trends of flow of funds in the indian capital market in 2016-17- features first ipo by an indian...

TRANSCRIPT

Trends of Flow of Funds in the Indian Capital Market

Susanta Kumar DasMarch 2, 2017

Trends in Primary Market

Slide 2

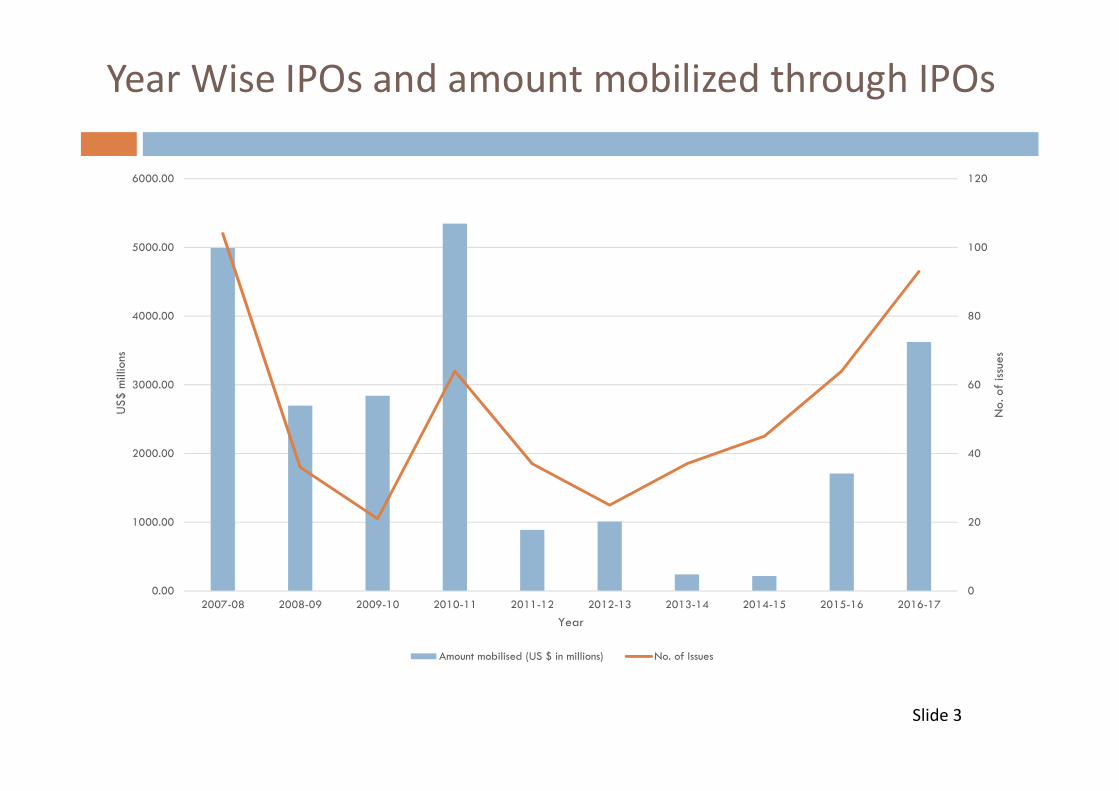

Year Wise IPOs and amount mobilized through IPOs

Slide 3

0

20

40

60

80

100

120

0.00

1000.00

2000.00

3000.00

4000.00

5000.00

6000.00

2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17

No.

of

issue

s

US$

mill

ions

Year

Amount mobilised (US $ in millions) No. of Issues

Sector-Wise IPOs

Slide 4

28.8

4.2

14

00

0.4 0

52.6

2010-11Bank/Fis/Finance

Cement and construction

Power

Automobile

Airline

Healthcare andpharmaceuticalsRoads and Highways

Miscelleneous

32.6

0.3

3.613.65.2

7

5.4

32.3

2015-16Bank/Fis/Finance

Cement and construction

Power

Automobile

Airline

Healthcare and pharmaceuticals

Roads and Highways

Miscelleneous

54.10

2.650.005.24

0.00

9.020.00

28.99

2016-17 Bank/Fis/Finance

Cement and construction

Power

Automobile

Airline

Healthcare andpharmaceuticalsRoads and Highways

Miscelleneous

37.61

21.72

15.750

00.62 0

24.3

2007-08 Bank/Fis/Finance

Cement and construction

Power

Automobile

Airline

Healthcare andpharmaceuticals

Roads and Highways

Miscelleneous

Fresh Capital as % of Issue Amount

Slide 5

0

20

40

60

80

100

120

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

IPO in 2016-17- Features

First IPO by an Indian insurer; First IPO by an Indian Stock Exchange; First private sector bank IPO in a decade; IPO by small finance banks; IPO by India’s largest enzyme manufacturer ; Most of the IPOs are backed by private equity- money raised to

provide exit to existing investors; Strong participation by domestic institutional investors; Companies from newer sectors have raised capital ( manpower

consulting, medical diagnostic, coffee chain, beverage makers, etc.)

