thomas a. danjczek president steel manufacturers association may 16, 2013 tri – spring membership...

TRANSCRIPT

Thomas A. DanjczekPresidentSteel Manufacturers AssociationMay 16, 2013

TRI – Spring Membership Meeting

4-22-13

The Refractories Institute

Outline

•About the SMA

•Safety

•Set the Tone - Economy

•Set the Tone - Steel

•US Steel Imports

•Expanding Future US Steel Production

•Changes/Challenges Impacting Steel

•What’s Happening in Washington, DC

•Final Thoughts

TRI – Spring Meeting

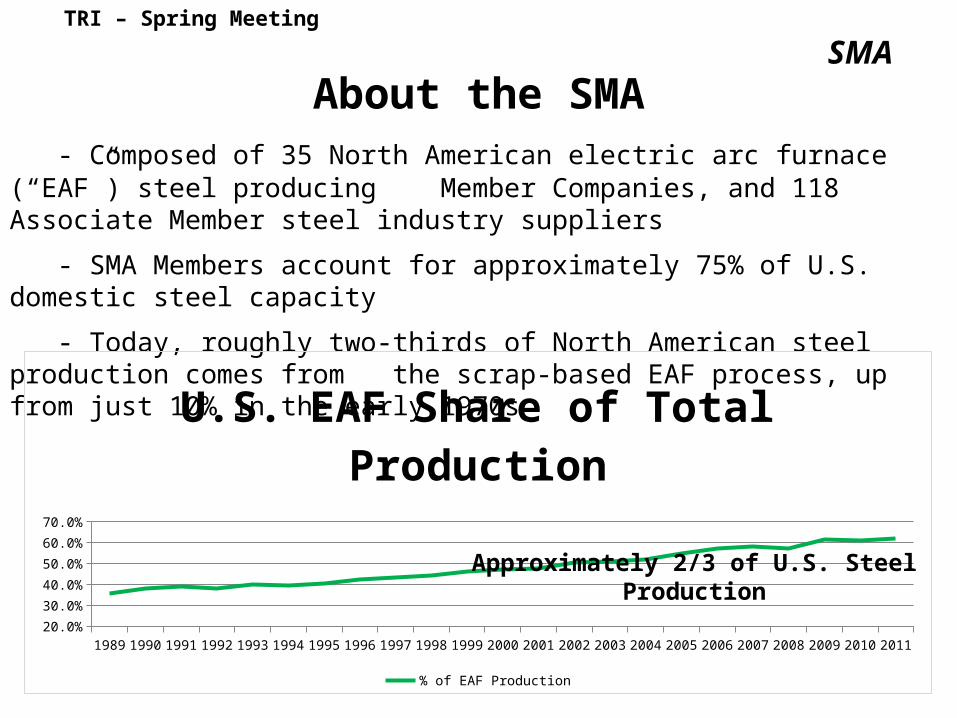

About the SMA- Composed of 35 North American electric arc furnace (“EAF”) steel producing Member Companies, and 118 Associate Member steel industry suppliers

- SMA Members account for approximately 75% of U.S. domestic steel capacity

- Today, roughly two-thirds of North American steel production comes from the scrap-based EAF process, up from just 10% in the early 1970s

TRI – Spring Meeting

SMA

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 201120.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

