the$northamericancarsharing$industry$ zipcar,$inc .... zip car... ·...

TRANSCRIPT

The North American Carsharing Industry Zipcar, Inc. and 3 Major Competitors

Susan Goldman -‐ May 2008

LIS4203 Liz Keating

The North American Carsharing Industry Zipcar, Inc. and 3 Major Competitors

Susan Goldman -‐ May 2008

2

Industry Profile

The principle of carsharing is simple: households and businesses gain the benefit of private vehicle use without bearing the costs and responsibilities of ownership. Generally, participants are required to pay a onetime or annual membership fee, and then pay a predetermined rate each time they use a vehicle. Carsharing is unique in that this “car rental” service is sold in hourly increments, includes gas and insurance, and is designed to fulfill a just-‐in-‐time need for personal access to passenger cars. The logistics for carsharing differ slightly among industry operators; however, the basic actions required of members are (1) reserve a car online or by phone, (2) walk to the designated carsharing parking space, (3) open the doors with an electronic device or code, (4) drive away, and (5) return one or several hours later and park in the same space.

Common Goals A major impact of carsharing is a reduction in vehicle ownership, although the industry does acknowledge that differences in data collection and study methodologies make it difficult to precisely measure to what degree this is the case. In 2006, U.S. and Canadian studies and member surveys suggest that 11% -‐ 26% of carsharing participants sold a personal vehicle after joining a carsharing program, and that 12% -‐ 68% avoided or postponed a planned vehicle purchase (Sheehan, Cohen & Roberts). These wide-‐ranging metrics aside, it can be said that carsharing organizations in North America share four common goals:

Transportation -‐ reducing congestion and auto ownership Environmental -‐ reducing emissions by lowering overall vehicle miles traveled and using clean fuel vehicles (gasoline-‐electric hybrid cars) Land use – reducing the number of parking spaces needed Social effects – gaining or maintaining vehicle access without bearing the full costs of auto ownership; increasing mobility options of low-‐income households and college students, and increasing connectivity among transportation modes

Geographic Market Carsharing became popularized in Europe in the mid-‐1980s and by the mid-‐1990s this interest had migrated to North America, with start up operations in several major U.S. and Canadian urban cities. The industry peaked early at 40 operators; although the current market has adjusted itself to 31 carsharing programs, with 18 in the U.S. and 13 in Canada, representing combined coverage in about 100 cities. Most are privately held and organized as non-‐profit entities, although there are a few for-‐profit operations, including several co-‐operatives. There are an estimated 8,000 vehicles in North American carsharing fleets, plus an estimated 500 vehicles on college and university campuses. Direct competition among major operators exists in about 10% of these cities (Brook, 2008).

The North American Carsharing Industry Zipcar, Inc. and 3 Major Competitors

Susan Goldman -‐ May 2008

3

Who is Attracted to Carsharing? Individuals attracted to carsharing are generally residents of dense urban areas where public transit, walking, and cycling are viable transportation options, parking pressures prevail (space and cost), and residents do not necessarily require cars to go about their daily activities. Low vehicle ownership rates are one of the best predictors of the economic viability of carsharing programs. Over 80% of North America’s carsharing membership is comprised of people who live in this residential demographic, followed by significantly smaller percentages in business, college, and low-‐income groups. To indentify and understand what common points draw people to carsharing, recent industry studies and surveys analyzed existing users by three key attributes: demographic characteristics, shared attitudes about environmental and social concerns, and behaviors pertaining to how members use carsharing. From this data, the following customer snapshot was created.

Demographic characteristics Age: mean age late 30’s Income: household income 50% $60,000-‐$100,000; 18% > $100,000; 13% < $30,000 Education: highly educated (excludes college members), 35% bachelors; 48% post graduate Gender: 50% male; 50% female Race and ethnicity: 87% white or Caucasian; 6% Asian; 4% black; 3% Hispanic Household size: 64% two or more occupants; 36% single occupant Auto ownership: 72% households with no cars (no data on single car ownership) Shared attitudes – Based on users’ responses to specific questions, five model user personalities were identified. Correlations were made between these personality types and demographic characteristics of age and income (Burkhardt & Millard-‐Ball, 2006). Social activists: 90% agreed “It’s my responsibility to help create a better world.”

Environmental protectors: 88% agreed “I am very concerned about environmental issues.” Innovators: 86% agreed “I like to try out new ideas.” Economizers: 82% agreed “Saving money is important to me.” Practical traveler: 17% agreed “The car I drive is an important reflection of my personality”

Behaviors – Respondents were asked “For which of your trips do you feel that you really need to travel by car (personal, carsharing or rental)? Their responses in order of ranked importance: recreation and social trips, other shopping, grocery shopping, personal business, and meeting clients and other work-‐related. Other reasons given included, transporting family and friends, moving furniture, hauling or picking up large loads, and medical appointments. Industry Resources No formal North American carsharing association has been established, although there are several respected online discussion forums at which people involved in the carsharing industry routinely exchange industry knowledge, insights, conference highlights, and other information

The North American Carsharing Industry Zipcar, Inc. and 3 Major Competitors

Susan Goldman -‐ May 2008

4

of interest to followers of the carsharing industry. The Journal of the Transportation Research Record is a frequent publisher of articles and studies written by various field experts, as is the Institute for Transportation Studies, University of California Davis. These and other selected references are included at conclusion of this report. Additionally, several U.S. and Canadian operators have joined to draft a code of ethics, professional business standards that will protect and enhance the concept and credibility of carsharing. Industry Outlook The consensus of industry research about the residential demographic identifies primary motivations for joining a carsharing organization as the desire to save money, concerns about environmental issues, the convenience of not owning a car (or a second car), and changes in one’s personal life situation. This last item speaks to the observation that very few people actually sell a vehicle and join a carsharing organization when they first hear about carsharing; typically it takes some economic or social disruption in normal routine for carsharing membership to be considered as a replacement for vehicle ownership. While the residential market remains the staple demographic market in North America, many operators are pursuing opportunities to increase individual and organizational memberships through third party collaborations. In 2006, business markets accounted for approximately 12% of U.S. memberships, and colleges a 5% share. These U.S. markets are on the rise in several key markets, and industry forecasts predict the business and college segments will each reach close to 23%, by 2011.

Competitive Assessment

Zipcar, Inc. a Cambridge, Massachusetts company is a leader in the North American carsharing industry with 200,000 members in 50 markets in the U.S., Europe, and Canada. Zipcar’s membership is concentrated across residential, business, and college markets. In an ongoing effort to increase membership, increase asset utilization, and strengthen Zipcar’s overall position in the North American carsharing industry, top management has set two critical goals:

1) Attract new customers from within Zipcar’s existing demographic and geographic markets across the United States.

2) Identify new opportunities through which customer growth may be achieved, including partnerships with other service providers, local governments, communities, and other organizational affiliations.

In support of these goals, Zipcar and three carsharing industry competitors have been profiled and a SWOT analysis prepared for each. The competitors: Co-‐operative Auto Network, PhillyCarShare, and U Car Share were selected for two reasons, (1) their operations reflect major markets in which Zipcar currently competes -‐ residential, college, and business; and (2) they represent three organizational types common in the carsharing industry -‐ multiple locations, non-‐profit, and car rental.

