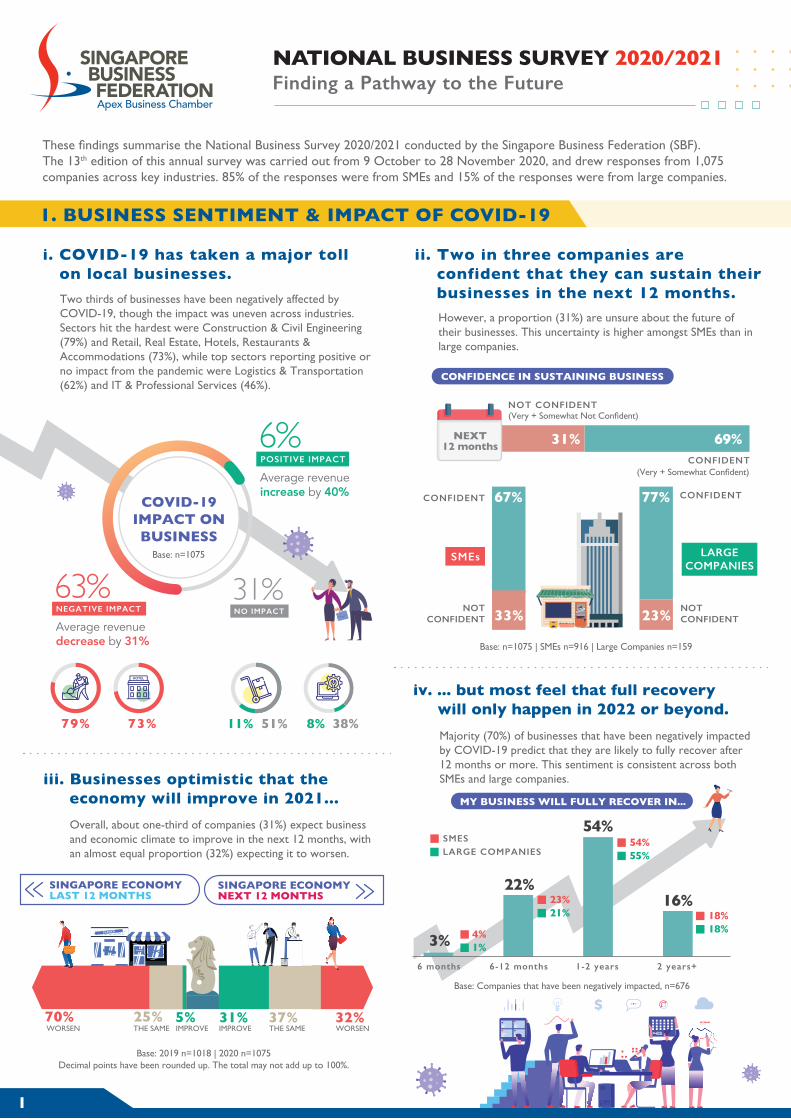

1. business sentiment & impact of covid-19

TRANSCRIPT

NATIONAL BUSINESS SURVEY 2020/2021Finding a Pathway to the Future

These findings summarise the National Business Survey 2020/2021 conducted by the Singapore Business Federation (SBF).The 13th edition of this annual survey was carried out from 9 October to 28 November 2020, and drew responses from 1,075companies across key industries. 85% of the responses were from SMEs and 15% of the responses were from large companies.

i. COVID-19 has taken a major toll on local businesses.

Two thirds of businesses have been negatively affected by COVID-19, though the impact was uneven across industries. Sectors hit the hardest were Construction & Civil Engineering (79%) and Retail, Real Estate, Hotels, Restaurants & Accommodations (73%), while top sectors reporting positive or no impact from the pandemic were Logistics & Transportation (62%) and IT & Professional Services (46%).

ii. Two in three companies are confident that they can sustain their businesses in the next 12 months.

