wind farms in a gross pool market: australian national electricity market hugh outhred school of...

TRANSCRIPT

Wind Farms in a Gross Pool Market:Australian National Electricity Market

Hugh OuthredSchool of Electrical Engineering and Telecommunications

The University of New South Wales

Sydney, Australia

Tel: +61 2 9385 4035; Fax: +61 2 9385 5993; Email: [email protected]

www.sergo.ee.unsw.edu.au

Perspectives from AbroadSustainable Energy Ireland, Dublin 13 June

2

Outline

• Scope & design of the Australian NEM

• Managing supply-demand balance

• Ancillary service, spot & derivative markets

• Renewable energy certificate trading

• Network connection issues

• Conclusions

3

Electricity industry structure in SE Australia

Gen 1

Gen 2

Gen X

GenerationSector:-

largegenerators

Gen 3

TransmissionSector

NSWVictoria

South Aust.Queensland& possiblyTasmania

TransmissionSector

NSWVictoria

South Aust.Queensland& possiblyTasmania

Electricity

Financial instrument& REC (emission) trading

Distributor 1

Distributor 2

Distributor Y

Distributionsector

Electricity

Multi-regionNational

ElectricityMarket(NEM)

Intentionsoffers &

payments

Retailer Z

Retailer 2

Retailer 1

Retailsector

Intentionsbids &

payments

Tx networkpricing

Tx networkpricing

Networkaccess End-use

Equipment&

DistributedresourcesElectricity

End-usesector

Contestablecustomers

Franchisecustomers

RetailMarkets

Embeddedgenerators

4

Key NEM features

• NEM covers all participating states:– A multi-region pool with intra-regional loss factors– Ancillary services, spot market & projections– Auctions of inter-regional settlement residues– Operated by NEMMCO (owned by states)

• Compulsory participants in NEM:– All generators & dispatchable links > 30 MW– Network service providers & retailers

• Contestable consumers may buy from NEM

5

Region boundaries & inter-connectors

• Regions boundaries selected so that:– Transmission constraints are rare within a region– Frequently-occurring constraints are placed on

region boundaries

• Region boundaries to be reset as required:– Whenever a constraint occurs > 50 hours/year

• Unregulated inter-connectors are allowed:– If dispatchable so that it can bid like a generator:

• ‘Directlink’ the first (operating since July 2000):– 180 MW DC link between NSW & Queensland regions

6

Scope of the NEM

• Queensland• New South Wales & ACT• Victoria• South Australia• Tasmania (on connection to the mainland)

NEM regions are indicated, and theirboundaries need not be on state borders

(e.g. two regions in NSW)

7

NEM regional spot market model(Based on NEMMCO, 1997)

1,500 MW

NSW

Snowy

Victoria

850 MW

3,000 MW

1,100 MW

Queensland

750 MW

750 MW

South Aust

500 MW

250 MW

300 MW

Tasmania480 MWBasslink

thermalor stabilityflow limits

Directlink180 MW

(unregulated DC)

Murraylink 220 MW (unregulated DC)& possibly SANI (regulated AC)

8

Supply-demand balance in the electricity industry

• Frequency is a measure of supply-demand balance– always varying due to fluctuations in power flows

• Wind farms will make frequency more variable: – Does this matter & if so, who should pay for additional

control action?

ThermalPower stations

Wind farms

Hydrogenerators

Industrial

Commercial

Residential

Generator input power Load electrical power

+ _

9

Managing supply-demand balance in Australian NEM

Spot market forecast &derivative markets

Frequency controlancillary service

markets for period tSupply/demand

projections & FCASderivative markets

FCAS marketsfor period t+1

Spot marketfor period t

Spot marketfor period t+1

time

spotperiod t

spotperiod t+1

increasing uncertainty

Physical issues

Commercial issues

10

NEMMCO processes for managing supply-demand balancePower system reliability & security standards

NEMMCO Forecasts of supply & demand• 10 year (annual)• 2 year (weekly)• 1 week (hourly)• day-ahead spot price& dispatch (30 min)

NEMMCO operation:•Participant bid/offers•Network data•Demand forecast•Reserve threshold•Security constraints•Reliability safety net