The North American Carsharing Industry Zipcar, Inc. and 3 Major Competitors

Susan Goldman -‐ May 2008

5

Zipcar “Wheels When You Want Them” Corporate Headquarters: Cambridge, MA www.zipcar.com

• History: Established in 1999 by Robin Chase and Antje Danielson (both left pre 2003)

• Current leadership: Scott Griffith, Chairman and CEO (2003); Mark Norman, President and Chief Operating (2007); Edward Goldfinger, CFO (2007)

• Vision: “Providing reliable and convenient access to on-‐demand transportation, complementing other means of mobility.”

• Major markets: Residential, Business, College/University (70 schools, projected 140 campuses by fall 2008)

• Locations: 50 cities including Atlanta, Boston, Chicago, London, New York, Philadelphia, Pittsburgh, Portland, San Francisco, Seattle, Toronto, Vancouver and Washington DC. Complete listing www.zipcar.com/find-‐cars/

• Operations Organization: for-‐profit, privately held

Revenue: $100 million (2007)

Employees: 200

Membership: 180,000 -‐ 200,000; member to car ratio 40:1 (estimated)

Cars: 5,000 vehicles, 20 makes and models, 1-‐2 yrs old, fleet consists of hybrids SUVs, pickup trucks, sedans and high-‐end vehicles e.g. the Mini Cooper and BMW

November 2007 acquired Flexcar, Inc. 2nd largest U.S. carsharing company, absorbing assets, customers, and operations in 25 cities

• Membership Requirements: eligibility -‐ 21 yrs (18 yrs college), valid license for 1 yr, meet driving record requirements; fees -‐ $25 one-‐time application, $50 annual, no surcharge for under 25 yrs

Rates: Basic -‐ $8 per hour or $60 per day in smaller markets such as Ann Arbor to about $10.50 per hour or $73 per day in New York City. Extra Value – no annual fee, $50-‐$250 monthly fee, 10% discount on hourly/daily; high-‐end cars premium rate. Business – discounts depending on number of driver and 7am-‐7pm rates. All plans include, gas, maintenance and insurance; and 180 free miles per day

Access: 24/7, reserve online/phone specific car/location, personal Zipcard unlock, return to same location; reservations may be extended, gas card provided (see how-‐to video http://www.zipcar.com/how/ )

Customer service: Google map car/location mashup, email, 24/7 phone, online chat, comprehensive online FAQs

The North American Carsharing Industry Zipcar, Inc. and 3 Major Competitors

Susan Goldman -‐ May 2008

6

Co-‐operative Auto Network (CAN) “Driving Change” Corporate Headquarters: Vancouver, BC, Canada http://www.cooperativeauto.net/

• History: Established 1997 by Tracy Axelsson, with 16 members and 2 cars; North America’s second oldest car cooperative

• Current leadership: Tracy Axelsson, Executive Director

• Vision: “We believe CAN is an environmentally responsible and economically sound choice for many people's mobility needs. Through car sharing we aim to improve air quality, reduce stresses on green space and eliminate many non-‐point sources of pollution.”

• Locations: British Columbia -‐ Vancouver, Burnaby, North Vancouver, New Westminster, Courtenay, Whistler, Nanaimo, Tofino, and Cortes Island

• Major markets: Residential and Business

• Operations Organization: co-‐operative

Revenue: undisclosed

Employees: 10

Membership: 2000; member to car ratio 20:1 (estimated)

Cars: 113 vehicles, hatchbacks, sedans, minivans, and pickup trucks

• Membership Requirements: eligibility – valid license for 3 yrs, meet driving record requirements; fees -‐ one-‐time refundable share of $500 (members are co-‐op owners), $500-‐$1000 for businesses; $20 registration; or No Deposit plan $50 annual fee

Rates: Low/Med/High usage plans, $6 -‐ $40 monthly plus $2.50/hr and $0.18 -‐ $0.38 per kilometer. No charge $0 if zero usage in a month; free overnight for business users; individual No Deposit plan $7. All plans include gas and maintenance.

Access: 24/7, reserve online/phone specific car/location, lockbox key to access vehicle key, return to same location, manually record mileage in car log, gas receipt for reimbursement

Customer service: Google map car/location mashup, email, 24/7 phone, comprehensive online FAQs

The North American Carsharing Industry Zipcar, Inc. and 3 Major Competitors

Susan Goldman -‐ May 2008

7

PhillyCarShare “Our Wheels. Your Freedom” Corporate Headquarters: Philadelphia, PA http://www.phillycarshare.org/

• History: Established 2002 by five volunteers, their $23,000 personal contribution, nine members, and two cars – a Prius and a Matrix wagon; one year later there were 535 members sharing 13 environmentally-‐friendly cars (who gave up 270 personal vehicles)

• Current leadership: Tanya Seaman, Executive Director (co-‐founder); Clayton Lane, AICP, Deputy Executive Director (co-‐founder)

• Mission: “To maximize the economic, environmental, and social benefits of reduced automobile dependence in the Philadelphia region through community-‐based car sharing”

• Locations: Philadelphia and Wilmington, DE – over 200 neighborhood locations; over 13 college campuses; no information available about business share

• Major markets: Residential, Business, College/University

• Operations Organization: non-‐profit

Revenue: $10 million

Employees: 45

Membership: 35,000

Cars: unable to determine fleet size, 20 makes and models; hybrids (>50% fleet) minivans, pickup trucks, sedans and high-‐end vehicles e.g. Mini Cooper and BMW

April 2004, the City of Philadelphia became the first government worldwide to share cars with local residents in a major fleet reduction effort.

January 2008, PhillyCarShare and the University of PA launch the largest university carsharing program in North America, deploying 40 vehicles on or near campus.

• Membership Requirements: eligibility – 18 yrs, valid license for 2 yrs, meet driving record requirements; fees -‐ none

Rates: Basic -‐ $4/hr or $40/day to $5/hr and $50/day; Freedom $6/hr or $50/day to $8/hr and $60/day; high-‐end cars premium rate. Business – similar rates, discounts depending on number of drivers. All plans include, gas, maintenance and insurance; and 210 free miles per day.

Access: 24/7, reserve online/phone specific car/location, personal key fob unlock, return to same location; reservations may be extended, gas card provided

Customer service: Google map car/location mashup, email, 24/7 phone, online chat, comprehensive online FAQs

The North American Carsharing Industry Zipcar, Inc. and 3 Major Competitors

Susan Goldman -‐ May 2008

8

U Car Share “Sustainability in Motion” Corporate Headquarters (U-‐Haul International): Phoenix, AZ https://www.ucarshare.com/

• History: Established June 2007

• Current leadership: Edward Shoen, CEO U-‐Haul Intl Mark Shoen, President U-‐Haul Intl, Michael Coleman, Program Manager

• Mission: “U Car Share is an alternative to car ownership, allowing you access to a vehicle by the hour without the hassles of gas, insurance, parking fees and maintenance costs.”

• Locations: 26 U-‐Haul Centers in Ann Arbor, Boston, Chicago, Madison, Philadelphia, Portland, San Francisco, Seattle, and Washington D.C.