However, a proportion (31%) are unsure about the future of their businesses. This uncertainty is higher amongst SMEs than in large companies.

iv. ... but most feel that full recovery will only happen in 2022 or beyond.

Majority (70%) of businesses that have been negatively impacted by COVID-19 predict that they are likely to fully recover after 12 months or more. This sentiment is consistent across both SMEs and large companies.

NEGATIVE IMPACT

63%Average revenuedecrease by 31%

POSITIVE IMPACT

6%Average revenueincrease by 40%

NO IMPACT

31%

COVID-19IMPACT ONBUSINESS

(Very + Somewhat Confident)CONFIDENT

CONFIDENT

(Very + Somewhat Not Confident)NOT CONFIDENT

MY BUSINESS WILL FULLY RECOVER IN...

6 months 6-12 months 1-2 years 2 years+

3% 4%1%

23%21%

54%55%

18%18%

22%

54%

16%

31% 69%NEXT12 months

1. BUSINESS SENTIMENT & IMPACT OF COVID-19

1

CONFIDENCE IN SUSTAINING BUSINESS

OPEN

SMEs

67% 77%

23%33%

LARGECOMPANIES

CONFIDENT

NOTCONFIDENT

NOTCONFIDENT

Base: n=1075

Base: n=1075 | SMEs n=916 | Large Companies n=159

iii. Businesses optimistic that the economy will improve in 2021...

Overall, about one-third of companies (31%) expect business and economic climate to improve in the next 12 months, with an almost equal proportion (32%) expecting it to worsen.

SINGAPORE ECONOMYNEXT 12 MONTHS

WORSEN70%

WORSEN32%5%

THE SAME IMPROVE31%IMPROVE

25%THE SAME37%

SINGAPORE ECONOMYLAST 12 MONTHS

Base: 2019 n=1018 | 2020 n=1075Decimal points have been rounded up. The total may not add up to 100%.

