wisconsin homeowners manual - penn national insurance · o akita o american staffordshire terrier o...

TRANSCRIPT

Partners Mutual Insurance Wisconsin Homeowners Manual

WISCONSIN HOMEOWNERS MANUAL

Rev. 6/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 2

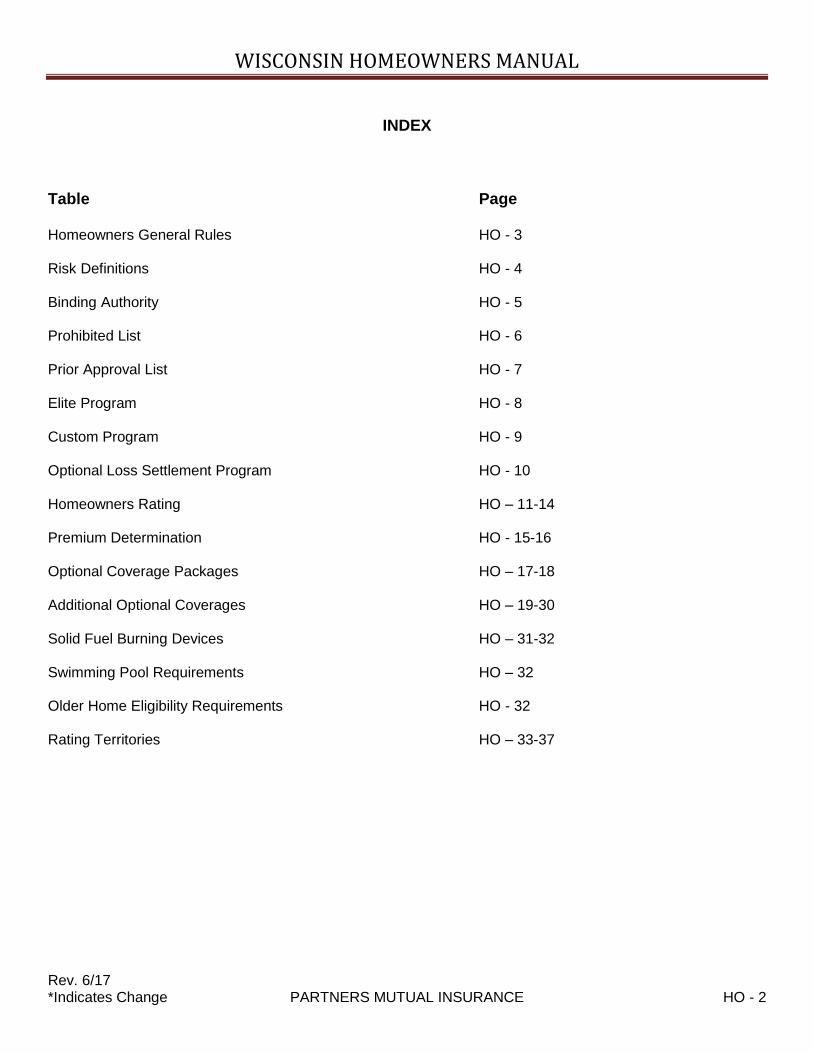

INDEX

Table Page Homeowners General Rules HO - 3 Risk Definitions HO - 4 Binding Authority HO - 5 Prohibited List HO - 6 Prior Approval List HO - 7 Elite Program HO - 8 Custom Program HO - 9 Optional Loss Settlement Program HO - 10 Homeowners Rating HO – 11-14 Premium Determination HO - 15-16 Optional Coverage Packages HO – 17-18 Additional Optional Coverages HO – 19-30 Solid Fuel Burning Devices HO – 31-32 Swimming Pool Requirements HO – 32 Older Home Eligibility Requirements HO - 32 Rating Territories HO – 33-37

WISCONSIN HOMEOWNERS MANUAL

Rev. 6/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 3

PARTNERS MUTUAL HOMEOWNERS GENERAL RULES You may bind coverage for those situations designated as ELIGIBLE in these guidelines. PROHIBITED exposures have proven to be historically unprofitable. We do not wish to write risks falling into this category. All homes and premises must be above average in condition and reflect pride of ownership. PRIOR APPROVAL REQUIRED items, including requests for limits other than those shown, require special underwriting attention and cannot be bound until approval is granted by the Regional Office. If you have not received approval DO NOT accept deposit premiums. To help us provide you with a prompt decision; please include the required underwriting information. APPLICATION AND SUBMISSION REQUIREMENTS 1. A fully, correctly and truthfully completed ACORD application signed by the applicant and

producer; 2. A completed replacement cost estimate; and 3. A photograph of the dwelling; other structures for which a specific charge is made; any coal or

wood burning stove or furnace; any free standing fireplace, fireplace insert or space heater is required and must accompany each application for Homeowners insurance.

HOME AND PREMISES INSPECTIONS - Initiated by Partners Mutual 1. Exterior and/or interior inspections are conducted at the discretion of Partners Mutual

Insurance. 2. Please advise your insured that an inspector may call to set up an appointment for an interior

inspection. If the insured refuses the inspection, the risk will be canceled. 3. Inspectors from our contracted inspection vendors will identify themselves and will carry

photo identification for their respective inspection companies. Inspectors will indicate that they are doing the inspection on behalf of Partners Mutual.

WISCONSIN HOMEOWNERS MANUAL

Rev. 6/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 4

RISK DEFINITIONS A. Dwelling — Owner occupied dwelling used exclusively for private residential purposes containing

not more than two families and not more than two boarders or roomers per family.

B. Tenant — Non owner occupant of a dwelling or apartment. If there are non-related tenants occupying a single unit, separate policies must be issued to each.

C. Condominium — Owner-occupant of a condominium unit which is used exclusively for residential

purposes and is occupied by not more than one additional family or more than two boarders or roomers.

D. Builders Risk — One or two family dwelling in the course of construction by a qualified general

contractor, provided the policy is issued only in the name of the intended owner-occupant of the dwelling. Builders Risk endorsements are to be used with eligible new construction only.

E. Other interests

1. Life Estate - Contracts of Sale - The owner life estate or seller (contract of sale) interest is covered by adding HO 04 41 "Additional Insured."

2. Trusts - The interest of a trust is covered by adding HO 05 43, Residence Held in Trust.

F. Co-Ownership of a Two Family Dwelling — Co-owners who occupy separate living quarters are covered by issuing an HO-2 or HO-3 to one owner with a HO 04 41 "Additional Insured" endorsement attached listing the second owner. The second owner may be covered by a tenant policy.

WISCONSIN HOMEOWNERS MANUAL

Rev. 6/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 5

BINDING AUTHORITY Refer to Program specific section of this manual for further information.

PROGRAM ELITE (Preferred) CUSTOM (Standard) OPTIONAL LOSS SETTLEMENT (Market Value)

FORMS HO-3 or HO-5 HO-2,3,4, or 6 HO-2

Insurance to Value 100% of Replacement Cost 100% of Replacement Cost 100% of Market Value and Minimum 50% of

Replacement Cost

Coverage A Minimum $150,000 $100,000 $90,000

Coverage A Maximum (PPC 1-8) $700,000 $500,000 $200,000

Coverage A Maximum (PPC 9-10) PC 9 $400,000

PC 10 Not Eligible $400,000 $150,000

Coverage C Minimum 75% of Cov. A 40% of Cov. A ($20,000 HO-4 & 6) 40% of Cov. A

Coverage C Maximum 100% of Cov. A 75% of Cov. A ($350,000 HO-4 & 6) 75% of Cov. A

Minimum Deductible $1,000 $1,000 ($500 HO-4 and 6) $1,000

Age of Dwelling Built since 1950 Built since 1900 Built since 1900

If over 40 years, must meet Older Home Requirements on page HO-32

Public Protection Class 1-9 1-10 (PPC 10 must be located

within 8 miles of the primary responding fire department)

1-10 (PPC 10 must be located within 8 miles of the primary responding fire department)

Supplemental Heating/Solid Fuel Heating

Not Eligible Prior Approval Prior Approval

Must meet requirements on page HO- 31-32

Seasonal or Secondary Homes Dwellings

Not Eligible Prior Approval.

Coverage A not to exceed $200,000

Prior Approval. Coverage A not to exceed

$200,000

Partners Mutual must write Homeowners coverage on the primary residence.

Liability Minimum $100,000

Liability Maximum $500,000

Earthquake 30 day wait unless added at inception or renewal. See HO-20, Item F.

Sewer Backup 30 day wait unless added at inception or renewal.

Homes Over 40 Years Old Must meet the Older Home requirements on page HO-32 are ELIGIBLE

Swimming Pools Above and Inground Pools meeting the requirements on page HO-32 are ELIGIBLE

Trampolines Trampolines meeting the requirements on page HO-13 are ELIGIBLE

WISCONSIN HOMEOWNERS MANUAL

Rev. 6/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 6

This list is not all inclusive. If something falls outside of our acceptable guidelines and is not listed here, please contact your underwriter for prior approval before binding.

Construction and Risk Characteristics

Homes without thermostatically controlled, central heating systems

Homes with less than 100 amp electrical service

Historic homes

Unique or ornate construction

Geodesic dome or underground construction

Homes with pier foundations

Mobile Homes structures &/or contents including double wide, trailer homes, house trailers and these type structures that have been physically altered, built on to, etc. (This applies to primary, seasonal, secondary or rental properties).

Aluminum wiring

Knob & Tube wiring

Federal Pacific Stab-Lok breakers

Asbestos roofing &/or siding

Fuse boxes only

Risks with Any of the Following Liability Characteristics

Potentially dangerous liability exposures such as unfenced in-ground swimming pools, skate board ramps, three wheeled ATV’s, etc.

Home Day Care Coverage exceeding three children.

The following specified dog breeds: o Akita o American Staffordshire Terrier o Chow Chow o Dingo o Doberman o Pit Bull o Presa Canario o Rottweiler o Wolf Hybrid o Mix of any of the previously listed

breeds.

Any animal with vicious tendencies or a history of biting

Coverage for more than four (4) rental units. A rental unit is defined as the living quarters for one family. More than four (4) such exposures are considered Commercial Lines.

Homemade, barrel, or other DIY stoves

Homes with no primary heat source

Vacant and or unoccupied for more than 30 consecutive days

Applicant(s) have been convicted of arson in last 5 years

Uncorrected fire or building code violations

House for sale

Risks with a roof that is primary flat or less than a 3/12 pitch.

