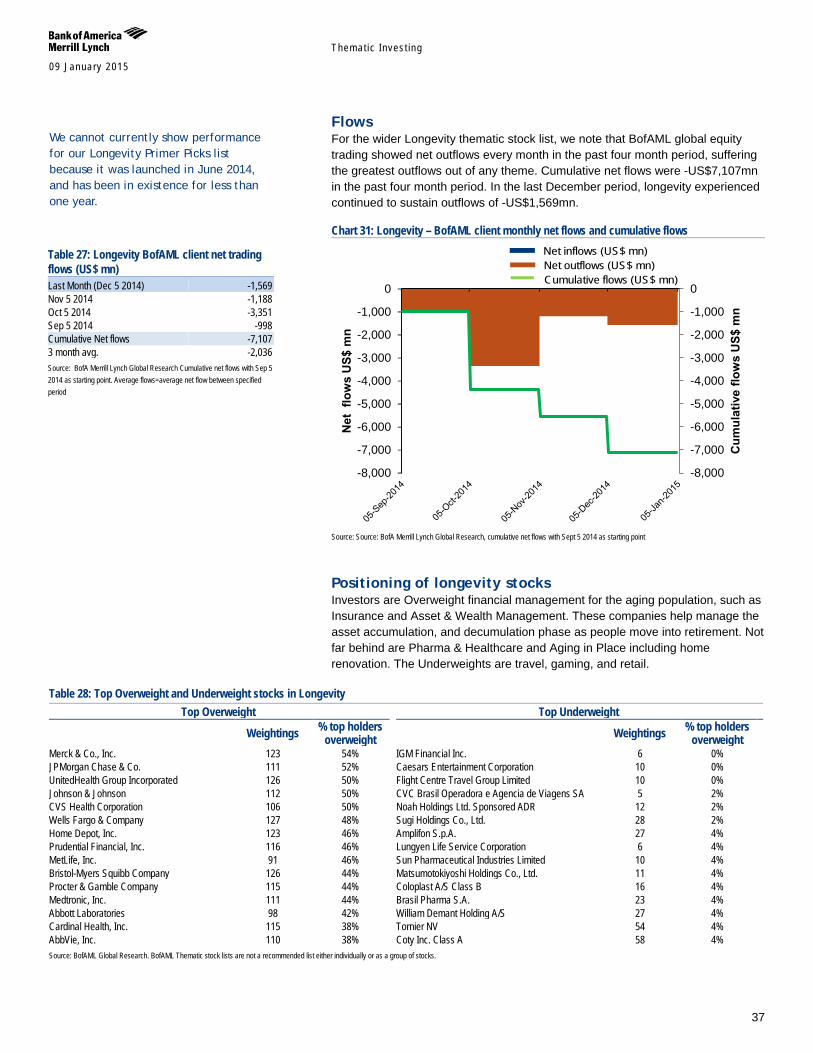

No inflows: longevity & climate change see largest outflows We analysed BofAML equity client flows globally, which showed outflows every month over the last year, totalling -US$17,315mn since 5 September 2014. Longevity had the most significant outflows with -US$7,107mn, followed by climate change with -US$3,274mn. Education, the best performer to date, was the only theme with relatively flat trading flows of -US$23mn.

We prefer obesity over energy efficiency & climate change We have screened our entire thematic universe using our BofAML Style Cycle model. Given current macroeconomic conditions, obesity and health & wellness lists have the highest exposure to stocks that screen attractivly in a ‘Recession’. Conversely, stocks exposed to the energy efficiency and climate change & extreme weather themes screened as unattractive.

2

Themat ic Inves t ing 09 January 2015

Contents Introducing Theme Watcher 3

BofAML Thematic Investing Stock Lists & Primer Picks 4

Performance – how themes fared 5

Style cycle – what should you invest in 8

Ownership – where are you invested 11

How is the market positioned 11

ESG and Thematic positioning 16

Equity Flows – Recent trading 17

Themes 18

Climate change & extreme weather - A perfect storm 18

Education - Stay in school 24

Energy efficiency – Efficient frontier 30

Demographics - Longevity revolution 36

Obesity and health & wellness - Globesity 40

Safety & Security - Safer world 46

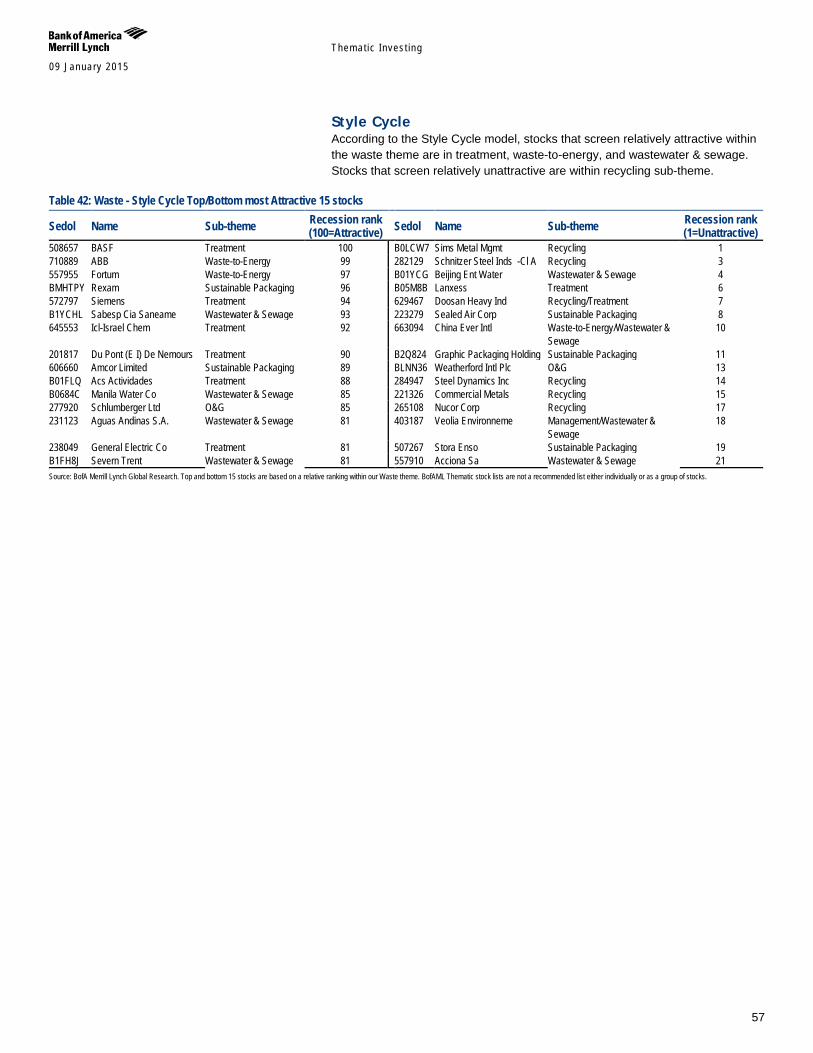

Waste - No time to waste 52

Water - Blue revolution 58

Methodology Appendix 64

Themat ic Inves t ing 09 January 2015

3

Introducing Theme Watcher Theme Watcher is designed to help investors consider their strategic thematic asset allocations in light of current market conditions and macroeconomic events. It offers insights on performance, positioning, BofAML equity client trading flows, and the BofAML Style Cycle across the following themes: climate change & extreme weather, education, energy efficiency, longevity, obesity and health & wellness, safety & security, waste, and water.

Four key attributes In this new monthly research product, we review our themes on performance, positioning, BofAML equity client trading flows, and the BofAML Style Cycle.

Performance – how our Primer Picks (BUY-rated names with material thematic exposure) have fared. This measures the performance of our Primer Picks lists since inception (December 6, 2013) to the present.

Positioning – where are you actually invested . We look at investor positioning in two ways: i) all investors (FactSet snapshot of where 13k traditional long only funds/money is invested in our themes); and ii) Thematic/ESG funds vis-à-vis our themes. Both approaches highlight crowded and neglected trades in the thematic investing sphere.

BofAML equity client trading flows – recent trading trends. We provide an aggregated view of BofA Merrill Lynch client trading flows into and out of our stock lists (executed by the cash equities business of the firm). It is not meant to be predictive of the market, but aims to provide a view of trading flows within the thematic space.

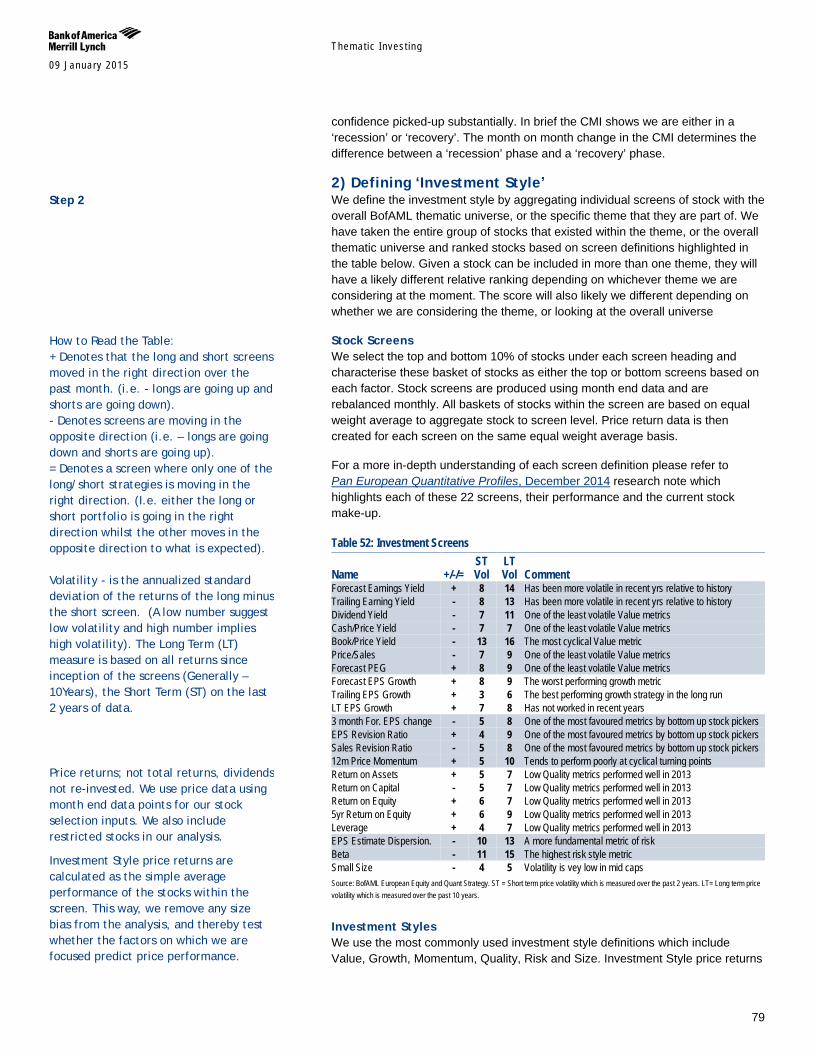

Style Cycle – what should you invest in. The BofAML Style Cycle model is produced by our Quant Research team and links the current phases of the economic cycle with investment style returns. It is a forward looking model that screens for stocks based on macro-economic indicators. We look at the universe of stocks which the Style Cycle implies will perform well in the current economic environment (Recession) and highlight thematic stocks which fit with the Style Cycle’s modelled outcomes.

Chart 1: Thematic Primer Picks performance since inception (through Jan 4 2015)

Source: BofA Merrill Lynch Global Research. We cannot show performance on Longevity theme because it was launched less than one year ago. Benchmark = MSCI AC World TR Gross (GDUEACWF). Past performance should not and cannot be viewed as an indicator of future performance. A complete performance record is available upon request

0% 5% 10% 15% 20% 25%

Education

Safety

Obesity

Waste

Energy Efficiency

Climate Change

MSCI AC World TR

Water

Performance

Themat ic Inves t ing 09 January 2015

4

BofAML Thematic Investing Stock Lists & Primer Picks Since December 5 2013, we have been publishing a number of BofA Merrill Lynch Global Research lists of stocks and “Primer Picks” which have exposure to 8 equity themes – Climate Change & Extreme Weather, Education, Energy Efficiency, Longevity, Obesity and Health and Wellness, Safety & Security, Waste, and Water. Our strategic view has been longer term and the names we have selected in each of these thematic stock lists are those which we believe should benefit in the long run from the theme. The aim of our stock lists has been to provide investors with information to understand company and sub-theme opportunities and risks inherent in the themes.

For each theme since the inception of each specific list, we have mapped a number of sector value chains to highlight various entry points or “sub-themes” within the theme. For each entry point, we have mapped opportunities and risks as we understand them to highlight a diverse range of entry points for investors wishing to invest in the theme. We have estimated the level and materiality of companies’ exposure to the energy efficiency themes, and the role of the themes as long-term drivers. We have characterised each company’s exposure as follows:

Low – Theme-related products, technologies, services, and solutions are not material to global revenues and/or growth but are one factor, among others, for the business model, strategy and R&D of the company.

Medium – Theme -related products, technologies, services, and solutions are an important factor for the business model, strategy and R&D of the company; material to sales and/or growth.

High – Theme-related products, technologies, services, and solutions are core to the business model, strategy and R&D of the company; material sales and/or growth driver; pure play (i.e., 100% of sales).

Since the inception of our Thematic Investing Stock Lists, each quarter we have published: (i) a broader list mapping out the full universe of stocks exposed to a theme based on our Low/Medium/High methodology and (ii) a separate list of “Primer Picks” which are those stocks which have both a Buy rating from our fundamental equity team and that have Medium to High exposure to the theme under our methodology. Although it is difficult to accurately gauge the link between such exposure and share price performance (as many factors outside the scope of this analysis are likely to play a role in short- and long-term price development), we still consider its thematic exposure as an important and positive point to track given that they are “A Transforming World” themes with a 25Y+ lifespan.

A company can be in more than one theme stock list, sub-theme, or Primer Picks.

Investors should consider the fundamentals of the companies and their own individual circumstances / objectives before making any investment decisions. The full rationale and investment thesis for our fundamental analyst’s recommendations on each stock is contained in the most recent report on the company, which we urge you to read.

Thematic stock lists are not a recommended list either individually or as a group of stocks.

Themat ic Inves t ing 09 January 2015

5

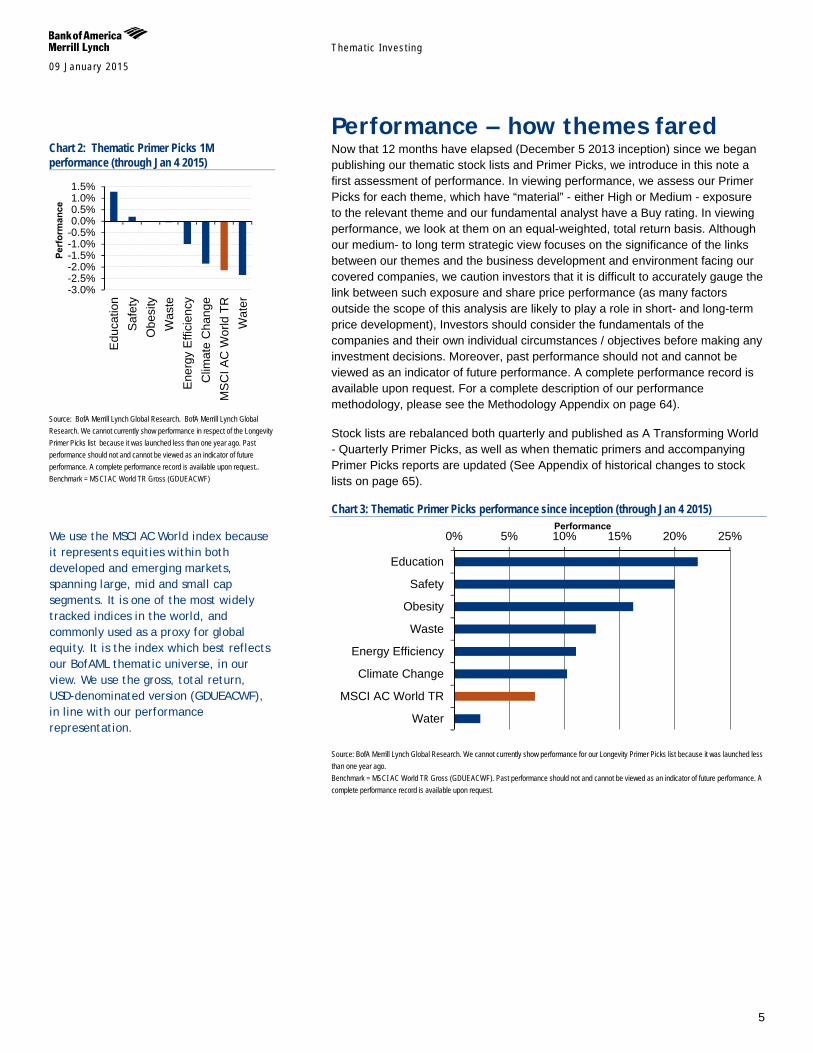

Performance – how themes fared Now that 12 months have elapsed (December 5 2013 inception) since we began publishing our thematic stock lists and Primer Picks, we introduce in this note a first assessment of performance. In viewing performance, we assess our Primer Picks for each theme, which have “material” - either High or Medium - exposure to the relevant theme and our fundamental analyst have a Buy rating. In viewing performance, we look at them on an equal-weighted, total return basis. Although our medium- to long term strategic view focuses on the significance of the links between our themes and the business development and environment facing our covered companies, we caution investors that it is difficult to accurately gauge the link between such exposure and share price performance (as many factors outside the scope of this analysis are likely to play a role in short- and long-term price development), Investors should consider the fundamentals of the companies and their own individual circumstances / objectives before making any investment decisions. Moreover, past performance should not and cannot be viewed as an indicator of future performance. A complete performance record is available upon request. For a complete description of our performance methodology, please see the Methodology Appendix on page 64).