• Major markets: Business, Individual

• Operations Organization: for-‐profit

Revenue: $2 billion U-‐Haul International, no data U Car Share

Employees: U-‐Haul center staffing

Membership: unable to determine

Cars: 160 Chrysler PT Cruisers

• Membership Requirements: eligibility – 18 yrs, valid license, meet driving record requirements; fees -‐ $25 one-‐time application, $50 annual

Rates: $10/hr or $65/day; $30 7:00 pm to 7:00 am. All plans include gas, maintenance and insurance; and 125 free miles per day.

Access: pickup only when U-‐Haul center is open generally 7:00am – 7:00 pm; reserve by email request or phone specific car/location, pick up key to access car, return to same location; reservations may be extended by phone, gas card provided

Customer service: email, 24/7 phone

The North American Carsharing Industry Zipcar, Inc. and 3 Major Competitors

Susan Goldman -‐ May 2008

9

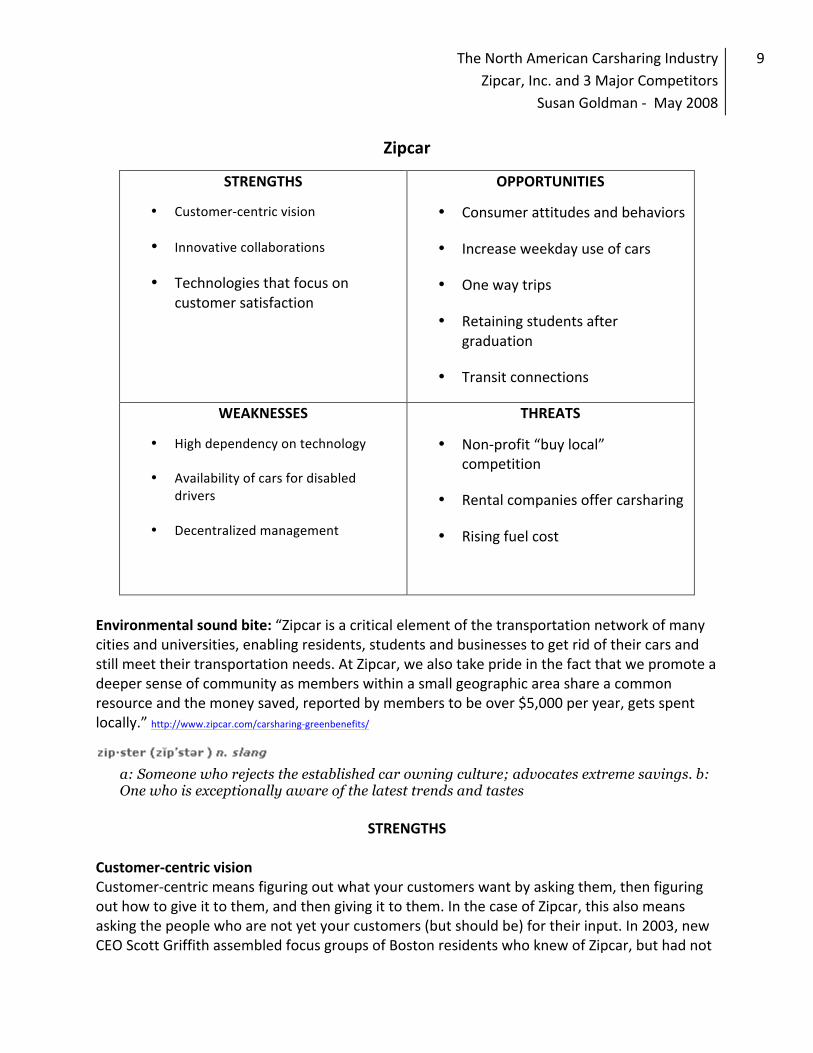

Zipcar

STRENGTHS

• Customer-‐centric vision

• Innovative collaborations

• Technologies that focus on customer satisfaction

OPPORTUNITIES

• Consumer attitudes and behaviors

• Increase weekday use of cars

• One way trips

• Retaining students after graduation

• Transit connections

WEAKNESSES

• High dependency on technology

• Availability of cars for disabled drivers

• Decentralized management

THREATS

• Non-‐profit “buy local” competition

• Rental companies offer carsharing

• Rising fuel cost

Environmental sound bite: “Zipcar is a critical element of the transportation network of many cities and universities, enabling residents, students and businesses to get rid of their cars and still meet their transportation needs. At Zipcar, we also take pride in the fact that we promote a deeper sense of community as members within a small geographic area share a common resource and the money saved, reported by members to be over $5,000 per year, gets spent locally.” http://www.zipcar.com/carsharing-‐greenbenefits/

a: Someone who rejects the established car owning culture; advocates extreme savings. b: One who is exceptionally aware of the latest trends and tastes

STRENGTHS

Customer-‐centric vision Customer-‐centric means figuring out what your customers want by asking them, then figuring out how to give it to them, and then giving it to them. In the case of Zipcar, this also means asking the people who are not yet your customers (but should be) for their input. In 2003, new CEO Scott Griffith assembled focus groups of Boston residents who knew of Zipcar, but had not

The North American Carsharing Industry Zipcar, Inc. and 3 Major Competitors

Susan Goldman -‐ May 2008

10

signed up. He learned that they perceived carsharing as inconvenient or unreliable in terms of a car being available when they needed one. He realized that they were not entirely wrong about this, that Zipcar did need to restructure their car placement to assure access. This valuable input was the start of what would become Zipcar’s standard practice of dividing neighborhoods into zones and creating “pods” of Zipcars (clusters of cars within a garage) to more accurately meet customers’ needs for cars. Customer-‐centric also means innovating on behalf of customers, figuring out what they don’t know they want and giving it to them. Noting that the average age of Zipcar members was rising, Zipcar expanded the fleet with high-‐end black BMWs and cool red MINI Coopers. For this “out to impress” demographic, Zipcar wisely opted to leave off the big green Zipcar logo typically displayed on the car door. Customers appreciated the cars and the discretion. Zipcar also recognized other purposeful niches, and added and promoted cars to fit specific needs, such as four wheel-‐drives for trips to the mountains, pickup trucks for DIY weekend activities, and minivans for taking family and gear to the beach for the day. Technologies that focus on customer satisfaction Zipcar’s values focus on convenience, selection, service, and value. Zipcar is successful because of its clearly defined purpose that aims at high quality customer services. Zipcar delivers a quality service to a diverse membership, and one thing that guarantees both the delivery and the enjoyment of this service is the technology that supports it. Zipcar follows the adage “before you get big, get tech.” Customers see and enjoy the benefit of the front-‐end systems that drive Zipcar, the online reservations, the electronic keycard for secure access, and automated billing systems. However, they probably do not know about the in-‐car computers that track and automatically send readings back to Zipcar wirelessly, assuring proactive and timely maintenance that means customers will not be delayed or disappointed when they use any Zipcar. Zipcar was also an early adapter of mashup technology within its reservation system. From the Zipcar Web site, users can find cars “pinned” to a neighborhood map of any Zipcar market, and then drill down to find out where the car is located, rates, and what cars are in the same pod. Innovative collaborations Among Zipcars business partnerships is their presence on over 70 college and university campuses nationwide. Initially Zipcar offered free memberships to students at Harvard and MIT in exchange for on-‐campus Zipcar parking and marketing help from the schools. Limiting car ownership and parking on campus is typical for most schools, and in 2005 Zipcar realized the potential for a new market. Initially Zipcar got the colleges to pay for insurance, but the big entry into this new market was Zipcar’s partnering with Liberty Mutual Insurance to create affordable insurance coverage, and service the under-‐21 drivers (a group deemed riskier by insurance companies). In January 2008, Zipcar lowered the college program minimum age to 18, thus increasing the pool of potential members. Zipcar has also partnered with office and apartment buildings to place Zipcar pods in their parking facilities , and customized the reservation and billing systems so that office managers could have maintain control and charge services back to departments and individuals.

