treehouse foods, inc. - secure.ctsinc.com of treehouse foods, inc., the president of bay valley...

TRANSCRIPT

October 2015

TreeHouse Foods, Inc.

TRAVEL AND ENTERTAINMENT EXPENSES POLICY

October 2015

Table of Contents

...................................................................................................... 3

TRAVEL AND ENTERTAINMENT EXPENSES POLICY ................................................................3

1. General ................................................................................................................................3

2. Credit Cards .........................................................................................................................5

3. Approval Requirements .......................................................................................................5

4. Air Travel .............................................................................................................................6

5. International Flights .............................................................................................................7

6. Frequent Flyer Benefit/Travel Club Memberships ...............................................................7

7. Car Rentals ..........................................................................................................................7

8. Taxi and Other Ground Transportation ...............................................................................8

9. Personal Car Use / Tolls ......................................................................................................8

10. Lodging ................................................................................................................................9

11. Non-reimbursable Expenses ...............................................................................................9

12. Personal Meals ................................................................................................................. 10

13. Business Meals and Entertainment .................................................................................. 10

14. Employee Outings ............................................................................................................ 11

15. Gifts .................................................................................................................................. 11

16. Telephone ......................................................................................................................... 12

17. Spousal (Family) Travel .................................................................................................... 12

18. Miscellaneous Expenses .................................................................................................. 12

19. Tipping / Gratuities ........................................................................................................... 12

20. Travel Advances ............................................................................................................... 13

21. Accounting and Administrative Instructions and Specific Forms ...................................... 13

22. Receipts/Substantiation Requirements and Document Support ...................................... 13

Page 3

TRAVEL AND ENTERTAINMENT EXPENSES POLICY

Purpose

The policies discussed in this section are to ensure that employee travel and entertainment expenses are reported in an accurate and timely manner and that they qualify as business deductions for income tax purposes. It is the responsibility of department heads and employees in supervisory capacities to acquaint employees under their direction with these instructions and to secure compliance with procedures for reporting all such expenditures.

This policy applies to TreeHouse Foods, Inc., Bay Valley Foods, LLC and all TreeHouse Foods, Inc. subsidiaries, divisions, regions, and/or business units (collectively “the Company”). Employees are to use the same expense report forms throughout the entire business unit. Expense reports are required to be processed through the applicable accounting department.

1. General

The Company intends to maintain a professional and economical travel policy. All travel and entertainment expenditures shall have a clear business purpose.

The Company has the responsibility to ensure appropriate agencies have been selected and are effectively used.

Travel Reservations The Company has engaged Best Travel as its company-wide travel agent. Company policy requires that all Company travel be arranged through Concur/ Best Travel, except for emergency or extraordinary circumstances which require an alternative. Company policy also is to use Concur’s online booking website at http://concursolutions.com since the Company is charged a higher fee when employees call the Best Travel agency. Employees should only call the travel agency directly when absolutely necessary. When using Concur, the following fees are incurred:

Booking travel over the phone - $40.

Booking travel on the Concur website - $14.

Phone calls outside the business hours of 8 am – 6 pm (regarding an existing itinerary) - $20.

Use of Concur ensures that the Company receives negotiated discounts and allows monitoring of agency cost effectiveness and other metrics relating to Company travel patterns and costs. This information is also used to negotiate volume discounts with providers.

Page 4

Company employees booking airfare service through Concur who do not have a Concur account, must send the following information to A/P:

The Best Travel confirmation email.

A copy of the approved expense report.

Travel for Third Parties Company expense reports are not to be used to pay for the travel or hotel accommodations of non-employees. Outside contractors, consultants, vendors, etc. who travel extensively on behalf of the Company are encouraged to use the services of Best Travel. If a non-employee will be a frequent traveler (traveling once a month or more), and will be engaged by the Company for six (6) months or more, the non-employee’s Supervisor must work with the Manager, Corporate Administration at 708-483-1311 CHREA to set up an account for Concur, the Company- designated expense reporting software system. Travel expenses should then be submitted through Concur.

For non-employees who will NOT be frequent travelers, they may use the services of Best Travel, but payment must be made by the non-employee’s use of his or her own major credit card. Expenses should be billed by the non-employee as part of their normal billing process, and should not be submitted through a Company expense report.

For employment candidates, the Candidate Travel Process should be followed. See Candidate Travel Process, issued on March 12, 2012.

Employee Conduct While Traveling Employees must abide by the Company Code of Ethics whether they are on the employer’s premises or traveling on business. Professional conduct is expected of employees at all times during travel, with the understanding that unacceptable behavior may lead to discipline. This requirement encompasses observation of all of the Company’s rules while traveling, including rules on personal appearance, alcohol and drug use, and sexual or other harassment.

In general, the quality of travel accommodations, entertainment, and related expenses should be governed by what is reasonable and appropriate to the business purpose involved. The general rule that should be applied by the employee is to use common sense and good judgment at all times.

Effective administration and control of travel and related expenses, the need for standardization of both documentation and application of such expenses, and the increasing reporting requirements of the Internal Revenue Service (“IRS”) and other regulatory bodies dictate that all employees of the Company be guided by a common set of expense guidelines. This policy sets forth those guidelines.

The Company strictly complies with the laws and regulations of all applicable jurisdictions in the conduct of its business, including travel and entertainment.

Exceptions to this policy must be approved in writing by the CEO, President, CFO, or General Counsel of TreeHouse Foods, Inc., the President of Bay Valley Foods, LLC, or the President of Flagstone Foods.