SMESLARGE COMPANIES

Base: Companies that have been negatively impacted, n=676

79% 73% 11% 51% 8% 38%

80% 81%

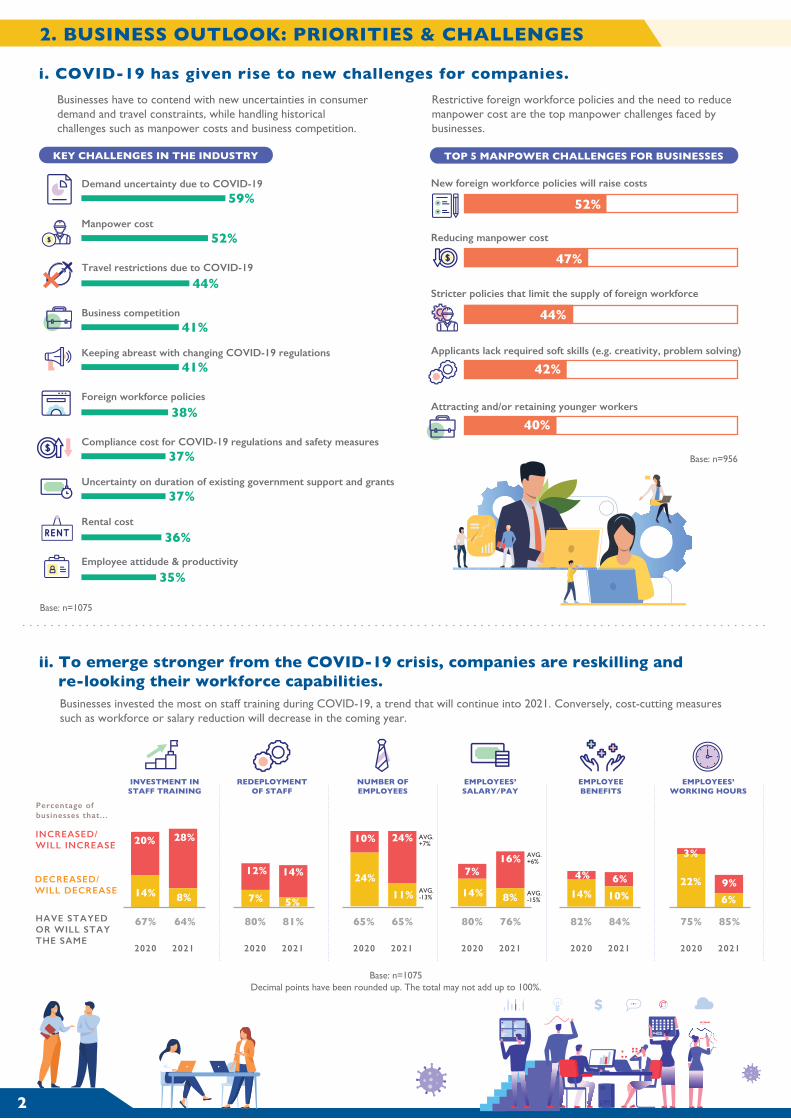

2. BUSINESS OUTLOOK: PRIORITIES & CHALLENGES

2

i. COVID-19 has given rise to new challenges for companies.Businesses have to contend with new uncertainties in consumer demand and travel constraints, while handling historical challenges such as manpower costs and business competition.

Restrictive foreign workforce policies and the need to reduce manpower cost are the top manpower challenges faced by businesses.

ii. To emerge stronger from the COVID-19 crisis, companies are reskilling and re-looking their workforce capabilities.

Businesses invested the most on staff training during COVID-19, a trend that will continue into 2021. Conversely, cost-cutting measures such as workforce or salary reduction will decrease in the coming year.

TOP 5 MANPOWER CHALLENGES FOR BUSINESSESKEY CHALLENGES IN THE INDUSTRY

New foreign workforce policies will raise costs

52%

Reducing manpower cost

47%

Stricter policies that limit the supply of foreign workforce

44%

Applicants lack required soft skills (e.g. creativity, problem solving)

Attracting and/or retaining younger workers

42%

40%

Demand uncertainty due to COVID-19

Manpower cost

Travel restrictions due to COVID-19

52%

44%

59%

Foreign workforce policies

38%

41%

Rental cost

36%

Employee attidude & productivity

35%

37%Compliance cost for COVID-19 regulations and safety measures

Uncertainty on duration of existing government support and grants

Business competition

Keeping abreast with changing COVID-19 regulations41%

37%

INVESTMENT INSTAFF TRAINING

REDEPLOYMENTOF STAFF

NUMBER OFEMPLOYEES

EMPLOYEES’SALARY/PAY

EMPLOYEEBENEFITS

EMPLOYEES’WORKING HOURS

INCREASED/WILL INCREASE

DECREASED/WILL DECREASE

HAVE STAYEDOR WILL STAYTHE SAME

14%

20%

67% 64%

8% 10%6%

6%9%

14%

4% 22%

3%

2020 2021 2020 2021

Percentage ofbusinesses that...

AVG.+7%

AVG.-13%

65% 65%

2020 2021

AVG.+6%

AVG.-15%

80% 76%

2020 2021

8%

28%

5%7%

14%12%24%

10% 24%

11%

16%7%

14%

82% 84%

2020 2021

75% 85%

2020 2021

Base: n=1075

Base: n=956

Base: n=1075Decimal points have been rounded up. The total may not add up to 100%.