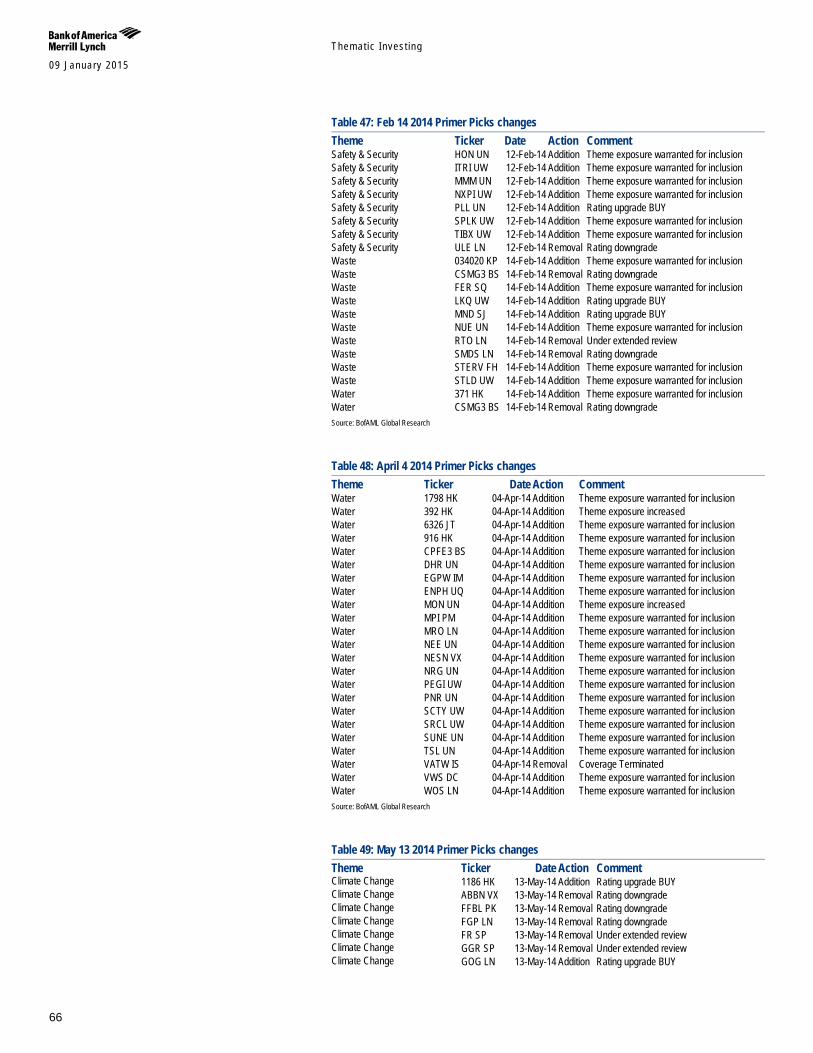

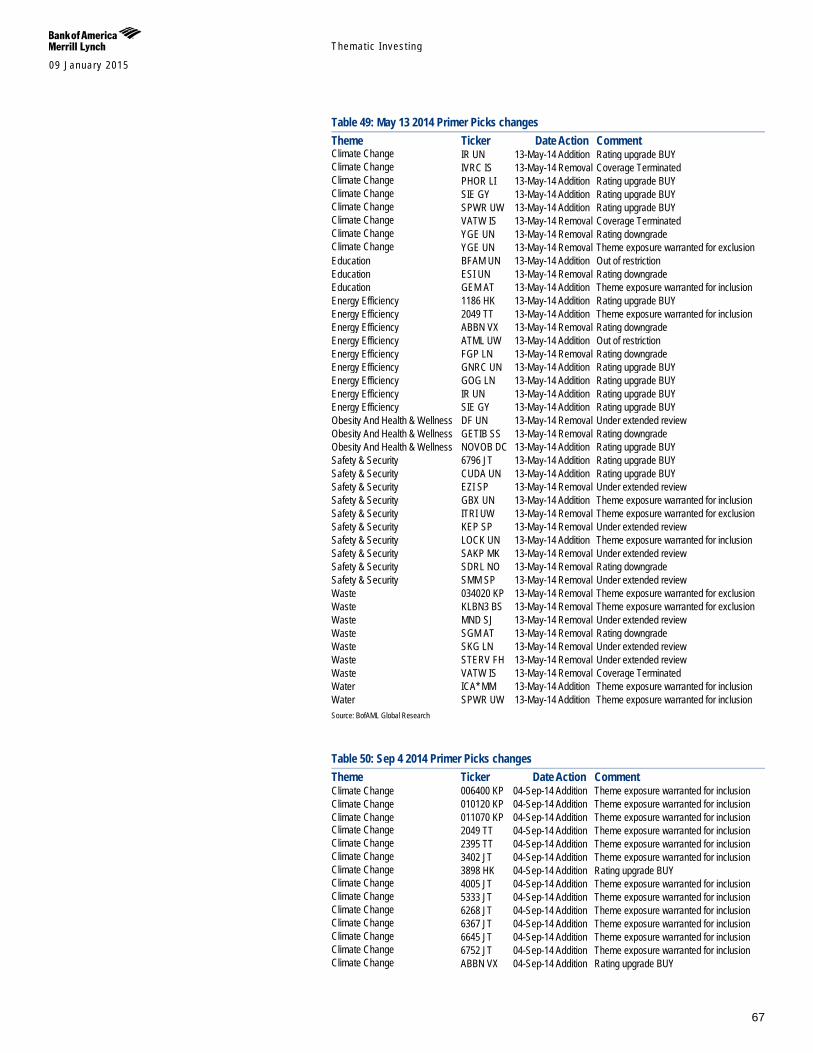

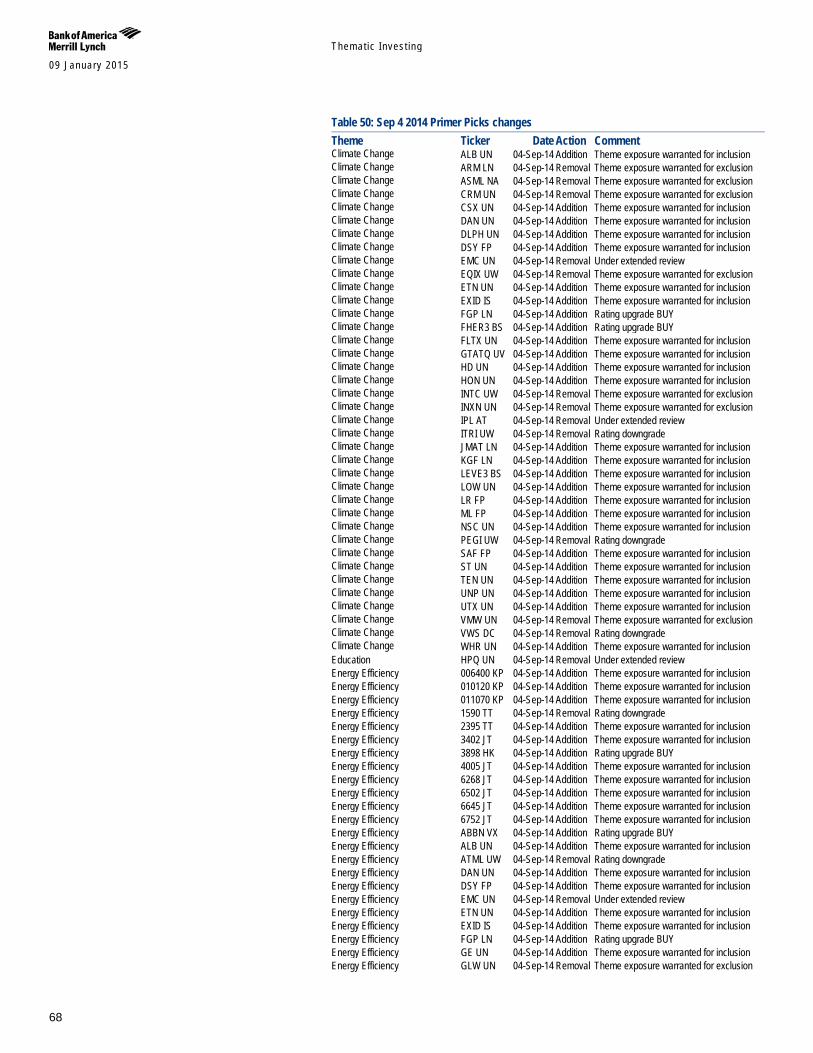

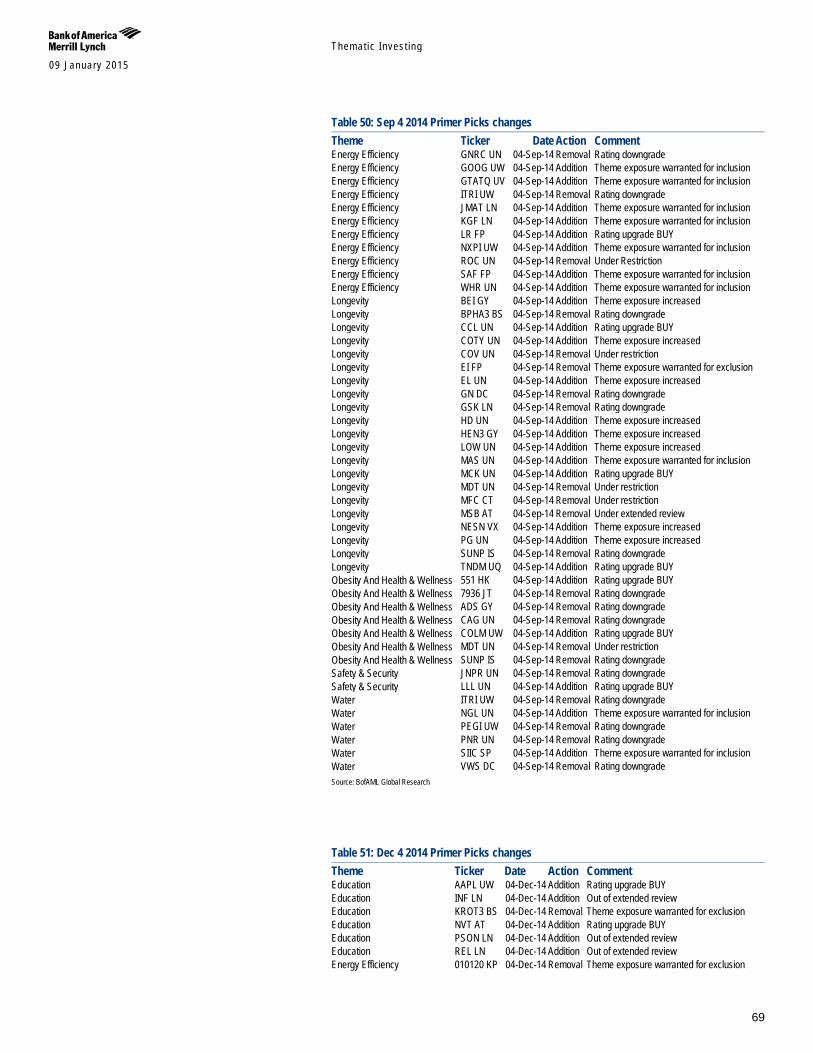

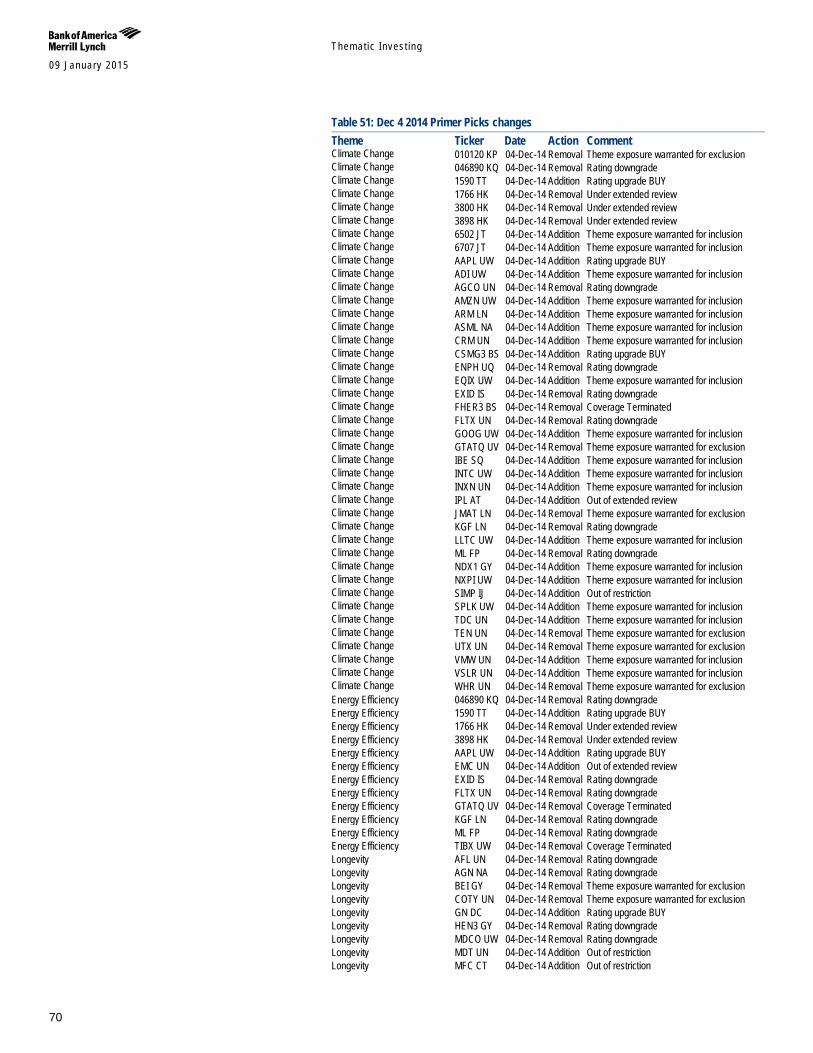

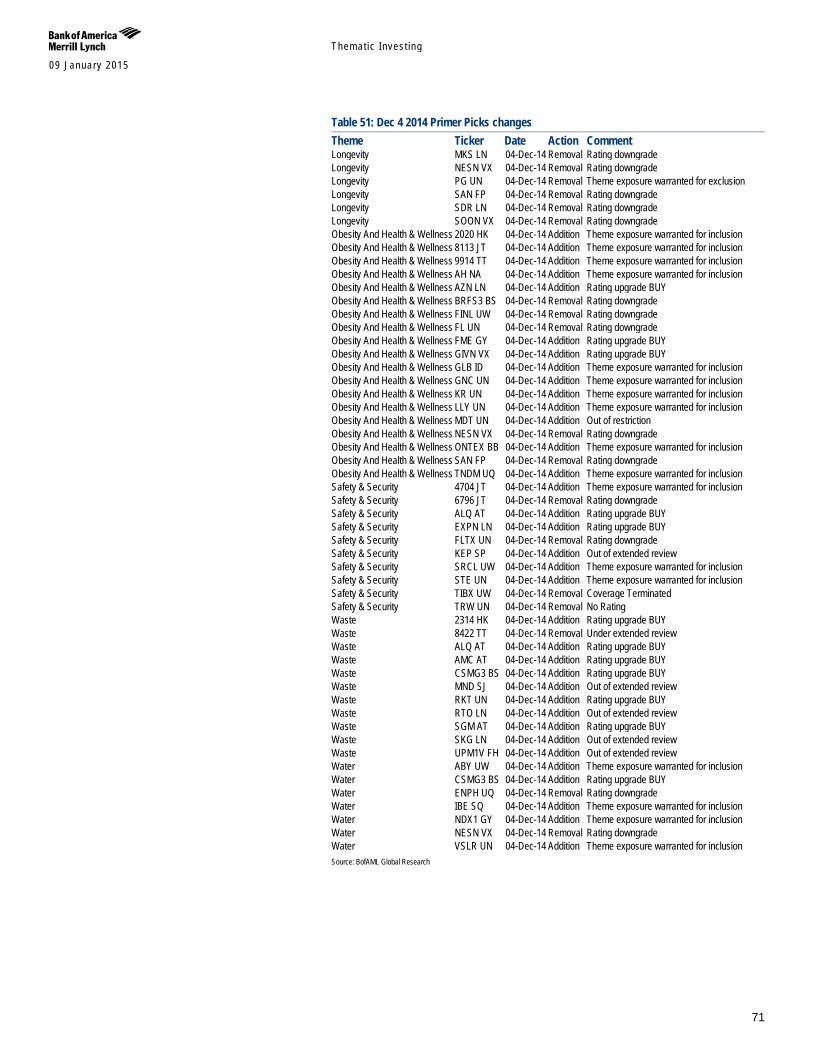

Stock lists are rebalanced both quarterly and published as A Transforming World - Quarterly Primer Picks, as well as when thematic primers and accompanying Primer Picks reports are updated (See Appendix of historical changes to stock lists on page 65).

Chart 3: Thematic Primer Picks performance since inception (through Jan 4 2015)

Source: BofA Merrill Lynch Global Research. We cannot currently show performance for our Longevity Primer Picks list because it was launched less than one year ago. Benchmark = MSCI AC World TR Gross (GDUEACWF). Past performance should not and cannot be viewed as an indicator of future performance. A complete performance record is available upon request.

0% 5% 10% 15% 20% 25%

Education

Safety

Obesity

Waste

Energy Efficiency

Climate Change

MSCI AC World TR

Water

Performance

Chart 2: Thematic Primer Picks 1M performance (through Jan 4 2015)

Source: BofA Merrill Lynch Global Research. BofA Merrill Lynch Global Research. We cannot currently show performance in respect of the Longevity Primer Picks list because it was launched less than one year ago. Past performance should not and cannot be viewed as an indicator of future performance. A complete performance record is available upon request.. Benchmark = MSCI AC World TR Gross (GDUEACWF)

-3.0%-2.5%-2.0%-1.5%-1.0%-0.5%0.0%0.5%1.0%1.5%

Edu

catio

n S

afet

y O

besi

ty W

aste

Ene

rgy

Effi

cien

cyC

limat

e C

hang

eM

SC

I AC

Wor

ld T

R W

ater

Perf

orm

ance

We use the MSCI AC World index because it represents equities within both developed and emerging markets, spanning large, mid and small cap segments. It is one of the most widely tracked indices in the world, and commonly used as a proxy for global equity. It is the index which best reflects our BofAML thematic universe, in our view. We use the gross, total return, USD-denominated version (GDUEACWF), in line with our performance representation.

Themat ic Inves t ing 09 January 2015

6

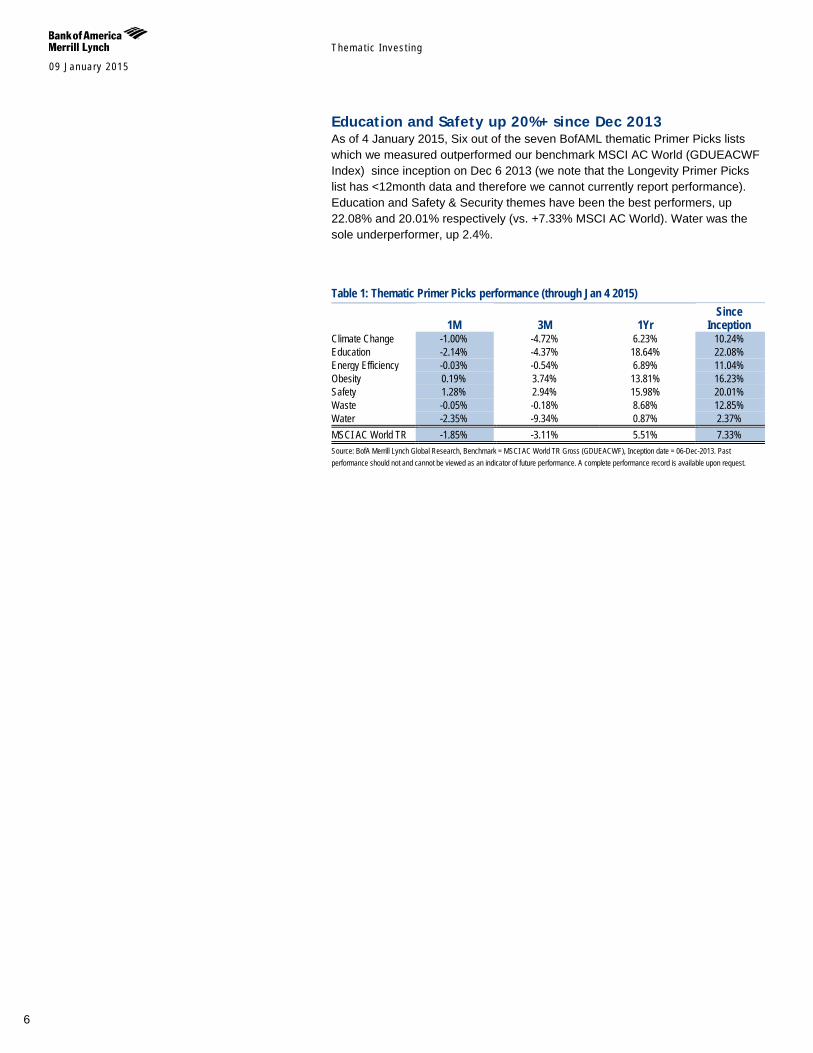

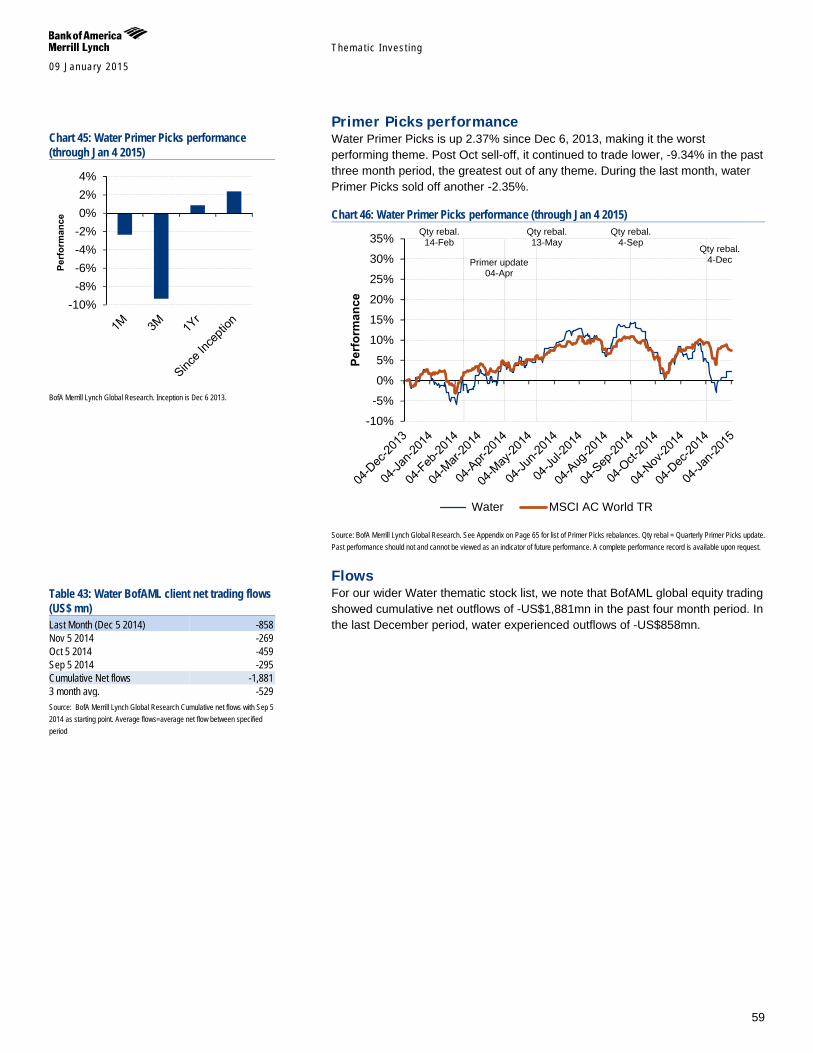

Education and Safety up 20%+ since Dec 2013 As of 4 January 2015, Six out of the seven BofAML thematic Primer Picks lists which we measured outperformed our benchmark MSCI AC World (GDUEACWF Index) since inception on Dec 6 2013 (we note that the Longevity Primer Picks list has <12month data and therefore we cannot currently report performance). Education and Safety & Security themes have been the best performers, up 22.08% and 20.01% respectively (vs. +7.33% MSCI AC World). Water was the sole underperformer, up 2.4%.

Table 1: Thematic Primer Picks performance (through Jan 4 2015)

1M 3M 1Yr Since

Inception Climate Change -1.00% -4.72% 6.23% 10.24% Education -2.14% -4.37% 18.64% 22.08% Energy Efficiency -0.03% -0.54% 6.89% 11.04% Obesity 0.19% 3.74% 13.81% 16.23% Safety 1.28% 2.94% 15.98% 20.01% Waste -0.05% -0.18% 8.68% 12.85% Water -2.35% -9.34% 0.87% 2.37% MSCI AC World TR -1.85% -3.11% 5.51% 7.33% Source: BofA Merrill Lynch Global Research, Benchmark = MSCI AC World TR Gross (GDUEACWF), Inception date = 06-Dec-2013. Past performance should not and cannot be viewed as an indicator of future performance. A complete performance record is available upon request.

09 January 2015

Them

atic Investing

7

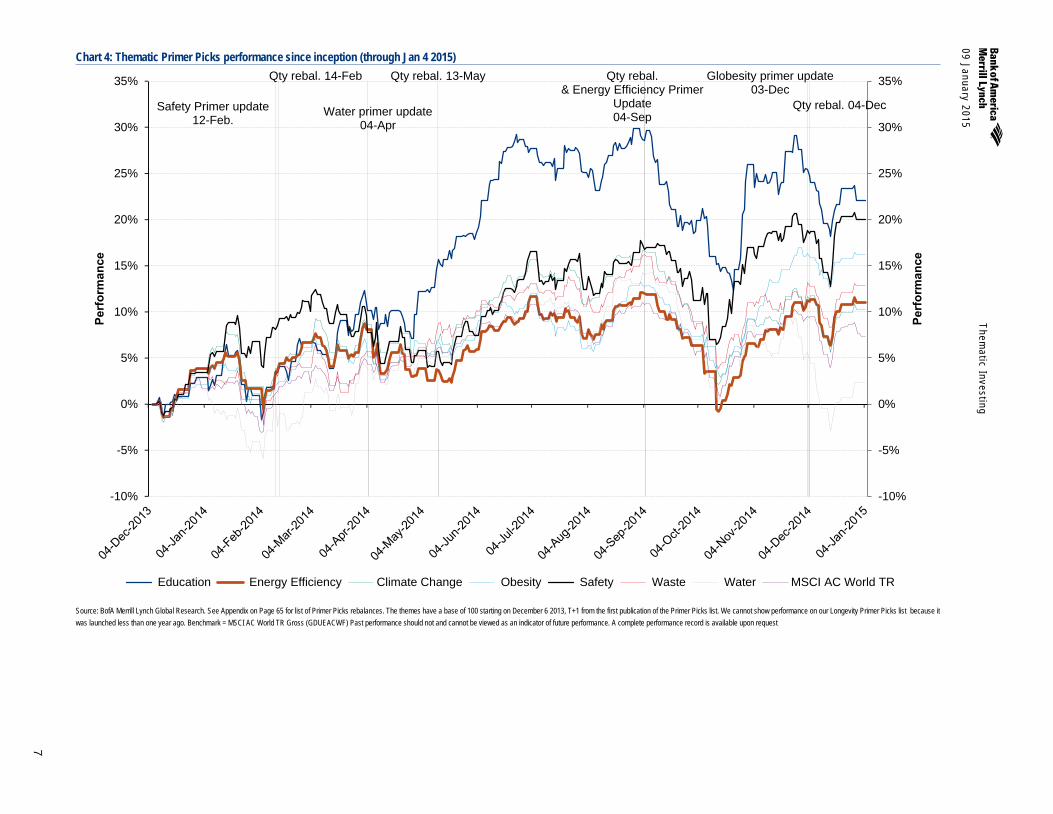

Chart 4: Thematic Primer Picks performance since inception (through Jan 4 2015)

Source: BofA Merrill Lynch Global Research. See Appendix on Page 65 for list of Primer Picks rebalances. The themes have a base of 100 starting on December 6 2013, T+1 from the first publication of the Primer Picks list. We cannot show performance on our Longevity Primer Picks list because it was launched less than one year ago. Benchmark = MSCI AC World TR Gross (GDUEACWF) Past performance should not and cannot be viewed as an indicator of future performance. A complete performance record is available upon request

Qty rebal. 14-Feb

Safety Primer update 12-Feb.

Water primer update 04-Apr

Qty rebal. 13-May Qty rebal. & Energy Efficiency Primer

Update 04-Sep

Globesity primer update 03-Dec

Qty rebal. 04-Dec

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

Perf

orm

ance

Perf

orm

ance

Education Energy Efficiency Climate Change Obesity Safety Waste Water MSCI AC World TR

Themat ic Inves t ing 09 January 2015

8

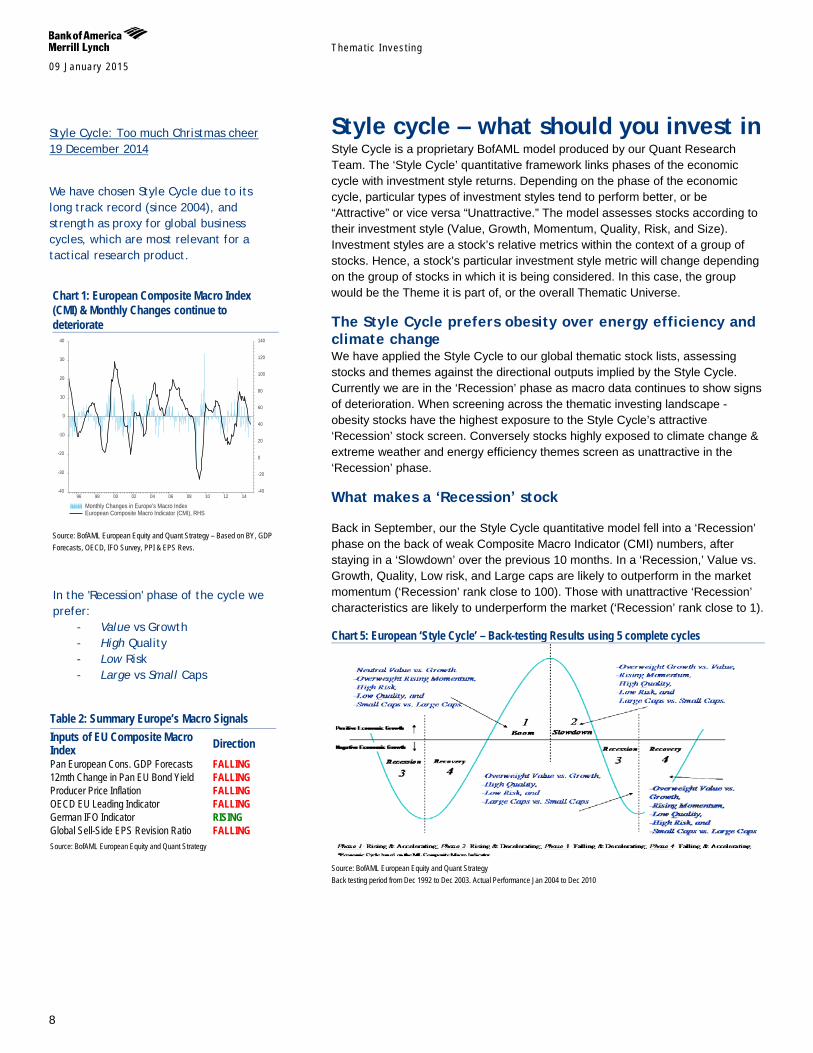

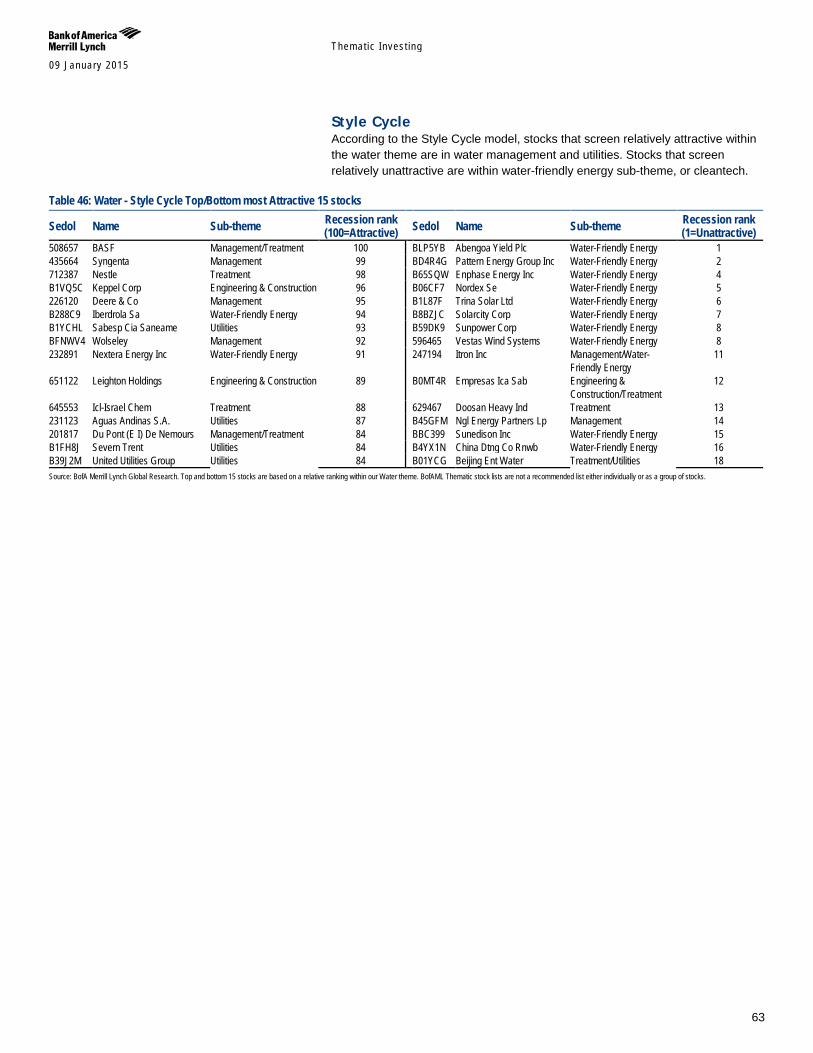

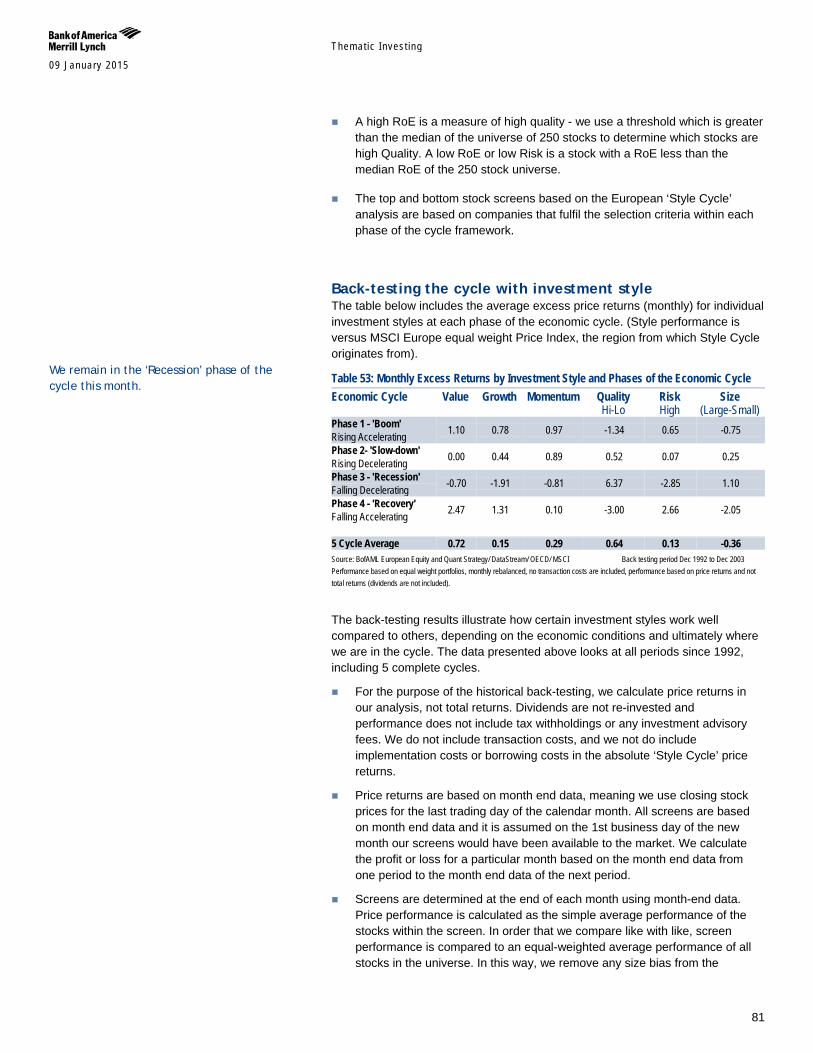

Style cycle – what should you invest in Style Cycle is a proprietary BofAML model produced by our Quant Research Team. The ‘Style Cycle’ quantitative framework links phases of the economic cycle with investment style returns. Depending on the phase of the economic cycle, particular types of investment styles tend to perform better, or be “Attractive” or vice versa “Unattractive.” The model assesses stocks according to their investment style (Value, Growth, Momentum, Quality, Risk, and Size). Investment styles are a stock’s relative metrics within the context of a group of stocks. Hence, a stock’s particular investment style metric will change depending on the group of stocks in which it is being considered. In this case, the group would be the Theme it is part of, or the overall Thematic Universe.