Spot& FCASMarkets

DerivativeMarkets

11

Bidding & dispatch(source: NEMMCO)

Day -2 Day -1 Day 0 Day 1

Dispatch Day

Commitment notices

Initial Offers/Bids 1230hrsthen re-bids until dispatch time

ST PASA 1400hrs

1st Pre-dispatch 1600hrsUpdated 3hrly

5-minute & 30-minute prices as set;previous days data at 0800hrs

CapacityEnergy/RoC

12

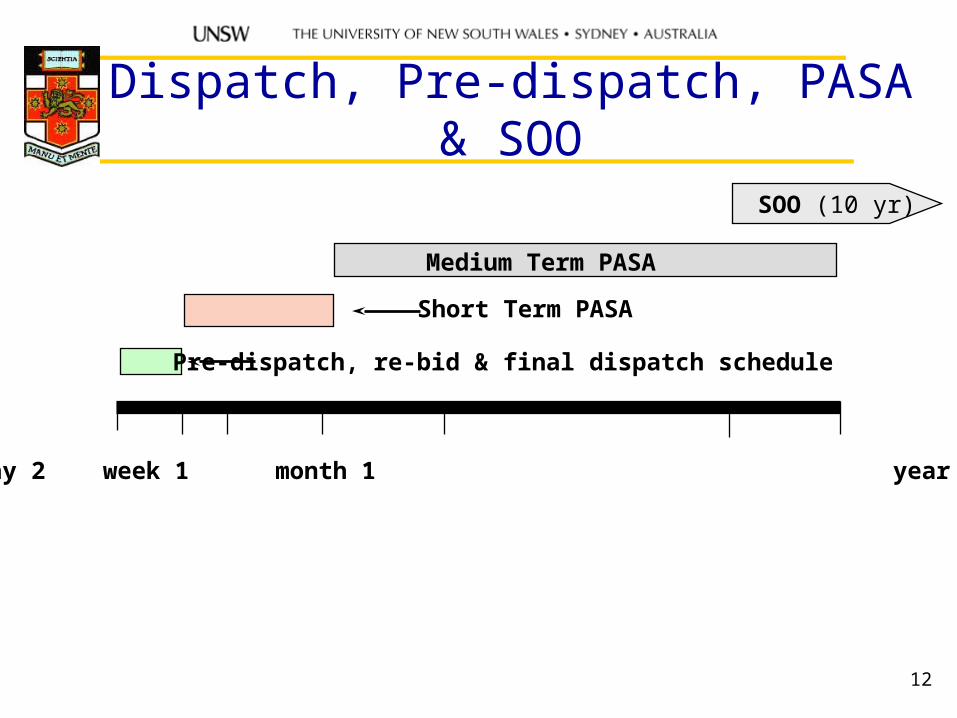

Dispatch, Pre-dispatch, PASA & SOO

0 day 1 day 2 week 1 month 1 year 1 year 2

Medium Term PASA

Pre-dispatch, re-bid & final dispatch schedule

Short Term PASA

SOO (10 yr)

