week-7 economic analysis of financial structure & bank failures money and banking econ 311...

TRANSCRIPT

Week-7 Economic Analysis of Financial Structure & Bank Failures

Money and Banking Econ 311Instructor: Thomas L. Thomas

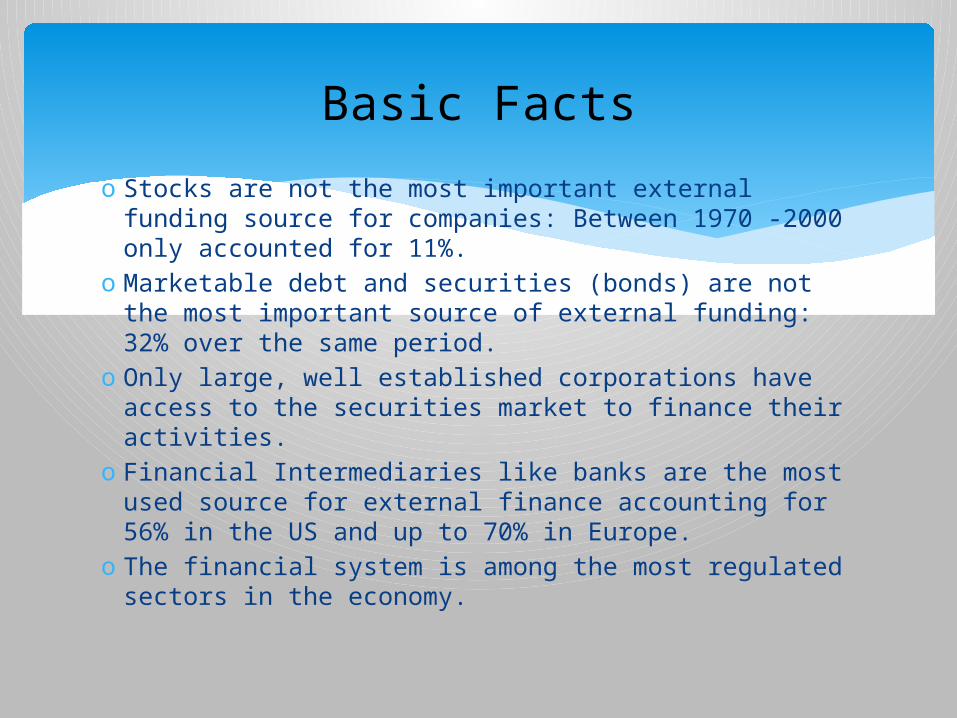

o Stocks are not the most important external funding source for companies: Between 1970 -2000 only accounted for 11%.

o Marketable debt and securities (bonds) are not the most important source of external funding: 32% over the same period.

o Only large, well established corporations have access to the securities market to finance their activities.

o Financial Intermediaries like banks are the most used source for external finance accounting for 56% in the US and up to 70% in Europe.

o The financial system is among the most regulated sectors in the economy.