The Style Cycle prefers obesity over energy efficiency and climate change We have applied the Style Cycle to our global thematic stock lists, assessing stocks and themes against the directional outputs implied by the Style Cycle. Currently we are in the ‘Recession’ phase as macro data continues to show signs of deterioration. When screening across the thematic investing landscape - obesity stocks have the highest exposure to the Style Cycle’s attractive ‘Recession’ stock screen. Conversely stocks highly exposed to climate change & extreme weather and energy efficiency themes screen as unattractive in the ‘Recession’ phase.

What makes a ‘Recession’ stock Back in September, our the Style Cycle quantitative model fell into a ‘Recession’ phase on the back of weak Composite Macro Indicator (CMI) numbers, after staying in a ‘Slowdown’ over the previous 10 months. In a ‘Recession,’ Value vs. Growth, Quality, Low risk, and Large caps are likely to outperform in the market momentum (‘Recession’ rank close to 100). Those with unattractive ‘Recession’ characteristics are likely to underperform the market (‘Recession’ rank close to 1).

Chart 5: European ‘Style Cycle’ – Back-testing Results using 5 complete cycles

Source: BofAML European Equity and Quant Strategy Back testing period from Dec 1992 to Dec 2003. Actual Performance Jan 2004 to Dec 2010

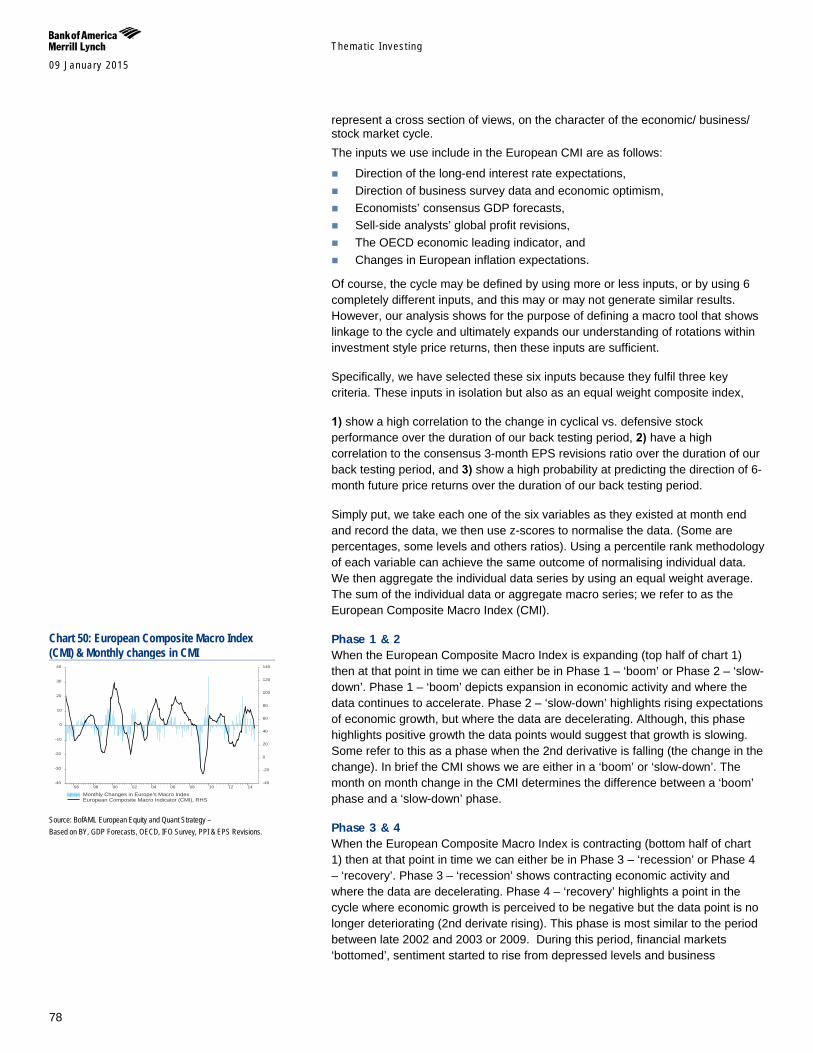

Chart 1: European Composite Macro Index (CMI) & Monthly Changes continue to deteriorate

Source: BofAML European Equity and Quant Strategy – Based on BY, GDP Forecasts, OECD, IFO Survey, PPI & EPS Revs.

Table 2: Summary Europe’s Macro Signals Inputs of EU Composite Macro Index Direction Pan European Cons. GDP Forecasts FALLING 12mth Change in Pan EU Bond Yield FALLING Producer Price Inflation FALLING OECD EU Leading Indicator FALLING German IFO Indicator RISING Global Sell-Side EPS Revision Ratio FALLING Source: BofAML European Equity and Quant Strategy

Source: Thomson Reuters Datastream

96 98 00 02 04 06 08 10 12 14-40

-30

-20

-10

0

10

20

30

40

-40

-20

0

20

40

60

80

100

120

140

Monthly Changes in Europe's Macro IndexEuropean Composite Macro Indicator (CMI), RHS

In the 'Recession' phase of the cycle we prefer:

- Value vs Growth - High Quality - Low Risk - Large vs Small Caps

Style Cycle: Too much Christmas cheer 19 December 2014

We have chosen Style Cycle due to its long track record (since 2004), and strength as proxy for global business cycles, which are most relevant for a tactical research product.

Themat ic Inves t ing 09 January 2015

9

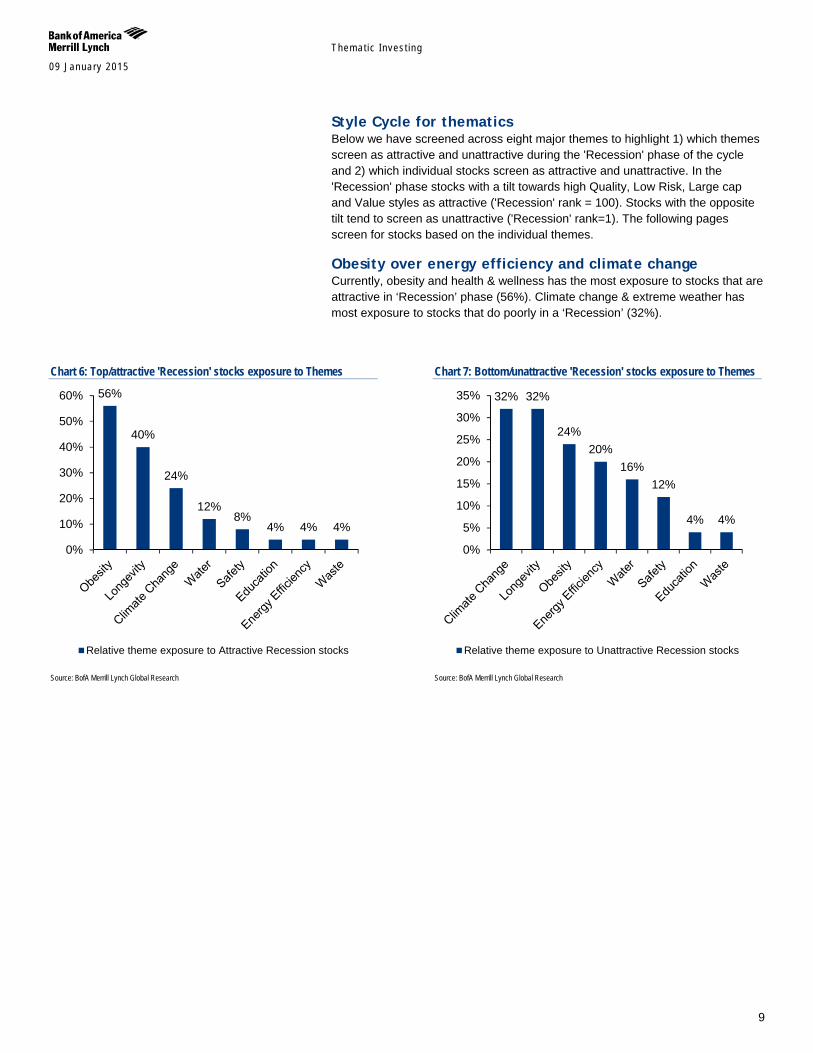

Style Cycle for thematics Below we have screened across eight major themes to highlight 1) which themes screen as attractive and unattractive during the 'Recession' phase of the cycle and 2) which individual stocks screen as attractive and unattractive. In the 'Recession' phase stocks with a tilt towards high Quality, Low Risk, Large cap and Value styles as attractive ('Recession' rank = 100). Stocks with the opposite tilt tend to screen as unattractive ('Recession' rank=1). The following pages screen for stocks based on the individual themes.

Obesity over energy efficiency and climate change Currently, obesity and health & wellness has the most exposure to stocks that are attractive in ‘Recession’ phase (56%). Climate change & extreme weather has most exposure to stocks that do poorly in a ‘Recession’ (32%).

Chart 6: Top/attractive 'Recession' stocks exposure to Themes

Source: BofA Merrill Lynch Global Research

Chart 7: Bottom/unattractive 'Recession' stocks exposure to Themes

Source: BofA Merrill Lynch Global Research

56%

40%

24%

12% 8%

4% 4% 4%

0%

10%

20%

30%

40%

50%

60%

Relative theme exposure to Attractive Recession stocks

32% 32%

24% 20%

16% 12%

4% 4%

0%

5%

10%

15%

20%

25%

30%

35%

Relative theme exposure to Unattractive Recession stocks

Themat ic Inves t ing 09 January 2015

10

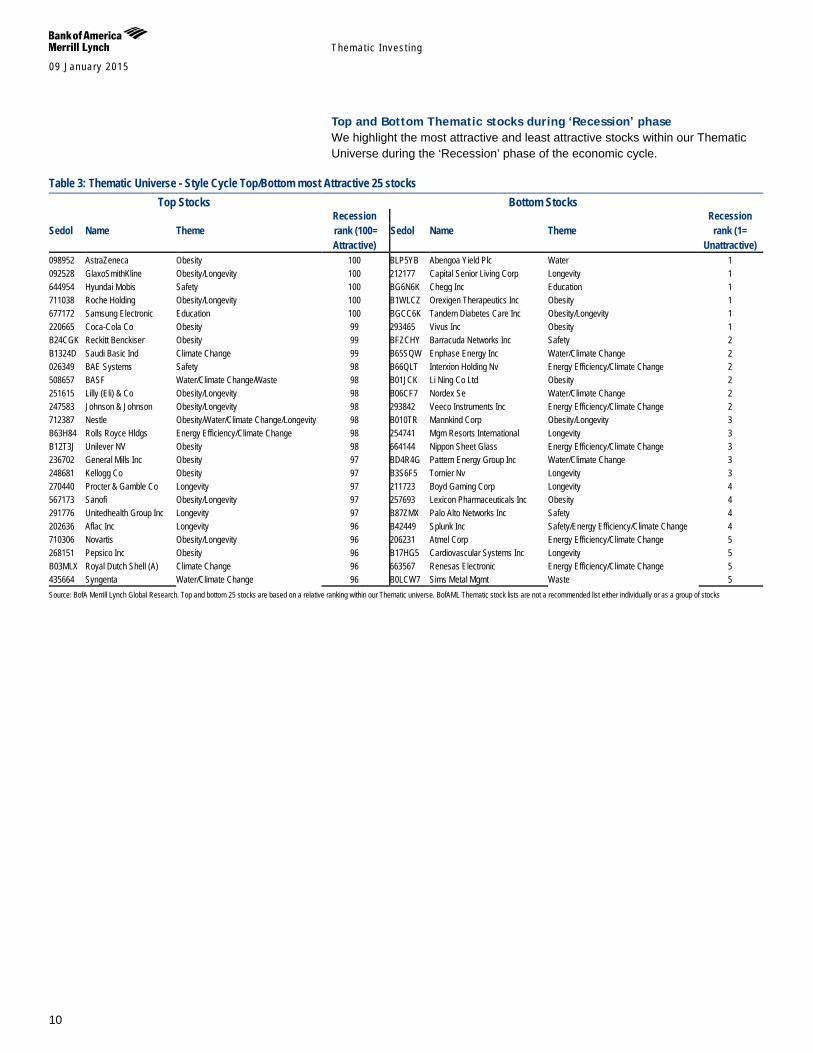

Top and Bottom Thematic stocks during ‘Recession’ phase We highlight the most attractive and least attractive stocks within our Thematic Universe during the ‘Recession’ phase of the economic cycle.

Table 3: Thematic Universe - Style Cycle Top/Bottom most Attractive 25 stocks Top Stocks Bottom Stocks

Sedol Name Theme Recession

Sedol Name Theme Recession

rank (100= rank (1= Attractive) Unattractive)

098952 AstraZeneca Obesity 100 BLP5YB Abengoa Yield Plc Water 1 092528 GlaxoSmithKline Obesity/Longevity 100 212177 Capital Senior Living Corp Longevity 1 644954 Hyundai Mobis Safety 100 BG6N6K Chegg Inc Education 1 711038 Roche Holding Obesity/Longevity 100 B1WLCZ Orexigen Therapeutics Inc Obesity 1 677172 Samsung Electronic Education 100 BGCC6K Tandem Diabetes Care Inc Obesity/Longevity 1 220665 Coca-Cola Co Obesity 99 293465 Vivus Inc Obesity 1 B24CGK Reckitt Benckiser Obesity 99 BFZCHY Barracuda Networks Inc Safety 2 B1324D Saudi Basic Ind Climate Change 99 B65SQW Enphase Energy Inc Water/Climate Change 2 026349 BAE Systems Safety 98 B66QLT Interxion Holding Nv Energy Efficiency/Climate Change 2 508657 BASF Water/Climate Change/Waste 98 B01JCK Li Ning Co Ltd Obesity 2 251615 Lilly (Eli) & Co Obesity/Longevity 98 B06CF7 Nordex Se Water/Climate Change 2 247583 Johnson & Johnson Obesity/Longevity 98 293842 Veeco Instruments Inc Energy Efficiency/Climate Change 2 712387 Nestle Obesity/Water/Climate Change/Longevity 98 B010TR Mannkind Corp Obesity/Longevity 3 B63H84 Rolls Royce Hldgs Energy Efficiency/Climate Change 98 254741 Mgm Resorts International Longevity 3 B12T3J Unilever NV Obesity 98 664144 Nippon Sheet Glass Energy Efficiency/Climate Change 3 236702 General Mills Inc Obesity 97 BD4R4G Pattern Energy Group Inc Water/Climate Change 3 248681 Kellogg Co Obesity 97 B3S6F5 Tornier Nv Longevity 3 270440 Procter & Gamble Co Longevity 97 211723 Boyd Gaming Corp Longevity 4 567173 Sanofi Obesity/Longevity 97 257693 Lexicon Pharmaceuticals Inc Obesity 4 291776 Unitedhealth Group Inc Longevity 97 B87ZMX Palo Alto Networks Inc Safety 4 202636 Aflac Inc Longevity 96 B42449 Splunk Inc Safety/Energy Efficiency/Climate Change 4 710306 Novartis Obesity/Longevity 96 206231 Atmel Corp Energy Efficiency/Climate Change 5 268151 Pepsico Inc Obesity 96 B17HG5 Cardiovascular Systems Inc Longevity 5 B03MLX Royal Dutch Shell (A) Climate Change 96 663567 Renesas Electronic Energy Efficiency/Climate Change 5 435664 Syngenta Water/Climate Change 96 B0LCW7 Sims Metal Mgmt Waste 5 Source: BofA Merrill Lynch Global Research. Top and bottom 25 stocks are based on a relative ranking within our Thematic universe. BofAML Thematic stock lists are not a recommended list either individually or as a group of stocks

Themat ic Inves t ing 09 January 2015

11

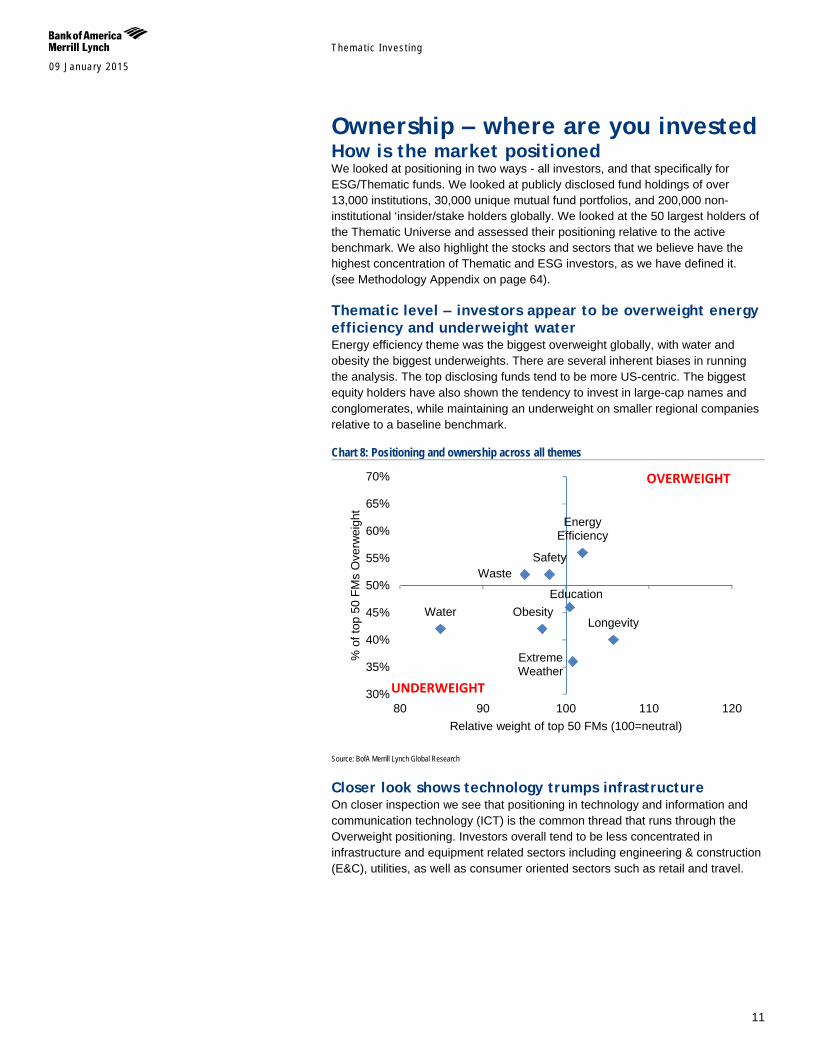

Ownership – where are you invested How is the market positioned We looked at positioning in two ways - all investors, and that specifically for ESG/Thematic funds. We looked at publicly disclosed fund holdings of over 13,000 institutions, 30,000 unique mutual fund portfolios, and 200,000 non-institutional ‘insider/stake holders globally. We looked at the 50 largest holders of the Thematic Universe and assessed their positioning relative to the active benchmark. We also highlight the stocks and sectors that we believe have the highest concentration of Thematic and ESG investors, as we have defined it. (see Methodology Appendix on page 64).

Thematic level – investors appear to be overweight energy efficiency and underweight water Energy efficiency theme was the biggest overweight globally, with water and obesity the biggest underweights. There are several inherent biases in running the analysis. The top disclosing funds tend to be more US-centric. The biggest equity holders have also shown the tendency to invest in large-cap names and conglomerates, while maintaining an underweight on smaller regional companies relative to a baseline benchmark.

Chart 8: Positioning and ownership across all themes

Source: BofA Merrill Lynch Global Research

Closer look shows technology trumps infrastructure On closer inspection we see that positioning in technology and information and communication technology (ICT) is the common thread that runs through the Overweight positioning. Investors overall tend to be less concentrated in infrastructure and equipment related sectors including engineering & construction (E&C), utilities, as well as consumer oriented sectors such as retail and travel.

Water

Waste

Longevity

Extreme Weather

Safety

Energy Efficiency

Education Obesity

30%

35%

40%

45%

50%

55%

60%

65%

70%

80 90 100 110 120

% o

f top

50

FMs

Ove

rwei

ght

Relative weight of top 50 FMs (100=neutral)

UNDERWEIGHT

OVERWEIGHT

Themat ic Inves t ing 09 January 2015

12

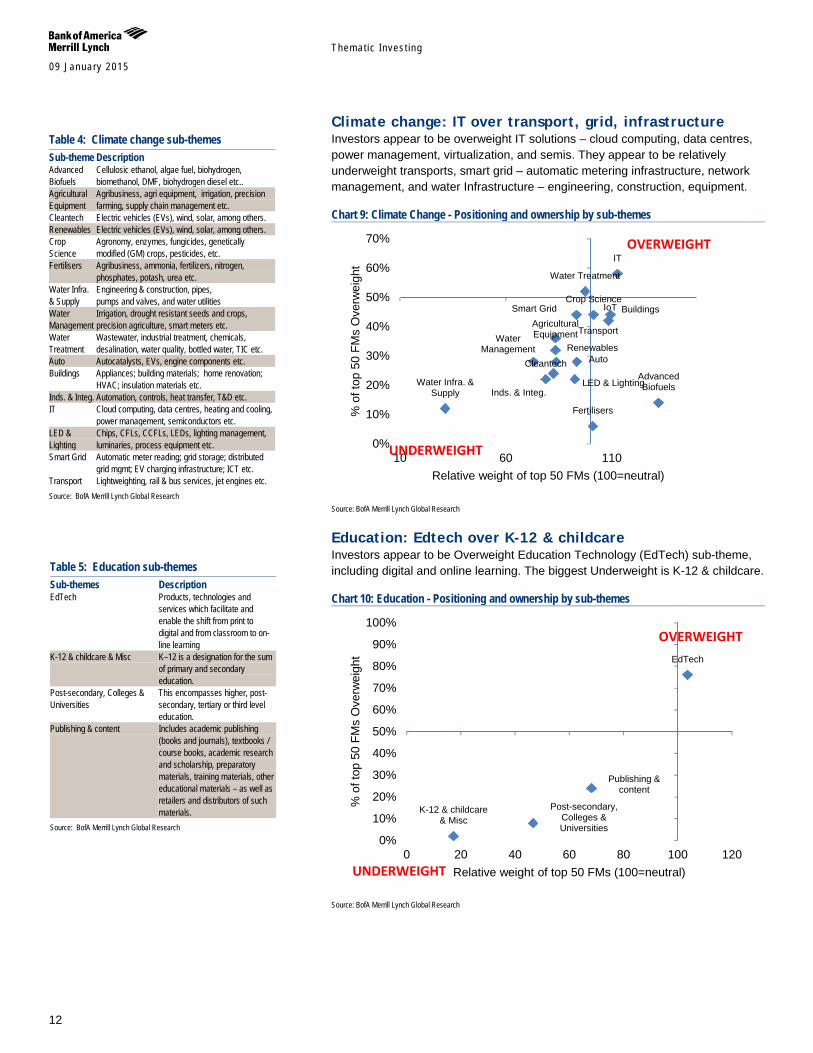

Climate change: IT over transport, grid, infrastructure Investors appear to be overweight IT solutions – cloud computing, data centres, power management, virtualization, and semis. They appear to be relatively underweight transports, smart grid – automatic metering infrastructure, network management, and water Infrastructure – engineering, construction, equipment.

Chart 9: Climate Change - Positioning and ownership by sub-themes

Source: BofA Merrill Lynch Global Research

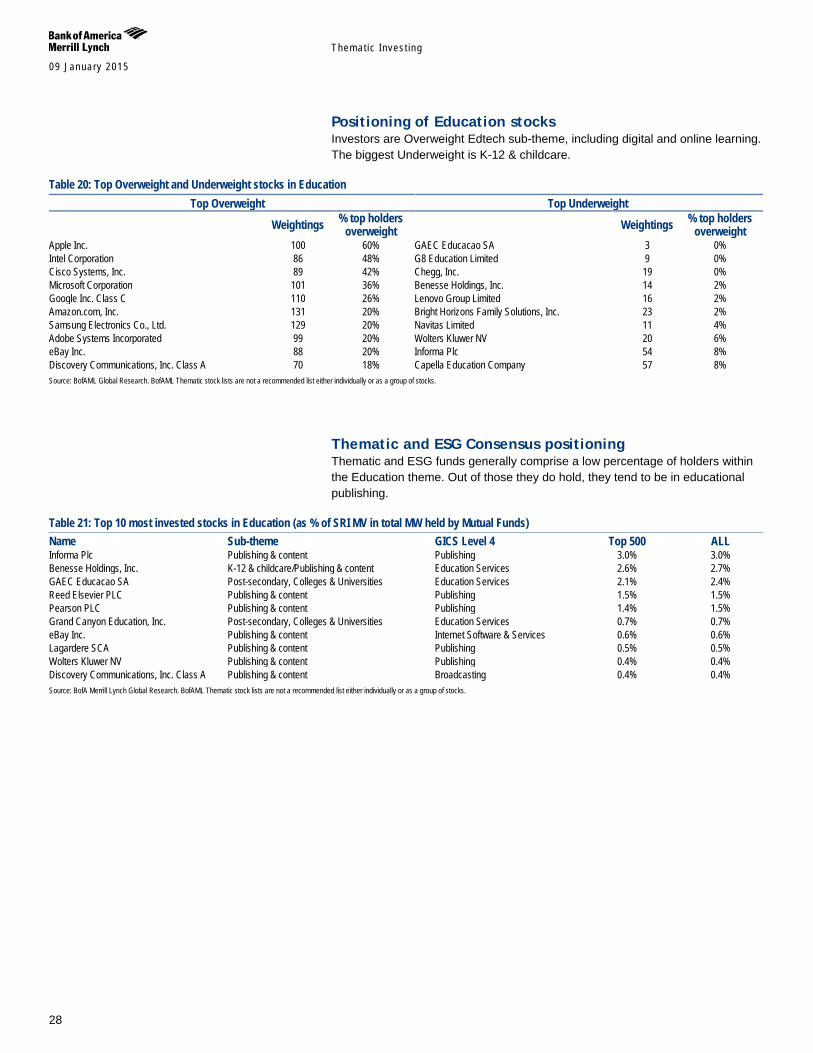

Education: Edtech over K-12 & childcare Investors appear to be Overweight Education Technology (EdTech) sub-theme, including digital and online learning. The biggest Underweight is K-12 & childcare.