13

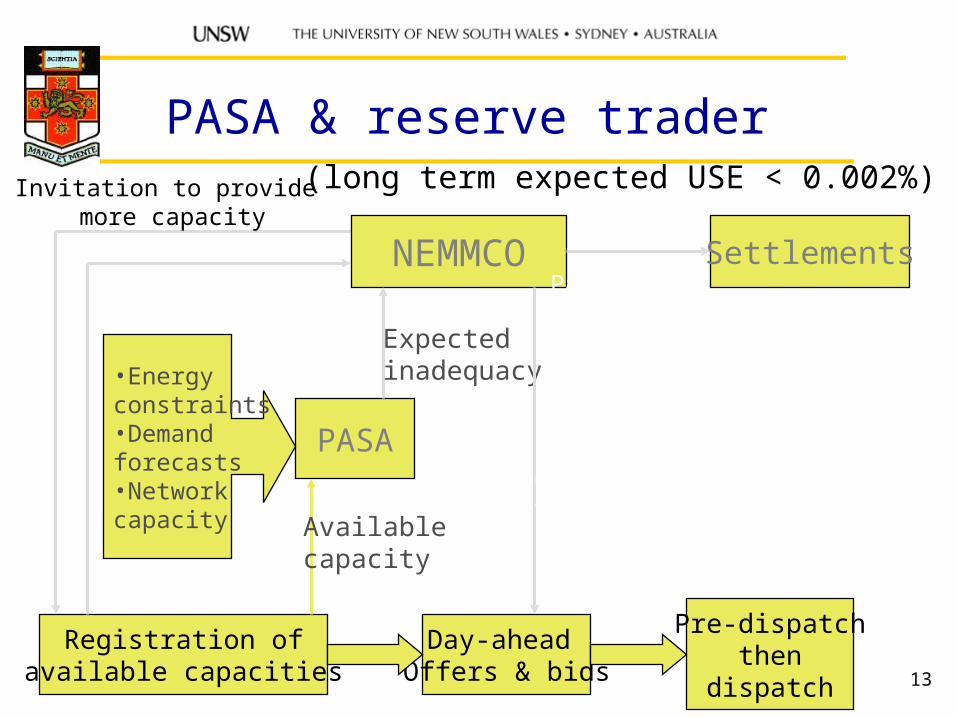

PASA & reserve trader

PASA

•Energyconstraints•Demandforecasts•Networkcapacity

Registration ofavailable capacities

Day-ahead Offers & bids

Pre-dispatchthen

dispatch

Invitation to provide more capacity

Purchase of more capacity

NEMMCO

Expectedinadequacy

Purchased capacityoffered to market (usually at VOLL)Available

capacity

SettlementsPayment for purchased capacity

(long term expected USE < 0.002%)

14

Spot market offers & bids

• Generators, retailers & consumers:– Price-quantity curve (sell/buy) for each half hour:

• ≤ 10 daily prices, quantities changeable until dispatch

– Demand forecasts ‘bid in’ at $10000/MWH (VoLL)

• Dispatchable links between regions:– Flow offer curve based on price difference

• Bids & offers ranked to give dispatch stack:– Considering loss factors & inter-tie constraints– 5 minute prices set by economic dispatch:

• Half-hourly averages are calculated in ‘real time’

15

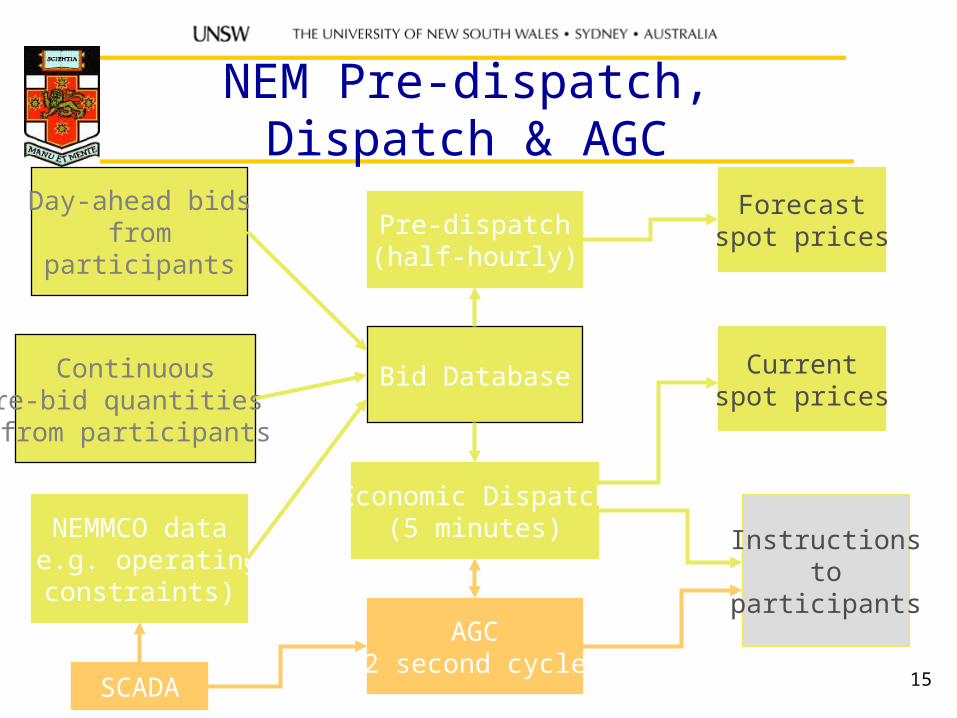

NEM Pre-dispatch, Dispatch & AGC

Bid Database

Instructionsto

participants

Forecastspot prices

Currentspot prices

Pre-dispatch(half-hourly)

