welcome to the webinar! we will start within a few · worldwide • network of 50.000+ solar pv ......

TRANSCRIPT

Welcome to the webinar!

We will start within a few minutes

Agenda• Introduction

Shushan Khachatryan (Solarplaza)

• Dive into the dynamic and evolving Solar PV market in Asia; Which markets are the most promising for the year ahead

Benjamin Attia– GTM Research

• Tracking country investment attractiveness for solar energy; Strategies to create bankable PV projects in Asia

Rohan Singh

• Q&A

• End of the webinar

Unlocking Solar Capital Asia

28-29 September 2017 /// Singapore

200+ executives connect and engage in in-depth discussions to solve LATAM's solar energy funding gap - and get projects realized

• 200+ international finance and project development executives

• Regional focused approach: Covering all countries from Southeast Asia to Central Asia

• 50+ leading experts on stage sharing their vision, expertise and experience

• Guaranteed match-making through our customized software, interactive breaks and a matchmaking session

• Established in 2004

• 80 events organized

• In 25+ countries worldwide

• Network of 50.000+ solar PV professionals

About Solarplaza

"Empowering professionals in solar business development by building the most valuable solar PV network"

Practical notes

• Technical issues? Use chatbox

• The presentation slides will be available afterwards

Benjamin Attia

• ANALYST- GTM RESEARCH

Rohan Singh

• MANAGING PARTNER ASIA - FINERGREEN

Q&A time

Website: asia.unlockingsolarcapital.com

Shushan Khachatryan

• Email: [email protected]

• Skype: shushan.solarplaza

• Phone: +31 10 302 7909

The Solar Future NL18 May 2017Baarn, The Netherlandswww.thesolarfuture.nl

Upcoming Events

Unlocking Solar Capital Asia28-29 September 2017

Singapore

asia.unlockingsolarcapital.com

Renewable Energy Trade Mission Iran17-21 September 2017Tehran, Iranwww.retrademissioniran.com

Solar Asset Management Asia8-9 June 2017

Tokyo, Japan

www.solarassetmanagement.asia

Unlocking Solar Capital LATAM15-16 June 2017

Miami, USA

latam.unlockingsolarcapital.com

Overview of Asian Solar PV Market and Financing Opportunities

SolarPlaza Webinar: Unlocking Solar Capital Asia

Benjamin Attia

Analyst, Global Solar Demand

12 May 2017

1

GTM Research is the premier market intelligence provider on the

decarbonization and decentralization of energy

CleanGeneration

GridModernization

CustomerEvolution

We guide companies leading

the electricity transformation

GTM RESEARCH

2

GTM RESEARCH

UpstreamFrom production to shipments of modules

Solar Research End-to-end coverage of the global solar market

Ingot

Wafer Cells

Polysilicon

Solar Systems & TechnologiesTo the components and costs of solar systems

DownstreamTo installations, and what’s driving them

• Inverters

• Racking

• Soft costs

• Emerging technologies

• Demand

• Competitive Landscape

• Policy & Regulatory

• System Economics

3

Q2 2017 Regional Demand Outlook: Asian Markets Comprise 65% of Global Demand

Global PV Demand by Region, 2007-2022E

6.8 7.7 8.8 10.0 12.1 13.9 15.3

44.3 41.3 37.9 35.3 30.8 28.7 28.3

5.3 10.2 10.0 11.3 13.2 15.1 15.72.0

2.0 2.6 3.2 4.2 5.3 6.51.8

2.8 5.1 7.0 9.09.6

11.21.6

2.4 5.87.1

7.89.7

11.5

15.513.1

12.014.2

16.418.0

19.4

0.60.9

1.31.7

1.9

2.4

3.0

0.6 0.9

1.21.4

1.7

2.0

77.8 80.984.5

91.196.8

104.4112.8

0

20

40

60

80

100

120

140

2016 2017E 2018E 2019E 2020E 2021E 2022E

An

nu

al In

stal

led

PV

(G

Wd

c)

Europe East Asia South Asia Southeast Asia MENAT Latin America North America Sub-Saharan Africa West Africa

Cumulative Forecast 2017-2022 = 572.9 GW

2017-2022E CAGR = 6.9%

4

Poll: Nearly all Asian solar markets are FIT-driven. Can FITs in emerging economies support long-term sustainable market growth?

Yes, FITs provide a predictable and stable incentive.