Basic Facts

Asymmetric Information: Adverse Selection and Moral Hazard

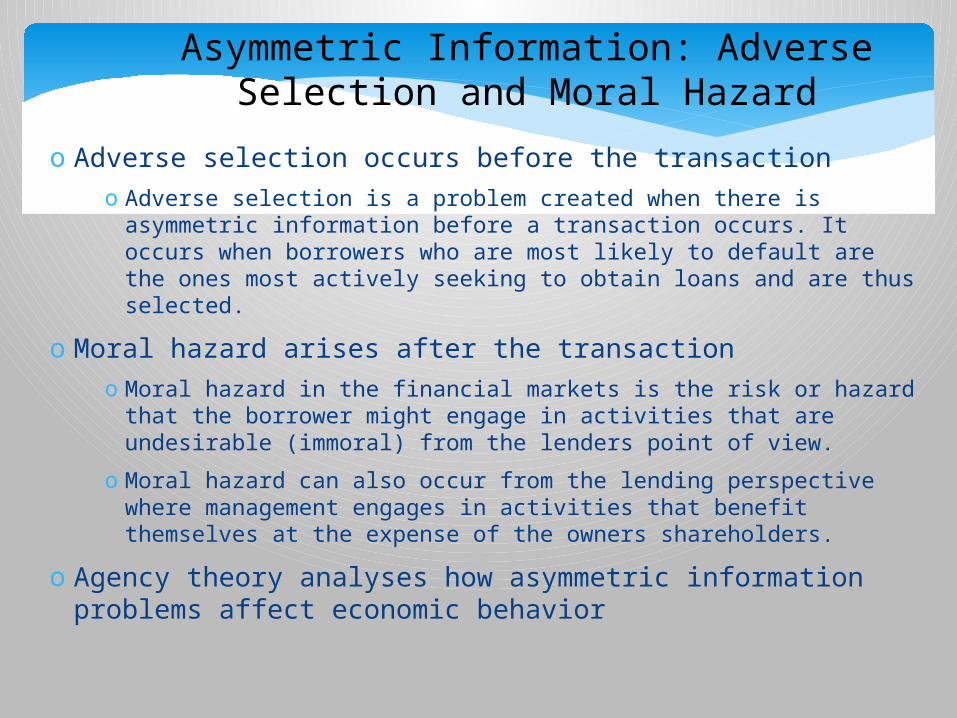

o Adverse selection occurs before the transactiono Adverse selection is a problem created when there is asymmetric information

before a transaction occurs. It occurs when borrowers who are most likely to default are the ones most actively seeking to obtain loans and are thus selected.

o Moral hazard arises after the transactiono Moral hazard in the financial markets is the risk or hazard that the borrower

might engage in activities that are undesirable (immoral) from the lenders point of view.

o Moral hazard can also occur from the lending perspective where management engages in activities that benefit themselves at the expense of the owners shareholders.

o Agency theory analyses how asymmetric information problems affect economic behavior

How Moral Hazard Affects the Choice Between Debt and Equity Contracts

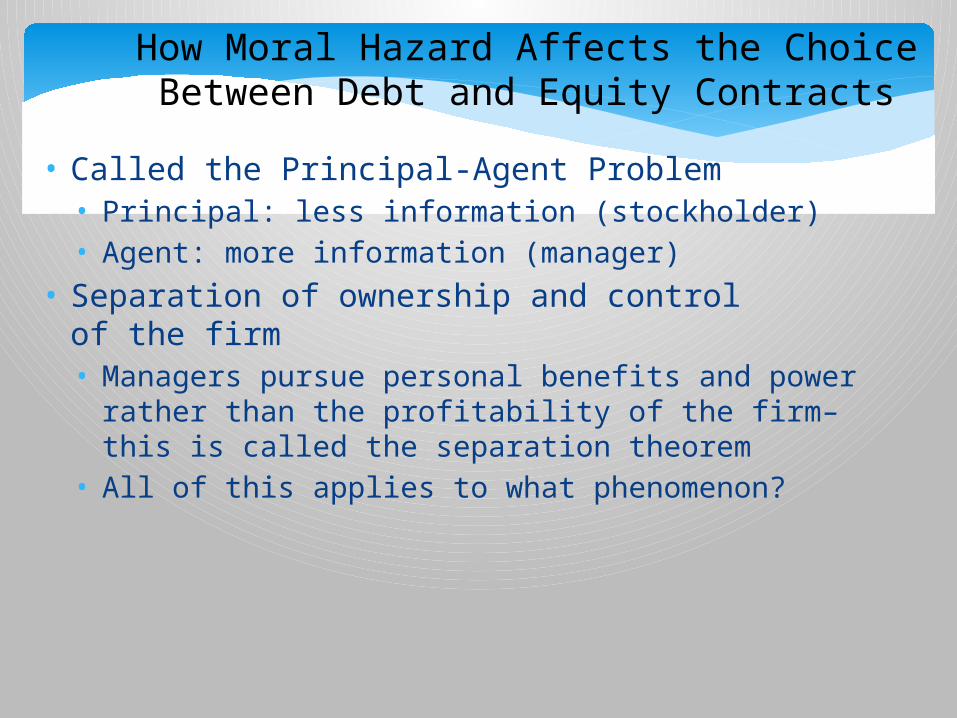

• Called the Principal-Agent Problem• Principal: less information (stockholder)• Agent: more information (manager)

• Separation of ownership and control of the firm• Managers pursue personal benefits and power rather

than the profitability of the firm– this is called the separation theorem

• All of this applies to what phenomenon?

