valoracion economica de empresas manuel carreño 2010 ®

TRANSCRIPT

VALORACIONVALORACIONECONOMICA DE ECONOMICA DE

EMPRESASEMPRESAS

Manuel Carreño 2010 ®

Financing and Valuation

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

McGraw-Hill/Irwin

Capital Project Adjustments

1. Adjust the Discount Rate Modify the discount rate to reflect capital

structure, bankruptcy risk, and other factors.

2. Adjust the Present Value Assume an all equity financed firm and then

make adjustments to value based on financing.

After Tax WACC

V

Er

V

DTcrWACC ED )1(

Tax Adjusted Formula

After Tax WACCExample - Sangria Corporation

The firm has a marginal tax rate of 35%. The cost of equity is 12.4% and the pretax cost of debt is 6%. Given the book and market value balance sheets, what is the tax adjusted WACC?

After Tax WACCExample - Sangria Corporation - continued

Balance Sheet (Book Value, millions)Assets 1,000 500 Debt

500 EquityTotal assets 1,000 1,000 Total liabilities

Balance Sheet (Book Value, millions)Assets 1,000 500 Debt

500 EquityTotal assets 1,000 1,000 Total liabilities

After Tax WACCExample - Sangria Corporation - continued

Balance Sheet (Market Value, millions)Assets 1,250 500 Debt

750 EquityTotal assets 1,250 1,250 Total liabilities

Balance Sheet (Market Value, millions)Assets 1,250 500 Debt

750 EquityTotal assets 1,250 1,250 Total liabilities

After Tax WACC

Example - Sangria Corporation - continued

Debt ratio = (D/V) = 500/1,250 = .4 or 40%

Equity ratio = (E/V) = 750/1,250 = .6 or 60%

V

Er

V

DTcrWACC ED )1(

After Tax WACCExample - Sangria Corporation - continued

V

Er

V

DTcrWACC ED )1(

%0.9

090.

60.124.40.)35.1(06.

WACC

After Tax WACCExample - Sangria Corporation - continued

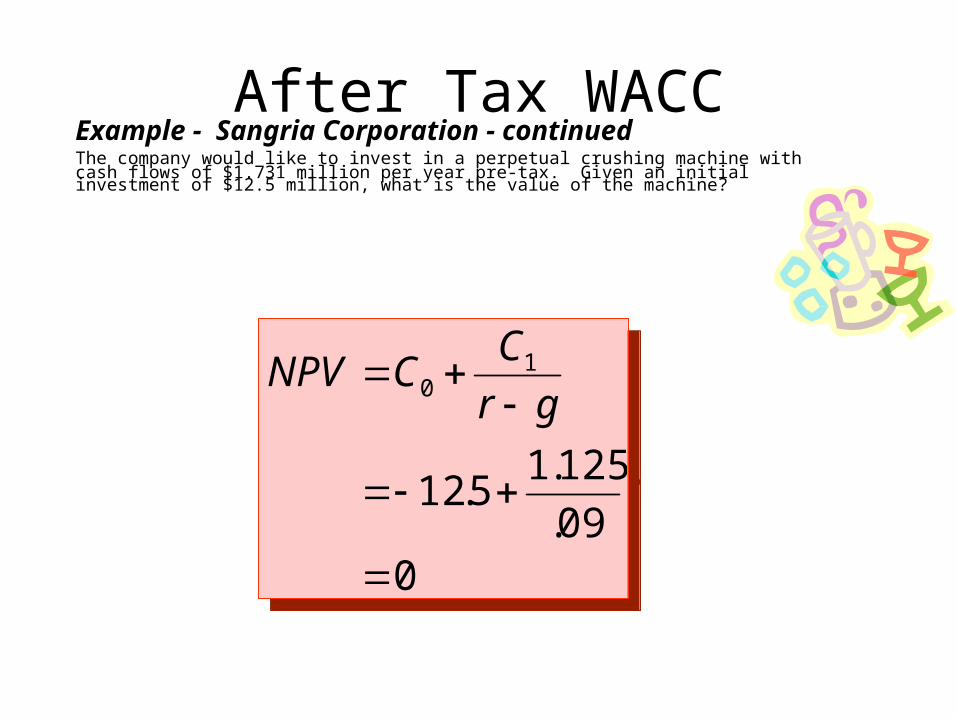

The company would like to invest in a perpetual crushing machine with cash flows of $1.731 million per year pre-tax.

Given an initial investment of $12.5 million, what is the value of the machine?