The North American Carsharing Industry Zipcar, Inc. and 3 Major Competitors

Susan Goldman -‐ May 2008

11

WEAKNESSES

High dependency on technology Zipcar depends on technology for all aspects of its operations: reservations, maintenance, billing, and customer service. While this is integral to the seamless flow of operations and to maintaining high customer satisfaction, the downside is that if technology fails them -‐ Web site goes down, business systems become corrupted, power failure occurs, hackers breach security or other technological catastrophes -‐ Zipcar’s ability to do business goes down as well. Protection through backups, contingency plans, and disaster recovery plans is critical. Availability of cars for disabled drivers Recently Zipcar made accommodations for its disabled members, by which with 24-‐hour notice hand controls can be added to some Zipcars. The only mention of this service appears as a small item buried among the FAQs. This option may be perceived as impractical and/or insufficient by some Zipcar member and prospective members. Additionally, the lack of Web site visibility or other promotion of it may be a detrimental to attracting new members. Decentralized management Zipcar operates in 21 major markets, each of which is run by a general manager and local staff. Although Zipcar has strong leadership at the top, and well documented policies and procedures as a framework for local operations, issues may arise from being spread out. Lack of direct contact and local cultures can lead to divergence from corporate direction.

OPPORTUNITIES

Consumer attitudes and behaviors Market segmentation identifies distinct groups of customers who share specific characteristics and are likely to exhibit similar purchasing behavior. Recent carsharing studies, along with surveys and unsolicited feedback from Zipcar’s membership support the belief that carsharing members tend to have strong views about a variety of environmental and social concerns. They also like to save money and are motivated by convenience. These characteristics work together (an ATM and a Starbucks on every corner) and they are critical to Zipcar’s attracting more customers. Zipcar knows its customers and its Web site contains a wealth of information about their services, along with various tools and testimonials to help potential users to decide “is Zipcar for me?” The key is getting the right people to visit Zipcar’s Web site. Zipcar is a recognized brand with those who use it, but is it with non-‐members? Most people do not pay attention to information until they have a need for it, or perhaps observe others benefiting from it. Very few people actually sell a vehicle and join a carsharing organization when they first hear about carsharing. There has to be a trigger, some economic or social interruption that creates a need, or at least the need for information about carsharing – Zipcar. Using demographics and promoting Zipcar in proximity to the things that get consumers thinking about it is critical.

The North American Carsharing Industry Zipcar, Inc. and 3 Major Competitors

Susan Goldman -‐ May 2008

12

Increase weekday use of vehicles Zipcars are used heavily at night and on weekends, and many are idle during the day. Scott Griffith calculated for Zipcar to make money on a vehicle it needs to be in use more than 40 percent of the time. This statistic is the impetus for finding ways in which to increase daytime use of Zipcar’s assets. One area of exploration is attracting customers through the organizations that operate during the day and already own fleets or depend on employees to provide transportation to accomplish their work. This could include municipal services and other government workers, as well as visiting care services (nurse, meals, and therapy). One-‐way travel between cities and designating cars for longer distances Through evaluating the driving patterns of its members, and listening to their feedback, Zipcar understands there is a market for, or at least interest in, one-‐way travel between cities and/or designating cars (and pricing structure) for longer distance driving. This opportunity bears exploration, subject to the consideration of several points. Is there enough consumer demand to sustain such a market and justify applying the resources required to develop and support it? What are the logistics and risks associated with managing cars that are not automatically returned to their home parking location? Zipcar has always been about short-‐term access, so would adding longer-‐term options to the service mix be moving too far from organizational purpose? Or is it a move toward creating new or lifetime memberships through greater service usability? Retaining students after graduation Zipcar’s established and growing presence on college and university campuses is creating Zipcar fans at a young age. It is a demographic that tends to take action when it comes to environmental and social issues, plus they are innovators and experimenters drawn to cultural trends (like carsharing). The students at universities are really part of the self-‐service economy, and so the self-‐service model that Zipcar has really fits in line with that generation. Although buying a new car is a traditional rite of passage after graduation, those students who experienced Zipcar on campus will hopefully change their mindset to where car-‐sharing is a new alternative to car ownership." Transit connections In Boston Zipcars are strategically parked near subway stations in the city giving members access to cars so that they may continue their journeys to locations not reachable by public transportation. Carsharing industry research supports that the transit connections niche is not fully served, that there is opportunity for growth in this segment. Additionally, Zipcars parked at subway, bus, or train stations outside the downtown area may attract new members.

The North American Carsharing Industry Zipcar, Inc. and 3 Major Competitors

Susan Goldman -‐ May 2008

13

THREATS

Nonprofit “buy local” competition After merging with Flexcar six months ago, Zipcar now competes in 50 markets in the U.S. and Canada, and competes directly with city-‐wide nonprofits in at least 9 markets. These operators, particularly larger operations like PhillyCarShare and I-‐Go (Chicago), bring a unique set of competitive factors related to their close ties at city and community levels. Their grassroots operations and nonprofit status may inadvertently make them the preferred choice for businesses seeking carsharing services. Rental companies offer carsharing In 2008, a few of the car rental companies made small entries into the carsharing marketplace. U Car Share in 26 cities, all operating out of existing U-‐Haul centers, Hertz in Boston, and Enterprise’s WeCar in St. Louis. Generally speaking, their advantage comes from economies of scale that is creating a niche business that is not too far removed from their core business, and takes advantage of existing facilities, expertise, and financial support. So far none have made outstanding inroads, in fact the access to their services and vehicles tends to be inconvenient, but that may change as the rental companies learn the carsharing business. Rising fuel cost This economic burden could result in Zipcar raising rates to cover their gasoline expense. And while this may not cause current customers to terminate their memberships, they may decide to reduce their Zipcar use, opting instead to use less costly transportation options or share rides. Higher rates may also deter new members from joining Zipcar.