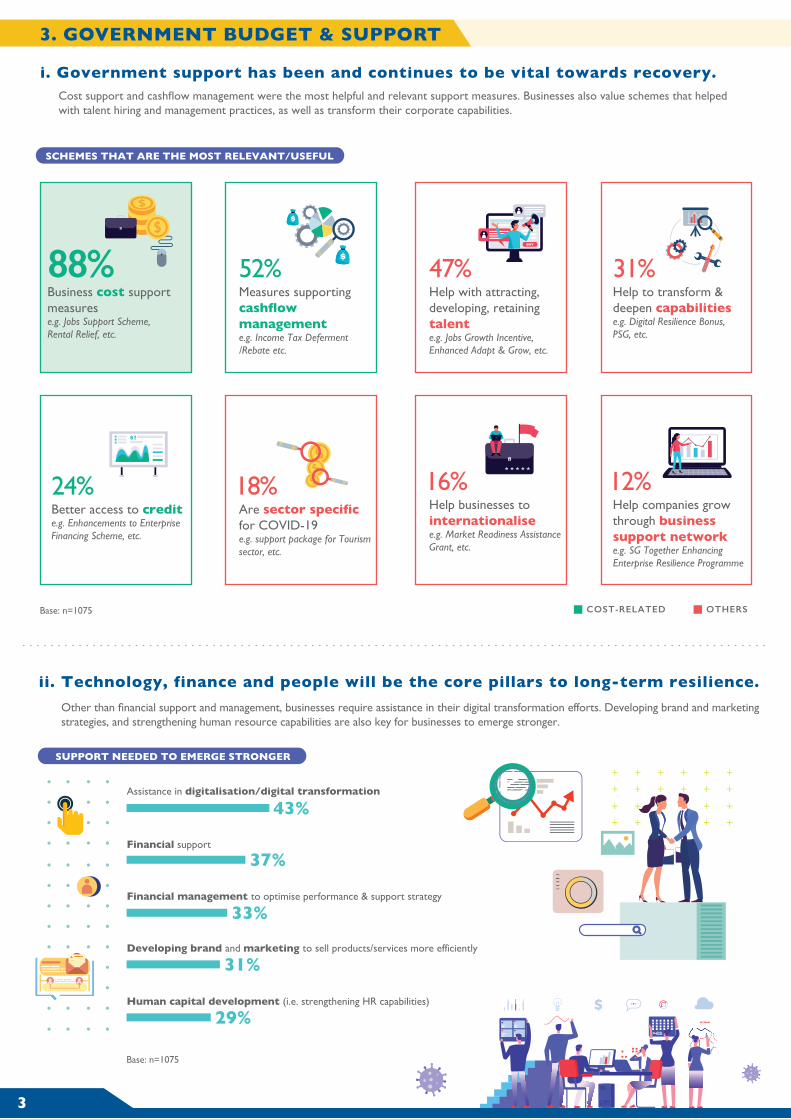

ii. Technology, finance and people will be the core pillars to long-term resilience.Other than financial support and management, businesses require assistance in their digital transformation efforts. Developing brand and marketing strategies, and strengthening human resource capabilities are also key for businesses to emerge stronger.

3. GOVERNMENT BUDGET & SUPPORT

3

i. Government support has been and continues to be vital towards recovery.Cost support and cashflow management were the most helpful and relevant support measures. Businesses also value schemes that helped with talent hiring and management practices, as well as transform their corporate capabilities.

SUPPORT NEEDED TO EMERGE STRONGER

SCHEMES THAT ARE THE MOST RELEVANT/USEFUL

Assistance in digitalisation/digital transformation

Financial support

Financial management to optimise performance & support strategy

Developing brand and marketing to sell products/services more efficiently

Human capital development (i.e. strengthening HR capabilities)

37%

33%

31%

29%

43%

OTHERSCOST-RELATED

88%Business cost supportmeasurese.g. Jobs Support Scheme,Rental Relief, etc.

52%Measures supportingcashflowmanagemente.g. Income Tax Deferment/Rebate etc.

24%Better access to credite.g. Enhancements to EnterpriseFinancing Scheme, etc.

18%Are sector specificfor COVID-19e.g. support package for Tourismsector, etc.

47%Help with attracting,developing, retainingtalente.g. Jobs Growth Incentive,Enhanced Adapt & Grow, etc.