Violation of Policy Employees who violate this policy are subject to discipline and/or termination at the Company’s sole discretion.

Page 5

2. Credit Cards For those employees who are issued Company credit cards, all business travel and entertainment expenses (other than airfare) must be paid for by using the Company-issued credit card so that the Company can utilize effective cost-control measures. Additionally, use of the Company-issued credit card allows the Accounting Department the ability to track business, travel and entertainment-related activity and monitor expense and travel patterns. This information will then be used to negotiate volume discounts with those providers. An explanation should be provided if the Company-issued credit card cannot be used. Travel expenses paid for with credit cards other than a Company-issued card will not be reimbursed, except in those cases where the Company-issued credit card was not accepted. An explanation for why the card was not used, within the expense report, is required.

The company agreement with American Express requires employee responsibility for monthly charges, and their submittal of applicable expense report for reimbursement.

3. Approval Requirements

Approval must be obtained for all expense reports prior to reimbursement, except as detailed below. Approval must be made by an employee’s supervisor or department manager, as authorized by operating and/or executive management. Expenses of heads of departments, GMs, COOs, VPs, etc. must be approved by the next higher level of authority. The expenses of the Chairman of the Board, the Board of Directors, the CEO, and the President of Bay Valley Foods, LLC are to be approved by the CFO.

The supervisor’s signature or approver in Concur indicating his/her approval of the expense report should be affixed only after careful review of the original expense report containing original documentation. The supervisor has the responsibility to review each item on the expense report for reasonableness of amount, proper explanation and documentation, account coding reasonableness and general compliance with this policy.

All expenses should be reported on a timely basis, preferably by month-end, and within thirty (30) days of the transaction. Any expenses submitted after sixty (60) days will require signature approval by the functional VP.

Approval of expenses incurred by an employment candidate in connection with an interview of employment must be approved by Human Resources and must be authorized in advance. Travel arrangements for employment candidates must be made utilizing Best Travel.

It should be understood that the expense report approval process is the key internal control over travel and entertainment expenses, and the authority to pay. When the designated supervisor or department manager approves the expense report, he/she attests to the fact that the expenses are properly reported and supported. He/she should not rely on subsequent accounting review to augment his/her approval, but should understand that the accounting review is clerical in nature (i.e., extension verification, account coding, notation of proper approval and final approval to pay.)

An exception to the policy that reimbursement must follow approval by the employee’s supervisor may be granted in the case of an employee whose direct report is at another geographic location. At regional management’s option, the employee’s location may process a copy of the expense report to facilitate prompt reimbursement, while, concurrently, the original expense report is forwarded to the designated person for proper approval. The process should allow for the signed original to be directed to the applicable accounting department.

Page 6

4. Air Travel

Coach class or the most economical available airfare should be used for all business travel. It is the obligation of each employee to choose the least expensive flight from all practical alternatives, using Concur to facilitate this effort. Booking upgradeable full fare coach tickets to take greater advantage of airline membership awards is not allowed. In most cases, employees should purchase nonrefundable fares, as penalties incurred by the Company over time will generally be less than the increased cost of refundable fares. Plan ahead. In many cases, a traveling employee can save hundreds of dollars by purchasing tickets that may require advance booking. Booking fourteen (14) to twenty-one (21) days in advance generally and incrementally provides for greater savings. Savings are also available on flights that may entail one stop, or that may depart and/or arrive at slightly less convenient times. The savings available on these flights frequently outweighs the traveler’s inconvenience, even when they necessitate travel schedule adjustments. Deviations from the lowest available fare should be infrequent. Considerable judgment is needed to weigh factors such as impractical connecting flights and loss of workday capacity. Best Travel is expected to offer you the lowest available fares. Their effort to assist you will be monitored in the future. Due to the proliferation of sharply discounted internet fares, prices may be shown as available at a lower cost than the price quoted by Best Travel on the Concur website. If this is observed, the employee should share the information with Best Travel, who can confirm the price discrepancy and compare it with the specific airline’s discount. Often Best Travel can find airline prices which are comparable, so employees should bring all discrepancies to their attention, prior to booking travel online. Generally, the internet prices should exceed 15% or greater before a departure from an online booking and associated discount is justified. Deviations require department head approval prior to booking and should be documented on the expense report. All airline tickets must be booked through the online travel booking website of Concur/ Best Travel. Infrequent exceptions require prior approval by the designated expense report approver. If using Southwest Airlines, tickets should also be booked through Concur and not directly with the airline. Purchases of additional flight insurance should be declined. Such expenses are not reimbursable. The Company will pay for one checked luggage bag. If a business trip lasts longer than one week, the Company will pay for two checked luggage bags. The ultimate responsibility for retrieving and compensating lost baggage lies with the airlines. The Company will not reimburse travelers for personal items lost while traveling on business. Measures that can be taken to minimize baggage losses include:

Always carry valuables (e.g., jewelry, laptop computers, cameras, etc.) on board the

aircraft

Always carry important and/or confidential documents on board the aircraft Clearly tag

luggage with name, address and phone number

Retain baggage claim receipts for checked-in luggage

If you purchase luggage insurance, the costs vary and are the responsibility of the traveler – these costs will not be reimbursed by the Company

Page 7

Follow these procedures if your bags are lost en-route:

Obtain a lost luggage report form from an airline representative in the baggage claim area

Keep a copy of the report, airline ticket and claim stubs

Airlines occasionally offer free tickets or cash allowances to compensate travelers for delays and inconveniences due to overbooking, flight cancellations, changes of equipment, etc. Travelers should not volunteer for denied boarding compensation when on Company business. Travelers who are involuntarily denied boarding should immediately obtain a free voucher from the airline and may keep the free travel voucher for personal use. Should an airline delay necessitate an overnight stay, the traveler must first attempt to secure complimentary or discounted lodging from the airline. If unsuccessful, the traveler should contact Best Travel for assistance. When a trip is cancelled after the ticket has been issued, a credit will be given and tracked by Concur/ Best Travel.