55.0%

60.0%

65.0%

U.S. EAF Share of Total Production

% of EAF Production

Approximately 2/3 of U.S. Steel Production

TRI – Spring Meeting

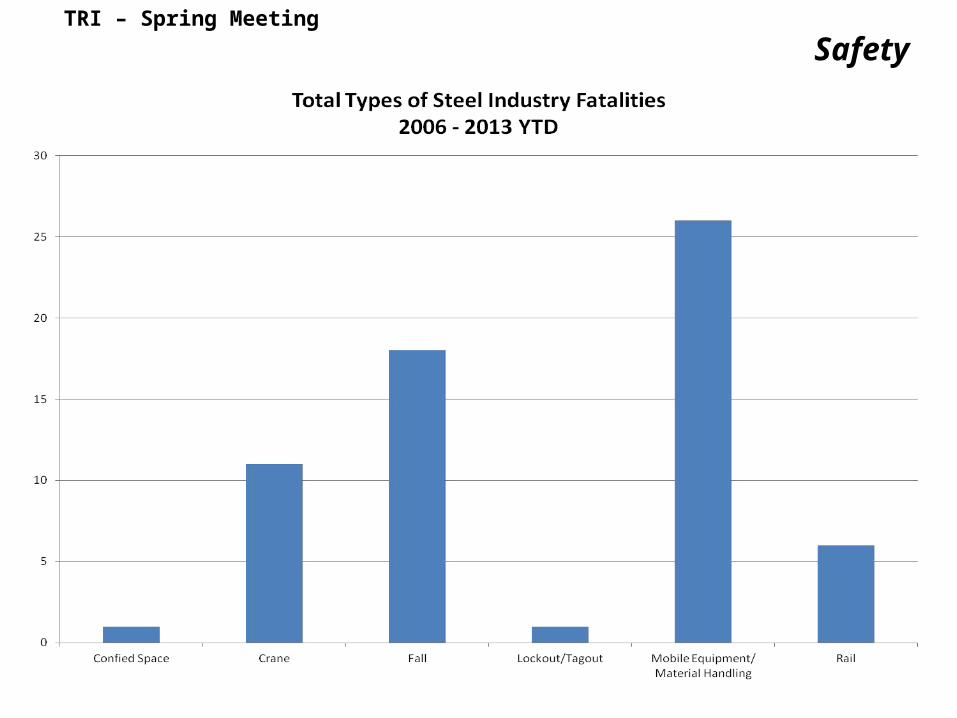

Safety

SafetyTRI – Spring Meeting

TRI – Spring Meeting

Safety

Set the Tone - Economy

• GDP forecasts are “soft” – 3% first quarter 2013 jerked around by sentiment reaction

• Pace of U.S. growth in 2013 near stagnation; China 7.8% now

• Euro Zone is at negative growth first 2 months of 2013

• While U.S. unemployment rate declined, still above pre-recession levels

• Rising energy production and housing rebounding are bright spots (“race to gas”)

• Capital spending is a downside risk

• U.S. trade deficit is unsustainable

TRI – Spring Meeting

Global Economic Outlook

• Global GDP Forecasts– Global growth forecast for 2014 at 4.1%– Major uncertainties worldwide – Eurozone forecast for 2014 at 1.0%

• Global Outlook– USA

• Economy is growing at a slow pace with limitations created by weak exports and cautious business spending• Credit conditions are easing and demand for vehicles and houses are gaining momentum

– Asia• Japan’s economy continues to struggle with weak export market and declining industrial production• India’s GDP continues to grow, although problems remain with inflation and weak domestic and foreign

investment• China’s territorial disputes with neighboring Asian countries could result in severe economic disruptions, but

growth still projected at over 8%– Europe

• The Eurozone is in recession. France and Germany show modest growth but are slowing• A Eurozone breakup no longer seems imminent but serious concerns remain about Spain and Italy

IMF DataGDP Jan 23rd, 2013 2011 2012 2013 FORECAST

WORLD +3.9% +3.2 % +3.5 %

USA +1.8% +2.3 % +2.0 %

China +9.3% +7.8% +8.2%

Developing Asia +8.0% +6.6 % +7.1 %

Eurozone +1.4% (0.4) % (0.2) %

TRI – Spring Meeting

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 20120.00

50,000.00

100,000.00

150,000.00

200,000.00

250,000.00

300,000.00

350,000.00

Source: US Census Bureau

Total US Trade Deficit with China(in million US$)

2012 US trade deficit with China was a record $315.1 billion, accounting for 43.3% of overall $727.9 billion US trade deficit.

2012 US steel imports from China were 1,505,751 metric tons, a 33.9% increase over 2011 levels, and a 92.8% increase over 2010 levels.

