west coast data round up matthew toole buyouts west november 18, 2008

TRANSCRIPT

WEST COAST DATA ROUND UP

Matthew TooleBuyouts WestNovember 18, 2008

Worldwide M&A Activity down 37% - Private Equity-backed M&A declines 75% over 2007

0

200

400

600

800

1,000

1,200

1,400

1,600

1Q05 2Q05 3Q05 4Q05 1Q06 2Q06 3Q06 4Q06 1Q07 2Q07 3Q07 4Q07 1Q08 2Q08 3Q08

Vo

lum

e ($

bil

)

0%

5%

10%

15%

20%

25%

30%

% P

riva

te E

qu

ity

Act

ivit

y

Strategic M&A

Private Equity M&A

Private Equity M&A as % of Total M&A

US M&A Activity down nearly 40%; Private Equity-backed M&A declines 85% over 2007

0

100

200

300

400

500

600

700

1Q05 2Q05 3Q05 4Q05 1Q06 2Q06 3Q06 4Q06 1Q07 2Q07 3Q07 4Q07 1Q08 2Q08 3Q08

Vo

lum

e ($

bil

)

0%

5%

10%

15%

20%

25%

30%

35%

40%

% P

riva

te E

qu

ity

Act

ivit

y

Strategic M&A

Private Equity M&A

Private Equity M&A as % of Total M&A

West Coast Buyout Investments up 18% over 2007;Number of West Coast Buyout Investments Decline

0

500

1000

1500

2000

1Q05 2Q05 3Q05 4Q05 1Q06 2Q06 3Q06 4Q06 1Q07 2Q07 3Q07 4Q07 1Q08 2Q08 3Q08

Vo

lum

e ($

bil

)

0

20

40

60

80

100

120

140

160

180

Nu

mb

er o

f D

eals

Buyout Investments by West Coast Firms ($bil)

Number of Deals

0

100

200

300

400

500

600

Americas Europe Central Asia/Asia-Pacific

Japan Africa/Middle East

Vo

lum

e ($

bil

)

Volume: 1/1/2008-11/17/2008 Volume: 1/1/2007-11/17/2007

Private Equity Slump is a Global Phenomenon

-59%

-81%

-4% -51% -72%

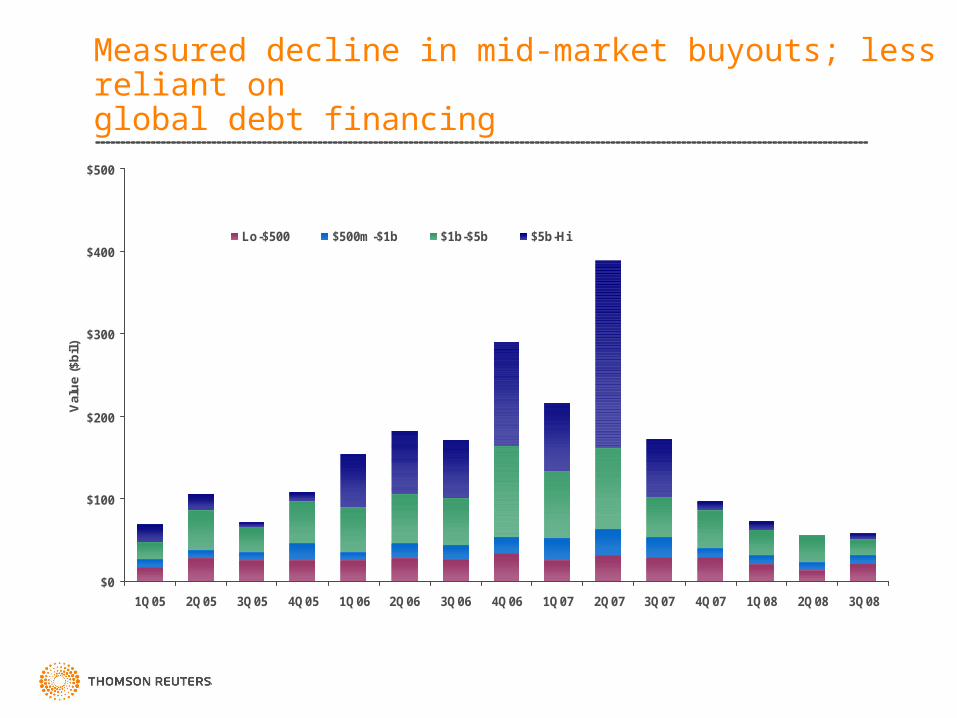

Measured decline in mid-market buyouts; less reliant on global debt financing

$0

$100

$200

$300

$400

$500

1Q05 2Q05 3Q05 4Q05 1Q06 2Q06 3Q06 4Q06 1Q07 2Q07 3Q07 4Q07 1Q08 2Q08 3Q08

Val

ue

($b

il)