5. International Flights

Employees are encouraged to travel a reasonable time prior to the business meeting, which allows the employee to adapt to the time change and be prepared for business meetings. Good judgment should be used when making international travel plans. Flying coach provides an opportunity to significantly reduce the Company travel expenses. Business class bookings require prior approval from the employee’s designated expense report approver. The Company’s Law Department or Best Travel will, when making overseas reservations, provide advice regarding all necessary documents, such as visas and passports. Please allow sufficient time to obtain a visa, as most visas take at least two weeks to obtain. The Company’s Law Department or Best Travel will advise the employee as to whether a passport or any additional documents must be carried while traveling outside the U.S.A. The duties and procedures listed below are established to assure that employees use proper Company resources for international travel, have the necessary documentation to get through a Host Country’s immigration/customs services as quickly and conveniently as possible, and comply with Host Country taxation laws. Prior to the start of any international trip for Company business, the Traveler must take the following steps:

1. Establish all reservations, if any, and complete any ticketing through Concur, the Company’s

travel services provider.[1] If the Traveler’s visit to the Host Country will not entail any reservations or ticketing (e.g., the Traveler plans to drive across the U.S.-Canada border for just one day), the Traveler obviously need not use the Company’s travel services provider, but must still take the next steps in this list.

2. Submit a completed International Travel Information Form, which can be found on the Z drive/Travel & Entertainment Policy:

a. The Traveler must provide all of the data requested in the Form. If the Traveler

has any questions, he or she should consult with Human Resources. b. The Traveler must document on the Form each and every trip, regardless of

duration or frequency. A Traveler can enter that information on a single Form or submit one Form for each separate trip.

[1] Employees in Canada currently use Egencia (Expedia), and Flagstone employees use Carlson Wagonlit

Travel. We anticipate that they will be required to use Concur at some future date.

Page 8

For example, if the Traveler is traveling to the Host Country from his or her Home Country an entire workweek, returning to the Home Country, and then returning to the Host Country for the following workweek, the Traveler must submit information on a Form for each of the workweeks. The Traveler should also note on the Form any dates during a trip on which the Traveler will not be engaged in any Company business (e.g., the employee stays over a weekend as a tourist or for other personal reasons).

c. The Traveler should submit the Form as soon as the Traveler knows the dates of international travel:

i. If possible, the Traveler should submit the Form at least two weeks prior to the start date of travel.

ii. Of course, sometimes such details are not known to the Traveler until the eve of the trip, in which case the Traveler should submit the Form as soon as practicable.

iii. If an employee knows that he or she will be traveling to a foreign country for a trip of 30 days or more or on a regular and continuing basis, we strongly recommend the employee contact the Payroll Department and Law Department (see contact names below) immediately, even without knowledge of specific dates. This will allow additional time to initiate and complete any more complicated processes that may be triggered by the duration or nature of the travel (e.g., formal Work Permit or Visa documents).

iv. If, during a particular business trip, either the scope of activities to be conducted in the Host Country change or the duration of that particular trip is extended, the Traveler must immediately inform the Payroll Department and Law Department by submitting an e-mail explaining the changes and attaching a revised International Travel Information Form. The Traveler may subsequently receive further instructions on how to proceed.

d. The completed Form should be sent by e-mail to the Payroll Department (Sarah

Laurent and/or Bobbi Hecker if the Traveler typically works in the United States; Jeanette Halper if the Traveler typically works in Canada), the TreeHouse Foods Law Department (Scott Gross) and your local Human Resources representative.

3. Understand and comply with all requirements communicated by the Payroll and/or Law

Departments. Based on the information a Traveler has provided through the International Travel Information Form, the Traveler will likely receive documents or requests for further information (for example, a business visitor letter to carry through Host Country immigration/customs, or a request for additional information needed for a more formal Visa required for entry). The Traveler should promptly follow any additional instructions and assure that he or she understands how to use properly any documentation provided.

In this regard, please note that no Traveler should rely on a “tourist visa” for any business trip on behalf of the Company. Involving the Law Department as early as possible in the travel planning process will assure that the Traveler has the proper Work Permit or Visa.

4. We strongly recommend that the Traveler review the TreeHouse Foods Code of Ethics and the TreeHouse Foods Travel and Entertainment Expenses Policy to assure familiarity with their details as well as important reminders on expected behaviors in a Host Country.

Employees should never violate any Host Country law, make any misrepresentations to embassy, consular or border/customs/immigration officials of any country, travel without required documentation, make “facilitation payments” to any immigration officials or third party agents (which are considered a bribe, regardless of how small or seemingly inconsequential) or otherwise violate in any manner the U.S. Foreign Corrupt Practices Act (see Section F below). To track each employee’s ongoing international travel, the Company will utilize the International Travel Information Forms as well as Company travel data and expense reports. If a Traveler exceeds any of

Page 9

the Company’s internal thresholds for tax equalization or immigration purposes, the Traveler will be notified of any additional requirements he or she will need to comply with.