Slide 6

SME PLATFORM

Slide 7

Listing on SME Exchange/Platform

Definition of SME for Listing:SMEs with post-issue (face value) capital less than 10 Cr.(US$ 1.5 million): Mandatory listing in SME platform.SMEs with post issue (face value) capital between 10 Cr.to 25 Cr. (US$ 1.5 million to US$ 4 million): Listing in eitherSME platform or main board.

SME Platform started in the year 2012

Capital raised to the tune of Rs. 1610 Cr (235.8 Million)

Features of SME

Filing and vetting of SME issue (public issue and right issue)with SEs, rather than SEBI.

Retail investors are ring fenced: minimum market lot of Rs. 1lakh (US$ 1600)

Minimum allottees at 50 (1000 in a normal IPO)

Less stringent continuous listing requirements- Periodicsubmissions can be half yearly instead of quarterly

100% Underwriting by Merchant bankers;

Abridged annual reports- Exemption from publishing financialresults (can make it available in their websites)

Listing and Fund Raising On SME Platform

Slide 10

1

19

39 37

46

58

1.32

27.72

53.55

40.545.39

76.73

2011-12 2012-13 2013-14 2014-15 2015-16 2016-17

No of Companies Listed Fund Raised (In Million USD)

Sector Wise Listed SME Companies

Slide 11

Manufacturing, 39%

Trading, 15%

Agro, 4%

NBFC , 15%

Realty, 6%

Service , 21%

Trends in SME IPO-2016-17

Cost of listing is significantly less compared to main board;

Less time to list;

Initial investors appear to be individuals who are from the same region as that of the company;

Early signs of participation by Institutional investors.

Slide 12

Measures taken by SEBI

Streamlining of Public Issue Process- Post issue timeline for listing reduced from T+12 to T+6 days;

ASBA made mandatory;

Reduction in the size of abridged prospectus

Additional disclosures include Track record of the merchant banker Justification of higher PE ration compared to the industry

average

Slide 13

Challenges

Uncertainty regarding FPI flows;

Proceeds not used for capital investment and creation of assets;

Liquidity - Ring fencing of retail investors

Slide 14

Foreign Portfolio Investors (FPIs)

Slide 15

Comparison - DII and FPI Investment

Slide 16

-20000

-10000

0

10000

20000

30000

40000

50000

60000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

USD

Mill

ion

Year

Comparison - DII and FPI Investment

DII Investment FPI Investment

FPI Net Investment – Equity & Debt

Slide 17

-7000

-6000

-5000

-4000

-3000

-2000

-1000

0

1000

2000

3000

4000

Jan Feb March April May June July Aug Sept Oct Nov Dec

in U

SD M

illio

n

Year

FPI Net Investment

Equity Debt Total

DII Net Investment

Slide 18

(20,000.00)

(15,000.00)

(10,000.00)

(5,000.00)

-

5,000.00

10,000.00

15,000.00

20,000.00

January,2016

February,2016

March, 2016 April, 2016 May, 2016 June, 2016 July, 2016 August, 2016 September,2016

October,2016

November,2016

December,2016

January,2017

DII

Mutual Funds (MFs)

Slide 19

Resource mobilization by Mutual Funds (in USD million)

Slide 20

0

50000

100000

150000

200000

250000

300000

2013-14 2014-15 2015-16 2016-17 (Till Dec )

Am

ount

in U

SD m

illio

n

Year

Resource mobilization by Mutual Funds (in USD million)

Net Flow AUM

Trends in B-15 cities

Slide 21

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

50000

2013-14 2014-15 2015-16 2016-17 (till Nov 2016)

Inve

stm

ent i

n U

SD m

illio

n

Year

Gross Inflows from B-15 cities

Equity Schemes Non-equity Schemes Total

Trends in mutual fund inflows

B 15 incentives to increase penetration No entry Load – Exit Load ploughed back to scheme Mutual Fund SIPs accounts crossed 10 million mark- Currently

about 12.3 million accounts MF industry has been adding about 619000 SIP accounts each

month Average SIP size is around USD 48

Slide 22

Thank you