Mill

ion

US

$TRI – Spring Meeting

US GOOds

Set the Tone - Economy

Annual Deficit is the most significant barrier to U.S. economic recovery

UNSUSTAINABLE

TRI – Spring Meeting

Set the Tone - Steel

• Primary metal 4% growth YTD 2012 over 2011 in US

• U.S. capacity utilization approx. 74.4% in 2012

Y.T.D. capacity utilization approx.76.9% (w/reduced capacity)

• Scrap price volatility (75% of minimill costs)

TRI – Spring Meeting

Year World Steel Production

(million metric tonnes)

US Steel Production

(million metric tonnes)

US Steel Imports

(million metric tonnes)

2007 1,347.0 98.1 30.2

2008 1,341.2 91.4 29.0

2009 1,235.8 58.2 14.7

2010 1,428.7 80.5 21.7

2011 1,490.1 86.2 25.9

2012 1,517.9 88.6 30.4

Sources: census.gov, worldsteel.org

U.S. Current Operating Environment

• Capacity Utilization – 2013 Capacity Utilization figures reflect a change in the overall capacity

due to the closure of several facilities in 2012 and new facilities coming online

– Flat Roll Mills – After peaking in 2Q, production rates for 3Q and 4Q were relatively flat. 1Q looks to be flat as well.

– Pipe & Tube – Imported OCTG mostly from Asia, caused NAFTA production cuts in the 2nd half. Rig counts stable.

– Long Products – Automotive continued strong performance, but nonresidential construction feel again in 2012.

– Note: Tonnage down Y.T.D. 2013 through April 13 was 27.3 million tons, capacity utilization 76%; 7.7% decrease for Y.T.D. 2012 at 29.6 million tons, capacity at 79.7% 12

2010 2011 2012 W/E 4/13/13

70.4% 74.7% 74.4% 75.8%

TRI – Spring Meeting

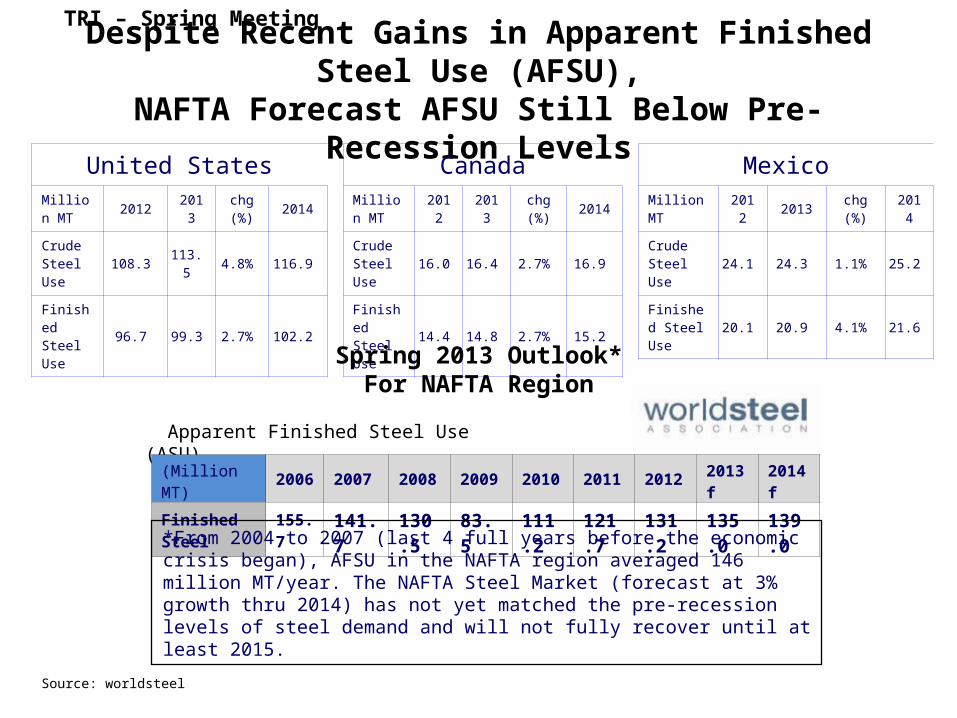

Despite Recent Gains in Apparent Finished Steel Use (AFSU),NAFTA Forecast AFSU Still Below Pre-Recession Levels