6. Frequent Flyer Benefit/Travel Club Memberships

Employees may participate and accumulate mileage and/or frequent stay points in programs when traveling on business, but this must not result in additional cost to the Company. The accumulation of “points” by participating in airline promotion and other programs is for the employee’s benefit. Any promotional program membership fees are at the employee’s personal expense. Exceptions may be made for certain executives based on the frequency of the executive’s travel.

7. Car Rentals

The use of a rental car must be justified as an economical need and not as a matter of personal convenience. Employees should rent vehicles based on the practical travel need, and when it is the most cost-effective method of transportation (i.e., versus a taxi, airport shuttle, etc.) Employees should also consider the cost-effectiveness of renting a car rather than using their personal vehicle when they are traveling more than 200 miles.

Travelers should book midsize / intermediate rental cars; however, travelers may book a class of service one level higher if: a) two or more Company employees are traveling together; b) the

employee is entertaining customers; c) cars in the authorized category are not available; d) the upgrade can be received at no extra cost; e) transporting excess baggage, such as booth displays, is required; or f) for pre-approved medical reasons (i.e., drivers with disabilities.). An explanation for using the higher level should be noted on the expense report. All car rental reservations must be made through Concur. Employees should choose National Enterprise, as a THS preferred vendor for the least expensive rental car rate available. Preferred car rental agencies, if necessary, are Hertz and Avis.

A copy of the rental car invoice or receipt is required as documentation for reimbursement of all car rental charges.

Insurance All Company employees (including all Canadian employees) who rent vehicles in the U.S.A. or Canada should decline additional rental insurance coverages from the rental company, regardless of the vendor. If the rental is arranged through National (US rentals only), full collision damage protection is provided through our agreement for a $1.00 per day charge. This is processed automatically. The Company’s auto policy provides liability coverage for all work-related rentals.

All Company employees who rent vehicles in any country other than the U.S.A. and Canada should take additional car rental insurance coverages from the rental company. All Company employees are prohibited from renting cars in any country currently on the U.S.A. State Department’s Travel Warning list (http://travel.state.gov/travel/cis_pa_tw/tw/tw_1764.html). As of June 2015, this list includes Mexico and Colombia.

Employees shall complete the following ASAP and not later than 24 hours of any accident or damage to a rental car:

Notify the rental company

Submit a Sharepoint incident report via this link: https://sharepoint.treehousefoods.com/Operations/Lists/EHS%20Incident/AllItems.aspx

Page 10

Send photos or other relevant documents (accident forms, police report, etc.) to the Sr. Director, EHS and Risk Management at the Oak Brook office. The desk phone is 708-836-2013.

Only employees of the Company who are also authorized by the rental company are approved to drive rental vehicles. Non-employees are not covered by our policy. If an accident occurs while a non-employee or non-approved person is driving, the cost of the accident is at the personal expense of the employee who rented the vehicle. When a rental car is necessary, the gas tank should be filled prior to returning the car. Gasoline costs are considerably higher when purchased from the rental car company. However, our agreement with National does allow for a special refueling rate capped at $1.00 over local pump price. When using National, re-fueling is not necessary.

8. Taxi and Other Ground Transportation

The cost of taxis or cab fare to and from places of business, hotels, or airports in connection with business activities is reimbursable. Good judgment should be used to determine the lowest cost alternatives.

9. Personal Car Use / Tolls

Employees using personal cars on Company business will be reimbursed at the current IRS guideline rate. This mileage allowance covers gas, oil, repairs, tires, maintenance, insurance, depreciation and other operating expenses; therefore, expenses of this nature are not reimbursable in addition to mileage allowance. Parking fees and tolls are reimbursable in addition to mileage allowance. Airport parking is reimbursable at the most reasonable rate only if no alternate, less costly means of transportation to the airport is available. Short-term parking can be utilized for business

trips with duration of 24 hours or less. Long-term parking or taxis should be used for business trips in excess of 24 hours. Employees who use their personal automobile in connection with business travel are required to carry automobile insurance at levels not less than $300,000 for liability. An employee’s submission of a signed expense report requesting reimbursement of personal automobile expenses will be considered an attestation that the employee has the required insurance.

10. Lodging

Hotels must be booked through Concur/Best Travel. Any infrequent exceptions require prior approval by the designated expense report approver. Exceptions may be made if one is able to obtain a lower rate than the Best Travel rate by calling the hotel directly (for example, when the Company’s corporate rate is sold out at a particular hotel, or there are no rooms available according to Concur’s site, etc.). The reason for not using Concur must be noted on the expense report. All rooms will be guaranteed for late arrival by Best Travel. Should your travel plans change, it is important that you cancel through Best Travel or directly with the hotel. Please record the date, cancellation number and the reservation person’s name, which will be given to you at the time of cancellation. Any charges that result from reservations not being cancelled properly become the responsibility of the traveler. It is recognized that, depending upon where an employee is in the world, standards applied to

Page 11

class-of-hotel and room rates may vary widely. Therefore, employees should use reasonable prudence in the choice of hotel. The Company has negotiated corporate rates at various hotels and hotel chains. Using negotiated rates will result in savings to the Company. Common sense dictates that recommended hotels and negotiated rates should be obtained from the business location being visited. Employees should make a reasonable attempt to take advantage of these rates through Best Travel when practical to the circumstances. The itemized hotel bill is required support to all lodging/hotel charges.