Risks with a roof that is in poor condition as evidenced by any of the following:

o Deterioration caused by the presence of algae and/or moss.

o Broken shingles o Shingles that are curled, warped or lifted o More than two layers of roof surfacing.

Kerosene or other portable space heaters older than 5 years and/or not U/L approved

Constructed prior to 1900

Home in Optional Loss Settlement program where market value of the home is less than 50% of the current replacement cost.

PROHIBITED LIST

WISCONSIN HOMEOWNERS MANUAL

Rev. 6/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 7

Prior Cancellation for Non-payment or canceled/non-renewed for underwriting reasons. Indicate the prior company, policy number and the reason for termination.

Supplemental heating systems, including wood burning stoves. Supplemental heating system must meet NFPA standards and be U/L approved. Additional requirements and rating information can be found on pages HO – 31-32.

Homes constructed with Exterior Insulation and Finish Systems (EIFS)

Homes of solid log construction. Log kit homes may be accepted. Hand hewn log and/or log and mortar homes are not eligible.

Farming activities and properties including former farms where the premises now has unused additional structures such as silos, implements, sheds, etc.

Other than domestic variety animals including but not limited to horses.

20 or more acres of land, including properties that are non-contiguous and/or not defined as residence premises.

Ponds on residence premises

On premises business pursuits including HO 04 42, Office, Professional, Private School or Studio

Risk with HO 24 71, Business Pursuits

Risks currently undergoing major renovations: o Renovations must be completed within 9 months o General contractors / sub-contractors involved in construction of the dwelling must maintain

Workers Compensation coverage.

Homes in the course of construction

Construction must be completed by a licensed contractor, other than the named insured

Construction may not exceed one year

Coverage A amount must equal 100% of the expected amount of insurance when completed

Risks located within 100 feet of a commercial exposure

Foreclosed Homes

Snowmobiles with engine size over 600 cc., ATV’s, and Personal Watercraft.

This list is not all inclusive. If something falls outside of our acceptable guidelines and is not listed here, please contact your underwriter for prior approval before binding.

PRIOR APPROVAL LIST

WISCONSIN HOMEOWNERS MANUAL

Rev. 6/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 8

ELITE HOMEOWNERS PROGRAM This is a preferred program and targets homes built since 1950 with Coverage A amounts from $150,000 to $700,000 and located in Public Protection Classes 1-9. This program requires Coverage A to be at 100% of replacement cost. Dwellings with solid fuel stoves are not eligible in this program. PROGRAM ELIGIBILITY 1. Coverage A amount of insurance must equal 100% of its replacement cost. 2. Market Value must be at least 70% of replacement cost. 3. The dwelling must have been built since 1950. 4. Dwellings over 40 years of age at the time of application must meet the Older Home

Requirements on page HO - 32. 5. The dwelling must be located in Public Protection Classes 1-9. 6. No losses in the last three years other than one weather related loss. 7. Solid fuel burning devices other than a built in fireplace not used as a heating source are not

eligible. 8. Seasonal dwellings are not eligible. 9. If there have been any losses other than one weather related claim in the past 5 years, risks

with insurance scores below 700 are not acceptable. PROGRAM REQUIREMENTS

1. Coverage A – 100% of replacement cost 2. Coverage C – Personal Property – Minimum amount of insurance is 75% of Coverage A and is written on a Replacement Cost basis. 3. Coverage D–Loss of Use — Amount of insurance is "Actual Loss Sustained" for 12 consecutive months after the date of direct physical loss or damage. 4. Automatic Increases — At each renewal, Partners Mutual will automatically increase Section I limits consistent with construction cost Indices. 5. The Partners Platinum Protection Plan providing additional coverages may be added to the policy at extra charge.

WISCONSIN HOMEOWNERS MANUAL

Rev. 6/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 9

CUSTOM HOMEOWNERS PROGRAM This is a standard program and targets homes built since 1900 with Coverage A amounts from $100,000 to $500,000 and located in Public Protection Classes 1-10. This program requires Coverage A to be at 100% of replacement cost. Dwellings with solid fuel stoves are eligible in this program with prior approval. HO-4 Tenant and HO-6 Condominium policies are written in this program. PROGRAM ELIGIBILITY 1. Coverage A amount of insurance must equal 100% of its replacement cost. 2. Market Value must be at least 70% of replacement cost. 3. The dwelling must have been built since 1900 and not be of ornate or unusual construction. 4. Dwellings over 40 years of age at the time of application must meet the Older Home

Requirements on page HO - 32. 5. The dwelling must be located in Public Protection Classes 1-9. 6. No losses in the last three years other than one weather related loss. 7. Solid fuel burning devices are eligible with prior approval and must meet the requirements on

pages HO-31-32. 8. Seasonal dwellings are eligible with prior approval. Insurance for the primary residence must

be provided by Partners Mutual. 9. If there have been any losses other than one weather related claim in the past 5 years, risks

with insurance scores below 600 are not acceptable. 10. Tenant and Condominium Coverage C–Personal property must be insured at 100% of

replacement cost. 11. Risks located in Public Protection Class 10 must be within eight road miles of the primary

responding fire department. PROGRAM REQUIREMENTS BY HO FORM Owner HO 00 02, HO 00 03, HO 00 05 - Coverage A–Dwelling 1. Coverage A – 100% of replacement cost 2. Automatic Increases - at each renewal Partners Mutual will automatically increase Section I

limits consistent with construction cost indices. 3. The Partners Plus Protection Plan providing additional coverages may be added to the policy

at extra charge. Tenant HO-00-04 — Contents Broad Form is written on a replacement cost basis with a minimum theft

deductible of $250. The amount of insurance must be equal to 100% of replacement cost value. 1. The Partners Plus Protection Plan providing additional coverages may be added to the policy at

extra charge. Condominium HO-00-06 — Unit Owners. The following coverage features are included at no additional

charge: 1. Coverage A-Dwelling is written on "additional risks of loss," replacement cost basis. The base

policy includes $10,000 of coverage. Higher limits are available. 2. Coverage C is written on “additional risks of loss” replacement cost basis. 3. Loss Assessment coverage is included up to $10,000. Higher limits are available. 4. The Partners Plus Protection Plan providing additional coverages may be added to the policy

at extra charge.

WISCONSIN HOMEOWNERS MANUAL

Rev. 6/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 10

OPTIONAL LOSS SETTLEMENT HOMEOWNERS PROGRAM This is a market value program and targets homes built since 1900 with Coverage A amounts from $90,000 to $200,000 and located in Public Protection Classes 1-10. This program requires Coverage A to be at least 50% of replacement cost. Dwellings with solid fuel stoves are eligible in this program with prior approval. PROGRAM ELIGIBILITY 1. Coverage A - Dwelling must be insured for 100% of market value less the value of land and at

least 50% of replacement cost. 2. The dwelling must have been built since 1900. 3. Dwellings over 40 years of age at the time of application must meet the Older Home

Requirements on page HO - 32. 4. Solid fuel burning devices are eligible with prior approval and must meet the requirements on

pages HO – 31-32. 5. Seasonal dwellings are eligible with prior approval. Insurance for the primary residence must

be provided by Partners Mutual. 6. Risks located in Public Protection Class 10 must be within eight road miles of the primary

responding fire department.

WISCONSIN HOMEOWNERS MANUAL

Rev. 6/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 11

HOMEOWNERS RATING Basic Premium Modifications Maximum total credit available for items A, C, D, E, F, G, I, J and solid fuel is 75%. A. Car/Home Discount 1. Eligibility. HO 2, 3, and 5 — A 22% discount will apply to the final policy premium if the named

insured also has a personal automobile policy with Partners Mutual or an application having an effective date within 60 days and the named insured on the auto and home policies are for the same individual (or husband and wife) except for the auto policy for a resident child or parent. The discount for HO 4 and 6 forms is 15%.

2. Effective Date a. New business policies will have the discount applied at once. b. Existing homeowner policies that become eligible as a result of a submitted automobile

application will receive the discount on the effective date of the automobile policy. c. If the automobile policy is canceled or non-renewed, the discount will be deleted from the

homeowner policy at the next renewal. 3. Qualifying applications must be quoted and issued under the same account number as the

existing automobile policy in order to receive the discount. B. Deductibles — Section I — Property — Effective April 1, 2015 the minimum All Peril Homeowners Deductible = $1,000 (HO 4 & 6 = $500) 1. Factors of the $500 deductible base premium. Deductible Factor Deductible Factor $100 ♦ 1.39 $1,000 0.85 $250 ♦ 1.18 $1,500 0.83 $500 ♦ 1.00 $2,500 0.80 $750 ♦ 0.94 $5,000 0.74 ♦ Not available for new business. 2. Flat Deductible with a 1% Windstorm or Hail Deductible - Form HO 03 12 Coverage A Up to $99,999 $100,000-$199,999 $200,000-$299,999 $300,000 and above $ 100 1.34 1.24 1.17 1.10 250 1.16 1.08 1.01 0.96 500 0.99 0.93 0.88 0.84 1,000 NA 0.82 0.78 0.74 2,500 NA NA NA 0.69 5,000 NA NA NA NA 3. Flat Deductible with a 2% Windstorm or Hail Deductible - Form HO 03 12 Coverage A Up to $99,999 $100,000-$199,999 $200,000-$299,999 $300,000 and above $ 100 1.31 1.13 1.01 0.91 250 1.09 0.98 0.89 0.81 500 0.95 0.86 0.78 0.71 1,000 0.84 0.76 0.68 0.62 2,500 NA NA 0.64 0.60 5,000 NA NA NA 0.56

WISCONSIN HOMEOWNERS MANUAL

Rev. 6/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 12

Car/Home Deductible — If the insured has both homeowners and car insurance with Partners Mutual at the time of a loss, the maximum deductible amount will not exceed the single highest deductible when multiple items of property are involved in the same occurrence.