31%Help to transform &deepen capabilitiese.g. Digital Resilience Bonus,PSG, etc.

16%Help businesses tointernationalisee.g. Market Readiness AssistanceGrant, etc.

12%Help companies growthrough businesssupport networke.g. SG Together EnhancingEnterprise Resilience Programme

Base: n=1075

Base: n=1075

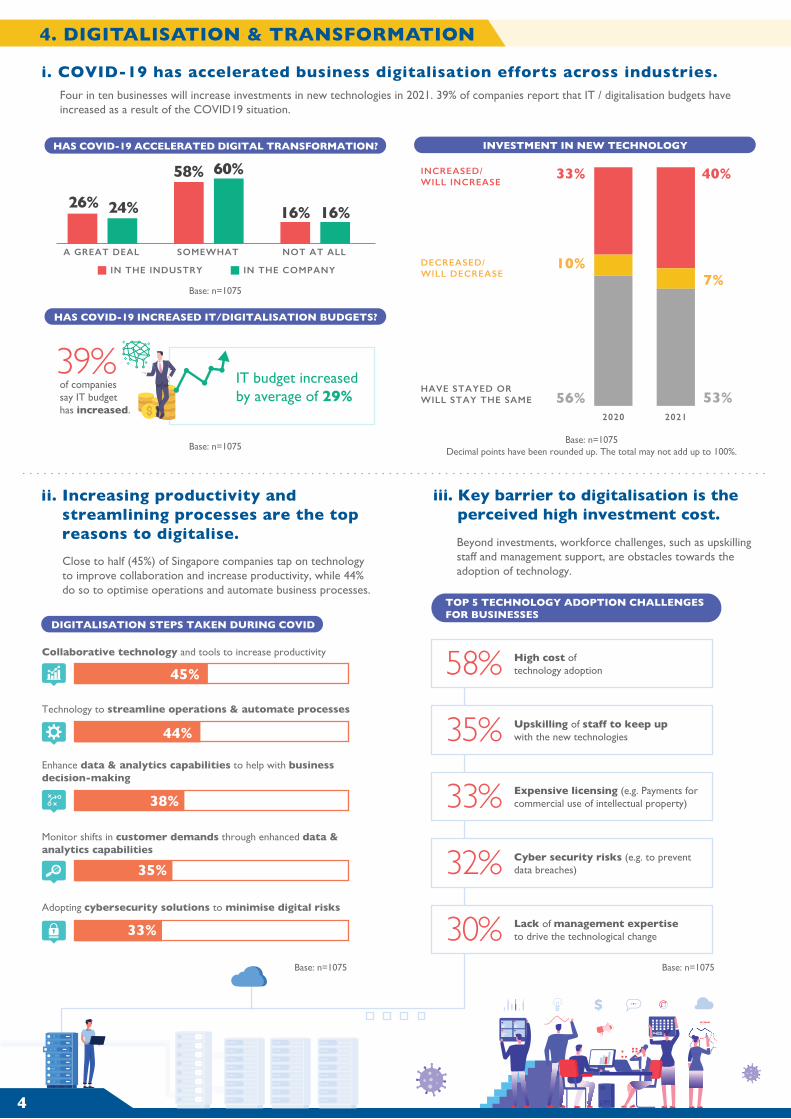

4. DIGITALISATION & TRANSFORMATION

4

i. COVID-19 has accelerated business digitalisation efforts across industries.Four in ten businesses will increase investments in new technologies in 2021. 39% of companies report that IT / digitalisation budgets have increased as a result of the COVID19 situation.

iii. Key barrier to digitalisation is the perceived high investment cost.

Beyond investments, workforce challenges, such as upskilling staff and management support, are obstacles towards the adoption of technology.

ii. Increasing productivity and streamlining processes are the top reasons to digitalise.