11. Non-reimbursable Expenses

The following items are considered personal expenses and are not reimbursable:

Airfare not booked through Concur, except for emergencies (e.g., severe storms causing disruptions in flights, and/or Best Travel is not readily available).

Travel expenses paid for with credit cards other than a Company-issued credit card, except in those cases where the Company-issued credit card was not accepted (which requires an explanation of why the card was not used).

Travel expenses for customers, vendors, or other third parties, unless pre-approved by the CFO.

Cost of in-room service or movies.

Travel insurance.

Airline and hotel travel clubs.

Personal supplies, except for those of necessity required as a result of lost luggage

Reading material, including technical manuals and books purchased for personal use by the employees.

Local mileage, except those in excess of normal commuting when incurred traveling to and from an airport. Cabs to an airport in lieu of local mileage will be reimbursed.

The cost of luncheons for Company employees unless a customer/client is present.

The cost of purchasing a cellular phone or attachments.

Rental of cellular car phones.

Air-phone usage, unless it is an emergency situation or a critical business issue is involved.

Dues, meals or other expenses attributable to civic service or similar organizations, except as they involve Company responsibilities.

Packaged liquor purchases.

Annual fees for personal credit cards.

12. Personal Meals

Only the actual cost of meals will be reimbursed. Meals include personal meals and related tips when alone or in the company of others who are paying for themselves.

Meals while the employee is away overnight are reimbursable, as is lunch on a one-day trip away from the work place. The spending limits should fall within the daily guidelines as follows:

Continental U.S.A. $75

International $100 Personal meals are partially deductible for IRS purposes.

Page 12

13. Business Meals and Entertainment

Third Parties Business meals are taken with clients or prospects during which a specific business discussion takes place. Employees will be reimbursed for business meal expenses according to actual and reasonable cost. All meals should be documented on the expense report indicating individuals present, business affiliation, location, date, and business purpose of the meeting. Employees Meals may also be purchased for other employees of the Company in certain circumstances. For events attended by multiple employees, the purpose, leader, and the names of employees present should be documented. Entertainment Reasonable entertainment expenses are reimbursable, and the expenditure should be incurred on a common sense basis. These expenses are reimbursable only if they are directly related to the active conduct of the Company’s business when directly preceding or following a business discussion, or are necessary to accomplish some useful purpose connected with the Company’s business.

Tickets to athletic events, theaters, etc., are normally treated as “entertainment” provided that a business discussion is carried on immediately before or after the “entertainment” in a clear business setting. A Company employee MUST be present at the event, and, therefore, tickets may not be given as gifts. In order to be reimbursed for these tickets, the following must be documented on the expense report:

Purpose.

Names of individuals attending the event and their affiliation.

Every attempt should be made to minimize entertainment expenses. Such expenses will be reimbursed for costs incurred to entertain present or prospective business associates and to promote employee welfare. This includes customers, suppliers, agents, professional advisors, and employees. An employee expecting reimbursement for such an expense must exercise good judgment regarding the benefit to the Company in incurring entertainment expenses. All entertainment expenses are documented on the expense report indicating individuals present, business affiliation, location, date, and business purpose of the activity. Meal and entertainment bills should be paid by the most senior position present. Business meals and

entertainment are generally partially deductible for IRS purposes.

14. Employee Outings

The following expenses are generally 100% deductible and, therefore, should be appropriately expensed:

Recreational expenses made primarily for the benefit of Company employees.

Entertainment expenses related directly to employee, director or officer meetings.

Food and beverages furnished to Company employees on Company business premises (see Section 12 for further guidance regarding employee meals).

Promotional items furnished to Company employees. These events/expenditures should be documented on the expense report indicating purpose, leader, and number of employees present.

Page 13

Examples of this type of expense are holiday parties, retirement lunches and dinners, ballpark outings, training related meals and shareholder meetings.

15. Gifts

Gifts given to non-Company employees that are a nominal value (up to $25 per annum per person) are 100% deductible. The portion of a gift to non-Company employees that exceeds the $25 threshold is not deductible.

Gifts of nominal value (up to $25 per annum per person) should be given only to Company employees for the purpose of promoting employee morale, and are 100% deductible (i.e., cups, t- shirts, holiday turkeys). Any gifts for employees that exceed $25 should not be expensed. If gifts are expensed, the following must be documented on the expense report in order to be reimbursed:

Purpose

Names of employees

Gift value per employee

16. Telephone

Travelers will be reimbursed for business calls that are reasonable and necessary for conducting business and which are made on non-Company-issued cellular phones, with a copy of the phone bill and all details attached to the expense report. Certain functional areas specifically restrict or disallow the use of cellular phones. Certain employees may be issued Company phones. The cost of purchasing a personal cellular phone is not a reimbursable expense. When traveling outside the U.S.A., employees with Company-issued telephones or Blackberries, should contact IT two weeks before the scheduled travel to activate the international communication feature on the device. Employees with a management approved home office may expense up to $50 per month for their internet connection. A copy of the bill should be attached to the expense report. Internet service charges for tablets are not reimbursable.

17. Spousal (Family) Travel

The travel expenses of a spouse or companion must be approved prior to travel by the CEO and the CFO or Controller in order to receive reimbursement.