C. Dwelling Age Adjustment — Age = Current policy term effective year minus year of construction of the dwelling.

HO Forms 2,3,5

Dwelling Age Factor Dwelling Age Factor Dwelling Age Factor

0 0.7800 13 0.9370 50-54 1.0400

1 0.7918 14 0.9494 55-59 1.0425

2 0.8036 15 0.9619 60-64 1.0450

3 0.8155 16 0.9744 65-69 1.0475

4 0.8274 17 0.9870 70-74 1.0500

5 0.8394 18 0.9996 75-79 1.0525

6 0.8514 19 1.0000 80-84 1.0550

7 0.8635 20-24 1.0250 85-89 1.0575

8 0.8756 25-29 1.0275 90-94 1.0600

9 0.8878 30-34 1.0300 95-99 1.0625

10 0.9000 35-39 1.0325 100+ 1.0650

11 0.9123 40-44 1.0350 12 0.9246 45-49 1.0375

HO Forms 4 & 6

Dwelling Age Factor Dwelling Age Factor Dwelling Age Factor

New 0.800 7 0.870 14 0.940

1 0.810 8 0.880 15 0.950

2 0.820 9 0.890 16 0.960

3 0.830 10 0.900 17 0.970

4 0.840 11 0.910 18 0.980

5 0.850 12 0.920 19 0.990

6 0.860 13 0.930 20 and older 1.000 D. Insurance Score Modifier

1. The insurance score premium modifier is based on the named insured’s insurance score. If there are multiple named insured’s, the highest score will apply.

2. The insurance score must be determined from the ATTRACT PROPERTY scoring system. 3. An insured may request to have an insurance score updated. The update will apply at the

policy renewal date.

*4. The insurance score premium modifier applies only to the basic premium charge.

TIER MODIFICATION TIER MODIFICATION 1 - 35% discount 6 - 0% discount 2 - 30% discount 7 +10% surcharge 3 - 20% discount 8 +30% surcharge 4 - 15% discount 9 +45% surcharge 5 - 10% discount 10 +60% surcharge

5. If a score is not available because of insufficient data or is a “No Hit”, Tier 8 applies.

WISCONSIN HOMEOWNERS MANUAL

Rev. 6/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 13

E. Protective Devices HO 04 16 — The following premium credits may be allowed for the installation of a burglar alarm, fire alarm, smoke detector, or automatic sprinkler system in the dwelling. Systems must be professionally installed and properly maintained. Proof of protective devices must be maintained in the agent’s office.

1. Central Station Fire Alarm System. 5% 2. Central Station Burglar Alarm system 5% 3. Automatic Sprinkler Systems with sprinklers in all areas 10% 4. Limited Automatic Sprinkler System (not installed in closets, attics, attached structures) 5% These credits apply to the Coverage A Base Premium. F. Roof Surfacing Adjustments 1. If the dwelling roof surfacing material is composed of wood shingles or wood shakes, add a

10% surcharge to the modified base policy premium. This surcharge or credit applies to the Coverage A Base Premium. * G. Residential Loss Rating Plan — Apply the following factor to the annual base dwelling premium

for claims incurred within the past three years. For the purpose of this rule, the total paid losses after the application of the policy deductible must exceed $500 for the surcharge to apply. There are no CAT exceptions.

H. Secondary Residence Credit — When liability coverage is provided on the primary residence as

well as the secondary seasonal residence, the basic premium for the seasonal residence shall be reduced $7.00. The policy covering the primary residence shall be extended under Section II to cover the additional insured location. See Optional Coverages and Additional Charges — Section II-Liability.

This credit applies to the Coverage A Base Premium. I. Senior Policyholder Discount — If the named insured or spouse is age 50 or over apply a 15%

credit to the base policy premium. The credit may be applied to new and renewal policies, but may not be applied mid-term.

This credit applies to the Coverage A Base Premium. J. Superior Construction Credit — A 10% credit applies to the Masonry Basic Premium when the

entire dwelling is constructed of non-combustible materials. This credit applies to the Coverage A Base Premium. K. Trampoline Surcharge — Trampolines located on the residence premises must meet the

following minimum underwriting requirements:

Non-Weather

Losses 0 1 2 3 4+

0 1.0000 1.1000 1.3000 1.5000 1.8000

1 1.1000 1.3000 1.5000 1.8000

2 1.3000 1.8000 1.8000

3 1.5000 1.8000

4+ 1.8000

Weather Losses

WISCONSIN HOMEOWNERS MANUAL

Rev. 6/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 14

1. The upper framework to which the bed of the trampoline is attached must be covered by padding at least one inch thick.

2. The area above the trampoline bed must be continuously enclosed by netting to a height of at least six feet. 3. The trampoline cannot be located next to a pool, waterway or other structure from which a

person could launch onto or land from the trampoline. 4. Trampoline must be secured in a manner to eliminate rollover during use or during a

windstorm.

Surcharge - Trampolines meeting the above requirements will have a flat annual surcharge of $40 applied. This charge is fully earned and not subject to seasonal removal or storage of the trampoline.

L. Affinity Group Discount Program An Affinity Group Discount of 3% shall be applied for individual members of a company approved risk group. A company approved risk group for the purpose of this rule must meet the following requirements: 1. The group must consist of 1,250 or more individuals who are employees or members of an organization such as, but not limited to, a credit union, association or government department, unit or agency; or 100 or more individuals who are employees of a corporation or partnership. a. This discount will also be available to current Partners Mutual Insurance Employees and to our licensed agents and agency staff members. 2. The group must have been in existence for at least 3 years and not formed primarily for the purpose of obtaining insurance. The group must complete the Affinity Marketing application, and Partners Mutual Insurance will notify the applicant in writing of the decision. We reserve the right to review each application for the Affinity Group Discount and make any inspections necessary to validate the status of any group or member applying for the Affinity Group Discount. An individual must meet the eligibility requirements of the Partners Mutual Homeowners Policy Program. Individual members include employees, members, or customers of an approved risk group. A group member will also include a resident relative of an employee, member, or customer of an approved risk group. The discount will only be added and removed upon renewal. There will be no mid-term adjustments to the policy. For all Forms, a factor of 0.97 shall be applied to the Base Premium.

WISCONSIN HOMEOWNERS MANUAL

Rev. 6/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 15

PREMIUM DETERMINATION Construction Definitions 1. Frame — Exterior wall of wood or other combustible construction, including wood-iron clad,

stucco or wood or plaster on combustible supports, or aluminum or plastic siding over frame. 2. Masonry Veneer — Exterior walls of combustible construction veneered with brick or stone. 3. Masonry — Exterior walls constructed of masonry materials such as adobe, brick, concrete,

gypsum block, hollow concrete block, stone, tile or similar materials and floors and roof of combustible construction.

4. Mixed (Masonry/Frame)— A combination of both frame and masonry construction shall be classed and coded as frame when the exterior frame walls exceed 33 1/3% of the total exterior wall area; otherwise class as masonry.

5. Superior Construction – Exterior walls and floors and roof constructed of, and supported by metal, masonry, or other non-combustible materials.

Public Protection Class 1. The Public Protection Class listings in the ISO Community Mitigation Classification Manual

apply to risks insured under Homeowner policies.

A. The protection class indicated applies in a municipality or classified area where a single class of fire protection is available throughout (6, 7, 8, etc.)

1. Class 8B may be assigned to a community that provides superior fire protection services and alarm facilities but lack the water supply required for a Class 8 or better.

B. In a classification where two or more classes are shown, the classification is as follows:

1. If the split is 6/9:

Distance to Primary Responding Fire Department Class

a. 5 road miles or less with hydrant within 1,000 feet 6

b. 5 road miles or less with hydrant beyond 1,000 feet 9

c. Over 5 road miles 10

C. In a classified area where a split classifications are shown where no hydrants are installed (Example: 9/10), or where the hydrant distance does not apply due to an alternate creditable water supply (Example: 7/10), the classification is determined as follows:

1. If the split class is x/10:

Distance to Primary Responding Fire Department Class

a. Within 5 road miles of fire station, unless otherwise indicated X

c. Over 5 road miles 10

WISCONSIN HOMEOWNERS MANUAL

Rev. 6/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 16

Public Protection Class – continued

Forms 2,3,5

Forms 4 & 6

Frame Masonry

Frame Masonry Protection Construction Construction

Protection Construction Construction

Class Factors Factors

Class Factors Factors

1 1.000 0.900

1 1.000 0.900 2 1.000 0.900

2 1.000 0.900

3 1.000 0.900

3 1.000 0.900 4 1.000 0.900

4 1.000 0.900

5 1.000 0.900

5 1.000 0.900 6 1.000 0.900

6 1.000 0.900

7 1.100 1.000

7 1.100 1.000 8 1.100 1.000

8 1.100 1.000

8B 1.150 1.050

8B 1.150 1.050 9 1.378 1.330

9 1.450 1.400

10 1.943 1.680

10 1.850 1.600 Premium Rounding All premiums shown on the policy are rounded to the nearest whole dollar on annual policies and to the next $ .50 on six month policies. Premium Computation Homeowner Program - Elite, Custom, Optional Loss Settlement

Base Premium X Key Factor Table (Coverage A Relativities) X Territory Factor X Program Factor (Elite, Custom OLS) X Form Factor (02, 03, 05, 08) X Protection Class/Construction (Frame, Masonry) Factor X Deductible Factor X •Dwelling Age Adjustment Factor X •Superior Construction Factor X •Senior Factor X •Protective Device Factor HO 04 16 X •Residential Loss Factor. X •Roof Surfacing Factor. X •Insurance Score Factor X •Solid Fuel Factor X •Car/Home Discount Factor X Base Policy Premium = Optional Coverages x Car/Home discount factor + Homeowner Premium = •See page HO-11 for the maximum total discount which can be applied to each risk

WISCONSIN HOMEOWNERS MANUAL

Rev. 6/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 17

OPTIONAL COVERAGE PACKAGES — SECTION I PROPERTY Elite Program – PARTNERS PLATINUM PROTECTION PLAN – Form 21165 $50. Elite risks not of geodesic, log or earth home construction can have the Partners Platinum Protection

Plan containing the following additional coverages added at an additional charge. A. Dwelling Replacement Coverage is increased to 125% of the Coverage A Dwelling amount. B. Coverage B–Other Structures amount is added to Coverage A–Dwelling if there are no other

structures on the residence premises. C. Refrigerated Products — Covers spoilage to food in a deep freezer or refrigerator from the perils

of power failure or mechanical failure up to $500. The Section I deductible applies to losses payable under this coverage.

D. Lock Coverage — Up to $250 coverage applies for re-keying house locks if keys are stolen. A

$25 deductible applies. E. Debris Removal — Expenses incurred to remove debris of trees, resulting from windstorm or hail

up to $500. F. Credit Card and Fund Transfer Card Coverage — The limit of liability is increased to $1,000. G. Coverage C - Personal Property ─ Special Limits of Liability Item 1. Money, bank notes, bullion,

gold other than goldware, silver, other than silverware, platinum coins and medals coverage is increased to $500.

