what’s happening to productivity growth? - brookings - …€¦ · · 2017-01-19what’s...

TRANSCRIPT

What’s Happening to Productivity Growth?

Key Macro Trends and Patterns

Karim Foda

January 13, 2017

Motivation

• GDP growth is slowing down around the world, driven in large part by weak productivity growth.

• Labor force participation rates for prime-working-age men have been falling.

• Many advanced and some emerging economies have aging populations.

Productivity is key to future growth

0

1

2

3

4

5

6

Advanced Emerging and Developing

per

cen

t

GDP per capita growth (annual average)

1990-1999 2000-2007 2008-2015

• There is a widespread slowdown in labor productivity growth across both advanced and emerging market economies.

• It is primarily driven by slowing TFP growth, but capital deepening has played a more visible role in recent years.

• The slowdown is broad-based, spanning manufacturing and service industries.

• The slowdown predates the crisis in advanced economies, beginning in 2004 in the U.S. after the ICT boom and earlier in Europe and Japan.

The Bottom Line

Source: The Conference Board.

Note: Output per person employed.

-2

-1

0

1

2

3

4

5

6

71

99

0

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

per

cen

t

Emerging & Developing

Advanced

Labor Productivity Growth

Data source: OECD Productivity Statistics.

Note: Output per hour worked.

-1

0

1

2

3

4

51

971

19

72

19

73

19

74

19

75

19

76

19

77

19

78

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

per

cen

t

Canada France Germany Italy Japan UK US

US

Trend Labor Productivity Growth in Advanced Economies

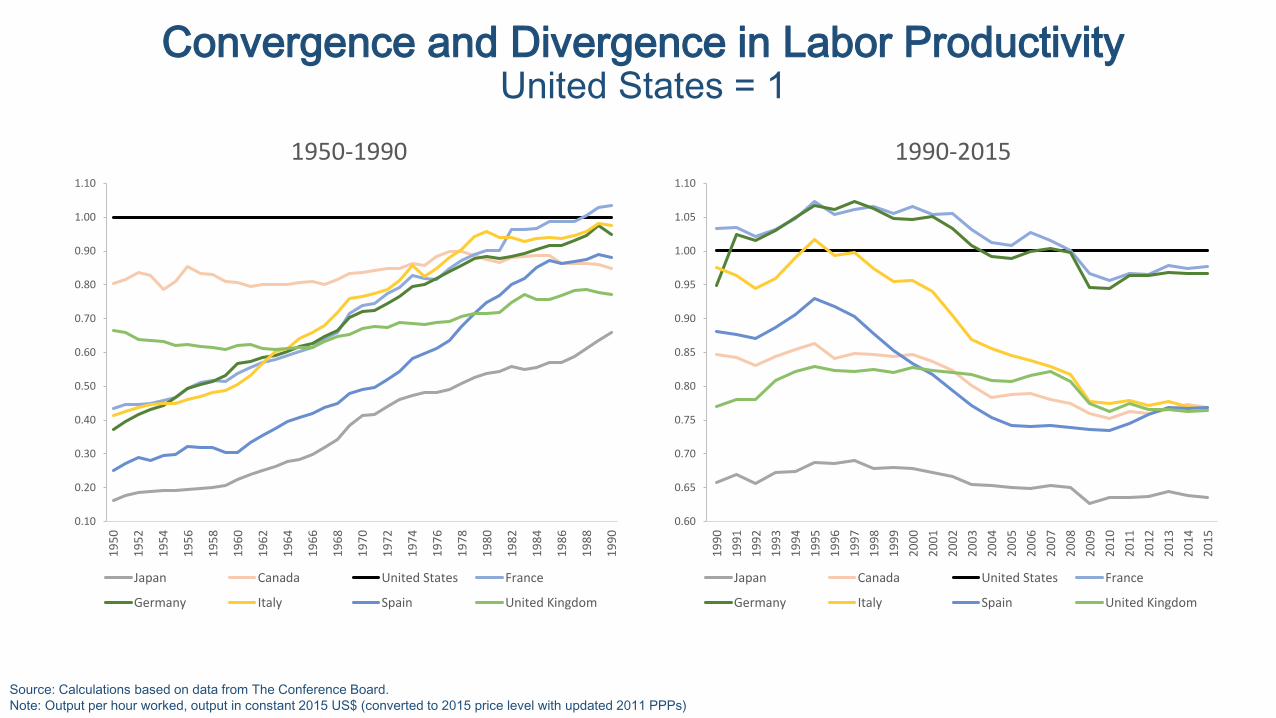

Convergence and Divergence in Labor ProductivityUnited States = 1

Source: Calculations based on data from The Conference Board.