United StatesMillion MT 2012 2013 chg

(%) 2014

Crude Steel Use 108.3 113.5 4.8% 116.9

Finished Steel Use 96.7 99.3 2.7% 102.2

CanadaMillion MT 2012 2013 chg

(%) 2014

Crude Steel Use 16.0 16.4 2.7% 16.9

Finished Steel Use 14.4 14.8 2.7% 15.2

MexicoMillion MT 2012 2013 chg

(%) 2014

Crude Steel Use 24.1 24.3 1.1% 25.2

Finished Steel Use 20.1 20.9 4.1% 21.6

Spring 2013 Outlook*For NAFTA Region

Apparent Finished Steel Use (ASU)

(Million MT) 2006 2007 2008 2009 2010 2011 2012 2013f 2014f

Finished Steel 155.7 141.7 130.5 83.5 111.2

121.7 131.2 135.0 139.0

Source: worldsteel

*From 2004 to 2007 (last 4 full years before the economic crisis began), AFSU in the NAFTA region averaged 146 million MT/year. The NAFTA Steel Market (forecast at 3% growth thru 2014) has not yet matched the pre-recession levels of steel demand and will not fully recover until at least 2015.

TRI – Spring Meeting

2012 Steel Shipments by Market Classification

TRI – Spring Meeting

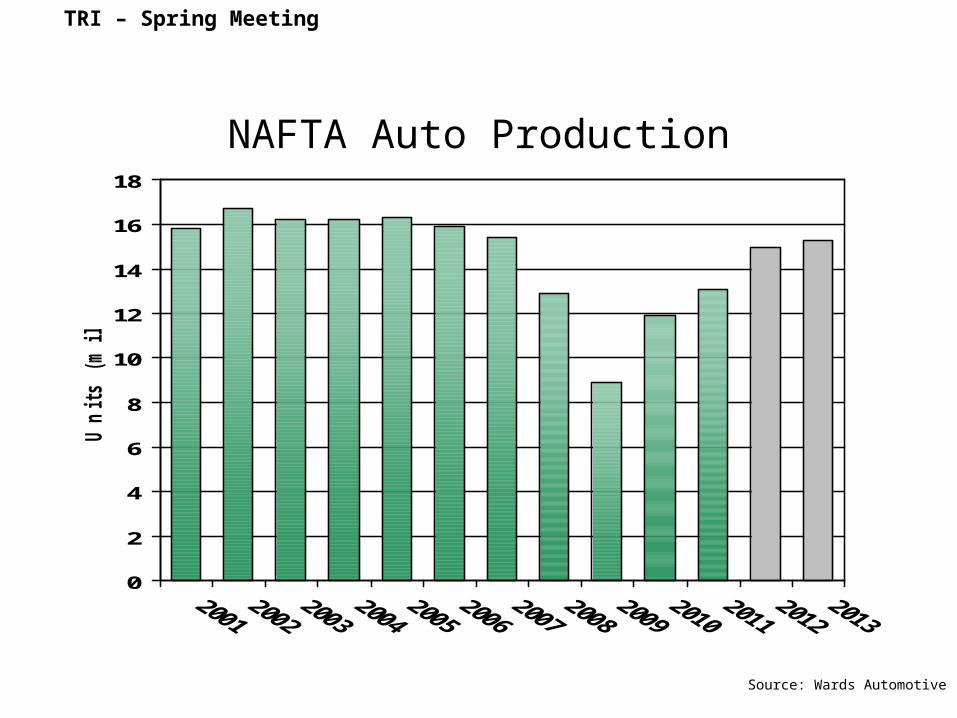

NAFTA Auto Production

Source: Wards Automotive

0

2

4

6

8

10

12

14

16

18

Units (m

illions)

TRI – Spring Meeting

Construction Activity*Non-building structures (e.g., infrastructure) not included

Source: McGraw-Hill (Dodge)

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

2007 2008 2009 2010 2011 2012 2013 2014 2015

Squa

re F

oota

ge (0

00)