Economic Dispatch(5 minutes)NEMMCO data

(e.g. operatingconstraints)

Day-ahead bidsfrom

participants

Continuousre-bid quantities from participants

AGC(2 second cycle)

SCADA

16

Modelling regulated interconnectors& intra-region location

• Regulated interconnector between 2 regions– Modelled by a linearised marginal loss function:

• A ‘dynamic’ network loss factor that depends on flow• Flow limits (security or thermal criteria)

• Locational effects within regions– Modelled by ‘static’ network loss factors (LFs)

• Annual average of estimated half-hour marginal losses for each generator node & group of consumer nodes

– Intra-regional constraints not modelled but a ‘constrained-on’ generator cannot set price

17

Financial instrument trading in support of NEM

• Trading in swap & cap contracts:– Bilateral trading– Over-the-counter instruments– Exchange-traded CFDs (swaps)

• Inter-regional hedges:– Specialised form of financial instrument:

• to manage regional price difference risks• funded by interconnector settlement residues

– NEMMCO inter-regional settlement residue auctions:

• Commenced in 1999

18

Monthly average NEM Regional Ref Prices (RRPs) since market inception (NECA, 03Q1 Stats, 2003)

19

Cumulative spot prices(7-day moving sum) (NECA, 2003)

20

Ave, Max & Min RRP in SA region (truncated at 300 $/MWH) (NECA, 03Q1 Stats, 2003)

21

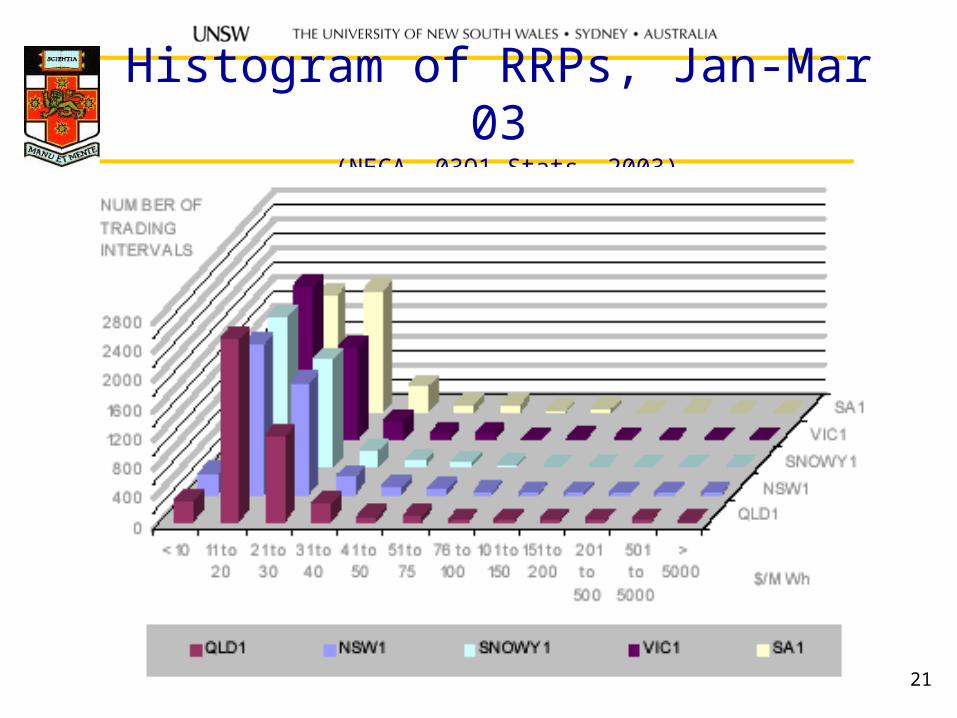

Histogram of RRPs, Jan-Mar 03 (NECA, 03Q1 Stats, 2003)