Yes, but only with long-term political commitment to renewables.

No, the FIT era is being replaced by competitive procurement and

represents necessary but burdensome policy.

No, policy uncertainty around Asian FITs introduces too much risk.

–A

–B

–C

–D

5

FITs in Southeast Asia Vary in Differential Relative to Power Prices

$0.078 $0.075

$0.217

$0.080 $0.091

$0.079

$0.194

$0.097

$0.077 $0.081

$0.172

$0.069

$0.152

$0.175

$0.153

$0.090

$0.00

$0.05

$0.10

$0.15

$0.20

$0.25

Malaysia Indonesia Philippines Vietnam

USD

/kW

h

Residential Commercial Industrial Average FIT

Residential, Commercial, and Industrial Retail Power Prices and Average Solar FIT, USD/kWh

6

29 Reverse Auction or Tender Procurement Programs Launched or Planned in 2017 so far

*Some markets not pictured due to scale: Bermuda, Cape Verde, CaymanIslands, El Salvador, French West Indies, Martinique, Palestine, Singapore, Qatar

Global: Markets With Tendering or Auction Schemes in Place, Under Discussion, or in Planning Stages, Q2 2017*

Tendering or Auction Scheme in Place

Tendering or Auction Scheme Discussed or Planned

By the numbers:

48 national markets where

tendering or auction scheme is in place, up from 32 in H2 2016

25 national markets where

tendering or auction scheme has been discussed or planned, up from 14 in H2 2016

Source: GTM Research Global Solar Demand Monitor Q2 2017

7

• East Asia: Demand peaked in

2016 at 44.3 GW

• China: Record-breaking 2016

with 34.23 GW installed

• Japan: Policy shift in Japan

restrains future growth, peaked

in 2015

• Australia: Utility-scale boom

through 2019 driven by Large-

Scale RET

• Taiwan: Aggressive targets and

local manufacturing contribute to

robust market

East Asia: China Far Exceeded Expectations in 2016, but Regional Growth Outlook Is Weak