Residential (1 & 2 family dwellings) Non-Residential

TRI – Spring Meeting

Energy Production

Source: Baker Hughes, U.S. Dept. of Energy

0

500

1,000

1,500

2,000

2,500

JA

N

AP

R

JU

L

OC

T

JA

N

AP

R

JU

L

OC

T

JA

N

AP

R

JU

L

OC

T

JA

N

AP

R

JU

L

OC

T

Ja

n

Ap

r

Ju

l

2008 2009 2010 2011 2012

RIG

CO

UN

T

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

$ M

cf

Total RIGS

Verticle RIGS

Horizontal RIGS

Natural Gas Price at Wellhead

TRI – Spring Meeting

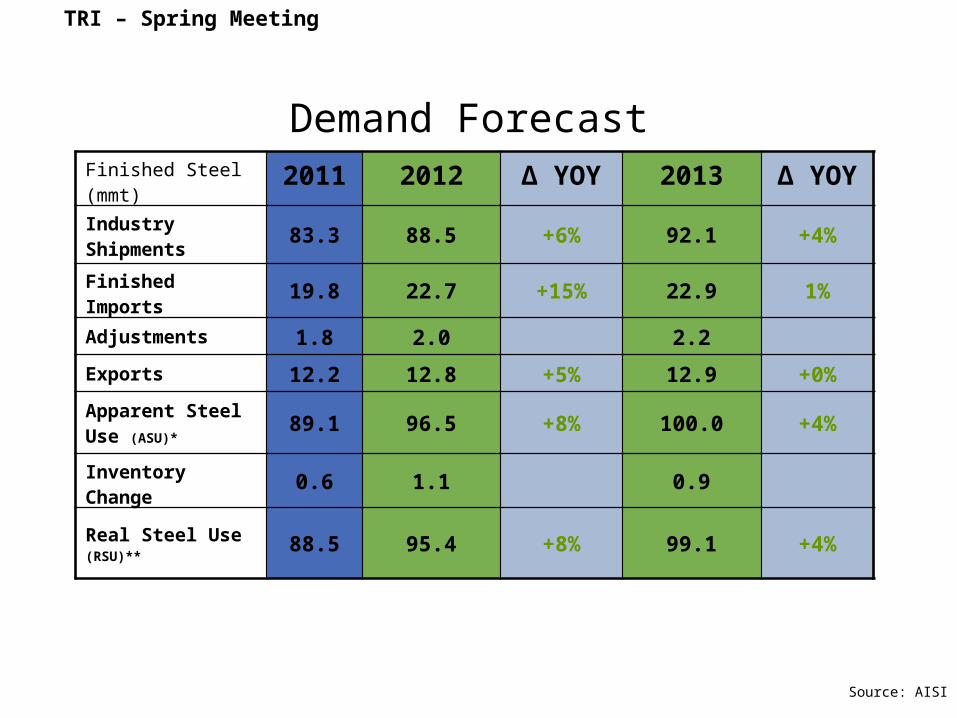

Source: AISI

Demand ForecastFinished Steel (mmt)

2011 2012 ∆ YOY 2013 ∆ YOY

Industry Shipments 83.3 88.5 +6% 92.1 +4%

Finished Imports 19.8 22.7 +15% 22.9 1%

Adjustments 1.8 2.0 2.2

Exports 12.2 12.8 +5% 12.9 +0%

Apparent Steel Use (ASU)*

89.1 96.5 +8% 100.0 +4%

Inventory Change 0.6 1.1 0.9

Real Steel Use (RSU)**

88.5 95.4 +8% 99.1 +4%

TRI – Spring Meeting

US Imports of Total Steel Products Up 17%

Source: U.S. Department of Commerce (Census Bureau)

2011 20120

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

28,515,276

33,474,583

Total Steel Imports (2011 vs 2012)Im

port

s (N

et

Ton

s)

TRI – Spring MeetingUS Steel Imports

Comparing 2012 to 2011 by product category:

• Semi-finished imports increased 14.2% to 6,772,056 metric tons;

• Flat product imports increased 16.4% to 9,550,032 metric tons;

• Pipe and tube imports increased 24.4% to 7,710,529 metric tons;

• Long product imports increased 14.6% to 5,191,504 metric tons;

• and stainless imports increased 13.5% to 1,143,515 metric tons.