Note: Output per hour worked, output in constant 2015 US$ (converted to 2015 price level with updated 2011 PPPs)

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1.10

19

50

19

52

19

54

19

56

19

58

19

60

19

62

19

64

19

66

19

68

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

1950-1990

Japan Canada United States France

Germany Italy Spain United Kingdom

0.60

0.65

0.70

0.75

0.80

0.85

0.90

0.95

1.00

1.05

1.10

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

1990-2015

Japan Canada United States France

Germany Italy Spain United Kingdom

Source: Calculations based on data from The Conference Board.

Note: Output per hour worked. Groups aggregated using GDP-PPP weights. Other Advanced includes Australia, Canada, Hong Kong, Israel, New Zealand, Singapore, South Korea and Taiwan.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Advanced United States Europe Japan Other Advanced

per

cen

t

1990-1995 1996-2004 2005-2015

Labor Productivity Growth in Advanced Economies

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

UK Euro Area France Germany Italy Spain Sweden Australia Canada

per

cen

t

1990-1995 1996-2004 2005-2015

Labor Productivity Growth in Advanced Economies

Source: Calculations based on data from The Conference Board.

Note: Output per hour worked. Groups aggregated using GDP-PPP weights.

Decomposing Labor Productivity Growth: TFP and Capital DeepeningUnited States

Data source: OECD Productivity Database.

Note: Decomposition of growth in output per hour worked.

0.7

1.6

0.6

0.4

0.6

0.2

0.3

0.3

0.3

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1990-1995 1996-2004 2005-2015

United States

pe

rce

nt

TFP

ICT capital deepening

Non-ICT capital deepening

Decomposing Labor Productivity Growth: TFP and Capital DeepeningUnited States

Data source: OECD Productivity Database.

Note: Decomposition of growth in output per hour worked.

0.7

1.6

0.6 0.7

0.3

0.4

0.6

0.20.3

0.1

0.3

0.3

0.3

0.4

-0.1

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1990-1995 1996-2004 2005-2015 2005-2011 2012-2015

United States

pe

rce

nt

TFP

ICT capital deepening

Non-ICT capitaldeepening

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

19

90

-19

95

19

96

-20

04

20

05

-20

15

19

90

-19

95

19

96

-20

04

20

05

-20

15

19

90

-19

95

19

96

-20

04

20

05

-20

15

19

90

-19

95

19

96

-20

04

20

05

-20

15

19

90

-19

95

19

96

-20

04

20

05

-20

15

19

90

-19

95

19

96

-20

04

20

05

-20

15

Japan United Kingdom France Germany Italy Spain

TFP

ICT capital deepening

Non-ICT capital deepening

Decomposing Labor Productivity Growth: TFP and Capital DeepeningOther Advanced Economies

Data source: OECD Productivity Database.

Note: Decomposition of growth in output per hour worked.

A Broad-Based Rise and Fall in US TFP GrowthPercentage point change in average industry TFP growth

Source: Calculations based on data from Bureau of Labor Statistics Multifactor Productivity database.

Note: Industries ranked by change in average value-added TFP growth between both periods, based on Byrne, Fernald and Reinsdorf (2016). Striped bars denote manufacturing industries.

Industries with largest positive acceleration in recent period (right panel) are (i) funds and trusts, (ii) water transport and (iii) oil and gas extraction. Industries with largest negative deceleration in the same period are (i) apparel and leather

and applied products, (ii) petroleum and coal products and (iii) computer and electronic products.

-15

-10

-5

0

5

10

15

0 10 20 30 40 50 60Industry

-20

-15

-10

-5

0

5

10

15

20

25

0 10 20 30 40 50 60

Industry

Broad Rise1988-1995 to 1996-2004

Broad Fall1996-2004 to 2005-2014

Source: Calculations based on data from Bureau of Labor Statistics Multifactor Productivity database.