Chart 10: Education - Positioning and ownership by sub-themes

Source: BofA Merrill Lynch Global Research

Advanced Biofuels

Agricultural Equipment

Cleantech

Renewables

Crop Science

Fertilisers

Water Infra. & Supply

Water Management

Water Treatment

Auto

Buildings

Inds. & Integ.

IoT

IT

LED & Lighting

Smart Grid

Transport

0%

10%

20%

30%

40%

50%

60%

70%

10 60 110

% o

f top

50

FMs

Ove

rwei

ght

Relative weight of top 50 FMs (100=neutral)

UNDERWEIGHT

OVERWEIGHT

EdTech

K-12 & childcare & Misc

Post-secondary, Colleges & Universities

Publishing & content

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0 20 40 60 80 100 120

% o

f top

50

FMs

Ove

rwei

ght

Relative weight of top 50 FMs (100=neutral) UNDERWEIGHT

OVERWEIGHT

Table 4: Climate change sub-themes Sub-theme Description Advanced Biofuels

Cellulosic ethanol, algae fuel, biohydrogen, biomethanol, DMF, biohydrogen diesel etc..

Agricultural Equipment

Agribusiness, agri equipment, irrigation, precision farming, supply chain management etc.

Cleantech Electric vehicles (EVs), wind, solar, among others. Renewables Electric vehicles (EVs), wind, solar, among others. Crop Science

Agronomy, enzymes, fungicides, genetically modified (GM) crops, pesticides, etc.

Fertilisers Agribusiness, ammonia, fertilizers, nitrogen, phosphates, potash, urea etc.

Water Infra. & Supply

Engineering & construction, pipes, pumps and valves, and water utilities

Water Management

Irrigation, drought resistant seeds and crops, precision agriculture, smart meters etc.

Water Treatment

Wastewater, industrial treatment, chemicals, desalination, water quality, bottled water, TIC etc.

Auto Autocatalysts, EVs, engine components etc. Buildings Appliances; building materials; home renovation;

HVAC; insulation materials etc. Inds. & Integ. Automation, controls, heat transfer, T&D etc. IT Cloud computing, data centres, heating and cooling,

power management, semiconductors etc. LED & Lighting

Chips, CFLs, CCFLs, LEDs, lighting management, luminaries, process equipment etc.

Smart Grid Automatic meter reading; grid storage; distributed grid mgmt; EV charging infrastructure; ICT etc.

Transport Lightweighting, rail & bus services, jet engines etc. Source: BofA Merrill Lynch Global Research

Table 5: Education sub-themes Sub-themes Description EdTech Products, technologies and

services which facilitate and enable the shift from print to digital and from classroom to on-line learning

K-12 & childcare & Misc K–12 is a designation for the sum of primary and secondary education.

Post-secondary, Colleges & Universities

This encompasses higher, post-secondary, tertiary or third level education.

Publishing & content Includes academic publishing (books and journals), textbooks / course books, academic research and scholarship, preparatory materials, training materials, other educational materials – as well as retailers and distributors of such materials.

Source: BofA Merrill Lynch Global Research

Themat ic Inves t ing 09 January 2015

13

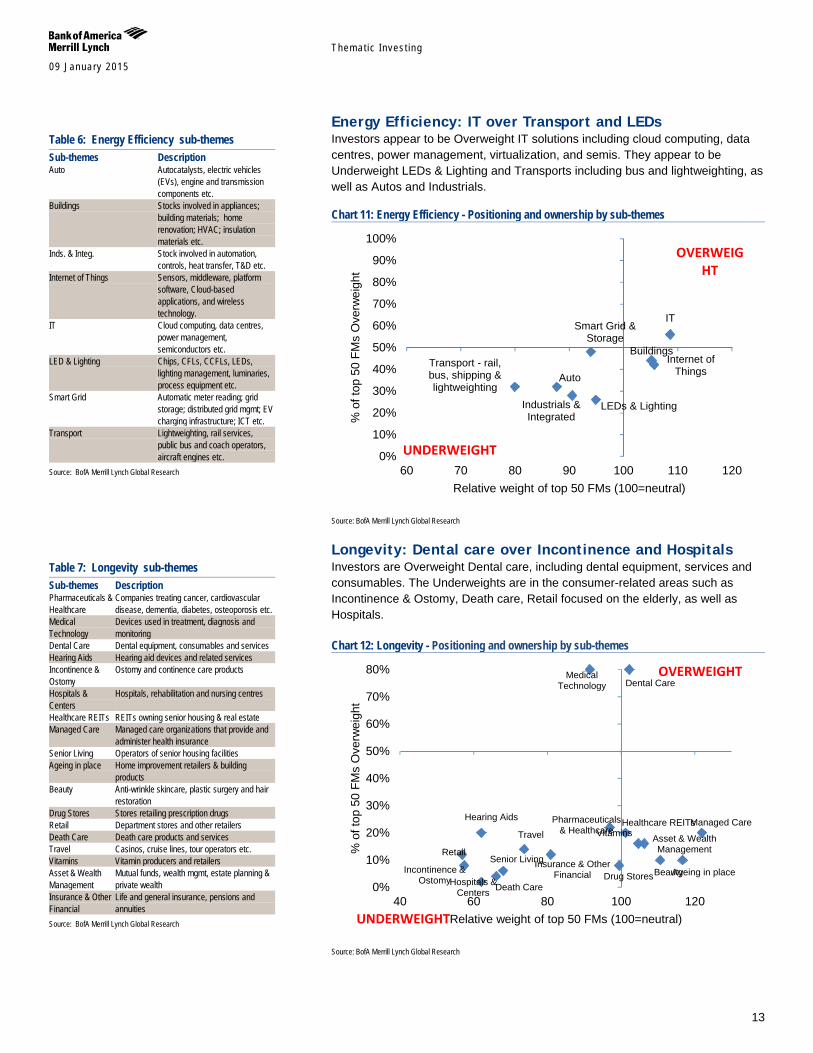

Energy Efficiency: IT over Transport and LEDs Investors appear to be Overweight IT solutions including cloud computing, data centres, power management, virtualization, and semis. They appear to be Underweight LEDs & Lighting and Transports including bus and lightweighting, as well as Autos and Industrials.

Chart 11: Energy Efficiency - Positioning and ownership by sub-themes

Source: BofA Merrill Lynch Global Research

Longevity: Dental care over Incontinence and Hospitals Investors are Overweight Dental care, including dental equipment, services and consumables. The Underweights are in the consumer-related areas such as Incontinence & Ostomy, Death care, Retail focused on the elderly, as well as Hospitals. Chart 12: Longevity - Positioning and ownership by sub-themes

Source: BofA Merrill Lynch Global Research

Auto

Buildings

Industrials & Integrated

Internet of Things

IT

LEDs & Lighting

Smart Grid & Storage

Transport - rail, bus, shipping & lightweighting

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

60 70 80 90 100 110 120

% o

f top

50

FMs

Ove

rwei

ght

Relative weight of top 50 FMs (100=neutral)

UNDERWEIGHT

OVERWEIGHT

Pharmaceuticals & Healthcare

Medical Technology Dental Care

Hearing Aids

Incontinence & Ostomy Hospitals &

Centers

Healthcare REITs Managed Care

Senior Living Ageing in place Beauty Drug Stores

Retail

Death Care

Travel Vitamins Asset & Wealth Management

Insurance & Other Financial

0%

10%

20%

30%

40%

50%

60%

70%

80%

40 60 80 100 120

% o

f top

50

FMs

Ove

rwei

ght

Relative weight of top 50 FMs (100=neutral) UNDERWEIGHT

OVERWEIGHT

Table 6: Energy Efficiency sub-themes Sub-themes Description Auto Autocatalysts, electric vehicles

(EVs), engine and transmission components etc.

Buildings Stocks involved in appliances; building materials; home renovation; HVAC; insulation materials etc.

Inds. & Integ. Stock involved in automation, controls, heat transfer, T&D etc.

Internet of Things Sensors, middleware, platform software, Cloud-based applications, and wireless technology.

IT Cloud computing, data centres, power management, semiconductors etc.

LED & Lighting Chips, CFLs, CCFLs, LEDs, lighting management, luminaries, process equipment etc.

Smart Grid Automatic meter reading; grid storage; distributed grid mgmt; EV charging infrastructure; ICT etc.

Transport Lightweighting, rail services, public bus and coach operators, aircraft engines etc.

Source: BofA Merrill Lynch Global Research

Table 7: Longevity sub-themes Sub-themes Description Pharmaceuticals & Healthcare

Companies treating cancer, cardiovascular disease, dementia, diabetes, osteoporosis etc.

Medical Technology

Devices used in treatment, diagnosis and monitoring

Dental Care Dental equipment, consumables and services Hearing Aids Hearing aid devices and related services Incontinence & Ostomy

Ostomy and continence care products

Hospitals & Centers

Hospitals, rehabilitation and nursing centres

Healthcare REITs REITs owning senior housing & real estate Managed Care Managed care organizations that provide and

administer health insurance Senior Living Operators of senior housing facilities Ageing in place Home improvement retailers & building

products Beauty Anti-wrinkle skincare, plastic surgery and hair

restoration Drug Stores Stores retailing prescription drugs Retail Department stores and other retailers Death Care Death care products and services Travel Casinos, cruise lines, tour operators etc. Vitamins Vitamin producers and retailers Asset & Wealth Management

Mutual funds, wealth mgmt, estate planning & private wealth

Insurance & Other Financial

Life and general insurance, pensions and annuities

Source: BofA Merrill Lynch Global Research

Themat ic Inves t ing 09 January 2015

14

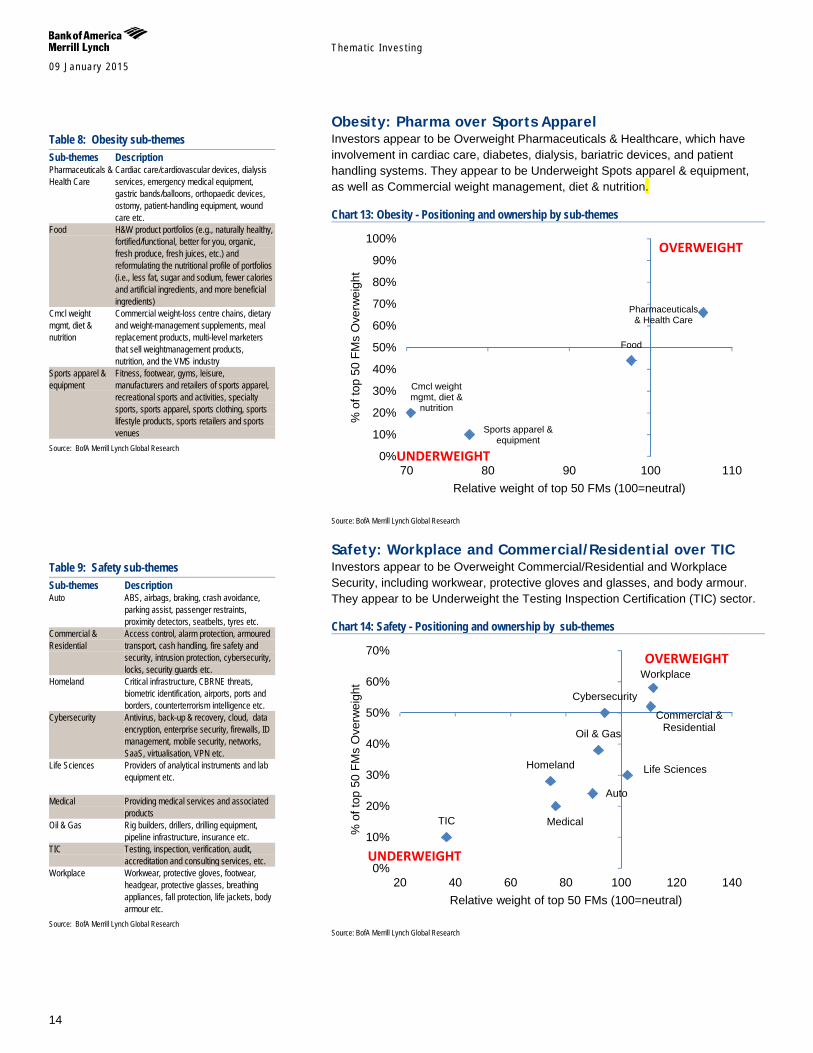

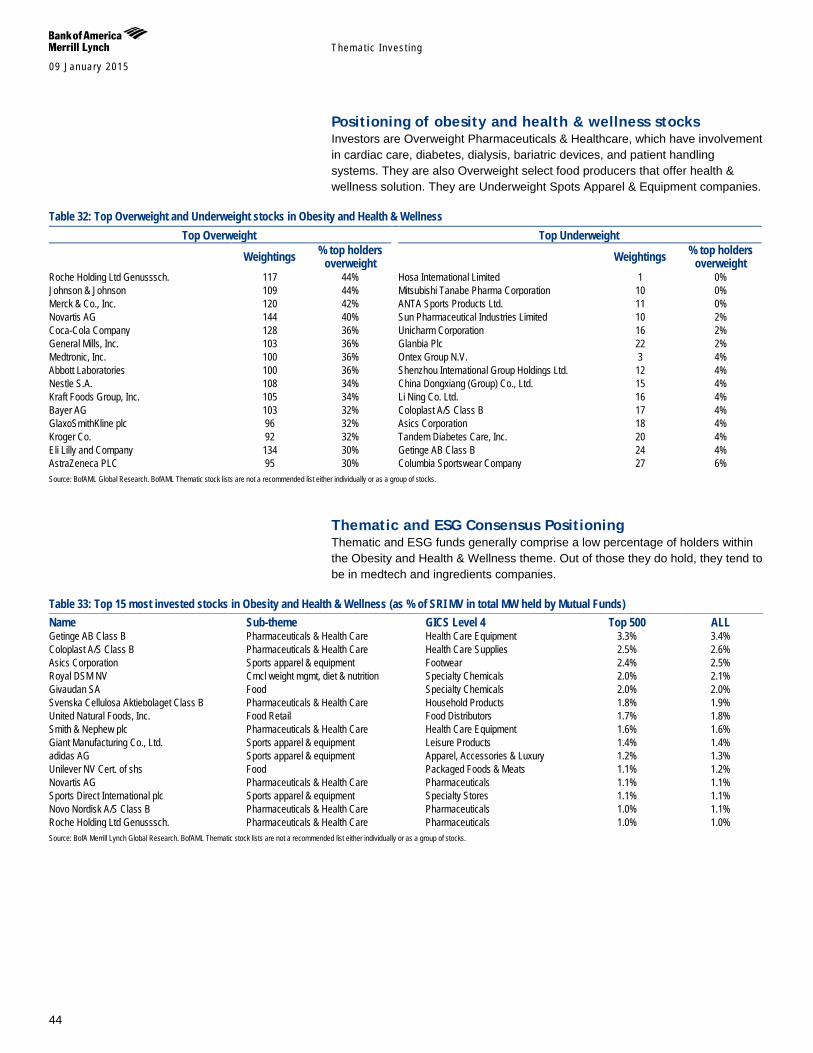

Obesity: Pharma over Sports Apparel Investors appear to be Overweight Pharmaceuticals & Healthcare, which have involvement in cardiac care, diabetes, dialysis, bariatric devices, and patient handling systems. They appear to be Underweight Spots apparel & equipment, as well as Commercial weight management, diet & nutrition.

Chart 13: Obesity - Positioning and ownership by sub-themes

Source: BofA Merrill Lynch Global Research

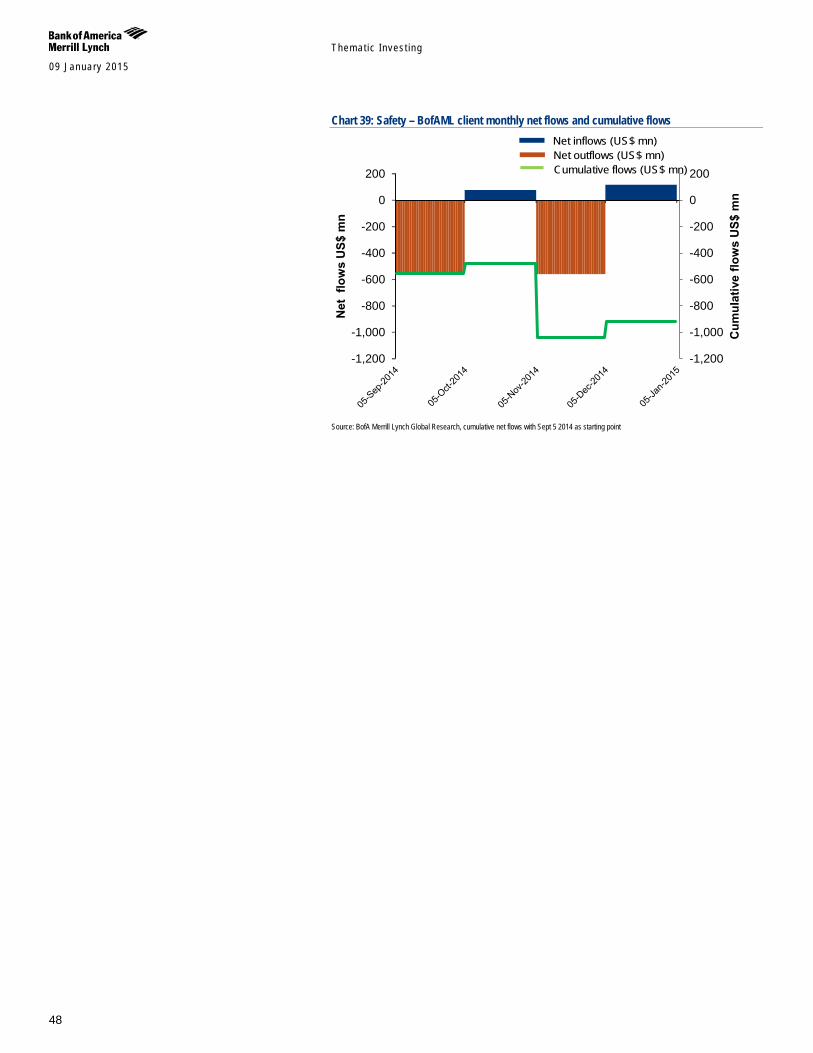

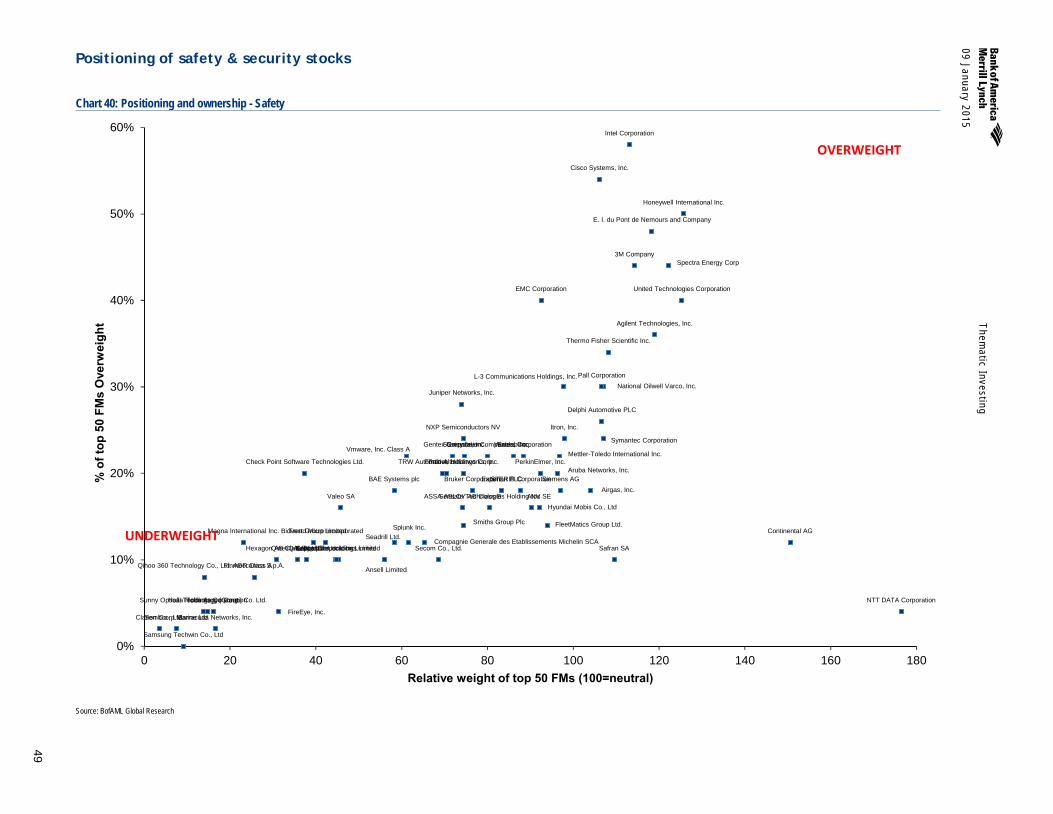

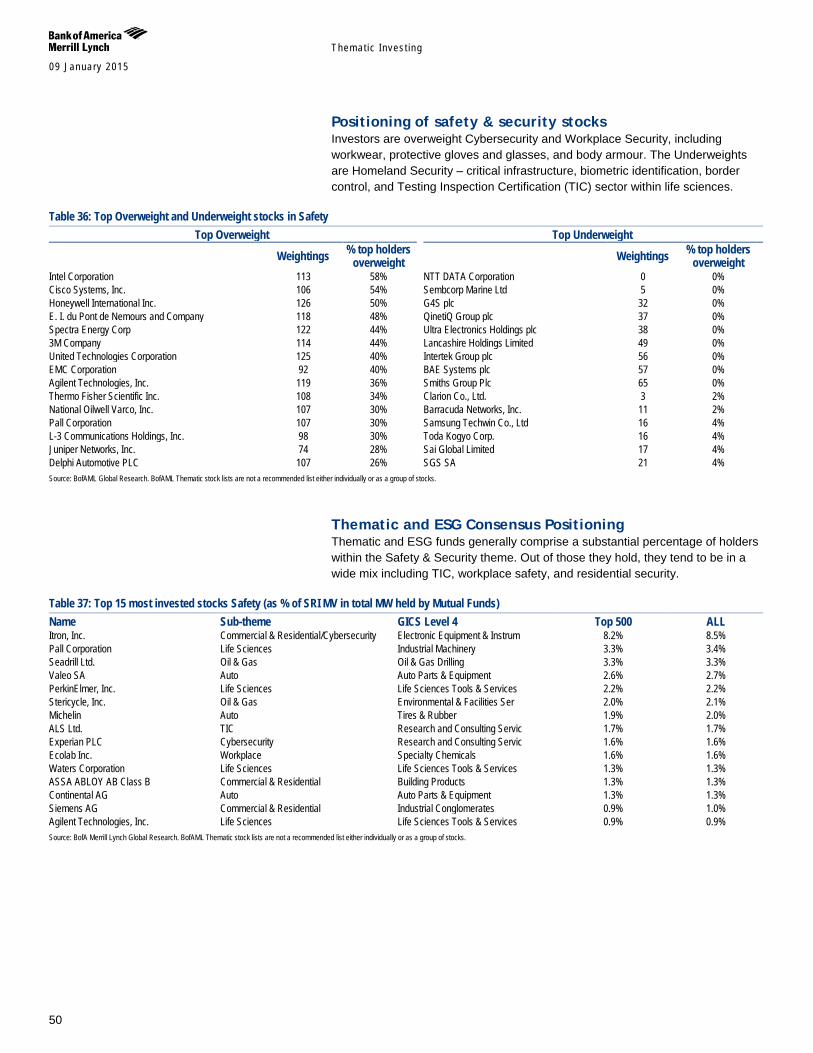

Safety: Workplace and Commercial/Residential over TIC Investors appear to be Overweight Commercial/Residential and Workplace Security, including workwear, protective gloves and glasses, and body armour. They appear to be Underweight the Testing Inspection Certification (TIC) sector.

Chart 14: Safety - Positioning and ownership by sub-themes

Source: BofA Merrill Lynch Global Research

Pharmaceuticals & Health Care

Food

Cmcl weight mgmt, diet &

nutrition

Sports apparel & equipment

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

70 80 90 100 110

% o

f top

50

FMs

Ove

rwei

ght

Relative weight of top 50 FMs (100=neutral)

UNDERWEIGHT

OVERWEIGHT

Auto

Commercial & Residential

Homeland

Cybersecurity

Life Sciences

Medical

Oil & Gas

TIC

Workplace

0%

10%

20%

30%

40%

50%

60%

70%

20 40 60 80 100 120 140

% o

f top

50

FMs

Ove

rwei

ght

Relative weight of top 50 FMs (100=neutral)

UNDERWEIGHT

OVERWEIGHT

Table 8: Obesity sub-themes Sub-themes Description Pharmaceuticals & Health Care

Cardiac care/cardiovascular devices, dialysis services, emergency medical equipment, gastric bands/balloons, orthopaedic devices, ostomy, patient-handling equipment, wound care etc.

Food H&W product portfolios (e.g., naturally healthy, fortified/functional, better for you, organic, fresh produce, fresh juices, etc.) and reformulating the nutritional profile of portfolios (i.e., less fat, sugar and sodium, fewer calories and artificial ingredients, and more beneficial ingredients)

Cmcl weight mgmt, diet & nutrition

Commercial weight-loss centre chains, dietary and weight-management supplements, meal replacement products, multi-level marketers that sell weightmanagement products, nutrition, and the VMS industry

Sports apparel & equipment

Fitness, footwear, gyms, leisure, manufacturers and retailers of sports apparel, recreational sports and activities, specialty sports, sports apparel, sports clothing, sports lifestyle products, sports retailers and sports venues

Source: BofA Merrill Lynch Global Research

Table 9: Safety sub-themes Sub-themes Description Auto ABS, airbags, braking, crash avoidance,

parking assist, passenger restraints, proximity detectors, seatbelts, tyres etc.

Commercial & Residential

Access control, alarm protection, armoured transport, cash handling, fire safety and security, intrusion protection, cybersecurity, locks, security guards etc.

Homeland Critical infrastructure, CBRNE threats, biometric identification, airports, ports and borders, counterterrorism intelligence etc.

Cybersecurity Antivirus, back-up & recovery, cloud, data encryption, enterprise security, firewalls, ID management, mobile security, networks, SaaS, virtualisation, VPN etc.