Close to half (45%) of Singapore companies tap on technology to improve collaboration and increase productivity, while 44% do so to optimise operations and automate business processes.

DIGITALISATION STEPS TAKEN DURING COVID

Collaborative technology and tools to increase productivity

45%

Technology to streamline operations & automate processes

44%

Enhance data & analytics capabilities to help with businessdecision-making

38%

Monitor shifts in customer demands through enhanced data &analytics capabilities

Adopting cybersecurity solutions to minimise digital risks

35%

33%

TOP 5 TECHNOLOGY ADOPTION CHALLENGESFOR BUSINESSES

INVESTMENT IN NEW TECHNOLOGY

High cost oftechnology adoption58%Upskilling of staff to keep upwith the new technologies35%Expensive licensing (e.g. Payments forcommercial use of intellectual property)33%Cyber security risks (e.g. to preventdata breaches)32%Lack of management expertiseto drive the technological change30%

INCREASED/WILL INCREASE

DECREASED/WILL DECREASE

HAVE STAYED ORWILL STAY THE SAME

33%

10%

56%

40%

7%

53%2020 2021

Base: n=1075Decimal points have been rounded up. The total may not add up to 100%.

HAS COVID-19 INCREASED IT/DIGITALISATION BUDGETS?

HAS COVID-19 ACCELERATED DIGITAL TRANSFORMATION?

39%of companiessay IT budgethas increased.