East Asia PV Demand, 2016-2022E

15.1

34.231.5

28.726.6

24.1 22.1 21.4

10.9

7.8

7.1

5.6

4.2

3.32.8 2.5

27.7

44.3

41.3

37.935.3

30.828.7 28.3

25%

60%

-7% -8%-7%

-13%

-7%-1%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

0

5

10

15

20

25

30

35

40

45

50

2015 2016 2017E 2018E 2019E 2020E 2021E 2022E

GW

dc

China Japan Australia Taiwan Rest of East Asia Annual Growth

Cumulative Forecast 2017-2022 = 202.4 GW

2017-2022E CAGR = -7.3%

Source: GTM Research Global Solar Demand Monitor Q2 2017

8

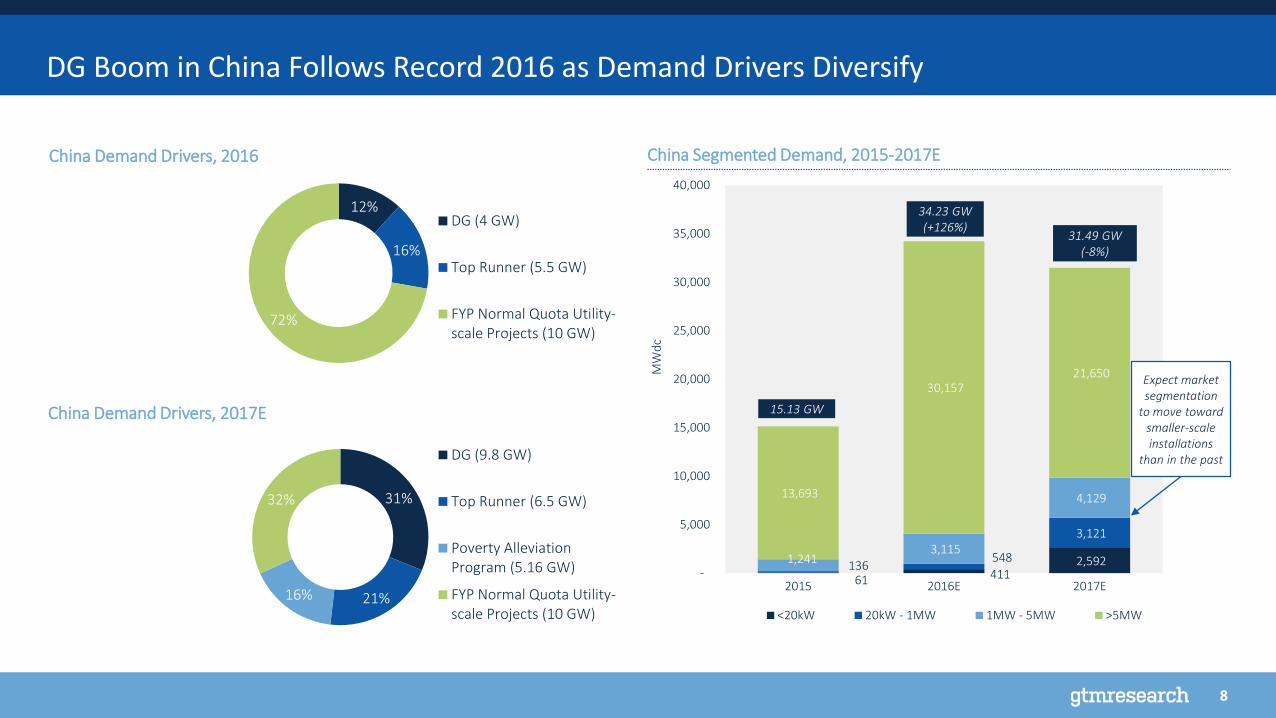

DG Boom in China Follows Record 2016 as Demand Drivers Diversify

61 411 2,592 136

548

3,121

1,241 3,115

4,129 13,693

30,157 21,650

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2015 2016E 2017E

MW

dc

<20kW 20kW - 1MW 1MW - 5MW >5MW

15.13 GW

34.23 GW(+126%)

31.49 GW(-8%)

Expect market segmentation

to move toward smaller-scale installations

than in the past

China Segmented Demand, 2015-2017E

12%

16%

72%

DG (4 GW)

Top Runner (5.5 GW)

FYP Normal Quota Utility-scale Projects (10 GW)

China Demand Drivers, 2017E

China Demand Drivers, 2016

31%

21%16%

32%

DG (9.8 GW)

Top Runner (6.5 GW)

Poverty AlleviationProgram (5.16 GW)

FYP Normal Quota Utility-scale Projects (10 GW)

9

Scenario 1: FITs remain and step

down gradually, slowly replaced with

competitive procurement to stem

curtailment and combat

backpayment issues. Behind-the-

Meter DG boom.

Scenario 2: Instead of next FIT cut

cycle on June 30, 2018, FIT is

scrapped entirely and NEA shifts

entirely to centrally managed

competitive reverse auction

program. Could lead to massive

installation rush in Q4.

NEA’s Opaque Policy Environment Leaves Two Likely Scenarios for Chinese Demand

34230 33,413

30,221

27,980

25,450

23,439 23,013

31,492

28,673

26,572

24,100

22,112 21,387

24,563

19,784

17,538 15,665 15,036 14,330

50

5,050

10,050

15,050

20,050

25,050

30,050

35,050

40,050

2016 2017E 2018E 2019E 2020E 2021E 2022E

MW

dc

Inst

alle

d

Upside Scenario Base Scenario Downside Scenario

2017-2022 Potential Upside = 9.1GW2017-2022 Potential Downside = 47.5 GW

CAGR = -7.2%

CAGR = -10.2%

CAGR = -7.4%

China PV Demand Scenarios, 2017-2022

10

2077 1927 20611539 1427 1129 1270 1144 1028 925

2764

4389 4298

2942 27122144 1693

1340 1166 1050

1467

24993497

27982498

1975

1058

653500 450

158

501

1050

486500

395

212

13183

75

6,467

9,316

10,905

7,765 7,136

5,643

4,232

3,267 2,777 2,499

-

2,000

4,000

6,000

8,000

10,000

12,000

2013 2014 2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E

MW

dc

Inst

alle

d

<20kW 20kW - 1MW 1MW - 5MW >5MW

Japan PV Demand, 2013-2022E

Source: GTM Research Global Solar Demand Monitor Q1 2017

Challenge of land access and labor costs will limit potential

for development of >5 MW projects

Tendering + FIT regime begins on April 1, 2017

Japan: Uncertainty Surrounding Policy Shift Likely to Spawn a Healthy Secondary Market