H. Thermopane Fogging ─ is covered up to $500. A special deductible of $250 applies to this

coverage. I. Arson Reward Coverage ─ A minimum reward of $500 and a maximum reward of $5,000 may be

offered subject to our discretion. J. Loss of Use — Coverage limit is actual loss sustained within 12 months immediately following a

covered loss. K. Business Property on the residence premises is increased to $5,000. L. Identity Theft Remediation costs of up to $2,500. M. Collapse from Subsurface Water. N. Personal Injury

WISCONSIN HOMEOWNERS MANUAL

Rev. 6/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 18

OPTIONAL COVERAGE PACKAGES — SECTION I PROPERTY Custom Program – PARTNERS PLUS PROTECTION PLAN – Form 21164 Rates: HO 2,3,4,5 = $35, HO 6 = $20 Custom risks insured to 100% of replacement cost and not of geodesic, log or earth home construction can have the Partners Plus Protection Plan containing the following additional coverages added at an additional charge. A. Dwelling Replacement Coverage is increased to a maximum of 125% of the Coverage A

Dwelling amount. B. Coverage B–Other Structures amount is added to Coverage A–Dwelling if there are no other

structures on the residence premises. C. Refrigerated Products — Covers spoilage to food in a deep freezer or refrigerator from the perils

of power failure or mechanical failure up to $500. The Section I deductible applies to losses payable under this coverage.

D. Lock Coverage — Up to $250 coverage applies for re-keying house locks if keys are stolen. A

$25 deductible applies. E. Debris Removal — Expenses incurred to remove debris of trees, resulting from windstorm or hail

up to $500. F. Coverage C–Personal Property — Coverage is afforded on a replacement cost basis. G. Credit Card and Fund Transfer Card Coverage — The limit of liability is increased to $1,000. H. Coverage C - Personal Property ─ Special Limits of Liability Item 1. Money, bank notes, bullion,

gold other than goldware, silver, other than silverware, platinum coins and medals coverage is increased to $500.

I. Thermopane Fogging ─ Covered up to $500. A special deductible of $250 applies to this

coverage. J. Arson Reward Coverage ─ Includes a minimum reward of $500 and a maximum reward of

$5,000 subject to our discretion. K. Loss of Use — Coverage limit is actual loss sustained within 12 months immediately following a

covered loss. L. Business Property — On the residence premises is increased to $5,000.

WISCONSIN HOMEOWNERS MANUAL

Rev. 6/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 19

ADDITIONAL OPTIONAL COVERAGES The following optional coverages are available with all programs unless specified otherwise. INCREASED LIMITS — SECTION I PROPERTY A. Coverage A – Dwelling 1. HO-6 Unit Owners. The Basic $10,000 open perils replacement cost limit can be increased for

$2.50 per $1,000. 2. HO-6 Unit-Owners Coverage A–Dwelling – Special Coverage HO 17 32 — The policy

automatically provides a basic Coverage A limit of $10,000 on a replacement cost basis for "additional risks of loss" without an additional premium charge.

B. Coverage B – Other Structures — Rates are per $1,000 of coverage. 1. Owner Occupied a. Designed and used for private garage purposes or with HO 04 48 $2

less than 250 sq. ft. ground floor area. The normal limit of 10% of Coverage A may be increased at the above rate per $1,000 increase: b. Other than a. All structures must be scheduled for coverage to apply $3 2. Rented to Others HO 04 40 $3 See Section II-Liability for exposure charge. 3. Permitted incidental occupancy (office, studio, or professional) HO 04 42 $3 See Section II-Liability for exposure charge. 4. Located Away From The Residence Premises HO 04 92 $5 Coverage only applies to specifically scheduled structures. C. Coverage C— Personal Property 1. The standard limit of 50% of Coverage A in the Custom and O.L.S. Programs and 75% in the Elite

Program may be increased at a rate of $1 per $1,000 of increase. 2. If the policy is not endorsed to provide coverage on a replacement cost basis, the Coverage C

limit can be reduced to 40% of Coverage A at a rate of $1 per $1,000 of reduction. 3. Property in Other Residences — HO 04 50 - The normal limit of 10% of Coverage C may be

increased at a rate of $6 per $1000 of insurance. 4. Permitted Incidental Occupancy (office, studio, or professional) HO 04 42 — $3. See Section II — Liability for exposure charge. 5. Special Limits of Liability HO 04 65 (Use H0 04 66 when HO 00 05 or HO 17 31 applies.) a. Jewelry, Watches and Furs — The special $1,500 Theft limit may be increased to $5,000

($1,000 per item limit) at a rate of $12 per $1,000 increase. b. Money and Securities — The special limit of $200 on money may be increased to $1,000

at a rate of $4 per $100 of increase. The special limit of $500 on money when the Homeowners Plus endorsement is attached may be increased to $1,000 at the same rate. The special limit of $1,500 on securities may be increased to $2,000 at a rate of $3 per $100 of increase.

c. Silverware, Goldware, Pewterware — The special limit of $2,500 for loss by theft may be increased to a maximum of $10,000 at a rate of $3 per $500 of increase.

d. Firearms — The special limit of $2,500 for loss by theft may be increased to $6,000 at a rate of $2 per $100 of increase.

e. Electronic Apparatus — The special limit of $1,500 may be increased to $5,000 at a rate of $10 per $500 of increase.

WISCONSIN HOMEOWNERS MANUAL

Rev. 6/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 20

6. Business Property — HO 04 12 — The special limit of $2,500 ($5,000 when the Partners Plus or Partners Platinum endorsement applies) may be increased to $10,000 at a rate of $25 per $2,500 of increase.

7. Credit Card — HO 04 53 —The special limit of $500 may be increased to $10,500 at a rate of $1 per $2,500 of increase.

8. Personal property located on the residence premises in uninsured structures. $3 per $1,000 of coverage.

D. Coverage D–Loss of Use — HO-2, HO-3 and HO-5 — The normal limit of 50% of Coverage A–

Dwelling may be increased at a rate of $2 per $1,000. The special limit of “Actual loss sustained” for 12 consecutive months after the date of direct physical damage applies to all policies to which the Partners Plus and Partners Platinum Coverages are applicable.

E. Loss Assessment — Form HO 04 35 — The residence premises special limit of $10,000 can be

increased up to $50,000 at a rate of $0.50 per $1,000. Coverage can be provided for each additional location not exceeding two at these premiums per location up to $50,000 at a rate of $0.50 per $1,000.

F. Fire Department Service Charge — Form 21188 — The special limit of $500 may be increased at a

rate of $2 per $100 of insurance. G. Personal Property Replacement Cost Coverage — Form HO 04 90.

Coverage Form HO 00 02, HO 00 03 or HO 00 05 may be broadened to provide personal property replacement cost coverage. The Coverage C limit of liability is increased to 75% of Coverage A and cannot be reduced. Premium is 10% of the Basic Premium. This coverage is automatically included on policies issued with the Partners Plus and Partners Platinum endorsements.

H. Special Personal Property Coverage, Coverage C — Personal Property may be insured for

"additional risks of loss". Not available for O.L.S. risks. 1. Dwelling — See HO 00 05. 2. Condominium — HO 17 31 - Included in base policy. I. Foundation Collapse and Theft of Building Materials Coverage for Homes Under Construction —

Builders Risk Changes — Form 2108 — Provides foundation collapse and $5,000 theft of building materials coverage for a dwelling under construction. See endorsement for conditions regarding when coverage ceases. The dwelling must be insured for 100% of its completed replacement cost. The flat charge is non-refundable. Select the same deductible as is applicable to the Homeowners policy. This coverage is for new construction only.

Deductible Premium $ 500 $40 750 38 1,000 34 1,500 33 2,500 32 5,000 30

WISCONSIN HOMEOWNERS MANUAL

Rev. 6/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 21

J. Equipment Breakdown Coverage — Provides coverage due to the breakdown of mechanical, electrical or pressurized systems.

1. Policy type and Coverage Forms Policy Coverage Limits HO 00 02 - 21181 2% of Coverage A* HO 00 03 - 21182 2% of Coverage A* HO 00 04 - 21183 $10,000 HO 00 05 - 21184 2% of Coverage A* HO 00 06 - 21185 $10,000 - Included in base policy.

* *Maximum policy limit of $50,000.

A $500 deductible applies to each occurrence under this coverage regardless of the policy deductible.

K. Earthquake — Form HO 04 54 — Optional coverage subject to a 10% limit of liability deductible with a

$250 minimum. 1. Rate per $1,000 of coverage. Deductible % Frame † and Superior Masonry† 5% 0.150 0.480 10% 0.120 0.400 15% 0.096 0.340

20% 0.078 0.280 25% 0.060 0.240 † If exterior Masonry Veneer is covered, rate as Masonry. If not covered — rate as frame. 2. Binding - Coverage cannot be bound for 30 days following a 4.0 earthquake or greater for

risks within 100 miles of the epicenter. L. Earthquake — Loss Assessment Coverage — Form HO 04 36 — Written in conjunction with Loss

Assessment Coverage HO 04 35. Coverage is bound based on the unit owner’s proportionate interest in total value of all collectively owned buildings and structures of the association. Rates per $1,000 are: Frame $.30; Masonry $.60.

M. Limited Water Backup of Sewers, Drains or Sumps — Form 21189 — Coverage may be extended

to cover direct loss caused by water which backs up through a sewer, drain, or sump. Maximum binding authority is $25,000. The regular Section I deductible applies. Coverage is Non-binding for 30 days from the date of request. Annual Rate: First $ 1,000 to $10,000 coverage limit $10 per $1,000

Next $11,000 to $25,000 coverage limit $ 8 per $1,000 Next $26,000 to $40,000 coverage limit $ 6 per $1,000

The coverage limit is the total amount we will pay for all losses during one 12 month policy term or any two consecutive 6 month policy terms. The premium is not pro-rated and is fully earned when coverage is made effective.

N. Home Day Care — Form HO 04 97 —Coverage may be extended to provide property coverage under

Coverage C and Section II Liability coverages for non-commercial Home Day Care business in the residence premises. Not eligible if: (1) there are more than 3 persons receiving care; (2) the day care provider is licensed with any state authority or; (3) other day care liability coverage is provided by another insurer. For rating liability refer to Optional Coverages, Section II.