Life Sciences

Providers of analytical instruments and lab equipment etc.

Medical Providing medical services and associated products

Oil & Gas Rig builders, drillers, drilling equipment, pipeline infrastructure, insurance etc.

TIC Testing, inspection, verification, audit, accreditation and consulting services, etc.

Workplace Workwear, protective gloves, footwear, headgear, protective glasses, breathing appliances, fall protection, life jackets, body armour etc.

Source: BofA Merrill Lynch Global Research

Themat ic Inves t ing 09 January 2015

15

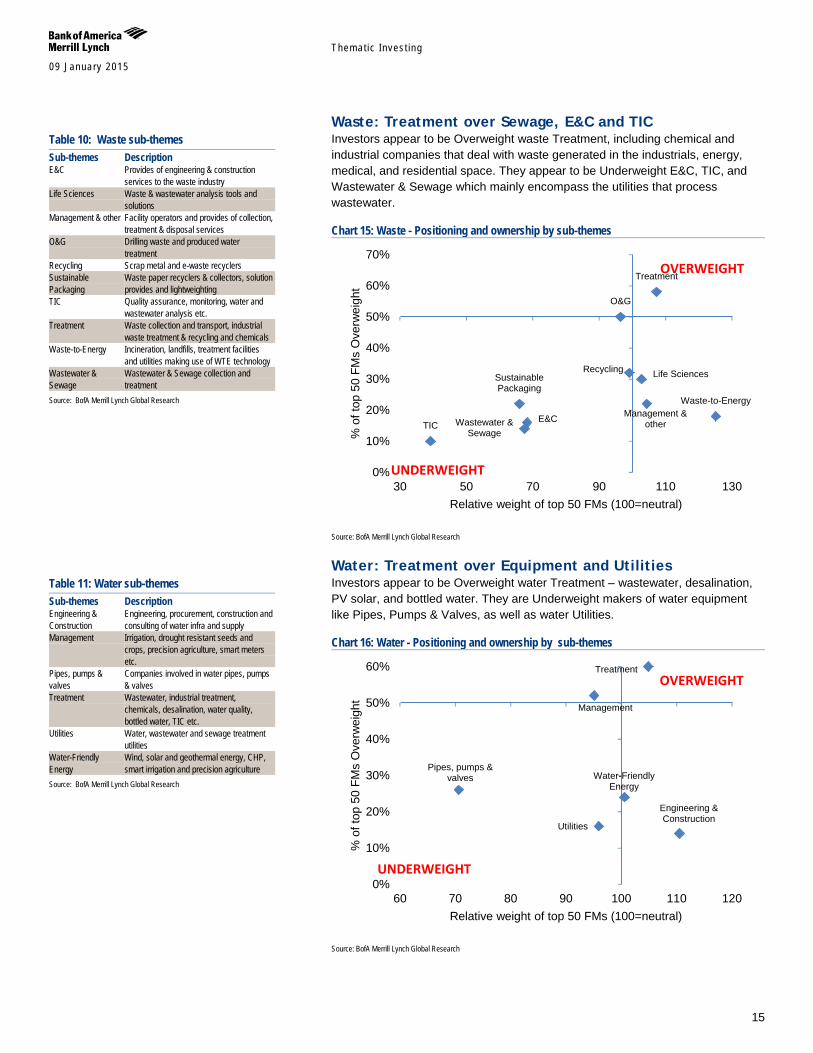

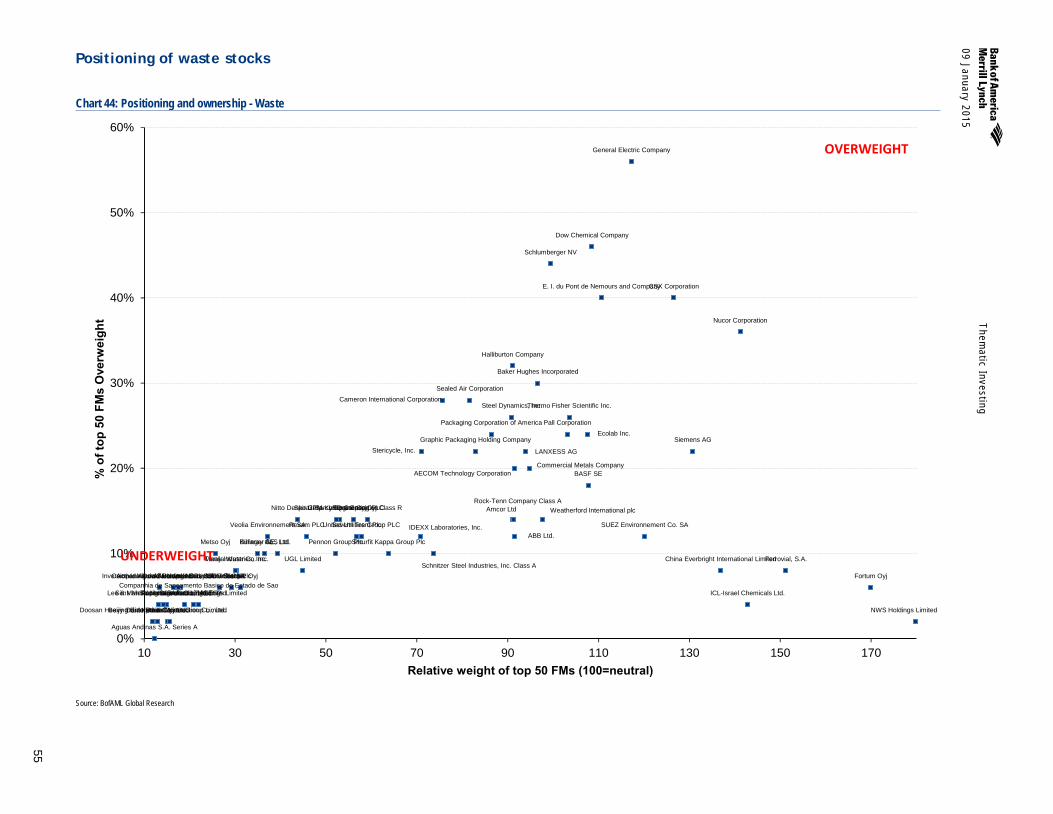

Waste: Treatment over Sewage, E&C and TIC Investors appear to be Overweight waste Treatment, including chemical and industrial companies that deal with waste generated in the industrials, energy, medical, and residential space. They appear to be Underweight E&C, TIC, and Wastewater & Sewage which mainly encompass the utilities that process wastewater.

Chart 15: Waste - Positioning and ownership by sub-themes

Source: BofA Merrill Lynch Global Research

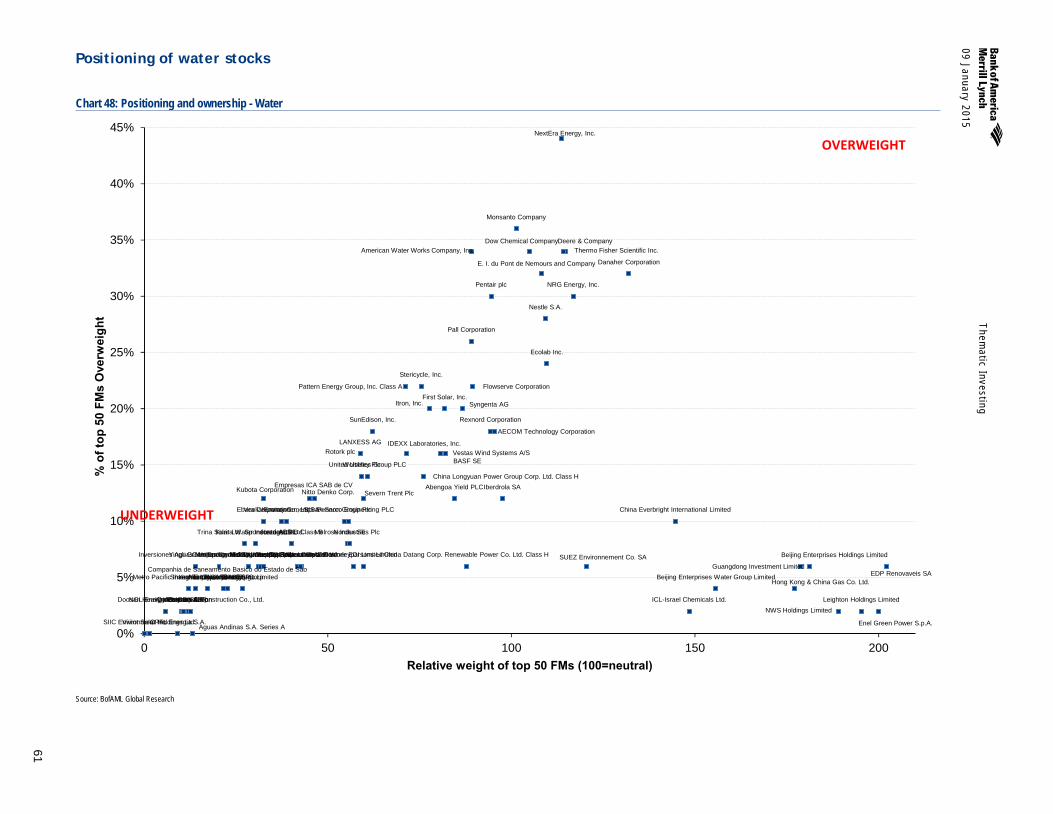

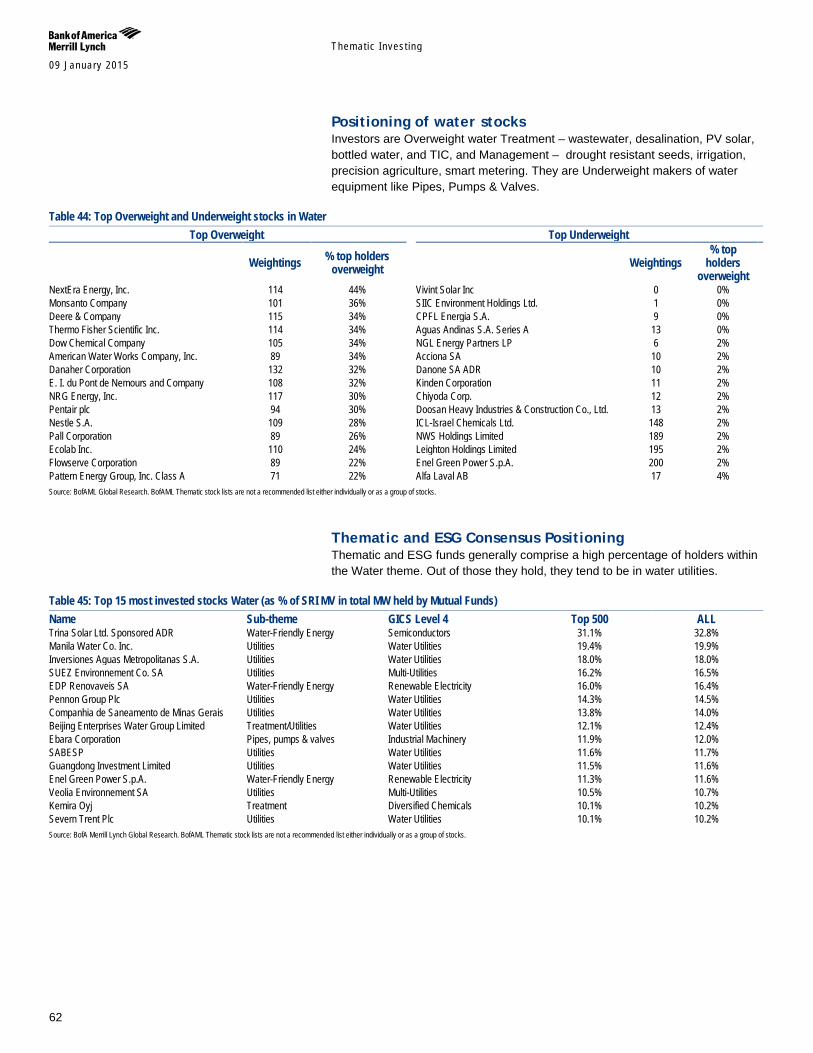

Water: Treatment over Equipment and Utilities Investors appear to be Overweight water Treatment – wastewater, desalination, PV solar, and bottled water. They are Underweight makers of water equipment like Pipes, Pumps & Valves, as well as water Utilities.

Chart 16: Water - Positioning and ownership by sub-themes

Source: BofA Merrill Lynch Global Research

E&C

Life Sciences

Management & other

O&G

Recycling Sustainable Packaging

TIC

Treatment

Waste-to-Energy

Wastewater & Sewage

0%

10%

20%

30%

40%

50%

60%

70%

30 50 70 90 110 130

% o

f top

50

FMs

Ove

rwei

ght

Relative weight of top 50 FMs (100=neutral)

UNDERWEIGHT

OVERWEIGHT

Engineering & Construction

Management

Pipes, pumps & valves

Treatment

Utilities

Water-Friendly Energy

0%

10%

20%

30%

40%

50%

60%

60 70 80 90 100 110 120

% o

f top

50

FMs

Ove

rwei

ght

Relative weight of top 50 FMs (100=neutral)

UNDERWEIGHT

OVERWEIGHT

Table 10: Waste sub-themes Sub-themes Description E&C Provides of engineering & construction

services to the waste industry Life Sciences Waste & wastewater analysis tools and

solutions Management & other Facility operators and provides of collection,

treatment & disposal services O&G Drilling waste and produced water

treatment Recycling Scrap metal and e-waste recyclers Sustainable Packaging

Waste paper recyclers & collectors, solution provides and lightweighting

TIC Quality assurance, monitoring, water and wastewater analysis etc.

Treatment Waste collection and transport, industrial waste treatment & recycling and chemicals

Waste-to-Energy Incineration, landfills, treatment facilities and utilities making use of WTE technology

Wastewater & Sewage

Wastewater & Sewage collection and treatment

Source: BofA Merrill Lynch Global Research

Table 11: Water sub-themes Sub-themes Description Engineering & Construction

Engineering, procurement, construction and consulting of water infra and supply

Management Irrigation, drought resistant seeds and crops, precision agriculture, smart meters etc.

Pipes, pumps & valves

Companies involved in water pipes, pumps & valves

Treatment Wastewater, industrial treatment, chemicals, desalination, water quality, bottled water, TIC etc.

Utilities Water, wastewater and sewage treatment utilities

Water-Friendly Energy

Wind, solar and geothermal energy, CHP, smart irrigation and precision agriculture

Source: BofA Merrill Lynch Global Research

Themat ic Inves t ing 09 January 2015

16

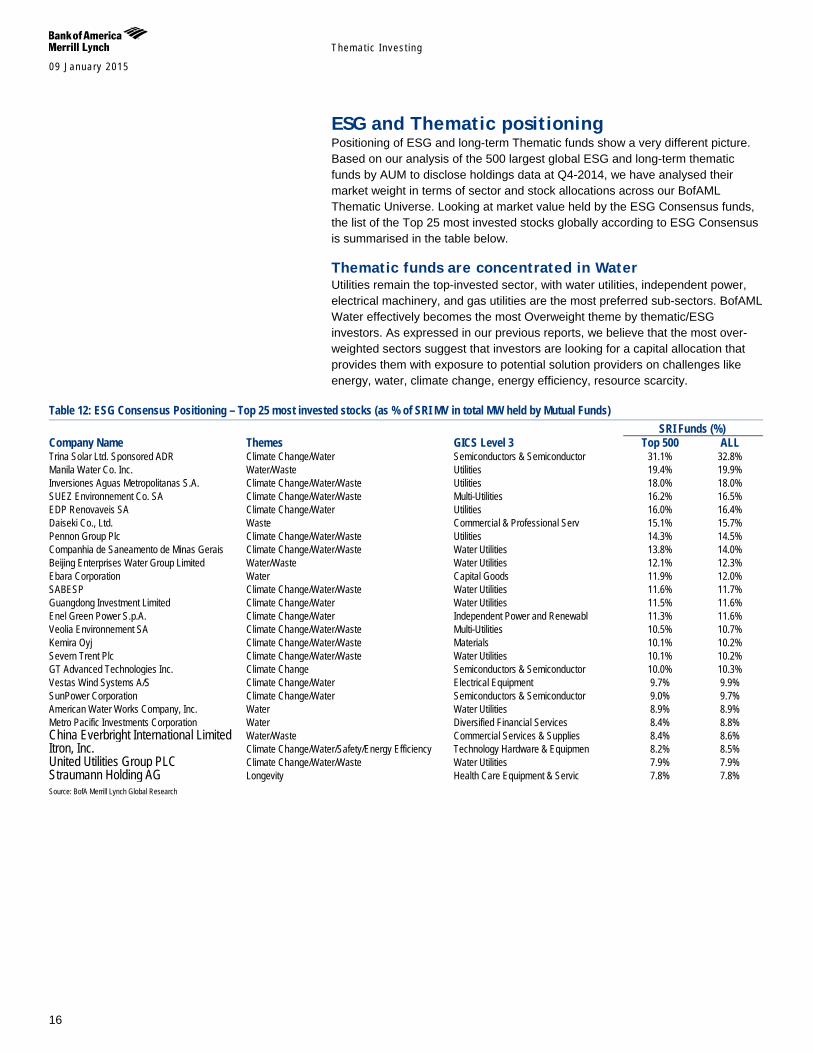

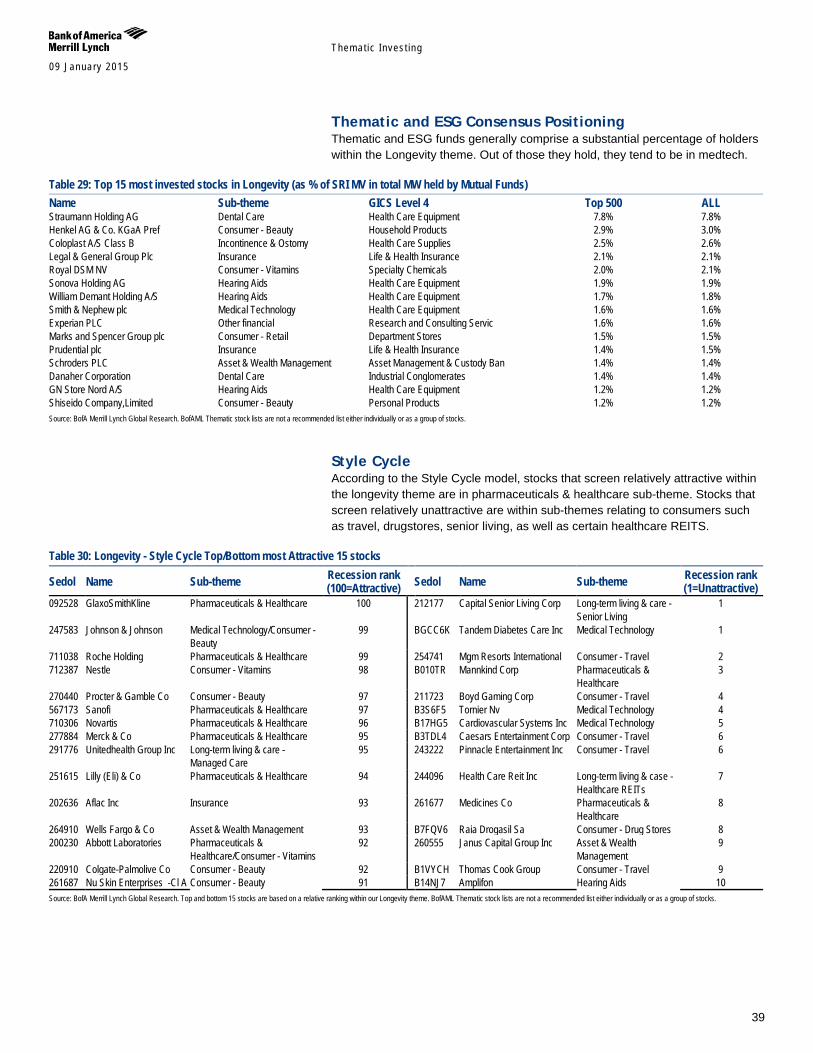

ESG and Thematic positioning Positioning of ESG and long-term Thematic funds show a very different picture. Based on our analysis of the 500 largest global ESG and long-term thematic funds by AUM to disclose holdings data at Q4-2014, we have analysed their market weight in terms of sector and stock allocations across our BofAML Thematic Universe. Looking at market value held by the ESG Consensus funds, the list of the Top 25 most invested stocks globally according to ESG Consensus is summarised in the table below.

Thematic funds are concentrated in Water Utilities remain the top-invested sector, with water utilities, independent power, electrical machinery, and gas utilities are the most preferred sub-sectors. BofAML Water effectively becomes the most Overweight theme by thematic/ESG investors. As expressed in our previous reports, we believe that the most over-weighted sectors suggest that investors are looking for a capital allocation that provides them with exposure to potential solution providers on challenges like energy, water, climate change, energy efficiency, resource scarcity.

Table 12: ESG Consensus Positioning – Top 25 most invested stocks (as % of SRI MV in total MW held by Mutual Funds) SRI Funds (%) Company Name Themes GICS Level 3 Top 500 ALL Trina Solar Ltd. Sponsored ADR Climate Change/Water Semiconductors & Semiconductor 31.1% 32.8% Manila Water Co. Inc. Water/Waste Utilities 19.4% 19.9% Inversiones Aguas Metropolitanas S.A. Climate Change/Water/Waste Utilities 18.0% 18.0% SUEZ Environnement Co. SA Climate Change/Water/Waste Multi-Utilities 16.2% 16.5% EDP Renovaveis SA Climate Change/Water Utilities 16.0% 16.4% Daiseki Co., Ltd. Waste Commercial & Professional Serv 15.1% 15.7% Pennon Group Plc Climate Change/Water/Waste Utilities 14.3% 14.5% Companhia de Saneamento de Minas Gerais Climate Change/Water/Waste Water Utilities 13.8% 14.0% Beijing Enterprises Water Group Limited Water/Waste Water Utilities 12.1% 12.3% Ebara Corporation Water Capital Goods 11.9% 12.0% SABESP Climate Change/Water/Waste Water Utilities 11.6% 11.7% Guangdong Investment Limited Climate Change/Water Water Utilities 11.5% 11.6% Enel Green Power S.p.A. Climate Change/Water Independent Power and Renewabl 11.3% 11.6% Veolia Environnement SA Climate Change/Water/Waste Multi-Utilities 10.5% 10.7% Kemira Oyj Climate Change/Water/Waste Materials 10.1% 10.2% Severn Trent Plc Climate Change/Water/Waste Water Utilities 10.1% 10.2% GT Advanced Technologies Inc. Climate Change Semiconductors & Semiconductor 10.0% 10.3% Vestas Wind Systems A/S Climate Change/Water Electrical Equipment 9.7% 9.9% SunPower Corporation Climate Change/Water Semiconductors & Semiconductor 9.0% 9.7% American Water Works Company, Inc. Water Water Utilities 8.9% 8.9% Metro Pacific Investments Corporation Water Diversified Financial Services 8.4% 8.8% China Everbright International Limited Water/Waste Commercial Services & Supplies 8.4% 8.6% Itron, Inc. Climate Change/Water/Safety/Energy Efficiency Technology Hardware & Equipmen 8.2% 8.5% United Utilities Group PLC Climate Change/Water/Waste Water Utilities 7.9% 7.9% Straumann Holding AG Longevity Health Care Equipment & Servic 7.8% 7.8% Source: BofA Merrill Lynch Global Research