• METI’s Competitive Reverse

Auction Program is capping new

demand

• Over half of the massive >50 GW

FIT-approved pipeline cancelled

• First auction expected next

quarter, 500 MW, ceiling price 21

¥/kWh

• 2017-2022E: -19% CAGR

11

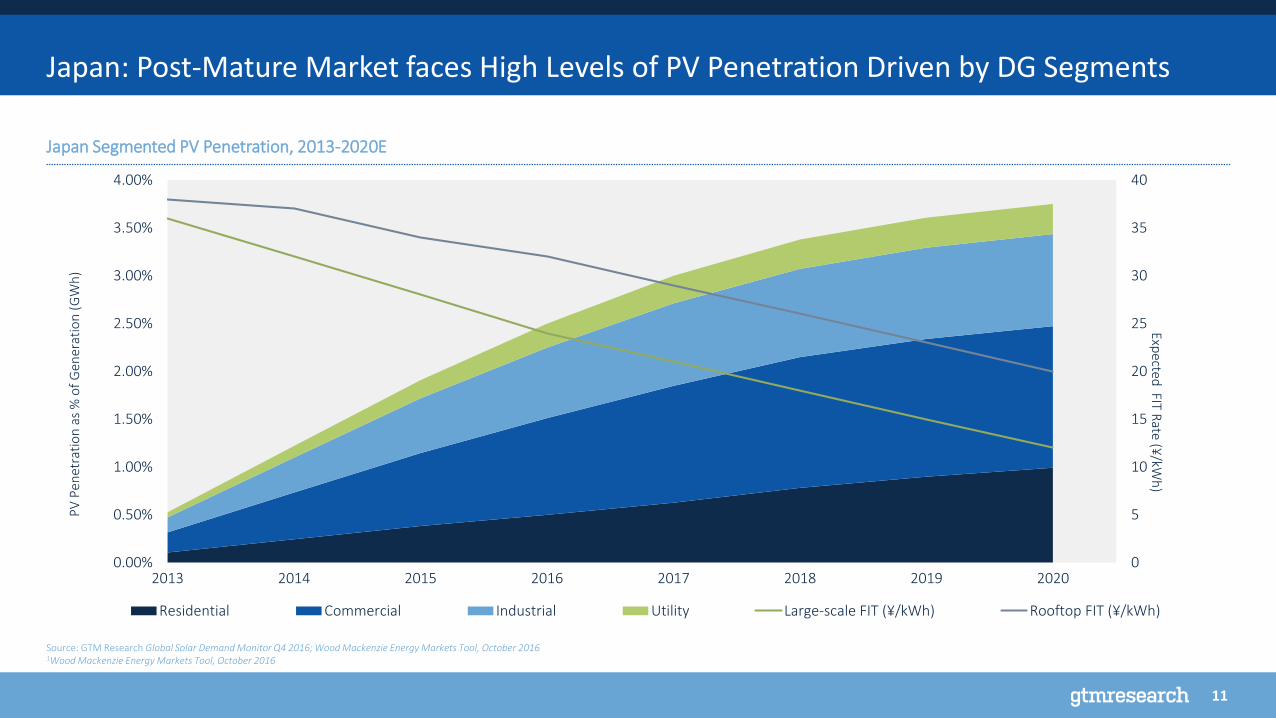

Japan: Post-Mature Market faces High Levels of PV Penetration Driven by DG Segments

Source: GTM Research Global Solar Demand Monitor Q4 2016; Wood Mackenzie Energy Markets Tool, October 20161Wood Mackenzie Energy Markets Tool, October 2016

Japan Segmented PV Penetration, 2013-2020E

0

5

10

15

20

25

30

35

40

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

2013 2014 2015 2016 2017 2018 2019 2020

Expected

FIT Rate (¥

/kWh

)

PV

Pen

etra

tio

n a

s %

of

Gen

erat

ion

(G

Wh

)

Residential Commercial Industrial Utility Large-scale FIT (¥/kWh) Rooftop FIT (¥/kWh)

12

2.1

4.9

9.4 8.910.0

11.613.0 13.2

0.2

0.2

0.50.6

0.8

0.9

1.1 1.3

2.2

5.3

10.2 10.0

11.3

13.2

15.115.7138%

136%

92%

-1%

13%17% 14%

4%

-20%

0%

20%

40%

60%

80%

100%

120%

140%

160%

0

2

4

6

8

10

12

14

16

18

2015 2016 2017E 2018E 2019E 2020E 2021E 2022E

GW

dc

India Pakistan Bangladesh Rest of South Asia Annual Growth

South Asia: 92% Growth in India Drives the Region, Reaching 15 GW Annually by 2021