The Lemons Problem: How Adverse Selection Influences Financial Structure

If quality cannot be assessed, the buyer is willing to pay at most a price that reflects the average quality

Sellers of good quality items will not want to sell at the price for average quality

The buyer will decide not to buy at all because all that is left in the market is poor quality items

Similar problems are exhibited in the bond market – Often buyers cannot distinguish good firms with high expected profits and low risk against firms with low expected profit and high risks.

If owners of a good firm have better info on their firm’s performance they will be unwilling to sell stock at an average market price.

The only firms that will be willing to sell at an average market price are high risk low profit firms where the average price is higher than the company’s actual stock value.

Since investors are not stupid and will not want to purchase poor performing stocks they will decide to not to purchase anything thereby retarding the market.

Tools to help solve the problem

One solution to reduce asymmetric information is by supplying more information and details about individuals and firms seeking financing –

Private companies like Standard and Poor’s and Moody’s Investment services specialize in selling such information.

However this does not completely solve the problem. A free-rider problem occurs when people who take advantage of the private information without paying for it (how do they do this).

The free rider – problem prevents the private market from producing enough information to eliminate asymmetry. One way is for the government to release information to help investors distinguish good and bad firms. SEC Filings and GAAP accounting are examples.

What are some examples ?

Note discloser agreements do not always work as some still cheat – give an example?

Financial Intermediation

o Just like used car dealers become experts at looking at a used car and determining its value – financial intermediaries are experts at producing information about firms and individuals who want to borrow money.

o An important element is a bank’s ability to profit from information it produces by not making it public thereby eliminating the free rider problem.

o Banks also exhibit economies of scale thereby reducing transaction costs (give some examples).

o Banks also spread risk though diversification.

Tools to Help Solve Moral Hazard in Debt Contracts

Monitoring and Enforcement of Restrictive Covenants Discourage undesirable behavior Encourage desirable behavior Keep collateral valuable Provide information

o Covenants discourage undesirable behavior – they can be designed to keep the borrower from engaging in risky behavior.

o Covenants encourage desirable behavior – for example cash flow covenants encourage borrowers to engage in activities that maintain sufficient cash flow to pay debt.

o Covenants keep collateral valuable – a covenant to monitor collateral and keep in good condition (like rental property) protects the lender against loss.

o Convents provide information – generally require borrowers to provide financial information in the form of quarterly accounting reports. (Still some moral hazard – why)

Financial Covenants & Moral Hazard

o Studies by AMIR SUFI of he University of Chicago Graduate School of Business suggest that banks provide credit lines that are contingent on maintenance of cash flow.

o Coverage covenants, are the most common financial covenant (70%) which are written on a measure of cash flow divided by interest, debt service, or fixed charge expense.

o Reductions in cash flow lead to covenant violations, which in turn lead to a restriction in the availability of a line of credit.

o when a firm violates a covenant, it loses access to a substantial portion of its line of credit.

o In terms of magnitudes, a covenant violation is associated with a 15 to 30% drop in the availability of both total and unused lines of credit.

Financial Covenants Reduce Exposure

o Collateral is a prevalent feature of debt contracts for both households and business. o Collateral is property that is pledged to the lender to

guarantee payment in the event of default. Collateralized debt is called a secured transaction. (Note the importance of seniority)

o Debt that is not guaranteed with collateral like a credit card is called unsecured transaction.

o The primary sources of repayment is three fold – What are they?