22

Cumulative duration curve, SA RRP, Jan-Mar 03 (NECA, 03Q1 Stats, 2003)

23

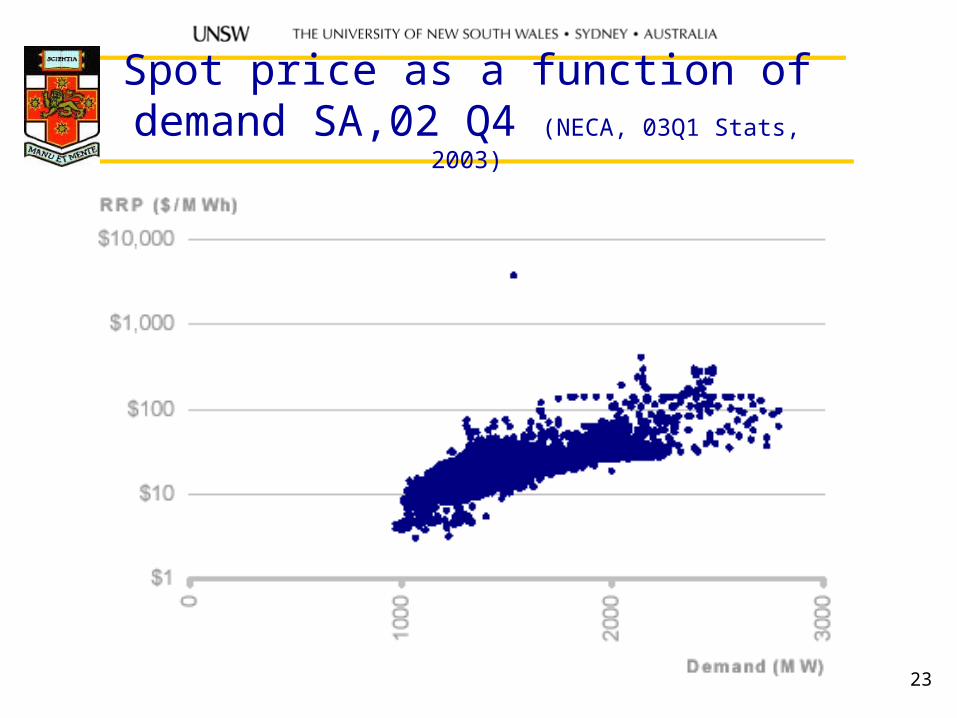

Spot price as a function of demand SA,02 Q4 (NECA, 03Q1 Stats, 2003)