WISCONSIN HOMEOWNERS MANUAL

Rev. 6/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 22

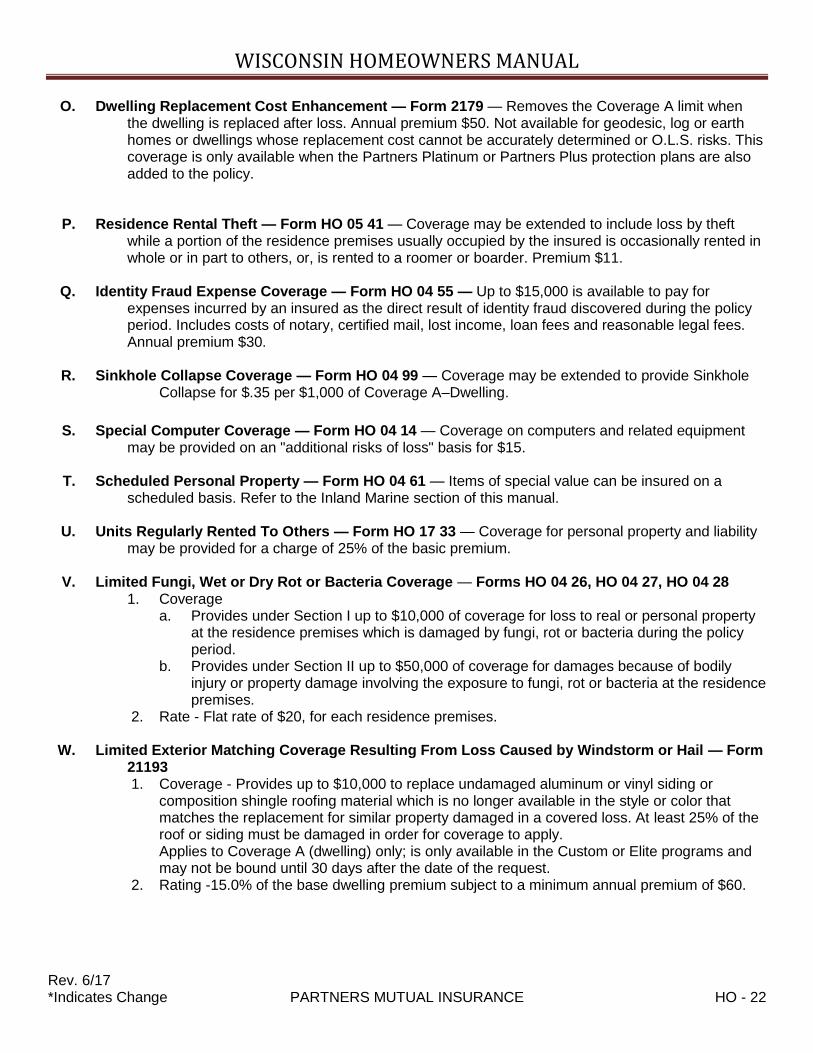

O. Dwelling Replacement Cost Enhancement — Form 2179 — Removes the Coverage A limit when the dwelling is replaced after loss. Annual premium $50. Not available for geodesic, log or earth homes or dwellings whose replacement cost cannot be accurately determined or O.L.S. risks. This coverage is only available when the Partners Platinum or Partners Plus protection plans are also added to the policy.

P. Residence Rental Theft — Form HO 05 41 — Coverage may be extended to include loss by theft

while a portion of the residence premises usually occupied by the insured is occasionally rented in whole or in part to others, or, is rented to a roomer or boarder. Premium $11.

Q. Identity Fraud Expense Coverage — Form HO 04 55 — Up to $15,000 is available to pay for

expenses incurred by an insured as the direct result of identity fraud discovered during the policy period. Includes costs of notary, certified mail, lost income, loan fees and reasonable legal fees. Annual premium $30.

R. Sinkhole Collapse Coverage — Form HO 04 99 — Coverage may be extended to provide Sinkhole

Collapse for $.35 per $1,000 of Coverage A–Dwelling.

S. Special Computer Coverage — Form HO 04 14 — Coverage on computers and related equipment

may be provided on an "additional risks of loss" basis for $15. T. Scheduled Personal Property — Form HO 04 61 — Items of special value can be insured on a

scheduled basis. Refer to the Inland Marine section of this manual. U. Units Regularly Rented To Others — Form HO 17 33 — Coverage for personal property and liability

may be provided for a charge of 25% of the basic premium. V. Limited Fungi, Wet or Dry Rot or Bacteria Coverage — Forms HO 04 26, HO 04 27, HO 04 28 1. Coverage

a. Provides under Section I up to $10,000 of coverage for loss to real or personal property at the residence premises which is damaged by fungi, rot or bacteria during the policy period.

b. Provides under Section II up to $50,000 of coverage for damages because of bodily injury or property damage involving the exposure to fungi, rot or bacteria at the residence premises.

2. Rate - Flat rate of $20, for each residence premises. W. Limited Exterior Matching Coverage Resulting From Loss Caused by Windstorm or Hail — Form

21193 1. Coverage - Provides up to $10,000 to replace undamaged aluminum or vinyl siding or

composition shingle roofing material which is no longer available in the style or color that matches the replacement for similar property damaged in a covered loss. At least 25% of the roof or siding must be damaged in order for coverage to apply. Applies to Coverage A (dwelling) only; is only available in the Custom or Elite programs and may not be bound until 30 days after the date of the request.

2. Rating -15.0% of the base dwelling premium subject to a minimum annual premium of $60.

WISCONSIN HOMEOWNERS MANUAL

Rev. 6/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 23

OPTIONAL COVERAGES AND ADDITIONAL CHARGES — SECTION II LIABILITY COVERAGES — The coverage limits of Coverage E - Liability and Coverage F - Medical Payments To Others must be uniform for all exposures covered by the policy. All Liability limits are per occurrence. All Medical Payments limits are per each person.

A. Increased Limits — Residence Premises E–Liability/F–Medical Pay $100,000/$1,000 $200,000/$1,000 $300,000/$1,000 $500,000/$1,000 Additional Premium — $ 0 $5 $9 $14 See Section B for the additional premium charge to increase medical payments above $1,000. B. Increased Limits — Coverage F — Medical Payments — Applicable to each Section II Optional

Coverage and Additional Charge. Add the premium for the limit shown below to the base premium for each optional coverage or additional charge made to the policy.

Coverage F - Medical Payments to Others $2,000 $3,000 $4,000 $5,000 Additional Premium $2 $4 $6 $8 C. Secondary Residence Premises Occupied by the Insured — Required coverage for an additional

residence occupied by the insured. This includes seasonal residences, time share condominiums, etc.

E–Liability/F–Medical Pay $100,000/$1,000 $200,000/$1,000 $300,000/$1,000 500,000/$1,000 1 or 2 family $7 $8 $9 $13 See Section B for the additional premium charge to increase medical payments above $1,000. D. Additional Residence Rented To Others — Form HO 24 70 — Optional liability coverage for

additional residence premises rented to others, not at the insured's residence premises. Not eligible if more than four (4) rental units. A rental unit is defined as the living quarters for one family. More than four (4) such exposures are considered Commercial Lines. See the Dwelling Fire Section for property rates.

E–Liability/F–Medical Pay $100,000/$1,000 $200,000/$1,000 $300,000/$1,000 $500,000/$1,000 1 Family $30 $33 $36 $42 2 Family 52 58 62 76 3 Family 67 74 80 96 4 Family 82 91 98 120 See Section B for the additional premium charge to increase medical payments above $1,000. E. Additional Insured — Form HO 04 41 — This form can be used to cover the interest of the dwelling

owner/seller in a land contract; dwelling owner in a life estate and; co-owners in a multiple unit dwelling. Coverage is provided under Homeowner coverages A, B, E, and F. A trust or other legal entity can be named under this form but, cannot be added as a named insured.

F. Residence Employees — A charge is required for each employee in excess of two other than

employees whose time of employment is not more than half of the customary full time or to whom the Workers' Compensation exclusion applies as set forth in Section II of the policy.

E–Liability/F–Medical Pay $100,000/$1,000 $200,000/$1,000 $300,000/$1,000 $500,000/$1,000 Premium $5 $5 $7 $9 See Section B for the additional premium charge to increase medical payments above $1,000.

WISCONSIN HOMEOWNERS MANUAL

Rev. 6/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 24

G. Business Pursuits — Form HO 24 71 — Optional coverage can be extended to provide liability coverage for the insured arising out of a business other than one solely owned by the insured. (For solely owned business coverage, consult the Commercial sections of this manual or the Home Business Section in the Homeowners General Rules.) Premiums apply to each person desiring coverage.

Business Class A. Clerical Office Employees: Salespeople, Collectors or Messengers — No installation,

demonstration or servicing operations. B. Salespeople, Collectors or Messengers — including installation, demonstration or

servicing operations. C. Teachers-Athletics, laboratory, manual training, physical training and swimming

instruction, excluding liability for corporal punishment of pupils. D. Teachers — Not otherwise classified, excluding liability for corporal punishment of

pupils. E. Teachers — Liability for corporal punishment of pupils. Additional premium for this

coverage must be added to C or D above. F. For all other occupations — Refer to company or Section V. Home Business Insurance

Coverage. E–Liability/F–Medical Pay $100,000/$1,000 $200,000/$1,000 $300,000/$1,000 $500,000/$1,000 Business Class A. $ 3 $ 3 $ 4 $ 6 B. 6 6 6 9 C. 10 11 11 16 D. 5 5 5 8 E. 4 4 5 9 See Section B for the additional premium charge to increase medical payments above $1,000. H. Incidental Farming Personal Liability — Form HO 24 72 —Optional coverage may be provided for

liability of an insured when there is farming or farm land rental on or away from the residence premises. Total farm related income must be less than $10,000 and farmed acreage less than 80. Please submit prior to binding.

E–Liability/F–Medical Pay $100,000/$1,000 $200,000/$1,000 $300,000/$1,000 $500,000/$1,000 On Premise $27.50 $31.90 $34.10 $37.40 Off Premises 55.00 63.80 68.20 74.80 See Section B for the additional premium charge to increase medical payments above $1,000. * This coverage can no longer be added at new business or new endorsements to existing business effective April 1, 2016.