All non-approved expenses incurred on a business trip in connection with a spouse, family or travel companion will be the responsibility of the employee. The IRS does not allow a corporate deduction for spousal travel unless there is a bona fide business purpose. Performance of incidental services does not constitute a bona fide business purpose. Therefore, any non-deductible Company expenses related to spousal travel should be segregated in a separate expense account in each subsidiary’s and/or business unit’s general ledger. The business purpose for the accompanying individual’s presence must be fully disclosed in an attachment to the expense report. The attachment should contain the approval signature of the appropriate parties listed above.

Page 14

18. Miscellaneous Expenses

Expenses for laundry and dry cleaning are allowed only when the trip exceeds five consecutive days away from the employee’s regular location or home. Receipts must be attached. Reasonable athletic workout fees while traveling on Company business will be reimbursed (if not available at the hotel). Good judgment should be used to determine the necessity of paying fees.

19. Tipping / Gratuities

Reasonable tips are customary and reimbursable. As a general guideline:

15% – Taxi Drivers

15% – 20% – Wait Staff

20. Travel Advances

No advances are allowed. Exceptions must be approved by the CEO and the CFO or Controller.

21. Accounting and Administrative Instructions and Specific Forms

Employees must use Concur to process travel and entertainment expenses for reimbursement.

22. Receipts/Substantiation Requirements and Document Support

Completion of Expense Reports

Expense Reports The substantiation of any travel, meal or entertainment expenses incurred by a Company employee must be documented on an expense report, which gathers all the necessary details, as described below for each expense:

the amount

time and place

business purpose

names and business relationship of persons entertained, etc.

The business purpose for the expense must also be included in the header of the expense report. When importing transactions from the Company-issued credit card, the Expense Title and Purpose must be edited, as these fields are automatically populated. See screenshots from Concur below:

Page 15

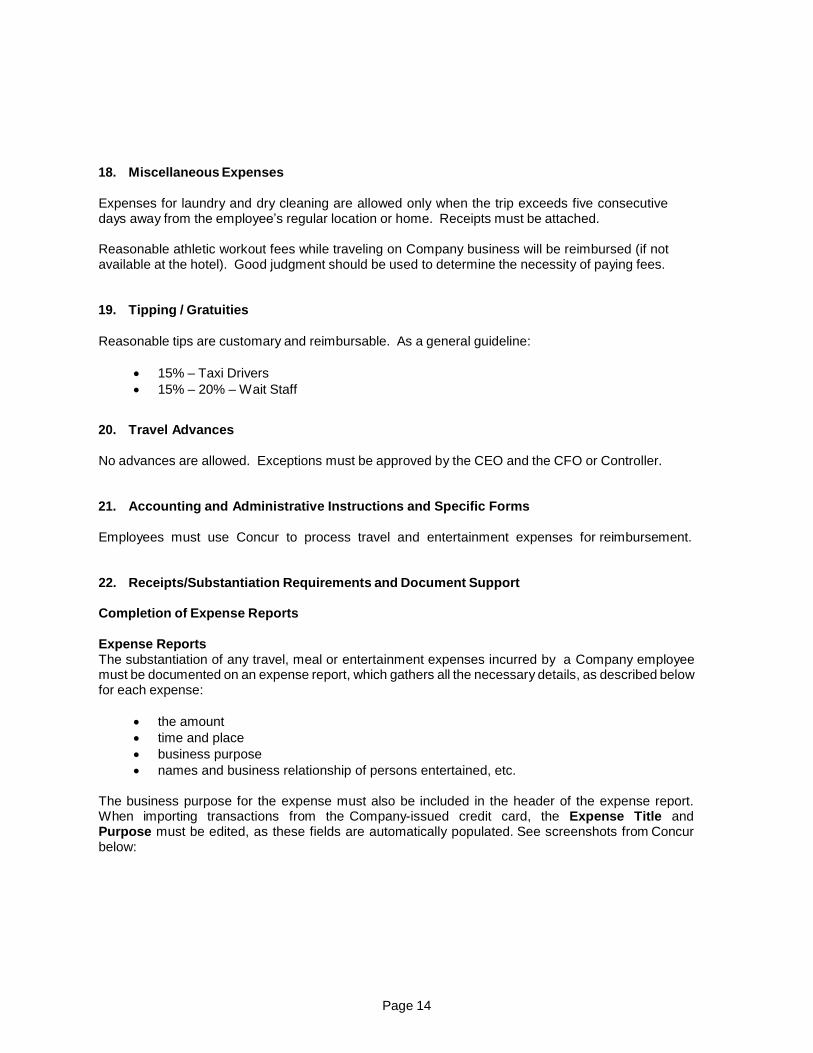

Procedure for creating a New Expense Report Expense reports should include the report name (which should be the purpose of the trip), company code (1000 for THS / 1100 for BVF) and corresponding cost center depending on employee’s department.

Importing Expenses onto Report Once the expense report is created, the next step is to add expenses on to the report. This can be done by entering out-of-pocket expenses by selecting “New Expense” and filling out the corresponding information or importing expenses from available receipts. Once your corporate credit card is linked with your Concur profile, imported expenses will appear as line items with an icon identifying the source of

the expense (credit card e-receipt airfare hotel or car rental ). If adding a corporate card transaction, this can be done by clicking on “Import Expenses” and selecting the desired line item transaction from the “Available Expenses” list, select the ‘Move’ dropdown, then select “To Current Report”.

Page 16

Once selected transactions are added to report, if e-receipts are not attached to the transactions,

receipts need to be uploaded to Concur. By selecting the icon and then clicking “Attach Receipts”, receipt images can be uploaded and attached to each line item. Uploaded receipts will be indicated by

the icon.