Note: Recreated from Baily and Montalbano (2016), but with changes in average value-added TFP growth between both periods, based on Byrne, Fernald and Reinsdorf (2016).

Manufacturing

Agriculture, Forestry and Fishery

Mining

Utilities

Construction

Wholesale Trade

Retail Trade Transportation

Information

Finance, Insurance and Real Estate

Services

-6

-4

-2

0

2

4

6

8

-8 -6 -4 -2 0 2 4 6

Faster growth1996-2004

Slower growth2005-2015

Rising and Falling TogetherAverage US industry TFP growth

Industry Contributions to the Rise and Fall in US TFP Growth

Source: Calculations based on data from Bureau of Labor Statistics Multifactor Productivity database.

Note: Domar weights used to aggregate industry contributions. Recreated from Baily and Montalbano (2016).

The Rise The Fall

1.08

-0.17

-0.08

-0.05

0.02

0.07

0.09

0.10

0.11

0.15

0.40

0.43

-0.4 -0.2 0.0 0.2 0.4 0.6 0.8 1.0 1.2

Aggregate TFP Growth

Utilities

Construction

Mining

Transportation

Retail Trade

Information

Agriculture

FIRE

Wholesale Trade

Manufacturing

Services

Contributions to TFP Growth 1996-2004 minus Contributions 1987-1995

-1.36

0.18

0.13

0.04

0.04

-0.07

-0.08

-0.09

-0.15

-0.30

-0.31

-0.74

-1.6 -1.4 -1.2 -1.0 -0.8 -0.6 -0.4 -0.2 0.0 0.2 0.4

Aggregate TFP Growth

FIRE

Mining

Utilities

Information

Transportation

Construction

Agriculture

Services

Wholesale Trade

Retail Trade

Manufacturing

Contributions to TFP Growth 2005-2014 minus Contributions 1996-2004

Holding Industry Weights FixedUnited States average TFP growth

Source: Byrne, Fernald and Reinsdorf (2016).

Note: Orange bars show actual average growth in business sector TFP. Blue bars show counterfactual where industry weights (shares in aggregate value added) are held constant at 1987 values.