I. Permitted Incidental Occupancies — Form HO 04 42 — Optional Office, Studio, Professional. See

Section I-Property coverages for property rates. Liability premiums for incidental occupancy in the dwelling, another structure on the residence or at an additional residence (HO 24 43) are:

E–Liability/F–Medical Pay $100,000/$1,000 $200,000/$1,000 $300,000/$1,000 $500,000/$1,000 Residence Premises $ 7 $ 9 $10 $14 Additional Residence Occupied by Insured 10 11 12 16 See Section B for the additional premium charge to increase medical payments above $1,000.

WISCONSIN HOMEOWNERS MANUAL

Rev. 6/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 25

J. Watercraft Liability — Form HO 24 75 — Optional Watercraft Liability is provided for outboard motor powered watercraft at no charge. For all other watercraft apply these premiums. For personal watercraft (Jet Skis or Wave Runners) apply the over 30 MPH charge.

E–Liability/F–Medical Pay $100,000/$1,000 $200,000/$1,000 $300,000/$1,000 $500,000/$1,000 Under 30 feet AND Under 16 mph $15 $17 $19 $25 16-30 mph 31 36 40 47 Over 30 mph 77 88 98 128 Sailboats 26-40 ft. 31 35 40 45 with no auxiliary power

Sailboats with auxiliary power are rated as inboards. Coverage should be written for the full policy period. These rates contemplate a navigational season of 7 months or less.

See Section B for the additional premium charge to increase medical payments above $1,000. K. Recreational Vehicles — Form 2102 — Optional liability coverage can be provided for each

recreational vehicle owned by an insured. Vehicle types eligible for this coverage include four-wheeled ATVs, UTVs, golf carts, snowmobiles, and residential service vehicles including small personal tractors. All other vehicle types, refer to your underwriter prior to binding.

E–Liability/F–Medical Pay $100,000/$1,000 $200,000/$1,000 $300,000/$1,000 $500,000/$1,000 1-600 cc 2 Stroke and 1-749 cc 4 Stroke Engine First vehicle $24 $30 $35 $52 Each additional vehicle 8 10 12 21 All Other. Refer to your underwriter prior to binding. First vehicle $48 $60 $70 $104 Each additional vehicle 16 20 24 42 See Section B for the additional premium charge to increase medical payments above $1,000. All Other vehicle types will increase at a $4 increment instead of $2. L. Personal Injury Liability — Form HO 24 82 — Optional coverage extension for personal injury such

as false arrest, libel or invasion of privacy included in Partners Platinum. E–Liability/F–Medical Pay $100,000/$1,000 $200,000/$1,000 $300,000/$1,000 $500,000/$1,000 Premium $10 $11 $12 $15 M. Home Day Care Coverage — Form HO 04 97 — Optional liability coverage not available when more

than three persons are receiving care, the day care provider is State licensed or if any day care liability is written elsewhere.

E–Liability/F–Medical Pay $100,000/$1,000 $200,000/$1,000 $300,000/$1,000$500,000/$1,000

Premium $100 $117 $133 $149 See Section B for the additional premium charge to increase medical payments above $1,000. N. Waterbed Liability — Form 21128 — Optional ─ A Tenant’s policy may be endorsed to pay all sums

for which an insured is legally liable to pay. Coverage E Limit of Liability $100,000 $200,000 $300,000 $500,000 Premium $15 $18 $20 $25

WISCONSIN HOMEOWNERS MANUAL

Rev. 6/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 26

HOME BUSINESS COVERAGE A. Eligibility 1. The Home Business Insurance Coverage Endorsement may be used in conjunction with a

Homeowners policy to cover the Section I and Section II exposures of a permitted business. 2. To be eligible for coverage under this endorsement a risk must meet the following criteria: a. The home business: (1) Must be owned by the named insured or by a partnership, joint venture or other

organization comprised only of the named insured and resident relatives. (2) Must be operated from the residence premises that is declared on the Homeowners

Declaration and used principally for residential purposes. (3) May be operated from the home and/or other structure on the residence premises. (4) May have up to three employees; and (5) Must not involve the (a) manufacture, sale or distribution of food products; or (b) manufacture, sale or distribution of personal care products such as shampoo,

hair color, soap, perfume or other like items applied to the body or consumed; b. For all business classifications described in Paragraph B., the Gross Annual Receipts of

the home business may not exceed $250,000. 3. A permitted business that is operated from the residence premises is afforded coverage under

either the Permitted Incidental Occupancy or Home Day Care Coverage Endorsement, cannot be afforded coverage under the Home Business Endorsement.

B. Coverages — Form HO 07 01 1. Section I - Property The Home Business Endorsement: a. Provides coverage for the property of the described business and for property of others

in the care of the business up to the Coverage C limit of liability entered on the Homeowners Declarations. Therefore, the Coverage C limit should reflect the values of the personal and business property to be insured.

b. Provides coverage for: (1) Accounts receivable ($5,000 limit); (2) Loss of business income extra expense (actual cost for a maximum of 12 months);

and (3) Valuable papers ($2,500 limit). c. Increases the Coverage C Special Limits of Liability on: (1) Money to $1,000; (2) Credit Cards to $1,000; and (3) Business property away from the residence premises to $5,000.

WISCONSIN HOMEOWNERS MANUAL

Rev. 6/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 27

2. Section II - Business Liability a. The Home Business Endorsement provides coverage for such business liability

exposures as premises operations, products-completed operations, advertising injury, and personal injury. The limits of liability for these coverages are on an annual aggregate basis and are determined in the following manner:

(1) For Products Completed Operations Hazard Liability, the limit is the same as the Coverage E limit shown in the Homeowners Declarations;

(2) For All Other Business Liability, the limit is twice the sum of the combined Coverage E and Coverage F Limits shown in the Homeowners Declarations; and

(3) For the Coverage F Sublimit of liability, the limit is the same as the Coverage F limit shown in the Homeowners Declarations.

b. The limit of liability for Additional Coverage 3., Damage to Property of Others is increased to $2,500.

3. Professional Liability

NO PROFESSIONAL LIABILITY COVERAGE IS PROVIDED IN THE HOME BUSINESS ENDORSEMENT.

C. Classifications — Only those operations described below are eligible for the Home-Based Business

Endorsement. 1. Office — Businesses involving professional or administrative activities. Accounting Service Counseling Desktop Publishing Drafters Financial Planning

General (excl. medical or professional) Graphic Art Insurance Agent Real Estate Agent Word Processing

2. Service — Businesses providing repair or other services. Barber (excl. tanning) Beautician (excl. tanning) Bicycle Repair Carpet or Upholstery Cleaning Clock, Jewelry or Watch Repair Computer or Electronic Repair Dog or Cat Grooming (no training) Instruction (music, etiquette, etc.) Locksmith

Mailing and Addressing Manicurist Musical Instrument Repair Photography (weddings, etc.) Picture Framing Printer Shoe Repair Tailoring/Sewing

3. Sales — Business involved in product sales, other than crafts made at the residence and sold

from the home or other locations. Artist and Craft Supplies Coins and Stamps Collectibles Cosmetics Decorative Housewares Florists

Gifts Household and Kitchen Products Personal Care Products Stationery and Paper Products Trophy Sales

WISCONSIN HOMEOWNERS MANUAL

Rev. 2/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 28

4. Crafts — Businesses involved in selling, from the home, other structure or other locations, crafts made in the home or other structure.

Baskets Calligraphy Candles Ceramics Dry Flower Arrangements Jewelry Leather Goods Metal work Needlework Pottery Quilts Sculptures Stained Glass Weaving Wood Products Wreaths D. Home Business Additional Premium 1. Section I — Property — When a home business is operated from one or more other

structures on the residence premises, multiply each structure’s coverage amount by $4. Per $1,000 of coverage.

2. Section II - Business Liability Limits and Premium Homeowners Home Business Coverage E Coverage F Products- All Other Personal Medical Payments Completed Business Annual Liability to Others Operations Liability Premium $100,000 $1,000 $100,000 $ 202,000 $100 200,000 1,000 200,000 402,000 115 300,000 1,000 300,000 602,000 124 400,000 1,000 400,000 802,000 130 500,000 1,000 500,000 1,002,000 135 3. Coverage F ─ Increased Limits — When the Homeowners Coverage F limit is increased to: $2,000 add $2 3,000 add $4 4,000 add $6 5,000 add $8

WISCONSIN HOMEOWNERS MANUAL

Rev. 2/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 29

COUNTRY HOMEOWNER COVERAGE — The Country Homeowner Rating Plan is offered to the rural property owner who is not otherwise eligible for a Homeowners policy due to farm structures or minimal farming operations.

Exposures meeting the intent of this endorsement are typically referred to as Hobby farms or

Gentleman’s farms whereas a small farm is maintained for pleasure rather than a source of significant income. These farms will not produce large amounts of food, grain, or livestock for major markets.

A. Eligibility — Risks qualifying for the Country Homeowner Program must meet the following conditions: 1. the primary residence is an owner occupied dwelling insured for at least $100,000; 2. the Insureds do not derive more than $5,000 of gross annual income from all farm-related

operations (including, but not limited to: produce stand sales, sale of livestock, crops, etc.); 3. no Farm Personal Property is insured elsewhere and the Partners Mutual coverage limit does

not exceed $20,000; 4. the total limit of insurance for all farm buildings does not exceed 50% of the dwelling limit; 5. maximum acres owned and/or farmed by the insured at the insured location 40 6. the property is ineligible if it contains any of the following exposures: a. Insureds conducting any of the following operations on the premises: (1) raising, boarding, training or using horses or ponies for racing, show, or riding

purposes (contact your Underwriter prior to binding if riding is exclusively by the insured);

(2) pet kennel operations, including grooming and boarding; (3) custom farming operations; (4) production or sale of milk, butter or cheese; (5) any commercial business such as fur farms, sawmills, warehouses, cattle dealers,

sales barns, etc; (6) pick your own operations such as blueberry, strawberry, vegetables, etc. (7) Christmas tree farms and other harvest your own trees and/or similar nursery

operations. b. vacant or unoccupied buildings; c. property not maintained in a neat, clean and orderly manner; d. properties in the process of foreclosure or sale or where the owner has filed bankruptcy; e. raising of exotic animals (llama, bison, ostrich, elk, deer, etc); f. any building with exposed urethane, styrene, or EIFS insulation; g. tenant or condominium policies; h. homes or houses of the mobile or trailer type; i. farm employees; j. solid fuel stoves or furnaces located in farm buildings; k. storage of chopped hay, silage, or other combustible crop material; l. storage of property of others (boats, cars, trailers, etc.). m. four or more horses. n. four or more head of cattle. 7. Risks located in Public Protection Class 10, regardless of mileage to responding fire

department are not eligible for Coverages G or H. B. Coverages — Form 21151 1. Property Coverages a. Coverage G - Scheduled Farm Personal Property b. Coverage H - Farm Barns, Buildings and Structures c. Perils applicable to both Coverage G and Coverage H

WISCONSIN HOMEOWNERS MANUAL

Rev. 2/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 30

Windstorm or Hail Explosion Riot or Civil Commotion Aircraft Vehicles Smoke Vandalism & Malicious Mischief Theft Collision Electrocution of Livestock Country Homeowner Rates: 1. Rate the dwelling, other structures designed and used exclusively for private garage

purposes, household personal property, loss of use and optional coverages in the appropriate program including charges for increased liability and medical payments limits.