Procedure for Submitting Airfare Expenses in Concur In order to confirm the propriety of charges we receive for travel and comply with both our corporate travel policy and the Sarbanes-Oxley documentation process, an expense report with a copy of the Best Travel Itinerary needs to be submitted through Concur each time you book an airline ticket. If airfare is the only expense for this trip, it still needs to be submitted through Concur. Expenses should be submitted no more than 30 days from the date they are incurred. Reports will automatically be sent for approval when submitted. Your airfare will come over to the expense side of Concur and look like this:

You can now select this line and add it to an expense report. When you do that, you will get this warning message. Since airfare is company paid, you will not have a credit card transaction associated with this flight. Just click “Yes” to continue with your report.

Page 17

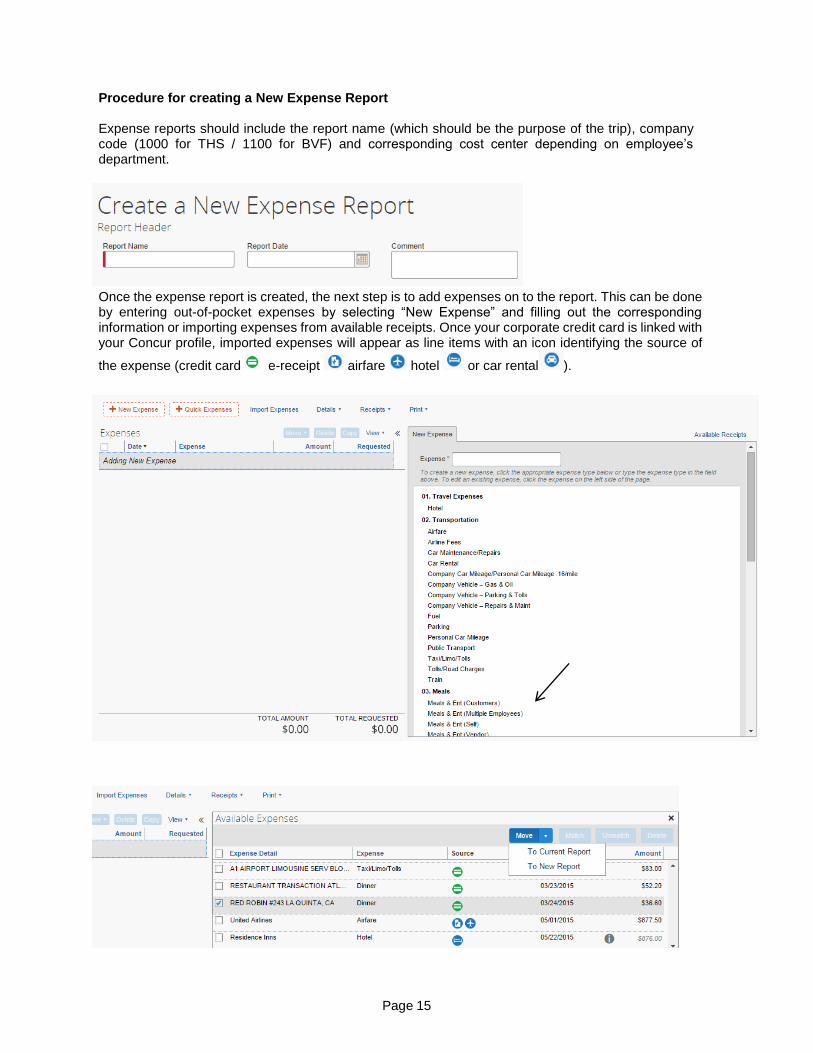

The following outlines the information needed for your Concur report for airfare:

Airfare will default to Company Paid as the payment type. This is all you need to show it is non-reimbursable. Anything marked Company Paid will not be reimbursed to you because the company paid for it already. Below is an example of an itinerary from Best Travel. This is sent as a confirmation e-mail when the trip is booked. This is where you will get the information for your Concur expense report. This is also the form that should be attached to the report as your receipt.

Page 18

When you are applying funds from a cancelled ticket to a new ticket, there will be a section at the bottom of your itinerary. When filling out your expense report in this situation you would still want to include the deducted amount in your final total. That will flag us to look into these and see another ticket is being applied. *** For this examples shown, your total price on your expense report would be $297.80 ($232.22 + $65.58).

To submit the expense report, click submit expense report and the final review window will appear to verify the information for accuracy, then click accept & submit.

Expense reporting is based on actual and reasonable expenses. In order to be reimbursed, all expenses must be listed separately on an appropriate travel expense reporting form with supporting original receipt documentation attached. Hotel bills should be itemizes to ensure each line item is treated correctly for tax purposes. Receipts A vendor receipt noting date, amount and items purchased should support each expense greater than $25. All receipts for expenses greater than $25 are required, even if charged on the Company-issued card. In the case that the vendor is not clearly identifiable on the receipt obtained, the vendor name must be documented on the expense report. Differences between the vendor invoice and the amount claimed for reimbursement must be clearly documented on the expense report.