The North American Carsharing Industry Zipcar, Inc. and 3 Major Competitors

Susan Goldman -‐ May 2008

14

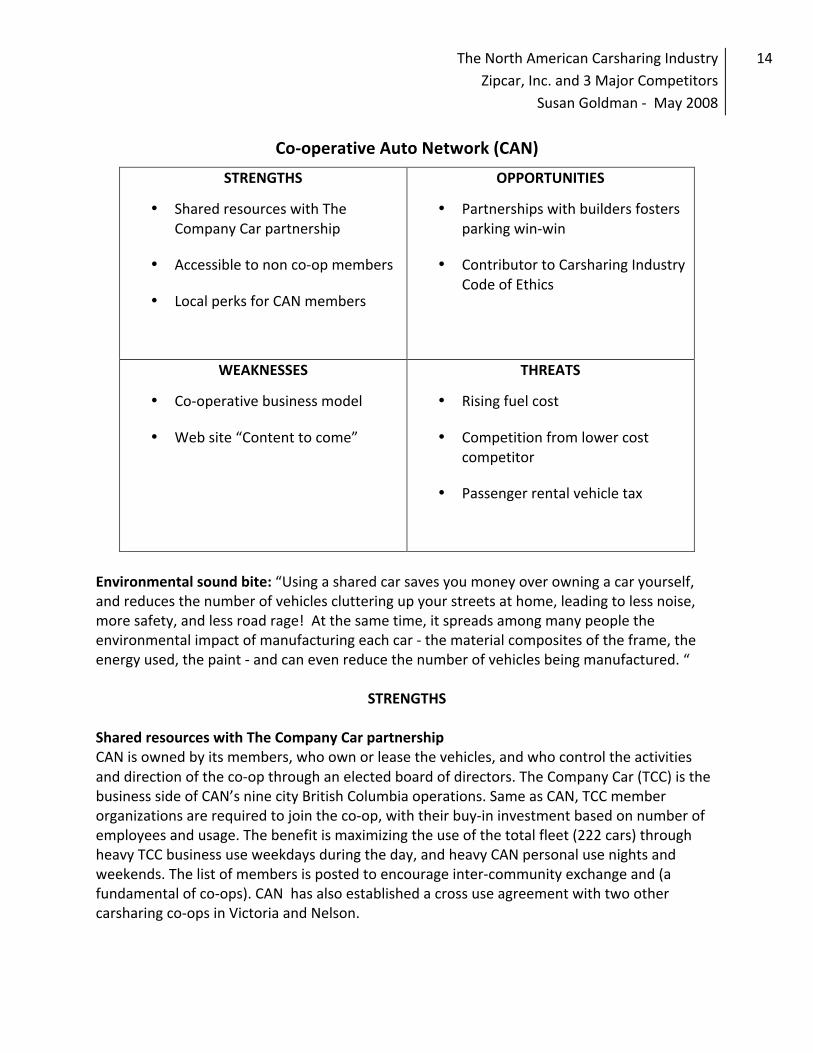

Co-‐operative Auto Network (CAN)

STRENGTHS

• Shared resources with The Company Car partnership

• Accessible to non co-‐op members

• Local perks for CAN members

OPPORTUNITIES

• Partnerships with builders fosters parking win-‐win

• Contributor to Carsharing Industry Code of Ethics

WEAKNESSES

• Co-‐operative business model

• Web site “Content to come”

THREATS

• Rising fuel cost

• Competition from lower cost competitor

• Passenger rental vehicle tax

Environmental sound bite: “Using a shared car saves you money over owning a car yourself, and reduces the number of vehicles cluttering up your streets at home, leading to less noise, more safety, and less road rage! At the same time, it spreads among many people the environmental impact of manufacturing each car -‐ the material composites of the frame, the energy used, the paint -‐ and can even reduce the number of vehicles being manufactured. “

STRENGTHS

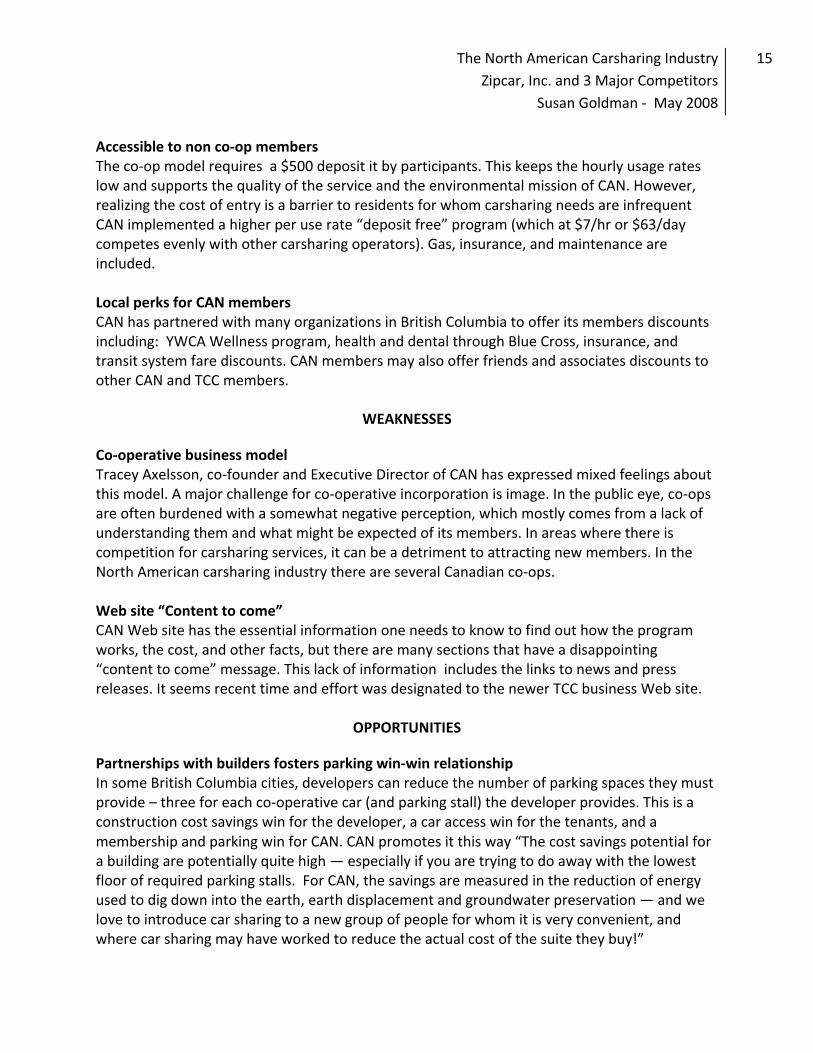

Shared resources with The Company Car partnership CAN is owned by its members, who own or lease the vehicles, and who control the activities and direction of the co-‐op through an elected board of directors. The Company Car (TCC) is the business side of CAN’s nine city British Columbia operations. Same as CAN, TCC member organizations are required to join the co-‐op, with their buy-‐in investment based on number of employees and usage. The benefit is maximizing the use of the total fleet (222 cars) through heavy TCC business use weekdays during the day, and heavy CAN personal use nights and weekends. The list of members is posted to encourage inter-‐community exchange and (a fundamental of co-‐ops). CAN has also established a cross use agreement with two other carsharing co-‐ops in Victoria and Nelson.

The North American Carsharing Industry Zipcar, Inc. and 3 Major Competitors

Susan Goldman -‐ May 2008

15

Accessible to non co-‐op members The co-‐op model requires a $500 deposit it by participants. This keeps the hourly usage rates low and supports the quality of the service and the environmental mission of CAN. However, realizing the cost of entry is a barrier to residents for whom carsharing needs are infrequent CAN implemented a higher per use rate “deposit free” program (which at $7/hr or $63/day competes evenly with other carsharing operators). Gas, insurance, and maintenance are included. Local perks for CAN members CAN has partnered with many organizations in British Columbia to offer its members discounts including: YWCA Wellness program, health and dental through Blue Cross, insurance, and transit system fare discounts. CAN members may also offer friends and associates discounts to other CAN and TCC members.