IT budget increasedby average of 29%

IN THE INDUSTRY IN THE COMPANY

A GREAT DEAL SOMEWHAT

26% 24%

58% 60%

16% 16%

NOT AT ALL

Base: n=1075

Base: n=1075 Base: n=1075

Base: n=1075

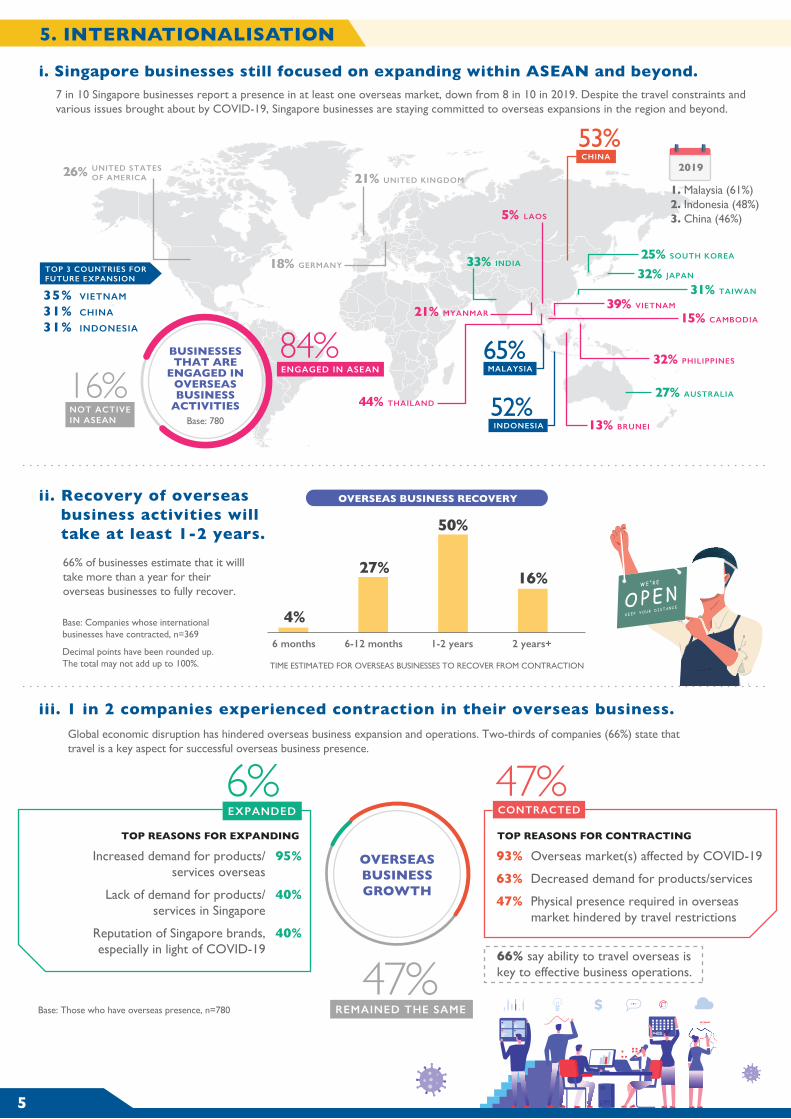

Global economic disruption has hindered overseas business expansion and operations. Two-thirds of companies (66%) state that travel is a key aspect for successful overseas business presence.

ii. Recovery of overseas business activities will take at least 1-2 years.

iii. 1 in 2 companies experienced contraction in their overseas business.

66% of businesses estimate that it willl take more than a year for their overseas businesses to fully recover.

TIME ESTIMATED FOR OVERSEAS BUSINESSES TO RECOVER FROM CONTRACTION

5. INTERNATIONALISATION

5

i. Singapore businesses still focused on expanding within ASEAN and beyond.7 in 10 Singapore businesses report a presence in at least one overseas market, down from 8 in 10 in 2019. Despite the travel constraints and various issues brought about by COVID-19, Singapore businesses are staying committed to overseas expansions in the region and beyond.

6 months 6-12 months 1-2 years 2 years+

4%

27%

50%

16%

OVERSEAS BUSINESS RECOVERY

OVERSEASBUSINESSGROWTH

EXPANDED

6%

REMAINED THE SAME

47%

93% Overseas market(s) affected by COVID-19

63% Decreased demand for products/services

47% Physical presence required in overseas market hindered by travel restrictions

Increased demand for products/services overseas

Lack of demand for products/services in Singapore

Reputation of Singapore brands,especially in light of COVID-19

95%

40%

40%

TOP REASONS FOR CONTRACTINGTOP REASONS FOR EXPANDING

CONTRACTED

47%

MALAYSIA

65%

JAPAN32%

VIETNAM39%CAMBODIA15%

PHILIPPINES32%

BRUNEI13%

LAOS5%

SOUTH KOREA25%

UNITED KINGDOM21%

GERMANY18%

UNITED STATESOF AMERICA26%

INDONESIA

52%

CHINA

53%

MYANMAR21%

AUSTRALIA27%

INDIA33%

THAILAND44%

TAIWAN31%

ENGAGED IN ASEAN

84%NOT ACTIVEIN ASEAN

16%

2019

1. Malaysia (61%)2. Indonesia (48%)3. China (46%)

TOP 3 COUNTRIES FORFUTURE EXPANSION

35% VIETNAM

31% CHINA

31% INDONESIA

BUSINESSESTHAT ARE

ENGAGED INOVERSEASBUSINESS

ACTIVITIESBase: 780

66% say ability to travel overseas iskey to effective business operations.

Base: Those who have overseas presence, n=780

Base: Companies whose internationalbusinesses have contracted, n=369

Decimal points have been rounded up.The total may not add up to 100%.