0.0

0.5

1.0

1.5

2.0

1987-1995 1995-2004 2004-2013

per

cen

t

Counter-factual Actual

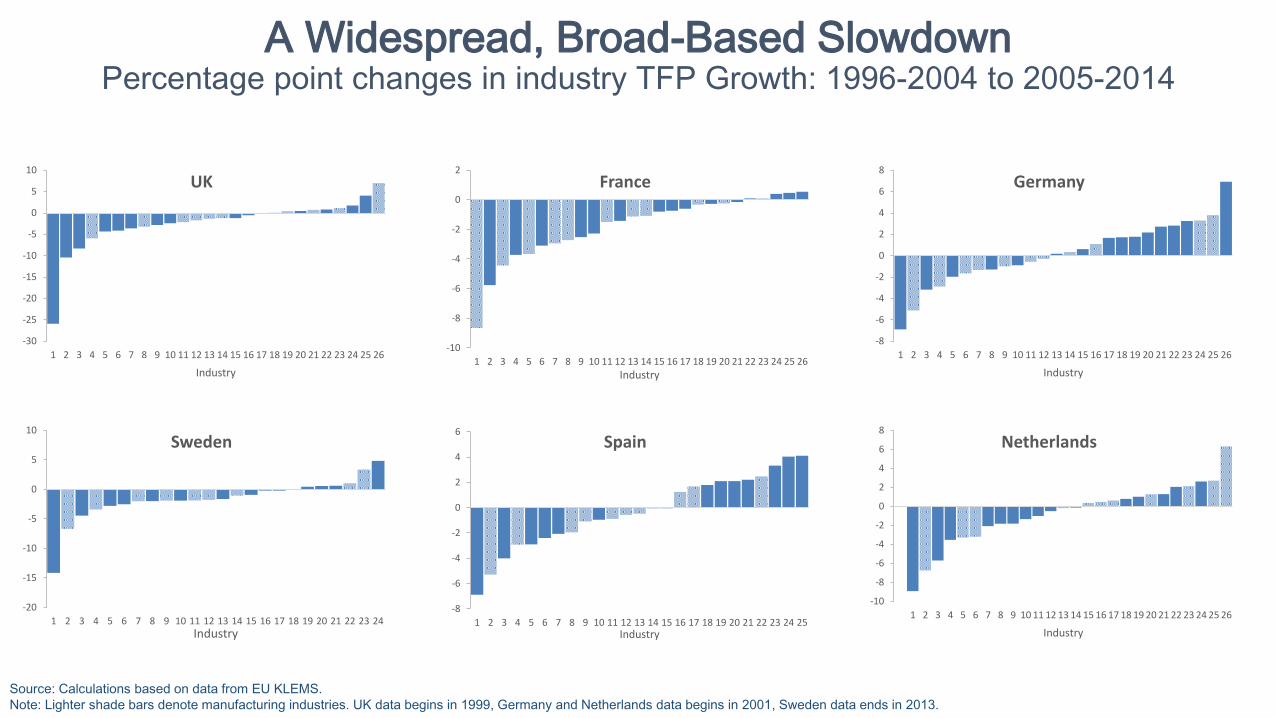

A Widespread, Broad-Based SlowdownPercentage point changes in industry TFP Growth: 1996-2004 to 2005-2014

Source: Calculations based on data from EU KLEMS.

Note: Lighter shade bars denote manufacturing industries. UK data begins in 1999, Germany and Netherlands data begins in 2001, Sweden data ends in 2013.

-10

-8

-6

-4

-2

0

2

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26

Industry

France

-30

-25

-20

-15

-10

-5

0

5

10

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26

Industry

UK

-8

-6

-4

-2

0

2

4

6

8

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26

Industry

Germany

-8

-6

-4

-2

0

2

4

6

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25Industry

Spain

-10

-8

-6

-4

-2

0

2

4

6

8

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26

Industry

Netherlands

-20

-15

-10

-5

0

5

10

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24Industry

Sweden

A Word on MeasurementAdjustments to growth in US output per hour

Source: Byrne, Fernald and Reinsdorf (2016).

Note: Other comprises Internet, free digital services, globalization and fracking.

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

1978-1995 1995-2004 2004-2014

per

cen

tage

po

ints

Published

data

computers/communications

software, specialized equipment

intangibles

other

Source: The Conference Board.

Note: Output per person employed.

-2

-1

0

1

2

3

4

5

6

7

8

9

EmergingMarkets andDevelopingEconomies

China India OtherDeveloping

Asia

Indonesia Latin America Sub-SaharanAfrica

South Africa

per

cen

t

1990-1999 2000-2007 2008-2015

Labor Productivity Growth in Emerging and Developing Economies

Source: The Conference Board.