Themat ic Inves t ing 09 January 2015

17

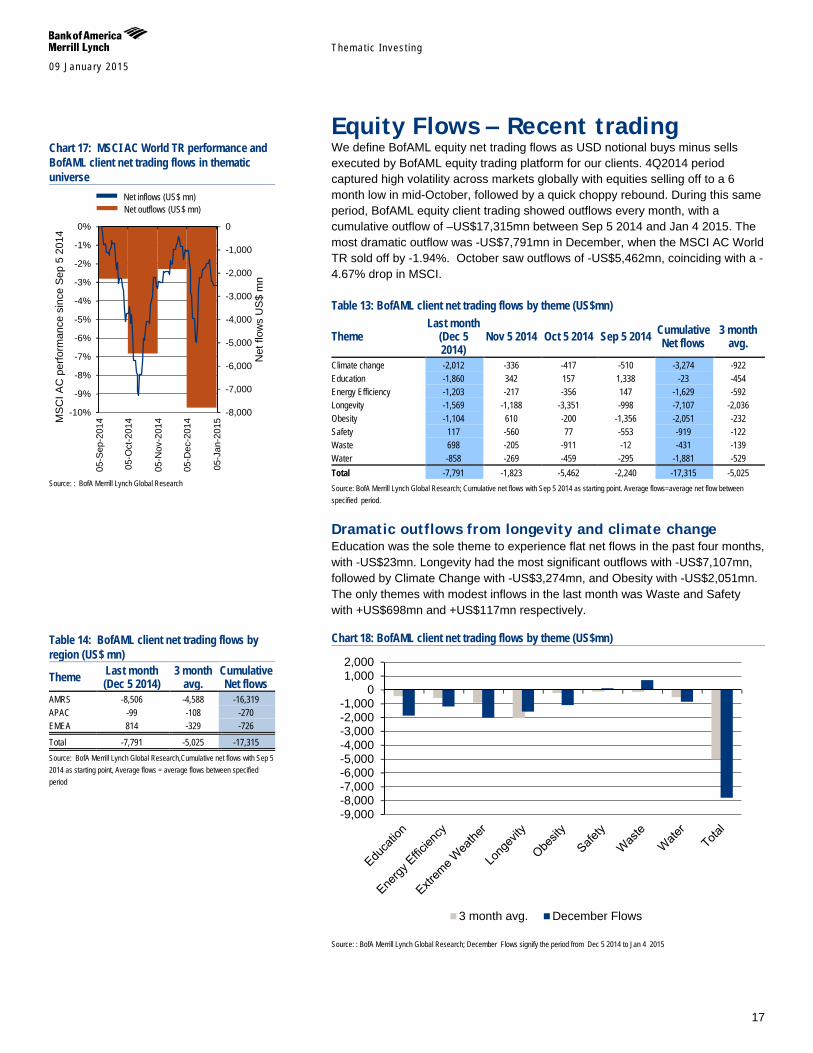

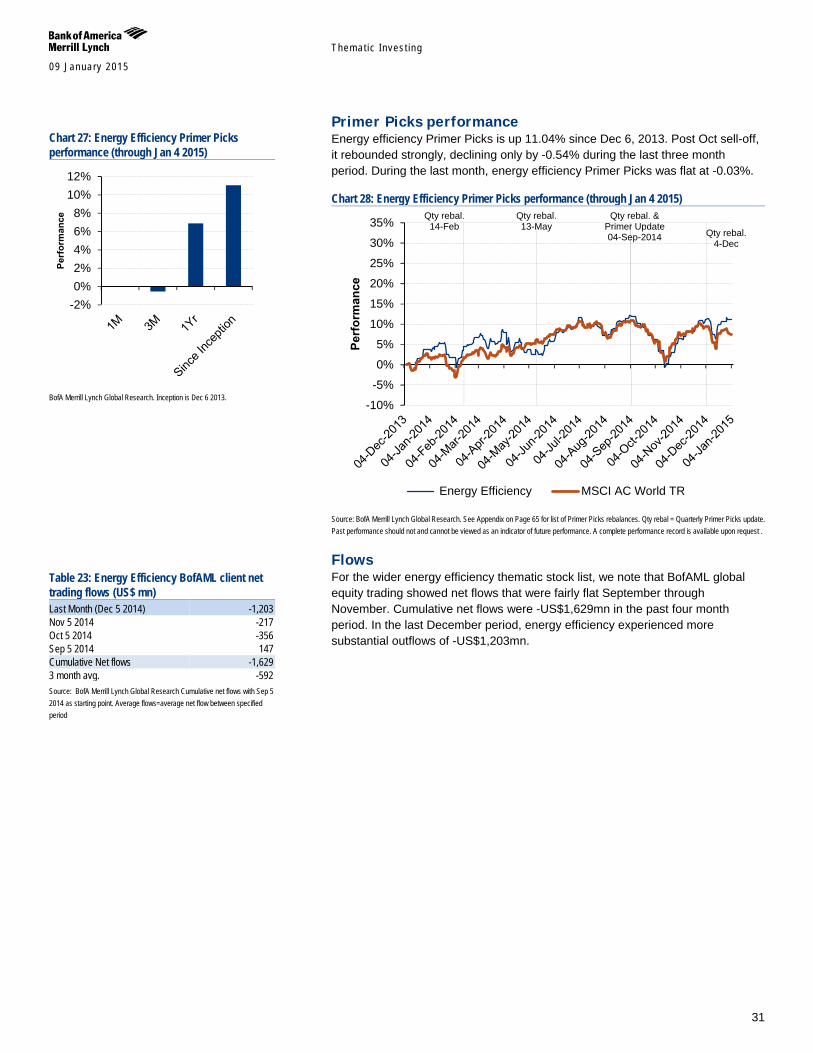

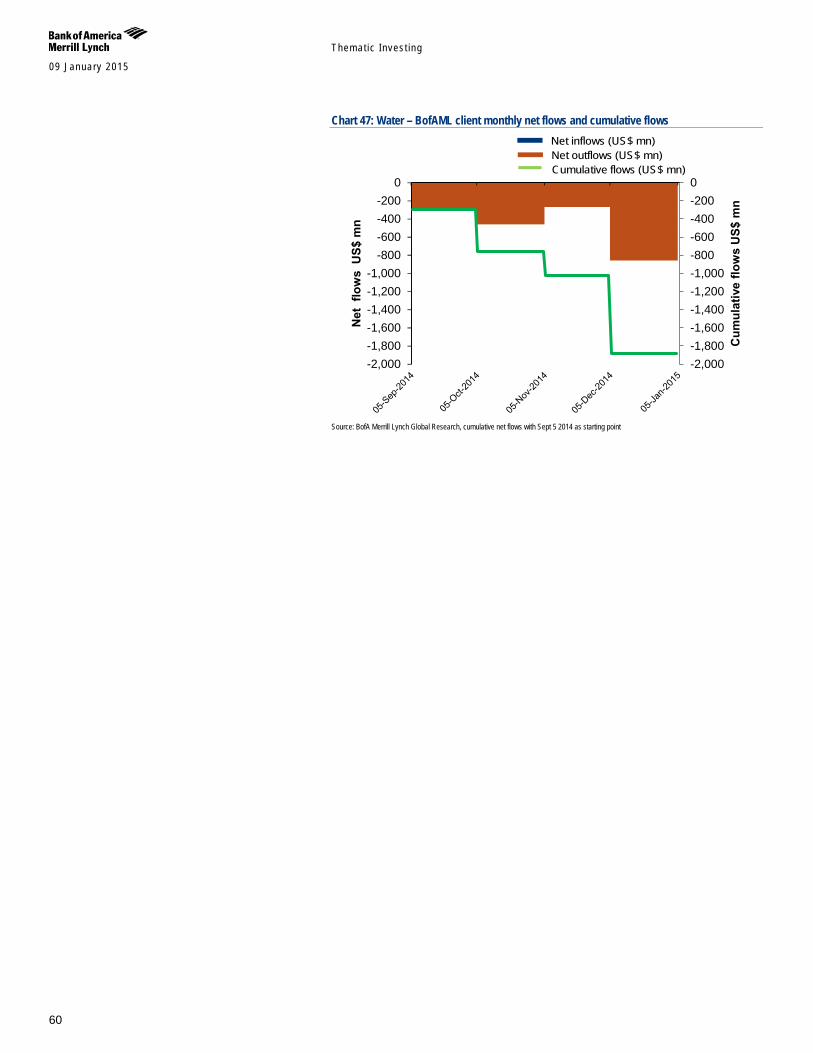

Equity Flows – Recent trading We define BofAML equity net trading flows as USD notional buys minus sells executed by BofAML equity trading platform for our clients. 4Q2014 period captured high volatility across markets globally with equities selling off to a 6 month low in mid-October, followed by a quick choppy rebound. During this same period, BofAML equity client trading showed outflows every month, with a cumulative outflow of –US$17,315mn between Sep 5 2014 and Jan 4 2015. The most dramatic outflow was -US$7,791mn in December, when the MSCI AC World TR sold off by -1.94%. October saw outflows of -US$5,462mn, coinciding with a -4.67% drop in MSCI.

Table 13: BofAML client net trading flows by theme (US$mn)

Theme Last month

(Dec 5 2014)

Nov 5 2014 Oct 5 2014 Sep 5 2014 Cumulative Net flows

3 month avg.

Climate change -2,012 -336 -417 -510 -3,274 -922 Education -1,860 342 157 1,338 -23 -454 Energy Efficiency -1,203 -217 -356 147 -1,629 -592 Longevity -1,569 -1,188 -3,351 -998 -7,107 -2,036 Obesity -1,104 610 -200 -1,356 -2,051 -232 Safety 117 -560 77 -553 -919 -122 Waste 698 -205 -911 -12 -431 -139 Water -858 -269 -459 -295 -1,881 -529 Total -7,791 -1,823 -5,462 -2,240 -17,315 -5,025 Source: BofA Merrill Lynch Global Research; Cumulative net flows with Sep 5 2014 as starting point. Average flows=average net flow between specified period.

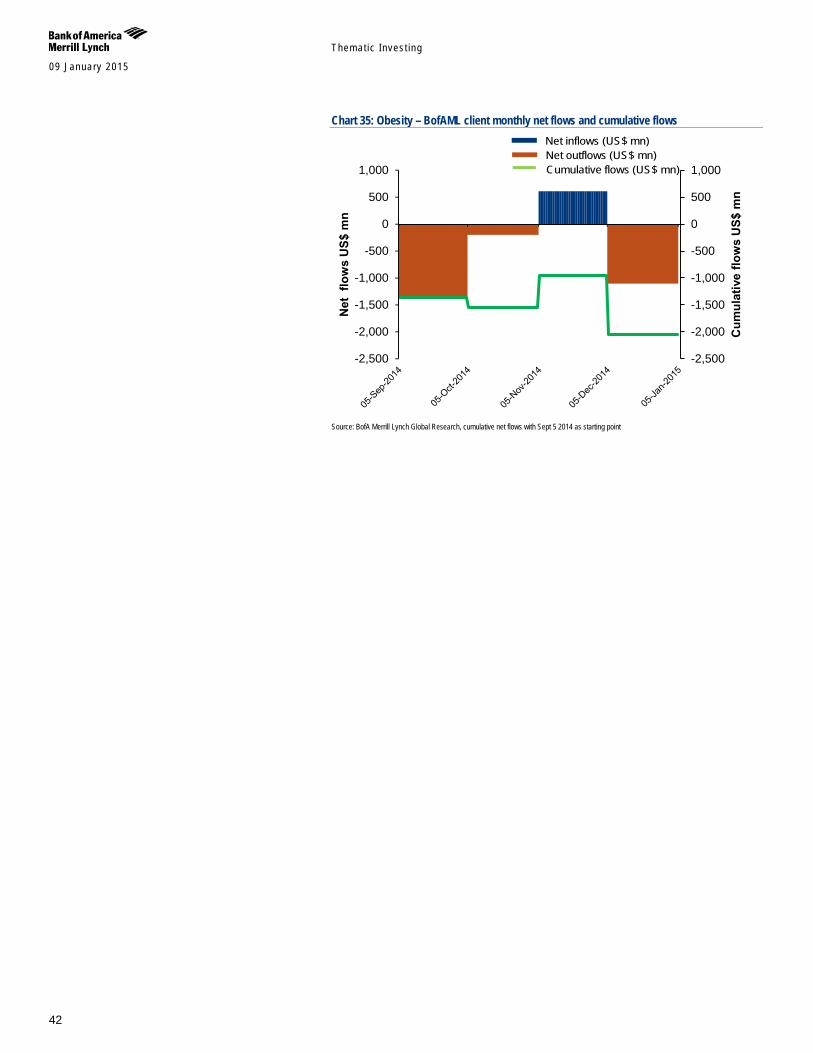

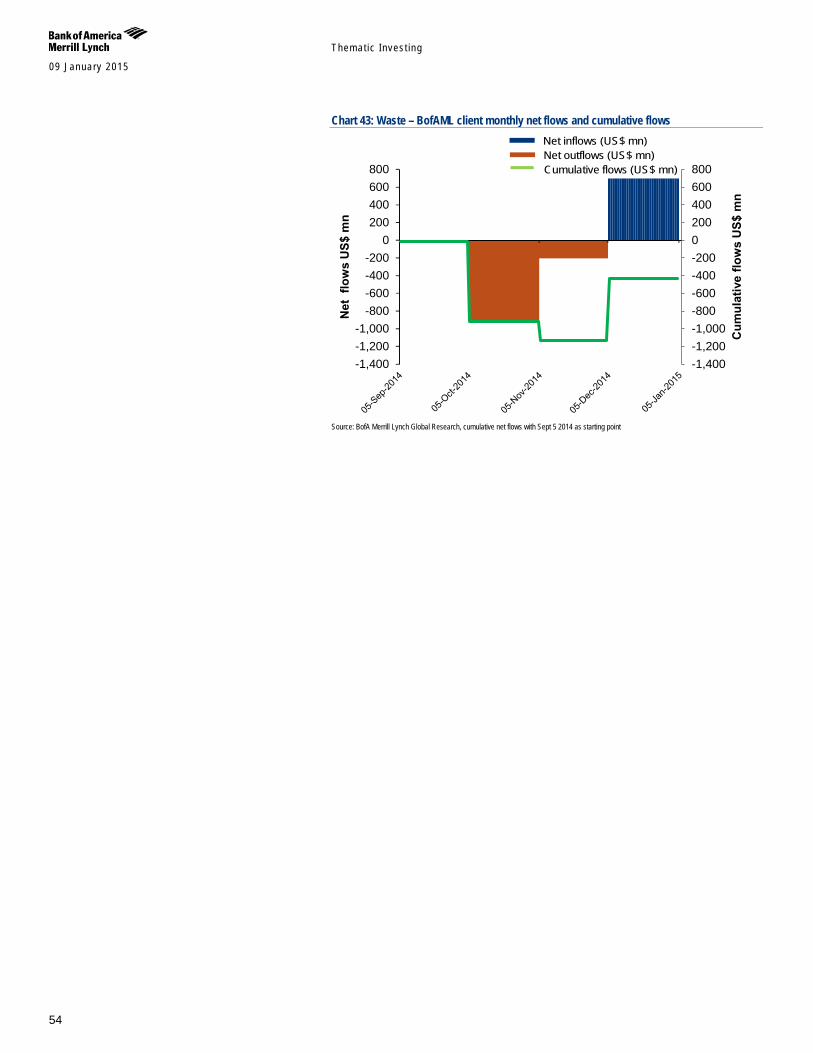

Dramatic outflows from longevity and climate change Education was the sole theme to experience flat net flows in the past four months, with -US$23mn. Longevity had the most significant outflows with -US$7,107mn, followed by Climate Change with -US$3,274mn, and Obesity with -US$2,051mn. The only themes with modest inflows in the last month was Waste and Safety with +US$698mn and +US$117mn respectively.

Chart 18: BofAML client net trading flows by theme (US$mn)

Source: : BofA Merrill Lynch Global Research; December Flows signify the period from Dec 5 2014 to Jan 4 2015

-9,000-8,000-7,000-6,000-5,000-4,000-3,000-2,000-1,000

01,0002,000

3 month avg. December Flows

Chart 17: MSCI AC World TR performance and BofAML client net trading flows in thematic universe

Source: : BofA Merrill Lynch Global Research

Table 14: BofAML client net trading flows by region (US$ mn)

Theme Last month (Dec 5 2014)

3 month avg.

Cumulative Net flows

AMRS -8,506 -4,588 -16,319 APAC -99 -108 -270 EMEA 814 -329 -726

Total -7,791 -5,025 -17,315 Source: BofA Merrill Lynch Global Research,Cumulative net flows with Sep 5 2014 as starting point, Average flows = average flows between specified period

-8,000

-7,000

-6,000

-5,000

-4,000

-3,000

-2,000

-1,000

0

-10%

-9%

-8%

-7%

-6%

-5%

-4%

-3%

-2%

-1%

0%

05-S

ep-2

014

05-O

ct-2

014

05-N

ov-2

014

05-D

ec-2

014

05-J

an-2

015

Net

flow

s U

S$

mn

MS

CI A

C p

erfo

rman

ce s

ince

Sep

5 2

014

Net inflows (US$ mn) Net outflows (US$ mn)

Themat ic Inves t ing 09 January 2015

18

Themes Climate change & extreme weather - A perfect storm A Transforming World thematic impacts: Earth, Government, Innovation, Markets, People. Extreme weather: welcome to the new normal - Climate anomalies are on the rise globally with 2013 marking the 28th consecutive year with a global temperature above the 20th century average (Source: NOAA). Extreme weather is becoming the new normal, with extremes now covering 10% of the globe vs. 0.1% to 0.2% from 1951-1980 (Source: NASA). While no single incident can be definitively attributed to climate change, there is overwhelming scientific evidence that we should expect more damaging extreme weather events, with up to 40% of global land area at risk from extreme heat by 2040E (Source: Coumou et. al.).

Losses are skyrocketing: we’re not sufficiently prepared - Global climate-related losses have risen to as much as US$200bn in 2005 as a result of Hurricane Katrina. 2011 and 2012 were the two worst years on record for extreme weather events, which caused a total of more than $170 billion in damages, much of that to businesses (Source: NOAA). 90% of the S&P Global 100 across industry sectors identify extreme weather and climate change as current or future business risks (Source: C2ES). But worryingly, less than 50% of companies have integrated climate change adaptation into their business strategies (Source: CDP)

It’s getting warmer: on track for a 2-4°Cwarmer world - Without further action to reduce greenhouse gas emissions (GHGs), scientists are predicting a 2-4°C rise in temperatures by 2100 and it could happen as early as the 2060s. This would mean unprecedented heat waves, severe drought, and major floods in many regions with serious impacts on human systems and ecosystems and new risks that would threaten our future adaptation needs (Source: World Bank). The U.S. National Climate Change Assessment (NCA) – released in May 2014 warns of climate change-related problems that are already disrupting the lives of ordinary Americans (e.g. extreme weather, sea-level rise, thawing of Arctic sea ice, shift in growing seasons et. al.) and calls for action to reduce GHG emissions.

A perfect storm is brewing: food-water-energy security - By 2030E, global food demand is set to increase by up to 50%, water demand by up to 40% and energy demand by up to 50%. Given how closely food, water and energy security are connected, this will mean increasing trade-offs and resource rationing. It also threatens to create a “perfect storm” of global events, which poses key questions for governments, stakeholders, corporates and investors as to how to meet these demands while adapting to and mitigating climate change.

Weathering the storm: 7 entry points for long-term solutions - In our view, a number of stocks are placed to benefit from their role as long-term solution providers for the perfect storm of food-water-energy security in an extreme weather and climate change constrained world. We have identified c200 stocks covered by BofAML Global Research across seven entry points: 1) Water; 2) Fertilizers; 3) Crop Science; 4) Farming and Agricultural Equipment; 5) Second Generation Biofuels; 6) Energy Efficiency; and 7) Renewables and Cleantech.

Thematic Investing: Extreme weather primer –weathering the perfect storm 12 September 2013

Themat ic Inves t ing 09 January 2015

19

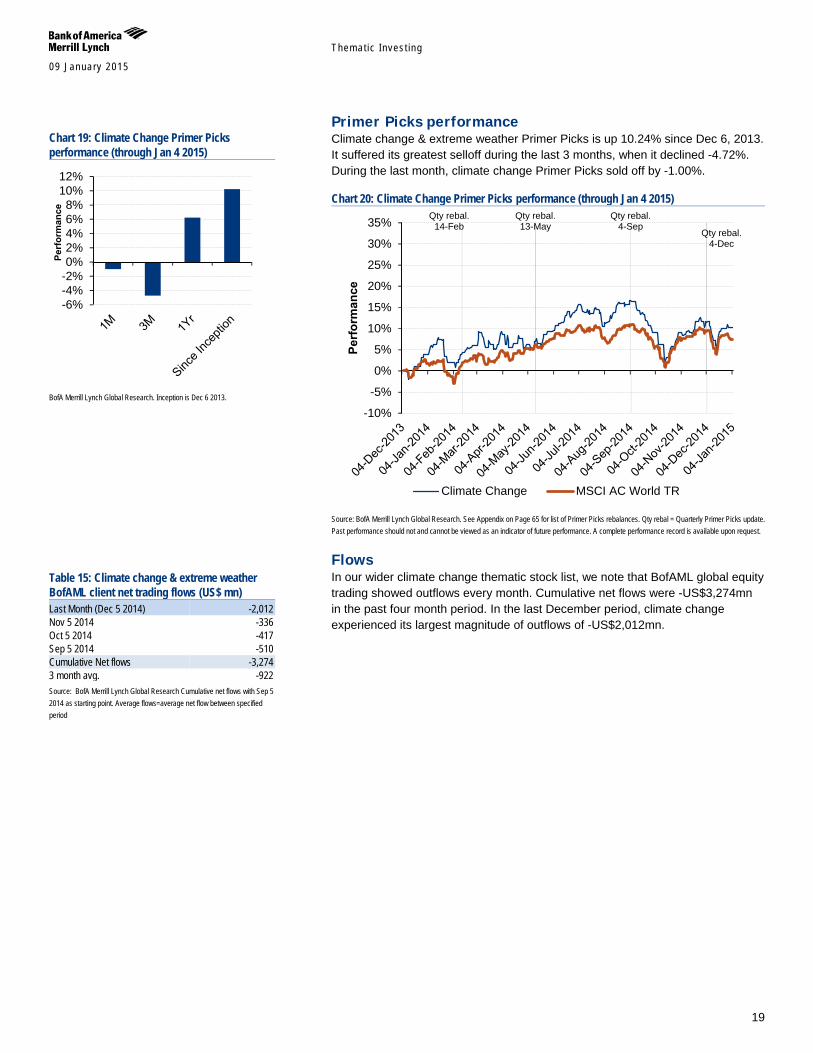

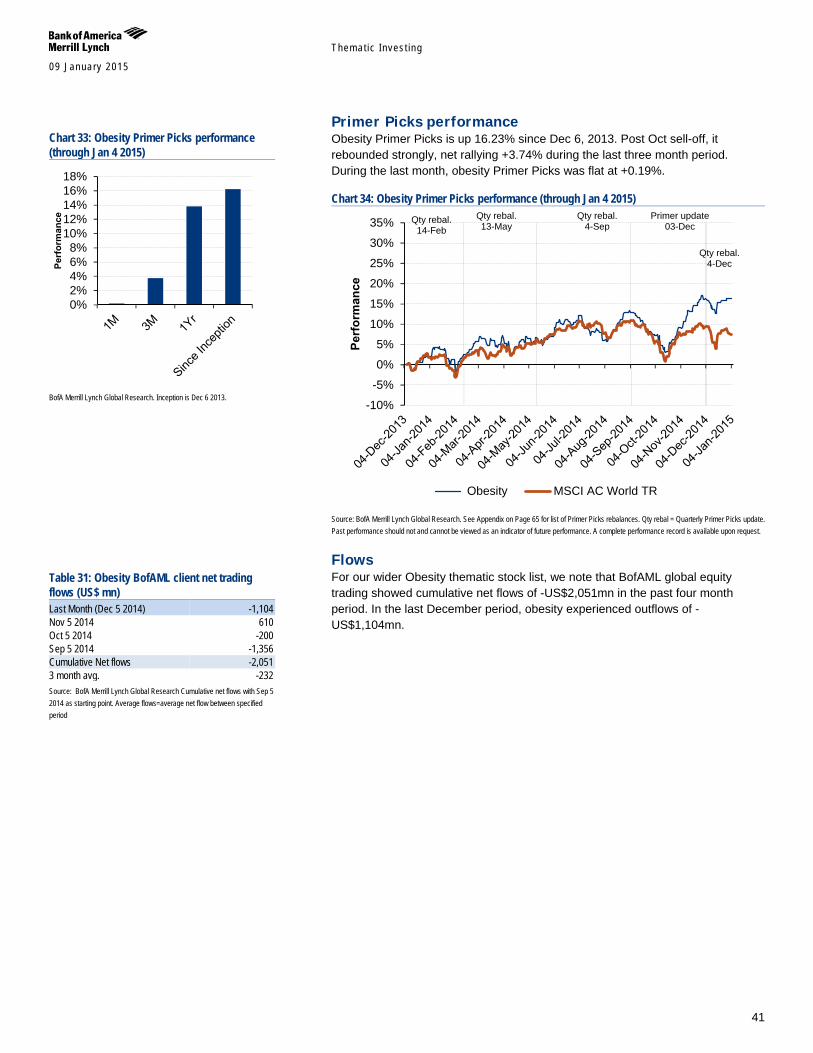

Primer Picks performance Climate change & extreme weather Primer Picks is up 10.24% since Dec 6, 2013. It suffered its greatest selloff during the last 3 months, when it declined -4.72%. During the last month, climate change Primer Picks sold off by -1.00%.

Chart 20: Climate Change Primer Picks performance (through Jan 4 2015)

Source: BofA Merrill Lynch Global Research. See Appendix on Page 65 for list of Primer Picks rebalances. Qty rebal = Quarterly Primer Picks update. Past performance should not and cannot be viewed as an indicator of future performance. A complete performance record is available upon request.

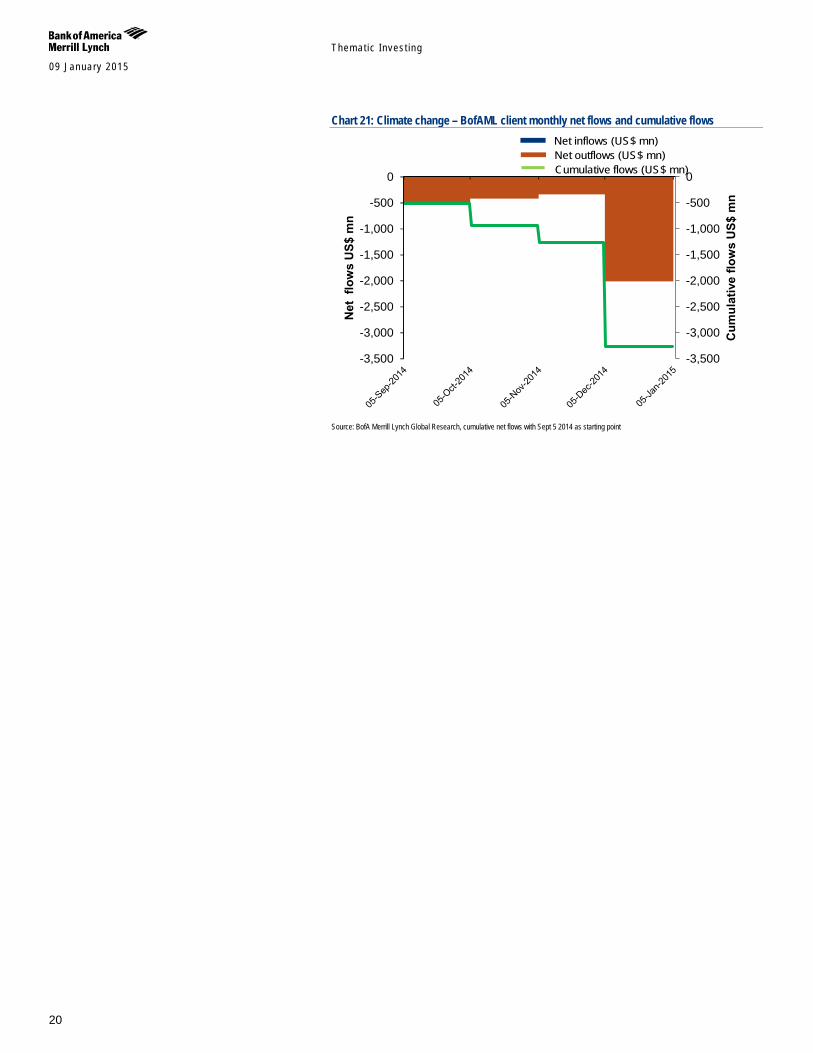

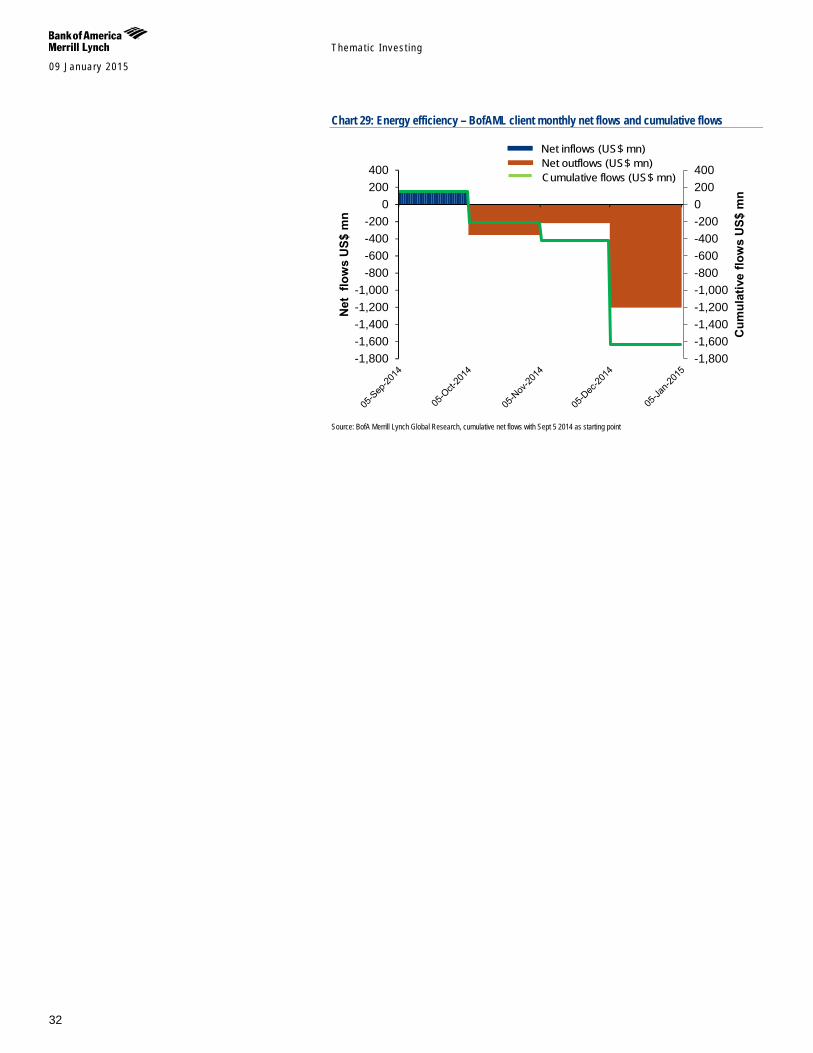

Flows In our wider climate change thematic stock list, we note that BofAML global equity trading showed outflows every month. Cumulative net flows were -US$3,274mn in the past four month period. In the last December period, climate change experienced its largest magnitude of outflows of -US$2,012mn.