WEAKNESSES

Co-‐operative business model Tracey Axelsson, co-‐founder and Executive Director of CAN has expressed mixed feelings about this model. A major challenge for co-‐operative incorporation is image. In the public eye, co-‐ops are often burdened with a somewhat negative perception, which mostly comes from a lack of understanding them and what might be expected of its members. In areas where there is competition for carsharing services, it can be a detriment to attracting new members. In the North American carsharing industry there are several Canadian co-‐ops. Web site “Content to come” CAN Web site has the essential information one needs to know to find out how the program works, the cost, and other facts, but there are many sections that have a disappointing “content to come” message. This lack of information includes the links to news and press releases. It seems recent time and effort was designated to the newer TCC business Web site.

OPPORTUNITIES

Partnerships with builders fosters parking win-‐win relationship In some British Columbia cities, developers can reduce the number of parking spaces they must provide – three for each co-‐operative car (and parking stall) the developer provides. This is a construction cost savings win for the developer, a car access win for the tenants, and a membership and parking win for CAN. CAN promotes it this way “The cost savings potential for a building are potentially quite high — especially if you are trying to do away with the lowest floor of required parking stalls. For CAN, the savings are measured in the reduction of energy used to dig down into the earth, earth displacement and groundwater preservation — and we love to introduce car sharing to a new group of people for whom it is very convenient, and where car sharing may have worked to reduce the actual cost of the suite they buy!”

The North American Carsharing Industry Zipcar, Inc. and 3 Major Competitors

Susan Goldman -‐ May 2008

16

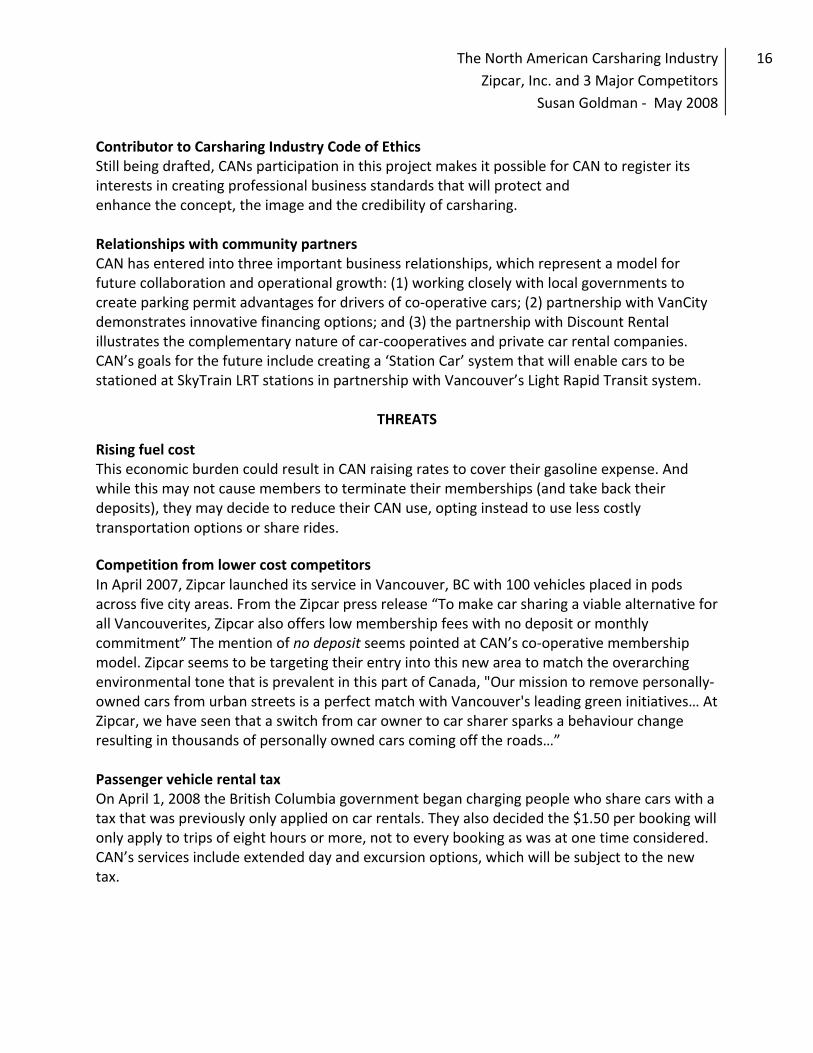

Contributor to Carsharing Industry Code of Ethics Still being drafted, CANs participation in this project makes it possible for CAN to register its interests in creating professional business standards that will protect and enhance the concept, the image and the credibility of carsharing.

Relationships with community partners CAN has entered into three important business relationships, which represent a model for future collaboration and operational growth: (1) working closely with local governments to create parking permit advantages for drivers of co-‐operative cars; (2) partnership with VanCity demonstrates innovative financing options; and (3) the partnership with Discount Rental illustrates the complementary nature of car-‐cooperatives and private car rental companies. CAN’s goals for the future include creating a ‘Station Car’ system that will enable cars to be stationed at SkyTrain LRT stations in partnership with Vancouver’s Light Rapid Transit system.

THREATS

Rising fuel cost This economic burden could result in CAN raising rates to cover their gasoline expense. And while this may not cause members to terminate their memberships (and take back their deposits), they may decide to reduce their CAN use, opting instead to use less costly transportation options or share rides. Competition from lower cost competitors In April 2007, Zipcar launched its service in Vancouver, BC with 100 vehicles placed in pods across five city areas. From the Zipcar press release “To make car sharing a viable alternative for all Vancouverites, Zipcar also offers low membership fees with no deposit or monthly commitment” The mention of no deposit seems pointed at CAN’s co-‐operative membership model. Zipcar seems to be targeting their entry into this new area to match the overarching environmental tone that is prevalent in this part of Canada, "Our mission to remove personally-‐owned cars from urban streets is a perfect match with Vancouver's leading green initiatives… At Zipcar, we have seen that a switch from car owner to car sharer sparks a behaviour change resulting in thousands of personally owned cars coming off the roads…” Passenger vehicle rental tax On April 1, 2008 the British Columbia government began charging people who share cars with a tax that was previously only applied on car rentals. They also decided the $1.50 per booking will only apply to trips of eight hours or more, not to every booking as was at one time considered. CAN’s services include extended day and excursion options, which will be subject to the new tax.