Source: GTM Research Global Solar Demand Monitor Q1 2017

South Asia PV Demand, 2016-2022E

Cumulative Forecast 2017-2022 = 75.5 GW

2017-2022E CAGR = 9.1%

• India is set to become the third

largest global market in 2017

• Aggressive tender bid

competition at Rewa and Bhadla

(Rs. 2.62/kWh), lowest global

module prices leading to margin

squeeze

• Pakistan has over 2.4 GW utility-

scale pipeline, NEPRA tenders

coming later this year

• Financing risks surrounding lack

of local debt and tight margins

for EPCs

13

India Doubled Its Solar Parks Target to 40 GW Amid Infrastructure Delays

Source: SECI, GTM Research Global Solar Demand Monitor Q1 2017

India’s Solar Parks Approved Capacity by State, Q1 2017

4000

3351

2750

2000

1500

1000 1000

700600

500 500 500 500 500 499

200

0

500

1000

1500

2000

2500

3000

3500

4000

4500

Capacity (MW)

MW

Ap

pro

ved

Andhra Pradesh Rajasthan Madhya Pradesh Karnataka Maharastra Himachal Pradesh Odisha Gujarat

Uttar Pradesh Chhattisgarh Haryana Tamil Nadu Telangana West Bengal Other States Kerala

14

• Southeast Asia: Policy uncertainty in

Thailand, the Philippines, Malaysia,

Indonesia, and Vietnam limits

region’s growth potential

• Vietnam: Local cell manufacturing

capacity and ripe market conditions

have materialized into a 5 GW

pipeline, but Decision 11 introduces

major project risks.

• Thailand: Despite only 40%

subscription to the self- consumption

program, Thailand will install 4.6 GW

by 2022. Agriculture Co-op program

tender could see over 500 MW.

• Malaysia: NEM Policy and utility-

scale tenders feed expectation that

national target will be well exceeded.

Southeast Asia: Foreign Investment in Thailand, Malaysia Is Driving 6.5 GW Market by 2022

Source: GTM Research Global Solar Demand Monitor Q2 2017

Southeast Asia PV Demand, 2016-2022E

Cumulative Forecast 2017-2022 = 25.73 GW

2017-2022E CAGR = 21.9%

0.7 0.8 0.9 1.0 1.1 1.2 1.40.7

1.00.4

0.6 0.70.8

0.91.1

0.30.4

0.40.5

0.7

0.8

0.2

0.30.5

0.7

0.9

1.2

0.3

0.4

0.7

1.1

1.5

2.1

1.1

2.0 2.0

2.6

3.2

4.2

5.3

6.5

59%

82%

2%

32%

22%

30%

27% 23%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0

1

2

3

4

5

6

7

2015 2016 2017E 2018E 2019E 2020E 2021E 2022E

GW

dc

Philippines Thailand Malaysia Indonesia Rest of Southeast Asia Annual Growth

15

Philippine Approved Solar Projects Pipeline is over 4 GW

Source: SECI, GTM Research Global Solar Demand Monitor Q2 2017, Department of Energy

Philippines Department of Energy Approved Project Pipeline, 2017

0

65.7

28.515

338

465

1179

0 200 400 600 800 1000 1200 1400

Mindanao

Visayas

Luzon

MWdcApproved COD H1 2017

The Department of Energy also has over 2.13 GW of

pending project applications

16

Over Two-Thirds of Vietnam’s >5 GW Announced Pipeline is from Local Developers

Source: SECI, GTM Research Global Solar Demand Monitor Q1 2017

Investment Origin for Vietnam’s 5,064 MW Pipeline, Q2 2017

68%

16%

10%

3% 2%

1%

Vietnam

South Korea

United States

Canada

India

China

AES Corporation (United States) has been granteda license to develop 300-500 MW in the Dak Lak region

Led by EVN and Xuan ThienDaklak for over 3.1 GW of Vietnam’s announced pipeline

South Korean investment announcements total 844 MW, from the likes of Hanwa Qcells, ShinsungSolar, and Solkiss.

17

Key Takeaways and Stats:

• Asian Markets will comprise 65% of Global PV Demand in 2017.