Qty rebal. 14-Feb

Qty rebal. 13-May

Qty rebal. 4-Sep

Qty rebal. 4-Dec

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

Perf

orm

ance

Climate Change MSCI AC World TR

Chart 19: Climate Change Primer Picks performance (through Jan 4 2015)

BofA Merrill Lynch Global Research. Inception is Dec 6 2013.

Table 15: Climate change & extreme weather BofAML client net trading flows (US$ mn) Last Month (Dec 5 2014) -2,012 Nov 5 2014 -336 Oct 5 2014 -417 Sep 5 2014 -510 Cumulative Net flows -3,274 3 month avg. -922 Source: BofA Merrill Lynch Global Research Cumulative net flows with Sep 5 2014 as starting point. Average flows=average net flow between specified period

-6%-4%-2%0%2%4%6%8%

10%12%

Perf

orm

ance

Themat ic Inves t ing 09 January 2015

20

Chart 21: Climate change – BofAML client monthly net flows and cumulative flows

Source: BofA Merrill Lynch Global Research, cumulative net flows with Sept 5 2014 as starting point

-3,500

-3,000

-2,500

-2,000

-1,500

-1,000

-500

0

-3,500

-3,000

-2,500

-2,000

-1,500

-1,000

-500

0

Cum

ulat

ive

flow

s U

S$ m

n

Net

flo

ws

US$

mn

Net inflows (US$ mn)Net outflows (US$ mn)Cumulative flows (US$ mn)

09 January 2015

Them

atic Investing

21

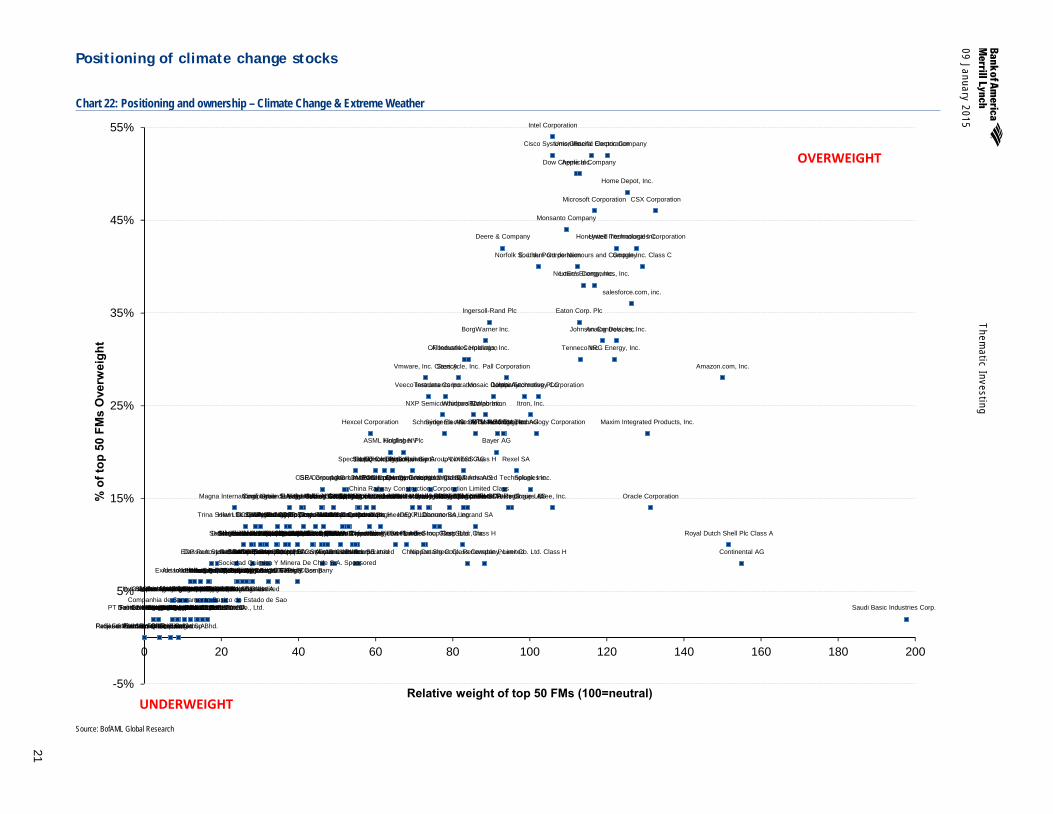

Positioning of climate change stocks

Chart 22: Positioning and ownership – Climate Change & Extreme Weather

Source: BofAML Global Research

ABB Ltd.

Acciona SA Adecoagro S.A.

Advantech Co., Ltd.

AECOM Technology Corporation

AGCO Corporation

Agrium Inc.

Aguas Andinas S.A. Series A

Inversiones Aguas Metropolitanas S.A.

Airtac International Group

Albemarle Corporation

Alfa Laval AB

Alstom SA

Amazon.com, Inc.

Analog Devices, Inc.

Apple Inc.

Aquarius Platinum Limited

ARM Holdings plc

ASML Holding NV

Atlas Copco AB Class A

Atmel Corporation BASF SE

Bayer AG

Beijing Enterprises Holdings Limited

Bombardier Inc. Class B

BorgWarner Inc.

Canadian National Railway Company

CF Industries Holdings, Inc.

China BlueChemical Ltd. Class H China Longyuan Power Group Corp. Ltd. Class H

Cisco Systems, Inc.

Continental AG

Companhia de Saneamento de Minas Gerais Cosan S.A. Industria e Comercio

Cosan Limited Class A

CPFL Energia S.A.

China Railway Construction Corporation Limited Class H Cree, Inc.

China Railway Group Limited Class H

Crompton Greaves Limited

CSR Corporation Limited Class H

CSX Corporation

Daikin Industries, Ltd.

Dana Holding Corporation

Danone SA

Dassault Systemes SA China Datang Corp. Renewable Power Co. Ltd. Class H

Deere & Company

Delphi Automotive PLC

Delta Electronics, Inc.

Doosan Heavy Industries & Construction Co., Ltd.

Dow Chemical Company

E. I. du Pont de Nemours and Company

Eaton Corp. Plc

Ecolab Inc.

EDP Renovaveis SA

Electrolux AB Class B

Enel Green Power S.p.A.

Enphase Energy, Inc.

Equinix, Inc.

Exide Industries Limited

Fauji Fertilizer Bin Qasim Limited

Fauji Fertilizer Co. Ltd.

First Solar, Inc.

FirstGroup plc

FleetMatics Group Ltd.

GCL-Poly Energy Holdings Limited

GEA Group AG Generac Holdings Inc.

General Electric Company

Go-Ahead Group plc

Golden Agri-Resources LTD

Google Inc. Class C

GT Advanced Technologies Inc.

Guangdong Investment Limited

Guangshen Railway Co. Ltd. Class H

Fertilizantes Heringer S.A.

Hexagon AB Class B

Hexcel Corporation

Hiwin Technologies Corp.

Hong Kong & China Gas Co. Ltd.

Home Retail Group plc

Honeywell International Inc.

Iberdrola SA

ICL-Israel Chemicals Ltd.

IDEXX Laboratories, Inc.

Infineon Technologies AG

Incitec Pivot Limited

Ingersoll-Rand Plc

Intel Corporation

Interxion Holding N.V.

Itron, Inc.

Johnson Controls, Inc.

Johnson Matthey Plc

K+S AG

Kemira Oyj

Keppel Corporation Limited

Kingfisher Plc

Kone Oyj Class B

Kuraray Co., Ltd.

Kurita Water Industries Ltd.

LANXESS AG

Legrand SA

LG Innotek Co., Ltd

LG Chem Ltd.

Linear Technology Corporation

LKQ Corporation

Lowe's Companies, Inc.

LS Industrial Systems Co., Ltd.

Magna International Inc.

Mahle-Metal Leve S.A.

Maxim Integrated Products, Inc.

Melrose Industries Plc

Metso Oyj

Compagnie Generale des Etablissements Michelin SCA

Microsoft Corporation

Mitsubishi Heavy Industries, Ltd.

Monsanto Company

Mosaic Company

MTU Aero Engines AG

Nabtesco Corporation

National Express Group PLC

Neste Oil Oyj

Nestle S.A.

Nexans SA

NextEra Energy, Inc.

NGK Insulators, Ltd.

Nippon Sheet Glass Company, Limited Nordex SE

Norfolk Southern Corporation

NRG Energy, Inc.

NXP Semiconductors NV

Obrascon Huarte Lain SA

OMRON Corporation

Oracle Corporation OSRAM Licht AG

Owens Corning

Pall Corporation

Panasonic Corporation

Pattern Energy Group, Inc. Class A

Petronas Chemicals Group Bhd.

Pennon Group Plc

Royal Philips NV

Phosagro OJSC Sponsored GDR RegS

Potash Corporation of Saskatchewan Inc.

Prysmian S.p.A.

Renesas Electronics Corporation

Rexel SA

Ritchie Bros. Auctioneers Incorporated

Rolls-Royce Holdings plc

Rotork plc

Royal Dutch Shell Plc Class A

Companhia de Saneamento Basico do Estado de Sao Paulo SABESP Saudi Basic Industries Corp.

Saudi Arabian Fertilizer Co.

Safran SA

Compagnie de Saint-Gobain SA

salesforce.com, inc.

PT Salim Ivomas Pratama Tbk

Samsung SDI Co., Ltd

Sanken Electric Co., Ltd.

SAP SE

Schneider Electric SE

Sensata Technologies Holding NV

Seoul Semiconductor Co., Ltd Severn Trent Plc

Shanghai Industrial Holdings Limited

Siemens AG

Siemens Limited

Sinofert Holdings Limited

SKF AB Class B

SMC Corporation

SolarCity Corp. Solvay SA

Spectris plc

Spirax-Sarco Engineering PLC

Splunk Inc.

Sociedad Quimica Y Minera De Chile S.A. Sponsored ADR Pfd Class B

STMicroelectronics NV

Stagecoach Group plc

Stericycle, Inc.

SUEZ Environnement Co. SA

Sumitomo Chemical Co., Ltd.

SunEdison, Inc.

SunPower Corporation

Syngenta AG

Tenneco Inc.

Teradata Corporation

Tesla Motors, Inc.

Home Depot, Inc.

Toray Industries, Inc.

Toshiba Corporation Trina Solar Ltd. Sponsored ADR Umicore

Union Pacific Corporation

United Technologies Corporation

United Utilities Group PLC Uralkali JSC Sponsored GDR RegS Vale S.A. Sponsored ADR Valeo SA

Vallourec SA

Veeco Instruments Inc.

Veolia Environnement SA

Vestas Wind Systems A/S

Victrex plc

Vivint Solar Inc

Vmware, Inc. Class A

Whirlpool Corporation

Yaskawa Electric Corporation

Yingli Green Energy Holding Co. Ltd. Sponsored ADR

Zhuzhou CSR Times Electric Co., Ltd. Class H

-5%

5%

15%

25%

35%

45%

55%

0 20 40 60 80 100 120 140 160 180 200

% o

f top

50

FMs

Ove

rwei

ght

Relative weight of top 50 FMs (100=neutral)

OVERWEIGHT

UNDERWEIGHT

Themat ic Inves t ing 09 January 2015

22

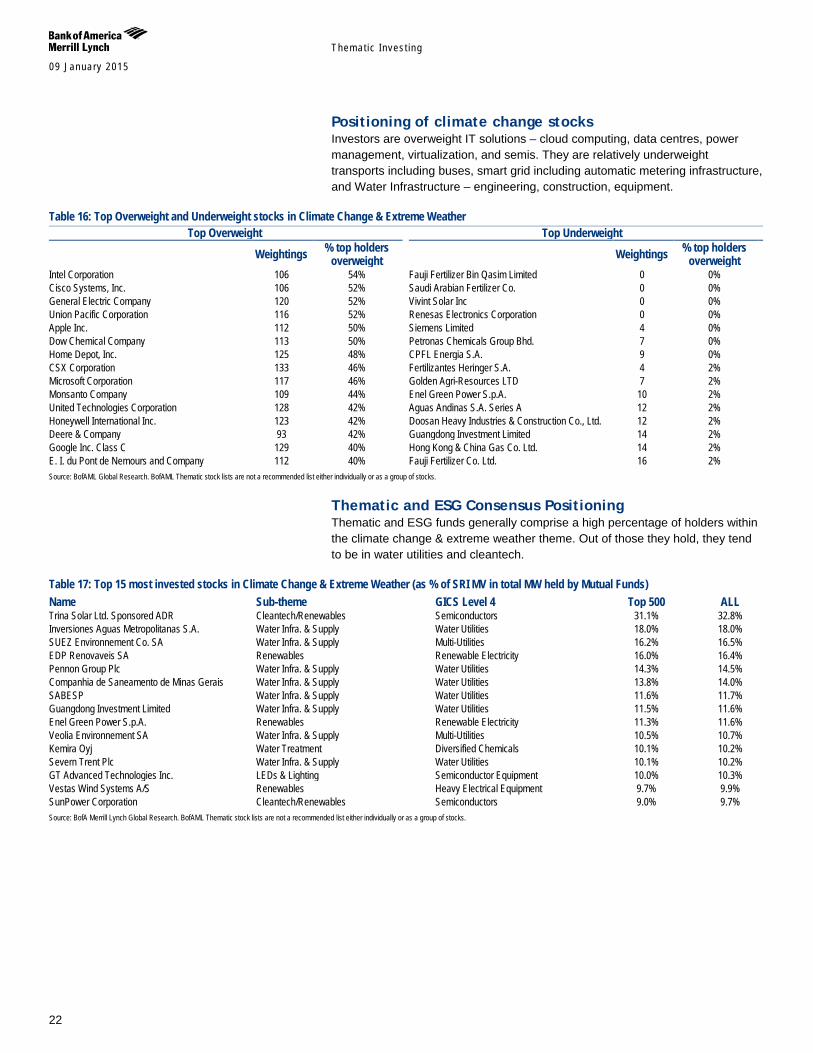

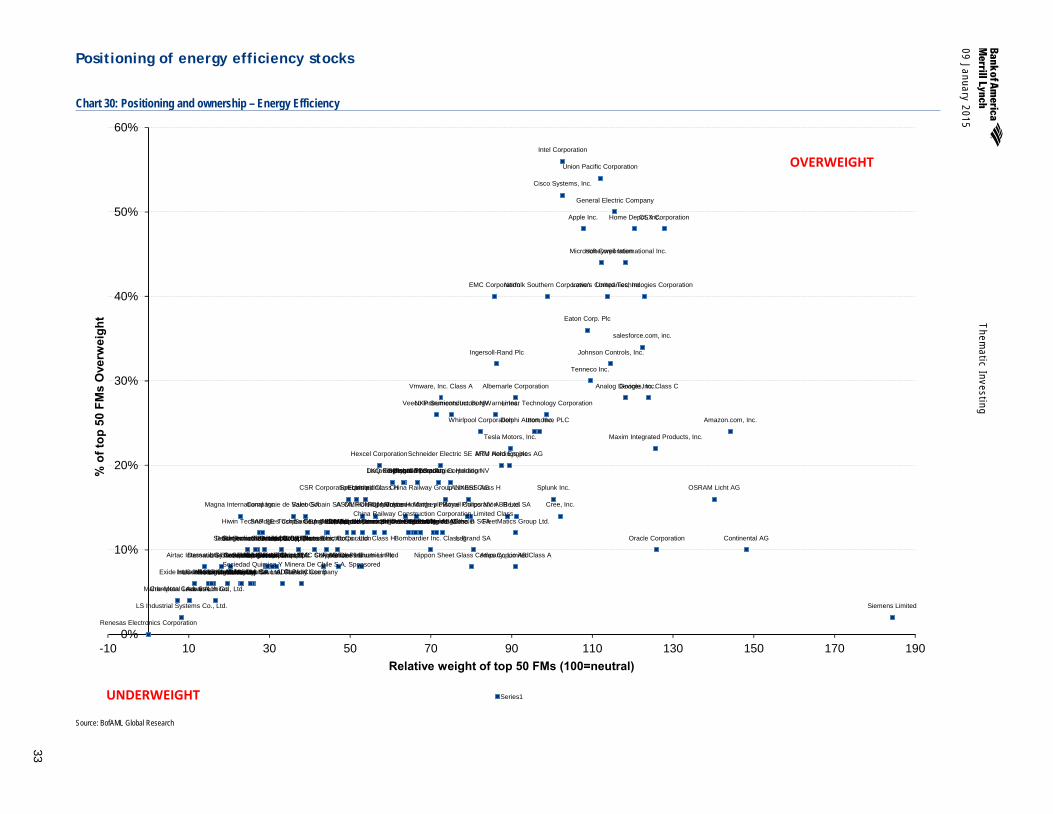

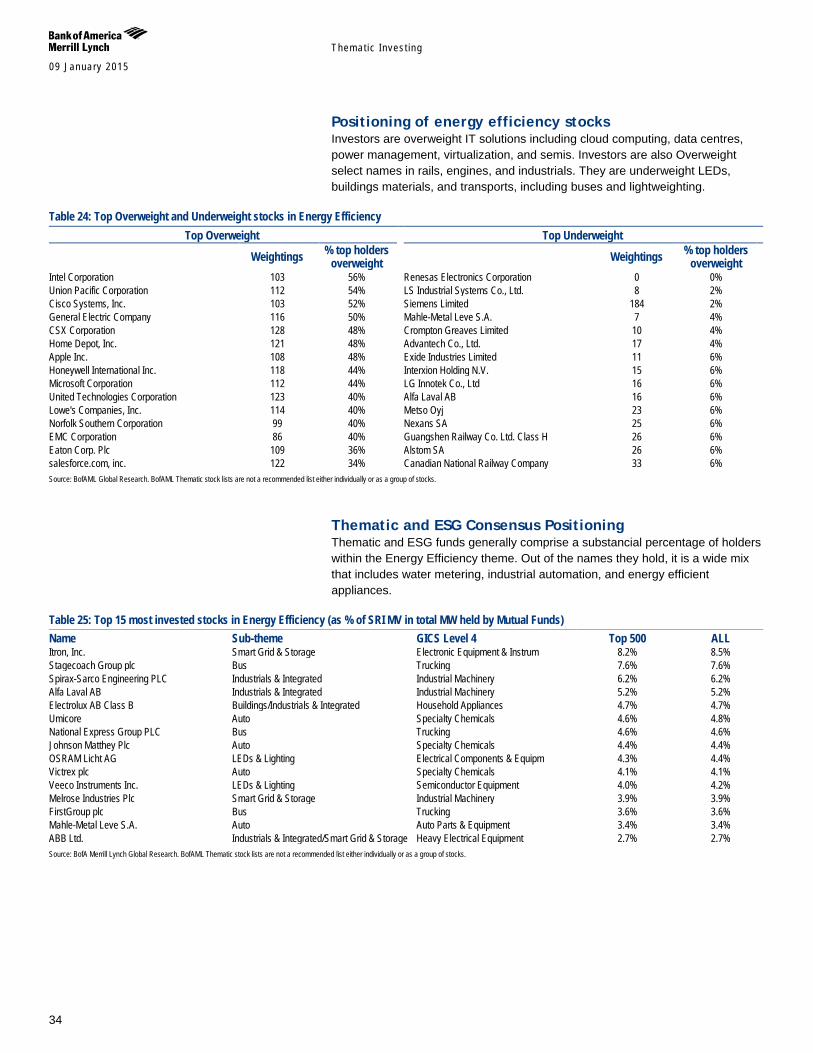

Positioning of climate change stocks Investors are overweight IT solutions – cloud computing, data centres, power management, virtualization, and semis. They are relatively underweight transports including buses, smart grid including automatic metering infrastructure, and Water Infrastructure – engineering, construction, equipment.

Table 16: Top Overweight and Underweight stocks in Climate Change & Extreme Weather Top Overweight Top Underweight

Weightings % top holders overweight Weightings % top holders

overweight Intel Corporation 106 54% Fauji Fertilizer Bin Qasim Limited 0 0% Cisco Systems, Inc. 106 52% Saudi Arabian Fertilizer Co. 0 0% General Electric Company 120 52% Vivint Solar Inc 0 0% Union Pacific Corporation 116 52% Renesas Electronics Corporation 0 0% Apple Inc. 112 50% Siemens Limited 4 0% Dow Chemical Company 113 50% Petronas Chemicals Group Bhd. 7 0% Home Depot, Inc. 125 48% CPFL Energia S.A. 9 0% CSX Corporation 133 46% Fertilizantes Heringer S.A. 4 2% Microsoft Corporation 117 46% Golden Agri-Resources LTD 7 2% Monsanto Company 109 44% Enel Green Power S.p.A. 10 2% United Technologies Corporation 128 42% Aguas Andinas S.A. Series A 12 2% Honeywell International Inc. 123 42% Doosan Heavy Industries & Construction Co., Ltd. 12 2% Deere & Company 93 42% Guangdong Investment Limited 14 2% Google Inc. Class C 129 40% Hong Kong & China Gas Co. Ltd. 14 2% E. I. du Pont de Nemours and Company 112 40% Fauji Fertilizer Co. Ltd. 16 2% Source: BofAML Global Research. BofAML Thematic stock lists are not a recommended list either individually or as a group of stocks.

Thematic and ESG Consensus Positioning Thematic and ESG funds generally comprise a high percentage of holders within the climate change & extreme weather theme. Out of those they hold, they tend to be in water utilities and cleantech.

Table 17: Top 15 most invested stocks in Climate Change & Extreme Weather (as % of SRI MV in total MW held by Mutual Funds) Name Sub-theme GICS Level 4 Top 500 ALL Trina Solar Ltd. Sponsored ADR Cleantech/Renewables Semiconductors 31.1% 32.8% Inversiones Aguas Metropolitanas S.A. Water Infra. & Supply Water Utilities 18.0% 18.0% SUEZ Environnement Co. SA Water Infra. & Supply Multi-Utilities 16.2% 16.5% EDP Renovaveis SA Renewables Renewable Electricity 16.0% 16.4% Pennon Group Plc Water Infra. & Supply Water Utilities 14.3% 14.5% Companhia de Saneamento de Minas Gerais Water Infra. & Supply Water Utilities 13.8% 14.0% SABESP Water Infra. & Supply Water Utilities 11.6% 11.7% Guangdong Investment Limited Water Infra. & Supply Water Utilities 11.5% 11.6% Enel Green Power S.p.A. Renewables Renewable Electricity 11.3% 11.6% Veolia Environnement SA Water Infra. & Supply Multi-Utilities 10.5% 10.7% Kemira Oyj Water Treatment Diversified Chemicals 10.1% 10.2% Severn Trent Plc Water Infra. & Supply Water Utilities 10.1% 10.2% GT Advanced Technologies Inc. LEDs & Lighting Semiconductor Equipment 10.0% 10.3% Vestas Wind Systems A/S Renewables Heavy Electrical Equipment 9.7% 9.9% SunPower Corporation Cleantech/Renewables Semiconductors 9.0% 9.7% Source: BofA Merrill Lynch Global Research. BofAML Thematic stock lists are not a recommended list either individually or as a group of stocks.