-2

-1

0

1

2

3

4

5

EmergingMarkets andDevelopingEconomies

China India OtherDeveloping

Asia

Indonesia Latin America Sub-SaharanAfrica

South Africa

per

cen

t

1990-1999 2000-2007 2008-2015

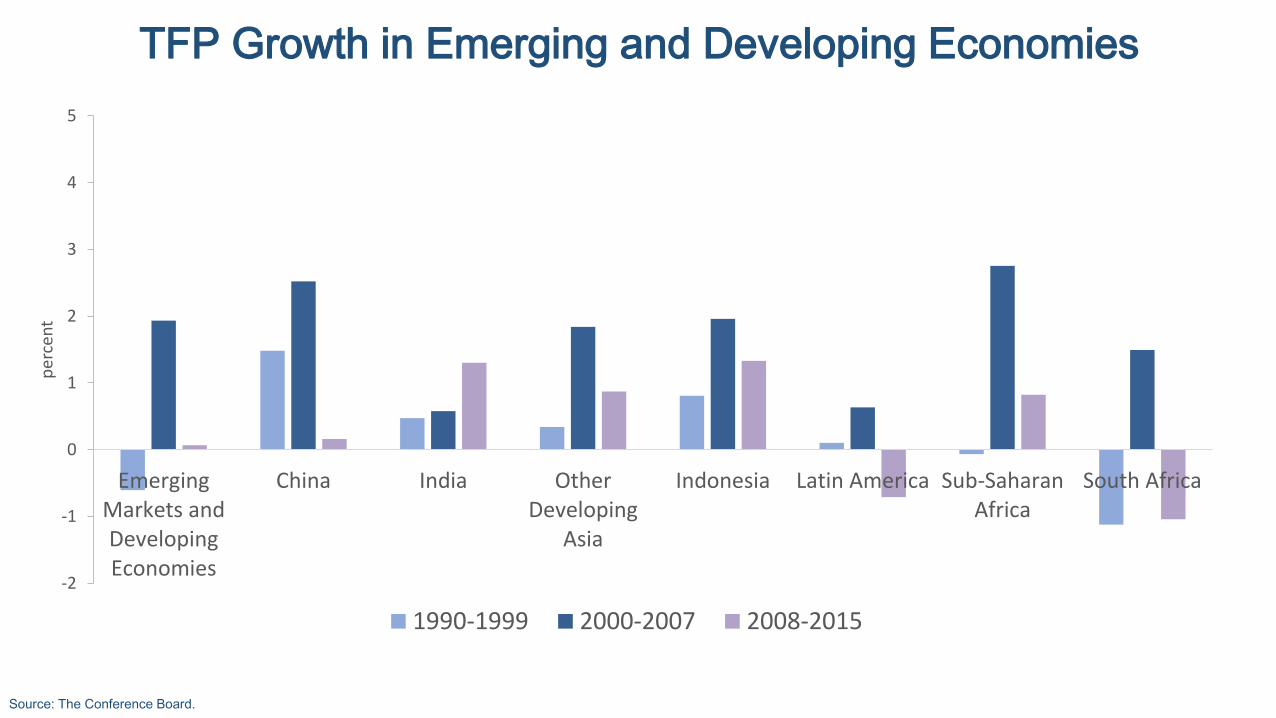

TFP Growth in Emerging and Developing Economies

Source: The Conference Board.

-3

-2

-1

0

1

2

31

99

0

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

per

cen

t

Emerging & Developing

Advanced

Total Factor Productivity Growth

Weak Investment in Advanced EconomiesSlowing Investment in Emerging and Developing

Sources: OECD Economic Outlook June 2015 for Real Gross Investment figure; IMF World Economic Outlook April 2015 for Investment-to-Capital ratios via Laeven and Valencia (2014).

Notes: For gross investment, “emerging” includes Brazil, China, India, Indonesia, Mexico, Russia, South Africa and Turkey. For investment-to-capital ratio, they include Brazil, China, India, Mexico,

Russia and Turkey.

6

8

10

12

14

16

18

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

per

cen

t

Emerging economies

Emerging economiesexcluding China

Real Gross Investment2007 Q4 = 100

Investment-to-Capital Ratio

40

60

80

100

120

140

160

180

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

07

Q4

= 1

00

OECD

Emerging economies

Emerging economiesexcluding China

Potential Output Growth in Advanced Economies(OECD)

Source: OECD Economic Outlook, June 2016.

Notes: Potential employment rate refers to potential employment as a share of the working-age population. Active population rate refers to the share of the population of working age in the total population.

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

per

cen

t

Capital per worker

TFP

Potential employment rate

Active population rate

Potential per capita growth

• There is a widespread slowdown in labor productivity growth across both advanced and emerging market economies.

• It is primarily driven by slowing TFP growth, but capital deepening has played a more visible role in recent years.

• The slowdown is broad-based, spanning manufacturing and service industries.

• The slowdown predates the crisis in advanced economies, beginning in 2004 in the U.S. after the ICT boom and earlier in Europe and Japan.

The Bottom Line

• Slowdown in innovation or diffusion? Dispersion in firm-level TFP growth suggests that weak diffusion has played a role (OECD 2015).

• Declining business dynamism and increased market concentration. Impacts on productivity?

• Weak investment despite lower price of investment (investment paradox?).

• Skill-biased technological change, skills mismatches and constraints.

• Barriers to innovation, regulatory distortions, misallocation of inputs.

Possible Explanations to Explore