TRI – Spring MeetingUS Steel Imports

Increase in Total Steel Imports is from Numerous Countries, Across the Globe

Source: U.S. Department of Commerce (Census Bureau)

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

Turkey Germany China Russia Japan South Korea Brazil

Impo

rts (N

T)

2011 vs. 2012 Total Steel Importsfrom Key Offshore Countries

2011 2012

+84% +24%

+34%

+74%

+30%

+30% +27%

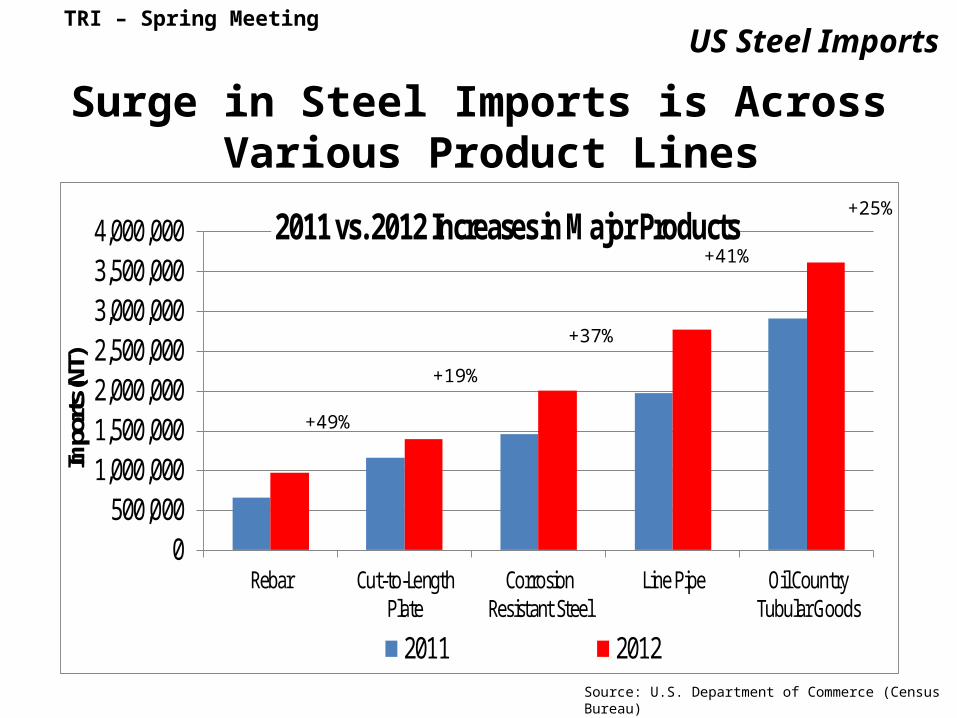

TRI – Spring MeetingUS Steel Imports

Surge in Steel Imports is Across Various Product Lines

Source: U.S. Department of Commerce (Census Bureau)

0500,000

1,000,0001,500,0002,000,0002,500,0003,000,0003,500,0004,000,000

Rebar Cut-to-LengthPlate

CorrosionResistant Steel

Line Pipe Oil CountryTubular Goods

Impo

rts (N

T)

2011 vs. 2012 Increases in Major Products

2011 2012

+49%

+19%

+37%

+41%

+25%

TRI – Spring MeetingUS Steel Imports

Factors in the Surge of Steel Imports

• Weakened global economy– Asian market downturn, large overcapacity of steel– European recession– U.S. market still weak

• Market interference by foreign governments:– Subsidies – Raw material export restrictions– Import restrictions on steel or steel containing products– Other interventions

TRI – Spring MeetingUS Steel Imports

• The US is a net importer of steel, yet domestic capacity is utilization only at appox 75%

• The US is the world’s largest exporter of scrap

• The US is a low cost steel producer

Expanding Future US Steel Production

The United States is unique among major steel producing nations:

TRI – Spring Meeting

• Is self-sufficient in steelmaking raw materials, especially scrap (2011 – generated 84mmt of scrap, but consumed only 55mmt)(~ 75%of production costs)

• Since 2002, imports 26.2% of steel consumption, while capacity utilization only appox 80%

• Has relatively low energy prices

• Has high productivity to offset wage rates

• Has the world’s largest capital market

TRI – Spring MeetingComparative Advantages in US

The United States:

• Need policies that encourage expanded domestic steel production to utilize domestic capacity

• Foreign export restrictions on steel scrap have many negative consequences

• Expanding US steel production through the conversion of scrap into steel would create high-paying jobs, increase GDP, reduce the trade deficit, and provide added tax revenues

• The expansion must occur without massive government investments, subsidies, and interventions; but needs to be based on comparative economics and market forces

• Significant amounts of imports should be replaced with domestically produced steel

TRI – Spring Meeting

Key Points

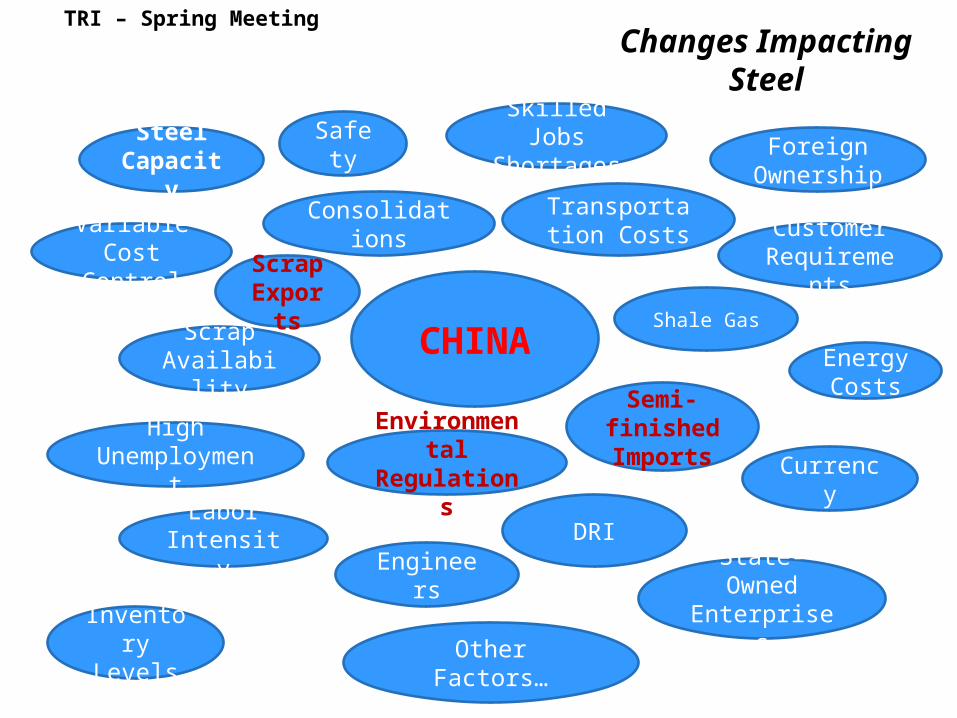

TRI – Spring MeetingChanges Impacting Steel

Steel Capacity

Variable Cost Control

Engineers

Scrap Availability

High Unemployment

Labor Intensity

Inventory Levels

CHINA

Safety

ConsolidationsCustomer

Requirements

Environmental Regulations

Foreign Ownership

Transportation Costs

Shale Gas

Energy Costs

Currency

State-Owned Enterprises

Other Factors…

Skilled Jobs Shortages

Semi-finished Imports

DRI

Scrap Exports

TRI – Spring Meeting

Challenges Impacting Steel

Scrap Exports

Restrictions

Import Penetration

SOEs

Capital

Scrap Price Volatility

China, China, China Gov’t Subsidies

Trained Workforce

Abundant Natural Gas is a

“Game Changer”

WTO Disputes

Health Care Costs

Tax Manipulation

& Reforms

Trade Restrictions

Another Recession

Indirect Steel %

Environmental Regulations

Global Steel Capacity Growth

Role of Developing World

Anti-Competitive

Behavior

Labor Regulations

Infrastructure Investment

Currency Undervaluation

EAF Growth

Political Climate/Tone

• Budget Issues – Impact?