Collateral

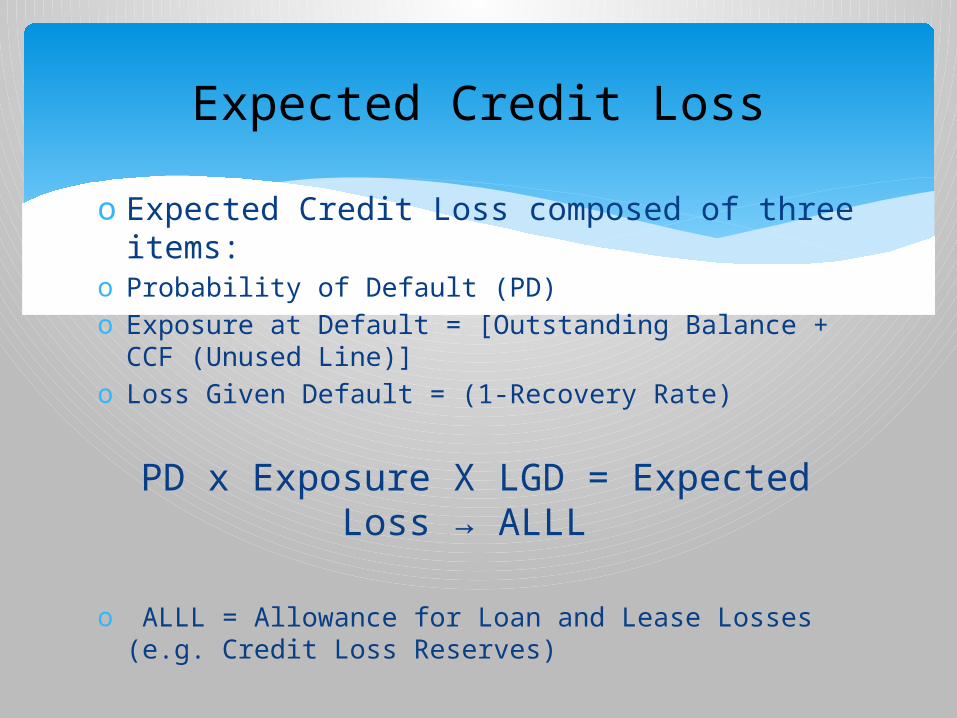

o Expected Credit Loss composed of three items:o Probability of Default (PD)o Exposure at Default = [Outstanding Balance + CCF (Unused Line)]o Loss Given Default = (1-Recovery Rate)

PD x Exposure X LGD = Expected Loss → ALLL

o ALLL = Allowance for Loan and Lease Losses (e.g. Credit Loss Reserves)

Expected Credit Loss

What is a Financial Crisis? A financial crisis occurs when there is a particularly large disruption to

information flows in financial markets, with the result that financial frictions increase sharply and financial markets stop functioning

Asset Markets Effects on Balance Sheets Stock market decline

Decreases net worth of corporations. Unanticipated decline in the price level

Liabilities increase in real terms and net worth decreases. Unanticipated decline in the value of the domestic currency

Increases debt denominated in foreign currencies and decreases net worth.

Asset write-downs.

Factors Causing Financial Crises

Deterioration in Financial Institutions’ Balance Sheets Decline in lending.

Banking Crisis Loss of information production and disintermediation.

Increases in Uncertainty Decrease in lending.

Factors Causing Financial Crises (cont’d)

Increases in Interest Rates Increases adverse selection problem Increases need for external funds and therefore adverse selection

and moral hazard. Government Fiscal Imbalances

Create fears of default on government debt. Investors might pull their money out of the country.