• China’s NEA holds significantly concentrated power over the global supply-demand balance, but

demand drivers are diversifying, reducing risk and increasing allocation transparency.

• India is set to be the third largest global market in 2017 with 9.4 GW of demand.

• Most Asian demand is still FIT-driven, though the transition to competitive procurement is being led

by Malaysia, Japan, and Thailand.

• Policy uncertainty around Decision 11 in Vietnam and Minister Decree No. 12/2017 in Indonesia, as

well as the non-renewal of Round 3 FITs in the Philippines are introducing risk to large multi-GW

pipelines.

Wrap Up: Enormous Opportunity in Asian Markets, but Limited by Policy Uncertainty

5

3

2

1

4

Prepared For:

12 May 2017

Analyst, Global Solar Markets

Benjamin Attia

Thank you!

@solarbenattia

Strategic Advisory

Debt Advisory

Equity Advisory

Str

ictly c

on

fidential

SOLARPLAZA WEBINAR

Overview of Asian Solar PV market and Financing opportunities

12/05/17

FINERGREEN| NEW ENERGY FINANCIAL ADVISORS

FINERGREEN

ACTIVITIES

Debt advisory Debt structuring

Support in negotiation

Due Diligences & legal documentation monitoring

Equity advisory Buy-side / Sell-side equity advisory on

greenfield and brownfield projects

Sourcing of investors in the Renewable Energy sector

Strategic advisory

Enterprise valuation

Market screening & target selection

Support in negotiation & advisors coordination

FINERGREEN is a French financial advisor, founded in 2013 and dedicated to renewable energies and energy efficiency projects (solar, wind, biogas, hydroelectricity).

GEOGRAPHICAL COVERAGE

459 M €

CLOSED TRANSACTIONS

706 PLANTS

FINANCED PROJECTS

215 MWp

DELIVERED POWER

2

FINERGREEN| NEW ENERGY FINANCIAL ADVISORS

ASIA – CONTEXT

900 500

STRONG AMBITIONS except… ▶ Access to financing solutions remains difficult to small

or mid-size projects.

▶ Local developers used to have a strong footprint but face a lack of experience in renewables deals structuring.

▶ New additional sources of financing should inflow the

Asian continent and respond therefore to this growing demand

▶ Provide guidance to project developers to structure their projects so as to be in line with international standards will be a key component to the bankability of the project

GW to be installed by 2030

million people to give electricity access to

147 bn USD/year required to invest

in renewables

3

FINERGREEN| NEW ENERGY FINANCIAL ADVISORS

ASIAN SOLAR INVESTMENT ATTRACTIVENESS

4

MONGOLIA

CHINA

VIETNAM

INDIA

SRI LANKA

MYANMAR

INDONESIA

PHILIPPINES

THAILAND

LAOS CAMBODIA

MALAYSIA

20-25% electricity generation by 2020

Feed-in-tariff

9% capacity from RE by 2018

Auctions, tax benefit

100% target by 2030 FiT enacted in 1997 Capital subsidies

15-18% target by 2020 Tax benefits

2 GW PV by 2020 Feed-in-tariff

800 MW PV by 2020 Feed-in-tariff 100% RE target

110 GW capacity by 2020

Feed-in-tariff

700MW PV by 2025 <1% RE share in 2017

1.35 GW PV by 2020 Feed-in-tariff

500 MW PV by 2020 Feed-in-tariff

5 GW PV by 2025 Feed-in-tariff

30% target by 2025

FINERGREEN| NEW ENERGY FINANCIAL ADVISORS

ASIAN SOLAR CAPITAL ATTRACTIVENESS

5

A broad range of diverse sources of funding can help bridging the gap with the capital requirements

FEW EXAMPLES

Pakistan’s hydropower plant USD 955m.Sukuk issue marked one of the largest infrastructure deals in the country to use Islamic financing

Meezan Bank Pakistan finances energy projects Alternative financing solutions available with Multilateral institutions State Bank of Pakistan SBP Financing Scheme for Renewable Energy

Malaysian government encourages Sharia’-compliant financing Energy related financing:

Green Technology Financing Scheme: The scheme could benefit companies who are producers and users of green technology.