Themat ic Inves t ing 09 January 2015

23

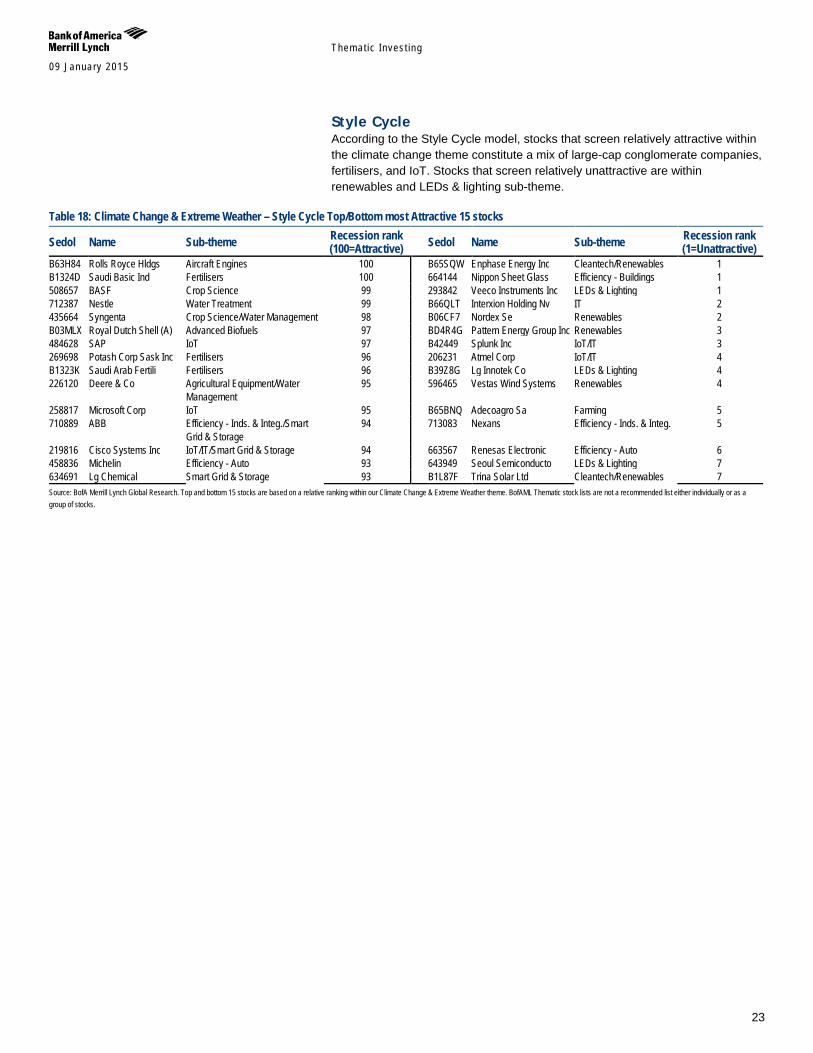

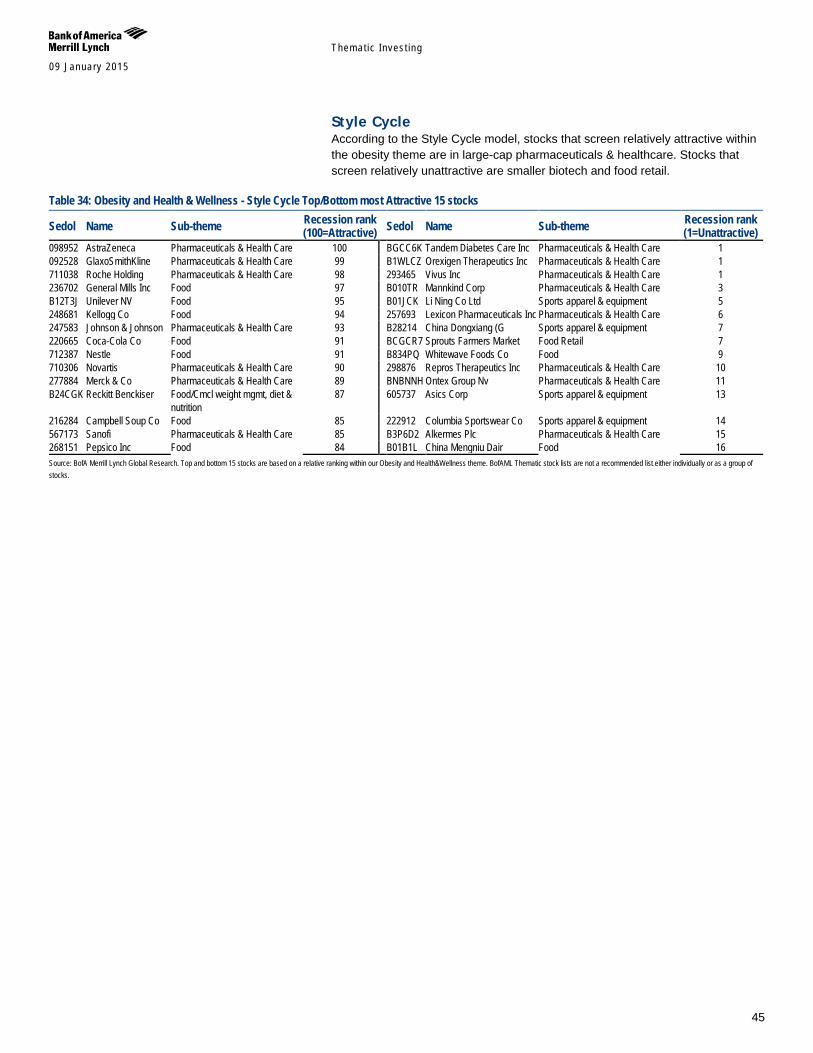

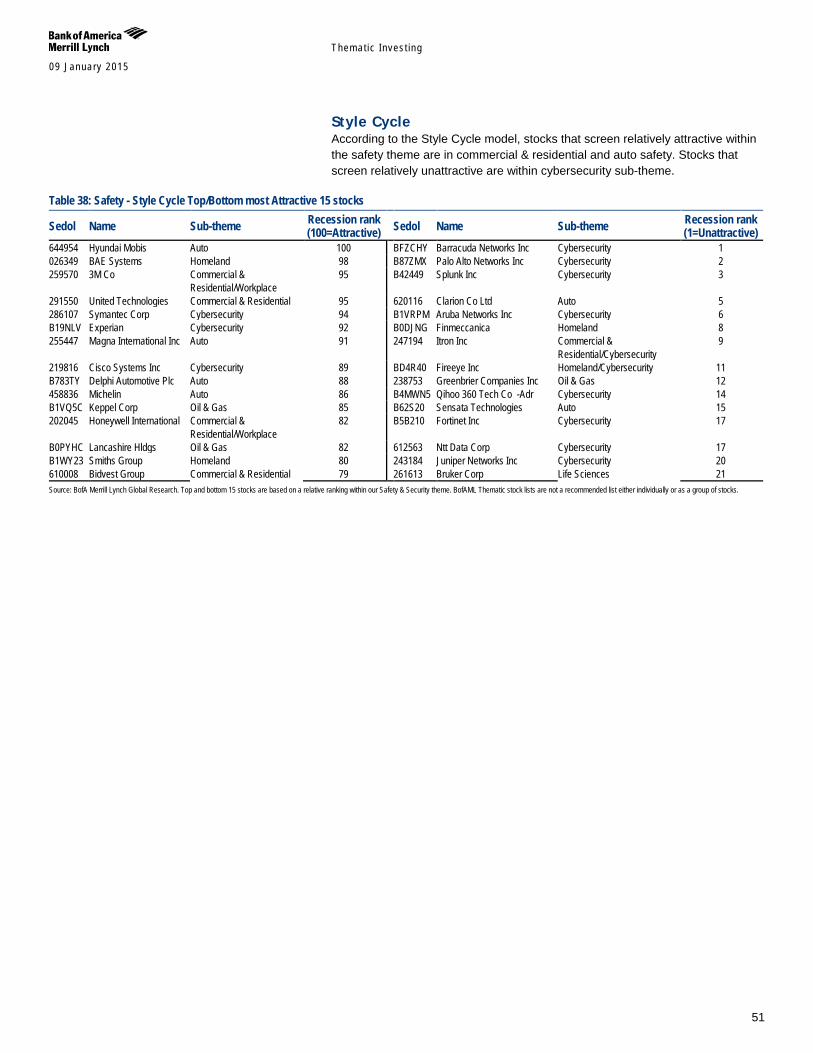

Style Cycle According to the Style Cycle model, stocks that screen relatively attractive within the climate change theme constitute a mix of large-cap conglomerate companies, fertilisers, and IoT. Stocks that screen relatively unattractive are within renewables and LEDs & lighting sub-theme.

Table 18: Climate Change & Extreme Weather – Style Cycle Top/Bottom most Attractive 15 stocks

Sedol Name Sub-theme Recession rank (100=Attractive) Sedol Name Sub-theme Recession rank

(1=Unattractive) B63H84 Rolls Royce Hldgs Aircraft Engines 100 B65SQW Enphase Energy Inc Cleantech/Renewables 1 B1324D Saudi Basic Ind Fertilisers 100 664144 Nippon Sheet Glass Efficiency - Buildings 1 508657 BASF Crop Science 99 293842 Veeco Instruments Inc LEDs & Lighting 1 712387 Nestle Water Treatment 99 B66QLT Interxion Holding Nv IT 2 435664 Syngenta Crop Science/Water Management 98 B06CF7 Nordex Se Renewables 2 B03MLX Royal Dutch Shell (A) Advanced Biofuels 97 BD4R4G Pattern Energy Group Inc Renewables 3 484628 SAP IoT 97 B42449 Splunk Inc IoT/IT 3 269698 Potash Corp Sask Inc Fertilisers 96 206231 Atmel Corp IoT/IT 4 B1323K Saudi Arab Fertili Fertilisers 96 B39Z8G Lg Innotek Co LEDs & Lighting 4 226120 Deere & Co Agricultural Equipment/Water

Management 95 596465 Vestas Wind Systems Renewables 4

258817 Microsoft Corp IoT 95 B65BNQ Adecoagro Sa Farming 5 710889 ABB Efficiency - Inds. & Integ./Smart

Grid & Storage 94 713083 Nexans Efficiency - Inds. & Integ. 5

219816 Cisco Systems Inc IoT/IT/Smart Grid & Storage 94 663567 Renesas Electronic Efficiency - Auto 6 458836 Michelin Efficiency - Auto 93 643949 Seoul Semiconducto LEDs & Lighting 7 634691 Lg Chemical Smart Grid & Storage 93 B1L87F Trina Solar Ltd Cleantech/Renewables 7 Source: BofA Merrill Lynch Global Research. Top and bottom 15 stocks are based on a relative ranking within our Climate Change & Extreme Weather theme. BofAML Thematic stock lists are not a recommended list either individually or as a group of stocks.

Themat ic Inves t ing 09 January 2015

24

Education - Stay in school One of the most pressing socio-economic challenges - We believe that education presents one of the most pressing socioeconomic challenges today, with 100m children never having attended school, tens of millions of dropouts, 800m illiterate adults, and major gaps in lifelong skills and training in both emerging and developed markets. We also believe that education for all (EFA) offers a once-in-a-generation investment opportunity to build healthy, prosperous and equitable societies, with every dollar invested in education generating US$10-15 in economic returns (source: UN).

US$4.5-5.1tn market today, US$5.9-7.8tn by 2017E - The global education sector is worth US$4.5-5.1tn today, encompassing K-12, post-secondary, corporate and government learning, e-learning, child care and language learning. Going forward, we see the fastest growth coming from e-learning and for-profit education, as well as from emerging markets’ increasing focus and spend (notably China and Brazil). By 2017E, global education is on target to become a US$5.9-7.8tn market (source: GSV Advisors, BofA Merrill Lynch estimates).

Strong growth drivers, EMs leading the way - Growth drivers include strong spending (c5% of global GDP), increasing enrolment rates (90% for primary completion, 71% for secondary enrolment), demographic opportunities (booming population of 5-17 year olds in EMs), more women in education, EMs upping their spend on education (disposable spending on education in China, India and Brazil is 10-13%), increasing global mobility, and a growing realisation of employment, earnings and economic development needs and opportunities (developed market graduates earn >US$1m more than high school dropouts over their lifetime).

Structural shifts, for-profit/private & EdTech - We believe the high cost of education is placing a burden on cash-strapped governments and households, which means increasing dependence on private spending (32% of funding for higher education in the OECD, 62% in the US), a growing role for for-profit education companies, and an increasing focus on affordability and results. Further, we think the integration of ICT and the shift to EdTech (from print to digital and from classroom to online learning) means e-learning is set to become a US$250bn+ market by 2017E, posing threats and opportunities for many incumbents.

Four major entry points for investors - We have mapped education across a number of sectors’ value chains to highlight the diverse range of entry points available to those wishing to invest in the theme: 1) K-12, 2) post-secondary, 3) content and 4) EdTech.

Thematic Investing: Global Education Primer - Stay in school 01 November 2013

Themat ic Inves t ing 09 January 2015

25

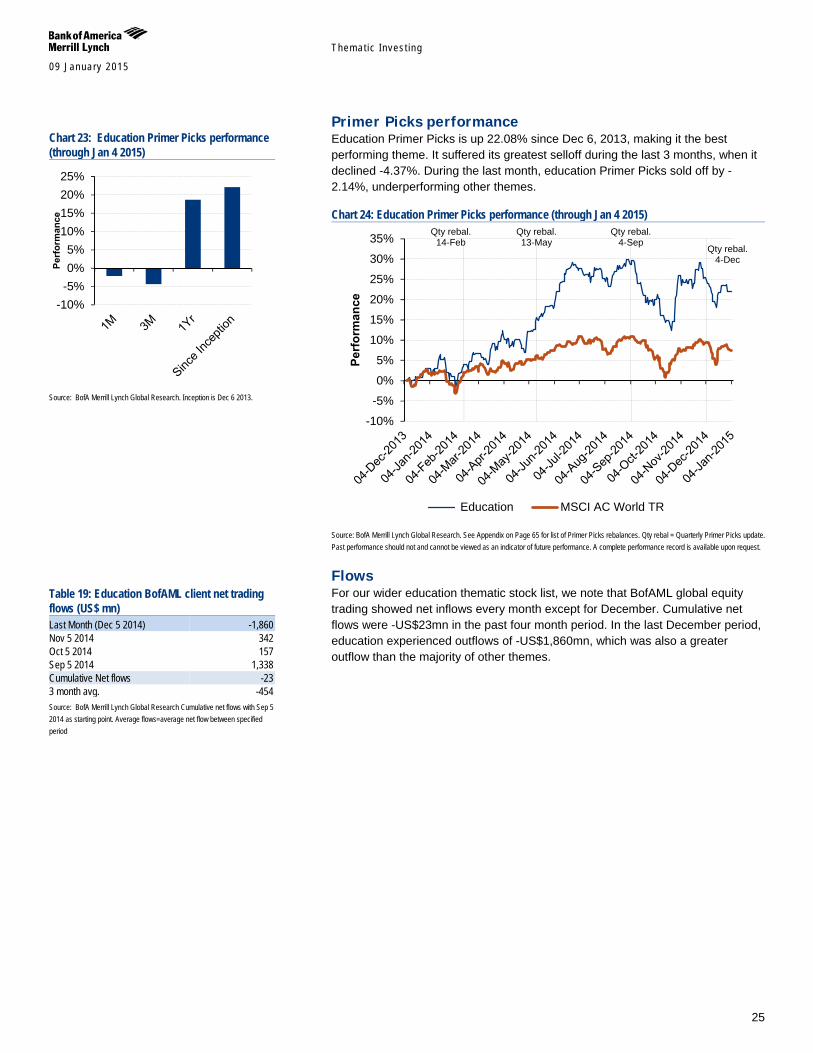

Primer Picks performance Education Primer Picks is up 22.08% since Dec 6, 2013, making it the best performing theme. It suffered its greatest selloff during the last 3 months, when it declined -4.37%. During the last month, education Primer Picks sold off by -2.14%, underperforming other themes.

Chart 24: Education Primer Picks performance (through Jan 4 2015)

Source: BofA Merrill Lynch Global Research. See Appendix on Page 65 for list of Primer Picks rebalances. Qty rebal = Quarterly Primer Picks update. Past performance should not and cannot be viewed as an indicator of future performance. A complete performance record is available upon request.

Flows For our wider education thematic stock list, we note that BofAML global equity trading showed net inflows every month except for December. Cumulative net flows were -US$23mn in the past four month period. In the last December period, education experienced outflows of -US$1,860mn, which was also a greater outflow than the majority of other themes.

Qty rebal. 14-Feb

Qty rebal. 13-May

Qty rebal. 4-Sep

Qty rebal. 4-Dec

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

Perf

orm

ance

Education MSCI AC World TR

Chart 23: Education Primer Picks performance (through Jan 4 2015)

Source: BofA Merrill Lynch Global Research. Inception is Dec 6 2013.

Table 19: Education BofAML client net trading flows (US$ mn) Last Month (Dec 5 2014) -1,860 Nov 5 2014 342 Oct 5 2014 157 Sep 5 2014 1,338 Cumulative Net flows -23 3 month avg. -454 Source: BofA Merrill Lynch Global Research Cumulative net flows with Sep 5 2014 as starting point. Average flows=average net flow between specified period

-10%-5%0%5%

10%15%20%25%

Perf

orm

ance

Themat ic Inves t ing 09 January 2015

26

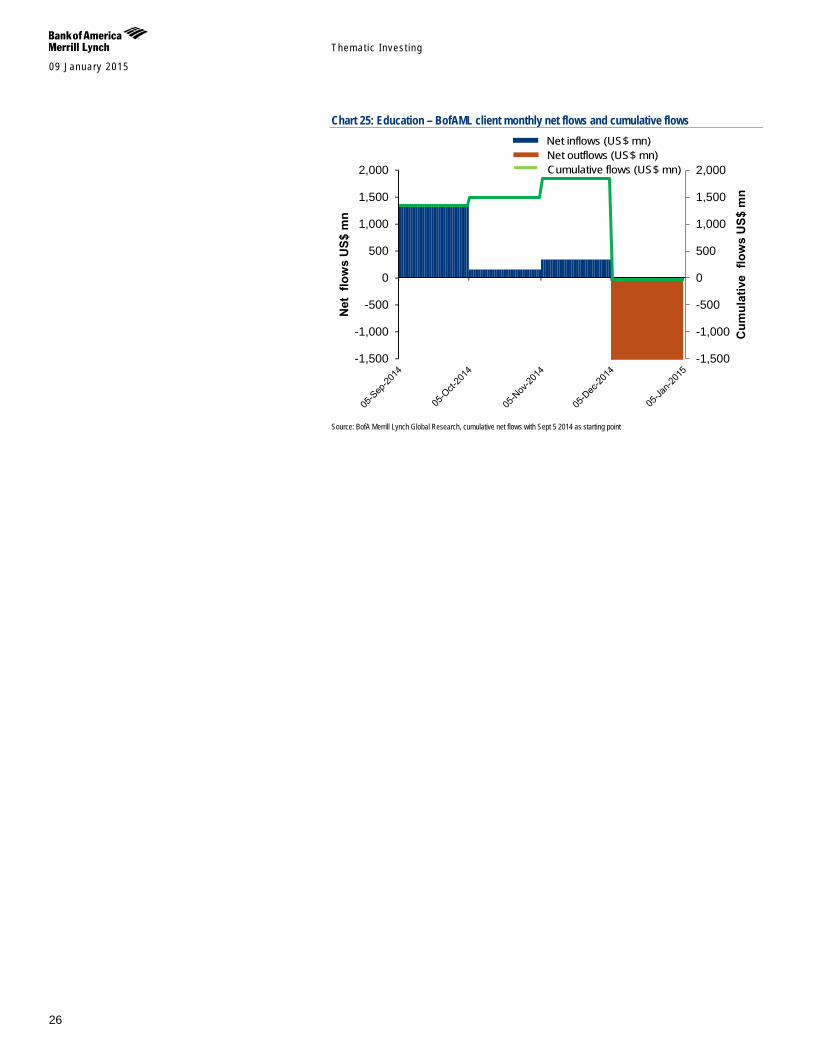

Chart 25: Education – BofAML client monthly net flows and cumulative flows

Source: BofA Merrill Lynch Global Research, cumulative net flows with Sept 5 2014 as starting point

-1,500

-1,000

-500

0

500

1,000

1,500

2,000

-1,500

-1,000

-500

0

500

1,000

1,500

2,000

Cum

ulat

ive

flow

s U

S$ m

n

Net

flo

ws

US$

mn

Net inflows (US$ mn)Net outflows (US$ mn)Cumulative flows (US$ mn)

09 January 2015

Them

atic Investing

27

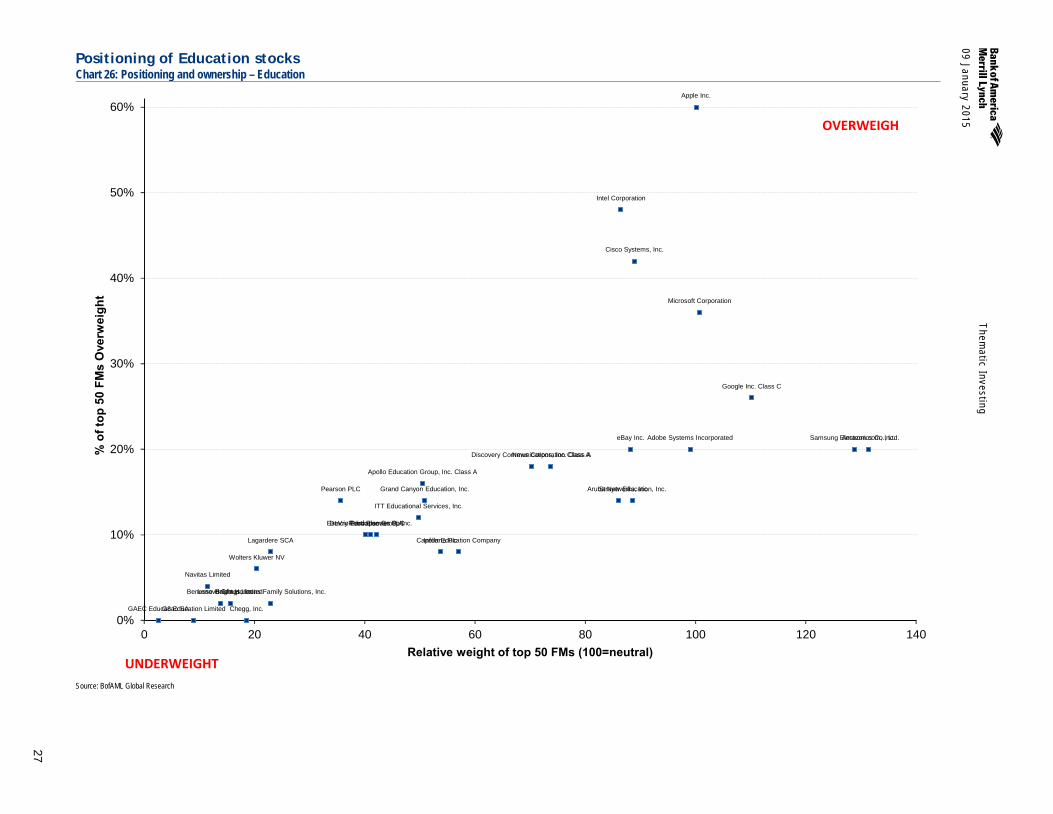

Positioning of Education stocks Chart 26: Positioning and ownership – Education

Source: BofAML Global Research

Adobe Systems Incorporated Amazon.com, Inc.

GAEC Educacao SA

Apollo Education Group, Inc. Class A

Apple Inc.

Aruba Networks, Inc.

Benesse Holdings, Inc. Bright Horizons Family Solutions, Inc.

Capella Education Company

Chegg, Inc.

Cisco Systems, Inc.

DeVry Education Group Inc.

Discovery Communications, Inc. Class A

eBay Inc.

Estacio Participacoes S.A.

G8 Education Limited

Google Inc. Class C

Grand Canyon Education, Inc.

Informa Plc

Intel Corporation

ITT Educational Services, Inc.

Lagardere SCA

Lenovo Group Limited

Microsoft Corporation

Navitas Limited

News Corporation Class A

Pearson PLC

Reed Elsevier PLC

Samsung Electronics Co., Ltd.

Strayer Education, Inc.

Wolters Kluwer NV

0%

10%

20%

30%

40%

50%

60%

0 20 40 60 80 100 120 140

% o

f top

50

FMs

Ove

rwei

ght

Relative weight of top 50 FMs (100=neutral)

OVERWEIGH

UNDERWEIGHT

Themat ic Inves t ing 09 January 2015

28

Positioning of Education stocks Investors are Overweight Edtech sub-theme, including digital and online learning. The biggest Underweight is K-12 & childcare.

Table 20: Top Overweight and Underweight stocks in Education Top Overweight Top Underweight

Weightings % top holders overweight Weightings % top holders

overweight Apple Inc. 100 60% GAEC Educacao SA 3 0% Intel Corporation 86 48% G8 Education Limited 9 0% Cisco Systems, Inc. 89 42% Chegg, Inc. 19 0% Microsoft Corporation 101 36% Benesse Holdings, Inc. 14 2% Google Inc. Class C 110 26% Lenovo Group Limited 16 2% Amazon.com, Inc. 131 20% Bright Horizons Family Solutions, Inc. 23 2% Samsung Electronics Co., Ltd. 129 20% Navitas Limited 11 4% Adobe Systems Incorporated 99 20% Wolters Kluwer NV 20 6% eBay Inc. 88 20% Informa Plc 54 8% Discovery Communications, Inc. Class A 70 18% Capella Education Company 57 8% Source: BofAML Global Research. BofAML Thematic stock lists are not a recommended list either individually or as a group of stocks.

Thematic and ESG Consensus positioning Thematic and ESG funds generally comprise a low percentage of holders within the Education theme. Out of those they do hold, they tend to be in educational publishing.

Table 21: Top 10 most invested stocks in Education (as % of SRI MV in total MW held by Mutual Funds) Name Sub-theme GICS Level 4 Top 500 ALL Informa Plc Publishing & content Publishing 3.0% 3.0% Benesse Holdings, Inc. K-12 & childcare/Publishing & content Education Services 2.6% 2.7% GAEC Educacao SA Post-secondary, Colleges & Universities Education Services 2.1% 2.4% Reed Elsevier PLC Publishing & content Publishing 1.5% 1.5% Pearson PLC Publishing & content Publishing 1.4% 1.5% Grand Canyon Education, Inc. Post-secondary, Colleges & Universities Education Services 0.7% 0.7% eBay Inc. Publishing & content Internet Software & Services 0.6% 0.6% Lagardere SCA Publishing & content Publishing 0.5% 0.5% Wolters Kluwer NV Publishing & content Publishing 0.4% 0.4% Discovery Communications, Inc. Class A Publishing & content Broadcasting 0.4% 0.4% Source: BofA Merrill Lynch Global Research. BofAML Thematic stock lists are not a recommended list either individually or as a group of stocks.

Themat ic Inves t ing 09 January 2015

29

Style Cycle According to the Style Cycle model, stocks that screen relatively attractive within the education theme are in large-cap Edtech and major publishing & content. Stocks that screen relatively unattractive are within sub-themes relating to post-secondary, colleges, & universities as well as K-12 & childcare.

Table 22: Education - Style Cycle Top/Bottom most Attractive 10 stocks

Sedol Name Sub-theme Recession rank (100=Attractive) Sedol Name Sub-theme Recession rank

(1=Unattractive) 677172 Samsung Electronic EdTech 100 BG6N6K Chegg Inc EdTech 1 067760 Pearson Publishing & content 96 B1VRPM Aruba Networks Inc EdTech 4 204369 Apollo Education Group Inc Post-secondary,

Colleges & Universities 89 B29631 G8 Education Ltd K-12 & childcare 7

219816 Cisco Systems Inc EdTech 89 200001 Amazon.Com Inc EdTech 11 204625 Apple Inc EdTech 86 200815 Adobe Systems Inc EdTech 14 258817 Microsoft Corp EdTech 82 B7MJWP Bright Horizons Family Soltn K-12 & childcare 18 BMJ6DW Informa Plc (Gb) Publishing & content 79 BBGVT4 News Corp Publishing & content 21 567151 Wolters Kluwer Publishing & content 75 285341 Strayer Education Inc Post-secondary,

Colleges & Universities 25

B2B0DG Reed Elsevier Publishing & content 71 B0GWDP Capella Education Co Post-secondary, Colleges & Universities

29

246324 Intel Corp EdTech 64 BFMXX8 Gaec Educacao S.A Post-secondary, Colleges & Universities

32

Source: BofA Merrill Lynch Global Research. Top and bottom 10 stocks are based on a relative ranking within our Education theme.. BofAML Thematic stock lists are not a recommended list either individually or as a group of stocks.

Themat ic Inves t ing 09 January 2015

30

Energy efficiency – Efficient frontier A Transforming World thematic impacts: Earth, Government, Innovation Global energy crisis: the current path is unsustainable - Primary energy demand accounts for more than 7% of global GDP, and with demand set to grow by up to 40% by 2035E, the world needs US$48-53tn in energy investments over the period (source: IEA). Today’s share of fossil fuels in the global energy mix is the same as it was 25Y ago, leaving much of the world dependent on energy imports and associated geopolitical risks. The current energy path is also putting us on a CO2 emissions trajectory consistent with long-term global temperature increases of 2.0°C -4.5°C, making irreversible climate change a reality.

Doing more with less: from hidden fuel to world’s #1 fuel - An energy-secure future for all will require a balanced energy mix, encompassing clean coal, gas, nuclear and renewables – as well as energy efficiency. Historical energy savings from efficiency have exceeded the output from any other single fuel source, and efficiency could halve the energy needed to power the world by 2035E (source: IEA). We believe that efficiency is the cheapest and easiest way to reduce energy demand and CO2 emissions, and that the combination of increasingly effective policies and high energy prices means that it will transition from hiding in plain sight to become the world’s “first fuel.”