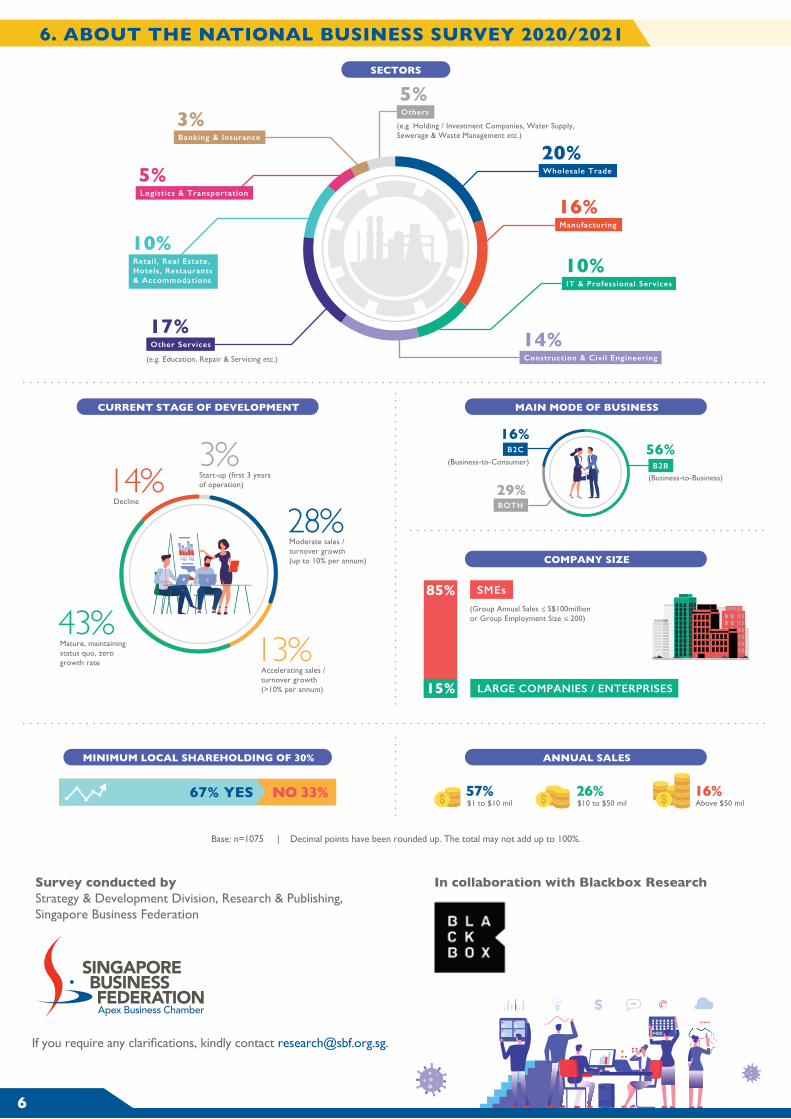

6. ABOUT THE NATIONAL BUSINESS SURVEY 2020/2021

6

Survey conducted byStrategy & Development Division, Research & Publishing,Singapore Business Federation

In collaboration with Blackbox Research

If you require any clarifications, kindly contact [email protected].

COMPANY SIZE

ANNUAL SALES

CURRENT STAGE OF DEVELOPMENT MAIN MODE OF BUSINESS

MINIMUM LOCAL SHAREHOLDING OF 30%

SMEs

(Group Annual Sales ≤ S$100millionor Group Employment Size ≤ 200)

LARGE COMPANIES / ENTERPRISES

85%

15%

(e.g. Education, Repair & Servicing etc.)

(e.g. Holding / Investment Companies, Water Supply,Sewerage & Waste Management etc.)

20%

16%

29%

56%(Business-to-Consumer)

(Business-to-Business)

B2B

B2C

BOTH

57%$1 to $10 mil

26%$10 to $50 mil

16%Above $50 mil

67% YES NO 33%

13%Accelerating sales /turnover growth (>10% per annum)

28%Moderate sales /turnover growth(up to 10% per annum)

14%Decline

3%Start-up (first 3 yearsof operation)

43%Mature, maintainingstatus quo, zerogrowth rate

Base: n=1075 | Decimal points have been rounded up. The total may not add up to 100%.

Wholesale Trade

16%Manufacturing

10%IT & Professional Services

14%Construction & Civil Engineering

17%Other Services

10%Retail, Real Estate,Hotels, Restaurants& Accommodations

3%Banking & Insurance

5%Others

SECTORS

5%Logistics & Transportation