New institutions Asian Infrastructure Investment Bank (AIIB), New Development Bank Green Sukuk scheme which promotes and develop Shari'ah-compliant financial products to

invest in climate change solutions National Rural and Renewable Energy Programme (NRREP), Scaling Up Renewable Energy

Programme in Low Income Countries (SREP), ElectriFI encouraged by the European Union… Development of additional commercial banks locally that could provide project financing

solutions

Pakistan

Malaysia

FINERGREEN| NEW ENERGY FINANCIAL ADVISORS

WHAT BANKABILITY REFERS TO? (1/2)

6

Financial parameters

Regional specificities

Technology & Strong

know-how

Makes the project financially viable until completion

Careful selection of clients / project developers based on their past experience

Give attention to all the assumptions including potential change in regulation (i.e. introduction of GST in India….)

Financing mechanism

Explore all sources of capital available for the project

Enables to adapt the technology at the local/regional level

How the product/plant will operate over its lifespan

Are there any guarantees or certification standards that verify the product/plant will work

Combines centralized processes and locally delegated tasks supported both by

local & international entities

How the non-recourse financing solutions is adaptable in Asian landscape?

What are the regional components differences from matured markets or other emerging countries?

FINERGREEN| NEW ENERGY FINANCIAL ADVISORS

WHAT BANKABILITY REFERS TO ? (2/2)

7

A solar PV project is considered bankable if lenders are willing to finance it taking into account:

SERVICE PROVIDERS

•Certified technology •Secured energy yields &

economic returns

INVESTORS

•Tax incentives •Project stability •Risks & Mitigants •Legal, technical & economic securities

PROJECT DEVELOPERS

•Track record •Attractiveness for investors / banks •Project stability

MODULE PRODUCERS

•Track record •Tier-1, 2…

•Certified quality

LENDERS

KEY CRITERIAS

Stable & predictable cash-flows

Coverage ratios satisfied (DSCR, DSRA…)

Non or limited-recourse finance

Leverage ratio taking into account the exposure reached by the lender in terms of country exposure, sub-sector exposure, credit rating exposure…