The North American Carsharing Industry Zipcar, Inc. and 3 Major Competitors

Susan Goldman -‐ May 2008

17

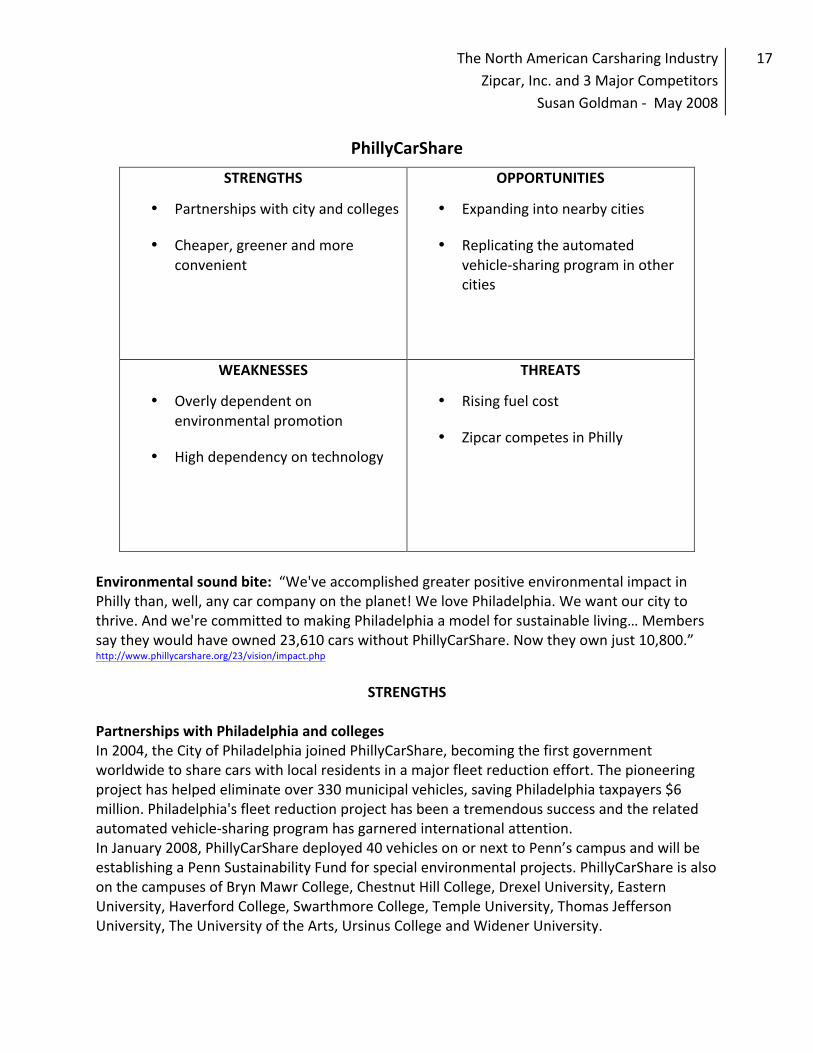

PhillyCarShare

STRENGTHS

• Partnerships with city and colleges

• Cheaper, greener and more convenient

OPPORTUNITIES

• Expanding into nearby cities

• Replicating the automated vehicle-‐sharing program in other cities

WEAKNESSES

• Overly dependent on environmental promotion

• High dependency on technology

THREATS

• Rising fuel cost

• Zipcar competes in Philly

Environmental sound bite: “We've accomplished greater positive environmental impact in Philly than, well, any car company on the planet! We love Philadelphia. We want our city to thrive. And we're committed to making Philadelphia a model for sustainable living… Members say they would have owned 23,610 cars without PhillyCarShare. Now they own just 10,800.” http://www.phillycarshare.org/23/vision/impact.php

STRENGTHS

Partnerships with Philadelphia and colleges In 2004, the City of Philadelphia joined PhillyCarShare, becoming the first government worldwide to share cars with local residents in a major fleet reduction effort. The pioneering project has helped eliminate over 330 municipal vehicles, saving Philadelphia taxpayers $6 million. Philadelphia's fleet reduction project has been a tremendous success and the related automated vehicle-‐sharing program has garnered international attention. In January 2008, PhillyCarShare deployed 40 vehicles on or next to Penn’s campus and will be establishing a Penn Sustainability Fund for special environmental projects. PhillyCarShare is also on the campuses of Bryn Mawr College, Chestnut Hill College, Drexel University, Eastern University, Haverford College, Swarthmore College, Temple University, Thomas Jefferson University, The University of the Arts, Ursinus College and Widener University.

The North American Carsharing Industry Zipcar, Inc. and 3 Major Competitors

Susan Goldman -‐ May 2008

18

Cheaper, greener, and more convenient A sampling of ways in which PhilyCarShare has integrated carsharing into Philadelphia and makes a strong case for carsharing an alternative to car ownership: Convenience: Hundreds of locations in Philly, with cars every block in many neighborhoods Availability: Most trips are booked within three hours of driving. 80% booked same day. Membership: Free to join; Eligibility: 18 yrs Transit connection: Ride rail transit free to PhillyCarShare Included Everything: gas, insurance, reserved parking, child seats, 24-‐hour roadside assistance Commitments: pay-‐as-‐you-‐go pricing Hybrids: 50% of PhillyCarShare’s fleet

WEAKNESSES Overly dependent on environmental promotion Stating environmental concern and promoting carsharing as an alternative to car ownership is common to all or most North American carsharing organizations; however, the heavy promotion of this idea that PhillyCarShare tends to do; may result in a diluted message. That is people may stop listening and that creates a challenge to getting new information through to customers and potential customers. A balance of promotion that attracts new customers who have a diverse reason for considering carsharing may be more effective. High dependency on technology PhillyCarShare depends on technology for all aspects of its operations: reservations, maintenance, billing, and customer service. While this is integral to the seamless flow of operations and to maintaining high customer satisfaction, the downside is that if technology fails them -‐ Web site goes down, business systems become corrupted, power failure occurs, hackers breach security or other technological catastrophes – then PhilyCarShare’s ability to do business goes down as well. Protection through backups, contingency plans, and disaster recovery plans is critical.

OPPORTUNITIES

Expanding into nearby cities In 2007 PhillyCarShare expanded service with 10 cars in nearby Wilmington, DE (pop 73,000). This has been a successful endeavor and may have merit for similar small scale operations in other neighboring small cities. Replicating the automated vehicle-‐sharing program in other cities The City of Philadelphia suggests that the automated vehicle-‐sharing program could be replicated for little cost in other municipalities, as long as an automated carsharing organization already exists. This may be an endeavor for PhillyCarShare to explore both within Pennsylvania and in other states.

The North American Carsharing Industry Zipcar, Inc. and 3 Major Competitors

Susan Goldman -‐ May 2008

19

THREATS

Rising fuel cost This economic burden could result in PhillyCarShare raising rates to cover their gasoline expense. And while this may not cause current customers to terminate their memberships, they may decide to reduce their PhillyCarShare use, opting instead to use less costly transportation options or share rides. Higher rates may also deter new members from joining PhillyCarShare. Zipcar competes in Philly Zipcar launched its carsharing service in Philadelphia in March 2008 (operated as Flexcar since October 2007) with 110 vehicles, including 20 hybrid Toyota Priuses. Although, PhillyCarShare’s fleet is 50% hybrid and with 35,000 members a good bet that they have more than 100 on hand.