After Tax WACCExample - Sangria Corporation - continuedThe company would like to invest in a perpetual crushing machine with cash flows of $1.731 million per year pre-tax. Given an initial investment of $12.5 million, what is the value of the machine?

Cash FlowsPretax cash flow 1.731Tax @ 35% 0.606After-tax cash flow $1.125 million

Cash FlowsPretax cash flow 1.731Tax @ 35% 0.606After-tax cash flow $1.125 million

After Tax WACCExample - Sangria Corporation - continuedThe company would like to invest in a perpetual crushing machine with cash flows of $1.731 million per year pre-tax. Given an initial investment of $12.5 million, what is the value of the machine?

009.

125.15.12

10

gr

CCNPV

009.

125.15.12

10

gr

CCNPV

After Tax WACCExample - Sangria Corporation – continued

Perpetual Crusher project

Balance Sheet - Perpetual Crusher (Market Value, millions)Assets 12.5 5.0 Debt

7.5 EquityTotal assets 12.5 12.5 Total liabilities

Balance Sheet - Perpetual Crusher (Market Value, millions)Assets 12.5 5.0 Debt

7.5 EquityTotal assets 12.5 12.5 Total liabilities

After Tax WACCExample - Sangria Corporation – continued

Perpetual Crusher project

93.0195.125.1)1(incomeequity Expected

195.5)35.1(06.)1(interestAfter tax

DTrC

DTr

CD

CD

93.0195.125.1)1(incomeequity Expected

195.5)35.1(06.)1(interestAfter tax

DTrC

DTr

CD

CD

After Tax WACCExample - Sangria Corporation – continued

Perpetual Crusher project

12.4%or 124.5.7

93.0

ueequity val

incomeequity expectedreturnequity Expected

Er

12.4%or 124.5.7

93.0

ueequity val

incomeequity expectedreturnequity Expected

Er

Capital BudgetingValuing a Business or Project• The value of a business or Project is usually

computed as the discounted value of FCF out to a valuation horizon (H).

• The valuation horizon is sometimes called the terminal value.

HH

HH

wacc

PV

wacc

FCF

wacc

FCF

wacc

FCFPV

)1()1(...

)1()1( 22

11

HH

HH

wacc

PV

wacc

FCF

wacc

FCF

wacc

FCFPV

)1()1(...

)1()1( 22

11

Capital Budgeting• Valuing a Business or Project

HH

HH

r

PV

r

FCF

r

FCF

r

FCFPV

)1()1(...

)1()1( 22

11

PV (free cash flows) PV (horizon value)

In this case r = waccIn this case r = wacc

Valuing a BusinessExample: Rio Corporation

Latest year0 1 2 3 4 5 6 7

1 Sales 83.6 89.5 95.8 102.5 106.6 110.8 115.2 118.72 Cost of goods sold 63.1 66.2 71.3 76.3 79.9 83.1 87 90.23 EBITDA (1-2) 20.5 23.3 24.4 26.1 26.6 27.7 28.2 28.54 Depreciation 3.3 9.9 10.6 11.3 11.8 12.3 12.7 13.15 Profit before tax (EBIT) (3-4) 17.2 13.4 13.8 14.8 14.9 15.4 15.5 15.46 Tax 6 4.7 4.8 5.2 5.2 5.4 5.4 5.47 Profit after tax (5-6) 11.2 8.7 9 9.6 9.7 10 10.1 108 Investment in fixed assets 11 14.6 15.5 16.6 15 15.6 16.2 15.99 Investment in working capital 1 0.5 0.8 0.9 0.5 0.6 0.6 0.4

10 Free cash flow (7+4-8-9) 2.5 3.5 3.2 3.4 5.9 6.1 6 6.8

PV Free cash flow, years 1-6 20.3 113.4 (Horizon value in year 6)PV Horizon value 67.6PV of company 87.9

Forecast

Valuing a BusinessExample: Rio Corporation – continued - assumptions

Assumptions

Sales growth (percent) 6.7 7 7 7 4 4 4 375.5 74 74.5 74.5 75 75 75.5 7613.3 13 13 13 13 13 13 1379.2 79 79 79 79 79 79 79

5 14 14 14 14 14 14 14

Tax rate, percent 35%WACC 9%Long term growth forecast 3%

Fixed assets and working capital

Gross fixed assets 95 109.6 125.1 141.8 156.8 172.4 188.6 204.5Less accumulated depreciation 29 38.9 49.5 60.8 72.6 84.9 97.6 110.7Net fixed assets 66 70.7 75.6 80.9 84.2 87.5 91 93.8Depreciation 3.3 9.9 10.6 11.3 11.8 12.3 12.7 13.1Working capital 11.1 11.6 12.4 13.3 13.9 14.4 15 15.4

Valuing a BusinessExample: Rio Corporation – continued

FCF = Profit after tax + depreciation + investment in fixed assets + investment in working capital

FCF = 8.7 + 9.9 – (109.6 - 95.0) – (11.6 - 11.1) = $3.5 million

Valuing a BusinessExample: Rio Corporation – continued

6.3

1.1

23.