24

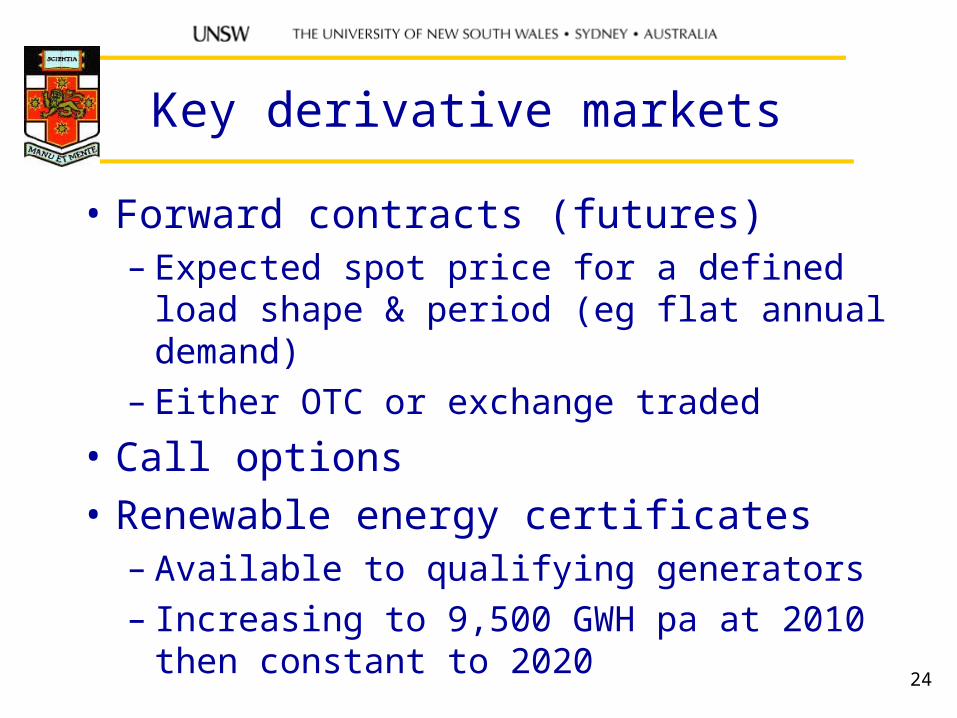

Key derivative markets

• Forward contracts (futures)– Expected spot price for a defined load shape

& period (eg flat annual demand)– Either OTC or exchange traded

• Call options

• Renewable energy certificates– Available to qualifying generators– Increasing to 9,500 GWH pa at 2010 then

constant to 2020

25

Flat forward contract prices, 1999-2006 (NECA, 02Q4 Statistics, 2003)

26

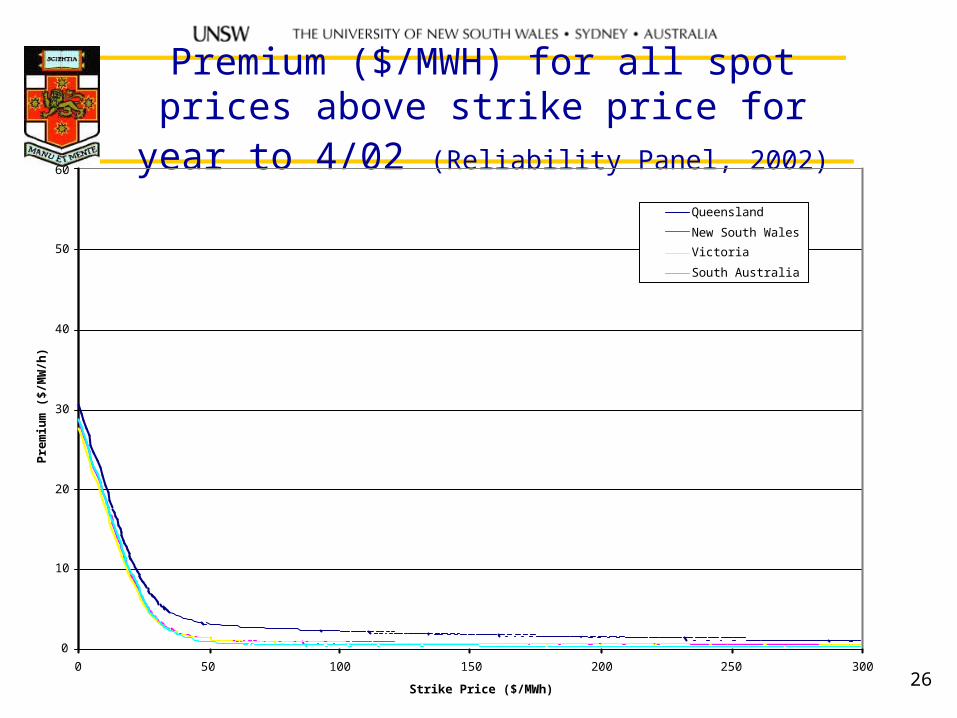

Premium ($/MWH) for all spot prices above strike price for year to 4/02 (Reliability Panel, 2002)

0

10

20

30

40

50

60

0 50 100 150 200 250 300

Strike Price ($/MWh)

Pre

miu

m (

$/M

W/h

)

Queensland

New South Wales

Victoria

South Australia

27

Renewable Energy Certificate Prices - forecast to 2020 (A$/MWH) (ORER, 2003)