2. Rate Farm Barns and Outbuildings and Scheduled Farm Personal Property as follows: Deductible Options Rate per $1,000 of Coverage $500 $750 $1,000 $1,500 $2,500 $5,000 a. Scheduled Farm Personal Property $5.50 $5.17 $4.68 $4.57 $4.40 $4.07 b. Farm Buildings ─ Includes all buildings not designed and used exclusively for private garage purposes. Barns and All Multi-story Buildings $7.70 $7.24 $6.55 $6.39 $6.16 $5.70 All Farm Buildings Other Than Barns $6.60 $6.20 $5.61 $5.48 $5.28 $4.88 c. Collapse— Add to the Barn, Other $1.10 $1.10 $1.10 $1.10 $1.10 $1.10 Than Barn or Farm Personal Property rate. Collapse Coverage may not be bound on structures over 20 years old. Effective April 1, 2016 the minimum Country Homeowners Deductible for New Business = $1,000 3. Country Homeowners Liability Additional Premium.

Coverage F Coverage E Medical Payments Annual Personal Liability to Others Premium $100,000 $1,000 $42.90 200,000 1,000 46.20 300,000 1,000 52.80 500,000 1,000 62.70 4. Coverage F — Increased Limits If Coverage F is increased to $2,000 add $2.20 $3,000 add $4.40 $4,000 add $6.60 $5,000 add $8.80

WISCONSIN HOMEOWNERS MANUAL

Rev. 2/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 31

SOLID FUEL BURNING DEVICES A. Acceptable heating devices are: 1. Auxiliary wood or coal central heating units attached to a gas or oil furnace central heating

system and stoves, freestanding fireplaces or fireplace inserts meeting requirements in B below. These types of heating devices may be used only in dwellings written in the Custom and Optional Loss Programs. Devices listed above and fueled by wood pellets or corn may be used in dwellings written in any program. These devices cannot be the primary source of heat.

2. A solid fuel heating device located in a structure separate from the insured dwelling which circulates hot water to the dwelling, is controlled by a thermostat and meets the requirements of B.2. through B.9 below. These devices are eligible in all programs. These devices can be the primary source of heat but not the only source of heat.

B. Acceptable solid fuel burning devices must meet the following requirements: 1. Items described under A.1. above cannot be used as a primary source of heat and there is

not more than one unit in the dwelling. 2. Photograph of the unit must accompany the application. 3. The solid fuel appliance application must be fully completed. 4. The device must meet the following standards: a. Factory made, listed and tested by a recognized testing laboratory such as Underwriters

Laboratory (U.L.) or Building Officials and Code Administrators (B.O.C.A.). b. Installed by a qualified contractor according to manufacturer’s specifications and in

conformity with building codes. c. Not installed in a garage or other structure where flammable liquids, dust or gases are present. 5. Chimney/Stove Pipe a. Shall not be connected to a flue serving any other device. b. Chimney must be:

(1) masonry, built from the ground up, have a metal clean out door, and lined with a mortared fire clay liner,

(2) double wall insulated stainless steel; or (3) triple wall stainless steel. c. If the pipe passes through a combustible partition, it must be fitted with a wall pass

through device bearing the listing of a recognized testing laboratory such as Underwriters Laboratories (U.L.).

6. Clearances to combustible materials must meet the following minimum requirements unless lesser distances are allowed by the testing laboratory in 4.a. above and documented on the stove or manufacturer’s installation instructions.

a. Heating device. (1) 48" to combustibles in front. (2) 36" to side and rear combustibles. b. Stove pipe. (1) 18" horizontal distance to walls (2) 36" vertical distance to ceiling.

All walls are considered combustible except for vented drywall on metal studs, solid concrete, solid concrete block or solid brick with no combustible studs located within them.

7. Flooring — Non-combustible flooring must be under the device and extend out 18" on all sides. 8. Ashes — Non-combustible containers are required for removal of ashes and must be placed

on a non-combustible surface. 9. Smoke Alarm — Required.

WISCONSIN HOMEOWNERS MANUAL

Rev. 2/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 32

C. Premium Charge —10% of the modified Base Policy Premium

No surcharge will be made to a solid fuel heating device meeting the following requirements:

1. Located outside of and at least 25' away from any insured structure and standing in the open without any enclosure. Structures such as wood sheds (but not wood piles) within 25' of the solid fuel device or any enclosure of the heating device will continue to result in a surcharge.

2. A solid fuel standalone or supplemental central furnace unit fueled by wood pellets or corn. The clearances to combustible materials must meet the requirements of item 6. above.

SWIMMING POOL REQUIREMENTS Above ground pool

Must have a removable or retractable ladder. In-ground pool

Pool or yard must be fenced with at least a four foot high fence with a self-latching gate. With diving or sliding board, ELIGIBLE minimum required depths:

One meter diving board – 8.5 feet

Deck mounted diving board – 8 feet

Sliding board – 4 feet

OLDER HOME ELIGIBILITY REQUIREMENTS ELECTRICAL SYSTEM:

Homes with electric heat or central air conditioning containing 100 amp service or higher are ELIGIBLE.

System repairs and/or upgrades performed by a licensed electrical contractor are ELIGIBLE.

System repairs and/or upgrades performed by other than a licensed contractor and subsequently inspected and approved are ELIGIBLE.

Risks with any knob and tube wiring present are PROHIBITED.

Risks with fuse boxes only are PROHIBITED.

Risks with aluminum wiring present are PROHIBITED.

Risks with less than 100 amp service are PROHIBITED. PLUMBING SYSTEM:

System must be in good repair and free of leaks.

System repairs and/or upgrades performed by a licensed plumbing contractor are ELIGIBLE.

System repairs and/or upgrades performed by other than a licensed contractor and subsequently inspected and approved are ELIGIBLE.

HEATING AND COOLING SYSTEMS: Oil and gas fired systems serviced within the past two years are ELIGIBLE. ROOF SURFACE:

Composition shingles and wood shingles aged 20 years or less are ELIGIBLE

Metal, Tile and EDM rubber shingles aged 40 years or less are ELIGIBLE

Slate shingles aged 50 years or less are ELIGIBLE

WISCONSIN HOMEOWNERS MANUAL

Rev. 2/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 33

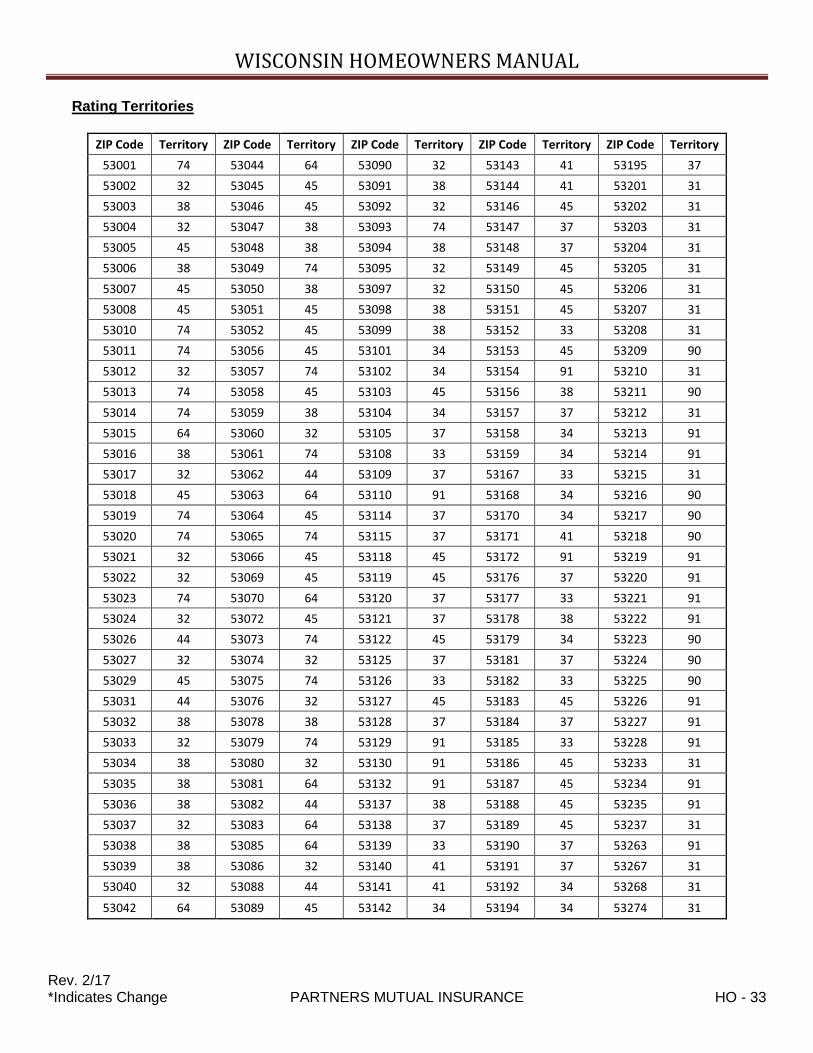

Rating Territories

ZIP Code Territory ZIP Code Territory ZIP Code Territory ZIP Code Territory ZIP Code Territory