Risks & mitigations

Guarantees

FINERGREEN| NEW ENERGY FINANCIAL ADVISORS

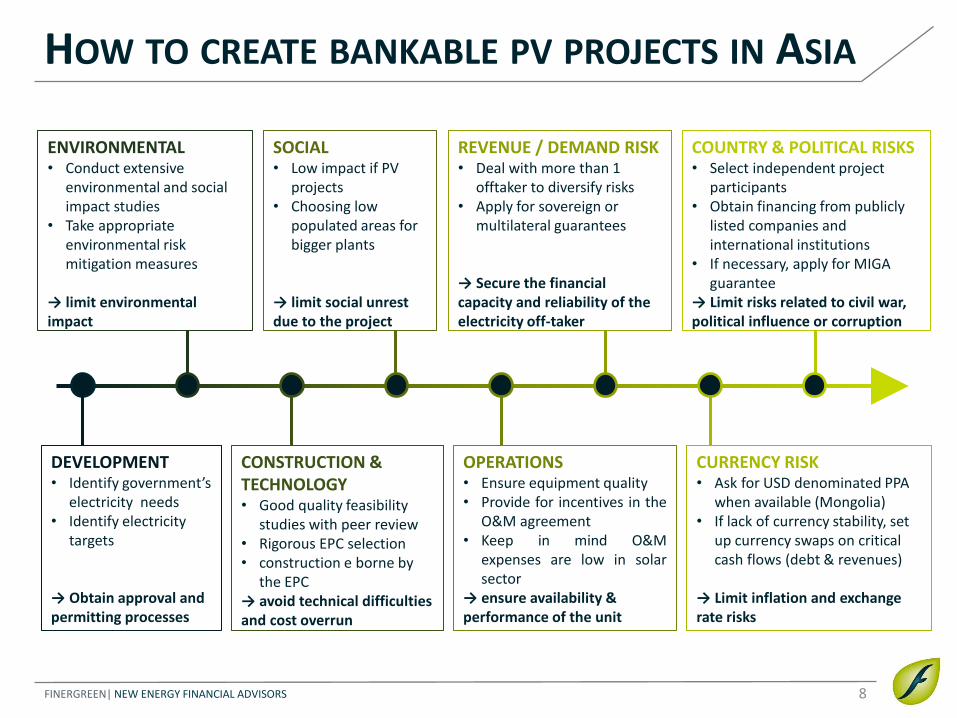

HOW TO CREATE BANKABLE PV PROJECTS IN ASIA

8

DEVELOPMENT • Identify government’s

electricity needs • Identify electricity

targets

→ Obtain approval and permitting processes

CONSTRUCTION & TECHNOLOGY • Good quality feasibility

studies with peer review • Rigorous EPC selection • construction e borne by

the EPC → avoid technical difficulties and cost overrun

OPERATIONS • Ensure equipment quality • Provide for incentives in the

O&M agreement • Keep in mind O&M

expenses are low in solar sector

→ ensure availability & performance of the unit

ENVIRONMENTAL • Conduct extensive

environmental and social impact studies

• Take appropriate environmental risk mitigation measures

→ limit environmental impact

SOCIAL • Low impact if PV

projects • Choosing low

populated areas for bigger plants

→ limit social unrest due to the project

REVENUE / DEMAND RISK • Deal with more than 1

offtaker to diversify risks • Apply for sovereign or

multilateral guarantees

→ Secure the financial capacity and reliability of the electricity off-taker

CURRENCY RISK • Ask for USD denominated PPA

when available (Mongolia) • If lack of currency stability, set

up currency swaps on critical cash flows (debt & revenues)

→ Limit inflation and exchange rate risks

COUNTRY & POLITICAL RISKS • Select independent project

participants • Obtain financing from publicly

listed companies and international institutions

• If necessary, apply for MIGA guarantee

→ Limit risks related to civil war, political influence or corruption

FINERGREEN| NEW ENERGY FINANCIAL ADVISORS

OUR RETURN ON EXPERIENCE IN ASIA

9

₹ CURRENCY RISK YIELD FACTOR DEBT (RE) FINANCING

We refinanced a USD denominated loan into a rupee denominated financing to suit the project’s revenue scheme.

▶ Mitigate therefore the

currency risk ▶ Economy of cash that

has been re-invested

After careful due-diligences, we convinced our client (IPP) to change panels from tier-2 quality up to tier-1 for part of the plant

▶ Give comfort to potential investors on the quality of the plant and its productivity

Once a project has been in operation for a couple of years, operational risks are perceived as lower which gives room for refinancing at better conditions

▶ Optimized debt structure allowed our client to refine its strategy in terms of investment / OPEX

FINERGREEN| NEW ENERGY FINANCIAL ADVISORS

TWO RECENT BUSINESS CASES

10

Decision No. 11 dated of April 2017 on the mechanism for encouragement of the development of solar power projects in Vietnam

Decision No.12/2017 dated of early 2017 from Regulation of Minister of Energy and Mineral Resources on the Utilization of Renewable Energy Resources for Electricity Supply

The regulation is a very good starting point of course. However, Decision No. 11 leaves a number of issues unresolved, which may have an impact on the bankability of solar projects:

• No mechanism for direct corporate PPAs

• Uncertainty after 30 June 2019

• Model PPA for solar power projects

This decision aimed at lowering the FiT at 85 - 100% of the National Utility’s regional generation cost, which causes bankability issues for a number of RE projects already developed

On specific sectors like hydro, direct selection is authorized which leaves room to some uncertainty

Conflicts with other regulations

Decision 12 is silent as to escalation…

Vietnam Indonesia

FINERGREEN| NEW ENERGY FINANCIAL ADVISORS

ASIA: A POTENTIAL NEEDS TO BE CAPTURED…

11

SOME LEADS Foster regional coordination and measures likewise in other regions (Western Africa for instance)

Leverage on international standardized organizations such as Terrawatt initiative, International Solar Alliance, etc.

Increase the coordination between public entities, local communities, and private institutions

Give additional guidelines to public entity to support them in drafting key documents like PPA, FiT…

Give additional guidelines to private companies like commercial banks who initiate the creation of a project financing department and need assistance to assess their 1st projects

Develop off-grid solutions and related financing solutions

CHALLENGES Increase the promotion of solar power and Renewable Energy in Asia

Make Renewables more affordable & viable in terms of implementation, risk mitigations, financing costs, …

Keep the growth pace in Renewables for some leading countries such as China, India, Thailand,…

Help Governments reaching their respective targets in Renewable Energy

Should new entrants countries at the end follow the model of advanced countries like India? Is it really doable in Myanmar?

Bring 24/7 power to local communities in remote areas

FINERGREEN| NEW ENERGY FINANCIAL ADVISORS

CONTACTS

Rohan SINGH Managing Partner - Asia

Mobile : +33 (0)7 87 77 76 22

12

www.finergreen.fr