20

25

30

35

40

45

50

55

60

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

28

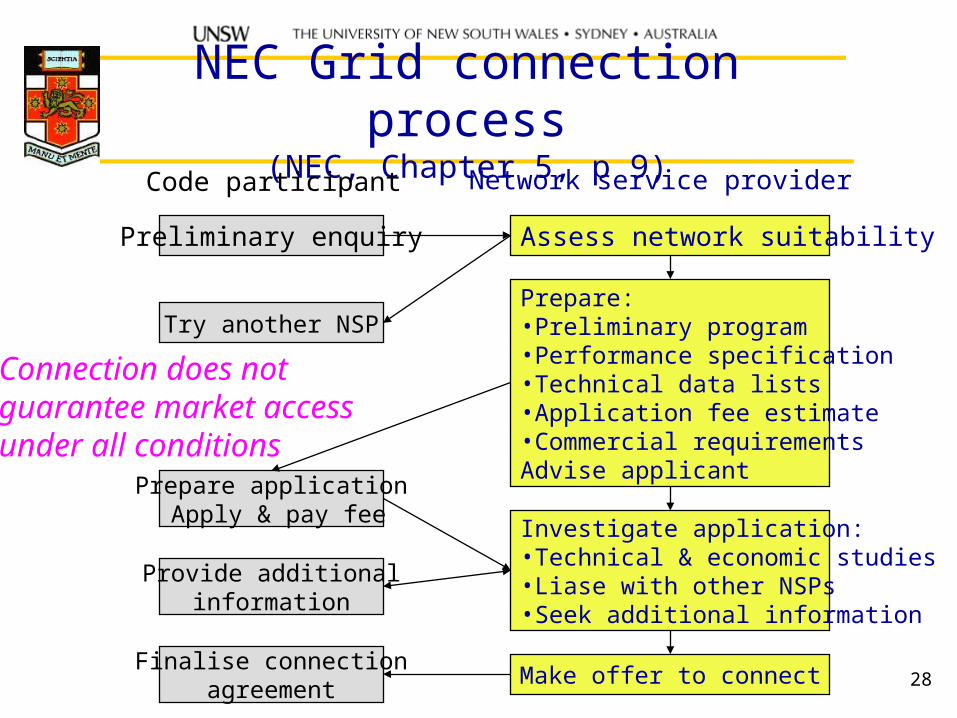

NEC Grid connection process(NEC, Chapter 5, p 9)

Code participant Network service provider

Preliminary enquiry Assess network suitability

Try another NSPPrepare:•Preliminary program•Performance specification•Technical data lists•Application fee estimate•Commercial requirementsAdvise applicant

Prepare application Apply & pay fee

Provide additionalinformation

Investigate application:•Technical & economic studies•Liase with other NSPs•Seek additional information

Make offer to connectFinalise connection

agreement

Connection does notguarantee market accessunder all conditions

29

National Electricity Code (NEC) connection requirements for generators

• Reactive power & voltage control capability

• Quality of electricity injected into network

• Protection requirements

• Remote control arrangements

• Excitation system requirements

• Loading rates

• Ride-through to avoid cascading outages:– Loss of largest generator; 175ms network fault

30

NEC categories of generators

• Either market, non-market or exempt– Market implies sell to NEM

• Can then also sell ancillary services

– Non-market or exempt implies sell to retailer

• Either scheduled or non scheduled:– Scheduled implies centrally dispatched:

• Must then participate in the NEM processes of bidding, pre-dispatch & PASA

• Default category for generation projects > 30 MW• Not appropriate for “intermittent” generation, eg wind

31

Future directions for NEM COAG Energy Market Review (2002) Recommendations

• Create a National Energy Regulator• Improve control of generator market power• Improve operation of derivative markets• Give NEMMCO a NEM-wide planning function• Increase number of NEM regions & aim for full

nodal pricing• Phase in interval metering & retail competition

for all end-users• Enhance competition and network scope for gas• Replace existing climate cahnge policies by

emission trading

32

Key web sites

• COAG Energy market review:– www.energymarketreview.org

• National Electricity Market Management Company:– www.nemmco.com.au

• National Electricity Code Administrator:– www.neca.com.au

• Electricity Supply Association of Australia:– www.esaa.com.au

• University of New South Wales - Sustainable energy research group:– www.sergo.ee.unsw.edu.au