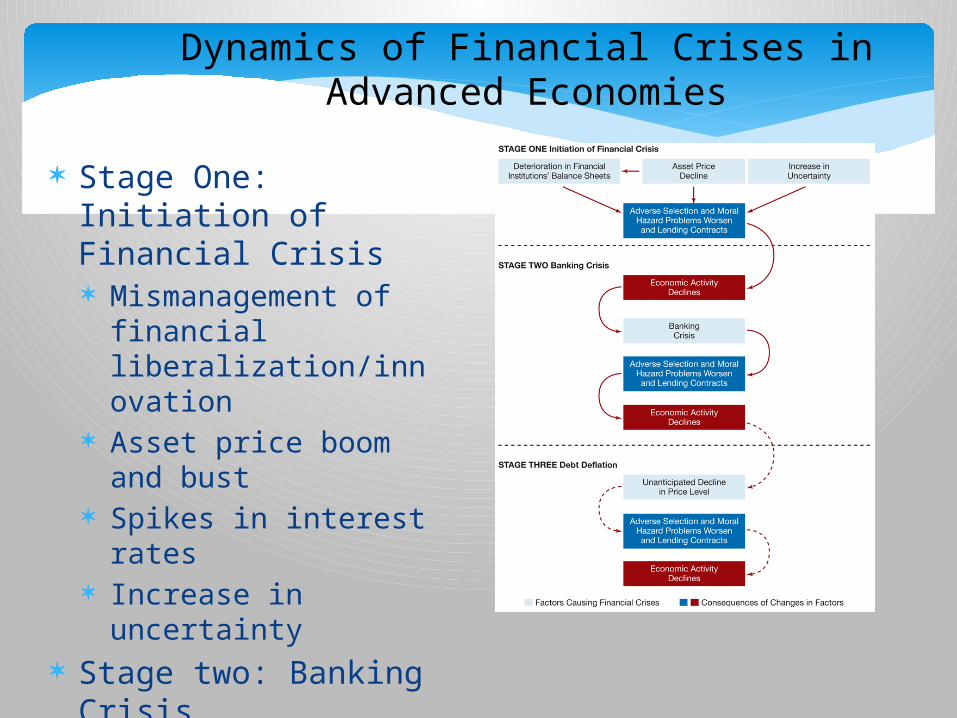

Dynamics of Financial Crises in Advanced Economies

Stage One: Initiation of Financial Crisis Mismanagement of

financial liberalization/innovation

Asset price boom and bust Spikes in interest rates Increase in uncertainty

Stage two: Banking Crisis Stage three: Debt Deflation

Dynamics of Financial Crises in Advanced Economies

o Stage two: Banking Crisiso Deteriorating Balance Sheets and tougher lead some

financial institution’s net worth to a negative position. o Unable to pay depositors and creditors can lead to a bank

panic in which multiple banks fail.o Moreover uncertainty about the health of the banking

system can lead to bank runs on good as well as bad banks leading called contagion – why

o With fewer banks information about the creditworthiness of borrowers disappears increasing adverse selection and moral hazard deepening the financial crisis.

Dynamics of Financial Crises in Advanced Economies

o Stage three: Debt Deflationo If the economic downturn leads to a sharp decline in the

aggregate price level it can short-circuit the a recovery.o This is called debt deflation where a substantial unanticipated

decline in the price level sets in leading to a further deterioration in a firm’s net worth because of the increase in the burden of debt.

o Due to the decline in the net worth of borrowers from a drop in price levels causes an increase in adverse selection and moral hazard problems facing lenders.

Bank Failures of the 1980s and 1990s

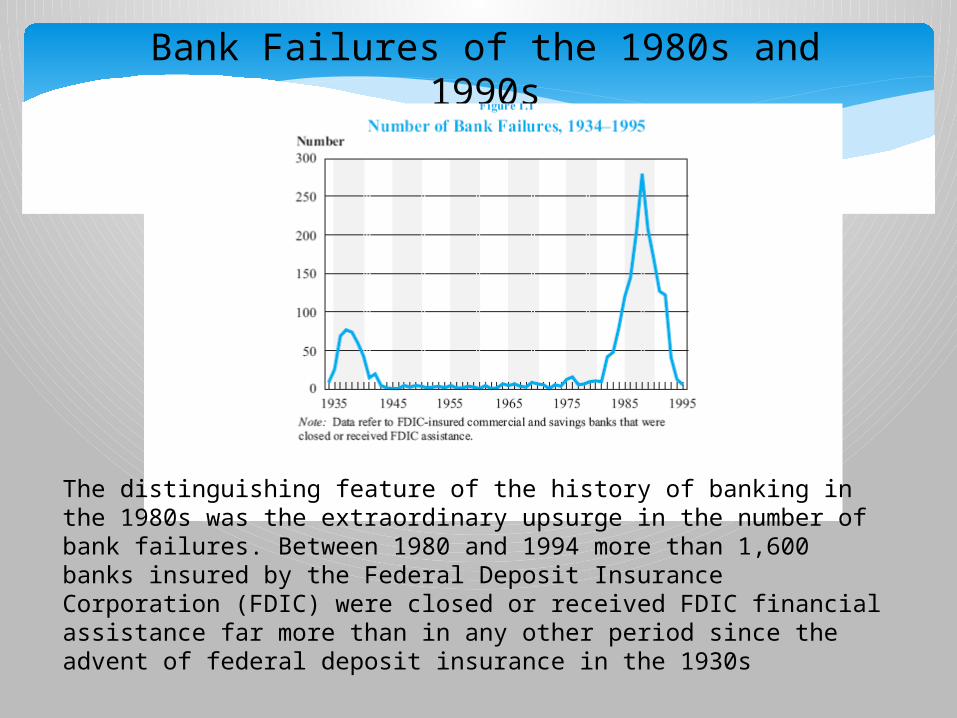

The distinguishing feature of the history of banking in the 1980s was the extraordinary upsurge in the number of bank failures. Between 1980 and 1994 more than 1,600 banks insured by the Federal Deposit Insurance Corporation (FDIC) were closed or received FDIC financial assistance far more than in any other period since the advent of federal deposit insurance in the 1930s