Lo-$500 $500m-$1b $1b-$5b $5b-Hi

Global Buyout Investments by Sector

Worldw ide Buyouts by Industry

21.6

14.4

119.5

8.9

6.3

5.8

5.3

4.8

4.3 3.6

4.5

Financials Energy and Power

High Technology Consumer Products and Services

Industrials MaterialsMedia and Entertainment Healthcare

Telecommunications Consumer Staples

Real Estate Retail

Global M&A - Buyouts Impact

0

50

100

150

200

250

300

350

400

450

500

Fin

anci

als

En

erg

y an

d P

ow

er

Co

nsu

mer

Pro

du

cts

Co

nsu

mer

Sta

ple

s

Mat

eria

ls

Ind

ust

rial

s

Hea

lth

care

Hig

h T

ech

Rea

l E

stat

e

Tel

eco

m

Med

ia

Ret

ail

Strategic Volume ($bil)

Buyout Volume ($bil)

*Data through 9/30/2008

PE Activity was a Key Driver of the M&A Market and Investment Banking Fees

Imputed Fee Estimates by Freeman & Co

0

2000

4000

6000

8000

10000

12000

14000

16000

2001 2002 2003 2004 2005 2006 2007

Fee

s ($

mil

)

M&A Exit

Equity Exit

Portfolio Activity

Buyout Financing

Buyout

Fees paid by Financial Sponsors

Global Retraction in Credit Markets Slows Buyout Activity; HY Activity down 80% over 2007

0

10000

20000

30000

40000

50000

60000

70000

80000

'04 '05 '06 '07 '080

20

40

60

80

100

120

140

160

180

High Yield Bonds ($mil) Number of Deals

0

50

100

150

200

250

300

350

400

450

500

'04 '05 '06 '07 '080

100

200

300

400

500

600

700

800

900

Leveraged Loans ($bil) Number of Deals

*Data through 9/30/2008

Frozen Exit Markets for Venture and Buyouts

0

10

20

30

40

50

60

70

80

90

2001 2002 2003 2004 2005 2006 2007 2008*

Venture-backed IPO Buyout-backed IPO

0

50

100

150

200

250

300

350

400

2001 2002 2003 2004 2005 2006 2007 2008*

Venture-backed M&A Buyout-backed M&A

US Initial Public Offerings US Mergers & Acquisitions

Global Private Equity Fundraising

0

50

100

150

200

250

300

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008*

Venture Fundraising ($bil) Buyout Fundraising ($bil)

*Data through 9/30/2008

West Coast Buyout Fundraising Down 38% from 2007 levels; Number of Funds on Par with Year-Ago

0

5

10

15

1Q05 2Q05 3Q05 4Q05 1Q06 2Q06 3Q06 4Q06 1Q07 2Q07 3Q07 4Q07 1Q08 2Q08 3Q08

Fu

nd

s ($

bil

)

0

5

10

15

20

25

Nu

mb

er o

f F

un

ds

Funds Raised by West Coast Buyout Firms ($bil) Number of Funds

* net of management fees and carried interest

• All calculations are done at the fund level* by Thomson Reuters based on cash flows and NAVs reported by participating LPs and GPs

• Cash flow database contains 1800+ US private equity funds (480+ buyout funds)

• Pooled IRR: IRR of a group of funds where their cash flows have been aggregated together before IRR calculation

• Investment Horizon Return: IRR calculated with Net Asset Value as capital outflow at beginning of period, Net Asset Value at end of period, and actual cash flow in between

Definitions:

Performance Methodology

US Performance Benchmarks

Fund Type 1 Yr 3 Yr 5 Yr 10 Yr 20 Yr

Early/Seed VC 2.10 4.90 5.00 32.90 21.40 Balanced VC 2.50 10.80 11.90 14.40 14.70 Later Stage VC 15.30 12.40 11.10 8.50 14.50 All Venture 5.10 8.50 8.80 16.60 16.90 Small Buyouts (8.40) 5.20 8.90 4.70 12.60 Med Buyouts 15.10 11.60 12.80 7.40 11.80 Large Buyouts 27.40 8.30 13.50 6.70 12.00 Mega Buyouts (1.90) 11.10 14.50 7.80 11.30 All Buyouts 0.40 10.50 13.90 7.40 11.60 Mezzanine 12.50 5.40 5.20 5.80 8.10 Buyouts and Other PE 0.80 11.40 13.70 7.80 11.40 All Priv Equity 1.60 10.60 12.30 9.50 13.30

*Data through 6/30/2008

US Private Equity Performance Index

-10

-5

0

5

10

15

20

1 yr 3yr 5yr 10yr 20yr

All Venture All Buyouts NASDAQ S&P 500

*Data through 6/30/2008