Confirmation # & Ticket #

Airfare Total

Page 19

Receipts should be attached to the expense report in an orderly manner to provide for an efficient and effective review process. A line item or stub portion from a credit card or other statements does not provide sufficient support for expenditure. Supporting receipts are required. If merchandise is purchased and submitted for reimbursement, a clear explanation of the merchandise, to whom it was presented, and the business purpose must be documented on the expense report. The use of tear-off stub receipts should be kept to a minimum. It is recognized that certain establishments do not take credit cards. Therefore, cash is occasionally required and such receipts cannot be avoided. It is every employee’s and approver’s responsibility to ensure these types of receipts are used infrequently. Tear-off stub receipts are the least credible and acceptable form of receipt and are inherently subject to abuse.

Missing Receipts or Personal Expenses If there are discrepancies between the receipt and the expense amount (i.e., part of the receipt amount is a personal expense and is not reimbursable), please add an explanation in the expense report.

It is recognized that, occasionally, missing receipts occur. When this happens for expenses that are $25 and greater, the employee should identify the missing receipt issue at the appropriate place within the expense report and the approver should mark “OK to pay” so as to minimize any rework and delay experienced in the subsequent accounting review. Please provide an explanation in the expense report to explain the reason for the missing receipt.

Use of Credit Cards Credit card statements should be included for any credit card purchases made in foreign currency, which could not be purchased using the Company-issued card. The credit card statement must show the exchange rate for foreign currency, to allow receipts to be reconciled to the amounts on the expense report.

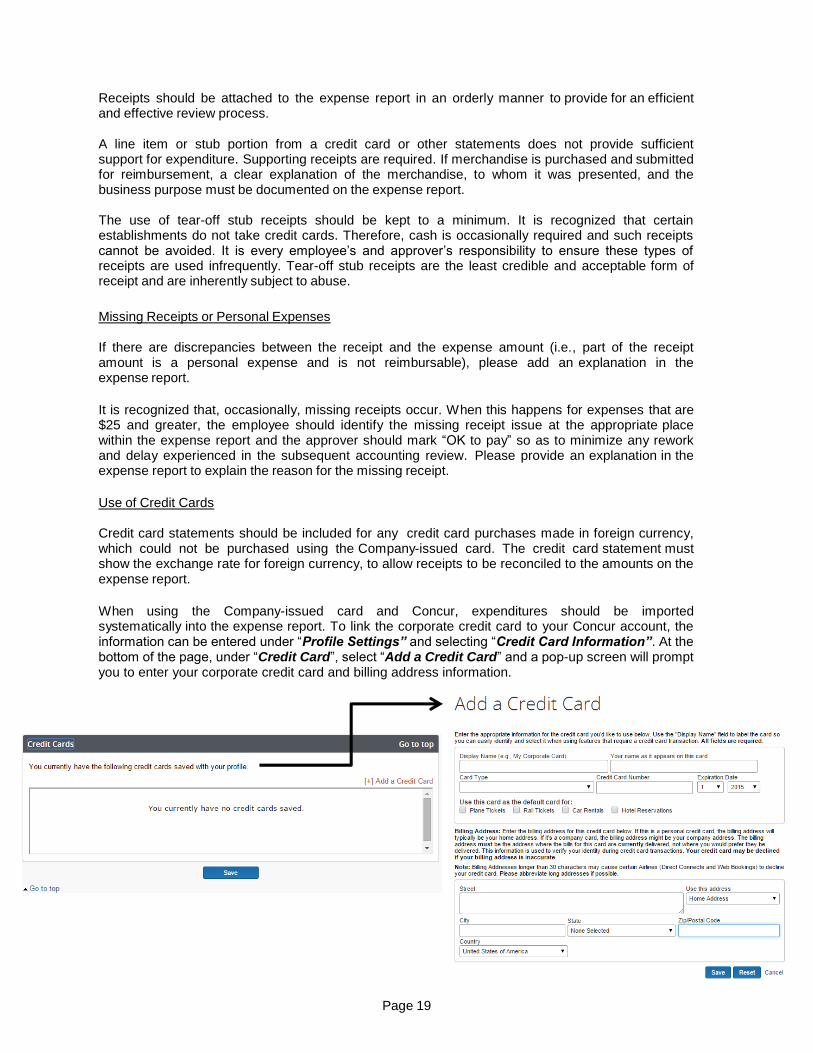

When using the Company-issued card and Concur, expenditures should be imported systematically into the expense report. To link the corporate credit card to your Concur account, the information can be entered under “Profile Settings” and selecting “Credit Card Information”. At the bottom of the page, under “Credit Card”, select “Add a Credit Card” and a pop-up screen will prompt you to enter your corporate credit card and billing address information.

Page 20

Cash Frequent use and large expenditures of cash should be minimized. If it is known and/or anticipated that a cash outlay for a planned event is or has been historically expected from a vendor, every effort should be made in advance to receive a vendor invoice. If a vendor is not willing to provide an invoice, it is a red flag as to the legitimacy of the transaction and should be avoided.

Reporting Expenses Due to differing tax treatments of various expense types, all expenses must be separately reported by type (hotel, airfare, meals, entertainment, etc.) Therefore, non-lodging costs (which are included on the hotel bill), such as meals, phone, parking, laundry and other charges are to be separated into their appropriate categories on the expense report and are not to be reported as a lodging expense.

Direct Billed Airfare All airfare should be supported by the Best Travel/Concur confirmation, NOT the trip itinerary/passenger receipt. Include the following information (see screenshots below):

The Best Travel confirmation email.

The Best Travel confirmation number from the email. Do not use the ticket locator number.

The Best Travel ticket numbers from the email including service fee ticket numbers.

The amount being charged to the company-issued credit card, including service fees.

Destination Policy Owner: Loretta Tierney