53001 74 53044 64 53090 32 53143 41 53195 37

53002 32 53045 45 53091 38 53144 41 53201 31

53003 38 53046 45 53092 32 53146 45 53202 31

53004 32 53047 38 53093 74 53147 37 53203 31

53005 45 53048 38 53094 38 53148 37 53204 31

53006 38 53049 74 53095 32 53149 45 53205 31

53007 45 53050 38 53097 32 53150 45 53206 31

53008 45 53051 45 53098 38 53151 45 53207 31

53010 74 53052 45 53099 38 53152 33 53208 31

53011 74 53056 45 53101 34 53153 45 53209 90

53012 32 53057 74 53102 34 53154 91 53210 31

53013 74 53058 45 53103 45 53156 38 53211 90

53014 74 53059 38 53104 34 53157 37 53212 31

53015 64 53060 32 53105 37 53158 34 53213 91

53016 38 53061 74 53108 33 53159 34 53214 91

53017 32 53062 44 53109 37 53167 33 53215 31

53018 45 53063 64 53110 91 53168 34 53216 90

53019 74 53064 45 53114 37 53170 34 53217 90

53020 74 53065 74 53115 37 53171 41 53218 90

53021 32 53066 45 53118 45 53172 91 53219 91

53022 32 53069 45 53119 45 53176 37 53220 91

53023 74 53070 64 53120 37 53177 33 53221 91

53024 32 53072 45 53121 37 53178 38 53222 91

53026 44 53073 74 53122 45 53179 34 53223 90

53027 32 53074 32 53125 37 53181 37 53224 90

53029 45 53075 74 53126 33 53182 33 53225 90

53031 44 53076 32 53127 45 53183 45 53226 91

53032 38 53078 38 53128 37 53184 37 53227 91

53033 32 53079 74 53129 91 53185 33 53228 91

53034 38 53080 32 53130 91 53186 45 53233 31

53035 38 53081 64 53132 91 53187 45 53234 91

53036 38 53082 44 53137 38 53188 45 53235 91

53037 32 53083 64 53138 37 53189 45 53237 31

53038 38 53085 64 53139 33 53190 37 53263 91

53039 38 53086 32 53140 41 53191 37 53267 31

53040 32 53088 44 53141 41 53192 34 53268 31

53042 64 53089 45 53142 34 53194 34 53274 31

WISCONSIN HOMEOWNERS MANUAL

Rev. 2/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 34

ZIP Code Territory ZIP Code Territory ZIP Code Territory ZIP Code Territory ZIP Code Territory

53278 31 53529 30 53571 30 53714 93 53817 85

53288 31 53530 37 53572 30 53715 93 53818 85

53290 31 53531 30 53573 85 53716 93 53820 85

53293 31 53532 30 53574 37 53717 93 53821 85

53295 31 53533 37 53575 30 53718 93 53824 85

53401 40 53534 77 53576 37 53719 93 53825 85

53402 40 53535 37 53577 38 53725 93 53826 85

53403 40 53536 37 53578 38 53726 93 53827 85

53404 40 53537 77 53579 38 53744 93 53901 38

53405 40 53538 38 53580 37 53777 93 53910 68

53406 40 53540 84 53581 84 53778 93 53911 38

53407 40 53541 37 53582 37 53779 93 53913 38

53408 40 53542 77 53583 38 53782 93 53916 38

53490 40 53543 37 53584 84 53783 93 53919 74

53501 37 53544 37 53585 37 53784 93 53920 86

53502 37 53545 77 53586 37 53785 93 53922 38

53503 37 53546 77 53587 37 53786 93 53923 38

53504 37 53547 77 53588 38 53788 93 53924 84

53505 37 53548 37 53589 30 53789 93 53925 38

53506 37 53549 38 53590 30 53790 93 53926 86

53507 37 53550 37 53593 30 53792 93 53927 86

53508 30 53551 38 53594 38 53793 93 53928 38

53510 37 53553 37 53595 37 53794 93 53929 68

53511 37 53554 85 53596 30 53801 85 53930 86

53512 37 53555 38 53597 30 53802 85 53931 44

53515 30 53556 84 53598 30 53803 85 53932 38

53516 37 53557 38 53599 37 53804 85 53933 38

53517 30 53558 30 53701 93 53805 85 53934 68

53518 85 53559 30 53702 93 53806 85 53935 38

53520 37 53560 30 53703 93 53807 85 53936 68

53521 37 53561 38 53704 93 53808 85 53937 38

53522 37 53562 30 53705 93 53809 85 53939 86

53523 30 53563 37 53706 93 53810 85 53940 38

53525 37 53565 37 53707 93 53811 85 53941 38

53526 37 53566 37 53708 93 53812 85 53942 38

53527 30 53569 85 53711 93 53813 85 53943 38

53528 30 53570 37 53713 93 53816 85 53944 68

WISCONSIN HOMEOWNERS MANUAL

Rev. 2/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 35

ZIP Code Territory ZIP Code Territory ZIP Code Territory ZIP Code Territory ZIP Code Territory

53946 86 54020 82 54138 98 54211 44 54404 87

53947 86 54021 82 54139 98 54212 44 54405 67

53948 68 54022 82 54140 96 54213 44 54406 92

53949 86 54023 82 54141 98 54214 44 54407 92

53950 68 54024 82 54143 98 54215 44 54408 67

53951 38 54025 82 54149 98 54216 54 54409 99

53952 86 54026 82 54150 99 54217 44 54410 87

53953 86 54027 82 54151 98 54220 54 54411 67

53954 38 54028 82 54152 96 54221 44 54412 87

53955 38 54082 82 54153 98 54226 44 54413 87

53956 38 54101 98 54154 98 54227 54 54414 97

53957 38 54102 98 54155 94 54228 54 54415 87

53958 38 54103 99 54156 98 54229 94 54416 97

53959 38 54104 98 54157 98 54230 54 54417 87

53960 38 54106 94 54159 98 54232 44 54418 99

53961 38 54107 97 54160 44 54234 44 54420 87

53962 86 54110 54 54161 98 54235 44 54421 67

53963 38 54111 97 54162 94 54240 44 54422 67

53964 86 54112 98 54165 94 54241 54 54423 92

53965 38 54113 96 54166 97 54245 54 54424 99

53968 68 54114 98 54169 74 54246 44 54425 67

53969 38 54115 96 54170 96 54247 54 54426 67

54001 82 54119 98 54171 98 54301 94 54427 67

54002 82 54120 99 54173 94 54302 94 54428 99

54003 82 54121 99 54174 98 54303 94 54429 87

54004 82 54123 44 54175 98 54304 94 54430 99

54005 82 54124 98 54177 98 54305 94 54432 87

54006 82 54125 98 54180 96 54306 94 54433 76

54007 82 54126 96 54182 97 54307 94 54434 76

54009 82 54127 97 54201 44 54308 94 54435 99

54010 82 54128 97 54202 44 54311 94 54436 87

54011 82 54129 74 54204 44 54313 94 54437 67

54013 82 54130 96 54205 44 54324 94 54439 76

54014 82 54131 96 54207 44 54344 94 54440 67

54015 82 54135 99 54208 94 54401 67 54441 87

54016 82 54136 96 54209 44 54402 87 54442 89

54017 82 54137 97 54210 44 54403 67 54443 87

WISCONSIN HOMEOWNERS MANUAL

Rev. 2/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 36

ZIP Code Territory ZIP Code Territory ZIP Code Territory ZIP Code Territory ZIP Code Territory

54446 67 54490 76 54547 83 54627 80 54669 80

54447 76 54491 99 54548 89 54628 84 54670 80

54448 67 54492 87 54550 83 54629 80 54701 81

54449 87 54493 67 54552 89 54630 80 54702 81

54450 97 54494 87 54554 89 54631 84 54703 81

54451 76 54495 87 54555 89 54632 84 54720 81

54452 89 54498 67 54556 89 54634 84 54721 82

54454 87 54499 97 54557 89 54635 80 54722 81

54455 67 54501 89 54558 89 54636 80 54723 82

54456 87 54511 99 54559 83 54637 86 54724 81

54457 87 54512 89 54560 89 54638 80 54725 82

54458 92 54513 89 54561 99 54639 84 54726 81

54459 89 54514 83 54562 89 54641 68 54727 81

54460 67 54515 89 54563 81 54642 80 54728 82

54462 99 54517 83 54564 89 54643 80 54729 81

54463 89 54519 89 54565 83 54644 80 54730 82

54464 92 54520 99 54566 99 54645 84 54731 81

54465 99 54521 89 54568 89 54646 68 54732 81

54466 87 54524 89 54601 80 54648 80 54733 82

54467 87 54525 83 54602 80 54649 80 54734 82

54469 87 54526 81 54603 80 54650 80 54735 82

54470 76 54527 83 54610 80 54651 84 54736 82

54471 67 54529 89 54611 80 54652 84 54737 82

54472 87 54530 81 54612 80 54653 80 54738 80

54473 92 54531 89 54613 68 54654 84 54739 81

54474 67 54532 89 54614 80 54655 84 54740 82

54475 87 54534 83 54615 80 54656 80 54741 81

54476 67 54536 83 54616 80 54657 85 54742 81

54479 67 54537 89 54618 68 54658 84 54743 80

54480 76 54538 89 54619 84 54659 80 54745 81

54481 87 54539 89 54620 80 54660 80 54746 87

54484 67 54540 89 54621 84 54661 80 54747 80

54485 99 54541 99 54622 80 54662 80 54748 81

54486 97 54542 99 54623 84 54664 84 54749 82

54487 89 54543 89 54624 84 54665 84 54750 82

54488 67 54545 89 54625 80 54666 80 54751 82

54489 87 54546 83 54626 85 54667 84 54754 80

WISCONSIN HOMEOWNERS MANUAL

Rev. 2/17 *Indicates Change PARTNERS MUTUAL INSURANCE HO - 37

ZIP Code Territory ZIP Code Territory ZIP Code Territory ZIP Code Territory ZIP Code Territory

54755 80 54828 81 54873 83 54937 74 54985 96

54756 80 54829 82 54874 83 54940 92 54986 96

54757 81 54830 82 54875 81 54941 86 54990 92

54758 80 54832 83 54876 81 54942 96

54759 82 54834 81 54880 83 54943 86

54760 80 54835 81 54888 81 54944 96

54761 82 54836 83 54889 82 54945 92

54762 82 54837 82 54890 83 54946 92

54763 82 54838 83 54891 83 54947 96

54764 82 54839 83 54893 82 54948 97

54765 82 54840 82 54895 81 54949 92

54766 81 54841 82 54896 81 54950 92

54767 82 54842 83 54901 96 54952 96

54768 81 54843 81 54902 96 54956 96

54769 82 54844 83 54903 96 54957 96

54770 80 54845 82 54904 96 54960 86

54771 67 54846 83 54909 87 54961 92