Common Characteristics 80s & 90S Bank Failures

1. Each followed a period of rapid expansion; in most cases, cyclical forces were accentuated by external factors.2. In all four recessions, speculative activity was evident. .Expert. opinion often gave support to overly optimistic expectations.3. In all four cases there were wide swings in real estate activity, and these contributed to the severity of the regional recessions.4. Commercial real estate markets in particular deserve attention because boom and bust activity in these markets was one of the main causes of losses at both failed and surviving banks.

Common Characteristics 80s & 90S Bank Failures

• Yet on the eve of the 1980s most banks gave few obvious signs that the competitive environment was becoming more demanding or that serious troubles lay ahead.

• At banks with less than $100 million in assets (the vast majority of banks), net returns on assets (ROA) rose during the late 1970s and averaged approximately 1.1 percent in 1980.a level that would not be reached again until 1993.

Large banks, however, showed clearer signs of weakness. In 1980 ROA and equity/assets ratios were much lower for banks with more than $1 billion in assets than for small banks and were also well below the large-bank levels they would reach in the early 1990s.

For the 25 largest bank holding companies in the late 1970s and early 1980s, the market value of capital decreased relative to and fell below its book value, suggesting that to investors, the franchise value of large banks was declining.

Common Characteristics 80s & 90S Bank Failures

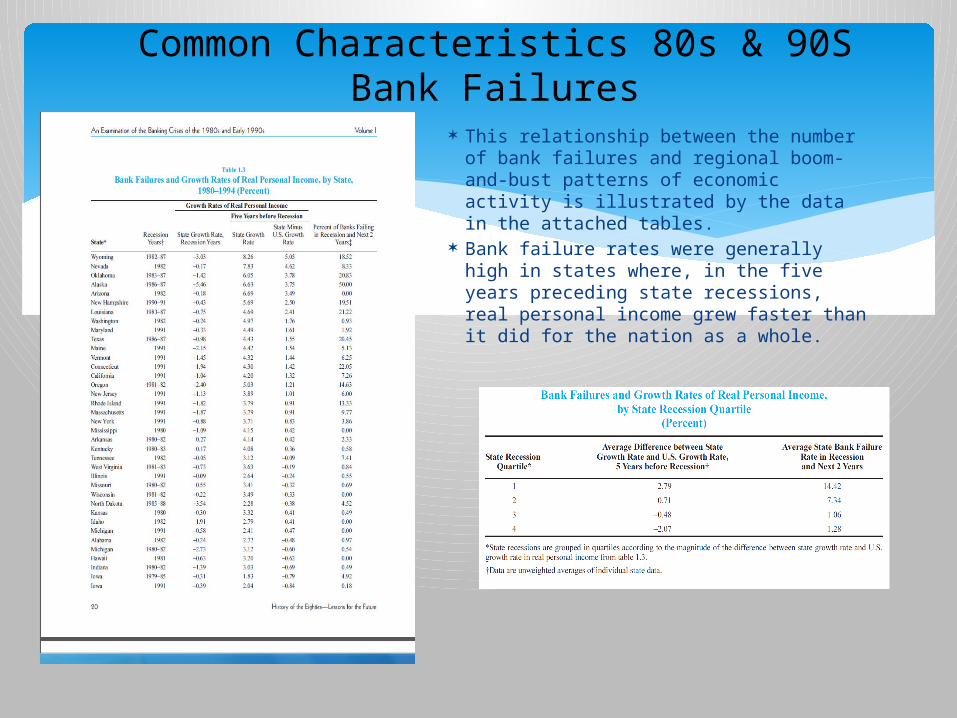

This relationship between the number of bank failures and regional boom-and-bust patterns of economic activity is illustrated by the data in the attached tables.

Bank failure rates were generally high in states where, in the five years preceding state recessions, real personal income grew faster than it did for the nation as a whole.