The North American Carsharing Industry Zipcar, Inc. and 3 Major Competitors

Susan Goldman -‐ May 2008

20

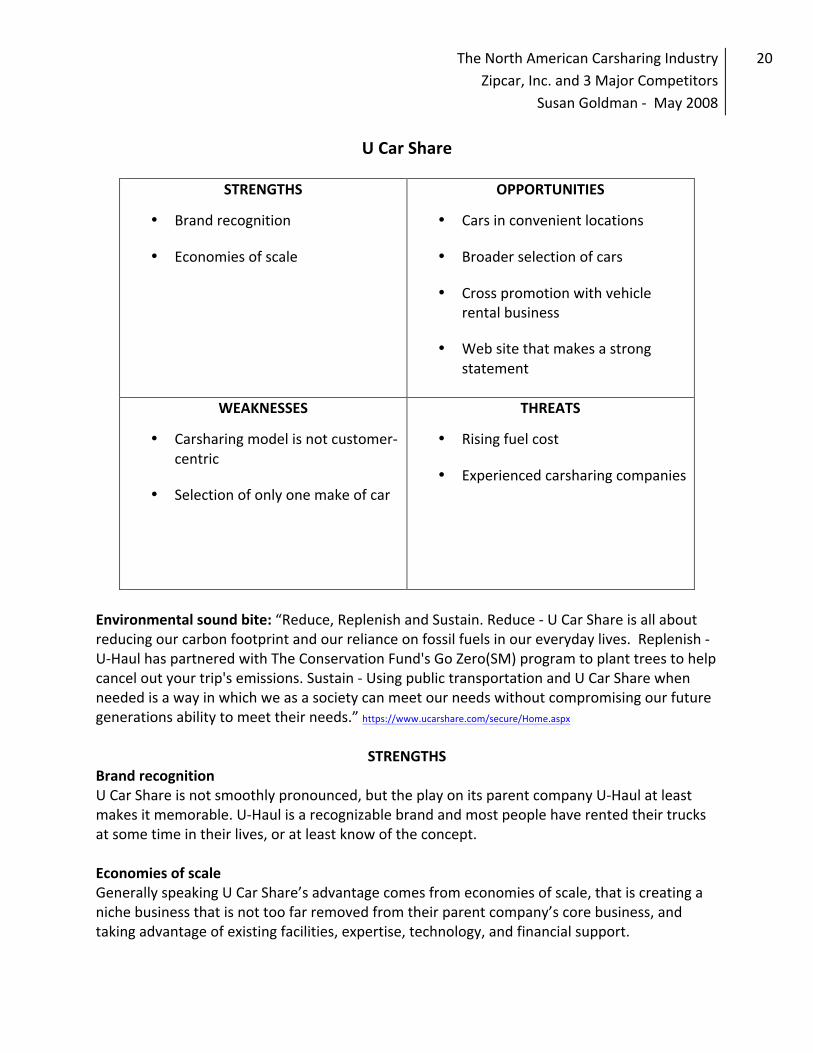

U Car Share

STRENGTHS

• Brand recognition

• Economies of scale

OPPORTUNITIES

• Cars in convenient locations

• Broader selection of cars

• Cross promotion with vehicle rental business

• Web site that makes a strong statement

WEAKNESSES

• Carsharing model is not customer-‐centric

• Selection of only one make of car

THREATS

• Rising fuel cost

• Experienced carsharing companies

Environmental sound bite: “Reduce, Replenish and Sustain. Reduce -‐ U Car Share is all about reducing our carbon footprint and our reliance on fossil fuels in our everyday lives. Replenish -‐ U-‐Haul has partnered with The Conservation Fund's Go Zero(SM) program to plant trees to help cancel out your trip's emissions. Sustain -‐ Using public transportation and U Car Share when needed is a way in which we as a society can meet our needs without compromising our future generations ability to meet their needs.” https://www.ucarshare.com/secure/Home.aspx

STRENGTHS Brand recognition U Car Share is not smoothly pronounced, but the play on its parent company U-‐Haul at least makes it memorable. U-‐Haul is a recognizable brand and most people have rented their trucks at some time in their lives, or at least know of the concept. Economies of scale Generally speaking U Car Share’s advantage comes from economies of scale, that is creating a niche business that is not too far removed from their parent company’s core business, and taking advantage of existing facilities, expertise, technology, and financial support.

The North American Carsharing Industry Zipcar, Inc. and 3 Major Competitors

Susan Goldman -‐ May 2008

21

WEAKNESSES

Carsharing model is not customer-‐centric The “U” in U Car Share seems to stand for “You come and get it,” because the company’s carsharing facilities are all located within 26 U-‐Haul centers in nine cities. Unless the member can share a ride with a friend or use public transportation to reach the center and return home afterwards, this model is inconvenient. Reservation requests can be made online, but confirmation of location, date, and time of pickup is sent in an email. Cars are only available for pick up during the hours the U-‐Haul center is open. Customer service is limited to phone and email, and the five page member handbook is filled with many “you will” statements. The experience seems very much what is required to rent a car, an experience most people consider a necessary evil. Selection of only one make of car PT Cruiser anyone? U Car Share has an inventory of 160.

OPPORTUNITIES Cars in convenient locations Parking cars in reserved spots convenient to pedestrian access or at transit connections will attract more customers to U Car Share carsharing. In St. Louis, WeCar locates cars at office parks, to capitalize on workers who carpool or commute to work without a car and need one to run errands during the day. Cross promotion with vehicle rental business Promote U Car Share in literature placed in the cabs of U-‐Haul vehicles and visible advertised on the outside of the vehicles, so that motorists and pedestrians can learn about the service. Web site that makes a strong statement Develop a Web site that at least seems like U Car Share wants to be in the carsharing business. The current site is extremely static with some basic information about the program, a mission statement, and links to the U-‐Haul centers that show hours of operation and location map.

THREATS Experienced carsharing companies Although U Car Share has economies of scale supporting it and the U-‐Haul name to lean on, this may not be a situation where those factors are the impetus for new customers. U Car Share has been operating for less than a year. Zipcar is already doing business in many of the markets where U Car Share is located, and with its brand reputation and convenient access to cars, it is likely to win out.

The North American Carsharing Industry Zipcar, Inc. and 3 Major Competitors

Susan Goldman -‐ May 2008

22

Selected References

Brook, D. (2008, March 17). Updated North American car sharing map. Retrieved May 11, 2008,

from Carsharing.us: http://carsharing.us/ Burkhardt, J. E., & Millard-‐Ball, A. (2006). Who is attracted to carsharing? Transportation

Research Recrod: Journal of the Transportation Research Board , 1986, 98-‐105. Clifford, S. (2008, March). How fast can this thing go, anyway? Inc. Magazine , 30 (3), pp. 94-‐

102. Friedhan, Jeffrey Allen. (2006, December 1). An exercise in cost saving: carsharing The Free

Library. (2006). Retrieved May 16, 2008 from http://www.thefreelibrary.com/An exercise in cost saving: carsharing.-‐a0160591964

Innovative Mobility Research. (2008). Transportation Sustainability Research Center (TSRC) at the University of California, Berkeley http://www.innovativemobility.org/

Institute of Transportation Studies at the University of California, Davis. (2008). http://www.its.ucdavis.edu/index.php

Sheehan, S. A., Cohen, A. P., & Roberts, J. D. (2006). Carsharing in North America: Market growth, current developments, and future potential. Transportation Research Record: Journal of the Transportation Research Board , 1986, 116-‐124.

Zipcar Press Center. (n.d.). Retrieved April 15, 2008, from Zipcar Inc.: http://www.zipcar.com/press/