• Bipartisanship versus Gridlock?

• Benefits of expanded US steel production?

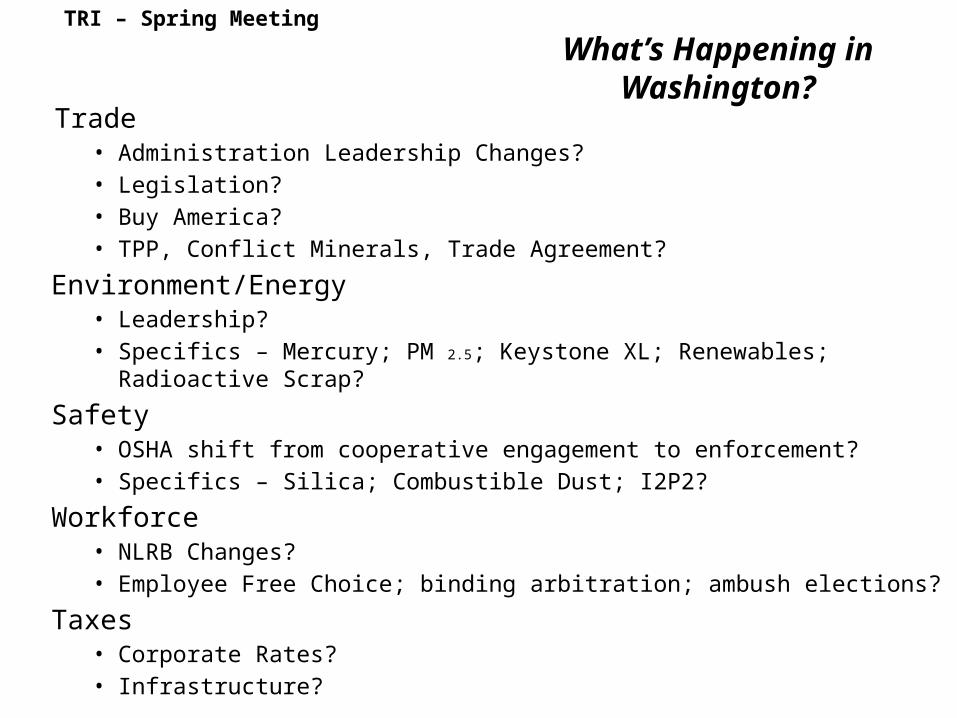

What’s Happening in Washington?TRI – Spring Meeting

Trade• Administration Leadership Changes?• Legislation?• Buy America?• TPP, Conflict Minerals, Trade Agreement?

Environment/Energy• Leadership?• Specifics – Mercury; PM 2.5; Keystone XL; Renewables; Radioactive Scrap?

Safety• OSHA shift from cooperative engagement to enforcement?• Specifics – Silica; Combustible Dust; I2P2?

Workforce• NLRB Changes?• Employee Free Choice; binding arbitration; ambush elections?

Taxes• Corporate Rates?• Infrastructure?

What’s Happening in Washington?TRI – Spring Meeting

Final Thoughts

• Volatile and fragile times continue. There is a “steel cycle.”• U.S. is in a traffic jam, moving slightly forward, but don’t know other

consequences. Gridlock continues

• Uncertainty will continue.• Increasing steel capacity without regard to market forces or comparative

advantage is wrong

• Reasons for optimism in steel in North America:– Favorable gains with reemerging manufacturing base, including benefits of shale gas– Scrap-based, 75% of cost – local supply– Low cost on global basis (energy is positive, labor less than 10%, others have higher

transportation costs)– Relatively strong market and resiliency– Better & stronger company balance sheets

TRI – Spring Meeting