1.1

20.

1.1

39.1

1.1

15.1

1.1

96.

1.1

.80-PV(FCF) 65432

6.3

1.1

23.

1.1

20.

1.1

39.1

1.1

15.1

1.1

96.

1.1

.80-PV(FCF) 65432

Valuing a BusinessExample: Rio Corporation – continued

6.67$3.1131.09

1 value)PV(horizon

3.11303.09.

8.6 PV Value Horizon

6

1H

gwacc

FCFH

6.67$3.1131.09

1 value)PV(horizon

3.11303.09.

8.6 PV Value Horizon

6

1H

gwacc

FCFH

Valuing a BusinessExample: Rio Corporation – continued

million $87.9

6.673.02

value)PV(horizonPV(FCF)s)PV(busines

million $87.9

6.673.02

value)PV(horizonPV(FCF)s)PV(busines

WACC & Debt RatiosExample continued: Sangria and the Perpetual Crusher project at 20% D/V

Step 1 – r at current debt of 40%

Step 2 – D/V changes to 20%

Step 3 – New WACC

0984.)6(.124.)4(.06. r

108.)25)(.06.0984(.0984. Er

0942.)8(.108.)2)(.35.1(06. WACC

Adjusted Present Value

APV = Base Case NPV + PV Impact

• Base Case = All equity finance firm NPV• PV Impact = all costs/benefits directly

resulting from project

Example:Project A has an NPV of $150,000. In order to finance the project we must issue stock, with a brokerage cost of $200,000.

Adjusted Present Value

Example:Project A has an NPV of $150,000. In order to finance the project we must issue stock, with a brokerage cost of $200,000.

Project NPV = 150,000Stock issue cost = -200,000Adjusted NPV - 50,000

don’t do the project

Adjusted Present Value

Example:Project B has a NPV of -$20,000. We can issue debt at 8% to finance the project. The new debt has a PV Tax Shield of $60,000. Assume that Project B is your only option.

Adjusted Present Value

Example:Project B has a NPV of -$20,000. We can issue debt at 8% to finance the project. The new debt has a PV Tax Shield of $60,000. Assume that Project B is your only option.

Project NPV = - 20,000Stock issue cost = 60,000Adjusted NPV 40,000

Do the project

Adjusted Present Value

Adjusted Present ValueLatest year

0 1 2 3 4 5 6 7

10 Free cash flow (7+4-8-9) 2,5 3,5 3,2 3,4 5,9 6,1 6 6,8

PV Free cash flow, years 1-6 19,7Pv Horizon value 64,6Base-case PV of company 84,3

Debt 51 50 49 48 47 46 453,06 3 2,94 2,88 2,82 2,761,07 1,05 1,03 1,01 0,99 0,97

PV Interest tax shields 5

APV 89,3

Tax rate, percent 35%Opportunity cost of capital 9,84%WACC (To discount horizon value to year 6) 9%Lomg term growth forecast 3%Interest rate (years 1-6) 6%

After tax debt service 2,99 2,95 2,91 2,87 2,83 2,79

ForecastLatest year0 1 2 3 4 5 6 7

10 Free cash flow (7+4-8-9) 2,5 3,5 3,2 3,4 5,9 6,1 6 6,8

PV Free cash flow, years 1-6 19,7Pv Horizon value 64,6Base-case PV of company 84,3

Debt 51 50 49 48 47 46 453,06 3 2,94 2,88 2,82 2,761,07 1,05 1,03 1,01 0,99 0,97

PV Interest tax shields 5

APV 89,3

Tax rate, percent 35%Opportunity cost of capital 9,84%WACC (To discount horizon value to year 6) 9%Lomg term growth forecast 3%Interest rate (years 1-6) 6%

After tax debt service 2,99 2,95 2,91 2,87 2,83 2,79

Forecast

Example – Rio Corporation APV

Adjusted Present ValueExample – Rio Corporation APV - continued

million

APV

3.89$0.53.84

shields)st tax PV(Intere NPV case Base

million

APV

3.89$0.53.84

shields)st tax PV(Intere NPV case Base